Embed Size (px)

Citation preview

1 Letter from CEO

2 Global Macro Outlook

By Michael Hasenstab, Ph.D. Chief Investment Officer Templeton Global Macro

7 Global Equity Outlook

By Edward D. Perks, CFA Chief Investment Officer Franklin Templeton Equity

12 Long-Term Capital Markets Outlook By Rick Frisbie

Head of Franklin Templeton Solutions Franklin Templeton Investments

14 More Investment Insights Online

WHAT’S INSIDE

Gregory E. Johnson

Chairman of the Board, Chief Executive Officer

Franklin Resources, Inc.

With thirty years of investment management experience, I have come to know rapid evolution and change are

constants. It’s a dynamic time in our industry and the financial markets in general, and I see many reasons for

continued optimism. It’s times like these when professional, active management matters most.

The pages that follow spotlight our highest level views from the senior leaders of three key areas central to many

investors’ portfolio decisions: the global macro environment, global equities and multi-strategy solutions.

Michael Hasenstab, Ph.D. – As CIO of Templeton Global Macro, Michael leads a team of economists,

trained in some of the leading universities in the world, who integrate global macroeconomic analysis with

in-depth country research to identify long-term imbalances that translate to investment opportunities.

Michael and his team manage Templeton global bond strategies, including unconstrained fixed income,

currency and global macro.

Ed Perks, CFA – Ed recently assumed an expanded role, overseeing our well-established equity teams

that include Franklin Equity Group, Templeton Global Equity Group, Templeton Emerging Markets Group,

Franklin Mutual Series and Franklin U.S. Value. Our equity teams continue to manage their own bottom-up

research. By sharing perspectives across teams embedded in several key equity markets, they can

strengthen their overall convictions.

Rick Frisbie – Rick heads Franklin Templeton (FT) Solutions, our group dedicated to multi-strategy

solutions. Every year, FT Solutions reviews the data and themes driving capital markets in order to build

asset return expectations for different asset classes for the next five to 10 years. The team incorporates

these expectations into their long-term portfolio positioning process.

The diversity of our perspectives, honed over nearly seven decades, enables us to say, “Gain from Our Perspective.”

While we can’t predict what the markets hold for 2016, we do hope the insights we’ve prepared will be valuable to

you as an investor to help you make important decisions about your portfolio to navigate the changing market

dynamics.

On behalf of the firm’s more than 9,000 employees around the world, I’d like to thank you for the trust you place in us

and extend my very best wishes for a happy and prosperous 2016.

Greg Johnson

January 2016

2016 INVESTMENT OUTLOOK | 1

Rising Interest Rates from the Fed and Additional Quantitative Easing from the BOJ and ECB Overall, we remain confident in the

economic outlook for the United States and

continue to expect rising interest rates from

the US Federal Reserve (Fed). Labor

conditions in the United States have been

strong while wages and earnings have

increased, which we believe will continue to

drive consumption. In our assessment,

global financial markets are poised to

benefit from the US economic expansion.

We also anticipate significant divergences

in monetary policies around the world in

2016; we expect the Fed to tighten policy

while the Bank of Japan (BOJ) and

European Central Bank (ECB) continue to

expand monetary accommodation through

quantitative easing (QE). The BOJ has

indicated that its QE program will likely

Global Macro Outlook

Global Growth Remains on Trend and Deflation Risks Remain Low Despite downward revisions to 2016 global growth projections by the International

Monetary Fund (IMF), we do not anticipate a global recession or global deflation.

Global growth remains on trend while the major economies remain relatively healthy;

our growth projections for 2016 are 2%–3% for the United States, above 1% for the

eurozone, around 1% for Japan and between 6% and 7% for China.

We believe that fears of global deflation are unwarranted. Markets have, in our view,

overestimated the extent to which lower headline inflation reflects structurally weaker

global demand. We believe that supply factors are the main driver behind falling

energy and commodity prices, which in turn have pushed headline inflation lower.

These are short-term effects, and their disinflationary impact should wane as

commodity prices stabilize. The belief that inflation has become structurally lower has

made some investors complacent on taking interest-rate risk, in what we believe is a

dangerous part of the yield cycle. When commodity price base effects on inflation roll

off in the first half of 2016, we expect US inflation to get back to the Fed’s target.

Underlying inflation in the United States has not been adequately priced into bond

yields in recent months, in our assessment, and we are wary of the lack of inflation

being priced into bond yields across the globe.

Although headline inflation has declined globally, underlying core inflation trends have

remained resilient. While we do not necessarily expect sharp inflation increases in the

United States, we could see inflation at or above the Fed’s stated target as the oil-

price impact falls away. Any normalization of inflation pricing in global bond yields and

in US Treasuries would drive yields higher.

— Continued

2016 OUTLOOK: “At the start of 2016, we are encouraged by the vast set of fundamentally

attractive valuations across the global bond and currency markets. We expect continued

depreciation of the euro and yen, rising US Treasury yields, and currency appreciation in

select emerging markets.”

continue into

2017, and the

ECB has

indicated it will

likely continue

QE through

March 2017. In

our assessment,

both the BOJ

and ECB need

to continue

these current expansionary policies, which

should continue to depreciate the yen and

euro against the US dollar. In the eurozone,

QE has been driving the euro weaker to

stimulate export-driven economic growth

and lift inflation toward the ECB’s target; in

Japan, QE has become explicit debt

financing for the government and a

cornerstone of “Abenomics.”

2 | 2016 INVESTMENT OUTLOOK

Michael Hasenstab, Ph.D.

Chief Investment Officer

Templeton Global Macro

2016 INVESTMENT OUTLOOK | 3

GLOBAL MACRO OUTLOOK

— Continued

China’s Economy Remains Resilient Despite its Moderation in Growth During the first week of the year, China’s

stock markets declined sharply, causing

widespread panic in investment markets

across the globe. While we understand this

may be unsettling to global investors, our

long-term analysis of the economic

situation in China leads us to believe that

the panic is unwarranted. On the whole,

our view remains that underlying conditions

in the Chinese economy are fundamentally

more stable than markets have recently

indicated. We believe that China’s

policymakers have both the tools and the

financial firepower to counter the recent

slowdown and keep growth on track at 6%–

7%, which in turn is sufficient to support

global growth.

The People’s Bank of China (PBOC) has

once again intervened to devalue the yuan,

and once again some commentators are

interpreting the devaluation as a signal that

policymakers remain deeply concerned

about the growth slowdown.

While some observers feel the Chinese

authorities may seek to engineer a

substantial depreciation to boost growth

through exports, leading to currency wars

that may disrupt global growth and the

global financial system, our view is

different.

We would note that before the depreciation

in August 2015, China’s currency had

appreciated by over 12% on a real effective

basis in the preceding 12 months.

Furthermore, China had experienced some

“hot money” outflows during the first half of

the year, which also clearly influenced

policymakers’ actions. Although the

renminbi has experienced a modest

depreciation, we do not feel the move is a

precursor to a larger uncontrolled

weakening, as feared by markets.

As we maintained in our Global Macro Shifts

deep-dive analysis of China, we do not

share the markets’ pessimisms over the

trajectory of China’s growth. We view the

recent moderation of growth in China as an

inevitable normalization for an economy of

its size; its nominal level of gross domestic

product (GDP) is now five times the size of

what it was 10 years ago. Thus a lower rate

of growth still represents a massive level of

global aggregate demand.

In our assessment, the quality of growth in

China has improved in recent years.

Increasing labor costs and interest rates

have put downward pressure on profits;

however, higher wages boost consumption,

which has increasingly become the anchor

of Chinese growth; we estimate that

consumption is close to 60% of GDP and

rising. Additionally, new interest-rate

liberalization policies can redirect capital to

the whole economy, particularly the private

sector, which we expect to be the future

driver of growth.

