Embed Size (px)

Citation preview

Inventory

Chapter 11

Robinson, Munter, Grant

Grant, Munter & Robinson

Chapter 11 2

Learning Objectives

• Understand the methods for determining inventory values and cost of goods sold

• Understand LIFO layers and liquidation

• Adjust statements for differences in inventory methods

• Explain the impact of capitalization of costs in inventory

Grant, Munter & Robinson

Chapter 11 3

Inventory BasicsCost Flow

BeginningInventory

GoodsPurchased

GoodsAvailable

ForSale

EndingInventory

Cost ofGoods Sold

Balance Sheet Income Statement

Grant, Munter & Robinson

Chapter 11 4

Inventory BasicsCost of Goods Sold

• Periodic Accounting System– Sales and purchases are recorded as they occur

– COGS is recorded at the end of the period after a physical count of ending inventory has been taken

– BI + Purchases (= COGAS) – EI = COGS

• Perpetual Accounting System– COGS is recorded at the time of the sale

– BI + Purchases (= COGAS) – COGS = EI

– Still take physical count to verify EI

Grant, Munter & Robinson

Chapter 11 5

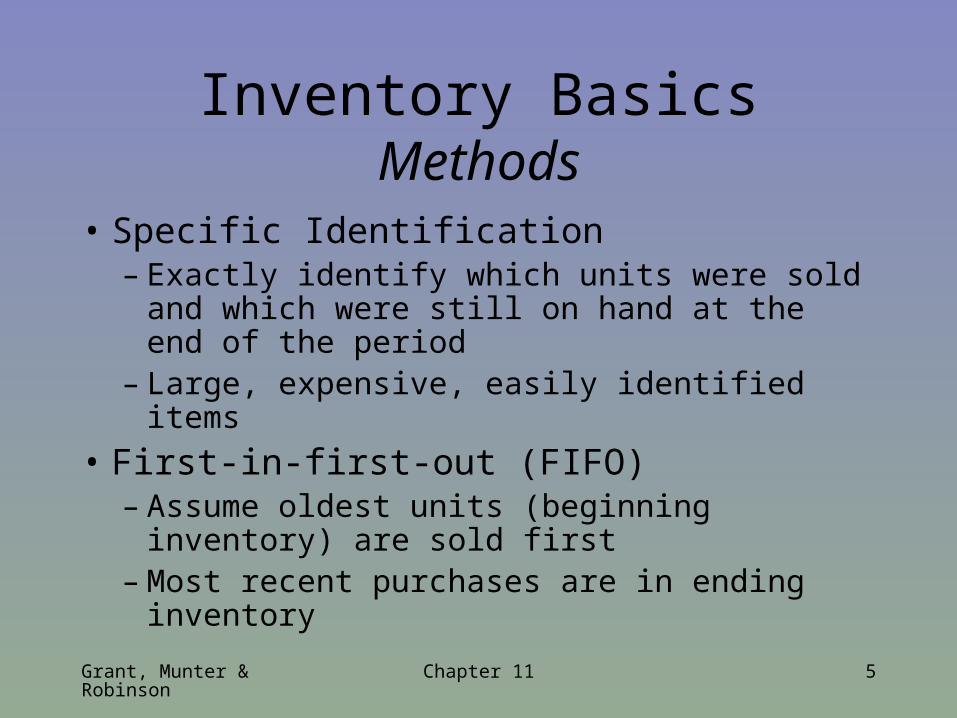

Inventory BasicsMethods

• Specific Identification– Exactly identify which units were sold and

which were still on hand at the end of the period

– Large, expensive, easily identified items

• First-in-first-out (FIFO)– Assume oldest units (beginning inventory) are

sold first– Most recent purchases are in ending inventory

Grant, Munter & Robinson

Chapter 11 6

Inventory BasicsMethods

• Last-in-first-out (LIFO)– Assume newest items are sold first– Oldest items remain in ending inventory– Increases COGS in periods of rising prices

