Embed Size (px)

Citation preview

INVESTOR PRESENTATIONJune 2013

Page 2

DISCLAIMER

June 2013

This presentation may contain forward-looking statements including, but not limited to,projections of future performance of products, financial conditions, results of operationsand cash flows. The statements are made on the basis of management’s views andassumptions regarding future events and business performance as of the time thestatements are made. Sonova cautions you that a number of important risks anduncertainties could cause actual results to differ materially from those discussed in theforward-looking statements. Such differences may result from the ability of Sonova tosuccessfully develop and introduce new products and market existing products, changesin competitive conditions and regulatory developments as well as from changes in theeconomic conditions that may affect the performance of the operations of Sonova.Sonova undertakes no obligation to update any forward-looking statements, whether asa result of new information, future events or otherwise. Therefore you should not placeundue reliance on them.

This presentation serves marketing purposes and constitutes neither an offer to sell nora solicitation to buy any securities. This presentation does not constitute an offeringprospectus within the meaning of Article 652a of the Swiss Code of Obligations nor alisting prospectus within the meaning of the listing rules of SIX Swiss Exchange.

Page 3

VISION

AT SONOVA, WE ENVISION …

June 2013

A WORLD WHERE EVERYONE

ENJOYS THE DELIGHT OF HEARING AND

THEREFORE LIVES A LIFE WITHOUT LIMITATIONS

Page 4

SONOVA GROUP

BROADEST OFFERING: HEARING INSTRUMENTS, COCHLEAR IMPLANTS …

… AND PROFESSIONAL AUDIOLOGICAL SERVICES

June 2013

HI Hearing Instruments Behind-The-Ear hearing instruments (BTE) FM systems

Custom In-The-Ear hearing instruments (ITE)

Hearing protection Wireless communication systems

Invisible extended-wear hearing instruments

Cochlear implants

CI Cochlear Implants

Page 5

BUSINESS CASE

CLEAR AND FOCUSED STRATEGY – CUSTOMER DRIVEN INNOVATION

June 2013

SONOVA: «HEAR THE WORLD»

Key to our success - Our customers and our employees

Broadest product and service offering / portfolio - Hearing instruments (Phonak, Unitron)

- Cochlear implants (Advanced Bionics)

- Professional services (Connect Hearing Group)

Strong competitive positions - Leading position in hearing instruments

- Strong contender on cochlear implants

- Strong position in selected key retail markets

Significant market share gain potential - High R&D spend – fast product introduction

- Differentiated multi-brand strategy

- Optimized multi-channel approach

Strong product pipelines - High innovation rate and rapid new product introduction

Productivity / efficiency gains - Leverage existing global infrastructure to expand margins

Financial targets until FY 2016/17(at constant FX rates)

- EBITA margin: return to mid-twenties

- ROCE: expand to low-thirties

Page 6

CONTENTS

1 MARKET PAGE 7

2 BUSINESS PAGE 11

3 CORPORATE STRATEGY PAGE 20

4 BUSINESS STRATEGIES PAGE 30

5 FINANCIAL INFORMATION PAGE 51

June 2013

1. MARKET

Page 8

MARKET

LOW PENETRATION RATE – AROUND 20% IN DEVELOPED COUNTRIES

MILD

MODERATE

PROFOUND

With hearing system Without hearing system

END-USER MARKET – PENETRATION*

- Profound loss- Moderate loss- Mild loss

70%50%10%

HI

HI

CI

HI

15%

* Source: Several industry statistics, Sonova estimates

AROUND 15% OF ADULTS HAVE SOME DEGREE OF HEARING IMPAIRMENT

June 2013

Page 9

MARKET

HEARING SOLUTIONS: INSTRUMENTS, IMPLANTS AND SERVICES

TOTAL HEARING CARE MARKET

- Market Size- Market CAGR- HI Size (units)- CI Size (units)

~ CHF 15-16 billion~ + 3-5%

10-11 million~ 40 thousand

COCHLEAR IMPLANTS CI

- Market Size- Market CAGR- CI Size (units)

~ CHF 900 million~ +10%

~ 40 thousand

HEARING INSTRUMENTS HI

- Market Size- Market CAGR- HI Size (units)

~ CHF 4.3 billion~ + 2-4%

10-11 million

CI

HI

June 2013

Page 10

MARKET

SERVICE CHANNELS: KEY TO ACCESS END-USERS

TOTAL HEARING CARE MARKET

- Market Size- Market CAGR- HI Size (units)- CI Size (units)

~ CHF 15-16 billion~ + 3-5%

10-11 million~ 40 thousand

COCHLEAR IMPLANTS CI

- Market Size- Market CAGR- CI Size (units)

~ CHF 900 million~ +10%

~ 40 thousand

HEARING INSTRUMENTS HI

- Market Size- Market CAGR- HI Size (units)

~ CHF 4.3 billion~ + 2-4%

10-11 millionINDEPENDENTS

GLOBAL KEY

ACCOUNTSLARGE RETAIL

ACCOUNTS

BUYINGGROUPS

HOSPITALS GOVERNMENT

OTHERS

June 2013

2. BUSINESS

Page 12

SONOVA GROUP

PERFORMANCE HISTORY – STRONG FINANCIAL TRACK RECORD

1H

SALESin CHF million

EBITAin CHF million

EBITAmargin in %

0

200

400

600

800

1'0001'200

1'400

1'600

1'800

2'000

07/08 08/09 09/10 10/11 11/12 12/13 13/140%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

50

100

150

200

250

300

350

400

450

07/08 08/09 09/10 10/11 11/12 12/13 13/14

FY 2008/09 FY 2009/10 FY 2010/11 FY 2011/12 FY 2012/13 CAGR 5-y

Sales growth reported +3.7% +20.1% +7.8% +0.2% +10.8% +8.3%

Sales growth in LC +10.8% +23.8% +13.3% +11.6% +7.4% +13.2%

EBITA margin 26.6% 28.0% 20.2% 19.5% 21.5% N/A

Basic EPS 4.35 3.32 3.50 3.71 4.62 +0.3%

Notes: FY 2007/08 Excluding one-off cost for the prohibited acquisition of the GN ReSound GroupFY 2009/10 Restated based on finalization of the acquisition accounting of Advanced BionicsFY 2012/13 Excluding one-off cost for AB Vendor B provision increase, AB Rixheim restructuring and settlement with a group of investors

2H

June 2013

Page 13

AB Center

Unitron Center

Sonova & Phonak HQ & Centers

DistributorsWHS Group Companies

Operation CentersPhonak Communications Center

InSound Center

Murten (CH)

