Embed Size (px)

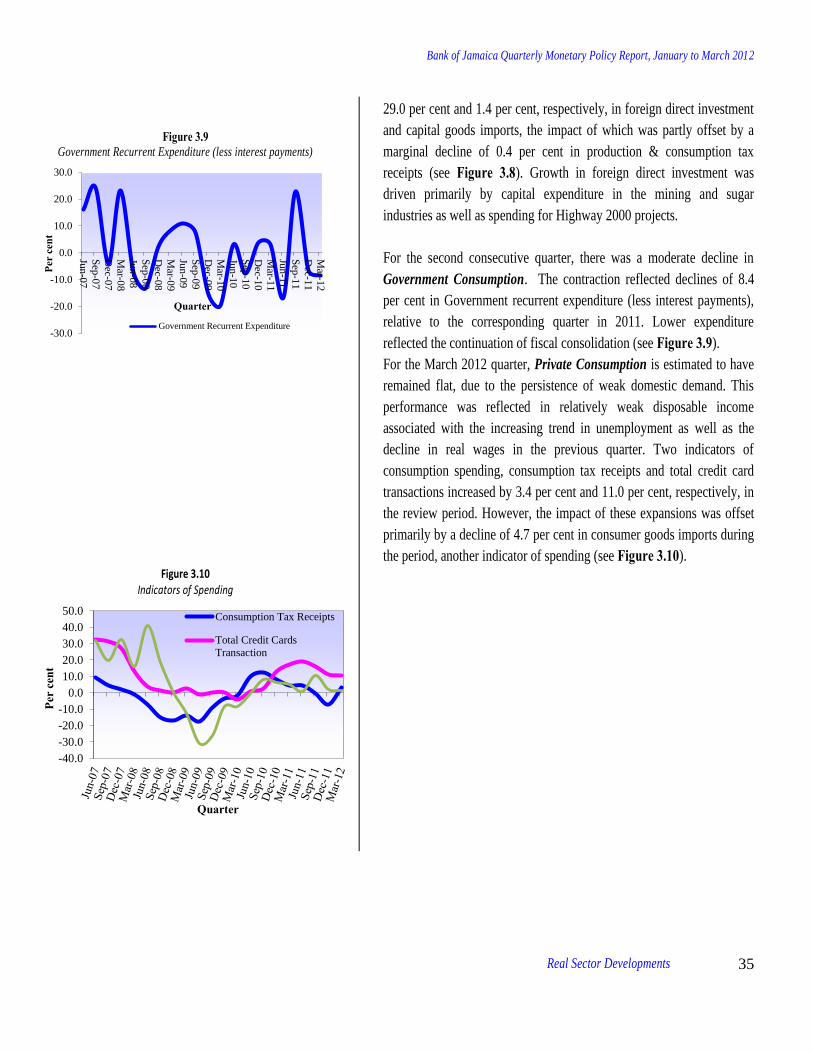

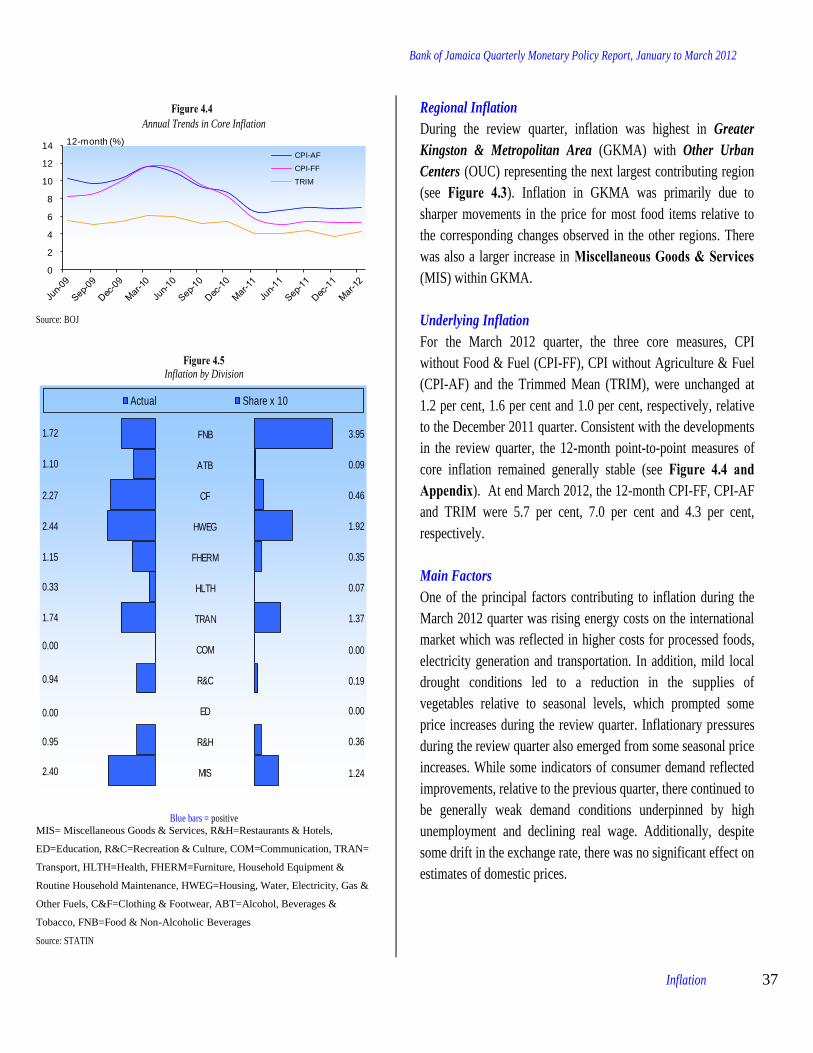

Citation preview

January – March 2012

Volume 12 No. 4

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Bank of Jamaica

Quarterly Monetary

Policy Report

Jan – March 2012

Volume 12 No. 4

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

© 2003 Bank of Jamaica Nethersole Place

Kingston

Jamaica

Telephone: (876) 922 0750-9

Fax: (876) 922 0854

E-mail: [email protected]

Website: www.boj.org.jm

ISSN 0799 1037

The report is available in PDF format at the Bank’s website.

Comments on this publication are welcome and can be sent directly to the Bank or to our website.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

CONTENTS Preface i

Overview iii 1. International Economic Developments 1

Box 1- External Competitiveness in Jamaica 8 2. Monetary Policy and Financial Markets

Money & Credit 14 Monetary Policy & Base Money Management 14

Money Supply 16 Private Sector Credit 19

Bond Market 22

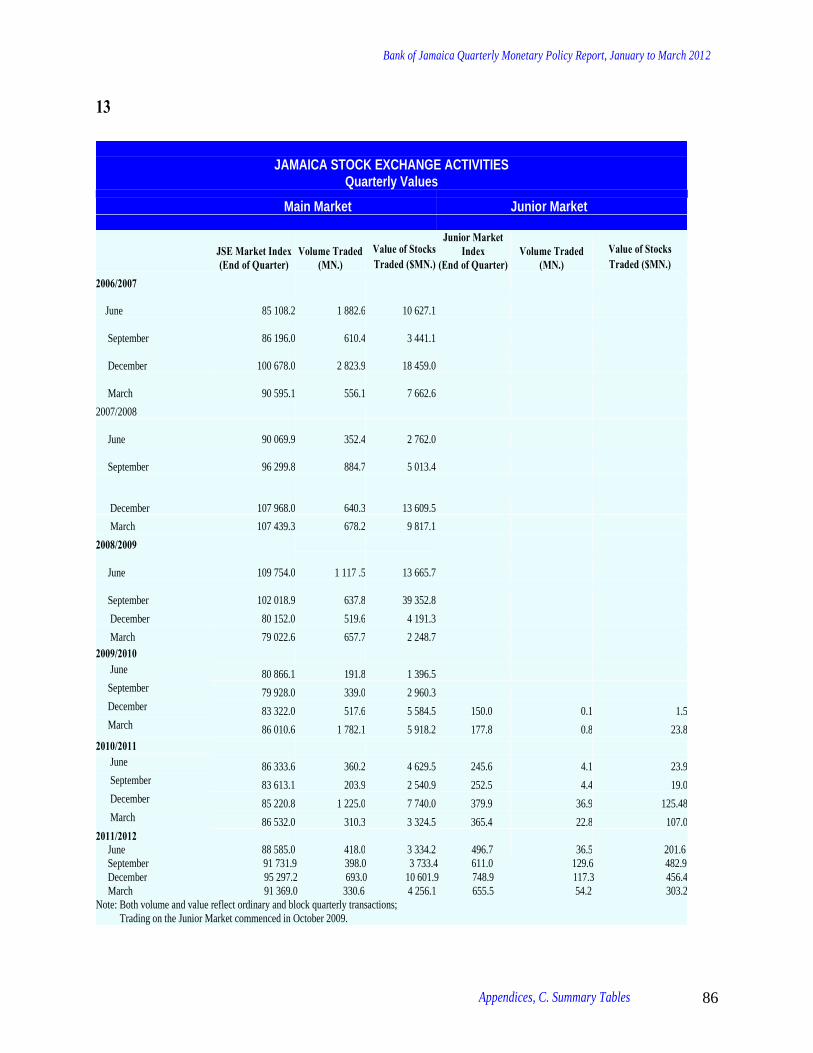

Stock Market 25

Foreign Exchange Market 29

3. Real Sector Developments 31

4. Inflation 36

5. Economic Outlook and Monetary Policy Perspectives 41

Appendices

A. Fiscal Developments 48 B. Monetary Policy Developments 52 C. Summary Tables 71

Glossary 97 List of Boxes in the QMPR 102

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

i

PREFACE

The Bank of Jamaica’s Quarterly Monetary Policy Report reviews the

conduct of monetary policy and the main factors that influence

inflation. It also presents the Bank’s perspective on emerging

economic trends and the path of monetary policy over the short- to

medium-term and features an exposition of Jamaica’s External

Competitiveness (Box 1).

The developments in the review quarter are set against policy targets

for the fiscal year, which runs from April to March. In some instances

the data used in the preparation of the report are provisional and are

therefore subject to change.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

