Embed Size (px)

Citation preview

Page 1 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA Steel Re-Rolling Mills’ Association of India www.srma.co.in

IRON AND STEEL

Page 2 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA Steel Re Rolling Mills Association of India www.srma.co.in

Executive Summary

Growth of Re-bar Industry in India

The Industrial Activity of Steel re-rolling mills.

Steel Market 2012 and 2013

Current Global Scenario and the Steel Industry

Enhance custom duty on steel long products - Budget 2013-14

Strategic Plan for next five years - Ministry of Steel

Environment And Safety

Labour Laws & Legal news

Events & News

CONTENTS

IRON AND STEEL SRMA

Steel Re Rolling Mills

Association of India

www.sram.co.in

Page 3 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

The Indian iron and steel industry is almost a century old, it was the first core sector to be completely freed from

the licensing regime (in 1990-91) and the pricing and distribution controls. The steel industry is expanding

worldwide. The economic modernization processes in these countries are driving the sharp rise in demand for

steel. The New Industrial policy adopted by the Government of India has opened up the iron and steel sector for

private investment by removing it from the list of industries reserved for public sector and exempting it from

compulsory licensing. Imports of foreign technology as well as foreign direct investment are freely permitted up

to certain limits under an automatic route.

This, along with the other initiatives taken by the Government has given a definite impetus for entry,

participation, and growth of the private sector in the steel industry. While the existing units are being

modernized/expanded, a large number of new/green field steel plants have also come up in different parts of the

country based on modern, cost effective, state of-the-art technologies. Soaring demand by sectors like

infrastructure, real estate, and automobiles, at home and abroad, has put India's steel industry on the world map.

The demand for steel in India is expected to rise 7 percent in the next financial year beginning April 1 as

compared to the sluggish 5.5 percent projected growth in 2012-13. The overall outlook for the steel sector is

positive and the demand was likely to pick up in the next financial year on the back of revival in economic

growth and the government's measures to ease infrastructure investment rules. In fiscal 2012-13, growth in

domestic steel demand is expected to be around 5.5 percent. Total demand is expected to be around 75 million

tonnes, up from 71 million tonnes in 2011-12. In 2013-14, demand is expected to be higher at around seven

percent.

India is currently the world's fourth largest producer of crude steel after China, Japan and the US. The steel

production is expected to reach 200 million tonnes by 2020 as compared to 71 million tonnes recorded last year .

In steel production, India is expected to leave behind USA and Japan in a couple of years. However, it will

substantially lag behind China that produces almost 700 million tonnes of steel per year.

As per the report of the Working Group on Steel for the 12th

Plan, there exist many factors which carry the

potential of raising the per capita steel consumption in the country, currently estimated at 55 kg (provisional).

These include among others, an estimated infrastructure investment of nearly a trillion dollars, a projected growth

of manufacturing from current 8% to 11-12%, increase in urban population to 600 million by 2030 from the

current level of 400 million, emergence of the rural market for steel currently consuming around 10 kg per annum

buoyed by projects like Bharat Nirman, Pradhan Mantri Gram Sadak Yojana, Rajiv Gandhi Awaas Yojana among

others.

At the time of its release, the National Steel Policy 2005 had envisaged steel production to reach 110 million

tonnes by 2019-20. However, based on the assessment of the current ongoing projects, both in greenfield and

brownfield, the Working Group on Steel for the 12th

Plan has projected that the crude steel capacity in the county

is likely to be 140 MT by 2016-17.

IRON AND STEEL SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

Page 4 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Re-bars were a major steel products in evident steel consumption among finished steel products in 2011-12 when

its share in India's total finished steel consumption reached about 28 percent. In India, re-bars are produced by

both the primary and secondary producers. The dominance of CTD Bars in India since the early 70's of the last

century was mainly due to the fact that most civil engineers at that time did not bother to check the vital

parameters like yield strength, Ultimate Tensile Strength (UTS), elongation etc. while using CTD bars in RCC.

The industrially developed countries had stopped the use of such CTD Bars by the start of 1970's. Then came the

era of Thermo-Mechanically Tested (TMT) Bars, which are even now being used by some civil engineers as they

believe that these bars are of the specified grade Fe-415 as per 1786/1985 and are for superior to the CTD bars

which were being used earlier. However, these so-called TMT Bars available in the market were being used

earlier. However, these so-called TMT Bars available in the market were often found on testing to have yield

strength of 350-390 N/mm2 only.

Reinforcement Steel Bars (Rebar) are long steel products that find application in the construction industry. The

usage of Reinforced Cement Concrete (RCC) has become the default standards for construction of residential and

commercial structures, flyovers, bridges, water retaining structures, industrial and power plants, etc. Rebar

constitute about 15-25 percent of the total materials cost for civil construction.

The Rebar industry has been a main steel product among the Finished Steel product categories. In 2009, the rebar

accounted for about 35 percent of the total steel production in the country. The construction and infrastructure

boom in the country in the past decade contributed to the rapid growth in the industry.

The rebar industry is characterized by both primary and secondary players operating in the market. Integrated

Steel Producers (ISPs) like SAIL, Tata Steel, JSW, that produce from the pure iron ore account for about 30

percent of the total rebar market. The remaining 70 percent is catered by about 300-400 producers. Some of the

leading secondary producers include Tulsyan, SRMB, Sujana etc. Medium and small players have regional

presence catering to the demand in a particular region.

Increased competition in the Rebar industry has resulted in the market becoming commoditized. Industry players

in the last 5 years have focused more on marketing and branding of the product. Tata Steel is the pioneer in this

aspect as the company has successfully branded its products, thereby sustaining its leadership. In 2009-10, Tata

Steel was also accorded the first “Super Brand” for this segment. Tata steel achieved a production of 1.56 million

tons of TMT rebar becoming the largest TMT rebar manufacturer.

IRON AND STEEL SRMA

Steel Re Rolling Mills

Association of India www.sram.co.in

Page 5 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Steel re-rolling is one of the most important sectors of the steel industry, as it constitutes an unavoidable link in

the total supply chain of iron and steel. The secondary steel production constitutes approximately 57% of the total

steel production in India. It mainly takes place in steel re-rolling mills (SRRM) that usually are family-run small

and medium enterprises (SMEs) with 75% of units in the small scale. The SRRM sector is comprised of about

1,800 (working) re-rolling mills.

This sector is self-sufficient in producing various common as well as most typical steel sections in their mills.

The TMT bar, the flats, squares, special window sections, thinner size HR strips, thinner gaze HR strips,

hexagons, wire rods, angles, channels, H-Beams, I-Beams, tele-channels etc are some of the products of this

sector.

The share of secondary is expected to grow in the near future, also because the sector has some competitive edge

due to flexibility in production for meeting low-tonnage requirements in various grades, shapes and sizes to serve

niche markets. The estimated domestic demand of the re-rolled products has been estimated at about eight million

tonnes. The industry has catered thousand and thousand tonnes of its products to core projects, dams, State

Electricity Boards and other infrastructure projects in the country. The steel re-rolling industry caters to the needs

of the domestic field up to the tune of 68 per cent of the total requirement. 80 per cent of the total exports of

rounds and bars have been recorded from the secondary steel producers.