Kitchener (CAN)

Ho Chi Minh City (VN)

Suzhou (CN)

Valencia (USA)

Newark (USA)

Stäfa (CH)

SONOVA GROUP

WELL ESTABLISHED GLOBAL INFRASTRUCTURE AND NETWORK

STRONG LOCAL PRESENCE – SUPPORTING CUSTOMERS WORLDWIDE

June 2013

Page 14

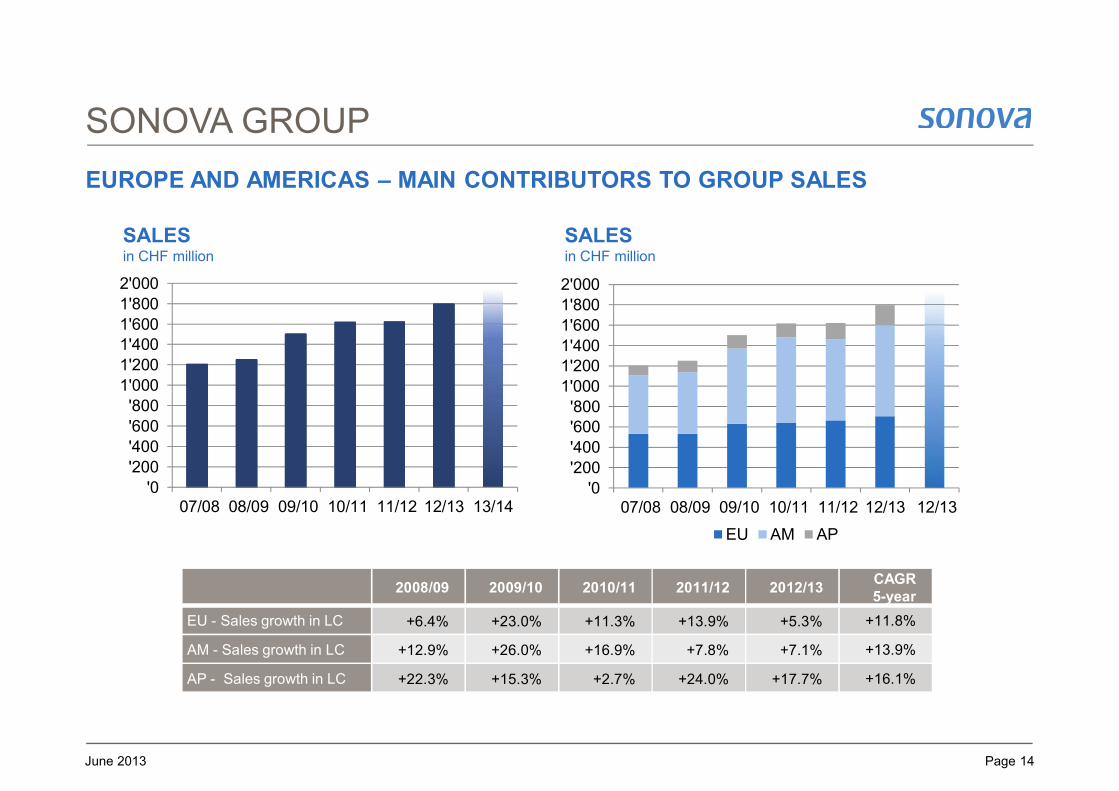

SONOVA GROUP

EUROPE AND AMERICAS – MAIN CONTRIBUTORS TO GROUP SALES

June 2013

SALESin CHF million

SALESin CHF million

2008/09 2009/10 2010/11 2011/12 2012/13CAGR5-year

EU - Sales growth in LC +6.4% +23.0% +11.3% +13.9% +5.3% +11.8%

AM - Sales growth in LC +12.9% +26.0% +16.9% +7.8% +7.1% +13.9%

AP - Sales growth in LC +22.3% +15.3% +2.7% +24.0% +17.7% +16.1%

'0

'200

'400

'600'800

1'000

1'2001'400

1'600

1'800

2'000

07/08 08/09 09/10 10/11 11/12 12/13 12/13

EU AM AP

'0

'200

'400

'600

'800

1'000

1'200

1'4001'600

1'800

2'000

07/08 08/09 09/10 10/11 11/12 12/13 13/14

Page 15

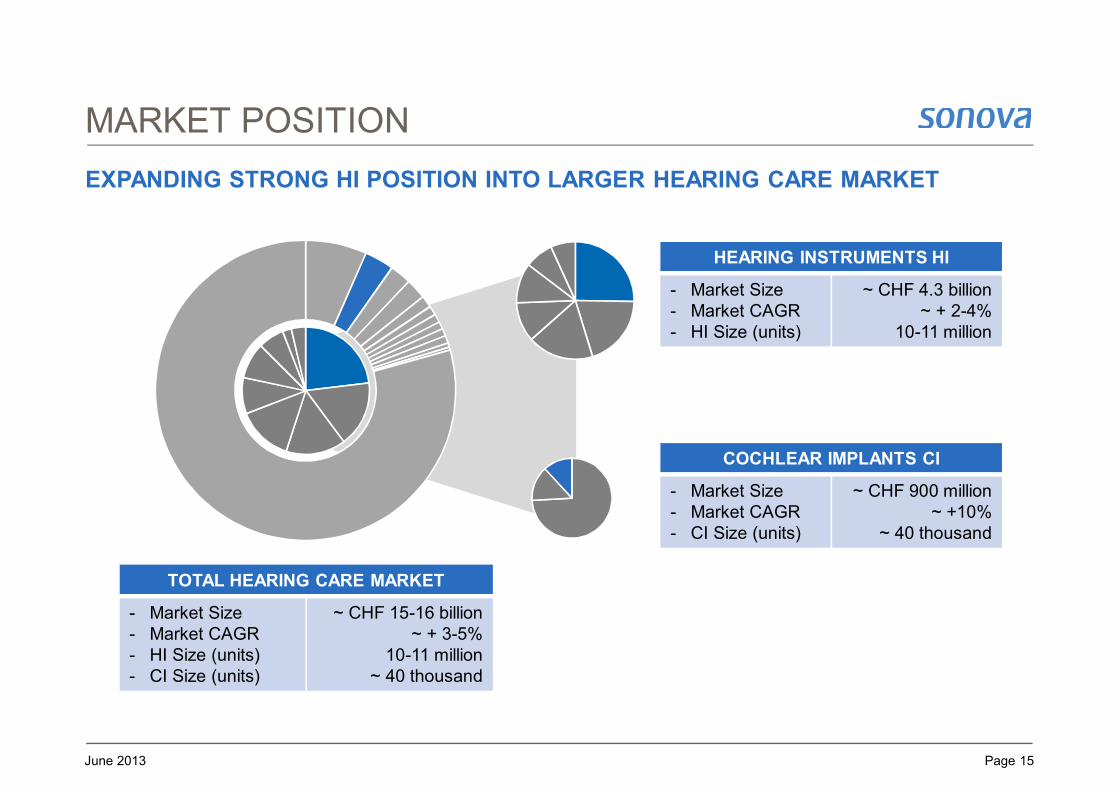

MARKET POSITION

EXPANDING STRONG HI POSITION INTO LARGER HEARING CARE MARKET

June 2013

TOTAL HEARING CARE MARKET

- Market Size- Market CAGR- HI Size (units)- CI Size (units)

~ CHF 15-16 billion~ + 3-5%

10-11 million~ 40 thousand

COCHLEAR IMPLANTS CI

- Market Size- Market CAGR- CI Size (units)

~ CHF 900 million~ +10%

~ 40 thousand

HEARING INSTRUMENTS HI

- Market Size- Market CAGR- HI Size (units)

~ CHF 4.3 billion~ + 2-4%

10-11 million

Page 16

MARKET POSITION

SERVICE CHANNELS: STRONG PARTNER TO IND, LRA, BG AND GOVT

TOTAL HEARING CARE MARKET

- Market Size- Market CAGR- HI Size (units)- CI Size (units)

~ CHF 15-16 billion~ + 3-5%

10-11 million~ 40 thousand

COCHLEAR IMPLANTS CI

- Market Size- Market CAGR- CI Size (units)

~ CHF 900 million~ +10%

~ 40 thousand

HEARING INSTRUMENTS HI

- Market Size- Market CAGR- HI Size (units)

~ CHF 4.3 billion~ + 2-4%

10-11 millionINDEPENDENTS

GLOBAL KEY

ACCOUNTSLARGE RETAIL

ACCOUNTS

BUYINGGROUPS

HOSPITALS GOVERNMENT

OTHERS

SOONSales Split

June 2013

Page 17

BUSINESSES

BALANCED PORTFOLIO OF PROFITABLE GROWTH BUSINESSES

June 2013

SONOVA Group

HEARING INSTRUMENT (HI)Segment

IMPLANT (CI)Segment

CIADVANCED

BIONICS

Business

HIPHONAK

Business

HIUNITRON

Business

HIRETAIL

Business

Page 18

HI SEGMENT

PERFORMANCE HISTORY – STRONG FINANCIAL TRACK RECORD

SALESin CHF million

EBITAin CHF million

EBITAmargin in %

0

200

400

600

800

1'000

1'200

1'400

1'600

1'800

2'000

07/08 08/09 09/10 10/11 11/12 12/130%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

50

100

150

200

250

300

350

400

450

07/08 08/09 09/10 10/11 11/12 12/13

1H 2H

FY 2008/09 FY 2009/10 FY 2010/11 FY 2011/12 FY 2012/13 CAGR 5-y

