Embed Size (px)

Citation preview

Introduction to modelling

Basic concepts and simple modelling techniques

04/19/23 1

• What does modelling involve?• How are models built?• What are the components of a model and

how do we identify these?• Are there different types of model?• How do models deal with time?• How do models deal with certainty,

uncertainty and risk?

04/19/23 2

3

Benefits of Producing Models

• Having a model to use is beneficial but the process of producing a model is equally if not more beneficial.

• Helps you to understand the problem.– Need to be explicit about your goals.– Need to quantify the variables which affect the goals.– Need to identify constraints and relationships between

variables.– Facilitates communication and understanding.

4

What does Modelling involve?

• variables are identified by analysing the problem• relationships among them are established.• Simplifications are made through assumptions. (untested beliefs or predictions). • A decision-maker can test assumptions using

what-if or sensitivity analysis. • Simpler models are cheaper but don’t model

reality so closely.

How are models built?

• Models can be built using statistical packages, forecasting software, modelling packages and end-user software tools like Excel.

04/19/23 5

Components of a Model

• Mathematical Models are made up of 3 basic components, decision variables, uncontrollable variables(and/or parameters) and result (outcome) variables.

• Mathematical formulae link these variables together.

04/19/23 6

• Decision variables represent alternative courses of action. The level of these is determined by the decision-maker e.g. the amount to invest.

• Result variables indicate the outcome of the decision, they are dependent on the occurrence of the decision and the uncontrollable or independent variables.

04/19/23 7

• Uncontrollable variables are factors which are not under the control of the decision-maker. These can be fixed or variable e.g. interest rates.

• Intermediate result variables reflect intermediate outcomes e.. if salary is a decision variable, employee satisfaction is an intermediate variable and productivity is the result variable.

04/19/23 8

Example : Simple profit model

04/19/23 9

Example : Printer model• Number of pages = pages per week* nweeks + oneoffs

• Total cost per page = fixed cost + var costs for year number of pages

Goal : minimise cost per page (tells us what we need to count).

Decision variable = cost of printerResult variable = cost per pageUncontrollable variable = cost of ink (given you’ve decided on

that printer)Assumptions : that the printer will work! That we’ll print x

many pages per week etc., That the college price will stay fixed.

