Embed Size (px)

Citation preview

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 1/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

Lesson: Introduction to Microeconomics

Lesson Developer: Dipavali Debroy

College/Department: SGGSCC, University of Delhi

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 2/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

Table of Contents1.Learning Outcomes2.Introduction3. Evolution of the Subject4. Methodology of Economics: Positive Economics and Normative Economics

5. Art or Science6. Scope of Economics - Related Subjects7. Models and Hypotheses8. Market and Equilibrium

8.1 Demand and Supply9. Concept of ceteris paribus – General Equilibrium Partial Equilibrium10. Static and Dynamic Equilibrium11. Short-Run and Long Run Equilibrium12. Nobel Prize in Economics13. Summary14. Exercises15. Glossary16. References17. Activity18. Quiz

1.Learning Outcomes

After you have read this chapter you should be able to define Micro-Economics. Macro-Economics, Market, Demand, Supply, Equilibrium, Partialand General Equilibrium, Static and Dynamic Equilibrium understand thecentral problems of an economy identify variables, constants andparameters differentiate Micro-Economics from Macro-Economics appreciatethe scope of the subject of Economics apply the knowledge of basic

Economics

2. Introduction

Micro-Economics is the branch of Economics that studies economic issues minutelyin individual details, as if under a microscope. In contrast, Macro-Economics is thebranch of Economics that studies economic issues in aggregative and overall forms,looking at the broad picture. . The word Micro comes from the Greek word Micros (small). Macro comes from Greek macros ( long or huge). Micro-Economics andMacro-Economics are thus two complements of the subject of Economics

But what is Economics?

Value Addition 1: Focus of the SectionTopic EconomicsThis section is to make you aware of what Economics is.The purpose of this section is to make you familiar with the variousDefinitions of Economics, the Evolution of the subject, its Scope,Methodology, Tools and Basic Concepts Concepts.

Text for the section

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 3/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

According to the renowned economist Alfred Marshall, it is the study of humanbeings as they go about their everyday life.To quote from Marshall’s Principles of Economics (1890, "a study of mankind in theordinary business of life; it (Economics) examines that part of individual and socialaction which is most closely connected with the attainment and with the use of thematerial requisites of wellbeing. Thus it is on one side a study of wealth; and on the

other, and more important side, a part of the study of man." For decades this wasthe most accepted definition till, in 1935, Lionel Robbins focused on another aspectof the subject and defined it as the study of choice under conditions of scarcity."Economics is a science which studies human behavior as a relationship between

ends and scarce means which have alternative uses."Productive Resources ( land, labour, capital goods such as machinery, technicalknowledge) are scarce or limited and the resource applied to the production of acertain commodity or service is unavailable for the production of another alternativeone. But human wants for the Consumption of goods and services ( cereals andpulses, meat and fish and poultry, vegetable, clothes, woolens, houses, roads, cars,railways, airplanes, books, theatre , film, television and countless others) areunlimited, and come from numerous members of the society .Economics is the studyof how people can choose to use the scarce or limited resources to produce variousgood and services and distribute them to various members of society for theirconsumption.The Central Problems of an Economy

Any society faces three fundamental and interdependent economic problems :1. What to Produce and How Much of them2. How to Produce, that is, by whom and by what resources and technology3. For Whom to Produce, that is, how is the total amount of production in the

society to be distributed among its members.Different kinds of society have different ways of solving them. A tribal society huntsand forages together and shares the fruits of their labour more or less equally. In thefeudal society , the serfs produce and pay certain shares of the production to the

feudal lords as per the traditions established by the lords. An advanced capitalistsociety produces through a complicated division of labour and distributes the totalproduct in a complex and unequal way.In a socialist state, central planning takes care of production and its equitabledistribution.But all societies must face the three problems :What to Produce, How and For Whom; in more technical terms, the problems of Allocation, Choice of Techniques andDistribution.The Production Possibility curve or frontier is a geometrical way of depicting thischoice problem. It depicts the production possibilities or “menu” as Paul Samuelsonhad put it.Suppose a society or economy, using all its resources fully, has the option ofproducing any combination out of a maximum of , say, food crops (represented bythe symbol X), and a maximum of aero planes (Y).Represent food crops (X) on the horizontal axis and aero planes (Y) on the vertical.Each point on the X-Y plane would then represent a numerical combination of foodgrains and aero plane.Suppose we have the following chart of alternative combinations of the maximumnumber of aero planes that can be produced along with a certain amount of foodgrains, or vice versa. That is, we have a chart of alternative combinations ofmaximum Y’s going with different X’s ( or, combinations of maximum X’s going with