Sales growth reported +3.7% +18.1% +4.8% -1.4% +8.2% +6.5%

Sales growth in LC +10.8% +21.7% +10.1% +9.7% +4.9% +11.3%

EBITA margin 27.2% 29.0% 24.1% 22.3% 23.3% N/A

Note: FY 2007/08 Excluding one-off cost for the prohibited acquisition of the GN ReSound Group

June 2013

Page 19

CI SEGMENT

PERFORMANCE HISTORY

SALESin CHF million

EBITAin CHF million

EBITAmargin in %

0

25

50

75

100

125

150

07/08 08/09 09/10 10/11 11/12 12/13-100%

-80%

-60%

-40%

-20%

0%

20%

-50

-40

-30

-20

-10

0

10

07/08 08/09 09/10 10/11 11/12 12/13

FY 2008/09 FY 2009/10 FY 2010/11 FY 2011/12 FY 2012/13 CAGR 3-y

Sales growth reported -- -- +180.5% +36.0% +52.3% > +80.0%

Sales growth in LC -- -- +202.1% +53.5% +47.1% > +80.0%

EBITA margin* -- -31.0% -63.4% -25.0% 1.2% N/A

1H 2H

* FY 2012/13 Excluding one-off cost for AB Vendor B provision at AB, AB Rixheim restructuring and settlement with a group of investors

June 2013

3. CORPORATE STRATEGY

Page 21

MISSION

June 2013

WE STRIVE TO BE RECOGNIZED AS THE INNOVATION LEADER …

… IN THE GLOBAL HEARING CARE MARKET

HI Hearing Instruments Behind-The-Ear hearing instruments (BTE) FM systems

Custom In-The-Ear hearing instruments (ITE)

Hearing protection Wireless communication systems

Invisible extended-wear hearing instruments

Cochlear implants

CI Cochlear Implants

Page 22

FINANCIAL TARGETS

ON COURSE FOR MID TERM FINANCIAL TARGETS

Notes: FY 2007/08 Excluding one-off cost for the prohibited acquisition of the GN ReSound GroupFY 2009/10 Restated based on finalization of the acquisition accounting of Advanced BionicsFY 2012/13 Excluding one-off cost for AB Vendor B provision at AB, AB Rixheim restructuring and settlement with a group of investors

June 2013

Page 23

STRATEGY

SIX KEY STRATEGIES DRIVING CORE SALES AND EARNINGS GROWTH

1 INNOVATION

2 MARKET

3 PRODUCT

4 PORTFOLIO

5 RESOURCE

6 ACQUISITION

CORPORATE STRATEGIES

1 HI PHONAK

2 HI UNITRON

3 HI RETAIL

4 CI ADVANCED BIONICS

BUSINESS STRATEGIES

June 2013

Page 24

INNOVATION STRATEGY

FOCUS ON CONTINUOUS INNOVATION TO GROW SALES AND EARNINGS

June 2013

Q1 15 Q2 15Q1 14 Q2 14 Q3 14 Q4 14Q1 13 Q2 13 Q3 13 Q4 13

MARKETING

SALES & DISTRIBUTION

PRODUCTIVITY & EFFICIENCY

RESOURCES & PROCESSES

NEW PRODUCTS

CORE: DRIVE STRONG NEW PRODUCT PIPELINE – GROSS R&D 7-8% OF SALES

Page 25

MARKET STRATEGY

GROW MARKET POSITION ALONG 4 MAIN GROWTH VECTORS

June 2013

FOCUS ON KEY INITIATIVES TO SUPPORT GROWTH STRATEGY

1

2

3

4

Penetrate existing markets– WHS account development– Dual-brand strategy– Continuous product innovation

