Embed Size (px)

Citation preview

JETRO’s FY2015 Survey on Business

Conditions of Japanese-Affiliated

Firms in the Middle East

February 2016

Middle East and Africa Division

Overseas Research Department

Japan External Trade Organization (JETRO)

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Japanese-affiliated companies in the Middle East

Despite public security risks and low oil prices, the majority of Japanese-affiliated

companies post a surplus and have an incentive to expand their business.

2 Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Key Points of Survey Results

1 2 3 4 5

In 2015, the majority of companies posted a surplus. In terms of operating profit forecasts for 2015, 56.2% of companies replied that they would post a surplus. The percentage of those which replied that they would suffer a loss remained at 15.7%. By country, the percentage of companies in the black in the UAE was largest, at 64.3%. Meanwhile, about 30% of companies in Saudi Arabia replied that they would suffer a loss, suggesting that they operated in a harsh business environment.

The business sentiment for 2016 indicated that a little over 40% of companies expected their business to improve. Asked about prospects for 2016, 44.1% of companies expected their operating profits to improve, indicating that more companies had brighter prospects of profitability than in the previous year. The largest reason for improvement was “sales increase in local markets” (74.0%), followed by “sales increase due to increased exports” (51.9%).

Seventy-percent of companies were having an incentive to expand their future business. As to business development policy for the next one to two years, about 70% of companies in each country and territory replied that they planned to expand their business. The two greatest reasons for expansion were “high growth potential” (68.3%) and “increasing sales” (67.5%), and many of them (75.6%) intended to expand their sales functions.

In order to localize management, companies aimed to hire more employees locally rather than bring them from Japan. Cited as major initiatives to localize management were “strengthen systems to train/cultivate local human resources” (54.0%), “encourage mid-level hiring activities to obtain competent local staff” (44.4%), and “assign local staff to a general manager/manager position” (40.6%), but “insufficient performance/awareness among local staff” (43.2%) and “difficulty in recruiting local candidates for executive positions” (39.3%) were cited as issues to be addressed. An overwhelming percentage of companies (about 70%) replied that in the future the number of Japanese employees would remain at almost the same level, but the percentage of companies that expected to hire more local employees in the years to come was high, at about 60%.

UAE’s investment environment was beneficial in terms of taxation and free zoning, but the challenge was growing costs. Many companies considered UAE’s investment environment as attractive because of “merits of tax systems (no corporate tax and no income tax)” (78.2%), “free zones (no regulation for foreign investment and one-stop service)” (70.6%), and “political/social stability” (63.0%), but many of them cited soaring costs such as real estate rent, personnel expenses, and handling fees as issues to be addressed.

Survey Items for this Year

3 Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Outline of the Survey for This Year

Company Profile

1. Operating Profit

(1) Operating Profit Estimate for 2015 (total, by country)

(2) Operating Profit Estimate for 2015, Forecast for 2016 (compared to results in the previous year, total, by country)

(3) Operating Profit Estimate for 2015, Reasons for Improvement or Decline (multiple answers allowed, total, by country)

(4) Operating Profit Forecast for 2016, Reasons for Improvement or Decline (multiple answers allowed, total, by country)

2. Future Business Plan

(1) Business Operations in the Next One or Two Years (total, by country)

(2) Reasons for Business “Expansion” and Functions to be Expanded in the Next One or Two Years (multiple answers allowed,

total, by country)

3. Management Localization

(1) Approaches to Management Localization (multiple answers allowed, total, by country)

(2) Challenges in Management Localization (multiple answers allowed, total, by country)

4. Changes in Human Resource Structures

(1) Changes in the Number of Local Staff Over the Past Year, Future Plans (total, by country)

(2) Changes in the Number of Japanese Staff Over the Past Year, Future Plans (total, by country)

5. Evaluation of Investment Environments in UAE

Advantages and Disadvantages of the Investment Environments in UAE

4

5

7

8

9

10

11

12

13

14

15

16

17

To grasp the actual condition of Japanese-affiliated companies’ business activities in the Middle East (United Arab Emirates (UAE), Saudi Arabia, and Turkey) and provide the results to the public

Objective

A questionnaire survey was locally conducted for Japanese-affiliated companies operating in the Middle East.

Valid replies were received from 191 companies (120 from UAE, 36 from Saudi Arabia, and 35 from Turkey)

Companies Surveyed

September 28 to October 22, 2015

Period

The response rate was 46.6% (questionnaires were distributed to 410 companies, and valid replies were received from 191 of them).

By country, the response rate was 49.2% for UAE (120 of 244 companies), 50.7% for Saudi Arabia (36 of 71), and 36.8% for Turkey (35 of 95).

