Embed Size (px)

Citation preview

INTRODUCTORY LEVEL

Paper FA1

Recording Financial Transactions

STUDY TEXT

P.2 KAP LA N P U BL IS HI NG

British Library Cataloguing-in-Publication Data A catalogue record for this book is available from the British Library. Published by: Kaplan Publishing UK Unit 2 The Business Centre Molly Millars Lane Wokingham RG41 2QZ ISBN: 978-1-78740-044-3 © Kaplan Financial Limited, 2017 Printed and bound in Great Britain.

Acknowledgments

We are grateful to the Association of Chartered Certified Accountants for permission to reproduce past examination questions. The answers have been prepared by Kaplan Publishing.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of Kaplan Publishing.

The text in this material and any others made available by any Kaplan Group company does not amount to advice on a particular matter and should not be taken as such. No reliance should be placed on the content as the basis for any investment or other decision or in connection with any advice given to third parties. Please consult your appropriate professional adviser as necessary. Kaplan Publishing Limited and all other Kaplan group companies expressly disclaim all liability to any person in respect of any losses or other claims, whether direct, indirect, incidental, consequential or otherwise arising in relation to the use of such materials.

KAP LA N P U BL IS HI NG P.3

CONTENTS

Page

Introduction P5

Syllabus and study guide P7

The examination P11

Study skills and revision guidance P13

Chapter

1 Business transactions 1

2 Types of business documentation 11

3 Double entry bookkeeping 35

4 Banking: payments and receipts 69

5 Sales and sales records 101

6 Recording sales 131

7 Purchases and purchase records 153

8 Recording purchases 175

9 Recording receipts and payments 185

10 Maintaining petty cash records 205

11 Payroll 225

12 Bank reconciliations 255

13 Control accounts 273

14 The trial balance 301

Answers to activities and exam-style questions 325

Index 379

Quality and accuracy are of the utmost importance to us so if you spot an error in any of our products, please send an email to [email protected] with full details.

Our Quality Co-ordinator will work with our technical team to verify the error and take action to ensure it is corrected in future editions.

P.4 KAP LA N P U BL IS HI NG

KAP LA N P U BL IS HI NG P.5

INTRODUCTION

This is the new edition of the FIA study text for FA1, Recording Financial Transactions, approved by the ACCA and fully updated and revised according to the examiner’s comments.

Tailored to fully cover the syllabus, this study text has been written specifically for FIA students. A clear and comprehensive style, numerous examples and highlighted key terms help you to acquire the information easily. Plenty of activities and self-test questions enable you to practise what you have learnt.

At the end of most of the chapters you will find multiple-choice questions. These are exam-style questions and will give you a very good idea of the way you will be tested.

P.6 KAP LA N P U BL IS HI NG

KAP LA N P U BL IS HI NG P.7

SYLLABUS AND STUDY GUIDE

Position of paper in the overall syllabus

No prior knowledge is required before commencing study for FA1. This paper provides the basic techniques required to enable candidates to prepare financial statements for various enterprises at a later stage. Candidates will, therefore, need a sound knowledge of the methods and techniques introduced in this paper to ensure they can employ them in later papers. The methods used in this paper are extended in FA2, Maintaining Financial Records, and further developed in FFA, Financial Accounting.

Syllabus

A TYPES OF BUSINESS TRANSACTION AND DOCUMENTATION

1. Types of business transaction

(a) Understand a range of business transactions including:

(i) Sales

(ii) Purchases

(iii) Receipts

(iv) Payments

(v) Petty cash

(vi) Payroll Ch’s 2 - 5

(b) Understand the various types of discount including where applicable the effect that trade discounts have on sales tax Ch’s 5& 9

(c) Describe the processing and security procedures relating to the use of: (i) Cash

(ii) Cheques

(iii) Credit cards

(iv) Debit cards for receipts and payments and electronic payment methods.

Ch’s 2 & 4

2 Types of business documentation

(a) Outline the purpose and content of a range of business documents to include but not limited to:

(i) Invoice

(ii) Credit note

(iii) Remittance advice Ch’s 2 & 5

(b) Prepare the financial documents to be sent to credit customers including:

(i) Sales invoices

(ii) Credit notes

(iii) Statements of account. Ch’s 2 & 5

(c) Prepare remittance advices to accompany payments to suppliers. Ch. 2

(d) Prepare a petty cash voucher including the sales tax element of an expense when presented with an inclusive amount.

