Embed Size (px)

Citation preview

LexisNexis® Company Law Guide 2017-2018

Including articles from featured contributors:

LexisNexis® Foreign Investment Law Guide 2017-2018

The ultimate complimentary guide to understanding foreign investment practices around the world with an Asia-Pacific focus

Including articles from featured contributors:

NEW DELHI Second Floor, 254, Okhla Industrial Estate, Phase III, New Delhi-110020 Tel: +91 11 4983 0000 Fax: +91 11 4983 0099 Email: [email protected] Website: www.phoenixlegal.in

MUMBAI Vaswani Mansion, Office No. 17 & 18, 3rd Floor, 120 Dinshaw Vachha Road, Churchgate, Mumbai – 400 020 Tel: +91 22 43408500 Fax: +91 22 43408501 Email: [email protected] Website: www.phoenixlegal.in

CHENNAI Seethakathi Business Centre, 9th Floor, Office Number 2B # 684-690, Anna Salai, Chennai-600 006 Tel: +91 44 2829 4626 Email: [email protected] Website: www.phoenixlegal.in

“It’s hard to think of areas where Phoenix Legal can improve. The firm is better than nearly all legal firms…” - Asia Law Profiles

PRACTICE AREAS ü Antitrust and

Competition ü Banking and Finance ü CMT ü Commercial

Contracts ü Corporate and Securities Laws ü Dispute Resolution -

Arbitration and Litigation ü Energy, Oil and Gas ü Environment ü Employment and

Industrial Relations ü Foreign Investment

and Exchange Control ü Infrastructure and

Project Finance ü Intellectual Property ü International Trade ü Information

Technology & Outsourcing ü Insurance ü Joint Ventures,

Foreign and Technical Collaborations ü Mergers and

Acquisitions ü Mining and

Resources ü Private Equity and

Funds ü Real Estate ü Regulatory Affairs ü Taxation ü Legal Compliance,

Bribery & Anti-Corruption ü Corporate Insolvency

and Restructuring

Phoenix Legal is a full service Indian law firm offering transactional, regulatory, advisory, dispute resolution and tax services. The firm advises a diverse clientele including domestic and international companies, banks and financial institutions, funds, promoter groups and public sector undertakings. Phoenix Legal was formed in 2008 and now has 15 Partners and 75 lawyers in its three offices (New Delhi, Mumbai and Chennai) making it one of the fastest growing law firms of the country.

Why Phoenix Legal?

What distinguishes the firm from its peers is the approach which is:

High Degree of Partner Involvement and Availability – We assure to our clients, partner involvement in all deals and transactions, at all times.

High Quality Legal Advice – We deliver services of the highest quality, which are capable of meeting the most exacting standards.

Availability and Responsiveness – We are proactive in our approach and are available to our clients at all times.

Legal Research and Analysis Based Advisory – While we do keep abreast of market practices applicable to legal interpretation, they are adopted and recommended only if they are supported by prevailing legal and regulatory framework.

Key Accolades In the short span of existence, the firm has firmly established itself in the Indian legal market and has received wide media recognition. Some of the key accolades include:

:

:

Highest client satisfaction rating amongst top 20 Indian law firms -2013 Indian Law Firm Ranking and Report by RSG Consulting

Best Firm in India Asia Women in Business LawAwards, 2016, Euromoney, Hong Kong

Winner in the category: Energy, Projects &Infrastructure - India Business Law JournalIndian Law Firm Awards 2014

Winner in the category: Finance Law - FinanceLaw Firm of the Year – India: Corporate INTLLegal Awards 2013

Highly recommended as a leading firm Variouspractice areas, Chambers Asia Pacific – 2012,2013, 2014, 2015, 2016 and 2017

Shortlisted as one of the Indian firms forChambers Asia Pacific Awards 2014 and 2015organised by Chambers & Partners

Highest client satisfaction rating amongst top 20Indian law firms - 2013 Indian Law Firm Rankingand Report by RSG Consulting

IBLJ, Indian Law Firm Award 2016 - Energy, projects & infrastructure, structured finance & securitization

Winner in the category: Finance Litigation LawFirm of The Year – India – Global Awards for2014 - Corporate Livewire

LexisNexis® Foreign Investment Law Guide 2017-2018

Contents

Jurisdictional Q&As:

Australia – Atanaskovic Hartnell .......................................................... 10

Bangladesh – The Legal Circle .............................................................. 18

India – Phoenix Legal ............................................................................ 29

Indonesia – Hutabarat Halim & Rekan ................................................ 42

Japan – STW & Partners ....................................................................... 52

Macau – Rato, Ling, Lei & Cortés Advogados ..................................... 66

Mauritius – BLC Robert & Associates ................................................... 76

Myanmar – MHM Yangon .................................................................... 92

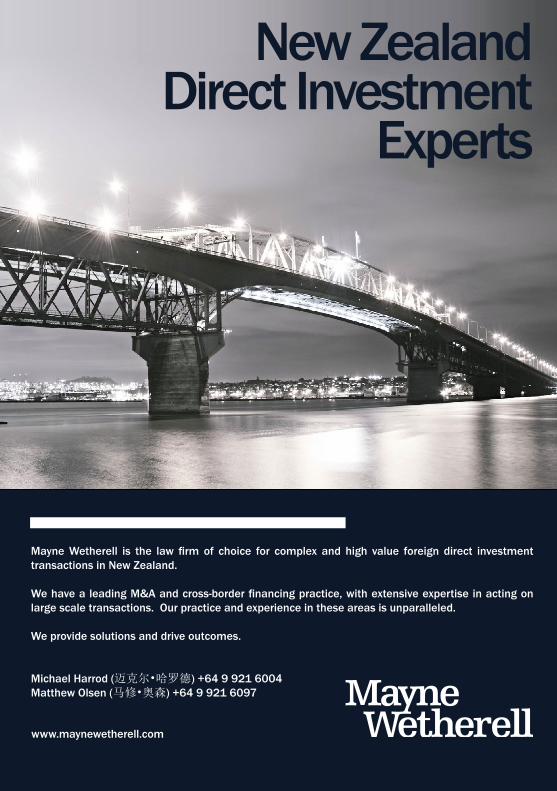

New Zealand – Mayne Wetherell....................................................... 105

Nigeria – Udo Udoma & Belo-Osagie .................................................117

Philippines – Martinez Vergara Gonzalez & Serrano ...................... 134

United Arab Emirates – RIAA Barker Gillette (Middle East) LLP ...... 146

Contents

LexisNexis® Company Law Guide 2017-2018

Jurisdictional Q&As

10 LexisNexis Foreign Investment Law Guide 2017-2018

1. What are the main reasons foreign investors invest in your jurisdiction?

Anecdotally, the main reasons motivating foreign investors in Australia are Australia’s relatively open and stable economy, need for capital investment and predictable overall legal and political framework. Notwithstanding occasional political sensitivities generally confined to specific asset classes, Australia is generally open to foreign investment to meet shortfalls from relatively limited domestic capital markets.

According to Australia’s Foreign Investment Review Board (FIRB), the non-statutory body established to advise the Australian Federal Treasurer (Treasurer) and Government on foreign investment policy:

(a) Australia’s mining sector has been the main target industry for foreign direct investment in Australia in recent times, representing over 40% of the total foreign direct investment stock in Australia at the end of 2015. Other sectors to benefit from significant foreign investment include manufacturing (representing 11.7% of that foreign direct investment stock) and real estate (at 8.7% of that stock); and

(b) the largest source by volume of approved foreign investment in Australia in the 2015-6 financial year was China (at A$47.3bn), followed by the United States of America (at A$31bn).

2. What foreign investment legislation is in place in your jurisdiction (e.g. Foreign Investment Law or Foreign Investment Catalogue)? Please provide a brief overview of such legislation.

The principal piece of generic foreign invest-ment primary legislation in Australia is the Foreign Acquisitions and Takeovers Act 1975 (Cth) (FATA) which applies in all Australian States and Territories and was recently subject to the most significant overhaul in the Act’s forty-year history in December 2015.

