Embed Size (px)

Citation preview

Research ArticleInventory Financing with Overconfident Supplier Based onSupply Chain Contract

Weifan Jiang 12 and Jian Liu 1

1School of Information Technology Jiangxi University of Finance and Economics Jiangxi Nanchang 330013 China2School of Business Administration Nanchang Institute of Technology Jiangxi Nanchang 330099 China

Correspondence should be addressed to Jian Liu liujian3816263net

Received 12 June 2018 Revised 13 August 2018 Accepted 1 September 2018 Published 25 September 2018

Academic Editor Yakov Strelniker

Copyright copy 2018 Weifan Jiang and Jian Liu This is an open access article distributed under the Creative Commons AttributionLicense which permits unrestricted use distribution and reproduction in any medium provided the original work is properlycited

Overconfidence is a universal psychological behavior Overconfidence on demand awareness will have a significant impact onoperation decisionsThe supplier estimated the demandwith excessive precision which influences the inventory financing decision-making deeply We built the demand function based on the supplierrsquos overconfidence Then we established the retailer supplierand the Bankrsquos profit function respectivelyThrough the analysis of the bilevel Stackelberg game we obtained the order quantity ofthe retailer with the capital constraint the wholesale price of overconfident supplier and the loan-to-value ratio of Bank and weanalyzed the influence of overconfidence on the decision variables We have several findings as follows First the overconfidencemakes the decisions of the retailer supplier and Bank deviate from the rational decisions Second the space of the market profitwill affect the decision variables in the joint decision-making Third the financing supply chain (including the Bank and supplychain) should have a positive attitude towards the overconfidence of the supplier Forth in the joint decision-making the supplierneed determines the buyback price according to the capital demand and in the decentralized decision-making the supplier shouldtry to use high buyback price strategy

1 Introduction

Fund shortage and high financing cost have been a bottleneckin the development of SMEs (small and medium-sizedenterprise) According to the 2014 China SMEs developmentreport released by China Southwestern University of Financeand Economics 258 of the 58 million SMEs of Chinahave loan demand However only 46 of these companiesreceived Bank loans 116 of these companies were rejectedand 424 of these companies did not apply the loan Dueto the characteristics of the enterprise weak solvency smallfinancing scale poor financial regulation and lack of perfectcorporate governance mechanism the SMEsrsquo ability to resistrisk is weak generally Since banks have set up complex riskcontrol procedures to control risks large financial institutionslack relevant financial services solutions for SMEs generallyIn this case large amount of money in Banks has nowhereto lend The SMEs usually obtained financing through

undergroundBanks private funds guarantee companies andinvestment companies

Think of the core enterprise in the supply chain and itsrelated upstream and downstream supporting enterprises asa whole according to the trading relationship of enterprisesin the supply chain and industry characteristics developing afinancingmode based on cargo rights and cash flow control asa whole financial solution The supply chain financing serviceis different from the traditional Bank financing productsAround the upstream and downstream enterprises whichhave good credit stable sales channels and return fundsources the supply chain financing service takes the largeenterprises as the core and selects qualified upstream anddownstream enterprises as the financing objects Supplychain financing solves the difficulty about upstream anddownstream enterprises financing and guarantees and elimi-nates the financing bottleneck of upstream and downstreamalso can reduce the supply chain financing costs and improve

HindawiMathematical Problems in EngineeringVolume 2018 Article ID 5054387 12 pageshttpsdoiorg10115520185054387

2 Mathematical Problems in Engineering

the competitiveness of the core enterprises and related enter-prises

The flow capital of a single enterprise is mainly occupiedin the form of accounts receivable and inventory Accordingto the difference of guarantee measures the financial institu-tions divide the basic products of supply chain financing intotwo categories accounts receivable financing and inventoryfinancing

Accounts receivable financing means a financing modethat SMEs use undue receivables committed by the coreenterprises in the supply chain to obtain the fund fromthe financial institutions Carrefour is a global top 500enterprise with a steady operation a clear term of paymentfor upstream suppliers and the ability to execute the contractCarrefour has tens of thousands of suppliers worldwideThe Bank can design a supply chain financing mode forCarrefourrsquos upstream suppliers In the past several yearsthe Banks has been giving the supplier a credit limit afterthe comprehensive assessment which can be recycled afterpayment andCarrefour needs to pay the Bank which formeda closed capital chain cycleThe supply chain financing modecan alleviate the pressure of suppliersrsquo funds and promote theBanks to get more customers

Inmany cases there is no corresponding accounts receiv-able and credit guarantee for the enterprises in the supplychain besides the goods At this time financial institutionscan give the credit to the enterprises with inventory financingmode Inventory financing is a financing business of SMEswhich uses raw materials semifinished products and fin-ished products as collateral to obtain loans from financialinstitutions The traditional Bank loans are concentrated onthe fixed assetsmortgage or the third-party corporation guar-antee Inventory financing is that the SMEs use inventory inthe trade between enterprises and upstream and downstreamenterprises as collateral and then the SMEs obtain loansfrom financial institutions such as Banks In the inventoryfinancing the financial institutions are to give credit to theenterprise after the evaluation of inventory values by thethird-party logistics enterprises For SMEs with financingneeds the lack of fixed assets makes it difficult to obtain loansfrom the Banks In the developed countries the inventoryfinancing business has been mature In developed countriessuch as the United States 70 of the guarantee comes fromaccounts receivable and inventory In China although theinventory financing just started its development speed wasastonishing Since the first inventory financing carried out byChina Materials Storage and Transportation Group Co Ltd(CMST) with the financial institutions in 1999 the CMSThave set up inventory financing with dozens of Banks suchas Bank of China and China Construction Bank

In the actual business process decision-makers areoverconfident Overconfidence is a universal psychologicalbehavior People often think that they are superior to othersin the analysis and judgment Fischhoff et al [1] througha study of 528 paid volunteers show that people are alwaysoverconfident They tend to have enough confidence in thejudgment and overestimate the chances of success Weinstein[2] tested 120 female college students and found that peoplealways overestimated their own favorable factors and they

did not think that others had the same factors at the sametime a survey of more than 200 college students foundthat people were always optimistic about the chances ofsuccess Moore [3] through the literature review on theoverconfidence found that overconfidence was always man-ifested in three categories overestimation overplacementand overprecision

At present most of the researches on inventory financingdecisions are based on the assumption that decision-makersare rational Decisions made by the overconfident decision-maker often deviate from traditional decisions This papermainly analyzed enterprise decision-making under inventoryfinancing environment This paper quantified the decisionvariables of all parties through the bilevel Stackelberg gameanalyzed the influence of the degree of overconfidence onthe decision-making of all parties and then discussed theinfluence of the different supplierrsquos buyback strategies on theinventory financing and sought a strategy that can benefit thethree parties in the inventory financing

The remainder of this paper is organized as follows Therelated research is reviewed in Section 2 The notation andassumptions are given in Section 3 The model of Bankprofit is given in Section 4 We studied the joint decision ofsupply chain in Section 5 We studied the wholesale pricecontract with buyback in Section 6 We carefully comparedthe profits under the different decision modes in Section 7We concluded the conclusion and operation suggestions inSection 8

2 Literature Review

Our work is related to two streams of literature one dealwith inventory financing and the other dealing with overcon-fidence

On the aspect of inventory financing business operationBurman [4] put forward two modes of inventory and receiv-ables financing from the perspective of practice Guttentag [5]introduced the businessmodes controlmethods advantagesand disadvantages of inventory financing in 1950s and 1960sMiller [6] analyzed the new characteristics of the commercialmode of inventory financing during the 1970s-1980s Lacroixand Varangis [7] compared the inventory financing of theUnited States and the developing countries and introducedthe related business modes and the measures to promote thedevelopment of financing Rutberg [8] analyzed the maincharacteristics of the inventory financing mode from theaspects of business characteristics and operation mode withUPS as an example Hofmann [9] provided a conceptualexplanation of the relevance and the implications of alterna-tive inventory financing by a logistics service provider Theearly research mainly focused on the discussion of inventoryfinancing business and analyzed the process characteristicsand operation mode of inventory financing

The inventory financing business is a new financialservice mode The Bank had developed the inventory financ-ing business actively It is necessary to set the loan cyclethe mark-to-market frequency the warning value and theinterest rate so as to control the risk effectively Jokivuolle

Mathematical Problems in Engineering 3

andPeura [10] studied the loan-to-value ratio of the inventoryfinancing when the price fluctuated with the Merton struc-tural method Cossin and Hricko [11] considered the creditrisk in the pledge management constructed the credit riskpricing model which is different from the newsboy modeldetermined the discount rate of the inventory financingbusiness and obtained the loan-to-value ratio by 1 minusthe discount rate He et al [12] established a model withthe formula AR (1)-GARCH (11)-GED using the databaseof spot steel forecasted the VaR of steel during the differentrisk windows in the impawn period through a methodof out-of-sample and got the impawn rate according withthe risk exposure of Banks Li [13] adopted risk evaluationmethod of ldquocorporate and debtrdquo considered the impact oftime to capture and liquidity risk established loan-to-valueratio decision model of inventory financing with randomly-fluctuate price then took copper for an example confirmedall model parameters and analyzed the impact of differentfactors on loan-to-value ratio He et al [14] proposed a newlong-term extreme price risk (value at risk and conditionalvalue at risk) measure method for inventory portfolio andan application to dynamic impawn rate interval Zhang etal [15] assumed that the short-term prices of the collateralfollow a geometric Brownian motion and use a set ofequivalent martingale measures to build the models abouta Bankrsquos maximum and minimum levels of risk tolerance inan environment with Knightian uncertainty However theseresearches only considered the loan decision of the Bankalone and did not consider the game between Bank and thecapital-shortage enterprise which will influence the decisionof the Bank

