Embed Size (px)

Citation preview

INVESTMENT BANKING AND CAPITAL MARKETS

Market Report—First Quarter 2005 Edition

New York, Frankfurt

May 31, 2005

THE BOSTON CONSULTING GROUP

TABLE OF CONTENTS

Chapter Page

Investment Banking Results First Quarter 2005

Impact of Rising U.S. Interest Rates on Global Fixed Income Revenues

Market Review

• Corporate Finance and Advisory

• Fixed-Income Trading

• Equity Trading

Data Definitions

2

10

18

25

30

36

-1-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Investment Banking Results First Quarter 2005

-2-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

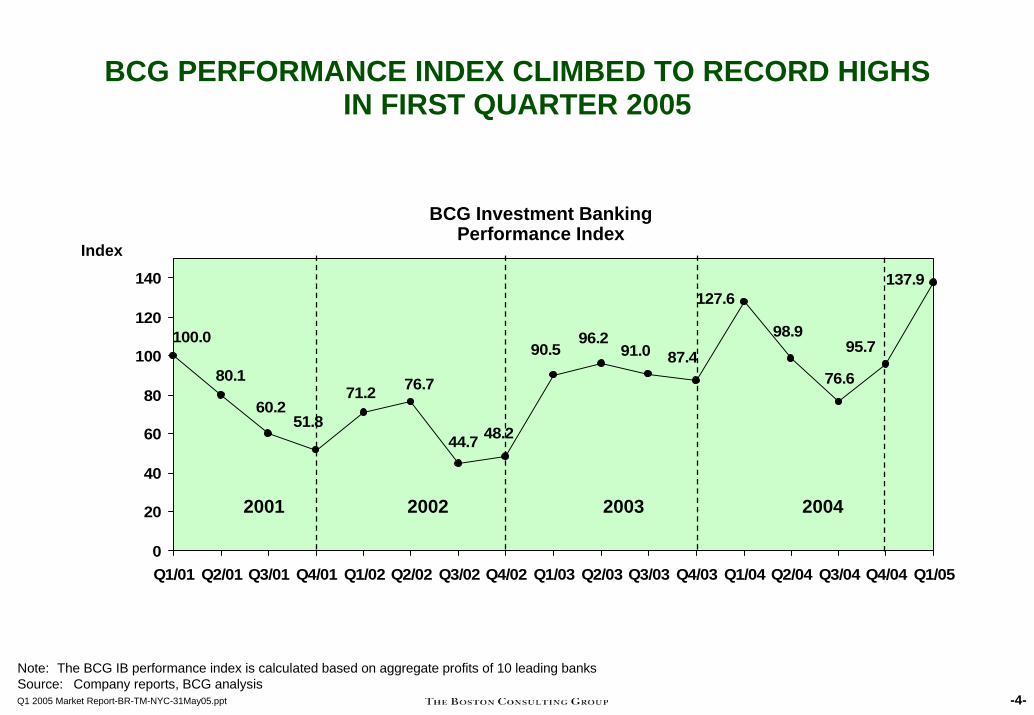

INVESTMENT BANKS HAD AN IMPRESSIVE FIRST QUARTER 2005

BCG performance index climbed over 40 points to a record high of 137 in first quarter 2005

Record earnings were driven by strong trading results while corporate finance and advisory business slowed down

• Trading revenues of ten leading banks increased by 43 percent on average from previous quarter

• Corporate finance and advisory businesses declined 9 percent

Fixed income trading results were especially impressive as they were achieved despite a flattening U.S. yield curve

• Fixed-income trading revenues grew by 54 percent compared to the previous quarter and by 15 percent compared to the strong first quarter 2004

• The spread between two-year and ten-year U.S. treasuries has declined by 54 percent since year-end 2004 and is currently at 50 basis points

• Average daily bond-trading volumes in the U.S. rose above $1 trillion for the first time

Profitability of the leading banks also improved from fourth quarter 2004 supported by the extraordinary trading results

• Pre-tax profit margins increased to 34.5 percent in first quarter 2005

-3-Q1 2005 Market Report-BR-TM-NYC-31May05.pptSource: Company reports, BCG analysis

BCG PERFORMANCE INDEX CLIMBED TO RECORD HIGHS IN FIRST QUARTER 2005

76.7

100.0

80.1

60.251.8

71.2

44.7 48.2

90.596.2

91.0 87.4

127.6

98.9

76.6

95.7

137.9

0

20

40

60

80

100

120

140

Q1/01 Q2/01 Q3/01 Q4/01 Q1/02 Q2/02 Q3/02 Q4/02 Q1/03 Q2/03 Q3/03 Q4/03 Q1/04 Q2/04 Q3/04 Q4/04 Q1/05

BCG Investment BankingPerformance Index

Index

2001 2002 2003 2004

-4-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Note: The BCG IB performance index is calculated based on aggregate profits of 10 leading banks Source: Company reports, BCG analysis

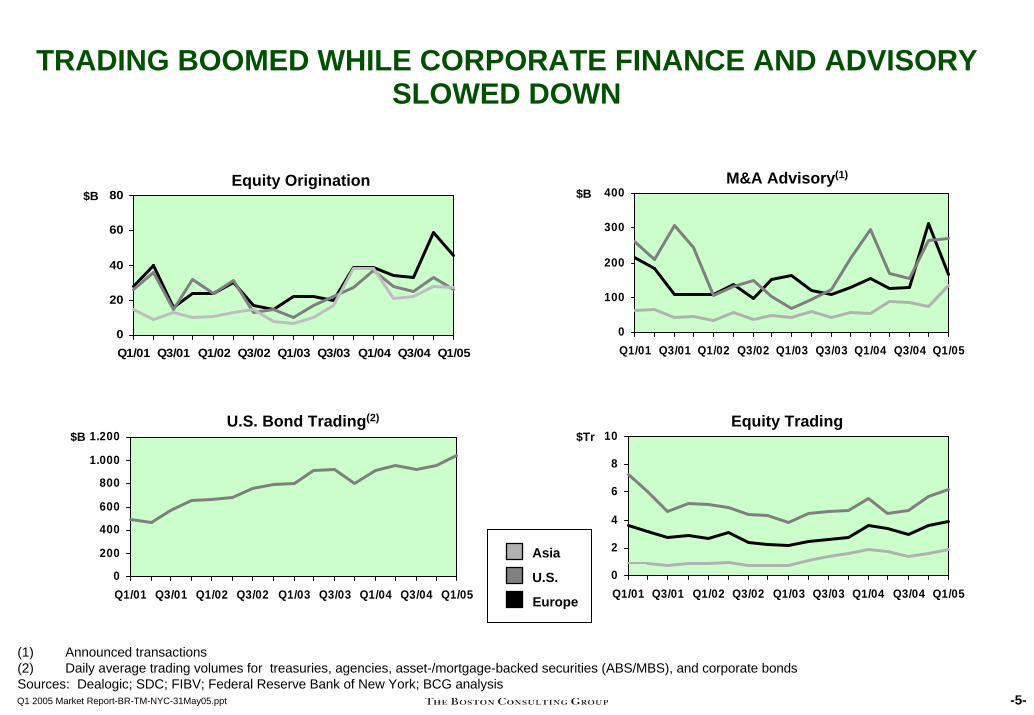

TRADING BOOMED WHILE CORPORATE FINANCE AND ADVISORY SLOWED DOWN

0

100

200

300

400

Q1/01 Q3/01 Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

M&A Advisory(1)

0

20

40

60

80

Q1/01 Q3/01 Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

$BEquity Origination

$B

0

2

4

6

8

10

Q1/01 Q3/01 Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/050

200

400

600

800

1.000

1.200

Q1/01 Q3/01 Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

$BU.S. Bond Trading(2)

$TrEquity Trading

U.S.

Asia

Europe

-5-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

(1) Announced transactions(2) Daily average trading volumes for treasuries, agencies, asset-/mortgage-backed securities (ABS/MBS), and corporate bondsSources: Dealogic; SDC; FIBV; Federal Reserve Bank of New York; BCG analysis

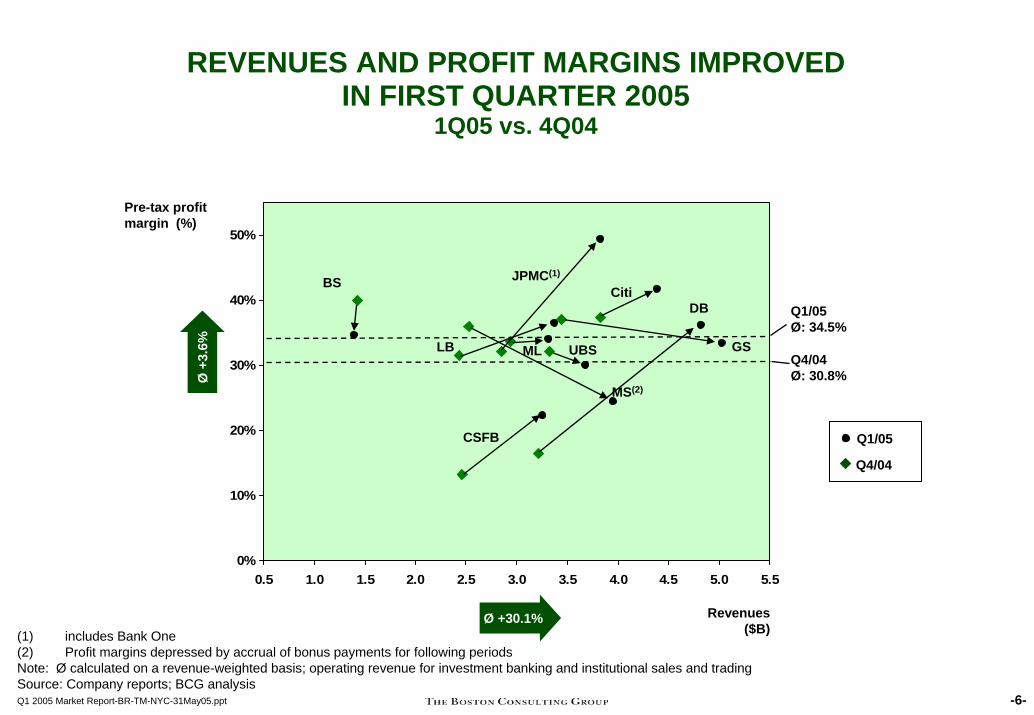

REVENUES AND PROFIT MARGINS IMPROVED IN FIRST QUARTER 2005

1Q05 vs. 4Q04

Pre-tax profit margin (%)