The private sector in China now contributes

more to job growth than the state-owned

sector, which has not been the case for the

past 30 years. China’s rapid urbanization

process will also necessitate development.

Plans for infrastructure investment are

underway as the railways sector is set to

expand along with demands for broader

water purification and environmental related

projects. Such projects could somewhat

offset the negative drags on growth from the

contractions in manufacturing and the

excess capacity in the real estate sector.

Furthermore, property prices appear to have

bottomed out due to earlier easing

measures.

Overall, based on our analysis, we believe

China will remain on course, with GDP

growth decelerating moderately toward the

6% mark over the next few years1 while the

economy shifts toward consumption,

services and higher value-added

manufacturing.

1. There is no assurance that any estimate or forecast will be realized.

This has important implications for the

global economy:

• We believe 6%+ growth in China will

support global growth.

• Together with the new round of

infrastructure investment, this will provide

some support to commodity markets.

Note, however, that China’s rebalancing

from investment to consumption will also

reduce demand for most industrial

metals. On balance, therefore, our China

outlook should be consistent with broadly

stable commodity prices in the next few

years.

• China’s rebalancing also has a

differential impact on trade flows: We

should see more trade with advanced

economies producing finished and

industrial goods, and relatively less with

commodity producers.

• Finally, sustained wage growth implies

that China should gradually export a

more inflationary impulse to the rest of

the world, reinforcing our view that,

starting with the United States, the

outlook remains for higher inflation rates

and higher interest rates.

In sum, China’s economy is in a crucial

stage of rebalancing, but we believe it is

not at risk of collapsing. Some of the

traditional engines of growth

(manufacturing, real estate and local

government spending) have stalled or

contracted but new engines of growth (the

service sector and a new generation of

private sector companies) are taking over.

Although we may continue to experience

volatility in the near term, we remain

optimistic about China’s outlook as it

searches for its new equilibrium.

GLOBAL MACRO OUTLOOK

— Continued

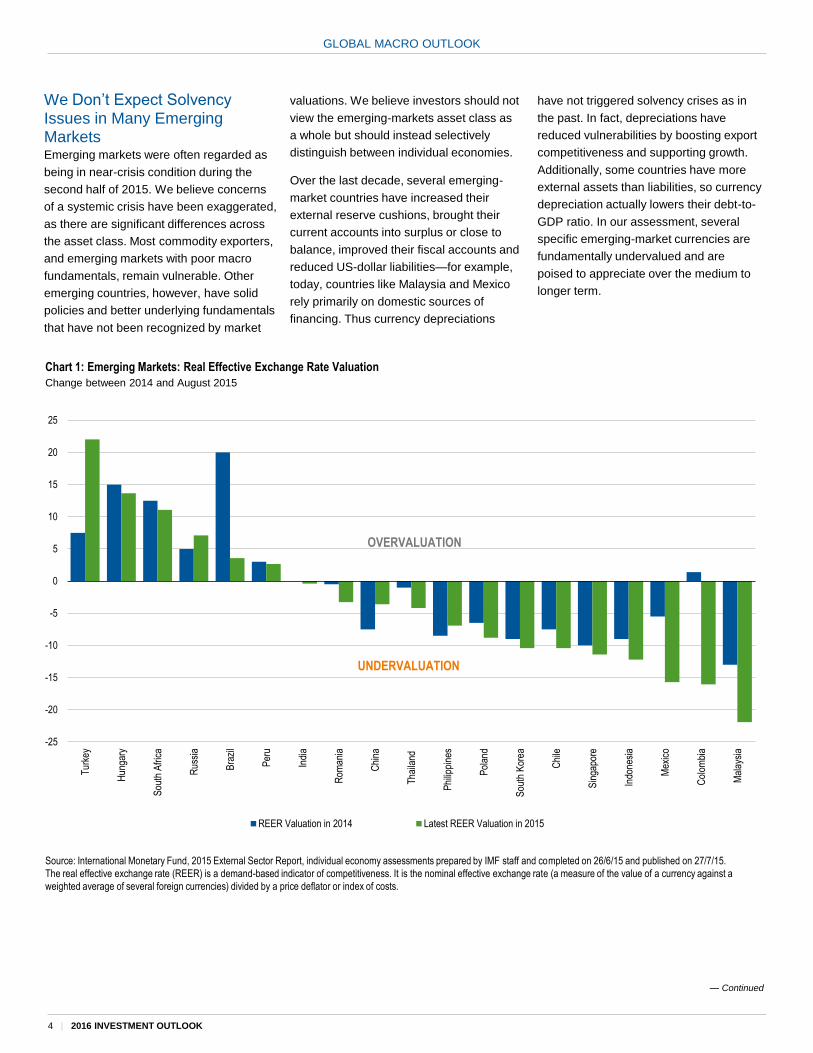

Chart 1: Emerging Markets: Real Effective Exchange Rate Valuation

Change between 2014 and August 2015

Source: International Monetary Fund, 2015 External Sector Report, individual economy assessments prepared by IMF staff and completed on 26/6/15 and published on 27/7/15.

The real effective exchange rate (REER) is a demand-based indicator of competitiveness. It is the nominal effective exchange rate (a measure of the value of a currency against a

weighted average of several foreign currencies) divided by a price deflator or index of costs.

-25

-20

-15

-10

-5

0

5

10

15

20

25

Tur

key

Hun

gary

Sou

th A

fric

a

Rus

sia

Bra

zil

Per

u

Indi

a

Rom

ania

Chi

na

Tha

iland

Phi

lippi

nes

Pol

and

Sou

th K

orea

Chi

le

Sin

gapo

re

Indo

nesi

a

Mex

ico

Col

ombi

a

Mal

aysi

a

REER Valuation in 2014 Latest REER Valuation in 2015

OVERVALUATION

UNDERVALUATION

4 | 2016 INVESTMENT OUTLOOK

We Don’t Expect Solvency Issues in Many Emerging Markets Emerging markets were often regarded as

being in near-crisis condition during the

second half of 2015. We believe concerns

of a systemic crisis have been exaggerated,

as there are significant differences across

the asset class. Most commodity exporters,

and emerging markets with poor macro

fundamentals, remain vulnerable. Other

emerging countries, however, have solid

policies and better underlying fundamentals

that have not been recognized by market

valuations. We believe investors should not

view the emerging-markets asset class as

a whole but should instead selectively

distinguish between individual economies.

Over the last decade, several emerging-

market countries have increased their

external reserve cushions, brought their

current accounts into surplus or close to

balance, improved their fiscal accounts and

reduced US-dollar liabilities—for example,

today, countries like Malaysia and Mexico

rely primarily on domestic sources of

financing. Thus currency depreciations

have not triggered solvency crises as in

the past. In fact, depreciations have

reduced vulnerabilities by boosting export

competitiveness and supporting growth.

Additionally, some countries have more

external assets than liabilities, so currency

depreciation actually lowers their debt-to-

GDP ratio. In our assessment, several

specific emerging-market currencies are

fundamentally undervalued and are

poised to appreciate over the medium to

longer term.

