Embed Size (px)

Citation preview

Investing Basics

October 6, 2008

Why do we invest?

Capital Preservation

Building Wealth, Retirement

Take Advantage of Time and Compounding

Savings Rate

Compound Interest

Investor A: Starts contributing $2,000 annually to an IRA at the age of 26.

Investor B: Contributes $2,000 per year to an IRA beginning at age 19 and ending at age 25.

Earn 10% per year.

Who ends up with more more at age 65?

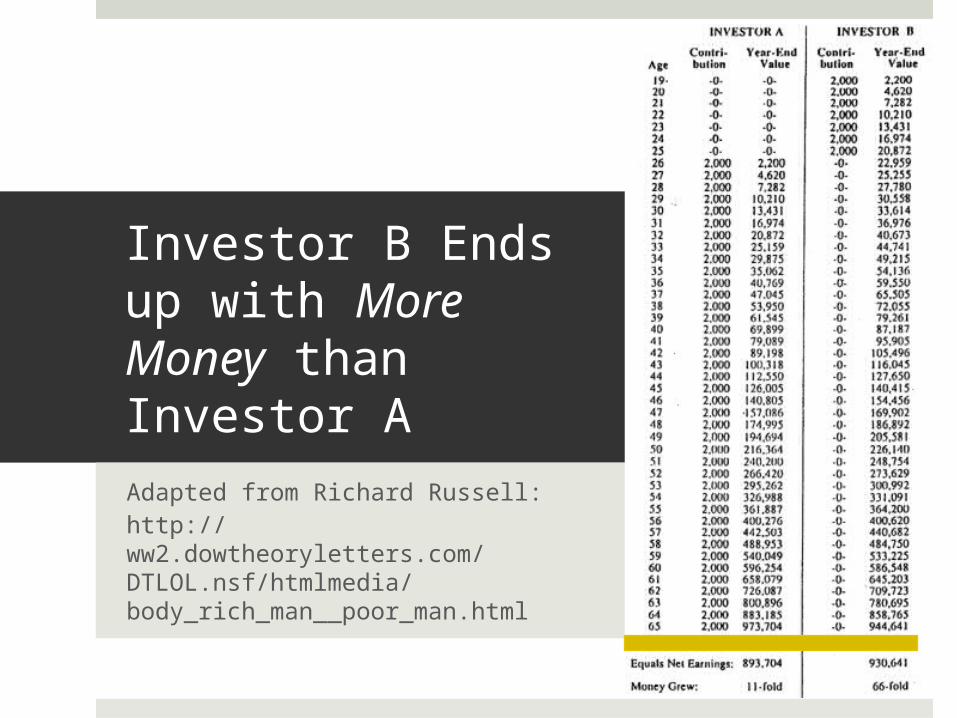

Investor B Ends up with More Money than Investor A

Adapted from Richard Russell:http://ww2.dowtheoryletters.com/DTLOL.nsf/htmlmedia/body_rich_man__poor_man.html

Morals of the Story

Start saving and investing as early as possible.

At a young age, savings rate is probably the most important factor in building wealth (although investing responsibly helps too).

(The moral isn’t necessarily to stop investing after age 25. Consider that a hypothetical investor C who started investing $2,000 annually at age 19 would have ended with nearly $2 million.)

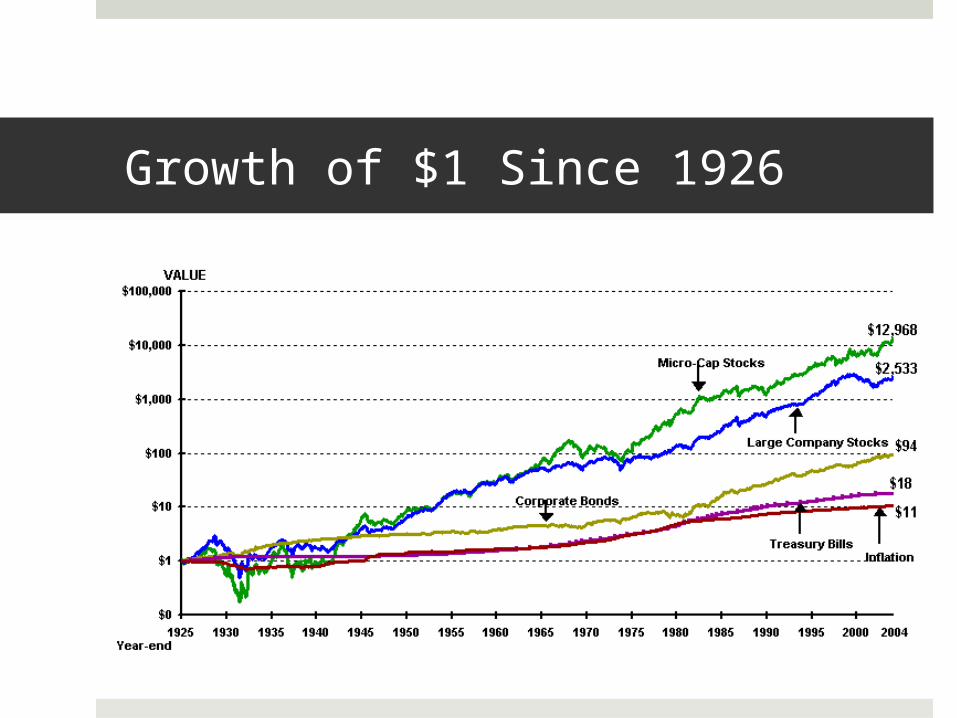

Growth of $1 Since 1926

Active vs. Passive Management

Definitions

Advantages and Disadvantages

Investing in Funds

What do these terms mean?