Response Rate

This was the third survey for UAE and the second for Saudi Arabia. For Turkey, it was the first survey that covered all industries; the previous ones targeted only the manufacturing industry.

JETRO informed companies to be surveyed of the URL for the questionnaire and asked them to complete and return it or sent them questionnaires written in Japanese by email.

Remarks

All response rates are shown in percentages (%). The response rate was rounded to the second decimal place. As a result, some total figures do not amount to 100%.

“N” stands for the number of valid responses.

Notes

Map of the Middle East

4

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Survey Overview

Turkey

Saudi Arabia

United Arab

Emirates

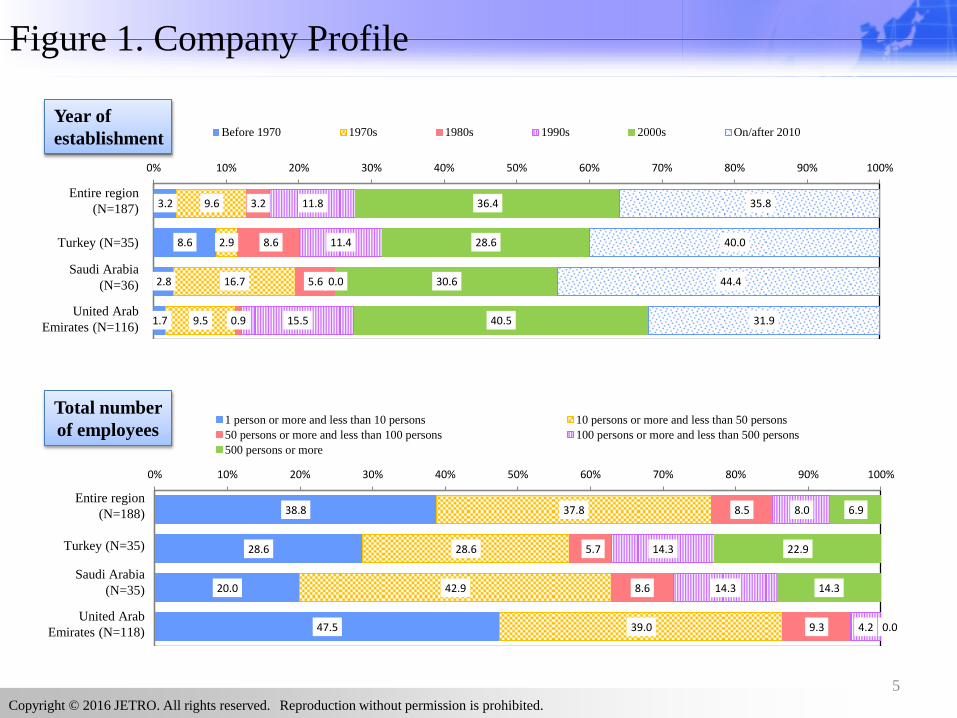

Figure 1. Company Profile

Year of

establishment

Entire region

(N=187)

Turkey (N=35)

Saudi Arabia

(N=36)

Total number

of employees

United Arab

Emirates (N=116)

3.2

8.6

2.8

1.7

9.6

2.9

16.7

9.5

3.2

8.6

5.6

0.9

11.8

11.4

0.0

15.5

36.4

28.6

30.6

40.5

35.8

40.0

44.4

31.9

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Before 1970 1970s 1980s 1990s 2000s On/after 2010

38.8

28.6

20.0

47.5

37.8

28.6

42.9

39.0

8.5

5.7

8.6

9.3

8.0

14.3

14.3

4.2

6.9

22.9

14.3

0.0

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1 person or more and less than 10 persons 10 persons or more and less than 50 persons

50 persons or more and less than 100 persons 100 persons or more and less than 500 persons

500 persons or more

Entire region

(N=188)

Turkey (N=35)

Saudi Arabia

(N=35)

United Arab

Emirates (N=118)

