Embed Size (px)

Citation preview

IN THE SUPREME COURT OF OHIO

E. J. Zeller, Inc., et al.

Plaintiffs-Appellees

Case No. 14-2174

On Appeal from the Defiance CountyCourt of Appeals, Third Appellate District

vs.

Auto Owners Insurance Company, et al Court of Appeal Case No. 04-14-004

Defendants-Appellants TC Case No. 12 CV 42075

MEMORANDUM OF PLAINTIFF-APPELLEE E. J. ZELLER INC. AND PLAINTIFF-APPELLEE AND CROSS-APPELLANT CITY RENTALS , INC. IN RESPONSE TO

DEFENDANT-APPELLANTS' MEMORANDUM IN SUPPORT OF JURISDICTION

Marc F. Warncke (0043133)Clemens, Korhn, Liming & VVarncke, LtdBlock Six Business Center419 Fifth Street, Suite 2000P.O. Box 787Defiance, Ohio 43512Phone: 419-782-6055Fax: 419-782-3227Email: mfwlaw a^defnet.com

Attorneys for Plaintiff-AppelleeE. JZeller, Inc. and Plaintiff-Appelleeand Cross-Appellant City Rentals, Inc.

1 ll -^

JAN ^ ^^^lo'

CLERK OF COURTSUPREME COURT OF OHIO

Gordon D. Arnold (0012195)Counsel of RecordPatrick J. Janis (0012194)Freund, Freeze & ArnoldFifth Third CenterI South Main Street, Suite 1800Dayton, Ohio 45402-2017Phone: 937-222-2424Fax: 937-222-5369Email: garnol.d(a^ffdlaw.comEmail: pjanis c^ffalaw.com

Attorneys for Defendants-Appellants,Auto Owners Insurance Company andOwners Insurance Company

/'- ^•_- .. 1 c .

} t f

# y:.€ . ... . . sr >.. _. ..... ^ .. _ , .. .. ^.. ' ...,.

TABLE OF CONT'EN'I'S

TABLE OF CONTENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

TABLE OF AUTHORITIES ................ ..................................................

STATEMENT OF WHY THE CASE DOES NOT INVOLVE QUESTIONSOR GREAT OR GENERAL PUBLIC fNTEREST ....................................... 1

STATEMENT OF THE CASE ............................................................... 2

STATEMENT OF FACTS .................................................................... 4

RESPONSE TO DEFENDANTS' PROPOSITION OF LAW . . . . .. . . . . .. . .. . . . . . . . . . . .. 8

PLAINTIFF-APPELLEE AND CROSS-APPELLANT CITY RENTALSPROPOSITION OF LAW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

CONCLUSION ................................................................................. 14

CERTIFICATE OF SERVICE ............ ........................... ...... ................... 15

i

TABLE OF AUTHORIT'IES

CASES:

A.B.S Clothing Collection, Inc. v. Home7nsurance Company (1995)34 Cal.App.4tn 1470 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 11

Andersen v. Highland House Co. (2001) 93 Ohio St. 3d 547 ........................... 10

Cincinnati Ins. Co. v. Hopkins Sporting Goods (1994) 522 NW.2d 837 .............. 12

City ofMiami Springs v. Travelers Indemnity Group (1978)365 So.2d. 1030 (Fla.App. 3 Dist.) ....................................................... 12

Columbiana Co. Board of Commissioners v. Nationwide Insurance Co.,130 Ohio App.3d 8 (1998) .................................................................. 9, 10

Glaser v. Hartford Casualty Ins. Co. (2005) 364 F.Supp.2d 529 . . . . .. .. .. . . .. . . . . . . .. 12

Globe Indemnity Co. v. Wolcott & Lincoln, Inc. (1945) 152 F.2d. 545 ................ 12

In re: Endeco 718 F.2d. 879 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . 12, 13

Karen Kane, Inc. v. Reliance Insurance Co. (1999) 202 F.2d 1180 (Ninth Circuit)34 Cal.App.4th at 1479, 41 Cal.Rptr.2d 166 .............................................. 12

King v. Nationwide Insurance Co., 35 Ohio St.3d 208 (1988) ......................... 10

Lager v. Miller-Gonzalez, 120 Ohio St.3d 47 (2008) .................................... 9

