Embed Size (px)

Citation preview

1

Investor Presentation

August 2011

Disclaimer

This announcement contains “forward-looking statements”. Such forward-looking statements include, without limitation: estimates of future earnings, the sensitivity of earnings to oil & gas prices and foreign exchange rate movements; estimates of future oil & gas production and sales; estimates of future cash flows, the sensitivity of cash flows to oil & gas prices and foreign exchange rate movements; statements regarding future debt repayments; estimates of future capital expenditures; estimates of reserves and statements regarding future exploration results and the replacement of reserves; and where the Company expresses or implies an expectation or belief as to future events or results, such expectation or belief is expressed in good faith and believed to have a reasonable basis. However, forward looking statements are subject to risks, uncertainties and other factors, which could cause actual results to differ materially from future results expressed, projected or implied by such forward-looking statements. Such risks include, but are not limited to oil and gas price volatility, currency fluctuations, increased production costs and variances in reserves or recovery rates from those assumed in the company’s plans, as well as political and operational risks in the countries and states in which we operate or sell product to, and governmental regulation and judicial outcomes. For a more detailed discussion of such risks and other factors, see the Company’s Annual Reports, as well as the Company’s other filings. The Company does not undertake any obligation to release publicly any revisions to any “forward looking statement” to reflect events or circumstances after the date of this release, or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws.

2

Corporate Overview

3

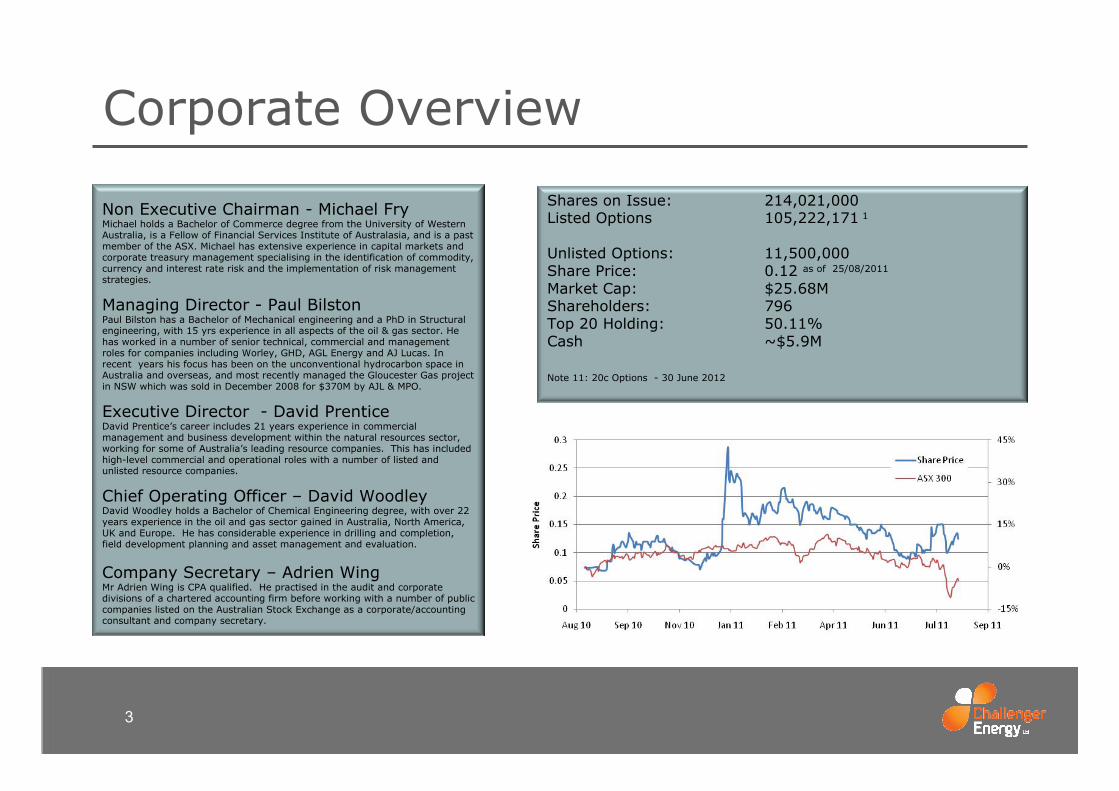

Non Executive Chairman - Michael FryMichael holds a Bachelor of Commerce degree from the University of Western Australia, is a Fellow of Financial Services Institute of Australasia, and is a past member of the ASX. Michael has extensive experience in capital markets and corporate treasury management specialising in the identification of commodity, currency and interest rate risk and the implementation of risk management strategies.

Managing Director - Paul BilstonPaul Bilston has a Bachelor of Mechanical engineering and a PhD in Structural engineering, with 15 yrs experience in all aspects of the oil & gas sector. He has worked in a number of senior technical, commercial and management roles for companies including Worley, GHD, AGL Energy and AJ Lucas. In recent years his focus has been on the unconventional hydrocarbon space in Australia and overseas, and most recently managed the Gloucester Gas project in NSW which was sold in December 2008 for $370M by AJL & MPO.

Executive Director - David PrenticeDavid Prentice’s career includes 21 years experience in commercial management and business development within the natural resources sector, working for some of Australia’s leading resource companies. This has included high-level commercial and operational roles with a number of listed and unlisted resource companies.

Chief Operating Officer – David WoodleyDavid Woodley holds a Bachelor of Chemical Engineering degree, with over 22 years experience in the oil and gas sector gained in Australia, North America, UK and Europe. He has considerable experience in drilling and completion, field development planning and asset management and evaluation.

Company Secretary – Adrien WingMr Adrien Wing is CPA qualified. He practised in the audit and corporate divisions of a chartered accounting firm before working with a number of public companies listed on the Australian Stock Exchange as a corporate/accounting consultant and company secretary.

Shares on Issue: 214,021,000Listed Options 105,222,171 1

Unlisted Options: 11,500,000Share Price: 0.12 as of 25/08/2011

Market Cap: $25.68MShareholders: 796Top 20 Holding: 50.11%Cash ~$5.9M

Note 11: 20c Options - 30 June 2012

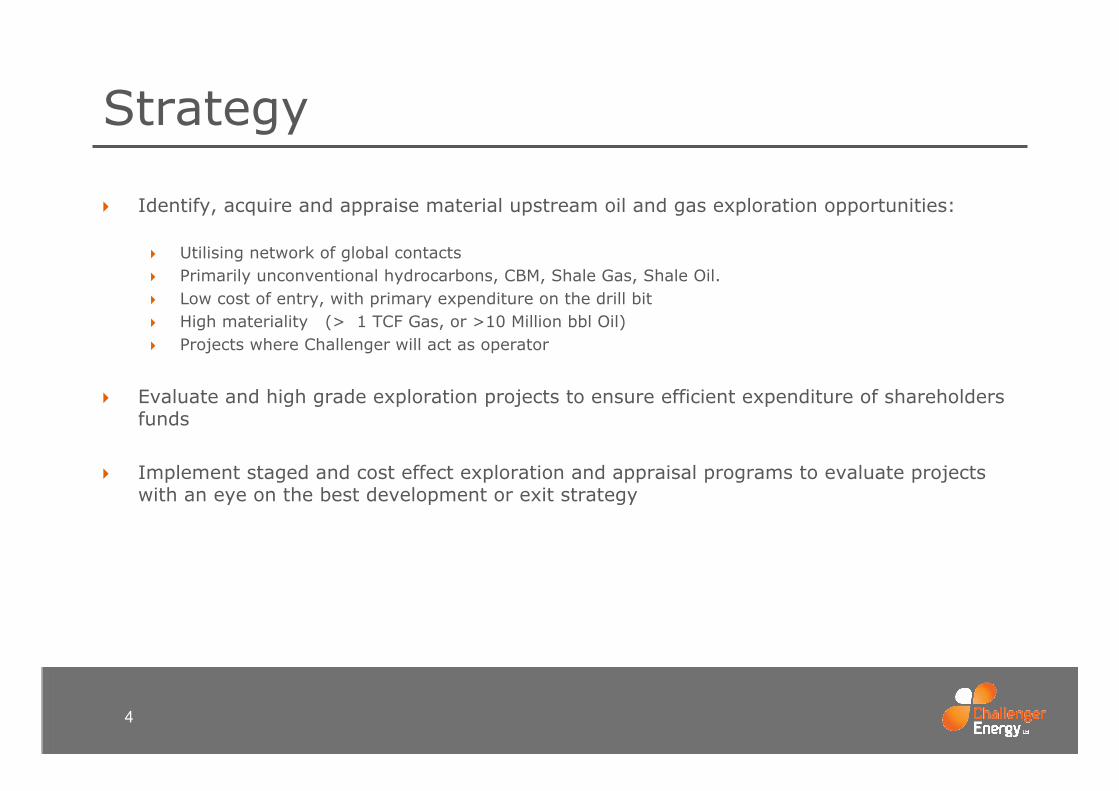

Strategy

Identify, acquire and appraise material upstream oil and gas exploration opportunities:

Utilising network of global contactsPrimarily unconventional hydrocarbons, CBM, Shale Gas, Shale Oil.Low cost of entry, with primary expenditure on the drill bitHigh materiality (> 1 TCF Gas, or >10 Million bbl Oil)Projects where Challenger will act as operator

Evaluate and high grade exploration projects to ensure efficient expenditure of shareholders funds

Implement staged and cost effect exploration and appraisal programs to evaluate projects with an eye on the best development or exit strategy

4

Why Unconventional Gas?

