Embed Size (px)

Citation preview

Overview of the Oxford MT Model

Oxford Global Macro Model

Oxford Global Sectoral Model

Global Machine Tools Model

Forecasts for major macroeconomic indicators across 175 economies:

• GDP

• Industrial production

• Investment

• Interest rates

• Exchange rate

• Inflation and costs

• Competitiveness

• Profitability

Forecasts for output across 85 sectors in 67 countries driven by:

• Mix of demand – ie consumption vs investment

• Inter-sector supply chain linkages – ‘input-output modelling’

• Sectoral competitiveness

Forecasts investment by sector, based on sectoral output growth and capacity utilisation, and macro drivers, such as interest rates and profits

Sectoral output and investment forecasts in key client sectors are then used to drive the global forecast for machine tools sales

Countries covered

Americas

Brazil Canada Mexico United States

Asia

China India Japan South Korea Taiwan Thailand

Europe

Austria Czech Rep France Germany Hungary Italy Poland

Russia Slovakia SpainSwitzerland UK Turkey

Three key points

There is still a very high level of uncertainty about the outlook especially in the US and Europe: ie FEAR still rules

Bernanke on uncertainty

Statement to Senate Banking Committee, 22 July:

"Even as the Federal Reserve continues prudent planning for the ultimate withdrawal of monetary policy accommodation, we also recognise that the economic outlook remains unusually uncertain.“

Keynote speech at Jackson Hole, Wyoming, 27 August:

“…macroeconomic projections are inherently uncertain, and the economy remains vulnerable to unexpected developments.”

OXFORD ECONOMICS FORECASTING RECORD

2007-2009(average absolute forecast divergence

for real GDP growth)

USA Eurozone Japan

OEF 0.7 1.4 2.0

Note: Forecasts made in December for year ahead.

OXFORD ECONOMICS FORECASTING RECORD

2007-2009(average absolute forecast divergence

for real GDP growth)

USA Eurozone Japan

OEF 0.7 1.4 2.0

EIU

Global Ins.

IMF

OECD

Consens.

Note: Forecasts made in December for year ahead.

OXFORD ECONOMICS FORECASTING RECORD

2007-2009(average absolute forecast divergence

for real GDP growth)

USA Eurozone Japan

OEF 0.7 1.4 2.0

EIU 1.0

Global Ins. 0.7

IMF 1.6

OECD 1.1

Consens. 1.0

Note: Forecasts made in December for year ahead.

OXFORD ECONOMICS FORECASTING RECORD

2007-2009(average absolute forecast divergence

for real GDP growth)

USA Eurozone Japan

OEF 0.7 1.4 2.0

EIU 1.0 2.2 2.6

Global Ins. 0.7 1.7 2.4

IMF 1.6 2.2 2.9

OECD 1.1 1.8 2.7

Consens. 1.0 1.8 2.4

Note: Forecasts made in December for year ahead.

Three key points

There is still a very high level of uncertainty about the outlook especially in the US and Europe: ie FEAR still rules

Crisis has been in part a story of two currency unions!!

The imbalances story times two

US running current account deficit of over $450billion

China running current account surplus of over $300 billion

Intervention by central bank leading to reserves rising on average by over $300 billion per annum in last five years

No sign of any change in next few years?

The imbalances story times two

US running current account deficit of over $450billion

China running current account surplus of over $300 billion

Intervention by central bank leading to reserves rising on average by over $300 billion per annum in last five years

No sign of any change in next few years?

France, PIGS current account deficit of over $300 billion

Germany Netherlands current account surplus of $250 billion

Banks were lending to Greek government, Spanish companies and Irish banks as offset to the above imbalances

ECB/EU governments will now fill the gap?

…Yuan is expected to slowly appreciate against $

0

2

4

6

8

10

12

14

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

4

5

6

7

8

9

US$

Loans interest rate(LHS)

Exchange rate(RHS)

Source: Oxford Economics

F'cast

China: Exchange and interest rates%

Worrying that trade imbalances widening again

-1000

-800

-600

-400

-200

0

200

400

600

1990 1994 1998 2002 2006 2010Source: Oxford Economics

$ billion

US

Japan

World: Current account imbalances

EU

Forecast

China

OPEC

Three key points

There is still a very high level of uncertainty about the outlook especially in the US and Europe: ie FEAR still rules

Crisis has been in part a story of two currency unions!!

