Embed Size (px)

Citation preview

1

Introduction to Risk and Return and opportunity cost of capital

Chapter 11 BBM

08/29/12

11-2

Risk and Return

Risk and Return are related.

How?

We now focus on risk and return and their relationship to the opportunity cost of capital.

How?

11-3

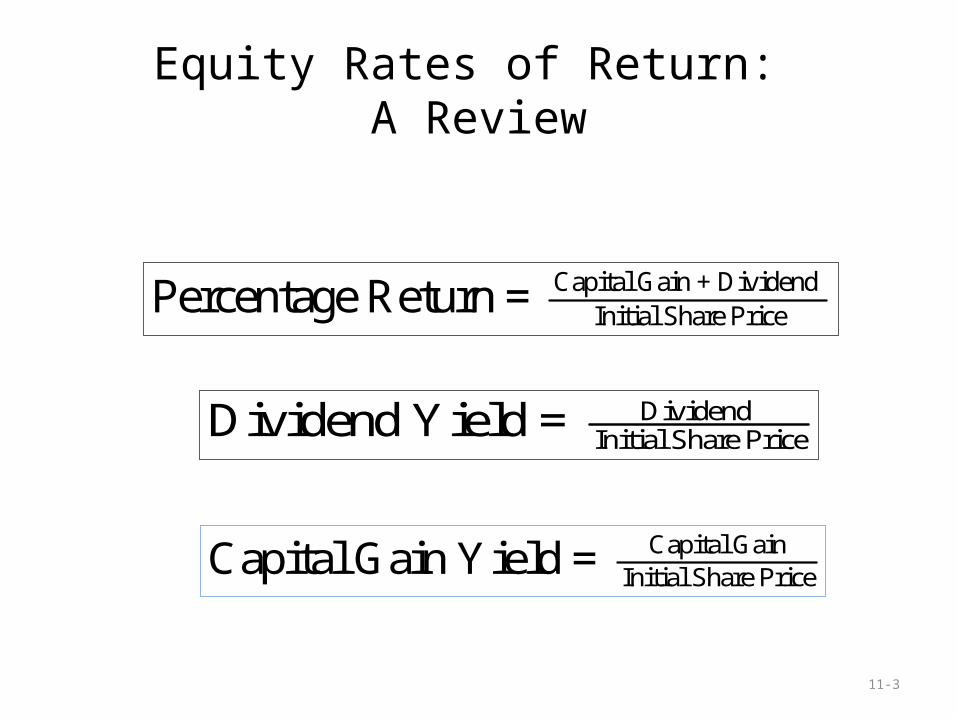

Equity Rates of Return: A Review

Capital Gain + Dividend Initial Share PricePercentage Return =

Capital GainInitial Share PriceCapital Gain Yield =

Dividend Initial Share PriceDividend Yield =

11-4

Real Rates of Return

1 + nominal rate of return1 + inflation rate1 real rate of return =

Example: Suppose inflation from December 2009 to December 2010 was 1.5%. What was GE stock’s real rate of return, if its nominal rate of return

was 23.93%?

Recall the relationship between real rates and nominal rates:

11-5

Total Returns for Different Asset Classes

The Value of an Investment of $1 in 1900

11-6

What Drives the Difference in Total Returns?

Maturity Premium: Extra average return from investing in longer term Treasury securities.

Risk Premium: Expected return in excess of risk-free return as compensation for risk.

11-7

Risk Premium: Example

Interest Rate on Normal RiskExpected Market Return = +

Treasury Bills Premium

1981: 21.4% = 14% + 7.4%

2008: 9.6% = 2.2% + 7.4%

11-8

Returns and Risk

How are the expected returns and the risk of a security related?

11-9

Measuring Risk

Variance: Average value of squared deviations from mean. A measure of volatility.

Standard Deviation: Square root of variance. Also a measure of volatility.

What is risk?

How can it be measured?

10

Market Indexes

Dow Jones Industrial Average (The Dow)Value of a portfolio holding one share in each of 30 large industrial firms.