GLOBAL MACRO OUTLOOK

— Continued

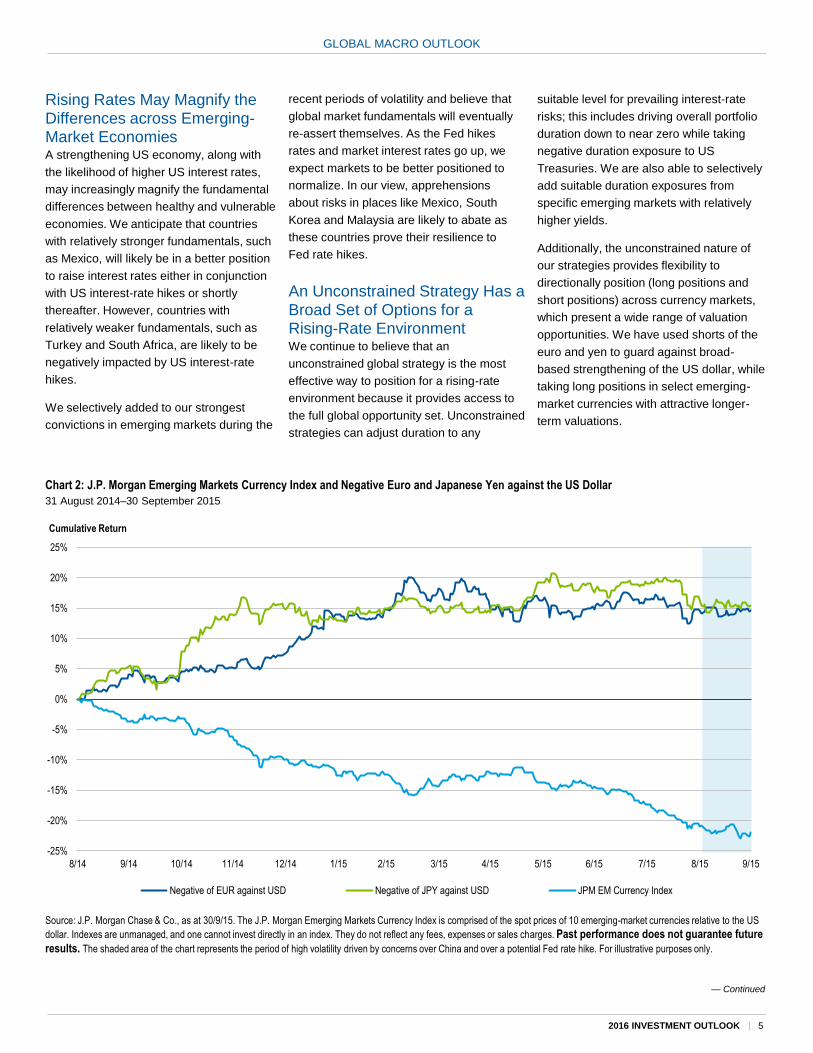

Chart 2: J.P. Morgan Emerging Markets Currency Index and Negative Euro and Japanese Yen against the US Dollar

31 August 2014–30 September 2015

Source: J.P. Morgan Chase & Co., as at 30/9/15. The J.P. Morgan Emerging Markets Currency Index is comprised of the spot prices of 10 emerging-market currencies relative to the US

dollar. Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. Past performance does not guarantee future

results. The shaded area of the chart represents the period of high volatility driven by concerns over China and over a potential Fed rate hike. For illustrative purposes only.

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

8/14 9/14 10/14 11/14 12/14 1/15 2/15 3/15 4/15 5/15 6/15 7/15 8/15 9/15

Cumulative Return

Negative of EUR against USD Negative of JPY against USD JPM EM Currency Index

2016 INVESTMENT OUTLOOK | 5

recent periods of volatility and believe that

global market fundamentals will eventually

re-assert themselves. As the Fed hikes

rates and market interest rates go up, we

expect markets to be better positioned to

normalize. In our view, apprehensions

about risks in places like Mexico, South

Korea and Malaysia are likely to abate as

these countries prove their resilience to

Fed rate hikes.

An Unconstrained Strategy Has a Broad Set of Options for a Rising-Rate Environment We continue to believe that an

unconstrained global strategy is the most

effective way to position for a rising-rate

environment because it provides access to

the full global opportunity set. Unconstrained

strategies can adjust duration to any

Rising Rates May Magnify the Differences across Emerging-Market Economies A strengthening US economy, along with

the likelihood of higher US interest rates,

may increasingly magnify the fundamental

differences between healthy and vulnerable

economies. We anticipate that countries

with relatively stronger fundamentals, such

as Mexico, will likely be in a better position

to raise interest rates either in conjunction

with US interest-rate hikes or shortly

thereafter. However, countries with

relatively weaker fundamentals, such as

Turkey and South Africa, are likely to be

negatively impacted by US interest-rate

hikes.

We selectively added to our strongest

convictions in emerging markets during the

suitable level for prevailing interest-rate

risks; this includes driving overall portfolio

duration down to near zero while taking

negative duration exposure to US

Treasuries. We are also able to selectively

add suitable duration exposures from

specific emerging markets with relatively

higher yields.

Additionally, the unconstrained nature of

our strategies provides flexibility to

directionally position (long positions and

short positions) across currency markets,

which present a wide range of valuation

opportunities. We have used shorts of the

euro and yen to guard against broad-

based strengthening of the US dollar, while

taking long positions in select emerging-

market currencies with attractive longer-

term valuations.

GLOBAL MACRO OUTLOOK

6 | 2016 INVESTMENT OUTLOOK

investment convictions and added to those

types of positions as prices became

cheaper during the periods of heightened

volatility.

At the start of 2016, we are encouraged by

the vast set of fundamentally attractive

valuations across the global bond and

currency markets. Currently we favor

currencies in countries where inflation is

picking up and growth remains healthy,

yet the local currency remains

fundamentally undervalued. Looking

ahead, we expect continued depreciation

of the euro and yen, rising US Treasury

yields, and currency appreciation in select

emerging markets.

We Are Positioned for Rising US Treasury Yields and Currency Appreciation in Select Emerging Markets On the whole, we have continued to

position our strategies for rising rates by

maintaining low portfolio duration and

aiming at a negative correlation with US

Treasury returns. We have also continued

to actively seek select duration exposures

that can offer positive real yields without

taking undue interest-rate risk, favoring

countries that have solid underlying

fundamentals and prudent fiscal, monetary

and financial policies. When investing

globally, several investment opportunities

may take time to materialize, which may

require weathering short-term volatility as

the longer-term investing theses develop.

During 2015, we shifted out of markets

that we were previously contrarian on (that

were once distressed but have now

recovered and become consensus) in

order to re-allocate to positions that have

fundamentally attractive valuations for the

medium-term ahead. We also maintained

our exposures to several of our strongest

TEAM OVERVIEW

Dr. Hasenstab and his team

manage Templeton’s global

bond strategies, including

unconstrained fixed income,

currency and global macro. This

economic team, trained in some

of the leading universities in the

world, integrates global

macroeconomic analysis with

in-depth country research to help

identify long-term imbalances

that translate to investment

opportunities.

During 2015, we shifted out of markets that we

were previously contrarian on (that were once

distressed but have now recovered and become

consensus) in order to re-allocate to positions

that have fundamentally attractive valuations for

the medium-term ahead.

“

”

Global Equity Outlook

— Continued

Edward D. Perks, CFA

Chief Investment Officer

Franklin Templeton Equity

2016 OUTLOOK: “With a generally healthy backdrop, a robust opportunity set and a focus on

the long term, we remain constructive on the prospects for active equity management across a

wide range of sectors and regions as we enter 2016.”

