Embed Size (px)

Citation preview

Investor Forum

March, 2010

Presentation outline

Overview of Hinduja Group

CV Market Outlook

AL’s Performance

Strategies / Plans

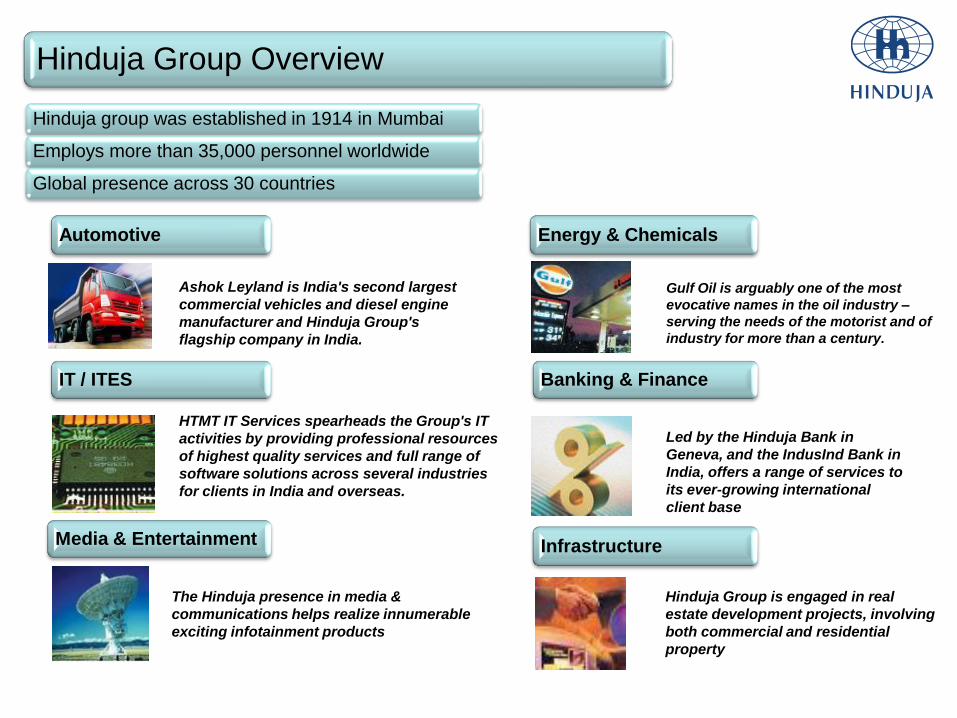

`Hinduja Group Overview

Led by the Hinduja Bank in

Geneva, and the IndusInd Bank in

India, offers a range of services to

its ever-growing international

client base

Gulf Oil is arguably one of the most

evocative names in the oil industry –

serving the needs of the motorist and of

industry for more than a century.

HTMT IT Services spearheads the Group's IT

activities by providing professional resources

of highest quality services and full range of

software solutions across several industries

for clients in India and overseas.

The Hinduja presence in media &

communications helps realize innumerable

exciting infotainment products

Hinduja Group is engaged in real

estate development projects, involving

both commercial and residential

property

Ashok Leyland is India's second largest

commercial vehicles and diesel engine

manufacturer and Hinduja Group's

flagship company in India.

Automotive

IT / ITES Banking & Finance

Infrastructure

Hinduja group was established in 1914 in Mumbai

Employs more than 35,000 personnel worldwide

Global presence across 30 countries

Media & Entertainment

Energy & Chemicals

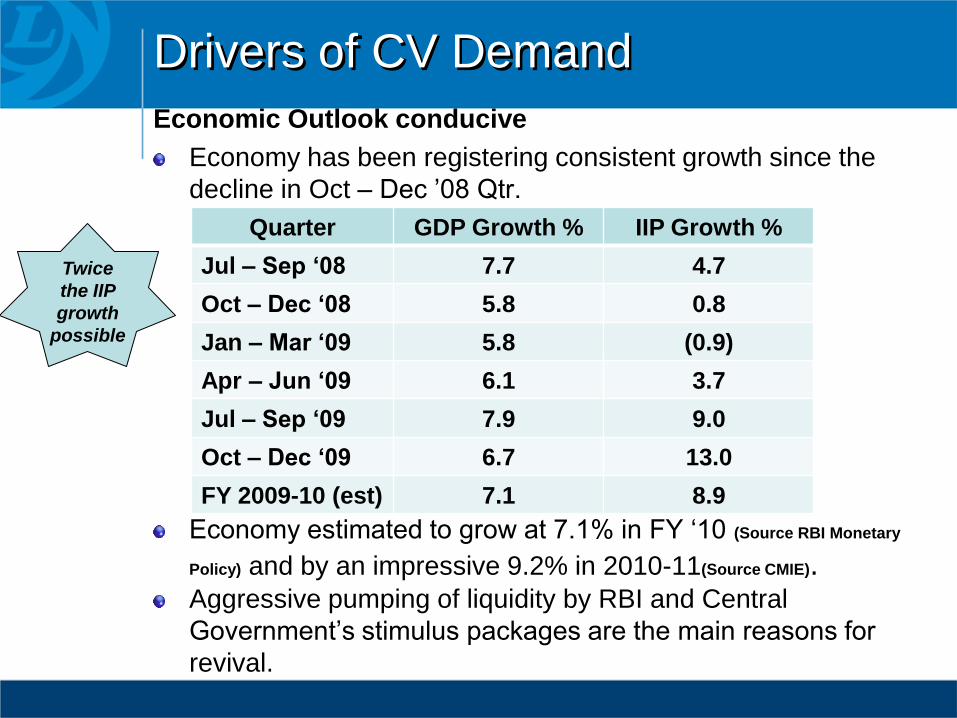

Drivers of CV Demand

Economic Outlook conducive

Economy has been registering consistent growth since the

decline in Oct – Dec ’08 Qtr.

Economy estimated to grow at 7.1% in FY ‘10 (Source RBI Monetary

Policy) and by an impressive 9.2% in 2010-11(Source CMIE).Aggressive pumping of liquidity by RBI and Central

Government’s stimulus packages are the main reasons for

revival.

Quarter GDP Growth % IIP Growth %

Jul – Sep ‘08 7.7 4.7

Oct – Dec ‘08 5.8 0.8

Jan – Mar ‘09 5.8 (0.9)