The recession was driven by the corporate sector and the shape of the recovery will depend on how corporates react in different countries

40

50

60

70

80

90

100

110

120

130

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

US: Sectoral indebtedness% of GDP

Source : Oxford Economics/Haver Analytics

Consumer

Non financial business

Domestic financial sector

The recession wasn’t consumer driven in US…

90

92

94

96

98

100

102

104

106

108

-6 -5 -4 -3 -2 -1 0 1 2 3 4

US : Consumer spendingtrough=100

Source : Oxford Economics

1980Q3

1982Q4

1975Q1

1991Q1

Periods from trough

2009Q2

2001Q4

Nor were bank job cuts as bad as feared

-7

-6

-5

-4

-3

-2

-1

0

1

US Japan UK Germany France Italy

GovernmentOther servicesFinance/businessIndustryConstructionAgriculture

Sectoral contribution to employment lossesContribution to peak-to-trough change in employment, % pts

Source : Oxford Economics/Haver Analytics

Sharp decline in investment for the US

…and globally, then magnified through trade

95

97

99

101

103

105

107

109

111

113

115

Q-5 Q-4 Q-3 Q-2 Q-1 Q0 Q1 Q2 Q3 Q4 Q5

100= GDP trough

Source: Oxford Economics

Germany: Investment recoveries compared

2008-10

Early 1970s

Early 1990s

Early 1980s

So corporates are now cash rich

-5

-4

-3

-2

-1

0

1

2

3

4

5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Oxford Economics\Haver Analytics

World: PNFC financial balances

US

Eurozone

UK

% of GDP, 4-quarter average

And also in China

20

25

30

35

40

45

50

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

Source: Oxford Economics

% of GDP

China : Corporate profits

Who will lead the recovery?

Governments!!

Consumers!!

Companies?

Emerging markets?

…households constrained by debt…

0

50

100

150

200

250

1995 1997 1999 2001 2003 2005 2007 2009

Household debt% of income

Source : Oxford Economics

US

UK

Eurozone

Germany

Ireland

SpainEurozone

…the weak labour market…

3

4

5

6

7

8

9

10

11

12

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

World: Unemployment%

Source : Oxford Economics

France

Eurozone

GermanyUK

US

Forecast

…and squeeze on real wages as well as higher taxes

-2

-1

0

1

2

3

4

5

6

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Real wagesAnnual % change

Source : Oxford Economics

US

UK

Eurozone

Forecast

So consumers will lag rather than lead recovery

…non-financials all cash rich

-10

-5

0

5

10

15

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010Source: Oxford Economics

% of GDP, 4QMA

Non financial corporate balance

France

US

UK

Germany

Japan

Corporate surpluses normally get spent in US…

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

1971 1975 1979 1983 1987 1991 1995 1999 2003 2007

US: Investment and corporate money% year

Source : Oxford Economics/Haver Analytics

Real corporate broad money

Non-residential investment

…and elsewhere

-30

-20

-10

0

10

20

30

40

50

1970 1976 1982 1988 1994 2000 2006

UK: Corporate liquidity and investment% year

Source : Oxford Economics/Haver Analytics

Business Investment

Real PNFC M4

We are seeing some recovery in M&A

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1996 1998 2000 2002 2004 2006 2008 2010Jan-Jul

ann.

World: M&AUS$ bn

Source : Dealogic/Thomson Reuters

What might hold companies back this time?

Unusual uncertainty

Excess capacity

Debt

Credit constraints

What might hold companies back this time?

Unusual uncertainty

Excess capacity

Debt

Credit constraints

Excess capacity holding back investment

65

70

75

80

85

90

1995 1997 1999 2001 2003 2005 2007 2009

-20

-15

-10

-5

0

5

10

15

% point

Source: Oxford Economics, Haver Analytics

Low capacity discourages new investment

Capacity utilisation

(LHS)

Non residential investment

(RHS)

% year

Eurozone: Capacity utilisation and real non-residential investment

US: Capacity utilisation and real non-residential investment

What might hold companies back this time?

Unusual uncertainty

Excess capacity

Debt

Credit constraints

Companies seeking to pay down debt

What might hold companies back this time?

