Embed Size (px)

Citation preview

CORPORATE FINANCE FINANCIAL ADVISORY SERVICES FINANCIAL RESTRUCTURING STRATEGIC CONSULTING

HL.com

Unlocking Value: Timing Profitable Growth Initiatives for Optimal Impact

February 3, 2015

Introduction

Today Speakers Introduction

2

Presenter Background

Jim Lavelle

Managing Director

Co-Head of Industrials Group

Mike Jennings

Managing Director

Strategic Consulting

David Calfee

Managing Director

Strategic Consulting

We Deliver Product Expertise Introduction

3

MERGERS AND ACQUISITIONS Sellside & Buyside Transactions Leveraged Transactions Minority Equity Transactions Activist Shareholder Advisory Takeover Defense

CAPITAL MARKETS Debt & Equity Private Placements High Yield Public Equity Offerings PIPEs Financings Liabilities Management Special Situations Advisory

ILLIQUID FINANCIAL ASSETS

Fairness Opinions Solvency Opinions Valuation Opinions Transaction Advisory Services Tax & Financial Reporting

Valuation Portfolio Valuation & Advisory

Services Derivatives Valuation & Advisory

Services Dispute Resolution & Financial

Expert Opinions

Chapter 11 Planning Restructuring Debt and Equity Debtor-in-Possession (“DIP”)

Financing Exchange Offers Plans of Reorganization Distressed Mergers and Acquisitions

Corporate Finance Financial Advisory Financial Restructuring

No. 1 M&A Advisor on U.S. Transactions Under $5 billion

No. 1 U.S. M&A Fairness Opinion Advisor

Over the Past 10+ Years

No. 1 Global Investment Banking Restructuring Advisor

Strategic Consulting

STRATEGY & EXECUTION Corporate & Business Unit Strategy M&A Support, Due Diligence, Post-

Merger Integration New Market Entry

SALES & MARKETING MANAGEMENT Sales & Marketing Effectiveness Product and Solutions Development Pricing Strategy

OPERATIONS & PERFORMANCE IMPROVEMENT Organization & Business Model

Design Supply Chain Optimization Strategic Sourcing & Supply

Management

Recognized Leader in Management Consulting (Kennedy Research)

Advisory Services Across the Investment Lifecycle

Market Update

244%

136%

126% 131%

0%

50%

100%

150%

200%

250%

US EurozoneJapan Emerging Markets

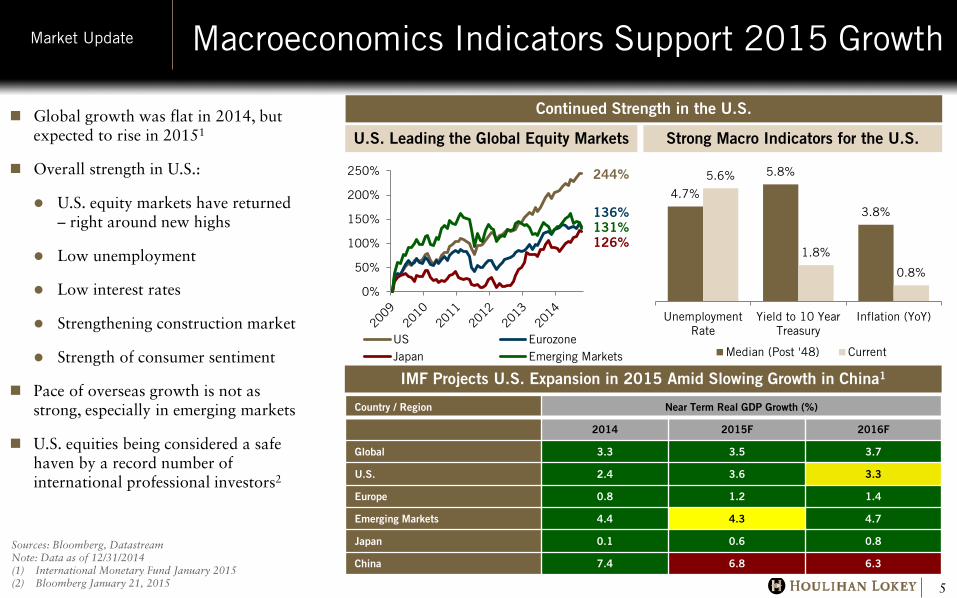

Macroeconomics Indicators Support 2015 Growth Market Update

5

Continued Strength in the U.S.

IMF Projects U.S. Expansion in 2015 Amid Slowing Growth in China1

Global growth was flat in 2014, but expected to rise in 20151

Overall strength in U.S.:

U.S. equity markets have returned – right around new highs

Low unemployment

Low interest rates

Strengthening construction market

Strength of consumer sentiment

Pace of overseas growth is not as strong, especially in emerging markets

U.S. equities being considered a safe haven by a record number of international professional investors2

U.S. Leading the Global Equity Markets

Country / Region Near Term Real GDP Growth (%)

2014 2015F 2016F

Global 3.3 3.5 3.7

U.S. 2.4 3.6 3.3

Europe 0.8 1.2 1.4

Emerging Markets 4.4 4.3 4.7

Japan 0.1 0.6 0.8

China 7.4 6.8 6.3

4.7%

5.8%

3.8%

5.6%

1.8%

0.8%

UnemploymentRate

Yield to 10 YearTreasury

Inflation (YoY)

Median (Post '48) Current

Strong Macro Indicators for the U.S.

Sources: Bloomberg, Datastream Note: Data as of 12/31/2014 (1) International Monetary Fund January 2015 (2) Bloomberg January 21, 2015