Steel production is an energy intensive process and there are more than 1200 small and medium sized (SME)

steel re-rolling mills in India, wherein 75 per cent of units are small scale. The SME steel re-rolling mill sector

constitutes an unavoidable link in the overall supply chain of steel in the country. The direct energy use in this

sector includes heating fuels (furnace oil, natural gas and coal), and electrical energy. The direct energy cost in

the SME mills is estimated at 25-30 per cent of overall production cost

IRON AND STEEL SRMA

Steel Re Rolling Mills

Association of India www.sram.co.in

Page 6 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Slow demand growth and range-bound steel prices are predicted in 2013. Steel prices, which had significantly

weakened in the last few months of 2012, will find support from production cuts and capacity reductions by

global steelmakers and near marginal production cost levels for Chinese steel producers. Excess capacity remains

the most significant issue in the steel sector. Global steelmakers continue to witness supply growth outpacing

demand, with capacity utilization rates remaining stubbornly below 80%. Slowdown in demand growth from

China and subdued steel prices will continue to weigh on the global steel sector in 2013. The global steel market

continues to be oversupplied, and the overproduction versus domestic demand from China is likely to persist as

the country’s steel mills are required to maintain employment and GDP targets. Building and machinery

construction represented the highest demand for steel in China being 57% and 21% respectively.

Subordinate industrial production and reduced investment in large scale infrastructure projects have resulted in a

marked decrease in the growth of steel demand from both the developed and emerging markets. Apparent global

steel usage in 2012 is expected to have grown by only 2.1% (compared to 6.2% growth in 2011), and steel

demand is expected to grow by only 3.2% in 2013. The most affected region is the Euro zone. With the debt crisis

weighing heavily on economic activity, apparent steel use in the EU is expected to have declined by 5.6% in 2012.

It is no doubt that steel demand will significantly improve in 2013, largely because of the continuing economic

crisis in developed countries and the structural shift in the Chinese economy. Moderate recovery is only expected

in 2014–15, although steel demand is likely to improve faster in emerging markets. We expect by 2015 demand

growth to be reaching 3.5%p.a., we showed that success in the new economy will depend on whether steelmakers

can respond to global challenges.

India on line to becoming the next steel powerhouse?

Although China is the dominant market in the steel sector, India is increasing its presence in the global steel

market, as a result of domestic steel consumption. The rising middle class population coupled with increased

urbanization will grow steel intensity in the economy. India has seen a rapid rise in production over the past few

years, becoming the fourth largest producer of crude steel and the largest producer of sponge iron in the world.

There are many opportunities that are helping grow the Indian steel market:

Rural demand picking up

Investment planned in road sector

Indian railway expansion

Automobile and power sectors offer opportunity for specialized steel

Refocus on manufacturing

However, there are also some challenges that India must overcome:

Land acquisition and environment regulations

Shortage of coking coal

Availability and pricing of domestic iron ore

Downstream value addition

Insufficient infrastructure and logistics

Overburdened port facilities

Adoption of modern technology

IRON AND STEEL SRMA

Steel Re Rolling

Mills Association of India

www.sram.co.in

Page 7 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

The steel industry has traditionally been very sensitive to the changing

economic conditions. The recent economic meltdown has created several

challenges – which when addressed appropriately, can be countered to

positive effect. However, unlike the previous global recessions, this time

around, all the countries have come together and taken action. Additionally,

there has been a tremendous amount of governmental response to the global

depression which is helping to bring about a possible easing of the situation.

ECONOMIC RECOVERY - The world economic recession had put an

abrupt end to the steel market upturn that began in 2002. The market had been

turbulent over the last three decades but today, the steel industry is better

prepared thanks to global restructuring and consolidation. The Group of Eight

(G8) industrialised nations have begun preparing for an economic recovery,

acknowledging signs of stabilisation in the economy. Despite short-term uncertainties, the long-term prospect of

the global steel market is strong and growth in steel demand will resume eventually supported by domestic-led

growth in many emerging economies. However, since many expansion projects continue to advance in some

emerging economies, world steel making capacity is expected to maintain an upward trend into 2010 which will

well exceed future demand levels. All this will further make the steel industry more competitive and efficient as

the world economy recovers.

CLIMATE CHANGE - Climate change is one of the most important issues that faces the steel industry in the

21st century. Steel fulfils a unique place in our lives and is essential for sustainable development. It is also key to

infrastructure, energy delivery, transportation, housing, construction and consumer goods. All major steel

producing countries are engaged in the process of substantive reduction in global emissions and learning to cope

with climate change, a phenomenon caused by greenhouse gas emissions that are warming the atmosphere. This

was possible through the adoption of several measures which included, among others, the installation of energy

efficient equipment and processes, improving by-product fuel recovery and usage, and waste heat recovery.

Looking towards the future, the steel industry’s main contribution to the reduction of CO2 emissions should be to

further develop the use of by-products and to work with its customers to help design better, long lasting, more

energy and material efficient products.

HEALTH AND SAFETY - The steel industry prioritises on health and safety. In most countries, the steel

industry has been synonymous with economic growth and prosperity. Steel is used in everything from

railroad tracks to automobiles to orthodontic instruments. However, the production of steel happens to

be one of the most hazardous jobs. A workplace fatality is tragic no matter what the circumstances are.

As an industry, everybody have the opportunity and responsibility to provide the best health and

wellness solutions to the employees.

COMPANY STRATEGY - Despite the current slowdown in consolidation within the global steel industry,

mergers and acquisitions remain a critically important business strategy for most corporate. Steel analysts are

expecting a new wave of consolidation to take place in the next three years. This creates opportunities to gain

market share from competitors who diversify and split their focus. Acquisitions and strategic alliances are also

critical to strengthen, refocus and position companies for increased growth and profitability.

IRON AND STEEL SRMA

Steel Re Rolling Mills

Association of India

www.sram.co.in

Page 8 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Item Existing ( 2012-13) Proposed ( 2013-14)

Excise Duty% Customs

Duty% Excise Duty%

Customs

Duty%

Pig iron 12.0% 5.0% 12.0% 5.0%

Semis 12.0% 5.0% 12.0% 5.0%

Non-alloy steel bars and wire rods 12.0% 5.0% 12.0% 10.0%

Alloy steel bars and wire rods 12.0% 5.0% 12.0% 10.0%

Strcuturals ( Alloy steel ) 12.0% 5.0% 12.0% 10.0%

HR Sheets/plates ( Non Alloy ) 12.0% 7.5% 12.0% 7.5%

HR Coils ( Non Alloy ) 12.0% 7.5% 12.0% 7.5%

CR Coils/ sheets ( Non Alloy) 12.0% 7.5% 12.0% 7.5%

GP/GC Sheets(Non Alloy) 12.0% 7.5% 12.0% 7.5%

HRGO/HRNGO( Non Alloy) 12.0% 7.5% 12.0% 7.5%

HR/CR alloy steel ( flat rolled ) other than

items of Headings No.( 72253090 ,

72254019 , 722550 and 72259900)

12.0% 5.0% 12.0% 5.0%

Flat Rolled Alloy products of heading (

7225 3090 , 72254019 , 722550 and

72259900 )

12.0% 7.5% 12.0% 7.5%

IRON AND STEEL SRMA

Steel Re Rolling Mills

Association of India

www.sram.co.in

Page 9 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Tinplates and TFS seconds 12.0% 10.0% 12.0% 10.0%

Defective CR coils 12.0% 10.0% 12.0% 10.0%

Stainless steel HR coils for coin blanks 12.0% 5.0% 12.0% 5.0%

Melting scrap( iron , steel & stainless steel

) 12.0% 0.0% 12.0% 0.0%

Re-rollable scrap 12.0% 5.0% 12.0% 5.0%

Iron ore 12.0% 2.50% 12.0% 2.50%

Ferro Alloys other than Ferro Nickel 12.0% 5.0% 12.0% 7.5%

Nickel viz Unwrought Nickel, Nickel

Oxide and Ferro Nickel 12.0% 2.5% 12.0% 0.0%

Request for Enhancement of Import Duty on Alloy Steel Long Products from the existing 5% to 10%.

