Embed Size (px)

Citation preview

Islamic Financial Institutions Course

International Program on Islamic Economic and Finance

Term II/2010

Lecturer: Sartini, S.E., M.Sc.Acc., Ak

First Week Discussion

Learning Contract Introduction to Islamic Financial

Institution Discussion

Learning Contract

About the Lecturer Overview of the Subject Learning Objectives Learning Methods Assessment References

About the Lecturer Name: Sartini, S.E., M.Sc.Acc., Ak Website: www.sartini.wordpress.com Phone: 0274-783 6898 Email: [email protected] Address: Griya Suryo Asri II No. A4 RW:9

Suryodiningratan MJ II Yogyakarta Consultation Hours: By appointment only

Overview of the Subject This subject focuses on the discussion of Islamic

Financial Institutions, one of some subgroups of Islamic Financial System. The IFIs included in this discussions are IFIs banks such as Islamic commercial bank and BPRS; as well as IFIs non-banks such as Islamic leasing, Islamic insurance, BMT, Rahn, Islamic Capital Market and Islamic Fund Manager.

Although IFIs will be the main topic to be discussed in this subject, it will also discuss topics related to the other Islamic Financial System subgroups, including: Islamic Financial Instruments Islamic Financial Rules and Regulations Islamic Financial Control and Supervision

Another related topic that will also be discussed is topic on Islamic Public Institutions such as Zakat institution and Wakaf Institution

Learning Objectives

This subject aims to provide student, an understanding of :

The important of Islamic financial system, The Islamic Financial Instruments, The operation of Islamic Financial

Institutions, The Islamic financial rules and regulations, The mechanisms of Islamic financial

controls and supervisions Islamic Public Institutions

Learning Methods

Tutorial Presentation and Discussion

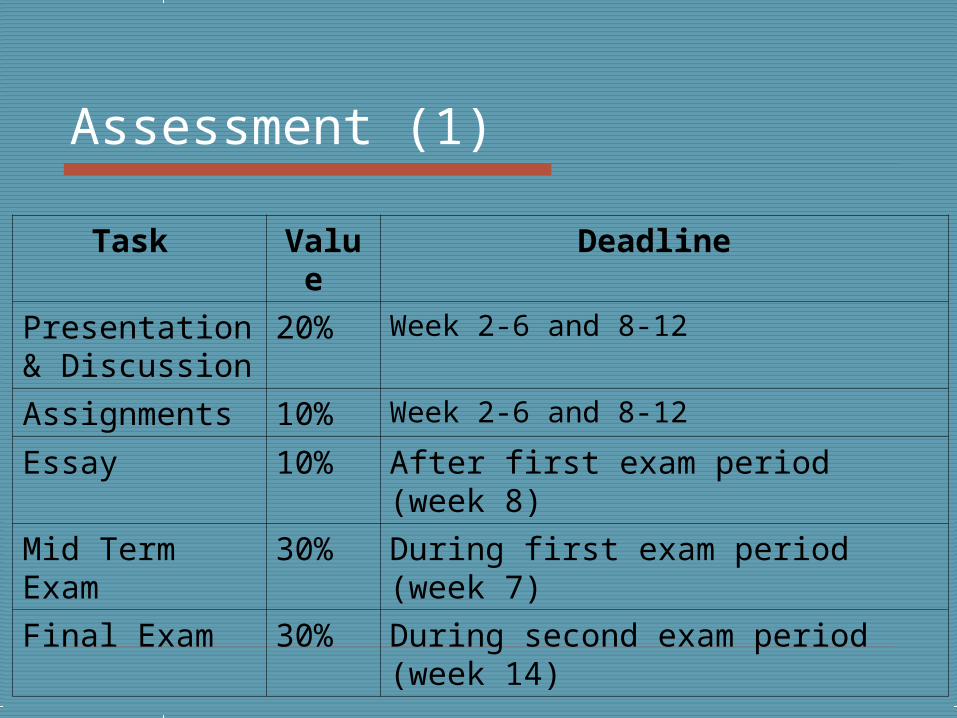

Assessment (1)

Task Value Deadline

Presentation & Discussion

20% Week 2-6 and 8-12

Assignments 10% Week 2-6 and 8-12

Essay 10% After first exam period (week 8)

Mid Term Exam 30% During first exam period (week 7)

Final Exam 30% During second exam period (week 14)

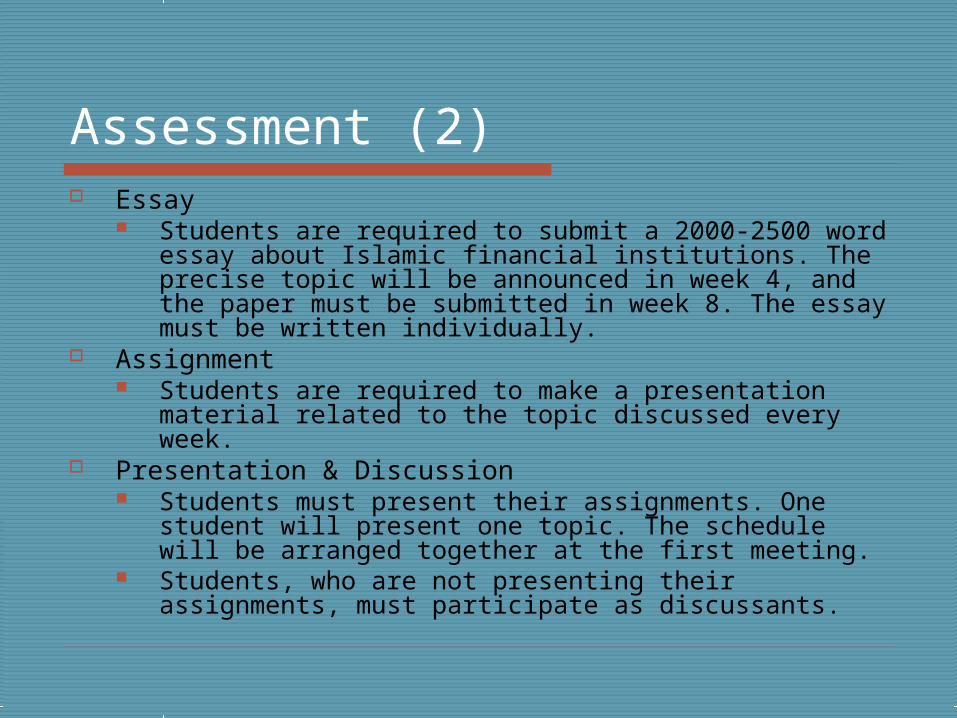

Assessment (2) Essay

Students are required to submit a 2000-2500 word essay about Islamic financial institutions. The precise topic will be announced in week 4, and the paper must be submitted in week 8. The essay must be written individually.

