Embed Size (px)

Citation preview

IPSAS Outlook

A message from Thomas Müller-Marqués BergerWelcome to this month’s edition of IPSAS Outlook, which brings you insights into recent IPSAS developments and emerging issues. In this issue of IPSAS Outlook, the focus is on the state of IPSAS adoption and implementation in Africa. We are very privileged to have Mr Nongo, Ms Poggiolini and Mrs Peloetletse share their views and insights with our readers. I would like to thank them and our colleagues in Africa for their contribution to IPSAS Outlook, making this a truly global publication.We welcome your feedback on IPSAS Outlook. Please contact us at [email protected].

Thomas Müller-Marqués Berger, IPSAS Global Leader

In this issue ...Spotlight on Nigeria’s IPSAS implementation

The role of ESAAG in promoting IPSAS adoption in east and southern Africa

Consultation on the IPSASB’s governance and oversight

IPSASB issues ED 54 and policy paperLook here for the summaries of ED 54 Reporting Service Performance Informationpolicy paper Process for Considering GFS Reporting Guidelines during Development of IPSASs

IPSASB project update

Resources

Spotlight on Nigeria’s IPSAS implementation

2

The South African experience and IPSASB’s ED on

IPSAS

4

The role of ESAAG in promoting IPSAS adoption in east and southern Africa

6

Consultation on the IPSASB’s governance and oversight

8

IPSASB issues ED 54 and policy paper

10

IPSASB project update

12

Resources 15

IPSAS issues for public

executives

ey.com/IPSAS

February/March 2014

Spotlight on Nigeria’s IPSAS implementation

A major feature of the IPSAS implementation process in Nigeria is that it has been phased over two stages – implementation of

were the reasons for this decision?

The implementation of accrual-based IPSAS is a major undertaking and some countries in advanced economies have estimated that it would take them more than 10 years to implement.1 From the time of the announcement of the implementation roadmap2 to the implementation itself, the time frame allowed for Nigerian public sector entities to implement

ambitious. What drove the government to make such a decision?

See Public consultation - Assessment of the suitability of the International Public Sector Accounting Standards for the Member States – Summary of Responses

See FG sets December Deadline for IPSAS Adoption

From your perspective as secretary, what is the subcommittee’s role in the reform process, and what strategy has the FAAC adopted regarding the nationwide implementation of IPSAS, given the wide scope of the reforms?

Freedom of Information Act 2011

James Y. Nongo

currently deputy director of

Roadmap for the Adoption of IPSAS

based IPSASs across its three tiers of government (federal, state and local) by January 2016. Mr James Nongo, deputy director of the OAG and secretary of the FAAC’s subcommittee on IPSAS, is leading this major undertaking on behalf of all tiers of the government. In this interview, he talks about the milestones achieved in this journey and the challenges that lie ahead.

2 | IPSAS Outlook February - March 2014

James, could you describe some of the major steps taken for the implementation so far?

federal ministers and permanent secretaries, all of the state

National Chart of Accounts

Users’ Manual of the NCOA

statistical reports, performance reports and accounting policies

The Adoption of IPSAS in Nigeria: What You Need to Know

Given that the budgetary process does not necessarily need to be affected by the implementation of IPSAS, is the budgetary process in Nigeria expected to be affected by the implementation of IPSAS?

4

What are some of the challenges that you have encountered and expect to encounter with the implementation of IPSAS across the tiers of government?

How has the overall experience of of IPSAS implementation in Nigeria been so far?

4

Country: Nigeria Government: Federal, 36 states, 1 capital territory, 774 local government areasGDP: USD 478.5 billion (2013 estimate)Population: 174.5 million (2013 estimate) Source: The World Factbook

3 | IPSAS Outlook February - March 2014

, and using the transitional

The First-Time Adoption of Accrual Basis IPSASs

The initial measurement of these assets for purposes of

collating the information necessary for the opening statement of

transfer them to local communities for housing, or sell them in the

The ED also permits entities to determine a deemed cost for an

The South African experience and

of IPSAS

Jeanine Poggiolini is

technical director at the

either the ASB or IPSASB.