FATA is accompanied in primary legislation by:

(a) the Foreign Acquisitions and Takeover Fees Imposition Act 2015 (Cth) (which applied a “user-pays” model to foreign investment approval applications for the first time in Australia); and

(b) the Register of Foreign Ownership of Water or Agricultural Land Act 2015 (ROFOWAL) (Cth) (which attempts to establish a register of foreign interests in Australian agricul-tural land and water rights).

Those Acts are now also supported by a range of secondary legislation, including:

(a) the Foreign Acquisitions and Takeovers Regulation 2015 (Cth) (FATR);

(b) the Foreign Acquisitions and Takeovers Fees Imposition Regulation 2015 (Cth); and

(c) the Register of Foreign Ownership of Agricultural Land Rule 2015 (Cth).

There are also other sector-specific foreign investment restrict ions applicable to banking, airlines, airports, shipping and telecommunications.

Jurisdiction: AustraliaFirm: Atanaskovic Hartnell Author: Lawson Jepps

Jurisdictional Q&A – Australia 11

3. What restrictions are placed on foreign investment? Does this differ at local levels of government?

Specific restrictions targeted uniquely at foreign investment are legislated at the federal level of Australian Government.

Australian foreign investment law pursues a dis-tinction between “notifiable” and “significant” transactions resulting in approval notifications in circumstances described in response to question 5 below.

Despite notification requirements which can delay the speed at which foreign investment in Australia might otherwise be implemented (see response to question 5) and therefore conceivably put foreign investors at a com-petitive disadvantage to domestic bidders in certain circumstances, foreign investment transactions are very rarely barred outright by the Australian Government. Outside of real estate, only five major transactions have been announced by FIRB as having been rejected since 2000, although approvals subject to conditions are not uncommon.

In our experience, since foreign investors’ inter-est in Australian assets is relatively common, it is usually the case that sellers’ timetables for transactions are set allowing for the obtaining of relevant foreign investment approvals.

4. What are the most common business vehicles for foreign investors? How long do they take to be set up? What are the key requirements for the establishment and operation of these vehicles?

Australian law permits the establishment of a similar range of business vehicles to other common law jurisdictions, including:

(a) companies with limited liability, either proprietary (private) with no more than 50 non-employee shareholders or public;

(b) general partnerships of up to 20 members; and

(c) common law trusts, including unit trusts.

As in other common law jurisdictions, the choice between these vehicles will often be driven by transaction specific taxation con-siderations responsive to the target asset class (e.g. the use of trusts for real estate) which are outside the scope of this guide.

Control of pre-registered shelf companies for subsequent amendment to suit the acquirer can be acquired within a working day and general partnerships and common law trusts technically only require as long to set up as it takes to draft their constitutional documents.

The key requirements for establishment and operation of:

(a) a proprietary company are at least one company director who must ordinarily reside in Australia; and at least one share-holder (a bespoke corporate constitution is not necessary, companies can generally rely on statutory “replaceable rules” in its absence);

(b) a general partnership are a partnership deed and at least two partners; and

(c) a common law trust is a trust deed, a trustee and at least one beneficiary.

In practice, it is likely that any of those vehicles if used for investment, will also undertake the additional process of acquiring at least an Australian Business Number (ABN) for the Australian Business Register (which facilitates interaction within a variety of government entities) and a Tax File Number (TFN) (sepa-rate to the TFN for individual investors) which facilitates interaction with the Australian Tax Office (ATO).

5. Under what circumstances are foreign investments subject to government approvals? What is the process and timeline for such approvals?

Some foreign investments, known as “notifiable transactions”, are subject to compulsory prior notification to the Treasurer for approval. Other foreign investments, known as “significant

12 LexisNexis Foreign Investment Law Guide 2017-2018

The process is now by online submission for approval to FIRB. The Treasurer has thirty calendar days to make a decision whether to notify objections after receiving notice that an action is proposed to be taken, of which the investor must effectively be informed within a further ten calendar days after the decision deadline. In our experience, it is imprudent to rely on a response from FIRB ahead of the statutory deadline.

For the timetable to decision to start running, submissions need to be accompanied by the prior payment of often substantial application fees (e.g. A$25,300 for business applications), which are not refundable in the event of an unsuccessful or withdrawn application.

The Treasurer may make orders against transactions considered to be “contrary to the national interest”. The national interest is not susceptible to statutory definition but some guidance is offered by Australia’s Foreign Investment Policy which suggests the Australian Government typically considers the following factors when assessing foreign investment proposals:

(a) national security (controversially applied in the S. Kidman & Co. Limited 2015 rejection decision but not in the decision ultimately to approve a 99-year lease of the Port of Darwin to a Chinese company prior to that);

(b) competition (FIRB apparently as a matter of course consults the Australian anti-trust authority, the Australian Competition and Consumer Commission on foreign invest-ment applications);

(c) other Australian Government policies (including tax). The potential application of conditions as to Australian taxation compliance for approved foreign investors is now subject to a specific FIRB guidance note;

(d) impact on the economy and the community; and

(e) character of the investor.

transactions”, are not subject to compulsory prior notification to the Treasurer but are effectively subject to a de facto prior approval requirement given that the Treasurer can make orders requiring the action to be unwound subsequent to implementation, if the action is found to be contrary to the national interest. Such orders cannot be made if the relevant foreign person is given a no objection notifi-cation subsequent to compulsory or voluntary approval submission.

The rules apply to actions by foreign persons which can extend in its legislative definition beyond investors who would necessarily consider themselves foreign to Australia, for instance to Australian-incorporated companies in which a foreign person is deemed to hold an interest of at least 20%.

The circumstances for “notifiable transactions” are generally when foreign persons acquire:

(a) an interest of at least 20% in an Australian entity worth at least A$252 million;

(b) a variety of “direct” interests in an Australian agribusiness worth at least A$55 million or Australian agricultural land worth at least A$15 million; and

(c) any interest in generic Australian land worth at least A$55 million (figures at present thresholds subject to indexation).

The additional circumstances for “significant transactions” are when foreign persons acquire any interest in an Australian entity or business worth at least A$252 million resulting in a change of control of that entity or business.

Acquiring a “direct” interest in an Australian entity or business of any size or starting an Australian business is compulsorily notifi-able for a foreign government investor which includes foreign governments but also emana-tions of foreign governments which might have otherwise considered themselves independent, such as sovereign wealth funds, and includes Chinese state-owned enterprises (SOEs).

Jurisdictional Q&A – Australia 13

6. What sectors are heavily regulated or restricted in your jurisdiction, if any? Conversely, what are some of the more open or unrestricted sectors, if any?

Foreign investment in the Australian media sector is more heavily regulated under the general Australian foreign investment regime. A foreign person acquiring an interest of 5% or more in an entity or business of any value that carries on an Australian business of publishing daily newspapers or broadcasting television or radio in Australia is automatically both a notifiable and a significant transaction. The Australian agribusiness sector is also more heavily regulated (see question 5). There are also “sensitive businesses” for which foreign investors are deprived of the more liberal regime that would otherwise apply due to the application of Australia’s free trade agreements, including supply of military equipment and extraction of radioactive materials. There are also the sector-specific regimes referred to in response to question 2.

7. Are there any restrictions on doing business with certain countries or territories in your jurisdiction? (For example, sanctions.)

The Australian Department of Foreign Affairs and Trade maintains a list of persons subject to sanctions in accordance with the Charter of United Nations Act 1945 (Cth) and the Australian Autonomous Sanctions Act 2011 (Cth) – see www.dfat.gov.au/sanctions/ consolidated-list.html.

8. What grants or incentives are on offer to foreign investors, if any?

A variety of grants and incentives are offered by the Australian Federal Government and individual States and Territories to support foreign investment in Australia. The first point of contact would generally be Austrade

(the Australian Trade and Investment Commission). Details of potential grants and assistance are available through the online Grant and Assistance Finder tool at the busi-ness.gov.au website.

9. Are there any free trade, special economic or industrial zones in your jurisdiction and what are their requirements?

There are no designated economic or industrial zones in Australia that are not subject to the statutory foreign investment regime.

Australia has entered into free trade or other arrangements with all of Chile, China, Japan, New Zealand, South Korea and the United States of America which liberalise to varying degrees the thresholds for approval notifica-tions described in the response to question 5.