Active Management The use of an active means such as stock selection or

market timing in an attempt to outperform the market.

Passive Management Matches the return of a given market index by owning all

(or substantially all) the securities in the underlying index.

Active Management

Incentive Problems: Fee structure. Risk.

Higher fees in general.

Higher turnover and lower tax efficiency.

Most actively managed funds underperform passive indexes over time. It’s also hard to pick funds that will be long term winners.

Advantages of Index Funds

Guaranteed market rate of return.

Diversified.Eliminates idiosyncratic risk.

Low expenses.

Usually tax efficient.

Easy to build a portfolio based on your risk tolerance.

Exchange Traded Funds (ETFs)

Advantages of Index-Tracking ETFs: Low ERs. No minimums. Traded on an exchange like stocks. Pay same commission as a regular trade.

Examples of Index-Tracking ETFs: VTI – Vanguard Total Stock Market (0.07%) IVV – iShares S&P 500 Index Fund (0.09%) VEU – Vanguard FTSE All World Ex-US (0.25%)

Index Mutual Funds

Higher minimums.

Better for small, frequent purchases (DCA).

Only priced and traded at the close of the day.

Vanguard (generally $3,000 minimum).

More on Investing in Funds Next Week…

Investing Basics

Business Analysis

Accounting Analysis

Financial Analysis

Valuation

Business Analysis

Remember last week?

Procter & Gamble Competitive advantages? Brand names? Ability to raise prices with inflation? Economic moat? Industry and type of product? Consistency?

Accounting Analysis

Do the firm’s accounting policies reflect the business reality of the firm?

If not, we must make adjustments.

More on accounting analysis later. Yes, it needs its own week (or two..).

Financial Statements

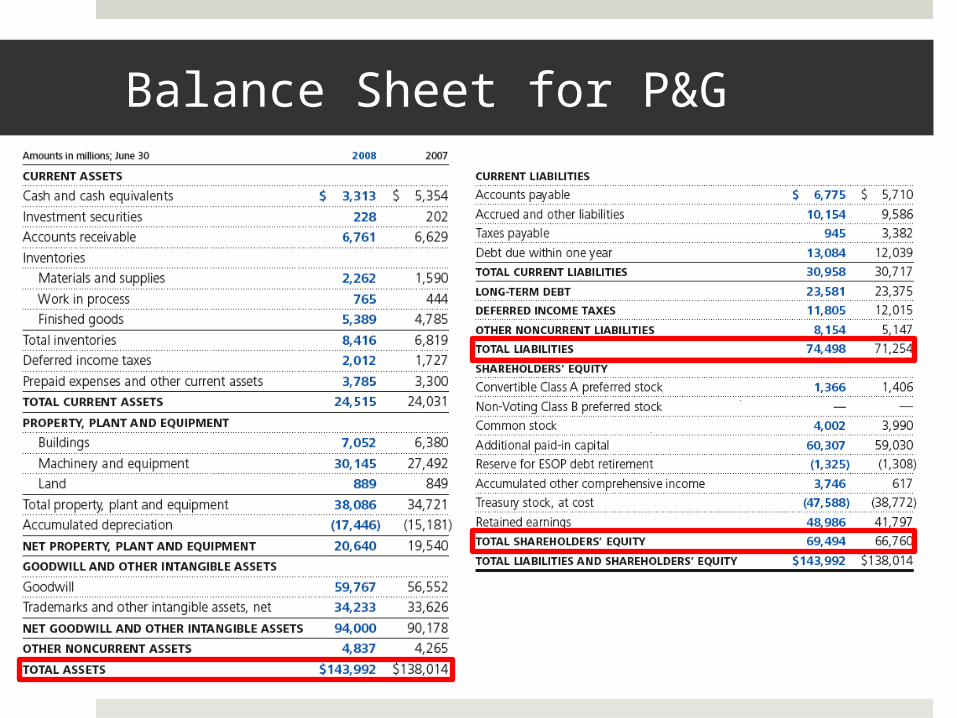

Balance Sheet: A list of the things owned and owed by the firm and the difference between the two.

Income Statement: A list of the resources acquired and consumed by a firm over a period of time.

Cash Flow Statement: A list of the flows of cash in and out of a company over a period of time.

Basic Accounting Terms

Balance Sheet Assets: Probable future benefits owned or controlled by a

firm. Liabilities: Probable future sacrifice of benefits. Equity: The difference between total assets and total

liabilities.

Income Statement Earnings: The increase in net assets (equity) resulting

from operations over a period of time.