Exempt 4% additional duty of customs on melting scrap of iron and steel imported by manufactures of

steel.

Deemed Duty Credit on Steel Scrap for availing CENVAT Credit

Increase Custom duty on Ferro alloys from 5% to 7.5%

To waive Customs Duty on raw materials i.e., ores and for production of Ferro Alloys.

Abolition of customs duty of Nickel, from 2.5% to NIL for production of steel.

To waive Import Customs Duty on Anthracite Coal.

Page 10 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Iron and steel has for ages provided the key input for building a nation’s physical infrastructure and industrial

base. Today India has emerged as the fifth largest producer of steel and also the single largest sponge iron

producing country in the world.

The Ministry’s vision for such a vibrant sector as already outlined in the National Steel Policy (NSP), is that of

building an industry of global standards with capacity to cater to different as well as diversified demand for all

types of steel and steel based items/ products. Therefore, the proposed strategic plan for the next five years i.e.

2011-16 will also focus on implementation of initiatives for achieving global competitiveness not only in terms of

cost, quality and product-mix but also of matching the global benchmarks of efficiency and productivity.

Vision - The ministry’s vision for the industry is to transform India into a global leader in the steel sector, both as

a steel producer as well as a steel consuming nation and to enhance the industry’s international competitiveness.

Mission - Promoting policies, initiatives and incentives for attaining a national steel production capacity

exceeding 100 million tonnes per annum by the year 2015-16. Streamlining the regulatory environment for

enabling optimal steel production; particularly regarding mineral policy and the mine allocation regime, tariff and

taxation measures, land allocation and environmental and forest clearances. Promoting the development of

infrastructure required for enhancing national steel production through coordinated efforts, particularly in sectors

like Railways, Roads, Ports, Power and Water supply. Enhancing domestic demand for steel through promotional

efforts and by enlarging the retail network of steel companies. Improving the techno-economic efficiency of

operations of steel ministry’s PSUs.

Objectives - To facilitate the early realization of steel investment proposals both in the public and private sector

through coordination and consensus building with state governments and agencies of the union government

particularly through the forum of the Inter Ministerial Group (I.M.G.); for attaining the national objective of total

finished steel production exceeding 100 million tonnes by 2015-16. Ensuring adequate availability of raw

materials for steel industry from domestic and overseas sources, particularly iron ore and coal by PSUs under the

steel ministry. To pursue with the Ministry of Finance and the Ministry of Commerce for the adoption of fiscal

and tariff measures for ensuring the sustainability and future prospects of the Indian steel industry. Promotion of

Steel usage through cost effective steel products, dissemination of knowledge and ensuring higher steel

availability in rural areas. Promotion of Research and Development in steel sector. To improve the commercial

and technical efficiency of operations of all PSUs. To encourage implementation of Quality control standards in

manufacture of steel and steel based products.

Functions - Matters relating to production, distribution, imports and exports of iron and steel and Ferro alloys.

Matters relating to the PSUs including their subsidiaries under the ministry’s administrative control i.e. (i) Steel

Authority of India Ltd (SAIL); (ii) NMDC Limited ; (iii) Rashtriya Ispat Nigam Ltd (RINL); (iv) Manganese

(Ore) India Ltd (MOIL); (v) MSTC Ltd; (vi) Ferro Scrap Nigam Ltd (FSNL); (vii) Hindustan Steelworks

Construction Ltd (HSCL); (viii) MECON Ltd; (ix) KIOCL Ltd; and (x) Bird Group Ltd and also the

company/undertaking set up for foreign acquisition of coal assets i.e. the International Coal Ventures Limited

(ICVL) Planning, development and facilitation for setting up of iron and steel production facilities including

Electric Arc Furnace (EAF) units, Induction Furnace (IF) units, processing facilities like re-rollers, flat products

(hot/cold rolling units), coating units, wire drawing units and steel scrap processing including ship breaking.

IRON AND STEEL SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

Page 11 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

The Indian steel industry currently is at a crucial stage with challenges of climate change. While the industry is

expected to accelerate ramp up steel production to meet the needs of its population by infusion of additional

capacity, global issues like Climate change necessitate guided growth through low carbon intensive routes for

steel production. It is therefore imperative that all the steel makers across the country adopt energy efficient and

environment friendly technologies in all areas of iron and steel making in line with SOACT and BAT guidelines.

It is also necessary that all protection measures are adopted at the planning stage itself, as the cost of correction at

a later date will be very high. Existing plants need to evolve short term and long term action plan to phase out the

old and obsolete facilities by state-of-art clean and green technologies with an aim not only to achieve higher

standards of productivity but also to harness all waste energy with minimized damage to the environment.

Safety Measures The safety policy adopted in the Iron and Steel Industry in India is comparable to the policy followed

internationally. However, implementation and monitoring of these policy guidelines on the ground leave much to

be desired. As a result, the number of accidents, casualties, disabilities, loss to plant and machinery and

consequential loss of man-days and production is quite significant. It calls for an introspection and review of the

whole situation.

It has been observed that adherence to safety measures and policy is lacking due to many factors, viz. Indifference

on the part of management and workers, financial problems, lack of awareness, complicated and slack legal

machinery and lack of adequate statutory provisions. Use of many out-dated technologies still prevalent in India

exacerbates the hazards and risks in the plant.

Role of Government The Government has an important facilitating role in the development of the steel industry. As steel making is a

highly capital intensive and complex process requiring large-scale investment, historically the industry has

evolved with Government support. While direct Government involvement in steel making process may no longer

be required, the State will have to provide the necessary policy support to the sector to achieve the object of the

National Steel Policy to make India a global Steel producer. Some of the important areas, where Government

support is required, are – providing essential infrastructure facilities; assuring easy availability of critical inputs

such as iron ore, coal, gas and power; provision of training facilitity for manpower development and creation of a

consolidated and reliable data base for informed decision making by all stakeholders.