Unusual uncertainty

Excess capacity

Debt

Credit constraints

Corporate lending very weak…

-24

-20

-16

-12

-8

-4

0

4

8

12

16

20

24

28

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

% year

UK

Source: Haver Analytics

World: Lending to PNFCs*

Eurozone

US

*3 month moving average

…although that is a demand as well as supply issue

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

2007 2008 2009 2010

World: Firms' demand for credit for investment% net balance

Source : Oxford Economics/Haver Analytics

US

Eurozone

UK

Forecast takes a hopeful view on investment

But still subdued recovery for major economies

Emerging markets leading recovery?

Emergers leading recovery despite slowing in some

-20

-15

-10

-5

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010

% year

Source: Haver Analytics

BRICS: Industrial production

3 month moving average

Brazil

Russia

China

India

Emerging markets leading recovery?

Export markets slowing

But domestic demand is strong

… domestic demand generally solid

-12

-8

-4

0

4

8

12

16

20

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

% year

Brazil

Source: Haver Analytics

Brazil, Russia & China: Retail sales volumes

RussiaChina

3 month moving average

…and domestic demand is solid in the rest of Asia

-6

-3

0

3

6

9

12

15

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

% year

Source: Haver Analytics

Emerging Asia: Consumer spending

Malaysia

Taiwan

Thailand

Korea

Emerging markets leading recovery?

Export markets slowing

But domestic demand is strong

Still scope for further stimulus

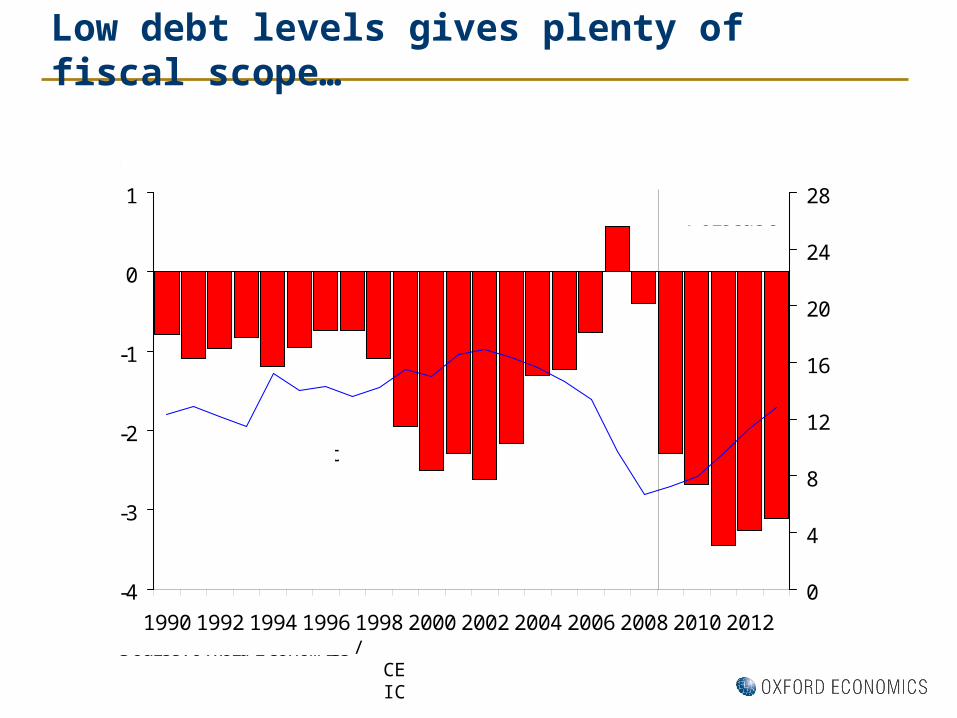

Low debt levels gives plenty of fiscal scope…

-4

-3

-2

-1

0

1

0

4

8

12

16

20

24

28

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

% of GDP

Government balance(LHS)

Government debt(RHS)

% of GDP

Source: Oxford Economics

Forecast

China: Government budget balance and debt

/CEIC

…and credit taps can turn on quickly if needed…

0

4

8

12

16

20

24

28

32

36

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

12-month % change

Source: Haver Analytics

China: Total RMB loans

CEIC

…and are already flowing in Brazil

-10

-5

0

5

10

15

20

25

30

35

40

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

% year

Source: Haver Analytics

Brazil: Bank lending

Industry & commerce sectors

Total private sector

…& capacity utilisation is high in several emergers

70

75

80

85

90

95

100

105

110

115

1995 1997 1999 2001 2003 2005 2007 2009

2005=100 (seasonally adjusted)