ii

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

iii

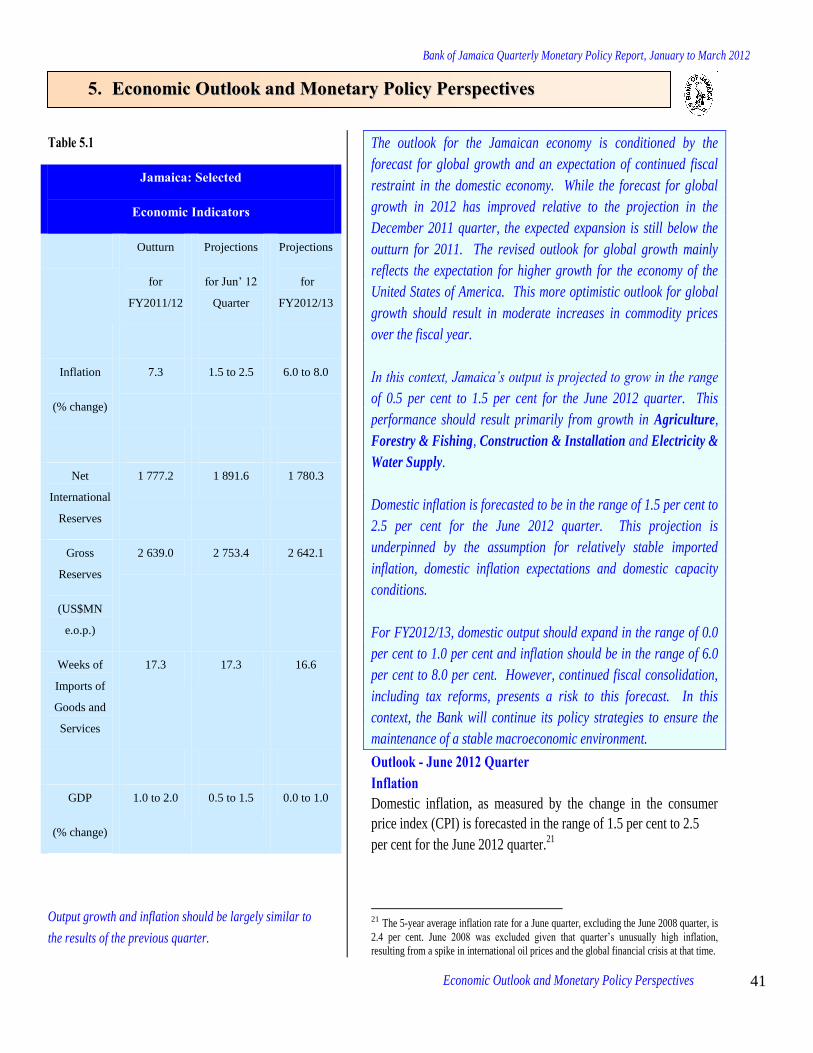

OVERVIEW

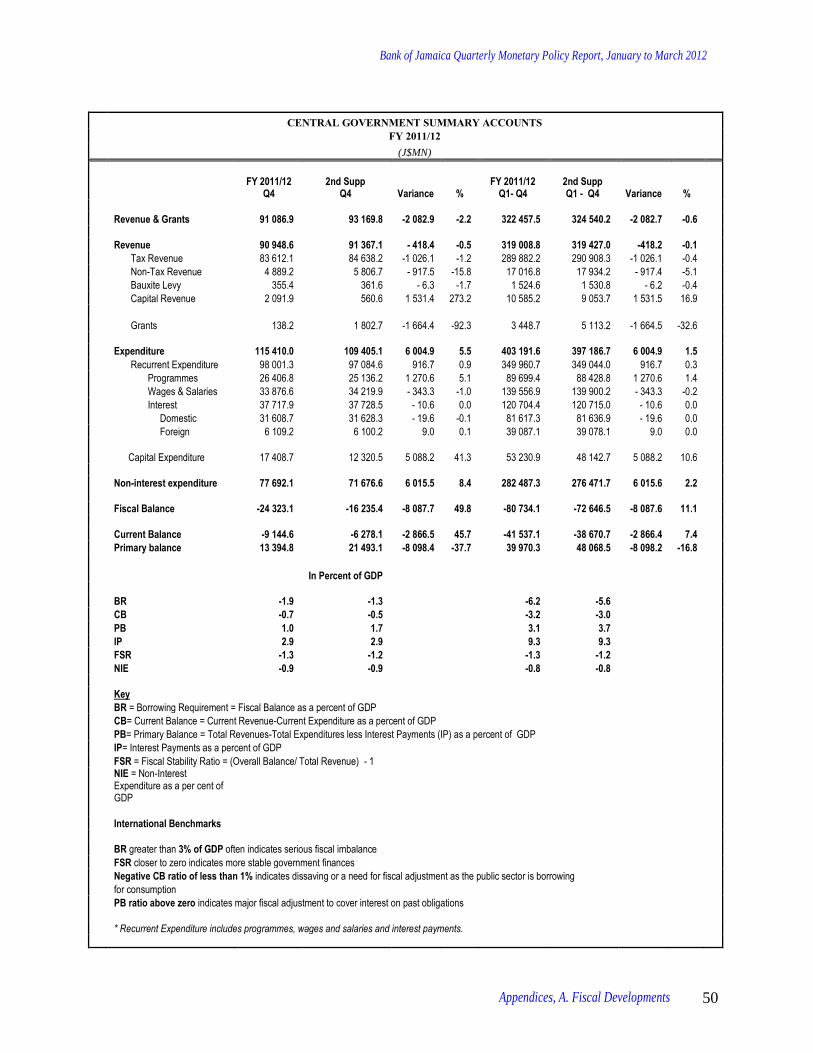

Recent Developments

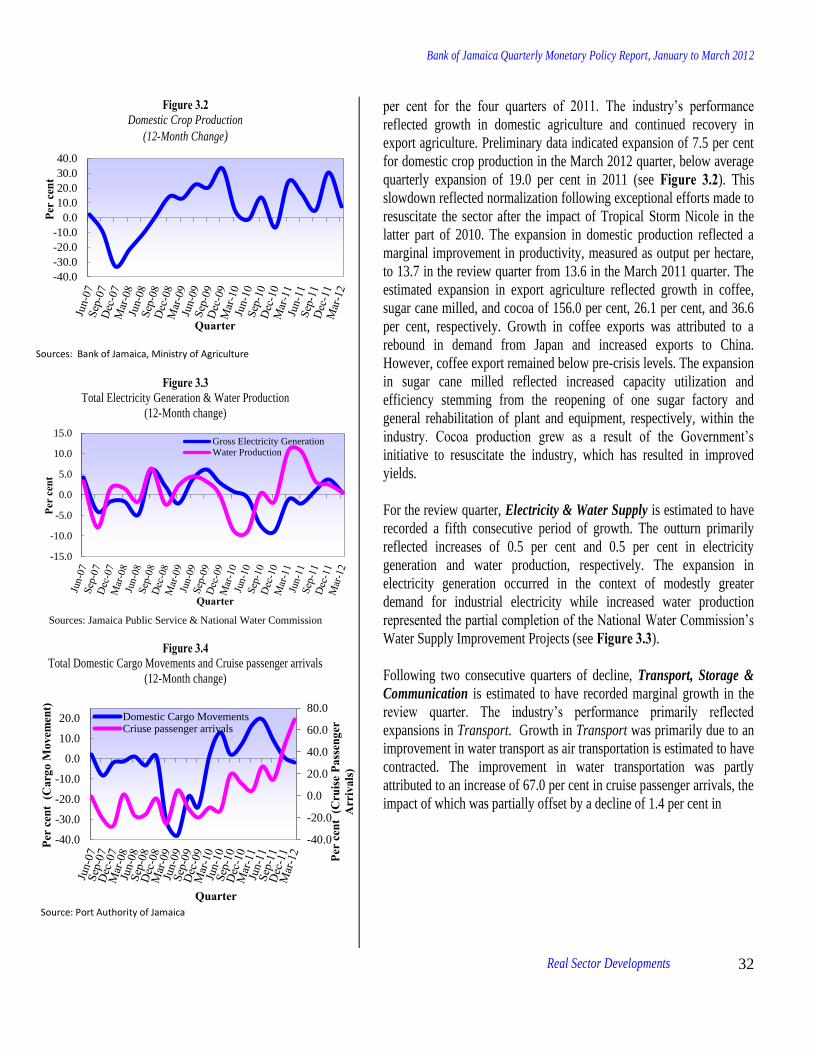

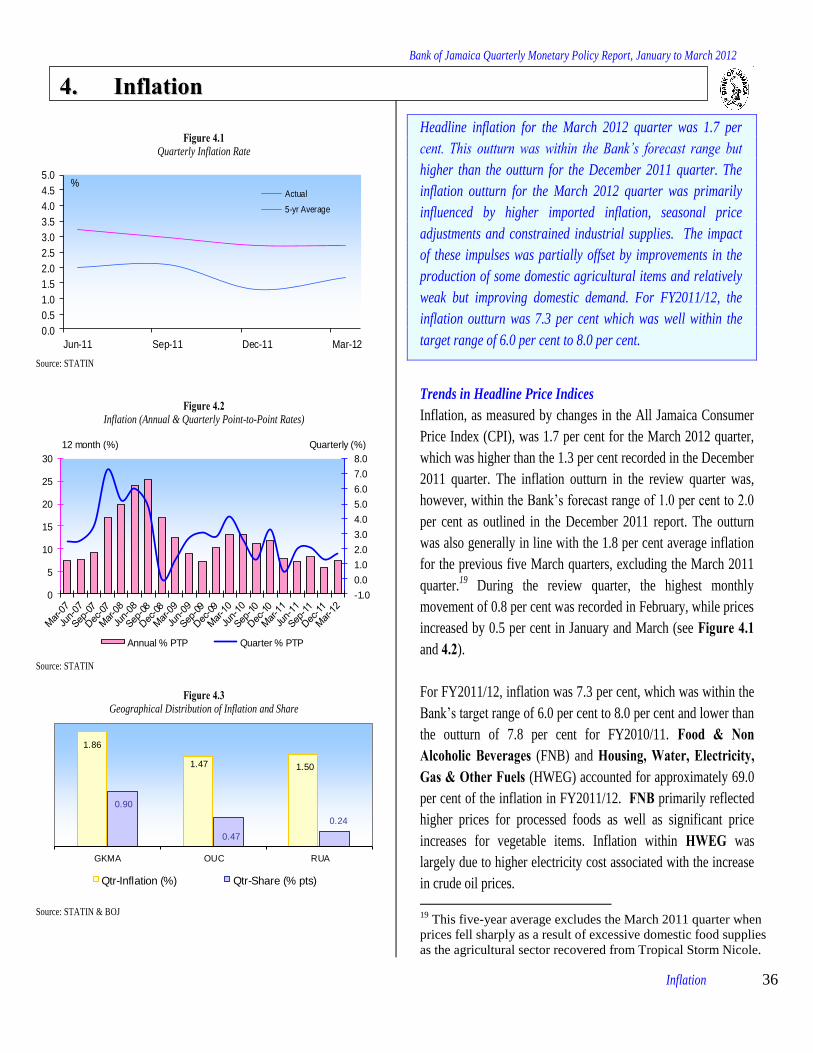

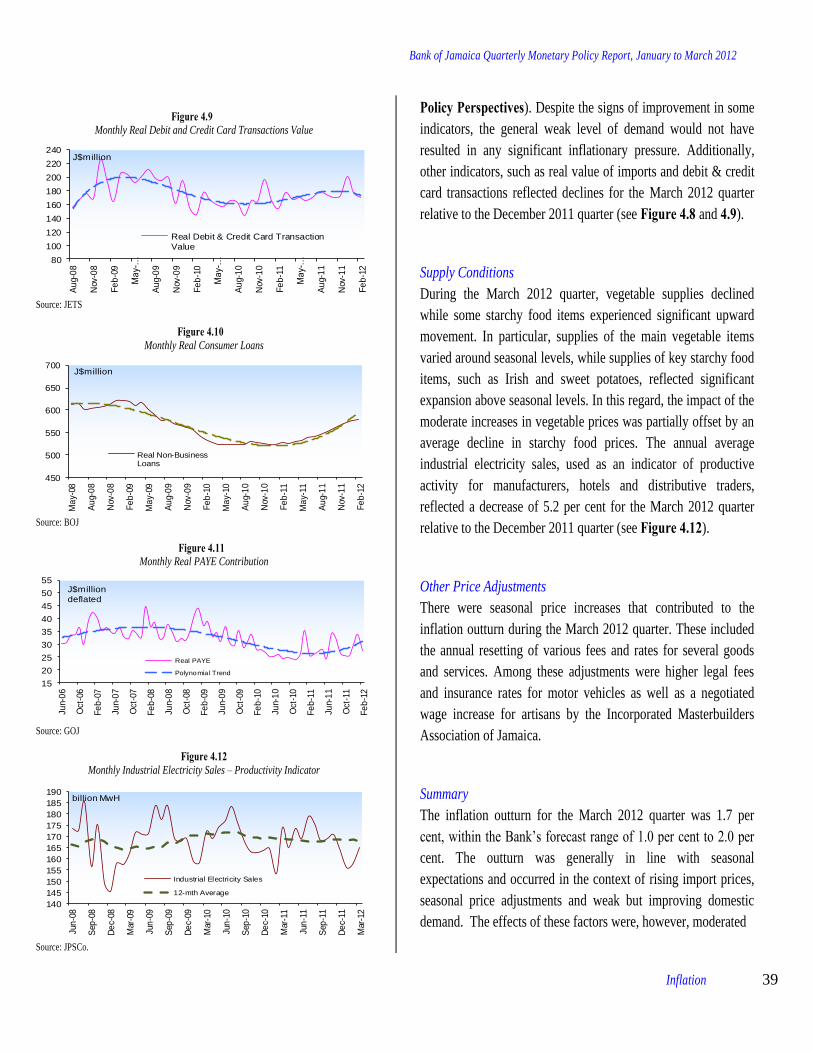

During the March 2012 quarter, the domestic economic

environment continued to be characterized by relatively

stable conditions. Inflation was in the Bank’s forecast

range, the foreign exchange market was generally stable

and the nascent recovery in economic activity continued.

However, there were uncertainties regarding the content

and timing of a new agreement with the IMF and the

impact of the upcoming fiscal budget as well as rising

international commodity prices. Against this background,

the Bank maintained its monetary policy rate at 6.25 per

cent for the review quarter.

Headline inflation for the March 2012 quarter was 1.7 per

cent. This outturn, which was within the Bank’s forecast

range of 1.0 per cent to 2.0 per cent, was primarily

influenced by higher international commodity prices and

moderate depreciation in the exchange rate. The impact of

these impulses was partially offset by reduction in the

prices of some domestic agricultural items due to

improvement in supplies as well as continued weak

domestic demand, albeit improving. For FY2011/12, the

inflation outturn was 7.3 per cent which was within the

target range of 6.0 per cent to 8.0 per cent.

The weighted average selling rate (WASR) of the US dollar

vis-à-vis the Jamaica Dollar, depreciated by 0.8 per cent in

the March 2012 quarter. Notwithstanding, the adequacy of

net private capital flows to finance the demand for current

account transactions for the quarter, there were intermittent

periods of excess demand for foreign currency. Against this

background, the Bank sold US$102.1 million (net) in the

market during the quarter. This contributed to a decline of

US$189.0 million in the net international reserves (NIR) to

US$1 777.1 million. The Bank’s gross reserves at end-

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

iv

March 2012 amounted to US$2 638.9 million, representing

17.0 weeks of projected goods and services imports.

Economic growth is estimated to be in the range of 0.0 per

cent to 1.0 per cent for the March 2012 quarter. This

followed average quarterly growth of 1.5 per cent for 2011.

The estimated growth for the review quarter was mainly

reflected in the following sectors: Agriculture, Forestry &

Fishing; Manufacture; Electricity & Water Supply and

Transport, Storage & Communication. Growth in the

economy was mirrored primarily in net external demand

which emanated from both an increase in exports and a

reduction in imports. Other components of aggregate

demand were estimated to have declined or remained flat in

the review period. For FY2011/12 economic activity is

estimated to have expanded within the range of 1.0 per cent

to 1.5 per cent in comparison to an average decline of 1.6

per cent over the previous two fiscal years. The outturn was

broadly in line with the projection for the fiscal year.

Primarily reflecting the weak domestic demand conditions,

albeit improving, broad Jamaica Dollar money supply

(M3J) declined by 2.0 per cent during the March 2012

quarter, a sharper contraction than the reduction for the

corresponding quarter of 2011. For FY2011/12, M3J grew

by 8.9 per cent and was below the average increase of 9.6

per cent for the last five fiscal years. The contraction for the

review quarter occurred in spite of a 3.9 per cent growth in

private sector credit, albeit at a slower rate than that

recorded for the preceding quarter. The increased demand

for private sector loans during the March 2012 quarter may

be reflective of the continued contraction in rates offered

on overall credit, with the weighted average rate of interest

on private sector credit falling by 35 bps.

The quality of private sector credit improved marginally

during the review quarter. In this regard, the ratio of non-

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

v

performing loans, three-months and over declined to 8.4

per cent from 8.8 per cent for the December 2011 quarter.

During the March 2012 quarter, market determined interest

rates exhibited mixed movements. While the average yield

on the GOJ 30-day Treasury bill declined over the quarter,

there were marginal increases on the longer tenors. Of note,

there was convergence in yield on the 90-day tenor towards

equivalent yield on the BOJ’s 30-day Certificate of Deposit

(CD).

Outlook

The general price level for domestic consumer goods and

services is forecasted to expand by 1.5 per cent to 2.5 per

cent during the June 2012 quarter, following an increase of

1.7 per cent for the March 2012 quarter. Inflation for the

quarter is expected to be influenced by a forecast for

relatively stable imported inflation, domestic inflation

expectations and capacity conditions. The forecast for

imported inflation assumes that, in spite of some volatility

in crude oil price intra-quarter, the overall movement

should not be significantly different from the average price

which prevailed in the previous quarter. In addition, the

output gap is expected to remain negative but improving

relative to the previous quarter thus providing minimal

impetus to price increases. There is the possibility of

additional inflationary impulses emanating from fiscal

measures, which would result in a higher inflation.

Domestic output is anticipated to expand marginally for the

June quarter, largely similar to the estimated growth in the

March quarter. The main growth sectors are expected to be

Agriculture, Forestry & Fishing, Mining & Quarrying, Hotels &

Restaurants and Electricity & Water Supply.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

vi

For FY2012/13, headline inflation is currently forecasted to

be within the 6.0 per cent to 8.0 per cent range. The

anticipated rate of increase in the general price level partly

reflects expected general improvement in weather patterns

in the major grain producing countries. Inflation could also

be impacted by increased oil prices, given the improved

prospects for global growth and the continuing geopolitical

risks in some oil producing countries. However, inflation

could fall outside of the forecast range with the

implementation of measures to return the fiscal account to a

sustainable path.

Economic output for FY2012/13 is currently forecasted to

expand in the range of 0.0 per cent to 1.0 per cent. This

outlook reflects the expectation of continued weak

domestic demand, albeit improving relative to the crisis

period, coupled with a slower rate of expansion in global

growth in calendar year 2012 relative to 2011. Nonetheless,

the forecasted growth in the global economy is expected to

generate improved external demand for Jamaican goods

and services and acceleration in remittance flows to

Jamaica.

For FY2012/13 and beyond, strong and sustainable

improvement in domestic economic performance rests

critically on significant enhancement of the country’s

external competitiveness. This can be achieved through

adjustments to relative prices and the amelioration of

structural issues that impede competitiveness. Importantly,

attempts to address the issue of external competiveness

solely through adjustments to relative prices would be

inadequate.

Against this background, the Bank’s monetary policy

stance will continue to be supportive of the maintenance of

a stable macroeconomic environment within the context of

relatively stable financial markets and continued GOJ fiscal

consolidation.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

vii

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

International Developments 1

Table 1.1

Selected GDP Growth Rates***

Sep-11 Dec-11 Mar-12

Advanced Economies

USA 1.8 3.0 2.2

Canada 4.2 1.8 2.1*

Japan 7.1 -0.7 0.0

UK 0.3 0.5 0.6*

Euro area 1.3 0.7 -0.3*

Emerging Market Economies

China 9.1 8.9 8.1

Russia 5.0 4.8 3.7*

Brazil 2.1 1.4 1.8*

Sources: Central Statistics Offices *Bloomberg Consensus Forecasts **BOJ Forecasts

***Quarter-over-Quarter percentage change at annual rates

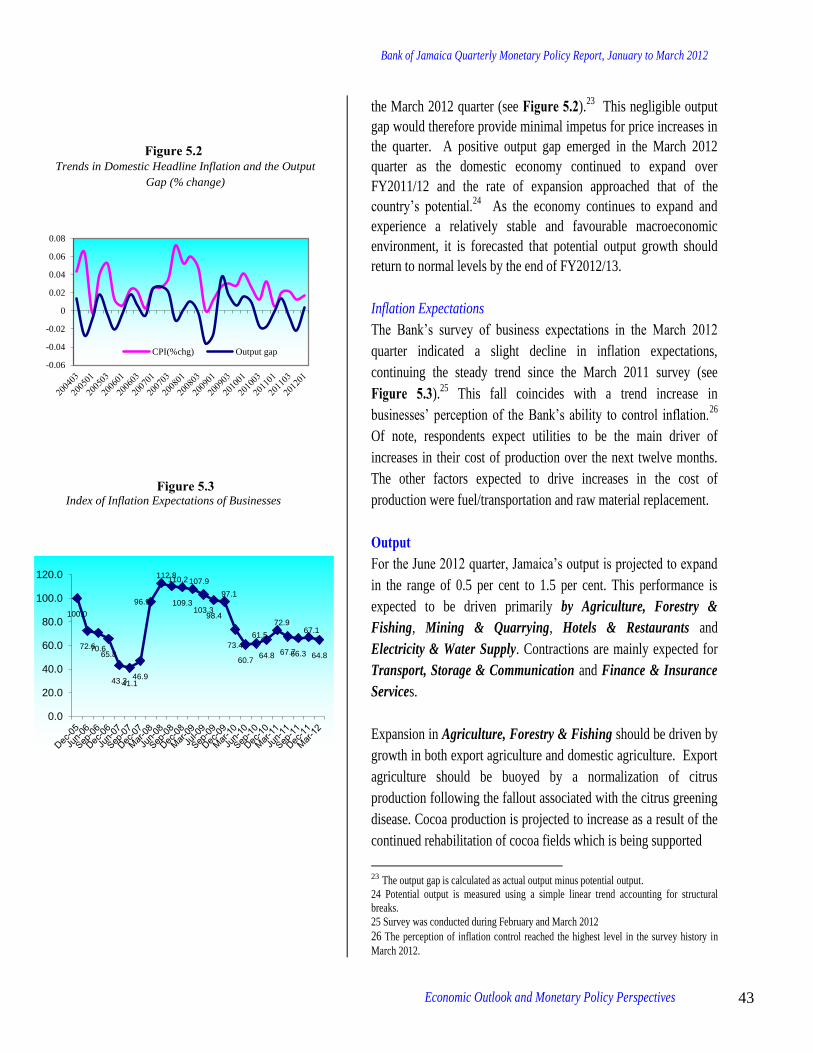

Global economic growth is estimated to have decelerated during the

March 2012 quarter

The pace of global economic growth is estimated to have

slowed in the March 2012 quarter reflecting a slower pace of

growth in some advanced and emerging market economies.