Ch’s 2 & 10

P.8 KAP LA N P U BL IS HI NG

3 Process of recording business transactions within the accounting system

(a) Identify the characteristics of accounting data and the sources of accounting data records, showing understanding of how the accounting data and records meet the business’ requirements. Ch’s 1 & 2

(b) Understand how users can locate, display and check accounting data records to meet user requirements and understand how data entry errors are dealt with. Ch’s 1 & 2

(c) Outline the tools and techniques used to process accounting transactions and period-end routines and consider how errors are identified and dealt with. Ch. 14 (and throughout)

(d) Consider the risks to data security, data protection procedures and the storage of data. Ch. 2

(e) Understand the principles of coding in entering accounting transactions, including

(i) describing the need for a coding system for financial transactions within a double entry bookkeeping system

(ii) describe the use of a coding system within a filing system. Ch. 3

(f) Code sales invoices, supplier invoices and credit notes ready for entry into the books of prime entry. Ch’s 3, 5 & 7

(g) Describe the accounting documents and management reports produced by computerised accounting systems and understand the link between the accounting system and other systems in the business. Ch’s 3, 6 & 9

B DUALITY OF TRANSACTIONS AND THE DOUBLE ENTRY SYSTEM

1. Books of prime entry

(a) Outline the purpose and content of the books of prime entry including their format. Ch. 3

(b) Explain how transactions are entered in the books of prime entry. Ch’s 3 & 5

(c) Outline how the books of prime entry integrate with the double entry bookkeeping system. Ch’s 5 & 7

(d) Enter transactions including the sales tax effect where applicable into the books of prime entry. Ch’s 5 & 7

2. Double entry system

(a) Define the accounting equation. Ch. 3

(b) Understand and apply the accounting equation. Ch. 3

(c) Understand how the accounting equation relates to the double entry bookkeeping system.

Ch. 3

(d) Process financial transactions from the books of prime entry into the double entry bookkeeping system Ch’s 5 - 11

3. The journal Ch’s 3, 13 & 14

(a) Understand the use of the journal including the reasons for, content and format of the journal.

(b) Prepare journal entries directly from transactions, books of prime entry as applicable or to correct errors.

4. Elements of the financial statements Ch. 3

(a) Define and distinguish between the elements of the financial statements.

(b) Identify the content of a statement of financial position and statement of profit or loss and other comprehensive income.

C BANK SYSTEM AND TRANSACTIONS

1. The banking process Ch. 4

(a) Explain the differences between the services offered by banks and banking institutions.

(b) Describe how the banking clearing system works.

(c) Identify and compare different forms of payment.

(d) Outline the processing and security procedures relating the use of cash, cheques, credit cards, debit cards for receipts and payments and electronic payment methods.

2. Documentation Ch. 2

(a) Explain why it is important for an organisation to have a formal document retention policy.

(b) Identify the different categories of documents that may be stored as part of a document retention policy.

KAP LA N P U BL IS HI NG P.9

D PAYROLL Ch. 11

1. Process payroll transactions within the accounting system

(a) Prepare and enter the journal entries in the general ledger to process payroll transactions including:

(i) Calculation of gross wages for employees paid by the hour, paid by output and salaried workers

(ii) Accounting for payroll costs and deductions

(iii)The employers' responsibilities for taxes, state benefit contributions and other deductions

(b) Identify the different payment methods in a payroll system, e.g. cash, cheques, automated payment.

(c) Explain why authorisation of payroll transactions and security of payroll information is important in an organisation.

E LEDGER ACCOUNTS

1. Prepare ledger accounts

(a) Enter transactions from the books of prime entry into the ledgers. Ch’s 5 - 11

(b) Record journal entries in the ledger accounts. Ch’s 3, 13 & 14

(c) Balance and close off ledger accounts. Ch’s 3, 13 & 14

F CASH AND BANK

1. Maintaining a cash book Ch. 9

(a) Record applicable transactions within the cashbook, including any sales tax effect where applicable.

(b) Prepare the total, balance and cross cast cash book columns.

(c) Identify and deal with discrepancies.

2. Maintaining a petty cash book Ch. 10

(a) Enter and analyse petty cash transactions in the petty cash book including any sales tax effect where applicable.

(b) Balance off the petty cash book using the imprest and non imprest systems.

(c) Reconcile the petty cash book with cash in hand.

(d) Prepare and account for petty cash reimbursement.

G SALES AND CREDIT TRANSACTIONS

1. Recording sales Ch. 5

(a) Record sales transactions taking into account:

(i) various types of discount

(ii) sales tax

(iii) the impact on the sales tax ledger account where applicable

(b) Prepare the financial documents to be sent to credit customers.