Source: Haver Analytics

Korea: Manufacturing operating rate

Oxford Economics/CEIC

Oxford Economics’ forecast

2008 2009 2010 2011 2012 2013US 0.0 -2.6 2.6 2.5 3.5 3.8

Japan -1.2 -5.2 2.6 1.1 2.1 2.0

Eurozone 0.3 -4.0 1.5 1.3 1.7 2.0

of which:

Germany 0.7 -4.7 3.1 1.8 1.7 2.0

France 0.1 -2.5 1.5 1.6 2.0 2.1

Italy -1.3 -5.1 0.9 1.0 1.2 1.4

UK -0.1 -5.0 1.6 2.0 2.7 3.2

China 9.6 9.1 9.7 9.0 9.2 8.8

India 7.4 6.7 8.2 8.3 9.0 8.8

Other Asia 4.0 2.0 6.6 5.4 6.2 6.0

Mexico 1.5 -6.6 4.7 4.5 5.4 4.8

Brazil 5.2 -0.2 7.3 4.5 5.1 4.6

Other Latin America 4.8 -0.6 4.5 4.0 4.7 4.3

Eastern Europe 4.8 -5.6 3.1 3.7 5.3 5.5

MENA 4.7 1.8 7.0 7.4 7.0 6.6

World 1.4 -2.0 3.6 3.3 4.0 4.2

World (PPP) 2.8 -0.7 4.5 4.2 4.9 5.0

World GDP Growth% Change on Previous Year

Co

rpo

rate

rec

ove

ry

Financial sector recovery

Outlook still highly uncertain

Co

rpo

rate

rec

ove

ry

Financial sector recovery

Outlook still highly uncertain

Oxford forecast■ Gradual rise in business confidence

encourages corporates to invest ■ But weak banks combined with excess

capacity limit scale of investment recovery

■ Consumer spending recovery limited by pace of job growth and fiscal retrenchment

■ But recovery strong enough that fiscal crisis remains contained

Co

rpo

rate

rec

ove

ry

Financial sector recovery

Outlook still highly uncertain

Renewed global boom■ Strong corporate liquidity feeds into new

investment boom■ Faster growth boosts business and

consumer confidence, and trade multiplier magnifies upturn

■ Bank balance sheets improve quickly and credit growth resumes

■ Strong growth boosts tax revenues/cuts social security payments, helping fiscal consolidation

Oxford forecast■ Gradual rise in business confidence

encourages corporates to invest ■ But weak banks combined with excess

capacity limit scale of investment recovery

■ Consumer spending recovery limited by pace of job growth and fiscal retrenchment

■ But recovery strong enough that fiscal crisis remains contained

Co

rpo

rate

rec

ove

ry

Sub-par recovery■ Business optimism remains low and

corporates continue to hoard cash■ Investment and job growth is modest as

capacity is underutilised■ Monetary policy supports banking sector

but fiscal coffers are empty■ Easier credit conditions mean benefits of

loose monetary policy feeds through to a stronger housing and consumer recovery

Financial sector recovery

Outlook still highly uncertain

Renewed global boom■ Strong corporate liquidity feeds into new

investment boom■ Faster growth boosts business and

consumer confidence, and trade multiplier magnifies upturn

■ Bank balance sheets improve quickly and credit growth resumes

■ Strong growth boosts tax revenues/cuts social security payments, helping fiscal consolidation

Oxford forecast■ Gradual rise in business confidence

encourages corporates to invest ■ But weak banks combined with excess

capacity limit scale of investment recovery

■ Consumer spending recovery limited by pace of job growth and fiscal retrenchment

■ But recovery strong enough that fiscal crisis remains contained

Corporates are key

200

250

300

350

400

450

500

550

600

650

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Base

Renewed boom

Sub-par recovery

Source: Oxford Economics

$2005 billions

US: Business investment

Scenarios for the global economy

2009 2010 2011 2012

Oxford Forecast (45%)US -2.6 2.6 2.5 3.5Eurozone -4.0 1.5 1.3 1.7China 9.1 9.7 9.0 9.2World -0.7 4.5 4.2 4.9