Penalosa Co-op Exchange v. Faymland Mut. Ins. Co., supra, 789 P.2d at p. 1200 ... 11, 12

Prairie Land Coop v. MilleN's Mut. Ins. Ass'n. oflll., Case No. 840 C2-91-1503(1992WL20705) (Minn App. Feb. 11, 1992) . ... . .. ..... . .. . . . . .. . .. .. . . .. . .. .. . . . . .. .. ... 12

Robben & Sons Heating Inc. v. Mid-Century InsuNanceCompany,Case No. 0101-01129 (Oregon Ct.App. Multnomah Co., August 13, 2003) .......... 12

Spartan Iron & Metal Coyporation v. Liberty Insurance Corp. (2001) 6 Fed.Appx.176 (2001 WL 301111) ....................................................................... 12

Weicker v. A%Iotorist's Mutual Ins. Co. (1998) 82 Ohio St.3d, 182 ...................... 9

White Dairy Company v. St. Paul Fire and Marine Insurance Company (1963)222 F. Supp.1014 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 12

I I

MISCELLANEOUS:

57 Ohio Jur.3d 410, Section 326 ........................... ............ ...................... 10

STATEMENT OF WHY THE CASE DOES NOT INVOLVE QUES'I'IONS OF GREATOR GENERAL PUBLIC INTEREST

The instant case presents no issues of great or general public interest which require the

intervention of this honorable Court. Although the precise issues of the case have not been

previously litigated in Ohio, the decision of the Third District Court of Appeals crossed no

threshold, broke no barriers, and did not purport to unveil any new or expansive legal theories.

Rather, the Court simply applied long settled principles of insurance law and contract

interpretation to the specific language of two insurance policies which are of little concern to

anyone outside the immediate parties to this lawsuit. With regard to the primary issue of the

case, (i.e. whether the policies afford the insureds with one or two yearly policy limits of

coverage), the Appeals Court diligently reviewed the contractual language, and used

longstanding rules of construction to reach the correct conclusion -- that the specific language

employed in those policies did not "clearly and unambiguously" entitle the Defendant-insurers to

the restrictive coverage decision they sought.

Although Plaintiff City Rentals has filed a Cross-Appeal in this matter, both Plaintiffs

believe that the Third District reached the correct decision on the primary issue and are willing to

accept the Court of Appeals decision as it stands. From a purely economic standpoint, it makes

little sense for either party to continue this litigation. While the defense expresses some concern

about the precedent established by the Third District's decision, and the need for a "clear

directive" as to the type of coverage these policies provide, the practical reality is that the

Defendant-Insurers can easily, and almost assuredly will amend the language of their future

policies if they believe the Third District's precedent (or any future decision by this Court) puts

them in a position of having to extend coverage which they do not wish to offer.

1

Should the Court be inclined to accept jurisdiction, however, equity demands that the

Court also review the propriety of the Court of Appeals decision on the "prior loss' issue which

is unique to the City Rentals' claim only. It would be filndamentally unfair for the Court to

review those aspects of the decision which were resolved in the Plaintiffs favor without also

reviewing the Court of Appeals decision on this secondary issue which was resolved in favor of

the Defendant.

STATEMENT OF TIHE CASE

This appeal involves an insurer's attempt to restrictively construe the language of an

"employee dishonesty" insurance policy to minimize the coverage available when an insured

sustains a large loss over several policy periods.

On August 8, 2008, Plaintiffs City Rentals, Inc. ("City Rentals") and E. J. Zeller, Inc.

("Zeller") discovered that a shared bookkeeper had embezzled a large amount of money from

both companies over several years. Throughout the relevant time frame, City Rentals was

continuously covered Lulder a series of insurance contracts written by Defendant Auto-Owners

Insurance Co. ("Auto-C7wners"), while Zeller was continuously covered under a series of polices

written by Defendant Owners Insurance Co. ("Owners"), which is an affiliate of Auto-Owners.

Each policy included coverage for losses due to "employee dishonesty" occurring during that

policy's term, up to a stated policy limit. At the end of each policy year, a new premium was

paid and a new policy issued.

