Embed Size (px)

Citation preview

IPAA Oil & Gas Investment SymposiumLondon

July 7, 2005

2

Forward-looking Statements

This presentation contains projections and other forward-looking

statements within the meaning of Section 27A of the U.S. Securities

Act of 1933 and Section 21E of the U.S. Securities Exchange Act of

1934. These projections and statements reflect the Company’s

current views with respect to future events and financial performance.

No assurances can be given, however, that these events will occur or

that these projections will be achieved, and actual results could differ

materially from those projected as a result of certain factors. A

discussion of these factors is included in the Company’s periodic

reports filed with the U.S. Securities and Exchange Commission.

3

Magnum Hunter Acquisition

• Merger closed June 7th

• Transaction summary– Issued 39.5 million shares (doubles market cap) – Total shares outstanding 81.3 million– Assumed $590 million of debt

• Doubles production

• Triples proved reserves

• Expands drilling program

• Adds Permian Basin and Gulf of Mexico operations

4

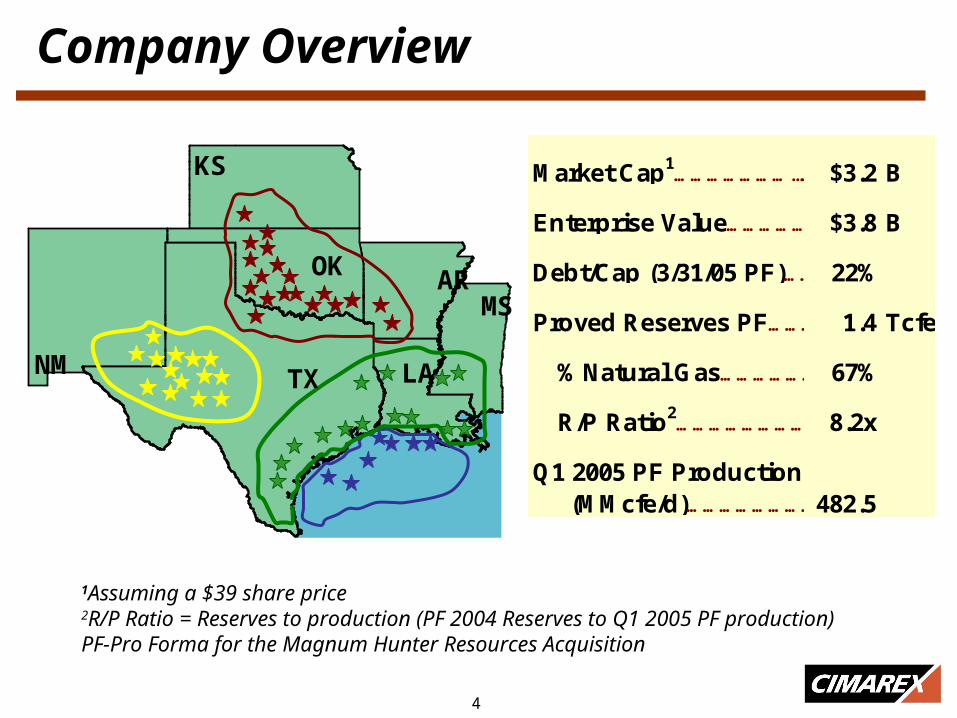

Company Overview

NM

KS

TX LA

MSAROK

Market Cap1…………………...…. $3.2 B

Enterprise Value…………………..$3.8 B

Debt/Cap (3/31/05 PF)…………………………..22%

Proved Reserves PF…………..1.4 Tcfe

% Natural Gas……………………..67%

R/P Ratio2…………………………….8.2x

Q1 2005 PF Production(MMcfe/d)………………………482.5

1Assuming a $39 share price2R/P Ratio = Reserves to production (PF 2004 Reserves to Q1 2005 PF production) PF-Pro Forma for the Magnum Hunter Resources Acquisition