2. Customer account balances and control accounts

(a) Understand the purpose of an aged receivable analysis. Ch. 6

(b) Produce statements of account to be sent to credit customers. Ch. 6

(c) Explain the need to deal with discrepancies quickly and professionally. Ch. 6

(d) Prepare the receivables control account or receivables ledgers by accounting for:

(i) sales

(ii) sales returns

(iii) payments from customers including checking the accuracy and validity of receipts against relevant supporting information

(iv) settlement discounts

(v) irrecoverable debt and allowances for irrecoverable debts including any effect of sales tax where applicable.

Ch’s 6 & 13

P.10 KAP LA N P U BL IS HI NG

H PURCHASES AND CREDIT TRANSACTIONS

1. Recording purchases Ch. 7

(a) Record purchase transactions taking into account:

(i) various types of discount

(ii) sales tax

(iii) the impact of the sales tax ledger account where applicable

(b) Enter supplier invoices and credit notes into the appropriate book of prime entry.

2. Supplier balances and reconciliations

(a) Prepare the payables control account or payables ledgers by accounting for:

(i) purchases

(ii) purchase returns

(iii) payments to suppliers including checking the accuracy and validity of the payment against relevant supporting information

(iv) settlement discounts Ch’s 8 & 13

I RECONCILIATION Ch’s 12 & 13

1. Purpose of control accounts and reconciliation

(a) Describe the purpose of control accounts as a checking devise to aid management and help identify bookkeeping errors.

(b) Explain why it is important to reconcile control accounts regularly and deal with discrepancies quickly and professionally.

2. Reconcile the cash book

(a) Reconcile a bank statement with the cash book.

3. Reconcile the receivables control account

(a) Reconcile the balance on the receivables control account with the list of balances.

4. Reconcile the payables control account

(a) Reconcile the balance on the payables control account with the list of balances.

J PREPARING THE TRIAL BALANCE Ch. 14

1. Prepare the trial balance

(a) Prepare ledger balances, clearly showing the balances carried down and brought down as appropriate.

(b) Extract an initial trial balance.

2. Correcting errors

(a) Identify types of error in a book-keeping system that are disclosed by extracting a trial balance.

(b) Identify types of error in a book-keeping system that are not disclosed by extracting a trial balance.

(c) Use the journal to correct errors disclosed by the trial balance.

(d) Use the journal to correct errors not disclosed by the trial balances.

(e) Identify when a suspense account is required and clear the suspense account using the journal.

(f) Redraft the trial balance following correction of all errors.

KAP LA N P U BL IS HI NG P.11

THE EXAMINATION

Format of the examination Number of marks

50 multiple-choice questions (2 marks each) 100

Time allowed: 2 hours

You can sit this paper as paper-based or computer-based exam.

Computer-based examinations

• Be sure you understand how to use the software before you start the exam. If in doubt, ask the assessment centre staff to explain it to you.

• Questions are displayed on the screen and answers are entered using keyboard and mouse. At the end of the examination, you are given a certificate showing the result you have achieved.

• Objective test questions might ask for numerical answers, but could also involve paragraphs of text which require you to fill in a number of missing blanks or to write a definition of a word or phrase. Others may give a definition followed by a list of possible key words relating to that description.

• Don’t panic if you realise you’ve answered a question incorrectly – you can always go back and change your answer.

Answering the questions

Multiple-choice questions – read the questions carefully and work through any calculations required. This paper comprised a mixture of narrative and computational questions.

If you don’t know the answer, eliminate those options you know are incorrect and see if the answer becomes more obvious. Remember that only one answer to a multiple-choice question can be right!

If you get stuck with a question skip it and return to it later. Answer every question – if you do not know the answer, you do not lose anything by guessing. Towards the end of the examination spend the last five minutes reading through your answers and making any corrections.

Equally divide the time you spend on questions. In a two-hour examination that has 50 questions you have about 2.4 minutes per a question.

If sitting a paper-based examination, before you finish, you must fill in the required information on the front of your answer booklet.

Do not treat multiple-choice questions as an easy option. Do not skip any part of the syllabus and make sure that you have learnt definitions, know key words and their meanings and importance, and understand the names and meanings of rules, concepts and theories.

P.12 KAP LA N P U BL IS HI NG

KAP LA N P U BL IS HI NG P.13

STUDY SKILLS AND REVISION GUIDANCE

Preparing to study

SET YOUR OBJECTIVES

Before starting to study decide what you want to achieve – the type of pass you wish to obtain.

This will decide the level of commitment and time you need to dedicate to your studies.

DEVISE A STUDY PLAN

Determine when you will study.

Split these times into study sessions.

Put the sessions onto a study plan making sure you cover the course, course assignments and revision.

Stick to your plan!

Use the MURDER method

Mood – set the right mood.

Understand – issues covered and make note of any uncertain bits.

Recall – stop and put what you have learned into your own words.

