Embed Size (px)

Citation preview

CMP 336.70

Target Price 378.00

ISIN: INE154A01025

JUNE 6th

2014

ITC LIMITED

Result Update (PARENT BASIS): Q4 FY14

BUY

Index Details

Stock Data

Sector FMCG

BSE Code 500875

Face Value 1.00

52wk. High / Low (Rs.) 386.75/285.40

Volume (2wk. Avg.) 756000

Market Cap (Rs. in mn.) 2677842.44

Annual Estimated Results (A*: Actual / E*: Estimated)

YEARS FY14A FY15E FY16E

Net Sales 332386.00 365624.60 394874.57

EBITDA 135619.80 149431.96 161027.81

Net Profit 87852.10 97273.21 104925.66

EPS 11.05 12.23 13.19

P/E 30.48 27.53 25.52

Shareholding Pattern (%)

1 Year Comparative Graph

ITC LTD S&P BSE SENSEX

SYNOPSIS

ITC is one of the India's foremost FMCG private sector companies with a market capitalization of over US $ 45 billion and a turnover of US $ 7 billion.

During the 4th quarter of the year, Net Turnover at Rs. 91451.4 mn registered a growth of 11.8%.

Pre-tax profits at Rs. 32227.4 mn and Post-tax profits at Rs. 22780.1 mn grew at an impressive rate of 18.1% and 18.2% respectively over the same period last year.

EBIDTA is Rs. 34701.00 mn as against Rs. 29603.00 mn in Q4 FY13, an increase of 17.22%.

Gross Revenue for the year grew by 11.7% to Rs. 467126.2 mn. Net Revenue at Rs. 328825.6 mn grew by 11.1%.

During FY14, Pre-tax profit increased by 18.5% to Rs. 126591.1 mn while Net Profit at Rs. 87852.1 mn registered a growth of 18.4%.

During the year, Non-Cigarette FMCG segment registers robust revenue growth of 16%.

The FMCG-Others Segment recorded its maiden profit during the year with a PBIT of Rs. 220 mn.

During the year, the Paperboards, Paper and Packaging segment recorded a growth of 14.7% in Revenue.

During the year, Agri Business profits grow 14.2% driven by improved realizations and higher volumes.

ITC Ltd has recommended a dividend of Rs. 6/- each per Ordinary share of Re. 1/- each for the financial year ended March 31, 2014.

Net Sales and PAT of the company are expected to grow at a CAGR of 10% and 12% over 2013 to 2016E respectively.

PEER GROUPS CMP MARKET CAP EPS P/E (X) P/BV(X) DIVIDEND

Company Name (Rs.) Rs. in mn. (Rs.) Ratio Ratio (%)

ITC Ltd. 336.70 2677842.44 11.05 30.48 10.22 600.00

Hindustan Unilever Ltd 638.40 1371410.30 17.88 35.46 51.29 1300.00

Dabur India Ltd 191.10 335970.40 3.83 49.95 20.91 175.00

Godrej Consumer Ltd 875.00 299532.90 16.59 53.04 9.01 525.00

Recommendation & Analysis - ‘BUY’

ITC continued to deliver strong financial performance with healthy growth in revenues and high quality earnings.

During the 4th quarter of the year, Net Turnover at Rs. 91451.4 mn registered a growth of 11.8% driven by

robust performance in the Non-Cigarette FMCG, Paperboard, Paper & Packaging and Cigarettes segments. Pre-tax

profits at Rs. 32227.4 mn and Post-tax profits at Rs. 22780.1 mn grew at an impressive rate of 18.1% and 18.2%

respectively over the same period last year.

Gross Revenue for the year grew by 11.7% to Rs. 467126.2 mn. Net Revenue at Rs. 328825.6 mn grew by 11.1%

primarily driven by a 16.0% growth in the non-cigarette FMCG segment, 14.7% growth in Paperboards, Paper &

Packaging segment and 10.6% growth in the Cigarettes business. Pre-tax profit increased by 18.5% to Rs.