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 4/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

different Y’s).Each such combination has its position on the X -y plane. Join them toget the Production Possibility Curve (PPC).Each point on the PPC represents a maximum of X ( at a certain Y) or a maximum ofY ( at a certain X). All points below and including the PPC represents combinations ofX and Y that are Attainable by the society concerned but only points on the PPCrepresent points of maximum X(given the Y’s) or maximum Y ( given the X’s). Points

below the PPC ( including the two axes and so, the origin) represent what the societyconcerned can produce but without using its (scarce) resources fully.

When, for some reason or the other, the society becomes capable of producing moreof X ( at every given Y) or more of Y (at every given X), the PPC curve shiftsforward. This indicates Economic Growth. When the reverse happens, the PPCshrinks back.

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 5/16

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 6/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

`marginalists’) were Menger, Jevons and Alfred Marshall. It i s their work thatconstitutes the foundation of Micro- economics. Especially Marshall’s Principles ofEconomics ( published first in 1890).There evolved the concept of the `economicman’, that is, the individual producer or consumer, who made his choices or decisions perfectly rationally. On the basis of his preferences or cost patterns, theconsumer’s objective was always to maximize his utility or satisfaction and the

producer’s, to maximize his profits. The individual consumer or producer was the unitconcerned, not the entire national entity.Although the Classical economists had been concerned with the nation or the countryas a whole, and therefore are more macro than micro, Macro-economics as an areaof study began really after the Great Depression of the 1930s. Europe and Americaboth suffered from it and so did their colonies in other parts of the globe. Widespreadunemployment followed the closing down of production units. Both employers andemployees suffered. It was then that John Maynard Keynes came up with hisanalysis of the phenomenon in terms of Aggregate Demand falling short ofAggregate Supply and emphasized the role of the Government of a country in

stepping up its own expenditure in order to give Aggregate Demand a boost.His analysis laid the foundation of Macro-Economics. Later John Hicks, MiltonFriedman, Lucas and others have contributed to the subject of Macro-Economics.Paul. Samuelson has emphasized that there is no essential opposition betweenMacro-Economics and Micro-Economic s. Both are “vital” to the understanding of thesubject ( Economics , 7 th edn, p 362). It is usual in most universities to offer a coursein Micro-Economics prior to that in Macro-Economics. But it is not a necessarypractice and is changing.In the words of Paul A. Samuelson. “Macroeconomics deals with the big picture – with the macro aggregates of income, employment, and price levels. But do notthink that microeconomics deals with unimportant details. After all, the big picture ismade up of its parts.” ( Economics , 7 th edn, p 362)

4. The Methodology of Economics – Positive Economics and NormativeEconomics

Economics can be subjected to another distinction, that between Positive Economicsand Negative Economics. The distinction is that between `what is ’ and `what oughtto be’ so far as economic issues are concerned. To `posit’ means to state or evenexplain something as an objective principle or fact. A `norm’ on the other handmeans a standard or ideal set up subjectively.According to economists like Milton Friedman ( who wrote Essays in PositiveEconomics, 1953), economists should not pass moral strictures or make v̀alue

judgements’. In other words, Economics should just `posit’ or be Positive. It cansay:’ If the price of a commodity goes up, its quantity consumed falls, other thingsremaining the same’. But it should not go on to pass judgements or give advice such as : ‘If the price of acommodity goes up, its consumer should reduce the quantity to be consumed.That does not mean that Economics cannot contain policy prescriptions. It simplymeans that such prescriptions or recommendations should be expressed in anobjective way.E.g.,’ If there is economic depression and the government increases its consumptionexpenditure, the depression is likel y to get corrected’. To state it as follows is to be normative:

‘If there is economic depression, the government of the country should increase itsconsumption expenditure’.

