Embed Size (px)

Citation preview

Investing in Michigan’s Future:Community Investment Policies for

Michigan’s Higher Education Institutions

Jason Camis, Juan Bustamante and Kanthi Karipineni

Community and Economic Development Occasional Papers • June 2003

Michigan State University, Center For Urban AffairsCommunity & Economic Development Program

Investing in Michigan’s Future:Community Investment Policies for

Michigan’s Higher Education Institutions

Jason Camis, Juan Bustamante and Kanthi Karipineni

Community and Economic Development Occasional Papers • June 2003

Michigan State University, Center For Urban Affairs, Community & Economic Development Program

Table of Contents iii

Executive Summary 1

Introduction 2

Endowments and Investments 3

Socially Responsible Investing 4History of Socially Responsible InvestingComponents of Socially Responsible InvestingRates of ReturnUniversity SRI Campaigns

Community Investing 7Options for Community InvestingSecondary Rate of ReturnCommunity Investing by Educational InstitutionsThe Williams College Example

Endowments - MSU and U of M 11Michigan State University’s EndowmentUniversity of Michigan’s EndowmentPotential Impact of Community Investing in Michigan

Analysis and Recommendations 14

References 15

Selected Web Resources on Community Investing 17

Publications of the MSU Center for Urban Affairs 18

Table of Contents

Investing in Michigan’s Future:Investment Policies for Michigan’s Higher Education Institutions

Jason Camis, Juan Bustamante and Kanthi Karipineni

Executive SummaryAround the country for the past 10 years

elected officials, scholars, and the general publichave made numerous calls for a renewed visionof civic engagement by universities and colleges.The reason – many communities are in decline-resulting from years of neglect, which includesdeclining revenues and increasing expenses. Asthese distressed communities are trying torebuild, often their most significant need is in theform of financial capital. While securing finan-cial capital is often difficult, universities andcolleges have the ability to help by using theirknowledge and resources, both human andfinancial.

For years, many American educationalinstitutions have been building endowments ofmillions or billions of dollars. As security for thefuture, these endowments are invested in avariety of ways including stocks, bonds, realestate, natural resources, mutual funds, and otheroptions. However, recently some institutionshave realized that they can use their endowmentsto build stronger communities while beingfiscally responsible and ensuring institutionalstability. This can be done through communityinvesting, which is one aspect of socially respon-sible investing. Socially responsible investing(SRI) is the process of integrating money andideals to create positive social change whenmaking investment decisions. Presently, one out

of every eight dollars under professional invest-ment management in the United States is subjectto some form of SRI criteria.

Currently, community investing is the fastestgrowing component of socially responsibleinvesting. Community investing is the practiceof investing in job creation, affordable housing,small business development, and other commu-nity development projects in economicallydistressed communities. Investors are free tochoose investments that have a particular focusor impact a specific geographic area. Commu-nity investing takes place when investors direct aportion of their endowments toward communityinvestment options such as community develop-ment financial institutions and communitydevelopment banks. When investments areplaced in these various community investmentvehicles, they receive a modest yet reliable rateof return, often comparable to traditional invest-ments. At the same time, investors walk awaywith the knowledge that they are providing low-income communities the financial capital theyneed to build better neighborhoods, and ulti-mately a better society.

With renewed calls for civic engagement, theneed to attack the root problems of distressedcommunities, and positive research about com-munity investing, it is now time for universitiesto explore how they can be involved with com-munity investing and rebuilding communities.

This paper was originally prepared for the Fall 2002 course in Urban Policy Analysis (Urban and Regional Planning 848) at Michigan StateUniversity, instructed by Rex L. LaMore, State Director of the MSU Center for Urban Affairs, Community and Economic Development Program.

Communities throughout the United Stateswill never be fully complete until all of theircitizens can build a life for themselves, both therich and the poor. And currently one of thestumbling blocks for poor communities ingeneral is a lack of capital. This capital is neededto rebuild the infrastructure of various neighbor-hoods, provide decent affordable housing, andcreate meaningful employment. A recent surveyfor the Fannie Mae Foundation found that themost important influence shaping U.S. cities overthe next 50 years is the growing gap between therich and the poor (Rysavy, 2002). This wideninggap affects cities of all sizes. Investing in thesecommunities is not only a way to reduce this gap;it is a way to create vibrant and healthy commu-nities that are socially just, with economic equityand opportunity for all.

Universities have not traditionally investedfinancial resources in poor communities. Theirtypical investment in these communities has beenin the form of human resources through commu-nity service, service-learning, outreach programs,and faculty research. While these programs areimportant and have often produced solutions tovarious issues, they fail to use the institution’sfull capacity to attack one of the root problems ofdistressed communities, the lack of financialcapital.

Meanwhile, universities and colleges buildsizeable endowments for the purpose of support-ing their education mission in perpetuity. Endow-ments can provide stability for years and evendecades. They provide funds for faculty, studentscholarships, and university-based programs.However, while these large endowments providestability, universities have the opportunity to lookinward at their mission statements and determinewhat more they can do with this valuable re-source.

A traditional defining characteristic of theAmerican university has been its capacity andwillingness to help advance the economic, social,and civic vitality of our nation (Sandman, 1996).

Introduction“Our mandate is to inspire young men and

women to embrace both the challenges of schol-arship and the values of citizenship. This is amandate that does not fall to Trinity alone, but toall colleges and universities, places that at theirbest combine excellence in the classroom andlaboratory with the highest ideals of service tocommunity and nation. And yet, today, many ofour institutions of higher learning are failing topractice what they teach. As they call students tothe lessons of citizenship, they continue to hide inthe academic watchtower, protected by ironfences and lofty rhetoric. They continue to sitatop endowments that in many cases are in thehundreds of millions, even billions of dollars;arguing that to draw down these resources forcivic purposes would undermine their long-terminstitutional viability,”

- Evan S. Dobelle, Former President, Trinity College

Trinity College is one of several examples ofcolleges and universities that are investingfinancially in their community. Trinity hascommitted $6 million of its endowment toward acomprehensive $200 million neighborhoodrevitalization effort. Former Trinity CollegePresident Evan S. Dobelle’s speech emphasizedthat university leaders need to understand that theconnection between a university and the commu-nities they serve is more than typical research andoutreach. His belief is that Trinity College as awhole, along with individual students, as a part ofthe community of Hartford, Connecticut, has aresponsibility to help its community with what itneeds most – financial resources. With this inmind, he recommends that all colleges anduniversities reevaluate their commitment to thecommunities with whom they are linked. Oneway to do this is for universities and colleges toinvest a portion of their endowments in thesecommunities. Not investments as charity offer-ings, but investments made at market rates, whichbuild stronger communities and provide solidreturns to the institution.