10. What are the main taxes that could apply to foreign investors in your jurisdiction? (For example, Personal Income Tax, Corporation Tax, Value Added Tax and Social Security Payments).

Australia imposes an income tax on the taxable income of resident and non-resident individ-uals. Non-resident individuals are subject to income tax on their Australian source income, which includes income from passive invest-ments such as real property.

Companies that are resident in Australia for Australian tax purposes are liable for income tax on their Australian source taxable income and on certain foreign source income. Companies that are not tax resident in Australia are generally liable for Australian income tax only on their Australian source income.

Australia imposes a value added tax known as the Goods and Services Tax (GST) of 10% on most goods, services and other items consumed in Australia and entities are liable to pay GST on Australian taxable supplies irrespective of residence.

14 LexisNexis Foreign Investment Law Guide 2017-2018

(subclass 888) (which is derivative from the subclass 188 visa).

12. Can foreign investors acquire real property and land in your jurisdiction? Are there any restrictions or limitations?

There are significant foreign investment restric-tions and limitations concerning Australian real property and land.

Australian land encompasses four separate categories, being:

(a) agricultural land (meaning land related to a primary production business), as to which see response to question 5 above;

(b) residential land, acquisitions of any inter-ests by foreign persons in respect of which are generally notifiable actions regardless of value;

(c) commercial land (defined essentially as land other than agricultural or residential land), acquisitions of any interests by foreign persons in respect of which are generally notifiable actions regardless of value if the commercial land is vacant or at least A$55m if not vacant; and

(d) a mining or production tenement, acqui-sitions of any interests by foreign persons in respect of which are generally notifiable actions regardless of value other than for beneficiaries of free trade agreements with Chile, New Zealand and the United States of America.

Foreign investment particularly in residential real estate remains politically sensitive in Australia and is an area subject to frequent announcements by FIRB on the effectiveness of FIRB’s efforts to enforce the foreign investment regime.

There are also now obligations under ROFOWAL of a foreign person to notify the ATO of starting to hold:

(a) a freehold interest in agricultural land; or

(b) a lease or licence of agricultural land reasonably likely to exceed five years.

Payroll taxes are subject to State and Territory-specific legislation. Companies are subject to compulsory superannuation (i.e. pension) payments in respect of employees and certain contractors at the rate of 9.5% of their “ordinary time earnings”. If employers do not make the relevant contributions, those employers have to pay a “superannuation guarantee charge” of equivalent amount.

11. What are some of the employment regulations in your jurisdiction that foreign investors should be aware of? Is it possible to secure residency permits or work visas for foreign nationals under investment?

Employer/employee relations are compre-hensively regulated in Australia under the Fair Work Act 2009 (Cth) which sets out ten National Employment Standards (NES) that apply to all permanent employees with limited exceptions.

Australian workforces are relatively heavily unionized compared to other jurisdictions and the NES can often be supplemented in practice by the provisions of “modern awards” governing employment terms and conditions in particular industries or occupations or “enterprise agreements” in relation to particular workforces.

Australian employment is subject to Work Health and Safety legislation familiar in other jurisdictions which is technically State-based, but common to national standards across most States.

There are a variety of visas for foreign nation-als under investment in Australia including the Business Innovation and Investment (Provisional) visa (subclass 188) (which includes investor streams with investment requirements ranging from A$1.5m to A$15m); the Investor visa (subclass 191) (which requires a designated investment of A$1.5m to be maintained for four years); and the Business Innovation and Investment (Permanent) visa

Jurisdictional Q&A – Australia 15

Australia is also a signatory to the United Nations Convention on the Recognition and Enforcement of Arbitral Awards 1958 (New York Convention) and enacted the International Arbitration Act 1974 (Cth) giving effect to the 2006 version UNCITRAL Model Law on International Commercial Arbitration.

Australian courts have a demonstrable track record in enforcing agreements and awards made for the purposes of transnational arbi-tration, including High Court authority (the highest available) upholding the constitutional validity of application of the UNCITRAL Model Law in Australia.

17. Does your jurisdiction have any bilateral or multilateral investment protection treaties with Asia-Pacific jurisdictions that are commonly used for investing into the country?

Australia has entered into bilateral investment protection treaties with all of China; Hong Kong; Indonesia; Laos; Papua New Guinea; Philippines and Vietnam.

More significant for the purposes of the foreign investment restrictions described in response to question 5 are the free trade agreements referred to in response to question 9, which amongst other things raise the investment threshold for investors from an “agreement country” (including China, Japan, New Zealand and South Korea) to A$1,094m.

18. What intellectual property rights protections are available in your jurisdiction to foreign investors?

Australia maintains an intellectual property regime typical of common law jurisdictions including protection for registrable patents for up to 20 years, registrable trade marks (renewable for ten year periods), registrable designs (subject to restrictions on the use of the Australian flag) and unregistered copyright protection.

13. Are there any processes in your jurisdiction that can block foreign investment under specific circumstances?

Yes – the Treasurer can make orders pro-hibiting proposed actions and ordering transactions consummated without approval to be unwound, but they are rarely exercised (see response to question 3).

14. What foreign currency or exchange controls should foreign investors be aware of?

Unlike jurisdictions such as Brazil and China, Australia does not have a general exchange control regime. However, the Australian Department of Foreign Affairs and Trade may impose exchange control rules in accord-ance with the sanctions regime described in response to question 7. Australia does impose withholding tax on interest paid by an Australian resident company to a non-resident lender at the rate of 10% unless the lender pro-vides the loan in connection with a business carried on through an Australian branch or the Australian resident borrows in connection with a business it carries on through a foreign branch.

15. Are there any restrictions, approval requirements or potential penalties if a foreign investor withdraws their investment in your jurisdiction?

Per the response to Question 14, Australia does not have a general exchange control regime which would prevent divestment in the ordinary course.

16. What contract enforcement and investor protection mechanisms are in place in your jurisdiction, if any?

Contracts are enforceable by foreign investors through the courts of Australia subject to applicable governing law and jurisdiction clauses.

16 LexisNexis Foreign Investment Law Guide 2017-2018

investment application fee imposed at the time the property was acquired; and

(b) introducing from 1 July 2017 a new busi-ness exemption certificate allowing foreign investors in securities to have access to an exemption certificate allowing pre-approval for multiple investments in one application rather than having to apply separately for each investment.

22. Are there any other features regarding foreign investment in your jurisdiction or in Asia that you wish to highlight?

Given that the ultimate decision whether notified proposals are contrary to the “national interest” resides with a political appointee, the Treasurer, foreign investment approval decisions in Australia have inevitably been to some degree politicized and therefore subject to a degree of variation in political sensitivity leading to marginal unpredictability in out-comes for publicised transactions.

Equally, it is doubtful whether the political pressure leading to the technicalities of the new agricultural land regime was really pro-portionate to the facts of foreign investment on the ground, in that 99% of Australian farm businesses and 90% of Australian agricultural land were thought to be entirely Australian-owned in 2015.

Nonetheless, Australia’s regime very rarely acts strictly to inhibit foreign investment and given its relatively strong economic performance since the GFC in 2008 amongst similar devel-oped countries, the Australian Government remains fairly exceptional in its willingness to emphasise its continuing commitment to welcoming foreign investment as “essential to Australia’s economic growth and prosperity”.

This guide reflects the law in Australia as at 9 June 2017 and is intended to give a generic analysis of the law which is not a substitute for legal advice specific to individual circumstances.

19. Are there any environmental policies and regulations that (potential) foreign investors should be aware of prior to or throughout the investment process in your jurisdiction?

Australia’s foreign investment policy indicates that, when examining whether foreign invest-ment proposals in the agricultural sector are in the national interest, the Australian Government typically considers the effect of the proposal on factors including environmental factors such as “the quality and availability of Australia’s agricultural resources, including water” and “biodiversity”.

Most major mining development projects will require the navigation of regulation and obtain-ing of approvals at both State/Territory level but also at federal level, where the Commonwealth Environmental Planning and Biodiversity Act 1999 (Cth) applies wherever a project is likely to have a significant impact on a matter of national environmental significance.

20. Are there any government agencies or non-governmental bodies that (potential) foreign investors can turn to for more information on investment in your jurisdiction?

Foreign investors would be recommended to approach the Australian Trade and Investment Commission (Austrade).