• Average cost– Average cost of a unit sold = $COGAS/# units

available for sale– Use when individual items are indistinguishable

Grant, Munter & Robinson

Chapter 11 7

Inventory BasicsExample

• Beginning inventory consists of 1,000 units at at cost of $5.00 each ($5,000 total)

• 10,000 units were purchased at a cost of $6.00 each

• 2,000 units remain in ending inventory

• 9,000 units were sold for $10.00 each

Grant, Munter & Robinson

Chapter 11 8

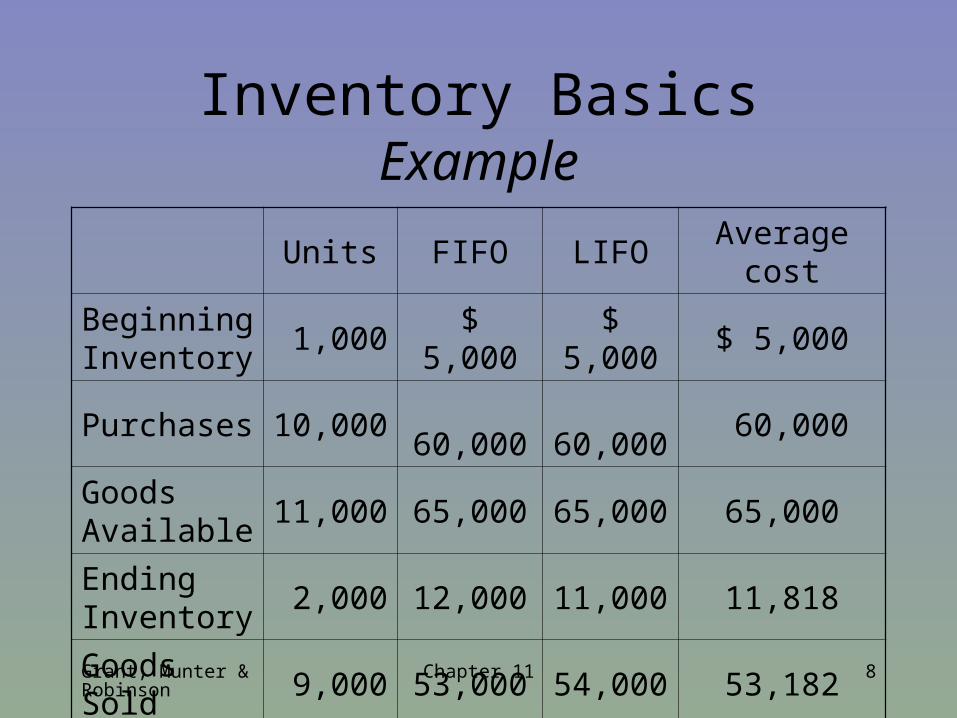

Inventory BasicsExample

Units FIFO LIFO Average cost

Beginning Inventory

1,000 $ 5,000 $ 5,000 $ 5,000

Purchases 10,000 60,000 60,000 60,000

Goods Available

11,000 65,000 65,000 65,000

Ending Inventory

2,000 12,000 11,000 11,818

Goods Sold 9,000 53,000 54,000 53,182

Grant, Munter & Robinson

Chapter 11 9

Impact of FIFO on Financial Statements

• Ending inventory always consists of the company’s most recent purchases.

• FIFO COGS does not necessarily reflect current market conditions.

• Holding gains occur when older, lower cost items are sold at current prices.

• In industries with declining prices (technology) holding losses can occur.

Grant, Munter & Robinson

Chapter 11 10

Impact of LIFO on Financial Statements

• LIFO provides a matching of current revenues and current costs on the income statement.

• Inventory amount on balance sheet does not reflect current costs.

• LIFO layers are added (liquidated) in every period in which purchases exceed (are less than) sales.

