Embed Size (px)

Citation preview

January 2015

IR Presentation May 2015

CONTENTS

Ⅱ. New order & Backlog

Ⅲ. Products & Market Situation

Ⅰ. Financial Highlights

CONTENTS

Ⅱ. New order & Backlog

Ⅲ. Products & Market Situation

Ⅰ. Financial Highlights

Revenue & Operating Profit

Quarterly Results (recent 4Q)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

-

5.0

10.0

15.0

20.0

2010 2011 2012 2013 2014

Offshore Shipbuilding E&I OP margin

Revenue & OP Margin Trend

13.1 13.4

14.5 14.8

12.9

10.8

8.7

8.3

6.2

(KRWt) (%) 2014 2015

2Q 3Q 4Q 1Q

Revenue 3,107 3,263 3,078 2,610

Operating Profit 262 182 101 26

OP Margin 8.4% 5.6% 3.3% 1.0%

Income Before Tax 263 175 46 33

Net Profit 206 172 41 11

Revenue decline in 1Q15 :

- Lower sales contribution of drillships and less working days

Lower operating margin in 1Q15 :

- Sales mix change

· More revenue of low margin P/J (Ichthys&Egina), and less revenue of high margin drillships

- One off extra cost for Egina P/J occurred

(KRWb)

1.4

- 3 -

Financial Summary

Consolidated Statements of Income

2010 2011 2012 2013 2014 2015 1Q

Revenue 13,146 13,391 14,490 14,835 12,879 2,610 2,610

Operating Profit 1,432 1,160 1,206 914 183 26 26

OP Margin 10.8% 8.7% 8.3% 6.2% 1.4% 1.0% 1.0%

Income Before Tax 1,298 1,150 1,045 819 190 33 33

Net Profit 1,000 851 796 632 106 11 11

(KRWb)

- 4 -

Financial Summary

Consolidated Statements of Financial Position

2010 2011 2012 2013 2014

Total Assets 18,850 16,414 16,635 17,427 17,122

Cash & Cash Equiv. 1,255 1,289 1,164 1,140 893

Inventories 607 540 699 842 1,169

Accounts Receivable 5,449 4,078 5,091 5,935 6,400

Advanced Payments 1,638 1,675 1,501 1,354 1,204

Hedge Related 3,370 2,592 2,064 2,035 1,113

Total Liabilities 14,718 11,770 11,352 11,581 11,549

Advanced Receipts 5,431 5,602 3,967 3,885 3,799

Interest Bearing Debt 2,838 1,784 3,193 2,937 3,827

Hedge Related 3,578 2,452 1,458 1,725 1,093

Total Equity 4,132 4,644 5,283 5,846 5,573

Paid in Capital 1,155 1,155 1,155 1,155 1,155

Treasury Stock △662 △659 △657 △656 △970

(KRWb)

- 5 -

Risk Hedging Policy

SHI Focuses on minimizing profit volatility

Building Event

Time Gap (months) 12 5 3 10

Currency

Receivable

Payable

Raw Material

Main Engine

Machinery

Steel Plate

Bulk Part

Contract Steel Cutting Keel Laying Launching Delivery

: Hedging, Order : Execution, Delivery

Foreign currency exposure is fully covered through forward transaction at the stage of shipbuilding contract

Main engine and machinery are ordered within 1~2 months after contract signing

- 6 -

CONTENTS

Ⅲ. Products & Market Situation

Ⅰ. Financial Highlights

Ⅱ. New order & Backlog

New Order

Apr 2015

Trend

-

2

4

6

8

10

12

14

16

2011 2012 2013 2014 2015.Apr

Container Ship LNG Carrier

Tanker Drilling Rig

Production Facility Others(WTIV etc.)

2.5

14.9

9.6

13.3

7.3

(USDb)

- 8 -

Container

-ship

64%

LNG

Carrier

17%

Tanker

19%

Unit USDb

Containership 10 1.6

LNG Carrier 2 0.4

Tanker 8 0.5

Total 20 2.5

$2.5 billion (20 Units)

Order Backlog

Apr 2015

Trend

0

5

10

15

20

25

30

35

40

45

2011 2012 2013 2014 2015.Apr

Shipbuilding Offshore

38.3 37.2 37.5

32.6

Container

Ship 13%

LNG Carrier

16%

Tanker 6%

Drilling Rig

23%

Production

Facility 39%

Others 3%

(USDb)

- 9 -

Unit USDb

Containership 32 4.1

LNG Carrier 25 5.3

Tanker 22 1.7

Drilling Rig 13 7.8

Production 9 12.7

Others 7 1.0

Total 108 32.6

$32.6 billion (108 Units)