04/19/23 10

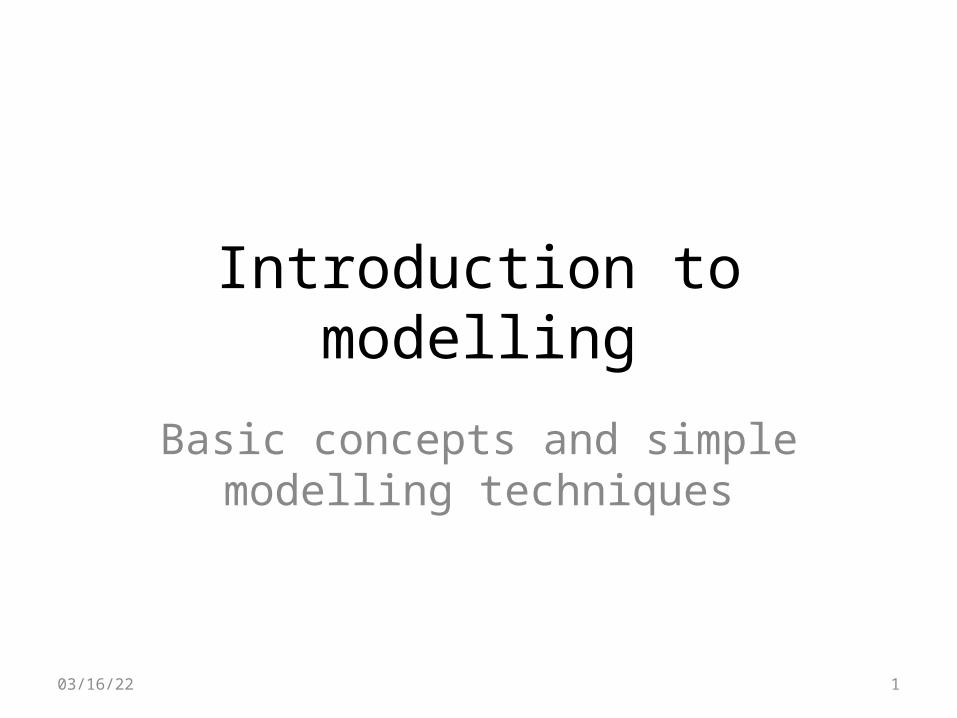

• Look at the cash flow model and identify – Decision variables– Uncontrollable variables– Result variables.

04/19/23 11

04/19/23 12

Data Section Fixed Costs per month € 6,000.00Corporation Tax € 18,000.00 Costs per UnitSelling Price € 40.00 Material € 20.00New Vehicle Costs € 8,000.00 Labour € 4.00Old Vehicle Sale Price € 600.00 Overheads € 2.00Estimated Cash Sales Units per Month 100Discount on cash Sales 5%

Opening Cash -€ 3,000.00

May June July August September October November DecemberProduction Units 1200 1400 1600 2000 2400 2600 2400 2200Estimated Credit Sales Units 1000 1200 1400 1600 1800 2000 2200 2600

04/19/23 13

Cash Flow Calculations

July Aug Sept Oct Nov Dec

Income

Product Cash Sales

Product Credit Sales

Sale of Vehicle

Total

Outgoings

Materials

Labour

Variable Overheads

Fixed Costs

Corporation Tax

Purchase of Vehicle

Total

Receipts Less Payments

Balance Brought Forward

Balance Carried Forward

Aspects of Modelling

• Normative vs descriptive models• Static vs dynamic models• Treating certainty, uncertainty and risk

– What if analysis– Sensitivity analysis– Scenario analysis

04/19/23 14

Types of ModelNormative

(Optimisation)

• the chosen alternative is demonstrably the best of all possible alternatives.

• e.g. Linear Programming

1504/19/23

Descriptive

•Describe things as they are, or as they are believed to be.•Checks the outcome of a given set of alternatives not of all alternatives.•No guarantee of an optimal solution.e.g. simulation models which are used to explore different solutions and relationships between variables

Optimisation Examples

• Get the highest level of goal attainment from a given set of resources e.g. max profit from €1000000 investment.

• Find alternative with highest ratio of goal attainment to cost.

• Find alternative with the lowest cost that wll achieve acceptable level of goals.

04/19/23 16

Example : Optimisation

04/19/23 17

Good Enough or Satisficing• decision-maker sets up an aspiration, goal or

desired level of performance and searches the alternatives until one is found which achieves this level. This involves:-

• Generating Alternatives• Predicting the outcome of each alternative• Measuring outcomes –value in terms of goal

attainment e.g. profit ,customer satisfaction – no. complaints, level of loyalty to product, ratings found by surveys.

04/19/23 18

Descriptive Model Examples• Scenario analysis• Environmental impact analysis• Simulation• Waiting line (queue) management• Narratives.

04/19/23 19

Static Analysis

Static models take a single snapshot of a situation. During this, everything occurs in a single interval or fixed time frame. During a static analysis stability of the relevant data is assumed. e.g. buy or make.

04/19/23 20

Dynamic Analysis -time-dependent models• scenarios that change over time e.g. 5 year profit and loss projection,

in which the input data such as costs, prices and quantities change over time.

e.g. in determining how many checkouts need to be open in a supermarket the time of day must be considered.

Dynamic simulation represents when conditions vary from the steady state over time:- there may be variations in the raw materials, or unforeseen events.

Dynamic models are important because they use, represent or generate trends and patterns over time. e.g. 5 year profit projection where input data such as costs, prices and quantities change over time.

