Embed Size (px)

Citation preview

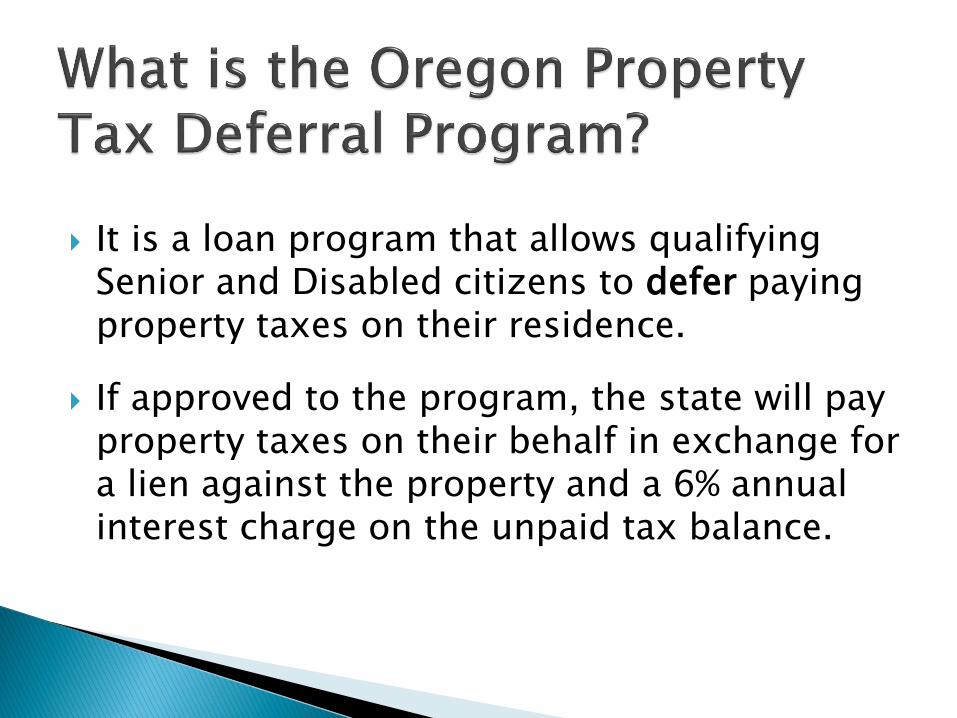

It is a loan program that allows qualifying Senior and Disabled citizens to defer paying property taxes on their residence.

If approved to the program, the state will pay property taxes on their behalf in exchange for a lien against the property and a 6% annual interest charge on the unpaid tax balance.

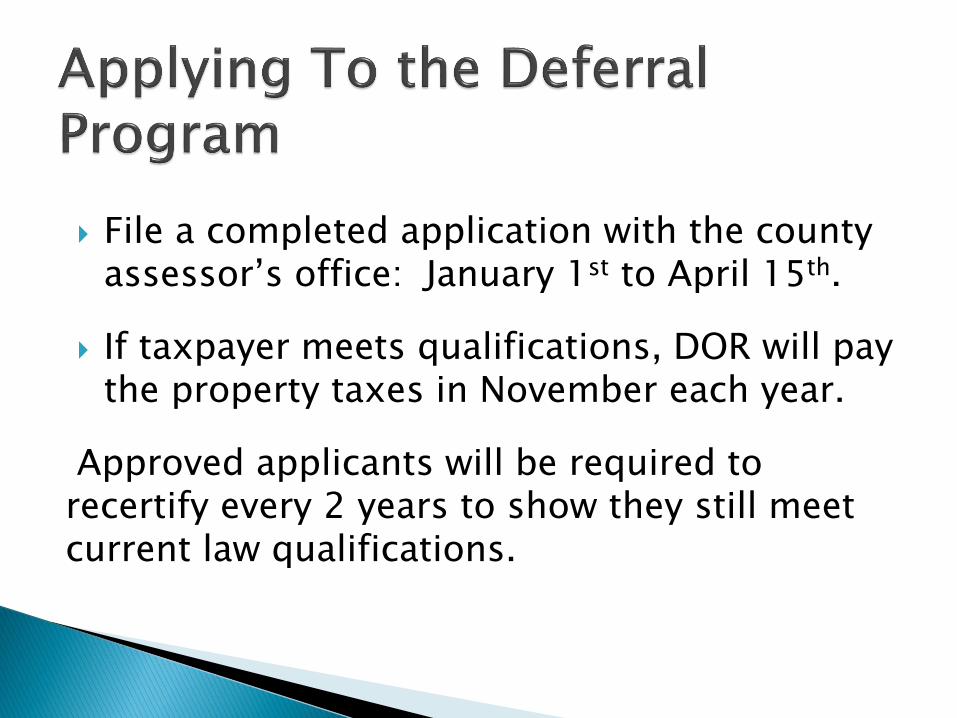

File a completed application with the county assessor’s office: January 1st to April 15th.