2016 INVESTMENT OUTLOOK | 7

Prospects for a “Sweet ’16” During much of 2015, global equity markets

labored under the weight of sputtering

growth in developed economies, slumping

emerging markets, and collapsing prices for

a wide range of commodities and natural

resources that had far-reaching

consequences. Although extraordinary

monetary policy measures from key central

banks have been employed in efforts to

stimulate economic growth over the last

several years, these measures proved

somewhat less effective in meeting 2015

growth targets in economies that comprise

a substantial amount of global GDP,

including the United States, the eurozone,

the United Kingdom and Japan. This

challenging backdrop occurred amid

uncertainties surrounding economic growth

in China and the country’s transition from

an investment-led economy to one driven

more by domestic consumption. Finally,

involving China: sharp volatility in Chinese equity markets, additional downward

movement in the foreign exchange value of the Chinese yuan, and renewed

concerns about the decelerating pace of Chinese economic growth. In addition,

financial markets in the first week of trading in 2016 were somewhat unnerved by

geopolitical tensions between Saudi Arabia and Iran, reports of nuclear military

tests taking place in North Korea, and additional incremental weakness in global

energy prices. While we take each of these factors into thorough consideration

while formulating our investment views, we feel comfortable that—provided there is

not substantial escalation in geopolitical tensions—markets will eventually look

beyond these short-term headlines and return their primary focus to the merits and

fundamentals of individual securities. Indeed, overreaction by financial markets to

short-term negative news headlines oftentimes creates attractive investment

opportunities for disciplined long-term investors.

We remain generally constructive on the prospects for global equity performance

potential due to a host of factors such as further declines in unemployment in key

regions, an improving wage outlook for a broader segment of the global economy

and the resiliency of corporate profitability, the latter of which continues to enable

tremendous flexibility in capital allocation.

Navigating Shifts in Central Bank and Government Policies While many market participants view the recent Fed decision to raise interest rates

as a so-called “lift-off,” we prefer to view it as a process of normalization. The

implementation of the zero interest rate policy (ZIRP) back in December 2008 was

markets

remained fixated

on the timing of

the Fed’s “lift-off”

in raising interest

rates and the

potential market

implications that

may exist for the

duration of the

current business

cycle.

Succumbing to the pressure of these

headwinds, global equity markets generally

stalled out in 2015.

Shifting our gaze to this year, the first week

of calendar 2016 trading brought with it

another wave of incremental financial

markets volatility. A host of global macro-

economic factors increased investors’

anxiety, including a combination of issues

GLOBAL EQUITY OUTLOOK

— Continued

8 | 2016 INVESTMENT OUTLOOK

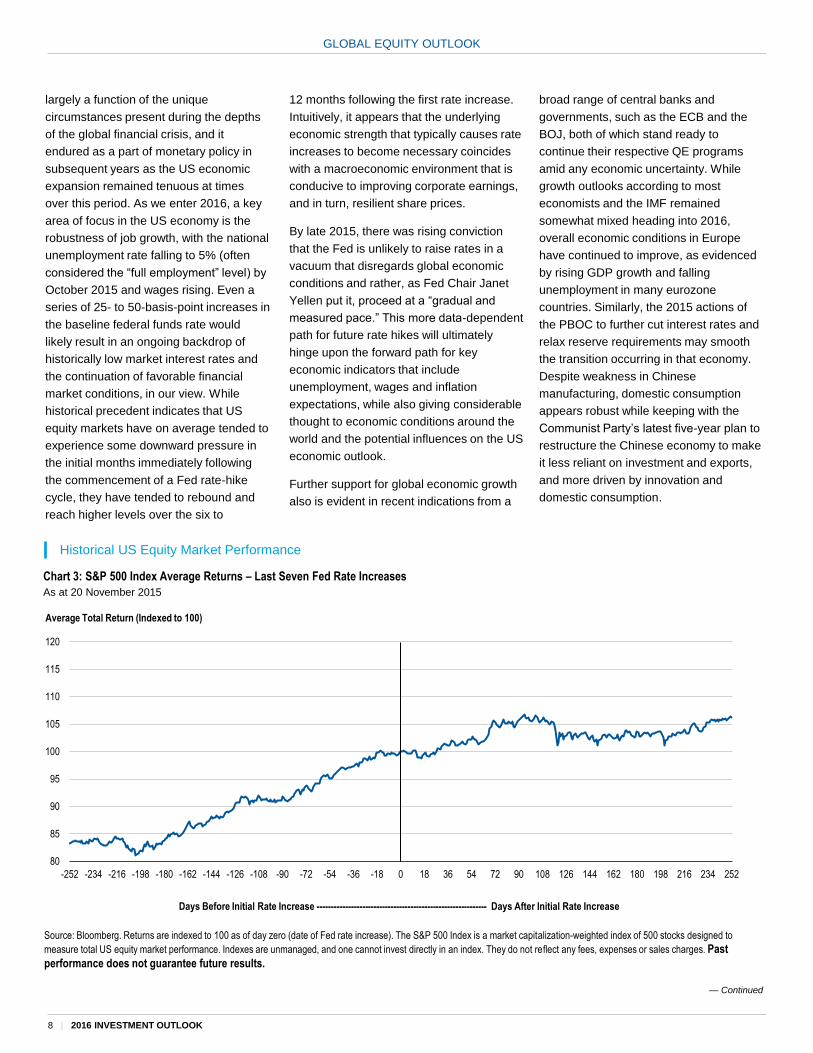

Chart 3: S&P 500 Index Average Returns – Last Seven Fed Rate Increases

As at 20 November 2015

Source: Bloomberg. Returns are indexed to 100 as of day zero (date of Fed rate increase). The S&P 500 Index is a market capitalization-weighted index of 500 stocks designed to

measure total US equity market performance. Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. Past

performance does not guarantee future results.

80

85

90

95

100

105

110

115

120

-252 -234 -216 -198 -180 -162 -144 -126 -108 -90 -72 -54 -36 -18 0 18 36 54 72 90 108 126 144 162 180 198 216 234 252

Average Total Return (Indexed to 100)

Days Before Initial Rate Increase ------------------------------------------------------------ Days After Initial Rate Increase

Historical US Equity Market Performance

12 months following the first rate increase.

Intuitively, it appears that the underlying

economic strength that typically causes rate

increases to become necessary coincides

with a macroeconomic environment that is

conducive to improving corporate earnings,

and in turn, resilient share prices.

By late 2015, there was rising conviction

that the Fed is unlikely to raise rates in a

vacuum that disregards global economic

conditions and rather, as Fed Chair Janet

Yellen put it, proceed at a “gradual and

measured pace.” This more data-dependent

path for future rate hikes will ultimately

hinge upon the forward path for key

economic indicators that include

unemployment, wages and inflation

expectations, while also giving considerable

thought to economic conditions around the

world and the potential influences on the US

economic outlook.

Further support for global economic growth

also is evident in recent indications from a

broad range of central banks and

governments, such as the ECB and the

BOJ, both of which stand ready to

continue their respective QE programs

amid any economic uncertainty. While

growth outlooks according to most

economists and the IMF remained

somewhat mixed heading into 2016,

overall economic conditions in Europe

have continued to improve, as evidenced

by rising GDP growth and falling

unemployment in many eurozone

countries. Similarly, the 2015 actions of

the PBOC to further cut interest rates and

relax reserve requirements may smooth

the transition occurring in that economy.

