Embed Size (px)

Citation preview

Is Stress Testing more effective than VaR?

UCITS Risk Management conference, May 2011

Aristides ProtopapadakisManaging Director

2

Stress Testing vs. VaR

► Old concept… but renewed interest. Why?

− Senior managers have lost confidence in modeling?

− Regulatory stress testing exercises

3

Factors in favor of stress testing

► Post-crisis skepticism about VaR model assumptions

− Fat Tails? Correlation structures?...

► Stress results easier accepted by senior management

► Stress scenarios based on insight of experienced managers

► Can cover risk types poorly managed in VaR models

► Particularly relevant to managing the risks on hedge fund

strategies

4

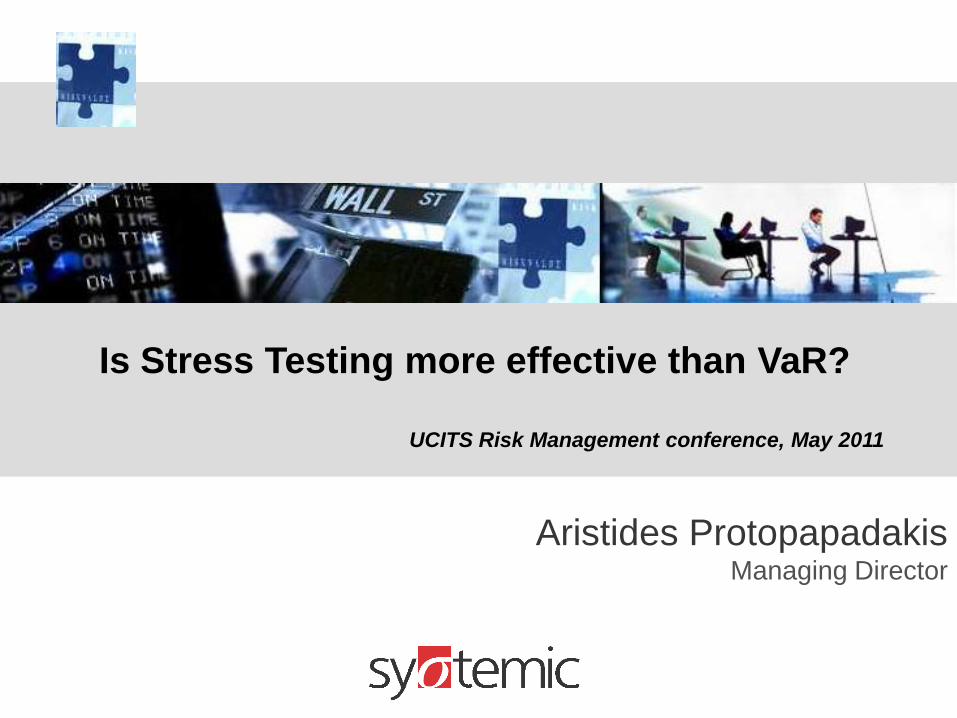

Are VaR models suitable to Hedge Fund strategies?

► Static Strategies

− Hedge fund strategies may reflect expectations about future

occurrence of historically rare events

− The VaR methodology will be likely based on the same data used to

formulate the strategies => Not independent view!

► Dynamic Strategies

− Buy/ Sell accross time upon specific events

− Long term cumulative risks typically ignored by VaR models!

► Unlike VaR, stress scenarios must be strategy specific

− Risk Manager must identify strategies expressed in the portfolio

− Implement scenario sets that stress the particular strategies

5

Examples

► Strategy #1 (Static)

− Long-short CDS on paired names/ diff. tenors/ CDS vs. Bond basis/

index tranches at various attachment points

− Stress Scenarios: Idiosyncratic movement of spreads, spreads term

structure, Bond vs. CDS liquidity premium, base correlation curve

across index or between indexes

► Strategy #2 (Dynamic)

− G7 ccy strategy: Borrow GBP and sell against USD when spot rate +

interest differential <> equilibrium view

− Stress scenarios: Dynamic paths of FX and interest rates, and then

simulate the buy and sell decisions across each path

6

ESMA Guidelines: Risk management process

► Applies to Investment Co (self-managed UCITS) or ManCo

► Should comprise procedures enabling the ManCo to assess

the UCITS risk exposure (risk measures, limits…)

► All material risks must be addressed:

− Market risks

− Liquidity risks

− Counterparty & Issuer Concentration risks

− Operational risks

► Assessment at least on a daily basis

7

Stress Testing in ESMA Risk Guidelines

► Program in line with UCITS risk profile (freedom…)

► Must capture all risk factors, in particular those not captured

by VaR model.