Important Definitions of the Environmental Acts

The Water (Prevention & Control of Pollution) Act, 1974

Section Key word Definition

Section 2 (d)

Occupier

In relation to any factory or premises, means the person who has control over

the affairs of the factory or the premises, and includes, in relation to any

substance, the person in possession of the substance

Section2(dd) Outlet Any conduit pipe or channel, open or closed, carrying sewage or trade

effluent or any other holding arrangement which causes or is likely to cause

pollution

IRON AND STEEL SRMA

Steel Re Rolling Mills

Association of India www.sram.co.in

Page 12 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Section 2 (e) Pollution Contamination of water or such alteration of the physical, chemical or

biological properties of water or such discharge of any sewage or trade

effluent or of any other liquid, gaseous or solid substance into water (whether

directly or indirectly) as may, or is likely to, create a nuisance or render such

water harmful or injurious to public health or safety, or to domestic,

commercial, industrial, agricultural or other legitimate uses, or to the life and

health of animals or plants or of aquatic organisms

Section 2 (g) Sewage

effluent

Effluent from any sewerage system or sewage disposal works and includes

sullage from open drains

Section2 (gg) Sewer Any conduit pipe or channel, open or closed, carrying sewage or trade

effluent

Section 2 (j) Stream Includes river, water course (whether flowing or for the time being dry),

inland water (whether natural or artificial), sub-terranean waters, sea or tidal

waters to such extent or, as the case may be, to such point as the state

government may, by notification in the official gazette specify in this behalf

Section 2 (k) Trade

effluent

Includes any liquid, gaseous or solid substance, which is discharged from any

premises used for carrying on any industry, operation or process, or treatment

and disposal system, other than domestic sewage

Section 47 (2)

(a)

Company Any body corporate, and includes a firm or other association of individuals

Section 47 (2)

(b)

Director In relation to a firm means a partner in the firm

The Air (Prevention & Control of Pollution) Act, 1981

Section Key word Definition

Section 2 (a) Air

pollutant

Any solid, liquid or gaseous substance (including noise) present in the

atmosphere in such concentration as may be or tend to be injurious to human

beings or other living creatures or plants or property or environment

Section 2 (b) Air

pollution The presence in the atmosphere of any air pollutant

Section 2 (c) Approved

appliances

Any equipment or gadget used for the bringing of any combustible material

or for generating or consuming any fume, gas of any particulate matter and

approved by the State Board

Section 2 (d) Approved

fuel

Any fuel approved by the State Board for the purpose of the Act

Section 2 (h) Chimney Includes any structure with an opening or outlet from or through which any

air pollutant may be emitted

Section 2 (i) Control

equipment

Any apparatus, device, equipment or system to control the quality and manner

of emission of any air pollutant and includes any device used for securing the

efficient operation of any industrial plant

Section 2 (k) Industrial

plant

Any plant used for any industrial or trade purposes and emitting any air

pollutant into the atmosphere

Section 2 (j) Emission Any solid or liquid or gaseous substance coming out of any chimney, duct or

flue or any other outlet

Section 2 (m) Occupier The person who has control over the affairs of the factory or the premises,

and includes, in relation to any substance, the person in possession of the

substance

Section40 (2) (a) Company Any body corporate, and includes a firm or other association of individuals

Section40 (2) (b) Director In relation to a firm means a partner in the firm

Page 13 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Salient Features of the “Contract Labour (Regulation & Abolition) Act, 1970”

“The Contract Labour (Regulation and Abolition) Act , 1970” provides for regulation of the employment of

contract labour and its abolition under certain circumstances. It covers every establishment in which 20 or more

workmen are employed on any day of the preceding 12 months as ‘contract labour’ and every contractor who

employs or who employed on any day of the preceding 12 months, 20 or more contract employee. It does not

apply to establishments where the work is of intermittent and casual nature unless work performed is more than

120 days and 60 days in a year respectively (Section 1). The Act provides for setting up of Central and Stat e

Advisory Contract Labour Boards by the Central and State Governments to advise the respective Governments on

matters arising out of the administration of the Act (Section 3 & 4). The establishments covered under the Act are

required to be registered as principal employers with the appropriate authorities. Every contractor is required to

obtain a license and not to undertake or execute any work through contract labour, except under and in accordance

with the license issued in that behalf by the licensing officer. The license granted is subject to conditions relating

to hours of work, fixation of wages and other essential amenities in respect of contract as prescribed in the rules

(Section 7 & 12).

The Act has laid down certain amenities to be provided by the contractor to the contract labour for establishment

of Canteens and rest rooms; arrangements for sufficient supply of wholesome drinking water, latrines and urinals,

washing facilities and first aid facilities have been made obligatory. In case of failure on the part of the

contractor to provide these facilities, the Principal Employer is liable to provide the same (Section 16, 17, 18, 19

and 20). The contractor is required to pay wages and a duty is cast on him to ensure disbursement of wages in the

presence of the author ised representative of the Principal Employer. In case of failure on the part of the

contractor to pay wages either in part or in full, the Principal Employer is liable to pay the same. The contract

labour who performs same or similar kind of work as regular workmen, will be entitled to the same wages and

service conditions a s regular workmen as per the Contract Labour (Regulation and Abolition) Central Rules,

1971 (Section 21). 7

For contravention of the provisions of the Act or a ny rules made there under, the punishment is imprisonment for

a maximum term upto 3 months and a fine upto a maximum of Rs.1000/- (Section 23 & 24). Apart from the

regulatory measures provided under the Act for the benefit of contract labour, the 'appropriate government' under

section 10(1) of the Act is authorised, after consultation with the Central Board or State Board, as the case may

be, to prohibit, by notification in the official gazette, employment of contract labour in any establishment in any

process, operation or other work.

New Land Acquisition Act is pro people, but

not anti-industry : Jairam Ramesh Minister seeks cooperation of state governments in better implementation

IRON AND STEEL SRMA

Steel Re Rolling Mills

Association of India www.sram.co.in

Page 14 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Union Minister for Rural Development Shri Jairam Ramesh today allayed the fears expressed

by the Indian industry that the new Land Acquisition Act would make projects economically

unviable. Addressing a Press Conference in Mumbai on Sunday, Shri Ramesh said the new act

applies only to the land acquired by Central and State authorities for any public purpose, while

there is no bar whatsoever, on purchase of private land. He said “industry must look beyond

land acquisition by Government and explore land purchase opportunities. In fact, in 20 years

from now, there should only be land purchases and no land acquisition”.

Reiterating his stand that land acquisition should become an act of last resort, Shri Ramesh said

his Ministry has been working towards improving land records management in the country and

promoting transparency in land sales. He informed that Rs 1000 crore National Land Record

Modernization Programme is being implemented with focus on computerization of land

records, digitization of maps and resurvey. He said Maharashtra has progressed well but is yet

to catch up with Haryana, Gujarat, Karnataka and Tripura.

Shri Ramesh said a Bill seeking amendment to the Registration Act of 1908 has been

introduced in Parliament, which when passed, will put all land sales and registration records in

public domain. “When transparency increases, it will become easier for corporate to purchase

land” he observed.

