Embed Size (px)

Citation preview

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

INVESTOR DECK CLEANTECH VENTURES

Sept 2017

This document is for informational purposes only and is neither an offer to sell nor a solicitation to buy securities

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

Over the years, the principals of Genesis Partners have achieved a successful track record of value creation through the formation and management of companies. To date Genesis Partners has successfully invested US$15 million in a diversified portfolio of start-ups and early stage companies. Greenvestment, the General Partner firm, represents a joint-partnership between Genesis Partners and MAS Recursos Naturales S.A. Greenvestment will manage CleanTech Ventures Investment Fund (CleanTech Ventures) that will continue its philosophy of investing its own capital, while opening up opportunities for new investors. It has established the fund with a spirit of a true partnership. CleanTech Ventures will have a 10-year lifespan (with a potential extension of 2 years) and will target a maximum fund size of US$27 million, of which US$13.5 million will be contributed from Limited Equity Partners (LPs) and US$13.5 million from CORFO, the Government Sponsored Economic Development Agency1. The first closing will occur at US$10 million of commitment or greater with a maximum of US$15 million. Minimum Limited Partners commitment would be at least US$2 million with an expected 25% annual drawdowns. The main financial incentives for Limited Partners include a leverage of 1:1 quasi-capital commitment from CORFO plus a project finance leverage scheme with up to 70:30 deb-to-equity ratio depending on each particular project. Greenvestment, as General Partner, will be investing directly into the fund with a commitment of 2%. The main goal is to set up a hands on investment and development fund of greenfield and brownfield non-conventional renewable energy projects, throughout an active participation, leading to successful returns expected between 2x to 2.5x capital invested over a (average) 5-year holding period. The average investment ticket will be $5.4 million, and up to US$18 million through financial leverage. Risk diversification will encompass greenfield and brownfield investments into at least three different Non-Conventional Renewable Energy (NCRE) projects, each representing no more than 10% of the total contributed capital. The Fund’s corporate governance includes SVS Supervision (Chile’s Securities & Exchange Commission), Annual Audited Financial Statements, Quarterly Management Reports, Monthly Deal flow Reports. Annual Investor Day and a 100% open door policy followed by management. The management fee will be set to US$382,000 per year (to be drawn from Private LPs only) and a success fee of 20% over a minimum nominal rate of return of 8% (annual hurdle rate). This document is meant to provide prospective Limited Partners an overview of the Greenvestment team, the Company’s Ethos and summary of CleanTech Ventures.

01- EXECUTIVE SUMMARY

1 http://www.english.corfo.cl/

4 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

02- BUSINESS OPPORTUNITY

• Over the past 10 years Non Conventional Renewable Energy (NCRE) has become a key contributor to the Chilean National Grid, due to its low environmental impact and declining engineering, construction and operational costs.

• The business opportunity to continue developing NCRE plants has particular interest to the Chilean economy, due to the great domestic energy potential and regulatory framework in place, aimed to reduce CO2 emissions by 2030, and projecting to reach 2025 with at least 20% of its energy generation footprint by means of NCRE technologies (solar, wind, hydro, biomass, etc.)

• Of all the NCRE technologies, Solar2 is the one experiencing fastest growth: 76% of Chilean NCRE projects comprise solar technology, representing 5% of the total installed capacity to the Central Interconnected System (SIC). When former President Bachelet left office back in 2014, NCRE comprised just 7% of the total Power Grid. Fast forward to 2017, these figures have more than doubled currently set at 17% (including testing centrals).

• One of the contributing factors of such growth, according to ENEL Green Power, is due to the overall cost reduction of these technologies. Costs associated to Solar panels have decreased ca.90% since 2009 and approx. 50% in wind farm installations.

• Few barriers still remain though in the expansion of a “greener” energy footprint in Chile, such as the capacity shortage in the transmission lines and several out-dated power plants presenting difficulties to adapt and interconnect with new NCRE technologies.

• In particular to green energy production, the NCRE is affected by “intermittence and variability” factors and the difficulty of storing all such energy when it is done at scale. It requires an almost close-match between supply and demand curves in order to avoid waste. Clean Tech Venture seeks to develop an innovate business model through diversification, which will allow us to generate NCRE energy minimising these “by nature” characteristics.

• It is important to note that a diversified portfolio of NCRE projects will also bring about stability to the National Power Grid.

2 http://www.latercera.com/noticia/17-la-energia-producida-chile-proviene-fuentes-renovables-no-convencionales/

6 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

• The mission of CORFO’s Development and Growth Fund is to promote and support investment vehicles that could finance and foster the development of small and medium Chilean businesses, with high growth potential and throughout their expansion phase.