(1) includes Bank One(2) Profit margins depressed by accrual of bonus payments for following periodsNote: Ø calculated on a revenue-weighted basis; operating revenue for investment banking and institutional sales and tradingSource: Company reports; BCG analysis

Revenues($B)

Ø +30.1%

Ø+3

.6%

0%

10%

20%

30%

40%

50%

0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5

ML GS

MS(2)

CitiBS

DB

UBS

Q4/04

Q1/05

JPMC(1)

Q1/05 Ø: 34.5%

Q4/04 Ø: 30.8%

CSFB

LB

-6-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

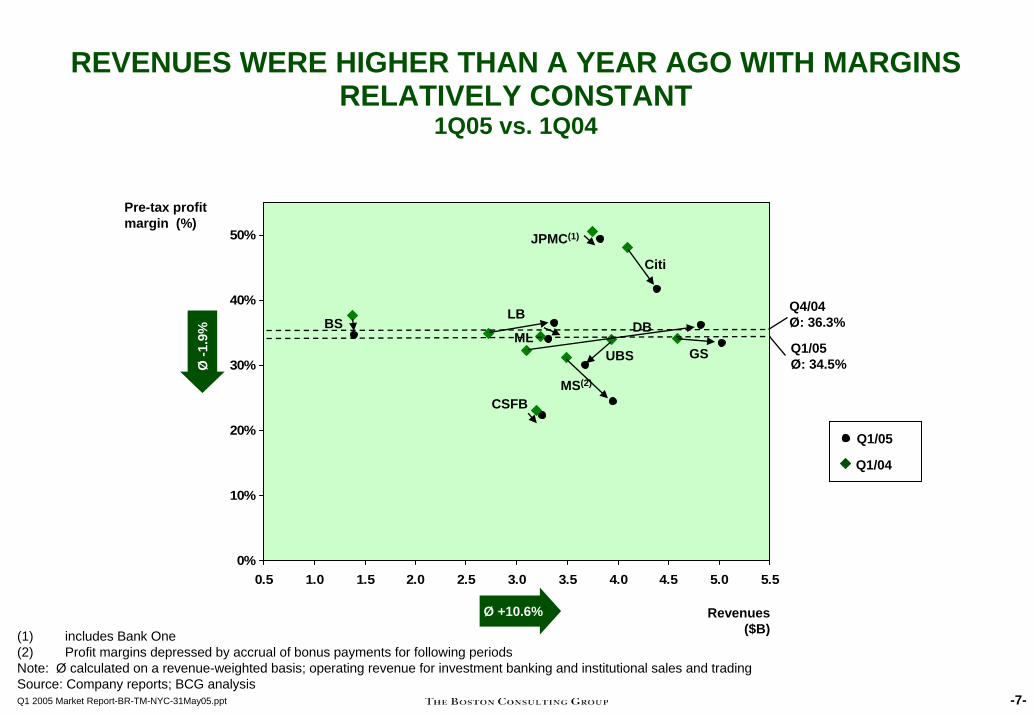

REVENUES WERE HIGHER THAN A YEAR AGO WITH MARGINS RELATIVELY CONSTANT

1Q05 vs. 1Q04

Pre-tax profit margin (%)

-7-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

(1) includes Bank One(2) Profit margins depressed by accrual of bonus payments for following periodsNote: Ø calculated on a revenue-weighted basis; operating revenue for investment banking and institutional sales and tradingSource: Company reports; BCG analysis

Revenues($B)

Ø +10.6%

Ø-1

.9%

0%

10%

20%

30%

40%

50%

0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5

MLGS

MS(2)

Citi

BS DB

UBS

Q1/04

Q1/05

JPMC(1)

Q1/05 Ø: 34.5%

Q4/04 Ø: 36.3%

CSFB

LB

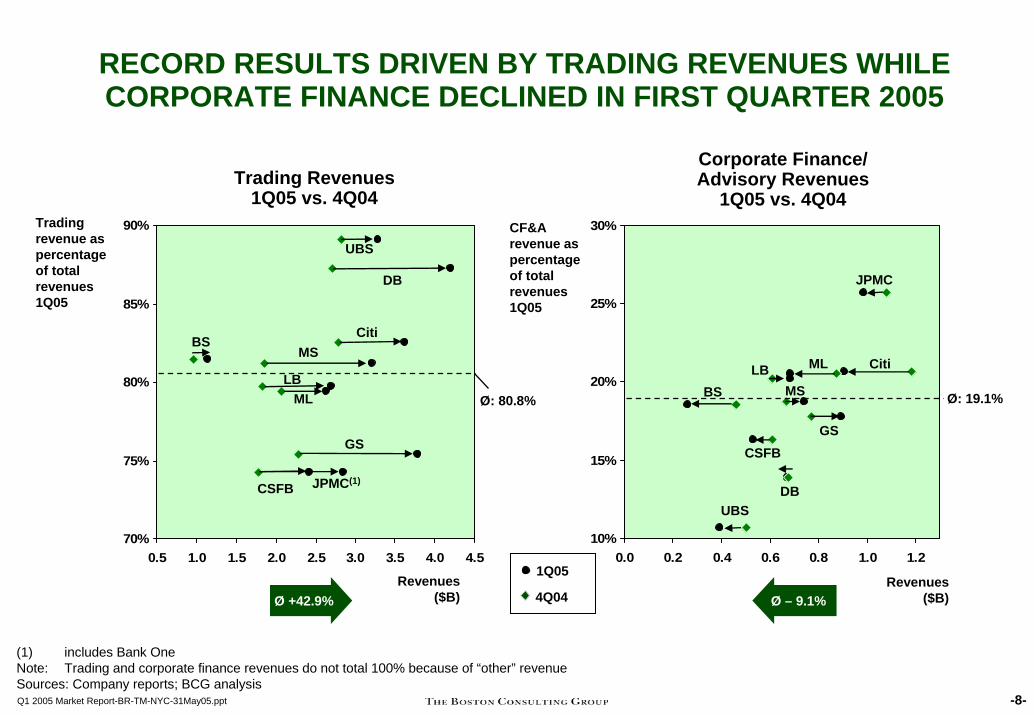

RECORD RESULTS DRIVEN BY TRADING REVENUES WHILE CORPORATE FINANCE DECLINED IN FIRST QUARTER 2005

70%

75%

80%

85%

90%

0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5

Trading Revenues1Q05 vs. 4Q04

4Q04

1Q05

10%

15%

20%

25%

30%

0.0 0.2 0.4 0.6 0.8 1.0 1.2

Corporate Finance/Advisory Revenues

1Q05 vs. 4Q04

MS

LB

Citi

GS

CF&A revenue aspercentageof totalrevenues1Q05

GS

LB Citi

MS

ML

JPMC

Revenues($B)

Revenues($B)

Tradingrevenue aspercentageof totalrevenues1Q05

Ø +42.9% Ø – 9.1%

ML

BS

BSØ: 80.8% Ø: 19.1%

JPMC(1)CSFB

DB

UBS

DBUBS

CSFB

-8-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

(1) includes Bank OneNote: Trading and corporate finance revenues do not total 100% because of “other” revenueSources: Company reports; BCG analysis

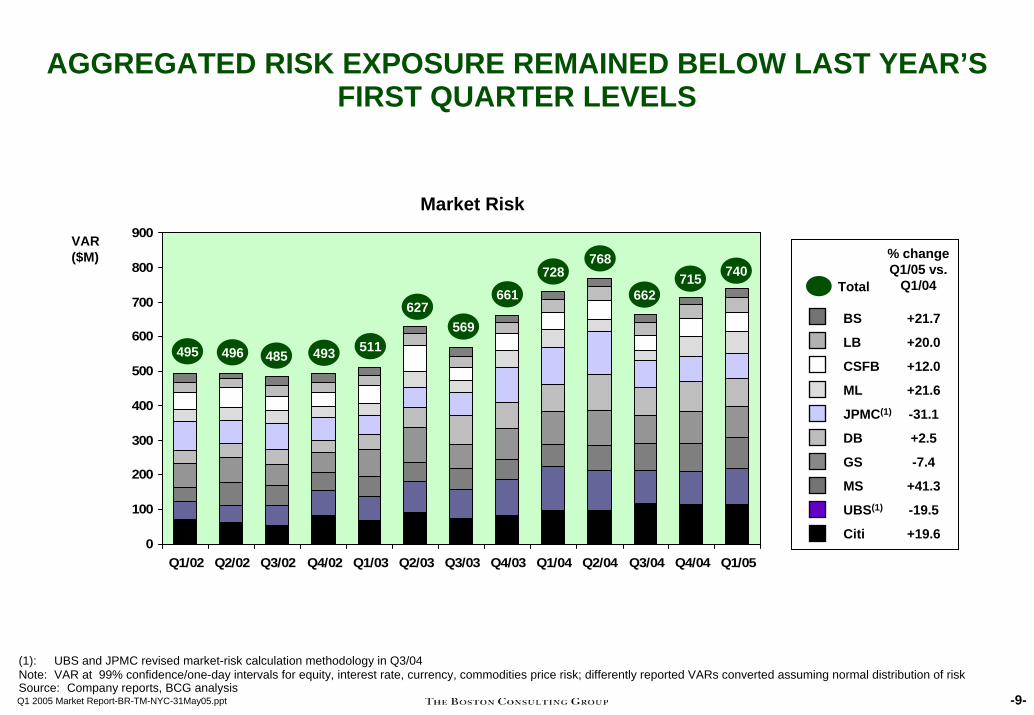

AGGREGATED RISK EXPOSURE REMAINED BELOW LAST YEAR’S FIRST QUARTER LEVELS

Market Risk

0

100

200

300

400

500

600

700

800

900

Q1/02 Q2/02 Q3/02 Q4/02 Q1/03 Q2/03 Q3/03 Q4/03 Q1/04 Q2/04 Q3/04 Q4/04 Q1/05

495 496 485 493 511

VAR($M)

Total

% changeQ1/05 vs.