Speaking about the SEZs, the Rural Development Minister said all land acquisition for future

SEZs will be in accordance with the new act. He however admitted that the Act presently has

no provision to deal with denotified SEZs. Shri Ramesh termed the new act, which replaces

119 year old act as ‘historic’. “The 1894 Act was undemocratic as it vested enormous

discretionary powers in the hands of District Collectors. On the contrary, the new act is

humane, its thrust is on rehabilitation and resettlement, and if any act promotes the welfare of

tribals and marginal farmers, it is in national interest” he asserted. He said to represent this

spirit the new act has been re-christened as the “Right to Fair Compensation and Transparency

in Land Acquisition, Rehabilitation and Resettlement Act.”

"I believe that the old law was anti-democratic as governments used to buy land from people at

lower price and sell it to business houses at a premium rate. The collector decided the urgency,

the amount of compensation and resettlement provisions if any. Hence the old act created

public anger nationwide and was the reason behind mass movements on land issues in Uttar

Pradesh, Madhya Pradesh, and Gujarat along with Odisha” said the Minister.

He elaborated that under the new act the powers of the Collectors, who often acted under the

instructions of state governments have been considerably curtailed. The purpose of land

acquisition has been clearly spelt out and major emphasis has been laid on rehabilitation and

resettlement. He said that consent of Gram Sabha in Schedule V areas – mostly tribal

dominated areas, and consultation with Gram Sabha in other areas, has been made mandatory.

The Minister further added, that if the Government failed to utilize the land so acquired for

public purpose within five years, it will be required to return the land to its owners.

The Minister also said that the new Act promises fair compensation for the farmers and those

who lose their lands. “Land is still considered the biggest social security in India. Since they

will be dispossessed of their assets, they are entitled for a fair and just compensation” he said.

Page 15 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

The new act stipulates that compensation will be paid at twice the rate of three year average of

highest selling price in urban areas and up to four times the average highest sale price in rural

areas. In addition, there is also a provision of leasing the land instead of selling it, thereby

opting to receive a regular income over a longer period of time.

The Minister said the new law has been made under the concurrent list of the Constitution and

States could only improve upon the quantum of compensation as well as other provisions in

favour of the land owners and farmers. He said it would be notified either on January 1, 2014

or April 1, 2014 and appealed to all state governments to implement it in right spirit.

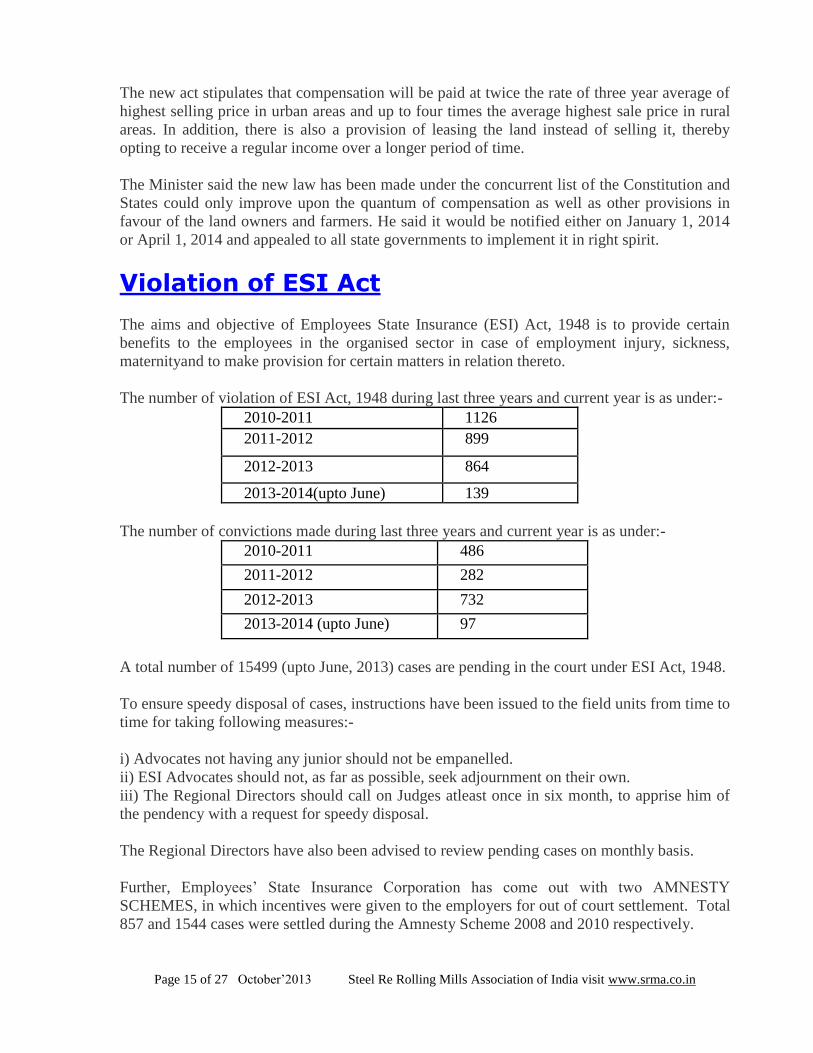

Violation of ESI Act

The aims and objective of Employees State Insurance (ESI) Act, 1948 is to provide certain

benefits to the employees in the organised sector in case of employment injury, sickness,

maternityand to make provision for certain matters in relation thereto.

The number of violation of ESI Act, 1948 during last three years and current year is as under:-

2010-2011 1126

2011-2012 899

2012-2013 864

2013-2014(upto June) 139

The number of convictions made during last three years and current year is as under:-

2010-2011 486

2011-2012 282

2012-2013 732

2013-2014 (upto June) 97

A total number of 15499 (upto June, 2013) cases are pending in the court under ESI Act, 1948.

To ensure speedy disposal of cases, instructions have been issued to the field units from time to

time for taking following measures:-

i) Advocates not having any junior should not be empanelled.

ii) ESI Advocates should not, as far as possible, seek adjournment on their own.

iii) The Regional Directors should call on Judges atleast once in six month, to apprise him of

the pendency with a request for speedy disposal.

The Regional Directors have also been advised to review pending cases on monthly basis.

Further, Employees’ State Insurance Corporation has come out with two AMNESTY

SCHEMES, in which incentives were given to the employers for out of court settlement. Total

857 and 1544 cases were settled during the Amnesty Scheme 2008 and 2010 respectively.

Page 16 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Manganese/Chrome Ores and Ferro-Alloys Summit Organiser: Federation of Indian Mineral Industries (FIMI)

Date : 16-17 December, 2013

Venue: Taj Bengal, Kolkata, India

Web Site:http://www.fedmin.com/online/general.php?eventid=28

==================================================================

Organiser: Metal Bulletin Events

Venue: Conrad Dubai, U.A.E

Web Site:http://www.metalbulletin.com/events/meis

============================================================

IRON AND STEEL SRMA

Steel Re Rolling Mills

Association of India www.sram.co.in

Page 17 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

STEEL NEWS

Primary Steel Producers are Likely to keep Finish Long Prices Unaffected

Primary steel producer had kept their finish long offers unchanged for November’13 and it

seems that they are likely to keep it same again for December’13 as finish long market need

some more improvements in demand.

On the other hand in secondary Re-bar market premium brands prices increased by INR 1,300-

1,900/MT.

In Maharashtra Guardian TMT a Mumbai based brand’s prices increased by INR 1,900/MT

from 1 Nov, to till date. 20mm TMT is offered at INR 35,300/MT exclude taxes.