Digest – go back and reconsider the information.

Expand – read relevant articles and newspapers.

Review – go over the material you covered to consolidate the knowledge.

Effective study techniques

Use the SQR3 method

Survey the chapter – look at the headings and read the introduction, summary and objectives. Get an overview of what the text deals with.

Question – during the survey, ask yourself the questions that you hope the chapter will answer for you.

Read through the chapter thoroughly, answering the questions and meeting the objectives. Attempt the exercises and activities, and work through all the examples.

Recall – at the end of the chapter, try to recall the main ideas of the chapter without referring to the text. Do this a few minutes after the reading stage.

Review – check that your recall notes are correct.

P.14 KAP LA N P U BL IS HI NG

While studying…

Summarise the key points of the chapter.

Make linear notes – a list of headings, divided up with subheadings listing the key points. Use different colours to highlight key points and keep topic areas together.

Try mind-maps – put the main heading in the centre of the paper and encircle it. Then draw short lines radiating from this to the main sub-headings, which again have circles around them. Continue the process from the sub-headings to sub-sub-headings, etc.

The best approach to revision is to revise the course as you work through it.

Also try to leave four to six weeks before the exam for final revision.

Make sure you cover the whole syllabus.

Pay special attention to those areas where your knowledge is weak.

If you are stuck on a topic find somebody (a tutor) to explain it to you.

Read around the subject – read good newspapers and professional journals, especially ACCA’s Student Accountant – this can give you an advantage in the exam.

Read through the text and your notes again. Maybe put key revision points onto index cards to look at when you have a few minutes to spare.

Practise exam-standard questions under timed conditions. Attempt all the different styles of questions you may be asked to answer in your exam.

Review any assignments you have completed and look at where you lost marks – put more work into those areas where you were weak.

Ensure you know the structure of the exam – how many questions and of what type they are.

Revision

KAPLAN PU BL ISHING 1

Chapter 1

BUSINESS TRANSACTIONS

This chapter introduces the common types of business transaction. Later chapters will look at how transactions are recorded, how accounting records are controlled and how the accuracy of these is scrutinised.

CONTENTS

1 Types of business transaction

2 Cash and credit transactions

3 Terminology

4 Petty cash

5 Payroll

6 Keeping a record

7 Key personnel

8 Control over transactions

9 Timing of transactions

LEARNING OUTCOMES

At the end of this chapter, you should be able to:

• understand the main types of transaction that a business is likely to undertake

• distinguish between cash and credit transactions

• distinguish between transactions in goods and in services

• distinguish between receipts and payments and income and expenditure

• understand the need to document business transactions

• identify the key personnel involved in initiating, processing and completing transactions

• understand the need for effective control over transactions

• identify the timing of various transactions.