Q1/04

BS

LB

CSFB

ML

JPMC(1)

DB

GS

MS

UBS(1)

Citi

+21.7

+20.0

+12.0

+21.6

-31.1

+2.5

-7.4

+41.3

-19.5

+19.6

661728

768

662715 740

627569

-9-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

(1): UBS and JPMC revised market-risk calculation methodology in Q3/04 Note: VAR at 99% confidence/one-day intervals for equity, interest rate, currency, commodities price risk; differently reported VARs converted assuming normal distribution of riskSource: Company reports, BCG analysis

Impact of Rising U.S. Interest Rates on Global Fixed Income Revenues

-10-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

IMPACT OF RISING INTEREST RATES LESS THAN GENERALLY EXPECTED

While rising interest rates affect several fixed-income businesses, the overall impact of rising rates in the U.S. is less than in previous interest rate cycles

• While fixed-income trading is still dominated by the U.S. debt markets, international markets have grown significantly and the U.S. investment banks have invested in their overseas trading operations. As a result, global fixed-income revenues are less dependent on U.S. interest rate moves than in previous rate cycles

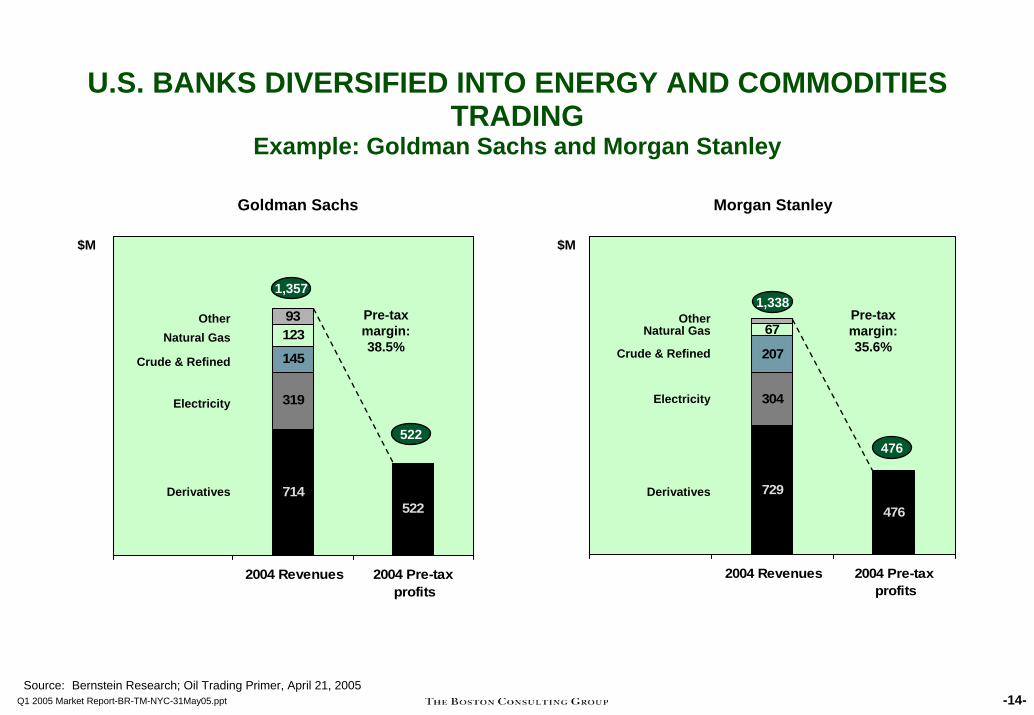

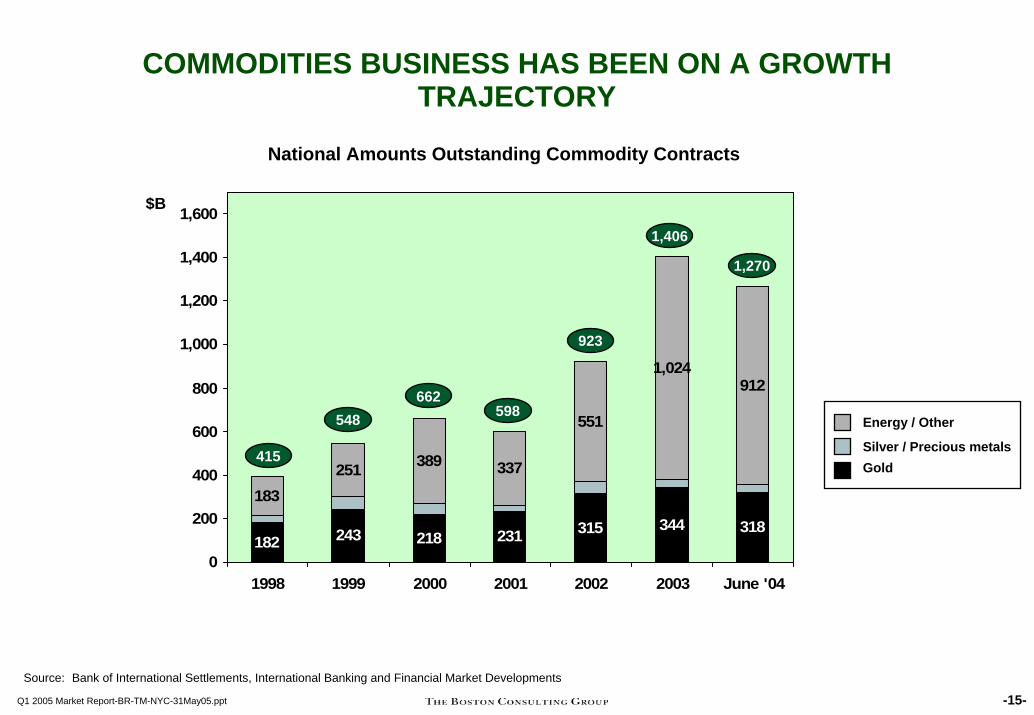

• Investment banks have diversified their trading activities in the last couple of years- Built and invested in energy and commodities trading businesses- Grew foreign exchange trading businesses

• Product innovation and a broader application of derivatives leaves banks less exposed to rising rates than in previous cycles

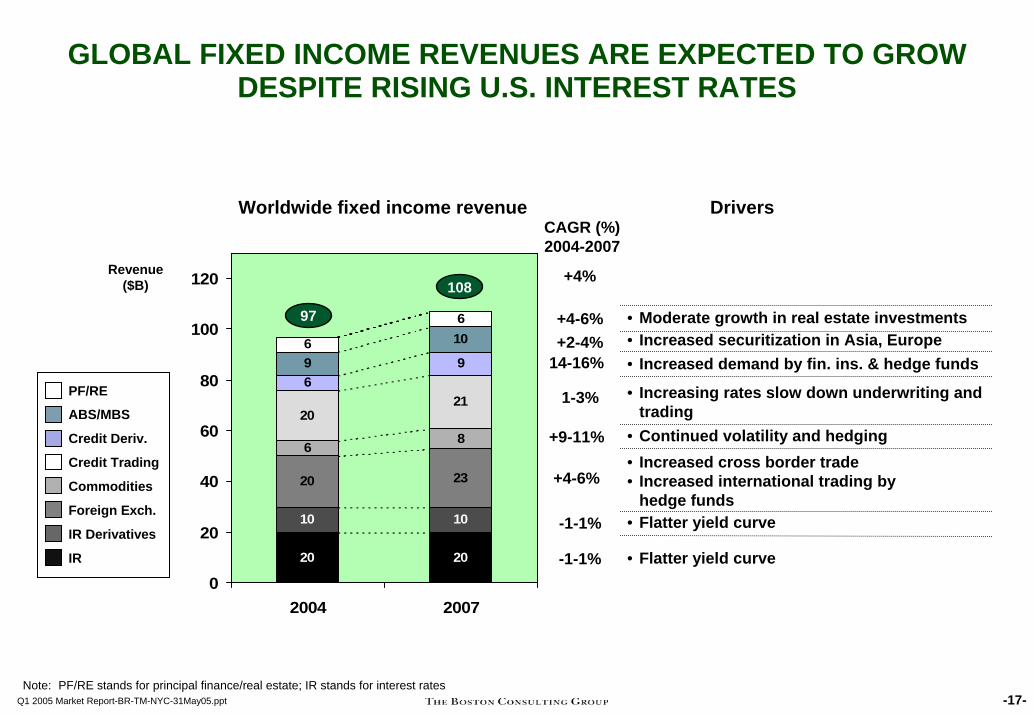

With only an estimated 25 percent of the global fixed-income revenues directly impacted by U.S. interest rate movements, we expect the global fixed-income business to continue to grow, albeit at a slower rate as over the last few years

• Global fixed-income revenues to grow by four percent p.a. until 2007

-11-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

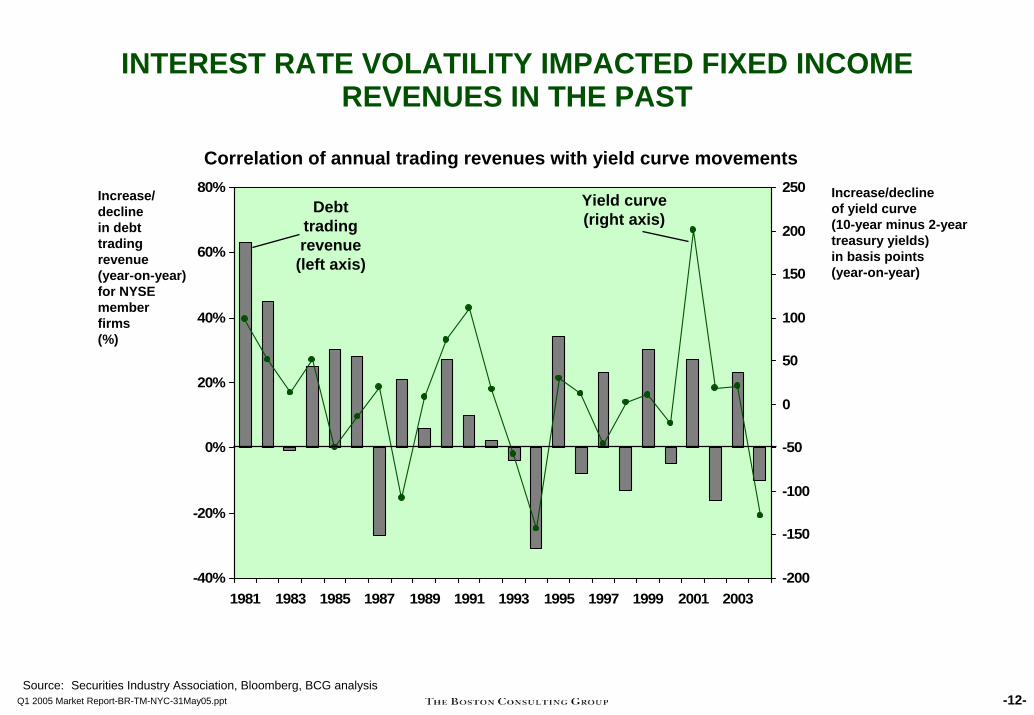

INTEREST RATE VOLATILITY IMPACTED FIXED INCOMEREVENUES IN THE PAST

-40%

-20%

0%

20%

40%

60%

80%

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003-200

-150

-100

-50

0

50

100

150

200

250Increase/declinein debttrading revenue(year-on-year) for NYSEmemberfirms(%)