Upon discovering the thefts, each Plaintiff submitted a timely claim to its respective

insurer. Auto-Owners tendered payment to City Rentals of $15,000, based upon what Auto-

Owners interpreted to be one year's coverage limit for employee thefts under its policy.

Similarly, Defendant Owners eventually paid $60,000 to Zeller, which was equal to one year's

2

coverage limit under the Zeller policies. Both insurers deny any further obligation to their

insureds.

On September 13, 2012, both Plaintiffs filed a Declaratory Judgment action in Defiance

County Common Pleas Court. Both Plaintiffs asserted that, because each separate policy

required a separate premium each year, a separateyear's policy limit should. be available under

that policy for employee thefts which took place during that policy year. Further, in the case of

City Rentals, Plaintiffs asserted that the applicable policy limit should be $60,000, not $15,000,

based on ambiguities in the "prior loss" provision of the policy in question. (Under the facts of

the case, the "prior loss" provision applies to the City Rentals claim, bu.t not the Zeller claim.)

Both Plaintiffs argued that the policies at issue were ambiguous and susceptible to more than one

reasonable interpretation, and that the Plaintiffs were therefore entitled. to have the policies

construed in their favor.

The original Common Pleas case was dismissed and later refiled, and both parties

eventually moved for Summary Judgment. On December 30, 2013, the Common Pleas Court

issued an opinion granting Summary Judgment in favor of both Defendants. Without any

specific discussion of the particular language employed in these policies, the Common Pleas

Court ruled that the policies "clearly and unambiguously" limited each Plaintiff to a single year's

coverage as the Defendant-insurer's claimed. Both Plaintiffs appealed.

The Court of Appeals considered all of the provisions cited in detail, and found nothing

in any of them which "clearly" limited coverage in the manner the Defendants claimed. As such,

the Court of Appeals agreed with the Plaintiffs and held that each policy provided a separate

policy limit of coverage for that policy's period of coverage. However, the Court further held

that each policy's coverage was limited by a "discovery of loss" requirement, which prohibited

3

the insureds from recovering for older losses that were not discovered within one year of the date

the policy terminated. Finally, the Court rejected the Plaintiffs argument that the "prior loss"

provision made it ambiguous which limit applied in the City Rentals case.

Defendants have now appealed the Court of Appeals decision, and City Rentals has filed

a cross-appeal of the Appellate Court's ruling on the "prior loss" issue. Because the "prior loss"

provision does not affect the other Plaintiff, Zeller did not cross-appeal the Appellate decision..

STATEMENT OF FACTS

Both of the Plaintiffs are closely held corporations owned by the Zeller family of

Defiance, Ohio. Beginning in 2003, Plaintiff E. J. Zeller, Inc. employed Robin Bauer as its

bookkeeper. In 2006, Bauer's job duties were expanded to include bookkeeping responsibilities

for City Rentals as well.

On August 8, 2008, the Plaintiffs discovered that Bauer had been stealing money from both

corporations for several years, and terminated her employment. It was eventually determined that

Bauer had been stealing from Zeller each year since 2003, and from City Rentals each year since

2006. All told, she had embezzled several hundred thousand dollars from the two companies.

Knowing they had purchased insurance coverage against such acts, each Plaintiff

provided timely notification of the claim to its respective insurer on August 11, 2008. In the case

of Zeller, each successive policy of insurance was issued for a period of one (1) year, beginning

on August 12 of the issuing year, until August 12 of the following year (emphasis added).

Throughout the relevant time frame, each Zeller policy carried a total yearly coverage limit of

$60,000 -- a basic "employee dishonesty" coverage of $10,000, plus an additional $50,000 of

coverage provided through a "Commercial Crime Endorsement" which Zeller purchased every

year.