21. Have there been any recent proposals for reforms or regulatory changes that will impact foreign investment in your jurisdiction?

In the 2017/18 Federal Budget, the Australian Government announced changes regarding the foreign investment framework including:

(a) an annual vacancy charge on new foreign owners of residential land where the property is not occupied or genuinely available on the rental market for at least six months each year equivalent to the foreign

About the Author:Lawson Jepps

Solicitor, Atanaskovic Hartnell

W: www.ah.com.au

A: Atanaskovic Hartnell House, 75-85 Elizabeth Street, NSW 2000, Sydney Australia

T: +61 2 9224 7091

Jurisdictional Q&A – Australia 17

18 LexisNexis Foreign Investment Law Guide 2017-2018

1. What are the main reasons foreign investors invest in your jurisdiction?

Bangladesh offers the most liberal foreign direct investment (“FDI”) regime in South Asia. It benefits from a cost-effective industrial work-force, strategic geopolitical location having good regional connectivity and complete duty and quota free access to EU, Japan, Canada, Australia and most other developed countries with access to international sea and air route. Also no restriction on equity participation and repatriation of profits and income, allowance of tax holidays and accelerated depreciation in most sectors, cash incentives for selected products, repatriation of dividend and capital at exit, equal treatment for local and foreign investors, protection of FDI from expropriation and nationalization under the Foreign Private Investment (Promotion & Protection) Act 1980 (‘FPIA 1980’) etc. are the key considerations to attract FDI in Bangladesh.

Additionally, the low cost of energy, good supply of natural gas, established export and economic zones, fertile & favorable land and climate, macroeconomic stability, open and diversified economy and other competitive incentives by the government provide foreign investors an economical and business friendly environment. It is also to be noted, that in spite of many constraints, Bangladesh has main-tained over 6% GDP growth rate per annum for the last 6 years. Due to its steady progress, now it is the second largest garments and apparel exporter in the world after China.

FDI inflow in Bangladesh has significantly increased over the past decade and it rose by 24% year-on-year to US$ 1.6 billion in 2013 and has climbed to US$ 2.2 billion in 2016. The FDI receipt was 44.1% higher compared to that of 2014.

Bangladesh also has published a robust FDI Policy Framework in September 2014 through the Ministry of Commerce which is pending further approval, which not only sanctions numerous attractive incentives to the foreign investors but also protects and guarantees the safety of the investments and their returns.

Moreover, Bangladesh is a signatory to Multilateral Investment Guarantee Agency (MIGA) of the World Bank Group, Overseas Private Investment Corporation (OPIC) of USA and International Centre for Settlement of Investment Disputes (ICSID) and is also a member of World Association of Investment Promotion Agencies, which facilitates foreign investment in Bangladesh.

2. What foreign investment legislation is in place in your jurisdiction (e.g. Foreign Investment Law or Foreign Investment Catalogue)? Please provide a brief overview of such legislation.

The most relevant laws, regulations and guidelines that play an operative role in FDI in Bangladesh are as follows:

(a) The Foreign Exchange Regulation (Amendment) Act, 2015 (‘FERA’)- This Act provides the legal basis for regulating

Jurisdiction: BangladeshFirm: The Legal Circle Authors: Masud Khan, N.M. Eftakharul Alam Bhuiya and Sameera M Reza

Jurisdictional Q&A – Bangladesh 19

certain payments, dealings in foreign exchange and securities in Bangladesh;

(b) The Guidelines for Foreign Exchange Transactions, Volume- 1 & 2 (2009) and updated by circulars of Bangladesh Bank (‘BB’) issued from time to time (collectively, the ‘FX Guidelines’). FX Guidelines are a compilation of instructions and directives issued by BB regulating foreign exchange transaction. It also deals with specific instructions to be followed by the author-ized dealers (banks authorized by BB to deal in foreign exchange under FERA and their constituents) (‘AD’).

(c) The FPIA 1980- This Act deals with promo-tion and protection of foreign investment in Bangladesh. The Act ensures equal treatment for local and foreign investors and legal protection to foreign investment in Bangladesh against nationalization and expropriation. It also guarantees repatria-tion of dividend and capital at the exit of business.

(d) The Bangladesh Export Processing Zone Authority Act, 1980 (‘BEPZAA 1980’)- This Act regulates the economic development of Bangladesh by encouraging and promot-ing foreign investments in certain areas (‘Export Processing Zones’ or ‘EPZ’) des-ignated by the government of Bangladesh (‘GOB’).

(e) Double Taxation Treaties- Bangladesh has entered into double taxation treaties with 28 (twenty-eight) countries, which reduces tax impediments of cross-border trade and investment and assist tax administration

Other relevant laws and regulations applicable or indirectly related to foreign direct invest-ment are:

(a) The Companies Act, 1994 (‘CA 1994’)- This Act regulates the formation and incor-poration of companies. This Act sets the framework for the management, opera-tion and administration of companies. It also regulates the Registrar of Joint Stock

Companies and Firms (‘RJSC’) which is the regulatory authority designated for registration and filings required by such companies. The Act also specifically governs the requirements for establishing foreign companies in Bangladesh and the rules for regulating them including preparation, maintenance, audit and submission of their accounts to the host country regulators.

(b) Bangladesh Economic Zones Act, 2010 (‘BEZA 2010’)- This Act makes provisions for the establishment of private economic zones in potential areas including under-developed regions jointly or individually by local, non-resident Bangladeshis or foreign investors.

(c) Bangladesh Investment Development Authority Act, 2016 (‘BIDA 2016’)- This law has established Bangladesh Investment Development Authority (‘BIDA’) for the purpose of promoting industrial invest-ments and offering facilities and assistance necessary for the establishment of indus-tries in the non-governmental sectors and to promote and facilitate investment both from domestic and overseas sources.

3. What restrictions are placed on foreign investment? Does this differ at local levels of government?

Depending on the sector of trade, restrictions may be placed by the GOB on FDI; please see answer to question no. 6 for the list of restricted and unrestricted sectors for FDI.

At the local levels of government, a foreign investor is required to be registered with BIDA, which is responsible for screening, reviewing and approving FDI in Bangladesh. The BIDA registration is mandatory for obtaining industrial plot in the special economic zone. It may take around 15-30 days to obtain a “Registration Certificate” from BIDA if all the required documents are submitted properly.

20 LexisNexis Foreign Investment Law Guide 2017-2018

Incorporation of 100% foreign owned company and Joint Venture companyA 100% foreign owned company or a Joint Venture company can either be registered as a “public limited company” or a “private limited company”. The type of company most com-monly chosen by foreign investors is private limited company. The CA 1994 s 2(q) defines a private limited company as one which by its articles restricts the right to transfer its shares, if any, prohibits any invitation to the public to subscribe for its shares or debenture, if any, and limits the number of its members to 50 not including persons who are in its employment.

As per the provisions of the CA 1994, the incorporation of a private limited company requires it to be first registered with the RJSC including name clearance from RJSC. Requisite documents such as memorandum and articles of association (‘MemArts’), necessary forms and schedules, and an encashment certificate obtained from an AD of a scheduled bank need to be submitted to RJSC for registration of such a company.

Furthermore once registration with RJSC is completed, the private limited company shall have to further obtain the following for the successful incorporation of the entity:

(a) Registration with BIDA;

(b) Trade license from the local governmental authority;

(c) TIN certificate from the National Board of Revenue (‘NBR’);

(d) VAT registration (if applicable) from NBR.

Time Frame

The set-up and securing of all required certif-icates for such an entity may take a minimum of 2 (two) months.

Establishing a Branch Office or Liaison Office in BangladeshA foreign investor wishing to merely have a presence in Bangladesh, but not incorporate a

Foreign investors, depending on the type of sector, may also be required to obtain many licenses and permits such as an Import Registration Certificate, Export Registration Certificate, Bond License, etc. to run their business in Bangladesh.

4. What are the most common business vehicles for foreign investors? How long do they take to be set up? What are the key requirements for the establishment and operation of these vehicles?

In order to choose the business vehicle, the foreign investors must first choose the type of business operation they wish to operate in Bangladesh. This could be either by establishing industrial projects/ factories/plants etc. or by operating a “Branch Office” or “Liaison Office” in Bangladesh.