Apr – Jun ‘09 6.1 3.7

Jul – Sep ‘09 7.9 9.0

Oct – Dec ‘09 6.7 13.0

FY 2009-10 (est) 7.1 8.9

Twice

the IIP

growth

possible

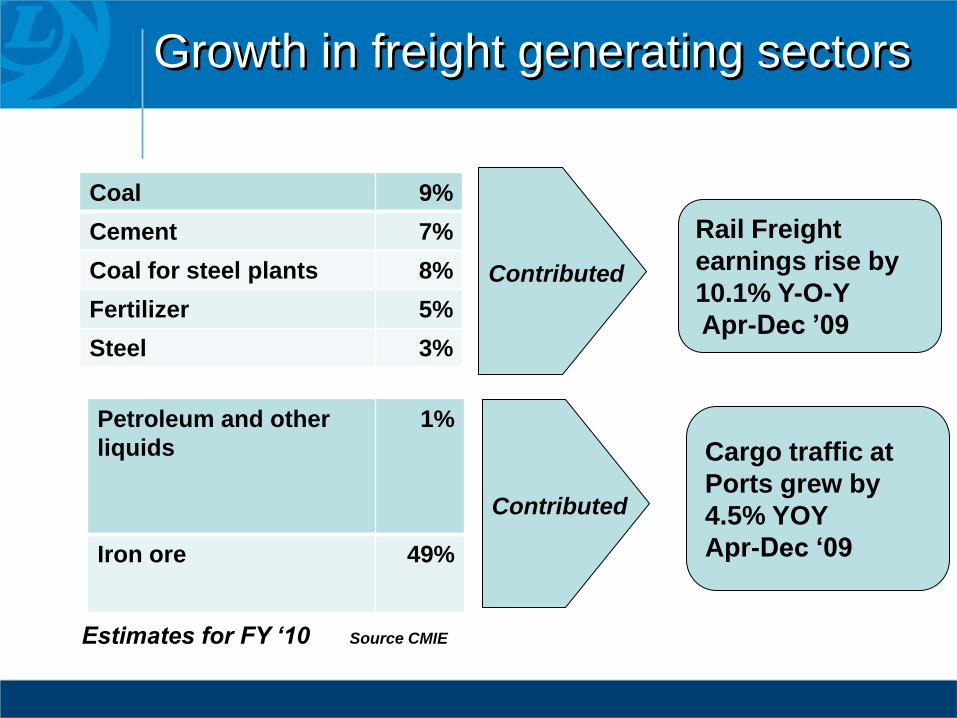

Growth in freight generating sectors

Coal 9%

Cement 7%

Coal for steel plants 8%

Fertilizer 5%

Steel 3%

Rail Freight

earnings rise by

10.1% Y-O-Y

Apr-Dec ’09

Contributed

Petroleum and other

liquids

1%

Iron ore 49%

Cargo traffic at

Ports grew by

4.5% YOY

Apr-Dec ‘09

Contributed

Estimates for FY ‘10 Source CMIE

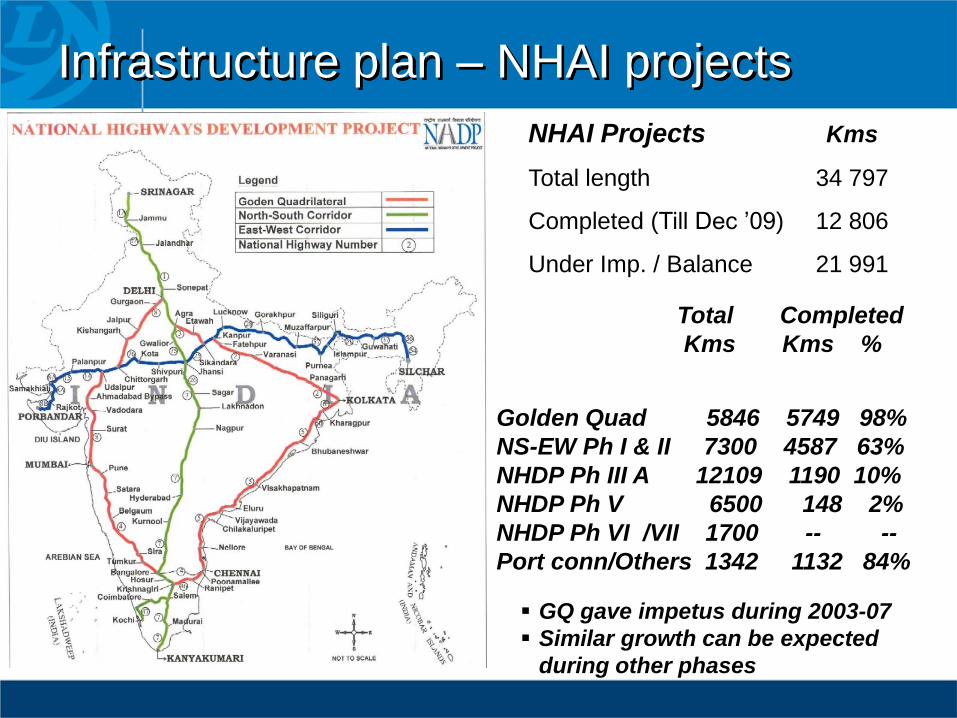

Infrastructure plan – NHAI projects

NHAI Projects Kms

Total length 34 797

Completed (Till Dec ’09) 12 806

Under Imp. / Balance 21 991

Golden Quad 5846 5749 98%

NS-EW Ph I & II 7300 4587 63%

NHDP Ph III A 12109 1190 10%

NHDP Ph V 6500 148 2%

NHDP Ph VI /VII 1700 -- --

Port conn/Others 1342 1132 84%

Total Completed

Kms Kms %

GQ gave impetus during 2003-07

Similar growth can be expected

during other phases

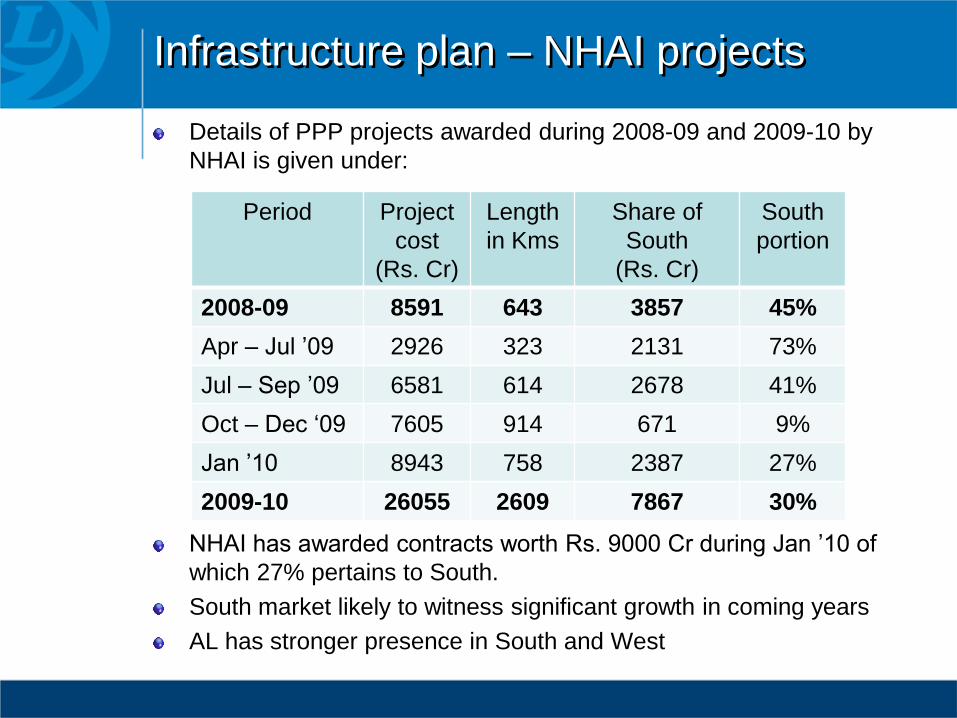

Infrastructure plan – NHAI projects

Details of PPP projects awarded during 2008-09 and 2009-10 by

NHAI is given under:

NHAI has awarded contracts worth Rs. 9000 Cr during Jan ’10 of

which 27% pertains to South.

South market likely to witness significant growth in coming years

AL has stronger presence in South and West

Period Project

cost

(Rs. Cr)

Length

in Kms

Share of

South

(Rs. Cr)

South

portion

2008-09 8591 643 3857 45%

Apr – Jul ’09 2926 323 2131 73%

Jul – Sep ’09 6581 614 2678 41%

Oct – Dec ‘09 7605 914 671 9%

Jan ’10 8943 758 2387 27%

2009-10 26055 2609 7867 30%

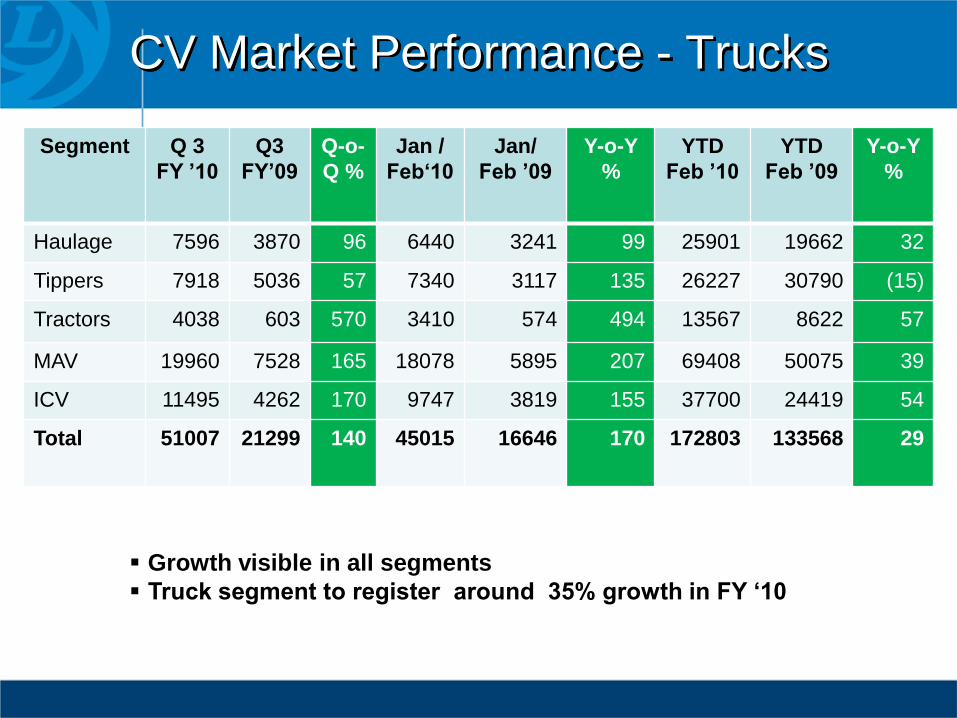

CV Market Performance - Trucks

Growth visible in all segments

Truck segment to register around 35% growth in FY ‘10

Segment Q 3

FY ’10

Q3

FY’09

Q-o-

Q %

Jan /

Feb‘10

Jan/

Feb ’09

Y-o-Y

%

YTD

Feb ’10

YTD

Feb ’09

Y-o-Y

%

Haulage 7596 3870 96 6440 3241 99 25901 19662 32

Tippers 7918 5036 57 7340 3117 135 26227 30790 (15)

Tractors 4038 603 570 3410 574 494 13567 8622 57

MAV 19960 7528 165 18078 5895 207 69408 50075 39

ICV 11495 4262 170 9747 3819 155 37700 24419 54

Total 51007 21299 140 45015 16646 170 172803 133568 29

CV Market Performance – Trucks contd…

Growth registered over Dec ‘09 in all segments

During Jan ’10, Tippers registered growth of

7% over Dec ‘09

Established players adding fleet; Good sign of

robust demand expected in near future for

MAV and Tractor segment in all regions

Positive sentiments, increased road building

activity and growth in IIP has enabled this

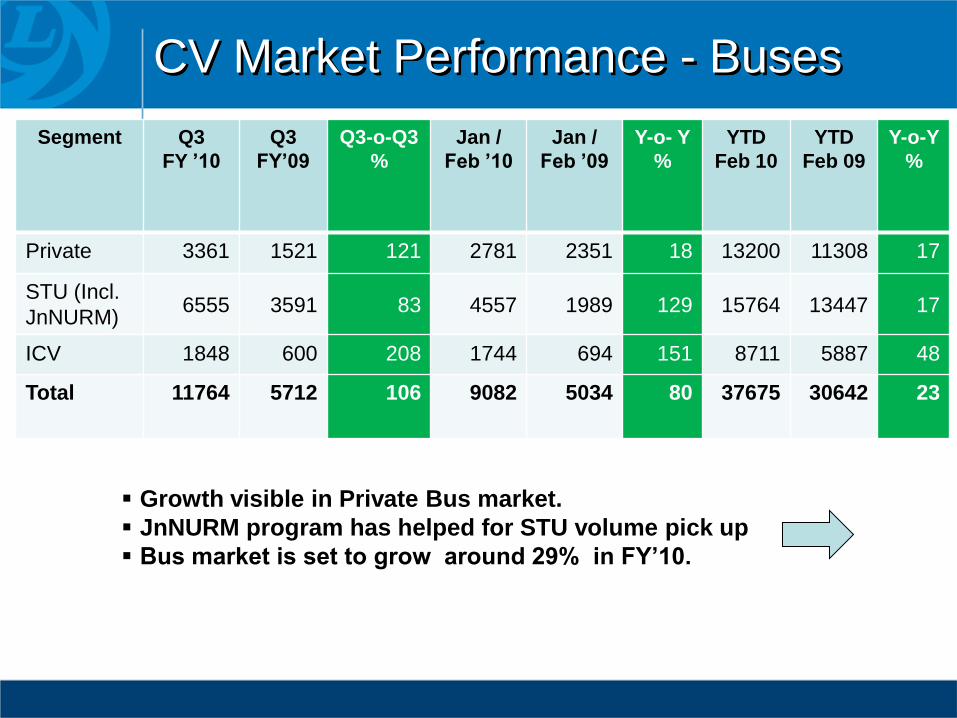

CV Market Performance - Buses

Growth visible in Private Bus market.

JnNURM program has helped for STU volume pick up

Bus market is set to grow around 29% in FY’10.

Segment Q3

FY ’10

Q3

FY’09

Q3-o-Q3

%

Jan /

Feb ’10

Jan /

Feb ’09

Y-o- Y

%

YTD

Feb 10

YTD

Feb 09

Y-o-Y

%

Private 3361 1521 121 2781 2351 18 13200 11308 17

STU (Incl.