2

investment in the future, it is a way of providinggoods and/or services not just today, but indefi-nitely into the future. Endowments provide fundsboth now and in the future through investmentearnings. They provide a reliable source offunding for future generations of students. Forthese precise reasons, colleges and universitiesoften build sizeable endowments to ensure theirfinancial stability and institutional future. How-ever, while much attention is given to the univer-sities with sizeable endowments, having anendowment is somewhat of a luxury. Manyuniversities and colleges have either smallendowments or none at all. The median endow-ment size at private colleges and universities isroughly $10 million and about two-third of thesecolleges have endowments less than $5 million.On the larger scale of endowments, 368 (roughly10%) of the nation’s colleges and universitieshave endowments over $50 million. Of those, atleast forty are over $1 billion. A study by theChronicle of Higher Education in 2001 revealedthe following about university endowments:

· Harvard University’s endowment is currentlythe largest, estimated at $17.9 billion in 2001.

· The University of Texas system has thelargest endowment of any public university at$9.3 billion.

· In only one year between 1984 and 2001 didthe average value of university endowmentsdecline.

· The combined total endowments ofMichigan’s 15 public universities was $4.58billion as of December 31, 2001.

Hundreds of millions of dollars in endow-ments are invested each year in various ways.Debt and equity are the two basic categories ofinvestments. Debt investments make loans tocompanies in the form of corporate bonds orbank notes. Equity investments are when inves-tors buy a part of a company (e.g., common stockshares). Equities are where most innovativeinvestors operate as they provide potentially

Thomas Jefferson believed that the purpose of theuniversity was to foster engaged citizenship.This purpose is being renewed today. Yet,discontent has settled in among the public in theirviews about the purpose of higher education.This discontent has led to several calls for arenewed civic purpose of universities (Katz &Dobelle, 1999; London, 2002). Research mustprovide answers to relevant social problems(Witt, 2000). Service must contribute to theuniversity’s mission of developing an effectiveand productive citizenry (MSU, 1982). Re-sources, both human and financial, must be madeavailable to benefit society as a whole.

The most recent argument by scholars is thatuniversity and colleges cannot afford to sit idle intheir ivory watchtowers on their endowments andnot be actively engaged with communities withwhich they are linked. Investing financialresources in areas such as community develop-ment, local purchasing, small business develop-ment and affordable housing is one way to beactively engaged with communities. The missionat Michigan State University (MSU) includes thefollowing statement, “Michigan State Universityis committed…to contributing to the understand-ing and the solution of significant societalproblems.” Could this now be the time for MSUto contribute to the solution of the most signifi-cant societal problem, lack of financial capital?If it is, it can do so by investing some of itsfinancial resources, particularly through itsendowment, in communities that lack thoseresources.

Endowments and InvestmentsEndowments date back to 15th century

England, however, they are truly an Americanphenomenon. They have been existent in univer-sities, hospitals, churches and other institutions inthe United States for over 300 years. An endow-ment is an aggregation of assets invested by acollege or university to support its educationalmission in perpetuity (ACE, 2000). As an

3

pension funds, non-profit organizations, andfaith-based institutions (Social InvestmentForum, 2002).

History of Socially Responsible InvestingSocially responsible investing dates back to

the late nineteenth and early twentieth centuries.The earliest expression of the concept came fromreligious institutions that chose not to invest incompanies that made alcohol or tobacco prod-ucts. In 1971, the presiding Bishop of theEpiscopal Church presented General MotorsCorporation with a resolution asking the com-pany to withdraw from South Africa. This wasthe beginning of over twenty years of divestmentin South African companies, primarily as anaction to end apartheid. In that same year, the PaxWorld Fund was established by a group ofMethodist clergy. This was the first mutual fundto screen for social issues (Kinder, Lyndenbergand Domini, 1992). Michigan State Universitywas a pioneering public higher education institu-tion when it adopted a South African divestmentpolicy. Through these actions, SRI was cata-pulted into national attention.

Socially responsible investing is growingrapidly in markets across the world. In theUnited States in 2001, one in every ten dollarsunder professional management was subject tosome form of SRI criteria (Social InvestmentForum, 2002). The article ‘Envisioning SociallyResponsible Investing: A model for 2006’suggests that “socially responsible investing hasemerged from an essentially obscure nichefinancial market to become a potentially impor-tant player in a major political debate aboutglobalization, the relationship between corpora-tions and society, and the role of capital increating both social and financialvalue”(Lyndenberg, 2002). The Social Invest-ment Forum’s 2001 Report on ResponsibleInvesting Trends in the United States showed thatassets in socially screened investment portfoliosgrew 36 percent during the previous two-year

higher returns. Some potential vehicles forgeneral investing include stocks, bonds, mutualfunds, government issues, real estate, naturalresources, and bank accounts.

Some universities have begun to realize thatamassing endowments of this magnitude – whilebeneficial for their school, students, and faculty –can also be utilized to benefit the communities inwhich they work, support, and recruit studentsfrom. The possible infusion of investmentmoney into distressed communities not onlyprovides needed capital for various communitydevelopment projects, but it can provide returnscomparable to traditional investments. And inmany cases, investors are willing to accept alower return on investment with the knowledgethat their investment will have a higher indirector secondary rate of return. By investing in localcommunities, universities show a true commit-ment to communities with which they are linked.This can demonstrate to students that service,which is often linked with scholarship on cam-puses, is more than meals served by students atthe local soup kitchen or mentoring programs forcommunity youth. Investing in communities isnot difficult. It simply takes institutional leader-ship to develop a socially responsible investing(SRI) policy that focuses on community invest-ing.

Socially Responsible Investing (SRI)Socially responsible investing is the process

of integrating money and ideals to affect positivesocial change through investment choices.Socially responsible investors make investmentdecisions based on individual or institutionalvalues regarding social and environmental issues.Their primary concern is to use their investmentsas a vehicle to build strong communities, whileearning a return on their investment similar totraditional investment options. Social investorsconsist of a broad spectrum of investors, includ-ing individuals, corporations, universities,hospitals, foundations, insurance companies,

4

dialogue on social and environmental issues.Resolutions typically direct a company and itsboard of directors to improve on some type ofcurrent social or environmental practice. Even ifthe resolutions are not passed, they may have animpact by bringing particular issues to the atten-tion of the public and stakeholders. An exampleof shareholder activism is when stockholdersdivested in U.S. corporations doing business withor in South Africa during the 1970s and 1980s.In this case, shareholder activism is credited withhelping eliminate apartheid. Another example isin 1997, when a shareholder resolution forcedTime magazine to print their magazine on chlo-rine free paper (Schade, 2002). Also in 1997,Pepsico and Texaco companies divested theirholdings in Burma (Myanmar) as a result ofshareholder resolutions (Shareholder ActionNetwork, 2002).

Community Investing is the practice ofinvesting to create positive social change such asaffordable housing, microenterprise and smallbusiness development, and other communitydevelopment initiatives in distressed communi-ties. Through community investing, investorsdirectly place their funds in investments that earna return that benefits communities. This can bedone in various geographic areas, ranging frominner cities to rural communities. It can also bedirected toward particular projects. The strengthof community investing is that it has a direct andmeasurable impact in communities where invest-ments are placed. Most community investmentsare accomplished through community basedfinancial institutions such as microenterprise loanfunds or community development credit unions.

Rates of ReturnThose who administer endowments are

required to demonstrate fiscal responsibility. Formost investors this is understood to mean, “seek-ing the most prudent and highest rate of return.”Over the last decade, a number of studies havelooked at whether socially responsible investing

period, whereas traditional funds grew only 22percent (Most, 2002).