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 7/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

5. Art or Science

Several decades ago, textbooks in Economics often discussed this issue: IsEconomics a science or an art? Etymologically, a science ( derived from sci, toknow) provides theoretical knowledge while an art ( derived from artem, to do)teaches us how to practice or do it. Now Economics teaches us all about, say, how a

producer maximized his profits. But it does not teach him how to make profits. Fromthis point of view, it is a science rather than an art. Again, the recent theoreticaldevelopments in Economics have made so much use of Mathematics, that a soundknowledge of Mathematics is essential even for its undergraduate Honours course,e.g., in Delhi University itself. This takes Economics closer to being a Sciencesubject.However, the hallmark of science is experiment. A science must provide room forcontrolled experiment so as to verify its hypotheses. But human beings cannot besubjected to experiments just to find out the effects of policies. In this sense,Economics definitely belongs to the Humanities stream. Most universities, regardEconomics as an art and award BA and MA degrees in it. However The LondonSchool of Economics does, in fact, award BSc and MSc degrees to its students ofEconomics.Indeed the scope of Economics is so wide that it is difficult to categories it as eitherscience or art. It is perhaps a mixture of both.As Paul Samuelson put it, “ Not only is Economics at once art and a science,economics as a subject can combine the attractive features of both the humanitiesand the sciences”(Economics, 7 th edn, Chapter 1,p 4).

A Social Science

Even if we use the term science to describe Economics, we must remember that it isa Social Science. It does not study individuals in isolation, doing everything byoneself. It studies individuals as members of a society or nation or Economy.An economy is the same as country or society but considered only in its economic

aspects. Every society or country has numerous people engaged in activities of allsorts. Some work in the fields, some work in factories, and yet others in offices.Some perform agricultural activities, some industrial, and some do services. Thosewho are in agriculture need to get industrial products and, say, banking services.Those who are factory-workers, say, need to get hold of foodstuff, and use somekind of transport services. The people engaged in the services sector need both foodand clothing . Thus all the three sectors with their separate kinds of activities need tohave relations. All the people of an economy need to act as well as inter-act. Thisthey do by exchanging the products of their various activities in various markets.The epithet `Social’ covers this aspect of the subject of Economics.

However, for analytical purposes, Economics sometimes uses the concept of aRobinson Crusoe Economy, or an economy consisting of a single person performingall the economic activities by himself. Robinson Crusoe is the title of a book writtenin 1719 by Daniel Defoe based on the life of Alexander Selkirk who was marooned onan island and survived all by himself for 28 years. A Robinson Crusoe Economy isthus a theoretical concept where the economy has a singleton member.

6. Scope of Economics - Related Subjects

Economics has a wide scope and has connections with various subjects.Mathematics and Statistics are necessary for the study of Economics. Mathematicshelps economists to analyze economic realities, to and derive conclusions from

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 8/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

them. Statistics aids this process by systematizing the economic realities as data andinferring from them by accepted statistical tools. In fact, the application of Statisticsto Economics had led to the development of a relatively new subject: Econometrics.It helps in empirical study and making projections both into the past and the future.Without a sound mathematical base, it is next to impossible to cope with academicEconomics. However, to have an general awareness of the economic occurrences of

the world, basic intelligence will do. To quote Samuelson, “ Although everyintroductory textbook must contain geometrical diagrams, knowledge ofmathematics itself is needed only for the higher reaches of economic theory. Logicalreasoning is the key to success in the mastery of basic economic principles, andshrewd weighing of empirical evidence is the key to success in mastery of economicappli cations.”( Economics, Ch 1. p 5) Actually, the earlier term for Economics was Political Economy. Several universitiesstill have a common department for Politics and Economics. Political Science is anuseful subject to supplement a course in Economics. History is also a subject thathas a close connection with Economics. Economic History is a compulsory paper inevery course in Economics, undergraduate as well as post-graduate. Severaluniversities offer a post-graduate course in Economic Geography.In recent times several subjects or courses have emerged from Economics, e.g.,Commerce, Business Economics, Business Administration, Business Management.While based on the fundamentals of Economics, they have their own distinctivecourse contents. But both Papers on Micro-Economics and Macro-Economics figure inall of them.

7. Models and Hypotheses

Economics has to deal with a complex mass of realities. So it sometimes puts theminto a simplified framework or Model. A Model is a theoretical construct thatrepresents economic realities by a set of inter-related variables. These relationshipscan be logical or quantitative. But putting them in a Model helps economists toanalyze realities better and even made future predictions.