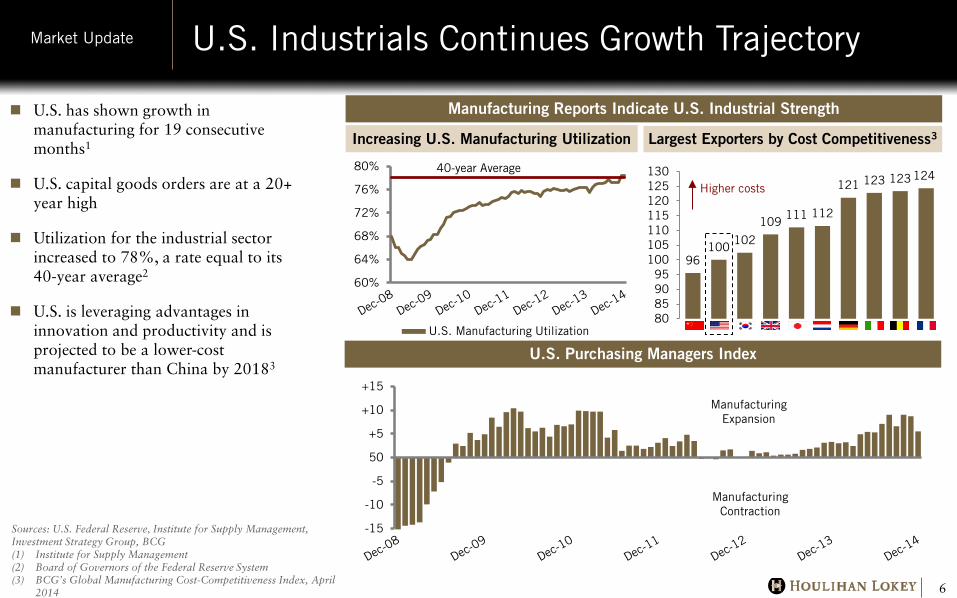

U.S. Purchasing Managers Index

Manufacturing Reports Indicate U.S. Industrial Strength

U.S. Industrials Continues Growth Trajectory Market Update

6

60%

64%

68%

72%

76%

80%

96 100 102

109 111 112

121 123 123 124

80859095

100105110115120125130

Higher costs

-15

-10

-5

50

+5

+10

+15

Manufacturing Expansion

Manufacturing Contraction

Largest Exporters by Cost Competitiveness3

U.S. Manufacturing Utilization

U.S. has shown growth in manufacturing for 19 consecutive months1

U.S. capital goods orders are at a 20+ year high

Utilization for the industrial sector increased to 78%, a rate equal to its 40-year average2

U.S. is leveraging advantages in innovation and productivity and is projected to be a lower-cost manufacturer than China by 20183

Increasing U.S. Manufacturing Utilization

Sources: U.S. Federal Reserve, Institute for Supply Management, Investment Strategy Group, BCG (1) Institute for Supply Management (2) Board of Governors of the Federal Reserve System (3) BCG’s Global Manufacturing Cost-Competitiveness Index, April

2014

40-year Average

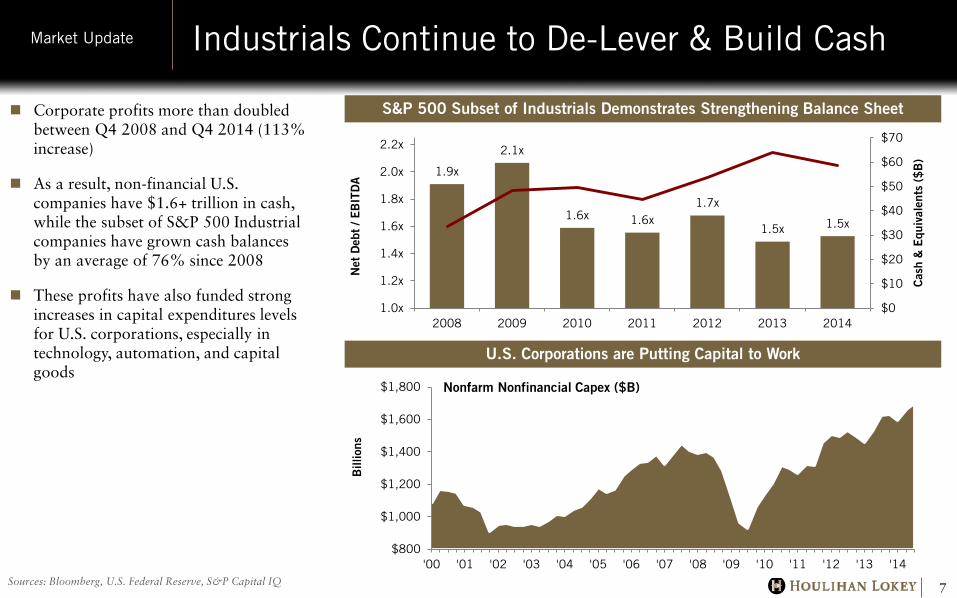

U.S. Corporations are Putting Capital to Work

S&P 500 Subset of Industrials Demonstrates Strengthening Balance Sheet

Industrials Continue to De-Lever & Build Cash Market Update

7

$800

$1,000

$1,200

$1,400

$1,600

$1,800

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Bill

ions

Nonfarm Nonfinancial Capex ($B)

Sources: Bloomberg, U.S. Federal Reserve, S&P Capital IQ

Corporate profits more than doubled between Q4 2008 and Q4 2014 (113% increase)

As a result, non-financial U.S. companies have $1.6+ trillion in cash, while the subset of S&P 500 Industrial companies have grown cash balances by an average of 76% since 2008

These profits have also funded strong increases in capital expenditures levels for U.S. corporations, especially in technology, automation, and capital goods

1.9x

2.1x

1.6x 1.6x 1.7x

1.5x 1.5x

$0

$10

$20

$30

$40

$50

$60

$70

1.0x

1.2x

1.4x

1.6x

1.8x

2.0x

2.2x

2008 2009 2010 2011 2012 2013 2014

Cas

h &

Equ

ival

ents

($

B)

Net

Deb

t / E

BIT

DA

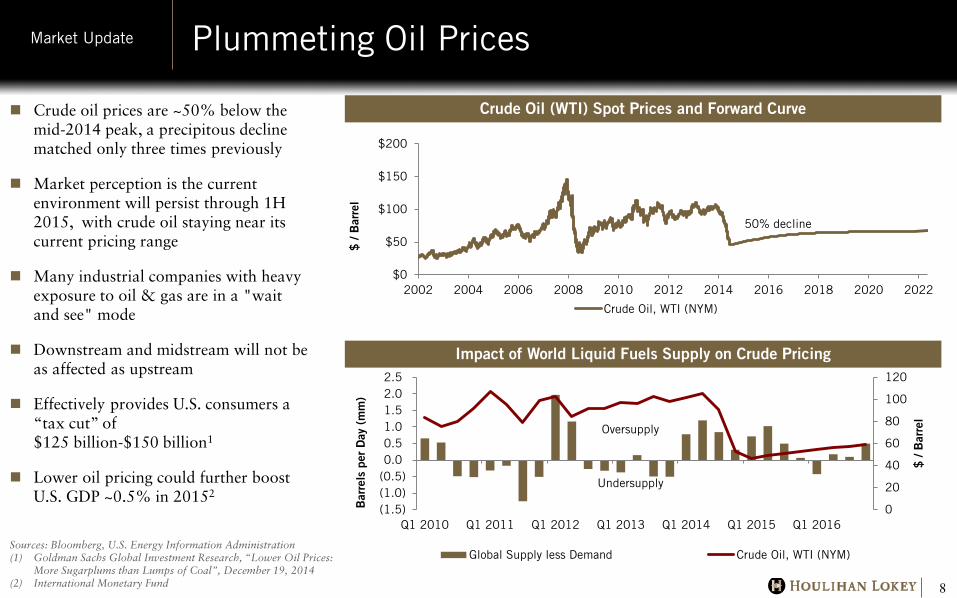

Crude Oil (WTI) Spot Prices and Forward Curve

Impact of World Liquid Fuels Supply on Crude Pricing

Plummeting Oil Prices Market Update

8

Sources: Bloomberg, U.S. Energy Information Administration (1) Goldman Sachs Global Investment Research, “Lower Oil Prices:

More Sugarplums than Lumps of Coal”, December 19, 2014 (2) International Monetary Fund

Crude oil prices are ~50% below the mid-2014 peak, a precipitous decline matched only three times previously

Market perception is the current environment will persist through 1H 2015, with crude oil staying near its current pricing range

Many industrial companies with heavy exposure to oil & gas are in a "wait and see" mode

Downstream and midstream will not be as affected as upstream

Effectively provides U.S. consumers a “tax cut” of $125 billion-$150 billion1

Lower oil pricing could further boost U.S. GDP ~0.5% in 20152

$0

$50

$100

$150

$200

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

$ /

Bar

rel

Crude Oil, WTI (NYM)

0

20

40

60

80

100

120

(1.5)(1.0)(0.5)0.00.51.01.52.02.5

Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014 Q1 2015 Q1 2016

$ /

Bar

rel

Bar

rels

per

Day

(m

m)

Global Supply less Demand Crude Oil, WTI (NYM)

Oversupply

Undersupply

50% decline

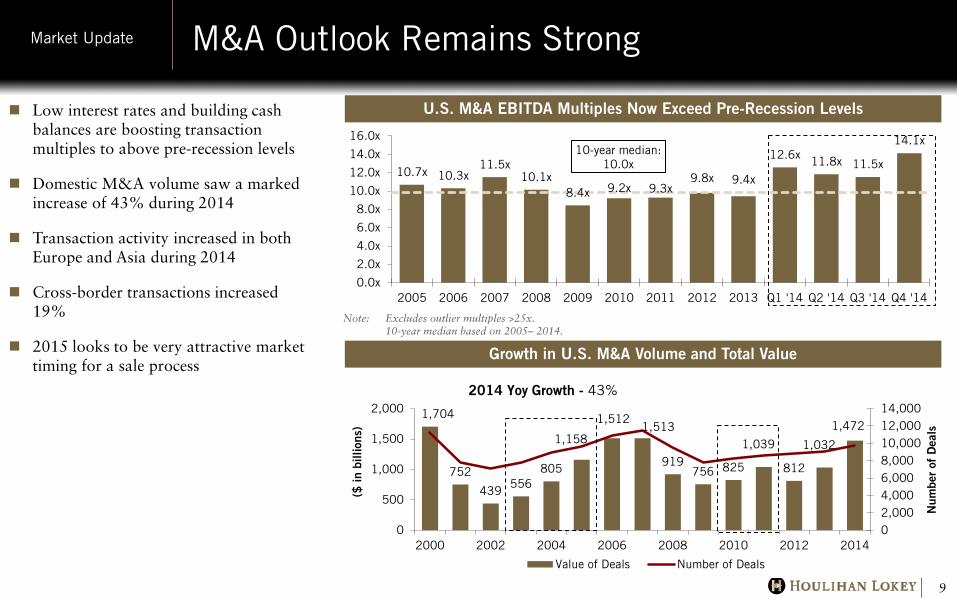

Growth in U.S. M&A Volume and Total Value

U.S. M&A EBITDA Multiples Now Exceed Pre-Recession Levels

M&A Outlook Remains Strong Market Update

9

1,704

752

439 556

805

1,158

1,512 1,513

919 756 825

1,039

812

1,032

1,472

02,0004,0006,0008,00010,00012,00014,000

0

500

1,000

1,500

2,000

2000 2002 2004 2006 2008 2010 2012 2014

Num

ber

of D

eals

($ in

bill

ions

)

Value of Deals Number of Deals

Note: Excludes outlier multiples >25x. 10-year median based on 2005– 2014.

Low interest rates and building cash balances are boosting transaction multiples to above pre-recession levels

Domestic M&A volume saw a marked increase of 43% during 2014

Transaction activity increased in both Europe and Asia during 2014

Cross-border transactions increased 19%

2015 looks to be very attractive market timing for a sale process

2014 Yoy Growth - 43%

10.7x 10.3x 11.5x

10.1x 8.4x 9.2x 9.3x

9.8x 9.4x

12.6x 11.8x 11.5x

14.1x 10-year median:

10.0x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

2005 2006 2007 2008 2009 2010 2011 2012 2013 Q1 '14 Q2 '14 Q3 '14 Q4 '14

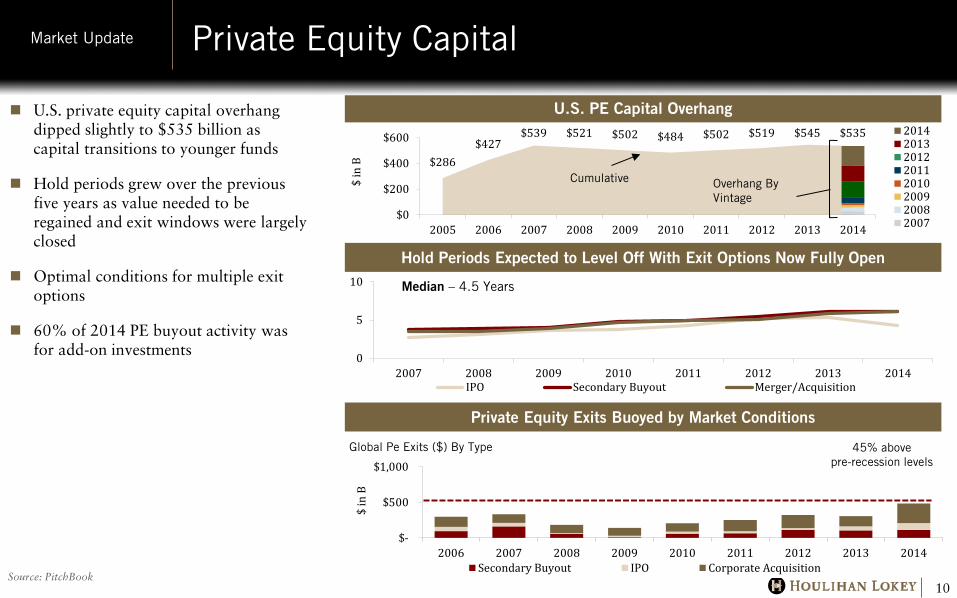

U.S. PE Capital Overhang

Private Equity Capital Market Update

10

$286 $427

$539 $521 $502 $484 $502 $519 $545 $535

$0

$200

$400

$600

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$ in

B

20142013201220112010200920082007

Cumulative Overhang By Vintage

0

5

10

2007 2008 2009 2010 2011 2012 2013 2014IPO Secondary Buyout Merger/Acquisition

$-

$500

$1,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

$ in

B

Global Pe Exits ($) By Type

Secondary Buyout IPO Corporate Acquisition

Hold Periods Expected to Level Off With Exit Options Now Fully Open

Private Equity Exits Buoyed by Market Conditions

Source: PitchBook

Median – 4.5 Years

U.S. private equity capital overhang dipped slightly to $535 billion as capital transitions to younger funds