Can be used to create averages per period or moving averages and to prepare comparative analysis. May facilitate the development of business plans, strategies,tactics.

04/19/23 21

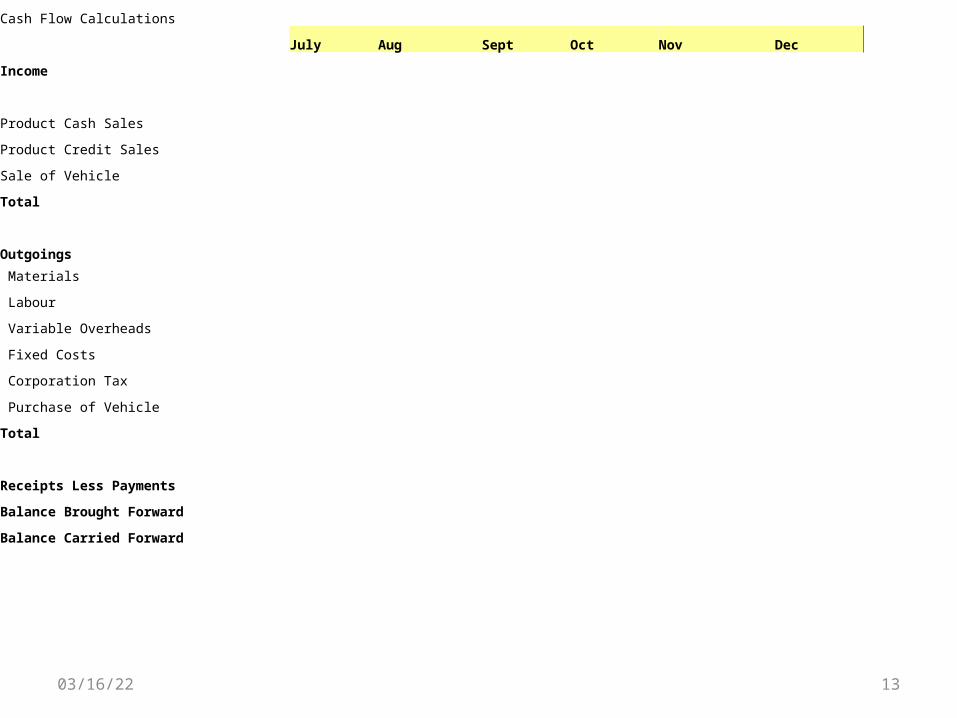

Certainty, Uncertainty and Risk• Certainty models- easy to develop and solve- models

constructed under assumed certainty e.g. many financial models.

• Uncertainty –the decision maker does not know, or can’t assess the probability of occurrence of certain outcomes. More information increases certainty.

• Risk analysis involves estimates of risk. Risk can thus be estimated.

• Uncertainty and risk can be examined using what-if and sensitivity analysis. It is a good idea when identifying variables to assess certainty.

04/19/23 22

What if analysis• The end user makes changes to variables or relationships

between variables and observes the resulting change in the values of other variables.

Example• Change a revenue amount (variable) or a tax rate formula

in a simple financial spreadsheet model, and recalculate all the affected variables. A manager would be interested in observing and evaluating any changes in values that occurred e.g. net profit after taxes.

• In may cases this is the “bottom line” i.e. a key factor in making many types of decisions.

• What would happen to sales if we cut advertising by 10%?