Balance Sheet for P&G

Things to Remember

The Balance Sheet Equation: Assets = Liabilities + Equities Equity is the residual left over for shareholders after a

company’s other creditors (represented by liabilities) have been satisfied.

One of the best sources of information is the company itself and its management. This means reading annual and quarterly reports, which

can be found on SEC.gov or on the company’s website. We still need to be cognizant of management’s incentives

and biases.

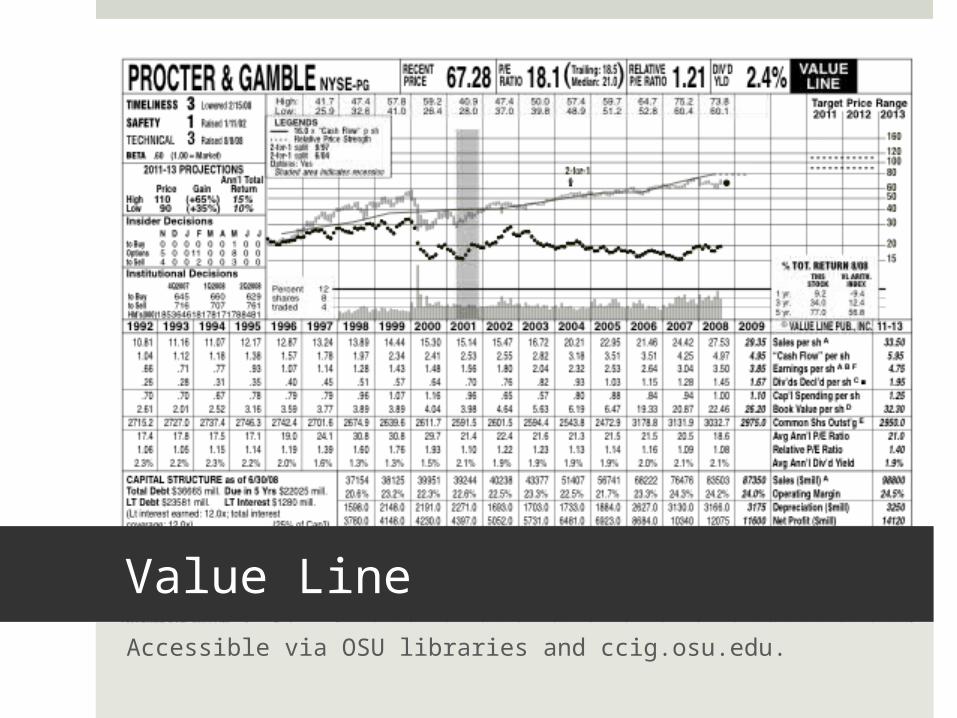

Value LineAccessible via OSU libraries and ccig.osu.edu.

Reminders About Value Line

Good starting point.

Usually a reliable source for objective data aggregated in a consistent format.

It’s generally a good idea to ignore Value Line’s predictions (or any analyst predictions for that matter).

The Basics of a Stock

Share of Stock: A security representing fractional ownership in a firm and a claim on its net assets and earnings.

Shares Outstanding: The total number of shares issued by a company.

Market Capitalization (Market Cap): The total market value of a company based on the share

price and number of shares outstanding. Share Price x Number of Shares Outstanding.

Marke

t Cap

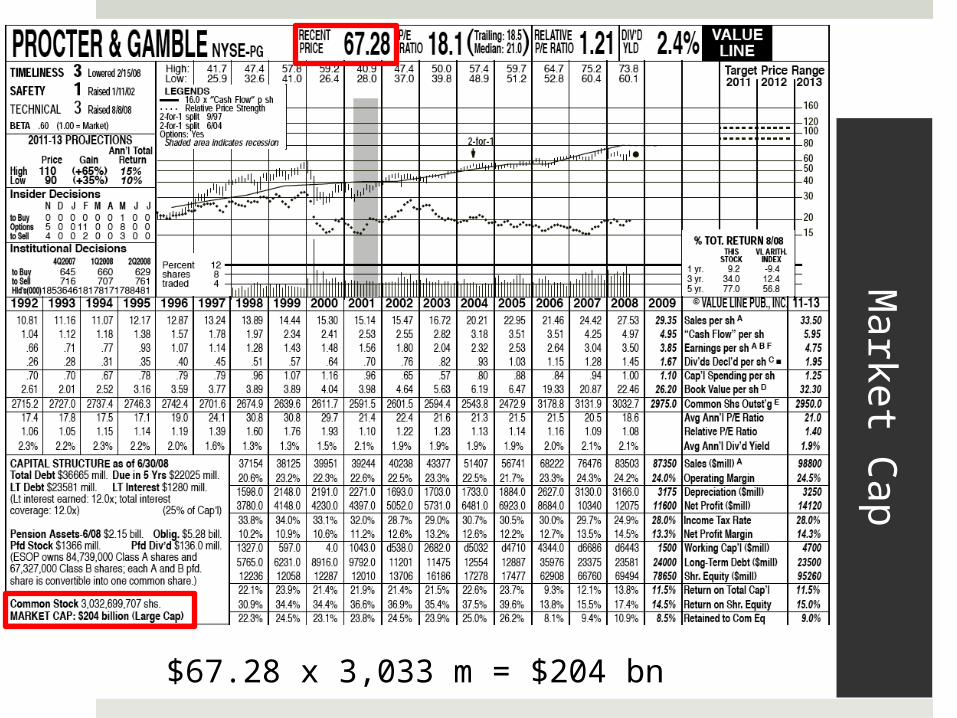

$67.28 x 3,033 m = $204 bn

Implications

Share Price One share of P&G costs $67.28.