Hold periods grew over the previous five years as value needed to be regained and exit windows were largely closed

Optimal conditions for multiple exit options

60% of 2014 PE buyout activity was for add-on investments

45% above pre-recession levels

Pre-Recession Levels of Financing Activity Market Update

11

5.2x 3.7x

2.5x 3.4x 3.8x 3.8x

4.6x 5.1x

5.6x

4.5x

3.3x

4.2x 4.3x 4.5x

4.8x 5.3x

0.0x

2.5x

5.0x

7.5xSenior Leverage Subordinated Leverage

Middle Market LBO Leverage Multiples Have Reached Pre-Recession Levels

Growth in U.S. Leveraged Loan New Issue Volume2

Leverage multiples have returned close to pre-recession levels

Default rates fell significantly over the course of 2014 to 0.34%1

Middle-market loan pricing has increased slightly in the last three months to (L+521) with a yield of 6.70%

Leveraged loan volume during Q1-Q3 2014 was on pace to match 2013’s record, until softer conditions in Q4 2014 emerged, still third largest year in history

$295

$480 $535

$157 $77

$236

$377 $466

$607 $529

$0

$200

$400

$600

$800($

in b

illio

ns)

Institutional Pro Rata

Sources: Houlihan Lokey DCM, S&P Leveraged Commentary & Data (1) Excluding TXU (2) Leveraged loan volume averaged $153 billion during Q1-Q3 2014,

but fell to $69 billion in Q4 2014

Key Takeaways Market Update

12

Strength in the U.S. economy during 2015

Industrial companies are financially healthy and spending money

Leverage multiples at historical highs, coupled with low interest rates

M&A volume and valuations are increasing

Private equity has numerous exit options

Lower crude oil prices are expected throughout 2015

Preparation well in advance of a sale is key to achieving a premium valuation…Mike and David can speak to some key ideas for your consideration

2015 looks to be an excellent time for an exit

Value Creation

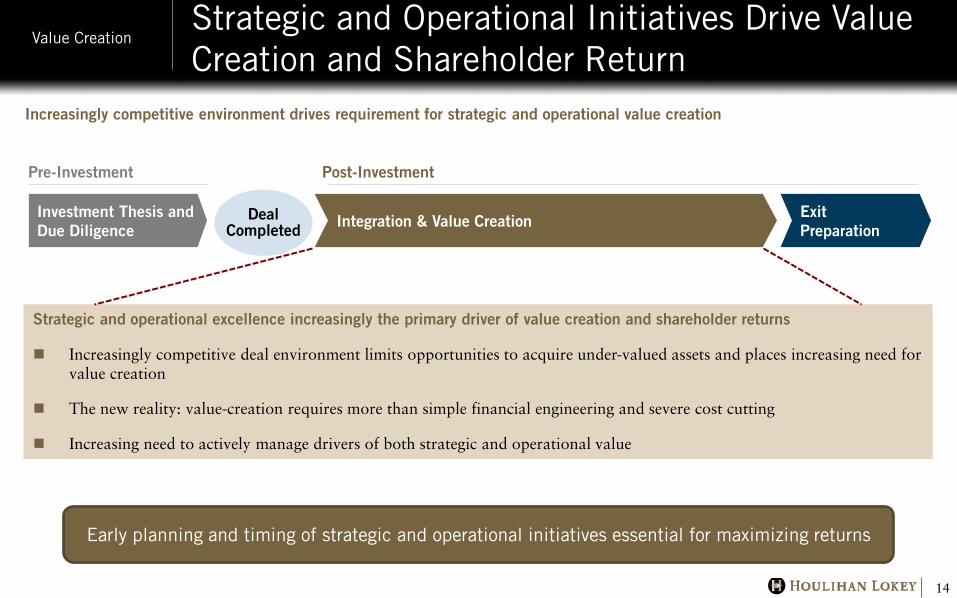

Strategic and Operational Initiatives Drive Value Creation and Shareholder Return

Value Creation

14

Increasingly competitive environment drives requirement for strategic and operational value creation

Investment Thesis and Due Diligence Integration & Value Creation Deal

Completed

Post-Investment Pre-Investment

Exit Preparation

Strategic and operational excellence increasingly the primary driver of value creation and shareholder returns

Increasingly competitive deal environment limits opportunities to acquire under-valued assets and places increasing need for value creation

The new reality: value-creation requires more than simple financial engineering and severe cost cutting

Increasing need to actively manage drivers of both strategic and operational value

Early planning and timing of strategic and operational initiatives essential for maximizing returns

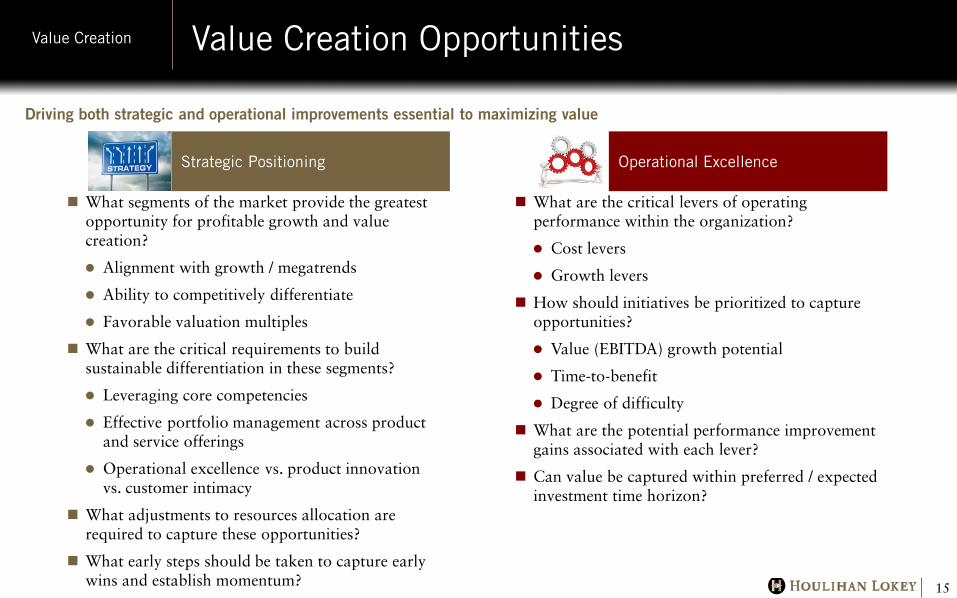

Value Creation Opportunities Value Creation

15

Driving both strategic and operational improvements essential to maximizing value

Strategic Positioning Operational Excellence

What segments of the market provide the greatest opportunity for profitable growth and value creation?

Alignment with growth / megatrends

Ability to competitively differentiate

Favorable valuation multiples

What are the critical requirements to build sustainable differentiation in these segments?