With respect to the advanced economies, the deceleration

largely reflected an estimated contraction in the Euro area as

well as a reduced pace of growth in the USA. For emerging

markets, the slowdown was mainly reflected in China.

Jamaica’s terms of trade (TOT) is estimated to have improved

for the March quarter. This primarily emanated from an

estimated rise in export prices, the impact of which was partly

offset by an increase in import prices.

In the context of weak domestic economic activity, central

banks in most advanced economies kept their target interest

rates unchanged and provided necessary liquidity to alleviate

credit constraints in financial markets. The central banks of

some emerging market economies also employed expansionary

monetary policy measures to mitigate the effects of a weak

global environment.

Market interest rates for US dollar-denominated assets rose

during the review quarter, primarily driven by reduced

concerns about Greece and the impact of the European debt

crisis on international financial markets. Against this

background, emerging market bonds yields declined during the

quarter.

Global Economic Growth

The pace of global economic growth in the March 2012 quarter

is estimated to have decelerated relative to the previous

quarter. The slower pace of growth largely reflected an

estimated contraction in the economies in the Eurozone as well

as a reduced pace of economic growth in USA. This was

however, partly offset by a rebound in economic output of the

Japanese economy. Growth among emerging economies,

particularly China is also estimated to have slowed during the

quarter (see Table 1.1).

11.. IInntteerrnnaattiioonnaall DDeevveellooppmmeennttss

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

International Developments 2

Table 1.2

Source: Central statistics offices * Bloomberg Consensus forecasts

Real GDP growth in the Euro area is estimated to have

contracted by 0.3 per cent in the March 2012 quarter following

a marginal expansion of 0.7 per cent in the preceding quarter.

This estimated contraction reflected the impact of the

implementation of fiscal austerity measures in some Euro area

countries affected by the sovereign debt crisis. In particular,

growth in Europe’s two largest economies, Germany and

France, is estimated to have decelerated to 0.8 per cent and 0.3

per cent, respectively, during the March quarter from 2.0 per

cent and 1.3 per cent in the December 2011 quarter.

For the USA, real GDP growth is estimated to have

decelerated to 2.2 per cent in the March 2012 quarter, relative

to a 3.0 per cent expansion in the December 2011 quarter. This

performance largely reflected an estimated reduction in net

export earnings stemming from a slowdown in global trade.

Similarly, investment expenditure declined during the quarter,

largely reflecting a deceleration in new home sales. The sale of

new homes, on an annualised basis, is estimated to have

moderated to 5.6 per cent from 11.7 per cent in the preceding

quarter. Growth in consumption expenditure, however,

accelerated reflecting more favourable labour market

conditions as well as an improvement in business and

consumer confidence during the quarter. The Japanese economy is estimated to have grown, on an

annualised basis, by 1.7 per cent in the March 2012 quarter,

following a contraction of 0.7 per cent in the previous quarter.

This rebound in growth reflected an improvement in the

manufacturing sector associated with increased domestic

demand influenced by reconstruction activities following the

natural disaster in 2011. Additionally, a 5.7 per cent

depreciation in the value of the Japanese Yen contributed to

the acceleration in export-led growth in that country.

With respect to emerging economies, real GDP for China

decelerated to 8.1 per cent in the March 2012 quarter, relative

to growth of 8.9 per cent in the previous quarter. This also

compares to average growth of 10.6 per cent in the previous

five March quarters. The deceleration in the rate of growth

Average Unemployment Rate for Selected Economies

Jun. 11 – Mar. 12

USA Canada Euro

area

Jun-11 9.0 7.5 10.0

Sept-11 9.1 7.3 10.2

Dec-11 8.7 7.5 10.5

Mar-12 8.3 7.4 10.7*

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

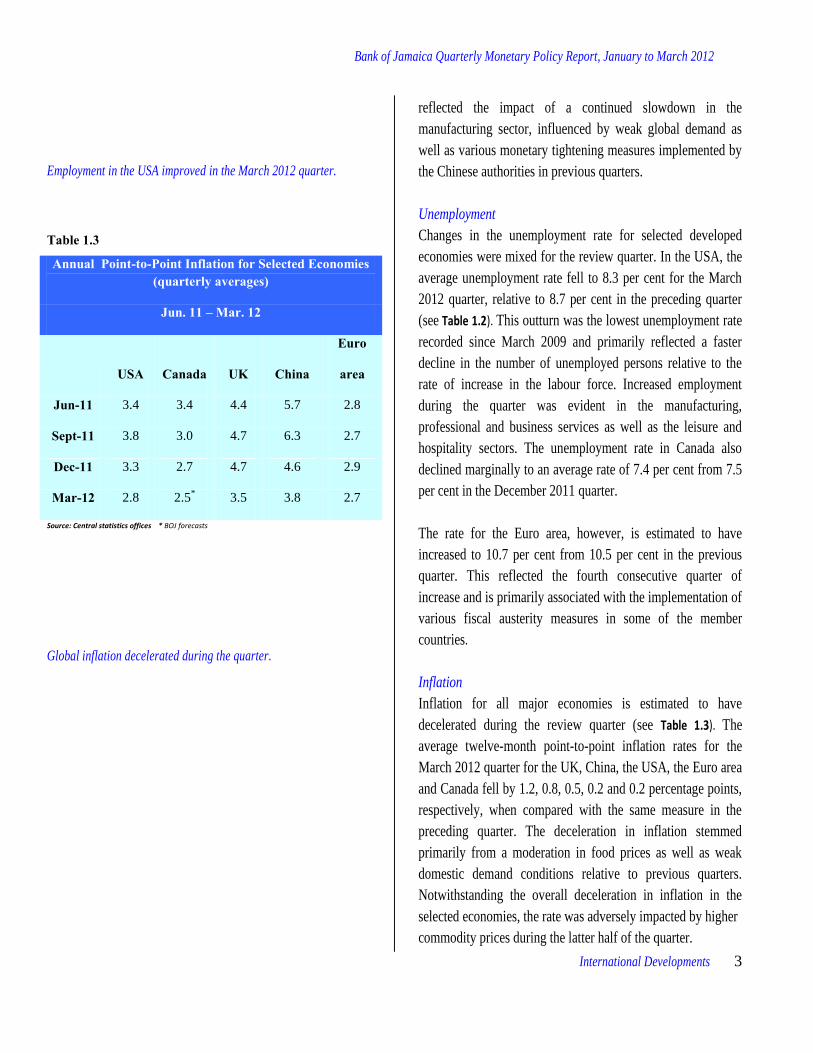

International Developments 3

Employment in the USA improved in the March 2012 quarter.

Table 1.3

Source: Central statistics offices * BOJ forecasts

Global inflation decelerated during the quarter.

reflected the impact of a continued slowdown in the

manufacturing sector, influenced by weak global demand as

well as various monetary tightening measures implemented by

the Chinese authorities in previous quarters.

Unemployment

Changes in the unemployment rate for selected developed

economies were mixed for the review quarter. In the USA, the

average unemployment rate fell to 8.3 per cent for the March

2012 quarter, relative to 8.7 per cent in the preceding quarter

(see Table 1.2). This outturn was the lowest unemployment rate

recorded since March 2009 and primarily reflected a faster

decline in the number of unemployed persons relative to the

rate of increase in the labour force. Increased employment

during the quarter was evident in the manufacturing,

professional and business services as well as the leisure and

hospitality sectors. The unemployment rate in Canada also

declined marginally to an average rate of 7.4 per cent from 7.5

per cent in the December 2011 quarter.

The rate for the Euro area, however, is estimated to have

increased to 10.7 per cent from 10.5 per cent in the previous

quarter. This reflected the fourth consecutive quarter of

increase and is primarily associated with the implementation of

various fiscal austerity measures in some of the member

countries.

Inflation

Inflation for all major economies is estimated to have

decelerated during the review quarter (see Table 1.3). The

average twelve-month point-to-point inflation rates for the

March 2012 quarter for the UK, China, the USA, the Euro area

and Canada fell by 1.2, 0.8, 0.5, 0.2 and 0.2 percentage points,

respectively, when compared with the same measure in the

preceding quarter. The deceleration in inflation stemmed

primarily from a moderation in food prices as well as weak

domestic demand conditions relative to previous quarters.

Notwithstanding the overall deceleration in inflation in the

selected economies, the rate was adversely impacted by higher

commodity prices during the latter half of the quarter.

Annual Point-to-Point Inflation for Selected Economies (quarterly averages)

Jun. 11 – Mar. 12

USA Canada UK China

Euro

area

Jun-11 3.4 3.4 4.4 5.7 2.8

Sept-11 3.8 3.0 4.7 6.3 2.7

Dec-11 3.3 2.7 4.7 4.6 2.9

Mar-12 2.8 2.5* 3.5 3.8 2.7

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

International Developments 4

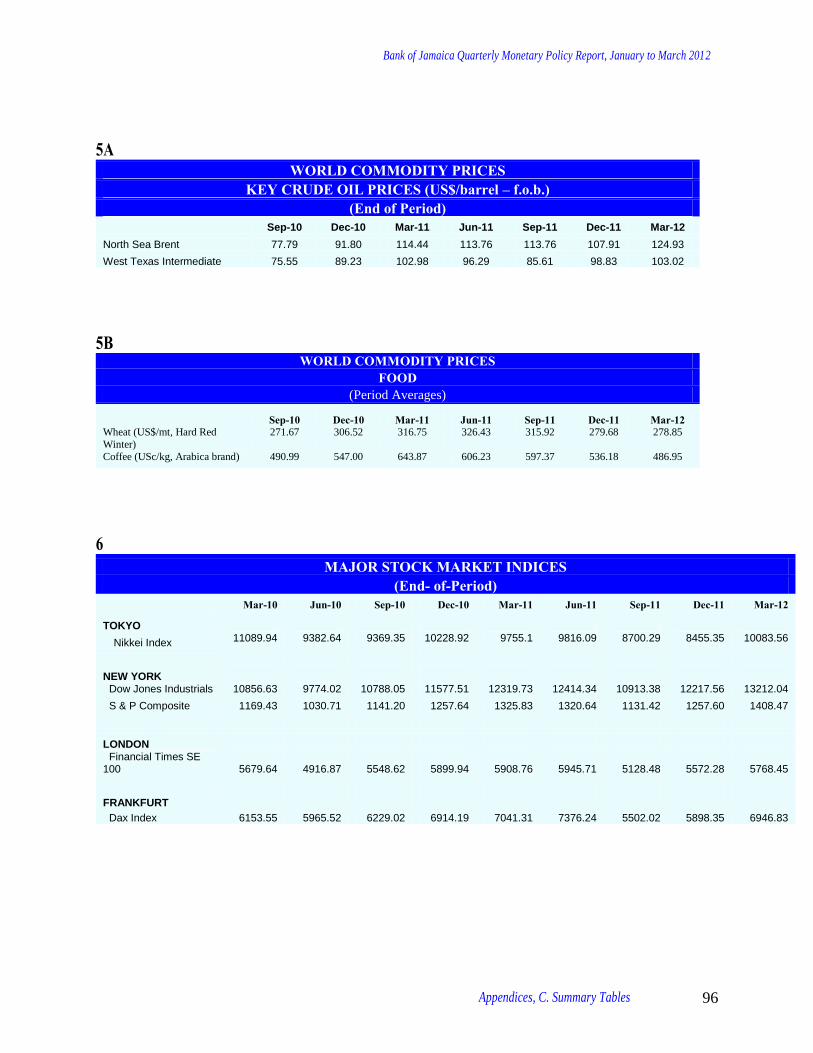

Higher crude oil and agricultural commodity prices characterized

the March 2012 quarter.

Table 1.4

Source: IMF Pink Sheets

* Tourism Implicit Price Index, **Aluminium is the proxy used for alumina prices

Jamaica’s Terms of Trade

Jamaica’s terms of trade (TOT), increased by an estimated 3.7

per cent for the March 2012 quarter, relative to the December

2011 quarter (see Table 1.4).1 This compares to an average

increase of 14.1 per cent over the past five March quarters. On

an annual basis, the TOT however, declined by 5.7 per cent.

The improvement during the review quarter was attributed to

an 8.3 per cent rise in the Export Price Index (EPI), which was

partly tempered by a 4.4 per cent increase in the Import Price

Index (IPI).

The rise in the EPI emanated from an estimated 77.2 per cent

increase in sugar prices. This was associated with a change in

the contractual arrangements to a higher priced private investor

during the quarter. The performance of the IPI was

underpinned by higher fuel and agricultural raw materials

prices during the review period. Notably, average crude oil

prices as measured by the West Texas Intermediate

benchmark, rose by 9.4 per cent during the March 2012 quarter

to average US$102.94 per barrel. This compares to a five-year

seasonal average increase of 4.8 per cent. Higher fuel prices

largely stemmed from concerns regarding possible supply

disruptions due to the implementation of sanctions against Iran

and the threat of a closure of the Strait of Hormuz, the transit

point for approximately 20.0 per cent of global oil. Price

movements were also influenced by the impact of favourable

macroeconomic conditions in the USA and the approval of a

second Greek bailout package in the latter half of the quarter.

Higher agricultural raw material prices were underpinned by

reduced yields in South America reflecting the impact of

drought conditions in Argentina and Brazil since late

December 2011. Average soybean, corn and wheat prices

therefore rose by 6.0 per cent, 3.1 per cent and 1.4 per cent,

respectively, and contributed to a 1.1 per cent increase in the

Bank’s agricultural raw material sub-index for the quarter.

1 The quarterly TOT index is measured by a 3-month average of BOJ’s monthly

index over the referenced period.