• CORFO’s financial leverage could be considered quasi-capital, as it works like a debt instrument with a contingent 10 year BCU interest rate (Chile Central Bank treasury bullet bond) CPI-indexed plus a 2%, to be paid at liquidation of the fund. In the event of an adverse outcome upon which the fund could incur into losses, CORFO will not claw back on its investment.

• The leverage effect of this financial support will allow investors (Limited Partners) to raise their ROI between 5 to 10 basic points, depending on the performance of the fund.

• CORFO credit line has a minimum size of US$5 million and a maximum size of US$2 million. The debt-capital matching principle is set to 1:1 with a potential upward of 1.5:1 (debt-to-equity) upon achieving pre-established milestones. The credit line may increase or decrease by 25%. By means of project finance leverage schemes, the maximum fund “dry powder” capacity would be approximately US$80 to US$90 million.

• The beneficiaries shall be companies with a maximum initial equity capital of US$9 million.

• Loans granted under CORFO’s program shall be bullet type repayment with a maturity term not exceeding 12 years and accrue interest at the annual BCU ten-year rate for loans expressed in UF (Unidades de Fomento, an inflation adjusted metric) with interest to capitalise on an annual basis on the last day of each calendar year.

FUND CHARACTERISTICS

Capital Commitment US$ 27 million

Investors (GP and LPs) US$ 13.5 million

Debt (CORFO) US$ 13.5 million

ASSETS

LIABILITIES

EQUITY INVESTORS (50%)

CLEA

NTEC

H VE

NTUR

ES

(50%)

04- CORFO: GOVERNMENT SPONSORED DEVELOPMENT FUND

10 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

• In the event of a dividend distribution, the fund shall pay CORFO an amount equal to the total dividend distribution multiplied by the leveraged ratio used per particular NCRE3 project (in accordance with the Fund balance used to calculate the dividends to be paid out) These amounts shall pay down against any accrued interest, and principal (in the event of surplus of the annual interest).

• Upon Fund liquidation, the resulting amounts shall be paid out in accordance with the following order of priority:

! Senior creditors (non CORFO) ! Accrued interest not yet paid on the loans granted by CORFO. ! Total outstanding principal not yet repaid to CORFO ! LPs principal investments expressed in UF ! Hurdle rates ! Remaining profits according to the Fund’s bylaws schedule

• CORFO shall be paid the amount necessary to complete the total 10-year BCU +2% per annum for the loans expressed in Unidades de Fomento on the amount effectively disbursed to the Fund, to be calculated with an annually capitalised interest.

• In any event, the amount CORFO might be entitled to upon a capital distribution may not exceed 25% of the amounts available (after having paid all investors in the order of priority previously indicated). To determine this additional interest, the total re-liquidation of the loan since its first disbursement shall be effected. To this end, payments received against capital and interest shall be re-calculated to the amount effectively disbursed by CORFO to the Fund.

• In the event that no capital distribution has occurred prior to the maturity date of the loan granted by CORFO, a penalty interest of 8% per annum shall accrue, calculated on the amount of capital owed and interest, capitalized annually, calculated up to said date.

• If, as a consequence of the need to liquidate the Fund, it is deemed necessary to transfer investments to investors in shares, the price to be agreed upon will be the result of financial evaluations carried out by two industry recognised independent appraisers proposed by the Fund Manager and authorized by CORFO.

3 Different NCRE project could bear different leverage ratios.

04- CORFO: CREDIT LINE CONDITIONS

11 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

Genesis Partners is an specialised strategic and financial advisory firm as well as an investment management company. Genesis Partners advises innovative companies and institutions with high growth potential.

We manage and participate in two Venture Capital Funds throughout a General Partner firm, focusing on early stage and growth companies throughout multiple economic sectors.

To date, Genesis Ventures Fund supports five investments in Chilean companies on different sectors of the local economy.

MAS Recursos Naturales is a business consulting firm who advises in the design and building of energy projects. MAS currently holds Energy trading projects and capitalises on this up to date commodity market. All these contractual agreements will be transferred to the new Fund and become part of its intangible assets.

MAS was founded in 2014 and its goal is to become the most trusted vehicle to develop energy and natural resources projects in Chile and Latin-America.

MAS has successfully incubated a number of turn-key greenfield and brownfield projects to date. Please refer to the Annex for more references.