5

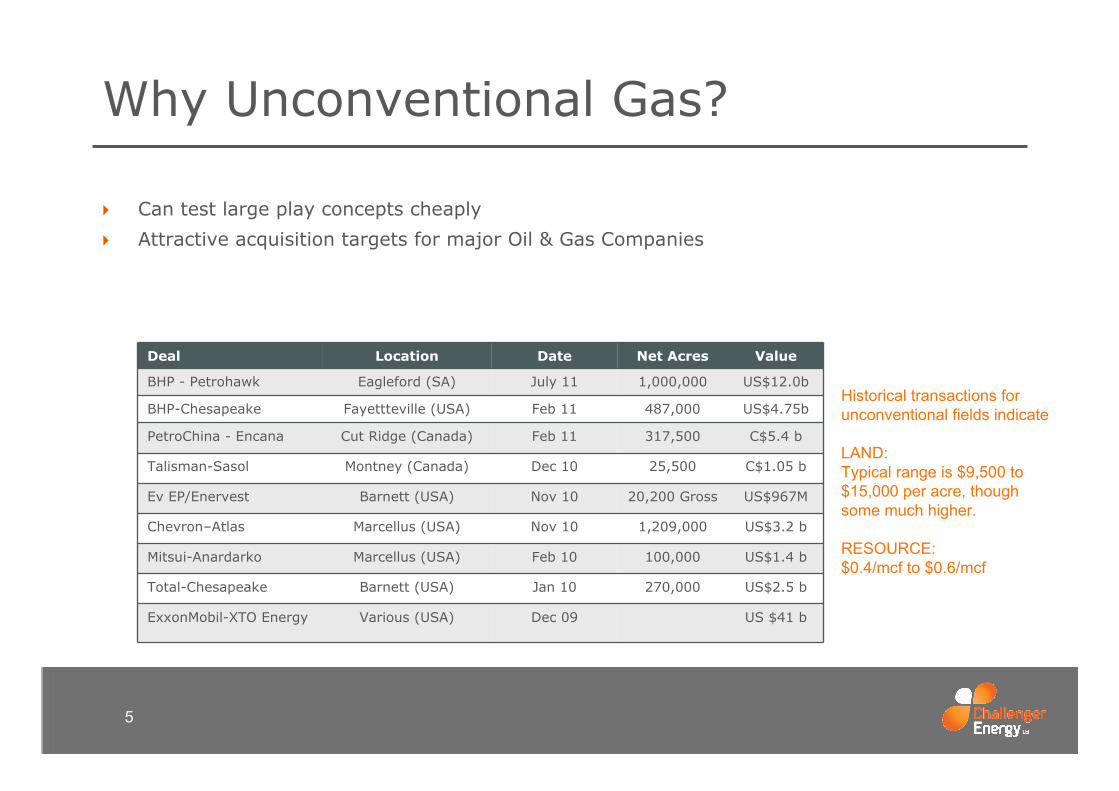

Deal Location Date Net Acres Value

BHP - Petrohawk Eagleford (SA) July 11 1,000,000 US$12.0b

BHP-Chesapeake Fayettteville (USA) Feb 11 487,000 US$4.75b

PetroChina - Encana Cut Ridge (Canada) Feb 11 317,500 C$5.4 b

Talisman-Sasol Montney (Canada) Dec 10 25,500 C$1.05 b

Ev EP/Enervest Barnett (USA) Nov 10 20,200 Gross US$967M

Chevron–Atlas Marcellus (USA) Nov 10 1,209,000 US$3.2 b

Mitsui-Anardarko Marcellus (USA) Feb 10 100,000 US$1.4 b

Total-Chesapeake Barnett (USA) Jan 10 270,000 US$2.5 b

ExxonMobil-XTO Energy Various (USA) Dec 09 US $41 b

Can test large play concepts cheaply

Attractive acquisition targets for major Oil & Gas Companies

Historical transactions for unconventional fields indicate

LAND: Typical range is $9,500 to $15,000 per acre, though some much higher.

RESOURCE:$0.4/mcf to $0.6/mcf

Asset Portfolio

Mercury Stetson Shale Gas ProspectBarnett ShaleWoodford Shale

Triple CrownHybrid Gas PlayEllenburger

South AfricaFort Brown Shales

6

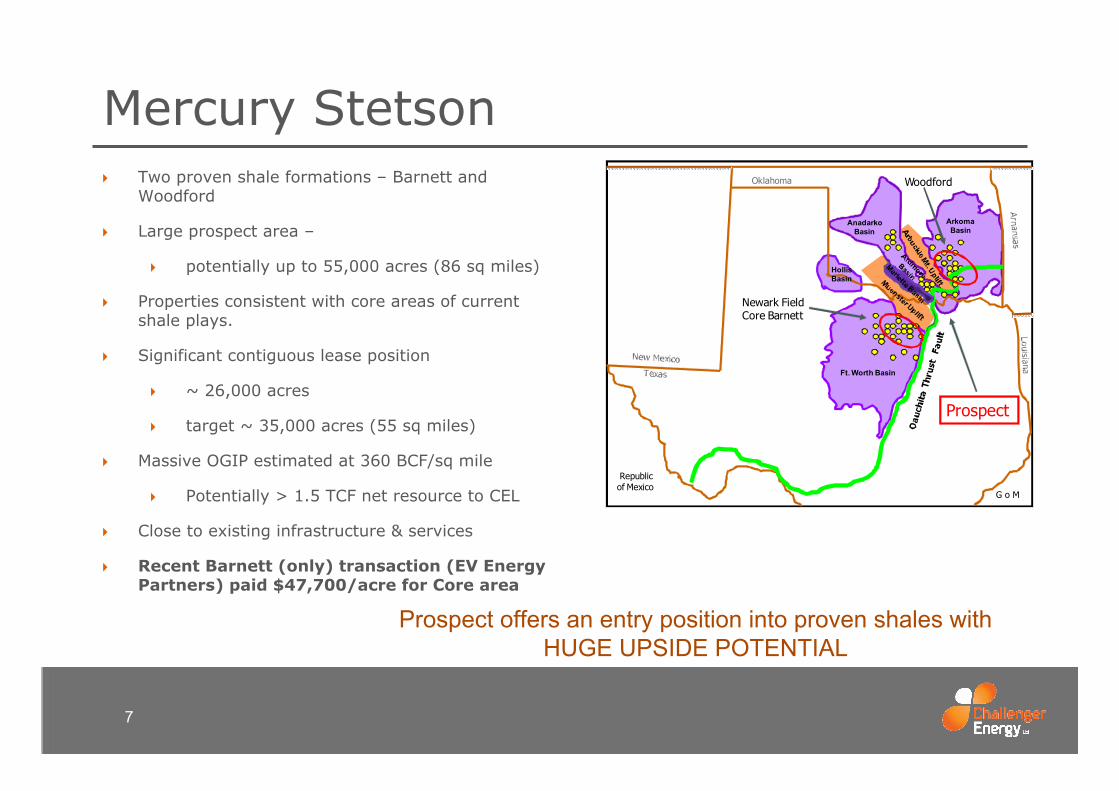

Mercury StetsonTwo proven shale formations – Barnett and Woodford

Large prospect area –

potentially up to 55,000 acres (86 sq miles)

Properties consistent with core areas of current shale plays.

Significant contiguous lease position

~ 26,000 acres

target ~ 35,000 acres (55 sq miles)

Massive OGIP estimated at 360 BCF/sq mile

Potentially > 1.5 TCF net resource to CEL

Close to existing infrastructure & services

Recent Barnett (only) transaction (EV Energy Partners) paid $47,700/acre for Core area

