Embed Size (px)

Citation preview

1

ISSUER SEMINARHKEx Combined Consultation Paper onProposed Changes to the Listing Rules

February 29, 2008

2

INTRODUCTION OF GUEST SPEAKERS

» David Hynes• Chairman, Global - Computershare Communication Services

David is Chairman elect of Computershare Communication Services Global Operations. He is a printer by trade and an entrepreneur in spirit. David was a co-founder of Chelsea Images “C.I.” which was subsequently bought by Computershare Limited (Australia) in 2000. Over the past seven years David has established the Communication Services capabilities and facilities in North America based in Toronto and Chicago. David continues to engage in strategic relations with all our key customers and ultimately remains accountable for their success. As well, he is keenly involved in most technology decisions and oversees CCS’s IT strategic direction.

» Andy Cotter• Head of Industry Relations, Computershare Investor Services UK

Andy is the chairman of the ICSA Registrars Group and a member of numerous industry working parties, dealing with legal and regulatory changes and involved in setting standards and best practice. Andy has extensive experience in the securities industry, ranging from involvement with the UK Government in the privatisations of the 1980s, the demutualisation of Building Societies and Insurance companies in the 1990s and the introduction of the CREST settlement system. During the past few years Andy has been actively involved in shaping and developing the registration and e-Communication aspects of the UK Companies Act 2006.

» James Wong• Chief Executive Officer, Computershare Hong Kong Investor Services Ltd

James Wong was a director of Hong Kong Clearing since 1995 until its merger with the other Hong Kong exchanges and clearing houses to form the Hong Kong Exchanges and Clearing Limited in 2000. After that James became a member of HKEx's Clearing Consultative Panel as well as the SFC'sShare Registrars' Disciplinary Committee until end of 2005. He is currently a member of the Hang Seng Index Advisory Committee, member of the Disciplinary Subcommittee of the Treasury Markets Association and Vice Chairman of the Hong Kong Federation of Share Registrars. Over the years, James has been actively involved in all aspects of market infrastructural and regulatory developments in Hong Kong and Mainland China's capital markets. He has been a member of various consultative committees and working groups initiated by the SFC. James was involved in the development of the QFII market practices and regulations, and has been working with various regulatory bodies in China on securities market infrastructure development issues.

» Phyllis Lee• Head of Product Development, Computershare Hong Kong Investor Services Ltd

Phyllis has worked for HSBC and Standard Chartered Bank in the custody and fund services providing securities services to institutional investors and has been responsible to maintain relationship with industry regulators to help drive market reforms. Phyllis has also worked with market participants and industry regulators in improving market infrastructure, notably of which was the successful implementation of a market-wide pre-matching service in CCASS in 2006.

3

AGENDA

� About Computershare

� HKEx Combined Consultation Paper on Proposed Changes to the Listing Rules � Discussion of the relevant issues

� The recent global regulatory developments of shareholder communications� Global experience sharing:

� Industry Dynamics

� Australia Experience

� The United States Experience

� United Kingdom Experience

� Best practice proposals for Hong Kong

� Benefits to Hong Kong Issuers

� How Computershare can help you

� What’s next

� Q & A

4

About Computershare

5

ABOUT COMPUTERSHARE

Globally

• Offices in over 20 countries and regions. Over 10,000 employees

• Servicing over 14,000 issuers and over 100 million investors

• Extensive involvement in development of market infrastructure, especially cross-border

• Using integrated technologies to produce more than 400 million shareholder communication p.a..

• Listed in Australia under CPU.AX. USD4.5 billion market cap.

6

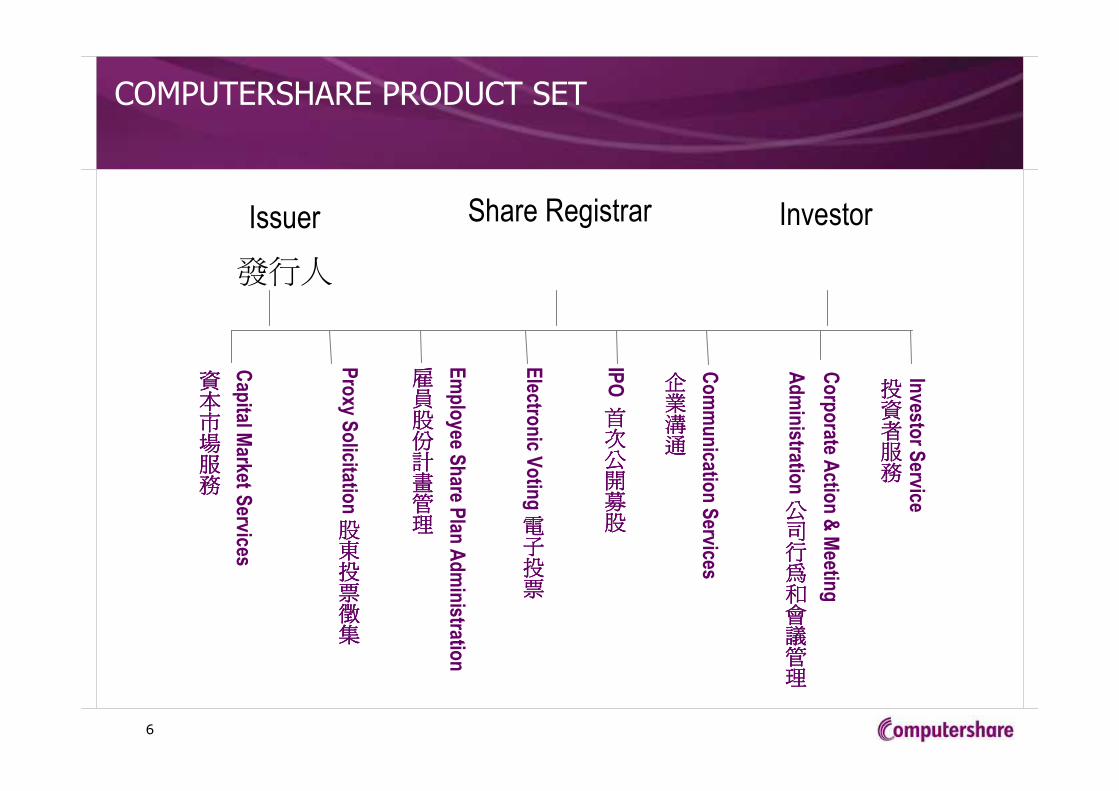

COMPUTERSHARE PRODUCT SET

Issuer

發行人Corporate A

ction & Meetin

g

Administratio

n

公司行為和會議管理

公司行為和會議管理

公司行為和會議管理

公司行為和會議管理

Electro

nic V

otin

g

電子投票

電子投票

電子投票

電子投票

Cap

ital Market

Services

資本市場服務

資本市場服務

資本市場服務

資本市場服務

IPO

首次公開募股

首次公開募股

首次公開募股

首次公開募股

Proxy

Solicitatio

n

股東投票徵集

股東投票徵集

股東投票徵集

股東投票徵集

Share Registrar Investor

Employee S

hare P

lan Administratio

n

雇員股份計畫管理

雇員股份計畫管理

雇員股份計畫管理

雇員股份計畫管理

Communicatio

n Services

企業溝通

企業溝通

企業溝通

企業溝通

Investo

r Service

投資者服務

投資者服務

投資者服務

投資者服務

7

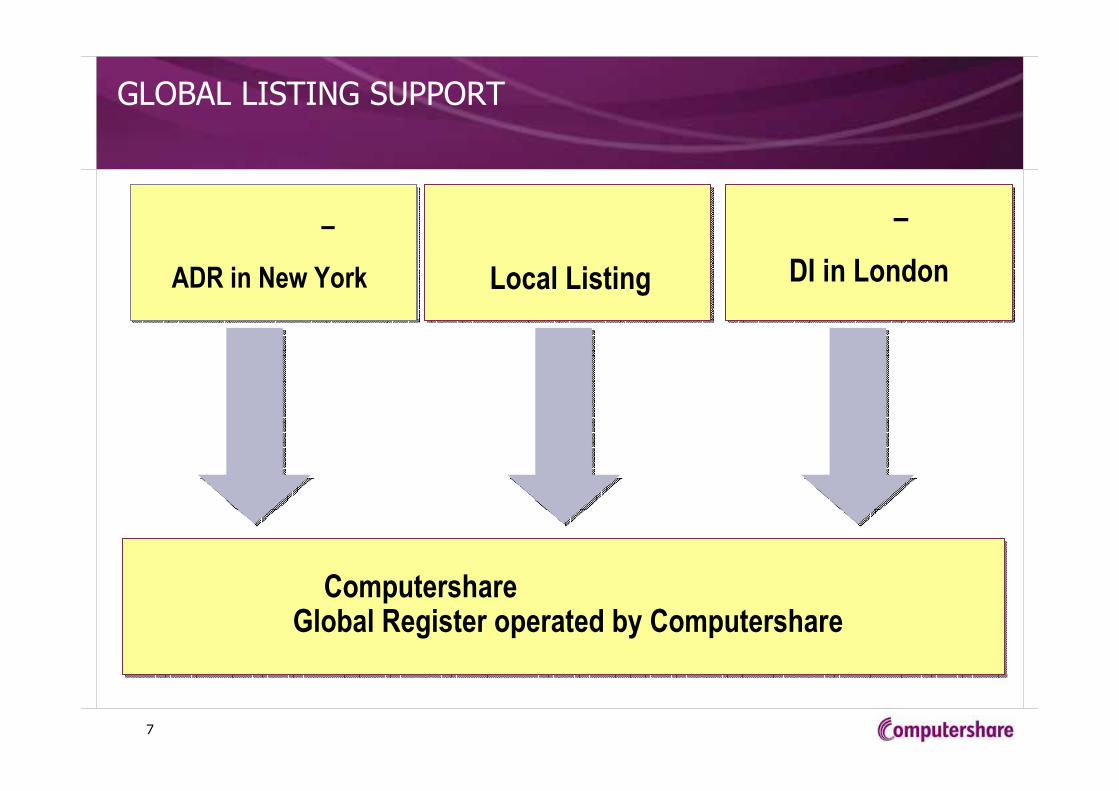

GLOBAL LISTING SUPPORT

–

ADR in New York Local Listing

–

DI in London

Computershare Global Register operated by Computershare

8

HKEx Combined Consultation Paper onProposed Changes to the

Listing Rules

DISCUSSION FORUM

9

POLICY ISSUES FOR CONSULTATION BY HKEx

Issue 1: Use of websites for communications with shareholders

Issue 8: Disclosure of changes in issued shared capitalIssue 9: Disclosure requirements for announcements regarding issues of securities for

cash and allocation basis for excess shares in rights issue

Issue 12: Voting at general meetings

Issue 2: Information gathering powersIssue 3: Qualified accountantsIssue 4: Review of sponsor’s independenceIssue 5: Public floatIssue 6: Bonus issues of a class of securities new to listingIssue 7: Review of the Exchange’s approach to pre-vetting public documents of listed

issuers

Issue 10: Alignment of requirements for material dilution in major subsidiary and deemed disposal

Issue 11: General mandates

Issue 13: Disclosure of information about and by directorsIssue 14: Codification of waiver to property companiesIssue 15: Self-constructed fixed assetsIssue 16: Disclosure of information in takeoversIssue 17: Review of director’s and supervisor’s declaration and undertakingIssue 18: Review of Model Code for Securities Transactions by Directors of Listed

Issuers

ISSUES FOR DISCUSSION

10

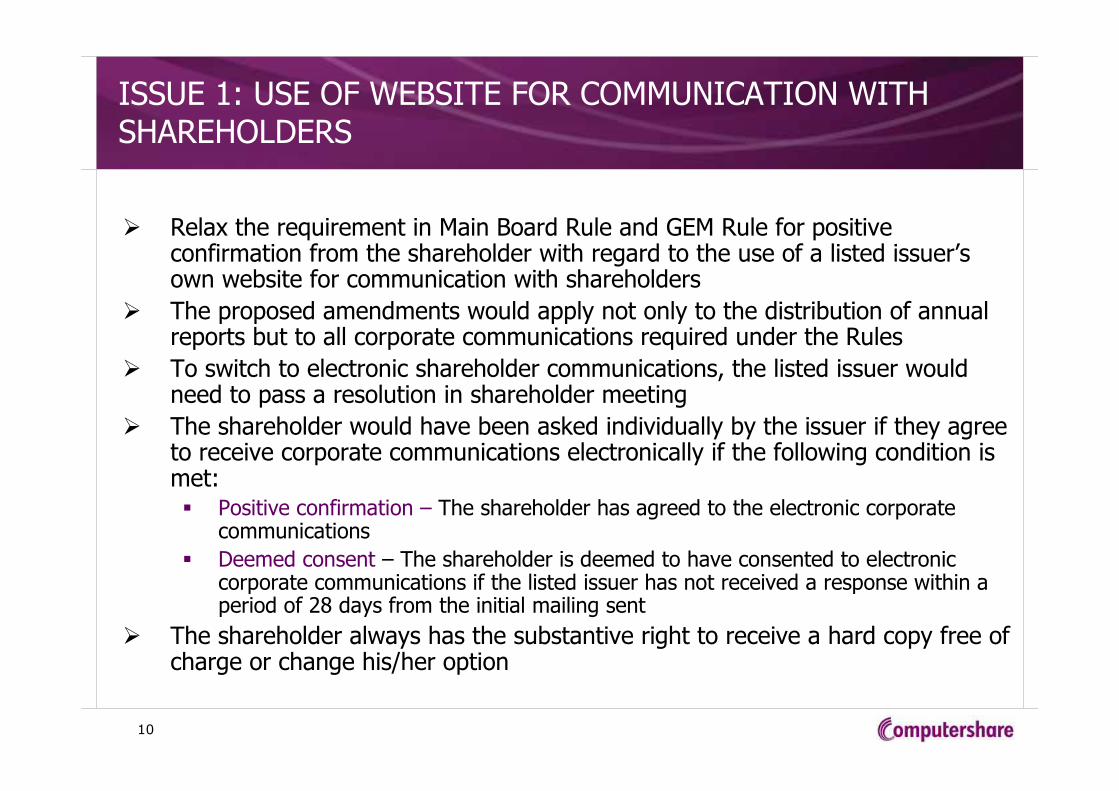

ISSUE 1: USE OF WEBSITE FOR COMMUNICATION WITH SHAREHOLDERS

� Relax the requirement in Main Board Rule and GEM Rule for positive confirmation from the shareholder with regard to the use of a listed issuer’s own website for communication with shareholders

� The proposed amendments would apply not only to the distribution of annual reports but to all corporate communications required under the Rules

� To switch to electronic shareholder communications, the listed issuer would need to pass a resolution in shareholder meeting

� The shareholder would have been asked individually by the issuer if they agree to receive corporate communications electronically if the following condition is met:� Positive confirmation – The shareholder has agreed to the electronic corporate

communications

� Deemed consent – The shareholder is deemed to have consented to electronic corporate communications if the listed issuer has not received a response within a period of 28 days from the initial mailing sent

� The shareholder always has the substantive right to receive a hard copy free of charge or change his/her option