126591.1 mn while Net Profit at Rs. 87852.1 mn registered a growth of 18.4%. Earnings Per Share for the year

stood at Rs. 11.09 (previous year Rs. 9.45). Cash flows from Operations aggregated Rs. 107600 mn compared to

Rs. 95960 mn in the previous year.

During the year, Non-Cigarette FMCG segment registers robust revenue growth of 16%, despite a challenging

operating environment. The FMCG-Others Segment recorded its maiden profit during the year with a PBIT of Rs.

220 mn representing a positive swing of Rs. 1030 mn over FY13 driven by enhanced scale, operating leverage,

supply chain efficiencies and strategic cost management initiatives. Agri Business profits grow 14.2% driven by

improved realizations and higher volumes. Paperboards, Paper & Packaging Segment Revenues up 14.7% aided

by higher volumes and product mix enrichment. Profitability impacted by steep increase in wood, coal and

chemical costs. Over FY2013-16E, we expect the company to post a CAGR of 10% and 12% in its top-line and

bottom-line respectively. Hence, we recommend ‘BUY’ for ‘ITC LTD’ with a target price of Rs. 378.00.

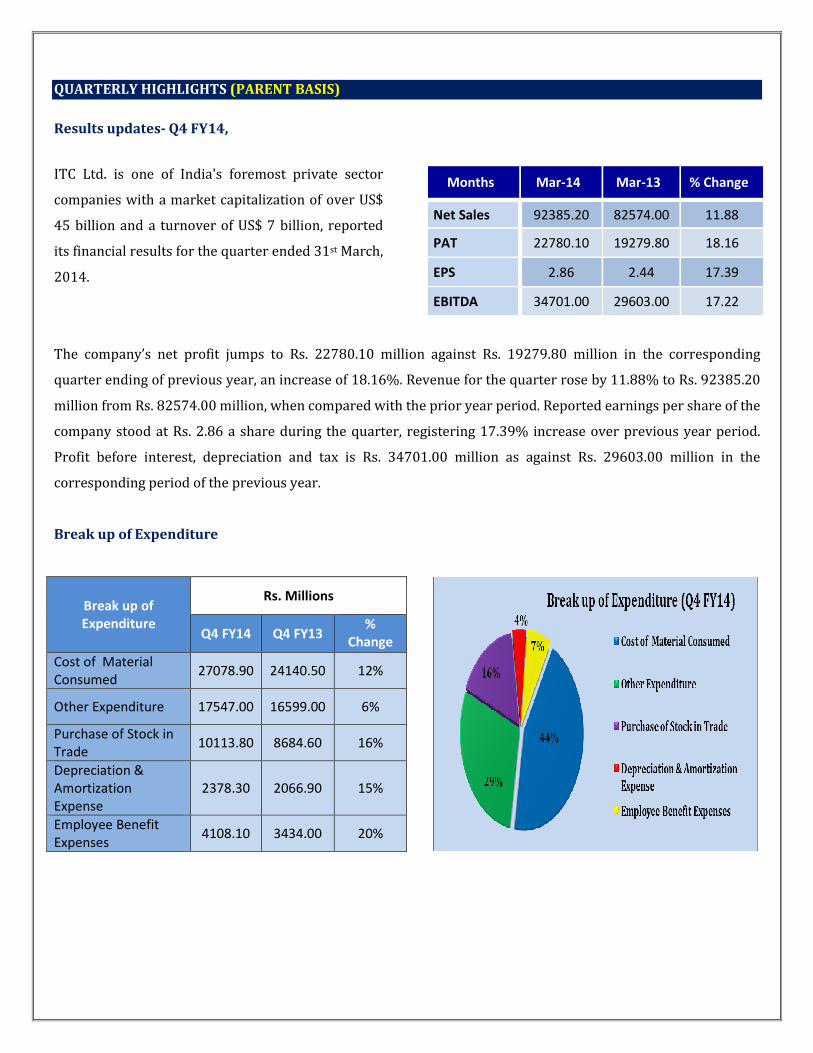

QUARTERLY HIGHLIGHTS (PARENT BASIS)

Results updates- Q4 FY14,

ITC Ltd. is one of India's foremost private sector

companies with a market capitalization of over US$

45 billion and a turnover of US$ 7 billion, reported

its financial results for the quarter ended 31st March,

2014.