As the loan enterprise of inventory financing its financ-ing decision will directly affect the operation performanceof the enterprise On the operation decision based on theinventory financing Buzacott and Zhang [16] studied assetsfinancing from the perspective of the enterprise first com-bined the loan risk management of financial institutions withthe inventory control of the loan enterprises and analyzedthe choice of the loan interest rate and the loan value ratioand their impact on the profits of the financial institutionsand the loan enterprises The problem of discussion is thatthe enterprise purchased the products by the loan and all theinventory is used as a pledge which belongs to a stage ofdecision-making process Wang et al [17] studied the robustinventory financing model under partial information thatis where the demand distribution is partly known In thissetting the robust method that maximizes the worst-caseprofit and minimizes the firmrsquos maximum possible regretof not acting optimally would be used to formulate theoptimal sales quantity SMEs credit risk is significant forguaranteeing supply chain financing in smooth operationLi et al [18] adopt the logistic regression tool to measurethe default probability of the risk model and made anempirical analysis of themodel based on 177 sample data fromChinarsquos commercial Banks concerning automobile and steelindustries Zhu et al [19] applied six methods to predict theSMEs credit risk

Inventory financing business cannot be carried out with-out the participation of third-party logistics Diercks [20]

illustrated the necessity of the third-party logistics enter-prises to participate in the inventory financing business Ininventory financing asymmetric information between theBanks and the third-party logistics enterprises may incurmoral risks and often causes economic losses of the Banks Toeffectively solve this problem Sun et al [21] designed a pureincentive scheme and a regulatory incentive scheme with theprincipal-agent theory Song et al [22] proposed a pricingmodel of inventory financing that canmaximize the cash flowof the 3PL enterprise when the default rate of the SMEs isaffected by the pledge priceThese researches do not considerthe impact of supply chain contract on financing

The decision of inventory financing enterprises is notisolated They are influenced by the business related par-ties The pricing strategy of the supplier and the lendingpolicy of the Bank will all affect the financing decisionof the enterprise On the supply chain management basedon the inventory financing Lee and Rhee [23] discussedcoordination mechanisms by explicitly assuming capital-constrained agents and positive inventory financing costsYan and Sun [24] designed a capital-constrained supply chainsystemwith amanufacturer and a capital-constrained retailerwho can obtain short-term financing from the commercialBank through inventory financing according to the value ofthe pledged warehouse receipt Using the system dynamicsmethodology they modelled the stock and flow diagramsand simulated the system characteristics for nonfinancingscheme and inventory financing scheme respectively Yan etal [25] designed a supply chain financing system with aman-ufacturer a retailer and a commercial Bank where both theretailer and the manufacturer are capital constrained underdemand uncertainties They formulated a bilevel Stackelberggame for the supply chain financing system in which theBank acts as the leader and themanufacturer as the subleaderConsidering the bankruptcy risks of the manufacturer andthe retailer they analyzed the optimal financing interestrate for the commercial Bank the optimal order for theretailer and the optimalwholesale price for themanufacturerrespectively On the basis Yan et al [26] performed a com-parative analysis of the optimal strategies among the variousfinancing scenarios Lin et al [27] found that the vendershould provide the complete buyback when the demandis uncertain and affected by retailersrsquo sales efforts so theyput forward three modified modes of inventory financingto achieve Pareto-Improvement Based on the analyticalformulation of the benefits of three relevant supply chainfinance schemes (Reverse Factoring Inventory Financingand Dynamic Discounting) Gelsomino et al [28] formalizedamodel that investigated the benefits that a buyer can achieveby onboarding suppliers onto these three schemes

The traditional operations researches are usually basedon the rational hypothesis and ignore the influence of psy-chological factors on the decision-making behavior whichleads to the deviation of the research results and the actualsituation In order to accurately reflect managersrsquo decision-making behavior many scholars have introduced humanbehavior factors into supply chain management In the fieldof operation and management Croson et al [29] introducedoverconfidence behavior into the supply chain model and

4 Mathematical Problems in Engineering

studied the newsboy model with overconfidence behaviorRen and Croson [30] studied decision-makers in the case ofoverprecision estimation and described the overconfidencebehavior of decision-makers through the newsboy model Itis proved that overconfidence is the cause of the mean biaseffect in the newsboy decision-making experiment Based onthese research results Ren et al [31] further demonstratedthat order bias is linear in the level of overconfidence andis increasing with the variance of the demand distributionOrder bias also has a U-shaped relationship with marketprofitability and the costs of overconfidence are convex Lu etal [32] studied inventory decision-making and performanceevaluation under various overconfidence forms respectivelyMa et al [33] studied advertising and pricing strategies ofoverconfident manufacturers in dual channel competitionenvironment Li et al [34] studied the effects and implica-tions of overconfidence in a competitive newsvendor settingThey found that when the productrsquos profit margin is highoverconfidence can lead to a first-best outcome In a similarvein they found that the more biased of two competingnewsvendors is not necessarily destined to a smaller expectedprofit than its less biased competitor Xu et al [35] analyzedthe impact of the retailerrsquos overconfidence on the supply chainperformance They considered a duopolistic market withuncertain demand where one overconfident retailer and onerational retailer compete in selling the same product Theseliteratures have studied the incentive contract in the contextof overconfidence but it is mainly about the production andsales decisions of supply chain enterprises and the coordi-nation between upstream and downstream Enterprises havecapital constraints in reality so it is necessary to study theinventory financing based on the overconfidence designthe corresponding incentive mechanism and eliminate thenegative effects of overconfidence

There are overconfidence behaviors in supply chainmem-ber enterprises Overconfidence has an important influenceon the inventory financing decision and operation strategyof supply chain Our study differs from the existing literaturein that it analyzes the inventory financing decisions ofsupplier retailer and Bank in the context of overconfidenceThe supplier is overconfident on demand and the retailerand the Bank are rational We went through Stackelberggame to quantify the decision variables analyze the effect ofsupplier overconfidence degree on the decision and discussthe impact of different supplier buyback policy on inventoryfinancing

3 Notation and Assumptions

The supplier in this article is overconfident in the accuracyof market demand forecasting and the retailer is rationalabout demand The retailer is a small and medium-sizedenterprise with limited funds and the retailer gets loansfrom the Bank through inventory financing In the inventorypledge business the supplier sets the wholesale price theretailer decides the order quantity and the Bank decides theloan-to-value ratio Inventory financing business processesare as follows First of all the supplier and the retailer signthe purchase contract then the retailer with the purchase

supplier

Bank

retailer

The third party logistics

1 Sign a purchase contract

2 Apply for a loan

2 Confirmation of buyback agreement3 Acceptance

bill

3 The completion of payment

4 Delivery of the goods

6 Delivery of the goods

5 Money of sales

Figure 1 The process of inventory financing

contract gets the inventory pledge loan from the Bank andat the same time the supplier signs the buyback agreementwith the bank According to the loan-to-value ratio the bankdraws the acceptance bill for the supplier The retailer paysthe remaining payment with their ownmoney to the supplierThe supplier sends the goods to the third-party logisticsenterprise which is designated by the Bank for supervisionthe Bank instructs the third-party logistics enterprise todeliver the goods according to the amount of money of thespecified supervision account which is from the sale of theretailer At the end of the sale term if the products haveremains the supplier will buy back the products accordingto the agreement signed with the Bank The inventory pledgebusiness is shown in Figure 1

31 Symbolic Description In order to facilitate the descrip-tion of the model various variables are given in Table 1

32 Assumptions Assumptions about the model are as fol-lows

(1) We assume that the market demand is 119863 whichis a nonnegative random variable The distribution anddensity function are 119865(sdot) and 119891(sdot) respectively Other nota-tions for the probability distribution include complementary119862119863119865 119865 = 1 minus 119865(sdot) and failure rate ℎ(sdot) = 119891(sdot)119865(sdot)The demand distribution is assumed to have an increasingfailure rate (IFR) a mild condition that is satisfied by mostcommonly used distributions We set the mean of119863 as 120583 andthe variance of119863 as 1205902

(2) We assume that the overconfident supplier deem thedemand is119863119900119863119900 = (1minus120573)119863+120573120583 [29 30 34]Thedistributionand density function is 119865119900(sdot) and 119891119900(sdot) respectively We canknow themean of119863119900 is 120583 the variance of119863119900 is (1minus120573)21205902Thesupplierrsquos overconfidence is about the accuracy of demandforecasting 0 le 120573 le 1 The larger the 120573 value the moreoverconfident the supplier is As the value of 120573 approaches1 the supplier considers the market demand to be a constant

Mathematical Problems in Engineering 5

Table 1 Decision variables and model parameters

Decision variable of the Bank120596 the loan-to-value ratioDecision variable of the supplier119908 the wholesale priceDecision variable of the retailer119902 the order quantity of the retailer 119902119900 is order quantity with overconfident supplier 119902119903 is order quantity with rational supplierParameters1199031 the deposit interest rate1199032 the loan interest rate which include all expenses incurred during the pledge period119901 the sale price of the product119888 the cost of the productV the buyback price of the product119904 the salvage value of the product119879 the period of the inventory pledge loan contract the unit is year value range is 0 lt 119879 le 1

rather than a random variable 120573 = 0 shows that the supplieris rational in the demand forecasting precision

(3)Without regard to the loss of sale the unsold productsare repurchased by the supplier with price V

(4) The Bank evaluates the product with the sale price(5) The retailer is short of money is more cautious with

their decisions and has a better view of the market so weassume that the retailer is rational and the Bank makes thedecision based on the loan application so the judgment ondemand of the Bank is the same as that of retailerrsquos

4 Model of Bank Profit

In the inventory pledge business the Bank provides loans tothe retailer with the loan interest rate of 1199032 the loan amountis 119861 = 120596119902119901 and the retailer pays the principal and interest120596119902119901(1 + 1198791199032) when the loan is due When the retailer failsto repay the loan the products will be repurchased by thesupplier at the price of V and the Bank loan will be repaidwith the buyback money

At the end of the sale the retailer will default if theretailerrsquos sales and buyback value of the remaining productscannot repay the Bankrsquos principal and interest Let theprobability of default be 120576 When the retailer defaults theBank returns are 119901min(119863 119902) + V(119902 minus 119863)+ minus 120596119902119901(1 + 1198791199031)otherwise the Bankrsquos profit is 120596119902119901(1 + 1198791199032) minus 120596119902119901(1 + 1198791199031)

Let the critical value of product demand be 120575 When theactual demand is the critical value the retailerrsquos product salesand buyback value of the remaining products are equal tothe Bankrsquos principal and interest Below this threshold theretailer will default

Proposition 1 The default probability of retailer is 120576 =119865((120596119902119901(1 + 1198791199032) minus V119902)(119901 minus V))Proof The default condition of the retailer is

119901min (120575 119902) + V (119902 minus 120575)+ le 120596119902119901 (1 + 1198791199032) (1)