Shares Outstanding There are about 3 billion shares outstanding, so if you buy

one share, you’re buying 1 / 3 billionth of the company.

Market Cap The total market value of P&G (based on the share price

and shares outstanding) is $204 billion.

Earnings

Definition Again: The increase in net assets (equity) resulting from operations over a period of time.

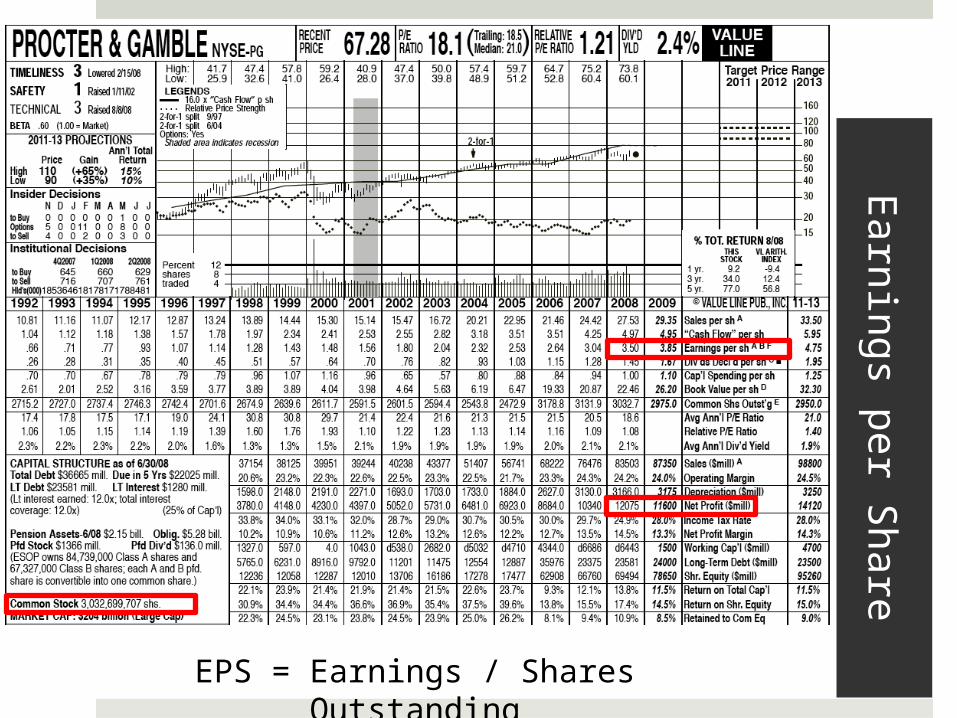

Earnings per Share (EPS) = Earnings / Number of Shares

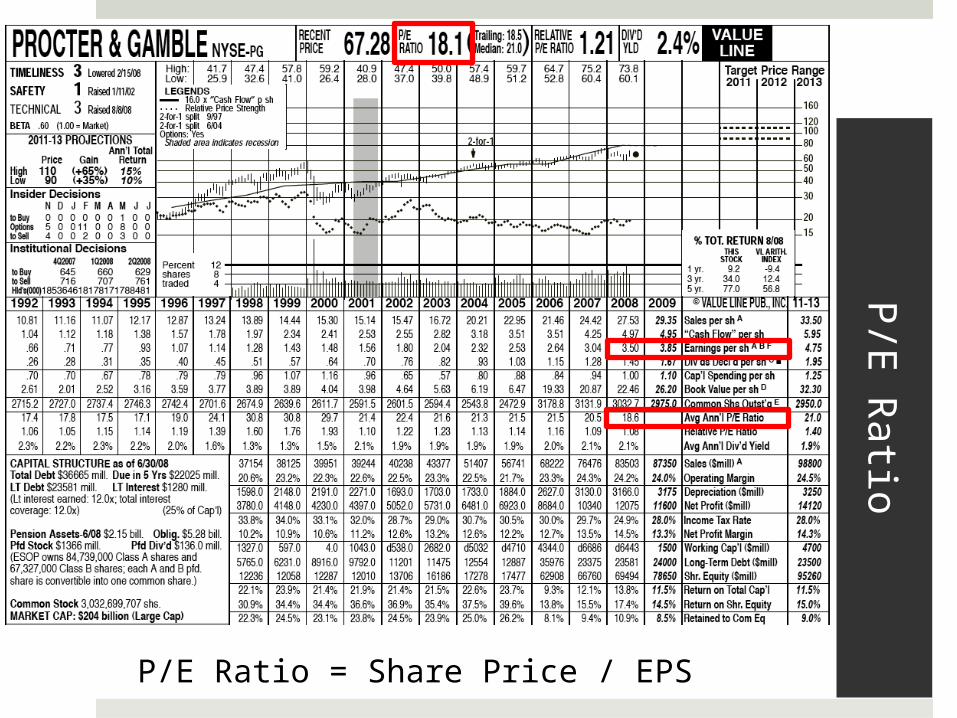

Price to Earnings Ratio (P/E Ratio) = Share Price / Earnings per Share

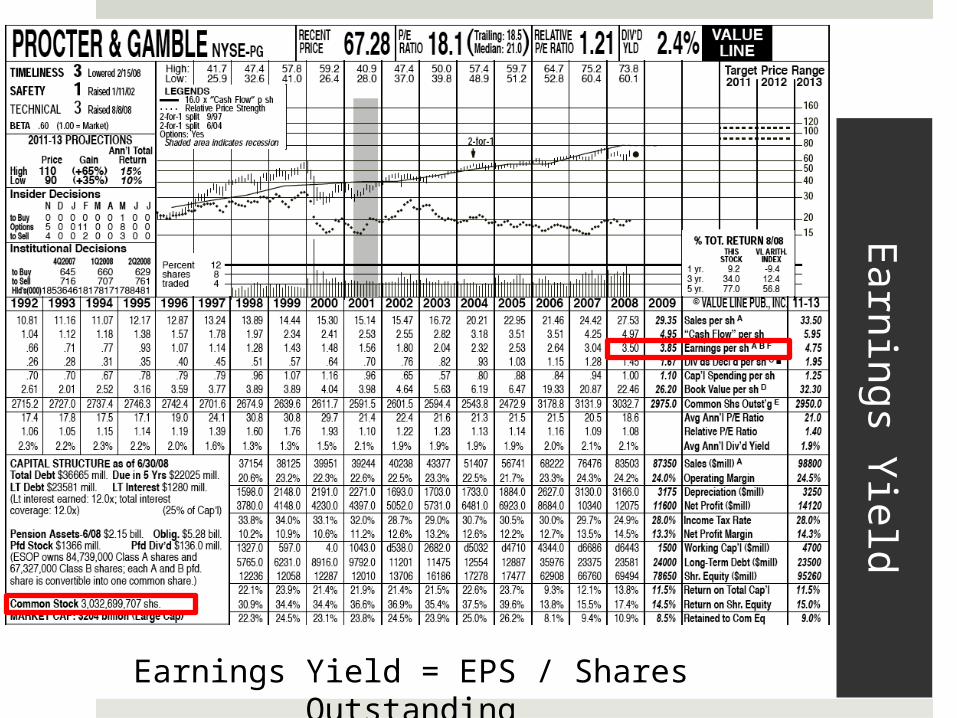

Earnings Yield = Earnings per Share / Share Price

Earn

ing

s per S

hare

EPS = Earnings / Shares Outstanding

P/E

Ratio

P/E Ratio = Share Price / EPS

Earn

ings Yie

ld

Earnings Yield = EPS / Shares Outstanding

Implications

P/E Ratio You’re paying $18.10 per dollar of P&G’s earnings. Depends on factors such as expected growth and industry.

Earnings Yield The initial yield you’re earning on your investment is

5.5%. Since the earnings yield is the reciprocal of the P/E ratio, a

lower P/E ratio results in a higher earnings yield.

Note: You might run those calculations and end up with numbers slightly different than those reported by Value Line because they use a weighted average of shares outstanding.