PAPER FA 1 : RECORDING F INANCIAL TR ANSACTIO NS

2 KAPLAN PU BL ISHING

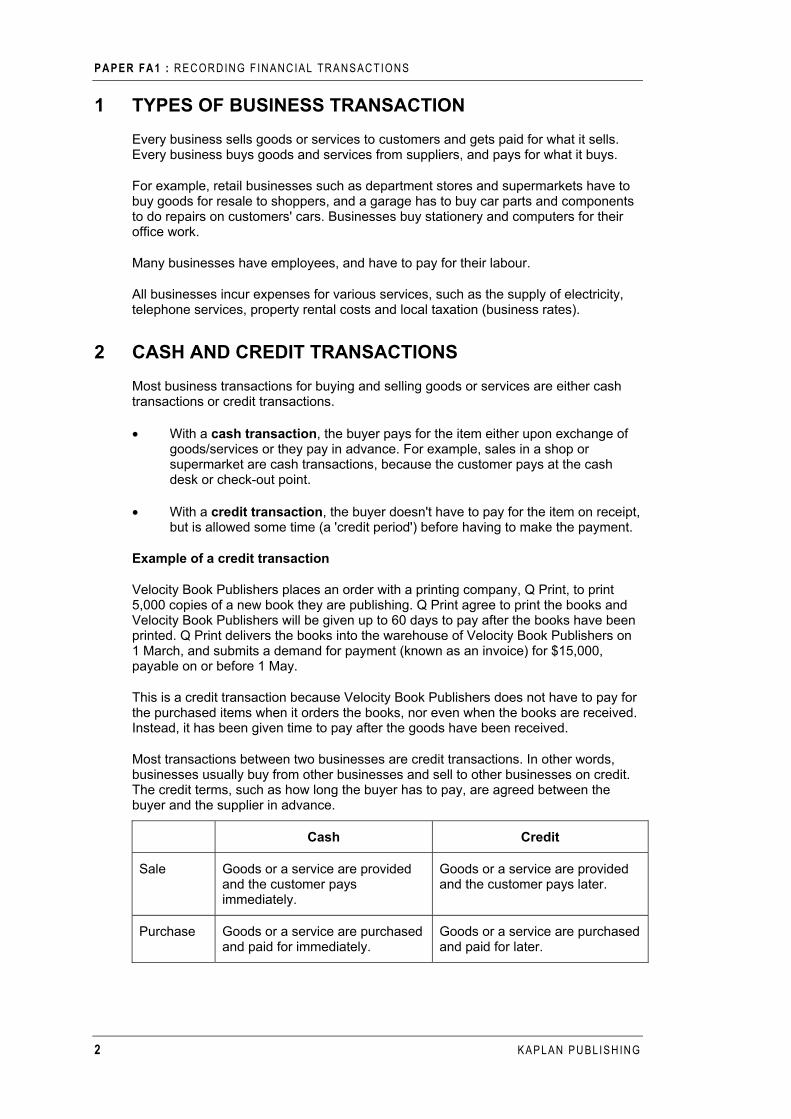

1 TYPES OF BUSINESS TRANSACTION

Every business sells goods or services to customers and gets paid for what it sells. Every business buys goods and services from suppliers, and pays for what it buys.

For example, retail businesses such as department stores and supermarkets have to buy goods for resale to shoppers, and a garage has to buy car parts and components to do repairs on customers' cars. Businesses buy stationery and computers for their office work.

Many businesses have employees, and have to pay for their labour.

All businesses incur expenses for various services, such as the supply of electricity, telephone services, property rental costs and local taxation (business rates).

2 CASH AND CREDIT TRANSACTIONS

Most business transactions for buying and selling goods or services are either cash transactions or credit transactions.

• With a cash transaction, the buyer pays for the item either upon exchange of goods/services or they pay in advance. For example, sales in a shop or supermarket are cash transactions, because the customer pays at the cash desk or check-out point.

• With a credit transaction, the buyer doesn't have to pay for the item on receipt, but is allowed some time (a 'credit period') before having to make the payment.

Example of a credit transaction

Velocity Book Publishers places an order with a printing company, Q Print, to print 5,000 copies of a new book they are publishing. Q Print agree to print the books and Velocity Book Publishers will be given up to 60 days to pay after the books have been printed. Q Print delivers the books into the warehouse of Velocity Book Publishers on 1 March, and submits a demand for payment (known as an invoice) for $15,000, payable on or before 1 May.

This is a credit transaction because Velocity Book Publishers does not have to pay for the purchased items when it orders the books, nor even when the books are received. Instead, it has been given time to pay after the goods have been received.

Most transactions between two businesses are credit transactions. In other words, businesses usually buy from other businesses and sell to other businesses on credit. The credit terms, such as how long the buyer has to pay, are agreed between the buyer and the supplier in advance.

Cash Credit

Sale Goods or a service are provided and the customer pays immediately.

Goods or a service are provided and the customer pays later.

Purchase Goods or a service are purchased and paid for immediately.

Goods or a service are purchased and paid for later.