4

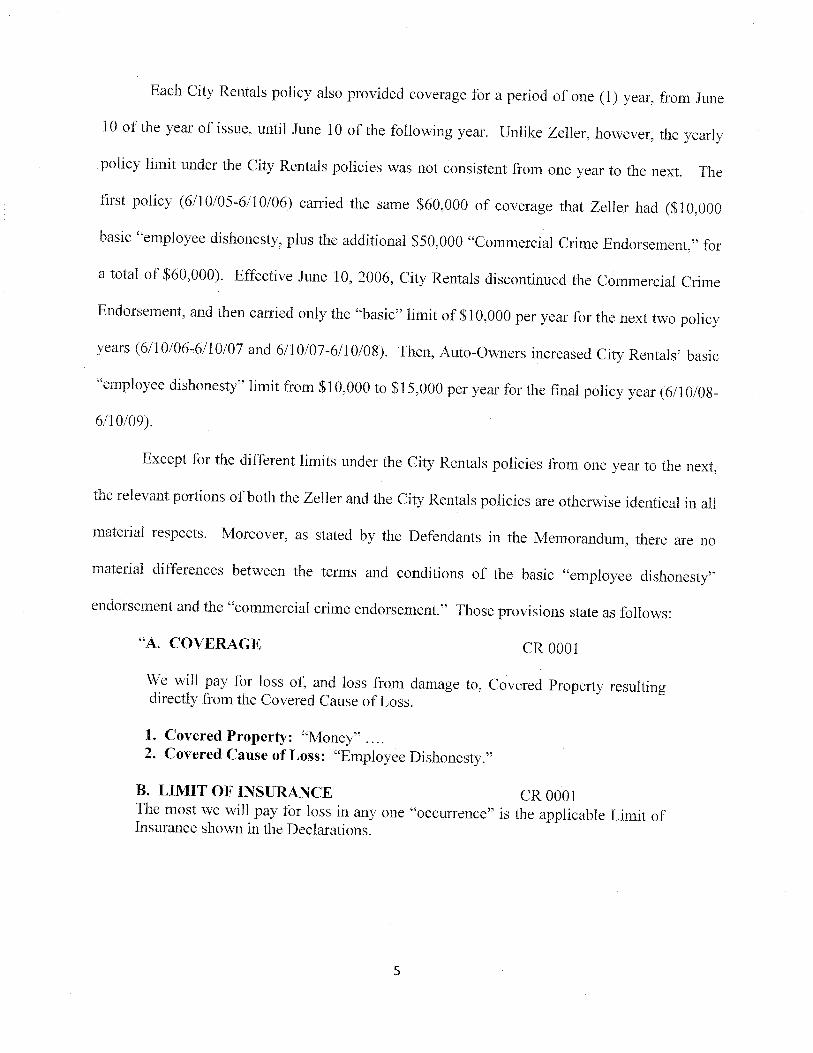

Each City Rentals policy also provided coverage for a period of one (1) year, from June

10 of the year of issue, until June 10 of the following year. Unlike Zeller, however, the yearly

policy limit under the City Rentals policies was not consistent from one year to the next. The

first policy (6/10/05-6/10/06) carried the saine $60,000 of coverage that Zeller had ($10,000

basic "employee dishonesty, plus the additional $50,000 "Commercial Crime Endorsement," for

a total of $60,000). Effective June 10, 2006, City Rentals discontinued the Commercial Crime

Endorsement, and then carried only the "basic" limit of $10,000 per year for the next two policy

years(6,10106-6/10/07 and 6/10/07-6/10/08). Then, Auto-Owners increased City Rentals' basic

"employee dishonesty" limit from $1.0,000 to $15,000 per year for the final policy year (6/10/08-

6/10/09).

Except for the different limits under the City Rentals policies from one year to the next,

the relevant portions of both the Zeller and the City Rentals policies are otherwise identical in all

material respects. Moreover, as stated by the Defendants in the Memorandum, there are no

material differences between the terms and conditions of the basic "employee dishonesty"

endorsement and the "commercial crime endorsement." Those provisions state as follows:

"A. COVERAGE CR 0001

We will pay for loss of, and loss from damage to, Covered Property resultingdirectly from the Covered Cause of Loss.

1. Covered Property: "Money" ....2. Covered Cause of Loss: "Employee Dishonesty."

B. LIMIT OF INSURANCE CR 0001The most we will pay for loss in any one "occurrence" is the applicable Limit ofInsurance shown in the Declarations.

5

D. ADDITIONAL ... DEFINITIONS CR 0001

3. Additional Definitionsb. "Occurrence" means all loss caused by, or involving one or more"employees," whether the result of a single act or series of acts.

D. GENERAL CONDITIONS CR 1000 (6-95)

4. Discovery Period for Loss: We will pay only for covered loss discovered nolater than one year from the end of the policy period.