7

Prospect

Oklahoma

Arkoma Basin

Ft. Worth Basin

Hollis Basin

Anadarko Basin

Republic of Mexico

G o M

Newark Field Core Barnett

Woodford

Prospect offers an entry position into proven shales with HUGE UPSIDE POTENTIAL

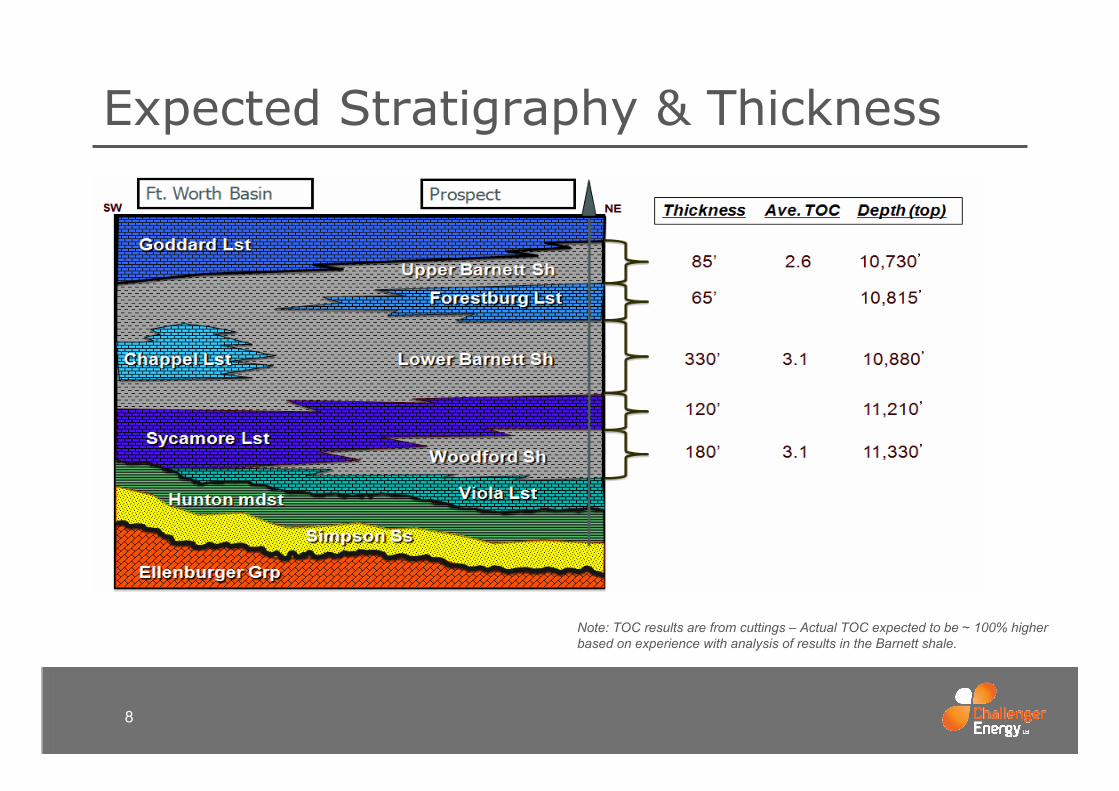

Expected Stratigraphy & Thickness

8

Note: TOC results are from cuttings – Actual TOC expected to be ~ 100% higher based on experience with analysis of results in the Barnett shale.

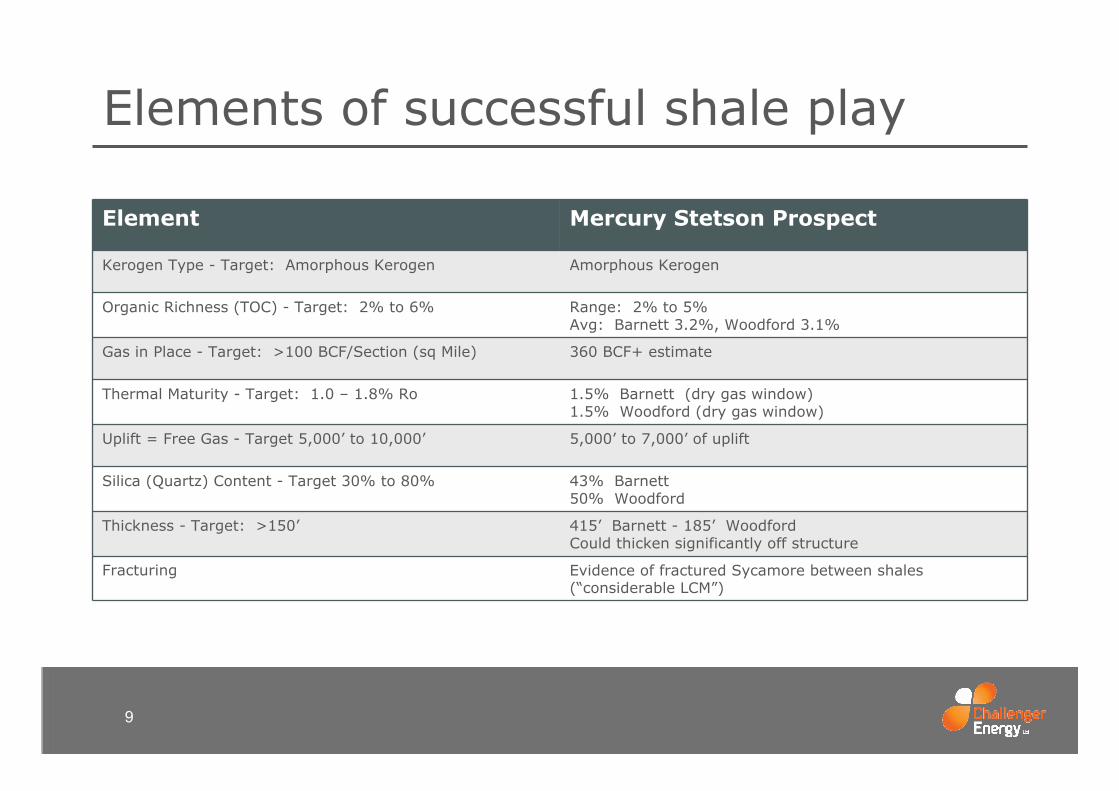

Elements of successful shale play

9

Element Mercury Stetson Prospect

Kerogen Type - Target: Amorphous Kerogen Amorphous Kerogen

Organic Richness (TOC) - Target: 2% to 6% Range: 2% to 5% Avg: Barnett 3.2%, Woodford 3.1%

Gas in Place - Target: >100 BCF/Section (sq Mile) 360 BCF+ estimate

Thermal Maturity - Target: 1.0 – 1.8% Ro 1.5% Barnett (dry gas window)1.5% Woodford (dry gas window)

Uplift = Free Gas - Target 5,000’ to 10,000’ 5,000’ to 7,000’ of uplift

Silica (Quartz) Content - Target 30% to 80% 43% Barnett50% Woodford

Thickness - Target: >150’ 415’ Barnett - 185’ WoodfordCould thicken significantly off structure

Fracturing Evidence of fractured Sycamore between shales (“considerable LCM”)

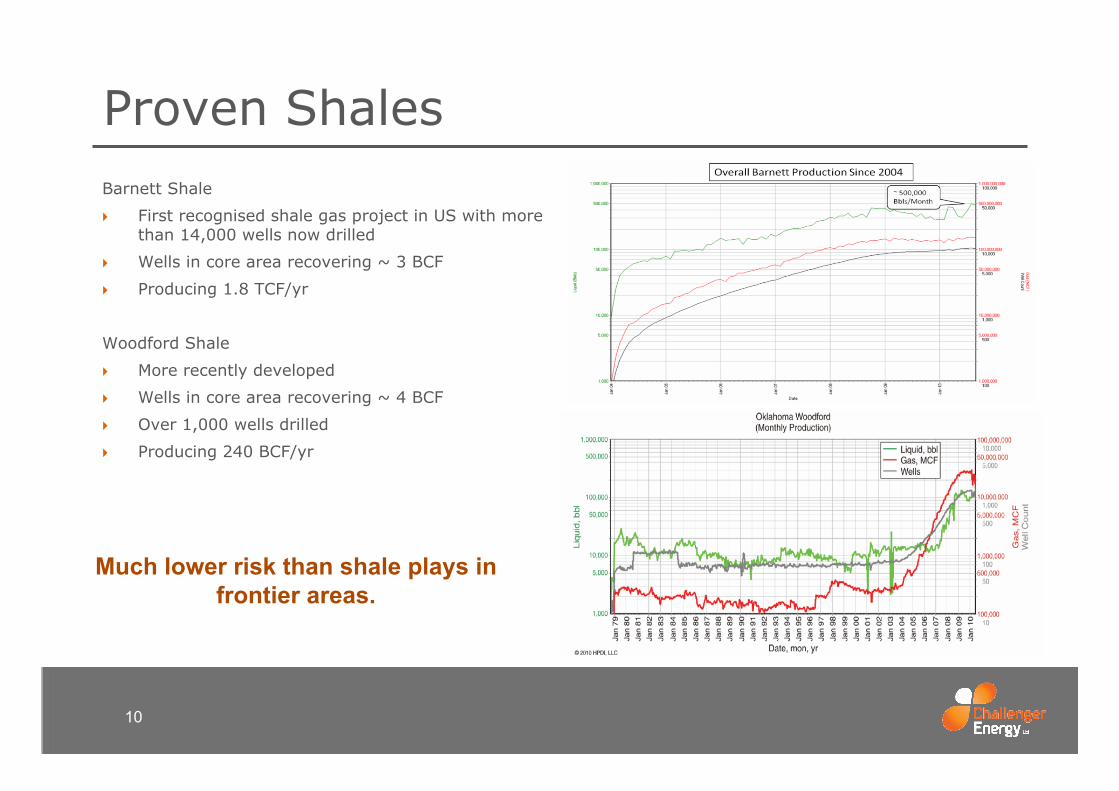

Proven Shales

10

Much lower risk than shale plays in frontier areas.