Grant, Munter & Robinson

Chapter 11 11

Comparison of LIFO and FIFO

• In periods of rising (falling) prices, the LIFO method normally results in lower (higher) gross profit than FIFO.– Except when LIFO layers are liquidated

• The LIFO Conformity Rule requires companies using LIFO for tax purposes to use LIFO for financial reporting as well.

Grant, Munter & Robinson

Chapter 11 12

Comparison of LIFO and FIFO

• LIFO reserve = FIFO inventory value – LIFO inventory value.

• When prices are rising and LIFO layers are added, the LIFO reserve will increase.

• Similarly, layers will be depleted when the LIFO reserve decreases.

Grant, Munter & Robinson

Chapter 11 13

Implications of Inventory Methods for Financial Analysis

• Caution must be used when net income (plus depreciation) is used to estimate cash flow because it:

• Overstates operating cash flow when prices are rising and the company is using FIFO

• Not useful for either LIFO or FIFO when old inventory layers are depleted

Grant, Munter & Robinson

Chapter 11 14

Implications of Inventory Methods for Financial Analysis

• ROA is lower under LIFO when prices are rising and no LIFO layers have been depleted

• LIFO inventory turnover seems to improve when prices are rising; numerator is higher (more current COGS) while denominator is lower (reflecting older costs)– Can adjust ratio: COGSLIFO/Avg. InventoryFIFO

Grant, Munter & Robinson

Chapter 11 15

Financial AnalysisPeer Comparisons

• If a company is using FIFO or average cost, there is no requirement to present comparable LIFO data.

• Adjustments should be made when subject company does not use the same inventory valuation methods as comparator firms or the industry.

• Using LIFO on the income statement and FIFO on the balance sheet can provide a clearer picture of operating performance.

Grant, Munter & Robinson

Chapter 11 16

Financial AnalysisManagement Decisions

• To avoid liquidation of LIFO layers – and the corresponding higher income tax payment – managers may purchase excess inventory.– Inventory could become obsolete.

• If earnings estimates will not be met, managers may defer inventory purchases, causing a LIFO liquidation and artificially inflating profits.– Income tax payments will also increase.

– May lose sales as a result of insufficient inventory.

Grant, Munter & Robinson

Chapter 11 17

Financial AnalysisMultiple Methods

• Neither LIFO nor FIFO needs to be used exclusively.

• LIFO can be applied to those portions of inventory where the company expects to derive benefits from doing so.

• LIFO may be applied to pools of different items or to individual items of inventory.

• LIFO liquidations are less likely to occur when firms pool inventory.