11. Loss Covered Under This Insurance and Prior Insurance Issued by Usor Any Affiliate: CR 1000 (6-95)

If any loss is covered:

a. Partly by this insurance; and

b. Partly by any prior cancelled or terminated insurance that we or anyaffiliate had issued to you or any predecessor in interest;

the most we will pay is the larger of the amount recoverable under thisinsurance or the prior insurance.

12. Non-Cumulation of Limits of Insurance: Regardless of the number ofyears that insurance remains in force or the number of premiums paid, no Limitof Insurance cumulates from year to year or period to period.

15. Policy Period

a. The Policy Period is show in the Declarations.

CR 1000 (6-95)

b. Subject to the Loss Sustained During Prior Insurance condition, we will payonly for loss that you sustain through acts committed or events occurring duringthe Policy Period.

(Emphasis added). The Employee Dishonesty Endorsement contained the sameexact provisions as set forth above, except for the following:

6

E. CENERAI, CONDITIONS

9. Non-Cumulation of Limits of Insurance: Regardless of the number ofyears this insurance remains in force or the number of premiums paid, no Limitof Insurancecumulates from year to year or period to period.(Emphasisadded)."

(As Defendants state, the only difference in the two non-cumulation conditionsis the article "that" in the Crime General Provisions, and the article "this" in theEmployee Dishonesty Endorsement, shown by the emphasis in the abovequotes.)

As stated, the trial court granted summary judgment in favor of the Defendant-Insurers.

Its opinion did not discuss the particular language employed in the policies at issue, but, simply

stated in conclusory fashion that they "were not capable of being misunderstood" and that the

policies "clearly and unainbiguously" limited each Plaintiff to a single year's policy limit of

coverage. Both Plaintiffs appealed.

The Court of Appeals devoted considerable discussion to each of the provisions cited by

the parties, and found nothing in them that would "clearly" restrict coverage in the manner

asserted by the Defendants. As such, the Court of Appeals ruled that each Plaintiff can make a

separate claim under each policy for any losses which were (1) sustained during that policy's

period of coverage, and (2) were discovered not more than one year after the date that policy

terminated. As applied, this means that Zeller has one policy limit of coverage available for

losses sustained under the (8/12/06-8/12l07 policy (which was still in its "discovery" period),

and also a second policy limit of coverage available for losses sustained under the (8/12,/07-

8I12/08) policy, which was the "current" policy in effect when the thefts were discovered.

Similarly, City Rentals has one policy limit of coverage available for losses sustained

under the 6/10/07-6/10/08) policy (which was in its "discovery" period), and a second policy

limit of coverage available for losses sustained under the (6/10/08-6/10/09) policy, which was

7

the "current" policy then in force. The Court of Appeals furtlier held that any older clairns of

either Plaintiff were barred by the policies' one year discovery rule.

Finally, the Court rejected City Rentals' argument that the "prior loss; provision made it

ambiguous which policy limit applied to the City Rentals claims, and affirmed the trial court's

decision on that issue.

RESPONSE TO DEFENDANTS' PROPOSITION OF LAW:

The Proposition of Law set forth by the Defendant-Insurers in their Memorandum is

flawed in at least two respects:

i. The policy provisions at issue in this case are not "clear andunambiguous" as the Defendants' maintain; and

ii. The Defendant's application of their Proposition of Law is fundamentallyinconsistent with the underlying concept of purchasing insurance to coveracts taking place within a stated time period, and leads to absurd results.

Prior to the instant case, there were no reported appellate decisions in Ohio construing the

particular policy provisions at issue in this litigation. Consequently, both parties relied heavily on

case law from other jurisdictions involving similar policy language in the context of multi-year

thefts. It was, and remains the position of the Plaintiffs that the relevant provisions of the

Defendants' policies, at a minimum, are ambiguous and susceptible to more than one reasonable

interpretation in the factual context of the instant case. Indeed, the procedural history of the

present case confirnls this fact. The Defiance County Common Pleas Court concluded that the

policy provisions cited by the Defendants "were not capable of being misunderstood" and found

them to be "clear and unambiguous" in favor of the Defendants. The Third District Court of

Appeals reached the opposite conclusion, and found that those same policy provisions contained

nothing that would "clearly" entitle the Defendants to the limitation of coverage they seek.