Barnett Shale

First recognised shale gas project in US with more than 14,000 wells now drilled

Wells in core area recovering ~ 3 BCF

Producing 1.8 TCF/yr

Woodford Shale

More recently developed

Wells in core area recovering ~ 4 BCF

Over 1,000 wells drilled

Producing 240 BCF/yr

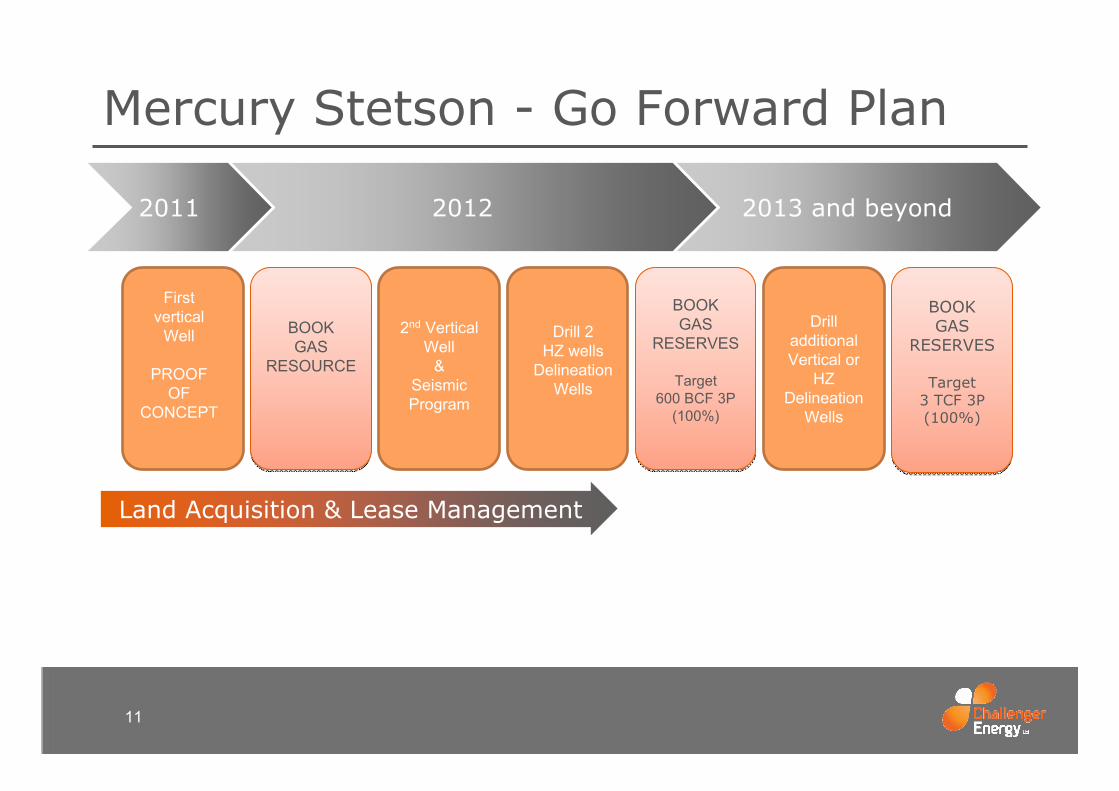

Mercury Stetson - Go Forward Plan

11

BOOK GAS

RESOURCE

First vertical

Well

PROOF OF

CONCEPT

Drill 2HZ wells

Delineation Wells

Drill additionalVertical or

HZ Delineation

Wells

Core Analysis

BOOK GAS

RESERVES

Target 600 BCF 3P

(100%)

2nd Vertical Well

&Seismic Program

BOOK GAS

RESERVES

Target 3 TCF 3P (100%)

BOOK GAS

RESERVES

Target 3 TCF 3P (100%)

20122011 2013 and beyond

Land Acquisition & Lease Management

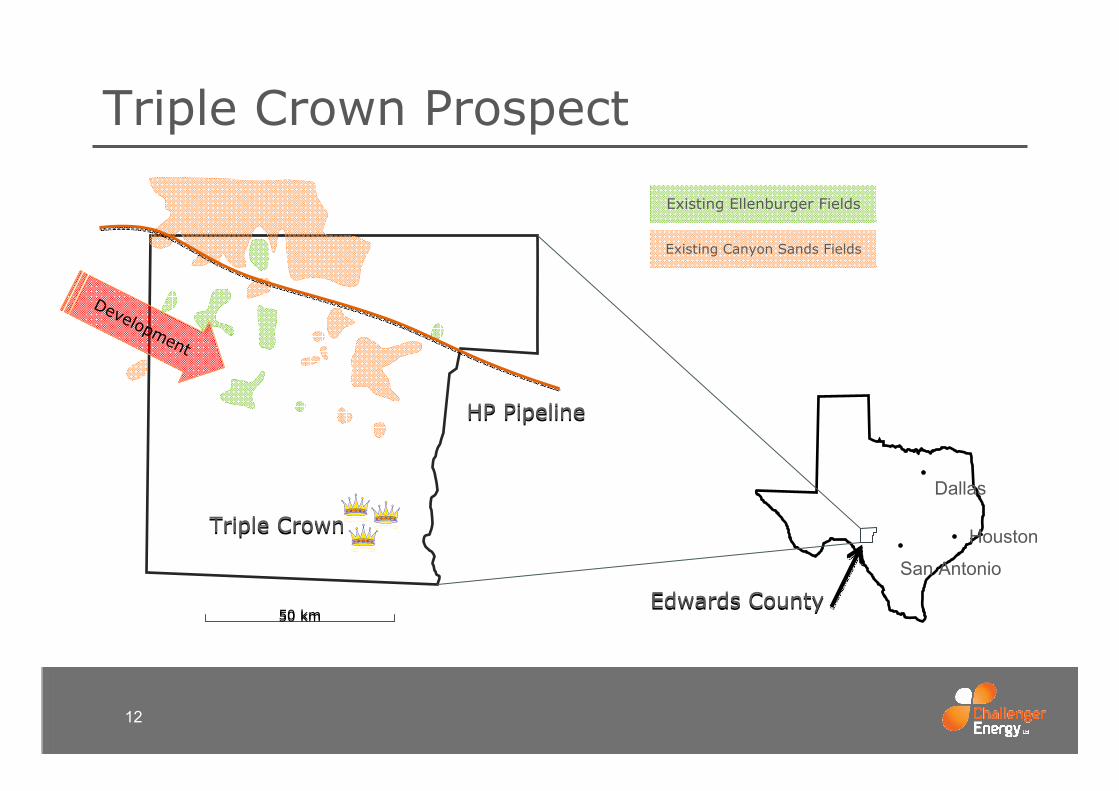

Triple Crown Prospect

12

Dallas

San Antonio

Houston

Existing Canyon Sands Fields

Existing Ellenburger Fields

HP PipelineHP Pipeline

Triple CrownTriple Crown

50 km50 km

Development

Edwards CountyEdwards County

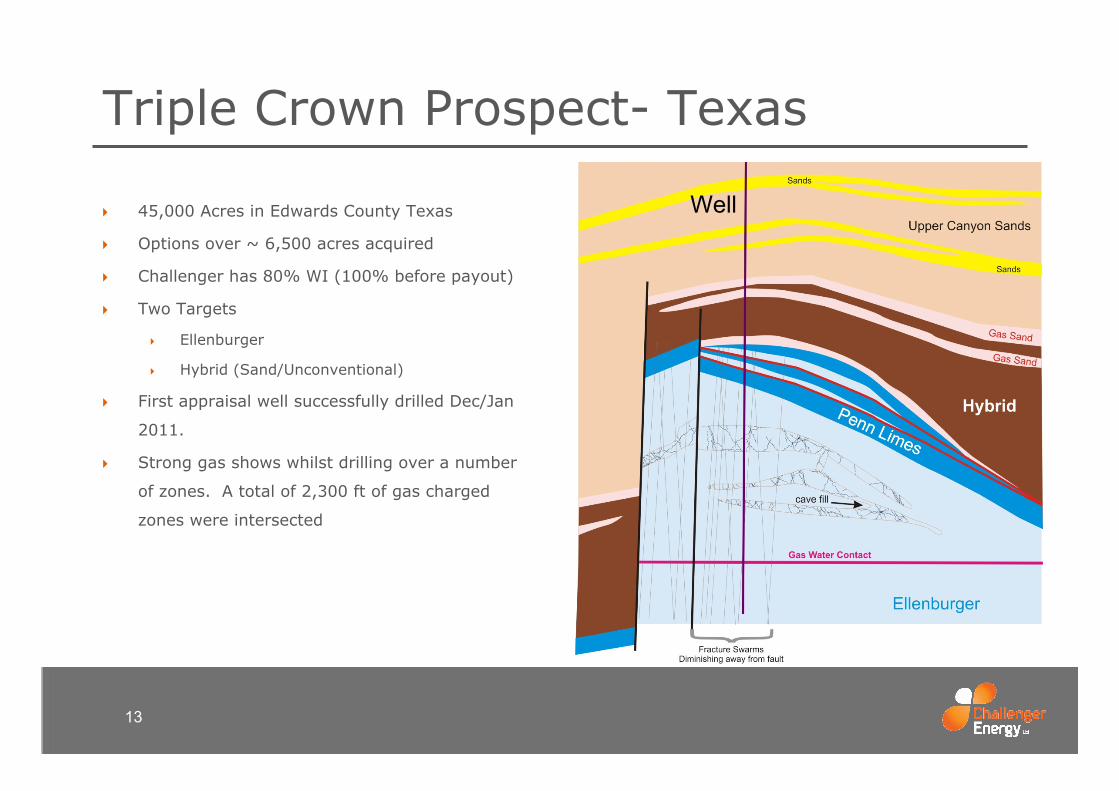

Triple Crown Prospect- Texas

45,000 Acres in Edwards County Texas

Options over ~ 6,500 acres acquired

Challenger has 80% WI (100% before payout)

Two Targets

Ellenburger

Hybrid (Sand/Unconventional)

First appraisal well successfully drilled Dec/Jan

2011.