Months Mar-14 Mar-13 % Change

Net Sales 92385.20 82574.00 11.88

PAT 22780.10 19279.80 18.16

EPS 2.86 2.44 17.39

EBITDA 34701.00 29603.00 17.22

The company’s net profit jumps to Rs. 22780.10 million against Rs. 19279.80 million in the corresponding

quarter ending of previous year, an increase of 18.16%. Revenue for the quarter rose by 11.88% to Rs. 92385.20

million from Rs. 82574.00 million, when compared with the prior year period. Reported earnings per share of the

company stood at Rs. 2.86 a share during the quarter, registering 17.39% increase over previous year period.

Profit before interest, depreciation and tax is Rs. 34701.00 million as against Rs. 29603.00 million in the

corresponding period of the previous year.

Break up of Expenditure

Break up of

Expenditure

Rs. Millions

Q4 FY14 Q4 FY13 %

Change

Cost of Material

Consumed 27078.90 24140.50 12%

Other Expenditure 17547.00 16599.00 6%

Purchase of Stock in

Trade 10113.80 8684.60 16%

Depreciation &

Amortization

Expense

2378.30 2066.90 15%

Employee Benefit

Expenses 4108.10 3434.00 20%

Segment Revenue

Latest Updates

• ITC Ltd has recommended a dividend of Rs. 6/- each per Ordinary share of Re. 1/- each for the financial year

ended March 31, 2014.

• During the quarter, ITC has issued and allotted 1,76,87,110 Ordinary Shares of Re. 1/- each e under the

Company’s Employee Stock Option Schemes. Consequently, the issued and paid-up Share Capital of the

Company as on 31st March, 2014 stands increased to Rs. 7,95,31,82,950/-.

• North East Nutrients Private Limited became a subsidiary of the Company with effect from 6th February,

2014, consequent upon acquisition of 76% of NENPL’s share capital.

COMPANY PROFILE

ITC is one of India's foremost private sector companies with a market capitalization of over US $ 45 billion and a

turnover of US $ 7 billion. ITC is rated among the World's Best Big Companies, Asia's 'Fab 50' and the World's

Most Reputable Companies by Forbes magazine, among India's Most Respected Companies by Business World

and among India's Most Valuable Companies by Business. ITC ranks among India's 10 Most Valuable (Company)

Brands'. ITC also ranks among Asia's 50 best performing companies.

ITC has a diversified presence in FMCG, Hotels, Paperboards & Specialty Papers, Packaging, Agri-Business, and

Information Technology. While ITC is an outstanding market leader in its traditional businesses of Cigarettes,

Hotels, Paperboards, Packaging and Agri-Exports, it is rapidly gaining market share even in its nascent

businesses of Packaged Foods & Confectionery, Branded Apparel, Personal Care and Stationery.

ITC's Agri-Business is one of India's largest exporters of agricultural products. The ITC group's contribution to

foreign exchange earnings over the last ten years amounted to nearly US$ 5.4 billion, of which agri exports

constituted 56%. The Company's 'e-Choupal' initiative is enabling Indian agriculture significantly enhance its

competitiveness by empowering Indian farmers through the power of the Internet. ITC's production facilities and

hotels have won numerous national and international awards for quality, productivity, safety and environment

management systems. ITC was the first company in India to voluntarily seek a corporate governance rating.