Domini Social Investments, an investmentcompany located in Providence, Rhode Island,currently manages more than $1.2 billion inassets for individual and institutional investorsinterested in socially responsible investing. ItsDomini Social Equity Fund is the nation’s largestsocially responsible index fund with over $920million in assets. Another large well-knownfund, the TIAA-CREF socially screened fund,has grown to well over $2 billion in recent years(Waddock & Graves, 2000).

Components of Socially Responsible InvestingSocially responsible investing has three key

strategies: Social Screening, Shareholder Advo-cacy, and Community Investing. Each strategyplays a unique part in an overall investmentstrategy of an individual or an institution. Inves-tors are able to choose any combination of thestrategies to accomplish their investment objec-tives and social goals.

Social Screening is the process of screeningthe investment portfolio for companies that aredeemed socially irresponsible. Some commonsocial screens include nuclear power, alcohol,weapons, gambling, tobacco products, andrepressive regimes. As of 2001, there were 230mutual funds in the United States that incorpo-rated social screening. According to the SocialInvestment Forum, a nonprofit organization thatpromotes socially responsible investing, 84% ofsocially screened portfolios exclude tobacco,72%, gambling, 69% weapons and 68% alcohol.

Shareholder Activism is the process ofinvestors influencing the practices of corporationswith regard to social and environmental issues.Shareholder activism consists of both dialogueand formal shareholder proposals known asshareholder resolutions or proxy statements(Social Investment Forum, 2002). The goal ofshareholder initiatives is to influence corporatepolicy by engaging management in productive

5

funds. Universities set yearly goals as to theinterest earnings they are attempting to earn fromtheir investments. For instance, Michigan StateUniversity in 2002 was striving for a return of10.9%. The percentage return that MSU strivesfor is reached by a historic analysis of investmentperformance. The university also takes into ac-count inflation and its desired spending from itsinvestments – currently 5.25% of the averagemarket value of the endowment as calculated forthe twelve quarters of the three calendar yearsprior to the beginning of the fiscal year (MSU,2003). Since the rate of return is such an impor-tant aspect of investment decisions, investorsoften argue that the nature of socially responsibleinvesting will lower financial returns, whichwould harm the university’s long-term goals.Yet research has begun to consistently prove thisargument wrong (Waddock & Graves, 2000;Guerard, 2002; Most, 2002).

University SRI CampaignsMany socially responsible investment cam-

paigns in higher education institutions grew outof the Vietnam War era, when many chemicaland weapons companies were targeted for divest-ment because of their involvement in the produc-tion of war weapons (Schade, 2002). This wasfollowed by the South African divestment cam-paign when Michigan State University, alongwith hundreds of colleges across the UnitedStates in the 1980s, divested from corporationshaving business interests in South Africa whenapartheid was still being practiced. SRI cam-paigns have gained momentum in colleges overthe past 20 years. The goal of these SRI cam-paigns is to encourage universities to adopt ethi-cal standards in their multi-million or billiondollar investments. For instance, the Universityof Washington, Stanford, Tufts, and Haverfordno longer invest in tobacco companies. The Uni-versity of Wisconsin and the University of Min-nesota divested from corporations withoperations that support the military regime in

impacts financial performance. Most of thesestudies have indicated that there is little or nodifference between socially screened andunscreened investments. According to a studypublished in the winter 1993 issue of FinancialAnalysts Journal, socially responsible mutualfunds do not earn less statistically significantreturns and the performance of these mutual fundsis not statistically different from that of conven-tional mutual funds (Hamilton, Jo and Statman,1993). A similar study published in winter 1997issue of Journal of Investing also found nosignificant differences in the mean returns ofsocially unscreened and socially screened equityinvestments for the 1987-1996 period. Over thelast decade (1991-2001), the index run by KLDResearch & Analytics Inc. posted annualizedreturns of 19.01 percent, while its comparablebenchmark, the S&P 500 posted only 17.48percent returns (Most, 2002). The recent perfor-mance of the market might suggest that a sociallyresponsible investment plan may be a very soundinvestment strategy.

Data released in 2002 by Lipper, a globalleader in supplying mutual fund information,showed that socially responsible mutual fundshad their assets increase by 3 percent betweenJanuary-June 2002, while conventional U.S.funds experienced a 9.5 percent decrease in totalassets (Social Investment Forum, 2002). Lipperdata also indicated that in June 2002, when the S& P 500 lost more than 13 percent, SRI mutualfunds received net inflows of $47 million. Mean-while, the quarterly mutual fund performancereleased by Social Investment Forum in July 2002found that 13 out of the 18 screened funds with$100 million or more in assets tracked by theSocial Investment Forum achieved the highestranking from both Lipper and Morningstar(Social Investment Forum, 2002).

This evidence suggests that university andcollege trustees who have a fiduciary responsibil-ity to maximize financial returns on their invest-ments can achieve adequate returns through SRI

6

other community development projects in eco-nomically distressed communities. Distressedcommunities need capital to survive, sustain, andeventually flourish. Financial capital is needed toconstruct, rehabilitate, acquire and refinancehousing, to begin or expand businesses, and toconstruct or rehabilitate community facilities(Kinder, Lynberg and Domini, 1992). Communityinvestments can provide some of this much neededcapital. Community investing is emerging as thefastest growing component of socially responsibleinvesting in the United States. According to astudy done by Social Investment Forum, indi-vidual and institutional assets flowing into com-munity investing organizations grew by 41 percentbetween 1999 and 2001 totaling $7.6 billion in2001 (Social Investment Forum, 2002).

Options for Community InvestingDepending on the investment decisions made

by an individual or the guidelines of an institution,there are three distinct options for communityinvesting: direct investment, community invest-ment portfolios and mutual funds (Social Invest-ment Forum, 2002).

Direct Investment: Individuals or institutionscan make direct investments in Community Devel-opment Financial Institutions (CDFI). These insti-tutions range from small non-profitmicroenterprise lenders with a few hundred bor-rowers, to larger banking institutions such as theSelf-Help Credit Union and Ventures Fund, whichhas 3600 borrowers and loans totaling $190 mil-lion (Freundlich, 2002). Typical rates of return forCDFIs range from 0-4 percent for terms of one tofive years (Calvert Group, 2002). The followingare five types of direct investment:

Community Development Banks (CDBs).These are local lending institutions that ad-dress community development needs. Theyoffer the same kinds of services as conven-tional banks, but with the purpose of providingthese products and services in communitiesthat are underserved by conventional banks.

Burma (Myanmar). Yale, Harvard, Stanford,Portland State, Columbia, Brown, Cornell, andTufts are among the many educational institu-tions with active committees on socially respon-sible investment (Students Transforming AndResisting Corporations, 2002). And WilliamsCollege recently developed a social choice fundfor potential college donors, so that they can di-rect their investments to create social change,while benefiting the college.