Strong gas shows whilst drilling over a number

of zones. A total of 2,300 ft of gas charged

zones were intersected

13

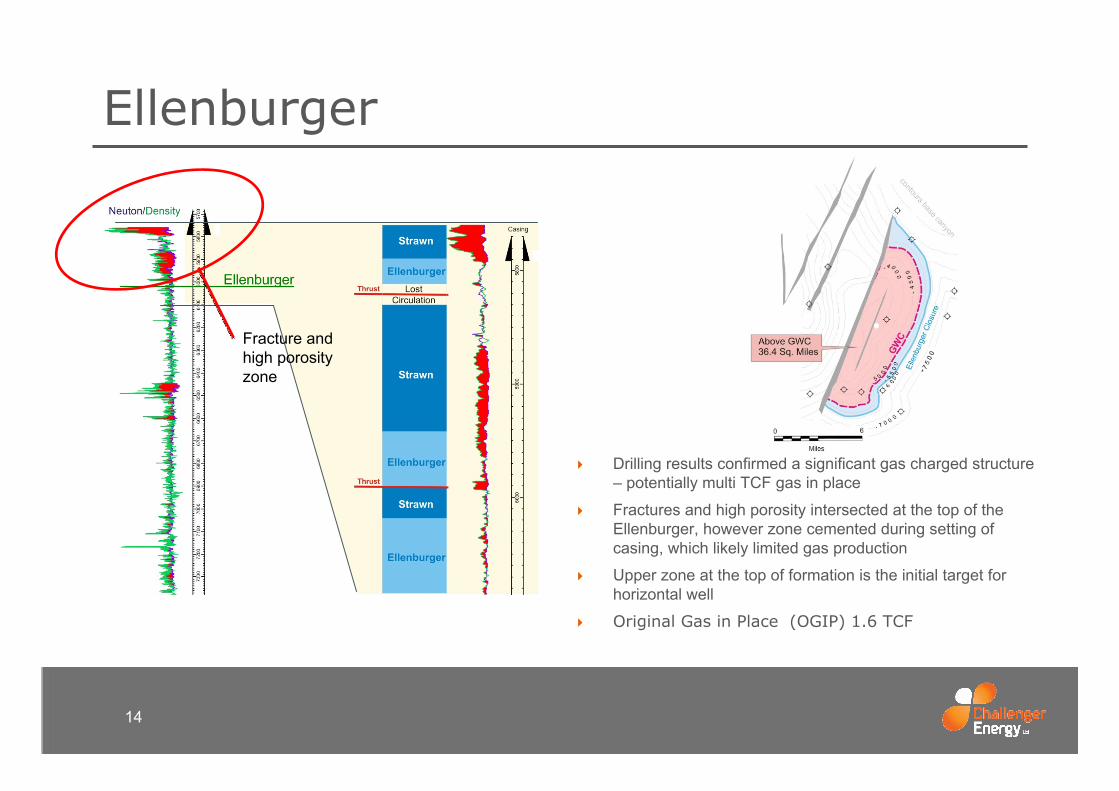

Well

Ellenburger

14

Drilling results confirmed a significant gas charged structure – potentially multi TCF gas in place

Fractures and high porosity intersected at the top of the Ellenburger, however zone cemented during setting of casing, which likely limited gas production

Upper zone at the top of formation is the initial target for horizontal well

Original Gas in Place (OGIP) 1.6 TCF

Fracture and high porosity zone

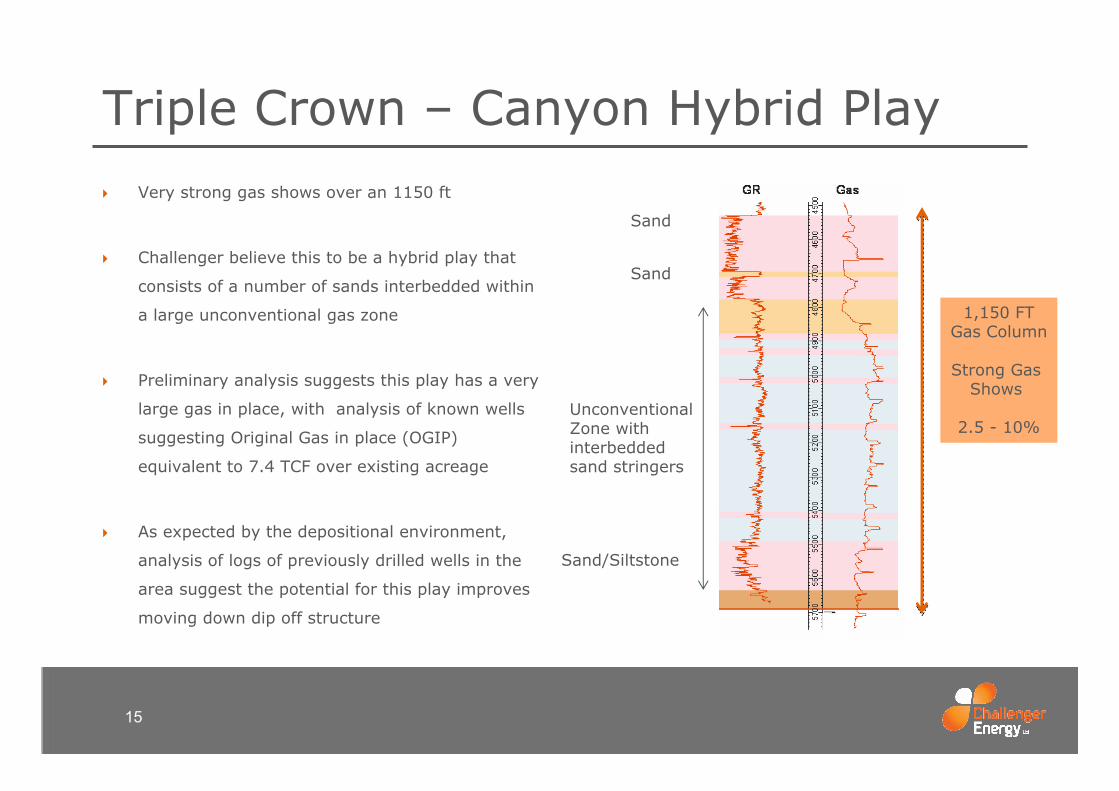

Triple Crown – Canyon Hybrid Play

15

Very strong gas shows over an 1150 ft

Challenger believe this to be a hybrid play that

consists of a number of sands interbedded within

a large unconventional gas zone

Preliminary analysis suggests this play has a very

large gas in place, with analysis of known wells

suggesting Original Gas in place (OGIP)

equivalent to 7.4 TCF over existing acreage

As expected by the depositional environment,

analysis of logs of previously drilled wells in the

area suggest the potential for this play improves

moving down dip off structure

Sand

Sand

Sand/Siltstone

Unconventional Zone with interbedded sand stringers

1,150 FTGas Column

Strong Gas Shows

2.5 - 10%

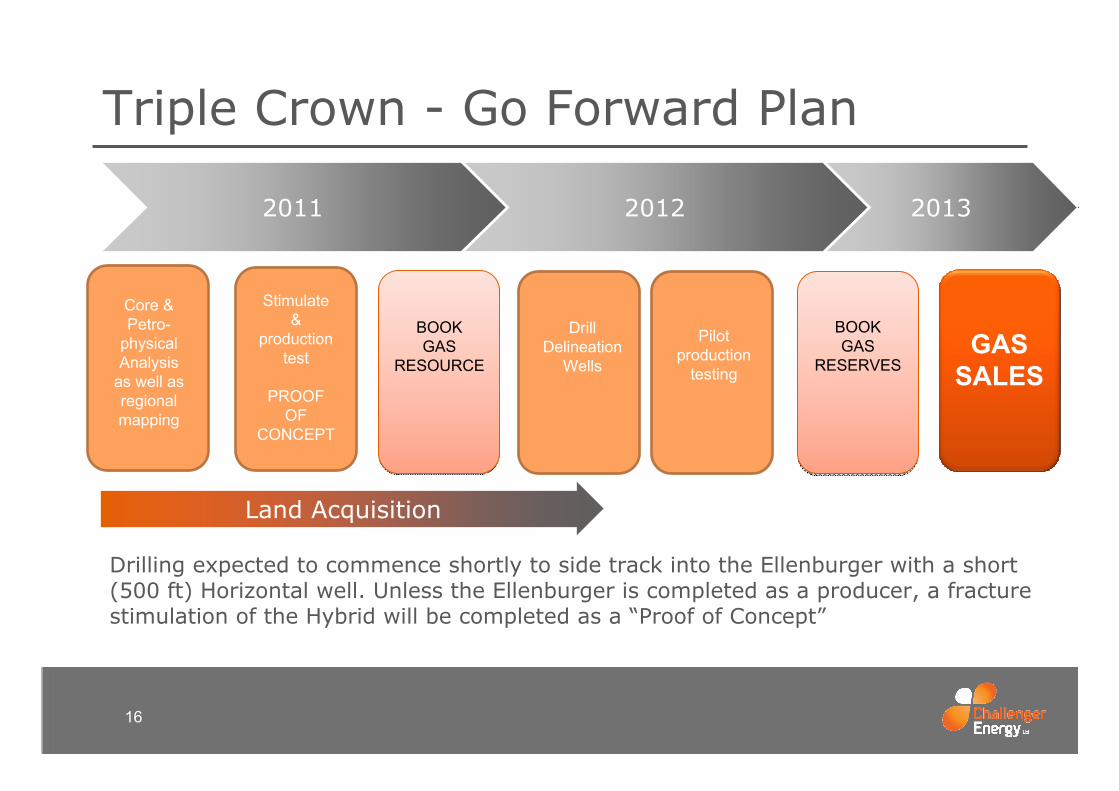

Triple Crown - Go Forward Plan

16

BOOK GAS

RESOURCE

Stimulate &

production test

PROOF OF

CONCEPT

Pilot production

testing

Core Analysis

BOOK GAS

RESERVES

Drill Delineation

Wells GAS

SALES

Core & Petro-

physical Analysis

as well as regional mapping

Drilling expected to commence shortly to side track into the Ellenburger with a short (500 ft) Horizontal well. Unless the Ellenburger is completed as a producer, a fracture stimulation of the Hybrid will be completed as a “Proof of Concept”