Assignment Students are required to make a presentation

material related to the topic discussed every week. Presentation & Discussion

Students must present their assignments. One student will present one topic. The schedule will be arranged together at the first meeting.

Students, who are not presenting their assignments, must participate as discussants.

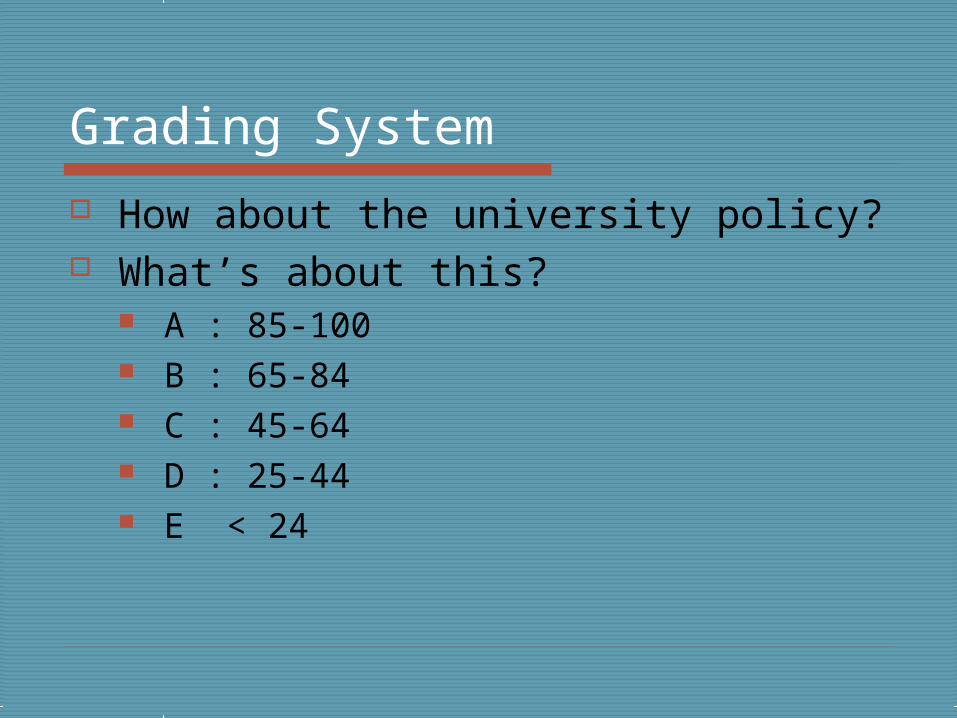

Grading System

How about the university policy? What’s about this?

A : 85-100 B : 65-84 C : 45-64 D : 25-44 E < 24

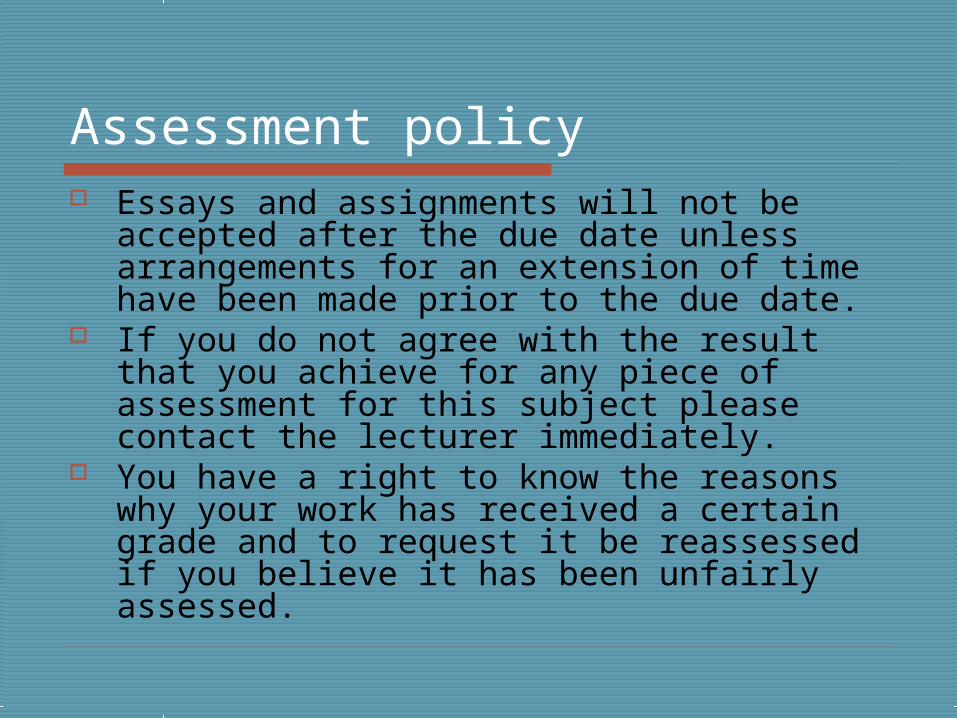

Assessment policy Essays and assignments will not be

accepted after the due date unless arrangements for an extension of time have been made prior to the due date.

If you do not agree with the result that you achieve for any piece of assessment for this subject please contact the lecturer immediately.

You have a right to know the reasons why your work has received a certain grade and to request it be reassessed if you believe it has been unfairly assessed.