However, while socially responsible invest-ing through social screening is important, theresults of these investments are only seen throughindirect relationships. Whereas with communityinvesting, investors actively create positive socialchange by addressing basic community needssuch as affordable housing, new jobs, and keysocial services through investments in local com-munity development organizations. Investing inlow-income communities through vehicles likecommunity development banks and communitycredit unions has the ability to create the neededfinancial capital to create visible short and long-term change. In return, investors receive a mod-est, but secure return on their investment. Inaddition, investors can eventually see a ‘second-ary’ rate of return through jobs created, housingunits built, and businesses developed. Each hasthe ability to improve their respective communi-ties. By doing so, universities are potentiallydeveloping stronger communities from whichthey are likely to draw future students. Thus thebenefit is seen both in distressed communitiesand on the university’s campus. The benefits to apublicly supported higher education institutionare obvious and significant. A healthy stateeconomy directly translates into a positive gen-eral fund position for the institution.Community Investing

One type of socially responsible investing iscommunity investing. Community investing isthe practice of investing in job creation, afford-able housing, small business development, and

7

community development efforts than CDBsand CDCUs since they are not governmentregulated and as such offer a unique set ofrisks.

Community Development Venture CapitalFunds. These are structured in a variety ofways including for-profits, non-profits, lim-ited partnerships and limited liability compa-nies. These funds are invested in equityinvestments in entrepreneurial businesses thathave the capacity to create jobs and wealth indisadvantaged communities. They primarilyprovide startup capital for real estate and newbusiness development.

Microenterprise Programs. These are pro-grams that lend money to businesses withfewer than five employees that do not haveaccess to commercial banking products andrequire loans of $25,000 or less. They areoften uninsured, however they provide train-ing, technical assistance, credit, and access tomarkets. There are over a dozenmicroenterprise programs located in Michi-gan. Two of the largest are the NorthernEconomic Initiatives Corporation inMarquette and the Lansing Community Mi-cro Enterprise Fund. In general, there arefew of these programs available to investors.

A list of nationwide community developmentfinancial institutions can be obtained from thewebsite www.socialinvest.org.

Community Investment Portfolios: The sec-ond option for community investing is throughcommunity investment portfolios. With this op-tion, investors can purchase a larger pool ofCDFI investments through intermediaries andreach a number of different types of programs atonce. Terms and rates are roughly similar to theCDLFs and CDCs they invest in, typically 0-4percent (Calvert Group, 2002). The intermediaryusually has a diverse portfolio of communityinvestments and offers investors the opportunityto invest by targeting a region or specific sector.

They are government regulated and providebanking services and loans to people whohave difficulty obtaining market rate financ-ing. They offer federally insured checkingaccounts, savings accounts, certificates ofdeposit (CDs), money market accounts, andindividual retirement accounts (IRA) (SocialInvestment Forum, 2002). The South ShoreBank in Chicago is one of the oldest commu-nity development banks that supports com-munity development efforts in the Chicagoand Detroit metropolitan areas (Equity Trust,2002).

Community Development Credit Unions(CDCUs). These are non-profit financialcooperatives that provide banking and loanservices to financially disadvantaged commu-nities. They promote local community lend-ing and generally offer all traditional depositproducts. They are easier to organize andhence are more numerous than communitydevelopment banks. CDCUs make loans onlyto their members within their designatedcommunities, but most of them do acceptdeposits from outside investors. Over 300community development credit unions existin low-income areas with total assets of morethan $400 million. Deposits are typicallyinsured up to $100,000. There are as manyas seven certified CDCUs in Michigan.

Community Development Loan Funds.These are private, non-profit, unregulatedand uninsured entities. They work with indi-viduals and institutional investors to financehigh-impact community developmentprojects. Hundreds of loan funds are in exist-ence. Though they are not insured, invest-ments are protected through collateral, loanloss reserves, and a fund’s net worth. Theyare more likely to net higher rates of returnthan other community investment options.Community development loan funds are alsomore flexible in making capital available for

8

Secondary Rate of ReturnOne advantage of socially responsible invest-

ing and community investing is what is under-stood as the “secondary rate of return.” That is,in addition to the primary rate of return, a so-cially responsible investor realizes “other” ben-efits from their investment portfolio. Thesecondary rate of return is often difficult to accu-rately quantify. It can be thought of in terms ofjobs created, houses built, and community ser-vices provided. For example, an investmentplaced with any of Michigan’s CDFIs wouldleverage significant other capital and providefinancing for new affordable housing units or jobcreation through development of new small busi-nesses.

A recently developed program at HarvardUniversity, the 20/20/2000 program, has lever-aged over $25 million for developing affordablehousing in the cities of Cambridge and Boston.The program is essentially a $20 million low-interest loan fund that has so far created over1700 affordable housing units in only its first 3years (of a 20-year program). A 2001 study ofthe economic impacts of housing developmentconcluded that building 100 multifamily units inurban Massachusetts would result in at least$5.73 million in income for residents, $1.15 mil-lion in revenue for state and local governments,and 120 jobs generated in the state. In additionto these immediate impacts, the expected recur-ring impacts of these 100 units included morethan two million dollars in annual income,$834,000 in annual revenue for state and localgovernments, and 54 jobs (Kotval, 2001).

For universities that invest their endowmentsin communities, numerous secondary rates ofreturn can be realized. For instance, local busi-ness development through community investingcould create additional jobs for students in theform of part-time supplemental income, coopopportunities, and internships. It could also cre-ate a healthier, exciting community, one that canhelp draw students to attend the university ini-

Two examples of pooled approaches include theCalvert Community Investment Program and theNational Federation of Community DevelopmentCredit Union’s Nominee Deposit Program(Calvert Group, 2002).

Mutual Funds: The third option, sociallyresponsible mutual funds, allows investors theopportunity to have an impact in communitieswhile investing in a more traditional way. Thesemutual funds pool investors’ money to buy aportfolio of securities. Overall they direct a por-tion of their assets to support community devel-opment initiatives. A few mutual funds have acommunity investment component built in.These assets are directed toward institutions un-der the direct investment option. They have theadvantage of being very liquid, however, inves-tors do not have control over the percentage ofthe mutual fund that is used for community in-vesting. In addition, investors do not control thetypes of projects that are funded. They can how-ever choose funds that target areas that investorsare interested in. The Calvert Group, DominiSocial Investments and Parnassus Investments arethree of the larger providers of socially respon-sible mutual funds (Social Investment Forum,2002). As an example, the Calvert Social Invest-ment Fund is a mutual fund that seeks to providean economic and social return to society that willcontribute to the quality of life for all. The fundis invested in three types of community-basedorganizations: low-income housing funds, com-munity development loan funds, andmicroenterprise funds. As of October 2002,Calvert Social Investment Fund had invested over$9 million in high impact social programs(Calvert Group, 2002).

Each of the three options for community in-vesting presents benefits and disadvantages. In-vestors are usually advised to explore whichoption(s) best suit their investment needs andprovides the desired impact in communities.

9

investment dollars would make a powerful, last-ing difference for people in disadvantaged com-munities. The fact that individual andinstitutional investors can achieve tremendousprogress in communities with little or no impactto their portfolios through the Social InvestmentForum’s community investment initiative is acompelling reason for social investors to takeaction (Social Investment Forum, 2002).Community Investing by EducationalInstitutions

Many would argue that educational institu-tions have a unique responsibility towards thesociety that nurtures and sustains them. By in-vesting financially in communities, both localand statewide, a college or university can furtherits mission and act upon their public trust respon-sibility. Universities and colleges are in a posi-tion to create lasting change by altering theircurrent investment practices.

