Embed Size (px)

Citation preview

Investment strategy for a volatile market

…

Kevin Scully, 16 July 2010

www.nracapital.com

Disclaimer

This material is for educational purposes only & does not constitute financial product advice. Netresearch-asia / NRA Capital does not represent or warrant that the material is complete or accurate. You should consider obtaining independent advice before making any financial decisions. To the extent permitted by Law, no responsibility for any loss arising in any way (including by way of negligence) from anyone acting or refraining from acting as a result of this material is accepted by Netresearch-asia / NRA Capital.

This disclaimer extends to any private discussions with the presenter/and staff of NRA Capital Pte Ltd.

There are no handouts but copies of the slides can be downloaded from this logo at www.nracapital.com

Investment strategy for a volatile market !!

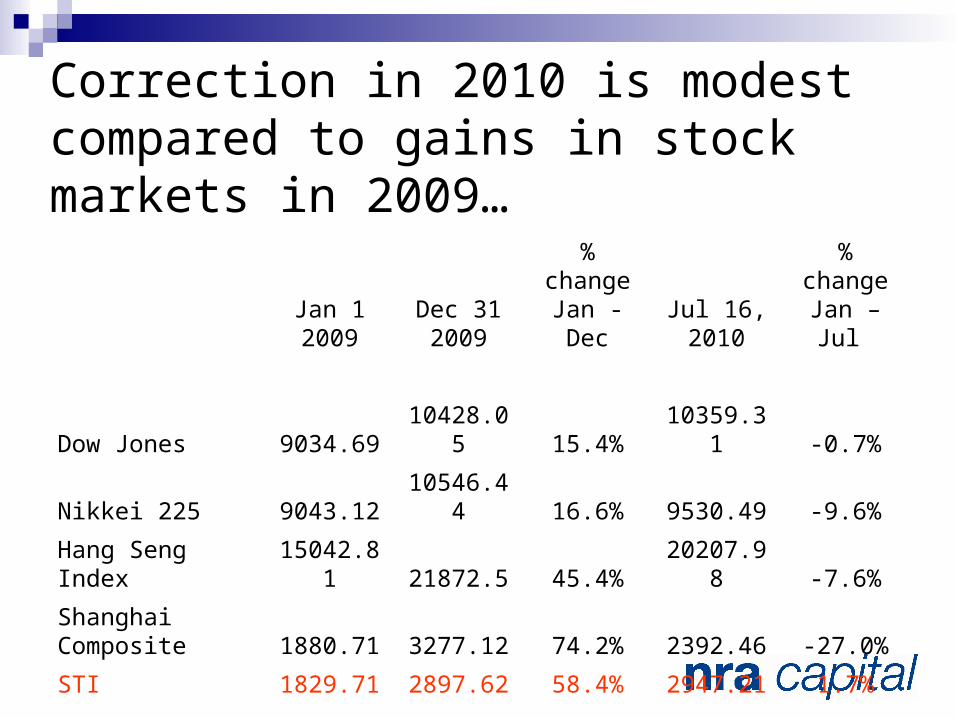

Correction in 2010 is modest compared to gains in stock markets in 2009…

Jan 1 2009

Dec 31 2009

% changeJan - Dec

Jul 16, 2010

% change Jan – Jul

Dow Jones 9034.69 10428.05 15.4% 10359.31 -0.7%

Nikkei 225 9043.12 10546.44 16.6% 9530.49 -9.6%

Hang Seng Index 15042.81 21872.5 45.4% 20207.98 -7.6%

Shanghai Composite 1880.71 3277.12 74.2% 2392.46 -27.0%

STI 1829.71 2897.62 58.4% 2947.21 1.7%

Markets appeared to be volatile in 2010 but were actually not….when compared to late 2008 and 2009