When default occurs the critical demand is 120575 le 119902 somin(120575 119902) = 120575

We can get 119901120575 + V(119902 minus 120575) le 120596119902119901(1 + 1198791199032)When 120575 le (120596119902119901(1+1198791199032)minusV119902)(119901minusV) the retailer chooses

to defaultSo we can get the default probability of the retailer 119875(119863 le120575) = 119865((120596119902119901(1 + 1198791199032) minus V119902)(119901 minus V))The critical value of product demand is 120575 = (120596119902119901(1 +1198791199032) minus V119902)(119901 minus V) and the Bankrsquos profit is as follows

120587119887 = 120596119902119901119879 (1199032 minus 1199031) 119863 ge 120575119901119863 + V (119902 minus 119863) minus 120596119902119901 (1 + 1198791199031) 119863 lt 120575 (2)

We can find that the expected profit of the Bank is

119864120587119887 = 120596119902119901119879 (1199032 minus 1199031) minus (119901 minus V) int1205750119865 (119909) 119889119909 (3)

By taking the first derivatives of 119864120587119887 with respect to120596 wehave

119889119864120587119887119889120596 = 119902119901119879 (1199032 minus 1199031) minus 119902119901 (1 + 1198791199032) 119865 (120575) (4)

Because 11988921198641205871198871198891205962 = minus([119902119901(1+1198791199032)]2(119901minusV))119891(120575) lt 0let 120597119864120587119887120597120596 = 0 and set119866 = 119879(1199032 minus1199031)(1+1198791199032) we find thatthe optimal loan-to-value ratio will satisfy

120596 = (119901 minus V) sdot 119865minus1 (119866) + V119902119902119901 (1 + 1198791199032) (5)

5 Joint Decision of Supply Chain

Theoverconfident supplier is the core enterprisewhichmakesthe decision in the joint decision-making Let 119902119900 be the orderquantity in the overconfident condition The overall profit ofthe supply chain is as follows

120587119888 = 119901min (119902119900 119863119900) + 119904 (119902119900 minus 119863119900)+ minus 119888119902119900 minus 1205961199021199001199011198791199032 (6)

6 Mathematical Problems in Engineering

We can obtain the whole supply chain expects profit asfollows

119864120587119888 = (119901 minus 119888) 119902119900 minus (119901 minus 119904) int119902119900

0119865119900 (119909119900) 119889119909119900 minus 1205961199021199001199011198791199032 (7)

Proposition 2 In the joint decision-making the optimal-order quantity and the loan-to-value ratio are

(1) 119902119900lowast = 119865119900minus1((119901 minus 119888 minus V1198791199032(1 + 1198791199032))(119901 minus 119904))(2) 120596 = ((119901 minus V) sdot 119865minus1(119866) + V119902119900lowast)119902119900lowast119901(1 + 1198791199032)

Proof Using Stackelberg game the supply chain first deter-mines the order quantity and then the Bank decides the loan-to-value ratio Using the inverse method the loan-to-valueratio of the Bank is determined first which is (5)

By taking the first derivatives of 119864120587119888 with respect to 119902119900we have

119889119864120587119888119889119902119900 = (119901 minus 119888) minus (119901 minus 119904) sdot 119865119900 (119902119900) minus 1205961199011198791199032

minus 119889120596119889119902119900 1199021199001199011198791199032

(8)

Because 119889120596119889119902119900 = minus(119901minus V)119865minus1(119866)1199021199002119901(1 +1198791199032) we cansimplify (8) to

119889119864120587119888119889119902119900 = (119901 minus 119888) minus (119901 minus 119904) 119865119900 (119902119900) minus

V1198791199032(1 + 1198791199032) (9)

Because 11988921198641205871198881198891199021199002 = minus(119901minus119904)119891119900(119902119900) lt 0 let 119889119864120587119888119889119902119900 =0 and we find that the optimal-order quantity will satisfy

119902119900lowast = 119865119900minus1 (119901 minus 119888 minus V1198791199032 (1 + 1198791199032)119901 minus 119904 ) (10)

We substitute (10) into (5)

120596 = (119901 minus V) sdot 119865minus1 (119866) + V119902119900lowast119902119900lowast119901 (1 + 1198791199032) (11)

Proposition 3 In the rational joint decision the order quan-tity is 119902119888119903lowast In the overconfident joint decision the order quantityis 119902119888119900lowast We can know that 119902119888119900lowast = (1 minus 120573)119902119888119903lowast + 120573120583Proof The optimal decision in a rational situation conformsto 119902119888119903lowast = 119865minus1((119901 minus 119888 minus V1198791199032(1 + 1198791199032))(119901 minus 119904))

We let 120578 = (119901 minus 119888 minus V1198791199032(1 + 1198791199032))(119901 minus 119904) and then wecan get 120578 = 119865(119902119888119903lowast)

Because 119863119900 = (1 minus 120573)119863 + 120573120583 we know119865119900 (119863119900) = 119875 ((1 minus 120573)119863 + 120573120583 le 119863119900) = 119865(119863119900 minus 1205731205831 minus 120573 ) (12)

The optimal decision in overconfident situation conformsto

119902119888119900lowast = 119865119900minus1 (119901 minus 119888 minus V1198791199032 (1 + 1198791199032)119901 minus 119904 ) = 119865119900minus1 (120578)120578 = 119875 (119902119888119900 le 119902119888119900lowast) = 119875 ((1 minus 120573) 119902119888119903 + 120573120583 le 119902119888119900lowast)= 119865(119902119888119900lowast minus 1205731205831 minus 120573 )

119865 (119902119888119903lowast) = 119865(119902119888119900lowast minus 1205731205831 minus 120573 )

(13)

We can get 119902119888119900lowast = (1 minus 120573)119902119888119903lowast + 120573120583Proposition 4 When demand follows normal distributed inthe high-profitmarket environment ie119901minus119888minusV1198791199032(1+1198791199032) gt(12)(119901 minus 119904) we have 119902119900lowast gt 120583 and the greater the degree ofoverconfidence in the accuracy of the prediction the lower theorder quantity and the greater the loan-to-value ratio in thelow profit market environment ie 119901 minus 119888 minus V1198791199032(1 + 1198791199032) lt(12)(119901 minus 119904) we have 119902119900lowast lt 120583 and the greater the degree ofoverconfidence in the accuracy of the prediction the higher theorder quantity and the lower the loan-to-value ratio while 119901 minus119888 minus V1198791199032(1 + 1198791199032) = (12)(119901 minus 119904) we have 119902119900lowast = 120583 and thedegree of overconfidence in the accuracy of the prediction hasno relationship with the order quantity and the loan-to-valueratio

Proof Standardizing (10) we have

119902119900 = 119865119900minus1 (120578) = (1 minus 120573) 120590 sdot Φminus1 (120578) + 120583 (14)

In (14) 120578 represents (119901 minus 119888 minus V1198791199032(1 + 1198791199032))(119901 minus 119904)In the high-profit market environment ie 120578 gt 05 andΦminus1(120578) gt 0 we can know that 119902119900lowast gt 120583 and the greater the

value of 120573 the lower the value of 119902119900 From (11) we can knowthat the greater 120573 value the greater the loan-to-value ratio 120596

In the low profit market environment ie 120578 lt 05Φminus1(120578) lt 0 we can know that 119902119900lowast lt 120583 and the greater thevalue of 120573 the greater the value of 119902119900 From (11) we can knowthat the greater the 120573 value the lower the loan-to-value ratio120596

While 119901minus 119888minus V1198791199032(1 + 1198791199032) = (12)(119901minus 119904) we can knowthat Φminus1(120578) = 0 so we have 119902119900lowast = 120583

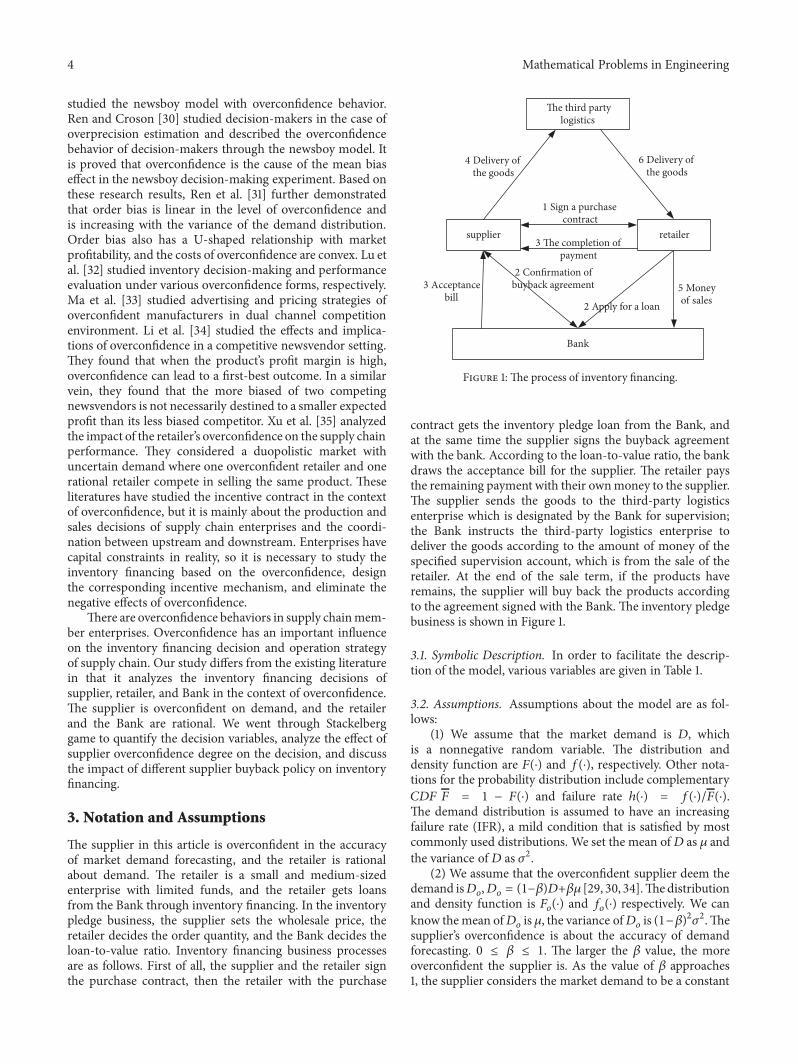

In order to better explain Proposition 4 we providenumerical examples 1199031 is the annual deposit interest rate andthe annual deposit interest rate is 2-3 in China 1199032 is theannual loan interest rate The annual loan interest rate of theBank is usually 6-8 in China plus management fees of theinventory pledged products and other expenses we took 1199032at 10 So we assume that the parameters are as follows 1199031 =003 1199032 = 01 119888 = 5 V = 4 119904 = 2 119879 = 1 and 119863 sim 119873(100 30)We set119901 = 9 as high-profitmarket environment and set119901 = 8as low profit market environment We can know the changetrend about order quantity and loan-to-value ratio visuallyfrom Figures 2 and 3