At the same time, university officers have aresponsibility to maintain the viability of eachinstitution. They are responsible for providingcurrent programs as well as regulating finances,both now and for the future. However, whilethey are often bound to maximize the financialreturns of the university’s investments, this doesnot preclude participating in community invest-ment. Community investments can yield a mod-est but reliable financial return and a significantsocial return. This can be beneficial for theschool in attracting donations from alumni andothers donors who want to contribute to the de-velopment of their community. It can also leadto the revitalization of the same communities thatit will recruit students from in the future. A casestudy of one such educational institution that hasdirected a portion of its investment towards com-munities follows.

The Williams College ExampleWilliams College is a private, residential

liberal arts school located in the Berkshires innorthwestern Massachusetts. It was established

tially and upon graduating, continue to reside inthat community. Another example is the creationof affordable housing. Affordable housing devel-opment might enable more faculty to live nearcampus, which could also help create a morevibrant and stable community. Finally, strongermore stable communities with jobs and betterhousing provide the state with a better revenuestream which can indirectly benefit universitiesthat receive support from state government.

A study commissioned in 2002 by the Com-munity Investing Program of the Social Invest-ment Forum entitled CDFIs: Bridges BetweenCapital and Communities found that communitydevelopment financial institutions have a betterpay back rate than commercial banks (Baue,2002). The 107 CDFIs that were surveyed by theNational Community Capital Association had adefault rate of 0.5 percent, or about half the 0.9percent rate of all commercial banks. This 0.5percent rate is the same rate experienced by com-mercial banks with less than $100 million in as-sets. The study also stated that investors havenever lost a penny of investment capital investedin CDFIs. The 107 CDFIs surveyed had suffi-cient equity capital bases and loan reserves toabsorb any losses in their portfolios. The cumu-lative financing of the 107 CDFIs helped createor maintain almost 180,000 jobs, develop147,000 housing units and helped advance 2500community projects (Community InvestmentProgram, 2002).

The Social Investment Forum is a nationalnon-profit membership association dedicated topromoting SRI. It has developed a programcalled the “One Percent in Community” Initia-tive. This initiative was designed to encourageinvestors to move a total of one percent of ac-tively managed social investment dollars intocommunity investing by the year 2005. By di-verting one percent of an investor’s overall port-folio, it would have a minimal impact on theindividual investor’s overall returns, and the col-lective impact of a new influx of community

10

Inc., 2002). The bulk of the fund is invested inCalvert Group’s Social Investment BalancedFund. It was designed so that after the fund grewto $10,000 ten percent of the fund would be in-vested in community development loan fundswith a focus on supporting the Berkshires (Baue,2002).Endowments – MSU and U of M

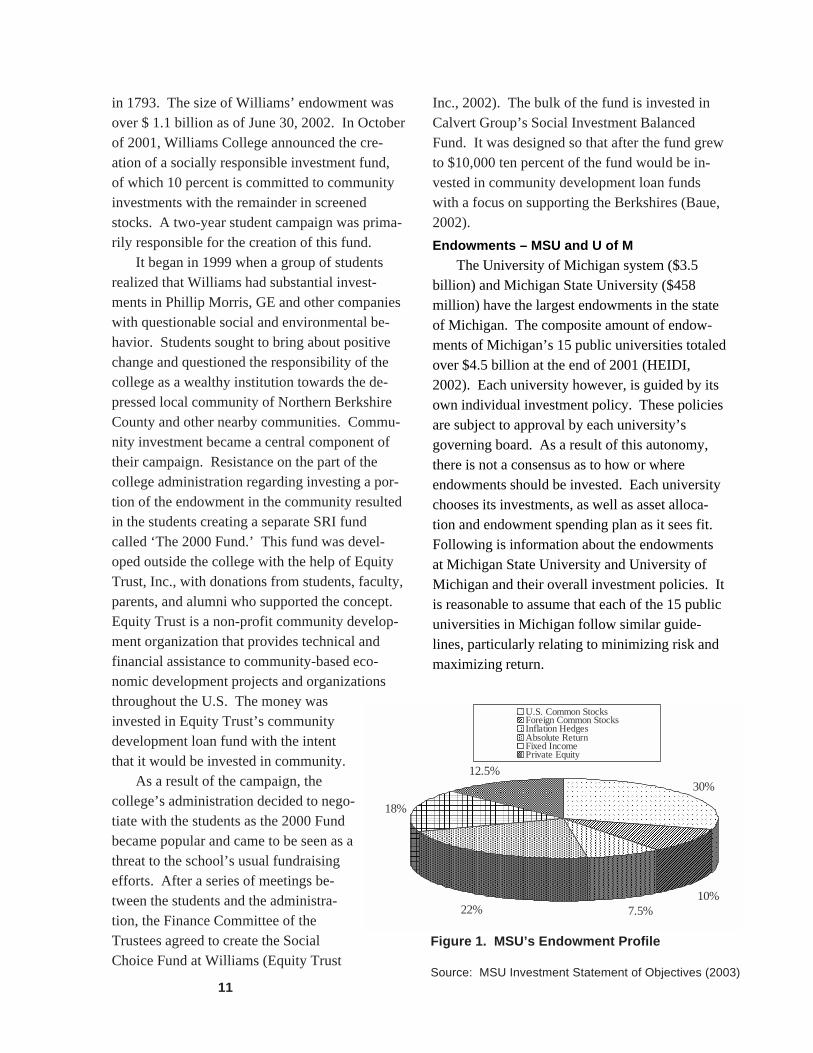

The University of Michigan system ($3.5billion) and Michigan State University ($458million) have the largest endowments in the stateof Michigan. The composite amount of endow-ments of Michigan’s 15 public universities totaledover $4.5 billion at the end of 2001 (HEIDI,2002). Each university however, is guided by itsown individual investment policy. These policiesare subject to approval by each university’sgoverning board. As a result of this autonomy,there is not a consensus as to how or whereendowments should be invested. Each universitychooses its investments, as well as asset alloca-tion and endowment spending plan as it sees fit.Following is information about the endowmentsat Michigan State University and University ofMichigan and their overall investment policies. Itis reasonable to assume that each of the 15 publicuniversities in Michigan follow similar guide-lines, particularly relating to minimizing risk andmaximizing return.

in 1793. The size of Williams’ endowment wasover $ 1.1 billion as of June 30, 2002. In Octoberof 2001, Williams College announced the cre-ation of a socially responsible investment fund,of which 10 percent is committed to communityinvestments with the remainder in screenedstocks. A two-year student campaign was prima-rily responsible for the creation of this fund.