34.8

CONTENTS

Ⅱ. New order & Backlog

Ⅰ. Financial Highlights

Ⅲ. Products & Market Situation

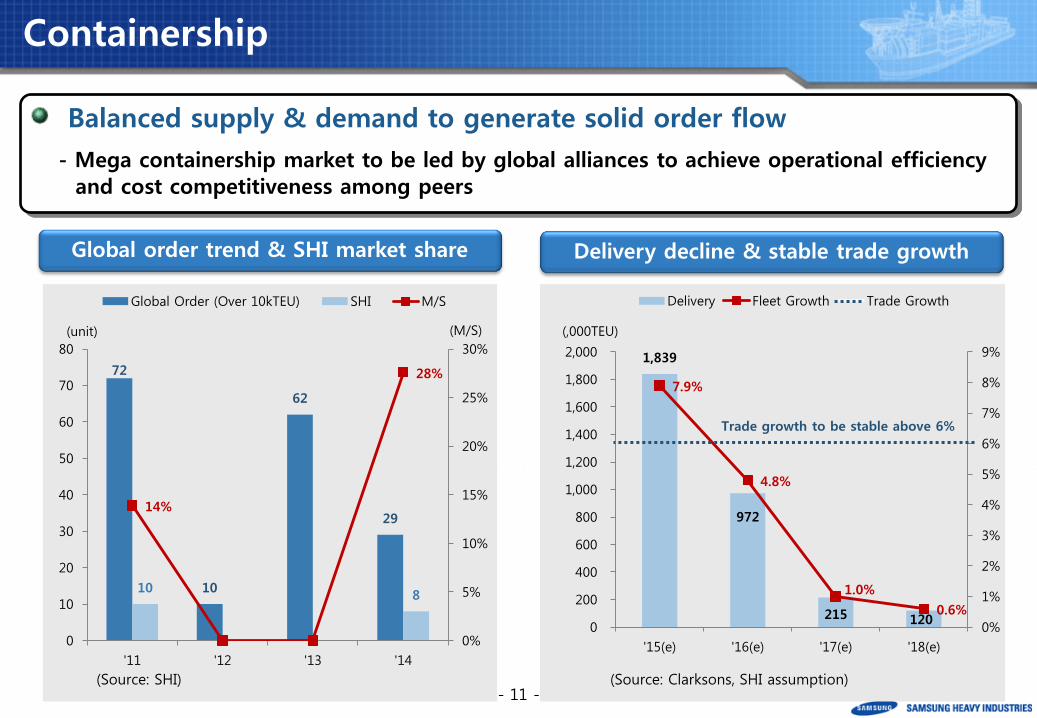

Balanced supply & demand to generate solid order flow

- Mega containership market to be led by global alliances to achieve operational efficiency

and cost competitiveness among peers

Containership

Delivery decline & stable trade growth Global order trend & SHI market share

(Source: Clarksons, SHI assumption)

72

10

62

29

10 8

14%

28%

0%

5%

10%

15%

20%

25%

30%

0

10

20

30

40

50

60

70

80

'11 '12 '13 '14

Global Order (Over 10kTEU) SHI M/S

(Source: SHI)

1,839

972

215 120

7.9%

4.8%

1.0%

0.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

'15(e) '16(e) '17(e) '18(e)

Delivery Fleet Growth Trade Growth

Trade growth to be stable above 6%

(unit) (,000TEU)

- 11 -

(M/S)

Short term demand to remain healthy due to shale gas export projects

in North America

LNG Carrier

US LNG export projects in progress

= approximately 120 vessels needed

Global order trend & SHI market share

48

32

39

59

18

4

14

5

38%

13%

36%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

10

20

30

40

50

60

70

'11 '12 '13 '14

Global Order SHI M/S

(Source: SHI)

P/J Export

Capacity (mtpa)

First LNG

Status

Sabine Pass 27.0 ’15~

Under construction

Free Port 13.2 ‘17~

Cove Point 5.8 ’17~

Cameron 12.0 ‘18~

Corpus Christi 13.5 ‘18~ Under

Development Lake Charles 15.0 ‘17~

Total 86.5

(Source: company data, SHI assumption)

(unit)

* transportation capacity / vessel ≒ 0.7mtpa

- 12 -

* around 30 vessels already ordered as of year 2014

(M/S)