Correlation of annual trading revenues with yield curve movements

Yield curve(right axis)

Increase/decline of yield curve (10-year minus 2-year treasury yields)in basis points(year-on-year)

Debttradingrevenue

(left axis)

-12-Q1 2005 Market Report-BR-TM-NYC-31May05.pptSource: Securities Industry Association, Bloomberg, BCG analysis

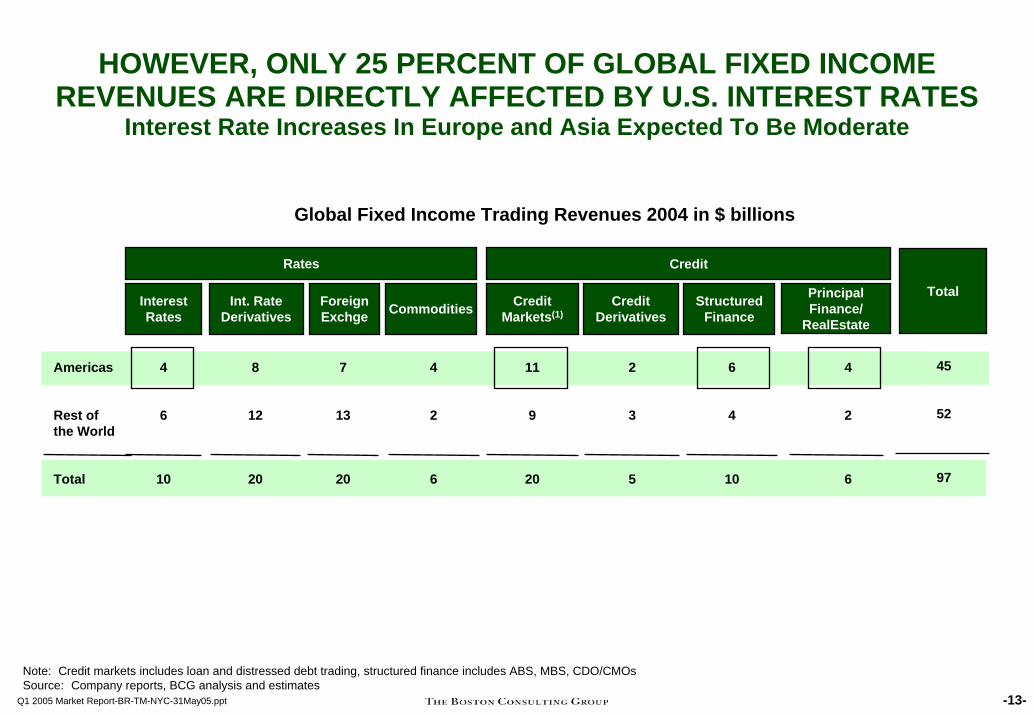

HOWEVER, ONLY 25 PERCENT OF GLOBAL FIXED INCOME REVENUES ARE DIRECTLY AFFECTED BY U.S. INTEREST RATES

Interest Rate Increases In Europe and Asia Expected To Be Moderate

Global Fixed Income Trading Revenues 2004 in $ billions

Rates

-13-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Americas

Rest of the World

Total

InterestRates

4

6

10

Int. Rate Derivatives

8

12

20

ForeignExchge

7

13

20

Commodities

4

2

6

Credit Markets(1)

11

9

20

Credit Derivatives

2

3

5

Structured Finance

Credit

Principal Finance/

RealEstate

Total

6

4

10

4

2

6

45

52

97

Note: Credit markets includes loan and distressed debt trading, structured finance includes ABS, MBS, CDO/CMOsSource: Company reports, BCG analysis and estimates

U.S. BANKS DIVERSIFIED INTO ENERGY AND COMMODITIES TRADING

Example: Goldman Sachs and Morgan Stanley

Goldman Sachs Morgan Stanley

$M

476

304

207

67

729

2004 Revenues 2004 Pre-taxprofits

$M

476

Pre-tax margin: 35.6%

OtherNatural Gas

Crude & Refined

Electricity

Derivatives

1,338

522

319

145

12393

714

2004 Revenues 2004 Pre-taxprofits

1,357

522

Pre-tax margin: 38.5%

OtherNatural Gas

Crude & Refined

Electricity

Derivatives

-14-Q1 2005 Market Report-BR-TM-NYC-31May05.pptSource: Bernstein Research; Oil Trading Primer, April 21, 2005

COMMODITIES BUSINESS HAS BEEN ON A GROWTH TRAJECTORY

National Amounts Outstanding Commodity Contracts

182 243 218 231 315 344 318

183251 389 337

551

1,024912

0

200

400

600

800

1,000

1,200

1,400

1,600

1998 1999 2000 2001 2002 2003 June '04

$B

415

548662

598

923

1,406

1,270

GoldSilver / Precious metals

Energy / Other

Source: Bank of International Settlements, International Banking and Financial Market Developments

-15-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

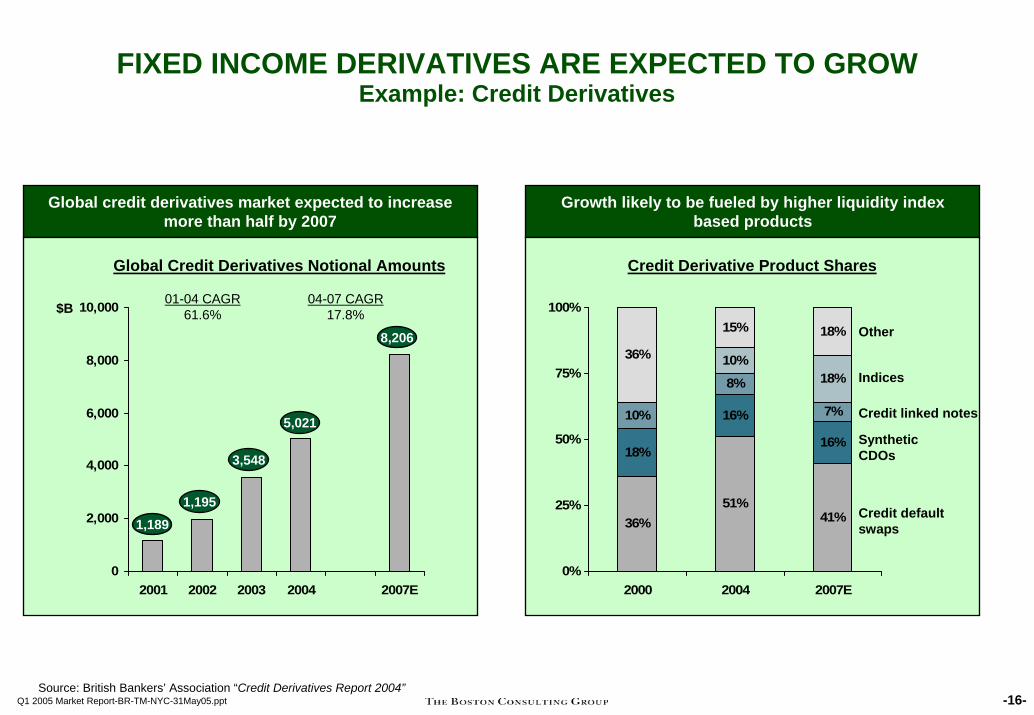

FIXED INCOME DERIVATIVES ARE EXPECTED TO GROWExample: Credit Derivatives

Global credit derivatives market expected to increase more than half by 2007

Growth likely to be fueled by higher liquidity index based products

Global Credit Derivatives Notional Amounts

-16-Q1 2005 Market Report-BR-TM-NYC-31May05.pptSource: British Bankers’ Association “Credit Derivatives Report 2004”

0

2,000

4,000

6,000

8,000

10,000

2001 2002 2003 2004 2007E

$B

36%51%

41%

18%

16%

16%

10%

8%

7%

10%18%

36%

15% 18%

0%

25%

50%

75%

100%

2000 2004 2007E

Credit default swaps

Synthetic CDOs

Credit linked notes

Indices

Other

Credit Derivative Product Shares

01-04 CAGR61.6%

04-07 CAGR17.8%

1,1891,195

3,548

5,021

8,206

GLOBAL FIXED INCOME REVENUES ARE EXPECTED TO GROW DESPITE RISING U.S. INTEREST RATES

20 20

10 10

20 23

68

2021

699

106

6

0

20

40

60

80

100

120

2004 2007

CAGR (%)2004-2007

-1-1%

-1-1%

14-16%

1-3%

+4-6%

Worldwide fixed income revenue

Revenue ($B)

IR

IR Derivatives

Foreign Exch.

Commodities

Credit Trading

Credit Deriv.