Economist often posit or propose explanations for economic phenomena. These areknown as Hypotheses. A hypothesis is not a theory. Only if a Hypothesis is verifiedor found to be true, can we call it a Theory . To be verified or falsified, that is tested,a hypothesis has to be framed in a certain way. Such a hypotheses is called aScientific hypothesis . Sometimes economists have no alternative but to take acertain hypothesis to be true, and proceed on the basis of it. Such a hypothesis iscalled a Working hypothesis. Statistics and Econometrics are the tools used inverifying a hypothesis.

Laws of Economics

The Classical and Neoclassical economists often used the term `law’ to describe thetendencies that they observed in functioning of the economy or society. The Law ofDemand, t he Law of Diminishing Returns, Say’s Law , Okun’s law are just a fewexamples. In no sense are these binding or enforceable or universal laws.However, law in the usual sense of the term does have a close connection withEconomics. For the market to function well, there must be law and order in thecountry. This is a basic idea of Neo-Classical Economics. Laws influence economicoccurrences. For example, the Permanent Settlement of 1793 had a far-reachinginfluence on India’s agriculture. After Independen ce, the government had to passseveral Abolition of Intermediaries Acts in order to correct the agricultural situation.The Monopolistic and Restrictive Trade Practices Act, the Consumer Protection Act ,

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 9/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

the various economic reforms, all testify to the close connection between Law andEconomics.

8. Market and Equilibrium

The word Market comes from Latin mercatus which meant trading, buying or selling

at an appointed time or place. A market is not necessarily a marketplace. It is acontext or background where buying and selling are taking place. The haat, bazaarand mandi , the shop and the mall are markets. But on line or telephonic sale andpurchase , which is quite common these days, are also market transactions.The distinguishing feature of the market is that market transactions are exchanges , usually performed through the medium of money . The seller ( who is sometimesthough not always the producer) of certain commodities/ services brings them to themarket and offers certain quantities of quantities of them at a certain price . Hethus supplies them in the market. The (prospective) buyer comes to the marketwanting to get certain commodities/ services at a certain price. He thus demands them in the market. If the demand of the buyer and the supply of the seller match ata certain configuration of price and quantity, the transaction takes place. If not, itdoes not.The transaction is thus both a sale and a purchase. It is sale from the point of viewof the Seller(producer) , that is, from the Supply side. It is purchase from the pointof view of the Buyer, that is, the Demand side.The transaction has two aspects or dimensions to it, viz., a quantity and a price. Forexample, the seller is agreeable to selling 2 kegs of rice at the rate of Rest 50, andthe buyer finds this offer reasonable. “Two kgs of rice at Rs 50” is then thedescription of the transaction. The total amount spent by the buyer/ consumer andreceived by the seller/supplier is thus Rs 100 (50 x 2), and this is called theExpendi ture from the buyer’s point of view and the Revenue from the seller’s. Thetransaction configuration and the total expenditure/revenue are thus distinctconcepts.The transaction configuration is known as the Equilibrium configuration, or simply,

Equilibrium. It is called so because it represents a matching or balancing of twoaspects – the Buyer’s and the Seller’s, that is, the Demand side and the Supply side. In Latin, aequus means equal and libra means scales or balances.( That is why in theZodiac, the sign Libra is shown by a pair of scales). When the two scales on the twosides of a scales instrument hang at the same level, there is aequilibrium , or, inEnglish, Equilibrium. Neither of the scales go up or down any more, and unless thereis some external disturbance, the balance, or equilibrium, holds.

8.1 Demand and Supply

The word Demand is from Latin demandare which means to claim or commission.Supply is from Latin supplere which means to fill up or complete.In the context of Economics it was Adam Smith in 1776 who first used them ascorresponding concepts. Marshall has compared them to the two blades of a pair ofscissors. Just as the scissors cannot work without either of the two blades, MarketEquilibrium cannot be determined without reference to both Demand and Supply.

Demand is desire backed by purchasing power. A buyer or consumer does notmerely desire a commodity or good (or service) but has some power or wherewithalto purchase it at a price. Similarly, a seller or producer does not merely offer hiscommodity or good (or service) but offers them at a price.

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 10/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

There exists at any one time a definite relationship between the marketprice of a good and the quantity demanded of that good. This relationshipbetween price and quantity demanded/bought is called the Demandschedule or Demand function or Demand curve.