Standard & Poor’s Composite Index (The S&P 500)Value of a portfolio holding shares in 500 firms. Holdings are proportional to the number of shares in the issues.

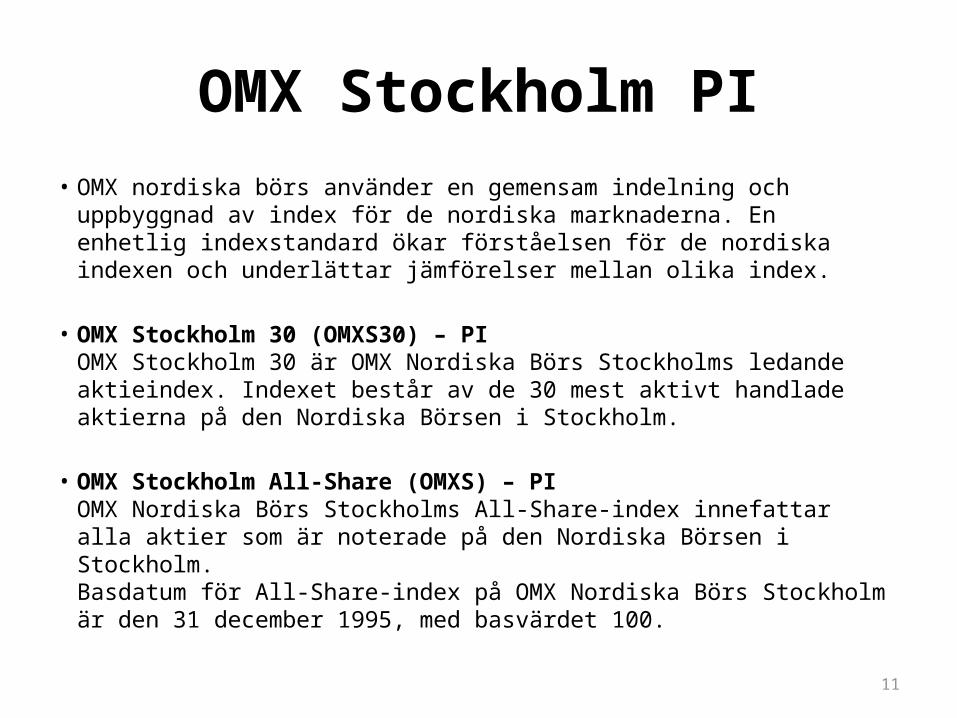

OMX SPI index

11

OMX Stockholm PI• OMX nordiska börs använder en gemensam indelning och uppbyggnad av

index för de nordiska marknaderna. En enhetlig indexstandard ökar förståelsen för de nordiska indexen och underlättar jämförelser mellan olika index.

• OMX Stockholm 30 (OMXS30) – PI OMX Stockholm 30 är OMX Nordiska Börs Stockholms ledande aktieindex. Indexet består av de 30 mest aktivt handlade aktierna på den Nordiska Börsen i Stockholm.

• OMX Stockholm All-Share (OMXS) – PI OMX Nordiska Börs Stockholms All-Share-index innefattar alla aktier som är noterade på den Nordiska Börsen i Stockholm. Basdatum för All-Share-index på OMX Nordiska Börs Stockholm är den 31 december 1995, med basvärdet 100.

12

Average Market Risk Premium (by country)

4,29 4,69 5,05 5,43 5,5 5,61 5,67 6,04 6,29 6,94 7,137,94 8,34 8,4 8,74 9,1 9,61 10,21

0123456789

1011D

enm

ark

Bel

giu

m

Sw

itze

rlan

d

Irel

and

Sp

ain

Nor

way

Can

ada

U.K

.

Net

her

lan

ds

Ave

rage

U.S

.

