Embed Size (px)

Citation preview

25th Annual

Tuesday & Wednesday, January 26‐27, 2016 Hya Regency Columbus, Columbus, Ohio

Oh

io T

ax

Workshop T

Ohio Sales & Use Tax: National Issues & Trends

Tuesday, January 26 4:15 p.m. to 5:15 p.m.

Biographical Information

Daniel E. Ernst, Manager Transaction Taxes American Electric Power

301 Cleveland Ave SW, Canton, OH 44702 [email protected] 330-438-7063

Dan is the Transaction Taxes Manager for American Electric Power (AEP), in Canton, Ohio. Headquartered in Columbus, Ohio, AEP is one of the largest electric utilities in the United States, serving nearly 5.4 million customers in 11 states. Dan has been with AEP for more than 33 years and has held various positions in tax, accounting, and information technology. Dan is responsible for state, local, and federal transaction taxes, including all areas of tax compliance, audits, planning, and research. Dan also is an adjunct professor at Walsh University in North Canton, Ohio where he teaches accounting and finance courses. Dan earned a BA in Accounting and an MBA from Walsh University. He is a past president of the Utility Excise Tax Association of Texas (UETAT), past member of the Sales Tax Symposia committee, and currently serves as treasurer for two non-profit corporations.

Sean Evans, Director, Tax Advisory Services DuCharme, McMillen & Associates, Inc.

7304 West 130th Street, Suite 110 Overland Park, KS 66213 (800) 309-2110, ext. 2145 [email protected]

Sean provides customized sales/use tax training courses in all areas of transaction tax. He also provides a variety of tax advisory services including sales/use tax process reviews, nexus studies, and voluntary disclosures. Additionally, Sean develops tax matrices designed to support clients’ business process requirements. He also serves as project manager for tax software implementations and business process reviews. Sean has nearly 20 years of sales/use tax experience. Prior to joining DMA, Sean was a Senior Tax Consultant for a national tax firm, where he conducted both public and on-site training courses on sales/use tax and federal tax reporting. In his private practice, Sean performed and directed nationwide managed audits, voluntary disclosures, transactional planning, nexus studies, matrix development, system surveys, procedure development, and corporate sales tax training.