5

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

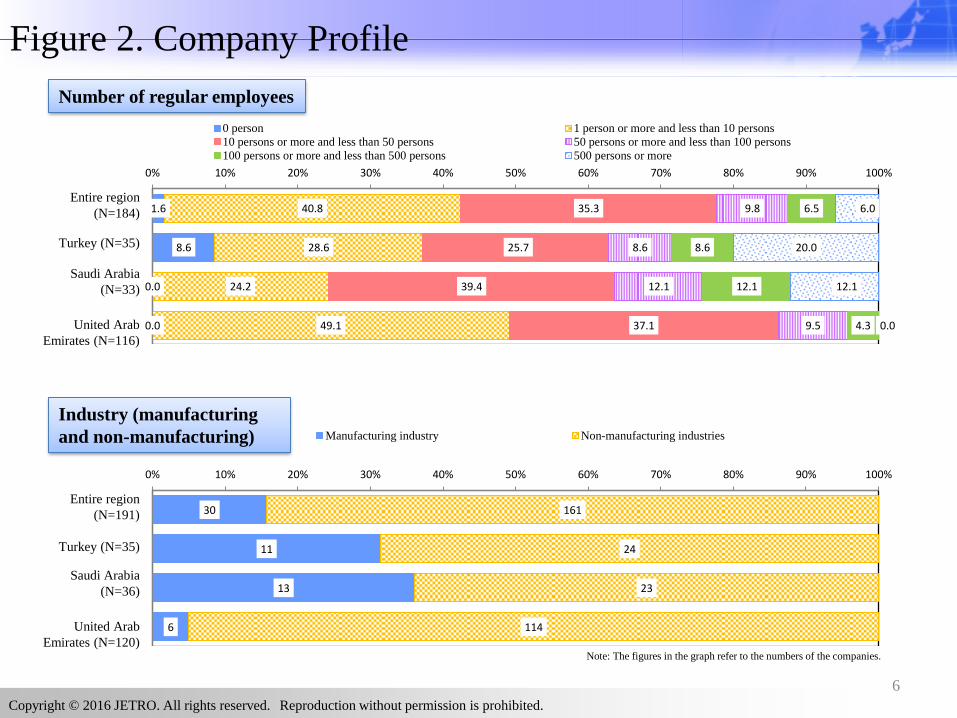

Figure 2. Company Profile

Number of regular employees

1.6

8.6

0.0

0.0

40.8

28.6

24.2

49.1

35.3

25.7

39.4

37.1

9.8

8.6

12.1

9.5

6.5

8.6

12.1

4.3

6.0

20.0

12.1

0.0

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

0 person 1 person or more and less than 10 persons

10 persons or more and less than 50 persons 50 persons or more and less than 100 persons

100 persons or more and less than 500 persons 500 persons or more

Entire region

(N=184)

Turkey (N=35)

Saudi Arabia

(N=33)

United Arab

Emirates (N=116)

Industry (manufacturing

and non-manufacturing)

30

11

13

6

161

24

23

114

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Manufacturing industry Non-manufacturing industries

Entire region

(N=191)

Turkey (N=35)

Saudi Arabia

(N=36)

United Arab

Emirates (N=120) Note: The figures in the graph refer to the numbers of the companies.

6

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Figure 3. Operating Profit Estimate (1)

A look at operating profit forecasts for the entire Middle East in 2015 indicated that the majority of companies replied that they

had posted a surplus and that the percentage of those which replied that they had suffered a loss was only 15.7%.

By country, the percentage of companies that answered, “Surplus,” in UAE was largest, at over 60%, followed by Turkey,

where it was also high, at a little less than 50%, but that for Saudi Arabia was low, at 30%. Meanwhile, the percentage of

companies that answered, “Deficit” was largest in Saudi Arabia, at 30%, suggesting that the Saudi business environment was

relatively harsh.

A comparison with the previous year showed that the percentage of companies operating at a profit declined from 65.4% to

64.3% in UAE and from 41.9% to 33.3% in Saudi Arabia. On the other hand, the percentage of loss-making companies in UAE

and Saudi Arabia also dropped, from 12.8% to 11.3% in UAE and from 35.5% to 33.3% in Saudi Arabia. The percentage of

companies that answered, “Break even” increased compared to the previous year.

Operating Profit Estimate for 2015

Entire region

(N=178)

Turkey (N=33)

Saudi Arabia

(N=30)

United Arab

Emirates (N=115)

56.2

48.5

33.3

64.3

28.1

36.4

33.3

24.3

15.7

15.2

33.3

11.3

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Surplus Break even Deficit

7

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Figure 4. Operating Profit Estimate (2)

A look at operating profit forecast for the entire Middle East showed that in 2016 the percentage of companies replying that the forecast would improve compared to the

previous year increased from 31.8% to 44.1%, while the percentage of companies replying that it would deteriorate decreased from 26.8% to 14.7%. Overall, for 2016, an

increasing percentage of companies had a brighter operating profit forecast than in the previous year.