Sw

eden

Au

stra

lia

Sou

th A

fric

a

Ger

man

y

Fra

nce

Jap

an

Ital

y

Risk premium, %

Country

Market risk premium = Market rate of return – risk-free rate

13

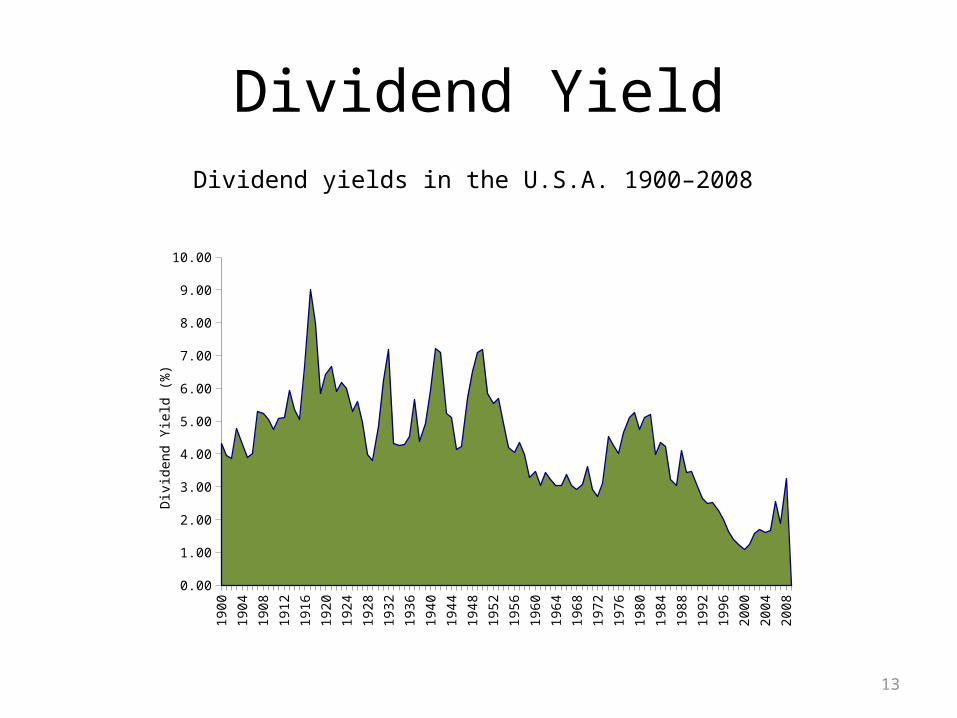

Dividend YieldDividend yields in the U.S.A. 1900–2008

1900

1903

1906

1909

1912

1915

1918

1921

1924

1927

1930

1933

1936

1939

1942

1945

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Div

iden

d Y

ield

(%

)