One usual form that the Demand curve can take is downward-sloping from left toright. Based on the Demand schedule below, this is depicted as follows:

Demand Schedule

Price(P) Quantity Demanded (Qd)Rs per kg Kg

A 5 9B 4 10C 3 12D 2 15E 1 20

Demand Curve

Prices are measures on the vertical axis and the quantities demanded on thehorizontal. Each pair of Q,P numbers from the Demand Schedule is plotted here as apoint on the Q-P plane, and a smooth curve passed through the points to yield the

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 11/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

Demand `curve’. It slopes downwards from Left to Right, showing an Inverse orNegative relation between price and quantity.

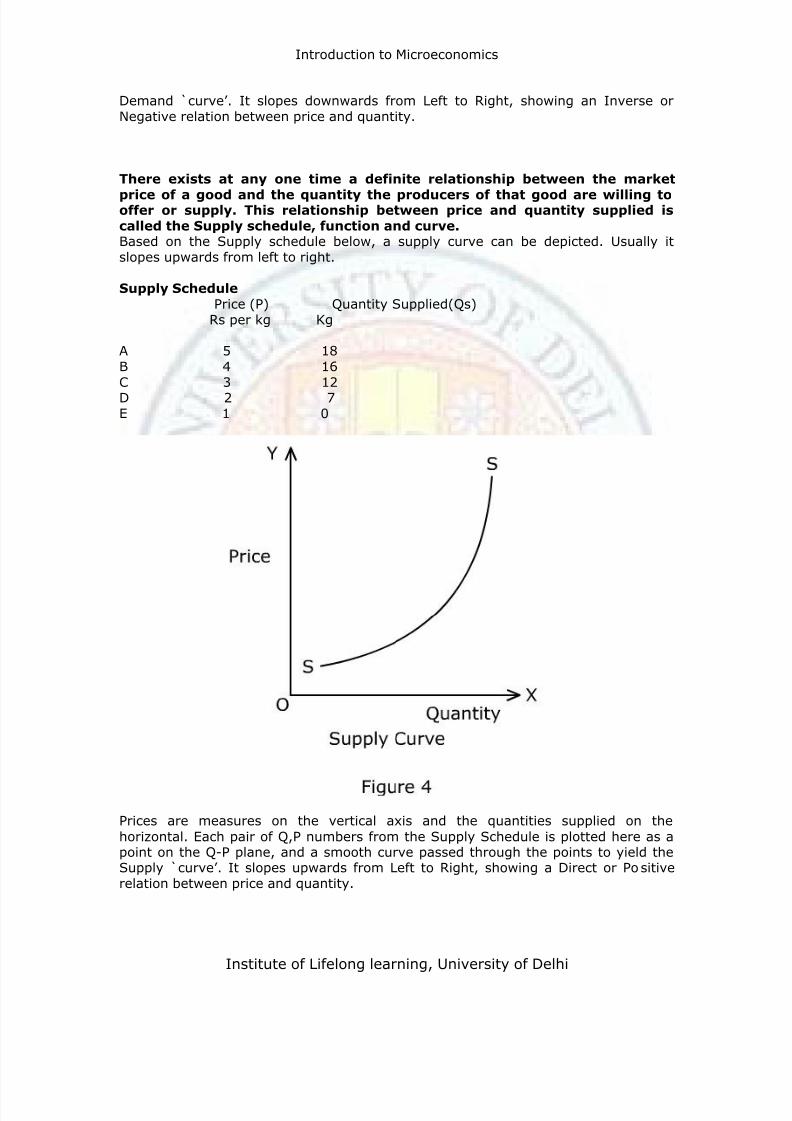

There exists at any one time a definite relationship between the market

price of a good and the quantity the producers of that good are willing tooffer or supply. This relationship between price and quantity supplied iscalled the Supply schedule, function and curve.Based on the Supply schedule below, a supply curve can be depicted. Usually itslopes upwards from left to right.

Supply SchedulePrice (P) Quantity Supplied(Qs)

Rs per kg Kg

A 5 18B 4 16C 3 12D 2 7E 1 0

Prices are measures on the vertical axis and the quantities supplied on thehorizontal. Each pair of Q,P numbers from the Supply Schedule is plotted here as apoint on the Q-P plane, and a smooth curve passed through the points to yield theSupply `curve’. It slopes upwards from Left to Right, showing a Direct or Po sitiverelation between price and quantity.

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 12/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

To find the Equilibrum, the two schedules must be matched or, the two curvessuperimposed on each other. At the price where the quantity demanded is the sameas the quantity offered, that is, at the point where the Demand curve and the Supplycurve intersect, there is a perfect matching or balancing, i.e., equilibrium.