JnNURM)6555 3591 83 4557 1989 129 15764 13447 17

ICV 1848 600 208 1744 694 151 8711 5887 48

Total 11764 5712 106 9082 5034 80 37675 30642 23

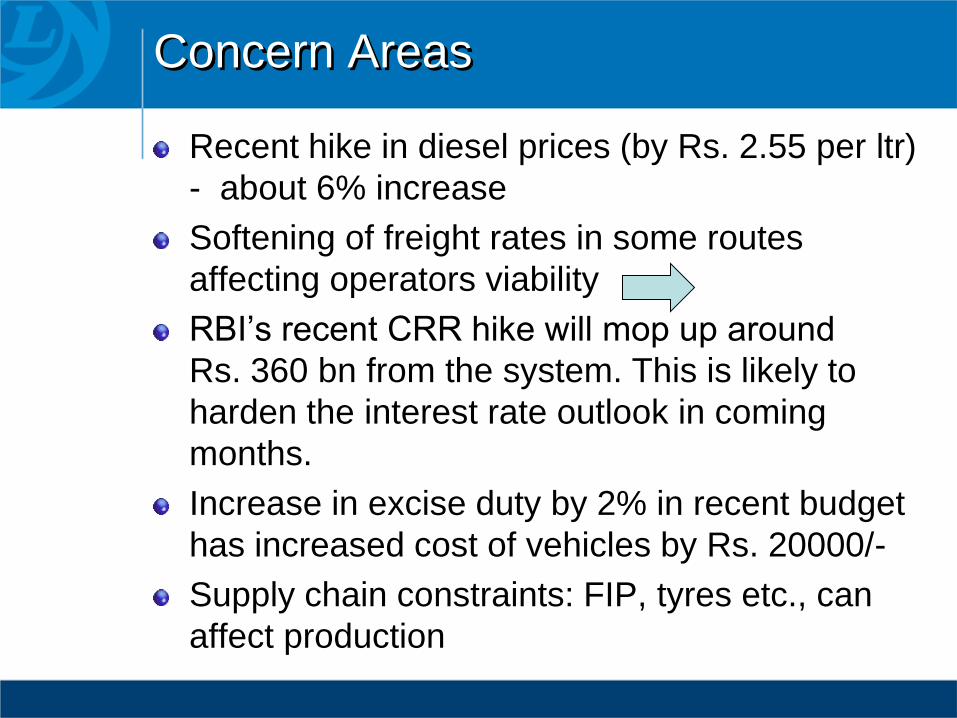

Concern Areas

Recent hike in diesel prices (by Rs. 2.55 per ltr)

- about 6% increase

Softening of freight rates in some routes

affecting operators viability

RBI’s recent CRR hike will mop up around

Rs. 360 bn from the system. This is likely to

harden the interest rate outlook in coming

months.

Increase in excise duty by 2% in recent budget

has increased cost of vehicles by Rs. 20000/-

Supply chain constraints: FIP, tyres etc., can

affect production

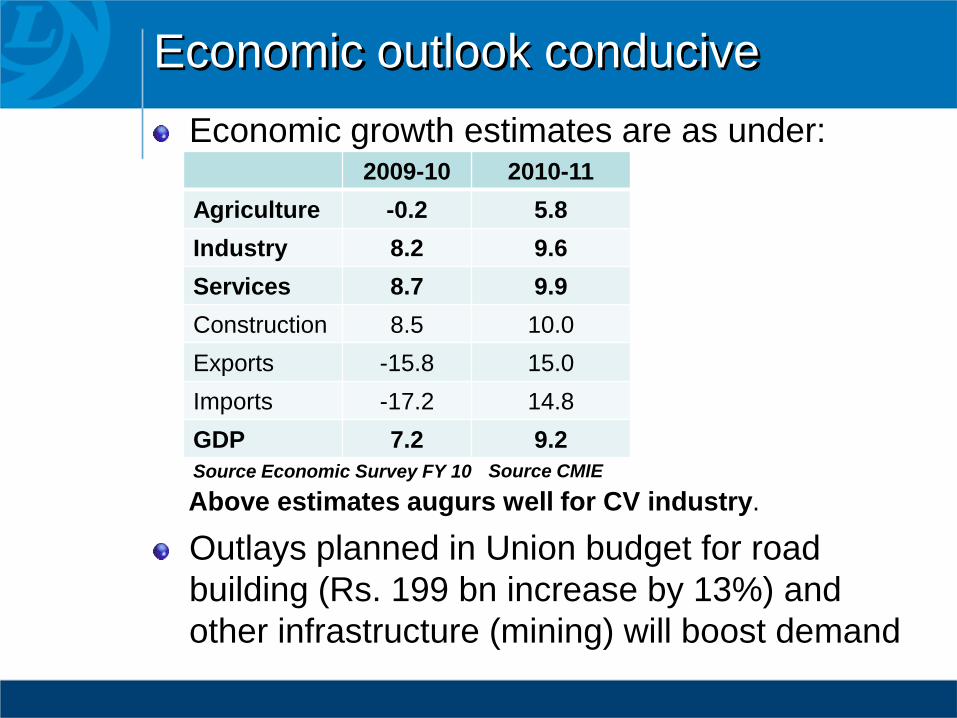

Economic outlook conducive

Economic growth estimates are as under:

Above estimates augurs well for CV industry.

Outlays planned in Union budget for road

building (Rs. 199 bn increase by 13%) and

other infrastructure (mining) will boost demand

2009-10 2010-11

Agriculture -0.2 5.8

Industry 8.2 9.6

Services 8.7 9.9

Construction 8.5 10.0

Exports -15.8 15.0

Imports -17.2 14.8

GDP 7.2 9.2

Source CMIESource Economic Survey FY 10

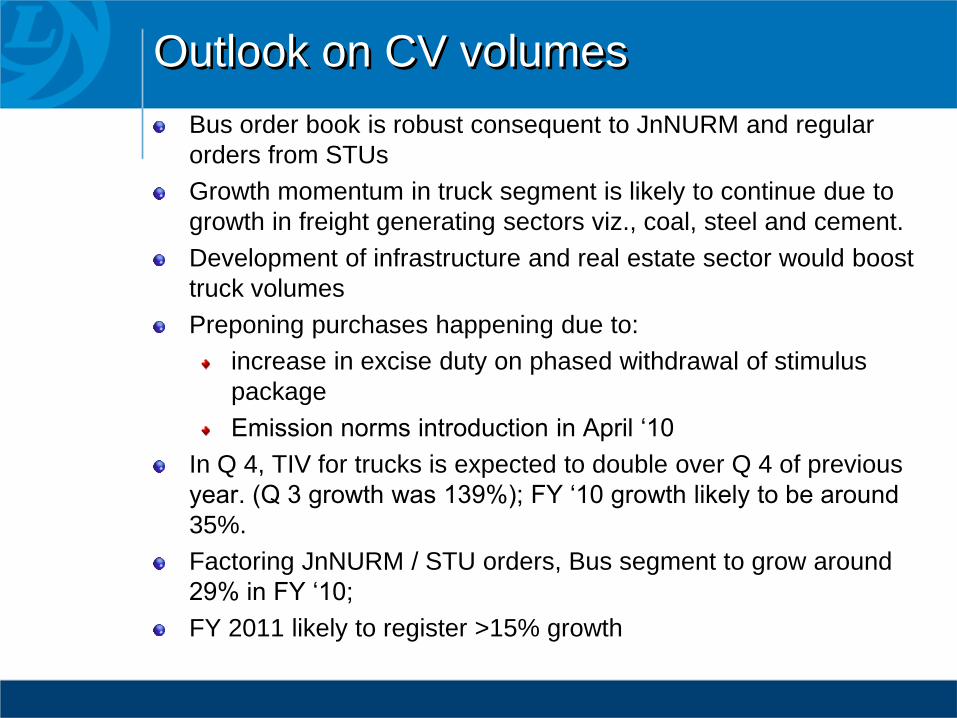

Outlook on CV volumes

Bus order book is robust consequent to JnNURM and regular

orders from STUs

Growth momentum in truck segment is likely to continue due to

growth in freight generating sectors viz., coal, steel and cement.

Development of infrastructure and real estate sector would boost

truck volumes

Preponing purchases happening due to:

increase in excise duty on phased withdrawal of stimulus

package

Emission norms introduction in April ‘10

In Q 4, TIV for trucks is expected to double over Q 4 of previous

year. (Q 3 growth was 139%); FY ‘10 growth likely to be around

35%.

Factoring JnNURM / STU orders, Bus segment to grow around

29% in FY ‘10;

FY 2011 likely to register >15% growth

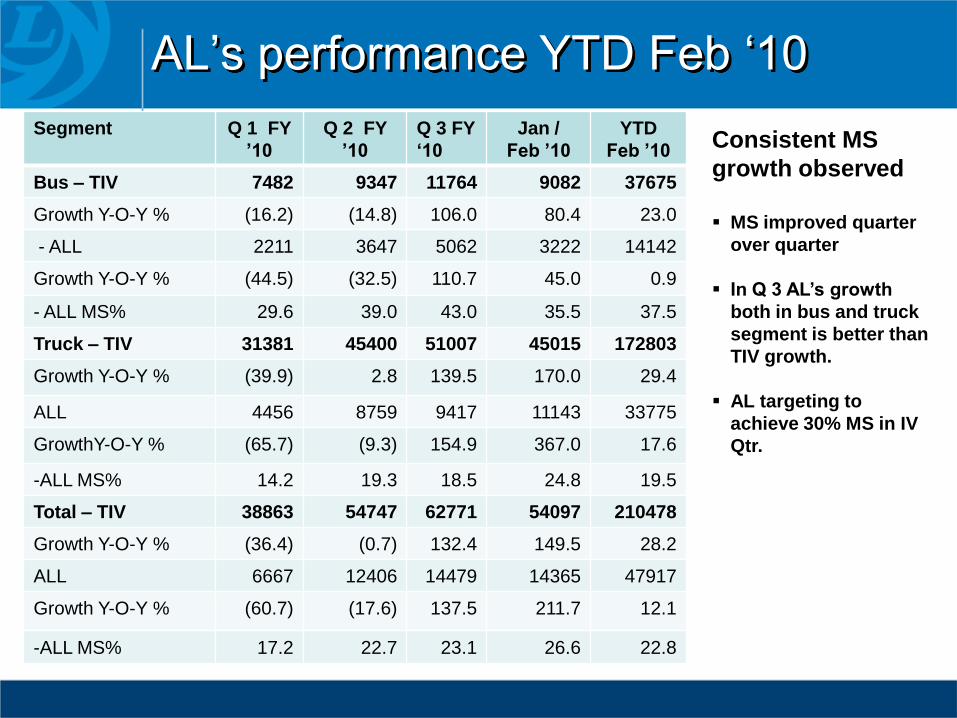

AL’s performance YTD Feb ‘10

Segment Q 1 FY

’10

Q 2 FY

’10

Q 3 FY

‘10

Jan /

Feb ’10

YTD

Feb ’10

Bus – TIV 7482 9347 11764 9082 37675

Growth Y-O-Y % (16.2) (14.8) 106.0 80.4 23.0

- ALL 2211 3647 5062 3222 14142

Growth Y-O-Y % (44.5) (32.5) 110.7 45.0 0.9

- ALL MS% 29.6 39.0 43.0 35.5 37.5

Truck – TIV 31381 45400 51007 45015 172803

Growth Y-O-Y % (39.9) 2.8 139.5 170.0 29.4

ALL 4456 8759 9417 11143 33775

GrowthY-O-Y % (65.7) (9.3) 154.9 367.0 17.6

-ALL MS% 14.2 19.3 18.5 24.8 19.5

Total – TIV 38863 54747 62771 54097 210478

Growth Y-O-Y % (36.4) (0.7) 132.4 149.5 28.2

ALL 6667 12406 14479 14365 47917

Growth Y-O-Y % (60.7) (17.6) 137.5 211.7 12.1

-ALL MS% 17.2 22.7 23.1 26.6 22.8

Consistent MS

growth observed

MS improved quarter

over quarter

In Q 3 AL’s growth

both in bus and truck

segment is better than

TIV growth.