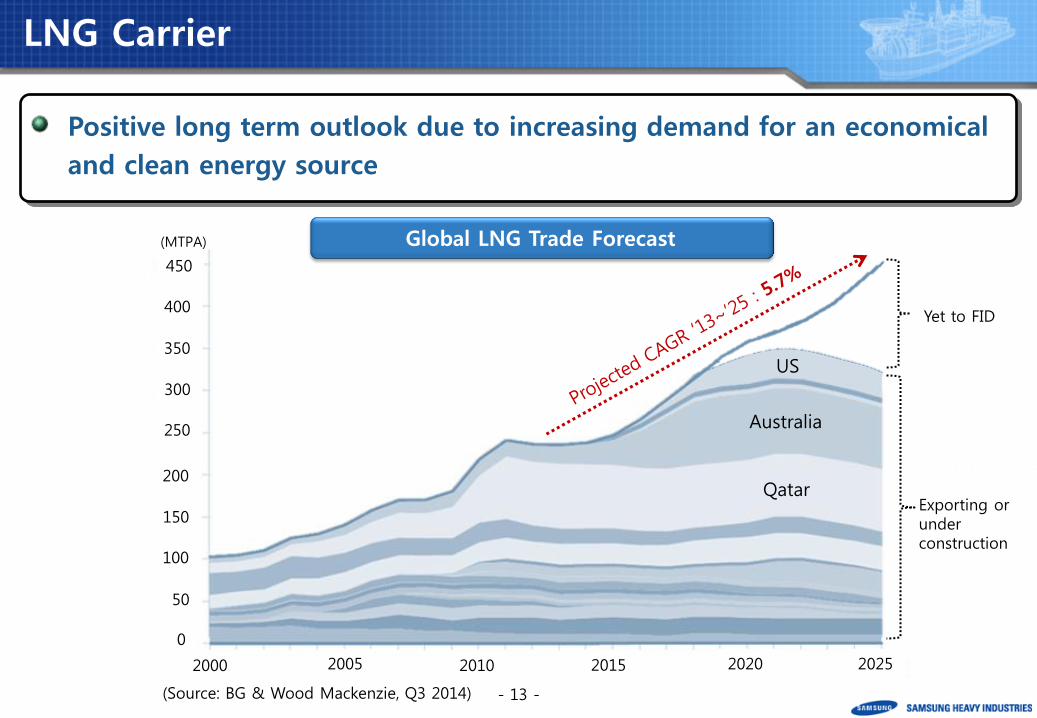

US

Australia

Qatar

Yet to FID

2000 2005 2010 2015 2020 2025

0

50

100

150

200

100 250

300

350

400

450

500

Exporting or under construction

- 13 - (Source: BG & Wood Mackenzie, Q3 2014)

LNG Carrier

Positive long term outlook due to increasing demand for an economical

and clean energy source

Global LNG Trade Forecast (MTPA)

Downturn to be continued for a while due to shrinking investment in

exploration but demand for high specification drillship is expected

Drillship

Next generation: 20K BOP drillship

New demand for 20K BOP drillship is expected

- For safe and efficient operation in high-pressure

and high-temperature deepwater reservoirs

Global order trend & SHI market share

(Source: SHI)

25

19

12

4

10 9

5

2

40%

47%

42%

50%

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

30

'11 '12 '13 '14

Global Order SHI M/S

(unit)

- 14 -

(M/S)

• BP-Maersk “Project 20K”

Jointly developing next generation drillship

using 20K BOP for Gulf of Mexico since

year 2013

Seeking both growth and profitability in offshore EPC market through

enhancement of EPC execution capability with ongoing projects

Production Facility

What we do for strengthening competitiveness Key projects under construction

- 15 -

Ichthys CPF(Gas), Austrailia

Egina Oil FPSO, Nigeria

Lessons Learned Program

- Accumulating and systemizing knowledge learned from current projects to execute following better

Reinforcement of engineering capacity

- New R&D center established only for FEED, FEED verification, detailed design etc.

- Recruiting experienced engineers and project managers

Organizational improvement

- Risk management team and offshore package procurement team established

SHI’s new growth engine

- Market to expand due to its cost advantages and environmental benefits

FLNG

Concept & Advantages

Production, treatment, liquefaction and offloading

of natural gas to be carried out on a vessel

- No need for extensive pipe lines and onshore

processing facilities

Less CAPEX required

Natural Gas

Pretreatment

Liquefaction

World-wide FLNG P/J under Consideration

Number Projects

Under construction

3 Prelude(Shell)

Kanowit, Rotan (Petronas)

Active 10

Browse1,2,3(Shell)

Mozmbique(ENI),

Block R(Ophir) etc.

Potential 38

Total 51

(Source: Clarkson World Offshore Register )

3 Projects will be delivered during year ‘15~’18,

and 10 projects are actively under study

- 16 -

SHI leads the market with solid relationship with strategic partners and

accumulated experience in the field

FLNG

Long term relationship with the leading companies

(Source: SHI, Shell)