Despite weakness in Chinese

manufacturing, domestic consumption

appears robust while keeping with the

Communist Party’s latest five-year plan to

restructure the Chinese economy to make

it less reliant on investment and exports,

and more driven by innovation and

domestic consumption.

largely a function of the unique

circumstances present during the depths

of the global financial crisis, and it

endured as a part of monetary policy in

subsequent years as the US economic

expansion remained tenuous at times

over this period. As we enter 2016, a key

area of focus in the US economy is the

robustness of job growth, with the national

unemployment rate falling to 5% (often

considered the “full employment” level) by

October 2015 and wages rising. Even a

series of 25- to 50-basis-point increases in

the baseline federal funds rate would

likely result in an ongoing backdrop of

historically low market interest rates and

the continuation of favorable financial

market conditions, in our view. While

historical precedent indicates that US

equity markets have on average tended to

experience some downward pressure in

the initial months immediately following

the commencement of a Fed rate-hike

cycle, they have tended to rebound and

reach higher levels over the six to

GLOBAL EQUITY OUTLOOK

— Continued

2016 INVESTMENT OUTLOOK | 9

Chart 4: By Deal Value (USD Trillions)

As at 23 November 2015

Source: Bloomberg.

Global M&A Monthly Activity

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

2014 2015

USD Trillions

Chart 5: By Region (USD Trillions)

As at 23 November 2015

Source: Bloomberg.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

NorthAmerica

LatinAmerica &Caribbean

WesternEurope

EasternEurope

DevelopedAsia Pacific

EmergingAsia Pacific

Middle East& Africa

2007 2013 2014 YTD 23/11/15

USD Trillions

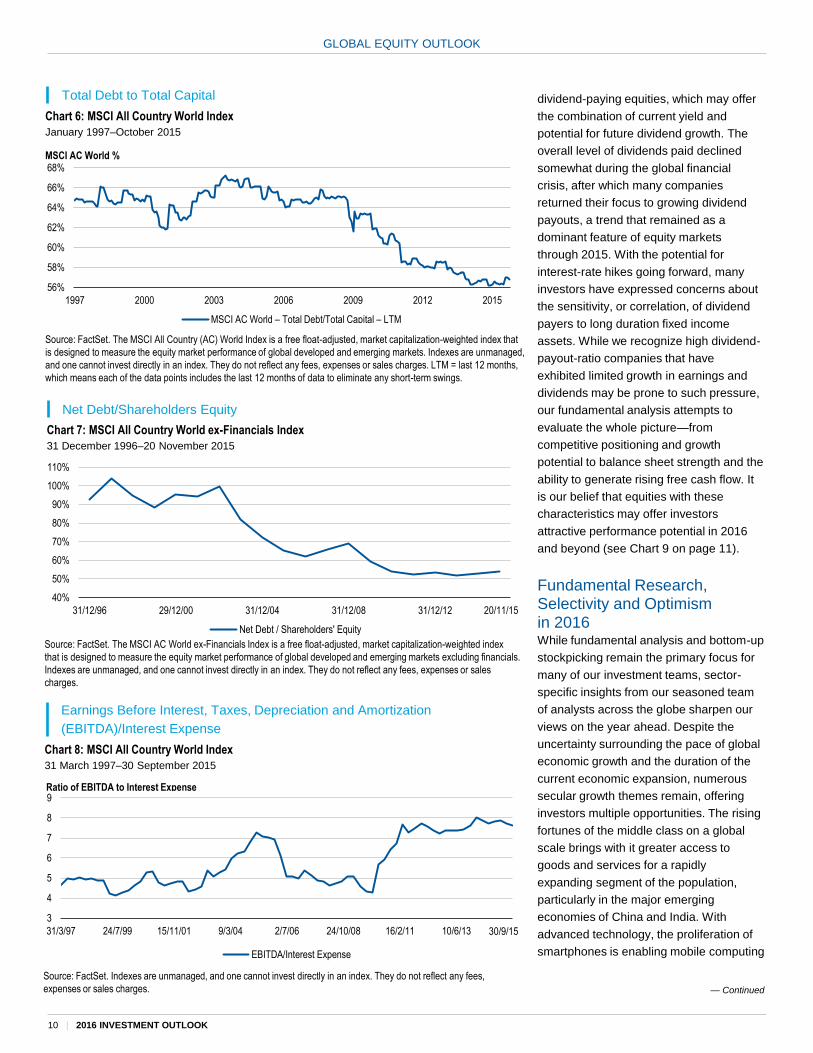

Multiple Paths to Corporate Strength and Flexibility in the Current Environment One defining characteristic of recent global

equity markets that we expect to remain a

key feature of 2016 is the discipline

exhibited in corporate capital allocation.

With profitability measures remaining at

historically elevated levels, corporate

decision makers have enjoyed tremendous

flexibility to consider a range of strategic

and shareholder-oriented measures like

merger-and-acquisition (M&A) activity,

increased investment and capital

expenditures, balance sheet enhancement,

dividend growth, and share buybacks.

Additionally, many companies through

either internal efforts and/or external

pressures have been looking inward at

their mix of businesses, with some firms

opting to shed non-core assets and re-

prioritize investment opportunities to drive

improvements in returns.

While our analysis indicates sales growth

has been modest across many sectors

lately, it is likely that what happens below

the top line will continue to have the

greater impact on whether or not today’s

healthy profit levels are sustained through

2016. In our opinion, favorable conditions

are likely to persist, aided by minimal

pressure on input costs (due in part to multi-

year low energy costs and prices for a wide

range of commodities), moderate wage price

pressures, and low interest costs and

leverage. Given expectations for rising

interest rates going forward, many investors

have grown concerned about the impact of

higher interest costs on corporate profits

and, ultimately, share prices. While the

impact would not be entirely insignificant, we

believe other factors need to be considered,

including the lower share of debt relative to

total capital, as well as the limited role total

debt and interest cost has on the majority

of corporate balance sheets and income

statements. Indeed, while the total quantity

of debt issued by corporations globally

over the past few years has been quite

sizable, we believe the lion’s share of this

debt issuance has been conducted for the

right reasons, such as replacing more-

expensive existing debt with less-

expensive debt, and taking advantage of

historically low market interest rates to lock

in attractive funding costs for several years

(see Charts 6–8 on page 10).

A Challenging Market for Income-Oriented Investors The generally low level of market interest

rates combined with the potential

headwind of higher interest rates moving

forward presents a challenge for income-

oriented investors. Increasingly, an

alternative for many investors remains

GLOBAL EQUITY OUTLOOK

— Continued

Chart 6: MSCI All Country World Index

January 1997–October 2015

Source: FactSet. The MSCI All Country (AC) World Index is a free float-adjusted, market capitalization-weighted index that

is designed to measure the equity market performance of global developed and emerging markets. Indexes are unmanaged,

and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. LTM = last 12 months,

which means each of the data points includes the last 12 months of data to eliminate any short-term swings.

Total Debt to Total Capital

Chart 7: MSCI All Country World ex-Financials Index

31 December 1996–20 November 2015

Source: FactSet. The MSCI AC World ex-Financials Index is a free float-adjusted, market capitalization-weighted index

that is designed to measure the equity market performance of global developed and emerging markets excluding financials.

Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect any fees, expenses or sales

charges.

Net Debt/Shareholders Equity

Chart 8: MSCI All Country World Index

31 March 1997–30 September 2015

Source: FactSet. Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect any fees,

expenses or sales charges.

