Embed Size (px)

Citation preview

It’s a Whole New World:Estate and Tax Planning

for Same-Sex Couples after the Demise of DOMA

Hawaii Estate Planning Council September 26, 2013

Susan von HerrmannSchiff Hardin, LLP

© Schiff Hardin LLP. All rights reserved.

• The Old World

• The New World• Hollingsworth v. Perry• U.S. v. Windsor

• Federal Rights and Responsibilities

• Modifying Estate Plans

• Tax Issues

Overview

© Schiff Hardin LLP. All rights reserved.2

Section 2No State, territory, or possession of the United States, or Indian tribe, shall be required to give effect to any public act, record, or judicial proceeding of any other State, territory, possession, or tribe respecting a relationship between persons of the same sex that is treated as a marriage under the laws of such other State, territory, possession, or tribe, or a right or claim arising from such relationship.

Section 3In determining the meaning of any Act of Congress, or of any ruling, regulation, or interpretation of the various administrative bureaus and agencies of the United States, the word “marriage” means only a legal union between one man and one woman as husband and wife, and the word “spouse” refers only to a person of the opposite sex who is a husband or a wife.

Federal Defense of Marriage Act (DOMA)

© Schiff Hardin LLP. All rights reserved.3

Statewide Marriage Prohibitions*

State with constitutional amendment restricting marriage to one man and one woman (30 states)

State with law restricting marriage to one man and one woman (6 states) *Source: Human Rights Campaign.

© Schiff Hardin LLP. All rights reserved.4

Marriage Equality & OtherRelationship Recognition Laws*

Marriage licenses issued to same-sex couples (12 states plus D.C.)

Statewide law providing some statewide spousal rights to same-sex couples within the state (1 state)Statewide law providing the equivalent of

statewide spousal rights to same-sex couples within the state (7 states plus D.C.)

*Source: Human Rights Campaign.

© Schiff Hardin LLP. All rights reserved.5

Same-sex couples, irrespective of their status under state law, were legal strangers under federal law.

State law status:• Married• Marriage Equivalent

• Civil Union• Registered Domestic Partnership

• No Legal Relationship

Old World: No Federal Rights

© Schiff Hardin LLP. All rights reserved.6

Reciprocal Beneficiaries ActCivil Union – as of January 1, 2012

• Available to both same-sex and opposite sex couples

• No residency requirement • Three steps:

1. Apply for civil union license2. Appear before civil union agent to

receive license3. Hold civil union ceremony

Focus on Hawaii

© Schiff Hardin LLP. All rights reserved.7

Duties of joint financial support and liability for family debtsParenting rightsRight to seek financial support after a break-upHospital visitation and medical decision-making powersRight to administer deceased partner’s estateRight to inherit in the absence of a willState employee benefitsRight to file joint state tax returnsUnlimited marital deduction for state estate tax

Hawaii Civil Union—Rights and Responsibilities

© Schiff Hardin LLP. All rights reserved.8

Hollingsworth v. Perry:•On August 4, 2010, Judge Vaughn R. Walker struck down Proposition 8, finding that it violates due process and equal protection rights under the United States Constitution•The Ninth Circuit Court of Appeals agreed that the ban on same-sex marriage in California is unconstitutional •On June 26, 2013, the U.S. Supreme Court declined to rule on the merits in Perry, leaving in place Judge Walker’s decision that Proposition 8 is unconstitutional. As a result, California’s state DOMA is dead, and same-sex couples again have the right to marry in this state

The New World: Return of Same-Sex Marriage in California

© Schiff Hardin LLP. All rights reserved.9

On June 26, 2013, the U.S. Supreme Court, in a 5-4 decision, held that Section 3 of the Defense of Marriage Act (DOMA) is unconstitutional as a violation of the right to equal protection that is guaranteed by the Fifth Amendment.

Validly married same-sex couples will now enjoy more than 1100 federal rights and responsibilities.

Became effective 25 days after the date of the decision (i.e., on or about July 21, 2013).