05- GOVERNANCE: GREENVESTMENT (GENERAL PARTNER)

13 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

CTV

Fund

GP

Project 4

Project 1

Project 3

Project 2

Investments Portfolio

Investment Committee

Supervision Committee

SVS

LP 1

LP 3

LP 2

LP 4

LP 5

05- GOVERNANCE: FUND STRUCTURE

15 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

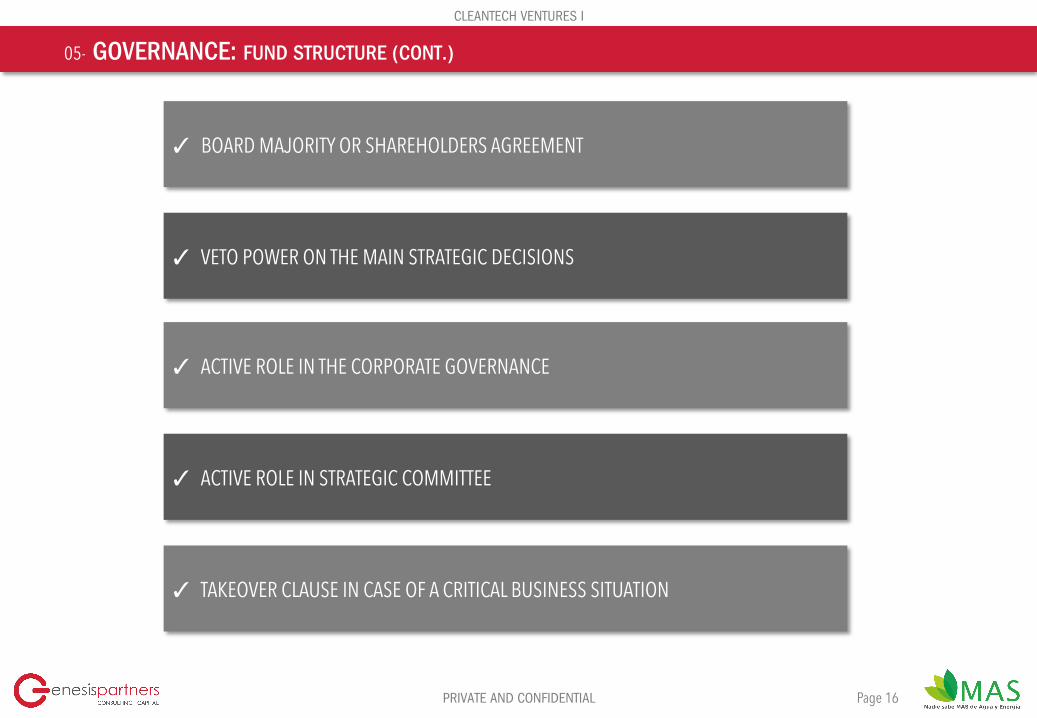

✓ BOARD MAJORITY OR SHAREHOLDERS AGREEMENT

✓ VETO POWER ON THE MAIN STRATEGIC DECISIONS

✓ ACTIVE ROLE IN THE CORPORATE GOVERNANCE

✓ ACTIVE ROLE IN STRATEGIC COMMITTEE

✓ TAKEOVER CLAUSE IN CASE OF A CRITICAL BUSINESS SITUATION

05- GOVERNANCE: FUND STRUCTURE (CONT.)