In order to establish industrial projects/ fac-tories/plants, it is essential to form a company and incorporate the same locally or incorporate a company abroad and register it with RJSC in Bangladesh. Companies in Bangladesh could be classified in the following major categories:

(a) Company limited by shares:

(i) Private limited company; and

(ii) Public limited company

(b) Company limited by guarantees.

The most common incorporation options for foreign investors include the following:

(a) A 100% foreign-owned company in Bangladesh where 100% directors and shareholders are foreign citizens (allowed in most sectors including construction, information technology and development);

(b) A “Joint Venture” company with local Bangladeshi partners / investor where Bangladeshi shareholders and foreign shareholders jointly hold stake in the company;

(c) A Branch Office or Liaison Office.

Jurisdictional Q&A – Bangladesh 21

company may set up a Branch Office or Liaison Office. It is essential for both a Branch Office and Liaison office to obtain approval from BIDA before setting up its office in Bangladesh. A Branch Office or Liaison Office does not have a separate legal entity and is considered to be an extension of its parent company. The parent company’s MemArts dictates the activities for the Branch Office or Liaison Office. Following are the traits of a Branch Office and Liaison Office:

Liaison Office

A Liaison Office can maintain liaison/ coordination between its principal and local agent, promote its products and do activities as approved under its application to BIDA. However it will have no local source of income in Bangladesh. All setup and operational costs including salaries of the foreign and local employees of the Liaison Office will have to be borne by the parent company aboard. No out-ward remittances of any kind from the Liaison Office will be allowed except the amount brought in from abroad that hasn’t been spent.

Branch Office

A Branch Office can undertake the same busi-ness as its head office and engage in commercial activities with prior approval of BIDA. It can also have a local source of income from the approved field of business.

Once approval from BIDA has been obtained, the Branch or Liaison Office, (whichever is applicable), will have to report to BB within thirty (30) days of obtaining such approval.

Furthermore such an office must also obtain the following before it can go into operation:

(a) Registration with RJSC;

(b) Trade license from the local governmental authority;

(c) TIN certificate from NBR;

(d) VAT registration (if applicable) from NBR.

It is also required that within 2 (two) months from the date of issuance of the BIDA approval,

a Liaison Office or Branch office bring in an inward remittance of foreign exchange equiv-alent to a sum of US$ 50,000 in Bangladesh through an AD, as an estimated initial estab-lishment cost and 6 (six) months’ operational cost.

Time Frame

The set-up and securing of all required approv-als for establishing of a Branch Office or Liaison Office may take a minimum of one (1) month.

5. Under what circumstances are foreign investments subject to government approvals? What is the process and timeline for such approvals?

Please see answer to question nos. 3 and 4 above.

6. What sectors are heavily regulated or restricted in your jurisdiction, if any? Conversely, what are some of the more open or unrestricted sectors, if any?

The National Council for Industria l Development (‘NCID’) has listed the following four sectors as “Restricted Sectors” for FDI:

(a) Arms and ammunitions and other military equipment and machinery;

(b) Nuclear power;

(c) Security printing and minting; and

(d) Forestation and mechanized extraction within the boundary of reserved forest.

NCID has again listed seventeen sectors as “Controlled Sectors” which require prior per-mission from the respective line ministries/authorities before allowing FDI. These are:

(a) Fishing in the deep sea;

(b) Bank/financial institution in the private sector;

(c) Insurance company in the private sector;

(d) Generation, supply and distribution of power in the private sector;

22 LexisNexis Foreign Investment Law Guide 2017-2018

j) Services etc.

7. Are there any restrictions on doing business with certain countries or territories in your jurisdiction? (For example, sanctions).

Bangladesh has placed a restriction in main-taining any diplomatic relationship with Israel. Hence, it can be presumed that Bangladesh shall not accept any FDI from any Israeli national or entity.

8. What grants or incentives are on offer to foreign investors, if any?

In addition to the benefits mentioned in answer to question no. 1, there are various incentives provided by the GOB to incentivize the foreign investors. These include the following:

Tax HolidayForeign investors enjoy a corporate tax holiday of 3 to 7 years for selected sectors subject to the relevant rules and procedures set by NBR. For instance, under the Income Tax Ordinance, 1984, Sch 6 Pt. A at para 33 (as amended by Bangladesh Income Tax Paripatra (Circular) 2015 and Finance Act, 2016), tax exemption is allowed on any income derived from the business of software development, information technology, information technology enabled services and nationwide telecommunication transmission network up to 30 June, 2024.

The location of the establishment also plays a role in determining such periods of tax holiday.

Tax ExemptionTax exemptions are permitted on the following:

a) Royalties, technical know-how and technical assistance fees and facilities received by any foreign firm, company or expert;

b) Income tax for foreign technicians, employed in industries as specified in the ITO 1984 for a period of up to three years;

(e) Exploration, extraction and supply of natural gas/oil;

(f) Exploration, extraction and supply of coal;

(g) Exploration, extraction and supply of other mineral resources;

(h) Large-scale infrastructure project (e.g. f lyover, elevated expressway, monorail, economic zone, inland container depot/container freight station);

(i) Crude oil refinery (recycling/refining of lube oil used as fuel);

(j) Medium and large industry using natural gas/condensed and other minerals as raw material;

(k) Telecommunication service (mobile/cellular and land phone);

(l) Satellite channel;

m) Cargo/passenger aviation;

n) Sea-bound ship transport;

o) Sea-port/deep sea-port;

p) VOIP/IP telephone; and

q) Industries using heavy minerals accumu-lated from sea bed.

On the other hand, some of the more unre-stricted and encouraged sectors of industries include the following amongst others:

a) Agro based;

b) Chemical;

c) Engineering;

d) Food and Allied;

e) Glass and Ceramics;

f) Printing, Publishing and Packaging;

g) Tannery and Rubber products;

h) Textile;

i) Energy and Infrastructure;

Jurisdictional Q&A – Bangladesh 23

promotion and protection of foreign invest-ments. Bangladesh is also a signatory to MIGA, OPIC, ICSID and a member of the World Intellectual Property Organization (‘WIPO’) permanent committee on development co-op-eration related to industrial property.

Export-oriented Industries:The foreign investors are provided the following incentives amongst others:

(a) 1% import duty on capital machinery and spare parts;

(b) Bonded warehouse and back to back letter of credit facility;

(c) Cash incentives and subsidies ranging from 5% to 20% on free on board (‘FOB’) value of the selected products;

(d) Fund for export promotion;

(e) Export credit guarantee scheme facility;

(f) 90% loans against letters of credit (by banks);

(g) 100% export-oriented industries located outside the EPZ are allowed to sell 20% of its products in the domestic market subject to payment of applicable tax and charges.

9. Are there any free trade, special economic or industrial zones in your jurisdiction and what are their requirements?

Export Processing Zones (‘EPZs’) have been established in Savar (Dhaka), Mongla, Ishwardi, Comilla, Uttara, Karnaphuli (Chittagong) and Adamjee (Dhaka) in accordance with BEPZAA 1980. 100% foreign owned (Type A), Joint Ventures (Type B) and 100% Bangladeshi-owned (Type C) companies are allowed to operate and enjoy the benefit of equal treatment in the EPZs.

In 2010, the Bangladesh Economic Zones Act, 2010 (‘BEZA 2010’) was enacted to facilitate the creation of privately-owned Special Economic Zones (SEZs) that can cater to export and domestic markets. The International Finance

c) Capital gains from the transfer of shares of public limited companies listed with a stock exchange; and

d) foreign loans in regard to its interest.

Investment and RepatriationBangladesh does not have any ceiling on the amount that can be brought in as foreign investment by foreign investors. There is also no restriction or the requirement of any prior approval from the GOB in remitting profits by the foreign companies operating in Bangladesh to their head offices. Hence full repatriation of invested capital, profits and dividends are allowed. Reinvested repatriable dividends or retained earnings are treated as new invest-ment. Employed foreigners in Bangladesh are allowed to remit up to 50% of their salaries and are also allowed to repatriate their savings and retirement benefits on their return. No prior approval for remittance of sale proceeds, including capital gains of portfolio investments of non-residents through stock exchanges in Bangladesh is required.