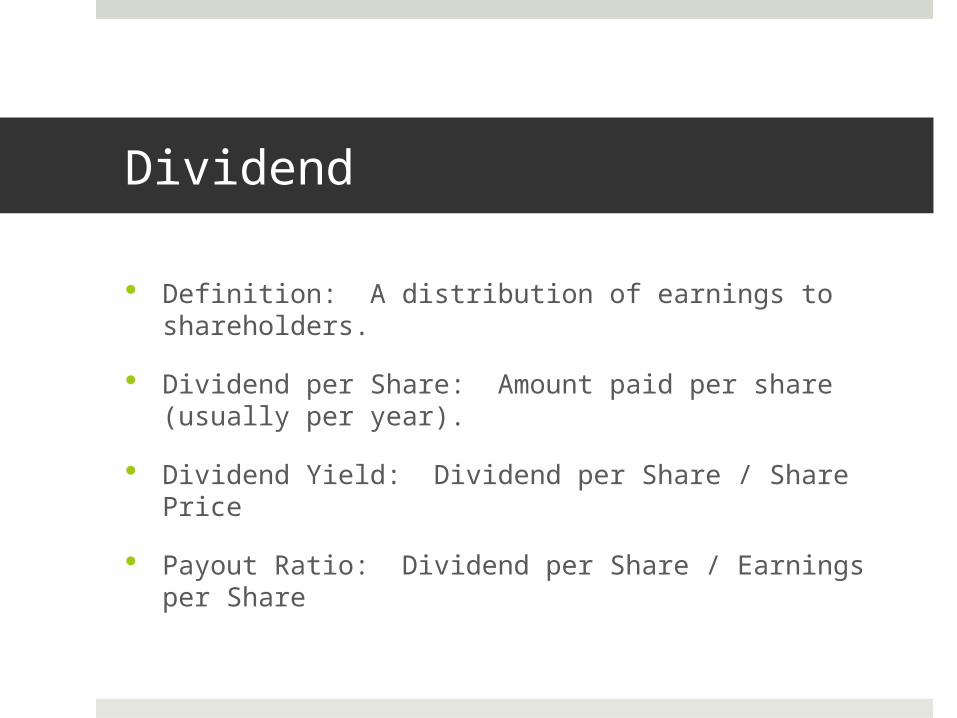

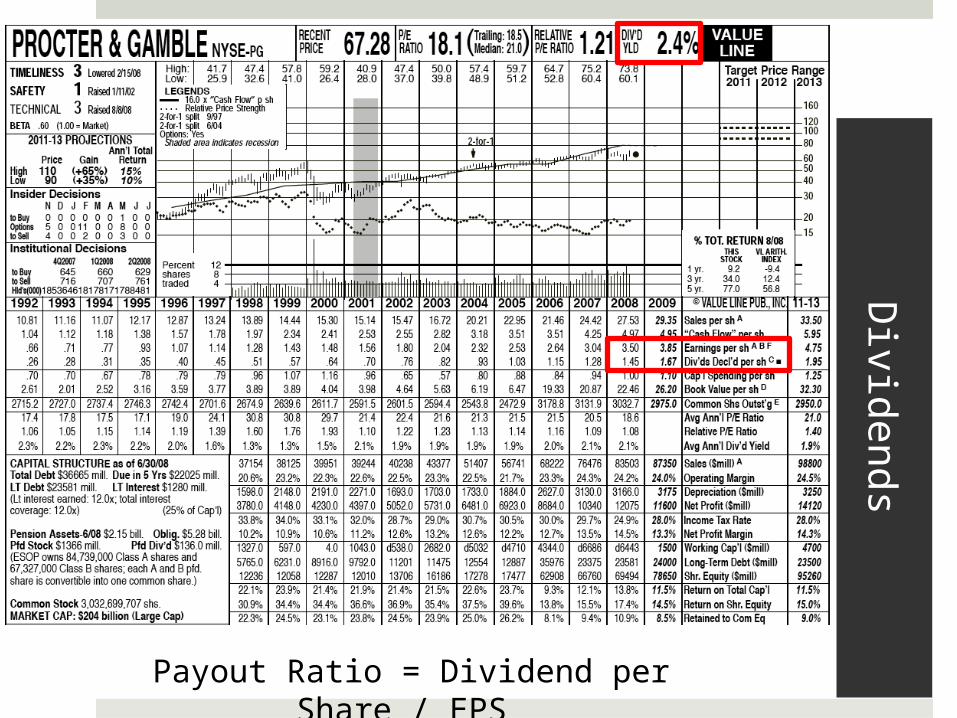

Dividend

Definition: A distribution of earnings to shareholders.

Dividend per Share: Amount paid per share (usually per year).

Dividend Yield: Dividend per Share / Share Price

Payout Ratio: Dividend per Share / Earnings per Share

Div

iden

ds

Payout Ratio = Dividend per Share / EPS

Implications

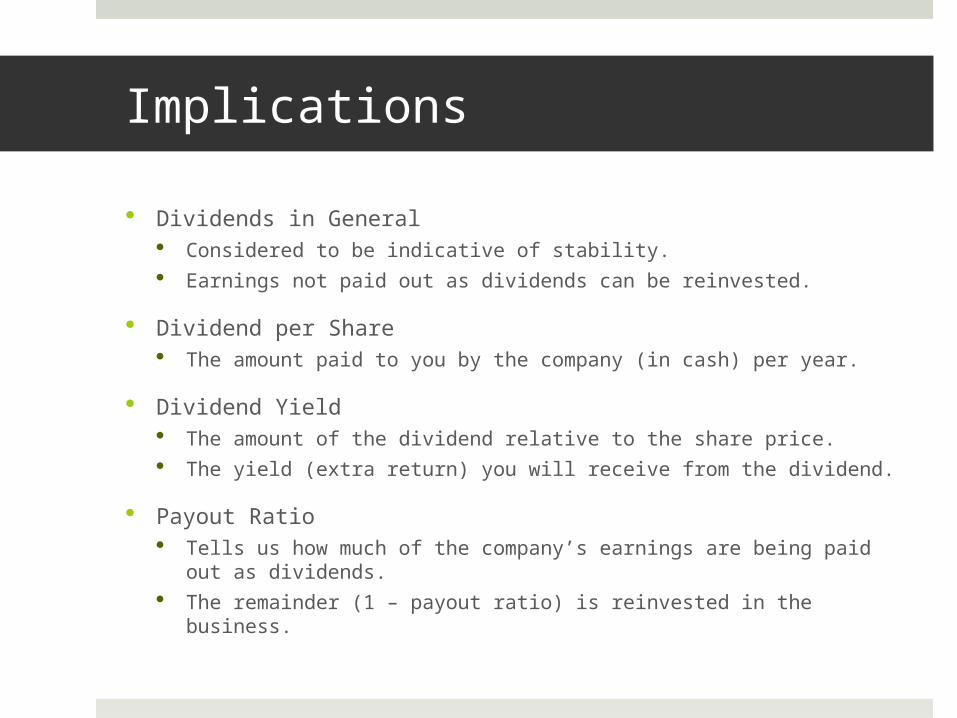

Dividends in General Considered to be indicative of stability. Earnings not paid out as dividends can be reinvested.