United States v. Windsor

© Schiff Hardin LLP. All rights reserved.10

Section 2 of DOMA is still intact. States that prohibit same-sex marriage do not have to recognize marriages celebrated in other states.

There is no federal right to same-sex marriage.

The federal government looks to state law to determine who is married and who is not for the purpose of applying federal law.

DOMA Not Completely Dead

© Schiff Hardin LLP. All rights reserved.11

Living in Marriage Recognition State

Living in Non-Recognition State

Married All federal rights and responsibilities

Most federal rights and responsibilities

RDPs/Civil Unions

Probably no federal rights

Probably no federal rights

No Legal Status

No rights No rights

The New World

© Schiff Hardin LLP. All rights reserved.12

• Social Security spousal and family protections

• Rights under Family Medical Leave Act to care for spouse

• Veteran and military benefits for spouse• Federal health and retirement benefits

for spouse• COBRA coverage for spouse• Right to petition for spouse to immigrate

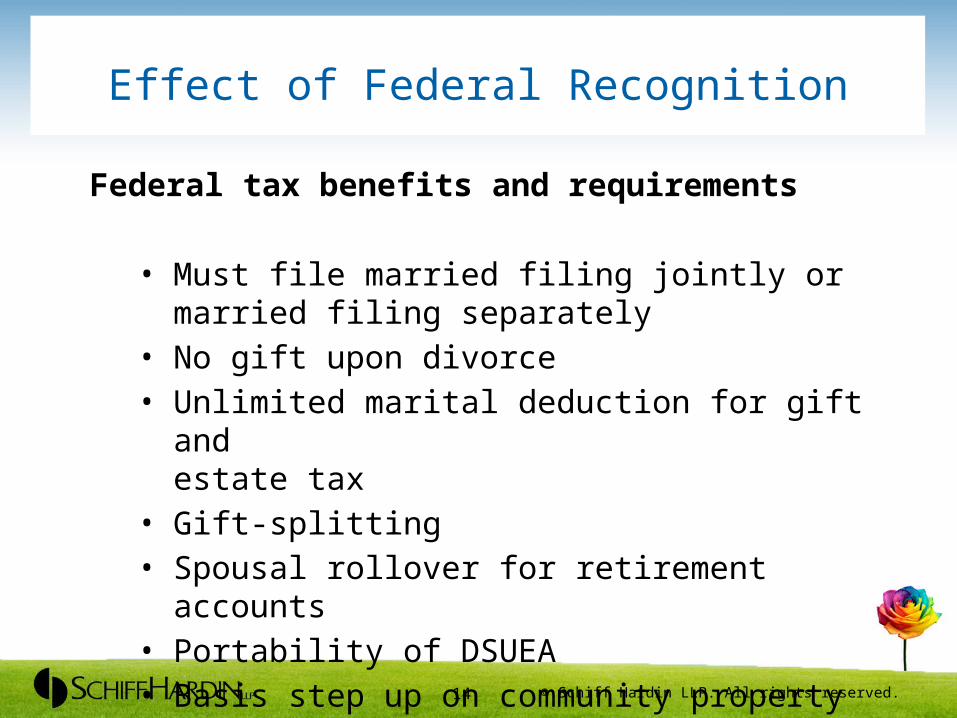

Effect of Federal Recognition

© Schiff Hardin LLP. All rights reserved.13

Federal tax benefits and requirements

• Must file married filing jointly or married filing separately

• No gift upon divorce• Unlimited marital deduction for gift and

estate tax• Gift-splitting• Spousal rollover for retirement accounts• Portability of DSUEA• Basis step up on community property

Effect of Federal Recognition

© Schiff Hardin LLP. All rights reserved.14

All validly married same-sex couples now have the right (and are required) to file either Married Filing Jointly or Married Filing Separately.

Federal Income Tax Returns

© Schiff Hardin LLP. All rights reserved.15

The so-called "marriage penalty" may cause two high-earning spouses to pay more tax jointly than if they had not married and could still file as single people.