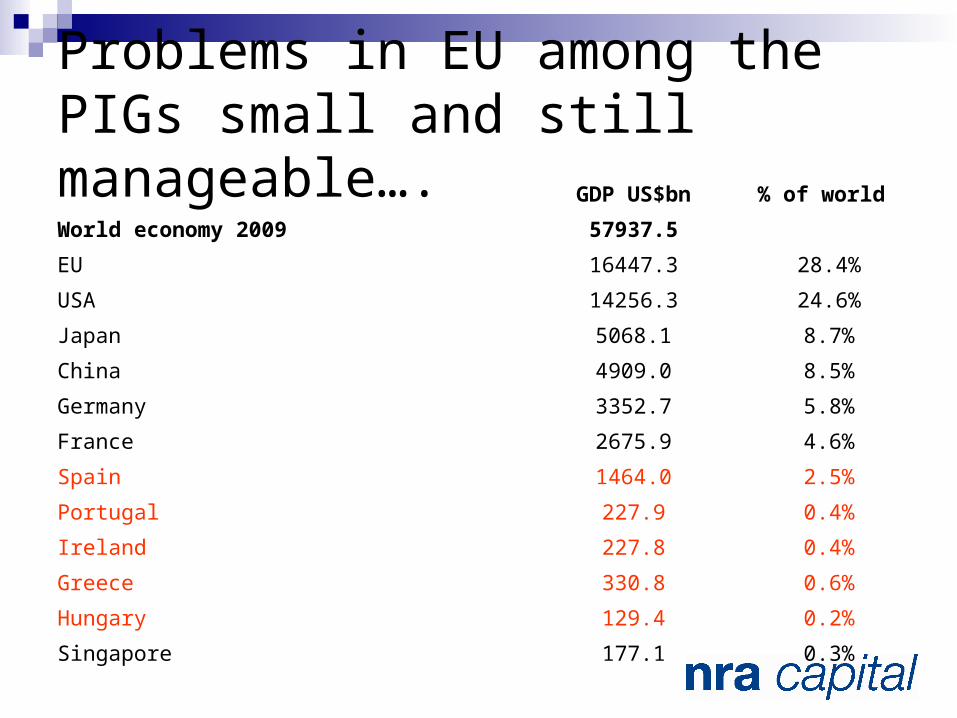

Sovereign debt crisis in Europeamong the PIGS (Portugal, Ireland, Greece and Spain)….in April 2010 started this hiccup

but the PIGS are small…..in terms of contribution to the Global economy

Problems in EU among the PIGs small and still manageable….

GDP US$bn % of world

World economy 2009 57937.5

EU 16447.3 28.4%

USA 14256.3 24.6%

Japan 5068.1 8.7%

China 4909.0 8.5%

Germany 3352.7 5.8%

France 2675.9 4.6%

Spain 1464.0 2.5%

Portugal 227.9 0.4%

Ireland 227.8 0.4%

Greece 330.8 0.6%

Hungary 129.4 0.2%

Singapore 177.1 0.3%

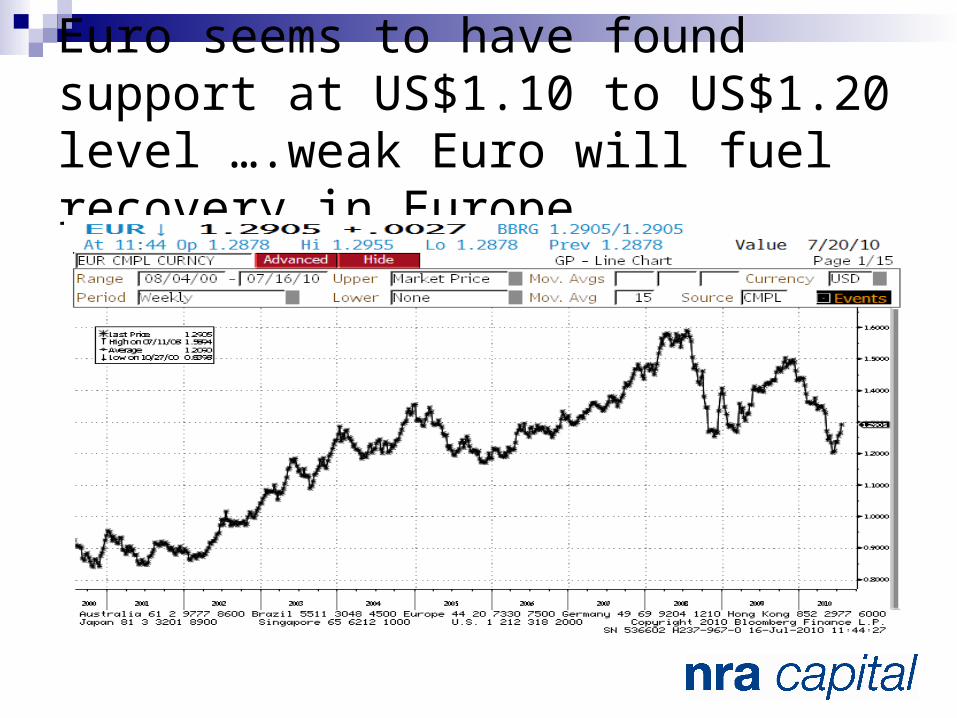

Euro seems to have found support at US$1.10 to US$1.20 level ….weak Euro will fuel recovery in Europe

Global economy recovering albeit at a more modest rate

Global economy recovering nicely from 2009 led by developing economies

World Bank – Global economy contracted by 2.1% in 2009 but forecasted to grow by 3.3% in 2010 and 3.3% in 2011

Developing economies grew by 7.1% in 2009 and forecasted to grow 8.7% in 2010 and 7.8% in 2011

US economy shrank 2.4% in 2009, but is expected to grow 3.3% in 2010 and 2.9% in 2011

China grew 8.7% in 2009 and forecasted to expand 9.5% and 8.5% in 2010 and 2011 respectively

US economy both manufacturing & services sectors are expanding

ISM Manufacturing ISM Non-Manufacturing

US unemployment near 10% but this is a lagging indicator in any economic recovery