11

ISSUE 1: USE OF WEBSITE FOR COMMUNICATION WITH SHAREHOLDERS

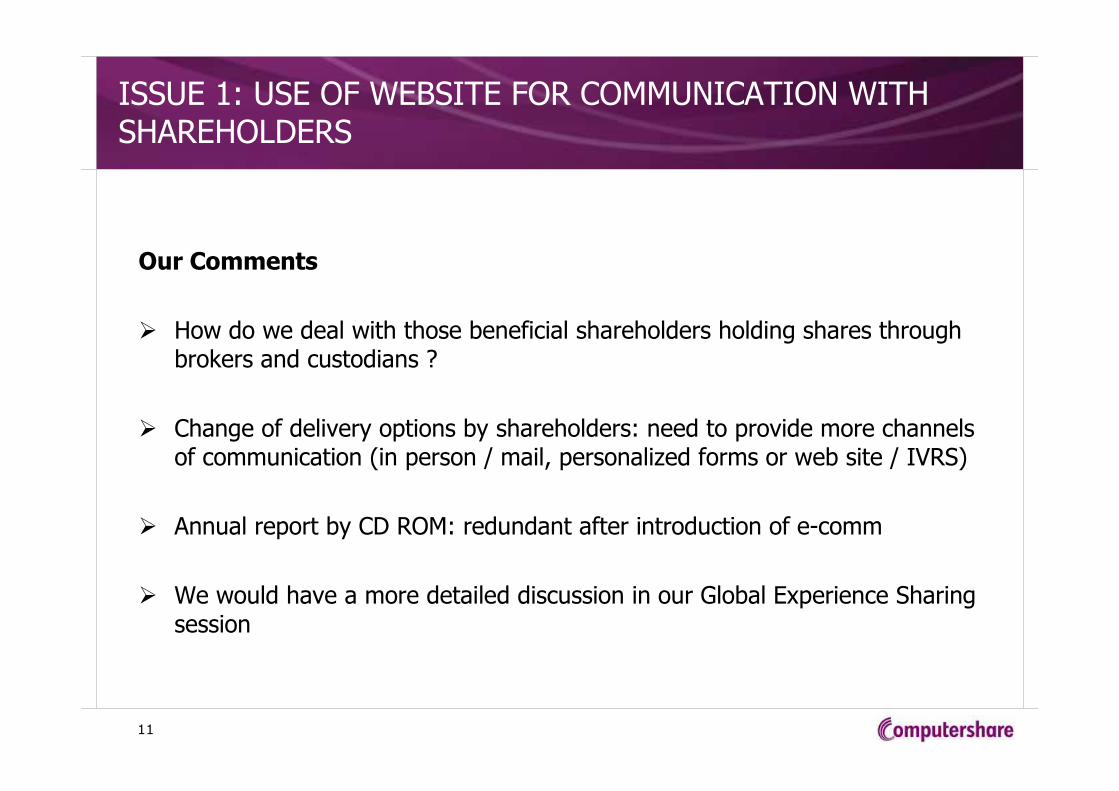

Our Comments

� How do we deal with those beneficial shareholders holding shares through brokers and custodians ?

� Change of delivery options by shareholders: need to provide more channels of communication (in person / mail, personalized forms or web site / IVRS)

� Annual report by CD ROM: redundant after introduction of e-comm

� We would have a more detailed discussion in our Global Experience Sharing session

12

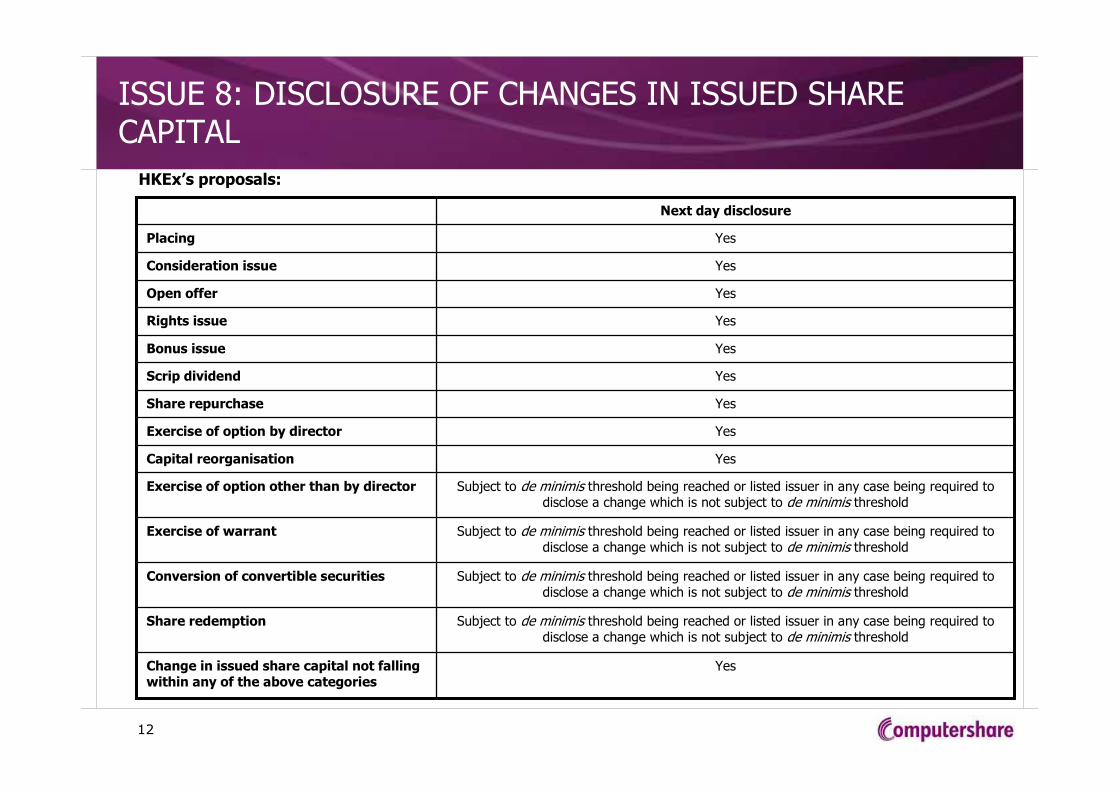

ISSUE 8: DISCLOSURE OF CHANGES IN ISSUED SHARE CAPITAL

HKEx’s proposals:

YesShare repurchase

YesExercise of option by director

YesCapital reorganisation

YesChange in issued share capital not falling within any of the above categories

Subject to de minimis threshold being reached or listed issuer in any case being required to disclose a change which is not subject to de minimis threshold

Share redemption

Subject to de minimis threshold being reached or listed issuer in any case being required to disclose a change which is not subject to de minimis threshold

Conversion of convertible securities

Subject to de minimis threshold being reached or listed issuer in any case being required to disclose a change which is not subject to de minimis threshold

Exercise of warrant

Subject to de minimis threshold being reached or listed issuer in any case being required to disclose a change which is not subject to de minimis threshold

Exercise of option other than by director

YesScrip dividend

YesBonus issue

YesRights issue

YesOpen offer

YesConsideration issue

YesPlacing

Next day disclosure

13

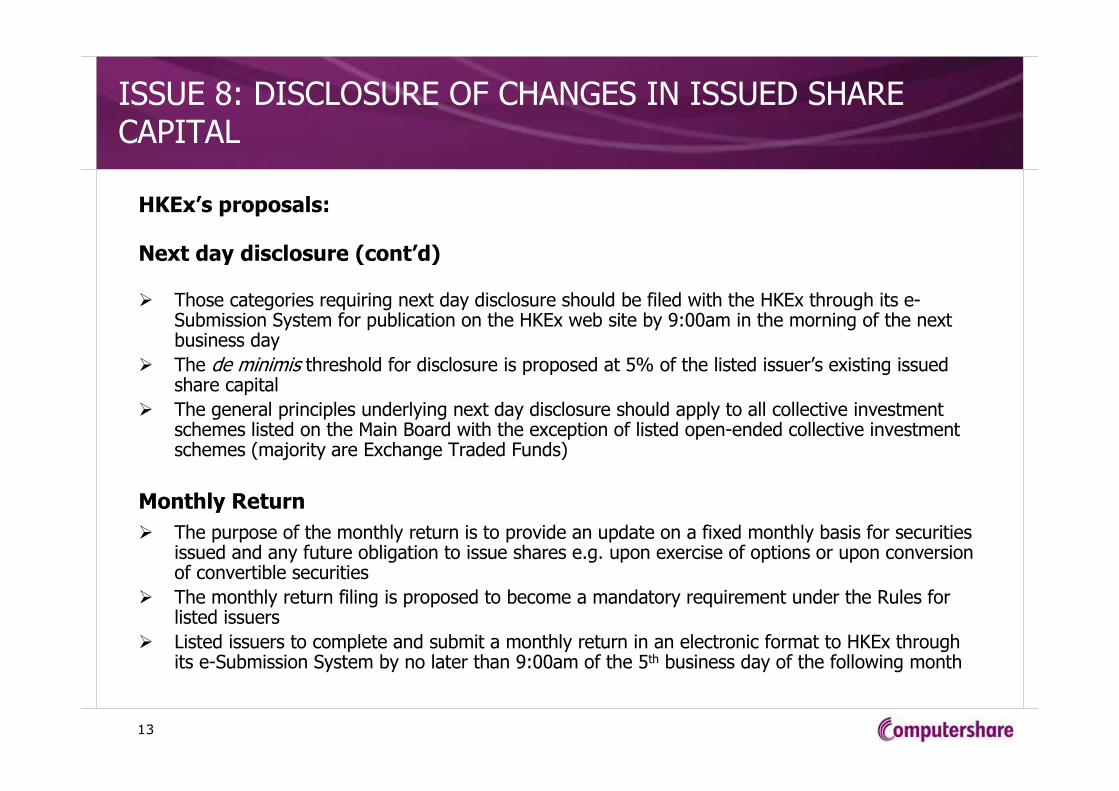

ISSUE 8: DISCLOSURE OF CHANGES IN ISSUED SHARE CAPITAL

HKEx’s proposals:

Next day disclosure (cont’d)

� Those categories requiring next day disclosure should be filed with the HKEx through its e-Submission System for publication on the HKEx web site by 9:00am in the morning of the next business day

� The de minimis threshold for disclosure is proposed at 5% of the listed issuer’s existing issued share capital

� The general principles underlying next day disclosure should apply to all collective investment schemes listed on the Main Board with the exception of listed open-ended collective investment schemes (majority are Exchange Traded Funds)

Monthly Return

� The purpose of the monthly return is to provide an update on a fixed monthly basis for securities issued and any future obligation to issue shares e.g. upon exercise of options or upon conversion of convertible securities

� The monthly return filing is proposed to become a mandatory requirement under the Rules for listed issuers

� Listed issuers to complete and submit a monthly return in an electronic format to HKEx through its e-Submission System by no later than 9:00am of the 5th business day of the following month

14

ISSUE 8: DISCLOSURE OF CHANGES IN ISSUED SHARE CAPITAL

Our Comments

� As share registrars we maintain records of issued share capital

� We provide Issued Capital Report to issuers – delivery via Issuer Online

� Need to understand better the definition of Next Day: does it mean next day of transaction, or next day of entry into register of the subject transaction?

� As Share Repurchases may come in the form of many low value transactions, we suggest there should be a de minimis threshold

� Would issuers have any difficulty in complying with Next Day disclosure?

� How can we help issuers to comply with the new filing requirements?

15

ISSUE 9: DISCLOSURE REQUIREMENTS FOR ANNOUNCEMENTS REGARDING ISSUES OF SECURITIES FOR CASH AND ALLOCATION BASIS FOR EXCESS SHARES IN RIGHTS ISSUES

� To amend Main Board Rule and GEM Rule that the specific disclosure requirements will be extended to any issue of securities for cash irrespective of whether general mandates are involved

� The proposed amendments would require the relevant announcement to contain a statement on:

• Whether the issue of securities is subject to shareholders’ approval;

• Whether the securities issued under a general mandate, details of such mandate;

• Whether the securities are issued by way of a rights issue or an open offer, with specific certain details applicable to the rights issue or open offer under the Rules

� The proposal would also require the listed issuers to disclose the basis of allocation of the excess securities in the announcement, circular and listing document for a rights issue or open offer

HKEx’s proposals

16

ISSUE 9: DISCLOSURE REQUIREMENTS FOR ANNOUNCEMENTS REGARDING ISSUES OF SECURITIES FOR CASH AND ALLOCATION BASIS FOR EXCESS SHARES IN RIGHTS ISSUES

Our Comments

� In general we are neutral on the Exchange’s proposal. But with respect to the requirement in 9.7 for issuers to disclose the basis of allocation of excess securities in the announcement, we felt this an opportunity to deal with a long standing unusual shareholder behaviour.

� In rights issues, shareholders would split their holdings into many odd lots under different names, with a view to obtaining multiple PAL’s / EAF’s and therefore opportunities to apply for excess as well as getting additional allocation in rounding up to nearest board lot. This would unduly increase the issuer’s cost of handling the rights issue.

� If the issuer discloses in their announcement that allocation would be board lots only and there would not be any rounding up of odd lot allocation, this would discourage such irregularities, and save shareholder communication, management and corporate action costs

17

ISSUE 12: VOTING AT GENERAL MEETINGS

HKEx’s proposals

� Whether the Rules should be amended to extend the requirement for voting by poll beyond the current scope so as to cover all resolutions at general meetings

� 1st alternative: require voting on all resolutions at annual general meetings to be by poll. Where voting is taken on a poll, listed issuer must comply with the current Rules to make publication on the next business day in an announcement of the results of the poll including details of proxies

� 2nd alternative: where the resolution is decided in a manner other than a poll, the listed issuer would be required to publish the total number of proxy votes in respect of which proxy appointment have been validly made together with the number of appointments which specify that:

i. The proxy is to vote for the resolution;

ii. The proxy is to vote against the resolution;

iii. The proxy is to abstain on the resolution; and

iv. The proxy may vote at the proxy’s discretion.

18

HKEx’s proposals

� Recommends final and detailed notices/agendas should be published at least 28 calendar days before all general meetings

• There may be grounds for extending the notice period for annual general meeting to 28 calendar days;

• However, the same applicable to extraordinary general meetings to 28 calendar days, or a period of between 14 and 28 calendar days, may be less persuasive.

ISSUE 12: VOTING AT GENERAL MEETINGS

19

ISSUE 12: VOTING AT GENERAL MEETINGS

Our Comments

� Vote by poll should remain a Recommended Best Practice

� The remaining issue would be how to provide those beneficial shareholders behind brokers and custodians with corporate communication and allow them to exercise their voting rights in an efficient manner

� Extending notice period to 28 days would allow more time for shareholders to make their considered voting decisions. The proposed timeframe would also align with the proposals in Issue 1 allowing more time for dispatch of notice of meeting if Rules amended.