If taxpayer meets qualifications, DOR will pay the property taxes in November each year.

Approved applicants will be required to recertify every 2 years to show they still meet current law qualifications.

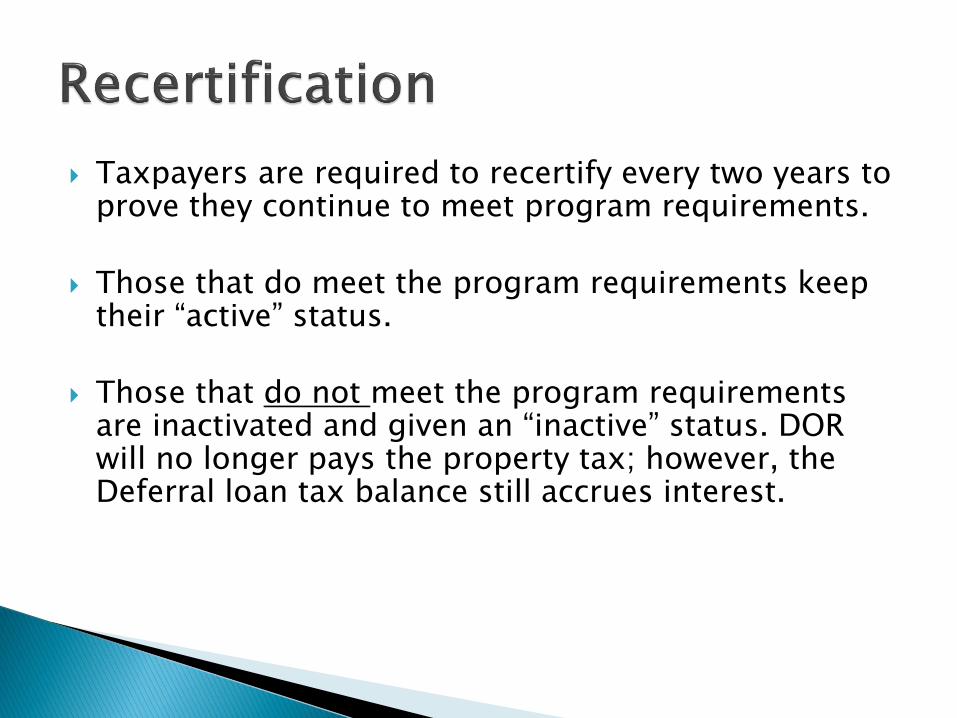

Taxpayers are required to recertify every two years to prove they continue to meet program requirements.

Those that do meet the program requirements keep their “active” status.

Those that do not meet the program requirements are inactivated and given an “inactive” status. DOR will no longer pays the property tax; however, the Deferral loan tax balance still accrues interest.

Taxpayers are inactivated from the program if:

o Income too high.

o Excessive Assets.

o No property insurance.

o Requested information was not provided.

o A failure to recertify.

o Property RMV exceeds limitation based on years lived & owned.

o Trust wasn’t provided.Trust is Irrevocable.

Clauses within the Trust could render it Irrevocable.

o A surviving spouse was not 59 ½ /disabled at time of the death.

Recertification notices (form/letter) are sent out early February. Our program participants have 65 days, from the date on the letter, to respond with recertifying. If they fail to respond or no longer meet program requirements, they become ineligible for the program. Their status becomes: Inactive.

Those failing to respond may petition the Department of Revenue Director for a retroactive deferral under ORS 311.681

Those not meeting program requirements can reapply with an application during the filing season, to attempt to get their “active” status back on the program.

2015 Legislature added a requirement that the Department of Revenue notify the Aging and Disability Resource Connection (ADRC) for those that have not recertified within 35 days of the Recertification notice.

Weekly updated reports are provided to ADRC, as they assist in reaching out to our program participants with their recertification process.

Applicants disqualify from the program if: ◦ The taxpayer dies.

◦ The property is sold (or changes ownership).

◦ The taxpayer moves from the property for other than health related reasons.

◦ The home is moved out of state (manufactured structures or floating home)

Inception date of 1963

Self-Sustaining Program

Legislation transferred $250,000 (2006) and $14.3 million (2008) to Oregon Project Independence (OPI)

The forecast of the program revealed it would no longer be self-sustaining.

Factors:

1. Dropping home values.

2. Decline in home sales that reduced the program cash flow.

3. Increased program participation.

Delayed payment to counties of the 2010 property taxes.

May 2011, deferral account had a zero balance.

SB 939 (2011) – Oregon State Treasury loaned $19 million to deferral program.

HB2543 (2011)- Structural Changes.