By country, the percentage of companies replying that in 2016 the forecast would improve compared to the previous year was largest in Saudi Arabia, at 53.3%, followed by

Turkey, where it was also high, at 48.5%. The percentage for UAE was relatively low, at 40.4%. On the other hand, the percentage of companies in Turkey replying that it

would deteriorate compared to the previous year was largest, 18.2%, followed by UAE, at 14.9%, and that for Saudi Arabia was lowest, at 10.0%.

A comparison with the previous year indicated that the percentage of companies that expected operating profit to improve increased in all countries, from 36.7% to 53.3% in

Saudi Arabia, from 27.3% to 48.5% in Turkey, and from 31.9% to 40.4% in UAE. On the other hand, the percentage of those which expected it to deteriorate nearly halved,

from 20.0% to 10.0% in Saudi Arabia, from 27.6% to 14.9% in UAE, and from 30.3% to 18.2% in Turkey. In all countries, the operating profit forecast change for the better.

2015 operating profit forecast (compared to 2014)

2016 operating profit forecast (compared to 2015)

Entire region

(N=179)

Turkey (N=33) Saudi Arabia

(N=30)

United Arab

Emirates (N=116)

Entire region

(N=177)

Turkey (N=33)

Saudi Arabia

(N=30)

United Arab

Emirates (N=114)

31.8

27.3

36.7

31.9

41.3

42.4

43.3

40.5

26.8

30.3

20.0

27.6

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Improve Remain the same Deteriorate

44.1

48.5

53.3

40.4

41.2

33.3

36.7

44.7

14.7

18.2

10.0

14.9

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Improve Remain the same Deteriorate

8

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Figure 5. Operating Profit Estimate (3)

A look at operating profit forecast for 2015 showed that in all countries the percentage of companies that cited “sales increase in local markets” as the main reason the forecast improved was largest, at 50-

70%, followed by companies that mentioned “sales increase due to export expansion” (over 40%) except for Saudi Arabia. In Saudi Arabia, on the other hand, a large percentage of companies cited “reduction

of labor costs” as the reason for improvement (a little less than 20%) with the percentage of “sales increase due to export expansion” being low, at less than 10%.

In all countries, the percentage of companies that citied “sales decrease in local markets” as the reason for deterioration was largest, at about 60%. In the entire region, the second largest reason was “sales

decrease due to export slowdown,” which accounted for a little more than 30%, but by country, the reasons were varied, with half of the companies in Turkey citing “effects of exchange rate fluctuation,” 40%

of those in Saudi Arabia mentioning “increase of labor costs” and “production costs insufficiently shifted to selling price of goods,” and the same percentage of those in UAE choosing “sales decrease due to

export slowdown.“

Reasons 2015 operating profit forecasts

Reasons 2015 operating profit forecasts deteriorate

N=57

N=47

(%)

(%)

70.2

42.1

15.8 7.0 5.3 5.3 3.5 1.8

17.5

66.7

44.4

11.1 11.1

0.0 0.0 0.0

11.1

22.2

54.5

9.1

0.0 0.0

18.2

0.0

9.1

0.0

27.3

75.7

51.4

21.6

8.1 2.7

8.1 2.7 0.0

13.5

0

10

20

30

40

50

60

70

80 Entire region Turkey Saudi Arabia United Arab Emirates

Sales increase in

local markets

Sales increase due

to export expansion

Effects of exchange

rate fluctuation

Reduction of

procurement costs

Reduction of labor

costs

Improvement of

sales efficiency

Reduction of other

expenditures (e.g., administrative/

utility costs/fuel costs)

Improvement of

production

efficiency

Other

59.6

31.9

21.3 21.3 19.1

10.6 8.5 2.1

27.7

60.0

20.0

50.0

20.0 20.0

20.0

10.0 10.0

20.0

60.0

0.0 0.0

40.0 40.0

20.0 20.0

0.0

40.0

59.4

40.6

15.6 18.8

15.6

6.3 6.3 0.0

28.1

0

10

20

30

40

50

60

70 Entire region Turkey Saudi Arabia United Arab Emirates

Sales decrease in

local markets

Sales decrease due

to export slowdown

Effects of exchange

rate fluctuation

Increase of labor

costs

Production costs

insufficiently

shifted to selling

price of goods

Increase of other

expenditures (e.g., administrative/

utility costs/fuel costs)

Increase of

procurement costs

Rising interest rates Other

9

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Multiple answers allowed

Figure 6. Operating Profit Estimate (4)

A look at operating profit forecast for 2016 indicated that in all countries 70-90% of companies cited “sales increase in local markets” as the largest reason operating profit improved.

The second reason was “sales increase due to export expansion.” However, in countries other than Saudi Arabia, 50-60% of companies mentioned “export expansion” as the reason for

improvement, but in Saudi Arabia, the percentage of such companies was low, at a little less than 30%, and the percentage of companies that cited “improvement of production

efficiency” was also high, at 50-60%.