AL targeting to

achieve 30% MS in IV

Qtr.

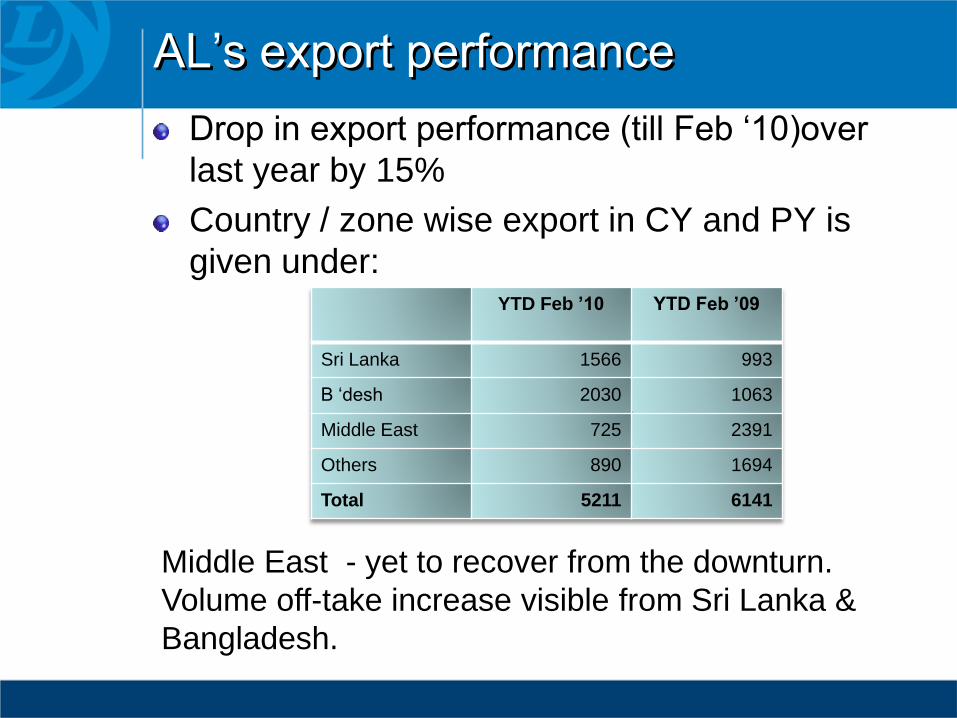

AL’s export performance

Drop in export performance (till Feb ‘10)over

last year by 15%

Country / zone wise export in CY and PY is

given under:YTD Feb ’10 YTD Feb ’09

Sri Lanka 1566 993

B ‘desh 2030 1063

Middle East 725 2391

Others 890 1694

Total 5211 6141

Middle East - yet to recover from the downturn.

Volume off-take increase visible from Sri Lanka &

Bangladesh.

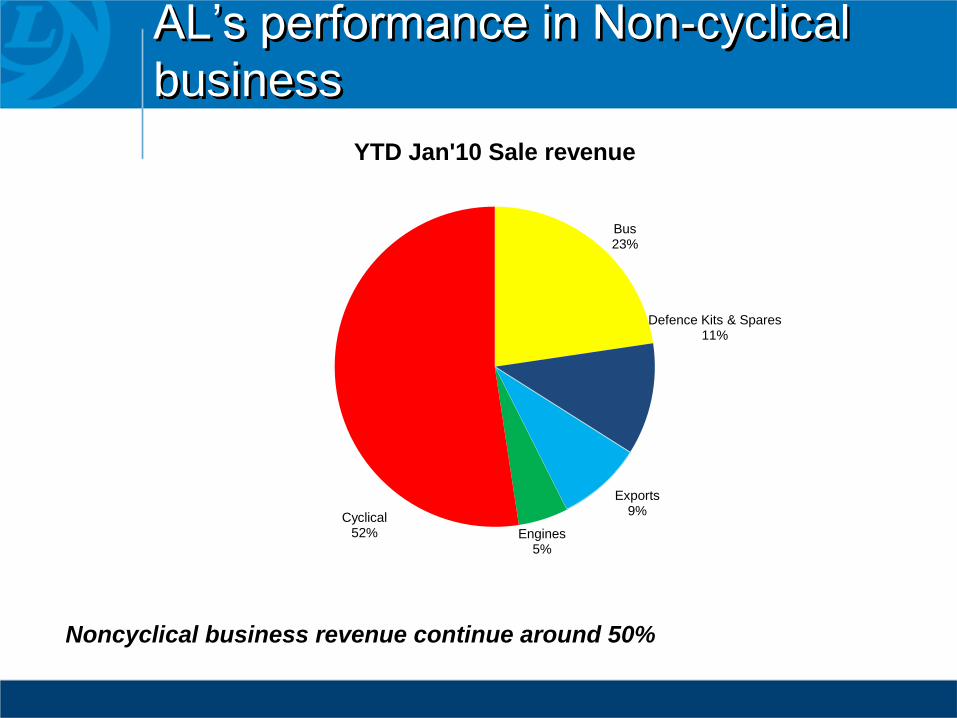

AL’s performance in Non-cyclical

business

Noncyclical business revenue continue around 50%

Bus23%

Defence Kits & Spares11%

Exports9%

Engines5%

Cyclical52%

YTD Jan'10 Sale revenue

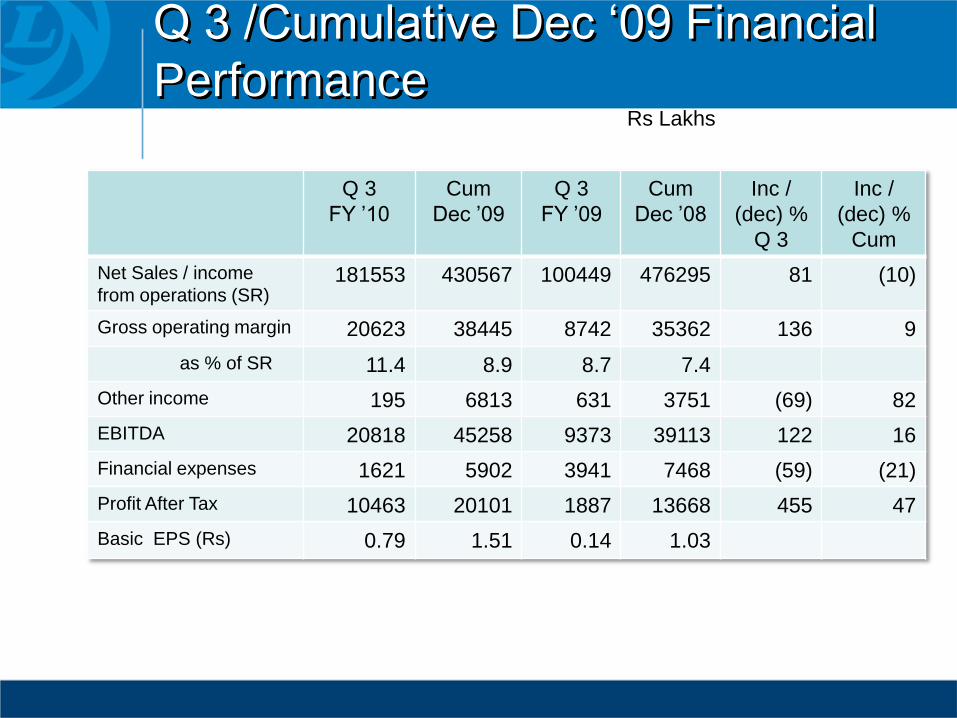

Q 3 /Cumulative Dec ‘09 Financial

Performance

Q 3

FY ’10

Cum

Dec ’09

Q 3

FY ’09

Cum

Dec ’08

Inc /

(dec) %

Q 3

Inc /

(dec) %

Cum

Net Sales / income

from operations (SR)181553 430567 100449 476295 81 (10)

Gross operating margin 20623 38445 8742 35362 136 9

as % of SR 11.4 8.9 8.7 7.4

Other income 195 6813 631 3751 (69) 82

EBITDA 20818 45258 9373 39113 122 16

Financial expenses 1621 5902 3941 7468 (59) (21)

