Embed Size (px)

Citation preview

IRS Audit Activity InvolvingExecutive Compensation and Benefits

ABA Tax Section (EO Committee)

Midyear MeetingJanuary 21, 2011

Ralph E. DeJong, Esq.

McDermott Will & Emery LLP

Robert W. Friz

PricewaterhouseCoopers LLC

2

Executive Compensation Still a Major Area of Concern

� Broader context is qualification for federal tax-exempt status,

particularly for charitable hospitals

� Executive pay and benefits still make headlines

� Sen. Grassley wanted tighter rules, but PPACA ultimately

included non-pay-related exemption requirements for

hospitals

3

Executive Compensation Still a Major Area of Concern (Cont’d)

� Form 990, as revised, provides more detail, but confusion

continues

– Double counting deferred compensation

– Disparate reporting practices

– Comparing pre-2009 and post-2007 Forms 990

– Difficult to link numbers and narrative explanations

4

IRS Executive Compensation Activity

� 2004 “soft contact” questionnaires included questions on

executive compensation

– Frequent unreported items

– Generally addressed through prospective changes in 990 reporting

� 2007 report on IRS findings

– Primarily focused on 990 reporting noncompliance

– Some concern as to loans

5

IRS Executive Compensation Activity (Cont’d)

� 2006 Hospital questionnaires included an executive

compensation section

– Conflicts of interest involving approval body

– Comparability data

� 2009 report on hospital project

– Nearly all hospitals responding used rebuttable presumption process

– 20 hospitals were audited, but pay was found to be reasonable

6

IRS Executive Compensation Activity (Cont’d)

� 2008 compliance check questionnaires, sent to 400 public

and private colleges and universities, included questions on executive compensation, types of executive benefits, and

review and approval process

� 2010 interim report on colleges and universities project,

noting follow-up audits being conducted at more than 30 of

the 400 institutions involved

7

IRS Executive Compensation Activity (Cont’d)

� 2010-12 employment audit program

– 2,000 employers per year for three years

– Includes roughly 1,500 EOs

– Focus on employee (vs. independent contractor) status, executive

fringe benefits, executive pay, and payroll tax compliance

� Combined Annual Wage Reporting (CAWR) Project

– IRS analysis of employment tax reporting by EOs for 4,000

organizations from FY 2007 – 2010

– Included focusing on reporting of officer compensation on Form 990

with no Form W-2 reporting

8

What Are the Risks?

� Challenge to exempt status based on private inurement or

more than insubstantial private benefit

– Corporate income tax liability

– Financial reporting considerations, including FIN 48 (ASC 740-10)

� Intermediate sanctions excise taxes on disqualified person

who received an excess benefit from a 501(c)(3) or (c)(4)

entity

� Automatic excess benefit transaction for any economic benefit (to a disqualified person), if the organization did not

clearly indicate its intent to treat the benefit as compensation

at the time of payment

9

What Are the Risks? (Cont’d)

� Penalties for failing to report, withhold as to, and pay

employment taxes as to, economic benefits that should have been treated as taxable compensation

Key Audit Issues / Observations

� Automatic Excess Benefit Transactions - accountable vs.

non-accountable plans

– Accountable Plan Requirements

– Business connection

– Substantiation

– Return of any amounts in excess of substantiated

expenses

10

� Automatic Excess Benefit Transactions - accountable vs.

non-accountable plans

– Non-accountable plan reimbursements generally implicate

– Form W-2 and Form 941 reporting

– Withholding and payment of employment taxes

– Form 1040 reporting

11

Key Audit Issues / Observations (cont’d)

Key Audit Issues / Observations (cont’d)

� Automatic Excess Benefit Transactions

– Intent to treat reimbursements as compensation for

services

– Written contemporaneous substantiation

– Reasonable cause exception

12

� Automatic Excess Benefit Transactions

– Key IRS focus areas

– Expense reimbursements not satisfying the strict

accountable plan rules

– Fringe benefits that may not be covered by a statutory

exclusion

– Loans to disqualified persons

– Existence of a bona-fide loan

– Imputed income issues for below-market loans

13

Key Audit Issues / Observations (cont’d)