► Run at least monthly

► Execution of the program must be documented and

traceable

8

Which statement appeals more to you?

A. VaR models where developed for Banks and are not well

suited to funds risk management

B. Stress tests are a meaningless regulatory requirement:

Too subjective to be taken under account seriously

C. Stress testing is a valuable risk assessment tool, in

addition to traditional VaR analysis.

9

Stress Testing in practice

I. Market Risk

10

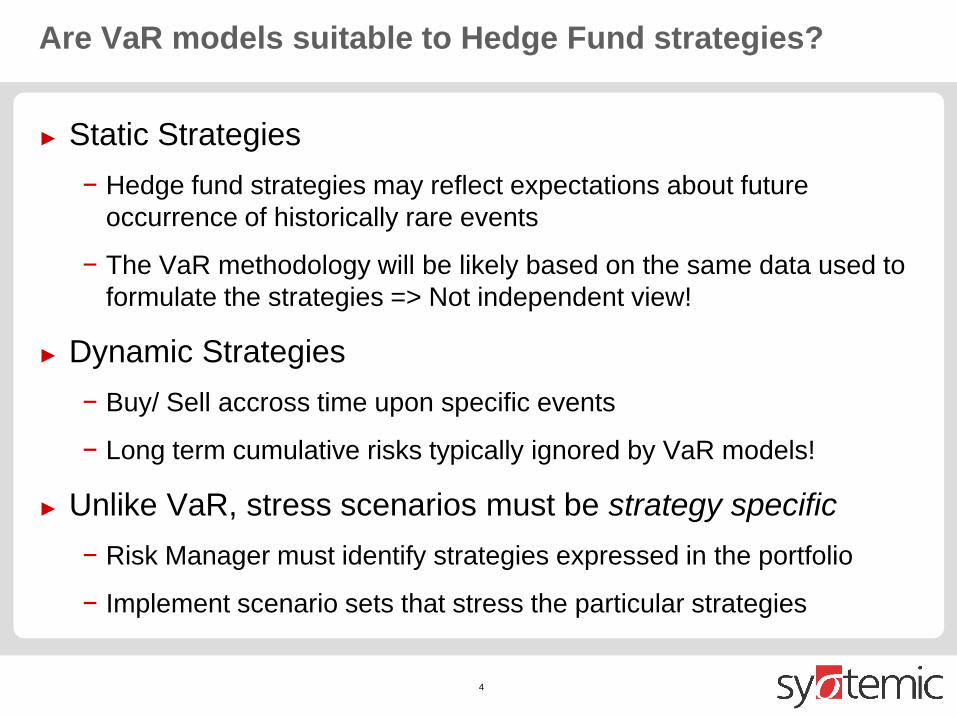

Gaussian vs. “Fat” tails

11

Gaussian vs. Real world dependence structure

Source:

Acharaya (2008)

12

Dependence in the real world

Source:

Jon Gregory (2008)

13

Tool: Use of PCA for stress testing interest rates

► Traditional analysis: Multiple, correlated risk factors

− ΔNPVbonds = f( 1m, 3m, 6m, 9m, 1y, 2y, 3y, 5y, 7y, 10y, 15y, … )

► PCA analysis

− ΔNPVbonds =

f( trend, tilt, curvature )

► Easy to stress a “six sigma” change in trend, tilt, or

curvature

14

Stress Testing + VaR: Stressed VaR!

► Bank Supervisors will be more proactive in using stress

testing as a determinant of a Bank’s capital requirements.

► Stressed VaR is a move in this direction

► This at least doubles capital for market risks

► Model inputs must be calibrated to historical data from a

continuous 12-month period of significant financial stress

relevant to the bank’s portfolio.