ITC's R&D Centre the first independent R&D centre in India to get ISO 9001 accreditation and certified with ISO

14001 for EMS by DNV. The R&D Centre is also certified for the standard ISO/IEC17025:2005, by National

Accreditation Board for Testing and Calibration Laboratories (NABL). This certification is awarded for "General

requirement for the competence of Testing & Calibration Laboratories".

Other Business Areas

• Hotels

ITC's hotels have evolved into being India's second largest hotel chain with over 90 hotels throughout the

country. ITC is also the exclusive franchisee in India of two brands owned by Sheraton International Inc. -

The Luxury Collection & Sheraton which ITC uses in association with its own brands in the luxury 5 Star

segment. Brands in the hospitality sector owned & operated by its subsidiaries include Fortune and

Welcome Heritage brands.

• Infotech India Ltd.

ITC's wholly owned Information Technology subsidiary, ITC Infotech India Ltd, provides IT services and

solutions to leading global customers. ITC Infotech has carved a niche for itself by addressing customer

challenges through innovative IT solutions.

• ITC's Agri-Business

ITC's Agri-Business is one of India's largest exporters of agricultural products. The Company's 'E-

Choupal' initiative is enabling Indian agriculture significantly enhance its competitiveness by

empowering Indian farmers through the power of the Internet.

FINANCIAL HIGHLIGHT (PARENT BASIS) (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as at March 31, 2013 -2016E