Program Requirements Prior to HB2543:

1. Age (62 or older) or Disabled.

2. Income-Federal Adjusted Gross Income (FAGI).

3. Ownership of Property.

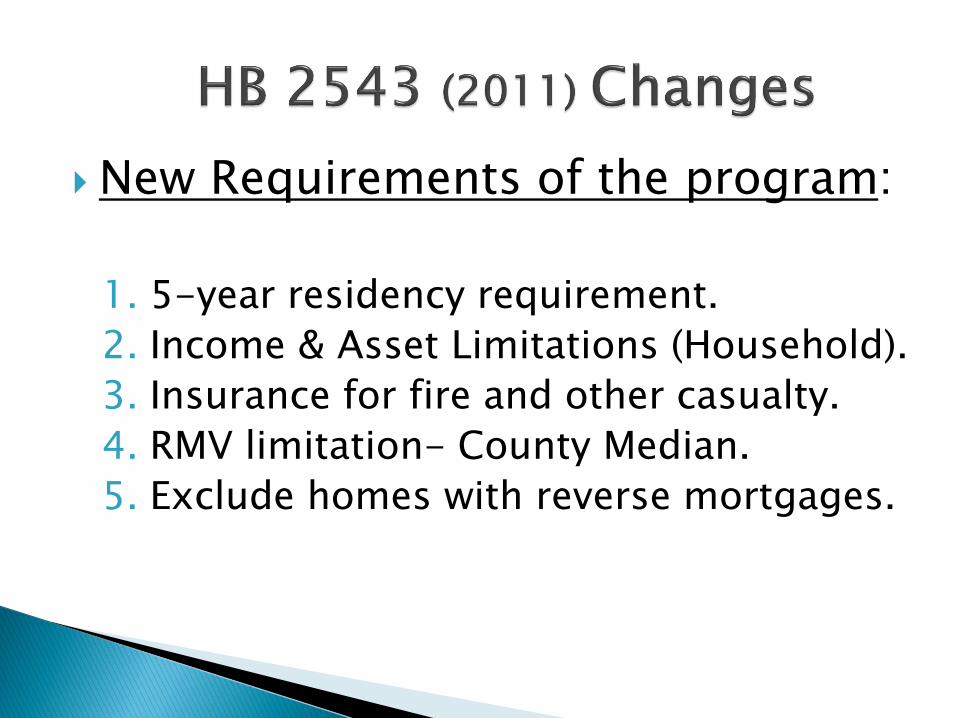

New Requirements of the program:

1. 5-year residency requirement.

2. Income & Asset Limitations (Household).

3. Insurance for fire and other casualty.

4. RMV limitation- County Median.

5. Exclude homes with reverse mortgages.

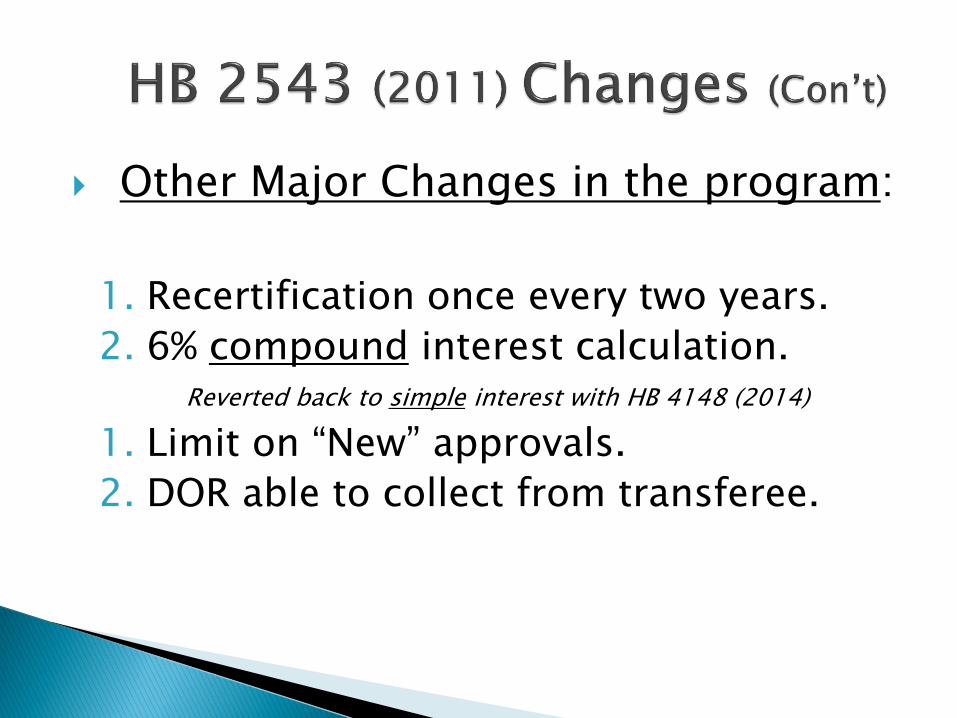

Other Major Changes in the program:

1. Recertification once every two years.

2. 6% compound interest calculation.Reverted back to simple interest with HB 4148 (2014)

1. Limit on “New” approvals.

2. DOR able to collect from transferee.

Program participation dropped due to increased requirements.