14

Audit Issues Generally

� Identify who is at risk, whose issues are implicated, to whom

the audit is directed, and who is the client

– Note the disparate interests, in a 4958 case, of the entity and the

recipient

� Potential conflict of interest for legal counsel that previously

advised as to any item being challenged

� Application of attorney-client and attorney work product

privileges

– Consultant reports and/or reasonableness opinions prepared at

direction of counsel

15

Audit Issues Generally (Cont’d)

– Counsel’s correspondence and/or risk assessments

– Drafts of final reports, opinions and correspondence

� Statute of limitations

– Which years are open?

– Normally a three-year period running from filing deadline for 990 on

which item is adequately reported

– If the contested issues have not been adequately reported on 990, a

six-year period applies

– An audit typically begins with a request to extend the limitations period

on open years being examined

16

Audit Issues Generally (Cont’d)

� Who defends? Check for applicable liability insurance and

rights of carrier to defend

� Bear in mind strategic options

– Requesting technical advice

– Showing reasonable cause

– Requesting abatement of certain taxes

17

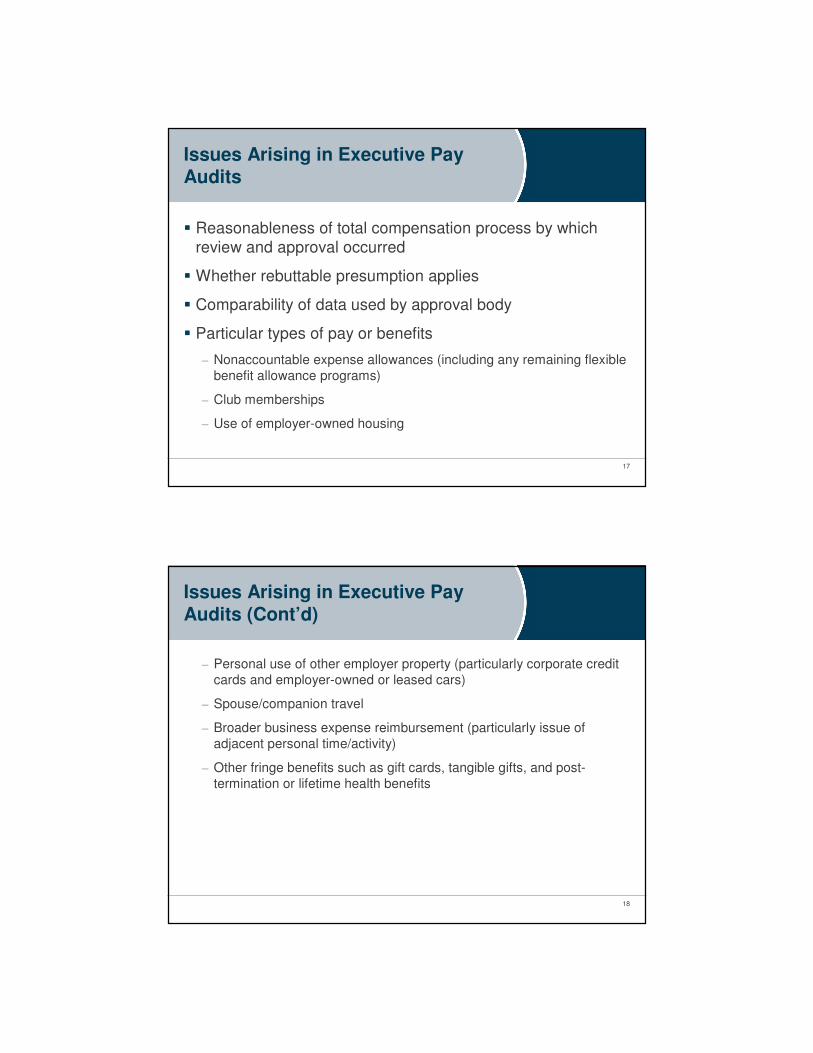

Issues Arising in Executive Pay Audits

� Reasonableness of total compensation process by which

review and approval occurred

� Whether rebuttable presumption applies

� Comparability of data used by approval body

� Particular types of pay or benefits

– Nonaccountable expense allowances (including any remaining flexible

benefit allowance programs)