16 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

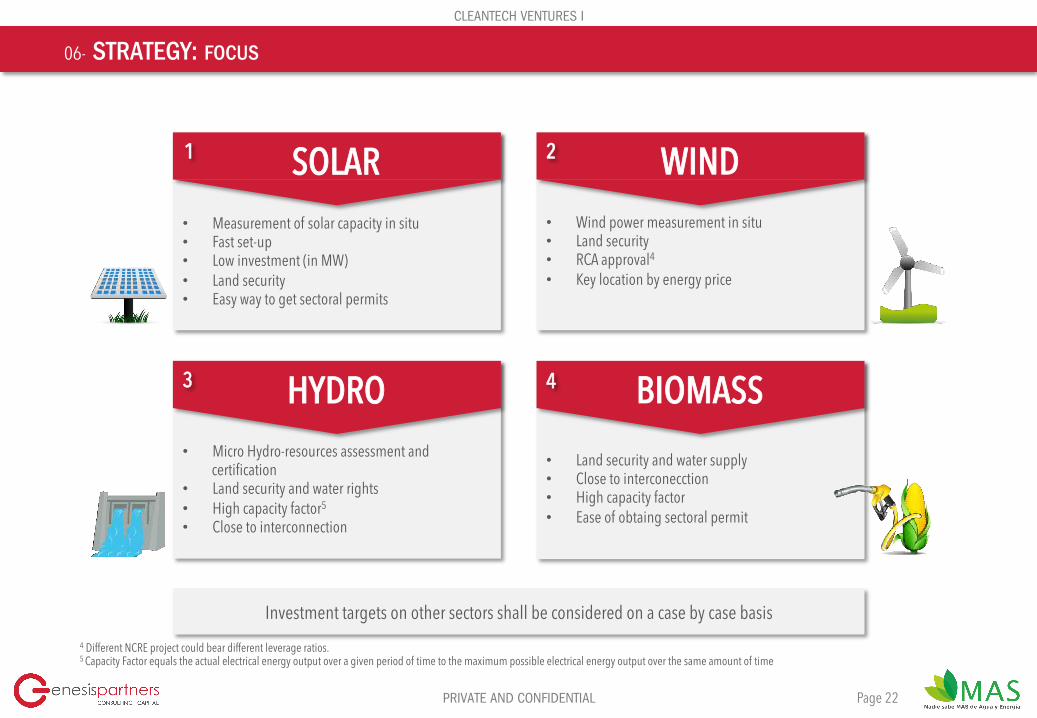

• Cleantech Ventures fosters a novel, transformational and scalable opportunity for small and medium NCRE companies, their expansion plans and capital needs. CTV required condition is to focus on commercial opportunities on medium and long term energy sales contracts.

• Cleantech’s goal is to invests on a portfolio of generation and distribution of NCRE projects, in different stages of development (design, engineering, construction and development).

• Four main streams: WIND, SOLAR, microHYDRO, and BIOFUEL, with other verticals to be considered on a case by case basis.

• Beneficiaries with an existing and maximum limited capital of US$ 9 million in accordance with CTV/CORFO bylaws

06- STRATEGY: FOCUS & DIVERSIFICATION

FOCUS

DIVERSIFICATION STRATEGY Based on 4 points: • Each investment shall be constraint to a maximum of 30% per company or project.

• Governance control throughout Shareholders agreement

• CleanTech will invest in 5 projects with an average investment ticket of US$5.4 million.

• Small and medium businesses, with an equity before investment of US$1.6 million.

21 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

• Micro Hydro-resources assessment and certification

• Land security and water rights • High capacity factor5

• Close to interconnection

• Land security and water supply • Close to interconecction • High capacity factor • Ease of obtaing sectoral permit

• Wind power measurement in situ • Land security • RCA approval4

• Key location by energy price

Investment targets on other sectors shall be considered on a case by case basis

• Measurement of solar capacity in situ • Fast set-up • Low investment (in MW) • Land security • Easy way to get sectoral permits

SOLAR

HYDRO

WIND

BIOMASS

1 2

3 4

06- STRATEGY: FOCUS

4 Different NCRE project could bear different leverage ratios. 5 Capacity Factor equals the actual electrical energy output over a given period of time to the maximum possible electrical energy output over the same amount of time

22 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

Cleantech Ventures counts with a portfolio of NCRE projects in different stages of development, able to meet the commercial commitments: Contract award notice, either by a bidding process or through free clients energy contracts. This portfolio of projects will allow CTV to set up a energy “generation curve” by means of NCRE projects subject to a BB+ risk classification by financial institutions. This energy curve has the following parameters: • Contract award will account between 55% and 70% of energy generation, with the rest to be

allocated throughout the spot sale market. • It will have a contract fulfilment minimum probability over 70% but seeking values above 80%.

Due to the main drivers of this generation curve, Clean Tech Ventures will be highly competitive and able to secure medium and long term energy contracts. One of the main features of this business model is the diversification of technologies. This will allow CTV to meet the required 24/7 supply of service mandatory contractual condition, either for free clients and/or throughout a public bidding process for regulated clients.