Exit policyOnce the investor wishes to leave the country after completion of all formalities, he/she can repatriate the net proceeds after obtaining approvals from BB.

Foreign employeesThere is no restriction on issuance of work per-mits to foreign employees related to the project. The foreign national may become citizen of Bangladesh by investing a minimum of US$ 5,00,000 or by transferring US$ 1,000,000 to any recognized financial institution (non-re-patriable). Also a foreign national can become a permanent resident by investing a minimum of US$ 75,000 (non-repatriable).

Avoidance of double taxationAs mentioned earlier Bangladesh has various international agreements in place, includ-ing bi-lateral agreements and investment treaties for avoiding double taxation and for

24 LexisNexis Foreign Investment Law Guide 2017-2018

HS Code (an internationally standardised system of names and numbers to classify traded products) of the products and/or services traded by the company. However, the most common rate of VAT in Bangladesh is 15%.

11. What are some of the employment regulations in your jurisdiction that foreign investors should be aware of? Is it possible to secure residency permits or work visas for foreign nationals under investment?

The Labour Act, 2006 (‘LA 2006’) and the Labour Rules, 2015 (‘LR 2015’) regulate and provide for prescribed guidelines in connec-tion to employment conditions, working hours, minimum wages, leave policies, health and sanitary conditions, compensation for injured workers, trade unions and other employment relations. Any labour related disputes/issues are generally resolved before a Labor Tribunal.

Furthermore, the EPZ Workers Association and Industrial Relations Act, 2004 regulates the consolidating laws for Trade Unions and Industrial Relations in the EPZs in Bangladesh.

Foreign nationals willing to be employed in Bangladesh must apply for their work permit by applying in the prescribed form to either BIDA (for private sector industrial enterprise, Branch Office and Liaison Office, outside of EPZ) or BEPZA (for employment of foreign national in the EPZs).

In order to issue the work permit, BIDA usually consider the following:

(a) The foreign national must not be below 18 years of age;

(b) Only nationals from countries recognized by Bangladesh are eligible;

(c) Foreign nationals are only considered for such job where there is scarcity of local experts/ technicians in that specific field;

(d) The number of foreign nationals employed should not exceed 5% in the industrial sector and 20% in commercial sector of the

Corporation (‘IFC’) is assisting the GOB in establishing a Special Economic Zone Authority, similar to that of the Bangladesh Export Processing Zones Authority (‘BEPZA’), which shall implement the new law and oversee the establishment of SEZs.

10. What are the main taxes that could apply to foreign investors in your jurisdiction? (For example, Personal Income Tax, Corporation Tax, Value Added Tax and Social Security Payments).

The most relevant taxes applicable under the prevailing laws of Bangladesh can be classified as follows:

Corporate TaxGenerally a foreign company is taxed only on the income received or deemed to be received from the operations of the company in Bangladesh. The tax year is calculated yearly, starting from July 1 to June 30 of the succeeding year. At present, the rate of corporate tax of a non-listed company is 35% of a company’s total income in a year, and 25% in case of a listed company (except for certain industries such as banks, financial institutions and merchant banks).

Personal Income TaxPersonal income tax is levied on capital gains and income from dividends. Income tax ranges from 10% to 25% depending on the taxable income. However, rates may also vary in accordance with the gender of the person.

However, a foreign technician employed in foreign companies will not be subjected to personal tax up to three (3) years, and beyond that period his/ her personal income tax payment will be governed by the existence or non-existence of agreement on avoidance of double taxation with the country of citizenship.

Value Added TaxIn Bangladesh VAT is applied to local sales. The rate of VAT usually depends on the respective

Jurisdictional Q&A – Bangladesh 25

(iii) Foreign Investors can invest into local businesses as joint partners and then acquire land and property in the name of the locally registered businesses.

13. Are there any processes in your jurisdiction that can block foreign investment under specific circumstances?

Please see answer to question no. 6 above, which discusses about Restricted Sectors and Controlled Sectors for FDI in Bangladesh.

14. What foreign currency or exchange controls should foreign investors be aware of?

The core legislation that governs this area is the FERA. The first thing to remember for a foreign investor is that any inward remittance transaction and/or outward remittance trans-action must be done through an AD. Secondly, any amount of foreign currency can be brought into the country; however it is essential that any amount above US$ 5,000 should be declared to customs authorities through a Foreign Currency Declaration form, commonly known as an FMJ form. Also if anyone wishes to buy foreign currency up to US$ 10,000, it must be done through an AD. Any purchases upwards of the above mentioned amount must be done with prior permission from BB. Not doing so would constitute an offence under FERA.

In addition, it is helpful to note that FX Guidelines issued by BB from time to time on practices to be adopted are also important to be aware of.

15. Are there any restrictions, approval requirements or potential penalties if a foreign investor withdraws their investment in your jurisdiction?

There are no such restrictions and penalties upon foreign investors who wish to withdraw their investments. It is considered an essential that the freedom to set up and the freedom to

total employees, including upper manage-ment employees;

(e) The employment of the foreign national may be considered for an initial term of two years, which may subsequently be extended for additional terms on the basis of merit of the case. After expiry of a term of work permit, the foreign national is required to leave the country and then re-apply for a fresh work permit;

(f) A security clearance certificate may be needed to be issued by the Ministry of Home Affairs for obtaining the work permit.

As discussed earlier, the foreign nationals may become citizens of Bangladesh by investing a minimum of US$ 5,00,000, or become a permanent resident by investing US$ 75,000 in Bangladesh.

12. Can foreign investors acquire real property and land in your jurisdiction? Are there any restrictions or limitations?

According to the Constitution of Bangladesh Art 42 only a citizen of Bangladesh can acquire real property and land in Bangladesh. A foreign investor can only acquire land under the capac-ity of its company’s name and not under his/her personal name. There are effectively three ways by which this can be done:

(i) The foreign investor can register his or her company with RJSC. This would cause the company to become a “local entity” whose name could be used to acquire land and property.

(ii) Foreign Investors who invest a minimum of US$ 5,00,000 or trans-fer US$ 1,000,000 to any recognized financial institution (non-repatriable) and can apply for Bangladeshi citi-zenship. Once citizenship is granted, a foreign investor can apply for the purchase of real property on the same basis as a Bangladeshi citizen.

26 LexisNexis Foreign Investment Law Guide 2017-2018

exit are preserved. There are essentially two ways by which a business can terminate- a business may choose to wind up on its own initiative under Section 286 of CA 1994 or a competent court under the CA 1994 s 241 can wind up a company.

Investors do have the opportunity to sell their shares to local concerns after which they may leave the country. The sales proceeds can be repatriated after proper and prior authorization from BB. As per FX Guidelines for such prior authorization of BB, the foreign investor is required to submit encashment certificate(s), form 117, copy of the registration certificate obtained from BIDA, if any, and other relevant reporting documents applicable for inward remittance, through its AD.

16. What contract enforcement and investor protection mechanisms are in place in your jurisdiction, if any?

The legal system of Bangladesh is a common law legal system that is modelled to a great extent on the English Common Law legal system. Therefore, contractual enforcement follows the trend that is familiar to most other common law traditions. One of the most striking prin-ciples of legal protection and enforceability is found in the Constitution Art 31 which affords the protection of the law to all within the juris-dictional boundaries of Bangladesh i.e. to both citizens and non-citizens alike.

In addition, it is widely becoming the status quo that commercial entities resort to methods of alternative dispute resolution (‘ADR’) to obtain a more amicable settlement of disputes, to pre-serve business relationships as far as possible. The Civil Procedure Code (Amendment) Act, 2012 (‘CPC 2012’) inserted sections 89A and 89B to allow parties to settle their disputes through arbitration and mediation. The growing inclination towards the use of ADR is evidenced by commercial parties regularly inserting ADR clauses into their contractual documents and agreements.

Bangladesh being a member of MIGA, addi-tional protection against political risks such as expropriation, war-damage and inconvert-ibility are also provided to foreign investors. Moreover, FPIA 1980 provides protection to foreign investors against expropriation and nationalization. In the event, where expropri-ation is necessary, the GOB is to adequately compensate the investors with the market value of the investment as per the said Act.