5

Combined Company Core Operating Areas

Gulf Coast

9%

GOM6%

Other2%

Permian45%

Mid-Continent

38%

GOM24%

Other5%

Permian14%

Gulf Coast27%

Mid-Continent

30%

NM

KS

TX LA

MSAROK

> $625 MM of 2005E PF Capital

2004 PF Reserves - 1,456 Bcfe2004 PF Reserves - 1,456 Bcfe Q1 2005 PF Prod. 482.5 MMcfepdQ1 2005 PF Prod. 482.5 MMcfepd

GOM14%

Other2%

Permian27%

Gulf Coast21%

Mid-Continent

36%

6

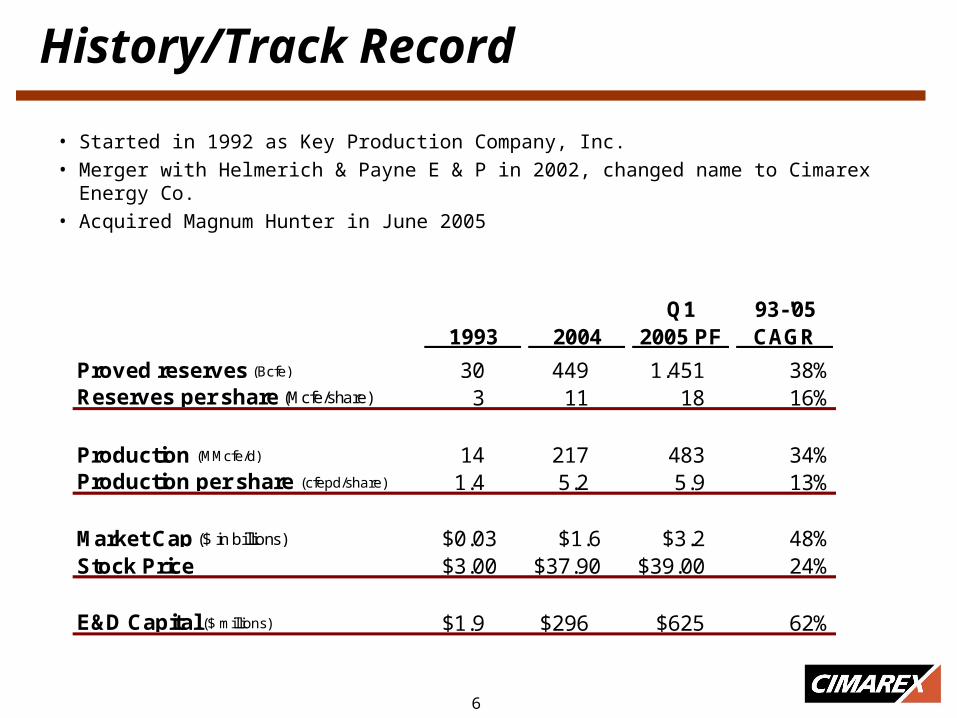

History/Track Record

• Started in 1992 as Key Production Company, Inc.• Merger with Helmerich & Payne E & P in 2002, changed name to Cimarex Energy Co.• Acquired Magnum Hunter in June 2005

Q1 93-'051993 2004 2005 PF CAGR

Proved reserves (Bcfe) 30 449 1,451 38%Reserves per share (Mcfe/share) 3 11 18 16%

Production (MMcfe/d) 14 217 483 34%Production per share (cfepd/share) 1.4 5.2 5.9 13%

Market Cap ($ in billions) $0.03 $1.6 $3.2 48%Stock Price $3.00 $37.90 $39.00 24%

E&D Capital ($ millions) $1.9 $296 $625 62%

7

Consistent Growth in Reserves and Production

0

100

200

300

400

500

600

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 Q1 2005PF

Production (MMcfe/d)

0

200

400

600

800

1000

1200

1400

1600

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2004 PF

Proved Reserves (Bcfe)