Profit After Tax 10463 20101 1887 13668 455 47

Basic EPS (Rs) 0.79 1.51 0.14 1.03

Rs Lakhs

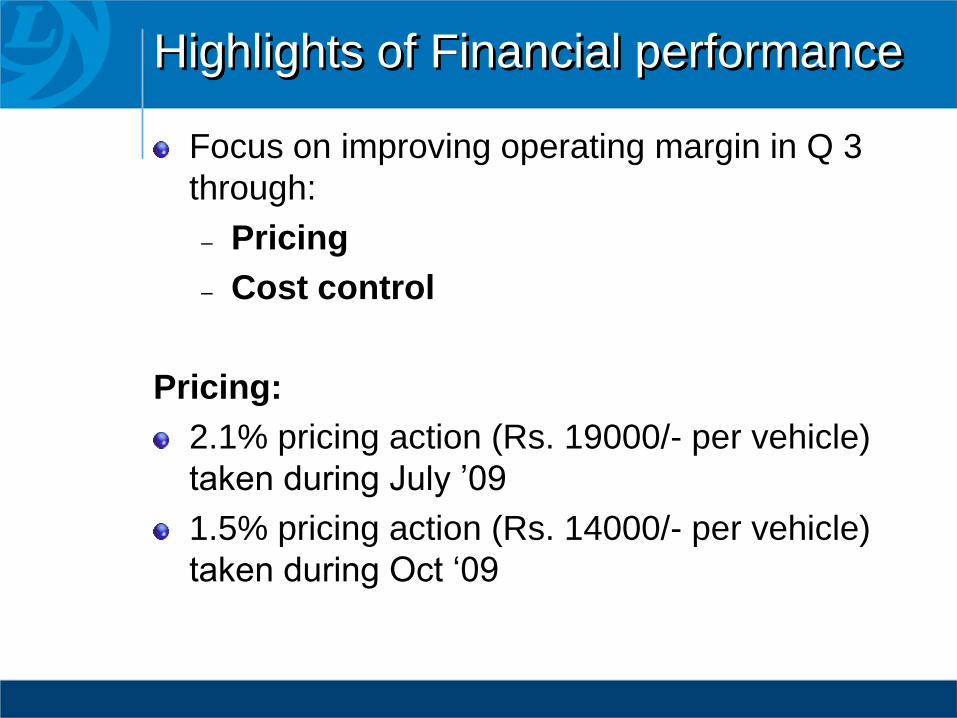

Highlights of Financial performance

Focus on improving operating margin in Q 3

through:

– Pricing

– Cost control

Pricing:

2.1% pricing action (Rs. 19000/- per vehicle)

taken during July ’09

1.5% pricing action (Rs. 14000/- per vehicle)

taken during Oct ‘09

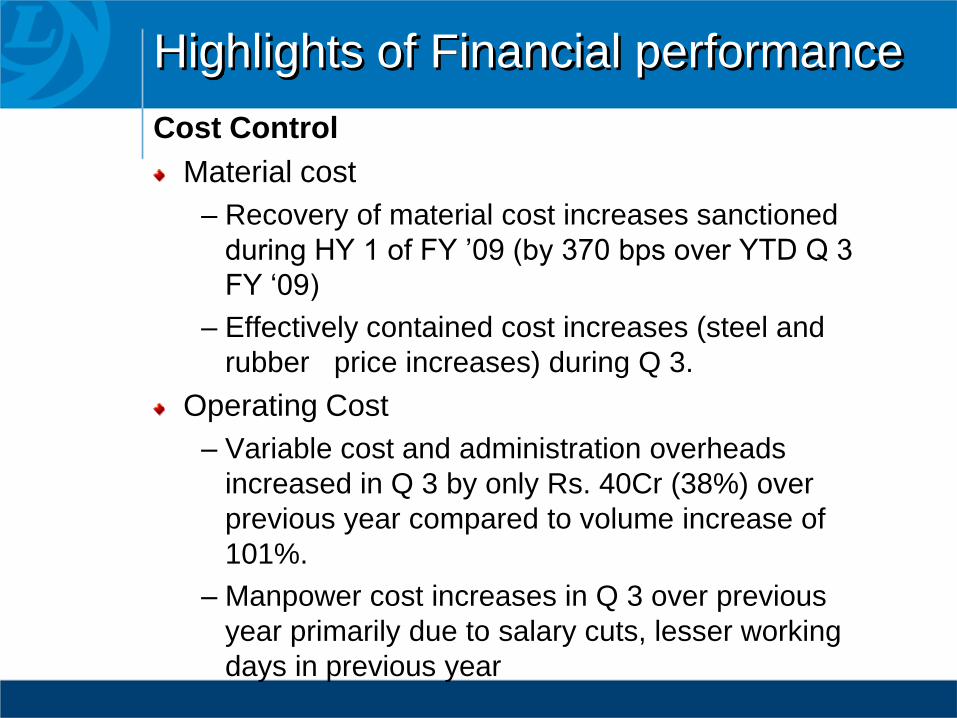

Highlights of Financial performance

Cost Control

Material cost

– Recovery of material cost increases sanctioned

during HY 1 of FY ’09 (by 370 bps over YTD Q 3

FY ‘09)

– Effectively contained cost increases (steel and

rubber price increases) during Q 3.

Operating Cost

– Variable cost and administration overheads

increased in Q 3 by only Rs. 40Cr (38%) over

previous year compared to volume increase of

101%.

– Manpower cost increases in Q 3 over previous

year primarily due to salary cuts, lesser working

days in previous year

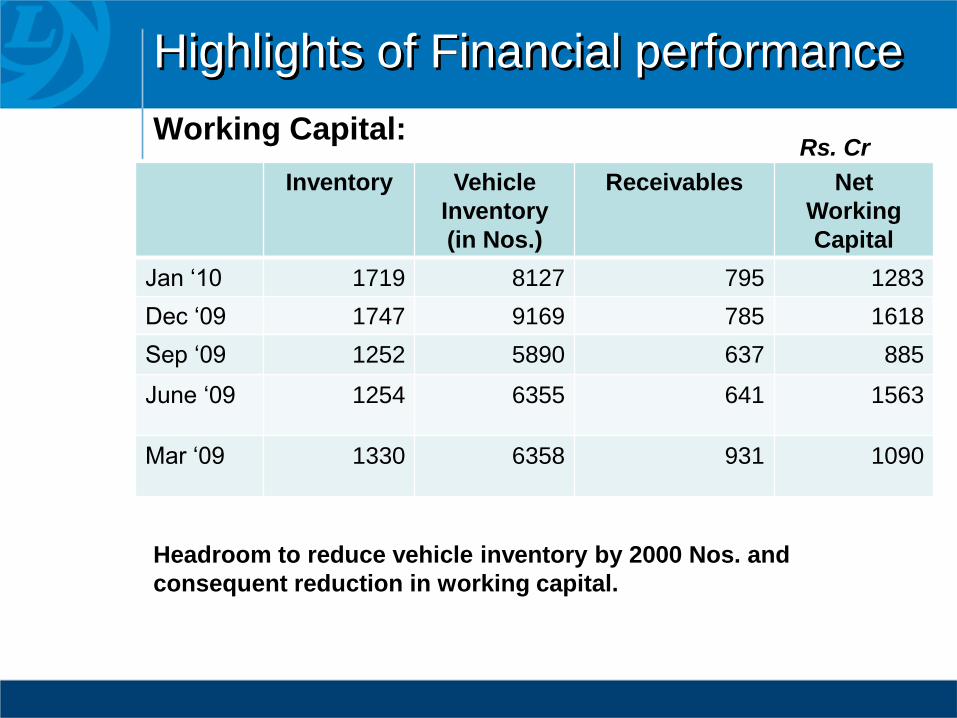

Highlights of Financial performance

Working Capital:

Inventory Vehicle

Inventory

(in Nos.)

Receivables Net

Working

Capital

Jan ‘10 1719 8127 795 1283

Dec ‘09 1747 9169 785 1618

Sep ‘09 1252 5890 637 885

June ‘09 1254 6355 641 1563

Mar ‘09 1330 6358 931 1090

Rs. Cr

Headroom to reduce vehicle inventory by 2000 Nos. and

consequent reduction in working capital.

Strategies/Plans

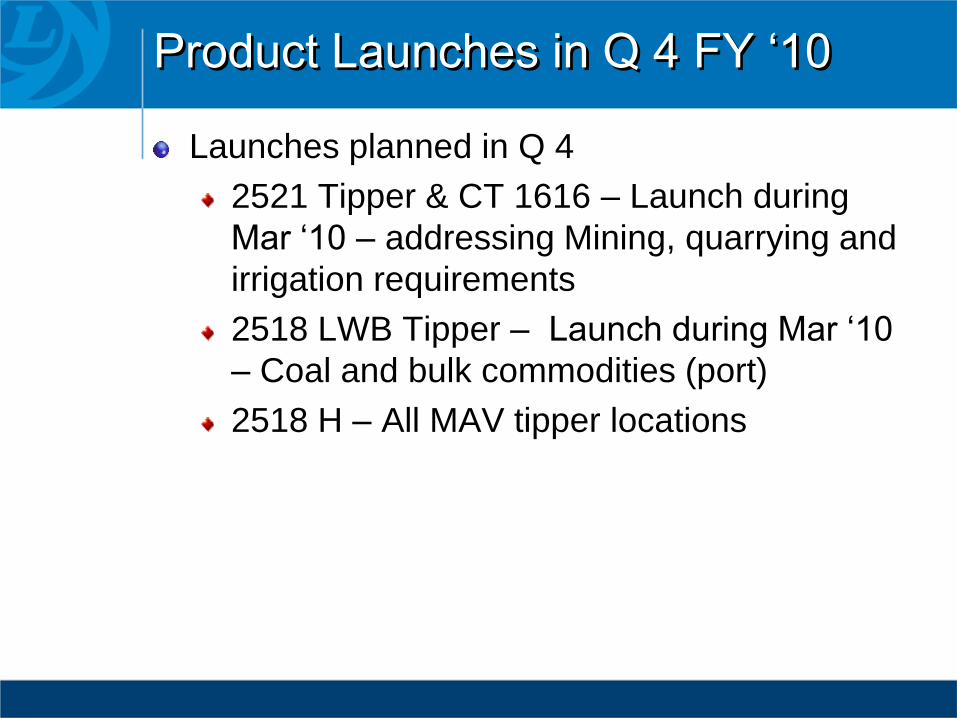

Product Launches in Q 4 FY ‘10

Launches planned in Q 4

2521 Tipper & CT 1616 – Launch during

Mar ‘10 – addressing Mining, quarrying and

irrigation requirements

2518 LWB Tipper – Launch during Mar ‘10

– Coal and bulk commodities (port)