17. Does your jurisdiction have any bilateral or multilateral investment protection treaties with Asia-Pacific jurisdictions that are commonly used for investing into the country?

Bangladesh has signed bilateral double taxation treaties with 28 countries, including Austria, the Belgium-Luxembourg Economic Union, China, Denmark, France, Germany, India, Indonesia, Iran, Italy, Japan, Democratic People’s Republic of Korea, Republic of Korea, Malaysia, Netherlands, Pakistan, Philippines, Poland, Romania, Singapore, Switzerland, Thailand, Turkey, United Arab Emirates, United Kingdom, United States, Uzbekistan and Vietnam. These treaties provide such ben-efits as tax holidays and prevent such incidences as double taxation, promoting good trade rela-tions and creating an environment conducive to proliferate investment.

Moreover, Bangladesh does have investment protection treaties with Asia-Pacific juris-dictions namely through, Asia-Pacific Trade Agreement (‘APTA’), South Asian Free Trade Area (‘SAFTA’) and Bay of Bengal Initiative for Multi-Sectoral, Technical and Economic Cooperation (‘BIMSTEC’).

18. What intellectual property rights protections are available in your jurisdiction to foreign investors?

Bangladesh is both a signatory to the Paris Convention on Industrial Property (instituted in the year 1883 and revised as it stands in 1979)

Jurisdictional Q&A – Bangladesh 27

Under the said act, the DOE is required to issue “Environmental Safety Clearance Certificates” when it is satisfied that the applicants have con-formed to the requisite safety standards. Any proposal for an undertaking that is industrial in nature must contain a comprehensive and appropriate environmental impact assessment and proposed environmental impact manage-ment measures.

Usually the DOE takes a minimum of 15 working days to issue an Environmental Safety Clearance Certificate for industries with low levels of adverse impact. For ventures that may pose a significant impact, the processing time extends to around 30 days or more.

20. Are there any government agencies or non-governmental bodies that (potential) foreign investors can turn to for more information on investment in your jurisdiction?

BIDA is the principal private investment pro-motion and facilitation agency of Bangladesh, which provides information regarding invest-ments in Bangladesh. Also, the Bangladesh Small Cottage and Industry Corporation (BSCIC) is dedicated to the advancement of small cottage industries in the private sector. Investors seeking to set up in the various EPZs often consult with BEPZA which possesses approval granting jurisdiction for all projects located in the designated EPZ.

In addition, there are numerous law firms and privately owned commercial think-tanks that are able to provide specialist knowledge and advice in various commercial matters on a more customer-oriented basis.

21. Have there been any recent proposals for reforms or regulatory changes that will impact foreign investment in your jurisdiction?

BIDA has drafted the One-Stop Service Act, 2017 aiming to attract foreign investors by

since 1991 and continues to be a member of WIPO since 1985. The importance of having a legal infrastructure to promote and protect intellectual property rights as an attraction to foreign investment is well understood and the legislations governing this vital area are listed below:

(a) Patent and Design Act, 1911;

(b) Patent and Designing Rule, 1933;

(c) Copyright Act, 1999;

(d) Trademarks Act, 2009 amended in 2015;

(e) Geographical Indication of Goods (Registration and Protection) Act, 2013;

(f) Trademarks (Amendments) Act, 2015; and

(g) Geographical Indication of Goods Act, 2015.

19. Are there any environmental policies and regulations that (potential) foreign investors should be aware of prior to or throughout the investment process in your jurisdiction?

Bangladesh is a country in the South-East Asian region with a particularly rich ecological diversity. It lies on one of the world’s richest delta regions boasting a rich network of nav-igable rivers, and fertile land for agriculture and habitation sustaining the livelihoods of many. Bangladesh also boasts possession of two-thirds of the world’s largest mangrove forest (the Sundarbans) and the world’s longest sea-beach at Cox’s Bazaar. It is considered to be of paramount importance that the richness in this country’s ecology is maintained and therefore the Department of the Environment (‘DOE’) is duty-bound to ensure that new and old ventures alike ensure that due respect and diligence is paid towards the protection of the environment. The Bangladesh Environment Conservation Act, 1995 (amended in 2010) is currently the main legislation governing envi-ronmental protection in Bangladesh, which provides the legal basis for the Environment Conservation Rules, 1997 (amended in 2002).

About the Authors:Masud Khan Senior Partner, The Legal Circle

T: +88 019 2080 4522

N.M. Eftakharul Alam Bhuiya

Senior Associate, The Legal Circle

E: [email protected]: +88 017 1112 0550

Sameera M Reza

Senior Associate, The Legal Circle

T: +88 017 7734 5636

W: www.legalcirclebd.com

A: The High Tower (9th floor), 9 Mohakhali C/A, Dhaka 1212, Bangladesh

T: +88 02 5881 4311

28 LexisNexis Foreign Investment Law Guide 2017-2018

licenses, land registration and mutation, envi-ronmental clearances, construction permits, explosives licenses and boiler certificates, connections for power, gas, water, telephone and the internet. It is expected that such a Once-Stop Service Centre will reduce the cost of doing business for foreign investors and will also reduce the time to obtain all regulatory permissions for doing business in Bangladesh.

22. Are there any other features regarding foreign investment in your jurisdiction or in Asia that you wish to highlight?

Please see answer to question numbers 1 and 8, which details the benefits, key considerations and incentives granted to foreign investors in Bangladesh, which makes it the most liberal jurisdiction for FDI in South Asia.

providing quick services from a single window. This law is being enacted in order to reduce various complexities in getting clearance from different government offices as was the case earlier. Rules will be framed under the said Act describing the timeframe for receiving various services from the “Once-Stop Service Centre”. Any failure to provide services within the timeframe stipulated in the rules will be deemed as ‘misconduct’ and will be punishable under the law.

According to the Act, four organizations- namely BIDA, BEPZA, Bangladesh Economic Zone Authority and Bangladesh Hi-tech Park Authority will act as the “Central One-Stop Service Authority” in their respective area. Sixteen (16) types of services will be provided to the investors from the Once-Stop Service Centre, which include issuance of trade

NEW DELHI Second Floor, 254, Okhla Industrial Estate, Phase III, New Delhi-110020 Tel: +91 11 4983 0000 Fax: +91 11 4983 0099 Email: [email protected] Website: www.phoenixlegal.in

MUMBAI Vaswani Mansion, Office No. 17 & 18, 3rd Floor, 120 Dinshaw Vachha Road, Churchgate, Mumbai – 400 020 Tel: +91 22 43408500 Fax: +91 22 43408501 Email: [email protected] Website: www.phoenixlegal.in

CHENNAI Seethakathi Business Centre, 9th Floor, Office Number 2B # 684-690, Anna Salai, Chennai-600 006 Tel: +91 44 2829 4626 Email: [email protected] Website: www.phoenixlegal.in

“It’s hard to think of areas where Phoenix Legal can improve. The firm is better than nearly all legal firms…” - Asia Law Profiles

PRACTICE AREAS ü Antitrust and

Competition ü Banking and Finance ü CMT ü Commercial

Contracts ü Corporate and Securities Laws ü Dispute Resolution -

Arbitration and Litigation ü Energy, Oil and Gas ü Environment ü Employment and

Industrial Relations ü Foreign Investment

and Exchange Control ü Infrastructure and

Project Finance ü Intellectual Property ü International Trade ü Information

Technology & Outsourcing ü Insurance ü Joint Ventures,

Foreign and Technical Collaborations ü Mergers and

Acquisitions ü Mining and

Resources ü Private Equity and

Funds ü Real Estate ü Regulatory Affairs ü Taxation ü Legal Compliance,

Bribery & Anti-Corruption ü Corporate Insolvency

and Restructuring

Phoenix Legal is a full service Indian law firm offering transactional, regulatory, advisory, dispute resolution and tax services. The firm advises a diverse clientele including domestic and international companies, banks and financial institutions, funds, promoter groups and public sector undertakings. Phoenix Legal was formed in 2008 and now has 15 Partners and 75 lawyers in its three offices (New Delhi, Mumbai and Chennai) making it one of the fastest growing law firms of the country.

Why Phoenix Legal?

What distinguishes the firm from its peers is the approach which is:

High Degree of Partner Involvement and Availability – We assure to our clients, partner involvement in all deals and transactions, at all times.