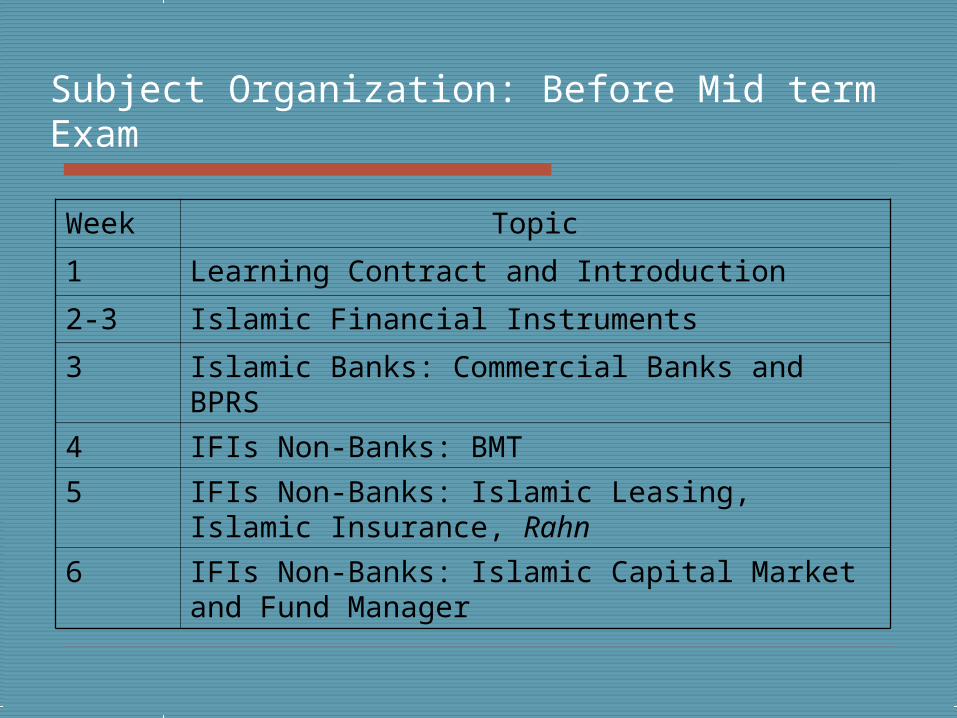

Subject Organization: Before Mid term Exam

Week Topic

1 Learning Contract and Introduction

2-3 Islamic Financial Instruments

3 Islamic Banks: Commercial Banks and BPRS

4 IFIs Non-Banks: BMT

5 IFIs Non-Banks: Islamic Leasing, Islamic Insurance, Rahn

6 IFIs Non-Banks: Islamic Capital Market and Fund Manager

Subject Organization: After Mid term Exam

Week Topic

8 Islamic Financial Rules and Regulations

9 Islamic Financial Controls an Supervisions

10 Islamic Public Institutions: Zakat Institution

11 Islamic Public Institutions: Wakaf Institution

12 Lesson from some IFIs and IPIs

13 Overview and RefreshmentFarewell Speeches

Introduction

The Need for This Subject

Background and Rationales Since the mid 20th century, there has been a

serious effort within Muslim societies to comply fully to the Islamic tenets in daily life.

This includes the application of Islamic economic teachings, as discussed in various verses of the holy Qur’an, in the ahadith, as well as exemplified in the real life of prophet Muhammad and his companions.

The real example of this effort can be seen in the establishment of Islamic financial institutions such as banks, insurance companies, capital markets, mutual funds and so forth, both in Muslim and non-Muslim countries.

Background & Rationales The proliferation of growth in the Islamic banking sector,

both nationally and internationally, has been remarkable. Islamic banks now stand side by side with their conventional counterparts in more than 150 countries worldwide.

Islamic Banking and Finance has become an important academic discipline and has attracted research in a number related areas such as the economics, finance, accounting, law, Syari’ah and others.

Demand for Islamic Banking and financial instruments as well as Islamic financial institutions have experienced a rapid growth internationally.

As an important financial activity in the Muslim world, knowledge and expertise in this discipline is very valuable, not only to the Islamic banks and financial institutions, but also to the Muslim world in ensuring sufficient number of experts and knowledgeable workers in this area

Scenario Patricia Aburdene (2007) in Megatrend 2010

The Power of Spiritualism Spirituality in Business

One of The Indonesian National Agendas President SBY Speech

Opening of Shariah Economic Festival http://www.indonesia.go.id/id/index2.php?option=com_content&do_pdf=1&id=6624

Budget BI for Economic Shariah Development (8 x Rp 1,3)Direktorat Perbankan Syariah BI (Dr. Mulya Siregar)

Overview of Islamic Economic

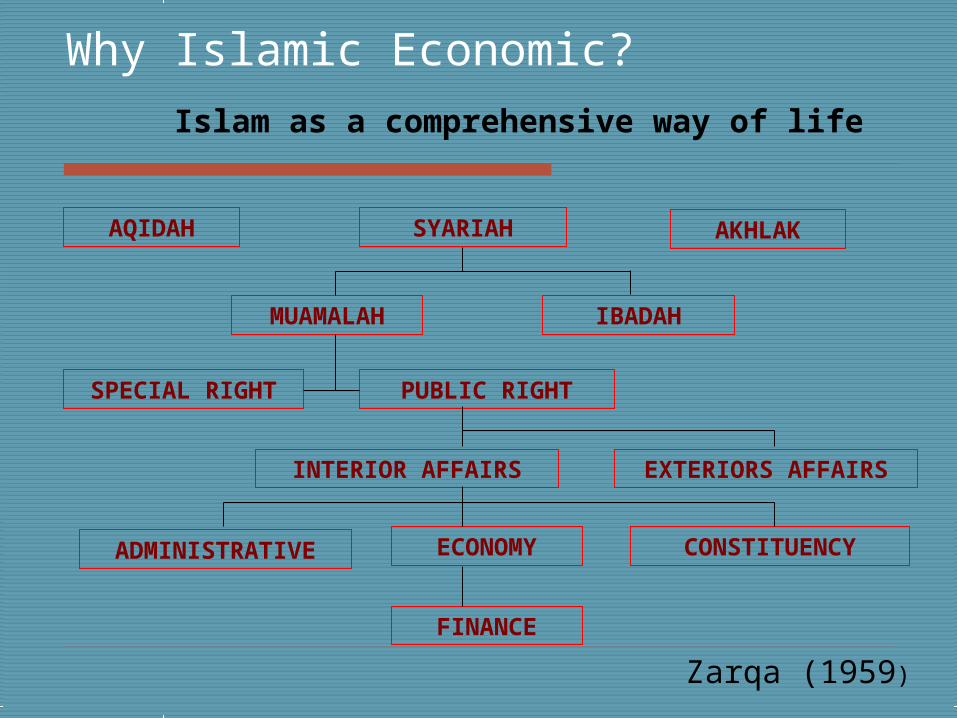

Why Islamic Economic?