Mathematical Problems in Engineering 7

01 02 03 04 05 06 07 08 09 10degree of overconfidence

95

96

97

98

99

100

101

102

orde

r qua

ntity

p=8p=9p=873

Figure 2 The relationship between 119902119900 and 120573

067

0675

068

0685

069

0695

07

0705

071

0715

the l

oan-

to-v

alue

ratio

01 02 03 04 05 06 07 08 09 10degree of overconfidence

p=8p=9p=873

Figure 3The relationship between 120596 and 120573

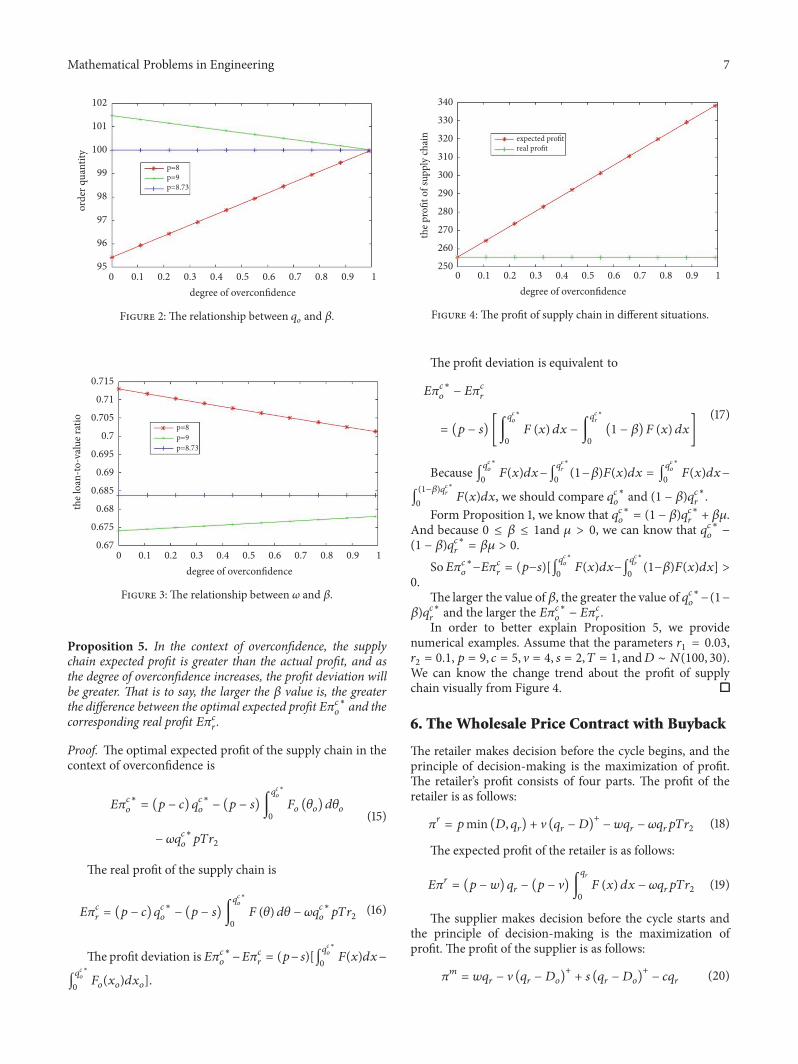

Proposition 5 In the context of overconfidence the supplychain expected profit is greater than the actual profit and asthe degree of overconfidence increases the profit deviation willbe greater That is to say the larger the 120573 value is the greaterthe difference between the optimal expected profit 119864120587119888119900lowast and thecorresponding real profit 119864120587119888119903Proof The optimal expected profit of the supply chain in thecontext of overconfidence is

119864120587119888119900lowast = (119901 minus 119888) 119902119888119900lowast minus (119901 minus 119904) int119902119888119900

lowast

0119865119900 (120579119900) 119889120579119900

minus 120596119902119888119900lowast1199011198791199032(15)

The real profit of the supply chain is

119864120587119888119903 = (119901 minus 119888) 119902119888119900lowast minus (119901 minus 119904) int119902119888119900

lowast

0119865 (120579) 119889120579 minus 120596119902119888119900lowast1199011198791199032 (16)

The profit deviation is 119864120587119888119900lowastminus119864120587119888119903 = (119901minus119904)[int119902119888

119900

lowast

0119865(119909)119889119909minus

int119902119888119900lowast0

119865119900(119909119900)119889119909119900]

expected profitreal profit

01 02 03 04 05 06 07 08 09 10degree of overconfidence

250

260

270

280

290

300

310

320

330

340

the p

rofit

of s

uppl

y ch

ain

Figure 4 The profit of supply chain in different situations

The profit deviation is equivalent to

119864120587119888119900lowast minus 119864120587119888119903= (119901 minus 119904) [int119902

119888

119900

lowast

0119865 (119909) 119889119909 minus int119902

119888

119903

lowast

0(1 minus 120573) 119865 (119909) 119889119909] (17)

Because int119902119888119900lowast0

119865(119909)119889119909minusint119902119888119903lowast0(1minus120573)119865(119909)119889119909 = int119902119888119900lowast

0119865(119909)119889119909minus

int(1minus120573)119902119888119903lowast0

119865(119909)119889119909 we should compare 119902119888119900lowast and (1 minus 120573)119902119888119903lowastForm Proposition 1 we know that 119902119888119900lowast = (1 minus 120573)119902119888119903lowast + 120573120583

And because 0 le 120573 le 1and 120583 gt 0 we can know that 119902119888119900lowast minus(1 minus 120573)119902119888119903lowast = 120573120583 gt 0So119864120587119888119900lowastminus119864120587119888119903 = (119901minus119904)[int119902

119888

119900

lowast

0119865(119909)119889119909minusint119902119888119903lowast

0(1minus120573)119865(119909)119889119909] gt0

The larger the value of 120573 the greater the value of 119902119888119900lowastminus(1minus120573)119902119888119903lowast and the larger the 119864120587119888119900lowast minus 119864120587119888119903 In order to better explain Proposition 5 we provide

numerical examples Assume that the parameters 1199031 = 0031199032 = 01119901 = 9 119888 = 5 V = 4 119904 = 2119879 = 1 and119863 sim 119873(100 30)We can know the change trend about the profit of supplychain visually from Figure 4

6 The Wholesale Price Contract with Buyback

The retailer makes decision before the cycle begins and theprinciple of decision-making is the maximization of profitThe retailerrsquos profit consists of four parts The profit of theretailer is as follows

120587119903 = 119901min (119863 119902119903) + V (119902119903 minus 119863)+ minus 119908119902119903 minus 1205961199021199031199011198791199032 (18)

The expected profit of the retailer is as follows

119864120587119903 = (119901 minus 119908) 119902119903 minus (119901 minus V) int1199021199030119865 (119909) 119889119909 minus 1205961199021199031199011198791199032 (19)

The supplier makes decision before the cycle starts andthe principle of decision-making is the maximization ofprofit The profit of the supplier is as follows

120587119898 = 119908119902119903 minus V (119902119903 minus 119863119900)+ + 119904 (119902119903 minus 119863119900)+ minus 119888119902119903 (20)

8 Mathematical Problems in Engineering

The expected profit of the supplier with overconfidence isas follows

119864120587119898 = (119908 minus 119888) 119902119903 minus (V minus 119904) int119902119903

0119865119900 (119909119900) 119889119909119900 (21)

The supplier as a core enterprise first decides its whole-sale price and then the retailer decides the order quantityand the Bank determines the loan-to-value ratio according tothe purchase contract and buy back agreement of the supplierand the retailer The Bankrsquos loan-to-value ratio is related tothe retailerrsquos order quantity and the retailerrsquos order quantity isrelated to the supplierrsquos wholesale priceTherefore the Bankrsquosloan-to-value ratio is also related to the supplierrsquos wholesaleprice through transmission The whole game process consistsof two parts one part the game between the Bank and theretailer and another part the game between the retailer andthe supplier so it is called bilevel Stackelberg The bilevelStackelberg is used to solve the problem and the retailer isfirst analyzed

61 Retailer Decision Analysis First we analyze the retailerrsquosdecision The first and second derivatives of (19) with respectto 119902119903 are

119889119864120587119903119889119902119903 = (119901 minus 119908) minus (119901 minus V) 119865 (119902119903) minus 1205961199011198791199032

minus 119889120596119889119902119903 1199021199031199011198791199032

(22)

Because 119889120596119889119902119903 = minus(119901 minus V)119865minus1(119866)1199021199032119901(1 + 1198791199032) we cansimplify (22) to

119889119864120587119903119889119902119903 = (119901 minus 119908) minus (119901 minus V) 119865 (119902119903) minus V1198791199032(1 + 1198791199032) (23)

Because 12059721198641205871199031205971199021199032 = minus(119901 minus V)119891(119902119903) lt 0 we let119889119864120587119903119889119902119903 = 0 and then we have

119902119903 = 119865minus1 (119901 minus 119908 minus V1198791199032 (1 + 1198791199032)119901 minus V) (24)

62 Supplier DecisionAnalysis Nowwe analyze the supplierrsquosdecision about wholesale price By taking the first derivativeof (21) with respect to 119908 we have

119889119864120587119898119889119908 = 119902119903 + [(119908 minus 119888) minus (V minus 119904) 119865119900 (119902119903)] 119889119902119903119889119908 (25)

We can take the derivative of 119902119903 with respect to 119908 from(24)

119889119902119903119889119908 = minus 1(119901 minus V) 119891 (119902119903) (26)

Substitute (26) into (25)