Expand accessible markets– BRIC markets– New product formats

Integrate service channels– Retail network expansion– Integration & productivity

Develop consumer base– Direct marketing– Lead generation processes

Page 26

PRODUCT STRATEGY

PROVIDE COMPLETE CUSTOMER SOLUTIONS: HW, SW AND SERVICES

June 2013

PLATFORM CONCEPT APPROACH TO SOLUTION DEVELOPMENT

Page 27

PORTFOLIO STRATEGY

DEVELOP BALANCED PORTFOLIO OF PROFITABLE GROWTH BUSINESSES

June 2013

LEAD INNOVATION IN HEARING INSTRUMENTS AND IMPLANTS

DOG

???

COW

STAR

MARKET SHARE

Hig

hLo

w

MA

RK

ET

GR

OW

TH

LYRIC

HighLow

Hig

hLo

w

HI

CI

COM

INVEST RETURN

Page 28

RESOURCE STRATEGY

LEVERAGE GLOBAL INFRASTRUCTURE TO EXPAND MARGINS

RE-BALANCE GLOBAL OPEX BASE TO CREATE NATURAL HEDGE

0

50

100

150

200

2012 2016

SALES

OPEX0

50

100

150

200

2012 2016

SALES

OPEX0

50

100

150

200

2012 2016

SALES

OPEX

AMERICAS EUROPE APAC

June 2013

Page 29

ACQUISITION STRATEGY

INVEST TO LEVERAGE EXISTING CHANNELS AND PRODUCTS

June 2013

TARGETS: STRICT CRITERIA FOR STRATEGIC AND FINANCIAL FIT

HI

CI

Channels

,0

3,000

06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16

ISM

AB

4. BUSINESS STRATEGIES

Page 31

PHONAK

SONOVA: BALANCED PORTFOLIO OF PROFITABLE GROWTH BUSINESSES

June 2013

SONOVA Group

HEARING INSTRUMENT (HI)Segment

IMPLANT (CI)Segment

CIADVANCED

BIONICS

Business

HIPHONAK

Business

HIUNITRON

Business

HIRETAIL

Business

Page 32

PHONAK

BUSINESS STRATEGY

PHONAK: «LIFE IS ON»

Mission / value proposition - Drive innovation leadership to expand market position

Markets - Cover broadest global (whole)sale, distribution & support network

Products - Offer complete range across all form factors and performance levels

Product pipeline - Drive high innovation rate and rapid new product introduction

Productivity / efficiency - Leverage global sales & production infrastructure to expand margins

Selected initiatives 2013/14 - B2B/B2C marketing campaign: «Phonak engaging voices»

- New product launch Spring 2013

- New product launch Fall 2013

- Lyric 2.3

- DM (2.4 GHz) communication / wireless connectivity standard “ROGER”

- China market growth and expansion (lead)

- etc.

June 2013

Page 33

PHONAK

MARKETS: COVER BROADEST GLOBAL SALES & SUPPORT NETWORK

FURTHER PENETRATE AM AND EU – EXPAND POSITIONS IN AP (CHINA)

AM EU

AP

June 2013

Page 34

PHONAK

PRODUCT PIPELINE: DRIVE HIGH INNOVATION & PRODUCT LAUNCH RATE

COMPLETE RANGE ACROSS ALL FORMATS AND PERFORMANCE LEVELS

SPICE (new HW / new DSP / 65nm) QUEST (new HW / new core SW / 65nm) NEXT PLATFORM

BT

E –

Bo

lero

Q

ITE

–V

irto

Q

RIC

–A

ud

éo Q

PO

WE

R –

Naí

da

Q

F 5

F 1

F 2

F 3

F 4

F 5

Lyric2 Lyric3

T 2.1 T 3.3T 3.0 T 4.0T 3.1 T 3.2 T 4.1 T 4.2T 2.0T 1.1

FM System (analog) Roger (digital / 2.4 GHz)

F1 / 4

HI - Premium

HI - Advanced

HI - Standard

HI - Essential/Basic

HI - Platform

HI - New EW Format

Fitting Software(TARGET)

Communication

F 1

F 3

F 1

F 1

F 2

F 2

F 4

F 5

F 5

1H 15 2H 151H 13 2H 131H 11 2H 11 1H 14 2H 141H 12 2H 12TIMELINE / CY

Note: Subject to change

June 2013

Page 35

PHONAK PRODUCT PORTFOLIO

June 2013

* based on previous generation platforms

BTE product line ITE product line RIC Power Pediatric

Premium Phonak Bolero Q90 Phonak Virto Q90 Audéo Q90 Naída Q90

Advanced Phonak Bolero Q70 Phonak Virto Q70 Audéo Q70 Naída Q70 Nios S V*

Standard Phonak Bolero Q50 Phonak Virto Q50 Audéo Q50 Naída Q50 Nios S III*

Essential Phonak Dalia* Phonak Dalia* Audéo Q30 Naída Q30

Basic Milo* Milo*

Page 36

UNITRON

SONOVA: BALANCED PORTFOLIO OF PROFITABLE GROWTH BUSINESSES

June 2013

SONOVA Group

HEARING INSTRUMENT (HI)Segment

IMPLANT (CI)Segment

CIADVANCED

BIONICS

Business

HIPHONAK

Business

HIUNITRON

Business

HIRETAIL

Business

Page 37

UNITRON

BUSINESS STRATEGY

UNITRON: «HEARING MATTERS»

Mission / value proposition - Drive leadership in customer experience

Markets - Deeper penetration in core markets in Europe and NA

Products - Offer flexible range across many form factors and all performance levels

Product pipeline - Drive focused innovation and rapid new product introduction

Productivity / efficiency - Leverage Sonova technology & production platform to expand margins

Selected initiatives 2013/14 - B2B Marketing campaign “favorite sound”

- UT customer experience initiatives

- New product launch Spring 2013

- New product launch Fall 2013

- China market growth and expansion (complement Phonak initiative)

- etc.