4 | IPSAS Outlook February - March 2014

There is a potential risk that identifying the exemptions that affect

proposed an exemption from segment disclosures during the

categories of exemptions using less neutral language, such as

Country: South AfricaGovernment: National, 9 provinces and 278 municipalities (8 metropolitan, 44 district and 226 local municipalities)GDP: USD 595.7 billion (2013 estimate)Population: 48.6 million (2013 estimate)Source: The World Factbook

5 | IPSAS Outlook February - March 2014

Could you tell us about ESAAG as an organization – what are its main objectives, who does it represent, and who are its stakeholders?

�

Regional and international representation and promoting

stakeholders

countries?

�

�practices

�

��

ESAAG has come out strongly in support of IPSAS adoption in member countries. Why is ESAAG an advocate for IPSAS in

countries and the region as a whole?

The role of ESAAG in promoting IPSAS adoption in east and southern Africa

Emma Peloetletse is the accountant general

of the East and

6 | IPSAS Outlook February - March 2014

Botswana Kenya Lesotho Malawi Mauritius Mozambique Namibia

Rwanda South Africa Swaziland Tanzania Uganda Zambia Zimbabwe

system of internal control to support the additional reporting

What challenges do you anticipate with the adoption of IPSAS and, in a broader sense, PFM reform in the region?

What is the role of ESAAG in the PFM reforms of its member countries? In what areas does/can ESAAG support member countries?

synergies

��

�

�

��

ESAAG member countries

7 | IPSAS Outlook February - March 2014

Background to the consultation

Objectives of the Review Group

The Review Group’s proposal

information, including organizations representing the interests

information, including organizations representing the interests

regulators

Consultation on IPSASB’s governance and oversightIn January 2014, the IPSASB Governance Review Group (the Review Group) issued its consultation paper The Future Governance of the International Public Sector Accounting Standards Board. Given the growing

8 | IPSAS Outlook February - March 2014

Next steps

9 | IPSAS Outlook February - March 2014

ED 54 Reporting Service Performance InformationBackground

Conceptual Framework

an entity performs, the nature of an entity and the regulatory

Status and scope of the recommended practice guidelines (RPG)