Earnings Before Interest, Taxes, Depreciation and Amortization

(EBITDA)/Interest Expense

56%

58%

60%

62%

64%

66%

68%

1997 2000 2003 2006 2009 2012 2015

MSCI AC World – Total Debt/Total Capital – LTM

MSCI AC World %

3

4

5

6

7

8

9

31/3/97 24/7/99 15/11/01 9/3/04 2/7/06 24/10/08 16/2/11 10/6/13

EBITDA/Interest Expense

30/9/15

Ratio of EBITDA to Interest Expense

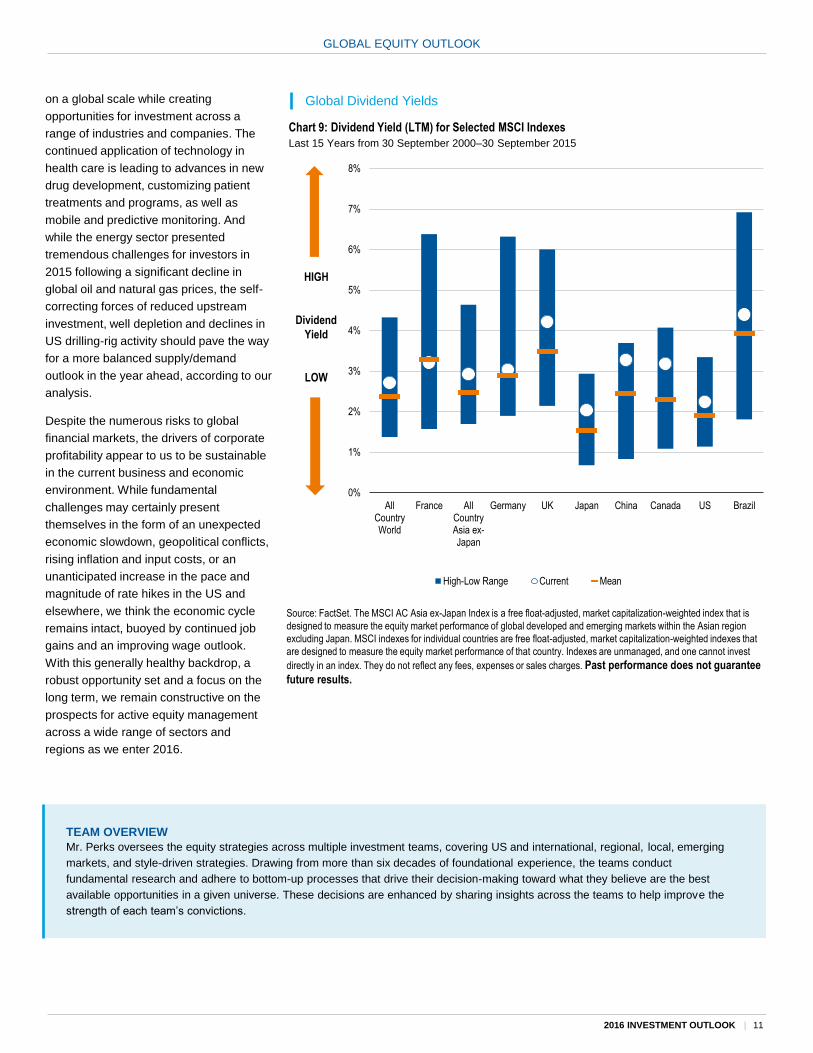

dividend-paying equities, which may offer

the combination of current yield and

potential for future dividend growth. The

overall level of dividends paid declined

somewhat during the global financial

crisis, after which many companies

returned their focus to growing dividend

payouts, a trend that remained as a

dominant feature of equity markets

through 2015. With the potential for

interest-rate hikes going forward, many

investors have expressed concerns about

the sensitivity, or correlation, of dividend

payers to long duration fixed income

assets. While we recognize high dividend-

payout-ratio companies that have

exhibited limited growth in earnings and

dividends may be prone to such pressure,

our fundamental analysis attempts to

evaluate the whole picture—from

competitive positioning and growth

potential to balance sheet strength and the

ability to generate rising free cash flow. It

is our belief that equities with these

characteristics may offer investors

attractive performance potential in 2016

and beyond (see Chart 9 on page 11).

Fundamental Research, Selectivity and Optimism in 2016 While fundamental analysis and bottom-up

stockpicking remain the primary focus for

many of our investment teams, sector-

specific insights from our seasoned team

of analysts across the globe sharpen our

views on the year ahead. Despite the

uncertainty surrounding the pace of global

economic growth and the duration of the

current economic expansion, numerous

secular growth themes remain, offering

investors multiple opportunities. The rising

fortunes of the middle class on a global

scale brings with it greater access to

goods and services for a rapidly

expanding segment of the population,

particularly in the major emerging

economies of China and India. With

advanced technology, the proliferation of

smartphones is enabling mobile computing

40%

50%

60%

70%

80%

90%

100%

110%

31/12/96 29/12/00 31/12/04 31/12/08 31/12/12

Net Debt / Shareholders' Equity

20/11/15

10 | 2016 INVESTMENT OUTLOOK

GLOBAL EQUITY OUTLOOK

Chart 9: Dividend Yield (LTM) for Selected MSCI Indexes

Last 15 Years from 30 September 2000–30 September 2015

Global Dividend Yields on a global scale while creating

opportunities for investment across a

range of industries and companies. The

continued application of technology in

health care is leading to advances in new

drug development, customizing patient

treatments and programs, as well as

mobile and predictive monitoring. And

while the energy sector presented

tremendous challenges for investors in

2015 following a significant decline in

global oil and natural gas prices, the self-

correcting forces of reduced upstream

investment, well depletion and declines in

US drilling-rig activity should pave the way

for a more balanced supply/demand

outlook in the year ahead, according to our

analysis.

Despite the numerous risks to global

financial markets, the drivers of corporate

profitability appear to us to be sustainable

in the current business and economic

environment. While fundamental

challenges may certainly present

themselves in the form of an unexpected

economic slowdown, geopolitical conflicts,

rising inflation and input costs, or an

unanticipated increase in the pace and

magnitude of rate hikes in the US and

elsewhere, we think the economic cycle

remains intact, buoyed by continued job

gains and an improving wage outlook.

With this generally healthy backdrop, a

robust opportunity set and a focus on the

long term, we remain constructive on the

prospects for active equity management

across a wide range of sectors and

regions as we enter 2016.

0%

1%

2%

3%

4%

5%

6%

7%

8%

AllCountryWorld

France AllCountryAsia ex-Japan

Germany UK Japan China Canada US Brazil

High-Low Range Current Mean

HIGH

Dividend

Yield

LOW

Source: FactSet. The MSCI AC Asia ex-Japan Index is a free float-adjusted, market capitalization-weighted index that is

designed to measure the equity market performance of global developed and emerging markets within the Asian region

excluding Japan. MSCI indexes for individual countries are free float-adjusted, market capitalization-weighted indexes that

are designed to measure the equity market performance of that country. Indexes are unmanaged, and one cannot invest

directly in an index. They do not reflect any fees, expenses or sales charges. Past performance does not guarantee

future results.

2016 INVESTMENT OUTLOOK | 11

TEAM OVERVIEW

Mr. Perks oversees the equity strategies across multiple investment teams, covering US and international, regional, local, emerging

markets, and style-driven strategies. Drawing from more than six decades of foundational experience, the teams conduct

fundamental research and adhere to bottom-up processes that drive their decision-making toward what they believe are the best

available opportunities in a given universe. These decisions are enhanced by sharing insights across the teams to help improve the

strength of each team’s convictions.

Long-Term Capital Market Expectations Every year, Franklin Templeton Solutions

reviews the data and themes driving capital

markets in order to build asset return

expectations for different asset classes for

the next five to 10 years. Our long-term

forecasts are based on our assessment of

current valuation measures, economic

growth and inflation prospects, as well as

historical risk premiums.

Slow Global Growth Since the 2007–2008 global financial crisis,

we have witnessed a weaker recovery by

historical standards even with supportive

central banks across the globe. We believe

underlying structural changes have been

driving down real growth globally. Debt

deleveraging is one of the main culprits.