8

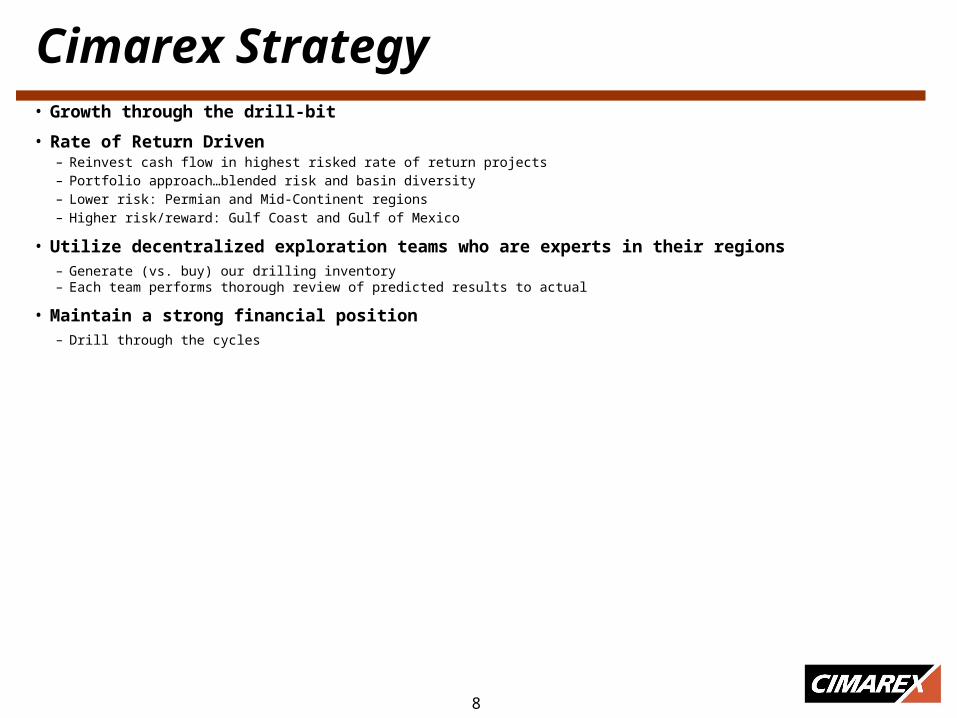

Cimarex Strategy• Growth through the drill-bit

• Rate of Return Driven– Reinvest cash flow in highest risked rate of return projects– Portfolio approach…blended risk and basin diversity– Lower risk: Permian and Mid-Continent regions– Higher risk/reward: Gulf Coast and Gulf of Mexico

• Utilize decentralized exploration teams who are experts in their regions– Generate (vs. buy) our drilling inventory– Each team performs thorough review of predicted results to actual

• Maintain a strong financial position– Drill through the cycles

9

Exploration Principles

• Blended / moderate-risk

exploration program

• Internally generated drilling

ideas

• Multi-basin, lower-48 focus

• Regional effort built upon

local expertise

• Integration between

geology, land &

engineering

• Monitor results and provide

continuous feedback

0

10

20

30

40

50

60

70

80

90

2002 2003 2004

Growing the Exploration Team

Geoscientists Land/Support Total

Operations Overview

11

Mid-Continent Basins

YE 2004 PF Reserves (Bcfe) 555

Q1 2005 PF production (MMcfe/d) 172

2005 Capital ($ MM) $185

Anadarko Basin

Mountain Front

Panhandles/Shelf

Hugoton

TTM Pro Forma Production

100

110

120

130

140

150

160

170

180

190

May-04Jul-0

4

Sep-04

Nov-04

Jan-05

Mar-05

Mm

cfe

per

day

Mid-Continent

Arkoma

12

Panhandle Area – Roberts & Hemphill Counties

Hemphill/Roberts Counties Granite Wash – Lower Morrow

– Depth: 11,000-13,000’