Renewed boom (20%)US -2.6 2.8 3.7 4.2Eurozone -4.0 1.7 2.4 2.8China 9.1 10.4 10.7 10.4World -0.7 4.8 5.5 5.9

Sub-par recovery (25%)US -2.6 2.4 1.8 2.2Eurozone -4.0 1.2 0.8 0.9China 9.1 8.8 7.2 7.5World -0.7 4.1 3.3 3.7

Alternative GDP growth forecasts

Co

rpo

rate

rec

ove

ry

Sub-par recovery■ Business optimism remains low and

corporates continue to hoard cash■ Investment and job growth is modest as

capacity is underutilised■ Monetary policy supports banking sector

but fiscal coffers are empty■ Easier credit conditions mean benefits of

loose monetary policy feeds through to a stronger housing and consumer recovery

Financial sector recovery

Outlook still highly uncertain

Renewed global boom■ Strong corporate liquidity feeds into new

investment boom■ Faster growth boosts business and

consumer confidence, and trade multiplier magnifies upturn

■ Bank balance sheets improve quickly and credit growth resumes

■ Strong growth boosts tax revenues/cuts social security payments, helping fiscal consolidation

Oxford forecast■ Gradual rise in business confidence

encourages corporates to invest ■ But weak banks combined with excess

capacity limit scale of investment recovery

■ Consumer spending recovery limited by pace of job growth and fiscal retrenchment

■ But recovery strong enough that fiscal crisis remains contained

Co

rpo

rate

rec

ove

ry

Renewed crisis■ Threat of double-dip means renewed

slump in asset prices as Eurozone sovereign debt crisis re-emerges

■ Pressure to cut budget deficits rapidly in all major economies

■ Rising unemployment and business failures feed back into banking

■ Limited scope for monetary policy offset

Sub-par recovery■ Business optimism remains low and

corporates continue to hoard cash■ Investment and job growth is modest as

capacity is underutilised■ Monetary policy supports banking sector

but fiscal coffers are empty■ Easier credit conditions mean benefits of

loose monetary policy feeds through to a stronger housing and consumer recovery

Financial sector recovery

Outlook still highly uncertain

Renewed global boom■ Strong corporate liquidity feeds into new

investment boom■ Faster growth boosts business and

consumer confidence, and trade multiplier magnifies upturn

■ Bank balance sheets improve quickly and credit growth resumes

■ Strong growth boosts tax revenues/cuts social security payments, helping fiscal consolidation

Oxford forecast■ Gradual rise in business confidence

encourages corporates to invest ■ But weak banks combined with excess

capacity limit scale of investment recovery

■ Consumer spending recovery limited by pace of job growth and fiscal retrenchment

■ But recovery strong enough that fiscal crisis remains contained

Industrial outlook

-30

-20

-10

0

10

20

30

MotorVehicles

MetalProducts

Aerospace Mechengineering

Comp &electronics

Elec equip Consumergoods

Intermediategoods

2009 2010

2011 2012

Source: Oxford Economics

Growth in industrial production of machine tools' customer sectors

…

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

1980 1984 1988 1992 1996 2000 2004 2008

3mth mav, mn

Production

Sales

Source: J D Power/Oxford Economics

Unit car sales & production†

† Covering the US, Western Europe & Japan

Aerospace orders now below deliveries

Investment outlook

200

600

1,000

1,400

1,800

2,200

2,600

3,000

1990 1993 1996 1999 2002 2005 2008

300

400

500

600

700

800

900

1,000

Deliveries(RHS)

Orders(LHS)