14

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

Rates of Return 1900-2008

Source: Ibbotson Associates Year

Perc

enta

ge R

etur

nStock Market Index Returns

15

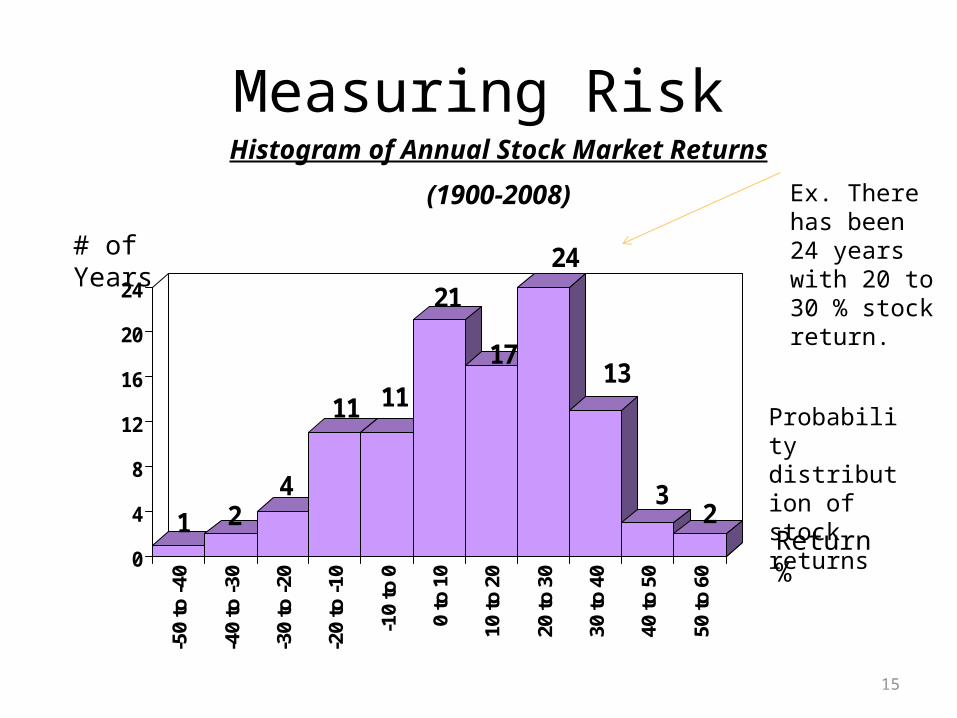

Measuring Risk

1 24

11 11

21

17

24

13

32

0

4

8

12

16

20

24

-50

to -

40

-40

to -

30

-30

to -

20

-20

to -

10

-10

to 0

0 to

10

10 t

o 20

20 t

o 30

30 t

o 40

40 t

o 50

50 t

o 60

Return %

# of Years

Histogram of Annual Stock Market Returns

(1900-2008)

Probability distribution of stock returns

Ex. There has been 24 years with 20 to 30 % stock return.

Thinking About Risk

• Message 1– Some Risks Look Big and Dangerous but Really Are

Diversifiable

• Message 2– Market Risks Are Macro Risks

• Message 3– Risk Can Be Measured

11-17

Historical Risk(1900-2010)

11-18

Risk and Diversification

DiversificationStrategy designed to reduce risk by spreading a portfolio across many investments.

Unique Risk:Risk factors affecting only that firm. Also called “diversifiable risk.”

Market Risk:Economy-wide sources of risk that affect the overall stock market. Also called “systematic risk.”

19

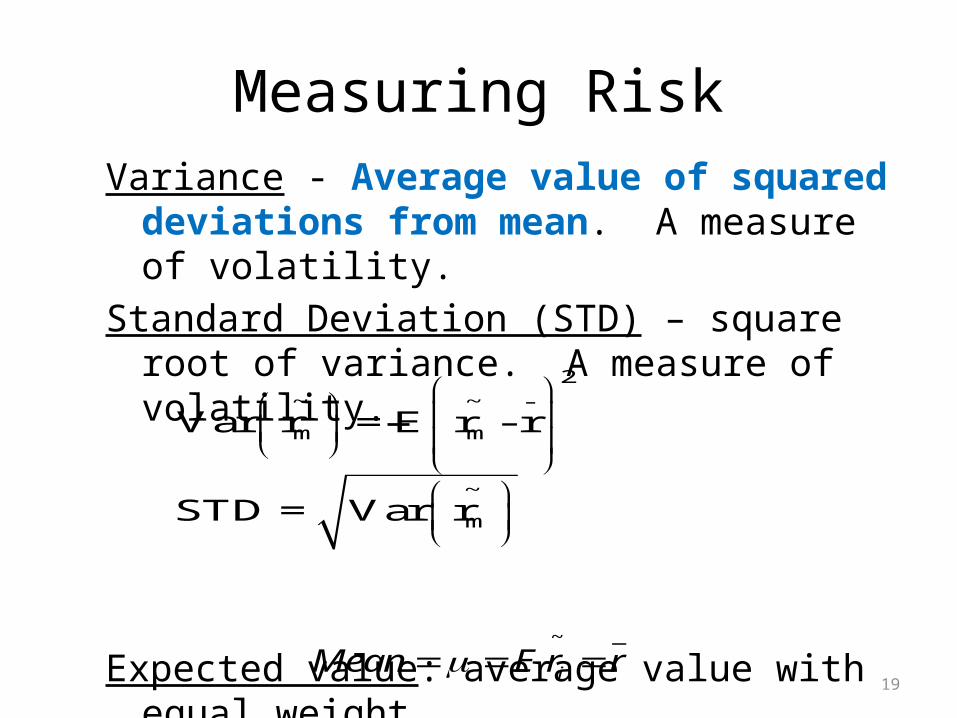

Measuring RiskVariance - Average value of squared deviations

from mean. A measure of volatility.Standard Deviation (STD) – square root of variance.