Anant TMT manufacturer, based at Indore, MP has increased its prices by INR 1,300/MT in

same period (from 1 Nov to till date). Presently its offer is at INR 36,100/MT for 20mm.

(Basic Price)

High Raw material and Semi finish products prices are the reasons behind these increment in

prices.

Primary TMT prices (in INR/MT) as on month Nov 2013

Region Particular Price (Basic) Price#(All Tax) M-O-M

North India Delhi/NCR 38,000 44,800 - 250

West India Mumbai 37,200 43,900 - 350

South India Chennai 38,800 45,800 - 250

Hyderabad 37,800 44,600 - 350

Monthly Assessment

Size – 12MM

Grade- 500 Fe

Excise Duty @ 12.36% ;VAT as applicable.

# Prices including all taxes

India: Re-Bar Prices increases owing to Shortage of Semi Finish Products

Indian Manufacturers have to increase the price of Re-bar by INR 200-500 per MT in last 2-3

days owing to the hike in prices of Semi Finish product.

In Central India, Re-bar prices have moved up by INR 200-300 per MT from yesterday owing

to shortage of Ingot and Sponge. In addition, there is some demand in Raipur and Raigarh from

MP. In Raipur and Indore 20 mm Re-bar is traded at INR 30,500 per MT and at INR 35,100

per MT respectively.

Page 18 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

In Maharashtra, Mumbai based Shree Vaishnav Industries Private Limited, with a Re-bar

production capacity of approx 18,000 MT per month has increased its Re-bar price by INR 400

per MT in last 2-3 days. 20 mm Re-bar is now offered at 34,100 per MT.

“The demand for finish product after Diwali was good, but right now we have a normal

demand for the product. It seems that steel market will either sustain or go up”, said a Re-bar

trader based at Mumbai.

Few days back, in Hyderabad, a spurt of INR 200-300 per MT was seen in TMT and Ingot due

to little increment in local demand. Presently 20 mm Re-bar is quoted around at INR 31,700-

32,000 per MT.

Market participants are of the view that there are fewer chances of rates to decrease, many

plants have shut down while some are running at very low production capacity, creating

product shortage across the cities.

Note: All prices are Basic.

Region Particular Price (Basic) Price

#(All

Tax) Change W-O-W M-O-M

Indian 12 mm Re-bar prices (in INR/MT) as on date 19-Nov-2013

North

India

Ghaziabad 32,800 38,700 0 + 400 - 700

Mandi

Gobindgarh 35,250 41,600 0 + 150 NA

Delhi/NCR 33,000 38,900 0 + 400 - 700

Muzaffarnagar 32,400 38,200 0 + 400 - 700

East

India

Rourkela 30,300 35,700 0 - 100 - 900

Durgapur 30,900 36,200 + 200 + 200 - 350

Central

India

Raipur* 31,100 36,000 0 + 450 - 500

Indore 35,500 41,900 + 300 + 600 - 150

Raigarh 30,000 35,400 0 0 - 600

West

India

Jalna 34,100 40,200 + 100 0 + 200

Mumbai 34,100 40,200 + 200 + 100 + 600

Ahmedabad 33,000 38,900 - 100 0 - 700

Goa 34,900 41,200 + 300 + 100 - 200

Jaipur 32,900 38,800 0 + 250 - 900

South

India

Chennai 33,400 39,400 0 0 - 400

Hyderabad 32,850 38,800 0 + 650 + 350

Bangalore 34,400 40,600 0 - 400 0

Daily Assessment

Grade-415/500 Fe

Excise Duty @ 12.36%; VAT as applicable.

*Payment next day

# Prices including all taxes

Page 19 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

India: Re-bar Prices inch up in Central and Northern Region

Re-bar prices increased by INR 200-300 per MT in Central and Northern Region from last

trade. Chhattisgarh

Re-bar prices have increased by INR 200-300 per MT in Raipur for

the reason that Semi finish prices increased in city. Ingot and Billet

manufacturers have cut their production on dull demand in steel

market. There are approx 15-20 manufacturers who have more than

two or three furnaces, using only one or two of them. This resulted in

shortage of Semi finish products and hike in product prices.

An average price for 20 mm TMT is around at INR 30,200-30,500 per MT which is increased

by INR 200-300 per MT. Whereas GK TMT’s price is untouched for the day and 20 mm Re-

bar is quoted at INR 31,200 per MT.

Madhya Pradesh

Anant Steel Pvt. Ltd. with a Re-bar production capacity of approx 14,000MT per month based

in Indore has increased its prices by INR 300 per MT from last trade. 20 mm TMT is offered

at INR 34,800 per MT.

Uttar Pradesh

Ingot and TMT prices have moved up by INR 100-300 per MT in Muzaffarnagar because of

increased Ingot prices in Mandi Gobindgarh. MS Ingot and 12 mm TMT are offered at INR

30,400 per MT and INR 32,500 per MT respectively.

Above mentioned all Prices are Basic.

Page 20 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

RE-BAR PRICES INCREASED BY INR 400-500/MT IN SOUTHERN REGION

IN LAST TWO DAYS.

Andhra Pradesh

In Hyderabad Semi Finish and Finish long product prices inched up as some furnaces and

rolling mills have shut down in city. Shortage of the material in market, resulted in its price

increase by INR 400-500/MT. 20 mm TMT is offered at INR 31,500/MT.

Karnataka

Ingot and TMT prices have moved up by INR 500/MT in Bangalore yesterday. This hike was

made on account of good demand from Hyderabad and local market. 12 mm TMT and MS

Ingot are offered at INR 34,800/MT and INR 29,700/MT respectively.

Tamil Nadu

Semi Finish and Finish Long prices are continuously unchanged from a long time in Chennai.

MS Ingot and 12 mm TMT offers are at INR 28,900/MT and INR 33,400/MT respectively.

According to market participants – “It will not be beneficial for us if we reduce the steel prices

according to the other steel market. When we reduce the product prices, buyers wait for some

more corrections. So we have decided not to make any changes according to the other

markets”.

ABOVE MENTIONED ALL PRICES ARE BASIC.