► Respected authors call this approach “ridiculous”!

avgctavgct sVaRmsVaRVaRmVaRc ,max,max 11

15

Stress Testing in practice

II. Specific (idiosyncratic) Risk

16

ESMA Guidelines: Choice of VaR model

► Historical, Monte Carlo simulation, or Parametric

− At least six tenors for interest rates

− Include non-linearity (gamma)

− Include vega risk

► VaR model must also account for idiosyncratic risk:

− Credit Spread risk

− Equity residual risk

− Premium/ discount (between cash and futures)

17

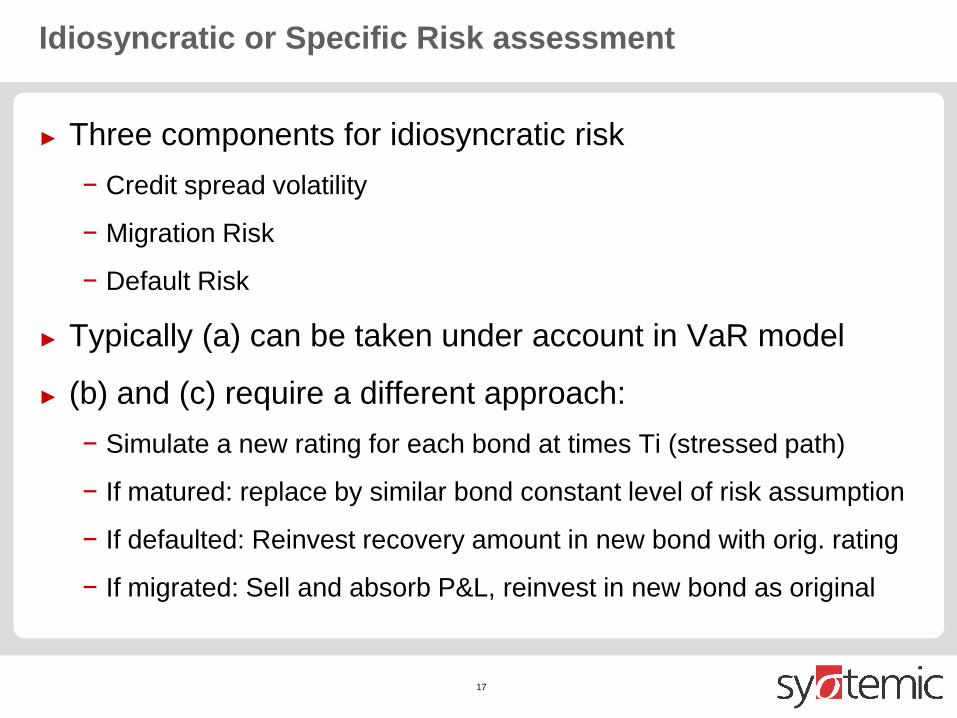

Idiosyncratic or Specific Risk assessment

► Three components for idiosyncratic risk

− Credit spread volatility

− Migration Risk

− Default Risk

► Typically (a) can be taken under account in VaR model

► (b) and (c) require a different approach:

− Simulate a new rating for each bond at times Ti (stressed path)

− If matured: replace by similar bond constant level of risk assumption

− If defaulted: Reinvest recovery amount in new bond with orig. rating

− If migrated: Sell and absorb P&L, reinvest in new bond as original

18

Stress Testing in practice

III. Liquidity Risk

19

Incorporating market liquidity in a VaR model

► Exogenous liquidity refers to the transaction cost (bid/ offer

spread) for trades of average size

► Endogenous liquidity: Is related to the cost of unwinding

portfolios large enough that the bid-ask spread cannot be

taken as given, but is affected by the trades themselves.

20

Exogenous vs. Endogenous liquidity

► Approach for

exogenous liquidity:

Integrate the variability

of the bid/ offer spread

for average

transactions as a risk

factor

21

Endogenous liquidity

► Particularly relevant in under stress conditions

− Margin requirements may cause different price movements on

assets with identical payoffs

− Delta hedging activities (buying an asset when price goes up).

Especially when many banks have same kind of positions against

investors who do not dynamically hedge.

► Approaches: Liquidity-adjusted returns, weighted bid/ as

spreads based on volume.

► Preferred approach: Varying time horizon.

− Parameter required for each position: Fraction of daily volume that

can be liquidated without significant impact to the market.