BUSINESS TRANSACTIONS : C HA P TER 1

KAPLAN PU BL ISHING 3

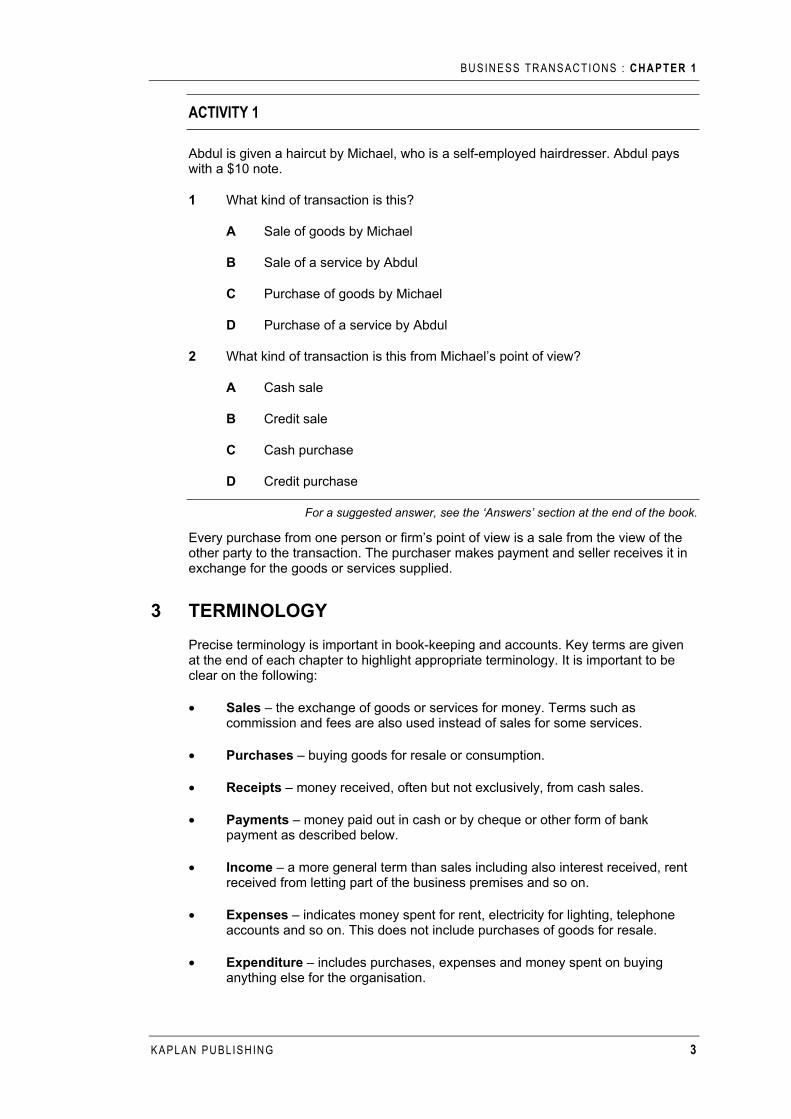

ACTIVITY 1

Abdul is given a haircut by Michael, who is a self-employed hairdresser. Abdul pays with a $10 note.

1 What kind of transaction is this?

A Sale of goods by Michael

B Sale of a service by Abdul

C Purchase of goods by Michael

D Purchase of a service by Abdul

2 What kind of transaction is this from Michael’s point of view?

A Cash sale

B Credit sale

C Cash purchase

D Credit purchase

For a suggested answer, see the ‘Answers’ section at the end of the book.

Every purchase from one person or firm’s point of view is a sale from the view of the other party to the transaction. The purchaser makes payment and seller receives it in exchange for the goods or services supplied.

3 TERMINOLOGY

Precise terminology is important in book-keeping and accounts. Key terms are given at the end of each chapter to highlight appropriate terminology. It is important to be clear on the following:

• Sales – the exchange of goods or services for money. Terms such as commission and fees are also used instead of sales for some services.

• Purchases – buying goods for resale or consumption.

• Receipts – money received, often but not exclusively, from cash sales.

• Payments – money paid out in cash or by cheque or other form of bank payment as described below.

• Income – a more general term than sales including also interest received, rent received from letting part of the business premises and so on.

• Expenses – indicates money spent for rent, electricity for lighting, telephone accounts and so on. This does not include purchases of goods for resale.

• Expenditure – includes purchases, expenses and money spent on buying anything else for the organisation.

PAPER FA 1 : RECORDING F INANCIAL TR ANSACTIO NS

4 KAPLAN PU BL ISHING

3.1 METHODS OF PAYMENT

You need to know about the different methods of receiving payments from customers, or making payments to a supplier. Four common methods of receiving payments and making payments are used in many businesses:

• payments in 'cash', in other words, in notes and coins

• payments by debit and credit cards and electronic payment methods

• payments by cheque

• automated receipts and payments through the business bank accounts. Examples are standing orders and direct debits.

Receiving and making payments by each of these methods will be described in later chapters.

4 PETTY CASH

Most businesses prefer to make as few payments in notes and coins ('cash') as possible. It is more secure to pay by cheque or online because there is less risk of loss or theft. However, sometimes it is more convenient, or even necessary, to make payment in cash.

Examples of items that might be paid for by a business in cash might include the following:

• payment for small office expenses such as coffee, biscuits, stamps etc

• payment for taxi fares for business purposes

• payment for travel costs such as rail and bus for business purposes

• payment for flowers to send to an employee who is off sick.

A small amount in cash is held on business premises for such purposes. In a business that rarely makes cash transactions, such as a large engineering firm, this is convenient. In the type of business that regularly handles cash such as a restaurant, it is useful to keep a small amount of petty cash separate from income received from sales. This makes it easier to reconcile the cash received with the records of meals served and investigate any discrepancies than it would be if a number of employees were able to take cash from the sales income to spend on various expenses at any time.

5 PAYROLL

Many businesses have employees who are paid by the employer for the work they do. Most employers will have a set day on which employees should be paid, and it is the payroll department's responsibility to ensure that wages are paid on the correct due days.

Weekly paid employees (wage earners) will be paid at least once a week, normally on the same day each week. Commonly the pay day will be either Thursday or Friday if the working week is from Monday to Friday.