Page 21 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

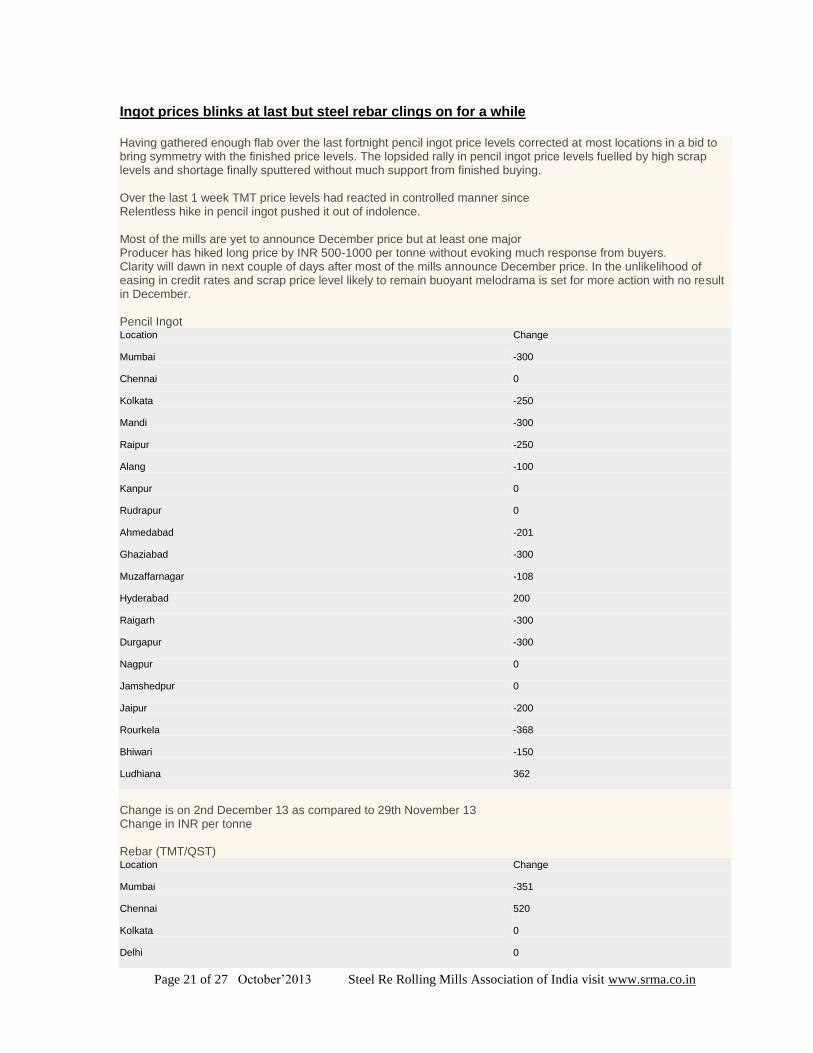

Ingot prices blinks at last but steel rebar clings on for a while Having gathered enough flab over the last fortnight pencil ingot price levels corrected at most locations in a bid to bring symmetry with the finished price levels. The lopsided rally in pencil ingot price levels fuelled by high scrap levels and shortage finally sputtered without much support from finished buying. Over the last 1 week TMT price levels had reacted in controlled manner since Relentless hike in pencil ingot pushed it out of indolence. Most of the mills are yet to announce December price but at least one major Producer has hiked long price by INR 500-1000 per tonne without evoking much response from buyers. Clarity will dawn in next couple of days after most of the mills announce December price. In the unlikelihood of easing in credit rates and scrap price level likely to remain buoyant melodrama is set for more action with no result in December. Pencil Ingot Location Change

Mumbai -300

Chennai 0

Kolkata -250

Mandi -300

Raipur -250

Alang -100

Kanpur 0

Rudrapur 0

Ahmedabad -201

Ghaziabad -300

Muzaffarnagar -108

Hyderabad 200

Raigarh -300

Durgapur -300

Nagpur 0

Jamshedpur 0

Jaipur -200

Rourkela -368

Bhiwari -150

Ludhiana 362

Change is on 2nd December 13 as compared to 29th November 13 Change in INR per tonne Rebar (TMT/QST) Location Change

Mumbai -351

Chennai 520

Kolkata 0

Delhi 0

Page 22 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Mandi 0

Raipur 0

Kanpur 0

Rudrapur 0

Ahmedabad 300

Hyderabad 0

Indore 600

Bangalore 0

Ludhiana 104

Muzaffarnagar 0

Change is on 2nd December 13 as compared to 29th November 13 Change in INR per tonne Source - Strategic Research Institute (www.steelguru.com)

India: Demand for Wires improve with rising offers

Indian Wires offers are on a consistent rise; an increase of INR 200-300/MT was recorded

today. Demand picked up as market participants expect prices to increase further.

In Raipur, Wire offers moved up by INR 200-300/MT from the last trade. 5.5 mm Wire Rod

and 20 Gauge Binding Wire was offered at INR 39,900/MT and INR 46,000/MT respectively.

Raipur is witnessing a shortage of Binding wires as some manufacturers have not stared

production after Diwali. Queries for GI and Barbed wires have increased quite a bit.

In Durgapur, wires are being quoted higher but buying is still low. 5.5 mm Wire Rod is being

offered at INR 38500/MT which is INR 200/MT higher than the last trade.

Note: Prices are Inclusive of VAT.

Page 23 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

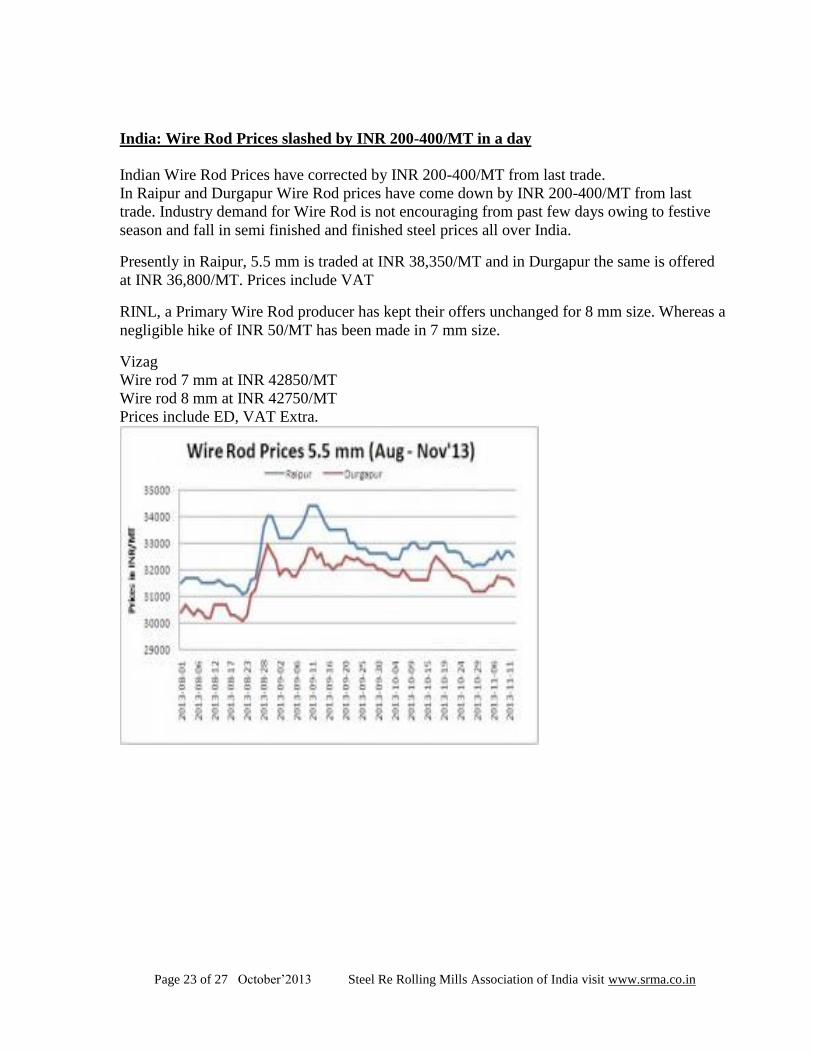

India: Wire Rod Prices slashed by INR 200-400/MT in a day

Indian Wire Rod Prices have corrected by INR 200-400/MT from last trade.