Islam as a comprehensive way of life

AQIDAH SYARIAH AKHLAK

MUAMALAH IBADAH

SPECIAL RIGHT PUBLIC RIGHT

INTERIOR AFFAIRS EXTERIORS AFFAIRS

ADMINISTRATIVE ECONOMY CONSTITUENCY

FINANCE

Zarqa (1959)

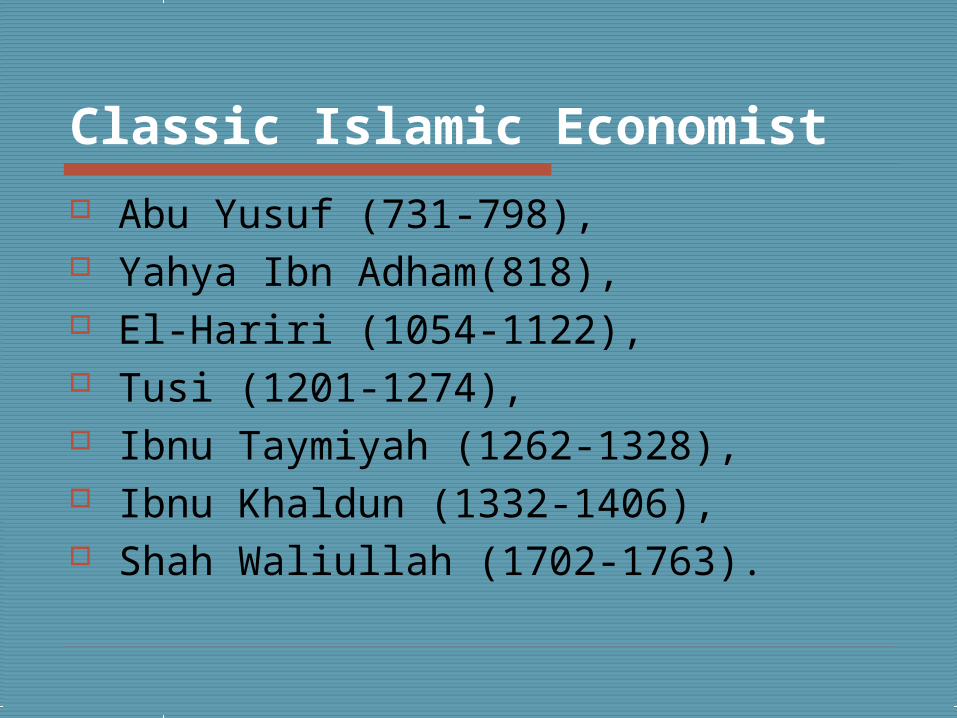

Classic Islamic Economist

Abu Yusuf (731-798), Yahya Ibn Adham(818), El-Hariri (1054-1122), Tusi (1201-1274), Ibnu Taymiyah (1262-1328), Ibnu Khaldun (1332-1406), Shah Waliullah (1702-1763).

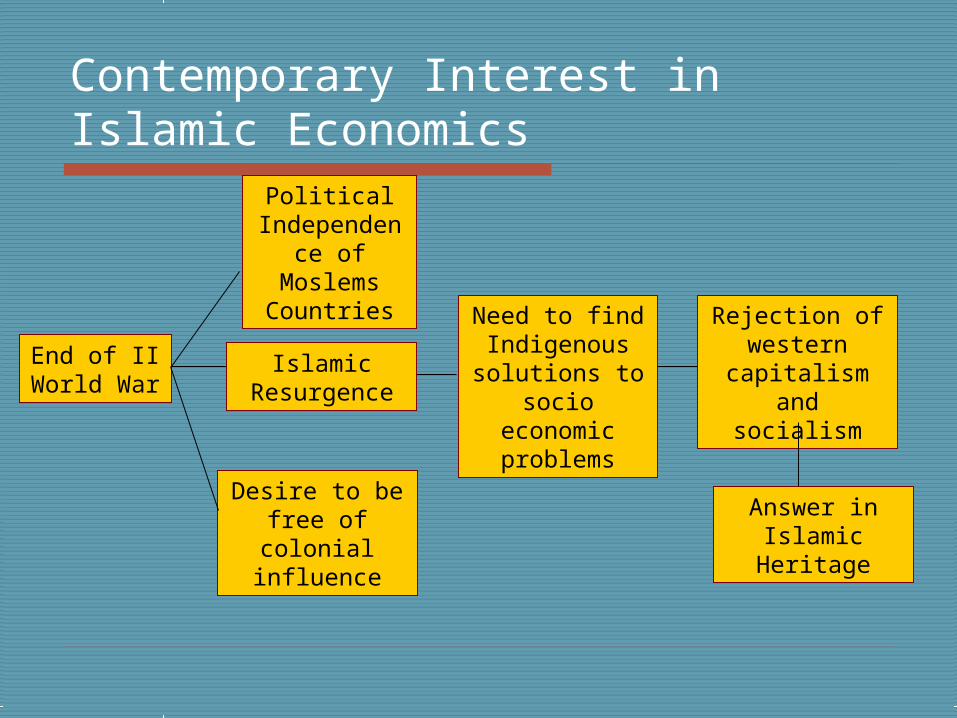

Contemporary Interest in Islamic Economics

End of II World War

Political Independence

of Moslems Countries

Islamic Resurgence

Desire to be free of colonial influence

Need to find Indigenous solutions to

socio economic problems

Rejection of western

capitalism and socialism

Answer in Islamic Heritage

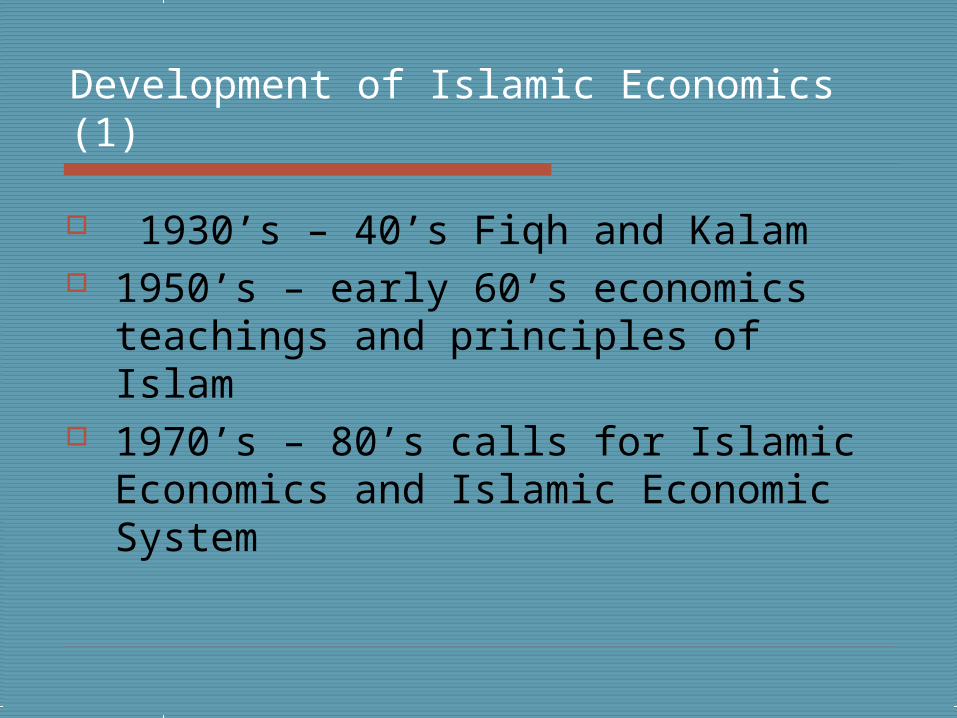

Development of Islamic Economics (1)