June 2013

Page 38

UNITRON

MARKETS: EXPAND GLOBAL NETWORK FROM STRONG BASE IN NA

DEVELOP POSITIONS IN EU – SUPPORT SONOVA EXPANSION IN AP (CHINA)

AM EU

AP

June 2013

Page 39

UNITRON

PRODUCT PIPELINE: DRIVE FOCUSED PRODUCT INNOVATION

FLEXIBLE RANGE ACROSS 3 FORMATS AND ALL PERFORMANCE LEVELS

ERA (new HW / new DSP / 65nm) NEXT PLATFORM Q

–F

LE

X 1

M–

FL

EX

1

Mo

xi K

iss

–R

IC

FL

EX

Tri

al&

Up

gra

de

F 1

F2

F 3

TF 1.1 TF 2.3TF 2.0 TF 2.3TF 2.1 TF 2.2 TF 4.0 TF 4.1TF 1.0

HI - Premium

HI - Advanced

HI - Standard

HI - Essential/Basic

HI - Platform

Fitting Software(TRUEFIT)

Q P

RO

MP

RO

Q-

M 2

Q P

RO

MP

RO

Q 1

M 1

1H 15 2H 151H 13 2H 131H 11 2H 11 1H 14 2H 141H 12 2H 12TIMELINE / CY

Note: Subject to change

June 2013

Page 40

UNITRON PRODUCT PORTFOLIO

June 2013

* based on previous generation platforms

BTE product line ITE product line RIC Power Flex Trial

Premium Quantum Pro Quantum Pro Moxi Kiss Pro Moxi Pro

Quantum 20 Quantum 20 Moxi Kiss 20 Moxi 20 Max 20

Quantum 12 Quantum 12 Moxi Kiss 12 Moxi 12

Standard Quantum 6 Quantum 6 Moxi Kiss 6 Moxi 6 Max 6

Essential Quantum E Quantum E Moxi Kiss E Moxi E Max E

Basic Shine* Shine*

Advanced

An

y Perfo

rman

ce

Level

Page 41

CONNECT HEARING

SONOVA: BALANCED PORTFOLIO OF PROFITABLE GROWTH BUSINESSES

June 2013

SONOVA Group

HEARING INSTRUMENT (HI)Segment

IMPLANT (CI)Segment

CIADVANCED

BIONICS

Business

HIPHONAK

Business

HIUNITRON

Business

HIRETAIL

Business

Page 42

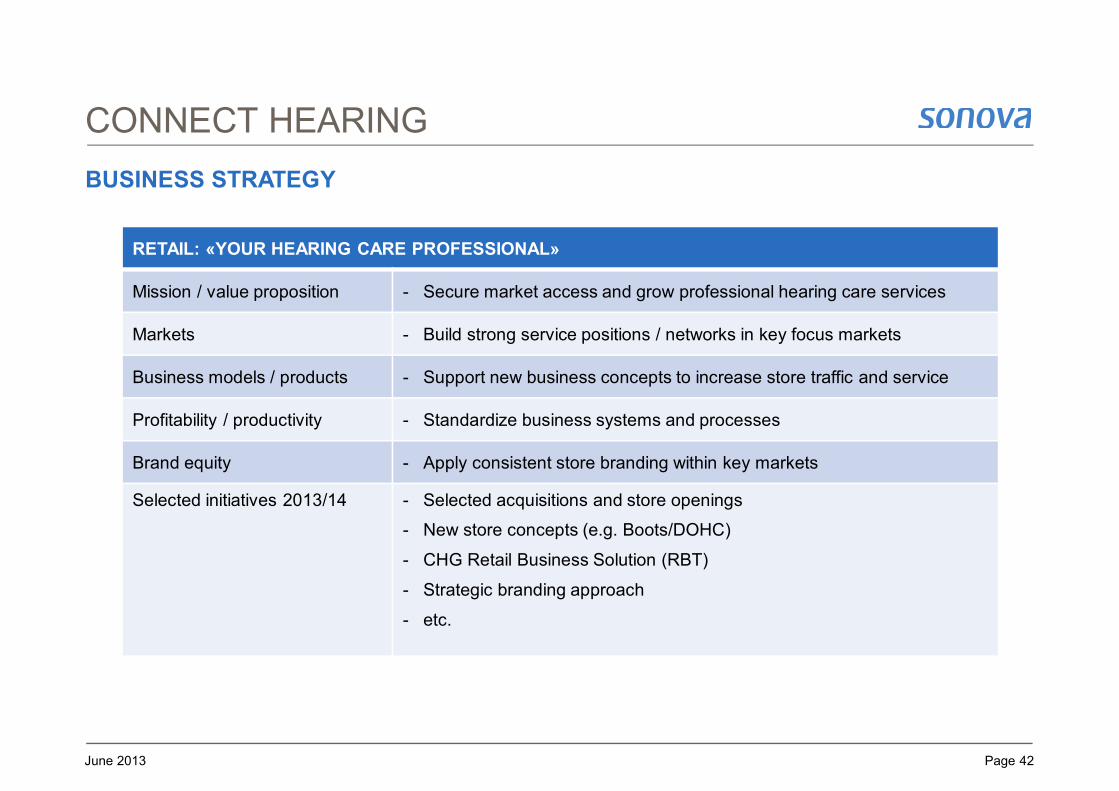

CONNECT HEARING

BUSINESS STRATEGY

RETAIL: «YOUR HEARING CARE PROFESSIONAL»

Mission / value proposition - Secure market access and grow professional hearing care services

Markets - Build strong service positions / networks in key focus markets

Business models / products - Support new business concepts to increase store traffic and service

Profitability / productivity - Standardize business systems and processes

Brand equity - Apply consistent store branding within key markets

Selected initiatives 2013/14 - Selected acquisitions and store openings

- New store concepts (e.g. Boots/DOHC)

- CHG Retail Business Solution (RBT)

- Strategic branding approach

- etc.