2518 H – All MAV tipper locations

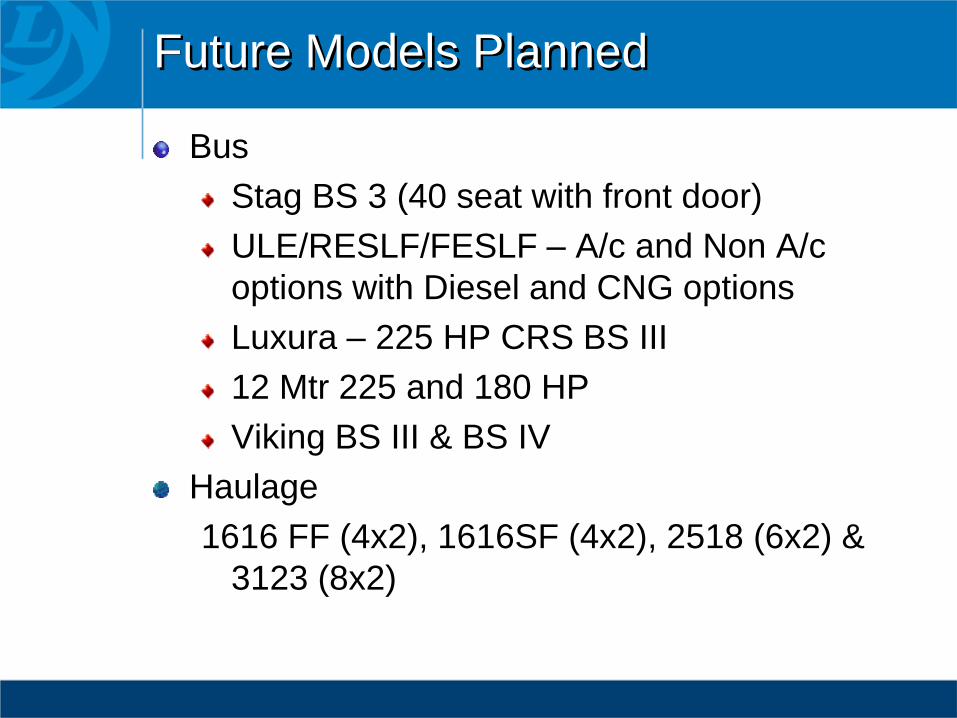

Future Models Planned

Bus

Stag BS 3 (40 seat with front door)

ULE/RESLF/FESLF – A/c and Non A/c

options with Diesel and CNG options

Luxura – 225 HP CRS BS III

12 Mtr 225 and 180 HP

Viking BS III & BS IV

Haulage

1616 FF (4x2), 1616SF (4x2), 2518 (6x2) &

3123 (8x2)

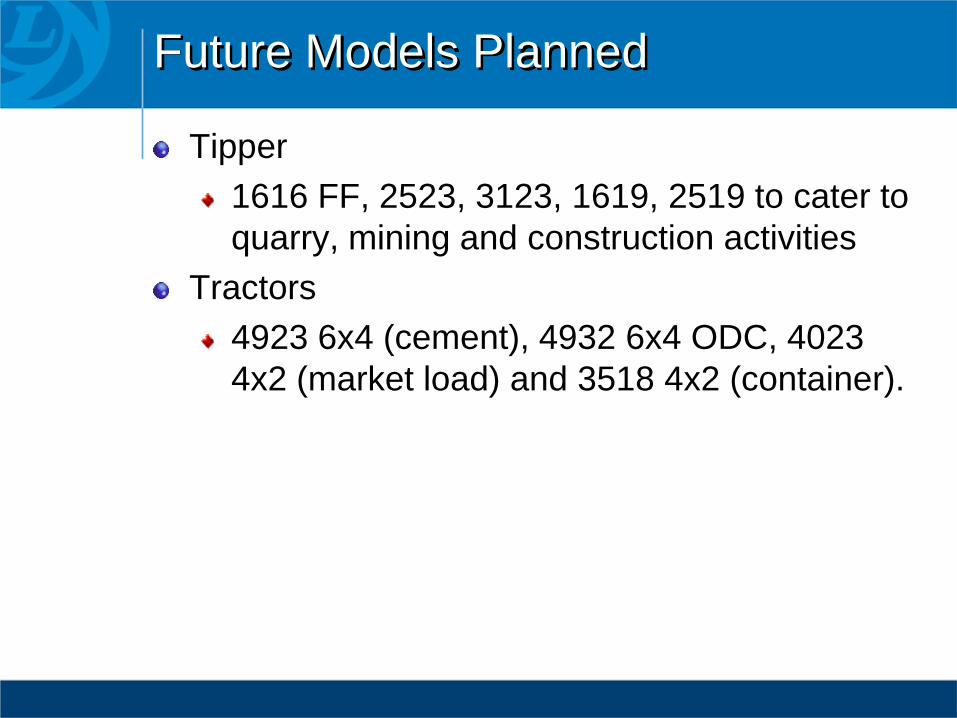

Future Models Planned

Tipper

1616 FF, 2523, 3123, 1619, 2519 to cater to

quarry, mining and construction activities

Tractors

4923 6x4 (cement), 4932 6x4 ODC, 4023

4x2 (market load) and 3518 4x2 (container).

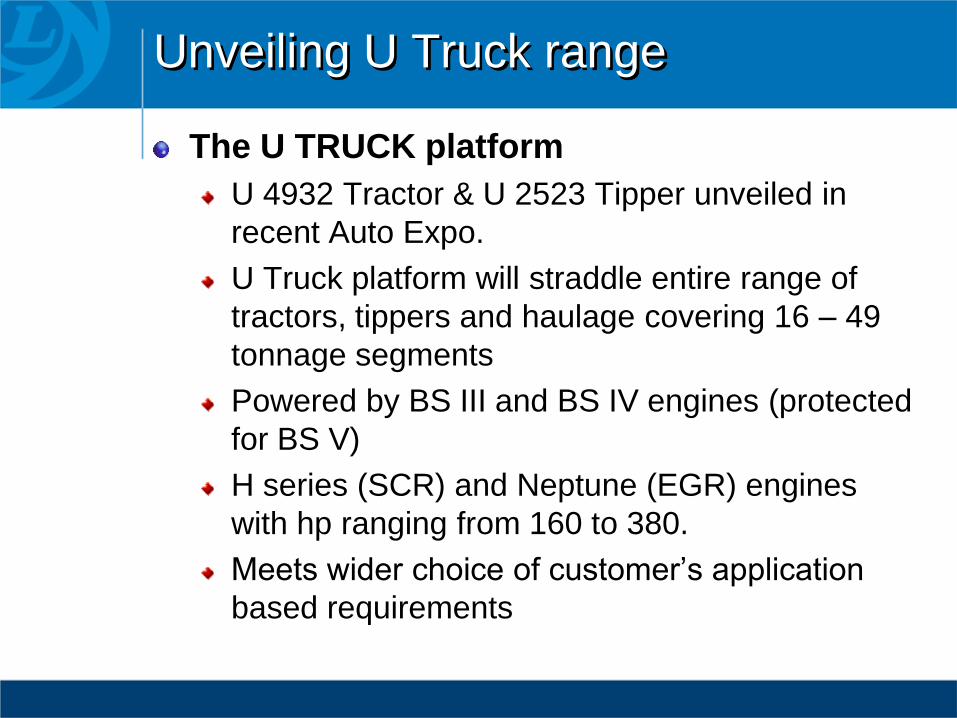

Unveiling U Truck range

The U TRUCK platform

U 4932 Tractor & U 2523 Tipper unveiled in

recent Auto Expo.

U Truck platform will straddle entire range of

tractors, tippers and haulage covering 16 – 49

tonnage segments

Powered by BS III and BS IV engines (protected

for BS V)

H series (SCR) and Neptune (EGR) engines

with hp ranging from 160 to 380.

Meets wider choice of customer’s application

based requirements

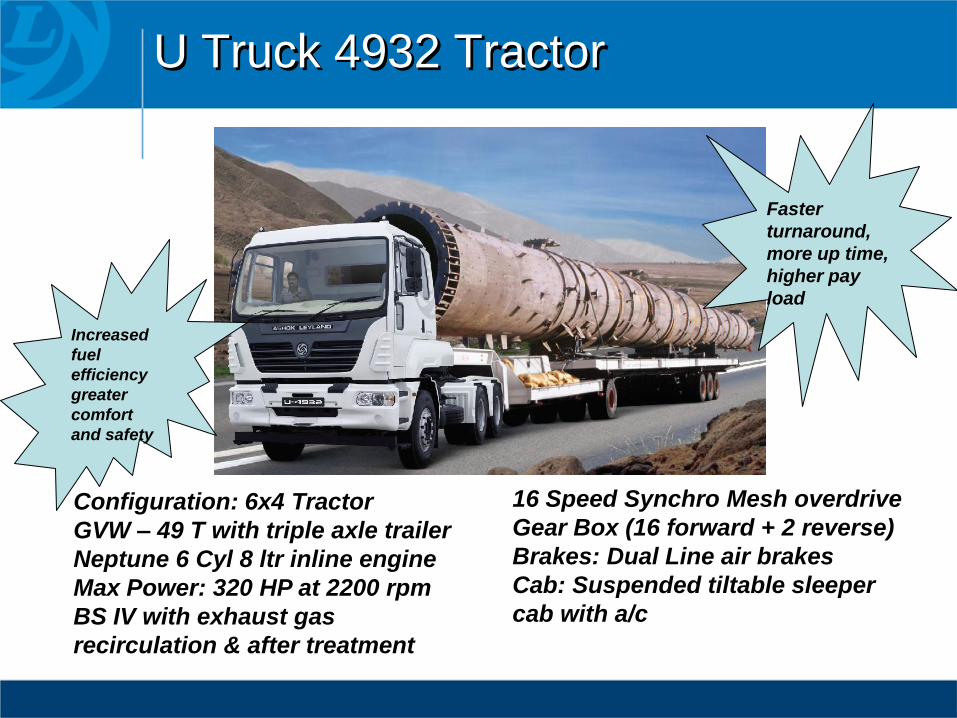

U Truck 4932 Tractor

Configuration: 6x4 Tractor

GVW – 49 T with triple axle trailer

Neptune 6 Cyl 8 ltr inline engine

Max Power: 320 HP at 2200 rpm

BS IV with exhaust gas

recirculation & after treatment

16 Speed Synchro Mesh overdrive

Gear Box (16 forward + 2 reverse)