1930’s – 40’s Fiqh and Kalam 1950’s – early 60’s economics

teachings and principles of Islam 1970’s – 80’s calls for Islamic

Economics and Islamic Economic System

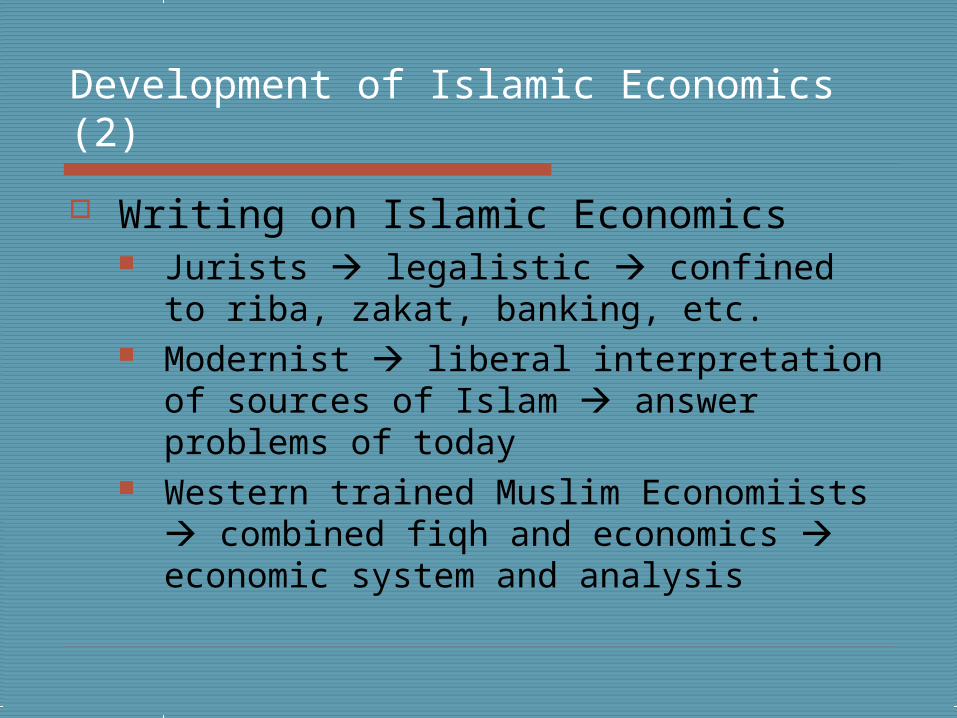

Development of Islamic Economics (2)

Writing on Islamic Economics Jurists legalistic confined to riba,

zakat, banking, etc. Modernist liberal interpretation of

sources of Islam answer problems of today

Western trained Muslim Economiists combined fiqh and economics economic system and analysis

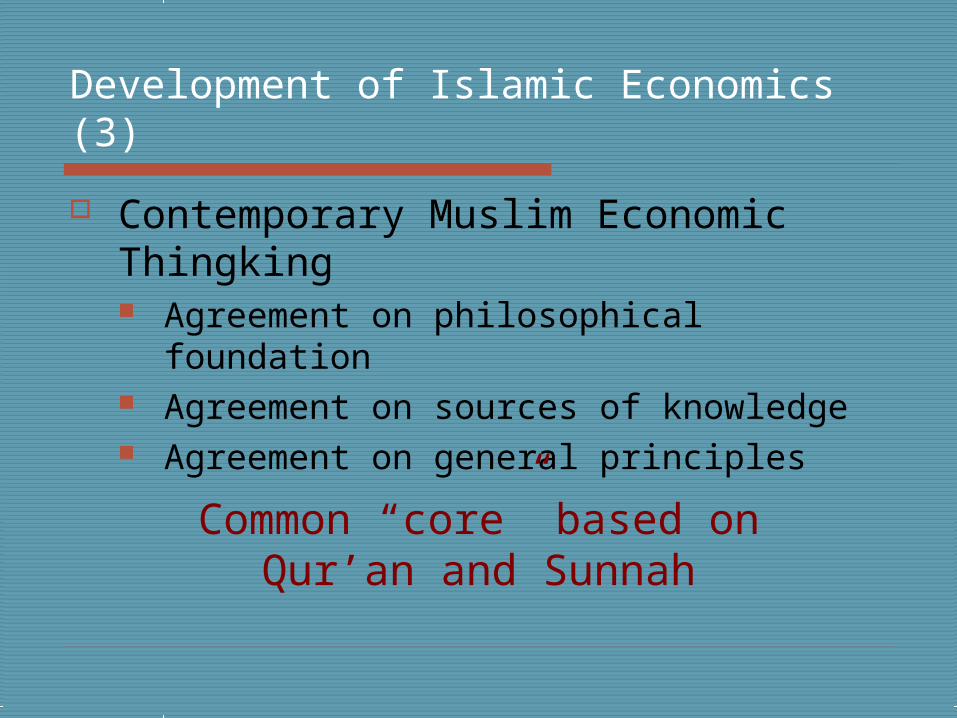

Development of Islamic Economics (3)

Contemporary Muslim Economic Thingking Agreement on philosophical foundation Agreement on sources of knowledge Agreement on general principles