04/19/23 23

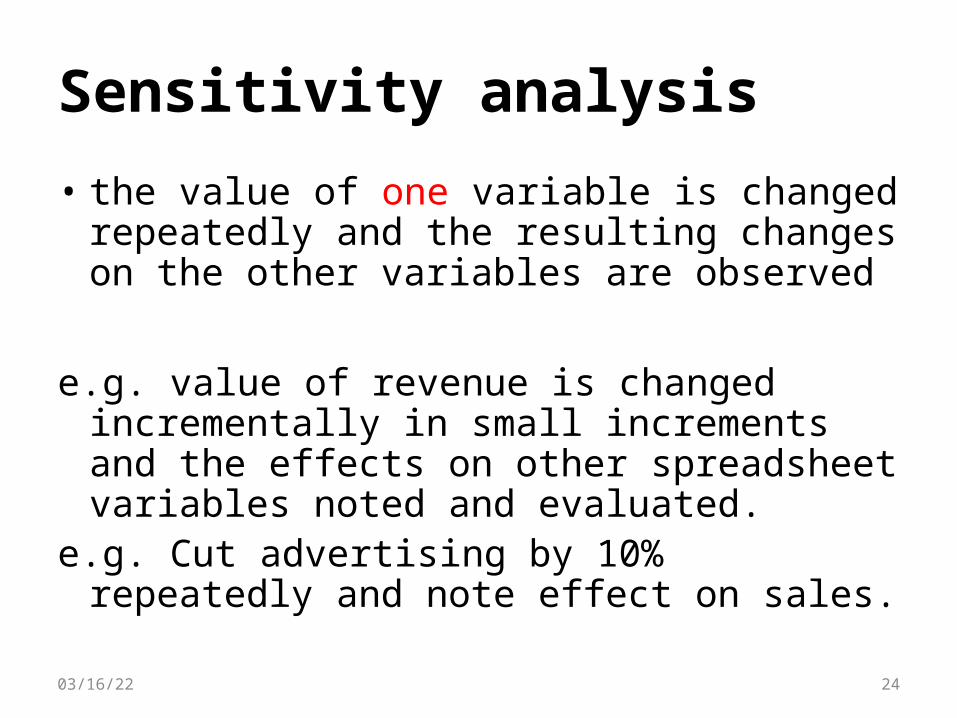

Sensitivity analysis

• the value of one variable is changed repeatedly and the resulting changes on the other variables are observed

e.g. value of revenue is changed incrementally in small increments and the effects on other spreadsheet variables noted and evaluated.

e.g. Cut advertising by 10% repeatedly and note effect on sales.

04/19/23 24

Scenario Analysis

• Examine the best case, worst case, most likely and average case scenarios.

04/19/23 25

Examine the Wilmington example.

• How does this model deal with uncertainty?

• What is the best case here for Wilmington?

• What is the worst case?

• What other factors do we need to consider in scenario analysis?