119889119864120587119898119889119908 = 119902119903 minus (119908 minus 119888) minus (V minus 119904) 119865119900 (119902119903)(119901 minus V) 119891 (119902119903) (27)

Because 11988921198641205871198981198891199082 = minus(2(119901 minus V)119891(119902119903) + (V minus 119904)119891119900(119902119903))[(119901 minus V)119891(119902119903)]2 minus (((119908 minus 119888) minus (V minus 119904)119865119900(119902119903))(119901 minusV)2[119891(119902119903)]3)1198911015840(119902119903) lt 0 we let 119889119864120587119898119889119908 = 0 and then wehave

119902119903 minus (119908 minus 119888) minus (V minus 119904) 119865119900 (119902119903)(119901 minus V) 119891 (119902119903) = 0 (28)

We can get 119902119903lowast and 119908lowast by solving the simultaneousequations which consist of (24) and (28)

63 Analysis of Each Decision Variable

Proposition 6 In decentralized decision-making the loan-to-value ratio of the Bank is negatively correlated with theretailerrsquos order quantity and the loan-to-value ratio of the Bankis positively correlated with the buyback price and wholesaleprice set by the supplier

Proof We can take the derivative of 120596with respect to 119902119903 from(5)

120597120596120597119902119903 = minus

(119901 minus V) 119865minus1 (119866)1199021199032119901 (1 + 1198791199032) lt 0 (29)

From (29) we can know that the loan-to-value ratio of theBank is negatively correlatedwith the retailerrsquos order quantityThat is to say the loan-to-value ratio of the Bank decreaseswith the increase of the retailerrsquos order quantity

We can take the derivative of 120596with respect to V from (5)

120597120596120597V =

119902119903 minus 119865minus1 (119866)119902119903119901 (1 + 1198791199032) gt 0 (30)

From (30) we can know that the loan-to-value ratio of theBank is positively correlated with the supplierrsquos the buybackprice That is to say the loan-to-value ratio of the Bankincreases with the increase of the supplierrsquos buyback price

Through (26) and (29) it is known that

120597120596120597119908 = 120597120596

120597119902119900 sdot120597119902119900120597119908

= minus(119901 minus V) 119865minus1 (119866)1199021199002119901 (1 + 1198791199032) sdot [minus

1(119901 minus V) 119891 (119902119903)]

= 119865minus1 (119866)1199021199002119901 (1 + 1198791199032) 119891 (119902119903) gt 0

(31)

From (31) we can know that the loan-to-value ratioof the Bank is positively correlated with the supplierrsquos thewholesale price That is to say the loan-to-value ratio of theBank increases with the increase of the supplierrsquos wholesaleprice

In order to find the relationship between order quantityand decision-making modes we provided numerical exam-ples Assume that the parameters 1199031 = 003 1199032 = 01 119888 = 5V = 4 119904 = 2 119879 = 1 and 119863 sim 119873(100 30)

Mathematical Problems in Engineering 9

joint decision-making(p=8)decentralized decision-making(p=8)joint decision-making(p=9)decentralized decision-making(p=9)

01 02 03 04 05 06 07 08 09 10degree of overconfidence

65

70

75

80

85

90

95

100

105

orde

r qua

ntity

Figure 5 The relationship between order quantity and decision-making modes

p=8p=9

01 02 03 04 05 06 07 08 09 10degree of overconfidence

7717273747576777879

8

who

lesa

le p

rice

Figure 6 The relationship between wholesale price and overconfi-dence

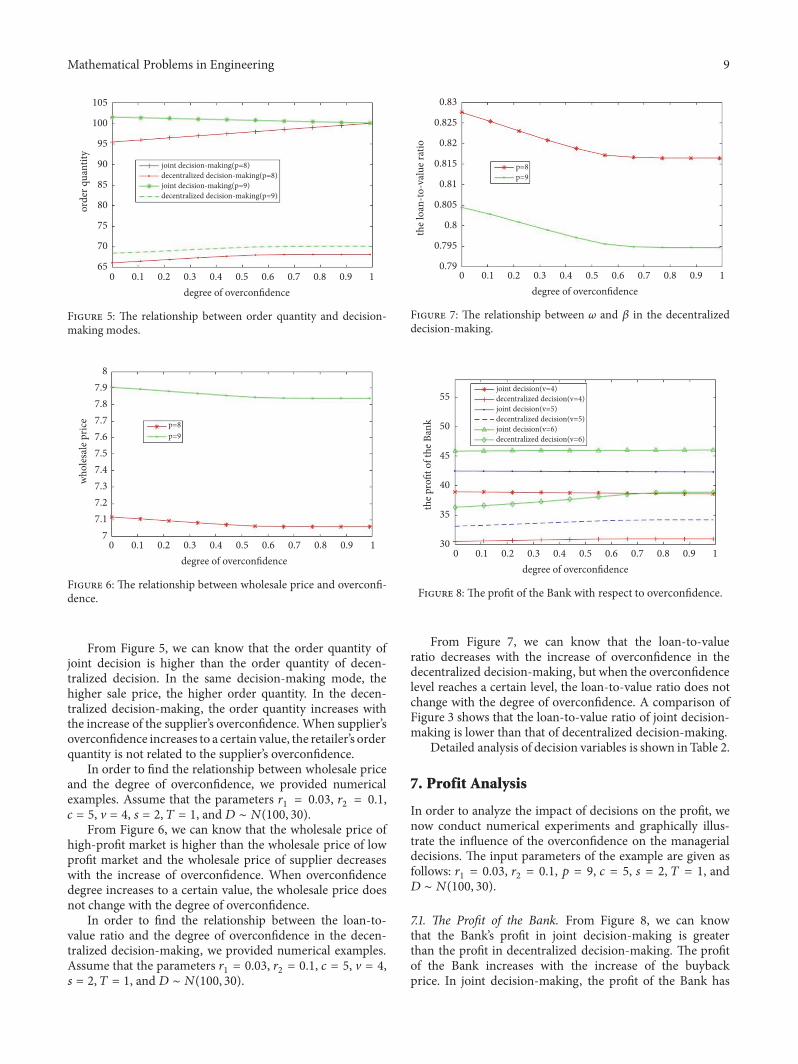

From Figure 5 we can know that the order quantity ofjoint decision is higher than the order quantity of decen-tralized decision In the same decision-making mode thehigher sale price the higher order quantity In the decen-tralized decision-making the order quantity increases withthe increase of the supplierrsquos overconfidence When supplierrsquosoverconfidence increases to a certain value the retailerrsquos orderquantity is not related to the supplierrsquos overconfidence

In order to find the relationship between wholesale priceand the degree of overconfidence we provided numericalexamples Assume that the parameters 1199031 = 003 1199032 = 01119888 = 5 V = 4 119904 = 2 119879 = 1 and 119863 sim 119873(100 30)

From Figure 6 we can know that the wholesale price ofhigh-profit market is higher than the wholesale price of lowprofit market and the wholesale price of supplier decreaseswith the increase of overconfidence When overconfidencedegree increases to a certain value the wholesale price doesnot change with the degree of overconfidence

In order to find the relationship between the loan-to-value ratio and the degree of overconfidence in the decen-tralized decision-making we provided numerical examplesAssume that the parameters 1199031 = 003 1199032 = 01 119888 = 5 V = 4119904 = 2 119879 = 1 and 119863 sim 119873(100 30)

p=8p=9

01 02 03 04 05 06 07 08 09 10degree of overconfidence

079

0795

08

0805

081

0815

082

0825

083

the l

oan-

to-v

alue

ratio

Figure 7 The relationship between 120596 and 120573 in the decentralizeddecision-making

joint decision(v=4)decentralized decision(v=4)joint decision(v=5)decentralized decision(v=5)joint decision(v=6)decentralized decision(v=6)

01 02 03 04 05 06 07 08 09 10degree of overconfidence

30

35

40

45

50

55

the p

rofit

of t

he B

ank

Figure 8 The profit of the Bank with respect to overconfidence

From Figure 7 we can know that the loan-to-valueratio decreases with the increase of overconfidence in thedecentralized decision-making but when the overconfidencelevel reaches a certain level the loan-to-value ratio does notchange with the degree of overconfidence A comparison ofFigure 3 shows that the loan-to-value ratio of joint decision-making is lower than that of decentralized decision-making

Detailed analysis of decision variables is shown inTable 2

7 Profit Analysis

In order to analyze the impact of decisions on the profit wenow conduct numerical experiments and graphically illus-trate the influence of the overconfidence on the managerialdecisions The input parameters of the example are given asfollows 1199031 = 003 1199032 = 01 119901 = 9 119888 = 5 119904 = 2 119879 = 1 and119863 sim 119873(100 30)71 The Profit of the Bank From Figure 8 we can knowthat the Bankrsquos profit in joint decision-making is greaterthan the profit in decentralized decision-making The profitof the Bank increases with the increase of the buybackprice In joint decision-making the profit of the Bank has