Sample Energy Generation Curve

06- STRATEGY: OPERATIONAL MODEL

23 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

INVESTMENT RECOMMENDATION: Buy option subject to PMGD (no PPA needed) Option Term: Two Years Ready to build from October 2017 Project Risk Guaranteed (construction and engineering)

6 PMGD are Small Distributed Energy Systems with a power output less than or equal to 9MW. Ref: http://www.sec.cl/ 7 ICC are the Norms and Regulations associated to PMGD projects. Ref: http://www.cgedistribucion.cl/productos-y-servicios/pmgd/ 8 Environmental Services Agency, Ref: http://www.sea.gob.cl/sea/quienes-somos

LA CANDELARIA

Technology Solar

Location San Francisco de Mostazal

Size 3 MW

Building Period 8 Months

Capacity Factor 25%

CAPEX required US$3.6 million

Contract PMGD6, ICC7

Permits SEA8

Geography

07- DEAL FLOW: GREENFIELD PROJECT EXAMPLES

25 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

INVESTMENT RECOMMENDATION: Buy option subject to PPA Option Term: Two Years Ready to build from October 2017 Project Risk guaranteed by Transnet9

LA ESTRELLA

Technology Wind Power

Location La Estrella

Size 50 MW

Plant Factor 30%

Environmental Approval OK

Transmission Contract Ready to be signed

Lease Contract Ready to be signed

IFC (Land Use Change) TBA

Geography

07- DEAL FLOW: GREENFIELD PROJECT EXAMPLES

9 Transnet (Grupo CGE), is a privately owned company dedicated to the transport and distribution of electrical energy services. Ref: http://www.transnet.cl/

26 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

SOLAR LO VARGAS

Technology Solar

Location Lampa

Size 3 MW

Plant Factor 21%

Distribution Contract ICC OK with ENEL / Chilectra10

Transmission Contract Ready to be signed

Lease Contract Buy Option

Mining Possessions Yes

IFC (Land Use Charges) OK

Geography

07- DEAL FLOW: GREENFIELD PROJECT EXAMPLES

INVESTMENT RECOMMENDATION: Buy Project and Land Due Diligence Pending Risk Limit Date ICC – Land Price 7 Ha

10 ENEL is a multinational energy company and one of the world’s leading integrated electricity and gas operators. Ref: https://www.enel.com/

27 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

LOS HELECHOS

Technology Mini Hydro

Location Loncoche

Size 1 MW

Plant Factor 50%

Environmental Approval OK

Distribution Contract F3 OK (Pending meeting with SAESA11

Easement Contract Pending in Forestal Arauco

Mining Possessions OK

IFC (Land Use Charges) Pending

Geography

07- DEAL FLOW: GREENFIELD PROJECT EXAMPLES

INVESTMENT RECOMMENDATION: Buy Project Due Diligence Risk Term to Get ICC – Evaluate Local Communities

11 SAESA is a privately owned company focused on energy services backed by Ontario Teachers Pension Plan Board (“OT-PPB”) and Alberta Investment Management Corp (“AIMCo”)

28 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

1) 70 MW WINDFARM: CALBUCO

2) 50 MW SOLAR: COPIAPO

3) 18 MW SOLAR: TIL TIL

4) 20 MW HYDRO: VIII y IX Región

5) 2,5 MW HYDRO: TERMAS DE CHILLAN

07- DEAL FLOW: STAND-BY PROJECTS

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

SOURCES OF DEAL FLOW OPPORTUNIES

INVESTMENT SELECTION PROCESS

POWER EACH PROJECT EXIT STRATEGY

Investment Cycle

4 EXIT STRATEGY

Where do we find a successful exit?

STRATEGIC INVESTORS: o Big competitive players such as Enel, Colbun, AES Gener, Engie, Orazul Energy, Pacific Hydro, Statkraft o Business groups that are developing a new investment diversification strategy or are looking for adding value to their core

business o Multinational companies

INSTITUTIONAL INVESTORS: o Investment Funds –venture or Private Equity- in Chile or abroad

41 Page

CLEANTECH VENTURES I

PRIVATE AND CONFIDENTIAL

INVITATION

• Opportunity to invest in a Green Energy focused Fund, to develop innovative greenfield and brownfield NCRE power plants (hydro, wind, solar, biomass) leveraging from the existing business opportunity of a domestic energy gap in the Chilean market.

• Fund target size set at US$27 million, US$13.5 million from private investors and US$13.5 million from CORFO, with a total maximum

fund size estimated at US$30 million. Holding period of 10~12 years and Target unlevered returns of 2.5x of contributed capital over an average holding period of 5 to 7 years.

• Seeking three Limited Partners able to invest US$2.7 million (with a maximum of US$4 million). US$5 million already committed from two LPs.

• Investment scheme through capital calls (with capital withdrawals after Investment Committee’s approval).

• Greenvestment (GP) to contribute US$400,000 of its own capital.

• Due date for the first capital call estimated for November 2017. Investments will be allocated on 5 projects with an average investment ticket of US$5.4 million.

• Each investment to be leveraged throughout project financing schemes using a ratio of up to 70:30, allowing a total GDV of US$18 million per project.

10- INVITATION

45 Page