� A longer notice period would also provide issuers with more time for proxy solicitation should this be required

� There are appropriate proxy and voting solutions provider in the market to assist issuers to manage additional time and costs required for poll voting

20

The Recent Global Regulatory Developments

of

Shareholder Communications

GLOBAL EXPERIENCE SHARING

21

Electronic Shareholder Communications

in

Australia

GLOBAL EXPERIENCE SHARING

22

AUSTRALIAN LEGISLATION

� The Simpler Regulatory System Act - Electronic distribution of annual reports

� Default delivery of annual reports to be via the company’s website

� Each year, company must notify securityholders when report is available on their website and where it can be located

� Notify securityholders in writing of their right to continue to receive a hard copy of the annual report

� The online annual report must be ‘reasonably accessible’ to securityholders

� Hard copy annual report must be provided free of charge to securityholders who request one

� Hard copy annual report requests are a standing request

� Timing: SRS enacted June 2007

� Computershare made submissions to Treasury strongly supporting the Act

23

CURRENT STATE OF CORPORATE REPORTING

� Relevance of corporate reporting

� Securityholder concerns� Retail investors turning their back on annual reports due to excessive

length and complexity of reported information � Only 30% remember receiving their annual report, only 4% read the

document

� Director’s concerns� Excessive length, complex jargon/not understandable� Inadequate disclosures in certain areas

� Management concerns� Expensive/time-consuming� Excessive disclosure/confidentiality, increasing ‘Red Tape’

I certainly can’t remember an analyst coming to the daily meeting and saying ‘Well, there’s something in the annual report that’s really interesting’. (PwC Investor Survey March – sell side analyst 2007)

24

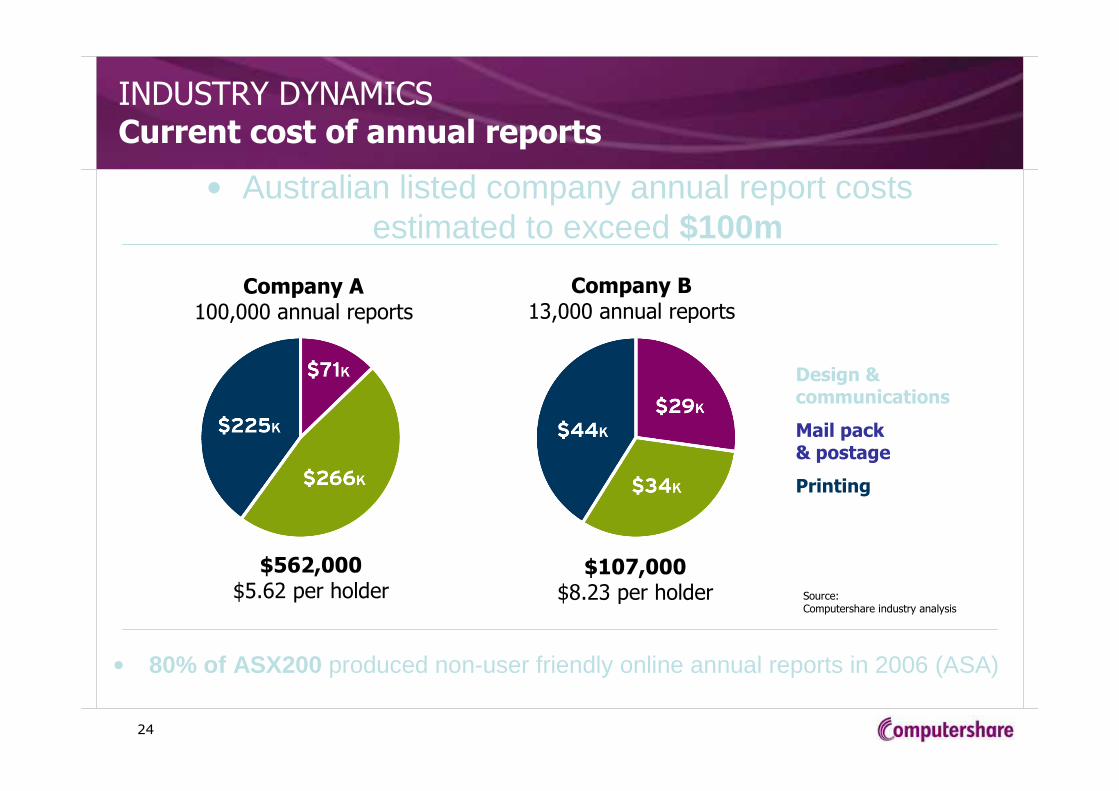

INDUSTRY DYNAMICSCurrent cost of annual reports

• Australian listed company annual report costs estimated to exceed $100m

Company A 100,000 annual reports

$562,000$5.62 per holder

$107,000$8.23 per holder

Design & communications

Mail pack & postage

Printing

• 80% of ASX200 produced non-user friendly online annual reports in 2006 (ASA)

Source: Computershare industry analysis

Company B 13,000 annual reports

25

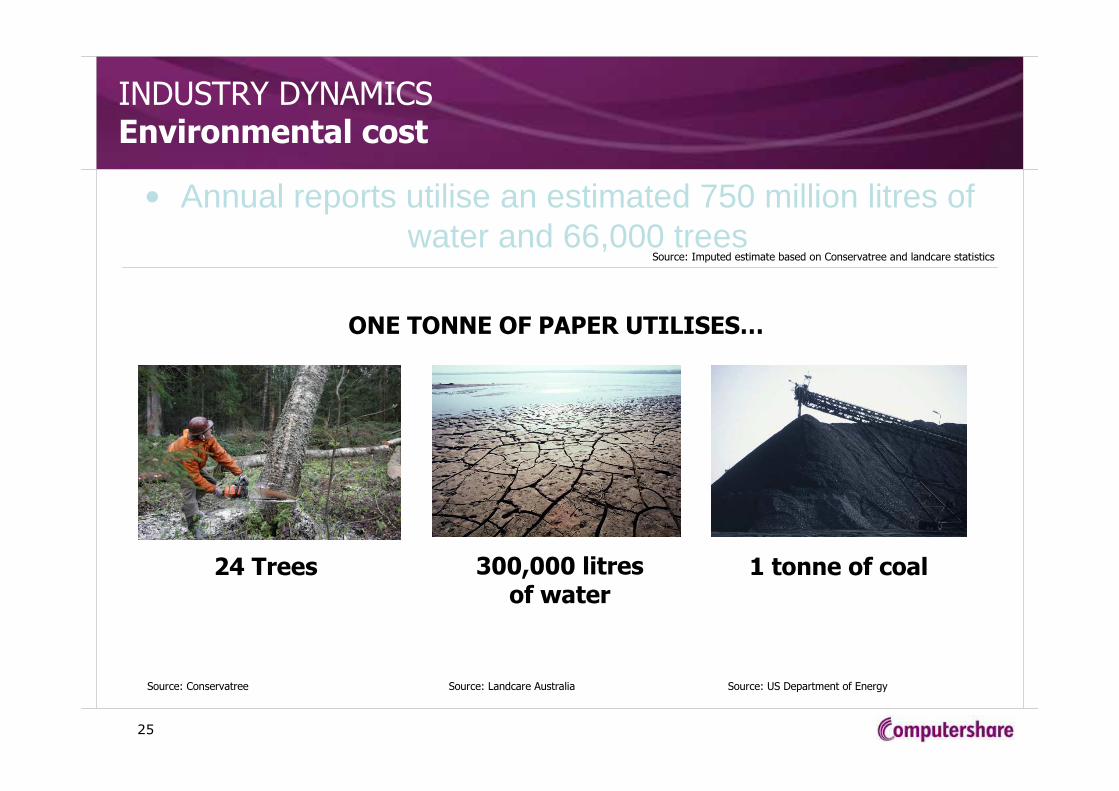

24 Trees

INDUSTRY DYNAMICSEnvironmental cost

• Annual reports utilise an estimated 750 million litres of water and 66,000 trees

300,000 litresof water

ONE TONNE OF PAPER UTILISES…

1 tonne of coal

Source: Conservatree Source: Landcare Australia Source: US Department of Energy

Source: Imputed estimate based on Conservatree and landcare statistics

26

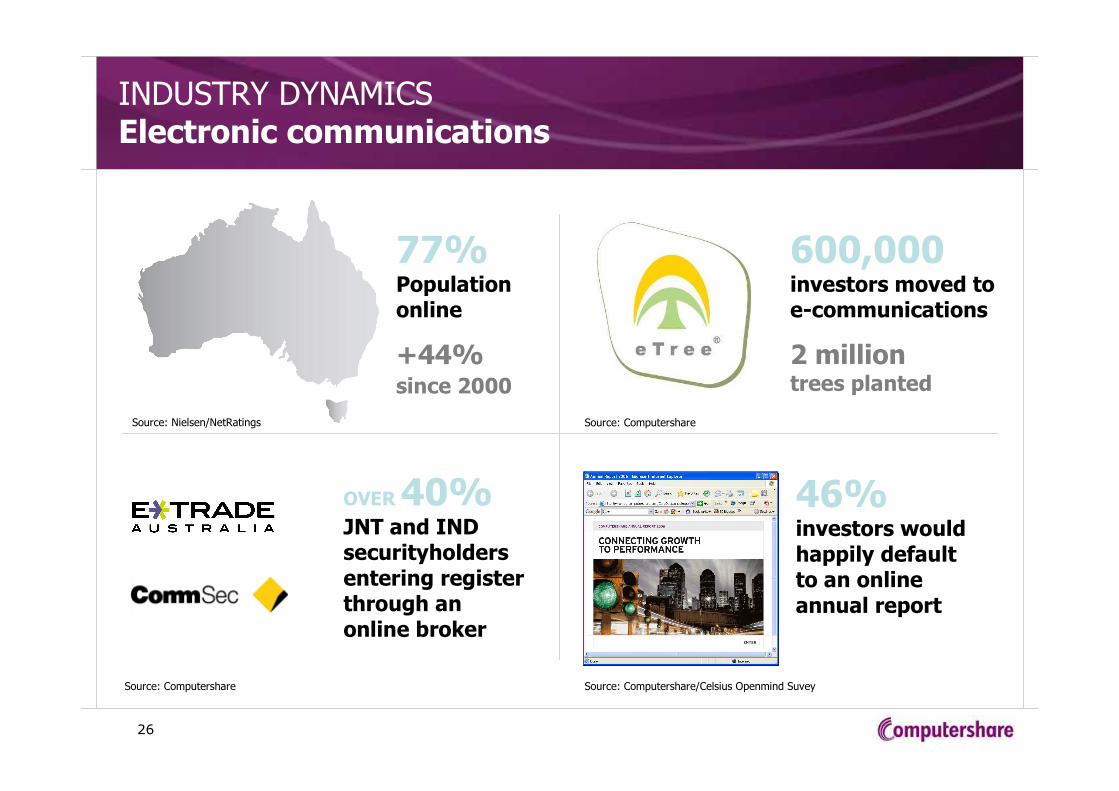

INDUSTRY DYNAMICSElectronic communications

77%Populationonline

+44%since 2000

600,000investors moved to e-communications

2 milliontrees planted

OVER 40%JNT and IND securityholders entering register through an online broker

46%investors would happily default to an online annual report

Source: Nielsen/NetRatings Source: Computershare

Source: Computershare/Celsius Openmind SuveySource: Computershare

27

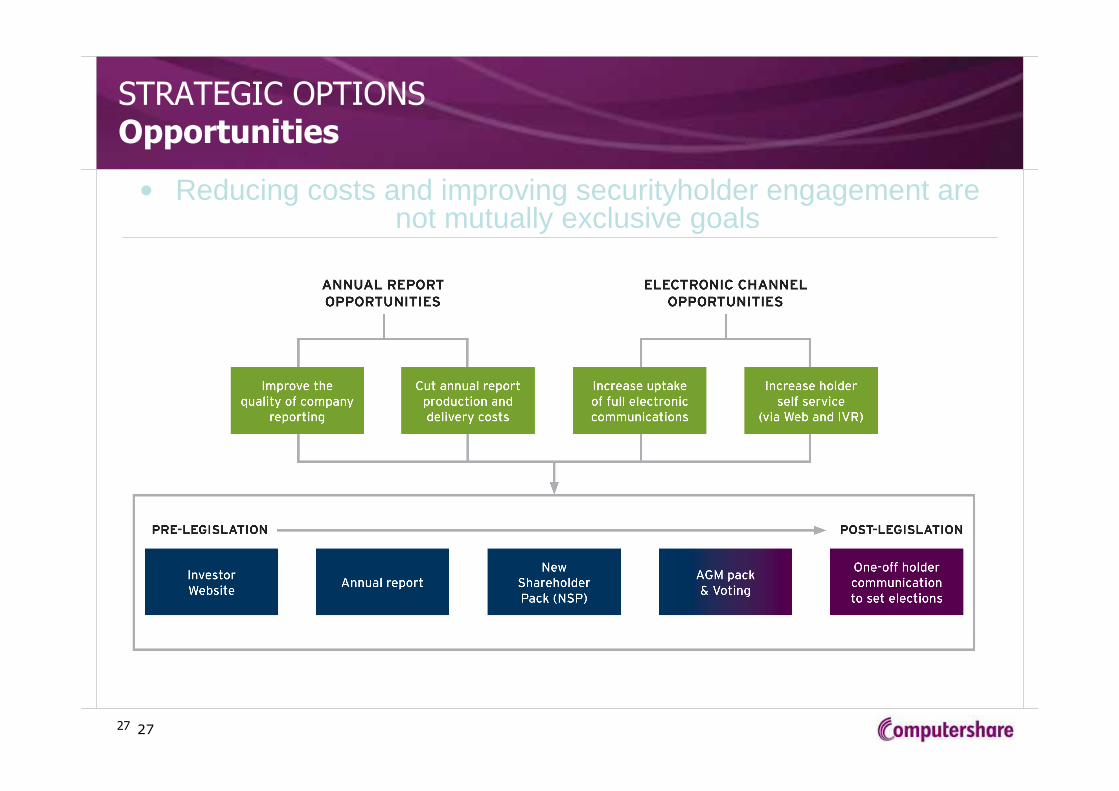

STRATEGIC OPTIONSOpportunities

27

• Reducing costs and improving securityholder engagement are not mutually exclusive goals

28

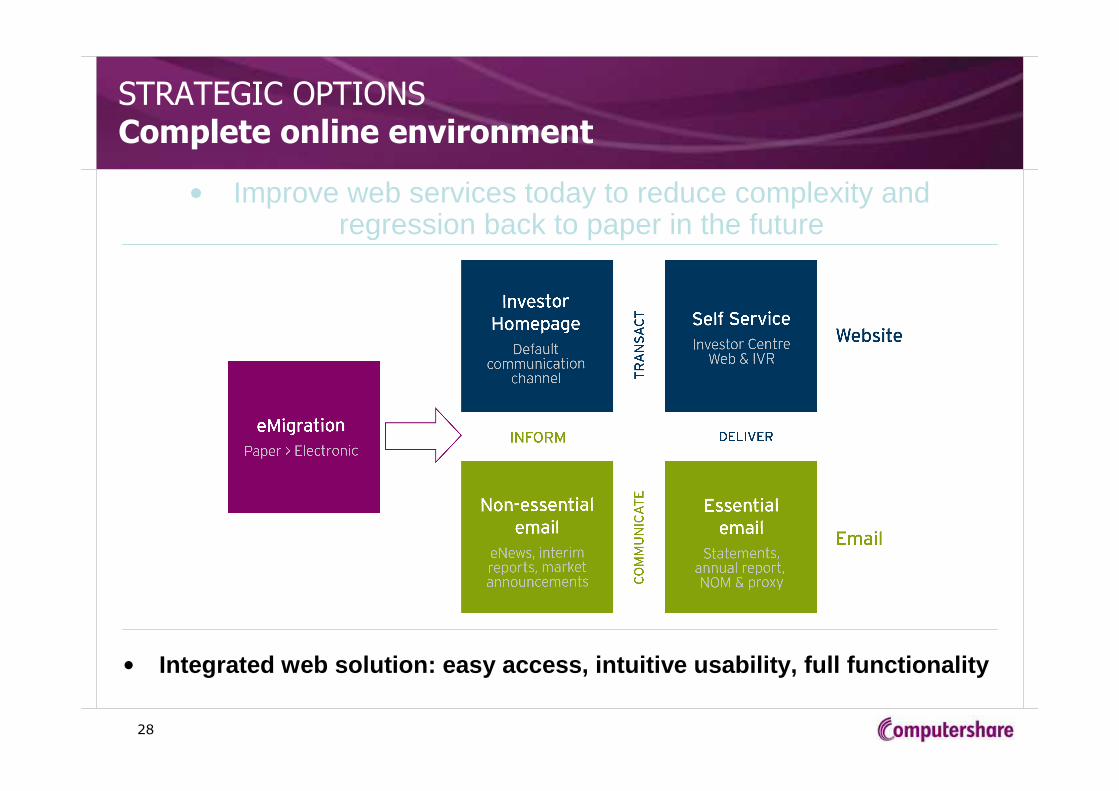

STRATEGIC OPTIONS Complete online environment

• Improve web services today to reduce complexity and regression back to paper in the future