Selected Import/Export Prices (period averages)

(Per cent changes relative to previous period)

Sept-11 Dec-11 Mar-12

TOT -2.8 -1.3 3.7

IPI -5.7 0.1 4.4

Crude Oil -12.5 4.8 9.4

Soybeans -1.4 -11.1 6.0

Corn -3.4 -10.9 3.1

Rice 14.8 5.9 -9.3

Wheat -8.6 -9.6 1.4

EPI -8.4 1.2 8.3

Sugar -8.0 0 77.2

Aluminium** -7.2 -13.3 5.0

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

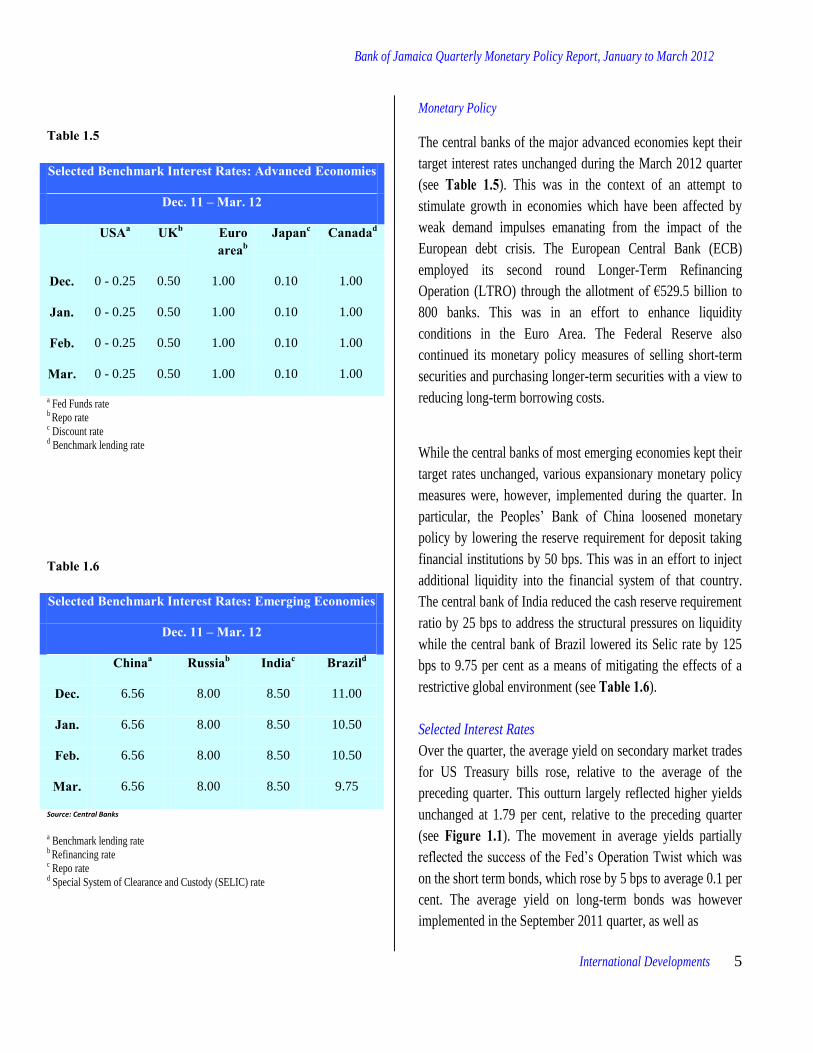

International Developments 5

Table 1.5

a Fed Funds rate b Repo rate c Discount rate d Benchmark lending rate

Table 1.6

Source: Central Banks

a Benchmark lending rate b Refinancing rate c Repo rate d Special System of Clearance and Custody (SELIC) rate

Monetary Policy

The central banks of the major advanced economies kept their

target interest rates unchanged during the March 2012 quarter

(see Table 1.5). This was in the context of an attempt to

stimulate growth in economies which have been affected by

weak demand impulses emanating from the impact of the

European debt crisis. The European Central Bank (ECB)

employed its second round Longer-Term Refinancing

Operation (LTRO) through the allotment of €529.5 billion to

800 banks. This was in an effort to enhance liquidity

conditions in the Euro Area. The Federal Reserve also

continued its monetary policy measures of selling short-term

securities and purchasing longer-term securities with a view to

reducing long-term borrowing costs.

While the central banks of most emerging economies kept their

target rates unchanged, various expansionary monetary policy

measures were, however, implemented during the quarter. In

particular, the Peoples’ Bank of China loosened monetary

policy by lowering the reserve requirement for deposit taking

financial institutions by 50 bps. This was in an effort to inject

additional liquidity into the financial system of that country.

The central bank of India reduced the cash reserve requirement

ratio by 25 bps to address the structural pressures on liquidity

while the central bank of Brazil lowered its Selic rate by 125

bps to 9.75 per cent as a means of mitigating the effects of a

restrictive global environment (see Table 1.6).

Selected Interest Rates

Over the quarter, the average yield on secondary market trades

for US Treasury bills rose, relative to the average of the

preceding quarter. This outturn largely reflected higher yields

unchanged at 1.79 per cent, relative to the preceding quarter

(see Figure 1.1). The movement in average yields partially

reflected the success of the Fed’s Operation Twist which was

on the short term bonds, which rose by 5 bps to average 0.1 per

cent. The average yield on long-term bonds was however

implemented in the September 2011 quarter, as well as

Selected Benchmark Interest Rates: Advanced Economies

Dec. 11 – Mar. 12

USAa UKb Euro areab

Japanc Canadad

Dec. 0 - 0.25 0.50 1.00 0.10 1.00

Jan. 0 - 0.25 0.50 1.00 0.10 1.00

Feb. 0 - 0.25 0.50 1.00 0.10 1.00

Mar. 0 - 0.25 0.50 1.00 0.10 1.00

Selected Benchmark Interest Rates: Emerging Economies

Dec. 11 – Mar. 12

Chinaa Russiab Indiac Brazild

Dec. 6.56 8.00 8.50 11.00

Jan. 6.56 8.00 8.50 10.50

Feb. 6.56 8.00 8.50 10.50

Mar. 6.56 8.00 8.50 9.75

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

International Developments 6

Figure 1.1 US Treasury Yield Curve

Table 1.7

Source: British Bankers’ Association

improvements in the US labour and equity markets. This

resulted in reduced demand for the relative safety of

Treasuries, particularly in the short-term.

Credit risk in US financial markets declined during the review

period. The average spread between the 3-month USD LIBOR

and the 3-month US Treasury bill (TED spread), an indicator

of this risk, fell by 2 bps, relative to the previous quarter, to

average 44.5 bps (see Table 1.7). This decline reflected

reduced concerns about the instability in the financial markets

and an upward revision to the pace of global economic growth,

particularly in the context of the approval of the second bailout

package for Greece during the quarter.

Emerging Market Bonds

The average yield on the EMBI+ declined by 28 bps to 5.54

per cent during the quarter. As a result, the spread between the

EMBI+ and US Treasury bond yields (USTB) narrowed by 30

bps during the review period. Notwithstanding, the spread

between GOJ global bond yields and the USTB yields widened

by 4 bps to 5.56 per cent during the March 2012 quarter

reflecting the impact of domestic factors on investors’

perceptions.2

Equities

Selected stock market indices rose during the review period. In

the USA, the Dow Jones Industrial Average (DJIA) and the

Standard & Poor’s 500 index(S&P 500) rose by 8.0 per cent

and 12.0 per cent, respectively, during the quarter.

The rise in the indices reflected increased investor preference

for equities during the quarter against the background of

improved macro-economic conditions, particularly in the

labour market. The FTSE 100 Index, UK’s main index, also

2The GOJGB composite bond index is calculated as a weighted average of the

yields on currently outstanding Government of Jamaica global bonds. The weights

used, are based on Basis Point Value (BPV) estimates, a derivative of duration

statistics. BPV quantifies the interest rate risk in a portfolio for small changes in

interest rates.

Selected Market Interest Rates

(period averages)

3-month USD

LIBOR

3-month US

Treasury Bill

TED Spread

(bps)

Jun-11 0.26 0.05 21.7

Sep-11 0.30 0.02 27.4

Dec-11 0.48 0.01 46.6

Mar-12 0.51 0.07 44.5

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

International Developments 7

Figure 1.2 Selected Stock Market Indices

increased by 3.5 per cent against the background of the

approval of the second bailout package for Greece as well as

monetary policy initiatives employed by the ECB during the

quarter. Japan’s main index, the Nikkei 225, also rose by 19.3 per cent as the depreciation in the Yen and increased demand

for Japanese exports heightened growth prospects in that

country (see Figure 1.2).

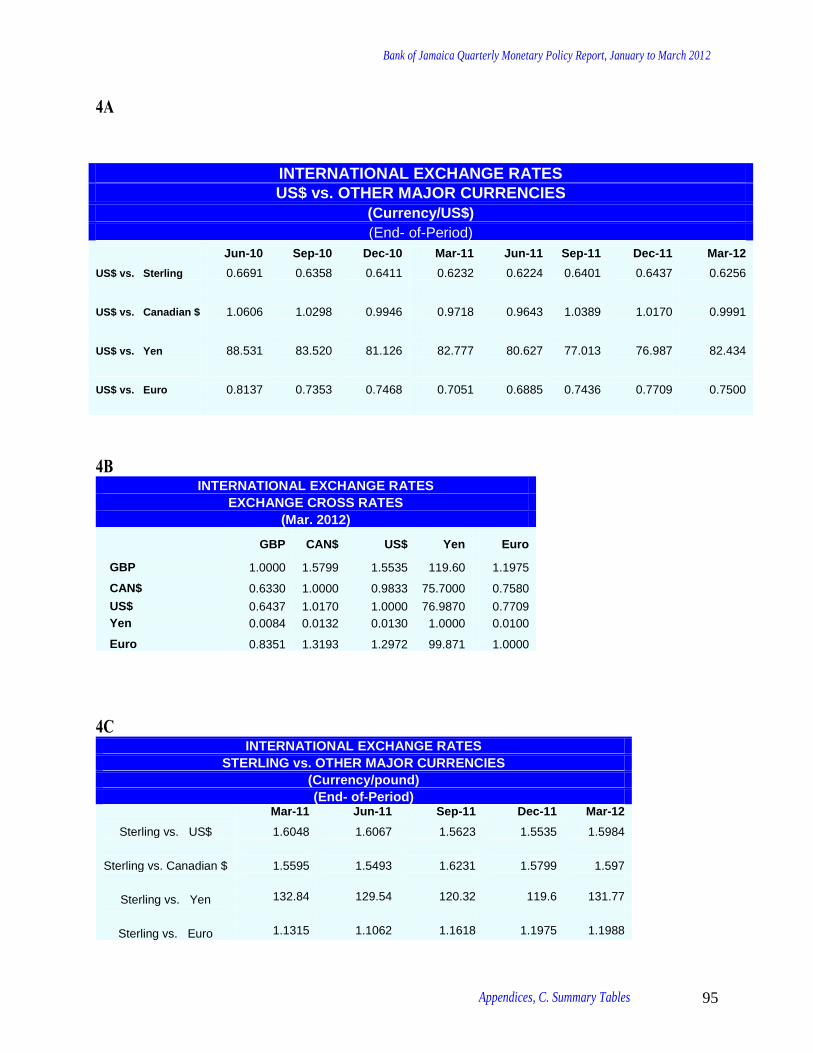

Foreign Exchange Market

The US dollar strengthened against some major currencies

during the review period. Notably, the Euro and the Yen

depreciated by 2.6 per cent and 2.4 per cent, respectively,

reflecting the impact of financial market instability,

particularly during the first half of the quarter. The Great

British Pound was unchanged relative to the previous quarter.

Higher oil and agricultural commodity prices resulted in

appreciation of the currencies of Canada, Brazil, and Mexico

relative to the US dollar during the quarter.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

8

Box 1: External Competitiveness in Jamaica Introduction In a context of persistently weak economic growth and high current

account deficits over the past decade, there has been heightened

focus among policy makers on the external competitiveness of the

Jamaican economy.3 It has been argued that Jamaica could see

significant improvements in these and other macroeconomic

indicators by producing goods and services at prices and qualities,

which are at least comparable to those of other producers in the

world. This would induce both domestic and external consumers to

demand more locally produced goods and services.

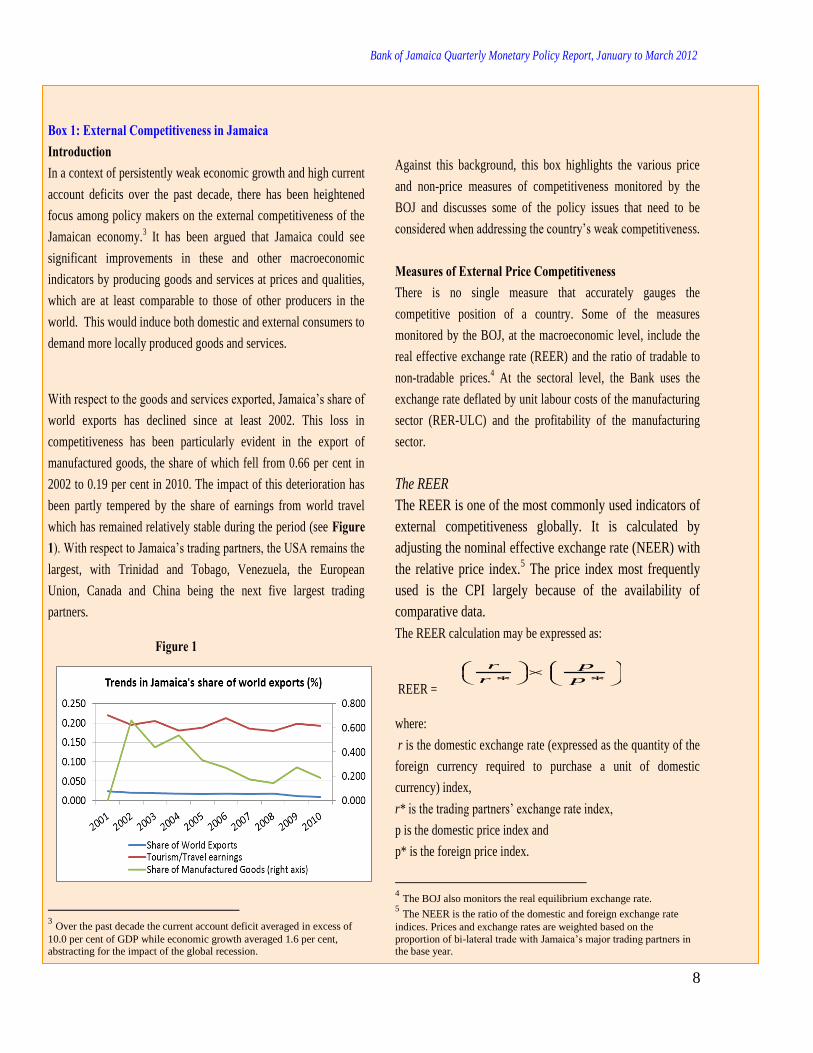

With respect to the goods and services exported, Jamaica’s share of

world exports has declined since at least 2002. This loss in

competitiveness has been particularly evident in the export of

manufactured goods, the share of which fell from 0.66 per cent in

2002 to 0.19 per cent in 2010. The impact of this deterioration has

been partly tempered by the share of earnings from world travel

which has remained relatively stable during the period (see Figure 1). With respect to Jamaica’s trading partners, the USA remains the

largest, with Trinidad and Tobago, Venezuela, the European

Union, Canada and China being the next five largest trading

partners.

Figure 1

3 Over the past decade the current account deficit averaged in excess of

10.0 per cent of GDP while economic growth averaged 1.6 per cent, abstracting for the impact of the global recession.

Against this background, this box highlights the various price

and non-price measures of competitiveness monitored by the

BOJ and discusses some of the policy issues that need to be

considered when addressing the country’s weak competitiveness. Measures of External Price Competitiveness There is no single measure that accurately gauges the

competitive position of a country. Some of the measures

monitored by the BOJ, at the macroeconomic level, include the

real effective exchange rate (REER) and the ratio of tradable to

non-tradable prices.4 At the sectoral level, the Bank uses the

exchange rate deflated by unit labour costs of the manufacturing

sector (RER-ULC) and the profitability of the manufacturing

sector.

The REER

The REER is one of the most commonly used indicators of

external competitiveness globally. It is calculated by

adjusting the nominal effective exchange rate (NEER) with

the relative price index.5 The price index most frequently

used is the CPI largely because of the availability of

comparative data.

The REER calculation may be expressed as:

REER =

where:

r is the domestic exchange rate (expressed as the quantity of the

foreign currency required to purchase a unit of domestic

currency) index,

r* is the trading partners’ exchange rate index,

p is the domestic price index and

p* is the foreign price index.

4 The BOJ also monitors the real equilibrium exchange rate.

5 The NEER is the ratio of the domestic and foreign exchange rate

indices. Prices and exchange rates are weighted based on the

proportion of bi-lateral trade with Jamaica’s major trading partners in the base year.

** p

p

r

r

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

9

An improvement in competitiveness, as measured by a decline in

the REER, emanates from either depreciation in the NEER or a

decline in relative prices. A depreciation in the NEER is

represented by a decline in the value of the domestic currency vis-

à-vis the foreign currency or an appreciation of the currencies of

the country’s main trading partners against the US dollar.

Similarly, the REER would decline if the rate of inflation for the

domestic economy is below that of the country’s main trading

partners.