– Club memberships

– Use of employer-owned housing

18

Issues Arising in Executive Pay Audits (Cont’d)

– Personal use of other employer property (particularly corporate credit

cards and employer-owned or leased cars)

– Spouse/companion travel

– Broader business expense reimbursement (particularly issue of

adjacent personal time/activity)

– Other fringe benefits such as gift cards, tangible gifts, and post-

termination or lifetime health benefits

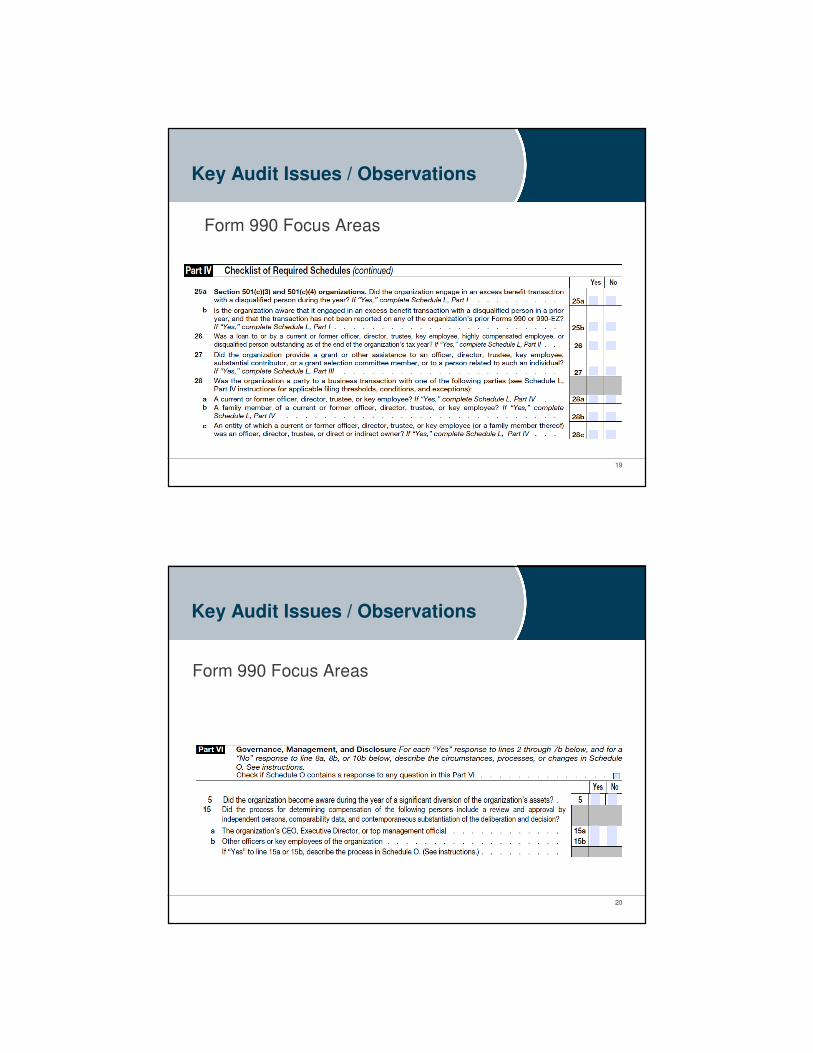

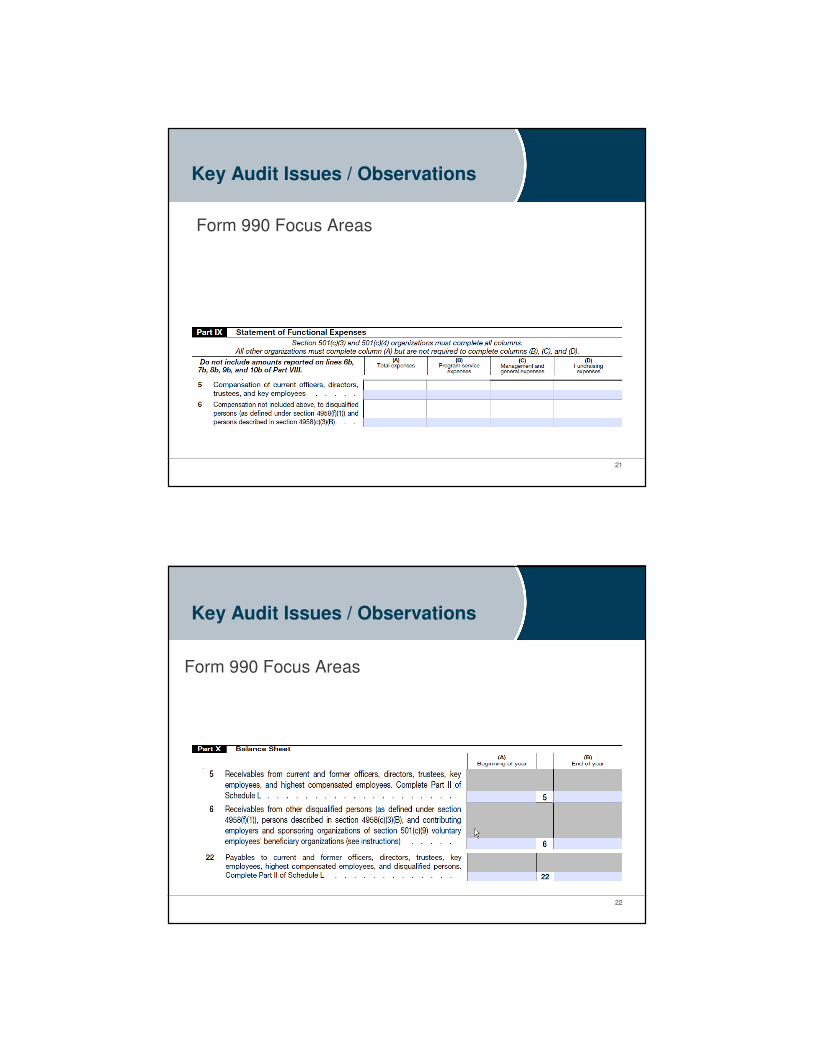

Key Audit Issues / Observations

Form 990 Focus Areas

19

Key Audit Issues / Observations

20

Form 990 Focus Areas

Key Audit Issues / Observations

Form 990 Focus Areas

21

Key Audit Issues / Observations

Form 990 Focus Areas

22

23

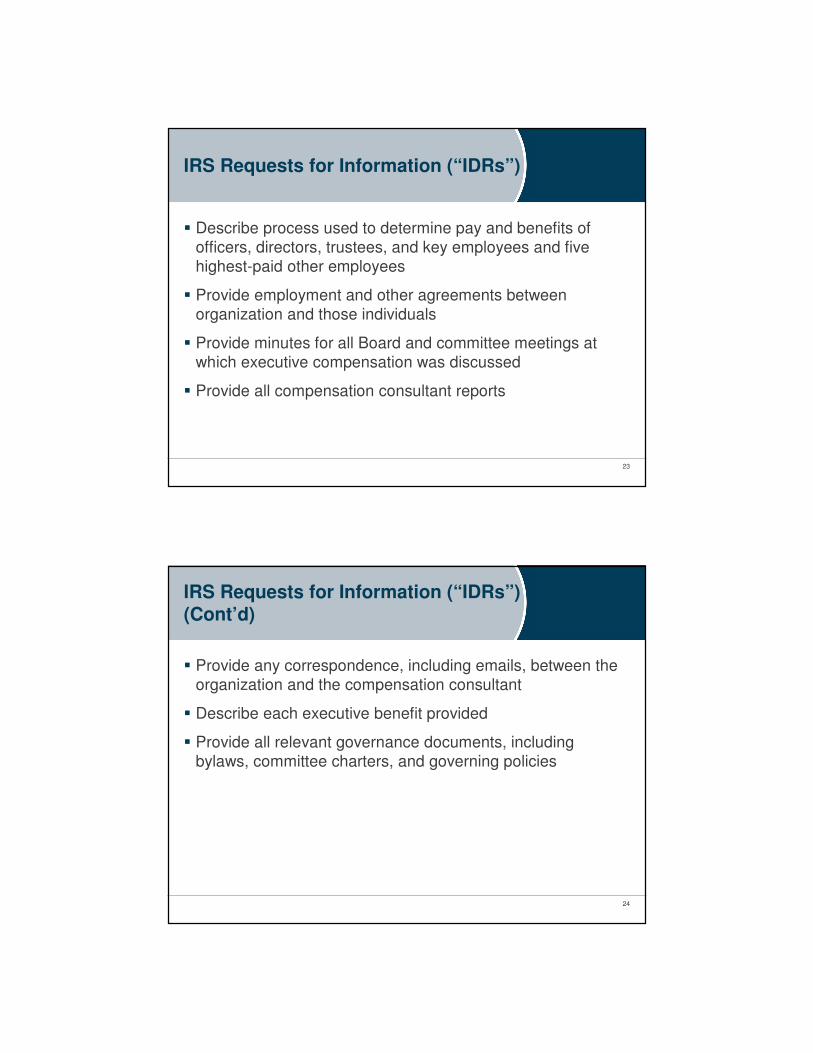

IRS Requests for Information (“IDRs”)

� Describe process used to determine pay and benefits of

officers, directors, trustees, and key employees and five

highest-paid other employees

� Provide employment and other agreements between

organization and those individuals

� Provide minutes for all Board and committee meetings at

which executive compensation was discussed

� Provide all compensation consultant reports

24

IRS Requests for Information (“IDRs”) (Cont’d)

� Provide any correspondence, including emails, between the