Common “core” based on Qur’an and Sunnah

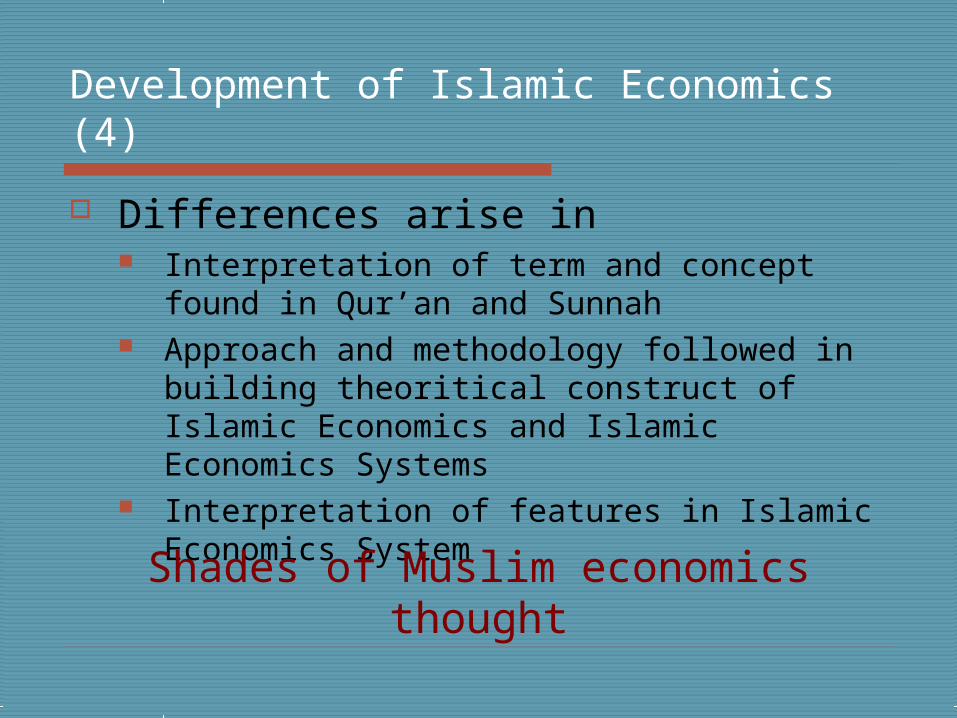

Development of Islamic Economics (4)

Differences arise in Interpretation of term and concept found in

Qur’an and Sunnah Approach and methodology followed in

building theoritical construct of Islamic Economics and Islamic Economics Systems

Interpretation of features in Islamic Economics System

Shades of Muslim economics thought

Development of Islamic Economics (5)

Need for comparative analysis of contemporary Moslem Economics thought Areas chosen approach and scope,

underlying assumptions, Features of an Islamic Economy, Distribution, Production

Scholar chosen (based on the literature written) M.A. Mannan, M.N. Siddiqi, S.N.H. Naqvi, M.Kahf, S.M. Taleghani, M. Baqir Al Sadr

For Further Discussion please refer to “Contemporary Islamic Economic Thought” written by M. Aslam Haneef

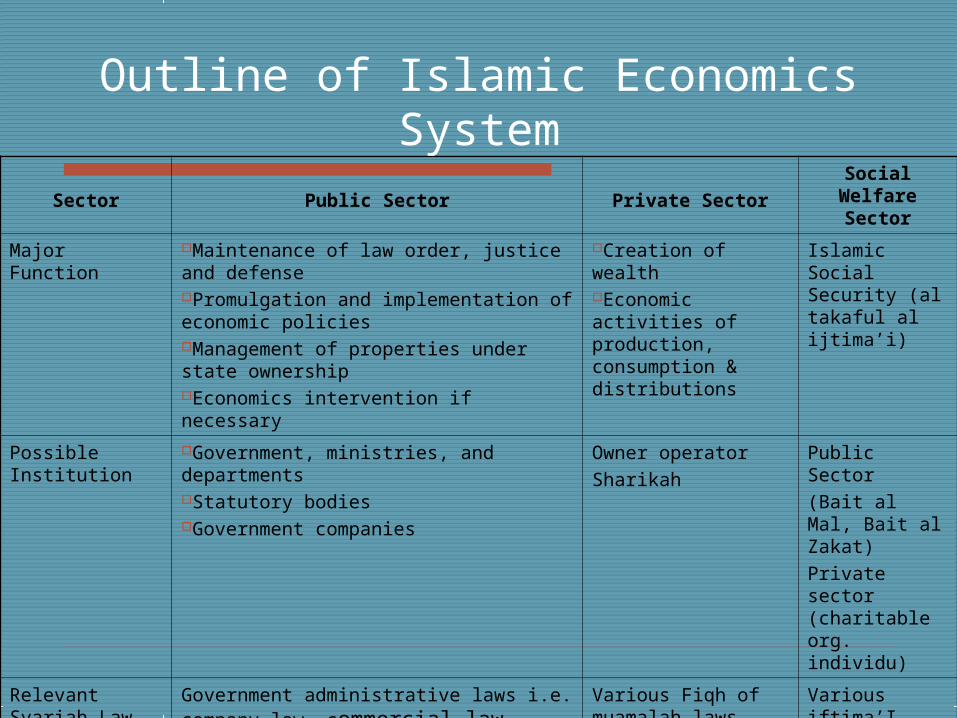

Outline of Islamic Economics System

Sector Public Sector Private SectorSocial

Welfare Sector

Major Function Maintenance of law order, justice and defensePromulgation and implementation of economic policiesManagement of properties under state ownershipEconomics intervention if necessary

Creation of wealthEconomic activities of production, consumption & distributions

Islamic Social Security (al takaful al ijtima’i)

Possible Institution

Government, ministries, and departmentsStatutory bodiesGovernment companies

Owner operatorSharikah

Public Sector (Bait al Mal, Bait al Zakat)Private sector (charitable org. individu)

Relevant Syariah Law

Government administrative laws i.e. company law, commercial law, Land law, taxation law