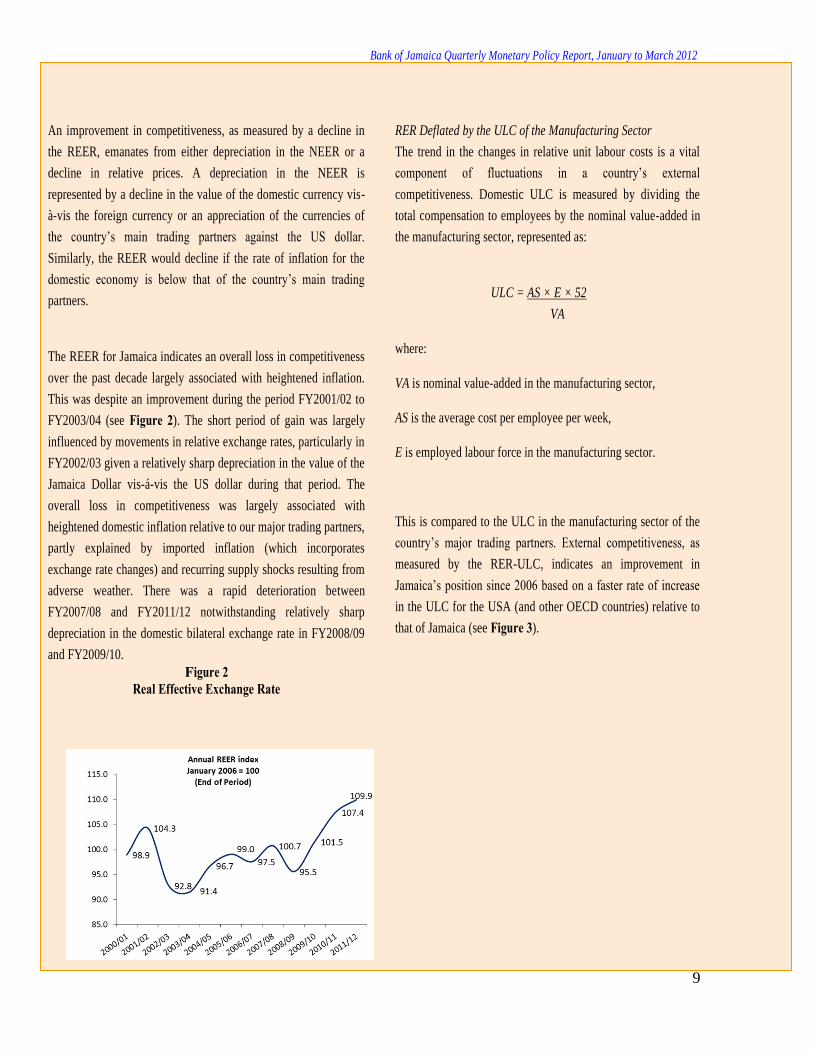

The REER for Jamaica indicates an overall loss in competitiveness

over the past decade largely associated with heightened inflation.

This was despite an improvement during the period FY2001/02 to

FY2003/04 (see Figure 2). The short period of gain was largely

influenced by movements in relative exchange rates, particularly in

FY2002/03 given a relatively sharp depreciation in the value of the

Jamaica Dollar vis-á-vis the US dollar during that period. The

overall loss in competitiveness was largely associated with

heightened domestic inflation relative to our major trading partners,

partly explained by imported inflation (which incorporates

exchange rate changes) and recurring supply shocks resulting from

adverse weather. There was a rapid deterioration between

FY2007/08 and FY2011/12 notwithstanding relatively sharp

depreciation in the domestic bilateral exchange rate in FY2008/09

and FY2009/10.

Figure 2 Real Effective Exchange Rate

RER Deflated by the ULC of the Manufacturing Sector

The trend in the changes in relative unit labour costs is a vital

component of fluctuations in a country’s external

competitiveness. Domestic ULC is measured by dividing the

total compensation to employees by the nominal value-added in

the manufacturing sector, represented as:

ULC = AS × E × 52

VA

where:

VA is nominal value-added in the manufacturing sector,

AS is the average cost per employee per week,

E is employed labour force in the manufacturing sector.

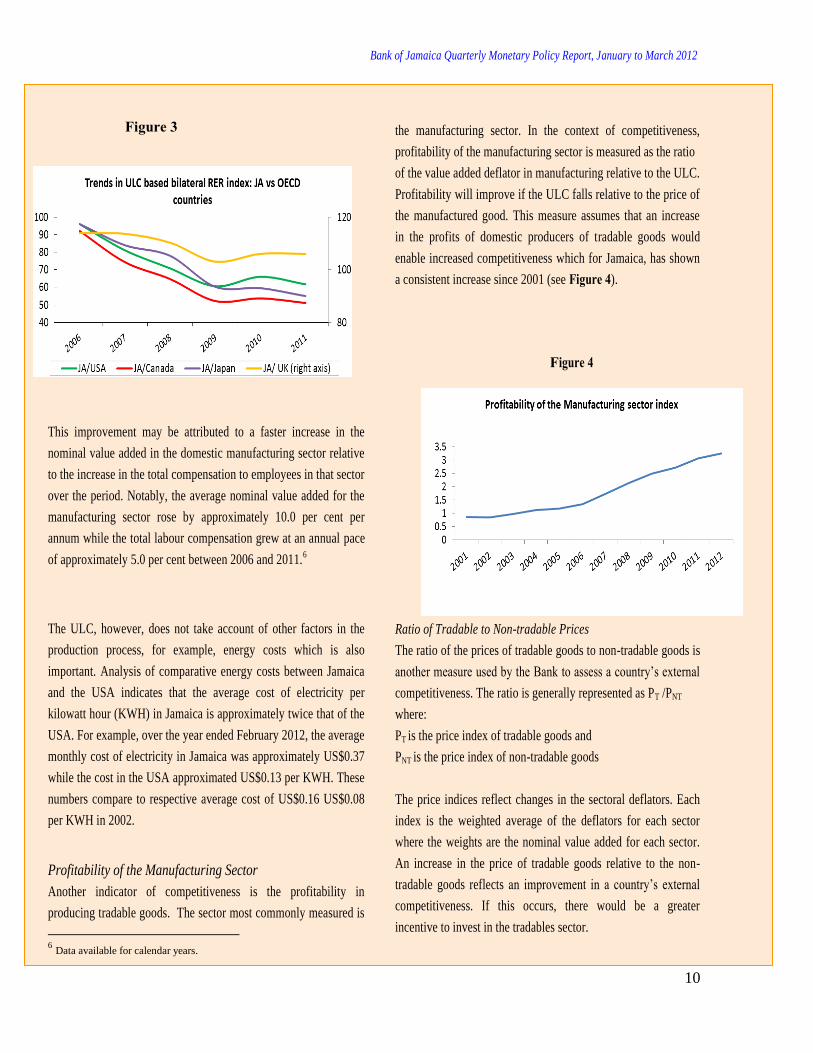

This is compared to the ULC in the manufacturing sector of the

country’s major trading partners. External competitiveness, as

measured by the RER-ULC, indicates an improvement in

Jamaica’s position since 2006 based on a faster rate of increase

in the ULC for the USA (and other OECD countries) relative to

that of Jamaica (see Figure 3).

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

10

Figure 3

This improvement may be attributed to a faster increase in the

nominal value added in the domestic manufacturing sector relative

to the increase in the total compensation to employees in that sector

over the period. Notably, the average nominal value added for the

manufacturing sector rose by approximately 10.0 per cent per

annum while the total labour compensation grew at an annual pace

of approximately 5.0 per cent between 2006 and 2011.6

The ULC, however, does not take account of other factors in the

production process, for example, energy costs which is also

important. Analysis of comparative energy costs between Jamaica

and the USA indicates that the average cost of electricity per

kilowatt hour (KWH) in Jamaica is approximately twice that of the

USA. For example, over the year ended February 2012, the average

monthly cost of electricity in Jamaica was approximately US$0.37

while the cost in the USA approximated US$0.13 per KWH. These

numbers compare to respective average cost of US$0.16 US$0.08

per KWH in 2002.

Profitability of the Manufacturing Sector

Another indicator of competitiveness is the profitability in

producing tradable goods. The sector most commonly measured is

6 Data available for calendar years.

the manufacturing sector. In the context of competitiveness,

profitability of the manufacturing sector is measured as the ratio

of the value added deflator in manufacturing relative to the ULC.

Profitability will improve if the ULC falls relative to the price of

the manufactured good. This measure assumes that an increase

in the profits of domestic producers of tradable goods would

enable increased competitiveness which for Jamaica, has shown

a consistent increase since 2001 (see Figure 4).

Figure 4

Ratio of Tradable to Non-tradable Prices

The ratio of the prices of tradable goods to non-tradable goods is

another measure used by the Bank to assess a country’s external

competitiveness. The ratio is generally represented as PT /PNT

where:

PT is the price index of tradable goods and

PNT is the price index of non-tradable goods

The price indices reflect changes in the sectoral deflators. Each

index is the weighted average of the deflators for each sector

where the weights are the nominal value added for each sector.

An increase in the price of tradable goods relative to the non-

tradable goods reflects an improvement in a country’s external

competitiveness. If this occurs, there would be a greater

incentive to invest in the tradables sector.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

11

For Jamaica, the Bank defines tradable goods to include export

agriculture, products generated from mining and quarrying

activities and manufactured goods such as textiles, while non-

tradable goods consist of construction and services (excluding

hotels). Since 2001, the price index for non-tradables has increased

at a faster pace resulting in a downward trend in the ratio (see

Figure 5). This suggests that Jamaica has lost competitiveness over

the review period.

Figure 5

External Non-price Competitiveness

Price measures alone are not sufficient in assessing a country’s

competitiveness. Non-price measures which include factors such as

technological capabilities, the quality of the country’s

infrastructure, the ease of doing business and social issues such as

crime also affect competitiveness. Hence, in addition to the price

measures cited above, the Bank also monitors some non-price

measures. Chief among them are the measures cited in the World

Economic Forum’s (WEF) Global Competitiveness Report and the

World Bank’s Doing Business Report.

WEF Global Competitiveness Report 2011-2012

The WEF computes a global competitiveness index (GCI) as

a weighted average of twelve pillars of competitiveness for

each country including, inter alia, institutions, infrastructure,

macroeconomic environment, health and primary education,

labour market efficiency and innovation. The GCI uses

over 110 indicators to assess and categorize a country's

competitiveness using data from public and private

sources. The data is then normalized for each indicator in

all countries to generate a grade using a scale. The grade in

individual indicators is then added for each country which

is in turn divided by the number of indicators. This results

in an average grade for all indicators which represents the

country's competitiveness index.

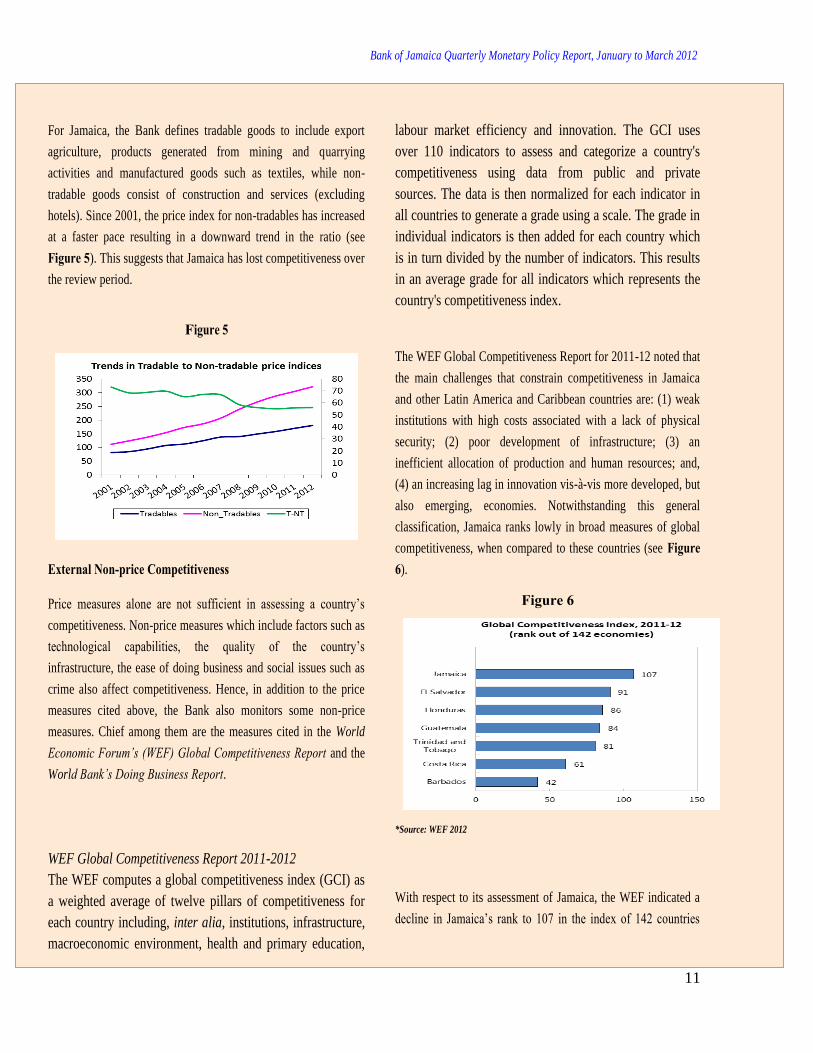

The WEF Global Competitiveness Report for 2011-12 noted that

the main challenges that constrain competitiveness in Jamaica

and other Latin America and Caribbean countries are: (1) weak

institutions with high costs associated with a lack of physical

security; (2) poor development of infrastructure; (3) an

inefficient allocation of production and human resources; and,

(4) an increasing lag in innovation vis-à-vis more developed, but

also emerging, economies. Notwithstanding this general

classification, Jamaica ranks lowly in broad measures of global

competitiveness, when compared to these countries (see Figure 6).

Figure 6

*Source: WEF 2012

With respect to its assessment of Jamaica, the WEF indicated a

decline in Jamaica’s rank to 107 in the index of 142 countries

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

12

relative to 95 out of the 139 countries in the 2010 survey.7

Analysis of previous years shows that for a number of indicators,

the ranking was partly influenced by a lower score. For example in

2008, Jamaica scored 3.6 in innovation. However, this score was

reduced to 3.4 by 2011. There were also a few indicators, for

example infrastructure, in which Jamaica gained a higher score but

received a lower rank.

For 2011, the decline in Jamaica’s ranking was primarily evidenced

in the Basic Requirement Pillar, representing a fall in Jamaica’s

rank to 116 from 103. With respect to the basic requirement index,

all the component rankings deteriorated. In this regard, Jamaica’s

ranking for the level of development of its infrastructure

deteriorated from a ranking of 65 to 79 in the 2011-12 report. The

country’s rankings in terms of the quality of roads, available airline

seats, fixed telephone lines and mobile telephone subscriptions all

deteriorated. There was also some deterioration in the Efficiency

Enhancer Index largely due to reduced rankings for financial

market development and technological readiness. The lower

ranking for financial market development was largely associated

with a downgrade of Jamaica’s status in relation to the availability

of venture capital while that for technological readiness reflected a

lower ranking for internet penetration. The most significant

deterrent to doing business in Jamaica continued to be crime and

theft, which deteriorated further relative to 2010-2011 (see

Figure 7).

Figure 7

*Source: World Bank 2012

7 In 2002, Jamaica was ranked 60th among a total of 80 countries.

World Bank Doing Business Report – 2012

The World Bank Doing Business Report for 2012 also

highlighted some major obstacles to doing business in Jamaica,

relative to the rest of the world. Chief among them were paying

taxes, enforcing contracts and registering property (See Figure 8). These factors mainly contributed to an overall ranking of 88

for Jamaica compared to a previous ranking of 85 for 2011 and

43 in 20068.

Figure 8

**Source: World Bank 2012

Summary and Policy Issues Most measures of competitiveness monitored by the BOJ

indicate that Jamaica has lost competitiveness over the past

decade. This loss in competitiveness can be addressed through

adjusting relative prices and the structural issues impeding

competitiveness. In this regard, any attempt to reverse this loss

in competitiveness through a reliance on relative price

adjustments alone would be insufficient.

With respect to relative prices, one avenue to regain

competitiveness is through a relatively sharp depreciation of the

8 The 2006 report reflects the least recent comparative ranking for each

country out of 155 countries.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

13

exchange rate which would have to significantly outweigh relative

price increases. However, this mechanism is dependent on the

extent of the pass through of exchange rate changes to domestic

inflation and the impact of the depreciation on the import cost in

the production process.9 In addition, elasticity estimates for

Jamaica show that the responsiveness of imports and exports to

exchange rate changes is generally low.10

In this regard, a sharp

depreciation of the exchange rate may not generate the required

response. Moreover, the exchange rate has traditionally served as

an important anchor to inflation expectations in Jamaica.

Given the impact of adverse weather on inflation, further measures

should be put in place to reduce the country’s vulnerability to these

types of shocks. A continuation of the drive towards cheaper and

more reliable sources of energy would also contribute to lower

inflation and an improvement in competitiveness.