• Integrated web solution: easy access, intuitive usability, full functionality

29

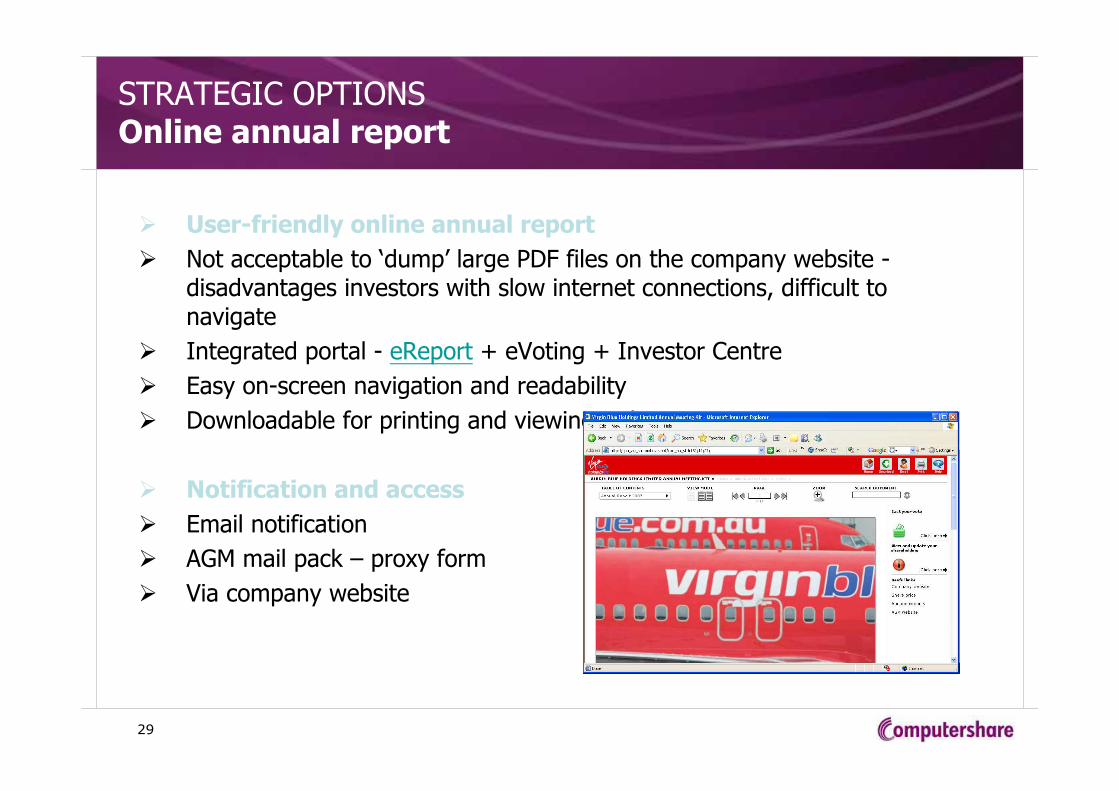

STRATEGIC OPTIONSOnline annual report

� User-friendly online annual report

� Not acceptable to ‘dump’ large PDF files on the company website -disadvantages investors with slow internet connections, difficult to navigate

� Integrated portal - eReport + eVoting + Investor Centre

� Easy on-screen navigation and readability

� Downloadable for printing and viewing at later time

� Notification and access

� Email notification

� AGM mail pack – proxy form

� Via company website

30

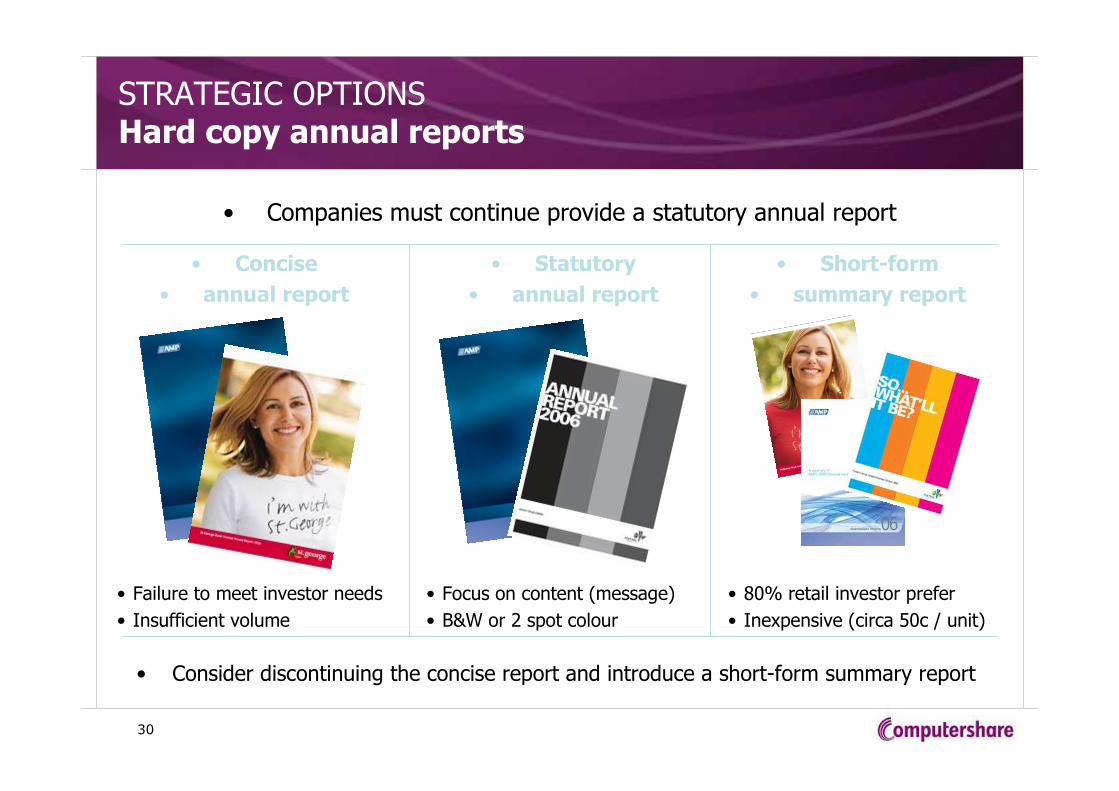

STRATEGIC OPTIONSHard copy annual reports

• Companies must continue provide a statutory annual report

• Consider discontinuing the concise report and introduce a short-form summary report

• Concise

• annual report

• Statutory

• annual report

• Short-form

• summary report

• Failure to meet investor needs

• Insufficient volume

• Focus on content (message)

• B&W or 2 spot colour

• 80% retail investor prefer

• Inexpensive (circa 50c / unit)

31

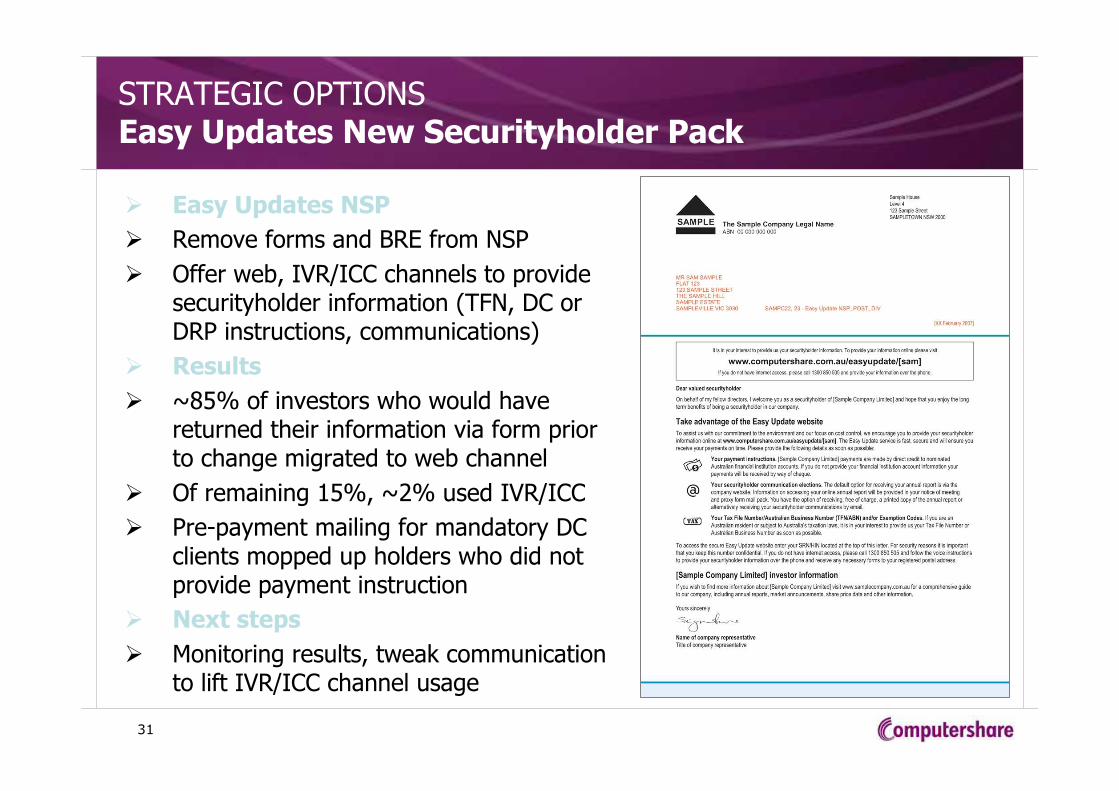

STRATEGIC OPTIONSEasy Updates New Securityholder Pack

� Easy Updates NSP

� Remove forms and BRE from NSP

� Offer web, IVR/ICC channels to provide securityholder information (TFN, DC or DRP instructions, communications)

� Results

� ~85% of investors who would have returned their information via form prior to change migrated to web channel

� Of remaining 15%, ~2% used IVR/ICC

� Pre-payment mailing for mandatory DC clients mopped up holders who did not provide payment instruction

� Next steps

� Monitoring results, tweak communication to lift IVR/ICC channel usage

32

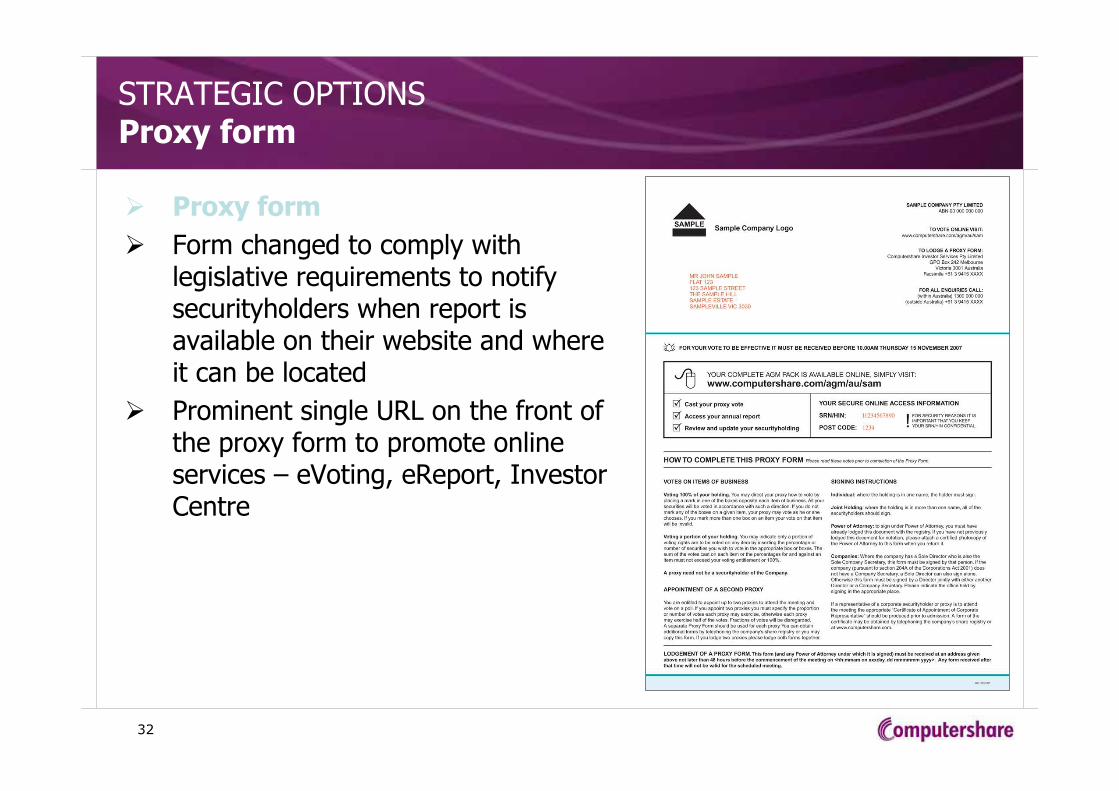

STRATEGIC OPTIONSProxy form

� Proxy form

� Form changed to comply with legislative requirements to notify securityholders when report is available on their website and where it can be located

� Prominent single URL on the front of the proxy form to promote online services – eVoting, eReport, Investor Centre

33

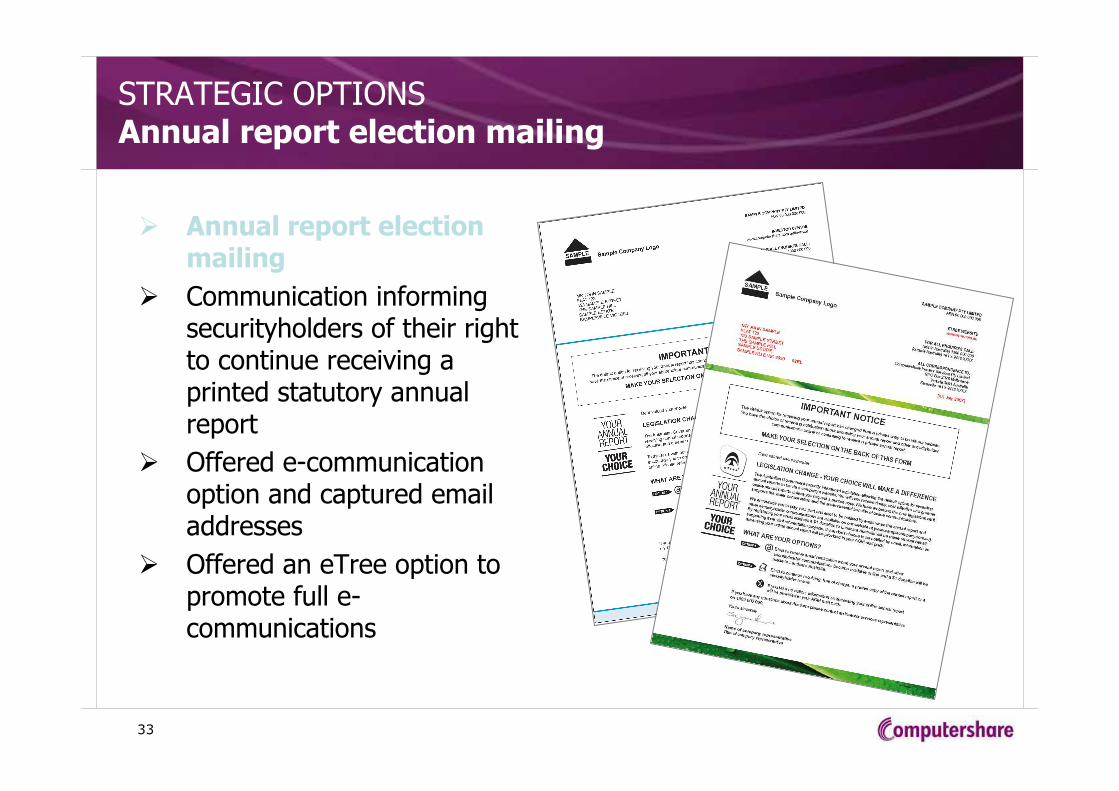

STRATEGIC OPTIONSAnnual report election mailing

� Annual report election mailing

� Communication informing securityholders of their right to continue receiving a printed statutory annual report