High Quality Legal Advice – We deliver services of the highest quality, which are capable of meeting the most exacting standards.

Availability and Responsiveness – We are proactive in our approach and are available to our clients at all times.

Legal Research and Analysis Based Advisory – While we do keep abreast of market practices applicable to legal interpretation, they are adopted and recommended only if they are supported by prevailing legal and regulatory framework.

Key Accolades In the short span of existence, the firm has firmly established itself in the Indian legal market and has received wide media recognition. Some of the key accolades include:

:

:

Highest client satisfaction rating amongst top 20 Indian law firms -2013 Indian Law Firm Ranking and Report by RSG Consulting

Best Firm in India Asia Women in Business LawAwards, 2016, Euromoney, Hong Kong

Winner in the category: Energy, Projects &Infrastructure - India Business Law JournalIndian Law Firm Awards 2014

Winner in the category: Finance Law - FinanceLaw Firm of the Year – India: Corporate INTLLegal Awards 2013

Highly recommended as a leading firm Variouspractice areas, Chambers Asia Pacific – 2012,2013, 2014, 2015, 2016 and 2017

Shortlisted as one of the Indian firms forChambers Asia Pacific Awards 2014 and 2015organised by Chambers & Partners

Highest client satisfaction rating amongst top 20Indian law firms - 2013 Indian Law Firm Rankingand Report by RSG Consulting

IBLJ, Indian Law Firm Award 2016 - Energy, projects & infrastructure, structured finance & securitization

Winner in the category: Finance Litigation LawFirm of The Year – India – Global Awards for2014 - Corporate Livewire

30 LexisNexis Foreign Investment Law Guide 2017-2018

1. What are the main reasons foreign investors invest in your jurisdiction?

India has emerged as one of the most attrac-tive destinations for foreign investment from around the globe. The United Nations Conference on Trade and Development’s World Investment Report 2017 ranks India within the top ten countries around the world for attracting foreign direct investment (‘’FDI’’) inflows and fourth amongst the Asian countries. According to the said report, India’s total FDI inflow in the year 2016 was USD 44,486 bn. As per the statistics made available by the Department of Industrial Policy and Promotion, the FDI into India during the period from April-September 2016 rose 30% year on year with the most investments in the service sector industries followed by telecom-munications and trading.

There are several reasons for India to remain as a top-notch destination for FDI inflow. While some of these are specific to different business sectors, many are common to all sectors. One of the key attraction across the board remains the low cost of labour intensive set up ranging from manufacturing units (which require both unskilled and skilled labour) to any service industry such as information technology (which needs an expert and technically skilled workforce).

Essentially the initiatives of the Government of India, have persistently worked towards liberalizing the FDI regime, and succeeded in boosting the growth of FDI over the years.

2. What foreign investment legislation is in place in your jurisdiction (e.g. Foreign Investment Law or Foreign Investment Catalogue)? Please provide a brief overview of such legislation.

Foreign investments into India are gov-erned by the Foreign Direct Investment Policy (‘’FDI Policy’’) of India issued by the Ministry of Commerce and Industry through the Department of Industrial Policy and Promotion.

With liberalization being the focus of the gov-ernment of India for over two decades, FDI in most of the sectors except few is permitted up to 100% under the automatic route. FDI in cer-tain sectors is still reserved under the approval route either up to 100% or over and above the prescribed sectoral cap for strategic or security reasons. Broadly, the FDI Policy lays down the sectoral cap on FDI in various business/indus-try sectors and terms and conditions relating to FDI in each of the said sectors.

Although there is no prior approval required in relation to the FDI except in few sectors, post investment notification is required to be provided to the Government of India. The FDI Policy prescribes various reporting requirements, including notification of receipt of remittance in foreign currency as FDI and allotment of shares to a foreign resident.

Additionally, a transaction involving foreign currency is governed by the Foreign Exchange Management Act 1999 (‘’FEMA’’) and regu-lations issued thereunder the central bank of India namely, the Reserve Bank of India. FEMA

Jurisdiction: IndiaFirm: Phoenix Legal Author: Manjula Chawla and Ritika Ganju

Jurisdictional Q&A – India 31

regulations play a vital role in governing FDI transactions.

3. What restrictions are placed on foreign investment? Does this differ at local levels of government?

Over the last few years, the government of India has revised the FDI norms to open the gates for FDI in most of the sectors and has been persistently making efforts to liberalize the FDI Policy to the greatest extent. The sectoral caps and restrictions are reviewed and revised from time to time with the aim of liberalization of the regime unless justified for the larger public interest and security reasons.

The current FDI Policy prohibits foreign investment in the sectors of lottery business, online lotteries, manufacturing of cigarettes or tobacco or tobacco related products, atomic energy, railways, gambling and betting includ-ing casinos, chit funds, ‘nidhi’ companies, trading in transferable development rights and the business of real estate or construction of farmhouses. Broadly, the restriction in terms of sectoral caps is 49% for most of the capped sectors. Investment that is over and above 49% of FDI in the capped sectors requires prior government approval.

The FDI Policy is applicable across India and the above described sectoral caps are applicable across all states. Among these sectors, it is only in relation to the sector of multi-brand retail that the state governments have been given discretion to permit FDI even up to 51%.

4. What are the most common business vehicles for foreign investors? How long do they take to be set up? What are the key requirements for the establishment and operation of these vehicles?

The current FDI Policy permits FDI through various business vehicles which primarily include a company, sole proprietorship and a limited liability partnership.

Conventionally, FDI has always been brought into India to be infused in a company which may either be a private or a public limited com-pany. A major consideration for foreign entities looking to bring FDI into India is whether to set up a wholly owned subsidiary to carry out business operations in India independently or to form a joint venture company with an expe-rienced Indian partner. In our experience, the decision between a wholly owned subsidiary and a joint venture company is influenced by the nature of business activity that is to be carried out and the level of local assistance that will be required to run the business effectively.

FDI in more recently liberalized business vehi-cles such as sole proprietorships and limited liability partnerships, are not common ways of infusing foreign direct investment into India at present.

The government of India, has recently integrated and simplified the process for incor-porating a company for foreign investors who are incorporating a joint venture company or a wholly owned subsidiary. Upon filing a single form, a company can be incorporated within 6-7 working days. The main requirements for incorporating a company are a minimum of two shareholders and two directors (one director being an Indian national).

5. Under what circumstances are foreign investments subject to government approvals? What is the process and timeline for such approvals?

There are very few sectors in which FDI can be brought in only with prior government approval. These are mining and mineral sep-aration of titanium bearing minerals and ores, publishing/printing of scientific and technical magazines/specialty journals/ periodicals, publication of facsimile edition of foreign news-papers, private security agencies, multi brand retail trading, pharmaceutical (brownfield) and satellites.

32 LexisNexis Foreign Investment Law Guide 2017-2018

and talked about of these being the requirement for all foreign multi-brand retailers to source at least 30% of the values of procurement of manufactured/processed products from Indian micro, small or medium industries.

Depending on the sector of business, there are also a number of industry specific regulators that regulate the functioning of entities in a particular industry, for instance the IRDAI (Insurance Regulatory and Developmental Authority of India) which regulates the functioning of the insurance and reinsurance companies in India, by way of issuing guide-lines and circulars. Similarly, the telecom industry is regulated by the TRAI (Telecom Regulatory Authority of India).

Foreign investment in other sectors such as manufacturing in the defence, insurance, power exchange, private sector banking and infrastructure companies in security are less restricted as FDI is permitted without central government approval up to a specified percent-age and investments crossing the prescribed threshold require central government approval. Additionally, FDI in certain sectors such as banking, broadcasting and multi brand retail trading are only permissible up to a specified limit regardless of government approval.

There are also sectors which are fully liberal-ized and 100% FDI under these sectors falls under the automatic route. These sectors include agriculture and animal husbandry, plantation sector, mining and exploration of metal and non-metal ores, greenfield projects under civil aviation and pharmaceutical companies, construction development (town-ships, housing, built-up infrastructure, new and existing industrial parks), cash and carry wholesale trading/wholesale trading, e-com-merce activities, railway infrastructure, asset reconstruction companies etc.