– CWC $2.0MM

– Expected Reserves: 1.0-3.0 BCF

2005 moving to 4 Rig Program

• Through 5-05 11 wells drilled; 45 wells planned for 2005

• MHR acquisition added 60 sections to Cimarex’s acreage position

13

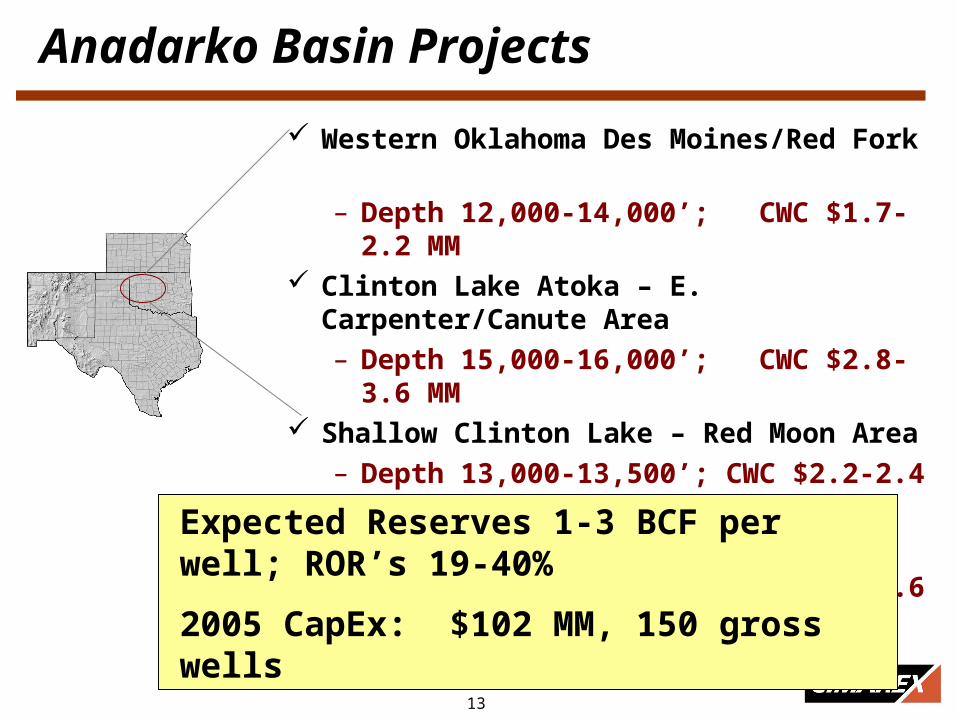

Anadarko Basin Projects

Western Oklahoma Des Moines/Red Fork – Depth 12,000-14,000’; CWC $1.7-2.2 MM

Clinton Lake Atoka – E. Carpenter/Canute Area– Depth 15,000-16,000’; CWC $2.8-3.6 MM