Brakes: Dual Line air brakes

Cab: Suspended tiltable sleeper

cab with a/c

Faster

turnaround,

more up time,

higher pay

load

Increased

fuel

efficiency

greater

comfort

and safety

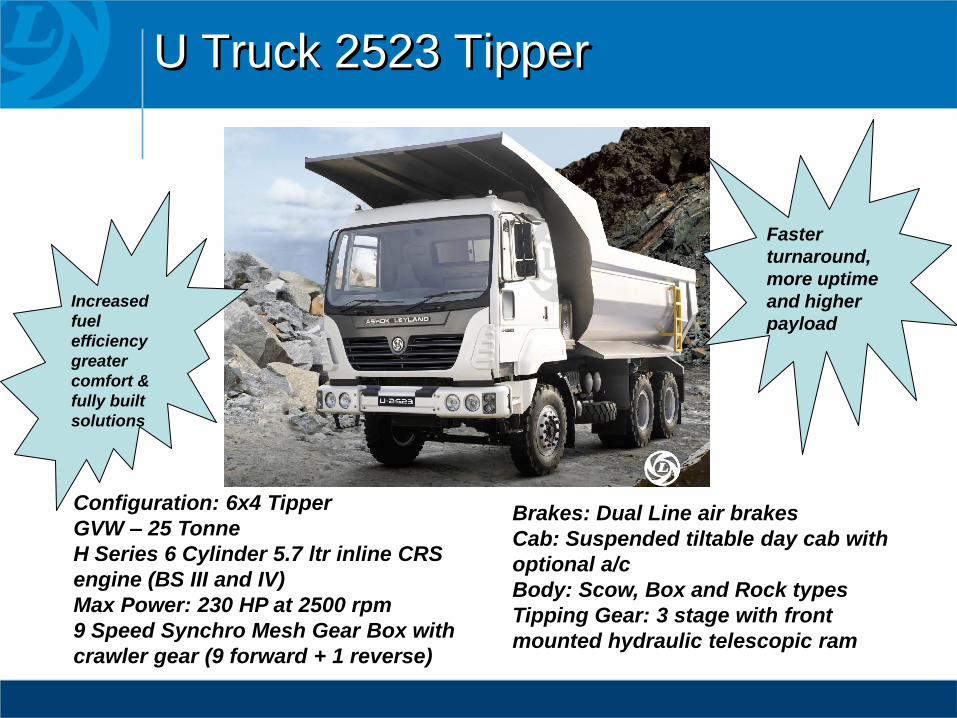

U Truck 2523 Tipper

Configuration: 6x4 Tipper

GVW – 25 Tonne

H Series 6 Cylinder 5.7 ltr inline CRS

engine (BS III and IV)

Max Power: 230 HP at 2500 rpm

9 Speed Synchro Mesh Gear Box with

crawler gear (9 forward + 1 reverse)

Brakes: Dual Line air brakes

Cab: Suspended tiltable day cab with

optional a/c

Body: Scow, Box and Rock types

Tipping Gear: 3 stage with front

mounted hydraulic telescopic ram

Increased

fuel

efficiency

greater

comfort &

fully built

solutions

Faster

turnaround,

more uptime

and higher

payload

EFFI Truck

EFFI truck unveiled

in recent Auto expo

with emphasis on

green and efficient

transportation. EFFI

embodies 20

technology

enhancements

with 20% better fuel

efficiency and 20%

reduction in CO2

emissions

India’s first plug-in CNG hybrid bus

& intelligent vehicle

Hybus India’s first plug-in CNG

hybrid bus was unveiled by AL in

recent auto expo.

Greener than CNG, 20-30% more fuel

efficient than a conventional bus

AL and Cisco signed an MOU to develop

sector specific solution to enable vehicle

to infrastructure communication. Focus

on transportation management,

emergency medical and mobile security

- targeted at Defence and Govt sectors.

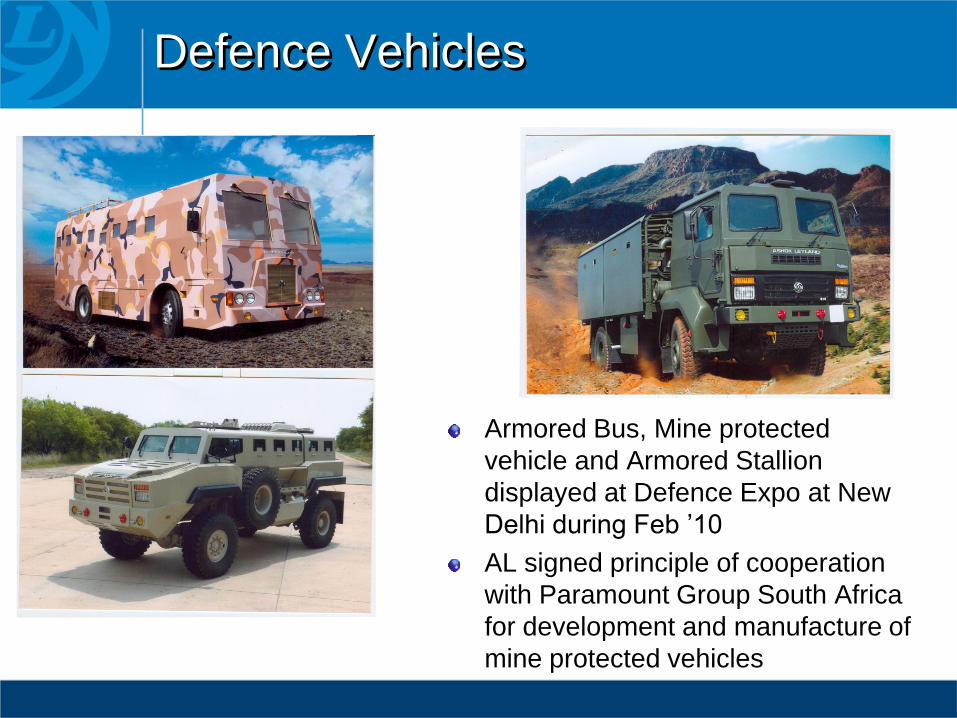

Defence Vehicles

Armored Bus, Mine protected

vehicle and Armored Stallion

displayed at Defence Expo at New

Delhi during Feb ’10

AL signed principle of cooperation

with Paramount Group South Africa

for development and manufacture of

mine protected vehicles

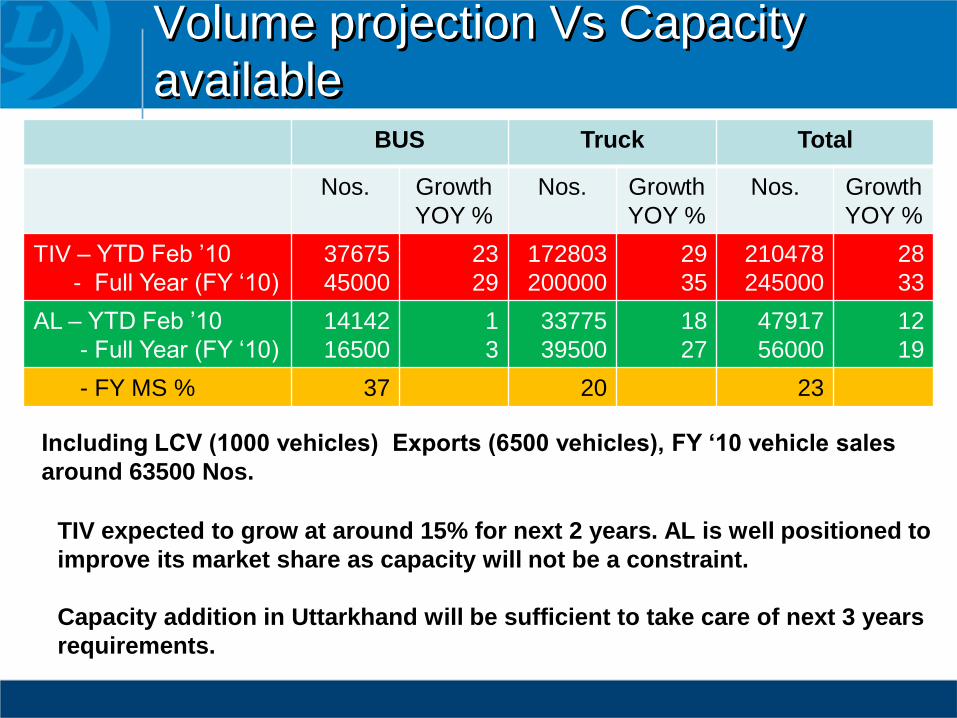

Volume projection Vs Capacity

availableBUS Truck Total

Nos. Growth

YOY %

Nos. Growth

YOY %

Nos. Growth

YOY %

TIV – YTD Feb ’10

- Full Year (FY ‘10)

37675

45000

23

29

172803

200000

29

35

210478

245000

28

33

AL – YTD Feb ’10

- Full Year (FY ‘10)

14142

16500

1

3

33775

39500

18

27

47917

56000

12

19

- FY MS % 37 20 23

Including LCV (1000 vehicles) Exports (6500 vehicles), FY ‘10 vehicle sales

around 63500 Nos.

TIV expected to grow at around 15% for next 2 years. AL is well positioned to

improve its market share as capacity will not be a constraint.

Capacity addition in Uttarkhand will be sufficient to take care of next 3 years

requirements.

Capacity creation at Uttarakhand

Uttarakhand plant would be highly integrated plant of

AL.

Total investment in the plant > Rs. 1100 Cr.

Supply sources identified within tax exempted areas

in Uttarakhand / Himachal Pradesh

All facilities commissioned on 5th Mar.2010

AL is likely to benefit from logistics for supply to

North, East and Western markets from this facility

Targeting to produce around 500 vehicles during

Mar. 2010

Capacity utilisation at Uttarakhand will be maximised

to secure these benefits in next few years

Margin Outlook

Targeting operating margins at around Q 3

levels for Q 4 to be supported by:

Pricing action Rs. 14500/- per vehicle

(1.4%) taken during Jan ‘10

Commodity based price increase pressure

(mainly steel, rubber and aluminum) to be

contained

Stringent controls on operating cost

incurrence to continue

Mix adverse due to higher quantum of STU

and JnNURM orders in Q 4

Full year margins targeted at around 10% of revenue

Light truck JV with Nissan

LCV JV progressing well

Understanding with NML for utilising existing

facilities of both partners to minimize initial

investment and maximise utilisation of capacity

on ground

Targeting to invest from AL around Rs. 400 Cr.

In next few years

Product range being discussed with JV partner

and decision to be taken shortly

Product introduction in 2011.

Construction equipment JV with John

Deere

New company formed with 50:50 partnership

with John Deere

Land already acquired;

Product plans in place;

Roll out before Dec 2010

Joint venture with ALTEAMS

Fully established to meet both Telecom and

automobile sector requirements

Supplies commenced to telecom industry

components.