Marriage Penalty Examples• Case 1: one spouse earns all income• Case 2: both spouses earn equally

Assume $1M of total income$700k wages; $150k qualified dividend; $150k interest

Federal Income Tax Returns

© Schiff Hardin LLP. All rights reserved.16

Federal Income Tax Returns

© Schiff Hardin LLP. All rights reserved.17

Tax Due Spouse A Spouse B Total Spouse A Spouse B TotalFederal 299,003 - 299,003 304,767 - 304,767 California 96,338 - 96,338 109,631 - 109,631

395,341 414,398

Married SingleTax Due Spouse A Spouse B Total Spouse A Spouse B TotalFederal 149,502 149,502 299,003 136,212 136,212 272,424 California 48,169 48,169 96,338 48,169 48,169 96,338

395,341 368,762

Case 1: One Spouse Earns AllMarried Single

Case 2: Both Spouses Earn Equally

There may be benefits of filing jointly other than lower marginal rates.

• Ability to combine one spouse’s capital losses with the other’s capital gains

• Ability to combine one spouse’s passive activity losses with the other’s passive income

• Ability to combine one spouse’s net operative or business loss with the other’s overall income

Benefits of Filing Jointly

© Schiff Hardin LLP. All rights reserved.18

Now that the federal government recognizes same-sex marriage, federal tax law relating to divorce also will apply to those couples.

Prior to Windsor:• Same-sex couples who terminated their

relationship and divided their property pursuant to a settlement agreement would not be protected against any negative tax consequences

• Alimony paid was not deductible

Tax Issues Related to Divorce

© Schiff Hardin LLP. All rights reserved.19

After Windsor:

• Divorce has the same tax implications for all validly married couples

• Division of property pursuant to a settlement agreement does not trigger any tax to either ex-spouse

• Alimony is deductible

Tax Issues Related to Divorce

© Schiff Hardin LLP. All rights reserved.20

• All states have some residency requirement for divorce.

• Same-sex couples living in non-recognition states may not be able to divorce (Hawaii)

• Some states now permit dissolution of a marriage celebrated in the state when neither party resides in a state that will grant dissolution (e.g. California, Delaware, Minnesota, Vermont, Washington D.C.).

• Jurisdiction over child custody based on child’s residence under the Uniform Child Custody Jurisdiction and Enforcement Act (UCCJEA).

Wedlocked?

© Schiff Hardin LLP. All rights reserved.21

Opposite-Sex Married Couple• Upon first spouse’s death, assets

transferred to surviving spouse tax-free• No estate tax until surviving spouse’s death

and assets pass to non-charitable beneficiaries

Same-Sex Married Couple, prior to Windsor• Upon first death, assets over the estate tax

exemption ($5.25M in 2013) transferred to survivor were taxed

• Estate tax possibly paid again at survivor’s death if assets not held in trust

Unlimited Marital Deduction for Estate and Gift Tax

© Schiff Hardin LLP. All rights reserved.22

Opposite-Sex Same-Sex Married Married Couple Couple, prior to Windsor

Year 1 20,000,000 First Spouse's Death Year 1 20,000,000 First Spouse's Death

Elects Portability (5,250,000) Estate Tax Exemption - to Survivor

20,000,000 14,750,000

- Tax (marital deduction) (5,900,000) Tax

20,000,000 Passes to Survivor 14,100,000 Passes to Survivor

Year 10 32,577,893 Year 10 22,967,414

(10,500,000) Estate Tax Exemption (5,250,000) Estate Tax Exemption

22,077,893 17,717,414

(8,831,157) Tax Paid (7,086,966) Tax Paid

13,246,736 Net Estate 10,630,448 Net Estate

8,831,157 Paid in Tax

12,986,966 Paid in Tax

23,746,736 Passes to Beneficiaries 15,880,448 Passes to Beneficiaries

AssumptionsNet Worth – $20MEstate Tax Exemption – $5.25MCombined Estate Tax Rate – 40%Asset Growth Rate – 5%

© Schiff Hardin LLP. All rights reserved.23

Lifetime transfers between spouses do not constitute taxable gifts.