Various Fiqh of muamalah laws i.e. mudharabah, musyarakah, ijarah, etc

Various iftima’I i.e. zakah, waqf, tarikhah, sadaqah, qard

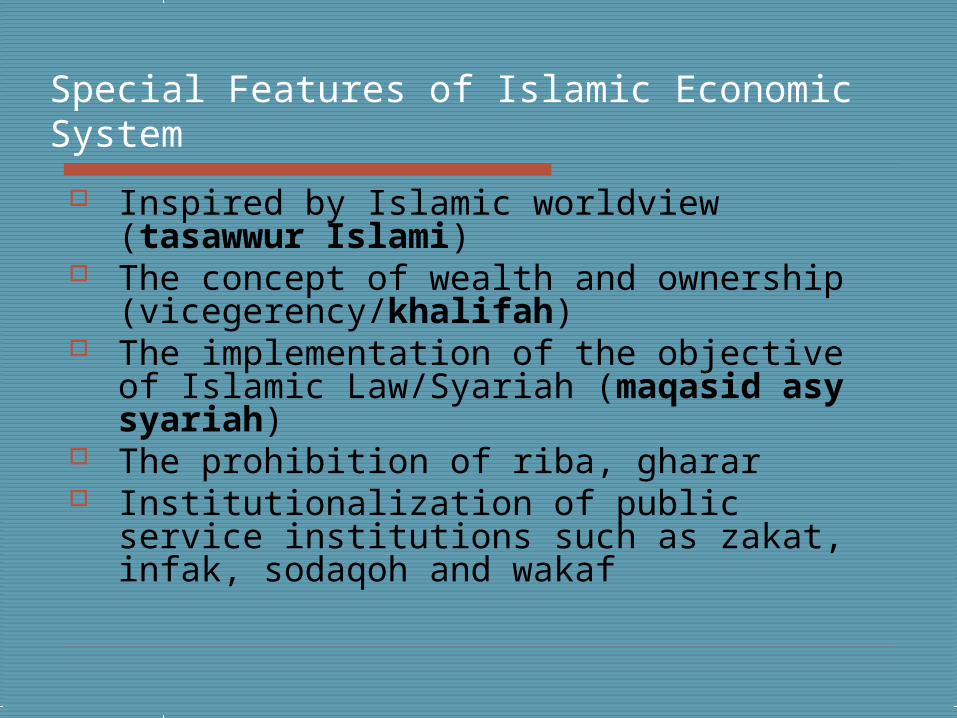

Special Features of Islamic Economic System

Inspired by Islamic worldview (tasawwur Islami)

The concept of wealth and ownership (vicegerency/khalifah)

The implementation of the objective of Islamic Law/Syariah (maqasid asy syariah)

The prohibition of riba, gharar Institutionalization of public service

institutions such as zakat, infak, sodaqoh and wakaf

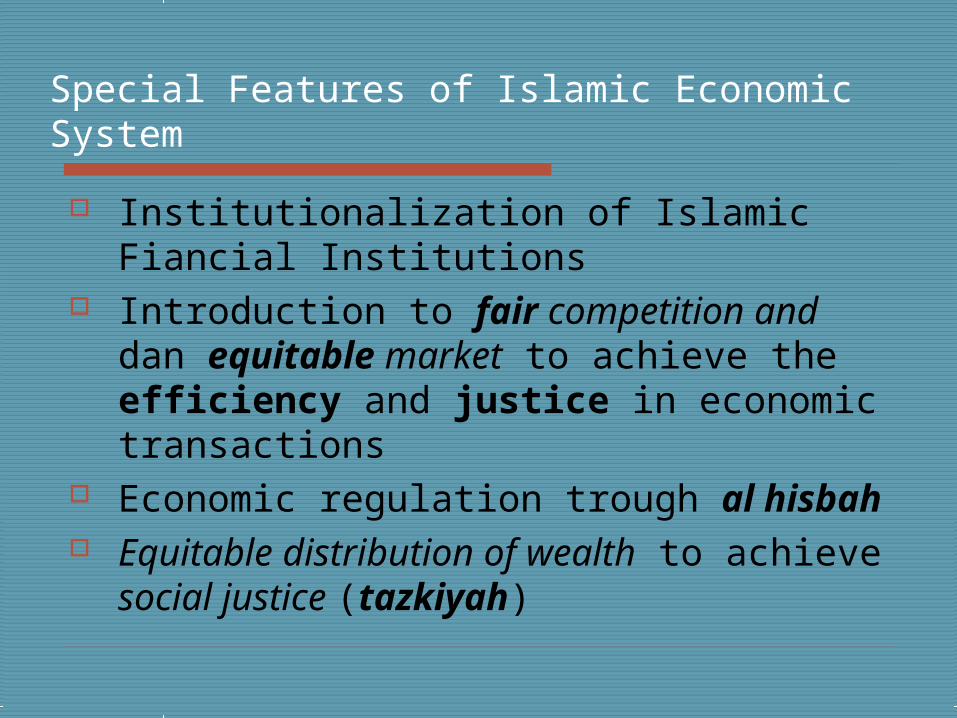

Institutionalization of Islamic Fiancial Institutions

Introduction to fair competition and dan equitable market to achieve the efficiency and justice in economic transactions

Economic regulation trough al hisbah Equitable distribution of wealth to

achieve social justice (tazkiyah)

Special Features of Islamic Economic System

Foundations of Islamic Institutions and Islamic Financial System

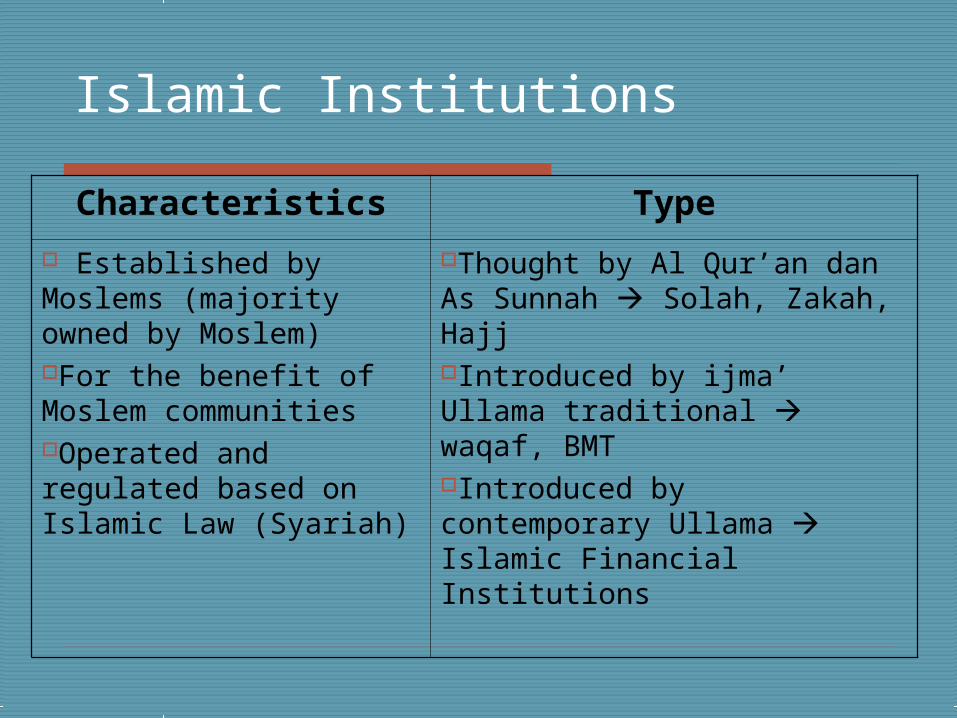

Islamic Institutions

Characteristics Type Established by Moslems (majority owned by Moslem) For the benefit of Moslem communitiesOperated and regulated based on Islamic Law (Syariah)