ABS/MBS

PF/RE

Drivers

• Flatter yield curve

• Flatter yield curve

• Increased cross border trade• Increased international trading by

hedge funds

• Continued volatility and hedging

• Moderate growth in real estate investments• Increased securitization in Asia, Europe+2-4%

• Increasing rates slow down underwriting and trading

• Increased demand by fin. ins. & hedge funds

97

108

+9-11%

+4-6%

+4%

-17-Q1 2005 Market Report-BR-TM-NYC-31May05.pptNote: PF/RE stands for principal finance/real estate; IR stands for interest rates

Market Review

Corporate Finance and Advisory

-18-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

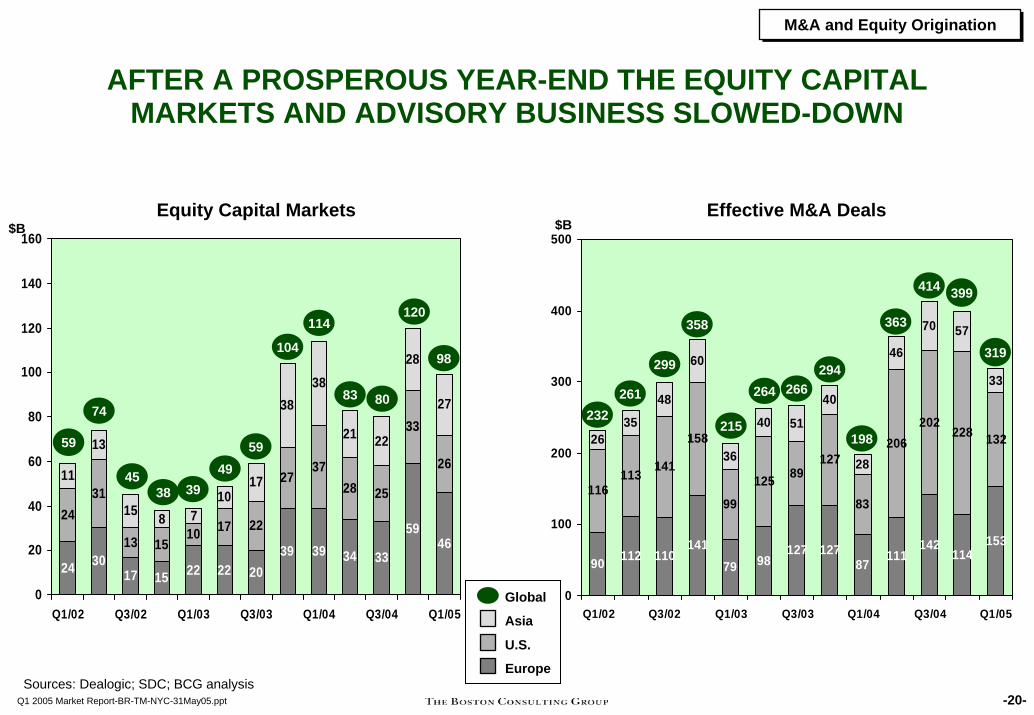

UNDERWRITING AND ADVISORY DEAL VOLUMES STARTED SUBDUED IN THE FIRST QUARTER 2005

Despite a 20 percent slowdown in global M&A in the first quarter 2005, momentum returned to the European market

• European M&A market grew by 34 percent compared to year-end 2004. The volume and business appears well-diversified across sectors and countries

The first quarter in equity underwriting is typically the weakest, but prospects for equity issuance are healthy

• Cautious stock markets led to a weak start in Europe and the U.S. Markets rose four percent in Europe and declined by three percent in the U.S.

• Privatizations will constitute a large proportion of the potential IPO pipeline

While overall global bond underwriting volumes grew a steady 7 percent in the first quarter, corporate bond issuance in the U.S. decreased by 27 percent

• Fixed income continues to play an important role for investment banks, as big revenue contributions come from fixed income

• While bond spreads have fallen sharply since 2002 and are near their lowest levels in years, they could widen further due to rising interest rates

-19-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

M&A and Equity OriginationM&A and Equity Origination

AFTER A PROSPEROUS YEAR-END THE EQUITY CAPITAL MARKETS AND ADVISORY BUSINESS SLOWED-DOWN

Equity Capital Markets

-20-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Sources: Dealogic; SDC; BCG analysis

24 3017 15 22 22 20

39 39 34 33

5946

2431

13 1510 17 22

2737

28 25

33

2611

13

15 8 710

17

3838

21 22

28

27

0

20

40

60

80

100

120

140

160

Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

$B

59

74

Global

U.S.

Asia

Europe

4538 39

Effective M&A Deals

90 112 110141

79 98127 127

87111

142114

153

116113 141

158

99

125 89127

83

206202

228 1322635

48

60

36

40 51

40

28

46

70 57

33

0

100

200

300

400

500

Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

$B

232

358

261

299

215

49

266

59

264

104294

114

198

83

363

80

414

120399

98 319

M&A and Equity OriginationM&A and Equity Origination

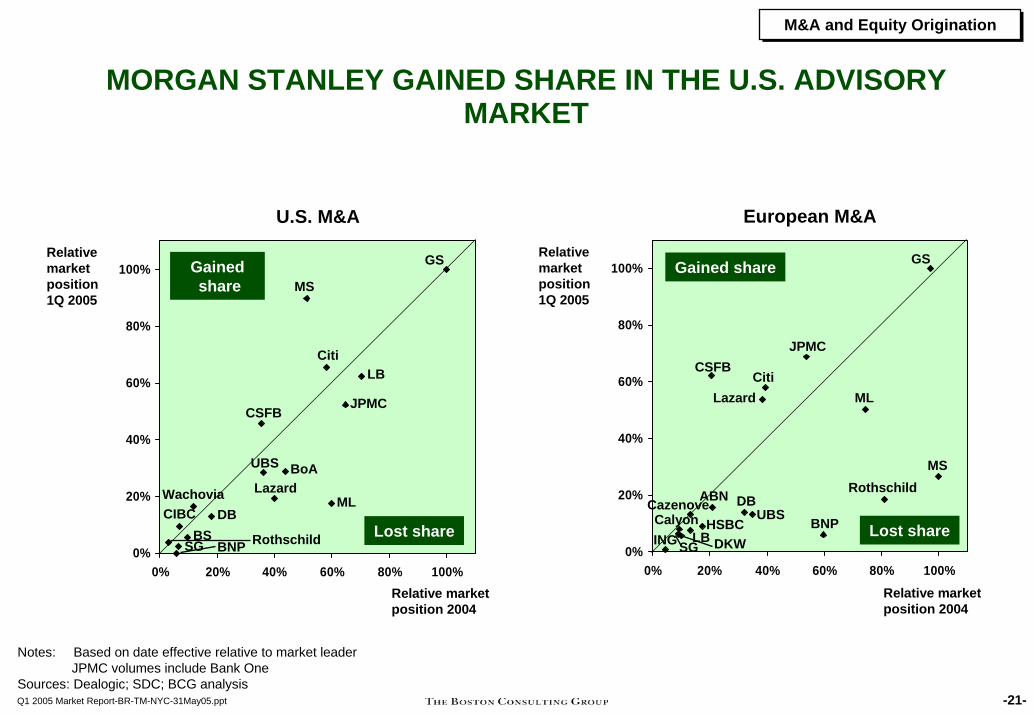

MORGAN STANLEY GAINED SHARE IN THE U.S. ADVISORY MARKET

-21-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

Gainedshare

Lost share

Gained share

Lost share

European M&A

BNP

ABN

GS

DB

CSFB

ML

MS

Citi

JPMC

UBS

Lazard

Calyon

Relative marketposition 2004

LBHSBC

U.S. M&A

Relativemarketposition1Q 2005

Relativemarketposition1Q 2005

GS

DB

CSFB

ML

MS

CitiLB

UBS

BS

Lazard

Relative marketposition 2004

BNP

BoA

JPMC

RothschildSG

WachoviaCIBC

RothschildCazenove

SG DKWING

Notes: Based on date effective relative to market leaderJPMC volumes include Bank One