Grant, Munter & Robinson

Chapter 11 18

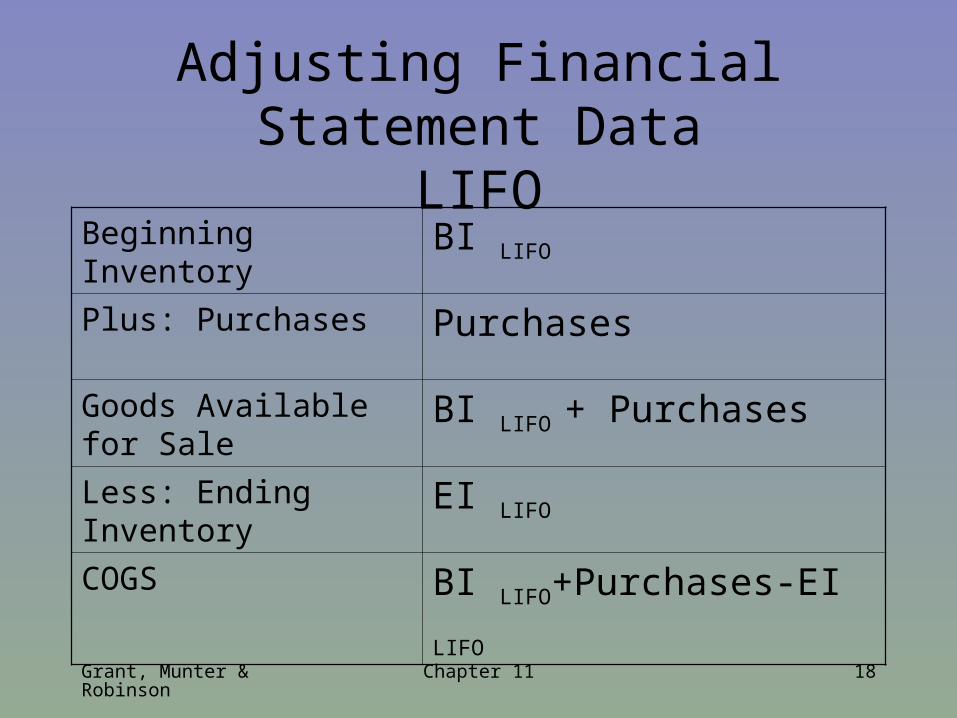

Adjusting Financial Statement DataLIFO

Beginning Inventory BI LIFO

Plus: Purchases Purchases

Goods Available for Sale BI LIFO + Purchases

Less: Ending Inventory EI LIFO

COGS BI LIFO+Purchases-EI LIFO

Grant, Munter & Robinson

Chapter 11 19

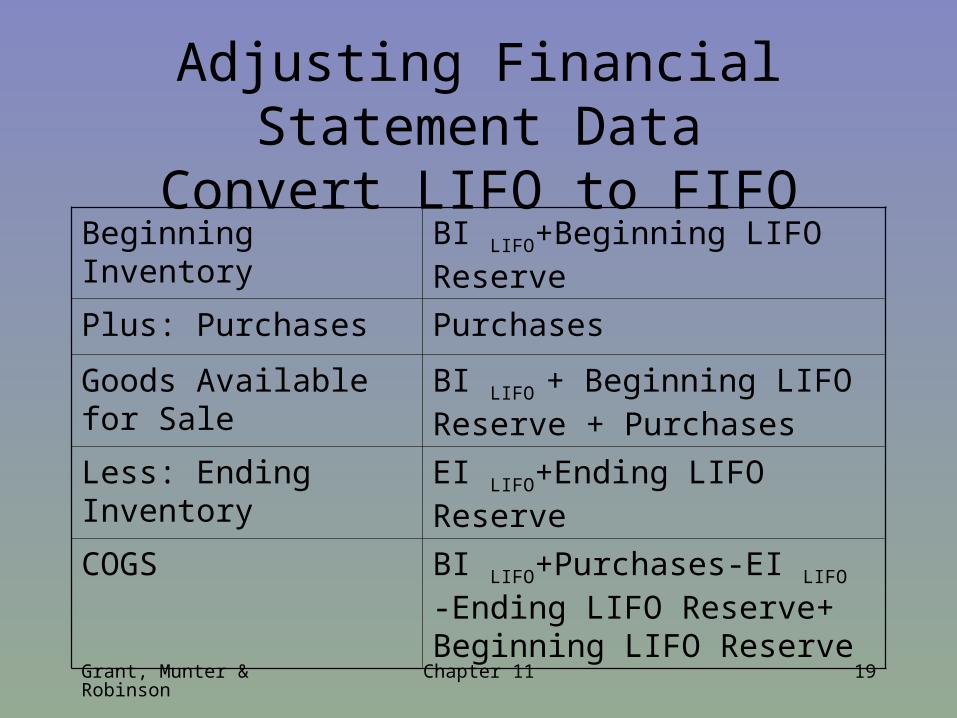

Adjusting Financial Statement DataConvert LIFO to FIFO

Beginning Inventory BI LIFO+Beginning LIFO Reserve

Plus: Purchases Purchases

Goods Available for Sale BI LIFO + Beginning LIFO Reserve + Purchases

Less: Ending Inventory EI LIFO+Ending LIFO Reserve

COGS BI LIFO+Purchases-EI LIFO -Ending LIFO Reserve+ Beginning LIFO Reserve

Grant, Munter & Robinson

Chapter 11 20

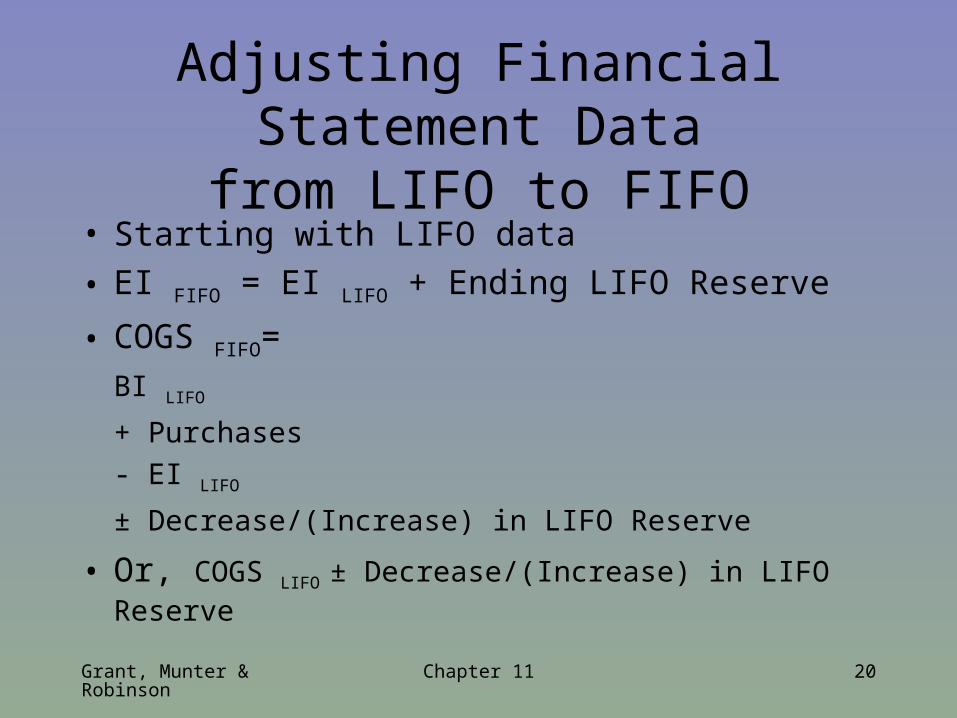

Adjusting Financial Statement Datafrom LIFO to FIFO

• Starting with LIFO data

• EI FIFO = EI LIFO + Ending LIFO Reserve

• COGS FIFO=

BI LIFO

+ Purchases

- EI LIFO

± Decrease/(Increase) in LIFO Reserve

• Or, COGS LIFO ± Decrease/(Increase) in LIFO Reserve

Grant, Munter & Robinson

Chapter 11 21

Adjusting Financial Statement Datafrom LIFO to FIFO

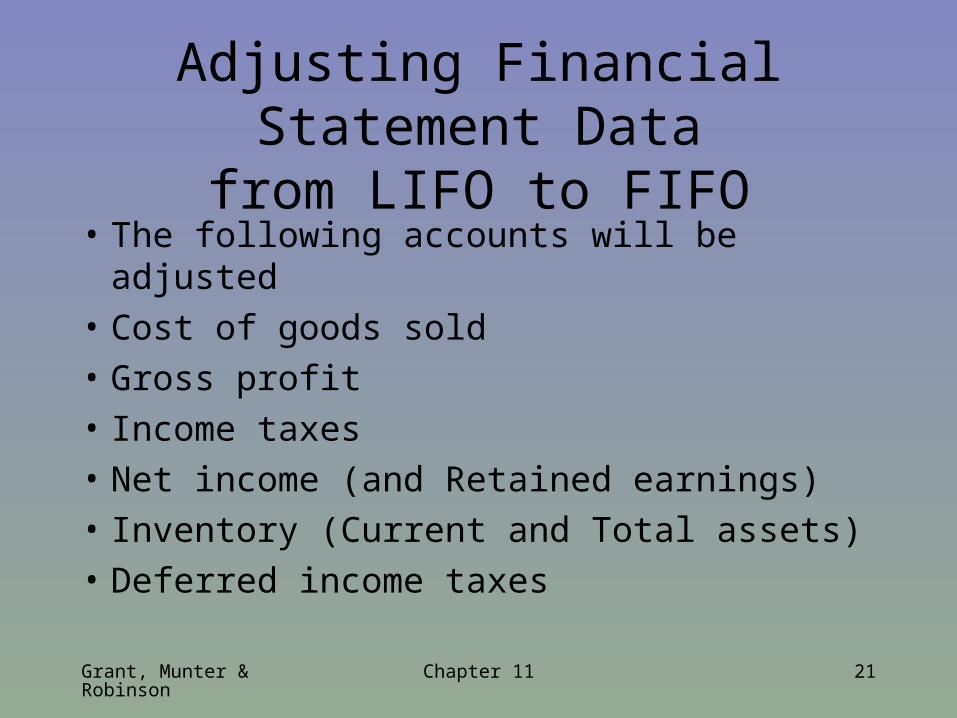

• The following accounts will be adjusted

• Cost of goods sold

• Gross profit

• Income taxes

• Net income (and Retained earnings)