Jamaica should also aim at improving the non-price measures and

structural problems that challenge or constrain competitiveness, as

cited by the World Bank Doing Business and the WEF Global

Competitiveness Reports. In doing so, Jamaica could likely see

significant improvement in its macroeconomic indicators, including

economic growth and the current account deficit.

9 McFarlene (2002) estimated that 80.0 per cent of the exchange rate

depreciation in the pre-1995 period was passed through within six

months. The BOJ estimates that this has now slowed to around 50 per cent. 10

See Henry, C. and Longmore, R., (2003) “Current Account Dynamics

and the Real Effective Exchange Rate: The Jamaican Experience.” Bank

of Jamaica Working Paper.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 14

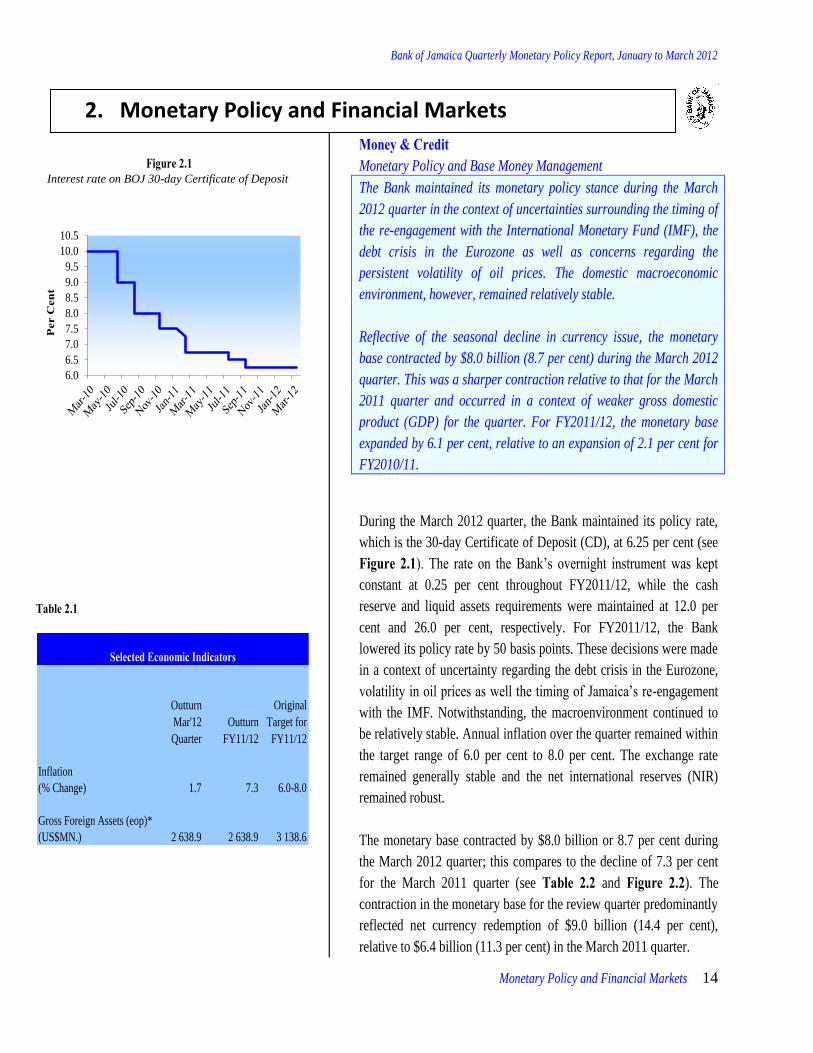

Figure 2.1 Interest rate on BOJ 30-day Certificate of Deposit

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

Per

Cen

t

Table 2.1

Outturn

Mar'12

Quarter

Outturn

FY11/12

Original

Target for

FY11/12

Inflation

(% Change) 1.7 7.3 6.0-8.0

Gross Foreign Assets (eop)*

(US$MN.) 2 638.9 2 638.9 3 138.6

Selected Economic Indicators

Money & Credit Monetary Policy and Base Money Management

The Bank maintained its monetary policy stance during the March

2012 quarter in the context of uncertainties surrounding the timing of

the re-engagement with the International Monetary Fund (IMF), the

debt crisis in the Eurozone as well as concerns regarding the

persistent volatility of oil prices. The domestic macroeconomic

environment, however, remained relatively stable.

Reflective of the seasonal decline in currency issue, the monetary

base contracted by $8.0 billion (8.7 per cent) during the March 2012

quarter. This was a sharper contraction relative to that for the March

2011 quarter and occurred in a context of weaker gross domestic

product (GDP) for the quarter. For FY2011/12, the monetary base

expanded by 6.1 per cent, relative to an expansion of 2.1 per cent for

FY2010/11.

During the March 2012 quarter, the Bank maintained its policy rate,

which is the 30-day Certificate of Deposit (CD), at 6.25 per cent (see

Figure 2.1). The rate on the Bank’s overnight instrument was kept

constant at 0.25 per cent throughout FY2011/12, while the cash

reserve and liquid assets requirements were maintained at 12.0 per

cent and 26.0 per cent, respectively. For FY2011/12, the Bank

lowered its policy rate by 50 basis points. These decisions were made

in a context of uncertainty regarding the debt crisis in the Eurozone,

volatility in oil prices as well the timing of Jamaica’s re-engagement

with the IMF. Notwithstanding, the macroenvironment continued to

be relatively stable. Annual inflation over the quarter remained within

the target range of 6.0 per cent to 8.0 per cent. The exchange rate

remained generally stable and the net international reserves (NIR)

remained robust.

The monetary base contracted by $8.0 billion or 8.7 per cent during

the March 2012 quarter; this compares to the decline of 7.3 per cent

for the March 2011 quarter (see Table 2.2 and Figure 2.2). The

contraction in the monetary base for the review quarter predominantly

reflected net currency redemption of $9.0 billion (14.4 per cent),

relative to $6.4 billion (11.3 per cent) in the March 2011 quarter.

2. Monetary Policy and Financial Markets

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 15

Figure 2.2 Base Money

(Quarterly Change)

Figure 2.3 Effects of the NIR, GOJ & OMO on Liquidity*

* Absorption – negative; Injection – positive

Table 2.2

*The original target for the NIR was US$1 800.7 million for

FY2011/12.

An increase of $1.0 billion in commercial banks’ cash reserves

partially offset the impact of the contraction in currency on the

monetary base. The sharp fall in currency was consistent with an

estimated deceleration in economic activity for the review quarter.

The contraction in the monetary base was largely influenced by a

decline of $16.9 billion (US$189.0 million) in the NIR, which was

partly offset by an increase of $8.9 billion in the net domestic assets

(NDA) (see Figure 2.3). For the NIR, the decline mainly reflected

intervention sales to the market as well as debt payments on behalf of

the Central Government. Within the NDA, there was net drawdown of

$20.5 billion in Central Government deposits, reflective of debt

payments, particularly in February. This liquidity impact was partially

offset by net placements of $12.7 billion on open market operation

(OMO) instruments.

For FY2011/12, the monetary base expanded by $4.8 billion (6.1 per

cent) relative to an expansion of 2.1 per cent for FY2010/11. This

growth largely reflected net currency issue of $3.3 billion (6.6 per

cent) as well as an increase of $2.4 billion (8.6 per cent) in

commercial banks’ cash reserves. The impact of these transactions

was partially offset by a decline of $920.1 million in commercial

banks’ current account. The main sources of the expansion in the

monetary base were net drawdown of $37.3 billion in Central

Government deposits at the Bank and net unwinding of $32.1 billion

in OMO securities. There was, however, a decline of $69.3 billion

(US$776.0 million) in the NIR.

Outturn

Dec'11

Quarter

Outturn

Mar'12

Quarter

%

Change

Net International Reserves 1 966.1 1 777.1 -9.6

(US$ MN.)

Net Domestic Assets

(J$MN.) -83 961.8 -75 089.9 10.6

Monetary Base

(J$MN.) 91 710.1 83 696.7 -8.7

Base Money Indicators

-20000

-10000

0

10000

20000

30000

J$ M

illio

n

NIR OMO GOJ

-15.0

-5.0

5.0

15.0

25.0

Mar-08 Mar-09 Mar-10 Mar-11 Mar-12

Per

cen

t

Quarter

Unadjusted Seasonally adjusted

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 16

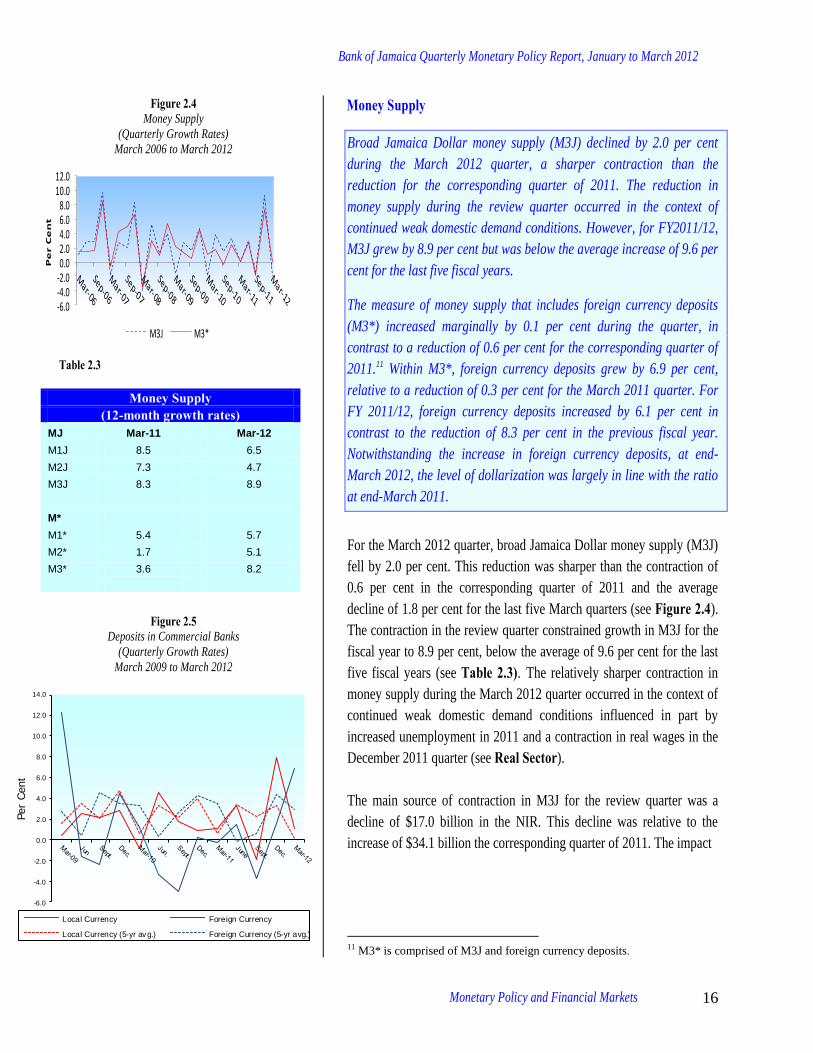

Figure 2.4 Money Supply

(Quarterly Growth Rates)

March 2006 to March 2012

-6.0-4.0-2.00.02.04.06.08.0

10.012.0

Pe

r C

en

t

M3J M3*

Table 2.3

Figure 2.5 Deposits in Commercial Banks

(Quarterly Growth Rates)

March 2009 to March 2012

Money Supply

Broad Jamaica Dollar money supply (M3J) declined by 2.0 per cent

during the March 2012 quarter, a sharper contraction than the

reduction for the corresponding quarter of 2011. The reduction in

money supply during the review quarter occurred in the context of

continued weak domestic demand conditions. However, for FY2011/12,

M3J grew by 8.9 per cent but was below the average increase of 9.6 per

cent for the last five fiscal years.

The measure of money supply that includes foreign currency deposits

(M3*) increased marginally by 0.1 per cent during the quarter, in

contrast to a reduction of 0.6 per cent for the corresponding quarter of

2011.11 Within M3*, foreign currency deposits grew by 6.9 per cent,

relative to a reduction of 0.3 per cent for the March 2011 quarter. For

FY 2011/12, foreign currency deposits increased by 6.1 per cent in

contrast to the reduction of 8.3 per cent in the previous fiscal year.

Notwithstanding the increase in foreign currency deposits, at end-

March 2012, the level of dollarization was largely in line with the ratio

at end-March 2011.

For the March 2012 quarter, broad Jamaica Dollar money supply (M3J)

fell by 2.0 per cent. This reduction was sharper than the contraction of

0.6 per cent in the corresponding quarter of 2011 and the average

decline of 1.8 per cent for the last five March quarters (see Figure 2.4).

The contraction in the review quarter constrained growth in M3J for the

fiscal year to 8.9 per cent, below the average of 9.6 per cent for the last

five fiscal years (see Table 2.3). The relatively sharper contraction in

money supply during the March 2012 quarter occurred in the context of

continued weak domestic demand conditions influenced in part by

increased unemployment in 2011 and a contraction in real wages in the

December 2011 quarter (see Real Sector).

The main source of contraction in M3J for the review quarter was a

decline of $17.0 billion in the NIR. This decline was relative to the

increase of $34.1 billion the corresponding quarter of 2011. The impact

11 M3* is comprised of M3J and foreign currency deposits.

Money Supply (12-month growth rates)

MJ Mar-11 Mar-12

M1J 8.5 6.5

M2J 7.3 4.7

M3J 8.3 8.9

M*

M1* 5.4 5.7

M2* 1.7 5.1

M3* 3.6 8.2

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Per

Cent

Local Currency Foreign Currency

Local Currency (5-yr avg.) Foreign Currency (5-yr avg.)

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 17

Table 2.4

Mar-11 Mar-12

Local Currency Deposits 1.2 -0.5

Demand deposits -1.3 -5.9

Savings deposits 0.3 0.3

Time deposits 3.3 -0.9

Other Deposits 2.9 1.6

Local Currency DepositsQuarterly Growth ( % )

Figure 2.6 Foreign Currency Deposits to Total Deposits

March 2009 to March 2012

Table 2.5

of the reduction in the NIR during the review quarter was

complemented by net placements on BOJ Certificates of Deposit (CDs)

of $12.7 billion, (12.8 per cent) relative to net placements of $14.5

billion (11.2 per cent) in the March 2011 quarter (see Base Money Management). There was a partially offsetting impact from growth of

3.0 per cent in private sector credit, continuing the trend since the start

of 2011.

The reduction in the money supply during the review quarter was

reflected in respective declines of 10.2 per cent and 0.5 per cent, in

currency in circulation and local currency deposits. The fall in currency

in circulation reflected the seasonal net redemptions following the

Christmas holidays. This net redemption was broadly in line with the

contraction of 10.4 per cent in the corresponding quarter of 2011 but

lower than the average decline of 12.6 per cent for the last five March

quarters. For FY 2011/12, growth in currency in circulation was 9.3 per

cent, above the expansion of 7.1 per cent for FY 2010/11. In real terms,

there was an increase of 1.9 per cent in currency in circulation for the

FY 2011/12 in contrast to the decline of 0.7 per cent for the previous

fiscal year. The real increase in currency may be attributed to the

nascent recovery in real economic activity during the last four quarters

(see Real Sector).

The decline in local currency deposits during the review quarter was in

contrast to the increase of 1.2 per cent in the corresponding quarter of

2011 and the average growth of 0.1 per cent for the last five March

quarters. The reduction in local currency deposits was reflected in

demand and time deposits (see Table 2.4). For FY2011/12, local

currency deposits grew by 8.8 per cent, relative to 8.5 per cent for the

previous fiscal year, largely buoyed by a significant increase in other

deposits.

During the review quarter, M3* grew marginally by 0.1 per cent, in

contrast to a reduction of 0.6 per cent for the March 2011 quarter (see

Figure 2.4). Within M3*, foreign currency deposits increased by 6.9 per

cent, following growth of 1.6 per cent in the December 2011 quarter.