Shallow Clinton Lake – Red Moon Area– Depth 13,000-13,500’; CWC $2.2-2.4 MM

Middle Atoka – Washita River Area– Depth 13,800-14,200’; CWC $2.4-2.6 MM

Expected Reserves 1-3 BCF per well; ROR’s 19-40%

2005 CapEx: $102 MM, 150 gross wells

14

Permian Basin

Permian

YE 2004 PF Reserves (Bcfe) 655

Q1 2005 PF production (MMcfe/d) 132

2005 Capital ($ MM) $95

TTM Pro Forma Production

25

45

65

85

105

125

145

May-04Jul-0

4

Sep-04

Nov-04

Jan-05

Mar-05

Mm

cfe

per

day

Permian

SE New Mexico

West Texas

15

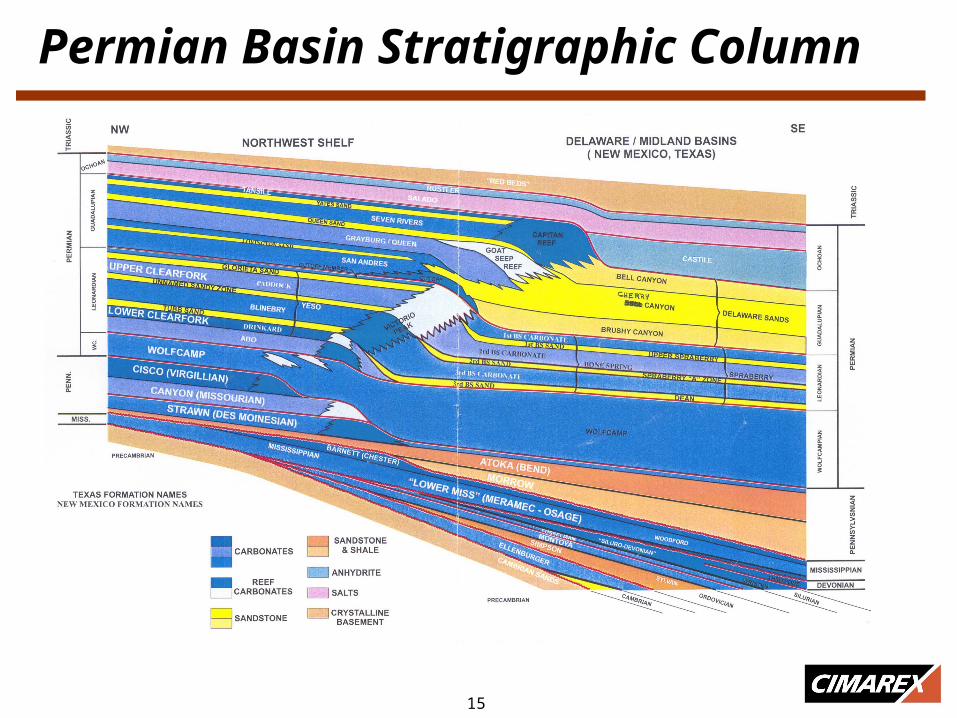

Permian Basin Stratigraphic Column

16

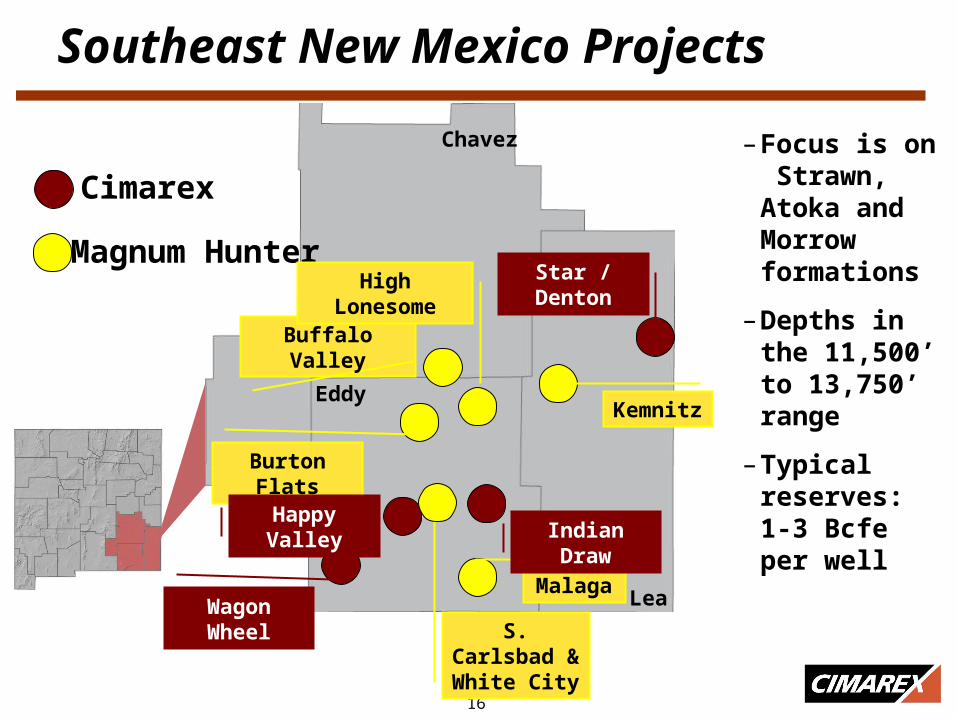

Southeast New Mexico Projects

Cimarex

Magnum Hunter

Chavez

Lea

Eddy

Buffalo Valley

Burton Flats

Wagon Wheel

Star / Denton

S. Carlsbad & White City

High Lonesome

Malaga

Happy ValleyIndian Draw

– Focus is on Strawn, Atoka and Morrow formations

– Depths in the 11,500’ to 13,750’ range

– Typical reserves: 1-3 Bcfe per well

Kemnitz

17

West Texas Projects

Suntura FieldTerry Co.

Will O FieldVal Verde Co.

White & Baker/Nut Ranch/Yucca Butte

areasPecos Co.

Arbol de Nada / Mash / Goldsmith

FieldsWinkler/Ector Co.

– Focus is on Ellenberger, Wolfcamp, and Devonian formations

– Depths range from 2,500’ to 14,000’

– Utilize vertical and horizontal drilling

– Typical per well reserve: 0.2-5 Bcf or 50-500 MBO

18

Gulf of Mexico

YE 2004 PF Reserves (Bcfe) 83

Q1 2005 PF production (MMcfe/d) 66

2005 Capital ($ MM) $150

TTM Pro Forma Production

Gulf of Mexico

-

10

20

30

40

50

60

70

80

90

May-04

Jun-04

Jul-04

Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

Jan-05

Feb-05

Mar-05

Apr-05

Mm

cfe

pe

r d

ay

ShallowWater Gulf of

Mexico

• 260 total blocks

• 55 with proved reserves

• WI range from 12.5-100%

19

Gulf Coast Projects

YE 2004 PF Reserves (Bcfe) 129

Q1 2005 PF production (MMcfe/d) 102

2005 Capital ($ MM) $165

TTM Pro Forma Production

Gulf Coast

25

35

45

55

65

75

85

95

105

115

May-04

Jun-04

Jul-04

Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

Jan-05

Feb-05

Mar-05

Apr-05

Mm

cfe

pe

r d

ay

Mississippi Salt Dome Trend

W. Gueydan Field

Hackberry Trend

Camerina/Miogyp Planulina

Miocene Trends

Yegua/Cook Mtn.