No. of aircraftNo. of aircraft

Airbus & Boeing: Orders & deliveries

Source: Company reports and forecasts

Motor Vehicle Investment

Investment outlook

Rest of Asia 13.5%

US8.3%

Germany 9.5%

Rest of Americas

8.5%

Japan 23.4%

China16.2%

Rest of Europe20.7%

Motor vehicle investment 2009

Source : Oxford Economics

-40

-30

-20

-10

0

10

20

30

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013Source: Oxford Economics

Motor vehicle investment

Europe

% yoy

Americas

Asia

General machinery output and investment

Investment outlook

US, 42.9%

Japan, 14.5%

China, 23.2%

Rest of Europe, 8.0%

Rest of Asia, 5.7%

Rest of Americas,

2.0%

Germany, 3.6%

General machinery investment 2009

Source : Oxford Economics

-30

-20

-10

0

10

20

30

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013Source: Oxford Economics

General machinery output

Europe

% yoy

Americas

Asia

Special Purpose Machinery – output and investment

Investment outlook

US, 11.8%

China, 25.0%

Germany, 4.9%

Rest of Americas,

3.1%

Rest of Asia, 15.1%

Japan, 24.9%

Rest of Europe, 15.1%

Special purpose machinery investment 2009

Source : Oxford Economics

-30

-20

-10

0

10

20

30

40

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013Source: Oxford Economics

Special purpose machinery output

Europe

% yoy

Americas

Asia

Oxford Economics forecast

2009 2010 2011 2012 2013 2014

China -2.6 18.2 15.1 20.1 19.1 17.1Germany -37.4 -12.3 29.9 18.6 13.9 9.9Japan -38.5 3.6 21.5 18.0 9.2 7.2US -52.7 -0.4 36.2 25.5 12.0 10.0Italy -44.3 10.1 11.7 14.6 11.3 11.3Korea -21.0 14.8 21.9 15.4 10.5 8.5Brazil -22.4 17.2 22.7 15.3 15.3 15.3Taiwan -43.0 18.1 22.6 14.1 10.1 8.1India -33.9 15.1 25.7 30.5 22.7 15.7Russia -26.7 4.0 22.5 25.5 15.5 10.5Mexico -20.5 11.2 19.9 15.7 9.7 8.7France -46.6 0.2 19.4 17.1 14.8 9.8Switzerland -44.0 -16.4 20.7 16.1 15.4 11.8Spain -49.9 -15.6 10.4 15.9 16.9 19.9UK -34.0 -19.3 19.7 22.8 15.4 11.4

Americas -44.1 11.1 27.9 20.5 12.5 11.2Asia -15.1 17.9 17.4 19.4 16.8 14.6Europe -44.5 -0.8 21.8 18.2 14.1 11.1World -30.7 11.4 19.9 19.3 15.5 13.2