� Offered e-communication option and captured email addresses

� Offered an eTree option to promote full e-communications

34

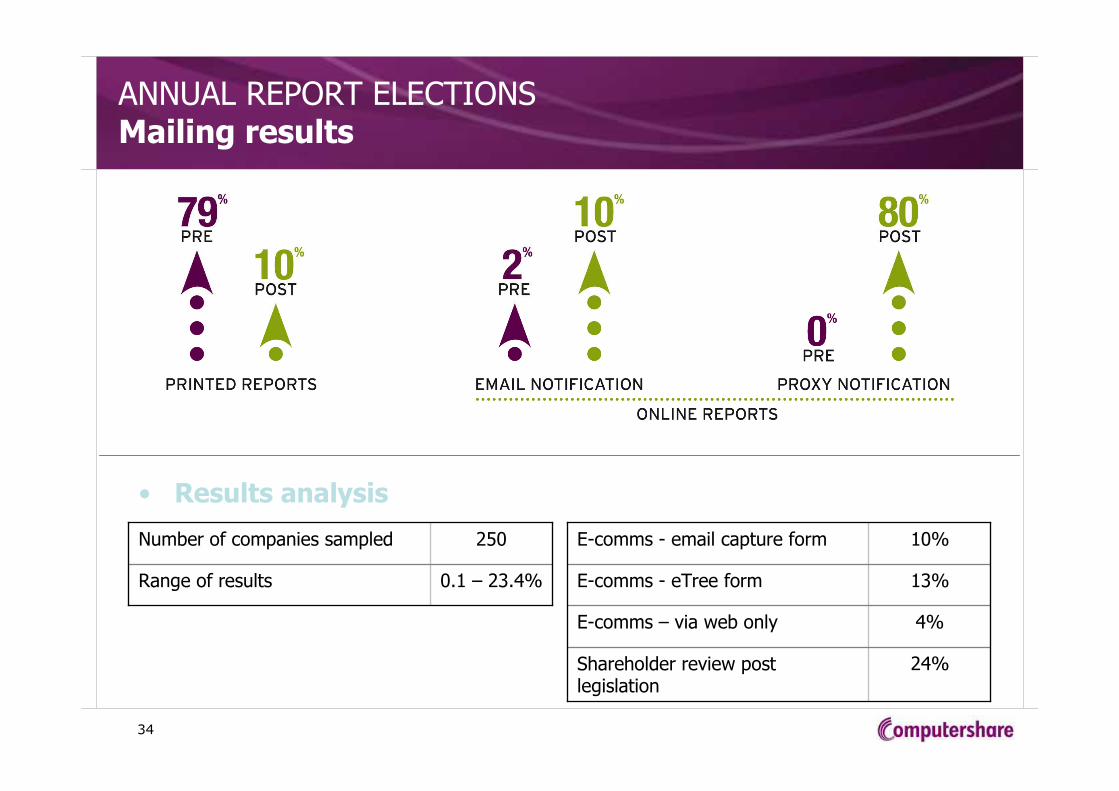

ANNUAL REPORT ELECTIONSMailing results

0.1 – 23.4%Range of results

250Number of companies sampled

• Results analysis

24%Shareholder review post legislation

4%E-comms – via web only

13%E-comms - eTree form

10%E-comms - email capture form

35

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2

Printed annual report E-communications No annual report - default notification

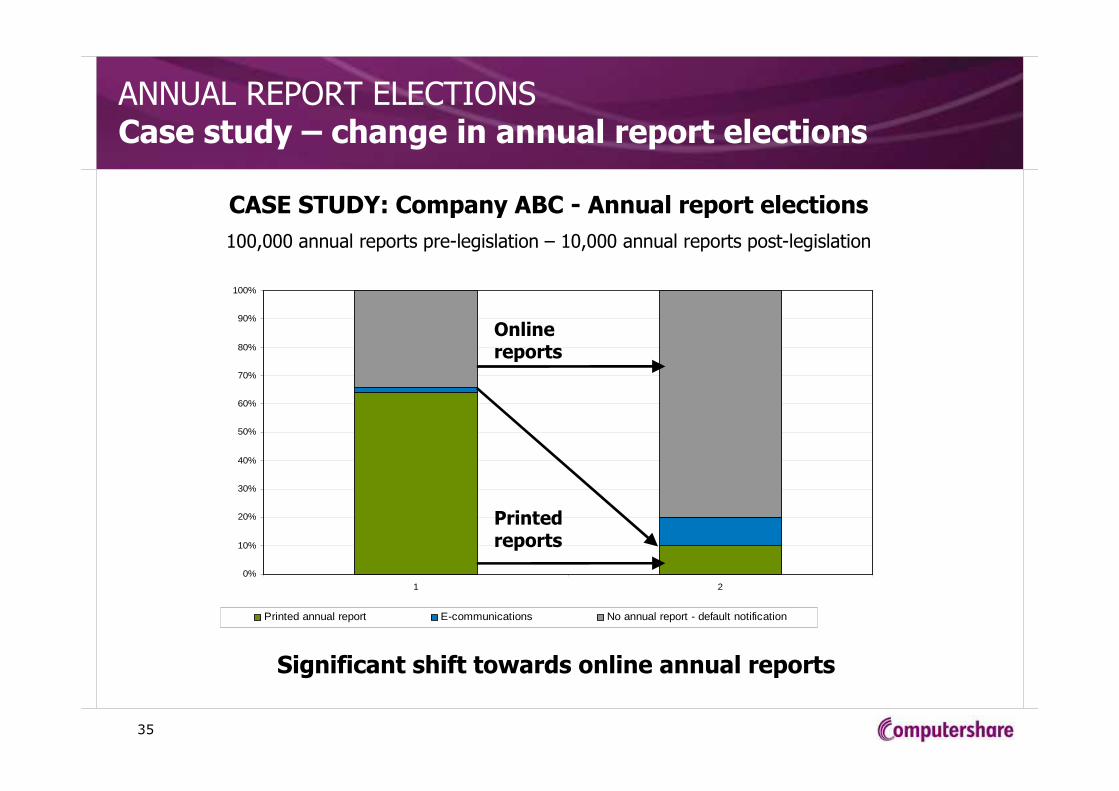

ANNUAL REPORT ELECTIONSCase study – change in annual report elections

CASE STUDY: Company ABC - Annual report elections

100,000 annual reports pre-legislation – 10,000 annual reports post-legislation

Significant shift towards online annual reports

Printed reports

Online reports

36

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

Current State Future State

Printing Postage AGM pack with no annual report

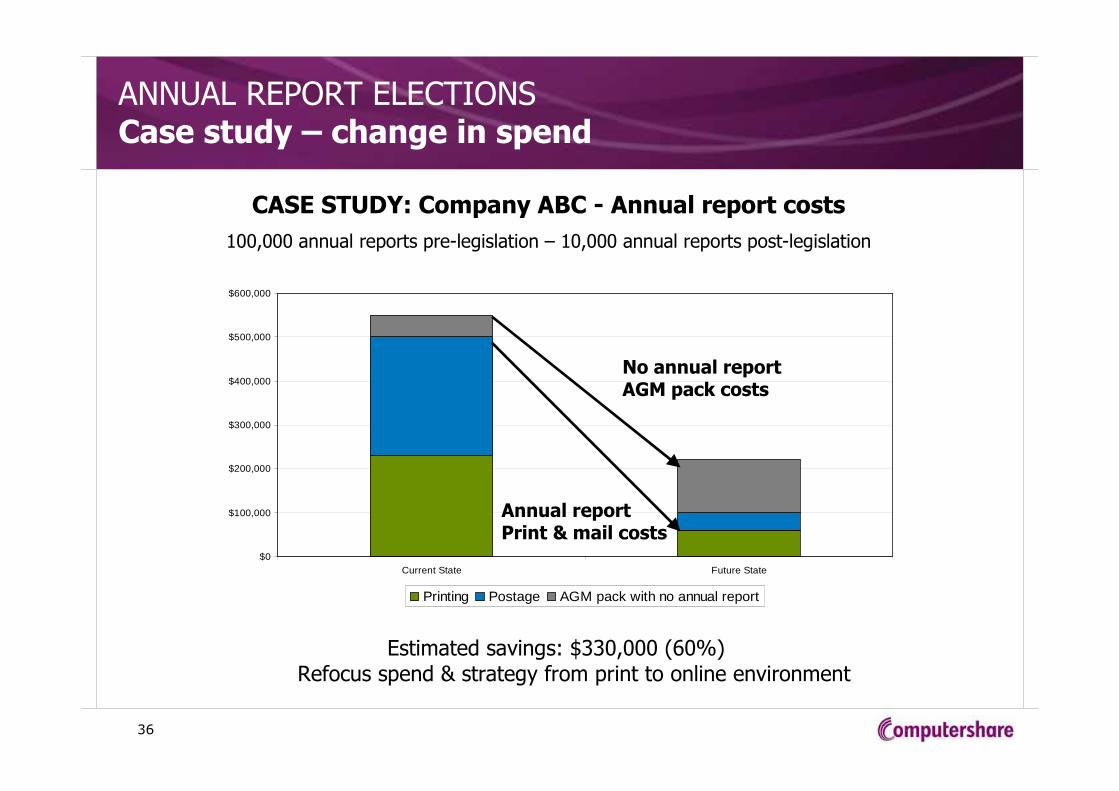

ANNUAL REPORT ELECTIONSCase study – change in spend

CASE STUDY: Company ABC - Annual report costs

100,000 annual reports pre-legislation – 10,000 annual reports post-legislation

Estimated savings: $330,000 (60%)Refocus spend & strategy from print to online environment

Annual report Print & mail costs

No annual report AGM pack costs

37

SUMMARY

� Legislation

� Annual report only, not proxy and NOM

� Election to receive a printed annual report is a standing request

� Holder must be notified when annual report becomes available online and be reasonably accessible

� Corporate reporting

� Not relevant – compliance driven and complex

� Industry dynamics

� Growing trend towards online channels – e-communications and self service

� Strategic options

� Improve web-based services, do more than dump a PDF of the annual report online

� Opportunities for alternative short form and interactive online annual reports

� Move to Easy Updates NSP, update proxy form, include email capture on the mandatory annual report election form (if possible)

38

Electronic Shareholder Communications

in

The United States

GLOBAL EXPERIENCE SHARING

39

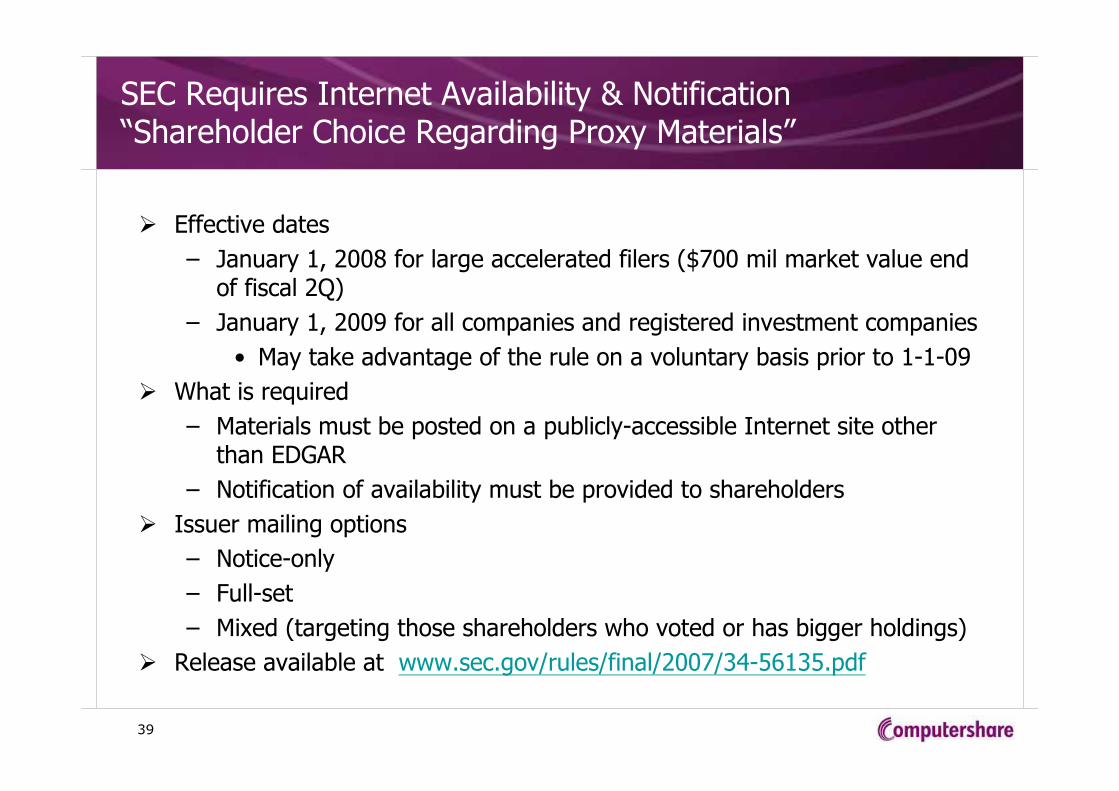

SEC Requires Internet Availability & Notification“Shareholder Choice Regarding Proxy Materials”

� Effective dates

– January 1, 2008 for large accelerated filers ($700 mil market value end of fiscal 2Q)

– January 1, 2009 for all companies and registered investment companies

• May take advantage of the rule on a voluntary basis prior to 1-1-09

� What is required

– Materials must be posted on a publicly-accessible Internet site other than EDGAR

– Notification of availability must be provided to shareholders

� Issuer mailing options

– Notice-only

– Full-set

– Mixed (targeting those shareholders who voted or has bigger holdings)