preclude the presentation of additional information, if such

IPSASB issues ED 54 and policy paper

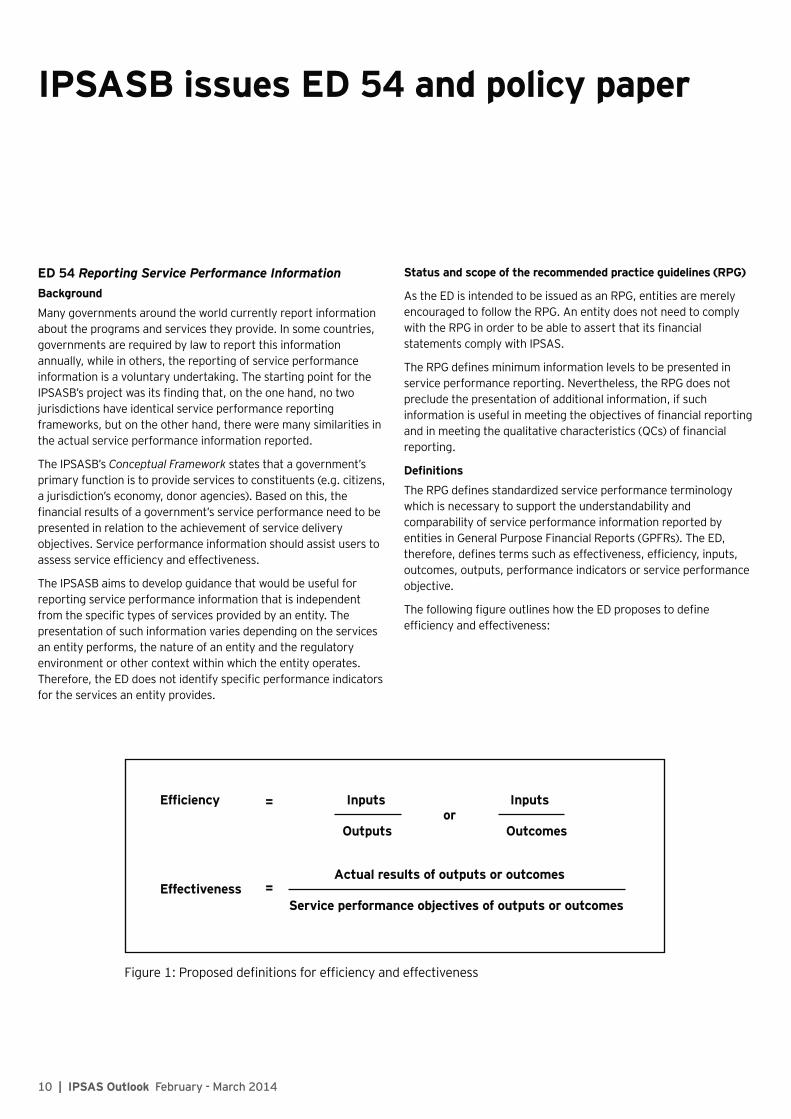

Inputs Inputs

Actual results of outputs or outcomes

Outputs Outcomes

Service performance objectives of outputs or outcomesEffectiveness

=or

=

10 | IPSAS Outlook February - March 2014

Reporting boundary

Reporting cycle and reporting period

Principles for reporting service performance information

Presentation of service performance information

�

�

�

�

�

IPSASB releases policy paper on dealing with GFS differences in standard setting

Process for Considering Relevance of Government Finance Statistics (GFS) Reporting Guidelines During Development of IPSASs

Next steps

11 | IPSAS Outlook February - March 2014

IPSASB project update

What’s new?

The following table shows new publications issued by the IPSASB and public consultations published for comment:

Projects Publication

Reporting service perfomance information

Reporting Service Performance InformationOutlook

Policy paper on Process for Considering GFS Reporting Guidelines during Development of IPSASs

Process for Considering GFS Reporting Guidelines during Development of IPSASs

Outlook

IPSASB Meeting December 2013 – current discussions

Projects Publication

Conceptual FrameworkA Review of the Conceptual Framework for Financial Reporting

���

�

Phase 2 – Elements and Recognition

��

12 | IPSAS Outlook February - March 2014

Projects Publication

�

�

Phase 3 – Measurement��

�

�

�

Phase 4 – Presentation in General Purpose Financial ReportsPresentation in General Purpose Financial Reports

��

�

Government business enterprises Government Business Enterprises

��

13 | IPSAS Outlook February - March 2014

Projects Publication

Emissions Trading Schemes

on ETS in the Government Finance Statistics Manual

instrumentsFinancial Instruments:

Presentation

�����

Financial Instruments: Recognition and Measurement Financial Instruments: Disclosures

Strategy

IPSASB project update

14 | IPSAS Outlook February - March 2014

Resources

Model Public Sector Group

IPSAS Explained

second edition of our practical guide

A snapshot of GAAP differences between IPSAS and IFRS

It further explains the sources and

Toward transparency

IPSAS Poster

15 | IPSAS Outlook February - March 2014

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s International Public Sector Accounting Standards GroupThe move to International Public Sector Accounting Standards (IPSAS) is an important initiative in public sector accounting, the impact of which stretches far beyond accounting to affect every key decision you make, not just how you report it. We have developed the global resources — people and knowledge — to support our client teams. And we work to give you the benefit of our broad sector experience, our deep subject matter knowledge and the latest insights from our work worldwide. It’s how Ernst & Young makes a difference.

© 2014 EYGM Limited. All Rights Reserved.

SCORE No. AU2225

ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com