10 Mathematical Problems in Engineering

Table 2 Analysis of the each decision variable

joint decision-making comparison decentralized decision-makingloan-to-value ratio

low profit market 120573 uarr 120596 darr lt 120573 uarr 120596 darr 120573 uarruarr 120596 997888rarrhigh profit market 120573 uarr 120596 uarr lt 120573 uarr 120596 darr 120573 uarruarr 120596 997888rarr

order quantitylow profit market 119902 lt 120583 120573 uarr 119902 uarr gt 120573 uarr 119902 uarr 120573 uarruarr 119902 997888rarrhigh profit market 119902 gt 120583 120573 uarr 119902 darr gt 120573 uarr 119902 uarr 120573 uarruarr 119902 997888rarr

wholesale pricelow profit market 120573 uarr119908 darr 120573 uarruarr119908 997888rarrhigh profit market 120573 uarr119908 darr 120573 uarruarr119908 997888rarr

v=4v=5v=6

01 02 03 04 05 06 07 08 09 10degree of overconfidence

10

15

20

25

30

35

40

the p

rofit

of t

he re

taile

r

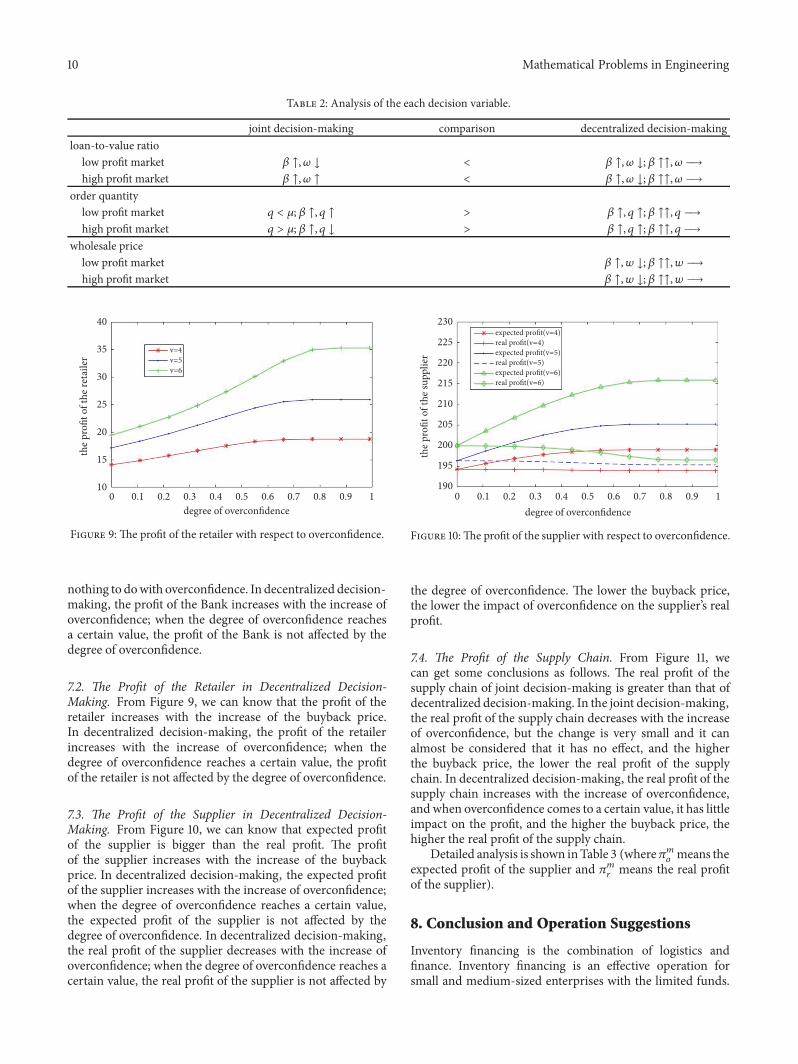

Figure 9 The profit of the retailer with respect to overconfidence

nothing to dowith overconfidence In decentralized decision-making the profit of the Bank increases with the increase ofoverconfidence when the degree of overconfidence reachesa certain value the profit of the Bank is not affected by thedegree of overconfidence

72 The Profit of the Retailer in Decentralized Decision-Making From Figure 9 we can know that the profit of theretailer increases with the increase of the buyback priceIn decentralized decision-making the profit of the retailerincreases with the increase of overconfidence when thedegree of overconfidence reaches a certain value the profitof the retailer is not affected by the degree of overconfidence

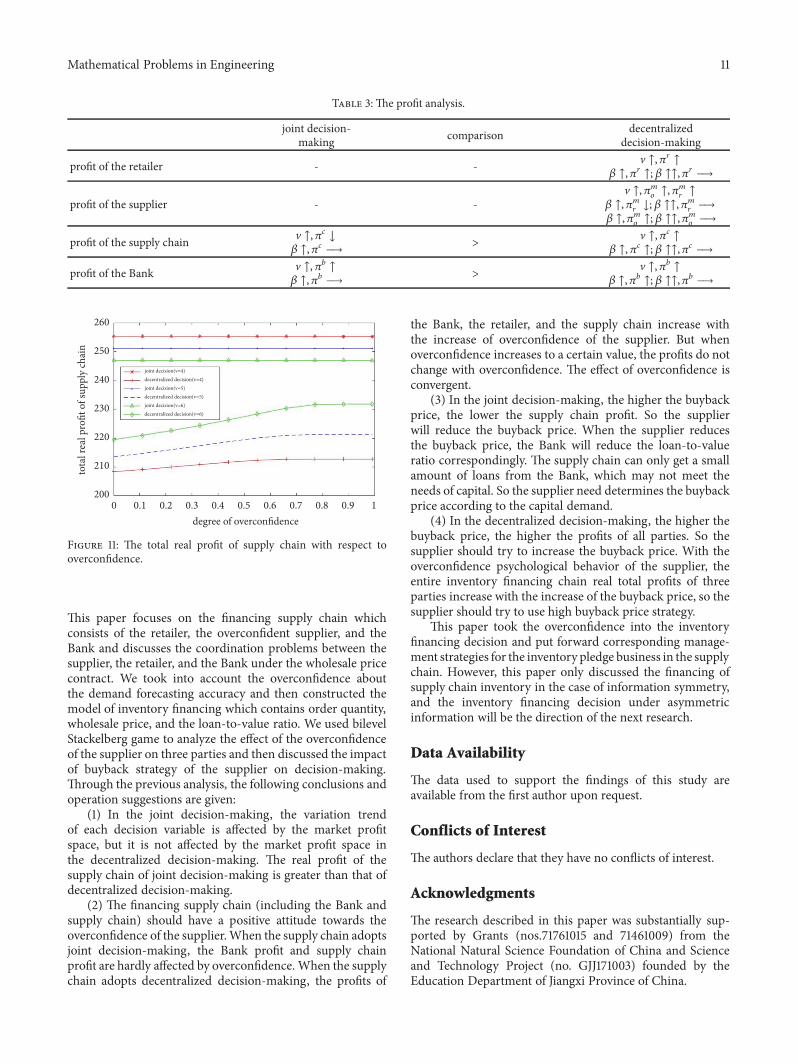

73 The Profit of the Supplier in Decentralized Decision-Making From Figure 10 we can know that expected profitof the supplier is bigger than the real profit The profitof the supplier increases with the increase of the buybackprice In decentralized decision-making the expected profitof the supplier increases with the increase of overconfidencewhen the degree of overconfidence reaches a certain valuethe expected profit of the supplier is not affected by thedegree of overconfidence In decentralized decision-makingthe real profit of the supplier decreases with the increase ofoverconfidence when the degree of overconfidence reaches acertain value the real profit of the supplier is not affected by

expected profit(v=4)real profit(v=4)expected profit(v=5)real profit(v=5)expected profit(v=6)real profit(v=6)

01 02 03 04 05 06 07 08 09 10degree of overconfidence

190

195

200

205

210

215

220

225

230

the p

rofit

of t

he su

pplie

r

Figure 10The profit of the supplier with respect to overconfidence

the degree of overconfidence The lower the buyback pricethe lower the impact of overconfidence on the supplierrsquos realprofit

74 The Profit of the Supply Chain From Figure 11 wecan get some conclusions as follows The real profit of thesupply chain of joint decision-making is greater than that ofdecentralized decision-making In the joint decision-makingthe real profit of the supply chain decreases with the increaseof overconfidence but the change is very small and it canalmost be considered that it has no effect and the higherthe buyback price the lower the real profit of the supplychain In decentralized decision-making the real profit of thesupply chain increases with the increase of overconfidenceand when overconfidence comes to a certain value it has littleimpact on the profit and the higher the buyback price thehigher the real profit of the supply chain

Detailed analysis is shown inTable 3 (where120587119898119900 means theexpected profit of the supplier and 120587119898119903 means the real profitof the supplier)

8 Conclusion and Operation Suggestions

Inventory financing is the combination of logistics andfinance Inventory financing is an effective operation forsmall and medium-sized enterprises with the limited funds

Mathematical Problems in Engineering 11

Table 3 The profit analysis

joint decision-making comparison decentralized

decision-making

profit of the retailer - - V uarr 120587119903 uarr120573 uarr 120587119903 uarr 120573 uarruarr 120587119903 997888rarrprofit of the supplier - -

V uarr 120587119898119900 uarr 120587119898119903 uarr120573 uarr 120587119898119903 darr 120573 uarruarr 120587119898119903 997888rarr120573 uarr 120587119898119900 uarr 120573 uarruarr 120587119898119900 997888rarrprofit of the supply chain V uarr 120587119888 darr120573 uarr 120587119888 997888rarr gt V uarr 120587119888 uarr120573 uarr 120587119888 uarr 120573 uarruarr 120587119888 997888rarrprofit of the Bank V uarr 120587119887 uarr120573 uarr 120587119887 997888rarr gt V uarr 120587119887 uarr120573 uarr 120587119887 uarr 120573 uarruarr 120587119887 997888rarr

joint decision(v=4)decentralized decision(v=4)joint decision(v=5)decentralized decision(v=5)joint decision(v=6)decentralized decision(v=6)

01 02 03 04 05 06 07 08 09 10degree of overconfidence

200

210

220

230

240

250

260

tota

l rea

l pro

fit o

f sup

ply

chai

n

Figure 11 The total real profit of supply chain with respect tooverconfidence

This paper focuses on the financing supply chain whichconsists of the retailer the overconfident supplier and theBank and discusses the coordination problems between thesupplier the retailer and the Bank under the wholesale pricecontract We took into account the overconfidence aboutthe demand forecasting accuracy and then constructed themodel of inventory financing which contains order quantitywholesale price and the loan-to-value ratio We used bilevelStackelberg game to analyze the effect of the overconfidenceof the supplier on three parties and then discussed the impactof buyback strategy of the supplier on decision-makingThrough the previous analysis the following conclusions andoperation suggestions are given

(1) In the joint decision-making the variation trendof each decision variable is affected by the market profitspace but it is not affected by the market profit space inthe decentralized decision-making The real profit of thesupply chain of joint decision-making is greater than that ofdecentralized decision-making

(2) The financing supply chain (including the Bank andsupply chain) should have a positive attitude towards theoverconfidence of the supplierWhen the supply chain adoptsjoint decision-making the Bank profit and supply chainprofit are hardly affected by overconfidence When the supplychain adopts decentralized decision-making the profits of

the Bank the retailer and the supply chain increase withthe increase of overconfidence of the supplier But whenoverconfidence increases to a certain value the profits do notchange with overconfidence The effect of overconfidence isconvergent