� Release available at www.sec.gov/rules/final/2007/34-56135.pdf

40

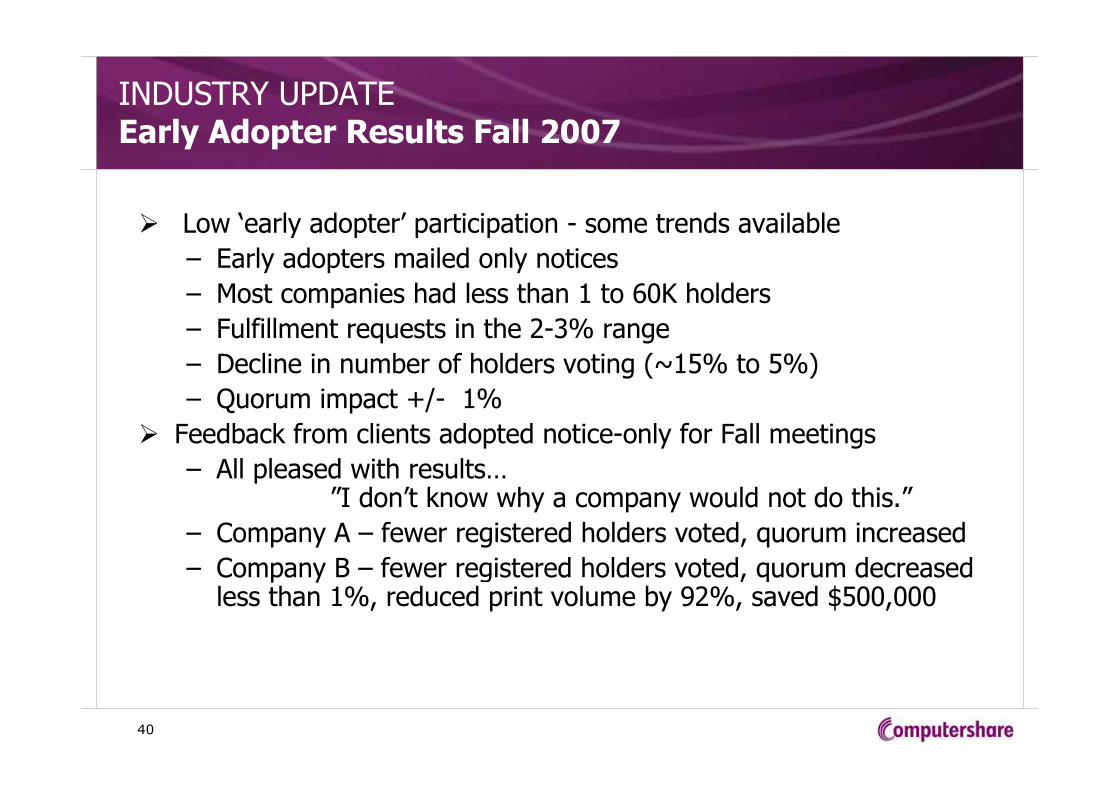

INDUSTRY UPDATEEarly Adopter Results Fall 2007

� Low ‘early adopter’ participation - some trends available

– Early adopters mailed only notices

– Most companies had less than 1 to 60K holders

– Fulfillment requests in the 2-3% range

– Decline in number of holders voting (~15% to 5%)

– Quorum impact +/- 1%

� Feedback from clients adopted notice-only for Fall meetings

– All pleased with results…”I don’t know why a company would not do this.”

– Company A – fewer registered holders voted, quorum increased

– Company B – fewer registered holders voted, quorum decreased less than 1%, reduced print volume by 92%, saved $500,000

41

INDUSTRY TRENDSIssuer Survey

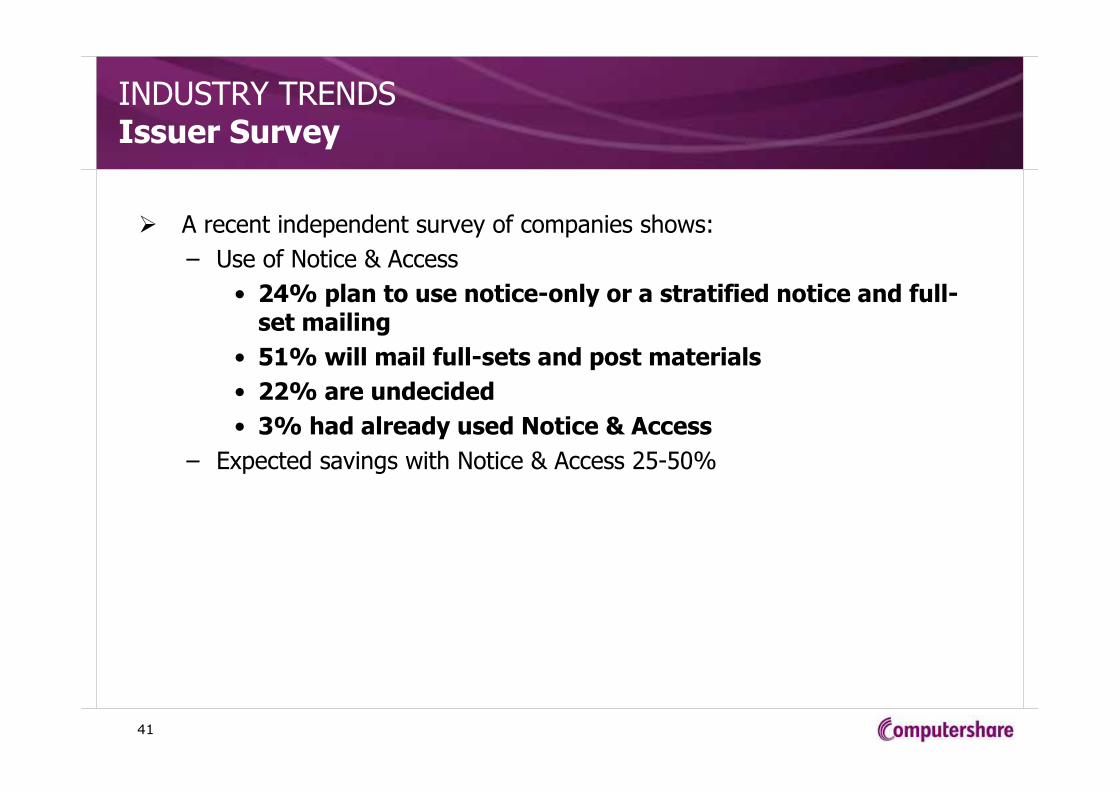

� A recent independent survey of companies shows:

– Use of Notice & Access

• 24% plan to use notice-only or a stratified notice and full-set mailing

• 51% will mail full-sets and post materials

• 22% are undecided

• 3% had already used Notice & Access

– Expected savings with Notice & Access 25-50%

42

Electronic Shareholder Communications

in

United Kingdom

GLOBAL EXPERIENCE SHARING

43

ELECTRONIC COMMUNICATIONS IN THE UK

� Changes in Companies Act 2006

� Received Royal Assent on 8 November 2006

� Disclosure and Transparency Rules - December 2006

� New eCommunications rules - 20th January 2007

� All provisions now in force

44

KEY CHANGES RELATING TO ELECTRONIC COMMUNICATION

� A company can make documents available on a website

� Shareholders can agree to receive documents electronically

OR

� If they have not responded within 28 days then ‘deemed consent’

� Always the option to ask for hard copy documents

� For listed companies, use of eComms must have been approved in general meeting (DTR 6.1.8 (1))

45

NOTICE OF AVAILABILITY

� Dividends› eComms and bank mandate – fully electronic› All others need notification

� Annual Report / NOMs / Proxy Forms› eComms – fully electronic; including

electronic proxy appointment and Annual Report on website

› Deemed Consent group – Notice of availability, optional proxy form and notice of meeting

� Interim Report

� Corporate Actions

46

IMPLEMENTATION ISSUES - ARTICLES

� Does the company have reference to eCommunication in its

Articles?

� If NO - still offer and encourage eCommunications but can’t use

website publication (the ‘deemed consent’ route)

� Even if Articles permit eCommunications - check that ‘deemed

consent’ is permissible

� Need to either change Articles or pass an enabling resolution

� Also, consider other possible changes (for example Information

Rights, multiple proxies and poll votes)

47

IMPLEMENTATION ISSUES –The Deemed Consent Mailing

� Simultaneous to the meeting where Articles are changed/resolution

passed, or separate mailing?

� Environmental concern likely to be a major incentive for

eCommunication

� Make the eCommunication option easy to use, more savings than

where shareholders opt to do nothing

� Email collection online or by mail

48

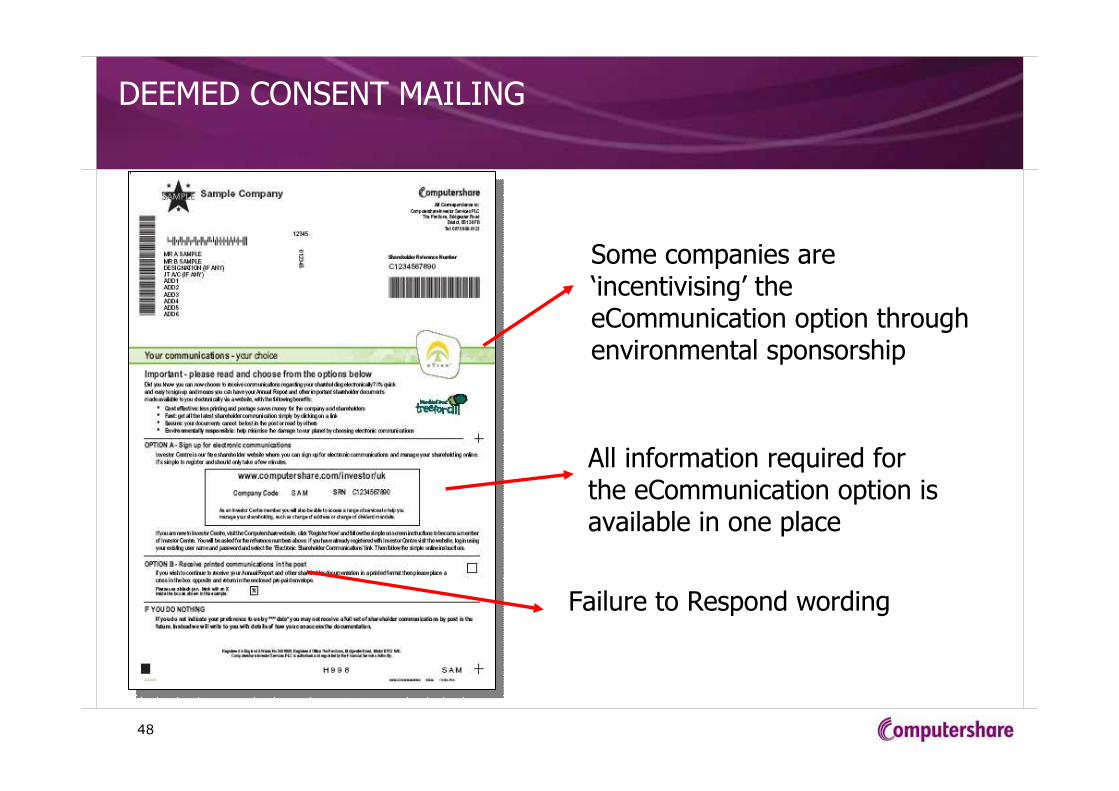

DEEMED CONSENT MAILING

Some companies are ‘incentivising’ the eCommunication option through environmental sponsorship