June 2013

Page 43

CONNECT HEARING

MARKETS: BUILD STRONG SERVICE POSITIONS IN KEY MARKETS

FOCUS ON: US, CA, BR, UK, FR, BE, AT, AUS/NZ

AMEU

AP

June 2013

Page 44

CONNECT HEARING OFFERING

MARKET LEADING SHOP IN SHOP CONCEPT – EXAMPLE DOHC / BOOTS (UK)

PREMIUM MARKET ACCESS BY PARTNERSHIP WITH LEADING PHARMACY CHAIN

Well-established partnership between David Ormerod Hearing Centres (DOHC) and Boots since 2003

Number of locations in the UK grew from 64 to more than 340 during that time

Boots hearingcare offers professional audiological services at attractive locations

Clear synergies for both sides from increased store traffic

Partnership expanded through 49% minority stake in DOHC by Boots

June 2013

Page 45

ADVANCED BIONICS

SONOVA: BALANCED PORTFOLIO OF PROFITABLE GROWTH BUSINESSES

June 2013

SONOVA Group

HEARING INSTRUMENT (HI)Segment

IMPLANT (CI)Segment

CIADVANCED

BIONICS

Business

HIPHONAK

Business

HIUNITRON

Business

HIRETAIL

Business

Page 46

ADVANCED BIONICS

BUSINESS STRATEGY

ADVANCED BIONICS: «PATIENTS ALWAYS FIRST»

Mission / value proposition - Strive for performance leadership – leverage AB and PH combination

Markets - Build global direct sales & support network - grow from strong US base

Products - Expand innovative range of processors, implants and electrodes

Product pipeline - Accelerate innovation rate – synchronize with PH pipeline and platforms

Productivity / efficiency - Leverage PH technology & process platform to expand margins

Selected initiatives 2013/14 - AB Partner Program for retail: «Think beyond Hearing Aids»

- AB / PH system & product pipeline

- New product launches 2013/14 (implants, electrodes, processors)

- China market development

- etc.

June 2013

Page 47

ADVANCED BIONICS

MARKETS: EXPAND GLOBAL NETWORK FROM STRONG BASE IN US

GROW POSITIONS IN EU, BR, JP – BUILD PLATFORM IN CHINA

AM EU

AP

June 2013

Page 48

ADVANCED BIONICS

HOW A COCHLEAR IMPLANT WORKS

SoundprocessorSound is captured and converted into detailed digital information

Magnetic headpieceTransmits digital signal wirelessly to the implant

ImplantConverts digital information into electrical signal

ElectrodeDelivers signal as electrical stimulation to the auditory nerve

June 2013

Page 49

ADVANCED BIONICS

PRODUCT PIPELINE: ACCELERATE INNOVATION RATE – LEVERAGE PH

EXPAND RANGE OF INNOVATIVE PROCESSORS, IMPLANTS, ELECTRODES

FDACE

FDACE

FDACE

WOLVERINE / QUEST (new HW / new DSP / 65nm) NEXT PLATFORM

CI - Electrodes

CI - Implants

CI - Processors

CI - Platform

Fitting Software(SOUNDWAVE)

N Pro 1 N Pro 2N Pro 2N Pro 3

N Imp 2 N Imp 3

N El 2 N El 3

1H 15 2H 151H 13 2H 131H 11 2H 11 1H 14 2H 141H 12 2H 12TIMELINE / CY

SW 2.0 SW 3.0 SW 4.0

NeptuneNeptune Naída CI Q70

N Imp 2

N Pro 3

N Imp 3

N El 3HiFocusMid-Scala N El 2

Note: Subject to change, timing dependent upon regulatory approvals

HiRes 90kAdvantage

June 2013

Page 50

ADVANCED BIONICS PRODUCT PORTFOLIO

June 2013

* approved in Europa and Canada, not yet approved in the US

Implant HiRes 90K Advantage HiRes 90K

Electrodes HiFocus Mid-Scala HiFocus 1j HiFocus Helix

Sound Processors Naída CI* Neptune Harmony BTE

Software SoundWave 2.1

5. FINANCIAL INFORMATION

Page 52

FULL YEAR 2012/13

SUMMARY OF FINANCIAL RESULTS

May 21, 2013

– Solid sales growth

– Sales of CHF 1’795.3 million – up 10.8% in Swiss francs and 7.4% in LC

– All major regions contributing to the increase

– Strong EBITA growth and margin expansion – normalized for one-off charges

– Normalized EBITA of CHF 386.4 million – up 22.6% in Swiss francs and 15.4% in LC

– Normalized EBITA margin of 21.5%, expanding by 200 bps and by 140 bps in LC

– Reported EBITA of CHF 182.8 million – fully reflecting Vendor B provision increase

– Both segments contributing

– Robust growth in hearing instruments (+4.9% in LC) – EBITA margin expanding by 100 bps

– Break-even target reached in cochlear implants – supported by a strong growth of +47.1% in LC