Sources: Dealogic; SDC; BCG analysis

M&A and Equity OriginationM&A and Equity Origination

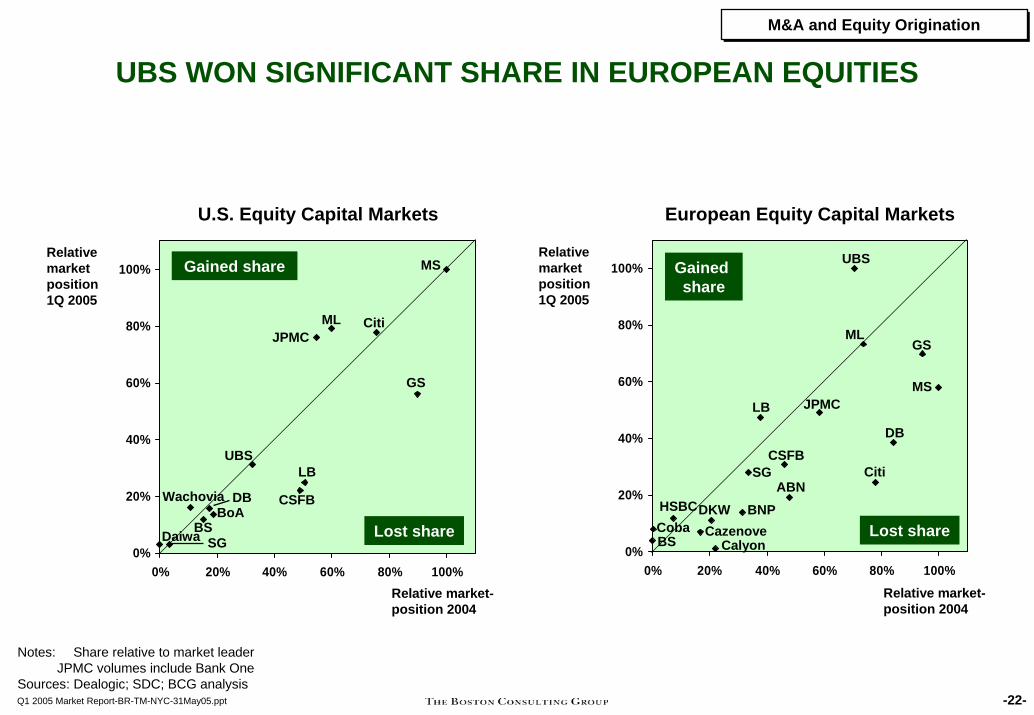

UBS WON SIGNIFICANT SHARE IN EUROPEAN EQUITIES

-22-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

Gained share

Lost share

U.S. Equity Capital Markets

Gained share

Lost share

European Equity Capital Markets

ABNHSBC

GS

DBCSFB

ML

MS

Citi

JPMC

UBS

BNPCazenove

Relative market-position 2004

CobaDKW

LB

SG

Relativemarketposition1Q 2005

Relativemarketposition1Q 2005

GS

DB CSFB

ML

MS

CitiJPMC

LBUBS

BSBoA

Relative market-position 2004

Wachovia

Notes: Share relative to market leaderJPMC volumes include Bank One

Sources: Dealogic; SDC; BCG analysis

SGDaiwa CalyonBS

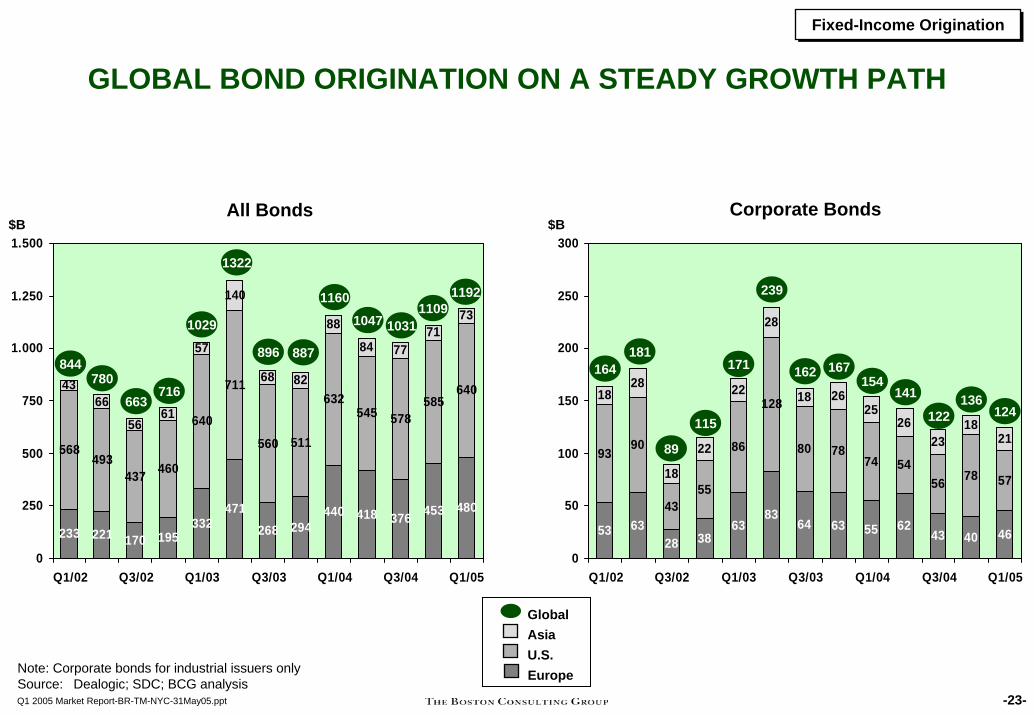

Fixed-Income OriginationFixed-Income Origination

GLOBAL BOND ORIGINATION ON A STEADY GROWTH PATH

Corporate BondsAll Bonds

233 221 170 195332

471268 294

440 418 376 453 480

568493

437 460

640

711

560 511

632545 578

58564043

66

5661

57

140

68 82

88

84 7771

73

0

250

500

750

1.000

1.250

1.500

Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

$B

844780

663716

1029

53 6328 38

6383

64 63 55 6243 40 46

9390

4355

86

128

80 7874 54

56 78 57

1828

18

22

22

28

18 2625

2623

1821

0

50

100

150

200

250

300

Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

$B

164181

89

115

171

1322

239

887167

896162

1160

154

1047

141

1031

122

1109

136

1192

124

Global

U.S.Asia

Europe

-23-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Note: Corporate bonds for industrial issuers onlySource: Dealogic; SDC; BCG analysis

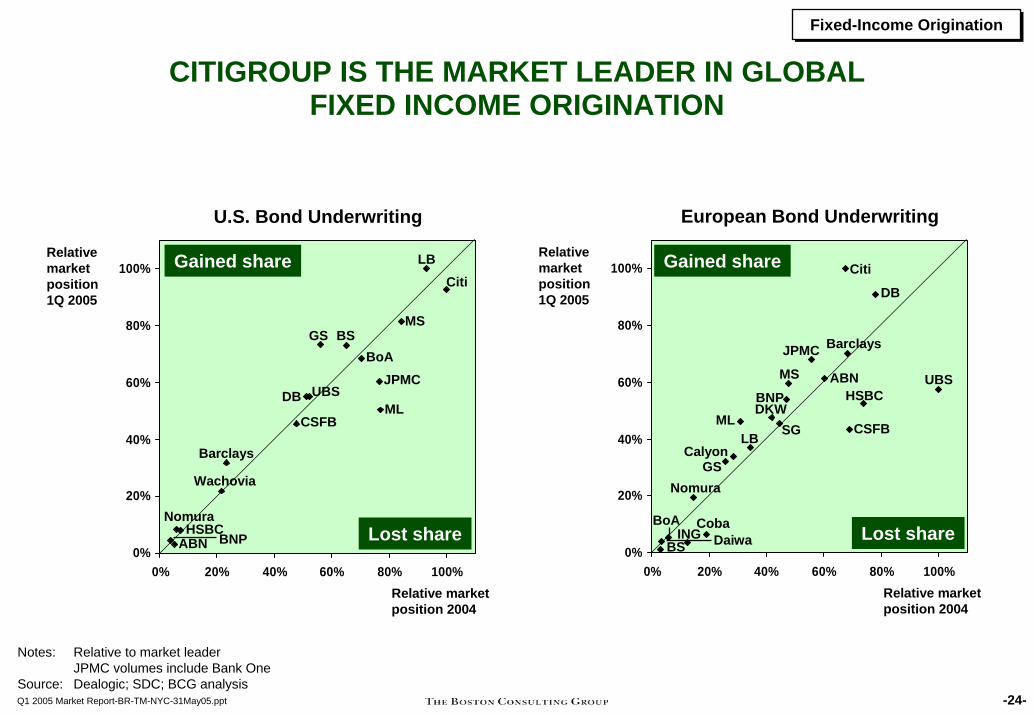

Fixed-Income OriginationFixed-Income Origination

CITIGROUP IS THE MARKET LEADER IN GLOBAL FIXED INCOME ORIGINATION

European Bond Underwriting

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%Relative marketposition 2004

BNPABN

U.S. Bond Underwriting

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%Relative marketposition 2004

Relativemarketposition1Q 2005

Relativemarketposition1Q 2005

Gained share

Lost share

-24-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Notes: Relative to market leaderJPMC volumes include Bank One

Source: Dealogic; SDC; BCG analysis

HSBC

SG

Barclays

Gained share

Lost share

DB

CSFB

ING

MS

Citi

DKW

JPMC

LB

UBS

BoA

GS

ML

Coba

Calyon

Nomura

BS

Barclays

GS

DB

CSFBML

MS

Citi

JPMC

LB

UBS

BS

Wachovia

BoA

NomuraBNP

HSBCABN Daiwa

Market Review

Fixed-Income Trading

-25-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Fixed-Income TradingFixed-Income Trading

FIXED-INCOME SALES & TRADING REVENUES REACHED QUARTERLY RECORD

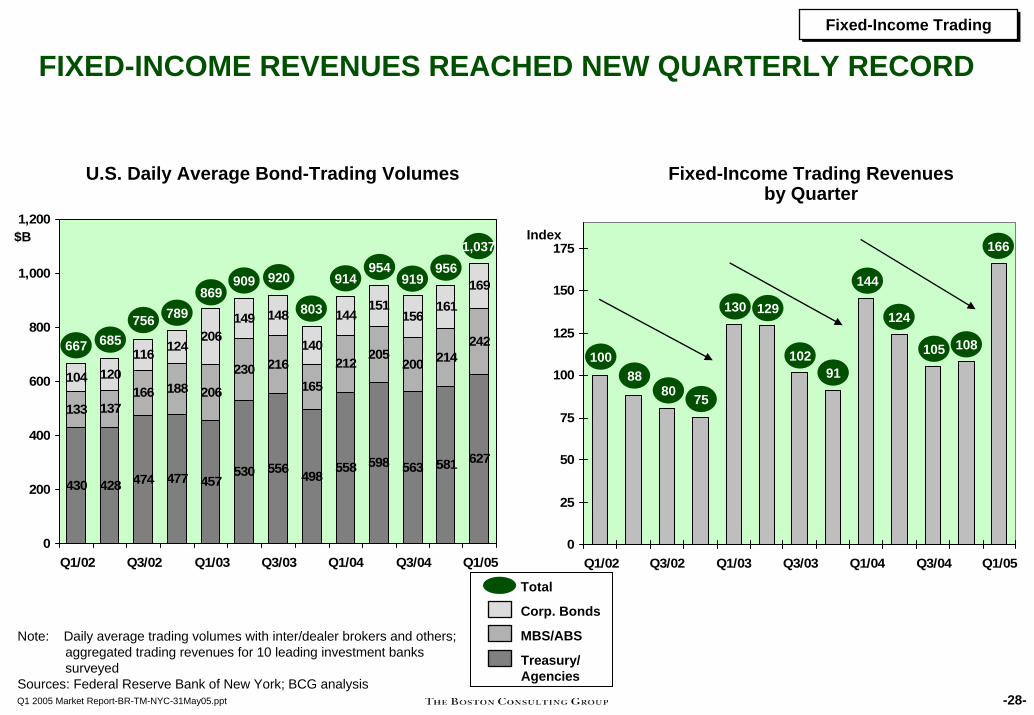

Investment banks achieved record revenues in fixed-income trading• Revenues grew by 54% compared to the previous quarter and were still 15% higher

compared to the strong first quarter 2004

U.S. bond trading activity reached a new quarterly high• Average daily bond-trading volumes rose above the $1 trillion for the first time in the

first quarter 2005

Results were especially impressive as they were achieved despite a flattening U.S. yield curve• The spread between two-year and ten-year U.S. treasuries has declined by 54 percent