A measure of volatility.

Expected value: average value with equal weight.

2~ ~ -

m m

~

m

Var r = E r - r

STD = Var r

_~

iMean E r r

Measuring RiskExample from page: 320. Coin Toss Game-calculating

variance and standard deviation(1) (2) (3)

Percent Rate of Return Deviation from Mean Squared Deviation

+ 40 + 30 900

+ 10 0 0

+ 10 0 0

- 20 - 30 900

Variance = average of squared deviations = 1800 / 4 = 450

Standard deviation = square of root variance = 450 = 21.2%

21

Measuring RiskYou start with 100 kr. Toss two coins at a time. Head up you

gain 20%, tails up you lose 10%. There are all together 4 outcomes. (HH) (HT) (TH) (TT). Coin Toss Game-calculating variance and standard deviation

22

Measuring Risk

Portfolio rate

of return=

fraction of portfolio

in first assetx

rate of return

on first asset

+fraction of portfolio

in second assetx

rate of return

on second asset

((

(())

))

Expected return is just a weighted average of individual stock returns.

23

Dow Jones RiskAnnualized Standard Deviation of the DJIA over the preceding 52 weeks

(1900 – 2008)

0

10

20

30

40

50

60

70

Years

Stan

dard

Dev

iatio

n (%

)

24

Measuring Risk

Diversification - Strategy designed to reduce risk by spreading the portfolio across many investments.

Unique Risk - Risk factors affecting only that firm. Also called “diversifiable risk.”

Market Risk - Economy-wide sources of risk that affect the overall stock market. Also called “systematic risk.”

Market IndexDeviations from Squared

Year Rate of Return, % Average Return, % Deviations

2002 -20.9 -29.4 864.362003 31.6 23.1 533.612004 12.5 4.0 16.002005 6.4 -2.1 4.412006 15.8 7.3 53.292007 5.6 -2.9 8.41

Total 51.0 1,480.08

Average return = 51.0/6 = 8.50%246.6815.71%

Variance = average of squared deviations = 1,480.08/6 = Standard deviation = square root of variance =

Obs: step 1, get the Mean 8,5%, step 2, get the deviations from the mean and step 3, square it to get the variance. Since we have 6 years’ observations, divide it with 6.

11-26

Risk and Diversification

27

Portfolio Risk

22

22

211221

1221

211221

122121

21

σxσσρx x

σxx2Stock

σσρx x

σxxσx1Stock

2Stock 1Stock

The variance of a two stock portfolio is the sum of these four boxes

)σσρxx(2σxσxVariance Portfolio 21122122

22

21

21

28

Portfolio RiskExample

Suppose you invest 60% of your portfolio in Campbell Soup and 40% in Boeing. The expected dollar return on your Campbell Soup stock is 3.1% and on Boeing is 9.5%. The expected return on your portfolio is:

%7.5)5.940(.)1.360(.Return Expected

29

Portfolio Risk

2222

22

211221

2112212221

21

)7.23()40(.σx7.238.151

60.40.σσρxxBoeing

7.238.151

60.40.σσρxx)8.15()60(.σx Soup Campbell

Boeing Soup Campbell

Example

Suppose you invest 60% of your portfolio in Campbell Soup and 40% in Boeing. The expected dollar return on your Campbell Soup stock is 3.1% and on Boeing is 9.5%. The standard deviation of their annualized daily returns are 15.8% and 23.7%, respectively. Assume a correlation coefficient of 1.0 and calculate the portfolio variance.

11-30

Do stock prices move together?

What effect does diversification have on a portfolio’s total risk, unique risk and market risk?

31

Portfolio RiskExample

Suppose you invest 60% of your portfolio in Campbell Soup and 40% in Boeing. The expected dollar return on your Campbell Soup stock is 3.1% and on Boeing is 9.5%. The standard deviation of their annualized daily returns are 15.8% and 23.7%, respectively. Assume a correlation coefficient of 1.0 and calculate the portfolio variance.