– High growth in cash flow – sound financial position

– Operating free cash flow of CHF 318.6 million – up 33% in Swiss francs

– Net cash position of CHF 185.8 million

– Normalized ROCE of 22.6%, up from 19.2% in FY 2011/12

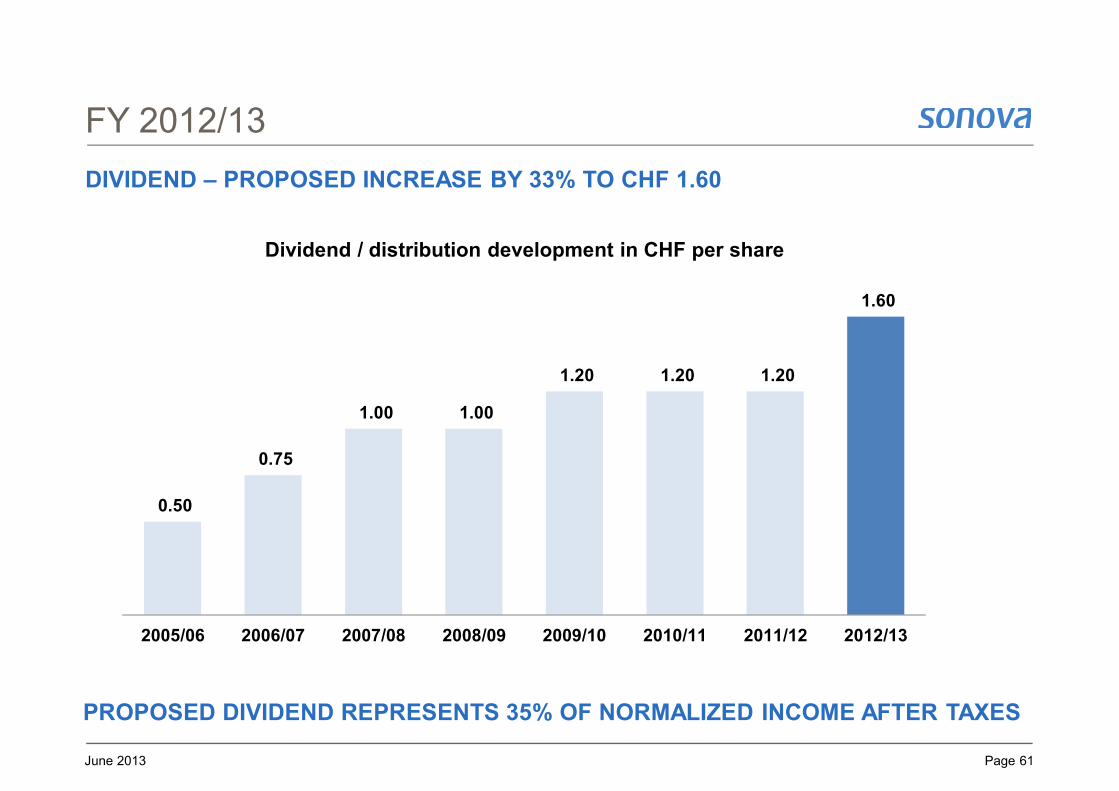

– Dividend increase of 33% to CHF 1.60 proposed

Page 53

FY 2012/13

June 2013

in CHF million FY 2011/12 FY 2012/13 Δ % in CHF Δ % in LC

Sales 1'619.8 1'795.3 10.8% 7.4%

Gross profit 1'105.9 1'240.1 12.1% 8.2%

- Gross profit margin 68.3% 69.1%

OPEX 790.7 853.7 8.0% 5.4%

EBITA 315.2 386.4 22.6% 15.4%

- EBITA margin 19.5% 21.5%

Operating free cash flow 239.5 318.6 33.0%

EPS (in CHF) 3.71 4.62 24.5%

ROCE 19.2% 22.6%

EXPANSION OF GROSS PROFIT MARGIN - IN BOTH SEGMENTS

SOLID FINANCIAL PERFORMANCE – NORMALIZED

Page 54

FY 2012/13

GROUP EBITA DEVELOPMENT

SOLID EBITA IMPROVEMENT FROM ORGANIC GROWTH – CI BREAKING EVEN

EBITA2011/12

Organic Growth

EBITA2012/13

normalized

FX effect

EBITA2012/13

const. FXnormalized

386.4

+22.7

315.2 +43.4

+48.5+15.4%

+71.2+22.6%Margin:

19.5%Margin:21.5%

+5.1

Acquisitions

363.7

Margin:20.9%

One-offcost

2012/13

EBITA (reported) 2012/13

-203.6

182.8

Notes: Average FX rates: USD/CHF 0.94 (prior year: 0.88) and EUR/CHF 1.21 (prior year: 1.21)One-off cost: AB Vendor-B case CHF 197.8m, restructuring AB Rixheim CHF 3.2m, settlement with a group of investors CHF 2.6m

Margin:10.2%

June 2013

Page 55

FY 2012/13

DETAILS BY BUSINESS SEGMENTS

in CHF million 2011/12 2012/13Growth

in lcGrowth in CHF

Sales

Hearing Instruments- thereof organic

1’523.5 1’648.5 +4.9%+2.6%

+8.2%

Cochlear Implants 96.3 146.7 +47.1% +52.3%

Group 1’619.8 1’795.3 +7.4% +10.8%

EBITA

Hearing Instruments 339.3 384.7 +6.7% +13.4%

Cochlear Implants -24.1 1.8 n/a n/a

Group 315.2 386.4 +15.4% +22.6%

June 2013

Page 56

FY 2012/13

June 2013

OPERATING EXPENSES

* One-off cost: AB Vendor B case CHF 197.8m, restructuring AB Sarl CHF 3.2m, settlement with group of investors CHF 2.6m

SALES & MARKETING, G&A INCREASE: DRIVEN BY RETAIL ACQUISITION INTEGRATION, CONCENTRATED PRODUCT LAUNCH AND LYRIC RAMP UP EFFORTS

in CHF million FY 2011/12 FY 2012/13 Δ % in CHF Δ % in LC

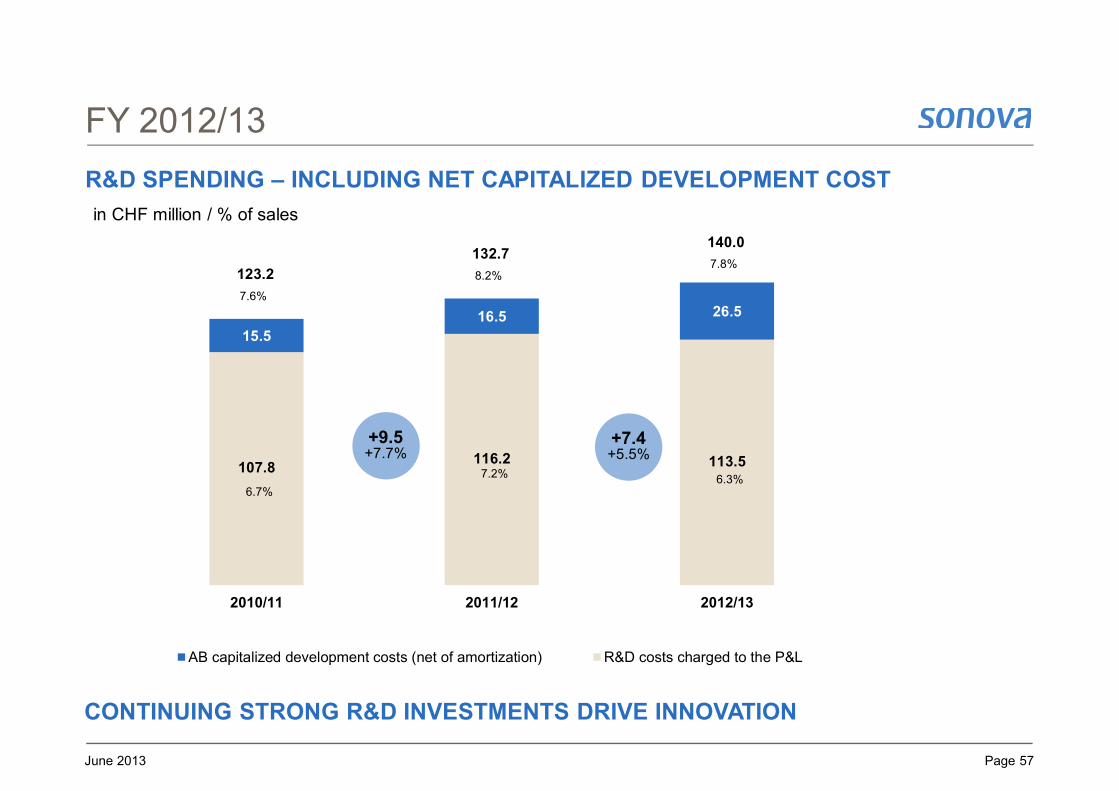

Research & Development 116.2 113.5 -2.3% -3.7%

in % of sales 7.2% 6.3%

Sales & Marketing 503.4 558.9 11.0% 8.0%

in % of sales 31.1% 31.1%

General & Administration 168.7 181.3 7.5% 5.4%

in % of sales 10.4% 10.1%

Subtotal 788.2 853.7 8.3% 5.7%

in % of sales 48.7% 47.6%

Other expenses* 2.5 203.6

Page 57

107.8116.2 113.5

15.5

16.5 26.57.6%

8.2%7.8%

123.2

132.7140.0

6.7%

7.2% 6.3%

2010/11 2011/12 2012/13

AB capitalized development costs (net of amortization) R&D costs charged to the P&L