In all countries, the largest reason for deterioration cited was “sales decrease in local markets” (57.7% for the entire region). The second reasons were “sales decrease due to export

slowdown” and “increase of labor costs” for the entire region (a little more than 20% for both), but by country, the reasons were varied, with 50% of companies in Turkey citing “effects

of exchange rate fluctuation,” 33.3% of those in Saudi Arabia mentioning “increase of labor costs” and “increase of procurement costs,” and 29.4% of those in UAE choosing “sales

decrease due to export slowdown.”

Reasons 2016 operating profit forecasts improve

Reasons 2016 operating profit forecasts deteriorate

N=77

N=26

(%)

(%)

74.0

51.9

14.3 6.5 6.5

5.2 5.2 3.9 18.2

68.8

50.0

25.0 18.8

6.3 6.3

18.8

0.0

25.0

93.8

25.0

0.0

6.3

25.0

0.0 0.0 0.0

18.8

68.9 62.2

15.6

2.2 0.0

6.7 2.2

6.7 15.6

0102030405060708090

100

Entire region Turkey Saudi Arabia United Arab Emirates

Sales increase in

local markets

Sales increase due

to export expansion

Improvement of

sales efficiency

Reduction of labor

costs

Improvement of

production

efficiency

Effects of exchange

rate fluctuation

Reduction of

procurement costs

Reduction of other

expenditures (e.g., administrative/

utility costs/fuel costs)

Other

57.7

23.1 23.1 19.2

15.4 15.4 7.7

0.0

26.9

50.0

16.7

33.3 33.3

50.0

33.3

16.7

0.0

16.7

66.7

0.0

33.3

0.0 0.0 0.0

33.3

0.0

33.3

58.8

29.4

17.6 17.6

5.9 11.8

0.0 0.0

29.4

0

10

20

30

40

50

60

70

80 Entire region Turkey Saudi Arabia United Arab Emirates

Sales decrease in

local markets

Sales decrease due to

export slowdown

Increase of labor

costs

Increase of other

expenditures (e.g., administrative/

utility costs/fuel costs

Effects of exchange

rate fluctuation

Production costs

insufficiently shifted

to selling price of

goods

Increase of

procurement costs

Rising interest rates Other

10 Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Multiple answers allowed

Figure 7. Business Expansion in the Next One or Two Years (1)

Asked about their approach to business development over the next one to two years from 2015, more than 60% of companies in each country

replied that they planned to expand their business. If companies that replied that they would maintain the status quo (about 30%) are included,

almost all companies expected that they planned to expand their business or maintain the status quo. However, 5.7% of companies in Turkey

chose to reduce their business, highlighting the difference between Turkey and other countries.

Business operations in the next one or two years

Entire region

(N=186)

Turkey (N=35)

Saudi Arabia

(N=32)

United Arab

Emirates

(N=119)

67.7

65.7

68.8

68.1

30.6

28.6

31.3

31.1

1.6

5.7

0.0

0.8

0.0

0.0

0.0

0.0

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Expansion Remaining the same Reduction Transferring to a third country/region or withdrawal from current local market

11

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Figure 8. Business Expansion in the Next One or Two Years (2)

Reasons for expansion

Functions to be expanded

The two major reasons for expansion were “high growth potential” and “sales increase,” each of which accounted for 60-70% of the companies surveyed. The third largest reason for

many companies was “reviewing production and distribution networks” for Turkey and UAE and “high receptivity for high-value added products” for Saudi Arabia.

An overwhelming percentage of companies planned to expand their “sales function” (50% to a little less than 90%). By country, the second and lower reasons were “production (high-

value added products)” and “production (ubiquitous products)” for Turkey (26.1% each), “production (high-value added products)” for Saudi Arabia (28.6%), and “function of regional

headquarters” for UAE (25.3%), indicating that the reasons varied from one country to another.