Land Acquisition

20122011 2013

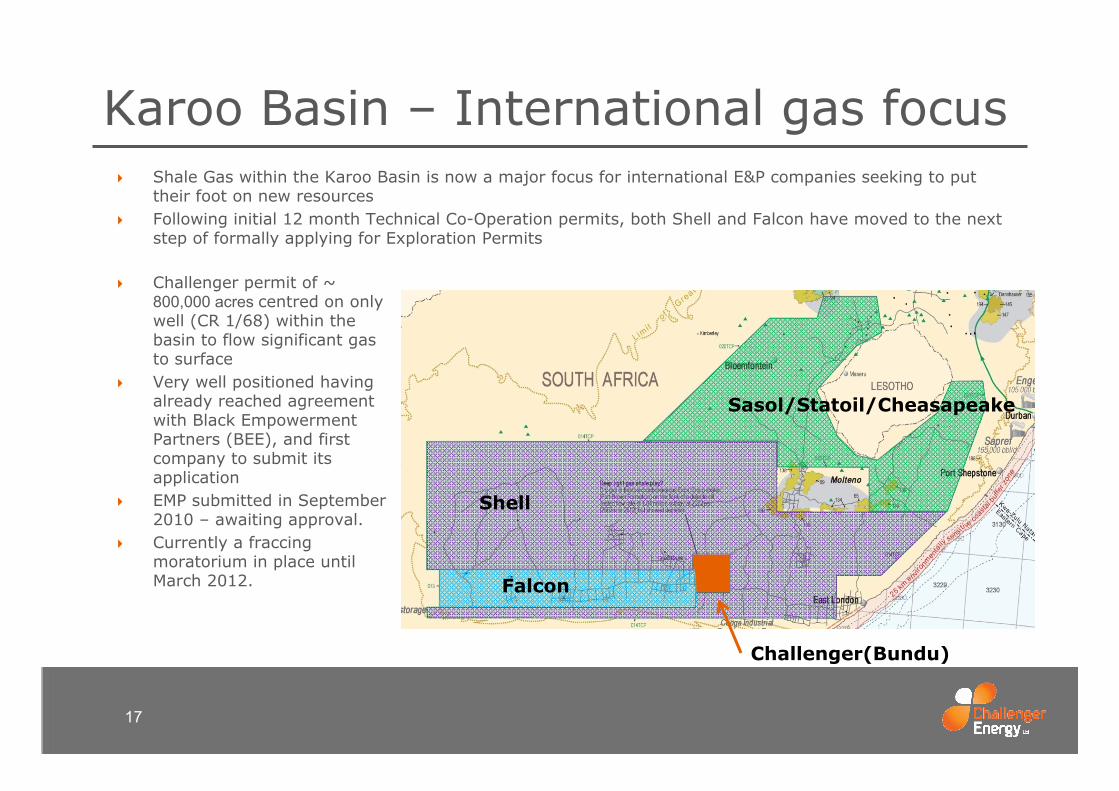

Karoo Basin – International gas focus

17

Shale Gas within the Karoo Basin is now a major focus for international E&P companies seeking to put their foot on new resourcesFollowing initial 12 month Technical Co-Operation permits, both Shell and Falcon have moved to the next step of formally applying for Exploration Permits

Shell

Falcon

Sasol/Statoil/Cheasapeake

Challenger(Bundu)

Challenger permit of ~ 800,000 acres centred on only well (CR 1/68) within the basin to flow significant gas to surfaceVery well positioned having already reached agreement with Black Empowerment Partners (BEE), and first company to submit its applicationEMP submitted in September 2010 – awaiting approval.Currently a fraccing moratorium in place until March 2012.

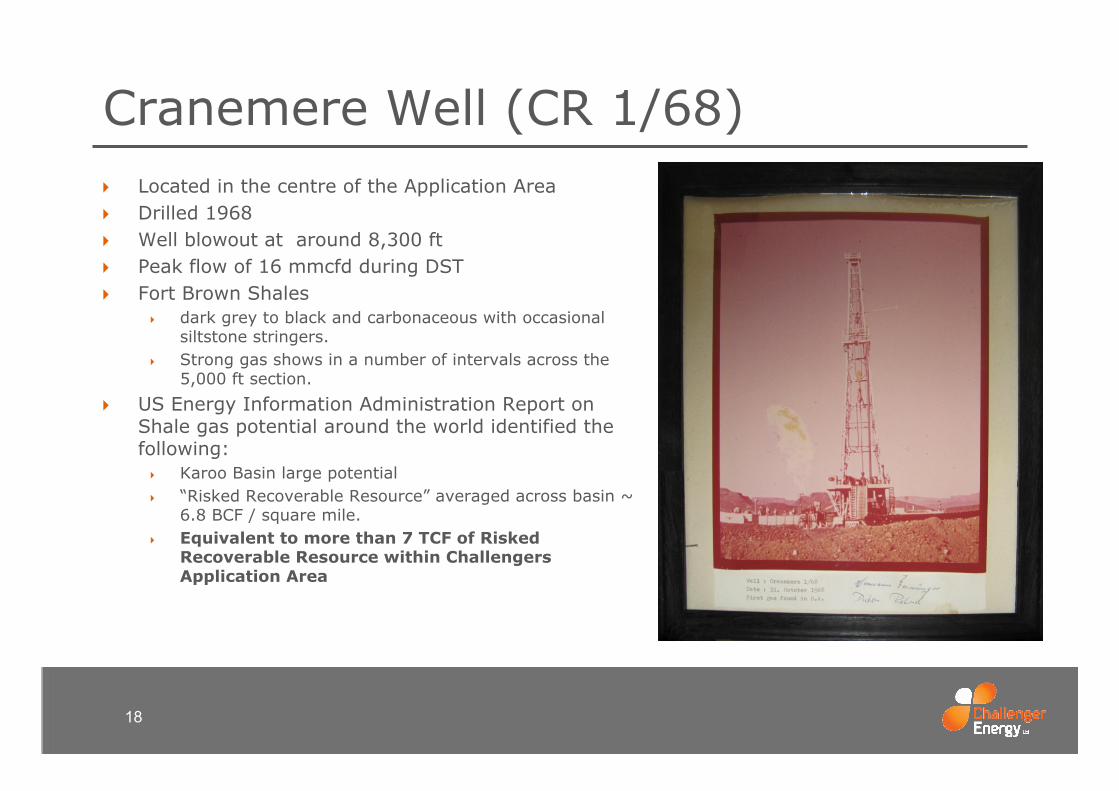

Cranemere Well (CR 1/68)Located in the centre of the Application AreaDrilled 1968Well blowout at around 8,300 ftPeak flow of 16 mmcfd during DST Fort Brown Shales

dark grey to black and carbonaceous with occasional siltstone stringers. Strong gas shows in a number of intervals across the 5,000 ft section.

US Energy Information Administration Report on Shale gas potential around the world identified the following:

Karoo Basin large potential“Risked Recoverable Resource” averaged across basin ~ 6.8 BCF / square mile.Equivalent to more than 7 TCF of Risked Recoverable Resource within Challengers Application Area

18

SummaryChallenger Energy’s strategy is to identify, acquire and appraise material upstream oil and gas exploration opportunities

Mercury Stetson Prospect in North Texas, USTwo proven shale formations – Barnett and Woodford Massive potential gas in place with OGIP estimated at 360 BCF/sq mileLarge prospect area – potentially up to 55,000 acres (86 sq miles)Prospect is close to existing infrastructureContiguous land position of ~ 26,000 acres with a short term target of 35,000 acres.

Triple Crown Prospect in Texas, USSignificant acreage – 45,000 acres with options over a further 6,500 acres.Large gas charged zones, Ellenburger (dolomite) and an unconventional Hybrid play which is geologically analogous to Montney Hybrid Play in Western Canada with an estimated OGIP of 9 TCF.Testing to commence shortly on both the Ellenburger and Hyprid Play

Karoo Basin in South AfricaShale gas in Karoo Basin now a major focus for international E&P companies (eg Shell, Cheasapeake, Statoil and Sasol)Challenger Energy’s permit of approx. 800,000 acres centred on only well within basin to flow significant gas to surface to date, awaiting approval.Independent US Energy Information Agency report suggests Risked Recoverable Resource of more than 7 TCF in application area.