FY 2012/13

June 2013

R&D SPENDING – INCLUDING NET CAPITALIZED DEVELOPMENT COST

+9.5+7.7%

+7.4+5.5%

in CHF million / % of sales

CONTINUING STRONG R&D INVESTMENTS DRIVE INNOVATION

Page 58

FY 2012/13

June 2013

REPORTED RESULTS AND INCOME TAXES

POTENTIAL TAX EFFECT OF VENDOR B PROVISION INCREASE NOT CAPITALIZED

in CHF million FY 2011/12 FY 2012/13 Δ % in CHF

EBITA 315.2 182.8 -42.0%

Amortization / Impairment -27.5 -26.1 -5.0%

Operating profit (EBIT)in % of sales

287.717.8%

156.78.7%

-45.5%

Financial result -5.9 -6.9 15.9%

Income before taxes 281.8 149.8 -46.8%

Income taxes -35.4 -37.8 6.8%

- Income tax rate 12.6% 25.2%

Income after taxesin % of sales

246.415.2%

112.06.2%

-54.5%

Page 59

FY 2012/13

June 2013

SIGNIFICANT INCREASE IN CASH FLOW

in CHF million FY 2011/12 FY 2012/13 Δ % in CHF

Cash flow before changes in NWC 387.5 443.7 14.5%

Changes in net working capital and taxes paid -82.7 -56.6 -31.5%

Operating cash flowin % of sales

304.818.8%

387.121.6%

27.0%

Cash flow from investing activities (excl. acquisitions) -65.3 -68.5 4.9%

Operating free cash flowin % of sales

239.514.8%

318.617.7%

33.0%

Cash consideration for acquisitions -83.1 -56.2 -32.4%

Free cash flow 156.4 262.4 67.7%

Cash flow from financing activities -127.5 -21.8 n/a

Changes in cash and cash equivalents 26.8 242.8 > 100%

OPERATING FREE CASH FLOW INCREASING 33.0%

Page 60

FY 2012/13

June 2013

BALANCE SHEET

TURNING NET CASH POSITIVE – INVENTORY INCREASES DRIVEN BY LAUNCHES

in CHF million FY 2011/12 FY 2012/13 Δ % in CHF

Net working capital 163.4 187.1 14.5%

Days sales outstanding (DSO) 72 71 -1.4%

Days inventory outstanding (DIO) 122 148 21.3%

Capital employed 1'540.3 1'449.5 -5.9%

Net cash -64.4 185.8 > 100%

Equity 1'475.9 1'635.3 10.8%

Equity in % of total assets 64.5% 61.0%

Page 61

FY 2012/13

June 2013

DIVIDEND – PROPOSED INCREASE BY 33% TO CHF 1.60

0.50

0.75

1.00 1.00

1.20 1.20 1.20

1.60

2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

Dividend / distribution development in CHF per share

PROPOSED DIVIDEND REPRESENTS 35% OF NORMALIZED INCOME AFTER TAXES

Page 62

OUTLOOK

FY 2013/14 GUIDANCE – IN LOCAL CURRENCIES

Guidance

FY 2013/14

Actual - normalized

FY 2012/13

Sales

Sales growth in LC

thereof acquisition related growth

FX-impact

Total sales growth in CHF

6%-8%

approx. 1%

n/a

n/a

7.4%

2.2%

3.4%

10.8%

EBITA

EBITA growth in lc

FX-impact

Total EBITA growth in CHF

9%-13%

n/a

n/a

15.4%

7.2%

22.6%

June 2013

Page 63

OUTLOOK

FY 2013/14 GUIDANCE – FX IMPACT ON SALES AND MARGINS

0.70

0.75

0.80

0.85

0.90

0.95

1.00

Ap

r-11

Ma

y-1

1

Ju

n-1

1

Jul-1

1

Au

g-1

1

Se

p-1

1

Oct

-11

Oct

-11

No

v-1

1

De

c-1

1

Ja

n-1

2

Fe

b-1

2

Ma

r-1

2

Ap

r-12

Ma

y-1

2

Ju

n-1

2

Jul-1

2

Au

g-1

2

USD/CHF EUR/CHF

Rate Sales EBITA

USD/CHF +/- 5% +/- CHF 38 million +/- CHF 11 million

EUR/CHF +/- 5% +/- CHF 24 million +/- CHF 12 million

June 2013

Page 64

BUSINESS CASE

CLEAR AND FOCUSED STRATEGY – CUSTOMER DRIVEN INNOVATION

SONOVA: «HEAR THE WORLD»

Key to our success - Our customers and our employees

Broadest product and service offering / portfolio - Hearing instruments (Phonak, Unitron)

- Cochlear implants (Advanced Bionics)

- Professional services (Connect Hearing Group)

Strong competitive positions - Leading position in hearing instruments

- Strong contender on cochlear implants

- Strong position in selected key retail markets

Significant market share gain potential - High R&D spend – fast product introduction

- Differentiated multi-brand strategy

- Optimized multi-channel approach

Strong product pipelines - High innovation rate and rapid new product introduction

Productivity / efficiency gains - Leverage existing global infrastructure to expand margins

Financial targets until FY 2016/17(at constant FX rates)

- EBITA margin: return to mid-twenties

- ROCE: expand to low-thirties

June 2013

THANK YOU VERY MUCH

![PIRAMAL HEALTHCARE LTD - Investor Presentation_June 2011[1]](https://img.pdfslide.net/doc/110x75/5500452f4a7959e6728b52a6/piramal-healthcare-ltd-investor-presentationjune-20111.jpg)