• Not limited to $14k per year• No reduction of lifetime exclusion ($5.25M)

Lifetime Gifting

© Schiff Hardin LLP. All rights reserved.24

Allows a gift made by one spouse to be treated as made one-half by each spouse for tax purposes.

• Optimizes use of annual exclusions• Gifts that cannot be made by both spouses

can be treated as made by both spouses for gift tax purposes (i.e., a spouse who is a beneficiary of a trust cannot make a gift to that trust)

Gift-Splitting

© Schiff Hardin LLP. All rights reserved.25

A surviving same-sex spouse can now roll over a deceased spouse’s retirement plan on an income-tax-free basis and defer distributions to age 70 ½.

Prior to Windsor, a same-sex surviving spouse had to commence taking distributions in the year following the death of his or her spouse.

Spousal Rollover for Retirement Accounts

© Schiff Hardin LLP. All rights reserved.26

If one spouse passes away and does not utilize all of his or her applicable exclusion amount (currently $5.25M), there exists a Deceased Spouse Unused Exclusion Amount (DSUEA).

The executor can elect to transfer any DSUEA to the surviving spouse, thereby preserving the exclusion to use during his or her life or at his or her own death. This election must be made on an estate tax return.

Portability of DSUEA

© Schiff Hardin LLP. All rights reserved.27

Under the IRC, same-sex spouses are now treated as “related parties” which can have some NEGATIVE tax implications.

• No loss on sales to related parties• Cannot trigger passive losses on sales to

related parties• Chapter 14 of the IRC applies to related

parties• Grantor trust implications

Treated as “Related Party”

© Schiff Hardin LLP. All rights reserved.28

Applicable State Law Married =

Federal Tax Benefits

Place of celebration(Revenue Ruling 2013-17)

All married couples; not RDPs/CUs

Social Security Benefits

Place of domicile; RDPs/CUs also potentially eligible

Married couples living in recognition states; RDPs/CUs living in marriage equivalent states

Private Employment Benefits

Place of celebration All married couples; not RDPs/CUs

Are We Validly Married?

© Schiff Hardin LLP. All rights reserved.29

Applicable State Law Married =

Medicare Place of celebrationAll married couples; not RDPs/CUs

Rights under Family Medical Leave Act

Place of domicileMarried couples living in recognition states

Veteran’s Benefits Place of celebration

All married couples; not RDPs/CUs

Are We Validly Married?

© Schiff Hardin LLP. All rights reserved.30

Are We Validly Married?

Applicable State Law Married =

Immigration Place of celebrationAll married couples; not RDPs/CUs

Military Spousal Benefits

Place of celebrationAll married couples; not RDPs/CUs

Benefits for Civil Federal Employees and Spouses

Place of celebrationAll married couples; not RDPs/CUs

© Schiff Hardin LLP. All rights reserved.31

Same-sex married couples living in Hawaii have most of the federal rights and responsibilities of marriage, including:

• Federal tax benefits• Private employment benefits• Medicare • Immigration rights• Military spousal and veterans benefits• Federal civil employee spousal benefits

Focus on Hawaii

© Schiff Hardin LLP. All rights reserved.32

Same-sex married couples living in Hawaii do not yet have these federal rights :

• Rights under Family Medical Leave Act• Social security survivor benefits

But this could change any day.

Focus on Hawaii

© Schiff Hardin LLP. All rights reserved.33

State Rights/Responsibiliti

es

Federal Rights/Responsibiliti

es

Married

All rights and responsibilities(lawful out of state marriage = civil union)

Most rights and responsibilities

Civil UnionAll rights and responsibilities

Probably no rights or responsibilities

Rights of Married and CU Couples in Hawaii

© Schiff Hardin LLP. All rights reserved.34

In August 2013 and in response to the Windsor case, state legislators presented the Hawaii Marriage Equality Act of 2013.

On September 9th, Governor Abercrombie called for a special legislative session to convene on October 28th to consider the bill.