SALES AND USE TAX: NATIONAL ISSUES AND

TRENDS

Sean EvansDMADirector, Tax Advisory

Dan ErnstAmerican Electric Power ServiceManager‐Transaction Tax

January 26, 2016Ohio Tax ConferenceColumbus, Ohio

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.2

STATE BUSINESS TAX CLIMATE

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.3

AVERAGE SALES TAX RATES

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.4

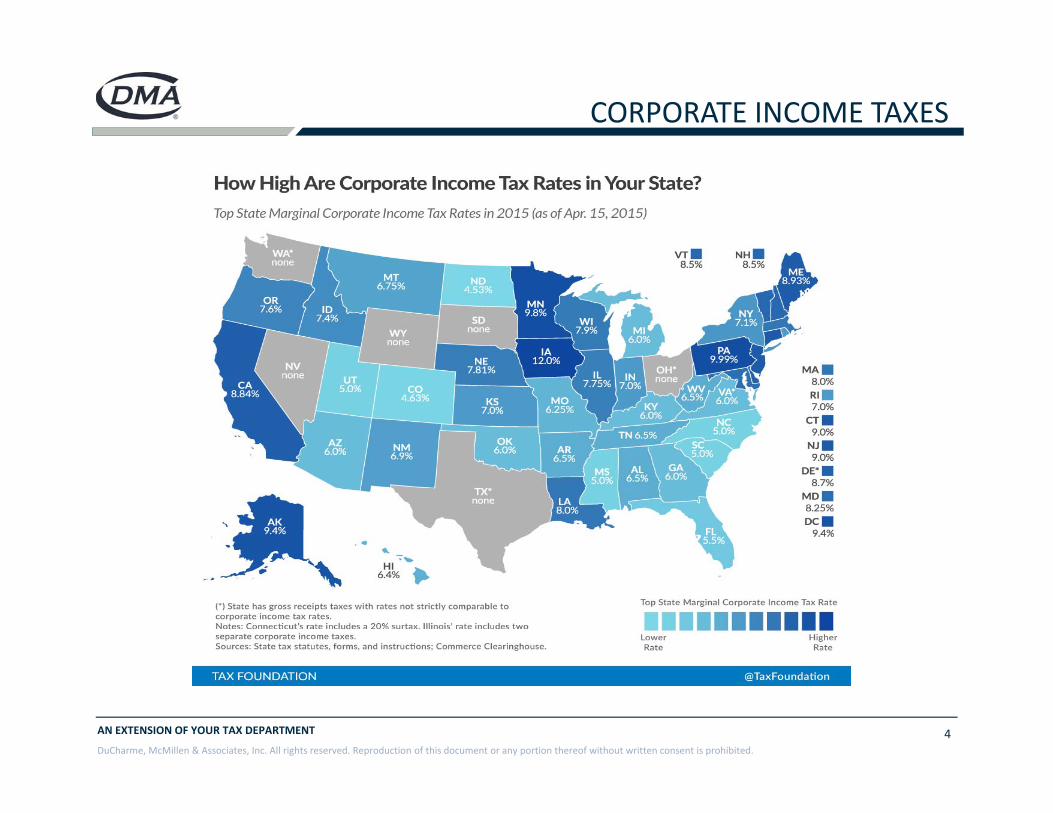

CORPORATE INCOME TAXES

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.5

GROSS RECEIPTS TAXES

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.6

Statutory Credits/Incentives – also known as “as‐of‐right” Generally provided once predefined eligibility requirements have

been met Form of benefit is generally a credit taken on a tax return Business case is usually not required

Quasi‐Statutory Credits/Incentives – discretionary in nature Authorized by government legislation but approval is not guaranteed Require pre‐approval by government officials before filing for any

benefits Generally need to make an argument for your project

Discretionary Incentives Negotiated and customized benefit Most often used in site selection to chose one site over another Majority are non‐tax related

CREDITS AND INCENTIVES ‐ TYPES

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.7

STATE TAX INCENTIVES

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.8

Continuation of targeted Incentives Continuation of expansion of tax bases

Services

Crack down on false refund claims Cross‐training of auditor to cover multiple taxes Local governments putting more enforcement on business

licenses Movement to nationwide tax base through the

consideration of Gross Receipts Taxes Consideration of repealing personal property tax in various

states

WHAT IS ON THE HORIZON

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.9

Services as a Tax Basis Some States are trying to increase base by adding tax to various

services. Others have taxed services, then the taxpayers protested which

caused repeal (i.e., Minnesota). Targeted areas for States

• SaaS, Paas, and IaaS• Professional Services• Consulting• Automatic Data Processing• Help Supply Services• Computer Services

TAXATION OF SERVICES

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.10

States with Personal Property Tax

CT11/01/16

AK*1/15/16

HI

ME4/16/16

RI1/31/16

VT4/15/16

NH

NY

PA

NJ

MD4/15/16

DE

VA*1/31/16

WV

NC1/31/16SC*

4/30/16GA4/1/16

IL OHIN

5/15/16

MI2/1/16

WI3/1/16

KY5/15/16

TN 3/1/16

AL12/31/16MS

4/1/16LA3/1/16

TX4/15/16

OK3/15/16

MO3/1/16

KS3/15/16

IA

MN

ND

SD

NE5/1/16

NM

AZ4/1/16

CO4/15/16

UT1/31/16

WY3/1/16

MT3/15/16

WA4/30/16

ID3/15/16

NV7/31/16

OR3/15/16

MA3/1/16

OVERVIEW

CA4/1/16

AR5/31/16

Key

DC7/31/16

FL 4/1/16

States without Personal Property Tax

NM2/28/16

2016 Personal Property Tax Rendition Deadlines

WV8/1/16

* Dates can vary

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.11

Arizona‐ POSTPONED AGAIN ( Except for Sedona ,AZ.)Beginning January 1, 2016, ADOR will become the single point of administration and collection of State, county and municipal transaction privilege tax.