All information required for the eCommunication option is available in one place

Failure to Respond wording

49

IMPLEMENTATION ISSUES –New Shareholders

› Deemed Consent mailing - 12 month minimum interval

› New shareholders joining after the dispatch date

› Care – Operational complexity of multiple anniversaries

› Encourage eCommunication on all mailings

› ICSA recommended best practice is to consult no more than every

other mailing cycle

50

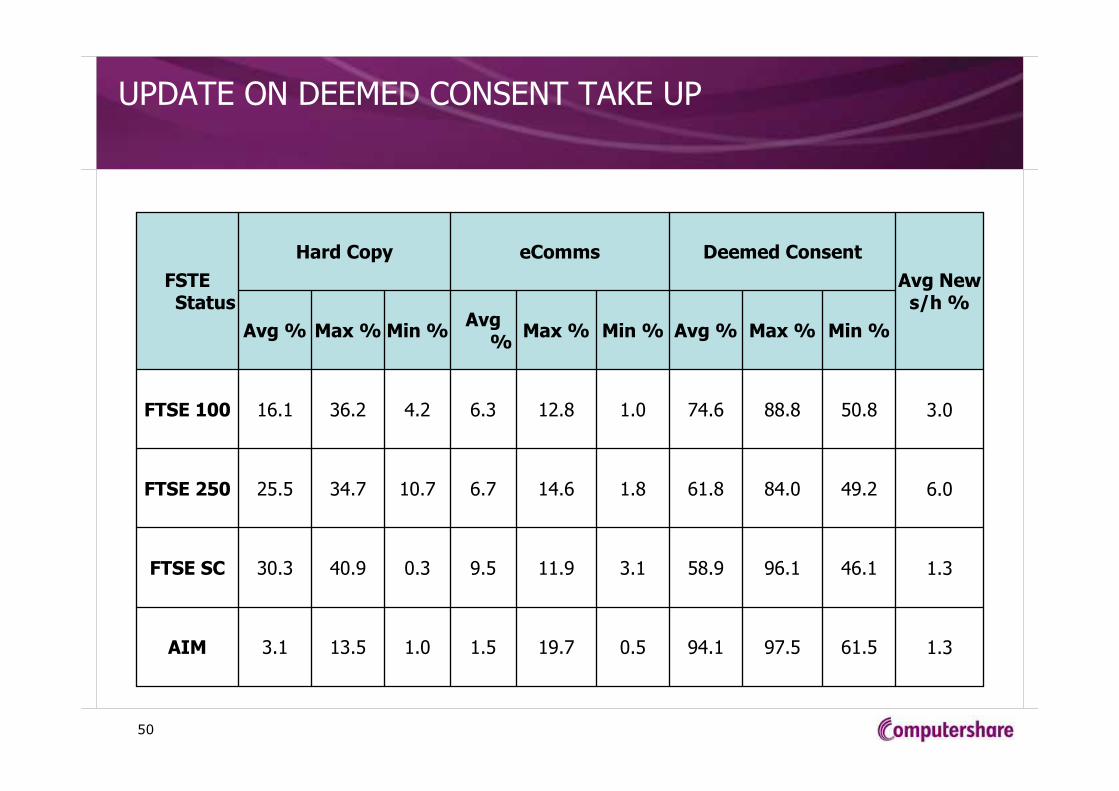

UPDATE ON DEEMED CONSENT TAKE UP

1.361.597.594.10.519.71.51.013.53.1AIM

1.346.196.158.93.111.99.50.340.930.3FTSE SC

6.049.284.061.81.814.66.710.734.725.5FTSE 250

3.050.888.874.61.012.86.34.236.216.1FTSE 100

Min %Max %Avg %Min %Max %Avg

%Min %Max %Avg %

Avg News/h %

Deemed ConsenteCommsHard Copy

FSTE Status

51

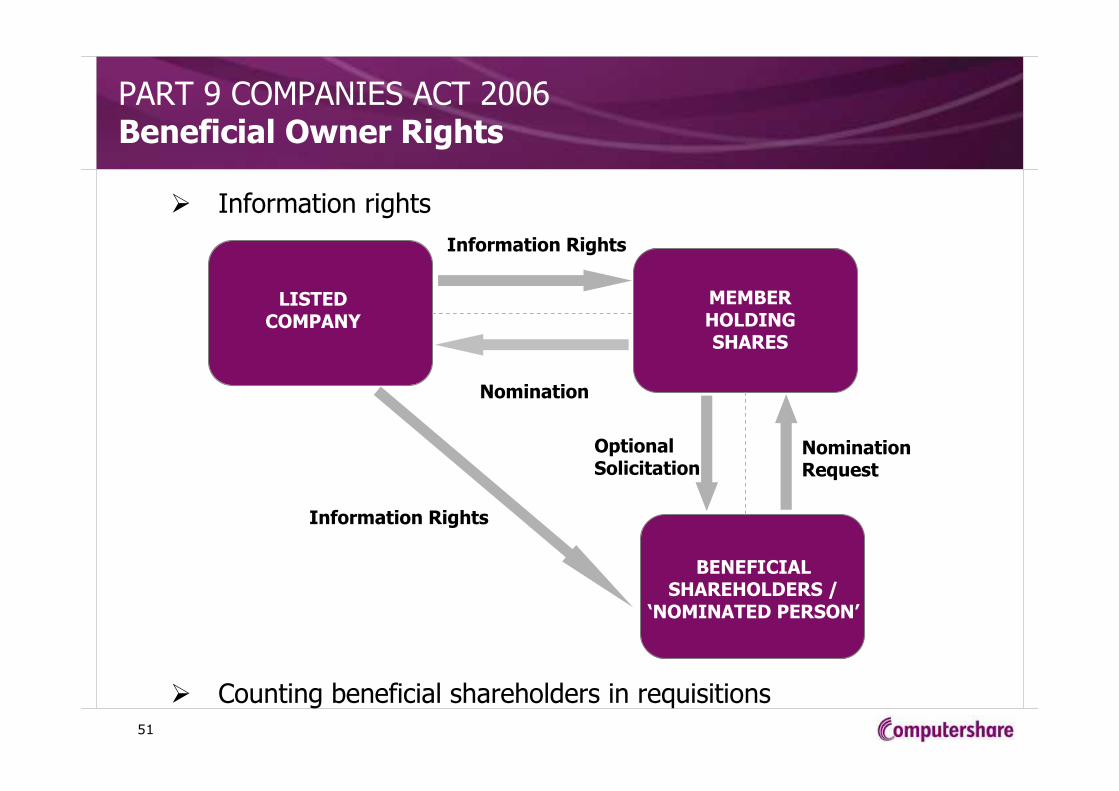

PART 9 COMPANIES ACT 2006Beneficial Owner Rights

� Information rights

� Counting beneficial shareholders in requisitions

LISTED COMPANY

BENEFICIAL SHAREHOLDERS /

‘NOMINATED PERSON’

MEMBER HOLDING SHARES

Information Rights

Nomination

Nomination Request

Information Rights

Optional Solicitation

52

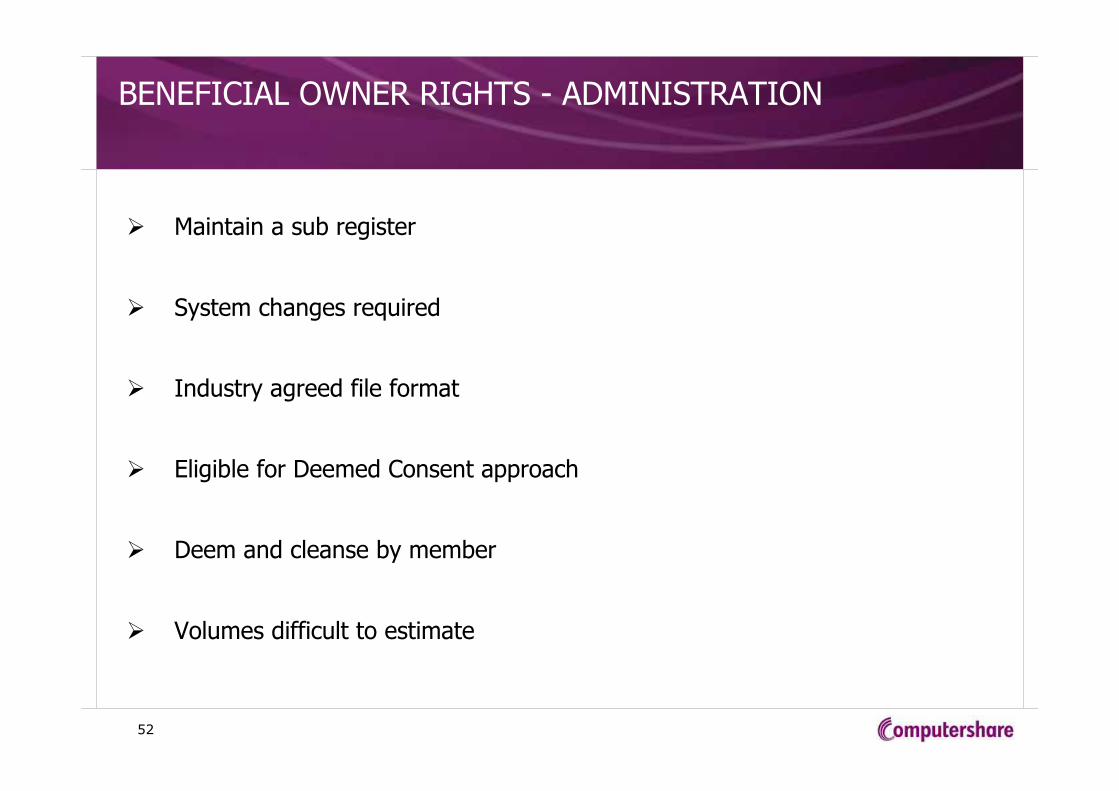

BENEFICIAL OWNER RIGHTS - ADMINISTRATION

� Maintain a sub register

� System changes required

� Industry agreed file format

� Eligible for Deemed Consent approach

� Deem and cleanse by member

� Volumes difficult to estimate

53

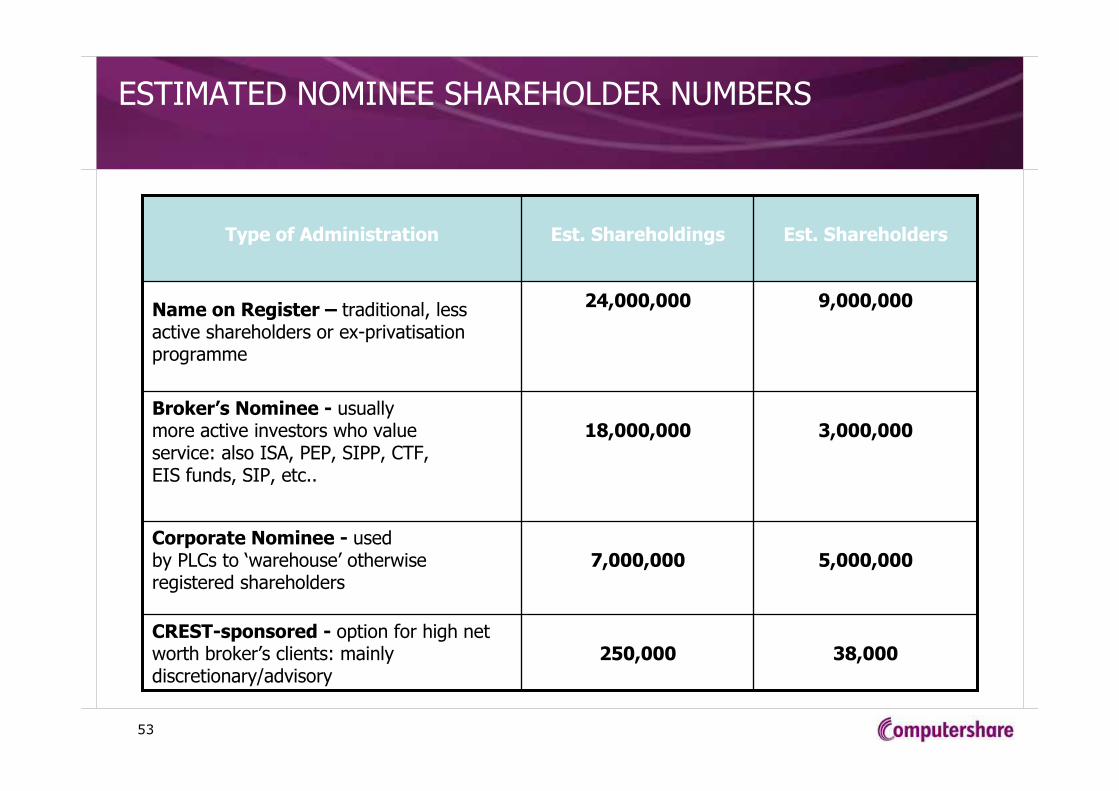

ESTIMATED NOMINEE SHAREHOLDER NUMBERS

38,000250,000CREST-sponsored - option for high net worth broker’s clients: mainly discretionary/advisory

5,000,0007,000,000Corporate Nominee - used by PLCs to ‘warehouse’ otherwise registered shareholders

3,000,00018,000,000Broker’s Nominee - usually more active investors who value service: also ISA, PEP, SIPP, CTF, EIS funds, SIP, etc..

9,000,00024,000,000Name on Register – traditional, less active shareholders or ex-privatisation programme

Est. ShareholdersEst. ShareholdingsType of Administration

54

BENEFICIAL OWNER RIGHTS

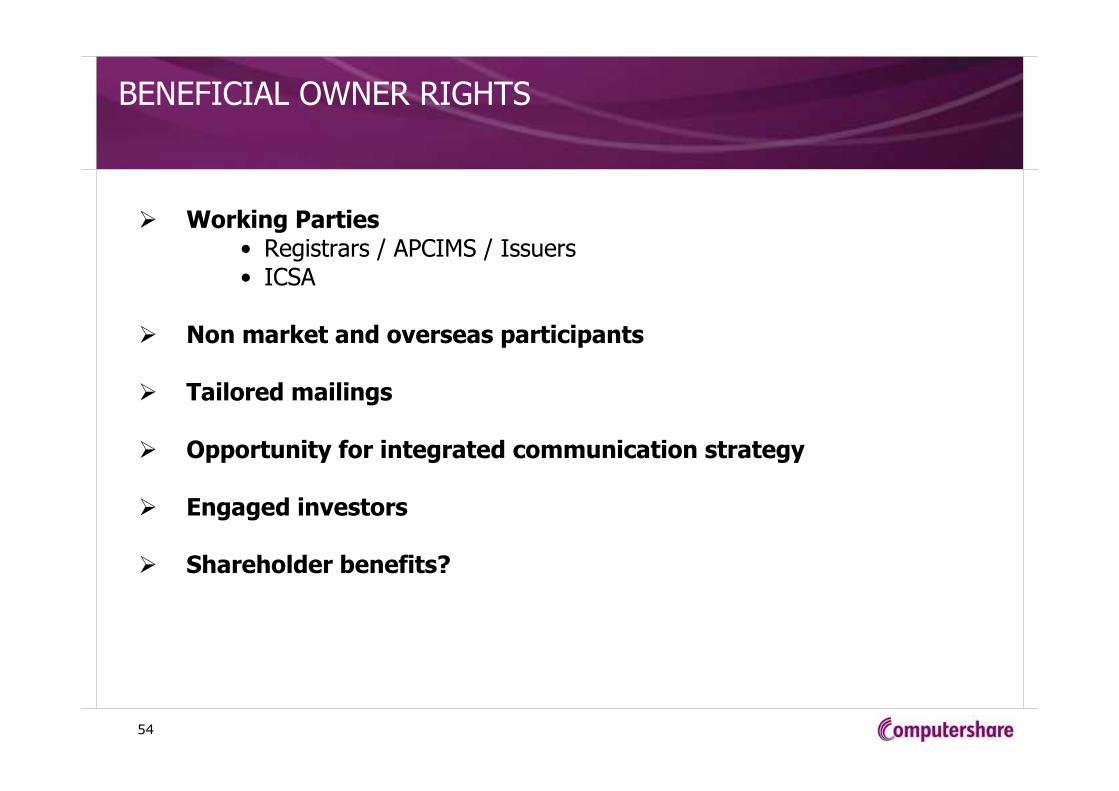

� Working Parties• Registrars / APCIMS / Issuers• ICSA

� Non market and overseas participants

� Tailored mailings

� Opportunity for integrated communication strategy

� Engaged investors

� Shareholder benefits?

55

ELECTRONIC COMMUNICATIONS IN THE UK

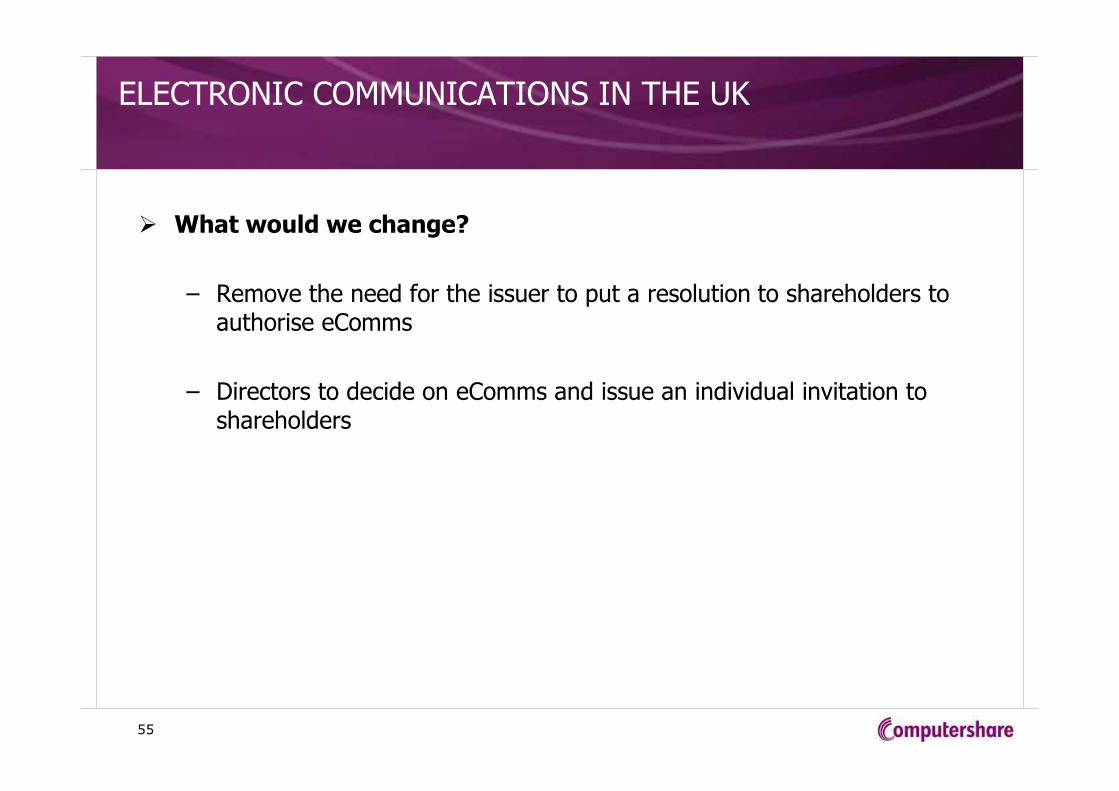

� What would we change?

– Remove the need for the issuer to put a resolution to shareholders to authorise eComms

– Directors to decide on eComms and issue an individual invitation to shareholders

56

Best Practice Proposals

for

Hong Kong

57

PROPOSED RESPONSE TO THE CONSULTATION

� Currently the HKEx proposal is based on the UK model but there are learning points we can pick up from implementation in US and AU

� 1.20(a) requires the shareholder communication to be hosted on the issuer’s own website. We suggest issuers should be allowed to appoint service providers (using the issuer’s URL) to enable greater flexibility

� New shareholders should be provided with a “mandatory election notice” with the ability to complete online. This should be implemented at the same time as the existing shareholders receive the election notice.