This increase was consistent with the uncertainties which usually

surround a general election as well as the on-going discussions with the

IMF. The growth in foreign currency deposits during the review

20.0

22.0

24.0

26.0

28.0

30.0

32.0

34.0

Per

cent

Mar-11 Dec-11 Mar-12

Currency to Deposits (%) 15.70 17.47 15.77

Reserves to Deposits (%) 12.85 12.84 12.05

Money Multiplier 4.05 3.87 4.16

COMPONENTS OF THE MONEY MULTIPLIER (M3J)

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 18

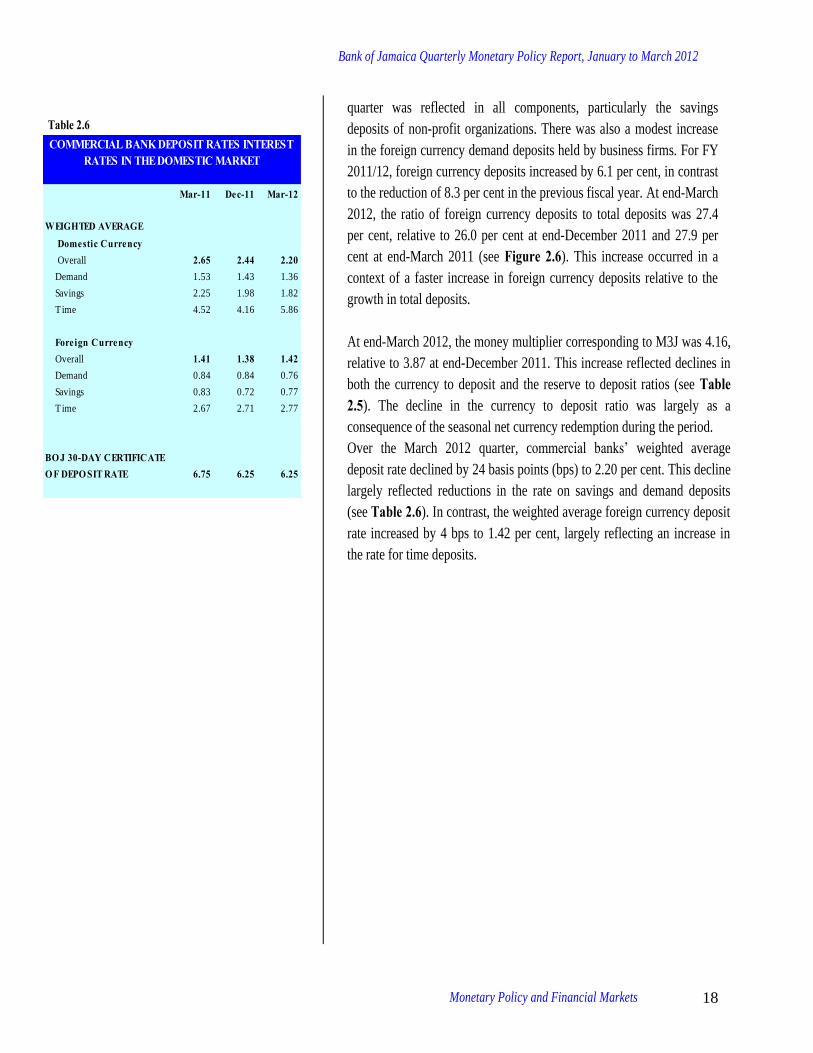

Table 2.6

quarter was reflected in all components, particularly the savings

deposits of non-profit organizations. There was also a modest increase

in the foreign currency demand deposits held by business firms. For FY

2011/12, foreign currency deposits increased by 6.1 per cent, in contrast

to the reduction of 8.3 per cent in the previous fiscal year. At end-March

2012, the ratio of foreign currency deposits to total deposits was 27.4

per cent, relative to 26.0 per cent at end-December 2011 and 27.9 per

cent at end-March 2011 (see Figure 2.6). This increase occurred in a

context of a faster increase in foreign currency deposits relative to the

growth in total deposits.

At end-March 2012, the money multiplier corresponding to M3J was 4.16,

relative to 3.87 at end-December 2011. This increase reflected declines in

both the currency to deposit and the reserve to deposit ratios (see Table 2.5). The decline in the currency to deposit ratio was largely as a

consequence of the seasonal net currency redemption during the period.

Over the March 2012 quarter, commercial banks’ weighted average

deposit rate declined by 24 basis points (bps) to 2.20 per cent. This decline

largely reflected reductions in the rate on savings and demand deposits

(see Table 2.6). In contrast, the weighted average foreign currency deposit

rate increased by 4 bps to 1.42 per cent, largely reflecting an increase in

the rate for time deposits.

Mar-11 Dec-11 Mar-12

WEIGHTED AVERAGE Domestic Currency Overall 2.65 2.44 2.20

Demand 1.53 1.43 1.36

Savings 2.25 1.98 1.82

Time 4.52 4.16 5.86

Foreign Currency Overall 1.41 1.38 1.42Demand 0.84 0.84 0.76

Savings 0.83 0.72 0.77

Time 2.67 2.71 2.77

BO J 30-DAY CERTIFICATEO F DEPO SIT RATE 6.75 6.25 6.25

COMMERCIAL BANK DEPOSIT RATES INTEREST RATES IN THE DOMESTIC MARKET

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 19

Mar-11 Dec-11 Mar-12

Business Lending -767.1 9 021.6 5 189.3Agriculture & Fishing -99.0 456.2 972.5

Mining & Quarrying 5.4 101.5 -74.3

Manufacturing 180.7 -21.4 595.0

Construction & Land Dev. -1 972.8 1 263.1 1 508.5

Transport, Storage & Comm. -75.3 2 815.8 -493.8

Tourism -551.0 -104.5 -1 565.8

Distribution 99.2 3 522.0 4 523.3

Professional & Other Services 240.0 897.0 -963.1

Electricity, Gas & Water 1 435.7 61.8 626.0

Entertainment -29.9 30.0 60.9

Personal & Other Lending 813.6 4 904.6 4 059.7Personal 829.2 4 917.1 4 279.4

Overseas Residents -15.7 -12.4 -219.7

Net Lending/(Repayment) 46.4 13 926.2 9 249.0

Commercial Bank Distribution of Total Loans & Advances to the Private Sector

(Quarterly Flows J$MN)

Figure 2.7 Quarterly Growth Rates of Private Sector Credit

March 2005 to March 2012

Table 2.7

Mar-11 Dec-11 Mar-12

Total Private Sector Credit 62.9 13 944.6 9 419.4Change (%) 0.03 6.2 3.9

of which

Loans and Advances 46.4 13 926.2 9 249.0

Domestic residents 62.1 13 938.7 9 468.7

Overseas residents -15.7 -12.4 -219.7

Corporate Securities 0.8 6.0 -49.3

Commercial Bank Distribution of Total Credit to the Private Sector

(Flows J$MN)

Table 2.8

Private Sector Credit

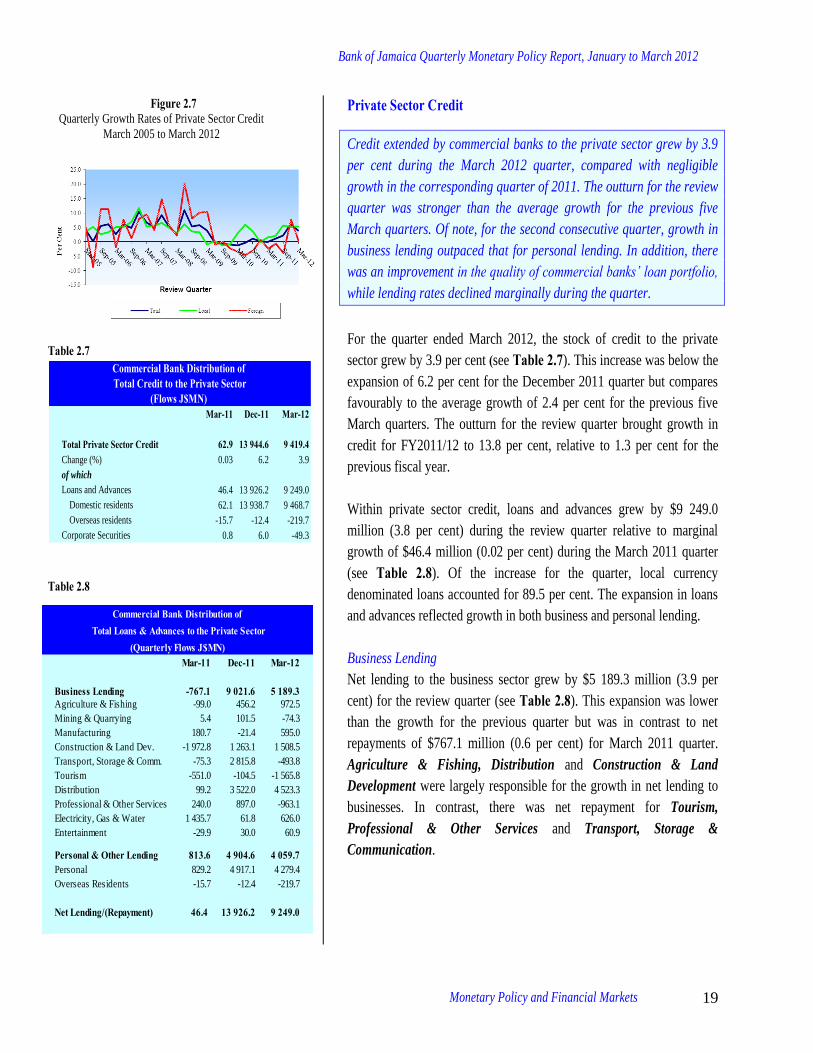

Credit extended by commercial banks to the private sector grew by 3.9

per cent during the March 2012 quarter, compared with negligible

growth in the corresponding quarter of 2011. The outturn for the review

quarter was stronger than the average growth for the previous five

March quarters. Of note, for the second consecutive quarter, growth in

business lending outpaced that for personal lending. In addition, there

was an improvement in the quality of commercial banks’ loan portfolio,

while lending rates declined marginally during the quarter.

For the quarter ended March 2012, the stock of credit to the private

sector grew by 3.9 per cent (see Table 2.7). This increase was below the

expansion of 6.2 per cent for the December 2011 quarter but compares

favourably to the average growth of 2.4 per cent for the previous five

March quarters. The outturn for the review quarter brought growth in

credit for FY2011/12 to 13.8 per cent, relative to 1.3 per cent for the

previous fiscal year.

Within private sector credit, loans and advances grew by $9 249.0

million (3.8 per cent) during the review quarter relative to marginal

growth of $46.4 million (0.02 per cent) during the March 2011 quarter

(see Table 2.8). Of the increase for the quarter, local currency

denominated loans accounted for 89.5 per cent. The expansion in loans

and advances reflected growth in both business and personal lending.

Business Lending

Net lending to the business sector grew by $5 189.3 million (3.9 per

cent) for the review quarter (see Table 2.8). This expansion was lower

than the growth for the previous quarter but was in contrast to net

repayments of $767.1 million (0.6 per cent) for March 2011 quarter.

Agriculture & Fishing, Distribution and Construction & Land

Development were largely responsible for the growth in net lending to

businesses. In contrast, there was net repayment for Tourism,

Professional & Other Services and Transport, Storage &

Communication.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 20

Table 2.9

Table 2.10

The expansion in Distribution was largely denominated in foreign

currency and represented a syndicated facility to a group for loan re-

financing and the provision of working capital (see Tables 2.9 and 2.10). The growth in Agriculture & Fishing is consistent with the

outlook for the real sector (see Economic Outlook and Monetary Policy Perspectives).

Personal and Other Lending

Personal loans expanded by $4 279.4 million (4.2 per cent) during the

review quarter, continuing the pattern of strong growth observed since

the June 2011 quarter (see Table 2.8). The expansion in the review

quarter was reflected in local currency denominated loans.

Within personal loans, term loans expanded by $2 660.6 million (8.4 per

cent), a continuation of the significant growth observed since June 2009

quarter. Instalment credit, another component of personal loans,

increased by $748.0 million (2.2 per cent) during the March 2012

quarter, approximately the same rate of growth realised in the March

2011 quarter. This increase was largely reflected in loans for motor cars

and debt consolidation, which grew by 4.8 per cent and 1.4 per cent,

respectively (see Table 2.11). Consistent with the growth in loans for

debt consolidation, growth in commercial banks’ credit card receivables

remained flat.

Interest Rates

The weighted average interest rate on commercial bank loans reflected

further reduction in sectoral lending rates during the March 2012

quarter. In particular, the weighted average rate on public sector loans

declined by 13 basis points (bps), while the equivalent rate on private

sector loans declined by 35 bps. These movements facilitated a decline

in the overall weighted average rate by 33 bps to 17.70 per cent (see

Table 2.12).

The decline in the weighted average lending rate on private sector loans

for the review quarter was reflected in all categories. The largest

decline of 58 bps was observed in the weighted average rate on

commercial loans, which has been falling consistently since the March

2011 quarter. There was also a notable decline in the weighted average

interest rate on mortgage financing, which followed a much sharper

reduction during the previous quarter. The continuous declines in

mortgage rates may be attributed to increased competition among

Mar-11 Dec-11 Mar-12Business Lending 876.0 2 779.1 3 703.9Agriculture & Fishing 344.9 364.7 855.6

Mining & Quarrying 7.7 110.8 -82.9

Manufacturing 118.1 -364.4 1 179.4

Construction & Land Dev. 292.4 -147.4 1 107.4

Transport, Storage & Comm. 89.1 -81.2 -452.0

Tourism 55.4 148.4 -309.3

Distribution 232.0 1 845.8 1 480.6

Professional & Other Services -234.4 707.2 -492.4

Electricity, Gas & Water 31.1 150.8 445.3

Entertainment -60.3 44.5 -27.8

Personal & Other Lending 1 274.2 4 686.4 4 573.5Personal 1 297.1 4 713.3 4 595.1

Overseas Residents -22.8 -26.9 -21.6

Net Lending/(Repayment) 2 150.2 7 465.5 8 277.4

Commercial Bank Distribution of Local Currency Loans & Advances to the Private Sector

(Quarterly Flows J$MN)

Mar-11 Dec-11 Mar-12Business Lending -18.3 69.8 10.1Agriculture & Fishing -5.2 1.0 1.2

Mining & Quarrying 0.0 -0.1 0.1

Manufacturing 0.8 3.9 -6.9

Construction & Land Development -26.3 15.9 3.2

Transport, Storage & Comm. -1.9 33.4 -1.1

Tourism -6.7 -4.0 -17.1

Distribution -1.4 19.1 34.1

Electricity, Gas & Water 16.5 -1.2 1.6

Entertainment 0.4 -0.2 1.0

Professional & Other Services 5.6 2.0 -6.0

Persoanl & Other Lending -5.2 2.0 -7.1Personal -5.4 2.1 -4.2

Overseas Residents 0.2 -0.1 -2.9

Total Net Lending/(Repayment) Flows -23.5 71.8 2.9

Commercial Bank Distribution of Foreign Currency Loans & Advances to the

Private Sector (Quarterly Flows US$MN)

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 21

Table 2.11

Table 2.12

2011 2012Mar Jun Sep Dec Mar

Overall 20.52 20.10 18.34 18.03 17.70

Public Sector 11.58 10.13 10.40 9.98 9.85 Local Govt. & Other

Public Entities 12.94 10.17 11.14 10.61 9.95

Central Government 11.00 10.12 10.12 9.77 9.80

Private Sector 20.97 20.54 18.65 18.31 17.96 Instalment 20.63 20.20 19.56 19.20 18.92

Mortgage 15.83 15.05 13.40 12.36 12.20

Personal 25.70 25.48 21.73 21.66 21.57

Commercial 16.63 15.91 15.12 14.63 14.05

Commercial BankDomestic Currency Average Weighted

Lending Rates by Loan Type(Per Cent)

Figure 2.8

Commercial Bank Past due Loans

(Three Months and over) to Total Loans

March 2010 to March 2012

building societies in the context of recent policy initiatives to spur

growth.12

The decline in the weighted average lending rate to the public sector for

the review quarter reflected a decline of 66 bps in the average lending

rate to Local Government & Other Public Sector entities. However, the

average lending rate to Central Government increased by 3 bps.