8

Outside Ohio, courts in at least eleven (11) other jurisdictions have considered the same,

or similar provisions and also found them to be vague and ambiguous in the factual setting

involving a series of thefts impacting multiple policy periods. In response, Defendants point to

decisions from a comparable number of other states which reach the opposite conclusion, and

dismissively state that that those Courts which did not find in the insurers' favor (including the

Third District) were simply "wrong."

All of the conflicting decisions were decided by experienced, highly capable and

dedicated trial and appellate Judges, at the height of their profession, and all of the cases cited

remain the law of the land in their respective jurisdictions. Contrary to the Defendants'

argurnent, the lack of a clear consensus is not the result of Judges who do not know how to read

aninsurance policy or are misapplying the law -- it is the result of imprecise Zanguage that does

not fit well with the current factual scenario and can reasonably be read in a variety of ways.

The Defendants' suinmary of Ohio law regarding the interpretation of insurance contracts

makes only passing reference to what Plaintiffs believe to be the single most important rule of

construction in the present case. Ohio courts have long recognized that insurance contracts are

contracts of adhesion, written by the insurers, with the insured having little ar no input into the

language chosen. As such, it is settled law that an insurance contract which contains terms

which are ambiguous, uncertain, or vague must be construed liberally in favor of the insured.

ff'eicker v. Motor°ist's Mutual Ins. Co. (1998) 82 Ohio St.3d 182. Contract ternis are ambiguous

when they are capable of more than one reasonable interpretation. Lager v. Miller-Gonzalez,

(2008) 120 Ohio St.3d 47. When policy language is determined to be doubtful,uncertain or

ambiguous, the language must be construed strictly against the insurer and liberally in favor of

the insured party. Columbiana Co. Board of Commissioners v. 1Vationwide Insurance Co. (1998)

9

130 Ohio.App.3d 8; King v. Nationwide Insur~ance Co., (1988) 35 Ohio St.3d 208. "Stated more

fully, when the provisions of an insurance policy are reasonably susceptible to more than one

interpretation, any reasonable construction which results in coverage for the insured must be

adopted by the trial court." 57 Ohio Jur.3d 410, Section 326. Finally, as this Court cogently

stated in Andersen v. Highland House Co. (2001) 93 Ohio St.3d 547:

"[I]n order to defeat coverage, the insurer must establish not merely that thepolicy is capable of the construction he favors, but rather that such aninterpretation is the only one that can fairly be placed on the language inquestion." (Emphasis added) (citing Home Indemnity Ins. Co. v. Plymoutli (1945)146 Ohio St. 96).

Reduced to its fundamental elements, the contractual agreement between the parties was

that the Defendant-insurers, in exchange for a premium, would provide their insureds with

coverage, up to the applicable policy limit, for employee thefts which took place during that

policy's year of coverage. When the first policy term expired, the insYired was required to pay a

new premium for coverage up to the applicable policy limit for employee thefts which took place

during the new -policy's term of coverage. As the "policy period" definition states:

"Subject to the Loss Sustained During Prior Insurance Provision, we will pay onlyfor loss that you sustain through acts committed or events occurrin during thePolicy Period." (Emphasis added).

Notwithstanding this definition, the Defendant-insurers insist that the intent of the

"occurrence" definition, the "prior loss" provision, and the "non-cumulation" provision is to

"clearly and unambiguously" prohibit the insured from making a separate claim under former

policies if a pattern of thefts is discovered stretching across more than one policy period.

Regardless of whether these provisions are characterized as "conditions," "exclusions," or

"definitions," for the Defendant-Insurers to be correct, they must show that their preferred

application of those provisions is the only way they can plausibly be read.

10

Courts from every corner of the nation have struggled to apply identical or comparable

language in the factual context of the present case, and many times found such provisions to be

individually and collectively ambiguous, and subject to multiple interpretations.