organization and the compensation consultant

� Describe each executive benefit provided

� Provide all relevant governance documents, including

bylaws, committee charters, and governing policies

25

Typical Disputed Issues in Executive Compensation Audit

� Application of rebuttable presumption

� Whether use of for-profit data was appropriate

� Whether compensation consultant was independent

� Did market data represent “similarly situated” organizations?

� Whether reasonable compensation starts at the market

median

� Whether 990 data of other organizations should be used to challenge or defend compensation as reasonable

26

Typical Disputed Issues in Executive Compensation Audit (Cont’d)

� Whether use of employer-owned property was sufficiently

business-related

27

Preparing for Possible Audit

� Do meeting minutes clearly describe compensation and

benefits considered and approved, approval process, rebuttable presumption and basis for reasonableness

conclusion?

� Are all elements of pay and benefits, and all uses of

employer property, identified and known to the Board or

applicable committee?

� Is the authority of the applicable committee to review and

approve compensation, and to qualify for the rebuttable

presumption, clear?

28

Preparing for Possible Audit (Cont’d)

� Has organization identified and resolved all conflicts and dualities of interest involving members of the applicable committee, so that an actual or perceived conflict does not become a sticking point?

� Is the compensation consultant sufficiently independent?

� Has the organization reported everything on the 990 in a manner that will cause the statute of limitations to run?

� Whether or not the compensation consultant has opined on reasonableness, has the Board or applicable committee reached its own supportable and well-articulated conclusion as to the reasonable of compensation?

29

Preparing for Possible Audit (Cont’d)

� Is the full Board at least aware of all executive

compensation?

� Is the organization aware of when the “initial contract

exception” (to 4958 excise taxes) might apply, and is the 990

reporting consistent with the position?

� For any known excess benefit transactions, has a thorough correction been made (that will serve as a good defense to

an exemption challenge), and is the 990 Schedule L

reporting clear and consistent?

30

Preparing for Possible Audit (Cont’d)

� Has the organization clearly stated which economic benefits

are intended at all times to constitute compensation (by contract, approval as compensation, or reporting on an

appropriate federal tax form), so as to avoid automatic

excess benefit transaction treatment?

27458846.1