Upset taxpayers.

Thousands of calls/emails to DOR, Legislators, and the Counties.

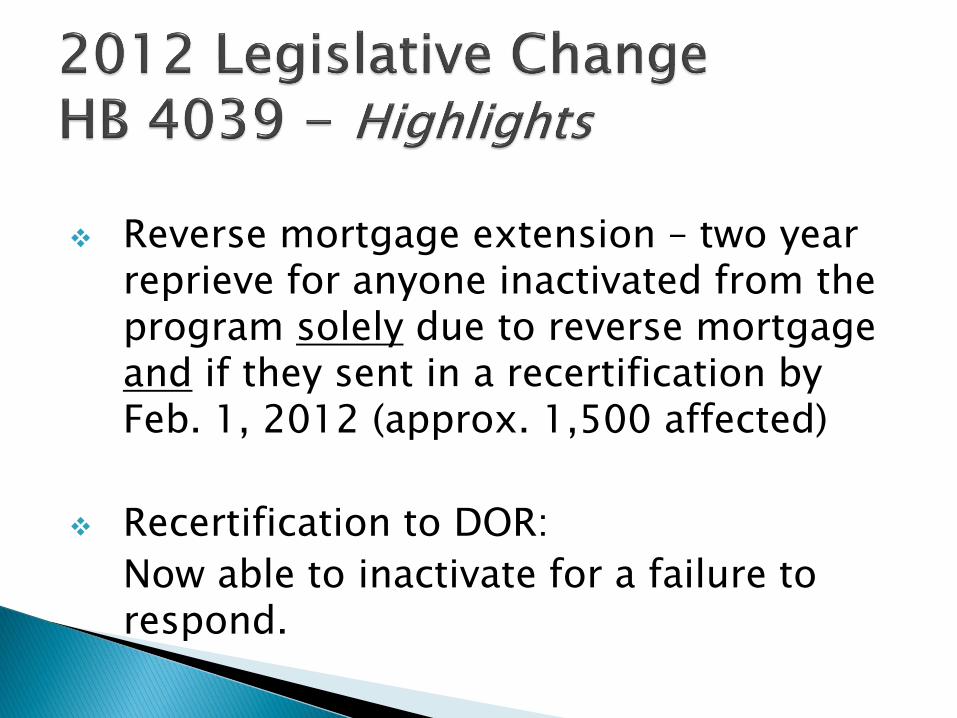

❖ Reverse mortgage extension – two year reprieve for anyone inactivated from the program solely due to reverse mortgage and if they sent in a recertification by Feb. 1, 2012 (approx. 1,500 affected)

❖ Recertification to DOR:

Now able to inactivate for a failure to respond.

HB 2489

HB 2510

Allows for a permanent inclusion for the HB 4039 cohort (approx. 1,500) even though they have a reverse mortgage.

Amends the laws that address collection from a transferee.

Allows participants who were inactivated in 2011 solely due to having a reverse mortgage, or not meeting the 5-year residency requirement, or both, to participate again starting 1/1/2014.

New participants are limited to 700 for the 2014/15 property tax year, with an allowed growth of 5% each year thereafter.

Change Delay of Foreclosure; not just delaying years prior to entry into the program. May cover any delinquent taxes prior to any “approval” in the program.

Revert back to simple interest by 2016.

We will recalculate all accounts when we convert to our new system December, 2015.

Added provisions for deferral participants to be able to “downsize” and move to a new home and waive the 5 year minimum residency requirement, as long as certain criteria is met.

If you have interested participants, have them call DOR.

➢ Allows DOR to purchase insurance for the deferral claimants who have insurable homes but do not otherwise have homeowner’s insurance. Cost will be added to the lien.

➢ Directs DOR to notify Aging Services for those participants who have been asked to recertify, but who have not responded within 35 days.

➢ Percent of County median RMV is increased for claimants having owned and lived in their homes for more than 20 years:

Address: Oregon Department of RevenueAttn: Deferral UnitPO Box 14380Salem, OR 97309

Phone: 503-945-8348Fax: 503-945-8737Email: [email protected]

Website: www.Oregon.gov/dor/deferral

ORS 311.666(10): The collection of deferral debt from “transferees” of the estate of deceased persons who had previously been on property tax deferral.

ORS 311.668(1): We now require a complete copy of any trust connected with the deferral program.

ORS 311.666(2): We can no longer allow ”adjoining tax lots having a common feature”.

The homestead = dwelling & the tax lot underneath.