China’s GDP chugging along nicely: 10.3% for Q2-2010 - a very good number

Investment strategy for rest of 2010 into 2011

I wanted to ask Paul the World Cup Octopus but he has pulled a mussel after being hired by Goldman Sachs for US$4.5mn

More moderate OECD economic recovery (NO DOUBLE DIP) means that global interest rates are likely to stay low until the middle of 2011 instead of Q3/Q4-2010

……equities which are “cheap” and undervalued remain the best investment class to be in

PER of the Dow at 12.7 times 2010 …low end of its historical range

PER of Shanghai now at 14.3 times 2010 at historical low since 2000

PER of Hang Seng Index now 13.4 times 2010–near historical low levels

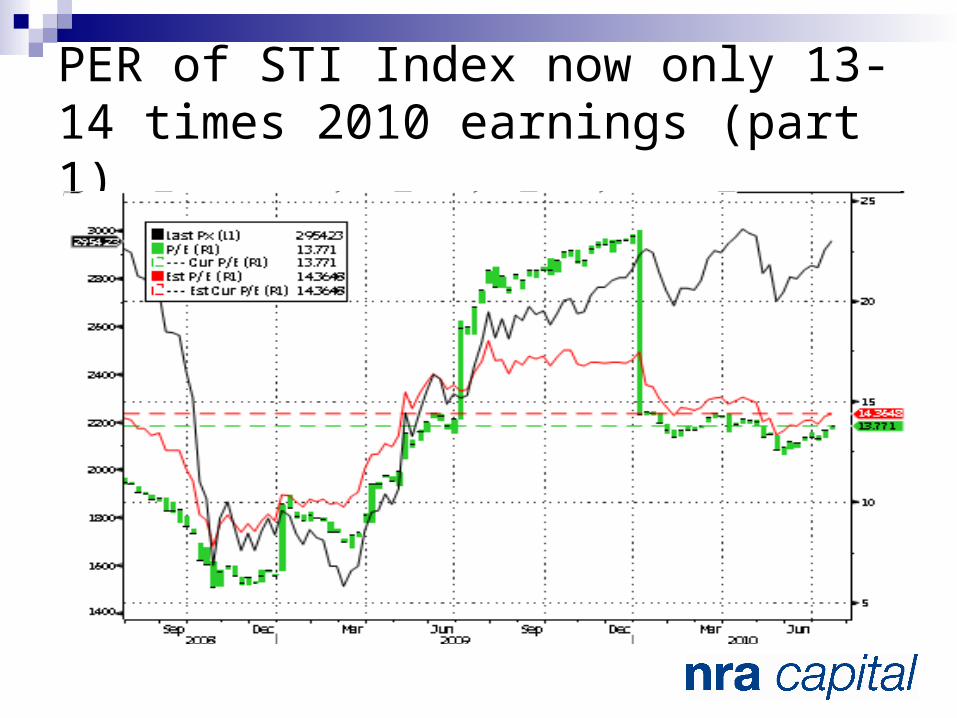

PER of STI Index now only 13-14 times 2010 earnings (part 1)

PER of STI Index now only 13-14 times FY2010 earnings– part 2

Summary Uncertainty in stock markets will continue….it took six months for

markets to stabilise after the crisis started in the US in Sept/Oct 2008….this would imply market stability sometime in Q3-2010

Look at the VIX for guidance….it rose sharply to 44 when the Euro crisis started but is now comfortably below the 30 level…..a sustained fall below 30 is a good signal to start accumulating again

Global economy on the road to recovery although growth rates in the US, EU and China are moderating.

Corporate earnings growth has been strong and stock market PERs are at their historic lows for the Dow, Shanghai, Singapore and to a lesser extent Hong Kong

My strategy….. Easy money is over - stock selection is more important now ! Until

trading liquidity returns, you need to take a six to nine month view for your stock investments

Look for undemanding PERs and attractive dividend yields as you may need to wait until Q4-2010 for markets to resume their uptrend.

I favor the technology sector (which is experiencing very strong Q1 and Q2 2010 performance and with good visibility until year end

Banks offer good exposure to the booming Singapore economy Construction stocks remain undervalued with many companies

trading below NTA and some even below cash levels….worth a look for medium term investors

Property stocks could underperform in the near term as the Government tries to control and moderate property price inflation

Dow is stabilizing and recently cut back up through its 50 and 200 day moving averages

STI Index has cut back up through its 50, 100 and 200 day moving averages

Shanghai Composite still has downside risks of another 10-20%

Stock recommendations

Visit www.nracapital.com “Kevin’s Stock Picks” …..we will soon to be releasing Stock Picks (yield)

This is only for subscribers of our premium research service but is available to investors who use or have a stock trading account with Lim and Tan Securities

Our Stock Picks have outperformed the STI Index since we started the portfolio in mid 2008

Thank You