Dividend per Share The amount paid to you by the company (in cash) per year.

Dividend Yield The amount of the dividend relative to the share price. The yield (extra return) you will receive from the dividend.

Payout Ratio Tells us how much of the company’s earnings are being paid out

as dividends. The remainder (1 – payout ratio) is reinvested in the business.

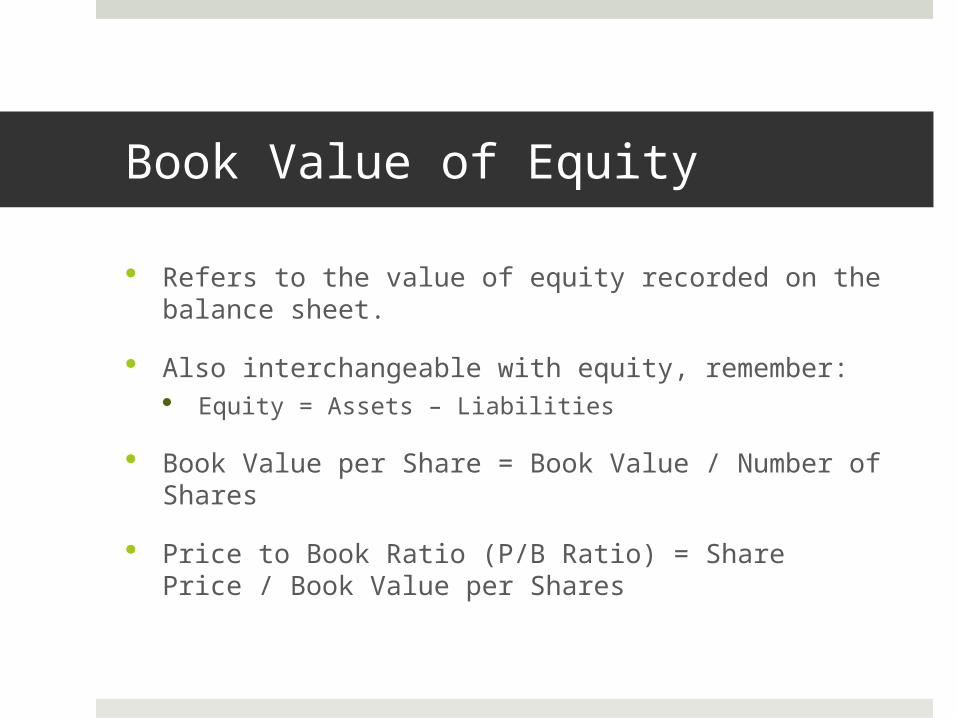

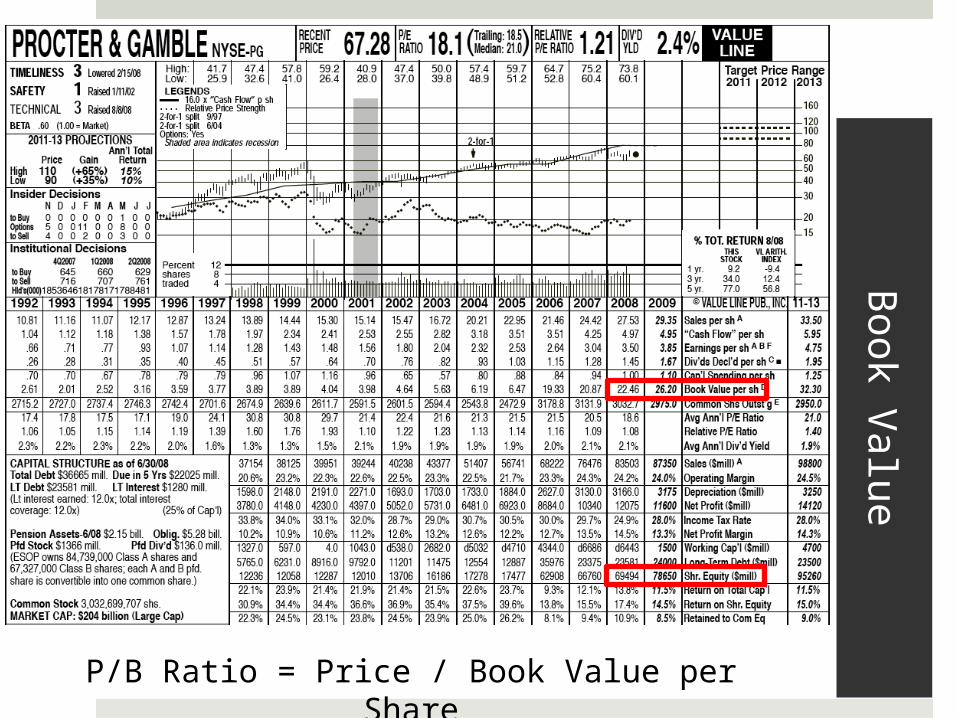

Book Value of Equity

Refers to the value of equity recorded on the balance sheet.