It began in 1999 when a group of studentsrealized that Williams had substantial invest-ments in Phillip Morris, GE and other companieswith questionable social and environmental be-havior. Students sought to bring about positivechange and questioned the responsibility of thecollege as a wealthy institution towards the de-pressed local community of Northern BerkshireCounty and other nearby communities. Commu-nity investment became a central component oftheir campaign. Resistance on the part of thecollege administration regarding investing a por-tion of the endowment in the community resultedin the students creating a separate SRI fundcalled ‘The 2000 Fund.’ This fund was devel-oped outside the college with the help of EquityTrust, Inc., with donations from students, faculty,parents, and alumni who supported the concept.Equity Trust is a non-profit community develop-ment organization that provides technical andfinancial assistance to community-based eco-nomic development projects and organizationsthroughout the U.S. The money wasinvested in Equity Trust’s communitydevelopment loan fund with the intentthat it would be invested in community.

As a result of the campaign, thecollege’s administration decided to nego-tiate with the students as the 2000 Fundbecame popular and came to be seen as athreat to the school’s usual fundraisingefforts. After a series of meetings be-tween the students and the administra-tion, the Finance Committee of theTrustees agreed to create the SocialChoice Fund at Williams (Equity Trust

11

Figure 1. MSU’s Endowment Profile

Source: MSU Investment Statement of Objectives (2003)

������������������������������������������������������������������������������������������������������������������������������������ ����

����������������

��������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� ����������������������

����������������������������������������������������������������������������������������

�������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

����������������������������������������������������������������������������������������������������������������

��������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

22%

18%

7.5%

12.5%30%

10%

���U.S. Common Stocks���Foreign Common Stocks

���Inflation Hedges���Absolute Return

������ Fixed Income���

Private Equity

In doing so, it hopes to provide continued supportfor university programs, be it funding for scholar-ships, faculty salaries, or facilities. Review ofother university investment objectives showssimilar desired outcomes.

In addition, at Michigan State Universitythere is a prescribed asset allocation as deter-mined by the Board of Trustees with input frominvestment consultants and the Trustee’s financecommittee. The purpose of asset allocation is tominimize risk and provide a desired rate of returnby investing in various classes of investment suchas common stocks (U.S. and/or foreign), inflationhedges, private equity, fixed income and absolutereturn. For each asset class there is a targetpercentage, which is within a range of percent-ages. This allows the university to adjust itsinvestments accordingly, particularly whenmarket conditions change. Beyond the assetallocation, the university adopts short-term andlong-term goals, which it compares to marketbenchmarks to determine its investing perfor-mance. Fig I. shows the target asset allocation ofMichigan State University’s endowment.

University of Michigan’s EndowmentThe University of Michigan (U of M) endow-

ment fund is 13th largest of U.S. higher education

Michigan State University’s EndowmentThe endowment at MSU is guided by an

investment policy that was most recently updatedin June 2003. It is divided into nine sectionsoutlining everything from the nature of fundsinvested in to the roles of investment managers,board of trustees, finance committee, investmentconsultant, university administration and invest-ment custodians. This document spells out rolesof individuals; however, each of these individualsmust follow the university’s fundamental invest-ment principles and a statement of investmentobjectives. Those documents are the guidelinesby which all university officials must followwhen making investment decisions.

Michigan State University’s endowment of$458 million is invested in the common invest-ment fund. This overall fund consists of follow-ing three separate funds:

• Institutional funds that cover long-terminvestments, which can include both retire-ment and endowment funds.

• Annuity and life income funds as permanentinvestments.

• Institutional cash (MSU, 2000).The endowment is invested in the first of thesefunds.

The investmentobjectives of the CommonInvestment Fund are toprovide a total rate ofreturn sufficient to satisfyannually the amount tooperate University’sprograms supported byendowment funds andachieve the desired returnwhile bearing a moderateamount of risk (MSU,2000). In simple terms,the university hopes tomaximize its return whilemaking safe investments.

12

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

����������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������

�����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������

��������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

24%

14%

21%1%

26%

14%

����U.S. Stocks

����Non U.S. Stocks����

Bonds����

Cash����Alternative Assets

����Absolute Return

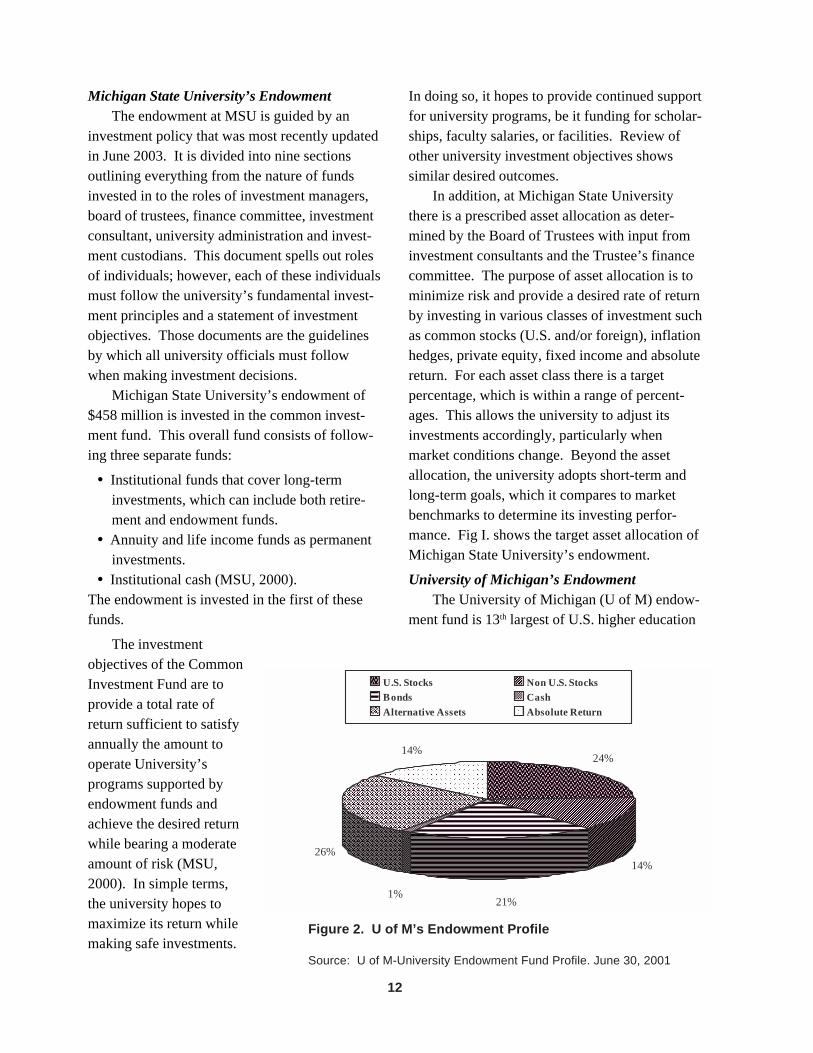

Figure 2. U of M’s Endowment Profile

Source: U of M-University Endowment Fund Profile. June 30, 2001

Michigan administrators and Board of Regents tolook for long-term alternatives of re-investments.University of Michigan’s endowment is com-posed with the following profile: 24% U.S.stocks, 14% non U.S. stocks, 21% bonds, 1%cash, 26% alternative assets (venture capital,private equity, real estate, energy investment) and14% absolute return (emphasizing manager skillsrather than market movements) (OD, 2001).Figure 2 shows the asset allocation of U of M’sendowment.