Putting the two schedules together, we find that only at P=3 will both Qd and Qs bethe same, viz., 12. Putting the two curves together, we find that they intersect at

(only) the point (12, 3). At the (point 12,3) thus, there is equilibrium. Thisequilibrium holds, until and unless there is some external reason tipping the scaleseither way. At any price lower than Rs 3 per kg, suppliers would not come forth withthe quantity that the buyers are demanding( 12 kgs). At any price that is higher,buyers will not be demanding the quantity that suppliers are willing to supply atthose(higher) prices. At any price higher or lower than Rs 3 per kg, there will beExcess Demand or Excess Supply in the market.

The above Demand and Supply are individual in nature, belonging to an individualperson, household or firm. In Macro-Economics the corresponding concepts areAggregate Demand and Aggregate Supply. They represent the total demand andsupply of the economy as a whole.Types of Markets

Markets can be of different types depending on the type of goods and services beingbought and sold in it.The most common is the market for specific goods or commodities, i.e., of concrete,physical things like items of food and clothing. Services can also be bought and sold,e.g., travel and entertainment, the treatment of physicians and lawyers. The ShareMarket is where shares of various companies are bought and sold. Domestic marketrefers to markets within the boundaries of a country, whereas the Foreign orInternational market refers to transactions taking place across two different

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 13/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

countries using two different currencies. All these markets come under the purviewof Economics. But there is a difference in the approach in which Micro-Economics andMacro-economics looks at markets.Micro-Economic looks at markets in the sense of individual buyers(consumers orhouseholds) and individual sellers ( producers or firms) coming together to performtheir respective roles in the market transactions. It is concerned with whether there

are numerous buyers and sellers or just a few ( or even one), whether the product(good, commodity, or service) is homogeneous or differentiated, whether there isperfect information about the products(output) and factors of production (input),whether the factors (inputs) can freely move between alternative uses, and suchconditions. Depending upon the configuration of such conditions, the market takesdifferent forms such as Perfect competition, monopolistic competition, Monopoly, andso on. A large part of Micro-Economics is devoted to the study of these marketforms.

In Macro-Economics, the markets concerned are overall or aggregate in nature.

Both Micro-economics and Macro –economics look beyond national boundaries.International Trade Theory, first formulated by none other than Adam Smith, is anessential part of Micro theory. Open Economy models, for example by Mundell andFleming, are also integral parts of Macro theory.

In addition to studying the exchange of actual goods and services, Micro Economicsalso studies the attainment of Satisfaction or Welfare that comes from suchexchange, both at individual and social levels. In fact, this is one of the basicquestions that Adam Smith was preoccupied with. How is Social Welfare , as distinctfrom the welfare of individuals, to be reached? Welfare Economics is the part ofMicro-economics which studies this, and there is no counterpart in Macro-economics.

9. Concept of ceteris paribus – General Equilibrium Partial Equilibrium

Economics is a complex subject, rooted in the reality but often analyzed through

abstract thinking and mathematical methods.As symbols of that reality, Economics makes use of the Mathematical concepts :Variables, Constants and Parameters.Variables are entities that take different values. They are usually symbolized by x, y ,z. and take values positive and negative ranging from minus infinity to plus infinity.Constants are entities that , for one particular analytical exercise, take oneparticular value. They are usually symbolized by a, b, c .. or alpha, beta, gama. Andagain, can take any value between plus-minus infinity but can take only one suchvalue during a particular analysis.Parameters are entities that can be assigned different values for different variants ofan exercise but in any one particular variant, can take only one such value.Variables can be dependent or independent. An in dependent variable takes onvalues by itself. A Dependent variable takes on values according to or as per theIndependent variable. This relation of dependence between the Independent and theDependent variable(s) is known as a functional relationship, or simply, a Function. Itmeans that the Dependent variable functions according to the Independent variable.It is a most powerful tool in the sturdy of Economics, both Micro and Macro.In Economics, a Function may involve more than one variable. Usually, severalvariables are interlinked. To examine whether any two have a causal ( cause-effect)relationship, it may be necessary to rule out others that complicate the issue or getin the way of analyzing it. Then what is done is to make an assumption known as theceteris paribus assumption.