ITC Ltd. FY13A FY14A FY15E FY16E

SOURCES OF FUNDS

Shareholder's Funds

Share Capital 7901.80 7953.20 7953.20 7953.20

Reserves and Surplus 214976.70 254667.00 299888.62 347870.80

1. Sub Total - Net worth 222878.50 262620.20 307841.82 355824.00

Non Current Liabilities

Long term borrowings 664.00 510.00 448.80 426.36

Deferred Tax Liabilities 12037.20 12969.60 13618.08 14162.80

Other Long term Liabilities 31.10 50.90 61.08 69.02

Long Term Provisions 1256.20 1100.00 990.00 1049.40

2. Sub Total - Non Current Liabilities 13988.50 14630.50 15117.96 15707.58

Current Liabilities

Short Term Borrowings 0.00 1.40 1.54 1.79

Trade Payables 16689.80 19875.90 22261.01 24041.89

Other Current Liabilities 35286.20 36318.80 37045.18 37786.08

Short Term Provisions 51331.30 58847.10 63554.87 66732.61

3. Sub Total - Current Liabilities 103307.30 115043.20 122862.59 128562.37

Total Liabilities (1+2+3) 340174.30 392293.90 445822.37 500093.95

APPLICATION OF FUNDS

Non-Current Assets

a) Fixed Assets 126971.30 143084.70 159711.61 176473.73

b) Non-current investments 20008.60 25121.70 29643.61 34090.15

c) Long Term loans and advances 17279.70 14800.20 13468.18 14276.27

1. Sub Total - Non Current Assets 164259.60 183006.60 202823.39 224840.15

Current Assets

Current Investment 50594.30 63112.60 74472.87 85643.80

Inventories 66002.00 73595.40 80954.94 87431.34

Trade receivables 11633.40 21653.60 29232.36 36832.77

Cash and Bank Balances 36150.00 32893.70 36183.07 39077.72

Short-terms loans & advances 5121.40 7835.10 9715.52 11464.32

Other current assets 6413.60 10196.90 12440.22 14803.86

2. Sub Total - Current Assets 175914.70 209287.30 242998.98 275253.80

Total Assets (1+2) 340174.30 392293.90 445822.37 500093.95

Annual Profit & Loss Statement for the period of 2013 to 2016E

Value (Rs.in.mn) FY13A FY14A FY15E FY16E

Description 12m 12m 12m 12m

Net Sales 299012.70 332386.00 365624.60 394874.57

Other Income 9387.00 11071.40 11957.11 12554.97

Total Income 308399.70 343457.40 377581.71 407429.54

Expenditure -192737.60 -207837.60 -228149.75 -246401.73

Operating Profit 115662.10 135619.80 149431.96 161027.81

Interest -864.70 -29.50 -172.94 -121.06

Gross profit 114797.40 135590.30 149259.02 160906.75

Depreciation -7955.60 -8999.20 -9899.12 -10691.05

Profit Before Tax 106841.80 126591.10 139359.90 150215.70

Tax -32657.90 -38739.00 -42086.69 -45290.03

Net Profit 74183.90 87852.10 97273.21 104925.66

Equity capital 7901.80 7953.20 7953.20 7953.20

Reserves 214449.20 254142.90 299888.62 347870.80

Face value 1.00 1.00 1.00 1.00

EPS 9.39 11.05 12.23 13.19

Quarterly Profit & Loss Statement for the period of 30th Sep, 2013 to 30th June, 2014E

Value (Rs.in.mn) 30-Sep-13 31-Dec-13 31-Mar-14 30-Jun-14E

Description 3m 3m 3m 3m

Net sales 78625.30 87268.50 92385.20 84994.38

Other income 2461.90 3910.60 2667.10 2533.75

Total Income 81087.20 91179.10 95052.30 87528.13

Expenditure -46866.90 -54425.50 -60351.30 -53070.49

Operating profit 34220.30 36753.60 34701.00 34457.64

Interest 326.70 -91.40 -95.30 -76.24

Gross profit 34547.00 36662.20 34605.70 34381.40

Depreciation -2208.70 -2259.20 -2378.30 -2449.65

Profit Before Tax 32338.30 34403.00 32227.40 31931.75

Tax -10033.00 -10549.60 -9447.30 -9771.11

Net Profit 22305.30 23853.40 22780.10 22160.63

Equity capital 7920.00 7935.50 7953.20 7953.20

Face value 1.00 1.00 1.00 1.00

EPS 2.82 3.01 2.86 2.79

Ratio Analysis

Particulars FY13A FY14A FY15E FY16E

EPS (Rs.) 9.39 11.05 12.23 13.19

EBITDA Margin (%) 38.68% 40.80% 40.87% 40.78%

PBT Margin (%) 35.73% 38.09% 38.12% 38.04%

PAT Margin (%) 24.81% 26.43% 26.60% 26.57%

P/E Ratio (x) 35.86 30.48 27.53 25.52

ROE (%) 33.36% 33.52% 31.60% 29.49%

ROCE (%) 55.43% 55.07% 51.68% 48.20%

EV/EBITDA (x) 22.26 19.04 17.18 15.86

Book Value (Rs.) 28.14 32.95 38.71 44.74

P/BV 11.97 10.22 8.70 7.53

Charts

OUTLOOK AND CONCLUSION

� At the current market price of Rs.336.70, the stock P/E ratio is at 27.53 x FY15E and 25.52 x FY16E

respectively.

� Earning per share (EPS) of the company for the earnings for FY15E and FY16E is seen at Rs.12.23 and

Rs.13.19 respectively.

� Net Sales and PAT of the company are expected to grow at a CAGR of 10% and 12% over 2013 to 2016E

respectively.

� On the basis of EV/EBITDA, the stock trades at 17.18 x for FY15E and 15.86 x for FY16E.

� Price to Book Value of the stock is expected to be at 8.70 x and 7.53 x respectively for FY15E and FY16E.

� We expect that the company surplus scenario is likely to continue for the next three years, will keep its

growth story in the coming quarters also. We recommend ‘BUY’ in this particular scrip with a target price of

Rs.378.00 for Medium to Long term investment.

INDUSTRY OVERVIEW

The FMCG industry witnessed a marked slowdown during the year in the backdrop of a challenging macro-

economic environment which, inter alia, saw growth in Private Final Consumption Expenditure in real terms

decelerating to around 3% during the year. Categories involving higher discretionary spends or with relatively

high penetration levels were impacted the most. The trend of premiumisation witnessed in recent years in most

major categories also did not carry through as strongly.