Prelude Browse

Region Austrailia Austrailia

LNG Capacity 3.5 12.0

Contract amount 6 USDb under discussion

FID 2011 2016 mid

Delivery 2016 under discussion

First Gas 2018 2021

Remark - Key pre-FEED work Completed,

Entering FEED in mid-2015

2 major projects are underway based on long term agreement with Royal Dutch Shell and Technip

that are leaders of FLNG market

- 17 -

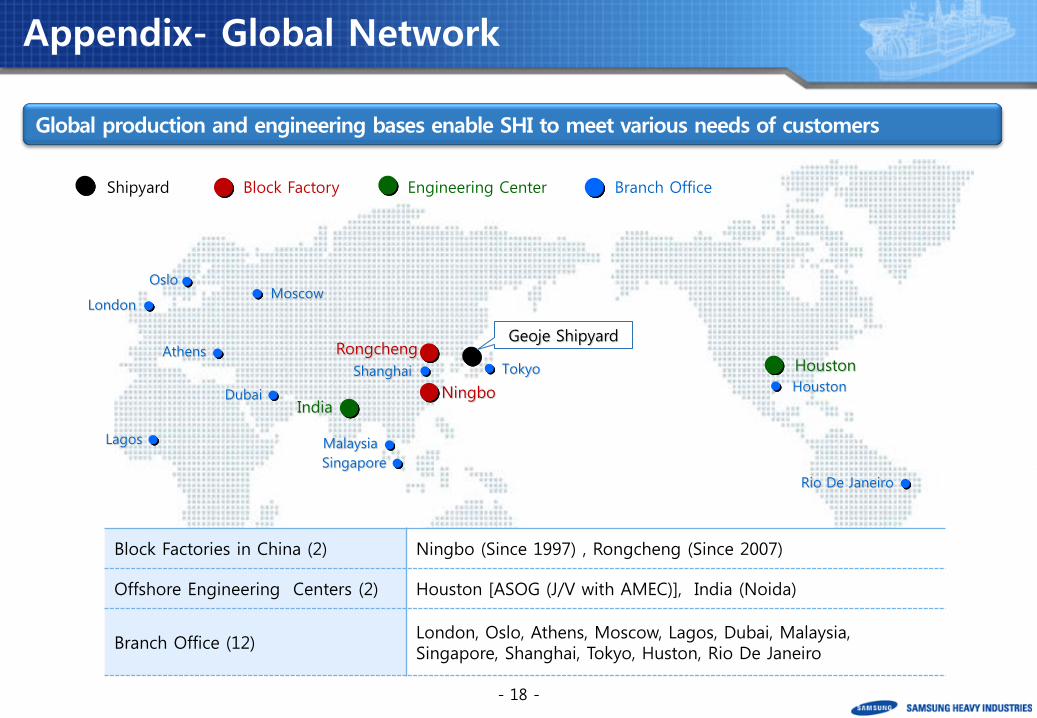

Appendix- Global Network

Oslo

London

Athens Tokyo

Dubai

Rongcheng

Ningbo

Singapore

Houston

Malaysia

Houston

India

Moscow

Rio De Janeiro

Lagos

Shanghai

Shipyard Block Factory Engineering Center Branch Office

Global production and engineering bases enable SHI to meet various needs of customers

Block Factories in China (2) Ningbo (Since 1997) , Rongcheng (Since 2007)

Offshore Engineering Centers (2) Houston [ASOG (J/V with AMEC)], India (Noida)

Branch Office (12) London, Oslo, Athens, Moscow, Lagos, Dubai, Malaysia, Singapore, Shanghai, Tokyo, Huston, Rio De Janeiro

Geoje Shipyard

- 18 -

Appendix- Shipyard View

Site : 4.0million ㎡

Quay Wall Length : 7.9Km (24 vessels)

3 Floating Cranes : 3,000 / 3,600 / 8,000ton

8 Docks (3 Dry Docks & 5 Floating Docks) ▪ No. 1 : 283m × 46m ▪ NO. 2 : 390m × 65m ▪ No. 3 : 640m × 98m ▪ G1 : 270m × 52m ▪ G2 : 400m × 55m ▪ G3 : 400m × 70m ▪ G4 : 420m × 70m ▪ G5 : 158m × 150m (only for Offshore)

SHI Focuses on minimizing profit volatility

Offshore Facilities

Dry Dock No.2

Floating Dock 3

Dry Dock No.3

Floating Dock 2

Floating Dock 4

Main Building

Dry Dock No. 1

ShinHanne Factory

Floating Dock 1

Floating Dock 5

- 19 -

Disclaimer

This presentation has been prepared by Samsung Heavy Industries Co., Ltd. and contains forward-looking

statements that are subject to risks, uncertainties, and assumptions.

The presentation is solely for your information, subject to change without notice, and makes no

representation or warranty, expressed or implied and no reliability should be placed on the accuracy,

fairness, or completeness of the information presented herein.

The Company, its affiliates, or representatives accept no liability for any losses arising from any information

contained in the presentation.

The contents of this presentation may not be reproduced, redistributed or circulated, directly or Indirectly,

to any other person or organization, or published, in whole or in part, for any purpose.

- 20 -