since year-end 2004 and is currently at merely 50 basis points

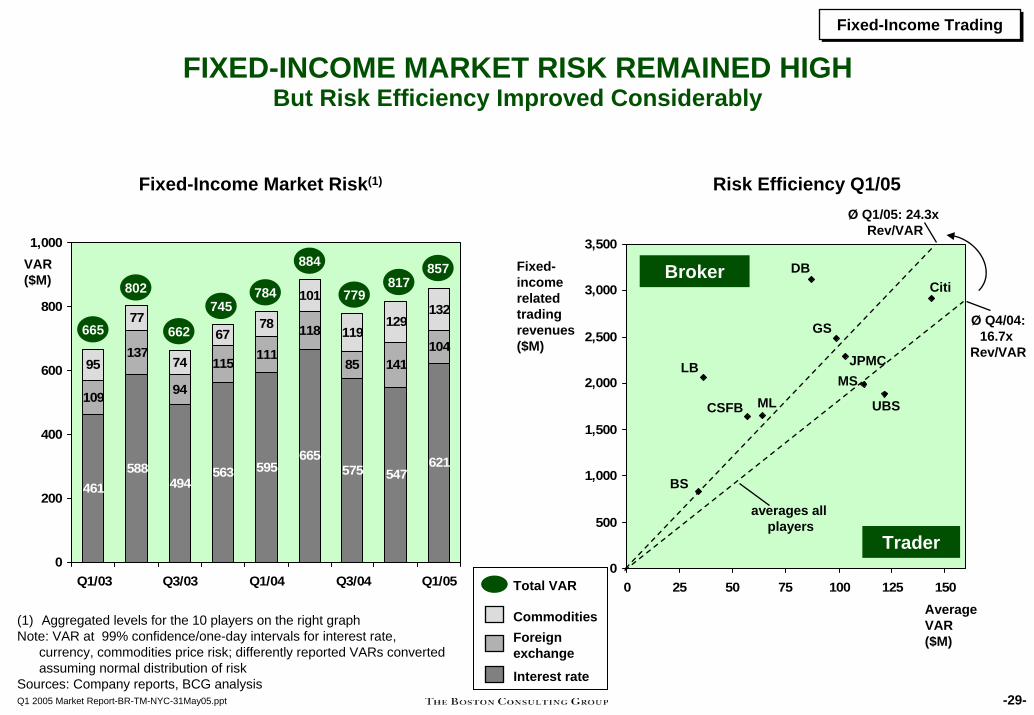

Risk efficiency has improved considerably• Banks earned 46 percent more revenue at a given level of value-at-risk than in 4th

quarter 2004

Even if debt related business slows down in the subsequent quarters, 2005 will most likely be a very good year in fixed income

-26-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Fixed-Income TradingFixed-Income Trading

YIELD CURVE FLATTENED

10-year/2-year U.S. Treasury Yield Spread

-100

-50

0

50

100

150

200

250

300

Jan 97 Jan 98 Jan 99 Dez 99 Dez 00 Dez 01 Dez 02 Dez 03 Dez 04

Basispoints

-27-Q1 2005 Market Report-BR-TM-NYC-31May05.pptSource: Bloomberg

Fixed-Income TradingFixed-Income Trading

FIXED-INCOME REVENUES REACHED NEW QUARTERLY RECORD

U.S. Daily Average Bond-Trading Volumes Fixed-Income Trading Revenues by Quarter

0

25

50

75

100

125

150

175

Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

10088

102

130

80 75

129

91

Index

144

124

430 428 474 477 457530 556 498 558 598 563 581 627

133 137166 188 206

230 216165

212 205200 214

242

104 120116 124

206149 148

140

144151

156161

169

0

200

400

600

800

1,000

1,200

Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

$B

667 685756 789

869909

803

920 914954

919

105

956

108

1661,037

Total

MBS/ABS

Corp. Bonds

Treasury/Agencies

-28-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Note: Daily average trading volumes with inter/dealer brokers and others; aggregated trading revenues for 10 leading investment bankssurveyed

Sources: Federal Reserve Bank of New York; BCG analysis

Fixed-Income TradingFixed-Income Trading

FIXED-INCOME MARKET RISK REMAINED HIGHBut Risk Efficiency Improved Considerably

Fixed-Income Market Risk(1) Risk Efficiency Q1/05

461563 595

665575 547

621

115 111

118

85 141104

7767

78

101

119129

132

494588

109 94

1377495

0

200

400

600

800

1,000

Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

665

Total VAR

Foreign exchange

Commodities

Interest rate

802

VAR($M)

Fixed-incomerelatedtradingrevenues($M)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0 25 50 75 100 125 150AverageVAR ($M)

Broker

Trader

JPMCMS

DBCiti

GS

UBSCSFB ML

LB

BS

Ø Q4/04:16.7x

Rev/VAR662

745784

884

Ø Q1/05: 24.3x Rev/VAR

averages all players

779817

857

-29-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

(1) Aggregated levels for the 10 players on the right graph Note: VAR at 99% confidence/one-day intervals for interest rate,

currency, commodities price risk; differently reported VARs convertedassuming normal distribution of risk

Sources: Company reports, BCG analysis

Market Review

Equity Trading

-30-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Equity TradingEquity Trading

EQUITIES TRADING REVENUES RECOVERED SIGNIFICANTLY

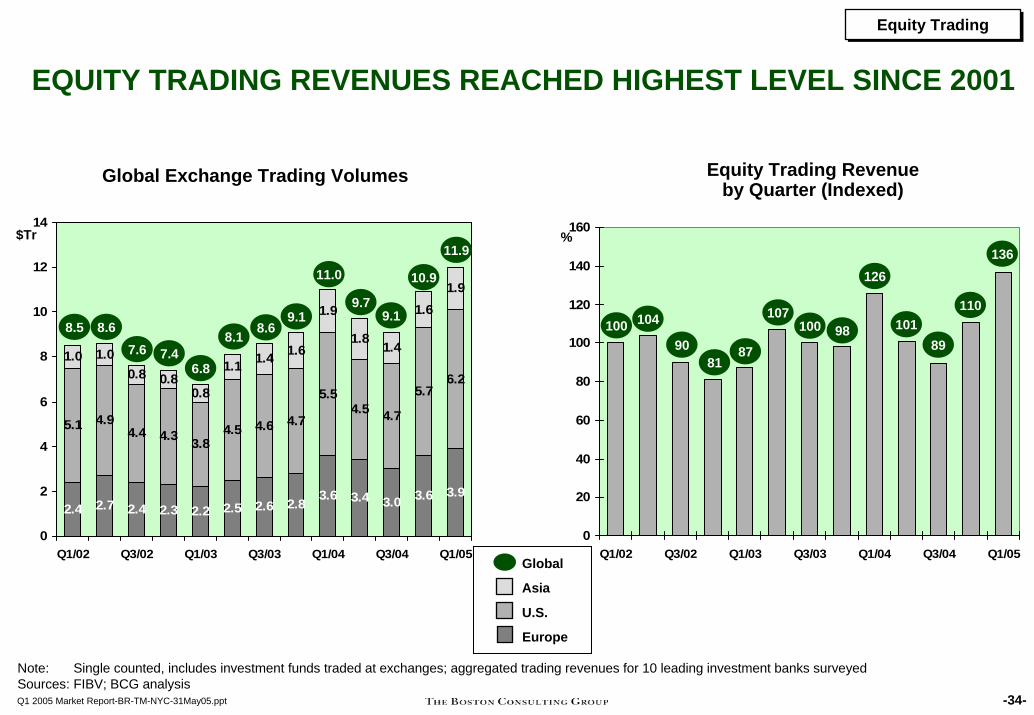

Global investment banks had best quarter in equity trading since 2001• Aggregated trading revenues increased by 24 percent from fourth quarter 2004 and

finished 36 percent higher than in the beginning of 2002

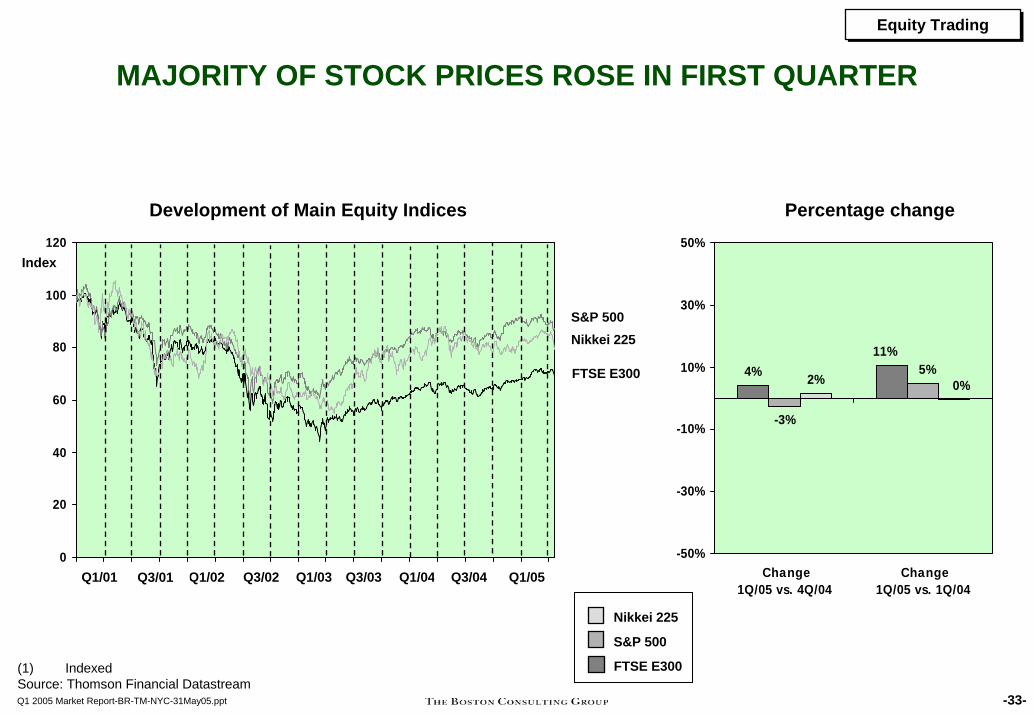

Several reasons were responsible for the upswing• Stock prices rose broadly except in the U.S.: European share prices increased by four