22

Stress Testing in practice

IV. Counterparty Risk

23

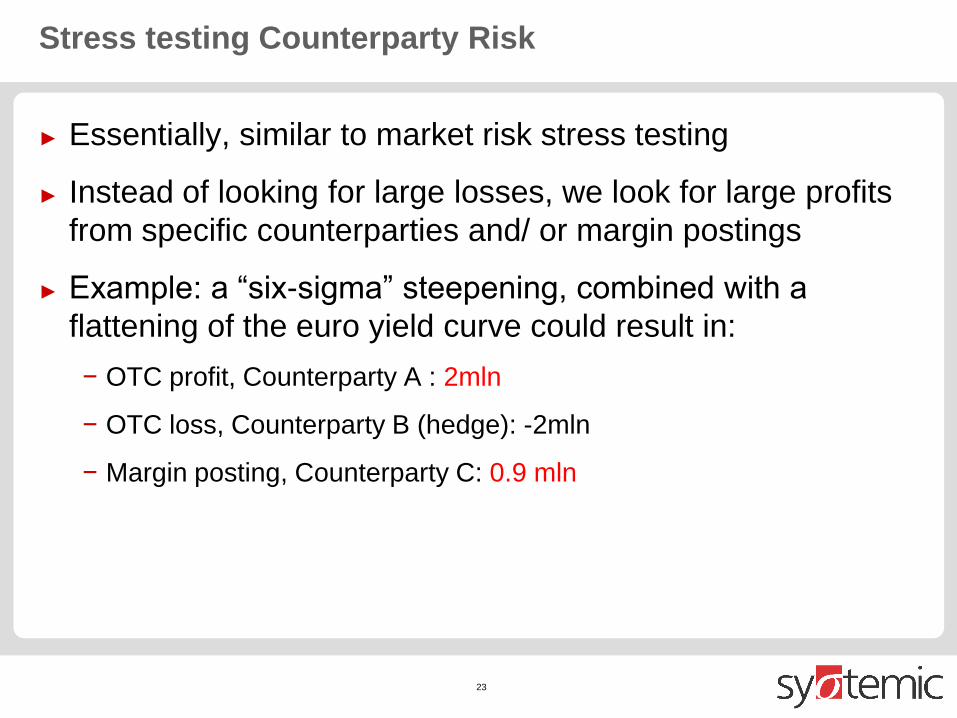

Stress testing Counterparty Risk

► Essentially, similar to market risk stress testing

► Instead of looking for large losses, we look for large profits

from specific counterparties and/ or margin postings

► Example: a “six-sigma” steepening, combined with a

flattening of the euro yield curve could result in:

− OTC profit, Counterparty A : 2mln

− OTC loss, Counterparty B (hedge): -2mln

− Margin posting, Counterparty C: 0.9 mln

24

Building a Stress Testing Framework

25

But: Stress tests are subjective!

► Euromoney 31/3/11 (criticizing the latest EU stress test)

− “Sure the economic scenario seems mostly fairly severe [but] the

. Equity prices are

assumed to fall by 15%; the DAX has just fallen 12.5% in three

weeks. Valuation haircuts on sovereign bonds are very small,

especially at the front end where banks hold much of their

exposure.”

− “Private tests would allow for much sterner stress scenarios to be

examined, perhaps involving multiple sovereign government

defaults. That would at least allow banks and regulators to

and overall balance

sheets in such a calamity. It wouldn’t necessarily matter if most

banks failed such private tests, because regulators might in turn

attach an .”

26

The problem with stress testing is…

► In traditional stress testing we don’t know the likelihood of

the scenario happening. There is no probability attached to

it.

► However, scope can be too vague: Framework required:

− what do I need to stress? combinations?

− by how much?

► Limited research guidelines compared to pricing, VaR etc.

27

Stress framework: Additional considerations…

► Different scenarios (idiosyncratic, market wide…)

► Multiple severity levels in each scenario

► Time dimension (Dynamic vs. Static)

► Different changes to different asset classes

28

Stress scenario construction

► Historical changes (absolute/ relative)

− Missing instruments: Beta model

− Missing Risk Factors: Behavior model

► Predictive:

− set a few RF changes => behavior model for the rest

► User-defined

− Dependency structure assumptions??

29

Reverse Stress Testing

► Algorithmic search for scenarios leading to intolerable loss

► Tool to facilitate brainstorming by stress testing committee

► The scenario is not fixed in advance. However Likelihood of

occurrence to such a scenario can still only be judgmentally

assessed!

► Scenarios need to respect correlation assumptions.

30

Conclusions

► Stress testing is a diagnostic tool to better understand your

institution’s risk profile

► It incorporates the insight of experienced managers

► It contains forward-looking elements

► It should trigger debates within your organization as to the

possibility of an unwanted situation and the acceptance of

its consequences

► Risk Management is by no means a mechanical exercise!

31

Thank you!

► Contact me any time

− www.twitter.com/ariproto

► Systemic in Social Media

− www.systemic-rm.com/linkedin

− www.twitter.com/SystemicRM (risk news)

− www.facebook.com/SystemicRM