N=126

(%)

(%)

N=123

68.3 67.5

23.0 20.6 17.5

5.6 3.2 0.0 6.3

65.2 60.9

26.1 17.4 17.4

0.0

8.7

0.0 0.0

59.1

77.3

4.5 9.1

27.3

4.5 0.0 0.0

4.5

71.6 66.7

27.2 24.7

14.8 7.4

2.5 0.0 8.6

0

10

20

30

40

50

60

70

80

90 Entire region Turkey Saudi Arabia United Arab Emirates

High growth

potential

Sales increase Reviewing

production and

distribution

networks

Relationship with

clients

High receptivity

for high-value

added products

Deregulation

Reduction of costs (e.g., procurement/

labor costs)

Ease in securing

labor force

Other

75.6

17.1 17.1 15.4 9.8 8.9

2.4

13.0

52.2

0.0

13.0

26.1 26.1

4.3 4.3

21.7

57.1

4.8

14.3

28.6

14.3 14.3

0.0

23.8

87.3

25.3 19.0

8.9 3.8

8.9 2.5

7.6

0

10

20

30

40

50

60

70

80

90Entire region Turkey Saudi Arabia United Arab Emirates

Sales function Function of regional

headquarters

Logistics function Production (high-

value added

products)

Production

(ubiquitous products)

Administrative

functions in

providing services (e.g., shared service

center, call center)

R&D Other

12

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Multiple answers allowed

Figure 9. Management Localization (1)

Approaches to management localization

In terms of approaches to management localization, the percentages of three replies were largest in all countries: “strengthen systems to train/cultivate local human

resources” (54.0% for the entire region), “encourage mid-level hiring activities to obtain competent local staff” (44.4%), and “assign local staff to a general

manager/manager position” (40.6%).

The percentages of the top three approaches were high in all countries, but those of approaches in lower ranks varied from one country to another. A look at the

characteristics of each country indicated that while in Saudi Arabia the percentage of “reform personnel systems, such as a merit-based promotion system by focusing on

localization of corporate management” was high (33.3%) compared to other countries, the replies of companies in UAE reflected the degree to which the duty to employ

people of the country was imposed, as they cited “strengthen authority in local office to allow them to make their own decisions for sales strategies” and “no particular

actions are taken” (19.3% each).

N=187

(%)

54.0

44.4 40.6

21.9

17.6 15.5 13.9 13.4

9.1

2.1 4.8

57.1

45.7

40.0

20.0 22.9

8.6

2.9

11.4

17.1

2.9

8.6

66.7

51.5 48.5

33.3

21.2

9.1 6.1

9.1

15.2

6.1

15.2

49.6

42.0 38.7

19.3 15.1

19.3 19.3 15.1

5.0 0.8 0.8

0

10

20

30

40

50

60

70

80Entire region Turkey Saudi Arabia United Arab Emirates

Strengthen systems

to train/cultivate

local human

resources by

focusing on

localization of

corporate

management

Encourage mid-

level hiring

activities to obtain

competent local

staff by focusing

on localization of

corporate

management

Assign local staff

to a general

manager/

manager position

Reform

personnel

systems, such as

a merit-based

promotion

system, by

focusing on

localization of

corporate

management

Strengthen R&D

capacity to

develop quality

of products/

services for local

markets

Strengthen

authority in local

office to allow

them to make their

own decisions for

sales strategies

No particular

actions are taken

Delegate

authority to local

office from

headquarters

Assign local staff

to an executive

position

Obtain human

resources/

management

resources

through M&As

Other

13

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Multiple answers allowed

Figure 10. Management Localization (2)

Asked about challenges in management localization, the largest percentage of companies cited “insufficient performance/awareness among local

staff” (43.2% for the entire region), followed by companies that mentioned “difficulty in recruiting local candidates for executive positions” (39.3%).

In Saudi Arabia, however, the percentage of companies that chose the two answers was as high as about 60% (59.4%), suggesting that they were the

challenges shared by companies that operated in the country.

Apart from the top two challenges, a look at the characteristics of each country showed that in Turkey the percentage of “little progress in delegating

authority from the headquarters to local offices” was high, at 25.7%, and in Saudi Arabia that of “a high turnover rate of local candidates for

executive positions” and “difficulty in reducing the number of Japanese expatriate staff” was high, at 25.0% each. One characteristic of UAE is that

the percentages of all replies except the top two were equalized, as none of them exceeded 20%.

N=183

(%)

43.2 39.3

18.6 17.5 16.4

13.7 12.6 9.8 8.7 8.2 7.1 7.1

6.0 5.5 5.5 4.9 2.2

51.4

40.0

25.7

8.6

22.9 22.9 20.0

2.9 2.9

11.4 14.3

8.6

2.9 8.6

14.3 11.4

2.9

59.4 59.4

15.6

25.0 25.0

6.3

12.5

3.1 3.1

12.5 9.4

3.1 6.3

12.5

6.3 3.1

6.3

36.2 33.6

17.2 18.1

12.1 12.9

10.3

13.8 12.1

6.0 4.3

7.8 6.9

2.6 2.6 3.4

0.9

0

10

20

30

40

50

60

70Entire region Turkey Saudi Arabai United Arab Emirates

Insufficient

performance/

awareness among

local staff

Difficulty in

recruiting local

candidates for

executive

positions

Little progress

in delegating

authority from

the

headquarters to

local offices

A high turnover

rate of local

candidates for

executive

positions

Difficulty in

reducing the

number of

Japanese

expatriate staff

Insufficient

capabilities for

local planning

and marketing

Insufficient

management

capabilities of

Japanese

expatriate staff

No plan for

promoting

management

localization

There is no

particular

issue

Inadequate

language skills

of Japanese

expatriate staff

(English and

local languages)