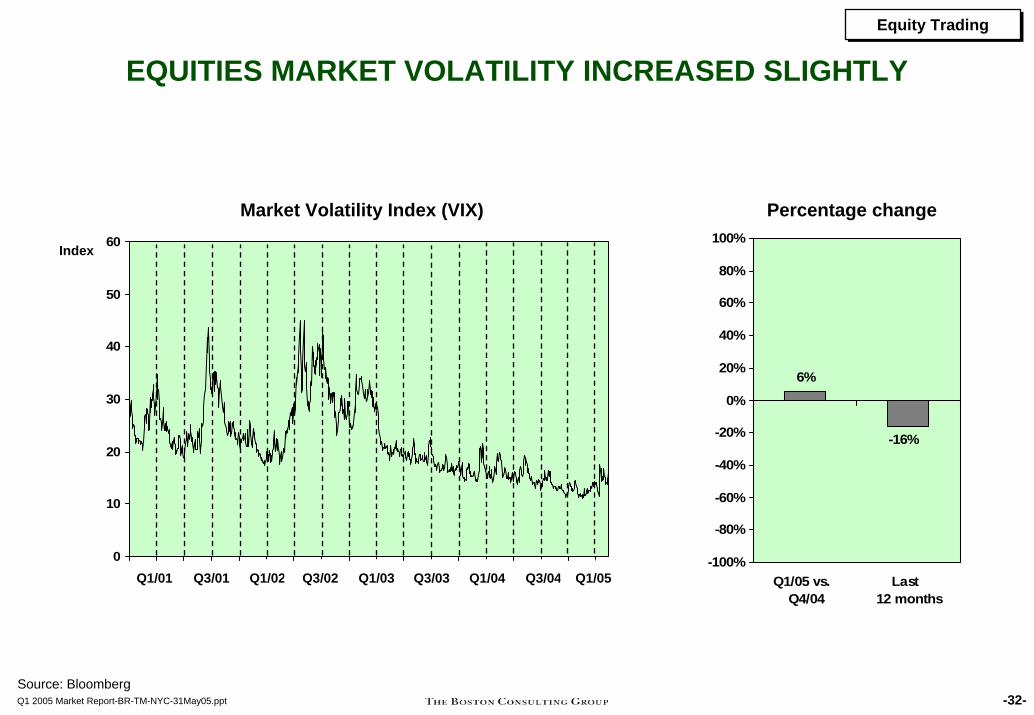

percent while the Japanese Nikkei was up two percent for the quarter• Market volatility increased for the first time since the first quarter 2003. The VIX (Volatility

Index) increased six percent from end of 2004• Continued growth in prime brokerage revenues from servicing hedge funds

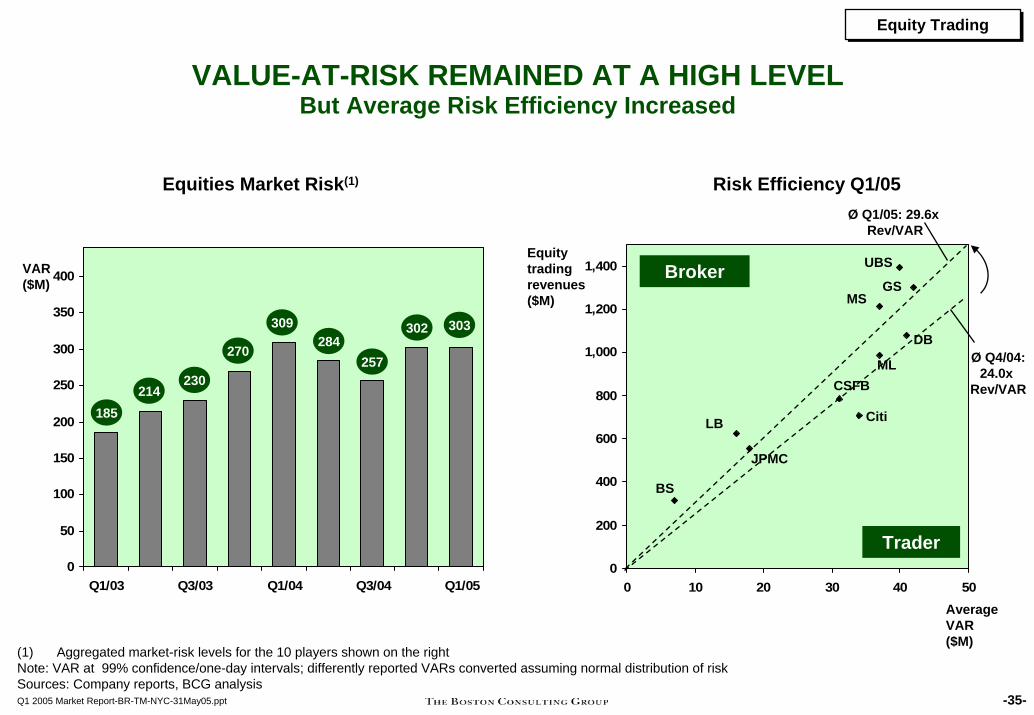

Equity market risks remained at a high level while banks improved their risk efficiency considerably• Aggregated value-at-risk of the leading banks remained unchanged• However, banks earned $5.60 more per dollar value-at-risk

-31-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Equity TradingEquity Trading

EQUITIES MARKET VOLATILITY INCREASED SLIGHTLY

Market Volatility Index (VIX) Percentage change

6%

-16%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Q1/05 vs. Q4/04

Last 12 months

0

10

20

30

40

50

60

J A J O J A J O J A J O J A J O J A

-32-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Source: Bloomberg

Q1/02Q3/01 Q3/02 Q1/03Q1/01 Q3/03 Q1/04 Q3/04 Q1/05

Index

Equity TradingEquity Trading

MAJORITY OF STOCK PRICES ROSE IN FIRST QUARTER

Development of Main Equity Indices Percentage change

0

20

40

60

80

100

120

J A J O J A J O J A J O J A J O J A

Nikkei 225 S&P 500

FTSE E300

Q1/02

-33-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

(1) Indexed Source: Thomson Financial Datastream

S&P 500

Nikkei 225

FTSE E300

Q3/01 Q3/02 Q1/03Q1/01 Q3/03

Index

Q1/04

4%

-3%

2%

11%5%

0%

-50%

-30%

-10%

10%

30%

50%

Change 1Q/05 vs. 4Q/04

Change 1Q/05 vs. 1Q/04

Q3/04 Q1/05

Equity TradingEquity Trading

EQUITY TRADING REVENUES REACHED HIGHEST LEVEL SINCE 2001

Global Exchange Trading Volumes

Global

U.S.

Asia

Europe

2.4 2.7 2.4 2.3 2.2 2.5 2.6 2.8 3.6 3.4 3.0 3.6 3.9

5.1 4.94.4 4.3 3.8

4.5 4.6 4.7

5.54.5 4.7

5.76.2

1.0 1.00.8 0.8

0.8

1.1 1.4 1.6

1.9

1.8 1.4

1.61.9

0

2

4

6

8

10

12

14

Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

$Tr

8.5 8.67.6 7.4

6.8

8.1 8.69.1

Equity Trading Revenue by Quarter (Indexed)

0

20

40

60

80

100

120

140

160

Q1/02 Q3/02 Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

%

100 104

9081

87

107100 98

126

101

11.0

9.79.1

89

10.9

110

11.9 136

-34-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

Note: Single counted, includes investment funds traded at exchanges; aggregated trading revenues for 10 leading investment banks surveyedSources: FIBV; BCG analysis

Equity TradingEquity Trading

VALUE-AT-RISK REMAINED AT A HIGH LEVELBut Average Risk Efficiency Increased

Equities Market Risk(1) Risk Efficiency Q1/05

-35-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

0

50

100

150

200

250

300

350

400

Q1/03 Q3/03 Q1/04 Q3/04 Q1/05

302

185214

VAR($M)

(1) Aggregated market-risk levels for the 10 players shown on the rightNote: VAR at 99% confidence/one-day intervals; differently reported VARs converted assuming normal distribution of riskSources: Company reports, BCG analysis

Equitytradingrevenues($M)

0

200

400

600

800

1,000

1,200

1,400

0 10 20 30 40 50AverageVAR ($M)

Broker

Trader

JPMC

MS

DB

Citi

GS

UBS

CSFBML

LB

BS

Ø Q4/04:24.0x

Rev/VAR

Ø Q1/05: 29.6x Rev/VAR

230

270

309284

303

257

Data Definitions

-36-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt

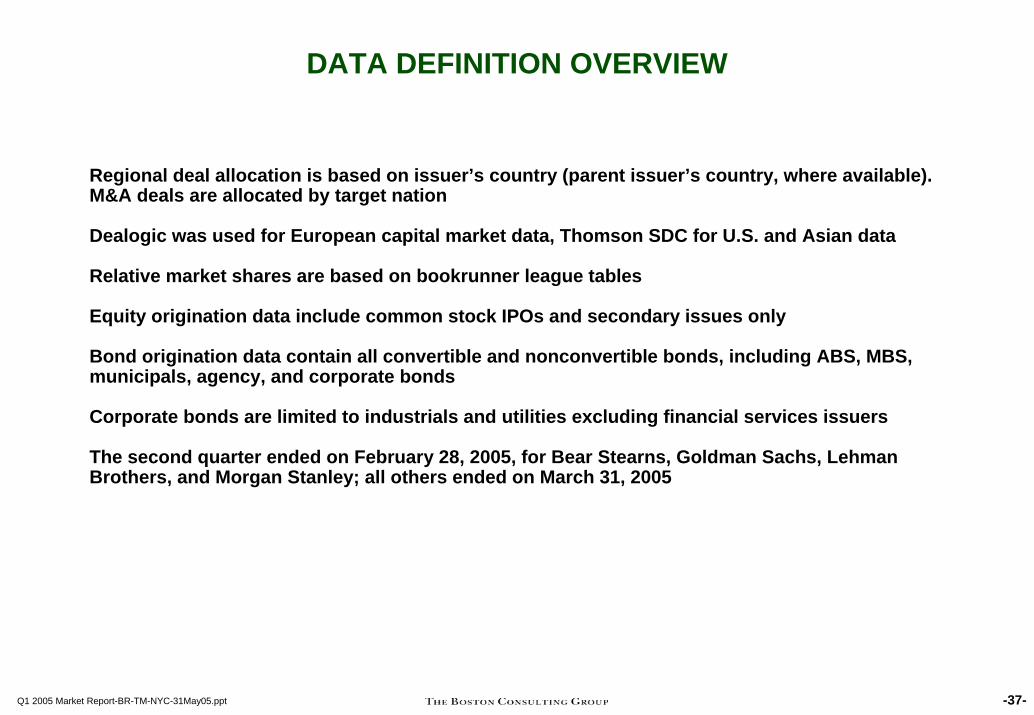

DATA DEFINITION OVERVIEW

Regional deal allocation is based on issuer’s country (parent issuer’s country, where available). M&A deals are allocated by target nation

Dealogic was used for European capital market data, Thomson SDC for U.S. and Asian data

Relative market shares are based on bookrunner league tables

Equity origination data include common stock IPOs and secondary issues only

Bond origination data contain all convertible and nonconvertible bonds, including ABS, MBS, municipals, agency, and corporate bonds

Corporate bonds are limited to industrials and utilities excluding financial services issuers

The second quarter ended on February 28, 2005, for Bear Stearns, Goldman Sachs, Lehman Brothers, and Morgan Stanley; all others ended on March 31, 2005

-37-Q1 2005 Market Report-BR-TM-NYC-31May05.ppt