Machine Tools Sales

% change on previous year

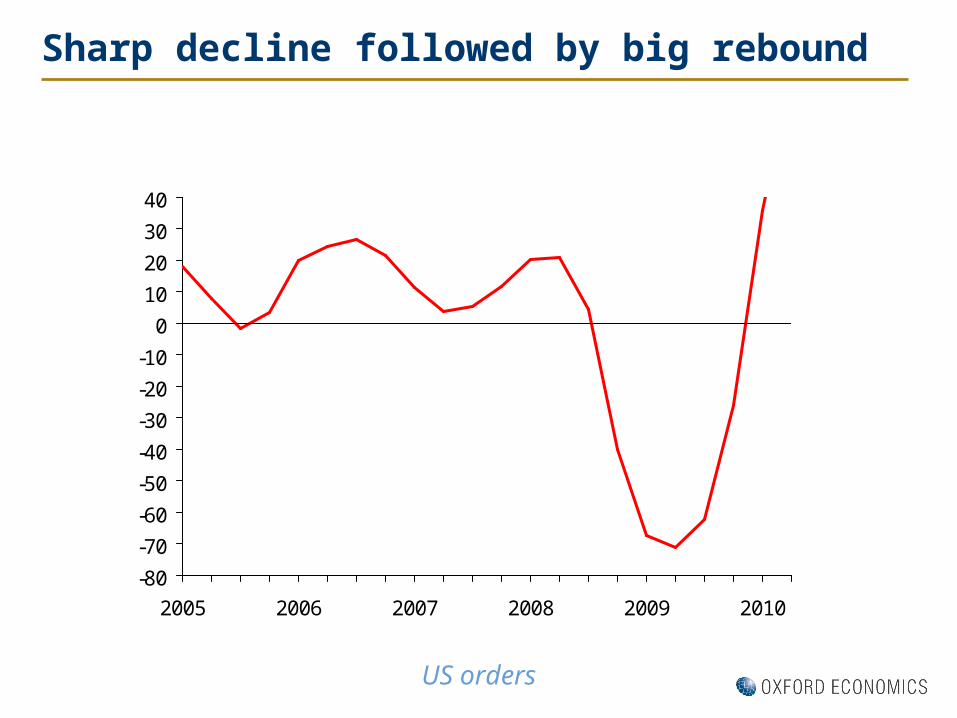

Sharp decline followed by big rebound

US orders

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

2005 2006 2007 2008 2009 2010

US machine tools orders annual growth

% yr

Source : Oxford Economics

Orders growth will slow next year

US orders

-80-70-60-50-40-30-20-10

0102030405060708090

2005 2006 2007 2008 2009 2010 2011

US machine tools orders annual growth

% yr

Source : Oxford Economics

Forecast

Quarterly USMTC orders forecast…

US orders

0.025

0.045

0.065

0.085

0.105

0.125

0.145

2004 2005 2006 2007 2008 2009 2010 2011

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2Forming machine tools, $bn Cutting machine tools, $bn

Forming machine tools (LHS)

Cutting machine tools (RHS)

US metalworking machine tools orders, USMTC

Forecast

Source : Oxford Economics

General regional rebound in 2010

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

2009 2010 2011

TotalNortheastSouthMidwestCentralWest

Source: Oxford Economics

Growth in value of orders for cutting machines by region

Very different story with forming orders

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2009 2010 2011

TotalNortheastSouthMidwestCentralWest

Source: Oxford Economics

Growth in value of orders for forming machines by region

Conclusions

Policy stimulus, turn in inventory cycle and rebound in world trade drove strong recovery

Global economic recovery should continue but there are growing downside risks

Machine tool orders up sharply from lows. Sales have so far been more subdued but these should now start to pick up.

MT sales are forecast to rebound sharply over the next few years in both developed and emerging markets

Strong rebound in developed economy markets follows very deep recession but focus of global MT market still increasingly moving toward emerging economies

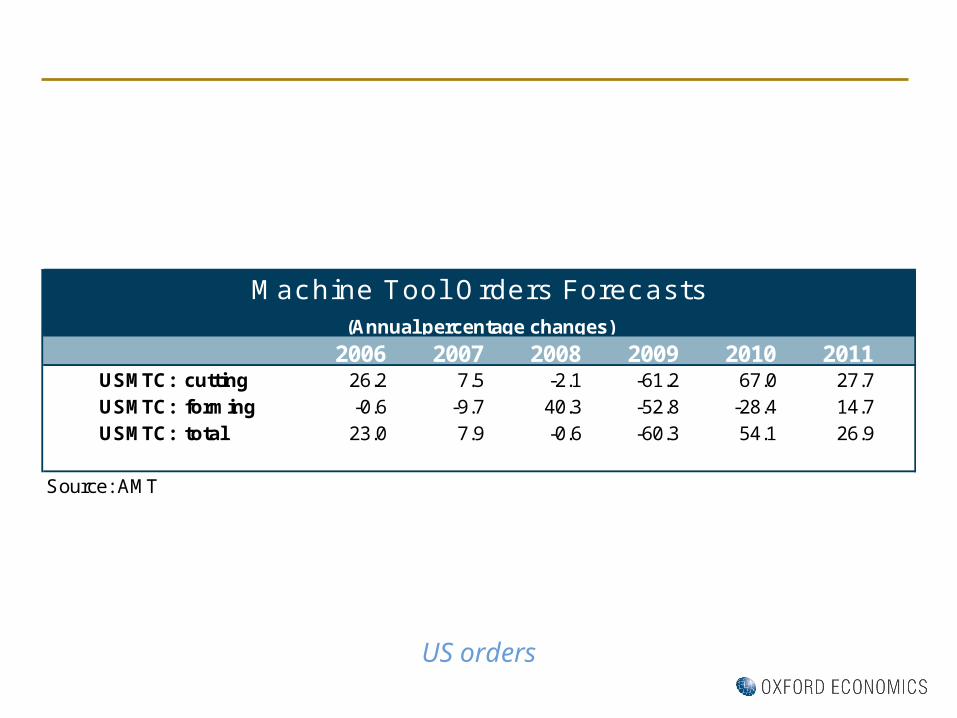

US orders

2006 2007 2008 2009 2010 2011USMTC: cutting 26.2 7.5 -2.1 -61.2 67.0 27.7USMTC: forming -0.6 -9.7 40.3 -52.8 -28.4 14.7USMTC: total 23.0 7.9 -0.6 -60.3 54.1 26.9

Source: AMT

Machine Tool Orders Forecasts(Annual percentage changes)