BUSINESS TRANSACTIONS : C HA P TER 1

KAPLAN PU BL ISHING 5

Monthly paid employees (salary earners) will be paid once a month, and there will be a formula for determining the pay day. For example, this may be:

• the last day of the calendar month

• the last Thursday or Friday of the calendar month

• the same date each month, such as the 26th.

Employees may be paid their wages in several ways:

• in cash

• by cheque

• by bank transfer

• through the Banks Automated Clearing System (BACS).

Making payments by these methods will be described in later chapters.

The payroll department also makes payments to outside agencies, such as tax and social services authorities and pension schemes.

ACTIVITY 2

1 Which of the following terms would be used to classify a payment for electricity to heat the business premises of a firm of plumbers?

A Expense

B Purchase

C Receipt

D Sales

2 Which of the following would be paid for by petty cash?

A Car repairs on the business owner’s private vehicle

B Packet of envelopes at local store

C Paying a supplier for goods bought on credit

D Wages and salaries

3 Which of the following transactions are associated with payroll?

A Income from cash sale of computer used to calculate salaries

B Postage and stationery, office expenses

C Taxes on employee income, pension scheme payments, wages

D Credit purchase of safety equipment for delivery staff

For a suggested answer, see the ‘Answers’ section at the end of the book.

PAPER FA 1 : RECORDING F INANCIAL TR ANSACTIO NS

6 KAPLAN PU BL ISHING

6 KEEPING A RECORD

A business keeps detailed records of its sales, purchases, receipts and payments. There are several reasons for keeping records.

• A business needs to keep track of how much it owes to its suppliers and how much it is owed by credit customers.

• Records of sales and purchases are useful in the event of a query or dispute with a customer or supplier.

• Keeping records of transactions means that checks can be carried out to make sure that they have been processed honestly, and that there have been no mistakes or fraud.

• Keeping records of sales, purchases and other expenses allows a business to monitor how well it is performing, and whether it is making a profit or a loss.

Similar reasons apply to keeping petty cash records. Payroll records must also be maintained to ensure that employees are properly rewarded for their work and to ensure that correct deductions are made.

Transactions are recorded in accounts. The system of recording transactions is therefore called the accounting system or the bookkeeping system. The system organises transactions into sets of structured ledger accounts. Accounting records will be explained in later chapters.

To maintain records, it is important to maintain documents providing evidence of transactions. Chapter 2 looks at these documents in some depth.

7 KEY PERSONNEL

In most businesses it is likely that a number of different people will be involved in different types of business transaction.

For example, in a department store, the sales will be made by the shop floor assistants. The purchases of goods for resale will be made by the departmental buyers. The general expenses will be paid by the accounts department, the wages by the payroll department and any purchases of equipment will probably be made by the store manager.

In a large organisation the number of people involved in business transactions may be in the thousands so it is important to have a system on control over the amount they spend or authorise to prevent the organisation getting into difficulties. Senior management authorise the larger items of expenditure because they have greater knowledge of the business policy and precise financial position of the organisation.

8 CONTROL OVER TRANSACTIONS

If so many people in an organisation are involved in so many different types of transaction then it is important that these transactions are properly controlled. This has two aspects.

• Only properly authorised employees can enter into transactions. For example only properly trained sales assistants can make sales to customers and only the departmental buyer can enter into a transaction to buy goods for the store.

BUSINESS TRANSACTIONS : C HA P TER 1

KAPLAN PU BL ISHING 7

• Transactions are carried out in the correct manner and following the correct procedures. For example, each time a shop assistant makes a sale the amount of the sale must be entered into the till and the money received placed into the till.

When a transaction takes place in a business, the systems that a business operates should ensure the correct recording of the transaction.

For example when money is received for a cash sale this receipt must be recorded as part of the monies received in the day and also as a sale. The accounting systems should ensure that the cash received is rung up on the till and recorded on the till roll. This receipt should then also be recorded in the accounting entries as a sale.

However, on occasions, errors may be made when transactions are recorded. A transaction, or one element of it, may fail to be recorded altogether or it may be recorded at the wrong amount.

Businesses will therefore usually have a variety of internal checks or controls in order to pick up any errors that have been made so that they can be corrected.

8.1 EXAMPLES

The types of internal checks and controls include:

• reconciliations of cash in the till to the till roll records

• checking of the addition of cheque listings used to complete paying in slips

• reconciliations of actual amounts of petty cash to the petty cash records

• checking of accounting entries

• checking of cheque payment or petty cash authorisations, and

• reconciliations of cash records to bank statements received.