04/19/23 26

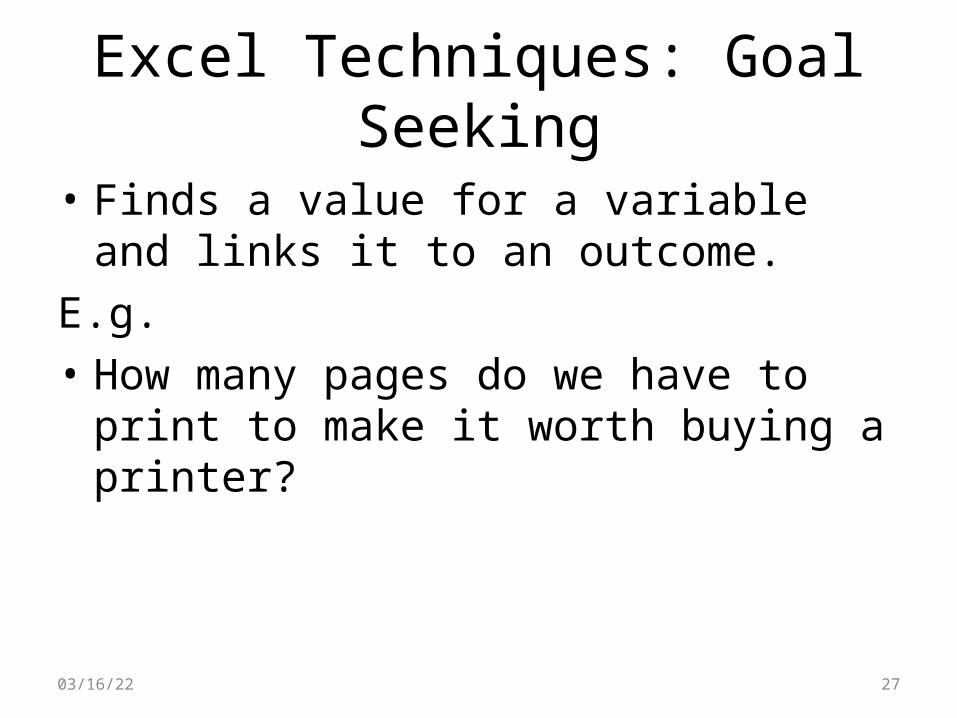

Excel Techniques: Goal Seeking

• Finds a value for a variable and links it to an outcome.

E.g.• How many pages do we have to print to make

it worth buying a printer?

04/19/23 27

04/19/23 Source Turban 2003 28

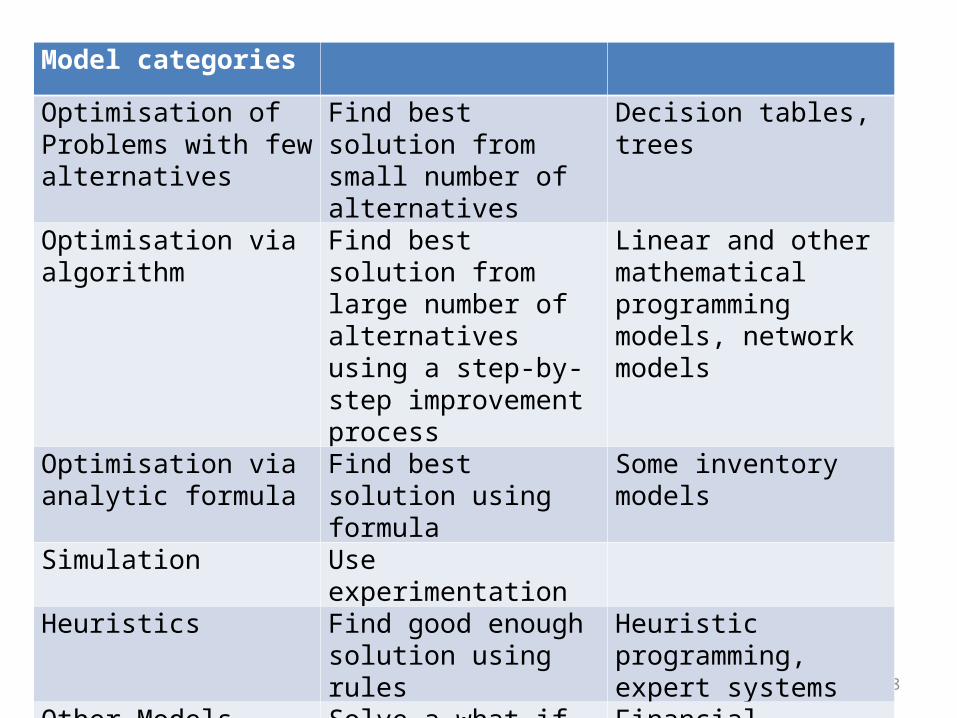

Model categories

Optimisation of Problems with few alternatives

Find best solution from small number of alternatives

Decision tables, trees

Optimisation via algorithm

Find best solution from large number of alternatives using a step-by-step improvement process

Linear and other mathematical programming models, network models

Optimisation via analytic formula

Find best solution using formula

Some inventory models

Simulation Use experimentationHeuristics Find good enough

solution using rulesHeuristic programming, expert systems

Other Models Solve a what-if case using a formula

Financial modelling, waiting lines

Predictive models Predict future for given scenario

Forecasting models