Also interchangeable with equity, remember: Equity = Assets – Liabilities

Book Value per Share = Book Value / Number of Shares

Price to Book Ratio (P/B Ratio) = Share Price / Book Value per Shares

Book V

alu

e

P/B Ratio = Price / Book Value per Share

Implications

Book Value Broadly refers to values assigned to various entries on a

firm’s balance sheet. Sometimes requires adjustments (for example, book value

of equity often requires the deduction of intangible assets that cannot be readily priced and sold).

P/B Ratio Above 1 indicates that the firm is priced at a value greater

than the book value of its net assets. Most firms trade at a market value above book value. Intangibles and other advantages can result in a higher

P/B ratio. High or low P/B ratio does not necessarily make

something a good or bad investment.

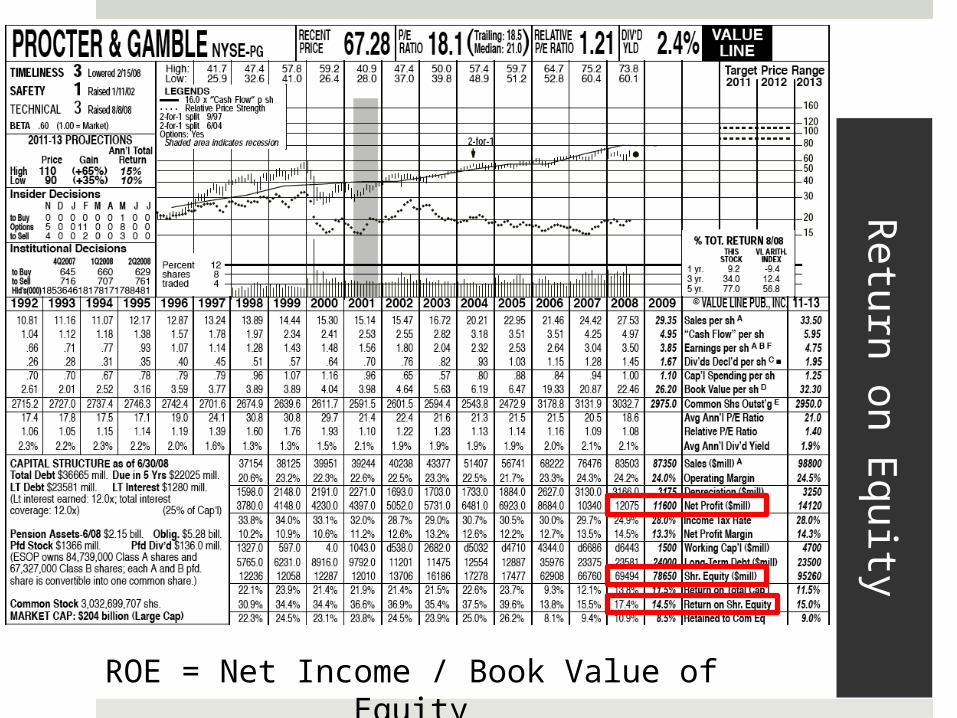

Measuring Return on Investment (ROI)

Return on Equity (ROE) = Net Income / Book Value of Equity

Return on Assets (ROA) = Net Income / Total Assets

There are a few more, but we can save those for later.

Retu

rn o

n E

qu

ity

ROE = Net Income / Book Value of Equity

Implications

Return on Equity A (relatively) comprehensive measure of how profitable a

firm is in relation to money invested by shareholders. We prefer an above-average ROE.

Return on Assets Measures a firm’s profitability relative to its total assets.

Differences Between ROE and ROA are generally caused by leverage, which can enhance a firm’s ROE.

We will break down these ratios later.

More on Valuation Later…

Don’t Feel Overwhelmed.

We covered a LOT of material today.

It takes time for these concepts to sink in.

After a few more meetings and some outside reading, you’ll catch on quickly.

This PowerPoint will be posted online for future reference and review.

Outside of meetings, ask questions on the Forum!

Some Recommended Reading for the Mean Time

The Wall Street Journal

The Superinvestors of Graham-and-Doddsville by Warren Buffett

The Dhandho Investor by Mohnish Pabrai

The Intelligent Investor by Benjamin Graham

Margin of Safety by Seth Klarman

Next Week

Getting Started Choosing a Broker Account Types

More on Investing in Funds

Starting the Club Portfolio Look at Core-Mark (CORE)

ccig.osu.edu

October 6, 2008