Embed Size (px)

Citation preview

Cost & Management Accounting

Lincy Rinil

Introduction

• Accounting– Accounting is a wider term and includes recording,

classifying and summarizing of business transactions in terms of money, preparation of financial reports and analysis and interpretation of these reports for the information and guidance of management.

– The business accounting system consists of three parts:i. Financial Accountingii. Cost Accountingiii.Management Accounting

Financial Accounting

• Financial accounting may be defined as the science and art of systematically recording, classifying and summarizing business transactions of financial character and finally interpreting the results for determining the financial profit or loss at the end of an accounting year.

• It also shows the financial position of the firm, and thus, records and reports financial statements – Balance sheet, income statement and statement of cash flows.

Cost Accounting

• Cost accounting is that branch of the accounting information system, which records, measures and reports information about costs.

• The primary purpose of cost accounting is cost ascertainment and its use in decision making and performance evaluation.

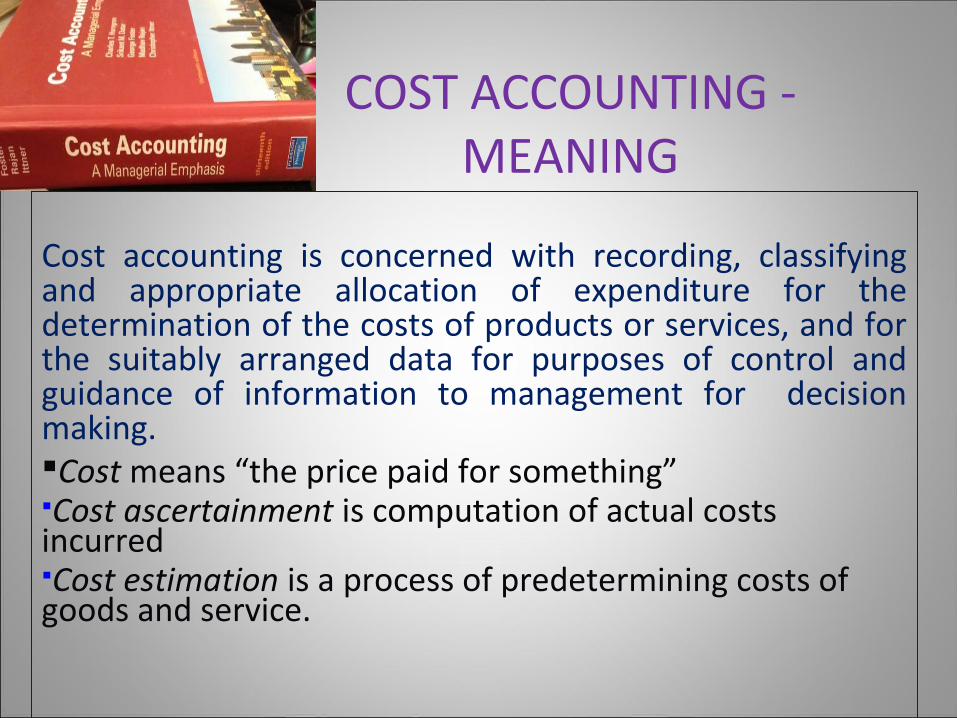

COST ACCOUNTING - MEANING

Cost accounting is concerned with recording, classifying and appropriate allocation of expenditure for the determination of the costs of products or services, and for the suitably arranged data for purposes of control and guidance of information to management for decision making.Cost means “the price paid for something”Cost ascertainment is computation of actual costs incurredCost estimation is a process of predetermining costs of goods and service.

OBJECTIVES OF COST ACCOUNTING

Estimation of costs

Ascertainment of costs

Cost control

Cost reduction

Determining selling price

Facilitating preparation of financial and other statement

Providing basis for operating policy

Elements of cost

Materials Labour Expenses

Direct Indirect Direct Indirect Direct Indirect

Overheads

Production or works overheads

Administration overheads

Selling & Distribution overheads

MATERIAL: The substance from which the finished product is made is known as material. (a) DIRECT MATERIAL: is one which can be directly or easily identified in the product Eg: Timber in furniture, Cloth in dress, etc.

(b) INDIRECT MATERIAL: one which cannot be easily identified in the product. Eg: disposable safety equipment, disposable tools, glue, tape, oil, etc.

LABOUR: The human effort required to convert the materials into finished product is called labour.

(a) DIRECT LABOUR: is one which can be conveniently identified or attributed wholly to a particular job,

product or process.Eg: wages paid to carpenter, fees paid to tailor, etc.

(b) INDIRECT LABOUR: is one which cannot be conveniently identified or attributed wholly to a particular job,

product or process.

EXAMPLES OF INDIRECT LABOUR

At factory level – foremen’s salary, works manager’s salary, gate keeper’s salary, etc

At office level – Accountant’s salary, GM’s salary, Manager’s salary, etc.

At selling and dist.level – salesmen salaries, Logistics manager salary, etc.

OTHER EXPENSES: are those expenses other than materials and labour.

DIRECT EXPENSES: are those expenses which can be directly allocated to particular job, process

or product. Eg : Excise duty, royalty, special hire charges,etc.