Notwithstanding the Defendant-Insurers' assertion, there is no "clear consensus" of case law

favoring the insurer's preferred interpretation, which the Court of Appeals failed to recognize or

follow. To the contrary, courts have struggled. and continue to struggle with the inherent

problems that arise when insurers try to force the "square peg" of their present contractual

language into the "round hole" created by the facts of the instant case. Among the ambiguities

are the following:

1. The definition of "occurrence" is inherently vague, as it could refer to any "seriesof acts" committed d.uring anLv time period (as defendants claim), or it could justas reasonably be construed to refer to any "series of acts" during the coverageperiod of the current policy.

2. The "prior loss" provision is likewise vague and ambiguous. Is its purpose to barcoverage under any prior policy as the defendants' claim, or is it merely to definewhich limit applies for claims when the insured suffers a lossin one policy year,as a result of a series of acts which took place in more than one policy year, andthe coverage limits are not the same from one year to the next?

3. The "non-cumulation" provision is also ambiguous and susceptible to more thanone reasonable interpretation. Is it intended to limit the insured to a single claim,subject to the current policy limit, as Defendant's claim, or is it intended toprevent the insured from carrying forward unused limits from earlier periods, andaggregating them to obtain coverage for a current loss in excess of the currentyear's policy limit?

Although space limitations prevent a detailed discussion of each case at this juncture,

other courts have found the same or similar language fraught with these and other ambiguities,

and allowed similarly-situated insureds to make separate claims under separate policy years in

the following cases: A.-8.S. Clothing Collection, Inc v. Home InsuNance Company (1995) 34 Cal

App.4th 1470; Penalosa Cooperative Exchange v. Farmland Mutual Insurance Co. (1990) 789

11

P.2d 1196; In re: Endeco (1983) 718 F.2d 879; White Dairy Company v. St. Paul Fire and

Marine Insurance Coynpany (1963) 222 F.Supp. 1014, City of Miami Springs v. Travelers

Indemnity Group (1978) 365 So.2d 1030 (Fla.App. 3 Dist); Spartan Metal & Iron Corporation v.

Liberty Insurance Corp. (2001) 6 Fed.Appx. 176 (2001 WL 301111); Glaser v. HaNtford

Casualty Ins. Co. (2005) 364 F.Supp.2d 529; Cincinnati Ins. Co. v. Hopkins Sporting Gooc'^s

(1994) 522 NW.2d 837; Globe Indemnity Co. v. Wolcott & Lincoln, Inc., (1945) 152 F.2d 545;

PNaiNie Land Coop v. Miller's Mut. Ins Ass'n of Ill., Case No. 840 C2-91-1503 (1992WL20705)

(P3Iitm.App. t'eb. 11 1992); Robben & Sons Heating Inc. v. Mid-CentuNy Insurance Company,

Case No. 0101-01129 (Oregon Ct.App., Multnomah Co., Aug. 13 2003); Karen Kane, Inc. v.

Reliance Insurance Co. (1999) 202 F.2d 1180 (Ninth Circuit), 34 Cal.App.4rh at 1479, 41

Cal.Rptr.2d 166.

In addition to the ambiguous terminology, Court have also struggled with the absurd

results that would follow if the Defendants-Insurers position were to be accepted. Under the

Defendants' theory, the insured is required to pay a separate premium for the first policy year,

and a separate premium each for each year that the policy is renewed, yet if same employee

causes the insured to sustain a loss in each of those years, the insurer would only provide a s^

year's policy limit of coverage. As several courts have observed, this obviously begs the

question: What did the insured get for their premium in the subsequent years if not another

policy limit of coverage? See Glaser; Penalosa; Robben; 11f1iami Springs; White Dair°y, all

supra. Moreover, if adopted in Ohio, the Defendant-Insurers position would actually allow an

insured who changes insurance carriers from one year to the next to obtain a separate policy

limit of coverage for each year in which theft losses are sustained, while an insured in the same

position who renews his coverage with the same carrier would receive only one year of coverage.

12

Surely this could not have been the intent of the parties when these contracts were written and

renewed. See In re Endeco, supra.

PLAINTIFF-APPELLEE AND CROSS-APPELLANT CITY RENTALS PROPOSITIONOF LAW:

When an Employee Dishonesty Insurance policy defines a series of acts committed acrossmultiple policy periods as a single "occurrence," such definition must be applied uniformlyacross the policy for all purposes, including the interpretation of a "prior loss" provisiondefining which policy's coverage limit applies to the loss. In determining the applicablecoverage limit, the Court must give the insured the benefit of any reasonable or plausibleconstruction of the policy, and allow the insured to recover the largest policy limit.