While it was already underway in the United

States and Europe, China is just joining the

Long-Term Capital Markets Outlook

Furthermore, an aging population in major developed and emerging countries is an

even stronger factor depressing the growth outlook. Starting in 2016, the working-

age population will decline in advanced economies, while the share of the

population over 65 years of age will skyrocket.4 We think that this demographic

change is a powerful force to reckon with. Japan is an important example of what

Europe and the rest of the developed world face in the future. The United States

may look better positioned in terms of this demographic crisis, but a stronger US

dollar not only adds to emerging-market woes but also impacts US economic

growth adversely.

Subdued Global Inflation Expectations In broad terms, we regard inflation as currently low in both developed- and

emerging-market economies. Given the slow growth expectation and low threat of

any supply shocks (like the oil embargo in the 1970s), it is hard to see inflation

accelerating to unexpected levels in the next five years. During the past few

decades, we saw a savings glut in China and Germany providing excess capital

that has held down interest rates and inflation. Going forward, the movement of a

large share of the population into the lower-consumption/higher-saving period of

their lives is likely to add to the excess savings while keeping interest rates low and

inflation moderate. Central banks have reacted to these economic forces and

implemented QE. They also had to keep QE in effect longer than they initially

expected to boost inflation closer to their desired target levels.

— Continued

Rick Frisbie

Head of Franklin Templeton Solutions

Franklin Templeton Investments

LONG-TERM OUTLOOK: “We note that underlying structural changes have been driving down

real growth globally and that it is hard for us to see inflation accelerating to unexpected levels

in the next five years. Our assessment of current valuation measures, as well as economic

growth and inflation prospects, leave us bullish in terms of opportunities in global equities,

systematic beta2 and oil, and bearish on global government bonds.”

trend, which

may take years

to unfold.

According to the

IMF, China has

replaced the

United States as

the top

contributor to

global growth,3

and therefore the drag on global growth as

a result of China’s deleveraging assumes a

proportionately larger impact. A

continuation of the slowdown in China and

the economy’s realignment toward

consumption and services is particularly

bad news for countries that export oil and

metals, in our view.

2. Systematic beta is a source of potential returns that is persistent, investable and liquid, and can be implemented systematically.

3. Source: International Monetary Fund, World Economic Outlook, October 2015. © 2015 By International Monetary Fund. All Rights Reserved.

4. Source: United Nations World Population Prospects, 2015 Revision.

12 | 2016 INVESTMENT OUTLOOK

LONG-TERM CAPITAL MARKETS OUTLOOK

Table 1: 10-Year Inflation Forecasts

Based on Consensus Estimates (as at October 2015) and Breakeven Rates (as at November 2015)

Sources: Consensus Economics Inc.: Consensus Forecasts, October 2015, and Bloomberg L.P., November 2015. The breakeven rate is a five-year, five-year forward inflation rate, which

measures expected inflation (on average) over the five-year period that begins five years from today. The breakeven rate derives from the difference between the yield on a nominal fixed-

rate bond and the real yield on an inflation-linked bond of similar maturity and credit quality. There is no assurance that any estimate or projection will be realized.

With this easy monetary policy, central

banks may succeed in bringing inflation

back to their targets, but we think the risk of

inflation overshooting significantly is very

low. Consensus estimates of long-term

inflation and breakeven rates from fixed

income markets support our views.

Lower Performance Potential Likely Everywhere Relative to History, but Global Equities Appear More Attractive to Us than Global Bonds We believe current yield is a good indicator

of future performance potential. As of late

2015, global bond yields were at historical

lows in major economies. Real earnings

yields of global equities (the inverse of the

price/earnings ratio) relative to their own

history were not looking particularly

attractive to us either. This analysis is in-

line with our views of growth and inflation.

Additionally, we do not see an environment

for commodities to offer returns similar to

the last decade given the gloomy outlook

on global growth. Following the same

argument of excess savings, ample capital

supply may reduce the real return required

by investors overall. While we are of the

opinion that returns overall are likely to be

subdued, we also think there are areas that

on a relative basis offer more compelling

opportunities than others. Relative to global

bonds, the risk premium of global equities

currently still looks attractive to us from a

historical standpoint. We also feel that

within global equities, there is opportunity in

emerging markets relative to developed

markets over the long term.

Our Strongest Convictions “For”: Global equities should continue to enjoy

tailwinds from easy central bank policies

from the ECB and the BOJ. In the short

term, there may be headwinds for the United

States and emerging-market countries given

the Fed’s rate-hike cycle. However, given

that the plans of these central banks are

well anticipated, we think the impact is likely

to be manageable. Consequently, we

believe global equities can enjoy

performance potential over the next

seven years.

Systematic beta (alternative risk premia)

may offer strong risk-adjusted performance

potential. Given our expectations of

relatively low returns from traditional asset

classes, systematic beta—which consists of

rules-based strategies that seek to capture

risk premia—could be a good alternative.

These strategies can be used as an overlay

to a portfolio of traditional beta assets

because of their potential diversification

benefits.

Oil may continue to be weaker for another

year or so in light of the ongoing supply glut

and the Fed’s rate-hike cycle. We saw the

price-action dip we expected during 2015

and regard current prices as of late-2015 as

very close to the optimal buying opportunity

for us. Oil inventories are expected to have

reached a peak, and at these current low

prices, we expect a further rig count decline

as marginal suppliers move offline due to

lack of profits.

Our Strongest Convictions “Against”: From a historical perspective, few

developed-market government bonds have

been more expensive than the levels seen

today. QE and the zero interest rate

policies that have been implemented by

key central banks have driven government

bond yields toward all-time lows, leaving

us with an expectation of lower

performance potential for them in the

future.

United States Canada Eurozone United Kingdom Japan Australia

Consensus Forecast 2.3% 2.0% 1.9% 2.1% 1.4% 2.6%

Breakeven Rate 1.6% 1.6% 1.5% 2.5% 0.8% 2.2%

TEAM OVERVIEW

Franklin Templeton Solutions is a

global investment management group

dedicated to multi-strategy solutions

and is comprised of individuals

representing various registered

investment advisory entity

subsidiaries of Franklin Resources,

Inc., a global investment organization

operating as Franklin Templeton

Investments.

2016 INVESTMENT OUTLOOK | 13

Visit our website to learn more about how our multiple world-class investment teams view the

complex, interconnected global financial markets they invest in. The portfolio managers listed

below describe what they foresee as investment opportunities and challenges in 2016.

MORE INVESTMENT

INSIGHTS ONLINE

FIXED INCOME

US Municipal Bond Investing: Sheila Amoroso & Rafael Costas

Franklin Templeton Fixed Income Group

Multi-Sector Fixed Income

Investing: Christopher J. Molumphy, CFA

Franklin Templeton Fixed Income Group

US Growth Investing: Grant Bowers &

Matthew J. Moberg, CPA

Franklin Equity Group

US Growth Investing:

Serena Perin Vinton, CFA

Franklin Equity Group

EQUITY

Emerging-Market Investing:

Mark Mobius, Ph.D.