It is important to note that the University ofMichigan has a significant diversification ofalternative assets and absolute returns. As a rule,it invests 40% of its total long-term investmentpolicy in alternative assets, most likely becausethey are not significantly dependent on thevolatility of the stock markets.Potential impact of using endowments forcommunity investing

Much of the community investing done byvarious institutions and individuals is throughalternative asset allocation. This allows investorsthe ability to make a social impact, while earningpotentially larger returns with riskier and moretraditional investments. The potential for socialimpact would be greater however, if each ofMichigan’s public universities chose to allocate aportion of their endowment investing in commu-nity investments, such as the Adrian DominicanFund, the McGehee Fund, or bonds issued by theMichigan State Housing Development Authority(MSHDA) . For example, if U of M invested 1%(as proposed by the Social Investment Forum forall investors) of their alternative assets into com-munity redevelopment, this could result in a totalof $9.1 million invested in Michigan communi-ties. Similarly, if Michigan State University in-vested 1% of its alternative assets (approx. 20%of total asset allocation) in communities, thiswould amount to $916,000.

On a larger scale, if each of the 15 publicuniversities invested 1% of their alternative as-sets in community investments (assuming each

institutions and the 4th largest among U.S. publicuniversity systems (NACUBO, 2003). It hasgrown to its current size of $3.5 billion throughan investment strategy of managing risk whilemaximizing return.

The endowment at U of M is divided into twotypes: true or permanent endowment and quasi-endowment. The true or permanent endowmentconsists of funds that come from outside donorsand the principal is invested in perpetuity withonly a portion of interest being spent annually.These distributions must be used in accord withthe donor’s desires. The quasi-endowmentconsists of funds that come from either outsidedonors or internal funds in which the principal isavailable to be spent as the institution sees fit(DP, 2000).

U of M’s endowment is organized similar toa mutual fund, which is somewhat different thanMSU. It has an overall endowment pool thatincludes the balances of both the true and quasiendowments. Money that is placed into anendowment account will buy shares in theendowment pool at the share value, which isdetermined quarterly. On average, the increase inthe value of a share at U of M is proportional tothe increase of the value of distributions. It hasalso increased steadily in over the past five years.For example, the share value for the University ofMichigan endowment in June 1997 was approxi-mately $2.20, and by June 2001 it had increasedto almost $7 per share (Office of Development,2001). Much of the increase of share value canbe attributed to university’s assets allocation andthe policies regarding the hiring of investmentmanagers.

The University of Michigan’s endowmentinvestments are quite diversified and hence, theinvestment risks are significantly lower (UM,2001). However, in the transition from the fiscalyear 2000 to 2001, the University of Michigan’sendowment lost almost $180 million due to thevolatility of the financial markets. Nonetheless, itre-affirmed the conviction of the University of

13

needs including the needs of under-privilegedmembers of the society.

· Michigan State University has initiated amajor capital campaign. A communityinvestment policy has the potential to attractadditional donations, particularly frompeople who feel strongly about ethicalinvesting. This could ultimately assist theinstitution, and others, in achieving donorcampaign goals.

· Community investing yields modest, yetreliable financial returns while maximizingthe use of investment funds. In return, itprovides a significant secondary rate ofreturn by providing affordable housing,creating jobs, and developing smallbusinesses.

Just as the university is cautious in develop-ing an overall investment policy, it should also bemethodical in implementing SRI as part of thatpolicy. MSU could easily develop guidelinesregarding socially responsible investing, with afocus on community investing.

One potential scenario for the universitywould be to form a committee to further explorehow it can promote its mission of solving societalproblems through community investing. Thecommittee’s goals would be to work with theBoard of Trustees, investment managers, andconsultants to develop a SRI policy that comple-ments the university’s current investment strat-egy. The committee would be composed of agroup of representatives across campus includingstudents, faculty, staff, university officials, andcommunity representatives. It would developguidelines regarding how community investing isaccomplished at MSU, including investment op-tions (such as through CDFIs or CDBs), geo-graphic targeting for community investments,and the type of impact the university would ulti-mately desire (building affordable housing orproviding small business loans for example). This

university has 15-25% placed in alternative as-sets), it would infuse as much as $11.5 millioninto communities to create jobs, develop afford-able housing and rebuild distressed neighbor-hoods. The impact for Michigan would besignificant. For example, $10 million invested inMichigan for a period of 5 years would create867 new affordable housing units, 4,500 newmicroenterprises, 700 new small businesses, ormore than 4,000 new jobs (Calvert Group, 2002).Over time, community investing could have alasting impact that benefits both distressed com-munities in Michigan and all of Michigan’s pub-lic universities.

Analysis and RecommendationsSocially Responsible Investing is increas-

ingly being practiced across the nation by bothindividual and institutional investors. A numberof well-respected universities and colleges haveincorporated SRI policies for their endowments.However, few private or public educational insti-tutions have a community investment componentin their SRI policies. In this regard, MichiganState University and other Michigan universitiescan lead the way by becoming some of the firstpublic universities to invest a portion of theirendowments in community investment vehicleslike Community Development Financial Institu-tions and community development banks. Thereare many reasons why MSU and ultimately otherpublic universities should adopt a communityinvesting as part of their overall investment strat-egy:

· Community investing can further theuniversity’s mission which states, “MSU iscommitted to contributing to theunderstanding and the solution of significantsocietal problems.”

· MSU is a public university and receivessubsidies from state government and otherforms of public financing. Utilization ofthese public resources implies that there is anawareness of responsibility toward public

14

vesting could have on rebuilding communities inMichigan could be significant. With all of therenewed calls for civic engagement in the pastyears, the time is ripe for universities to trulybecome fully and financially engaged with com-munities. Edward M. Hundert, president of CaseWestern Reserve University summed it up well ata recent conference when he said, “The city anduniversity cannot thrive without each other. Bothmust work together to build real solutions to theproblems we confront in these extraordinarytimes.” Community investing provides the op-portunity to build these solutions.

References

American Council on Education (ACE). 2000.Understanding College and University Endowments.Washington, DC: American Council on Education.

Baue, William. 2002. Community Investing Pays.Available from http://www.socialfunds.com/news/article.cgi/article945.html; Internet; accessed 12 No-vember 2002.

Baue, William. 2002. SRI Gains Momentum inUniversity and College Endowment Investments.Available from http://www.socialfunds.com/news/article.cgi/article981.html; Internet; accessed 29 No-vember 2002.

Calvert Group. 2002a. Socially Responsible In-vesting. Available from http://www.calvert.com/sri.html; Internet; accessed 15 October 2002.

Calvert Group. 2002b. Socially Responsible In-vesting. Available from http://www.calvertgroup.com/sri_2486.html; Internet; accessed 15 October2002.

Community Investment Program. 2002. BuildingCommunities. Available from http://www.communityinvest.org; Internet; accessed 17 Novem-ber 2002.

Development Partnership. 2000. Invested Funds[on-line]. Ann Arbor, MI: University of Michigan;available from http://www.umich.edu/~finops/Funds/ednprese.htm; Internet; accessed 30 September 2002.

Equity Trust Inc. 2002. Investing in SocialChange [Handbook]. Massachusetts, Equity TrustInc.