(3) In the joint decision-making the higher the buybackprice the lower the supply chain profit So the supplierwill reduce the buyback price When the supplier reducesthe buyback price the Bank will reduce the loan-to-valueratio correspondingly The supply chain can only get a smallamount of loans from the Bank which may not meet theneeds of capital So the supplier need determines the buybackprice according to the capital demand

(4) In the decentralized decision-making the higher thebuyback price the higher the profits of all parties So thesupplier should try to increase the buyback price With theoverconfidence psychological behavior of the supplier theentire inventory financing chain real total profits of threeparties increase with the increase of the buyback price so thesupplier should try to use high buyback price strategy

This paper took the overconfidence into the inventoryfinancing decision and put forward corresponding manage-ment strategies for the inventory pledge business in the supplychain However this paper only discussed the financing ofsupply chain inventory in the case of information symmetryand the inventory financing decision under asymmetricinformation will be the direction of the next research

Data Availability

The data used to support the findings of this study areavailable from the first author upon request

Conflicts of Interest

The authors declare that they have no conflicts of interest

Acknowledgments

The research described in this paper was substantially sup-ported by Grants (nos71761015 and 71461009) from theNational Natural Science Foundation of China and Scienceand Technology Project (no GJJ171003) founded by theEducation Department of Jiangxi Province of China

12 Mathematical Problems in Engineering

References

[1] B Fischhoff P Slovic and S Lichtenstein ldquoKnowing with cer-tainty The appropriateness of extreme confidencerdquo Journal ofExperimental Psychology Human Perception and Performancevol 3 no 4 pp 552ndash564 1977

[2] N DWeinstein ldquoUnrealistic optimism about future life eventsrdquoJournal of Personality and Social Psychology vol 39 no 5 pp806ndash820 1980

[3] D A Moore and P J Healy ldquoThe trouble with overconfidencerdquoPsychological Review vol 115 no 2 pp 502ndash517 2008

[4] R W Burman ldquoPractical aspects of inventory and receivablesfinancingrdquo Law amp Contemporary Problems vol 13 no 4 pp555ndash565 1948

[5] J Guttentag ldquoMortgage warehousingrdquo The Journal of Financevol 12 no 4 pp 438ndash450 1957

[6] R A Miller ldquoMas consultantrsquos role asset-based financingrdquo TheCPA Journal vol 52 no 4 pp 24ndash29 1982

[7] R Lacroix and P Varangis ldquoUsing warehouse receipts indeveloping and transition economiesrdquo Finance amp Developmentvol 33 no 3 pp 36ndash39 1996

[8] S Rutberg ldquoFinancing the supply chain by piggy-backing onthe massive distribution clout of united parcel servicerdquo SecuredLender vol 58 no 6 pp 40ndash46 2002

[9] E Hofmann ldquoInventory financing in supply chains a logisticsservice provider-approachrdquo International Journal of PhysicalDistribution and Logistics Management vol 39 no 9 pp 716ndash740 2009

[10] E Jokivuolle and S Peura ldquoIncorporating collateral valueuncertainty in loss given default estimates and loan-to-valueratiosrdquo European Financial Management vol 9 no 3 pp 299ndash314 2003

[11] D Cossin and T Hricko ldquoA structural analysis of credit riskwith risky collateral a methodology for haircut determinationrdquoEconomic Notes vol 32 no 2 pp 243ndash282 2003

[12] J He X-L Jiang JWang D-L Zhu and L Zhen ldquoVaRmethodsfor the dynamic impawn rate of steel in inventory financingunder autocorrelative returnrdquo European Journal of OperationalResearch vol 223 no 1 pp 106ndash115 2012

[13] Y Li ldquoNumerical analysis of loan-to-value ratio of inventoryfinancing based on logistics financial innovationrdquo InformationTechnology Journal vol 12 no 15 pp 3353ndash3356 2013

[14] J He J Wang X-L Jiang X-F Chen and L Chen ldquoThelong-term extreme price risk measure of portfolio in inventoryfinancing an application to dynamic impawn rate intervalrdquoComplexity vol 20 no 5 pp 17ndash34 2015

[15] H Zhang W Meng X Wang and J Zhang ldquoApplication ofBSDE in standard inventory financing loanrdquoDiscrete Dynamicsin Nature and Society vol 2017 Article ID 1031247 6 pages 2017

[16] J A Buzacott and R Q Zhang ldquoInventory management withasset-based financingrdquo Management Science vol 50 no 9 pp1274ndash1292 2004

[17] Y Wang J Zhou H Sun and L Jiang ldquoRobust inventoryfinancing model with partial informationrdquo Journal of AppliedMathematics vol 2014 Article ID 236083 9 pages 2014

[18] X Li P Zhang K Zhang and Y Li ldquoResearch on supply chainfinancing risk assessment of Chinarsquos commercial banksrdquo ICICExpress Letters vol 10 no 7 pp 1567ndash1574 2016

[19] Y Zhu C Xie G-J Wang and X-G Yan ldquoComparison ofindividual ensemble and integrated ensemble machine learn-

ing methods to predict Chinarsquos SME credit risk in supply chainfinancerdquoNeural Computing and Applications vol 28 pp 41ndash502017

[20] L A Diercks ldquoIdentifying and managing troubled borrowersin asset-based lending scenariosrdquo Commercial Lending Reviewvol 19 no 3 pp 38ndash41 2004

[21] X-H Sun X-J Chu and Z-D Wu ldquoIncentive regulation ofbanks on third party logistics enterprises in principal-agent-based inventory financingrdquo Advances in Manufacturing vol 2no 2 pp 150ndash157 2014

[22] Z Song H Huang W Ran and S Liu ldquoA study on the pricingmodel for 3PL of inventory financingrdquo Discrete Dynamics inNature and Society vol 2016 Article ID 6489748 7 pages 2016

[23] C H Lee and B-D Rhee ldquoCoordination contracts in thepresence of positive inventory financing costsrdquo InternationalJournal of Production Economics vol 124 no 2 pp 331ndash3392010

[24] N-N Yan and B-W Sun ldquoSystem dynamics modeling andsimulation for Capital-constrained Supply Chain based oninventory financingrdquo Information Technology Journal vol 12no 24 pp 8384ndash8390 2013

[25] N Yan H Dai and B Sun ldquoOptimal bi-level Stackelberg strate-gies for supply chain financing with both capital-constrainedbuyers and sellersrdquo Applied Stochastic Models in Business andIndustry vol 30 no 6 pp 783ndash796 2014

[26] N Yan B Sun H Zhang and C Liu ldquoA partial credit guar-antee contract in a capital-constrained supply chain financingequilibrium and coordinating strategyrdquo International Journal ofProduction Economics vol 173 pp 122ndash133 2016

[27] Q Lin X Su and Y Peng ldquoSupply chain coordination inconfirmingwarehouse financingrdquoComputers amp Industrial Engi-neering vol 118 pp 104ndash111 2018

[28] L M Gelsomino R de Boer M Steeman and A PeregoldquoAn optimisation strategy for concurrent Supply Chain Financeschemesrdquo Journal of Purchasing and Supply Management 2018

[29] C D Croson R Croson and Y Ren How to Manage anOverconfident Newsvendor Dallas Cox School of BusinessSouthern Methodist University 2008

[30] Y Ren and R Croson ldquoOverconfidence in newsvendor ordersan experimental studyrdquoManagement Science vol 59 no 11 pp2502ndash2517 2013

[31] Y Ren D C Croson and R T A Croson ldquoThe overconfidentnewsvendorrdquo Journal of the Operational Research Society vol68 no 5 pp 496ndash506 2017

[32] X Lu J Shang S-y Wu G G Hegde L Vargas and D ZhaoldquoImpacts of supplier hubris on inventory decisions and greenmanufacturing endeavorsrdquo European Journal of OperationalResearch vol 245 no 1 pp 121ndash132 2015

[33] JMaQ Li andB Bao ldquoStudy on complex advertising andpricecompetition dual-channel supply chain models consideringthe overconfidence manufacturerrdquo Mathematical Problems inEngineering vol 2016 Article ID 2027146 18 pages 2016

[34] M Li N C Petruzzi and J Zhang ldquoOverconfident competingnewsvendorsrdquo Management Science vol 63 no 8 pp 2637ndash2646 2017

[35] L Xu X Shi P Du K Govindan and Z Zhang ldquoOptimizationon pricing and overconfidence problem in a duopolistic supplychainrdquo Computers amp Operations Research 2018

Hindawiwwwhindawicom Volume 2018

MathematicsJournal of

Hindawiwwwhindawicom Volume 2018

Mathematical Problems in Engineering

Applied MathematicsJournal of

Hindawiwwwhindawicom Volume 2018

Probability and StatisticsHindawiwwwhindawicom Volume 2018

Journal of

Hindawiwwwhindawicom Volume 2018

Mathematical PhysicsAdvances in

Complex AnalysisJournal of

Hindawiwwwhindawicom Volume 2018

OptimizationJournal of

Hindawiwwwhindawicom Volume 2018

Hindawiwwwhindawicom Volume 2018

Engineering Mathematics

International Journal of

Hindawiwwwhindawicom Volume 2018

Operations ResearchAdvances in

Journal of

Hindawiwwwhindawicom Volume 2018

Function SpacesAbstract and Applied AnalysisHindawiwwwhindawicom Volume 2018

International Journal of Mathematics and Mathematical Sciences

Hindawiwwwhindawicom Volume 2018

Hindawi Publishing Corporation httpwwwhindawicom Volume 2013Hindawiwwwhindawicom

The Scientific World Journal

Volume 2018

Hindawiwwwhindawicom Volume 2018Volume 2018

Numerical AnalysisNumerical AnalysisNumerical AnalysisNumerical AnalysisNumerical AnalysisNumerical AnalysisNumerical AnalysisNumerical AnalysisNumerical AnalysisNumerical AnalysisNumerical AnalysisNumerical AnalysisAdvances inAdvances in Discrete Dynamics in

Nature and SocietyHindawiwwwhindawicom Volume 2018

Hindawiwwwhindawicom

Dierential EquationsInternational Journal of

Volume 2018

Hindawiwwwhindawicom Volume 2018

Decision SciencesAdvances in

Hindawiwwwhindawicom Volume 2018

AnalysisInternational Journal of

Hindawiwwwhindawicom Volume 2018

Stochastic AnalysisInternational Journal of

Submit your manuscripts atwwwhindawicom

2 Mathematical Problems in Engineering

the competitiveness of the core enterprises and related enter-prises

The flow capital of a single enterprise is mainly occupiedin the form of accounts receivable and inventory Accordingto the difference of guarantee measures the financial institu-tions divide the basic products of supply chain financing intotwo categories accounts receivable financing and inventoryfinancing