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 14/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

In Latin Ceteris means `other things or the rest’ and Paribus means ` at par orequal’. The phrase ceteris paribus thus means ‘other things being the same’. Itqualifies or conditions a causal relationship between an independent variable and thedependent variable that depends on it or functions according to it.Suppose we take up the following Functional RelationshipThe Quantity (Qx) of a Commodity being demanded ( symbolized by the variable x)

depends on the Price (Px) of the Commodity, the Prices of other commodities (say, yand z) that can complement or substitute it, the Income (Y) and Tastes(T) of theperson making the demand.Symbolically this can be written asQx = f( Px, Py, Pz, Y, T)where Qx is the dependent variable, Px, Py and Pz , Yand T the independentvariables, and f is the functional form.Now if we want to focus on the causal relationship between the Price of thecommodity (Px) and the Quantity of it that is demanded (Qx), and for the time beingput aside the prices of commodities and the tastes of the consumer, this can bewritten asQx = f(Px), ceteris paribus .This simple yet powerful technique, used extensively by Alfred Marshall, is known asPartial Equilibrium Analysis. However it lets only one market (at a time0 be inequilibrium and may not capture the complexities of the real world.General Equilibrium Analysis is a contrasting technique, first formalized by LeonWalras. This does not use the ceteris paribus assumption. It lets the inter-dependence of various variables play themselves out. Prices of Commodities aredetermined simultaneously and mutually. All markets are simultaneously inequilibrium.

10. Static and Dynamic Equilibrium

In a static equilibrium all quantities have unchanging values but in a dynamicequilibrium various quantities may be growing , only their ratios being unchanged.

Comparative Statics compares two static cases of equilibrium. ComparativeDynamics compares two dynamic equilibria.

11. Short-Run and Long-Run Equilibrium

A run is a length of time, not exactly specified. If all factors of production can bevaried during a length of time, it is called the Long Run. If some variables can bevaried but others cannot, i.e., are fixed, it is the Short Run. A Short Run Equilibriumis one that holds

12. Nobel Prize in Economics

The highest recognition for economists is the “Sveriges Riksbank Prize in EconomicSciences in Memory of Alfred Nobel” . Though created by Sweden’s Central Bank in1968, nearly 75 years after Nobel prizes in physics, chemistry, literature, peace andmedicine/physiology were set up in 1895, this is regarded as the Nobel Prize inEconomics. The first two to receive this were Ragnar Frisch and Jan Tinbergen in1969.Paul A. Samuelson received it in 1970. In 1998 , it went to Amartya Sen fromIndia.

Value Addition 2: Test Yourself

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 15/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

Now we suppose you should be able to answer the questions:1.What is Micro-Economics?2. Give three keywords that you think must be included to define it.(Hint: individual, branch)

13. Summary Economics studies human choice among alternative uses of scarce

resources. It is a Social Science has a wide scope. It aids the understanding of

the central problems of an economy. Demand and Supply of goods and services determine their

Equilibrium Price and Quantity in the Market. Markets can be of various forms. Equilibrium can be Partial and General, Long-Run and Short-Run,

Dynamic and Static.

14. Exercises

Short Questions

1. How would you define Micro-Economics?2. What are the three central problems of an economy?3. What does ceteris paribus mean ?

Long Questions

1. Describe the evolution of the subject Economics.

2. Explain the concept of Market Equilibrium.3. Is Economics a Science or an Art?4. What subjects have a relation with Economics?

15. Glossary

VariablesConstantsHypothesisModelDemand supplyMarketEquilibriumStatic EquilibriumDynamic EquilibriumLong RunShort runGeneral equilibriumPartial Equilibrium

16. References

8/10/2019 Introduction to Microeconomicsgggg

http://slidepdf.com/reader/full/introduction-to-microeconomicsgggg 16/16

Introduction to Microeconomics

Institute of Lifelong learning, University of Delhi

1. Economics , Paul A Samuelson2. Microeconomics , Robert S. Pindyck, DanieL.Rubinfeld, Prem L. Mehta

17. Activity

Go to the nearby market for fruits and vegetables and observe the people going

about the daily business of buying and selling.Go to a mall or supermarket and do the same.Jot down any differences you may find.

18. Quiz

Was Adam Smith English, American, Scottish or French?When was his book The Wealth of Nations published?Did Alfred Marshall teach at Oxford University, Cambridge University or the LondonSchool of Economics?Who won the Nobel Prize in Economics this year?