% 19.0 5.359 Deviation Standard

5.35915.8x23.7)2(.40x.60x

]x(23.7)[(.40)

]x(15.8)[(.60) Variance Portfolio22

22

Obs: Since the correlation coefficient is 1, there is no portfolio risk reduction at all! The average standard deviation for the two stocks is the same 18,96%=15,8*0,6+23,7*0,4

32

Portfolio RiskAnother Example

Suppose you invest 60% of your portfolio in Exxon Mobil and 40% in Coca Cola. The expected dollar return on your Exxon Mobil stock is 10% and on Coca Cola is 15%. The expected return on your portfolio is:

%12)1540(.)1060(. ReturnExpected

33

Portfolio RiskAnother Example

Suppose you invest 60% of your portfolio in Exxon Mobil and 40% in Coca Cola. The expected dollar return on your Exxon Mobil stock is 10% and on Coca Cola is 15%. The standard deviation of their annualized daily returns are 18.2% and 27.3%, respectively. Assume a correlation coefficient of 1.0 and calculate the portfolio variance.

% 21.8 0.477 DeviationStandard

0.47718.2x27.3)2(.40x.60x

]x(27.3)[(.40)

]x(18.2)[(.60) Variance Portfolio22

22

Again the correlation coefficient= 1, no gain on diversification! But it sure lowered the risk and the return by averaging.

34

Portfolio Risk

)rx()r(x Return PortfolioExpected 2211

)σσρxx(2σxσxVariance Portfolio 21122122

22

21

21

35

Portfolio RiskExample Correlation Coefficient = .4Stocks %s % of Portfolio Avg ReturnABC Corp 28% 60% 15%Big Corp 42% 40% 21%

Standard Deviation = weighted avg. = 33.6 (this is an average of the std)Standard Deviation = Portfolio = 28.1

Real Standard Deviation:Portfolio Variance = (282)(.62) + (422)(.42) + 2(.4)(.6)(28)(42)(.4) STD=sqrt (Variance) = 28.1 CORRECT

Mean: r = (15%)(.60) + (21%)(.4) = 17.4%

36

Portfolio RiskExample Correlation Coefficient = .4Stocks s % of Portfolio Avg ReturnABC Corp 28% 60% 15%Big Corp 42% 40% 21%

Standard Deviation = weighted avg = 33.6 Standard Deviation = Portfolio = 28.1 Return = weighted avg = Portfolio = 17.4%

Let’s Add stock New Corp to the portfolio

37

Portfolio RiskExample Correlation Coefficient = .3Stocks s % of Portfolio Avg ReturnPortfolio 28.1 50% 17.4%New Corp 30 50% 19%

NEW Standard Deviation = weighted avg. std= 31.80 NEW Standard Deviation = Portfolio = 23.43 NEW Mean = weighted avg = Portfolio = 18.20%

NOTE: Higher return & Lower risk How did we do that? DIVERSIFICATION

38

The Variance Covariance MatrixThe shaded boxes contain variance terms; the remainder contain covariance terms. Adding them up you get the portfolio variance.

1

2

3

4

5

6

N

1 2 3 4 5 6 NSTOCK

STOCK

To calculate portfolio variance add up the boxes

39

Portfolio Risk

Market Portfolio - Portfolio of all assets in the economy. In practice a broad stock market index, such as the S&P Composite, is used to represent the market.

Beta - Sensitivity of a stock’s return to the return on the market portfolio.

40

The Security Market LineThe return on Dell stock changes on average by 1.41% for each additional 1% change inthe market return. Beta = 1.41.

fMif

imm

fMf

rrEr

rrErrE

)(

)()(

The model is the famous CAPM: Capital asset pricing model, you get the r---required rate of return or cost of capital from this!