Freundlich, Timothy. 2002. Community Invest-ing: Putting your capital to work. Available fromhttp://www.socialfunds.com/education/

is how many universites and colleges have en-tered the SRI and community investing domain.

A second possible scenario is for the univer-sity to adopt socially responsible investing, par-ticularly community investing, as part of itscurrent investment strategy. It would be prudentto suggest that the only a portion of the MichiganState University endowment be used for sociallyresponsible investing and community investmentstrategies. The investment managers who arehired by the board of trustees look for invest-ments that tend to be lower risk, with a steadyrate of return in many asset allocations. Theycould utilize a portion money invested in fixedincome, absolute return or possibly inflationhedges. Investing a portion of one of these assetallocations opens the door for community invest-ing and socially responsible investment policiesas a new strategy to gain a solid rate of return andwhile contributing to the overall well being oflower income communities throughout the state.These investments could be made in communitydevelopment financial institutions like the Michi-gan Housing Trust Fund, in community landtrusts, or various microenterprise programs.MSU could also invest in socially responsiblemutual funds with a community investment com-ponent like the Calvert Social Investment Fund,the Domini Social Equity Fund, or the New Al-ternative Fund. However, it is important to notethat investing in mutual funds does not have thesame impact as direct investments in communityinvestment vehicles like CDFIs, since only a verysmall portion of each dollar goes toward commu-nity investments within each mutual fund.

Regardless of the path that Michigan StateUniversity, the University of Michigan, or any ofthe other 13 public universities decide to pursueregarding investment decisions for their endow-ment funds, it is time for them to seriously con-sider investing in communities that need financialresources to flourish. The risk can be minimizedand the rate of return can be comparable to somecurrent investments; the impact community in-

15

endowment_study/; Internet; accessed 25 March2003.

Office of Development. 2001. University En-dowment Fund Profile [Document]. Ann Arbor,Michigan. University of Michigan.

Rysavy, Tracy Fernandez. 2002. Investing inCommunities [Document]. Washington, DC. SocialInvestment Forum Foundation and Co-op America.

Sandman, Lorilee R. 1996. Fulfilling HigherEducation’s Covenant with Society: The EmergingOutreach Agenda [on-line]. East Lansing, MI:Michigan State University; available from http://www.msu.edu/unit/outreach/pubs/capstone/;Internet; accessed 22 October 2002.

Schade, Mike. 2002. Socially Responsible In-vesting: a look at how students can challenge corpo-rate power. Available from http://wings.buffalo.edu/sa/uben/articles/sri.htm; Internet; accessed 15 Octo-ber 2002.

Shareholder Action Network. 2002. UnitingInvestors for Corporate Responsibility. Availablefrom http://www.shareholderaction.org; Internet;accessed 26 November 2002.

Social Investment Forum. 2002. Making Changewith Socially Responsible Investing. Available fromhttp://www.socialinvest.org/areas/general/investors/individuals.htm; Internet; accessed 14 November2002.

Social Investment Forum. 2002. Social Invest-ment Forum News. Available from http://www.socialinvest.org/areas/news; Internet; accessed12 December 2002.

Students Transforming and Resisting Corpora-tions (STARC). 2002. Socially Responsible Invest-ing Project Cluster. Available from http://www.starcalliance/sri/; Internet; accessed 29 October2002.

University of Michigan. 2001. Financial Report[Document]. Ann Arbor, Michigan. University ofMichigan.

Waddock, Sandra, and Samuel B. Graves. 2000.Performance characteristics of social and traditionalinvestments. Journal of Investing 9 (Summer): 27-38.

Witt, Peter A. 2000. If leisure research is tomatter II. Journal of Leisure Research 32:186-189.

article.cgi?sfArticleId=7_1; Internet; accessed 14November 2002.

Guerard Jr., John B. 1997. Additional evidenceon the cost of being socially responsible in investing.Journal of Investing (Winter): 31-36.

Guerard Jr., John B. 2002. Social Screening doesnot harm performance. Pensions and Investments, 16September, 30-1.

Hamilton, Sally, Hoje Jo, and Meir Statman.1993. Doing well while doing good? The investmentperformance of socially responsible mutual funds.Financial Analysts Journal, 49 (Nov/Dec) 62-68.

Higher Education Institutional Data Inventory(HEIDI). 2002. Michigan Public University Endow-ment Assets [Document]. Obtained from PresidentsCouncil State Universities of Michigan.

Katz, Bruce, and Evan Dobelle. 1999. HigherEducation: Cities’ Hidden Asset. The PhiladelphiaDaily News, 14 February.

Kinder, Peter D., Steven D. Lyndenberg, andAmy L. Domini. 1992. The Social Investment Alma-nac. New York: Henry Holt and Company Inc.

Kotval, Zenia. 2001. The Economic Impact ofAffordable Housing: Multifamily Housing in Massa-chusetts. New England Journal of Public Policy(Spring/Summer), 35-47.

London, Scott. 2002. The Civic Mission ofHigher Education: From Outreach to Engagement[on-line]. Washington, DC: Kettering Foundation;available from http://www.scottlondon.com/reports/seminar2001.pdf; Internet; accessed 15 October 2002.

Lyndenberg, Steven D. 2002. Envisioning So-cially Responsible Investing: A Model for 2006.Journal of Corporate Citizenship (October).

Michigan State University (MSU). 1982. FacultyHandbook: Introduction [on-line]. East Lansing, MI:Michigan State University; available from http://www.msu.edu/unit/facrecds/FacHand/mission.html;Internet; accessed 29 October 2002.

Michigan State University (MSU). 2003. State-ment of Investment Objectives and Investment Policy[Handbook]. East Lansing, MI: Michigan State Uni-versity.

Mitlo, Cindy, and David Berge. 2000. IncreasingInvestment in Communities: A Community InvestmentGuide for Investment Professionals and Institutions.Washington, DC: Social Investment Forum.

Most, Bruce W. 2002. Socially Responsible In-vesting: An Imperfect World for Planners and Clients.Journal of Financial Planning 15 (February): 48-54.

National Association of College and UniversityBusiness Officers (NACUBO). 2003. 2002 Endow-ment Study [on-line]. Washington, DC: available fromhttp://www.nacubo.org/accounting_finance/

16

17

Selected Web Resources on Community Investing

Calvert Group, Bethesda, MD, www.calvert.com

Calvert Foundation, Bethesda, MD, www.calvertfoundation.org

Community Development Venture Capital Alliance, New York, NY, www.cdvca.org

Domini Social Investments, Providence, RI, www.domini.com

National Community Capital Association, Philadelphia, PA, www.communitycapital.org

National Federation of Community Development Credit Unions, New York, NY, www.natfed.org

National Housing Trust Fund, Washington D.C., www.nhtf.org

Shore Bank, Chicgao, IL, www.sbk.com

Social Investment Forum, Washington D.C., www.socialinvest.org

Social Investment Forum Foundation, Washington D.C., www.communityinvest.org

SRI World Group, Inc., Brattleboro, VT, www.socialfunds.com

Students Transforming and Resisting Corporations, Portland, OR, www.starcalliance.org

18