Shortage of

positions to be

allocated to

local staff

Insufficient

capabilities to

develop local

products and

services

Disagreement

over policy for

recruitment

between local

office and

headquarters

Other issues

with the

headquarters/

Japan side

Other issues with

the local side

Inadequate

language skills

of local staff

(Japanese and

English)

Other

14 Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Challenges in localization

Multiple answers allowed

Figure 11. Changes in Human Resource Structures (1)

Changes in the number of local employees over the past year

Future plans

A look at the changes in the number of local employees during the past year showed that the percentage of companies that had seen the number increase was

38.9% and that of those whose number had remained at almost the same level was 51.4%. By country, while more than 40% of companies in Turkey and Saudi

Arabia replied that the number had increased, the percentage of such companies in UAE remained at 35.6%. In Saudi Arabia, on the other hand, the percentage

of companies replying that the number had decreased was 18.8%, more than double that for Turkey (8.6%) and UAE (7.6%).

In terms of future plans, the percentage of “increase” (60.7%) exceeded that of “no change” (35.5%) with that of “decrease” being small, at 3.8%. By country,

the percentage of companies in Saudi Arabia that answered, “Increase,” was largest among the three countries, at about 70%, and that of companies that

answered, “Decrease,” was smallest among the three, at 3.0%. On the other hand, the percentage of “increase” for Turkey (45.7%) was smallest among the

three, and that of “decrease” (5.7%) was largest. This indicated that in the future, companies in Saudi Arabia would be most active in hiring local employees

and that those in Turkey would be relatively cautious.

Entire region

(N=185)

Turkey (N=35) Saudi Arabia

(N=32)

United Arab

Emirates (N=118)

Entire region

(N=183)

Turkey (N=35) Saudi Arabia

(N=33)

United Arab

Emirates (N=115)

38.9

45.7

43.8

35.6

51.4

45.7

37.5

56.8

9.7

8.6

18.8

7.6

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Increase No change Decrease

60.7

45.7

69.7

62.6

35.5

48.6

27.3

33.9

3.8

5.7

3.0

3.5

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Increase No change Decrease

15

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Figure 12. Changes in Human Resource Structures (2)

At look at the changes in the number of Japanese expatriate employees during the past year showed that the percentage of “no change” was 66.7%, that of “increase” was

21.1%, and that of “decrease” was 12.2%. By country, in terms of the percentage of companies replying that the number had increased, there was no major difference

among the three as the percentage stood at a little more than 20% in each, but the percentage of companies in Saudi Arabia replying that the number had decreased was

largest, at 21.9%, followed by UAE (10.6%) and Turkey (8.6%), and this highlighted a greater decrease for Saudi Arabia.

Asked about future plans, 71.2% of companies answered, “No change,” 20.3% replied, “Increase,” and 8.5% said, “Decrease.” By country, the percentage of companies

in Turkey replying that they planned to increase the number of Japanese expatriate employees was largest, at 28.6%, followed by Saudi Arabia (24.2%) and UAE

(16.5%). On the other hand, the percentage of companies in Saudi Arabia replying that they planned to decrease the number was largest, 21.2%, four times that for

Turkey (5.7%) and UAE (5.5%). In particular, for Saudi Arabia, the percentage of companies replying that they planned to decrease Japanese expatriate employees was

remarkably high.

Changes in the number of Japanese expatriate employees over the past year

Future plans

Entire region

(N=180)

Turkey (N=35)

Saudi Arabia

(N=32)

United Arab

Emirates (N=113)

Entire region

(N=177) Turkey (N=35)

Saudi Arabia

(N=33)

United Arab

Emirates (N=109)

21.1

22.9

21.9

20.4

66.7

68.6

56.3

69.0

12.2

8.6

21.9

10.6

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Increase No change Decrease

20.3

28.6

24.2

16.5

71.2

65.7

54.5

78.0

8.5

5.7

21.2

5.5

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Increase No change Decrease

16

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Figure 13. Investment Environment (United Arab Emirates Only)

• Overall, more than half of companies cited as the advantages of the investment environment in UAE “merits of tax systems (no corporate tax and no income tax)” (78.2%), “free zone (no regulation for

foreign investment and one-stop service)” (70.6%), “political/social stability” (63/0%), and “good living environment for Japanese expatriates” (59.7%). In the non-manufacturing industries, companies

generally gave almost the same replies as mentioned above, but manufacturers favorably evaluated “market scale or growth potential” (66.7%) and “sufficient infrastructures (electricity, distribution and

telecommunication, etc.” (50.0%) while the percentage of companies that chose “political/social stability” was low, at only 16.7%.