• The State will create one set of TPT audit procedures to apply to the state and all municipalities.

• The State will administer all (local) multi‐jurisdictional audits. • Municipalities will continue to have the authority to directly audit

single‐jurisdiction businesses. • When the state statutes and model city tax code are the same and

the Department has issued written guidance, the Department's interpretation will be binding.

• Stay tuned: http://www.azdor.gov/TPTSimplification.aspx

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.12

Indiana Research & Development

• Exemption expanded to include all materials and consumables that are integral to R&D

• Effective for purchases on invoices dated July 1, 2013 forward

Maine• Increase of sales tax rate to 6.5%• Enact a 6% service tax and 8% lodging tax

– Professional services included in the proposal which include legal, accounting, engineering and other similar services.

Kentucky Governor is proposing to allow local taxation in cities and counties

throughout Kentucky.‐REJECTED BY HOUSE but still being pushed by the Governor.

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.13

Maine Major tax reform has been proposed to several tax bases as

follows:• Increase of sales tax rate to 6.5%• Enact a 6% service tax and 8% lodging tax

– Professional services included in the proposal which include legal, accounting, engineering and other similar services.

• Reduce personal income tax from 7.95% to 5.75%• Reduce corporate income tax from 8.93% to 6.75%• High‐Tech, Biofuel and Job Credits being proposed.

Kentucky Governor is proposing to allow local taxation in cities and counties

throughout Kentucky.‐REJECTED BY HOUSE but still being pushed by the Governor.

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.14

NEVADA – Commerce Tax Effective July 1, 2015 Entities engaged in business in Nevada with Gross Revenue Exceeding $4

million First commerce tax return and payment will be due on August 15, 2016, for

the taxable year running from July 1, 2015, through June 30, 2016 The commerce tax rates vary (ranging from 0.051% to 0.331%). The tax is

equal to the amount obtained by subtracting $4 million from the business entity’s Nevada gross revenue for the taxable year and multiplying that amount by the applicable rate.

Business Entity Subject To Commerce Tax: Sec. 4 of SB 483• Each entity engaged in a business is subject to the tax, whether they are

corporations including S corporations, partnerships, proprietorships, limited liability companies, business associations, joint stock companies, holding companies, and business trusts.

• Engaged in business broadly defined (Sec. 6):– Commencing, conducting or continuing a business– The exercise of corporate or franchise powers regarding a business– Liquidation of business when entity was conducting the business

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.15

California Partial Exemption in California stated July 1, 2014.

• Applies to qualified property used in Manufacturing and R&D• Effective Date: July 1, 2014, sunsets on June 30, 2022• Annual Cap of $200 million of purchases of qualified TPP (combined

reporting group)• Partial State Level Exemption:

– 4.1875% tax exempt from 7/1/14 – 12/31/16– 3.9375% tax exempt from 1/1/17 – 6/30/22

Colorado For leases renewed or entered into on or after July 1, 2015, lessors

will now be considered to have substantial nexus and must collect local sales tax. Colorado Department of Revenue, February 2015.

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.16

North Dakota Proposed homestead tax credit increase from 42K to 52K per year 25 million dollar tax cut in corporate income 100 million dollar tax cut in personal income tax

Rhode Island Reduction of corporate income tax from 9% to 7% Considering eliminating sales and use tax

Ohio A.M. Castle & Co., (et al.) v. Testa, Ohio BTA (March 9, 2015) –

recent case on temporary employees ruled in favor of taxpayer exemption citing clear evidence of long‐term relationships rather than providing the same person for extended period.