Attractive assets have exciting potential to grow significant shareholder value

19

20

AppendicesSupporting Mercury Stetson Slides

August 2011

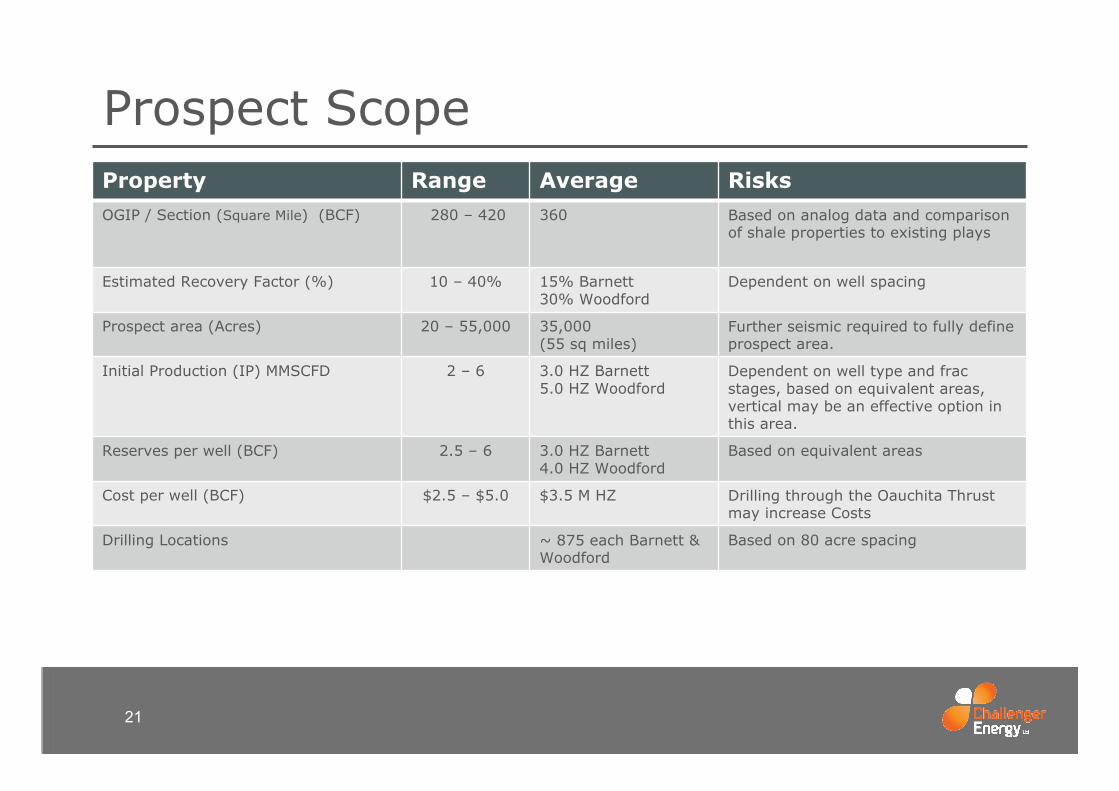

Prospect ScopeProperty Range Average Risks

OGIP / Section (Square Mile) (BCF) 280 – 420 360 Based on analog data and comparison of shale properties to existing plays

Estimated Recovery Factor (%) 10 – 40% 15% Barnett30% Woodford

Dependent on well spacing

Prospect area (Acres) 20 – 55,000 35,000(55 sq miles)

Further seismic required to fully define prospect area.

Initial Production (IP) MMSCFD 2 – 6 3.0 HZ Barnett5.0 HZ Woodford

Dependent on well type and frac stages, based on equivalent areas, vertical may be an effective option in this area.

Reserves per well (BCF) 2.5 – 6 3.0 HZ Barnett4.0 HZ Woodford

Based on equivalent areas

Cost per well (BCF) $2.5 – $5.0 $3.5 M HZ Drilling through the Oauchita Thrust may increase Costs

Drilling Locations ~ 875 each Barnett & Woodford

Based on 80 acre spacing

21

Joint Venture Agreement

Governs relationship between the parties until no leases held by any party.

Provides for Challenger to earn 50% interest in Phase 1, by the following:Payment of up to $2.2 million as and when required for the renewal and extension of existing leases plus the acquisition of additional leasesDrill, fracture stimulate, complete and test TWO vertical wells. The parties anticipate that the first well will incorporated the re-entry and completion of the existing well on the property, however in the event that is unsuccessful, a new well will be drilled and the value of the seismic program adjusted to keep Challenger whole. Conduct a seismic program funded partially by revenue from first well to fully define the extend of the shales in the prospect areaConnect the two wells to the nearby sales pipelineChallenger is required to pay the balance of the $2.2 M if it does not drill and complete the first well.

Phase 2Subject to the terms of the agreement, provides for the parties to enter into a Phase 2 program including two horizontal wells in each of the Barnett and Woodford shales.Parties to fund their share, or in the absence of all parties agreeing to fund their share, a mechanism exists for the funding parties to earn additional interest

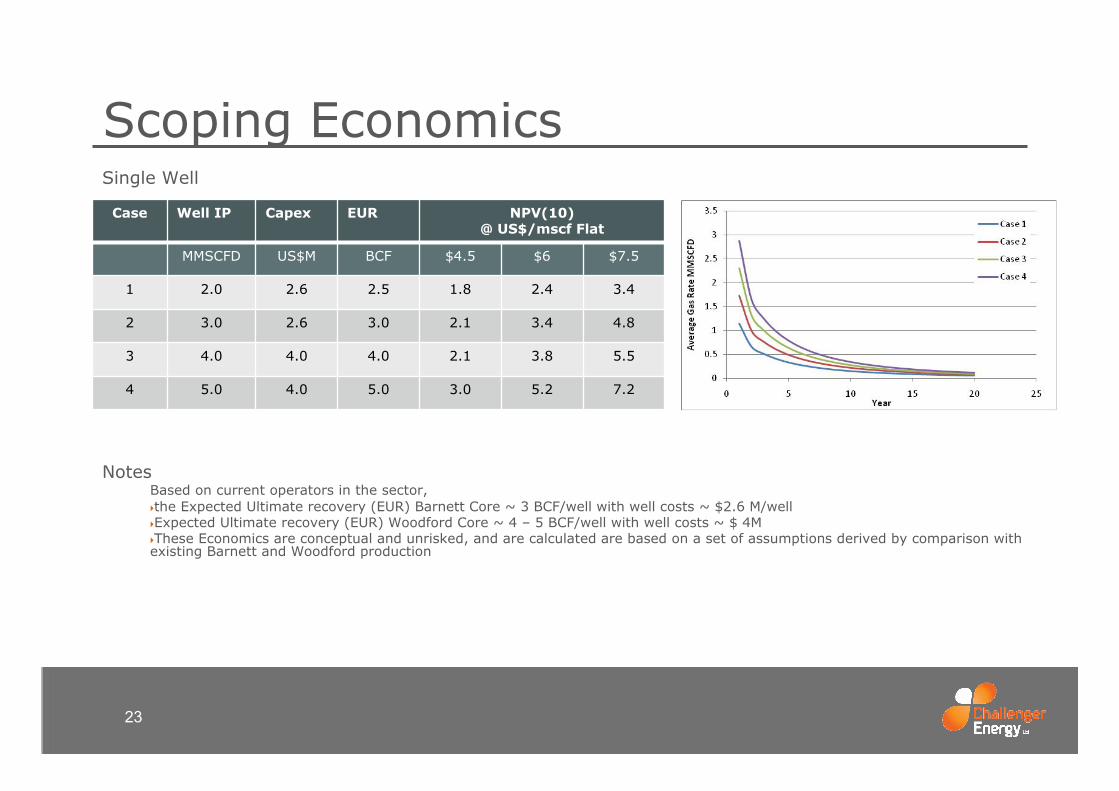

Case Well IP Capex EUR NPV(10) @ US$/mscf Flat

MMSCFD US$M BCF $4.5 $6 $7.5

1 2.0 2.6 2.5 1.8 2.4 3.4

2 3.0 2.6 3.0 2.1 3.4 4.8

3 4.0 4.0 4.0 2.1 3.8 5.5

4 5.0 4.0 5.0 3.0 5.2 7.2

Scoping Economics

23

NotesBased on current operators in the sector, the Expected Ultimate recovery (EUR) Barnett Core ~ 3 BCF/well with well costs ~ $2.6 M/wellExpected Ultimate recovery (EUR) Woodford Core ~ 4 – 5 BCF/well with well costs ~ $ 4MThese Economics are conceptual and unrisked, and are calculated are based on a set of assumptions derived by comparison with existing Barnett and Woodford production