South TexasVicksburg/Frio

20

Yegua/Cook Mountain – Liberty County

• 670 sq mi of 3D seismic data

• Reprocessed 3D into one dataset, leading to expanded 2005 inventory

• 2004:

– 14 gross wells / 6.4 net

– 10 of 14 successful

– $25MM of capital

• Aggressive 2005 program

– 19 wells; $36MM

– Mix of exploration and development

Harris

Liberty

Hardin

Jefferson

Chambers

Harris

RaywoodTrinity

Gas Well/Discovery

New Location

Dry Hole

21

Mississippi Multi-Dome 3-D Reprocessing

• Covington and Jones counties

• A “new look” with curved-ray pre-stack time migration

• Recent wells on Centerville and Dont Domes; Hosston interval

• Ellzy 2 producing 300 Bopd

• Speed 2 tested 350 Bopd

• Eight more wells planned for 2005

• Two wells currently drilling

Dont Dome

Centerville Dome

Kola Dome

Eminence Dome

Moselle Dome

22

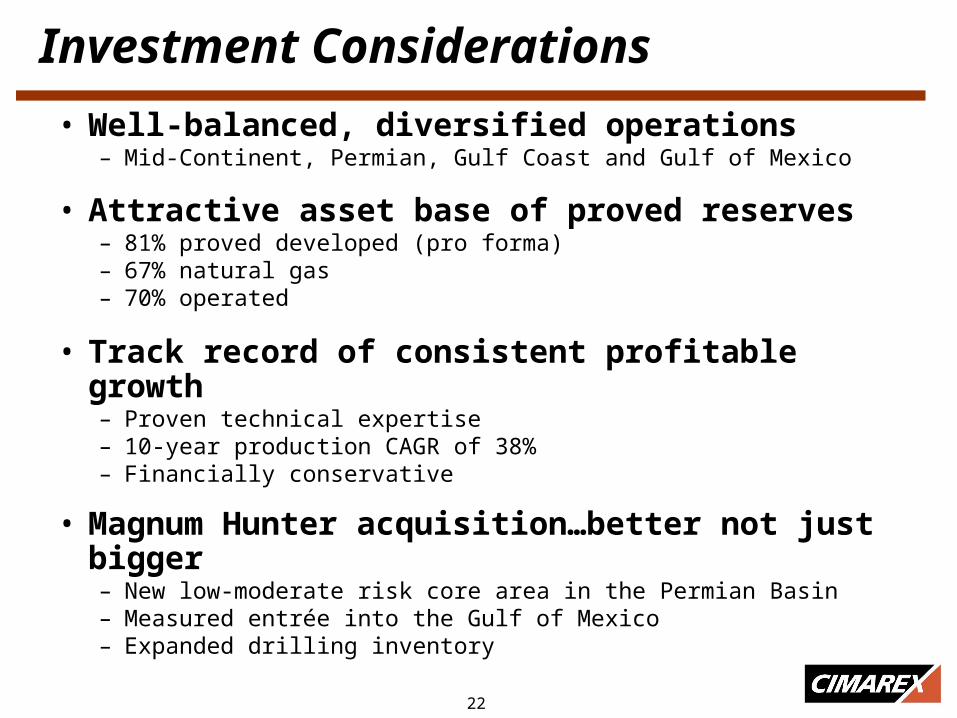

Investment Considerations

• Well-balanced, diversified operations– Mid-Continent, Permian, Gulf Coast and Gulf of Mexico

• Attractive asset base of proved reserves– 81% proved developed (pro forma)– 67% natural gas – 70% operated

• Track record of consistent profitable growth– Proven technical expertise– 10-year production CAGR of 38%– Financially conservative

• Magnum Hunter acquisition…better not just bigger– New low-moderate risk core area in the Permian Basin– Measured entrée into the Gulf of Mexico– Expanded drilling inventory

23

Contact Information

Paul Korus

Vice President and CFO

Mark Burford

Director of Capital Markets

Cimarex Energy Co.

1700 Lincoln Street, Suite 1800

Denver, CO 80203Phone (303) 295-3995

Fax (303) 285-9299

www.cimarex.com

IPAA Oil & Gas Investment SymposiumLondon

July 7, 2005