Leveraging core competencies

Effective portfolio management across product and service offerings

Operational excellence vs. product innovation vs. customer intimacy

What adjustments to resources allocation are required to capture these opportunities?

What early steps should be taken to capture early wins and establish momentum?

What are the critical levers of operating performance within the organization?

Cost levers

Growth levers

How should initiatives be prioritized to capture opportunities?

Value (EBITDA) growth potential

Time-to-benefit

Degree of difficulty

What are the potential performance improvement gains associated with each lever?

Can value be captured within preferred / expected investment time horizon?

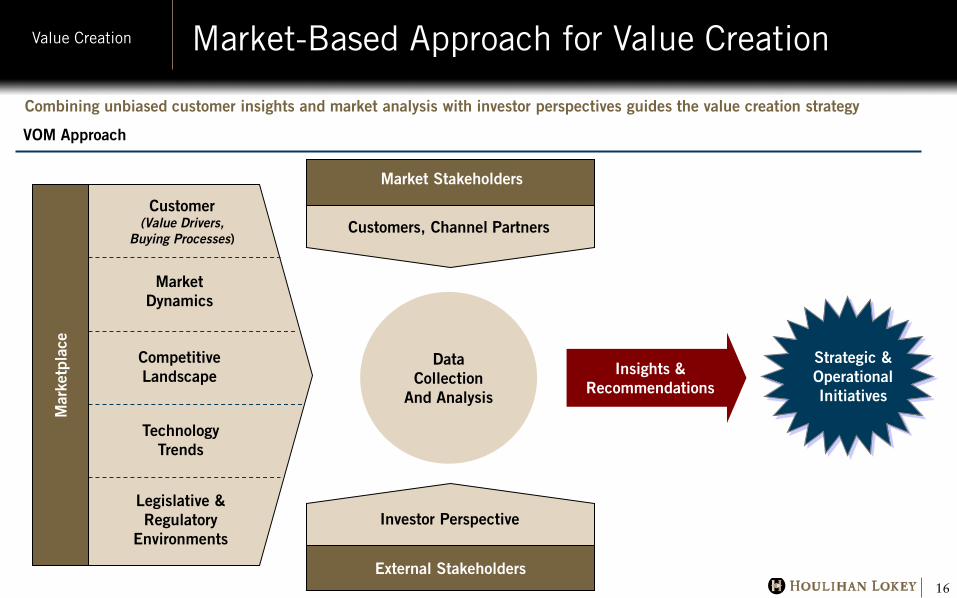

Market-Based Approach for Value Creation Value Creation

16

Combining unbiased customer insights and market analysis with investor perspectives guides the value creation strategy

VOM Approach

Customer (Value Drivers,

Buying Processes)

Market Dynamics

Competitive Landscape

Technology Trends

Legislative & Regulatory

Environments

Mar

ketp

lace

Customers, Channel Partners

Market Stakeholders

External Stakeholders

Investor Perspective

Data Collection

And Analysis

Strategic & Operational Initiatives

Insights & Recommendations

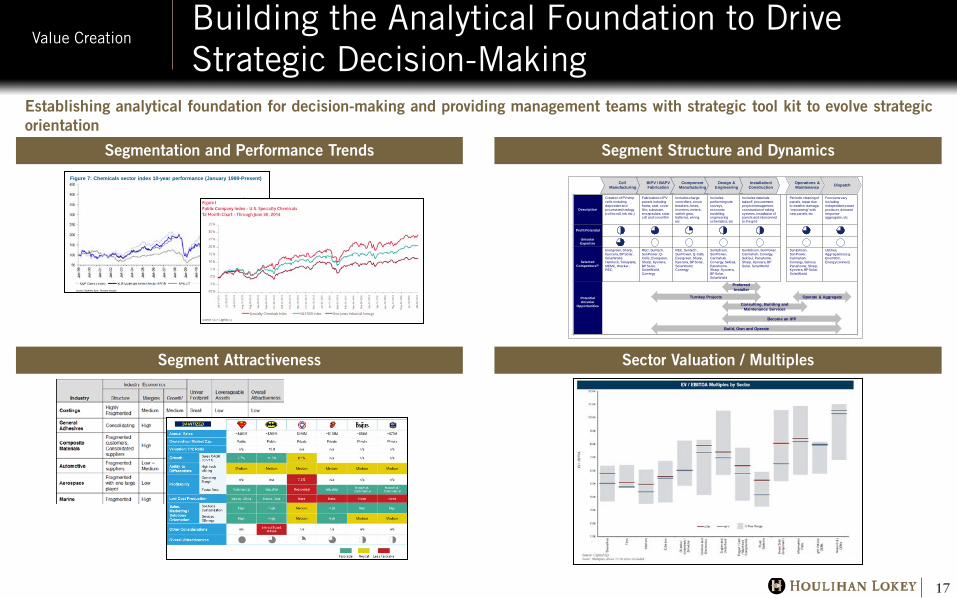

Building the Analytical Foundation to Drive Strategic Decision-Making

Value Creation

17

Establishing analytical foundation for decision-making and providing management teams with strategic tool kit to evolve strategic orientation

Figure 7: Chemicals sector index 10-year performance (January 1999-Present)Cell

ManufacturingBIPV / BAPV Fabrication

Component Manufacturing

Design & Engineering

Installation/ Construction

Operations & Maintenance Dispatch

Description

Creation of PV strip cells including deposition and process technology (roll-to-roll, ink, etc.)

Fabrication of PV panels including frame, seal, cover film, substrate, encapsulant, solar cell and cover film

Includes charge controllers, circuit breakers, fuses, inverters, meters, switch gear, batteries, wiring, etc

Includes performing site surveys, economic modeling, engineering schematics, etc

Includes materials takeoff, procurement, project management, construction of raking systems, installation of panels and interconnect to the grid

Periodic cleaning of panels, repair due to weather damage, “repowering” with new panels, etc

Functions vary including independent power producer, demand response aggregator, etc

Profit Potential

Unisolar Expertise

Selected Competitors(2)

Evergreen, Sharp, Kyocera, BP Solar, SolarWorld, Hemlock, Tokuyama, MEMC, Wacker, REC,

REC, Suntech, SunPower, Q-Cells, Evergreen, Sharp, Kyocera, BP Solar, SolarWorld, Conergy

REC, Suntech, SunPower, Q-Cells, Evergreen, Sharp, Kyocera, BP Solar, SolarWorld, Conergy

SunEdison, SunPower, Carmahah, Conergy, Sekisui, Panahome, Sharp, Kyocera, BP Solar, SolarWorld

SunEdison, SunPower, Carmahah, Conergy, Sekisui, Panahome, Sharp, Kyocera, BP Solar, SolarWorld

SunEdison, SunPower, Carmahah,Conergy, Sekisui, Panahome, Sharp, Kyocera, BP Solar, SolarWorld