• A large percentage of companies cited “increase of real estate rental fees” (64.1%) and “increase of labor costs” (59.8%) as the disadvantages of the investment environment in UAE, irrespective of whether

they were in the manufacturing or non-manufacturing industries. One characteristic of manufacturers was that the percentage of those which mentioned “political/social instability” was high, at 66.7%. In

the manufacturing industry, “transaction risks (such as debt collecting risk)” (33.3%) and “regulations for foreign investment” (16.7%) were also cited by many firms as problematic.

• (Note) (1) This survey was carried out only for companies operating in UAE. (2) Since non-manufacturing industries account for an extremely high percentage of all industries in UAE, the survey results

generally indicate the same trends as for the non-manufacturing industries.

Advantages of the investment environment in UAE

(%)

(%)

78.2 70.6

63.0 59.7

46.2 43.7 42.0

28.6 22.7 21.0

8.4 5.9 2.5 1.7

83.3 83.3

16.7

50.0

33.3

50.0

66.7

33.3

16.7 16.7

0.0 0.0 0.0 0.0

77.9 69.9

65.5 60.2

46.9 43.4 40.7

28.3 23.0 21.2

8.8 6.2 2.7 1.8

0102030405060708090

All industries Manufacturing industry Non-manufacturing industries

64.1 59.8

45.3 41.9

28.2 23.9

17.1 16.2 14.5 13.7

3.4 0.9 0.9 5.1

66.7

50.0

33.3

16.7 16.7

33.3

66.7

0.0

16.7

0.0 0.0 0.0 0.0 0.0

64.0 60.4

45.9 43.2

28.8 23.4

14.4 17.1 14.4 14.4

3.6 0.9 0.9 5.4

0

10

20

30

40

50

60

70

80

All industries Manufacturing industry Non-manufacturing industries

Merits of tax

systems

(No corporate tax

and no income tax)

Free zone

(No regulation for

foreign investment

and one-stop service)

Political/social

stability

Good living

environment for

Japanese

expatriates

Less linguistic/

communication

problems

Sufficient

infrastructures (electricity,

distribution and

telecommunication,

etc.

Market scale or

growth potential

Positive image

regarding Japan

Formation of local

industrial clusters

by relevant

companies (client

companies etc.)

No labor dispute Sufficient labor

supply

Quick

administrative

procedures

Good incentives

for investment

Other

Increase of real

estate rental fees

Increase of labor

costs

Increase of

administrative

commissions

Underdeveloped

legal system or

unclear legal

system operation

Slow

administrative

procedures

Transaction risks

(such as debt

collecting risk)

Political/social

instability

Labor shortage or

difficulty in

recruiting

Regulations for

foreign investment

Market scale or

growth potential

Insufficient

infrastructures

(electricity,

distribution and

telecommunication,

etc.)

Insufficient

incentives for

investment

Linguistic/

communication

problems

Other

Disadvantages of the investment environment in UAE

N=117

(including 6 manufacturers)

N=119

(including 6 manufacturers)

17

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Multiple answers allowed

Copyright © 2016 JETRO. All rights reserved. Reproduction without permission is prohibited.

Any use of information in this report shall be at the user’s discretion and under its own

responsibility. JETRO makes every effort to provide accurate information and data. However,

JETRO cannot be held liable whatsoever for damages or losses arising from the use of

information in this report.

Middle East and Africa Division

Overseas Research Department

Japan External Trade Organization (JETRO)

1-12-32 Akasaka, Minato-ku, Tokyo, 107-6006

Tel: +81-3-3582-5180

Fax: +81-3-3587-2485

Email: [email protected]

![Rotor 90 [.pdf 15.7 Mb]](https://img.pdfslide.net/doc/110x75/586ce1f41a28abf6518bbde9/rotor-90-pdf-157-mb.jpg)

![ดาวน์โหลด [15.7 Mb.]](https://img.pdfslide.net/doc/110x75/588c553b1a28abe9208b5126/-157-mb.jpg)