If the bill passes as proposed, Hawaii would become the 14th state to legalize same-sex marriage, and would begin issuing marriage licenses to same-sex couples as early as November 18, 2013.

Same-Sex Marriage in Hawaii?

© Schiff Hardin LLP. All rights reserved.35

State Rights/Responsibilit

ies

Federal Rights/Responsibilit

ies

Married All rights and responsibilities

All rights and responsibilities

Civil UnionAll rights and responsibilities

Probably no rights or responsibilities

Rights of Married and CU Couples in Hawaii if Hawaii becomes a Recognition

State

© Schiff Hardin LLP. All rights reserved.36

Powers of attorney:

• Advance health care directive• Durable power of attorney for financial

matters

Beneficiary designations on retirement assets and insurance policies

Wills/living trust agreements

Agreements that modify spousal rights

Basic Estate Planning

© Schiff Hardin LLP. All rights reserved.37

Even without the unlimited marital deduction, some couples may want to simplify their plans in light of the $5.25M estate tax exemption.

Consider Modifying Plans

© Schiff Hardin LLP. All rights reserved.38

Ann and Alison have been together for 15 years. They entered into a civil union in 2012. For tax reasons, they are not interested in getting married.

Avoiding double taxation was a prime concern at the time they did their estate planning. They both want to leave assets to Ann’s family after the second death.

Case Study #1—Ann and Alison

© Schiff Hardin LLP. All rights reserved.39

Traditional Planning for Same-Sex Couples

Ann’s LivingTrust

BypassTrust for

Alison

Ann’s nieces and nephews

Alison’s LivingTrust

BypassTrust for

Ann

40

Planning With a Disclaimer Trust

Ann’s LivingTrust

BypassTrust

Outright to Alison

Alison’s LivingTrust

BypassTrust

Outright to Ann

41

Ann’s nieces and nephews

Same-sex married couples should consider:

• Adding QTIP provisions if net worth warrants it and control is an issue

• Eliminating bypass trust and relying on portability

Consider Modifying Plans

© Schiff Hardin LLP. All rights reserved.42

Michael and Stephen have been together for 5 years. They entered into a civil union in Hawaii, married in California and have begun adoption proceedings. Each wants to make sure that his share of the estate ultimately goes to his child if he passes away first.

Case Study #2—Michael and Stephen

© Schiff Hardin LLP. All rights reserved.43

Adding a QTIP Trust

Michael’s LivingTrust

BypassTrust

Child of the relationship

Stephen’s LivingTrust

BypassTrust

44

Remainderto Marital

Trust

Remainderto Marital

Trust

Fast forward—assume now that Michael and Stephen have been together for 35 years. Their child is 30 years old; she does not intend to have children of her own.

Control is less of an issue now; each trusts the other to do the “right thing” if he is the survivor.

Maximizing use of gst exemption is not a concern.

Case Study #2—Michael and Stephen

© Schiff Hardin LLP. All rights reserved.45

Portability Plan

Michael’s LivingTrust

Outright to

Stephen

Stephen’s LivingTrust

Outright to

Michael

46

Child of the marriage

Civil union partners who entered into an agreement and decide to marry should consider updating the agreement.

All couples who marry should consider re-acknowledging any trust instrument that intentionally excludes a spouse.

Update Agreements

© Schiff Hardin LLP. All rights reserved.47

For Validly Married Couples—Regardless of Domicile

New Returns

File returns under new rules; to file as single for 2012 must have done so by 9/15/2013

Returns Filed/Statute of Limitations Open

Amend if would produce more favorable results

Older Returns IRS says can’t amend

Federal Taxes—After RR 2013-17

© Schiff Hardin LLP. All rights reserved.48

For same-sex married couples—regardless of domicile—gift and estate tax returns filed in prior years should be reviewed and possibly amended to claim the gift tax marital deduction for any transfers between spouses.