41

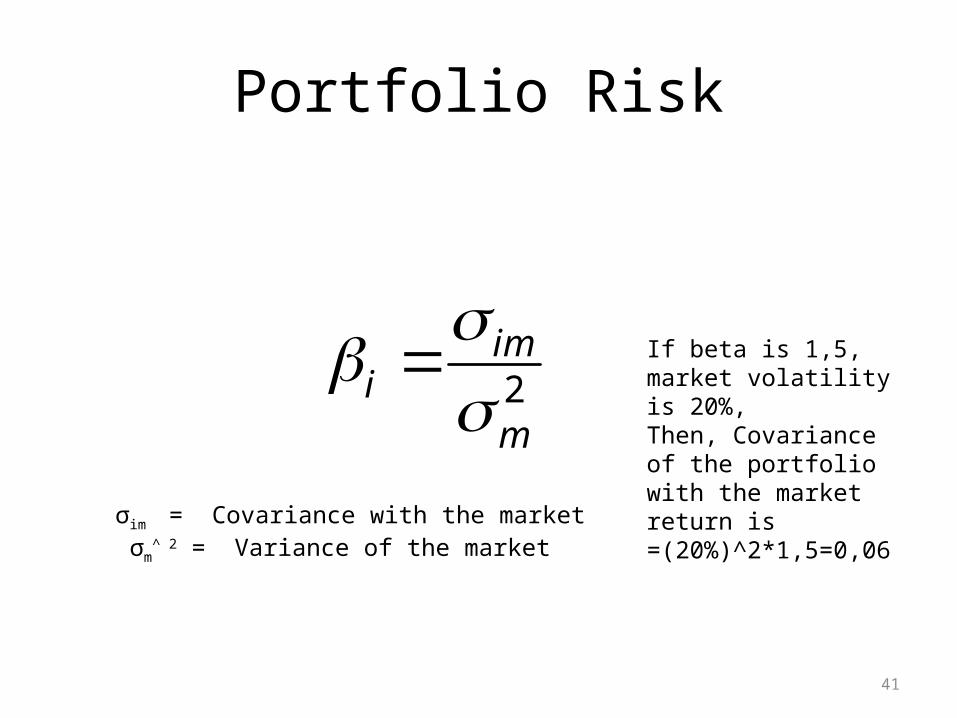

Portfolio Risk

2im

im

σim = Covariance with the market σm

^ 2 = Variance of the market

If beta is 1,5, market volatility is 20%, Then, Covariance of the portfolio with the market return is =(20%)^2*1,5=0,06