Formal dedication of factory on 20th Jan ‘10

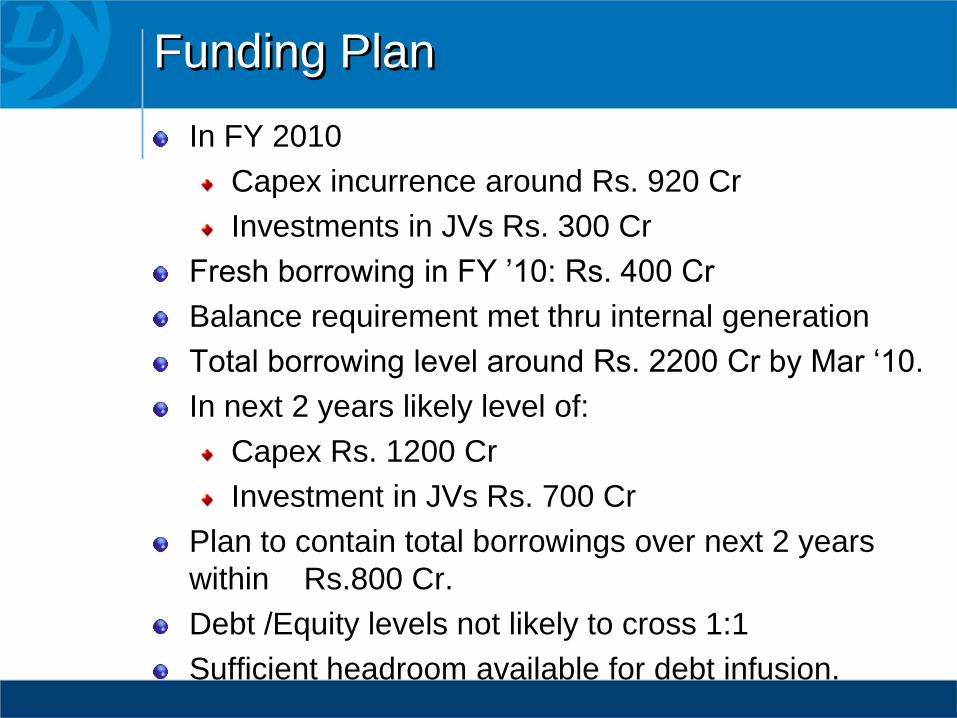

Funding Plan

In FY 2010

Capex incurrence around Rs. 920 Cr

Investments in JVs Rs. 300 Cr

Fresh borrowing in FY ’10: Rs. 400 Cr

Balance requirement met thru internal generation

Total borrowing level around Rs. 2200 Cr by Mar ‘10.

In next 2 years likely level of:

Capex Rs. 1200 Cr

Investment in JVs Rs. 700 Cr

Plan to contain total borrowings over next 2 years

within Rs.800 Cr.

Debt /Equity levels not likely to cross 1:1

Sufficient headroom available for debt infusion.

M&HCVLCVs Construction

equipment

Foundry Engines & Components Business

Auto Electronics Exhaust System

Technology

Engineering and Testing Services

Defence

Automotive Sector

Wider presence in Automobile Sector

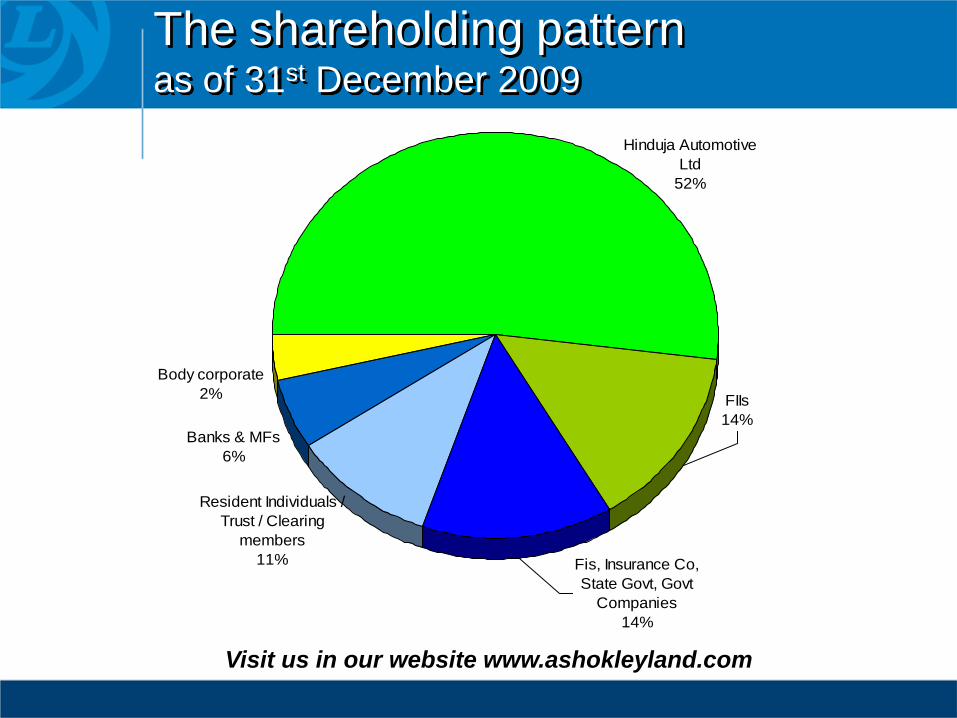

The shareholding pattern as of 31st December 2009

Banks & MFs

6%

Body corporate

2%

Hinduja Automotive

Ltd

52%

FIIs

14%

Resident Individuals /

Trust / Clearing

members

11% Fis, Insurance Co,

State Govt, Govt

Companies

14%

Visit us in our website www.ashokleyland.com

Thank You

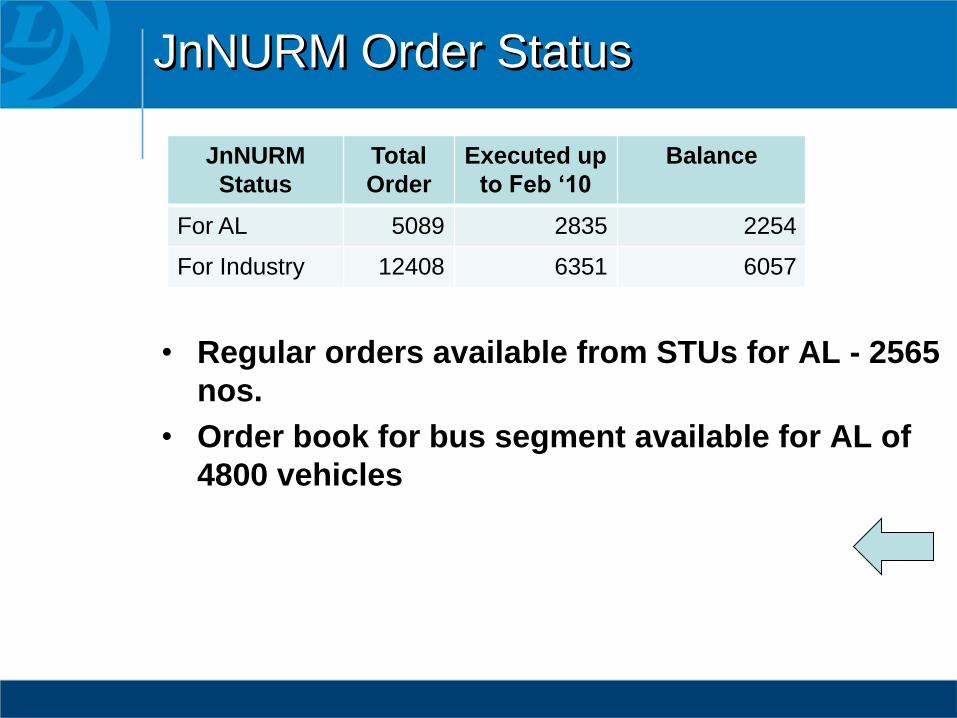

JnNURM Order Status

• Regular orders available from STUs for AL - 2565

nos.

• Order book for bus segment available for AL of

4800 vehicles

JnNURM

Status

Total

Order

Executed up

to Feb ‘10

Balance

For AL 5089 2835 2254

For Industry 12408 6351 6057

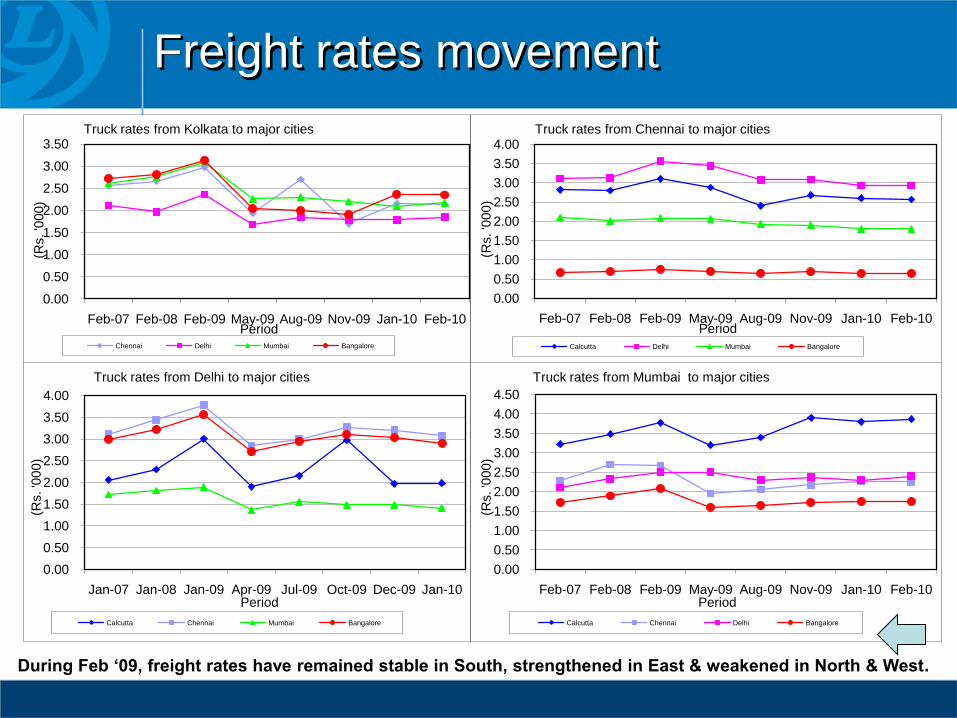

Freight rates movement

During Feb ‘09, freight rates have remained stable in South, strengthened in East & weakened in North & West.

Source: Business Line

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Feb-07 Feb-08 Feb-09 May-09 Aug-09 Nov-09 Jan-10 Feb-10

(Rs. '0

00)

Period

Truck rates from Kolkata to major cities

Chennai Delhi Mumbai Bangalore

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Feb-07 Feb-08 Feb-09 May-09 Aug-09 Nov-09 Jan-10 Feb-10

(Rs. '0

00)

Period

Truck rates from Chennai to major cities

Calcutta Delhi Mumbai Bangalore

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Jan-07 Jan-08 Jan-09 Apr-09 Jul-09 Oct-09 Dec-09 Jan-10

(Rs. '0

00)

Period

Truck rates from Delhi to major cities

Calcutta Chennai Mumbai Bangalore

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Feb-07 Feb-08 Feb-09 May-09 Aug-09 Nov-09 Jan-10 Feb-10

(Rs. '0

00)

Period

Truck rates from Mumbai to major cities

Calcutta Chennai Delhi Bangalore