Forms 706 and 709

© Schiff Hardin LLP. All rights reserved.49

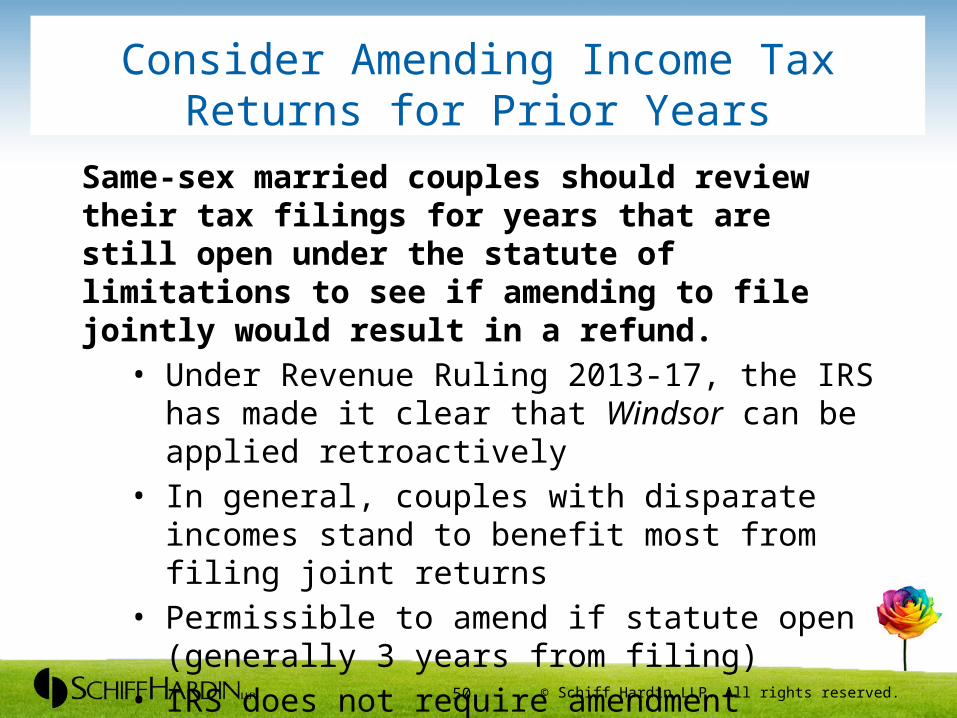

Same-sex married couples should review their tax filings for years that are still open under the statute of limitations to see if amending to file jointly would result in a refund.

• Under Revenue Ruling 2013-17, the IRS has made it clear that Windsor can be applied retroactively

• In general, couples with disparate incomes stand to benefit most from filing joint returns

• Permissible to amend if statute open (generally 3 years from filing)

• IRS does not require amendment

Consider Amending Income Tax Returns for Prior Years

© Schiff Hardin LLP. All rights reserved.50

Participants in welfare benefit plans are eligible to file for a refund of the income tax paid on the value of health coverage provided to a same-sex spouse; employers may also claim a refund for Social Security and Medicare taxes paid.

No stated requirement that taxpayers be consistent between years or returns.

Unclear if amendment for other reasons requires a change in filing status.

Consider Amending Income Tax Returns for Prior Years

© Schiff Hardin LLP. All rights reserved.51

A same-sex spouse of a qualified retirement plan participant will now be the participant’s default beneficiary.

Spouse must consent if another beneficiary is named.

IRS plans to issue further guidance; many unanswered questions.

•Q: How to treat a plan participant with a same-sex spouse who has already designated a non-spouse beneficiary without consent? Is notice required?

Retirement Plan Issues

© Schiff Hardin LLP. All rights reserved.52

U.S. v. Windsor = major step towards full marriage equality for same-sex couples.

Unanswered questions remain; the nation is a patchwork of inconsistent laws and policies on the state level.

It is important to be especially vigilant about issues of domicile and to pay attention to changes that are made, both on the state and federal level.

In the areas of estate and tax planning, maximize flexibility and plan for the future.

In Closing

© Schiff Hardin LLP. All rights reserved.53