Cigarette industry

The Cigarette industry had to contend with a steep increase in Excise Duty for the second year in succession

along with discriminatory and punitive increases in Value Added Tax (VAT) rates by some States. Such tax

increases not only undermine the legal domestic cigarette industry and sub-optimise revenue potential from this

sector but also fail to achieve the objective of tobacco control in the country.

According to various independent reports, there is a high degree of dual consumption with an estimated 60% of

cigarette consumers in India also consuming other forms of tobacco. High incidence of taxation and a

discriminatory regulatory regime on cigarettes have, over the years, led to a significant shift in tobacco

consumption to cheaper and revenue inefficient forms like bidis, chewing tobacco etc. Thus, while overall

tobacco consumption is increasing in India, the share of legal cigarettes in overall tobacco consumption has

declined from 21% in 1981/82 to below 12% in 2013/14. Consequently, India has a miniscule share of only 1.8%

of global cigarette consumption but constitutes nearly 84% of the global consumption of smokeless tobacco. In

fact, India's annual per capita consumption of cigarettes is the lowest in the world. The requirement therefore is

an India-centric tax and policy framework for tobacco that cognises for the unique consumption pattern in the

country.

High taxes on domestic cigarettes have also led to an increasing demand for cheaper tax-evaded cigarettes. The

revenue loss to the Government on account of this trade is estimated at over Rs. 6,000 crores. The menace of

illegal trade is compounded by the imposition of high VAT rates by States. Despite a consensus amongst the

Empowered Committee of State Finance Ministers that all tobacco products would be taxed at Revenue Neutral

Rates applicable to general category of goods, there are 29 different tax rates currently applicable on cigarettes

Hotels

The hospitality sector continued to be adversely impacted by the weak economic environment prevailing in

major international source markets and in India on the one hand, and significant additions to room supplies in

key Indian cities on the other. Against the backdrop of such a challenging business environment, Segment

Revenues saw a modest increase of 5.5% during the year. While the Hotels Business maintained its leadership

position in the industry in terms of operating margins, Segment Results were impacted mainly on account of the

relatively weak pricing scenario and increase in operating costs in an inflationary environment.

Paperboards & Specialty Papers

The global paper market continued to witness a structural shift with emerging economies, particularly in Asia

such as China and India, driving the demand growth. Though India has 17% of the world’s population, it

consumes only about 2% of global paper production. Per capita consumption in India is very low at only 9 kgs

compared to a global average of 55 kgs, 65 kgs in China and 215 kgs in Japan.

The domestic paper and paperboard industry is currently estimated at 11.6 million tonnes per annum, out of

which paperboards is 2.2 million tonnes per annum which is expected to grow at around 8% per annum aided by

value-added paperboard at 12% per annum.

Conclusion

While the rural market certainly offers a big attraction to marketers, it would be naïve to think that any company

can enter the market without facing any problems and walk away with a sizable share. Distribution is the most

important variable in the marketing plans of most consumer goods manufacturers, because managing such a

massive sales and distribution network is in itself a huge task.

This sector will continue to see growth as it depends on an ever-increasing internal market for consumption, and

demand for these goods remains more or less constant, irrespective of recession or inflation. Hence this sector

will grow, though it may not be a smooth growth path, due to the present world-wide economic slowdown, rising

inflation and fall of the rupee. This sector will see good growth in the long run and hiring will continue to remain

robust.

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation for the purchase or sale

of any financial instrument or as an official confirmation of any transaction. The information contained herein is

from publicly available data or other sources believed to be reliable but do not represent that it is accurate or

complete and it should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s affiliates shall

not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the

information contained in this report. This document is provide for assistance only and is not intended to be and must

not alone be taken as the basis for an investment decision.

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

B. Anil Kumar Auto, IT & FMCG

M. Vinayak Rao Diversified

C. Bhagya Lakshmi Diversified

B. Vasanthi Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com