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.17

Minnesota Effective September 1, 2014 July 1, 2015 Capital Equipment May Be Purchased Tax‐Free

• Combined its sales and use tax refund claim form into one form. (Form ST11)

• Machinery & Equipment Used in Manufacturing, Fabricating, Mining, or Refining Including:– Production Equipment– Research & Development Equipment– Environmental Control Devices

California SB 8 (Hertzberg) would tax services. Small business, under $100,000

in sales, and education and healthcare sectors would be exempt. AB 464 (Mullin, Gordon) would increase the maximum rate authorized

by cities and counties from 2% to 3%. Combined state and local tax rate limit would increase from 9.5% to 10.5%.

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.18

Washington New Nexus Standard for Wholesale Sales ‐ Effective Sept. 1, 2015

Effective Sept. 1, 2015, economic nexus standards apply to most out‐of‐state wholesaling businesses. This means that out‐of‐state businesses making wholesale sales into Washington will be subject to the wholesaling business and occupation (B&O) tax on wholesale sales delivered into Washington if the following economic nexus thresholds were met during the prior calendar year:• A business entity is organized or commercially domiciled in Washington

• More than $267,000 of gross income in Washington

• More than $53,000 of payroll in Washington

• More than $53,000 of property in Washington

• At least 25 percent of total property, payroll, or income in Washington

• Note ‐ These thresholds are effective for 2015. Please use these figures until revised. Please see ETA 3195.2015 for previous years and more information.

• ENGROSSED SUBSTITUTE SENATE BILL 6138, Part II, effective September 1, 2015

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.19

Michigan Cloud – The Department continues to struggle in the courts with

defending their position of taxability. Most recently the state was shot down in GXS Inc. v. Department of Treasury, Court of Claims (March 4,2015) viewing the transaction as a service and exempt.

Illinois Proposal for the following

• Lower Income Taxes• Freeze Property Taxes for 2 Years• Modernize the Sales Tax to Include Sales Taxes on Services• Considering taxing legal services only

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.20

Illinois‐Continued Revenue raising estimate is over $600M “Non‐necessity” service categories included:

• Legal fees – $167M• Computer programming services – $53M• Sewer and refuse services – $46M• Printing – $39M• Personal property rentals – $36M• Marketing consulting – $30M• Advertising agencies – $28• Maintenance and janitorial – $28M• Golf club membership fees ‐ $26M

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.21

Illinois‐ContinuedThe plan would exempt:

• Medical services• Certain professional services• Accounting• Architectural• Engineering• Laundromat services• Day care centers• Barbershops• Animal care

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.22

City of Chicago‐Lease Tax Effective January 1, 2015 Rate Increased from 8% to 9% Ruling # 12 – Effective Sept 1, 2015 Applies to Cloud Computing Delayed Enforcement Until Jan 1, 2016

• MPU Apportionment Allowed

Mayor Emanuel’s New Ordinance – Oct 14, 2015• Cloud‐based database services (e.g., LexisNexis) taxable at 9%• Cloud‐based software and infrastructure (e.g., Office365, Amazon

Web Services) taxable at 5.25%• Small Business Exemption

– Gross Annual Sales < $25MM– Operating < 60 months since first sale– Does not apply to subsidiaries of older businesses– Certification by City Comptroller Required

SELECTED STATE BY STATE OVERVIEW

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.23

Sales Taxes The current sales tax system will continue to apply until March 31,

2016.

Sales tax rate increased from 7%‐10.5% on July 1, 2015.

On April 1, 2016, the sales tax will be replaced with a VAT.

4% professional services tax taking effect October 1, 2015. Only applied at the state level.

Sales of taxable goods covered under contract before July 1, 2015 can still use the 7% tax rate.

PUERTO RICO

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.24

Value Added Tax The new value added tax will apply as of April 1, 2016. The rate of the VAT will be 10.5% on the sale of taxable goods and

services. Zero‐rated VAT

• Goods for Export• Services for Export• Sales of raw materials and equipment used in manufacturing plant

Input tax credit regulations are still being written. Same nexus rules will apply as for sales tax. VAT will be due on the 20th of each month.