Utilities,Aggregators (e.g. EnerNOC, EnergyConnect)

Potential Unisolar

Opportunities

Preferred Installer

Turnkey Projects

Consulting, Building and Maintenance Services

Become an IPP

Build, Own and Operate

Operate & Aggregate

Segmentation and Performance Trends Segment Structure and Dynamics

Segment Attractiveness Sector Valuation / Multiples

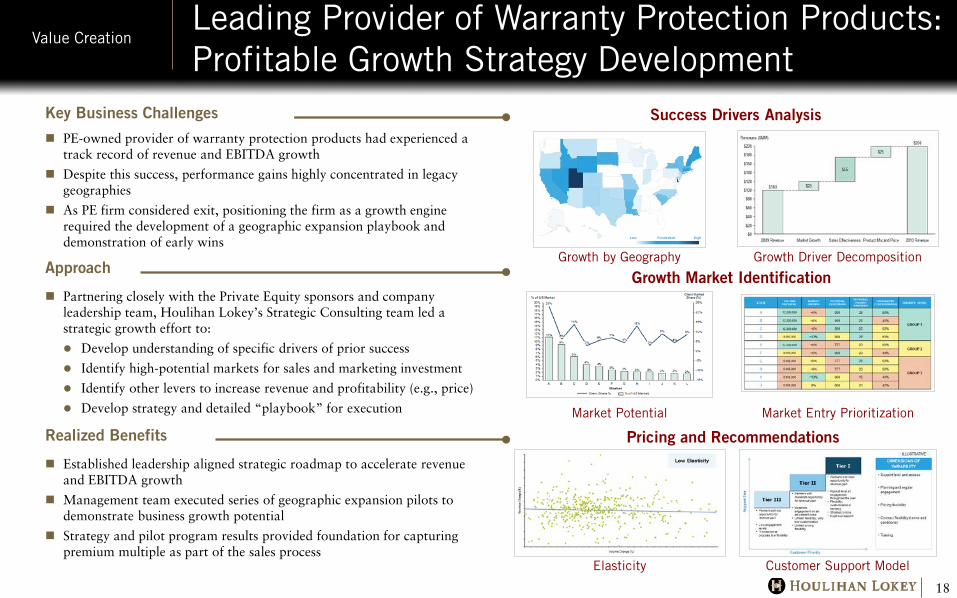

Leading Provider of Warranty Protection Products: Profitable Growth Strategy Development

Value Creation

18

Key Business Challenges

PE-owned provider of warranty protection products had experienced a track record of revenue and EBITDA growth

Despite this success, performance gains highly concentrated in legacy geographies

As PE firm considered exit, positioning the firm as a growth engine required the development of a geographic expansion playbook and demonstration of early wins

Approach

Partnering closely with the Private Equity sponsors and company leadership team, Houlihan Lokey’s Strategic Consulting team led a strategic growth effort to:

Develop understanding of specific drivers of prior success

Identify high-potential markets for sales and marketing investment

Identify other levers to increase revenue and profitability (e.g., price)

Develop strategy and detailed “playbook” for execution

Realized Benefits

Established leadership aligned strategic roadmap to accelerate revenue and EBITDA growth

Management team executed series of geographic expansion pilots to demonstrate business growth potential

Strategy and pilot program results provided foundation for capturing premium multiple as part of the sales process

Growth Market Identification

Pricing and Recommendations

Success Drivers Analysis

Growth by Geography Growth Driver Decomposition

Market Potential

Customer Support Model Elasticity

Market Entry Prioritization

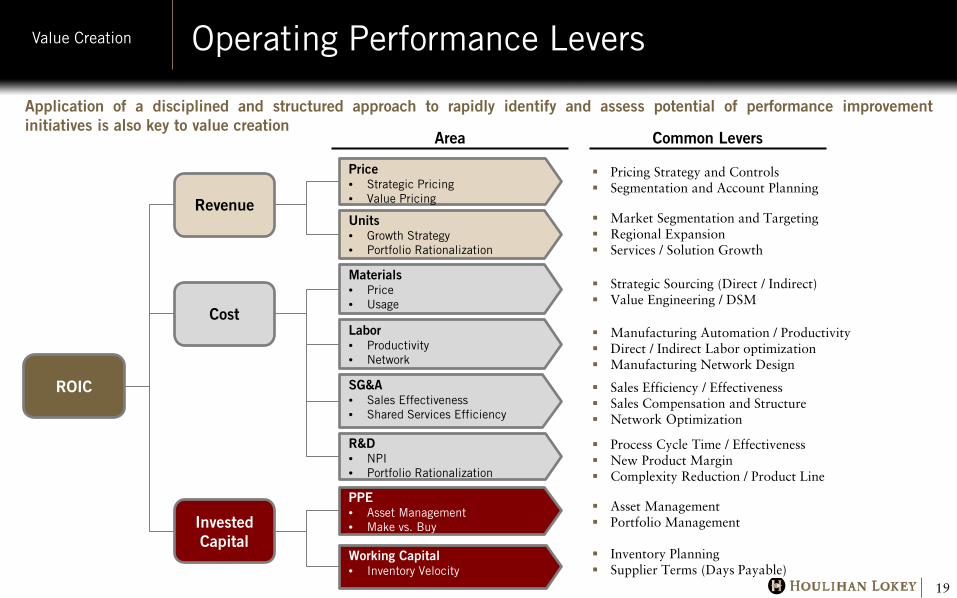

Operating Performance Levers Value Creation

19

Application of a disciplined and structured approach to rapidly identify and assess potential of performance improvement initiatives is also key to value creation

Strategic Sourcing (Direct / Indirect) Value Engineering / DSM

ROIC

Revenue

Cost

Invested Capital

Price • Strategic Pricing • Value Pricing

Units • Growth Strategy • Portfolio Rationalization

Materials • Price • Usage

Labor • Productivity • Network

SG&A • Sales Effectiveness • Shared Services Efficiency

R&D • NPI • Portfolio Rationalization

PPE • Asset Management • Make vs. Buy

Working Capital • Inventory Velocity

Inventory Planning Supplier Terms (Days Payable)

Manufacturing Automation / Productivity Direct / Indirect Labor optimization Manufacturing Network Design

Asset Management Portfolio Management

Process Cycle Time / Effectiveness New Product Margin Complexity Reduction / Product Line

Pricing Strategy and Controls Segmentation and Account Planning

Market Segmentation and Targeting Regional Expansion Services / Solution Growth

Sales Efficiency / Effectiveness Sales Compensation and Structure Network Optimization