42

Portfolio Risk

2m

imiB

Covariance with the market

Variance of the market

43

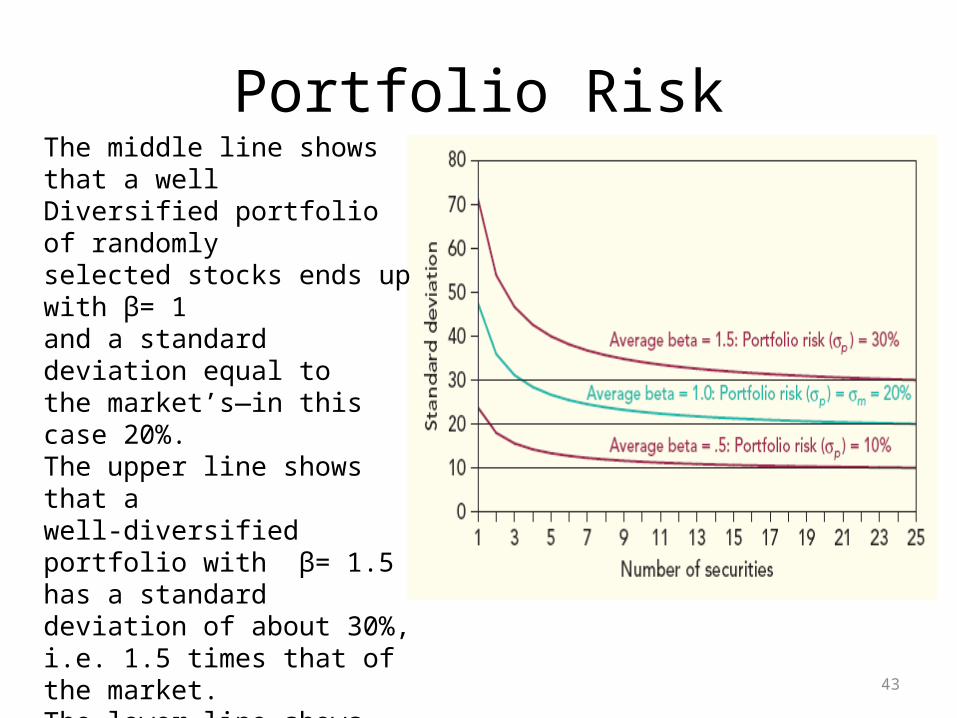

Portfolio RiskThe middle line shows that a wellDiversified portfolio of randomlyselected stocks ends up with β= 1and a standard deviation equal tothe market’s—in this case 20%.The upper line shows that awell-diversified portfolio with β= 1.5 has a standard deviation of about 30%, i.e. 1.5 times that of the market.The lower line shows that awell-diversified portfolio with β = .5 has a standard deviation of about 10%—half that of the market.

44

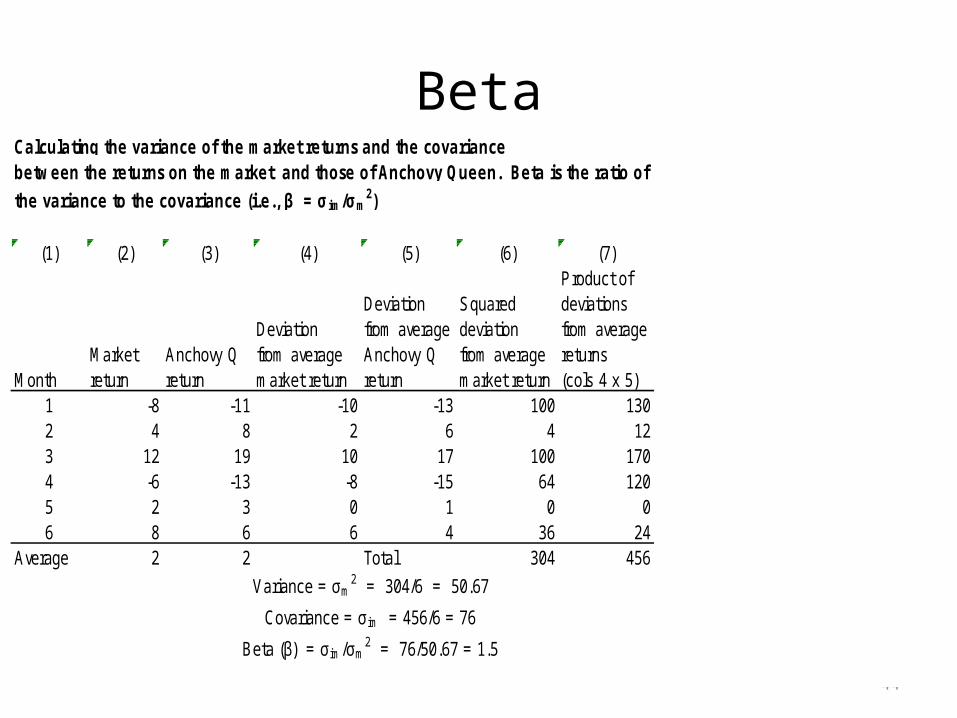

Beta

(1) (2) (3) (4) (5) (6) (7)Product of

Deviation Squared deviationsDeviation from average deviation from average

Market Anchovy Q from average Anchovy Q from average returnsMonth return return market return return market return (cols 4 x 5)

1 -8 -11 -10 -13 100 1302 4 8 2 6 4 123 12 19 10 17 100 1704 -6 -13 -8 -15 64 1205 2 3 0 1 0 06 8 6 6 4 36 24

Average 2 2 Total 304 456

Variance = σm2 = 304/6 = 50.67

Covariance = σ im = 456/6 = 76

Beta (β) = σ im /σm2 = 76/50.67 = 1.5

Calculating the variance of the market returns and the covariance between the returns on the market and those of Anchovy Queen. Beta is the ratio of

the variance to the covariance (i.e., β = σ im/σm2)

Check the figure see if it is right! Find out how to use excel to calculate variance and mean of a portfolio.