PUERTO RICO

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.25

CT‐3

AK

HI-3

ME3

RI‐3

VT‐3

PA‐3NJ‐4

MD‐4VA‐3WV 3

NC‐3

GA3

IL‐3OH4IN

3

MI4

WI‐4

AL3

MS3LA

3

TX4

OK-3

MO3

KS-3

IA3

MN3 ½

ND-3

SD-3

NE‐3

NM3

AZ4

CO3

UT3

WY3

WA4

ID3

NV3

MA‐3

SALES TAX STATUTES OF LIMITATIONS IN YEARS

CA3

AR3

DC‐3

FL3

NY‐3

MTOR

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.26

Federal Impact on State and Local Taxes

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.27

Attempted Unprecedented Authority on Out of State Business Non‐Collecting remote sellers reporting requirements. ‘Constitutionally Sufficient Solicitation’ Direct Marketing Association lawsuit sparked an injunction against broad

nexus interpretation House Bill 1193 Repealed Remote Selling Reporting Injunction issued by U.S. District Court on March 30, 2012 Injunction was dissolved on December 10, 2013 and the Department stated it

will not enforce any penalties for failure to comply during the period the injunction was in place.

Denver District Court grants preliminary injunction on February 18, 2014. On March 3, 2015 an unanimous 9‐0 decision, the United States Supreme

Court ruled in favor of a petition by the Direct Marketing Association (DMA) in a case that contested Colorado law that required out‐of‐state retailers to report purchases and personal information of state residents.

Justice Kennedy's concurring statement. “Given these changes in technology and consumer sophistication, it is unwise to delay any longer a reconsideration of the Court’s holding in Quill. A case questionable even when decided, Quill now harms States to a degree far greater than could have been anticipated earlier.

COLORADO – NEXUS STANDARD

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.28

Beginning in 2016, more than 21 states have enacted “Click‐Through” nexus, affiliate nexus, or both.

* 5 states have specific reporting requirements

CLICK‐THROUGH AND AFFILIATE SALES TAX NEXUS

Affiliate Nexus Only10

Click Through Nexus Only

6

Both13

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.29

State Effective DateAlabama 8/24/2012Arkansas 7/27/2011California 9/15/2012Colorado 3/1/2010Georgia 10/1/2012Illinois 7/1/2011Iowa 6/11/2013Kansas 7/1/2013Maine 10/9/2013Michigan 10/15/2015

Missouri 8/28/2013

New York 6/1/2009

State Effective DateNevada 9/1/2015OhioOklahoma ($100,000) 7/1/2010Pennsylvania (bulletin) 12/1/2011Rhode Island 7/1/2009South Dakota 7/1/2011Texas 1/1/2012Utah 7/1/2012Virginia 9/1/2013Wisconsin 7/1/2009Washington 9/1/2015West Virginia 1/1/2014

AFFILIATE NEXUS STATES

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.30

State Effective Date Annual Sales ThresholdArkansas 10/24/2011 $10,000

California 9/15/2012 $10,000

Connecticut 5/4/2011 $2,000

Georgia 12/31/2012 $50,000

Illinois 1/1/2015 $10,000

Kansas 10/1/2013 $10,000

Ohio 7/1/2015 $10,000

Maine 10/9/2013 $10,000

Michigan 10/1/2015 $10,000

Minnesota 7/1/2013 $10,000

Missouri 8/28/2013 $10,000

New Jersey 7/1/2014 $10,000

New York 6/1/2008 $10,000

Nevada 9/1/2015 $10,000

North Carolina 8/7/2009 $10,000

Pennsylvania Bulletin issued 12/1/11 ‐ no legislation

Rhode Island 7/1/2009 $5,000

Vermont When 15 states adopt $10,000

Washington 9/1/2015 $10,000

ENACTED CLICK‐THROUGH NEXUS

AN EXTENSION OF YOUR TAX DEPARTMENT

DuCharme, McMillen & Associates, Inc. All rights reserved. Reproduction of this document or any portion thereof without written consent is prohibited.31

CONTACT INFORMATION

Sean C. EvansDirector, Tax Advisory ServicesOverland Park, KS800‐309‐2110, ext. [email protected]