Loan Quality

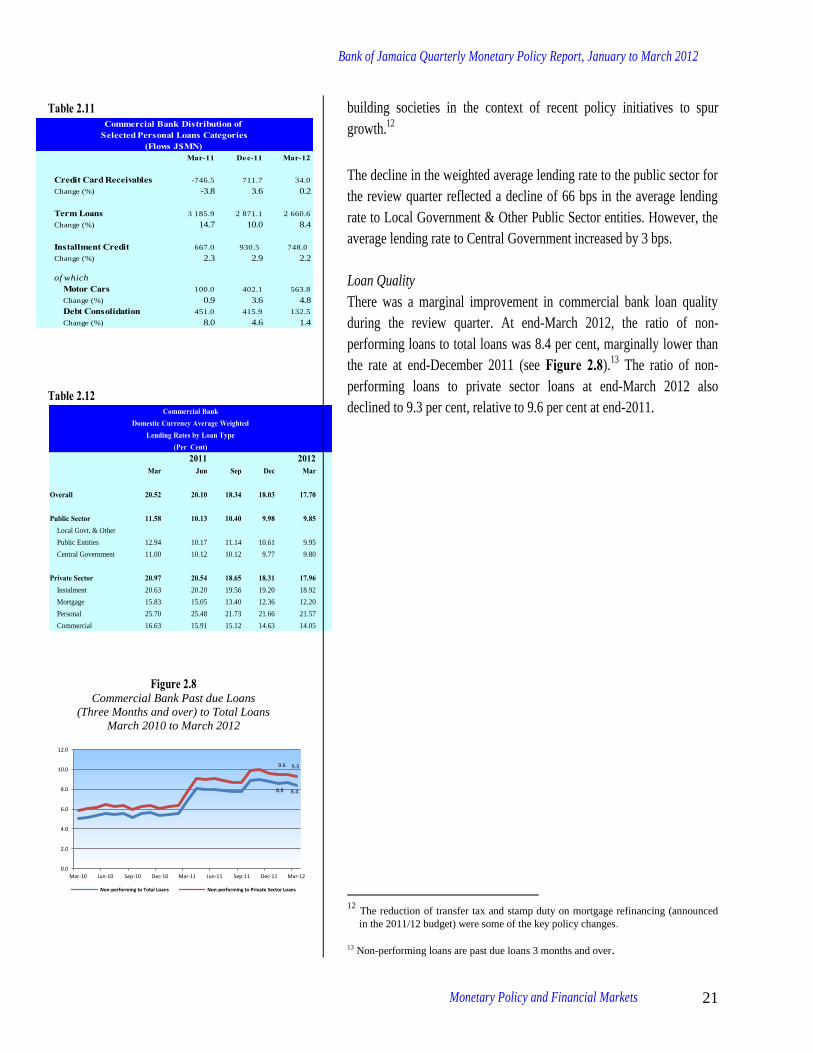

There was a marginal improvement in commercial bank loan quality

during the review quarter. At end-March 2012, the ratio of non-

performing loans to total loans was 8.4 per cent, marginally lower than

the rate at end-December 2011 (see Figure 2.8).13

The ratio of non-

performing loans to private sector loans at end-March 2012 also

declined to 9.3 per cent, relative to 9.6 per cent at end-2011.

12

The reduction of transfer tax and stamp duty on mortgage refinancing (announced

in the 2011/12 budget) were some of the key policy changes.

13 Non-performing loans are past due loans 3 months and over.

8.8 8.4

9.6 9.3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12

Non-performing to Total Loans Non-performing to Private Sector Loans

Mar-11 Dec-11 Mar-12

Credit Card Receivables -746.5 711.7 34.0

Change (%) -3.8 3.6 0.2

Term Loans 3 185.9 2 871.1 2 660.6

Change (%) 14.7 10.0 8.4

Installment Credit 667.0 930.5 748.0

Change (%) 2.3 2.9 2.2

of which

Motor Cars 100.0 402.1 563.8

Change (%) 0.9 3.6 4.8

Debt Consolidation 451.0 415.9 132.5

Change (%) 8.0 4.6 1.4

Commercial Bank Distribution of Selected Personal Loans Categories

(Flows J$MN)

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 22

Table 2.13

Issue Date Tenor Avg. yield Amount AmountAllotted Maturing

(days) (%) (J$MN) (J$MN)

14-Dec-11 28 6.49 400.0 400.0

23-Dec-11 91 6.21 400.0 400.0

23-Dec-11 182 6.46 400.0 400.0

18-Jan-12 28 6.41 400.0 400.0

25-Jan-12 91 6.22 400.0 400.0

25-Jan-12 182 6.53 400.0 400.0

15-Feb-12 28 6.36 400.0 400.0

15-Feb-12 91 6.21 400.0 400.0

15-Feb-12 182 6.57 400.0 400.0

21-Mar-12 28 6.24 400.0 400.0

21-Mar-12 91 6.27 400.0 400.0

21-Mar-12 182 6.47 400.0 400.0

Treasury Bill Auctions and MaturitiesDecember 2011 - March 2012

Bond Market

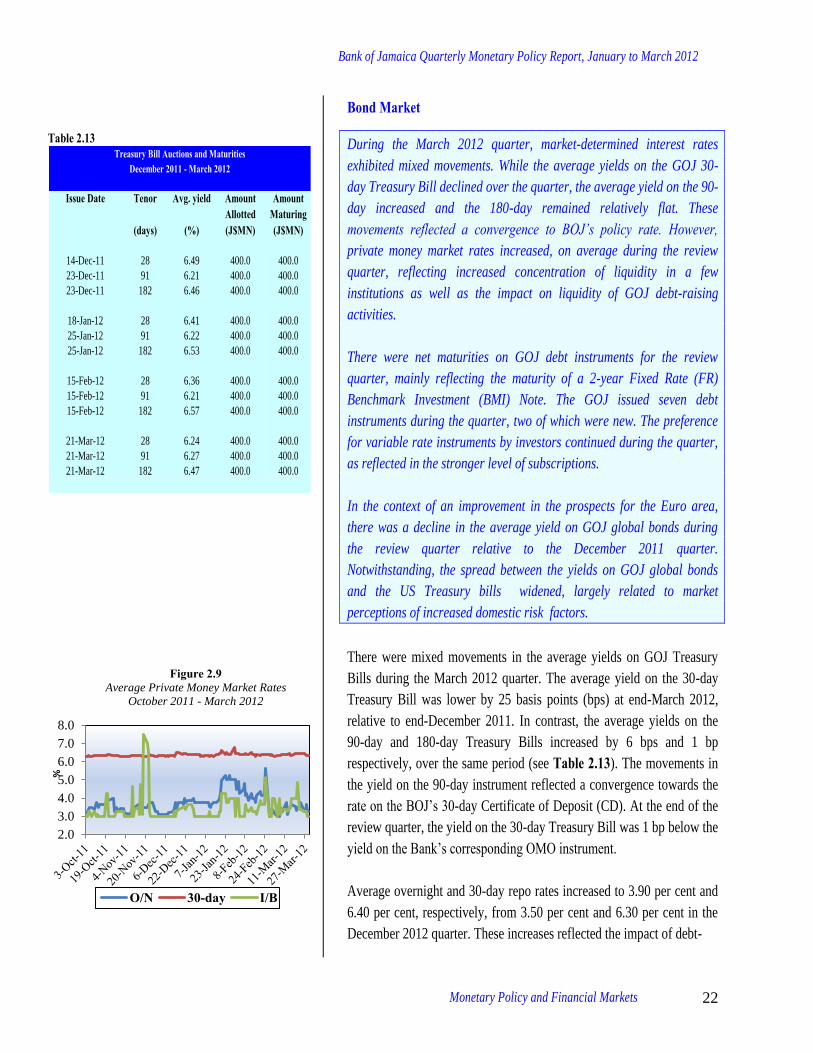

During the March 2012 quarter, market-determined interest rates

exhibited mixed movements. While the average yields on the GOJ 30-

day Treasury Bill declined over the quarter, the average yield on the 90-

day increased and the 180-day remained relatively flat. These

movements reflected a convergence to BOJ’s policy rate. However,

private money market rates increased, on average during the review

quarter, reflecting increased concentration of liquidity in a few

institutions as well as the impact on liquidity of GOJ debt-raising

activities.

There were net maturities on GOJ debt instruments for the review

quarter, mainly reflecting the maturity of a 2-year Fixed Rate (FR)

Benchmark Investment (BMI) Note. The GOJ issued seven debt

instruments during the quarter, two of which were new. The preference

for variable rate instruments by investors continued during the quarter,

as reflected in the stronger level of subscriptions.

In the context of an improvement in the prospects for the Euro area,

there was a decline in the average yield on GOJ global bonds during

the review quarter relative to the December 2011 quarter.

Notwithstanding, the spread between the yields on GOJ global bonds

and the US Treasury bills widened, largely related to market

perceptions of increased domestic risk factors.

There were mixed movements in the average yields on GOJ Treasury

Bills during the March 2012 quarter. The average yield on the 30-day

Treasury Bill was lower by 25 basis points (bps) at end-March 2012,

relative to end-December 2011. In contrast, the average yields on the

90-day and 180-day Treasury Bills increased by 6 bps and 1 bp

respectively, over the same period (see Table 2.13). The movements in

the yield on the 90-day instrument reflected a convergence towards the

rate on the BOJ’s 30-day Certificate of Deposit (CD). At the end of the

review quarter, the yield on the 30-day Treasury Bill was 1 bp below the

yield on the Bank’s corresponding OMO instrument.

Average overnight and 30-day repo rates increased to 3.90 per cent and

6.40 per cent, respectively, from 3.50 per cent and 6.30 per cent in the

December 2012 quarter. These increases reflected the impact of debt-

2.0

3.0

4.0

5.0

6.0

7.0

8.0

%

Figure 2.9 Average Private Money Market Rates

October 2011 - March 2012

O/N 30-day I/B

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 23

Table 2.14

Table 2.15

raising activities of the Government in mid-January and February. In

addition, the increases in rates were due to the concentration of domestic

liquidity emanating from OMO maturities in a few institutions during

the review period. In contrast to the movements in the other private

money market rates, average inter-bank rates declined to 3.50 per cent

in the March 2012 quarter from 3.60 per cent for the previous quarter.

There was an overall net placement of $14.9 billion on the Bank’s 30-

day CD during the review quarter, compared to net maturity of $28.2

billion the previous quarter (see Table 2.14). The net placement on

BOJ’s 30-day CD was partly financed from currency reflows as well as

proceeds from the maturity of the FR BMI Note in February. The Bank

continued to offer the 30-day and overnight instruments at 6.25 per cent

and 0.25 per cent, respectively, throughout the review quarter (see

Monetary Policy and Base Money Management).

The Government net redeemed approximately $7.7 billion in domestic

debt for the quarter, compared with a net issue of $14.4 billion for the

December 2011 quarter. Seven instruments were issued during the

quarter, two of which were new primary issues; a FR 7.20% BMI Note,

scheduled to mature in 2015 and an 8-year Variable Rate (VR) BMI

Note (see Appendix, Tables 8A and 8B). The FR 7.20% BMI Note

was a limited auction of $4.0 billion and was oversubscribed by 90.1 per

cent. The average yield on this instrument was 7.22 per cent.14

In

relation to the VR instrument, the re-pricing margin was set at 1.375

percentage points above the yield on the 180-day Treasury Bill, relative

to previously issued VR BMIs that were linked to the 90-day Treasury

Bill. Including the new primary issue, a total of four VR BMI Notes

were issued, representing 81.0 per cent of gross financing for the period.

With regards to amortisation, the FR 12.0% BMI Note which matured in

February yielding liquidity of $33.0 billion, represented the first

maturity of the debt instruments created in the Jamaica Debt Exchange

(see Table 2.15).

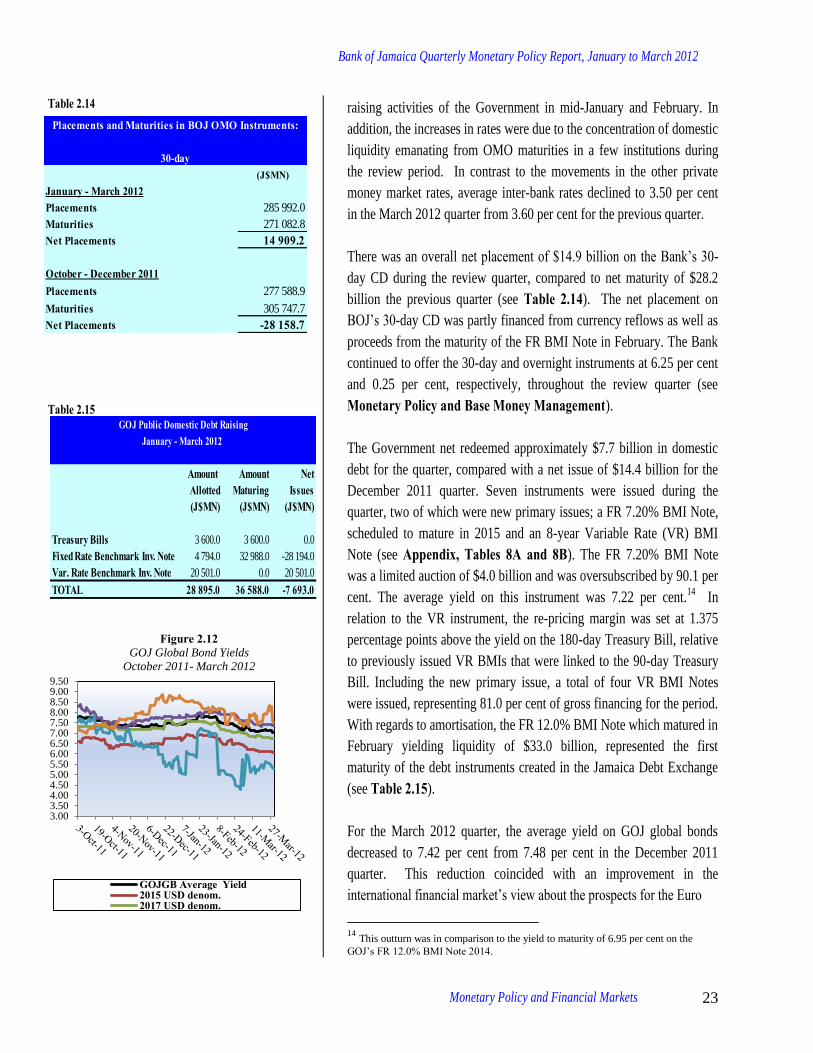

For the March 2012 quarter, the average yield on GOJ global bonds

decreased to 7.42 per cent from 7.48 per cent in the December 2011

quarter. This reduction coincided with an improvement in the

international financial market’s view about the prospects for the Euro

14

This outturn was in comparison to the yield to maturity of 6.95 per cent on the

GOJ’s FR 12.0% BMI Note 2014.

3.003.504.004.505.005.506.006.507.007.508.008.509.009.50

Figure 2.12 GOJ Global Bond Yields

October 2011- March 2012

GOJGB Average Yield2015 USD denom.2017 USD denom.

(J$MN)January - March 2012Placements 285 992.0

Maturities 271 082.8

Net Placements 14 909.2

October - December 2011Placements 277 588.9

Maturities 305 747.7

Net Placements -28 158.7

Placements and Maturities in BOJ OMO Instruments:

30-day

Amount Amount NetAllotted Maturing Issues(J$MN) (J$MN) (J$MN)

Treasury Bills 3 600.0 3 600.0 0.0

Fixed Rate Benchmark Inv. Note 4 794.0 32 988.0 -28 194.0

Var. Rate Benchmark Inv. Note 20 501.0 0.0 20 501.0

TOTAL 28 895.0 36 588.0 -7 693.0

GOJ Public Domestic Debt RaisingJanuary - March 2012

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 24

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Per

cen

tage

poi

nts

Figure 2.11Interest Rate Spread

GOJ Globals vs EMBI and US Treasuries

GOJ Global - EMBI

GOJ Global - US Treasuries

area in the context of the finalization of a second bailout package for

Greece. The decline in the average yield on GOJ global bonds was

largely reflected in the yields of the two euro-denominated bonds.

Notwithstanding the fall, the average spread between the yields on GOJ

global bonds and those on US Treasury bonds of a similar maturity

increased by 4 bps to 5.56 percentage points. The average yield spread

between the GOJ global bonds and the EMBI+ also increased by 34 bps

points to 2.05 percentage points, relative to the same measure at the end

of the previous quarter. This suggests that domestic risk factors affected

the market’s perception of Jamaican bonds over the quarter.

Bank of Jamaica Quarterly Monetary Policy Report, January to March 2012

Monetary Policy and Financial Markets 25

-15.0

-5.0

5.0

15.0

25.0

35.0

-10.0