In Raipur and Durgapur Wire Rod prices have come down by INR 200-400/MT from last

trade. Industry demand for Wire Rod is not encouraging from past few days owing to festive

season and fall in semi finished and finished steel prices all over India.

Presently in Raipur, 5.5 mm is traded at INR 38,350/MT and in Durgapur the same is offered

at INR 36,800/MT. Prices include VAT

RINL, a Primary Wire Rod producer has kept their offers unchanged for 8 mm size. Whereas a

negligible hike of INR 50/MT has been made in 7 mm size.

Vizag

Wire rod 7 mm at INR 42850/MT

Wire rod 8 mm at INR 42750/MT

Prices include ED, VAT Extra.

Page 24 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

Increased Steel Prices are Center of Attention to Finished Buyers

Steel prices (Ingot, Billet, Sponge and Finished products) increased by

INR 700-1,400/MT in last one week across India. Limited production of Ingot/Billet due to low conversion cost and shortage

of Raw material have increased the product prices creating center of

attention to finished buyers. Eyeing the spurt in Steel prices finished

demand has increased in some places of India.

In Rajasthan, Re-bar prices are increased by INR 1,400/MT on W-o-W basis. In Jaipur 12mm

Premier Re-bar is being quoted at INR 35,900/MT, INR 300 higher from last trade. (Basic

Price)

According to a Re-bar trader based at Jaipur –“Ingot prices are increasing 2-3 times in a day

and it is attracting the demand for finish buying.”

Whereas in some places Re-bar manufacturers have changed the prices of Re-bar gauge

difference to make a balance in conversion. In Muzaffarnagar, Jaipur and Durgapur the prices

on Re-bar gauge difference are increased to about INR 300-500 in various sizes.

Gauge Difference

Page 25 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

JSW hopes that 2014 will be a better year

Business Standard reported that with the possibility of iron ore prices coming down and steel prices remaining stable, leading domestic firm JSW Steel said that things are looking up for the industry next year. Mr Seshagiri Rao Joint MD and Group CFO of JSW Steel said that “On iron ore, analysts have a lot of expectations. Huge supply will be there in market next year. At the same time, demand from China is likely to come down. Based on these 2 factors, iron ore price may not go up next year.” Mr Rao said that “Steel demand this fiscal is flattish as the consuming industries are not growing. That is also getting reflected in flattish consumption of steel. The demand has to revive to see the growth in the steel sector.” He said that steel prices in India, which are often linked to international prices, would remain stable as demand for steel would be better next year with recovery happening in the US and the bottoming out of the European economy. He added that “Recovery happening in the US market and consumption will go up there. Europe is already at the bottom, so there can be some recovery there. Japan is reasonably doing well and Korea is quite okay. So, only thing we need to watch is China, which is expected to slow down next year. These would keep steel prices stable next year, when raw material prices are expected to come down. 2014 is expected to be better for steel industry.” Source – Business Standard (www.steelguru.com)

Majority of steel units in North India running below 50% capacity – CII CII Accenture report said that majority of iron and steel units in northern India are running at below 50% of their capacities primarily because of power shortage and spiralling input cost. The report said that “Most steel mills are running at less than 50% of their respective rated capacities because of poor supply and rising input cost. The power outages in northern states are resulting in production losses and forcing many mills to work only single shifts.” The report on ‘Indian Steel Industry-An overview and growth prospects of steel industry in north India further pointed out that rupee depreciation against the US dollar has not only raised industry’s input cost but also dealt a severe blow to industry as it faced cancellation of export orders. It said that “Depreciation of rupee resulted in significant increase in cost of imported steel melting scrap, a major input in secondary steel production. Further due to rupee depreciation, export orders have been cancelled or deferred, which is another set back for the steel industry in north India.” Suggesting measures for de-bottlenecking steel sector in north, the report said that the steel suppliers should play a major role in implementation of mega investment projects, including USD 100 billion Delhi Mumbai Industrial Corridor, export zones and industrial parks across Rajasthan, Haryana and western UP as these projects will continue to drive sustained demand for long steel. Presenting potential growth constraints, the report said the growth in steel market is expected to be muted in short term on account of poor growth in core consumer sectors. It said that “The demand is expected to rebound in later half of 2015 with growth in infrastructure as announced in 12th 5 year plan. Growth in automobile and consumer durable sectors will also support demand growth in long run.” Regulatory hurdles and land acquisition challenges remain the largest supply side constraint for Indian

Page 26 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in

steel market. India’s northern steel hub contributes about 16% to country’s annual steel output with hub comprising multiple small and medium units primarily induction furnaces and steel re rolling mills located in and around Punjab and Haryana. These units cater to construction and light engineering sector including bicycle and auto parts. Uttar Pradesh is the largest producer and consumer of steel in north India with production of 5.6 million tonne per annum. Source - PTI (www.steelguru.com)

Steel producers urge Punjab govt to slash entry tax

Business Standard reported that perturbed over the high entry tax in Punjab, as compared to states like Uttar

Pradesh, Haryana, Rajasthan and Delhi, iron and steel producers located outside the state feel that it is detrimental

to the iron and steel based industry in the state and urged the government to bring it on a par with the

neighbouring states.

It is worth mentioning that Haryana charges 1% entry tax on iron and steel. Recently, Uttar Pradesh has also

brought it on a par with that of Haryana by reducing it to 1% from 5%, whereas Punjab has imposed 5% as entry

tax, the highest among the neighbouring states. Further, states like Delhi and Rajasthan have no entry tax on iron

and steel produced outside the state.

Speaking to Business Standard Mr V R Sharma deputy MD and CEO of Jindal Steel & Power Limited said that

“With annual consumption of 5 million tonne of iron and steel, Punjab features among the states where there is

high consumption. But the imposition of five% entry tax on iron and steel produced outside the state is

detrimental to the iron and steel based industry located within the state.” According to him, this makes the input

cost higher as compared to other manufacturers which based in other states.

Sharing his views, Mr A S Cheema director of Cheema Boilers said that “It’s important that the manufacturers

using iron and steel as raw materials procured from outside the state, should do value addition in their finished

goods in order to sustain, otherwise it’s very difficult to survive in this price-sensitive market. Therefore,

manufacturers need to improve their understanding of buyer values and create innovative products targeted at

different customer segments.”

However, responding to industrialists request, Mr Karan Avtar Singh principal secretary of industries &

commerce Punjab said that “The imposition of entry tax on iron and steel was done in order to promote the

industry located inside the state. We expect new capacity addition will happen in this sector and it will attract new

investments.”

According to the state government officials, if the sale of goods is within the state, the entry tax is adjusted but if

it is outside the state, it cannot be reimbursed by the state.

Experts are of the view that the imposition of entry tax on iron and steel makes the input cost higher and the goods

manufactured in the state become non competitive as compared to the goods produced in other states.

Source – Business Standard (www.steelguru.com)

Page 27 of 27 October’2013 Steel Re Rolling Mills Association of India visit www.srma.co.in