Area Common Levers

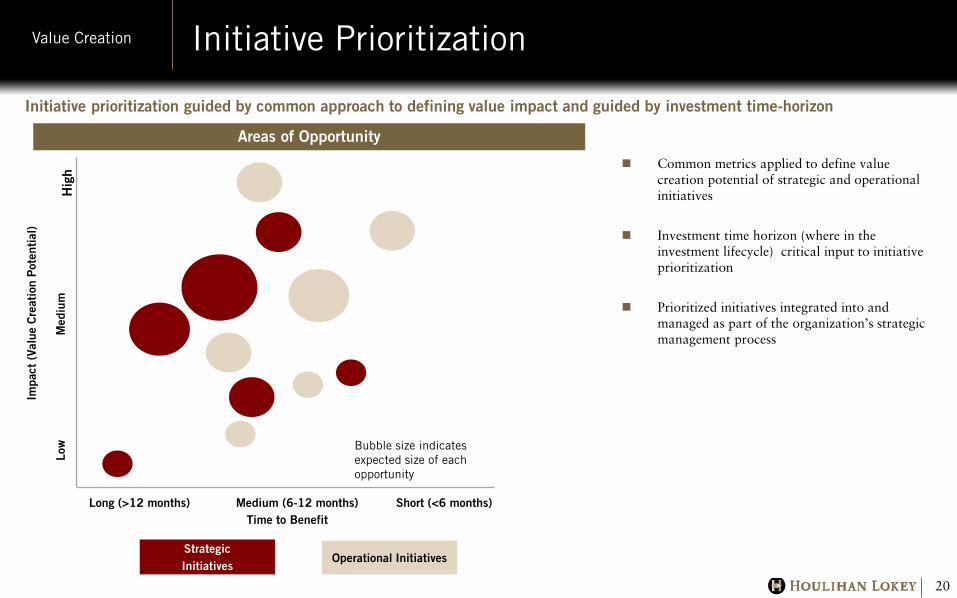

Initiative Prioritization Value Creation

20

Initiative prioritization guided by common approach to defining value impact and guided by investment time-horizon

Hig

h

Strategic Initiatives

Operational Initiatives

Time to Benefit Long (>12 months) Medium (6-12 months) Short (<6 months)

Low

M

ediu

m

Impa

ct (

Valu

e C

reat

ion

Pot

enti

al)

Bubble size indicates expected size of each opportunity

Common metrics applied to define value creation potential of strategic and operational initiatives

Investment time horizon (where in the investment lifecycle) critical input to initiative prioritization

Prioritized initiatives integrated into and managed as part of the organization’s strategic management process

Areas of Opportunity

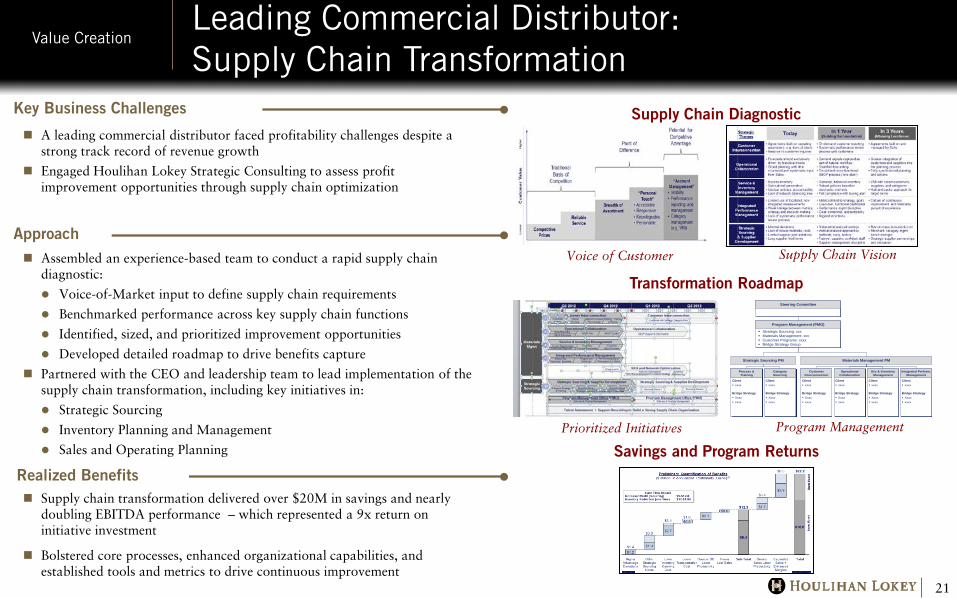

Leading Commercial Distributor: Supply Chain Transformation

Value Creation

21

Key Business Challenges

A leading commercial distributor faced profitability challenges despite a strong track record of revenue growth

Engaged Houlihan Lokey Strategic Consulting to assess profit improvement opportunities through supply chain optimization

Approach Assembled an experience-based team to conduct a rapid supply chain

diagnostic:

Voice-of-Market input to define supply chain requirements

Benchmarked performance across key supply chain functions

Identified, sized, and prioritized improvement opportunities

Developed detailed roadmap to drive benefits capture

Partnered with the CEO and leadership team to lead implementation of the supply chain transformation, including key initiatives in:

Strategic Sourcing

Inventory Planning and Management

Sales and Operating Planning

Realized Benefits Supply chain transformation delivered over $20M in savings and nearly

doubling EBITDA performance – which represented a 9x return on initiative investment

Bolstered core processes, enhanced organizational capabilities, and established tools and metrics to drive continuous improvement

Supply Chain Diagnostic

Transformation Roadmap

Savings and Program Returns

Client xxxx

Bridge Strategy Xxxx

xxxx

Process &Training

Steering Committee

Strategic Sourcing: xxx Materials Management: xxx Customer Programs: xxxx Bridge Strategy Group

Program Management (PMO)

Materials Management PM

Client xxxx

Bridge Strategy Xxxx

xxxx

CategorySourcing

Client xxxx

Bridge Strategy Xxxx

xxxx

Customer Interconnection

Client xxxx

Bridge Strategy Xxxx

xxxx

Operational Collaboration

Client xxxx

Bridge Strategy Xxxx

xxxx

Svc & Inventory Management

Client xxxx

Bridge Strategy Xxxx

xxxx

Integrated Perform. Management

Strategic Sourcing PM

Voice of Customer Supply Chain Vision

Prioritized Initiatives Program Management

Summary Value Creation

22

A disciplined approach to value creation – one that goes beyond financial engineering and pure cost cutting – is necessary

That approach should judiciously balance initiatives focused on operational excellence and strategic positioning

Such approaches and initiatives should be planned (and executed) earlier in the investment cycle rather than being shoe-horned in right before exit

Well-executed set of initiatives can deliver significant and differentiated value to key stakeholders and shareholders

Exiting corporate investments now is attractive

One wants to be as ready as possible prior to any harvesting event

Advancing new initiatives can drive incremental value

Appendix

Leading Advisor in Industrials Sector Appendix

24

Houlihan Lokey closes more middle market and industrials transactions than any other firm

453

353

294 284 283

200

250

300

350

400

450

500

Num

ber

of D

eals

No. 1 M&A Advisor to the Middle Market Recognized Market Leader

Completed Transactions Under $1 Billion since 2010 2014 M&A Advisory Rankings

U.S. Transactions Under $5 Billion

Rank AdvisorNumber of Deals

1 Houlihan Lokey 1432 Goldman Sachs & Co 141

3 JP Morgan 127

4 Barclays 110

5 Morgan Stanley 109

6 Bank of America Merrill Lynch 98

7 Credit Suisse 92

8 * Evercore Partners 90

8 * Citi 90

10 RBC Capital Markets 84

* denotes tie.