Templeton Emerging Markets Group

Global Equity Investing:

Stephen H. Dover, CFA

Franklin Local Asset Management

Global Value Investing: Norman J. Boersma, CFA &

Cindy L. Sweeting, CFA

Templeton Global Equity Group

Global Value Investing:

Peter A. Langerman

Franklin Mutual Series

MULTI ASSETS

Investing in Multi Asset Portfolios: Thomas A. Nelson, CFA &

Brooks Ritchey

Franklin Templeton Solutions

ALTERNATIVES

Hedge Fund Strategy Investing: David C. Saunders &

Robert Christian

K2 Advisors

Natural Resources Investing:

Frederick G. Fromm, CFA

Franklin Equity Group

Real Estate and

Infrastructure Investing:

Wilson Magee

Franklin Real Asset Advisors

14 | 2016 INVESTMENT OUTLOOK

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Currency rates may fluctuate significantly over short periods of

time, and can reduce returns. Derivatives, including currency

management strategies, involve costs and can create economic

leverage in a portfolio which may result in significant volatility

and cause it to participate in losses (as well as enable gains) on

an amount that exceeds its initial investment. A portfolio may not

achieve the anticipated benefits, and may realize losses when a

counterparty fails to perform as promised. The markets for

particular securities or types of securities are or may become

relatively illiquid. Reduced liquidity will have an adverse impact

on the security’s value and on the ability to sell such securities in

response to a specific market event. Foreign securities involve

special risks, including currency fluctuations and economic and

political uncertainties. Investments in emerging markets involve

heightened risks related to the same factors, in addition to those

associated with these markets’ smaller size and lesser liquidity.

Investments in lower-rated bonds include higher risk of default

and loss of principal. Bond prices generally move in the opposite

direction of interest rates. As the prices of bonds in an

investment portfolio adjust to a rise in interest rates, the value of

the portfolio may decline. Changes in the financial strength of a

bond issuer or in a bond’s credit rating may affect its value.

Stock prices fluctuate, sometimes rapidly and dramatically, due

to factors affecting individual companies, particular industries or

sectors, or general market conditions. Because some systematic

beta strategy signals are built using historical market events,

systematic beta strategies can be subject to model risk, whereby

the strategies perform differently than the model would expect for

various reasons, including but not limited to market and

economic conditions. In other words, the future performance and

correlations of systematic beta strategies may differ, potentially

significantly, from historical performance and correlations.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should

not be construed as individual investment advice or a

recommendation or solicitation to buy, sell or hold any security or

to adopt any investment strategy. It does not constitute legal or

tax advice.

The views expressed are those of the investment manager and

the comments, opinions and analyses are rendered as of the

publication date and may change without notice. The information

provided in this material is not intended as a complete analysis of

every material fact regarding any country, region or market. All

investments involve risks, including possible loss of

principal.

Data from third party sources may have been used in the

preparation of this material and Franklin Templeton Investments

(“FTI”) has not independently verified, validated or audited such

data. FTI accepts no liability whatsoever for any loss arising from

use of this information and reliance upon the comments, opinions

and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all

jurisdictions and are offered outside the U.S. by other FTI

affiliates and/or their distributors as local laws and regulation

permits. Please consult your own professional adviser for further

information on availability of products and services in your

jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One

Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL

BEN/342-5236, franklintempleton.com - Franklin Templeton

Distributors, Inc. is the principal distributor of Franklin Templeton

Investments’ U.S. registered products, which are available only in

jurisdictions where an offer or solicitation of such products is

permitted under applicable laws and regulation.

2016 INVESTMENT OUTLOOK | 15

Australia: Issued by Franklin Templeton Investments Australia

Limited (ABN 87 006 972 247) (Australian Financial Services

License Holder No. 225328), Level 19, 101 Collins Street,

Melbourne, Victoria, 3000. Austria/Germany: Issued by Franklin

Templeton Investment Services GmbH, Mainzer Landstraße 16,

D-60325 Frankfurt am Main, Germany. Authorized in Germany

by IHK Frankfurt M., Reg. no. D-F-125-TMX1-08. Canada:

Issued by Franklin Templeton Investments Corp., 5000 Yonge

Street, Suite 900 Toronto, ON, M2N 0A7, Fax: (416) 364-1163,

(800) 387-0830, www.franklintempleton.ca. Dubai: Issued by

Franklin Templeton Investments (ME) Limited, authorized and

regulated by the Dubai Financial Services Authority. Dubai office:

Franklin Templeton Investments, The Gate, East Wing, Level 2,

Dubai International Financial Centre, P.O. Box 506613, Dubai,

U.A.E., Tel.: +9714-4284100 Fax: +9714-4284140. France:

Issued by Franklin Templeton France S.A., 20 rue de la Paix,

75002 Paris, France. Hong Kong: Issued by Franklin Templeton

Investments (Asia) Limited, 17/F, Chater House, 8 Connaught

Road Central, Hong Kong. Italy: Issued by Franklin Templeton

Italia Sim S.p.A., Corso Italia, 1 – Milan, 20122, Italy. Japan:

Issued by Franklin Templeton Investments Japan Limited.

Korea: Issued by Franklin Templeton Investment Trust

Management Co., Ltd., 3rd fl., CCMM Building, 12 Youido-Dong,

Youngdungpo-Gu, Seoul, Korea 150-968. Luxembourg/

Benelux: Issued by Franklin Templeton International Services,

S.à r.l. – Supervised by the Commission de Surveillance du

Secteur Financier - 8A, rue Albert Borschette, L-1246

Luxembourg - Tel: +352-46 66 67-1 - Fax: +352-46 66 76.

Malaysia: Issued by Franklin Templeton Asset Management

(Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset

Management Sdn. Bhd. Nordic regions: Issued by Franklin

Templeton Investment Management Limited (FTIML), Swedish

Branch, Blasieholmsgatan 5, Se-111 48 Stockholm, Sweden.

FTIML is authorized and regulated in the United Kingdom by the

Financial Conduct Authority and is authorized to conduct certain

investment services in Denmark, Sweden, Norway & Finland.

Poland: Issued by Templeton Asset Management (Poland) TFI

S.A., Rondo ONZ 1; 00-124 Warsaw. Romania: Issued by the

Bucharest branch of Franklin Templeton Investment

Management Limited, 78-80 Buzesti Street, Premium Point, 7th-

8th Floor, 011017 Bucharest 1, Romania. Registered with CNVM

under no. PJM05SSAM/400001/ 14.09.2009, and authorized and

regulated in the UK by the Financial Conduct Authority.

Singapore: Issued by Templeton Asset Management Ltd.

Registration No. (UEN) 199205211E, 7 Temasek Boulevard,

#38-03 Suntec Tower One, 038987, Singapore. Spain: Issued by

the branch of Franklin Templeton Investment Management,

Professional of the Financial Sector under the Supervision of

CNMV, José Ortega y Gasset 29, Madrid. South Africa: Issued

by Franklin Templeton Investments SA (PTY) Ltd which is an

authorized Financial Services Provider. Tel: +27 (11) 341 2300

Fax: +27 (11) 341 2301. Switzerland & Liechtenstein: Issued

by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-

8002 Zurich. UK: Issued by Franklin Templeton Investment

Management Limited (FTIML), registered office: Cannon Place,

78 Cannon Street, London, EC4N 6HL. Authorized and regulated

in the United Kingdom by the Financial Conduct Authority.

Offshore Americas: In the U.S., this publication is made

available only to financial intermediaries by Templeton/Franklin

Investment Services, 100 Fountain Parkway, St. Petersburg,

Florida 33716. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-

0076 (Canada Toll-Free), and Fax: (727) 299-8736. Investments

are not FDIC insured; may lose value; and are not bank

guaranteed. Distribution outside the U.S. may be made by

Templeton Global Advisors Limited or other sub-distributors,

intermediaries, dealers or professional investors that have been

engaged by Templeton Global Advisors Limited to distribute

shares of Franklin Templeton funds in certain jurisdictions. This is

not an offer to sell or a solicitation of an offer to purchase

securities in any jurisdiction where it would be illegal to do so.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not

prepared or endorsed by MSCI.

See www.franklintempletondatasources.com for additional data provider information.

16 | 2016 INVESTMENT OUTLOOK

Copyright © 2016 Franklin Templeton Investments. All rights reserved. IBS YEOS 01/16

Please visit www.franklinresources.com to be

directed to your local Franklin Templeton website.