9 TIMING OF TRANSACTIONS

The timing and frequency of business transactions will vary. Some, such as sales, may take place on a daily basis, others, such as salaries, on a monthly basis. Items such as electricity and gas bills will tend to be paid on a quarterly basis. Purchases of equipment will probably not be particularly frequent.

Whenever transactions occur they should be promptly recorded in the accounts on the day that they occur. This is important to ensure that the business records are correct and up to date. It is also necessary for legal reasons in respect of sales and other taxes and, as you will see in your later studies, to ensure that the accounts provide a true and fair view of the business to management, owners and others.

PAPER FA 1 : RECORDING F INANCIAL TR ANSACTIO NS

8 KAPLAN PU BL ISHING

ACTIVITY 3

Rachael Linkins is the manager of the Research and Development Unit of a large chemical company. She has been given control of the investigation of the potential healing properties of a naturally occurring compound found in the Amazonian rainforest.

1 State why she will need to ensure careful records are maintained of the receipts and payments associated with this project.

2 Explain why Rachael will need to set up a system of authorisation and control for expenditure.

3 Explain why timing is important when dealing with financial transactions under such a project.

For a suggested answer, see the ‘Answers’ section at the end of the book.

CONCLUSION

All forms of business are set up to provide some form of goods or services to their customers or to benefit the public (i.e. charitable work). In order to facilitate the provision of such goods and services they will need to engage in a series of transactions. These transactions need to be recorded in the bookkeeping system so that the individuals that control the business can print off reports to help them understand the performance and position of the business. This information, if of a good quality, will help them run the business in a more effective and efficient manner.

Cash and credit transactions are used in the sale and purchase of goods and services and in the receipt of income and payment of expenditure.

Small, day-to-day transactions are commonly paid in cash. Larger transactions tend to be paid for by cheque or other payment made from the business bank account, for example; online transfers. Such expenditure is authorised at different levels in the business and within a system of financial control.

Payments to employees are also controlled and authorised and made regularly and in a timely manner, as are all other payments.

KEY TERMS

Account – A record of similar financial transactions in a business.

Expenses – Money spent for rent, electricity for lighting, telephone accounts and so on. This does not include purchases of goods for resale.

Income – A more general term than sales including also interest received, rent received from letting part of the business premises and so on.

Ledger – A set of related accounts.

Payroll – List of employees and the wages or salaries due to each.

Petty cash – A small amount of cash held for the payment of expenses.

Purchases – Buying goods for resale.

BUSINESS TRANSACTIONS : C HA P TER 1

KAPLAN PU BL ISHING 9

Receipt – Written statement of an amount of money that has been paid/received.

Sales – The exchange of goods or services for money. Terms such as commission and fees are also used instead of sales for some services.

Till roll – Printed listing of all payments received through a till/point of sale desk in a retail outlet.

SELF TEST QUESTIONS

Paragraph

1 Explain the difference between a customer and a supplier. 1

2 What is a cash transaction? 2

3 What is a credit transaction? 2

4 Give examples of purchases and expenses. 3

5 When would petty cash be used? 4

6 Name three payments made by the payroll department. 5

7 Give two reasons why a business keeps a record of business transactions. 6

8 Senior personnel authorise major expenditure in a business. Why? 7

9 Give a reason for maintaining a system of internal check or control. 8

10 Why is it important for a business to pay expenses, such as wages, on time? 9

EXAM-STYLE QUESTIONS

1 A business buys goods on credit. When will this require the accounting records to be updated?

A Only when the goods are received

B Only when the goods are paid for

C When the goods are received and again when they are paid for

D When the goods are received, again when they are paid for and when the goods are resold

2 Which of the following describes the receipts generated by an Internet Service Provider?

A Income from sale of goods

B Income from giving a service

C Payments for employees

D Payments for share capital

PAPER FA 1 : RECORDING F INANCIAL TR ANSACTIO NS

10 KAPLAN PU BL ISHING

3 How would you describe petty cash?

A Cash for some small everyday expenses

B An overdraft arranged by the bank

C Spare cash invested in a separate bank account

D Money in the current account

4 Jason Helm runs a stationery business and has sold computer supplies to Peter Simons and Sons for payment in one month. Which of the following are true in respect of this transaction?

(i) It is a cash transaction

(ii) The expenditure must be authorised by Jason Helm

(iii) A record of the transaction must be kept in case of future query

(iv) Jason Helm will need to ensure payment is received in one month

A (i) only

B (ii) and (iii)

C (iii) and (iv)

D All of the above

5 Which section of a grocery business pays salaries?

A Accounts department

B Payroll

C Sales

D Store manager

For suggested answers, see the ‘Answers’ section at the end of the book.