58

PROPOSED RESPONSE TO THE CONSULTATION

� 1.23(d) Generally emails are unauthenticated and unformatted, wesuggest making other more effective and automated processes (e.g. machine readable documents) or self-service channels (e.g. web site & IVRS) available for shareholders to change their elections;

� 1.24. HK incorporated companies cannot yet benefit from the proposed Listing Rules changes on Shareholder Communication. Companies Ordinance needs to be enabled for e-communication

� 1.25. Once electronic communication is in place, communication by CD ROM would become obsolete, so this part of the proposal would not be required

� We suggest that the proposals should be extended to allow electronic proxy voting as in all other countries

� We suggest that the proposals should be extended to cover beneficial shareholders

59

GLOBAL BEST PRACTICES IN CORPORATE GOVERNANCE

� Researches show that companies with good corporate governance would get a premium in their stock market valuation

� Often shareholders are also the company’s customers

� All shareholders should be treated equally, there must be equal rights to have access to communication and participate in voting

� Shareholder rights are best reflected in their ability to exercise their voting rights

� To encourage shareholders to participate in voting, the proxy process must be made as easy as possible. A good alternative is to offer electronic proxy – appointing proxies via the internet

� A prerequisite is for transparency of names, addresses and holdings of direct and beneficial shareholders at the time meeting notices are distributed

60

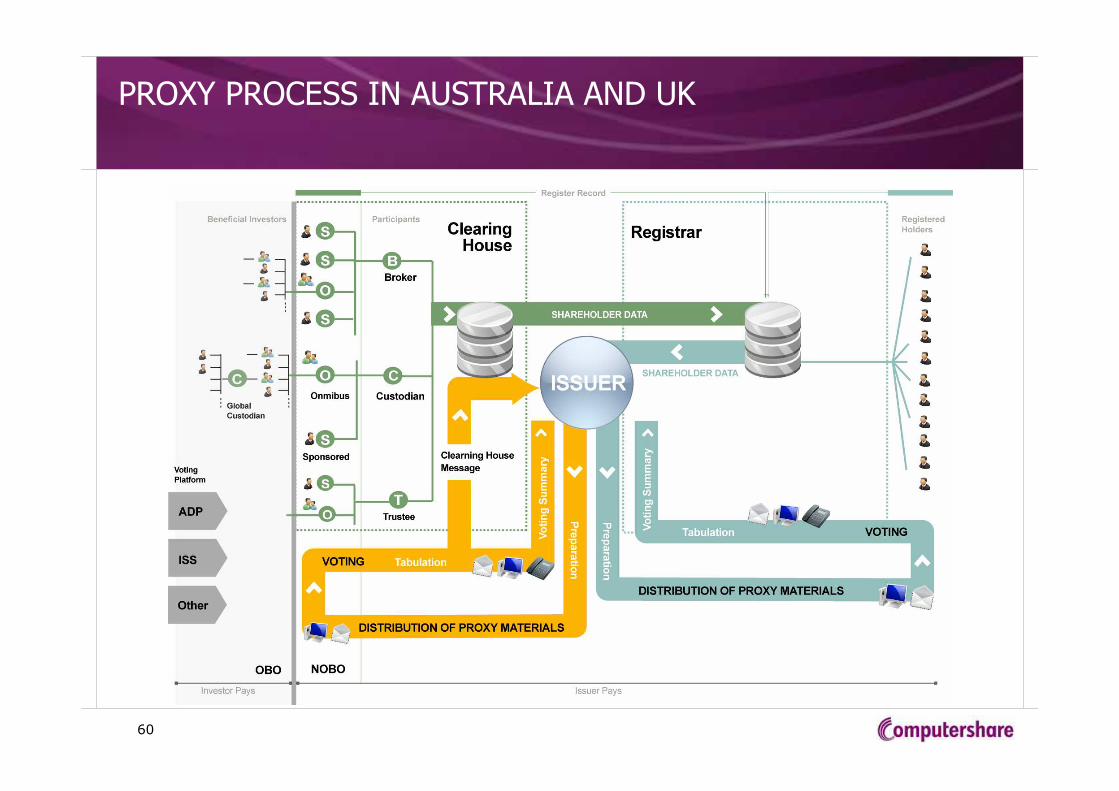

PROXY PROCESS IN AUSTRALIA AND UK

61

WAY FORWARD

� The HKEx Listing Rules changes proposal is a move in right direction

� However corresponding changes in HK Companies Ordinance would also be required so that HK companies can benefit

� SFC and HKEx should work with issuers and registrars on improving beneficial shareholder transparency and extend corporate communication / proxy voting service to them directly

� We will continue to work with issuers to migrate more shareholder service to e-channels and enhance shareholder experience, while generating cost savings and protecting the environment

62

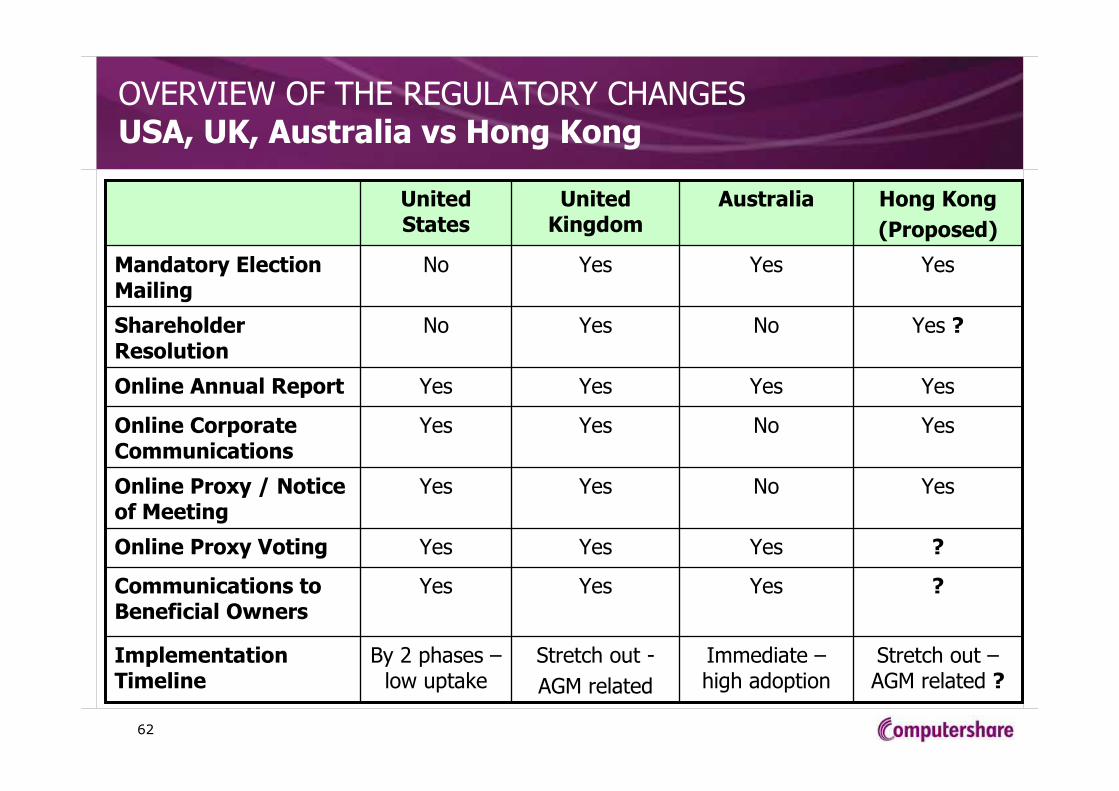

OVERVIEW OF THE REGULATORY CHANGESUSA, UK, Australia vs Hong Kong

Stretch out –AGM related ?

?

?

Yes

Yes

Yes

Yes ?

Yes

Hong Kong

(Proposed)

Immediate –high adoption

Stretch out -

AGM related

By 2 phases –low uptake

Implementation Timeline

NoYesNoShareholder Resolution

YesYesYesCommunications to Beneficial Owners

YesYesYesOnline Proxy Voting

NoYesYesOnline Proxy / Notice of Meeting

NoYesYesOnline Corporate Communications

YesYesYesOnline Annual Report

YesYesNoMandatory Election Mailing

AustraliaUnited Kingdom

United States

63

Benefits to Hong Kong Issuers

ELECTRONIC SHAREHOLDER COMMUNICATIONS

64

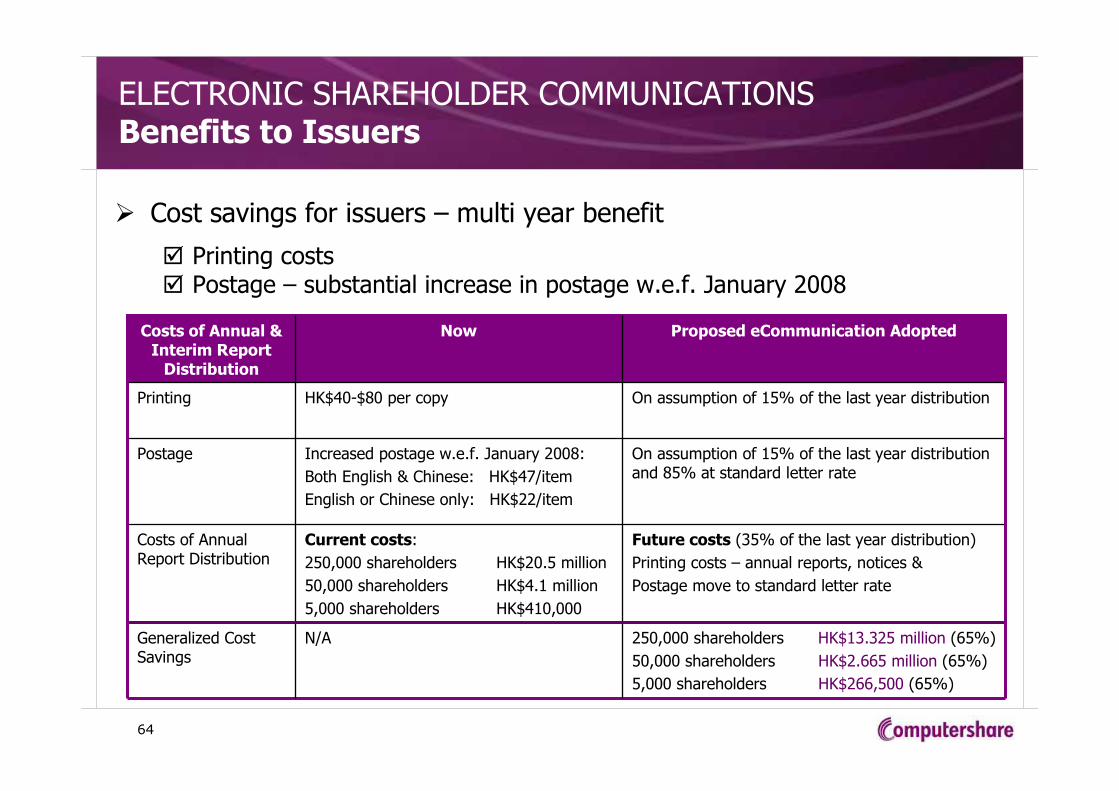

ELECTRONIC SHAREHOLDER COMMUNICATIONSBenefits to Issuers

� Cost savings for issuers – multi year benefit

� Printing costs� Postage – substantial increase in postage w.e.f. January 2008

Future costs (35% of the last year distribution)

Printing costs – annual reports, notices &

Postage move to standard letter rate

Current costs:

250,000 shareholders HK$20.5 million

50,000 shareholders HK$4.1 million

5,000 shareholders HK$410,000

Costs of Annual Report Distribution

250,000 shareholders HK$13.325 million (65%)

50,000 shareholders HK$2.665 million (65%)

5,000 shareholders HK$266,500 (65%)

N/AGeneralized Cost Savings

On assumption of 15% of the last year distribution and 85% at standard letter rate

Increased postage w.e.f. January 2008:

Both English & Chinese: HK$47/item

English or Chinese only: HK$22/item

Postage

On assumption of 15% of the last year distributionHK$40-$80 per copyPrinting

Proposed eCommunication AdoptedNowCosts of Annual & Interim Report

Distribution

65

� Case Study:

• Listed Issuer ‘A’ in HK with circa. 50,000 shareholders moved to electronic distribution of AGM pack

• 88% of shareholders have agreed to receive corporate communications via web site (by positive confirmation or being ‘deemed’ to have consented to e-communication)

• Still need to deal with the beneficial shareholders held under CCASS

ELECTRONIC SHAREHOLDER COMMUNICATIONSBenefits to Issuers

66

ISSUER STRATEGY

� Identify Drivers• Cost savings

• Corporate Social Responsibility impact

• Opportunity to review the existing shareholder communications

� Considerations• Use of integrated online solutions for Issuers and Investors

• The response rate to election mailing determines the cost savings – cultural difference between the Chinese community and the Western countries

� Planning• Timeline:

- Issuers incorporated outside HK: subject to the provisions under the jurisdictions of the place of incorporation to make available the electronic corporate communications

- Issuers incorporated in HK: await Companies Ordinance changes

• Annual report strategy - Shareholders deemed consent to ecomm can request for hard copy materials

- Our global experience suggested that only 15% of the shareholders want full hard copy packages

67

COMPUTERSHARE’s CUSTOMIZED ISSUER SERVICE SOLUTIONSOne-Stop Shareholder Communication Services

Print and Mail Web Hosting

Call Centre Interactive Voice Response System

Solutions for hard copy materials

Solutions for online materials & voting

Solutions for phone inquiries

Automated self-service phone services

68

COMPUTERSHARE’S CUSTOMIZED ISSUER SERVICE SOLUTIONSIntegrated Issuer and Investor Solutions

� Achieve optimal efficiency through integrated issuer and investor solutions:

� Issuer Online – provide critical information to issuers via internet on a timely basis e.g. information for issued capital report filing

� Investor Centre – promote the use of electronic communications and self-service channels for a broader range of investor information maintenance (e.g. change of address, dividend mandate, etc.) and transactions (e.g. proxy, corporate actions election, etc.) via internet and IVRS

69

WHAT’s NEXT?

� We will respond to the consultation paper and actively consult HKEx on the basis of our global experience

� Lobby the Government for the inclusion of the changes in the Companies Ordinance

� We have provided you with the Communication Package used in Australia to assist in your planning

70

QUESTIONS?

� Question-and-Answer

� If you have further questions, please contact your Relationship Manager at Computershare:

Ellen NgExecutive DirectorTel: 2862 8502Email: [email protected]

Romy ChengVice President Client ServicesTel: 2862 8508Email: [email protected]

Flora TseVice President Client ServicesTel: 2862 8530Email: [email protected]

Ada Lai-FockVice President Client ServicesTel: 2862 8504Email: [email protected]

Edrick YuAssistant Vice President Client ServicesTel: 2862 8604Email: [email protected]

Leslie LauAssistant Vice President Client ServicesTel: 2862 8621Email: [email protected]

Shawn ChanAssistant Vice President Client ServicesTel: 2862 8514Email: [email protected]

Julie ChuAssistant Vice President Client ServicesTel: 2862 8522Email: [email protected]

71