• Inventory (Current and Total assets)

• Deferred income taxes

Grant, Munter & Robinson

Chapter 11 22

Why use LIFO?

• Improve cash flow in periods of rising prices.– Tax deferral

• Better matching of current operating costs to revenues.

• No benefit from LIFO if– No tax due

– Immaterial, rapidly turning or declining prices of inventory

– LIFO is costly to maintain

Grant, Munter & Robinson

Chapter 11 23

Inventory Method Changes

• Tax regulations restrict changes– May require IRS approval

• If adopting LIFO, existing inventory value becomes first LIFO layer

• If switching from LIFO all periods in the financial statements must be restated

Grant, Munter & Robinson

Chapter 11 24

Costs to Capitalize

• IAS No. 2: Cost of inventories can include:• All costs of purchase

– Including taxes, transportation, discounts…

• Costs of conversion– Direct labor and direct overhead

• Other costs incurred in bringing inventories to their present location and condition– Indirect overhead, product design costs

Grant, Munter & Robinson

Chapter 11 25

Do Not Capitalize

• IAS No. 2: Cost of inventories exclude:

• Abnormal waste (materials, labor and OH)

• Storage costs except as part of production

• Administrative overhead

• Selling expenses

• Note: US GAAP is similar to IAS regarding capitalization of inventory costs

Grant, Munter & Robinson

Chapter 11 26

Service Firms

• Capitalize as inventory:

• Labor and other costs directly related to providing services– Including supervisory personnel

• Accumulate costs in inventory

• Expense when related revenues are reported

Grant, Munter & Robinson

Chapter 11 27

Tax Rules

• In the US, tax rules (§263A) require additional capitalization of indirect costs

• Storage and warehousing

• Depreciation

• Quality control

• A portion of General and Administrative costs

Grant, Munter & Robinson

Chapter 11 28

Inventory Overstatement

• Overstating ending inventory will overstate earnings– Include obsolete or nonexistent inventory– MiniScribe Corp. shipped bricks instead of disk

drives

• Firms may capitalize costs that should be expensed

Grant, Munter & Robinson

Chapter 11 29

Declines in Inventory Cost

• Inventory is reported at the lower of cost or market value

• When current market values fall below cost, the adjustment is to inventory and cost of goods sold

• Can lead to managerial manipulation

Grant, Munter & Robinson

Chapter 11 30

Summary

• Inventory valuation methods– LIFO, FIFO, Average cost, Specific

identification

• Differences between methods

• Adjustments necessary for financial statement analysis

• Costs capitalized in inventory