Source: Thomson Reuters

AdvisorNumber of

Deals

1 Houlihan Lokey 272 * Goldman Sachs & Co 262 * Citi 262 * Barclays 265 * Lincoln International 255 * Generational Equity 257 Lazard 228 Morgan Stanley 219 * JP Morgan 199 * Moelis & Co 199 * Bank of America Merrill Lynch 199 * Stout Risius Ross Inc 19

* denotes tie.

Source: Thomson Reuters.

2014 M&A Advisory RankingsU.S. Industrial Deals Under $1 Billion

Rank

J. Francis “Jim” Lavelle Appendix

25

Mr. Lavelle is a Managing Director and Co-Head of Houlihan Lokey’s Industrials Group. He has worked in investment banking for more than 25 years and is equally comfortable on domestic and cross-border transactions. Mr. Lavelle became a Houlihan Lokey shareholder in 2004 and is a member of the firm’s global management committee as well as its client approval committee. He is based in the firm’s New York office.

Mr. Lavelle co-heads the firm’s Industrials Group, which comprises the metals, mining, transportation, chemicals, plastics and packaging, industrial technologies, environmental and industrial services, and other related sectors. The bulk of his career has been focused on the industrial technologies and environmental and industrial services sectors.

Mr. Lavelle came to Houlihan Lokey in 2004 from The Nassau Group, a corporate strategy and M&A advisory firm that he founded and successfully managed for more than 12 years. His clients include numerous North American, European, and Asian public and private companies, ranging from emerging growth-oriented businesses to established middle-market leaders, to multibillion-dollar global enterprises. His assignments have ranged from integrated strategic advisory and/or proactive buyside mandates for large, strategic acquirers, to financial restructurings for financial sponsors, to exclusive sellside projects. He has also managed several private placements.

Before establishing Nassau, Mr. Lavelle spent five years at Baring Brothers & Co. in New York and London. Earlier, he was at Booz Allen & Hamilton, where his fields of expertise were international M&A advice and business strategy development.

Mr. Lavelle graduated cum laude with an A.B. from the Woodrow Wilson School of Public and International Affairs at Princeton University.

Michael Jennings Appendix

26

Mr. Jennings is a Managing Director in Houlihan Lokey’s Strategic Consulting business. He has more than a decade of strategy consulting and hands-on general management experience with industrial and consumer goods companies. Mr. Jennings is based in the firm’s Chicago office.

Mr. Jennings has advised industrial, consumer, energy, and technology clients throughout his career. Before joining Houlihan Lokey, he joined Bridge Strategy Group LLC, a management consulting firm, in 2000. He spent the first 10 years of his career as a general manager for Fortune 500 industrial and consumer goods companies. Mr. Jennings’ areas of expertise include corporate and business unit strategy, sales and marketing strategy, and supply chain management.

Mr. Jennings holds an MBA from Northwestern University’s Kellogg School of Management, a B.S. in Engineering from Washington University in St. Louis, and a B.A. in Physics from Grinnell College.

David Calfee Appendix

27

Mr. Calfee is a Managing Director in Houlihan Lokey’s Strategic Consulting business. He is an expert in strategy, human capital, and change management. Mr. Calfee is based in the firm’s Chicago office.

Before joining Houlihan Lokey, Mr. Calfee was a founder of Bridge Strategy Group LLC, a management consulting firm. He was also a leader of Renaissance Worldwide, CSC Index, and McKinsey & Co. Mr. Calfee’s expertise covers a wide variety of industries, including consumer, commercial, and industrial goods and services organizations, coupled with functional experience in strategy development and execution, human resources management, and change leadership.

Mr. Calfee holds an MBA with distinction from Northwestern University’s Kellogg School of Management, a J.D. from the University of Chicago Law School, and an A.B. cum laude from Harvard College.

Disclaimer Appendix

28

© 2014 Houlihan Lokey. All rights reserved. This material may not be reproduced in any format by any means or redistributed without the prior written consent of Houlihan Lokey.

Houlihan Lokey is a trade name for Houlihan Lokey, Inc. and its subsidiaries and affiliates which include: Houlihan Lokey Capital, Inc., a California corporation, a registered broker-dealer and SIPC member firm, which provides investment banking, capital markets, private placement, merger, acquisition and divestiture services; Houlihan Lokey Financial Advisors, Inc., a California corporation, which provides financial advisory, fairness opinion, solvency opinion, valuation opinion, restructuring advisory and portfolio management services; Houlihan Lokey Consulting, Inc., a California corporation, which provides strategic consulting services; and Houlihan Lokey (Europe) Limited, a company incorporated in England which is authorized and regulated by the U.K. Financial Conduct Authority and Houlihan Lokey (China) Limited, a company incorporated in Hong Kong SAR which is licensed in Hong Kong by the Securities and Futures Commission to conduct Type 1, 4 and 6 regulated activities to professional investors only, which provide investment banking, restructuring advisory, merger, acquisition and divestiture services, valuation opinion and private placement services and which may direct this communication within the European Economic Area and Hong Kong, respectively, to intended recipients including professional investors, high-net-worth companies or other institutional investors.

Houlihan Lokey gathers its data from sources it considers reliable; however, it does not guarantee the accuracy or completeness of the information provided within this presentation. The material presented reflects information known to the authors at the time this presentation was written, and this information is subject to change. Houlihan Lokey makes no representations or warranties, expressed or implied, regarding the accuracy of this material. The views expressed in this material accurately reflect the personal views of the authors regarding the subject securities and issuers and do not necessarily coincide with those of Houlihan Lokey. Officers, directors and partners in the Houlihan Lokey group of companies may have positions in the securities of the companies discussed. This presentation does not constitute advice or a recommendation, offer or solicitation with respect to the securities of any company discussed herein, is not intended to provide information upon which to base an investment decision, and should not be construed as such. Houlihan Lokey or its affiliates may from time to time provide investment banking or related services to these companies. Like all Houlihan Lokey employees, the authors of this presentation receive compensation that is affected by overall firm profitability.

![IN THE UNITED STATES BANKRUPTCY COURT FOR THE …€¦ · Objection to Retention of Houlihan Lokey [Dkt. No. 347, Aug. 6, 2009] (“The Official Committee believes that the Debtors’](https://img.pdfslide.net/doc/110x75/5f0b75717e708231d4309eaf/in-the-united-states-bankruptcy-court-for-the-objection-to-retention-of-houlihan.jpg)