As stated, the coverage limits of the City Rentals policies were not consistent from one

year to the next. `Vhen Bauer first began stealing from City Rentals in 2006, the (6/10/05-

6/10/06) policy was in place with a coverage limit of $60,000. Then City Rentals discontinued

the "Commercial Crime Endorsement," and had limits of $10,000 for the next policies. The fmal

City Rentals policy, in effect when Bauer's thefts were discovered, had a limit of $15,000.

As written, the City Rentals policies attempt to define all of Bauer's acts from January

2006 through August 2008 as a single "Occurrence." Because these acts took place during four

different policy years, reference must be made to the "prior loss" provision to determine which

limit applies:

"Loss Covered Under This Insurance and Prior Insurance Issued by Us orAny Affiliate: If any loss is covered:

(A) Partly by this insurance; and

(B) Partly by any prior or cancelled or terminated insurance that we or anyaffiliate had issued to you or any predecessor in interest;the most we will pay is the larger of the amount recoverable under thisinsurance or the prior insurance." (Emphasis added).

13

Plaintiff City Rentals maintains that if the policy aggregates Bauer's entire four (policy)

years of "acts" into a single "Occurrence," then the Court should look at the same four years'

policy limits when it determines which limit applies to that "Occurrence." Defendants, however,

argue that the one year "discovery requirement" means that only the final two policies are

relevant for this comparison. However, nowhere does the "prior loss" provision state that the

availability of the higher limit is "subject to" the one year rule -- although the Defendant-Insurers

who wrote the policy could have easily provided so if that was their intent. Under City Rentals'

view, if all of Bauer's acts constitute a single "Occurrence," then that "Occurrence" was timely

discovered and reported, and the highest of the potential limits -- $60,000 -- should apply. At the

very least, City Rentals believes that its interpretation is "one reasonable way" the policy could

be read.

CONCLIISION

The Court of Appeals correctly applied the law and reached the proper result on the

primary issue of the case. Although the Court of Appeals did not accept City Rentals' position

on the "prior loss" issue, both Plaintiffs are satisfied with the Court of Appeals decision and are

willing to accept the result. From an economic standpoint, it makes little sense for either party to

prolong this litigationa Existing rules of contract interpretation are more than sufficient to

resolve the issues presented by the instant case, and those rules were correctly employed by the

Court of Appeals. Further judicial review is not warranted, and the Court should therefore

decline jurisdiction.

14

However, if this honorable Court does choose to accept jurisdiction, the interest of justice

require it to review the entire case, including those aspects on which the Defendants were the

prevailing parties.

Respectfully submitJ

, ; ... ^.: . ....v..

Marc F. Warncke (0042133)Clemens, Korhn, Liming & Warncke, Ltd.419 Fifth St., Suite 2000Defiance, Ohio 43512Ph: (419)782-6055Fax: (419)782-3227mfwlawna,defriet.comAttorneys for Plaintiff-Appellee,E. J. Zeller, Inc., and Plaintiff-Appellee andCross-Appellant, City Rentals, Inc.

CERTIFICATE OF SERVICE

I hereby certify that a copy of the foregoing Memorandum of Plaintiff-Appellee E. J.

Zeller, Inc. and Plaintiff-Appellee and Cross-Appellant City Rentals, Inc. in Response to

Defendants-Appellants' Memorandum in Support of Jurisdiction was served upon Gordon D.

Arnold and Patrick J. Janis, Attorneys for Defendants-Appellants, Fifth Third Center, 1 South

Main Street, Suite 1800, Dayton, Ohio, 45402-2017, by placing the same in ordinary U.S. mail

this 12`t' day of January, 2015.

n_•. / .j.f

-.. 44,F'f ^ 4

^` >^3 ,r^j ^ .

Marc F. Warncke (0042133) ofClemens, Korhn, Liming & Warncke, Ltd.Attorneys for Plaintiff-Appellee,E. J. Zeller, Inc., and Plaintiff-Appellee andCross-Appellant, City Rentals, Inc.

15