Accounts receivable financing means a financing modethat SMEs use undue receivables committed by the coreenterprises in the supply chain to obtain the fund fromthe financial institutions Carrefour is a global top 500enterprise with a steady operation a clear term of paymentfor upstream suppliers and the ability to execute the contractCarrefour has tens of thousands of suppliers worldwideThe Bank can design a supply chain financing mode forCarrefourrsquos upstream suppliers In the past several yearsthe Banks has been giving the supplier a credit limit afterthe comprehensive assessment which can be recycled afterpayment andCarrefour needs to pay the Bank which formeda closed capital chain cycleThe supply chain financing modecan alleviate the pressure of suppliersrsquo funds and promote theBanks to get more customers

Inmany cases there is no corresponding accounts receiv-able and credit guarantee for the enterprises in the supplychain besides the goods At this time financial institutionscan give the credit to the enterprises with inventory financingmode Inventory financing is a financing business of SMEswhich uses raw materials semifinished products and fin-ished products as collateral to obtain loans from financialinstitutions The traditional Bank loans are concentrated onthe fixed assetsmortgage or the third-party corporation guar-antee Inventory financing is that the SMEs use inventory inthe trade between enterprises and upstream and downstreamenterprises as collateral and then the SMEs obtain loansfrom financial institutions such as Banks In the inventoryfinancing the financial institutions are to give credit to theenterprise after the evaluation of inventory values by thethird-party logistics enterprises For SMEs with financingneeds the lack of fixed assets makes it difficult to obtain loansfrom the Banks In the developed countries the inventoryfinancing business has been mature In developed countriessuch as the United States 70 of the guarantee comes fromaccounts receivable and inventory In China although theinventory financing just started its development speed wasastonishing Since the first inventory financing carried out byChina Materials Storage and Transportation Group Co Ltd(CMST) with the financial institutions in 1999 the CMSThave set up inventory financing with dozens of Banks suchas Bank of China and China Construction Bank

In the actual business process decision-makers areoverconfident Overconfidence is a universal psychologicalbehavior People often think that they are superior to othersin the analysis and judgment Fischhoff et al [1] througha study of 528 paid volunteers show that people are alwaysoverconfident They tend to have enough confidence in thejudgment and overestimate the chances of success Weinstein[2] tested 120 female college students and found that peoplealways overestimated their own favorable factors and they

did not think that others had the same factors at the sametime a survey of more than 200 college students foundthat people were always optimistic about the chances ofsuccess Moore [3] through the literature review on theoverconfidence found that overconfidence was always man-ifested in three categories overestimation overplacementand overprecision

At present most of the researches on inventory financingdecisions are based on the assumption that decision-makersare rational Decisions made by the overconfident decision-maker often deviate from traditional decisions This papermainly analyzed enterprise decision-making under inventoryfinancing environment This paper quantified the decisionvariables of all parties through the bilevel Stackelberg gameanalyzed the influence of the degree of overconfidence onthe decision-making of all parties and then discussed theinfluence of the different supplierrsquos buyback strategies on theinventory financing and sought a strategy that can benefit thethree parties in the inventory financing

The remainder of this paper is organized as follows Therelated research is reviewed in Section 2 The notation andassumptions are given in Section 3 The model of Bankprofit is given in Section 4 We studied the joint decision ofsupply chain in Section 5 We studied the wholesale pricecontract with buyback in Section 6 We carefully comparedthe profits under the different decision modes in Section 7We concluded the conclusion and operation suggestions inSection 8

2 Literature Review

Our work is related to two streams of literature one dealwith inventory financing and the other dealing with overcon-fidence

On the aspect of inventory financing business operationBurman [4] put forward two modes of inventory and receiv-ables financing from the perspective of practice Guttentag [5]introduced the businessmodes controlmethods advantagesand disadvantages of inventory financing in 1950s and 1960sMiller [6] analyzed the new characteristics of the commercialmode of inventory financing during the 1970s-1980s Lacroixand Varangis [7] compared the inventory financing of theUnited States and the developing countries and introducedthe related business modes and the measures to promote thedevelopment of financing Rutberg [8] analyzed the maincharacteristics of the inventory financing mode from theaspects of business characteristics and operation mode withUPS as an example Hofmann [9] provided a conceptualexplanation of the relevance and the implications of alterna-tive inventory financing by a logistics service provider Theearly research mainly focused on the discussion of inventoryfinancing business and analyzed the process characteristicsand operation mode of inventory financing

The inventory financing business is a new financialservice mode The Bank had developed the inventory financ-ing business actively It is necessary to set the loan cyclethe mark-to-market frequency the warning value and theinterest rate so as to control the risk effectively Jokivuolle

Mathematical Problems in Engineering 3

andPeura [10] studied the loan-to-value ratio of the inventoryfinancing when the price fluctuated with the Merton struc-tural method Cossin and Hricko [11] considered the creditrisk in the pledge management constructed the credit riskpricing model which is different from the newsboy modeldetermined the discount rate of the inventory financingbusiness and obtained the loan-to-value ratio by 1 minusthe discount rate He et al [12] established a model withthe formula AR (1)-GARCH (11)-GED using the databaseof spot steel forecasted the VaR of steel during the differentrisk windows in the impawn period through a methodof out-of-sample and got the impawn rate according withthe risk exposure of Banks Li [13] adopted risk evaluationmethod of ldquocorporate and debtrdquo considered the impact oftime to capture and liquidity risk established loan-to-valueratio decision model of inventory financing with randomly-fluctuate price then took copper for an example confirmedall model parameters and analyzed the impact of differentfactors on loan-to-value ratio He et al [14] proposed a newlong-term extreme price risk (value at risk and conditionalvalue at risk) measure method for inventory portfolio andan application to dynamic impawn rate interval Zhang etal [15] assumed that the short-term prices of the collateralfollow a geometric Brownian motion and use a set ofequivalent martingale measures to build the models abouta Bankrsquos maximum and minimum levels of risk tolerance inan environment with Knightian uncertainty However theseresearches only considered the loan decision of the Bankalone and did not consider the game between Bank and thecapital-shortage enterprise which will influence the decisionof the Bank

As the loan enterprise of inventory financing its financ-ing decision will directly affect the operation performanceof the enterprise On the operation decision based on theinventory financing Buzacott and Zhang [16] studied assetsfinancing from the perspective of the enterprise first com-bined the loan risk management of financial institutions withthe inventory control of the loan enterprises and analyzedthe choice of the loan interest rate and the loan value ratioand their impact on the profits of the financial institutionsand the loan enterprises The problem of discussion is thatthe enterprise purchased the products by the loan and all theinventory is used as a pledge which belongs to a stage ofdecision-making process Wang et al [17] studied the robustinventory financing model under partial information thatis where the demand distribution is partly known In thissetting the robust method that maximizes the worst-caseprofit and minimizes the firmrsquos maximum possible regretof not acting optimally would be used to formulate theoptimal sales quantity SMEs credit risk is significant forguaranteeing supply chain financing in smooth operationLi et al [18] adopt the logistic regression tool to measurethe default probability of the risk model and made anempirical analysis of themodel based on 177 sample data fromChinarsquos commercial Banks concerning automobile and steelindustries Zhu et al [19] applied six methods to predict theSMEs credit risk

Inventory financing business cannot be carried out with-out the participation of third-party logistics Diercks [20]

illustrated the necessity of the third-party logistics enter-prises to participate in the inventory financing business Ininventory financing asymmetric information between theBanks and the third-party logistics enterprises may incurmoral risks and often causes economic losses of the Banks Toeffectively solve this problem Sun et al [21] designed a pureincentive scheme and a regulatory incentive scheme with theprincipal-agent theory Song et al [22] proposed a pricingmodel of inventory financing that canmaximize the cash flowof the 3PL enterprise when the default rate of the SMEs isaffected by the pledge priceThese researches do not considerthe impact of supply chain contract on financing

The decision of inventory financing enterprises is notisolated They are influenced by the business related par-ties The pricing strategy of the supplier and the lendingpolicy of the Bank will all affect the financing decisionof the enterprise On the supply chain management basedon the inventory financing Lee and Rhee [23] discussedcoordination mechanisms by explicitly assuming capital-constrained agents and positive inventory financing costsYan and Sun [24] designed a capital-constrained supply chainsystemwith amanufacturer and a capital-constrained retailerwho can obtain short-term financing from the commercialBank through inventory financing according to the value ofthe pledged warehouse receipt Using the system dynamicsmethodology they modelled the stock and flow diagramsand simulated the system characteristics for nonfinancingscheme and inventory financing scheme respectively Yan etal [25] designed a supply chain financing system with aman-ufacturer a retailer and a commercial Bank where both theretailer and the manufacturer are capital constrained underdemand uncertainties They formulated a bilevel Stackelberggame for the supply chain financing system in which theBank acts as the leader and themanufacturer as the subleaderConsidering the bankruptcy risks of the manufacturer andthe retailer they analyzed the optimal financing interestrate for the commercial Bank the optimal order for theretailer and the optimalwholesale price for themanufacturerrespectively On the basis Yan et al [26] performed a com-parative analysis of the optimal strategies among the variousfinancing scenarios Lin et al [27] found that the vendershould provide the complete buyback when the demandis uncertain and affected by retailersrsquo sales efforts so theyput forward three modified modes of inventory financingto achieve Pareto-Improvement Based on the analyticalformulation of the benefits of three relevant supply chainfinance schemes (Reverse Factoring Inventory Financingand Dynamic Discounting) Gelsomino et al [28] formalizedamodel that investigated the benefits that a buyer can achieveby onboarding suppliers onto these three schemes

The traditional operations researches are usually basedon the rational hypothesis and ignore the influence of psy-chological factors on the decision-making behavior whichleads to the deviation of the research results and the actualsituation In order to accurately reflect managersrsquo decision-making behavior many scholars have introduced humanbehavior factors into supply chain management In the fieldof operation and management Croson et al [29] introducedoverconfidence behavior into the supply chain model and

4 Mathematical Problems in Engineering