Thought by Al Qur’an dan As Sunnah Solah, Zakah, HajjIntroduced by ijma’ Ullama traditional waqaf, BMTIntroduced by contemporary Ullama Islamic Financial Institutions

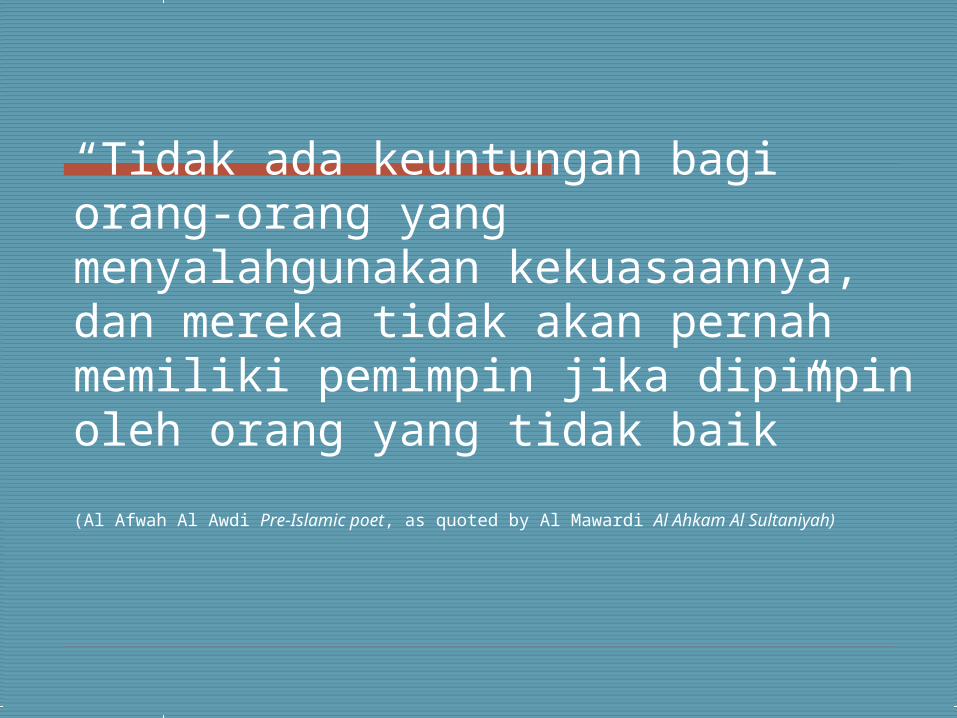

“Tidak ada keuntungan bagi orang-orang yang menyalahgunakan kekuasaannya, dan mereka tidak akan pernah memiliki pemimpin jika dipimpin oleh orang yang tidak baik”

(Al Afwah Al Awdi Pre-Islamic poet, as quoted by Al Mawardi Al Ahkam Al Sultaniyah)

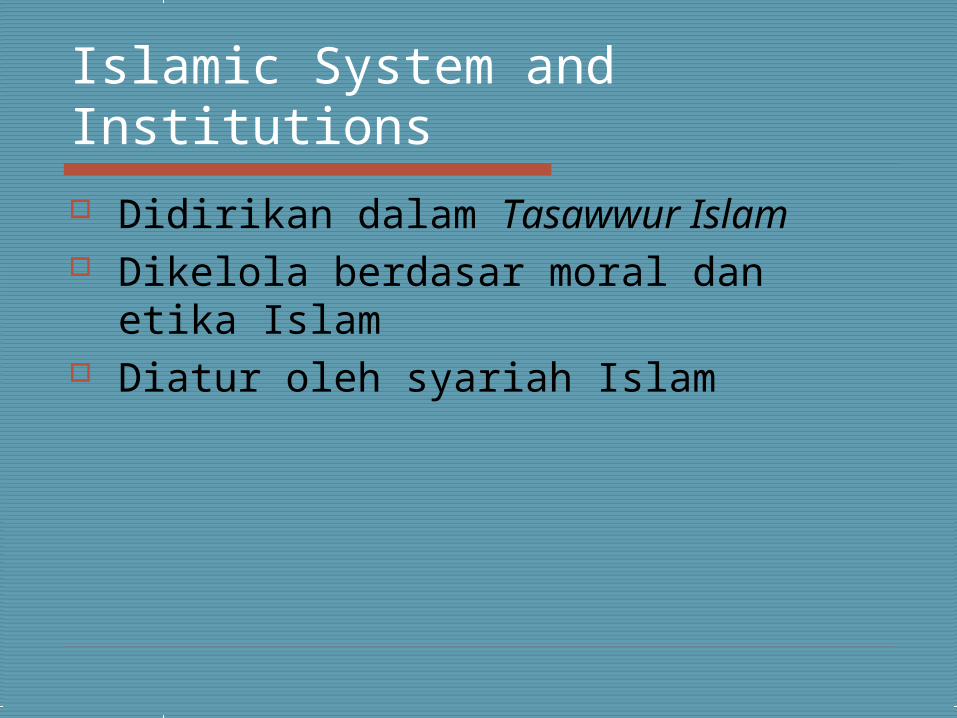

Islamic System and Institutions

Didirikan dalam Tasawwur Islam Dikelola berdasar moral dan etika

Islam Diatur oleh syariah Islam

Maslahah Prinsip-prinsip untuk mencapai

terpenuhinya kepentingan umum. Good is lawful, and lawful must be

good. Tujuannya adalah untuk melindungi

kepentingan yaitu (Imam Syatibi): Daruriyat (kebutuhan dasar) Hajiyyat (kebutuhan tambahan) Tahsiniyyat (kebutuhan pelengkap)

Daruriyat

Melindungi: Deen (agama) Nafs (jiwa) Nasl (keturunan/keluarga) Mal (harta) ‘Aql (akal)

Hajiyyat

Tambahan terhadap kebutuhan pokok Jika diabaikan mungkin menimbulkan

kekurangan/masalah. Contoh: pelarangan penjualan alkohol

untuk menghindari konsumsi alkohol. Contoh: kemudahan dalam

menjalankan ibadah bagi orang sakit ataupun musafir.

Tahsiniyyat

Pemenuhan kebutuhan ini memberikan peningkatan kualitas hidup.

More desirable. Contoh: menghindari pemborosan.

Islamic Accountability Tanggungjawab transedental terhadap

Allah SWT (hablunmminnalah) Tanggung jawab sosial (hablumminanass) Setiap manusia adalah khalifah Kebahagiaan dunia dan akhirat Tujuan ekonomi tidak hanya menyangkut

keakayaan bersih tetapi juga meliputi pembersihan diri dan kekayaan (tazkiyah)