Single Well

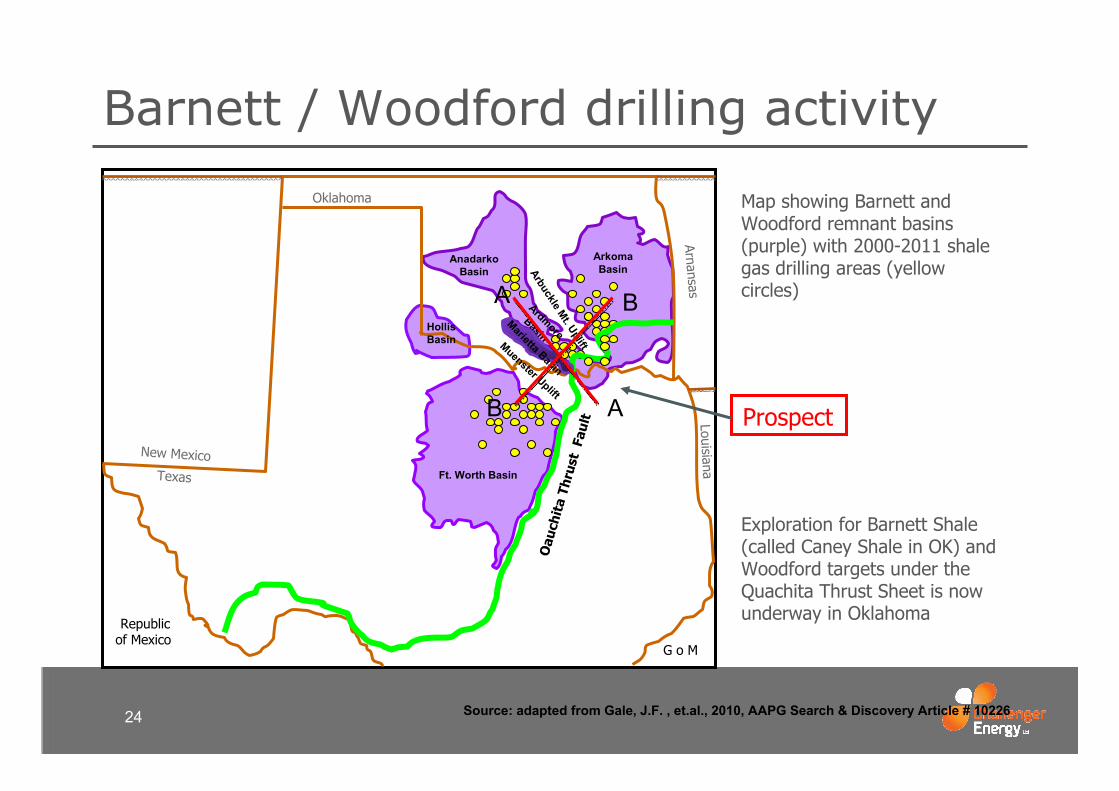

Map showing Barnett and Woodford remnant basins (purple) with 2000-2011 shale gas drilling areas (yellow circles)

Exploration for Barnett Shale (called Caney Shale in OK) and Woodford targets under the Quachita Thrust Sheet is now underway in Oklahoma

Barnett / Woodford drilling activity

Source: adapted from Gale, J.F. , et.al., 2010, AAPG Search & Discovery Article # 10226

Prospect

Texas

New Mexico

Oklahoma

Oau

chit

a Th

rust

Fau

ltArbuckle Mt. Uplift

Ardmore Basin

Arkoma Basin

Ft. Worth Basin

Hollis Basin Muenster Uplift

Anadarko Basin

ArnansasLouisiana

Republic of Mexico

G o M

Marietta Basin

B

B

A

A

24

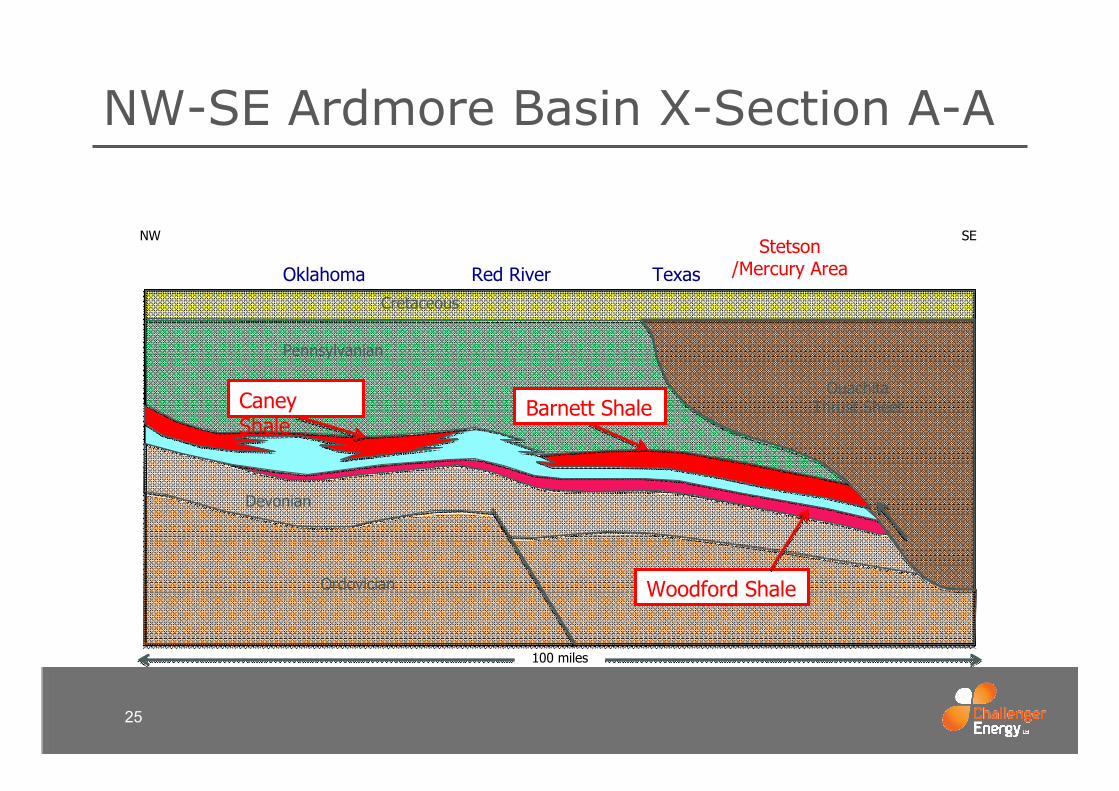

25

NW-SE Ardmore Basin X-Section A-A

Oklahoma

NW SE

Red River Texas Stetson

/Mercury Area

Cretaceous

Ouachita Thrust Sheet

Pennsylvanian

Ordovician

Devonian

Barnett Shale

Woodford Shale

Caney Shale

100 miles

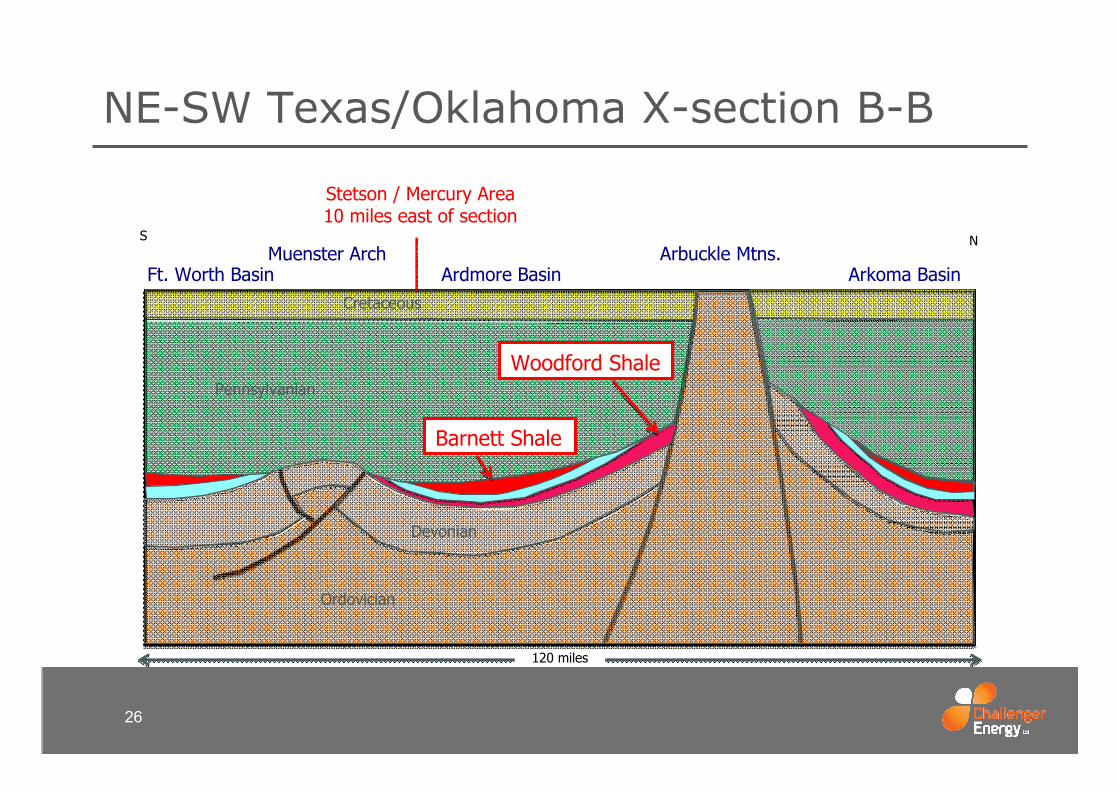

26

NE-SW Texas/Oklahoma X-section B-B

Ft. Worth Basin Arkoma Basin Ardmore Basin Arbuckle Mtns. Muenster Arch

Cretaceous

Pennsylvanian

Barnett Shale

Ordovician

Woodford Shale

NS

Devonian

Stetson / Mercury Area 10 miles east of section

120 miles