INDIRECT EXPENSES: are those expenses which cannot be directly allocated to particular job,

process or product.

Examples of other expenses

At factory level – factory rent, factory insurance, lighting, etc.

At office level – office rent, office insurance, office lighting, etc.

At sales & dist.level – advertising, show room expenses like rent, insurance, etc.

Fixed, Variable and Semi- Variable Costs

Fixed Costs – expenses that do not alter in the short run in relation to changes in output e.g. rent, insurance and depreciation. These costs are linked to time rather the level of business activity

Variable Costs – expenses that alter in the short run to changes in output e.g. raw materials, packaging and components. They are payments for the use of inputs

Semi Variable Costs – expenses that vary with output but not in direct proportion e.g. maintenance costs. They often comprise a fixed element and a variable element

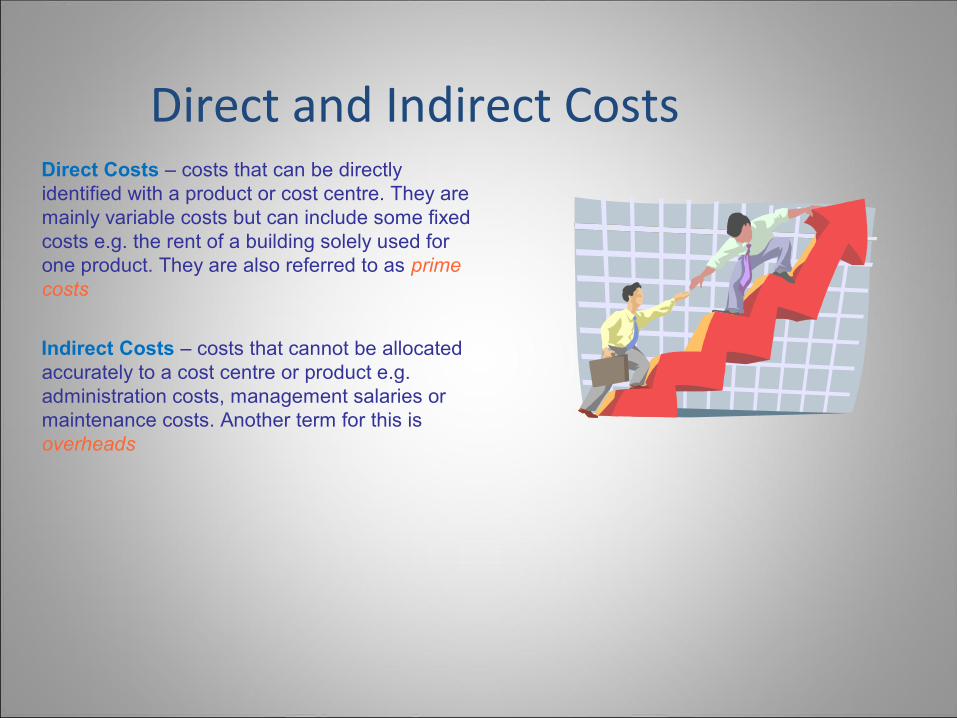

Direct and Indirect CostsDirect Costs – costs that can be directly identified with a product or cost centre. They are mainly variable costs but can include some fixed costs e.g. the rent of a building solely used for one product. They are also referred to as prime costs

Indirect Costs – costs that cannot be allocated accurately to a cost centre or product e.g. administration costs, management salaries or maintenance costs. Another term for this is overheads

Management Accounting

• Meaning

Management accounting involves furnishing of the accounting data to the management in such a way that it facilitates the decision making and improve the efficiency within the organization and finally helps in achieving the goals of the organization.

Definitions – Management Accounting

• According to American Accounting Association: Management Accounting includes the methods and concepts necessary for control through the evaluation and interpretations of performances.

• According to Robert N. Anthony: Management Accounting is concerned with accounting information that is useful to the management.

Objectives of management accounting

• Helpful in Planning & policy formation:-forecasting , setting goals,

framing policies on the basis of available information.

• Help in decision-making:-makes decision on cost, price, profit & savings.

• Helpful in controlling: management accounting devices like standard

costing & budgetary control are helpful in controlling performance

• Motivating to employee: delegation increase the job satisfaction of

employees & encourage them to look forward

• Provides accounting information to management

Management Accounting Vs. Financial Accounting

Dimension Management Financial

Accounting Accounting

1.Structure Varies according Unified Structure

to the information

2. Sources of Whatever is useful Generally Accepted

Principle to management Accounting Principles

3. Need Optional Statutory Obligation

4. Time orientation Historical and estimates Historical

of the future

5. Report entity Responsibility Centers Overall Organization

6. Purpose A means to the end of External reporting / assisting management statements for outside

7. Users Relatively small group: Relatively large group: known identity mostly unknown

Management Accounting Vs. Financial Accounting

Dimension Management Financial

Accounting Accounting

8. Information Monetary and Primarily Monetary

Content non-monetary

9. Information Many approximations Few approximations

Precision

10. Report frequency Varies with purpose: Quarterly and annual

monthly or weekly

11. Report Timeliness Report issued promptly Delay of weeks or even

after end of period covered months

12. Liability Potential Management will take Legally punishable.

action

Thank You