Embed Size (px)

Citation preview

Jewish Community Foundation of Montreal

Professional Development Seminar

NEW RULES FOR GIFTS OF MARKETABLE SECURITIES – TAX PLANNING AND INCENTIVES

Robert Kleinman, FCA Executive Director Jewish Community Foundation

June 13, 2006

New Rule on Gifts of Marketable Securities - Summary

Federal Budget May 2, 2006.

Effective May 2, 2006 donors who make gifts of stocks listed on a “Prescribed Stock Exchange” (as defined in Regulations 3200 and 3201 of the Income Tax Act Canada (the “Act”)) to a public charity, will no longer be subject to capital gains tax.

Gifts of marketable securities to private foundations are not eligible for this special tax savings.

Regulation 3200 – Stock Exchanges In Canada

Tier 1 and 2 of the TSX venture exchange Montreal stock exchange Toronto stock exchange

Regulation 3201 – Stock Exchanges Outside of Canada

Examples of foreign stock exchanges whose

shares will qualify: Belgium, France, Germany, Italy Hong Kong, Singapore London United States: American Stock Exchange,

Boston Stock Exchange, New York, NASDAQ

Donation of Mutual Funds to a Public Charity

Under the new rules the donation of mutual funds will also qualify for the exemption from capital gains when gifted to a public charity.

Quebec Rules

At the current time, Quebec has not harmonized its legislation in accordance with the new federal budget.

There are still significant tax savings for Quebec – the taxable capital gain is reduced in half.

The Tax Advantages of Making a Gift of Securities

Example: Mr. Schwartz donates $100,000 of Royal Bank

of Canada stock to the Jewish community foundation (“JCF”).

His alternative is to sell the stock and donate $100,000

Implications of Sale Vs. Gift

Stock Sale Stock Donation

Combined Federal Quebec Combined

Proceeds $100,000 $100,000 $100,000

Cost $50,000 $50,000 $50,000

Capital Gain $50,000 $50,000 $50,000

Taxable Capital Gain $25,000 $25,000 $25,000

Special Exemption ($0) ($25,000) (12,500)

Net Income $25,000 $0 $12,500

Income Taxes Payable $12,000 $0 $3,000 (12%) $3,000

Tax Receipt $100,000 $100,000 $100,000

Tax Savings $48,000 $24,000 $24,000 $48,000

Net Tax Savings $36,000 $24,000 $21,000 $45,000

Summary – Sale vs. Gift

On a combined federal and provincial basis, Mr. Schwartz would save $9,000 in taxes by donating the securities instead of the cash to the JCF.

What Would Happen If Quebec Harmonized Its Legislation?

No Provincial tax on the donation of the marketable securities.

Mr. Schwartz would save $12,000 by donating the securities instead of the cash.

Gifts of Marketable Securities by a Corporation

Same rules apply when a corporation makes a gift of marketable securities.

Sale of Marketable Securities by a Corporation

Example: Holdco donates $100,000 of Royal Bank of

Canada stock to the JCF. The alternative is for Holdco to sell the stock

and donate the $100,000.

Corporation Sale vs. Gift

Stock Sale Stock Donation

Combined Federal Provincial Combined

Proceeds $100,000 $100,000 $100,000

Cost $50,000 $50,000 $50,000

Capital gain $50,000 $50,000 $50,000

Taxable capital gain $25,000 $25,000 $25,000

Special exemption $0 ($25,000) ($12,500)

Net income $25,000 $0 $12,500

Income taxes payable $13,010 $0 $2,031

Tax receipt $100,000 $100,000 $100,000

Tax savings $52,000 $36,000 $16,000 $52,000

Net tax savings $38,990 $36,000 $13,969 $49,969

Corporate Sale vs. Gift - Summary

On a combined federal and provincial basis, Holdco would save $10,979 in taxes by donating the securities instead of the cash to the JCF.

Extra Corporate Bonus of Gifting Marketable Securities – CDA

Subsection 89(1) of the Act sets out the definition of the capital dividend account (“CDA”).

The non-taxable portion of the capital gain forms part of the CDA.

Under the new federal rules since the entire gain is not taxable the entire amount of the gain flows through to the CDA.

What About Quebec?

Section 570(b) Quebec Taxation Act and Regulation 570 (r2):

For Quebec purposes, the calculation of the CDA is based on the Federal calculation.

Therefore, the full amount of the capital gain is included in the CDA of the corporation for Quebec tax purposes as well.

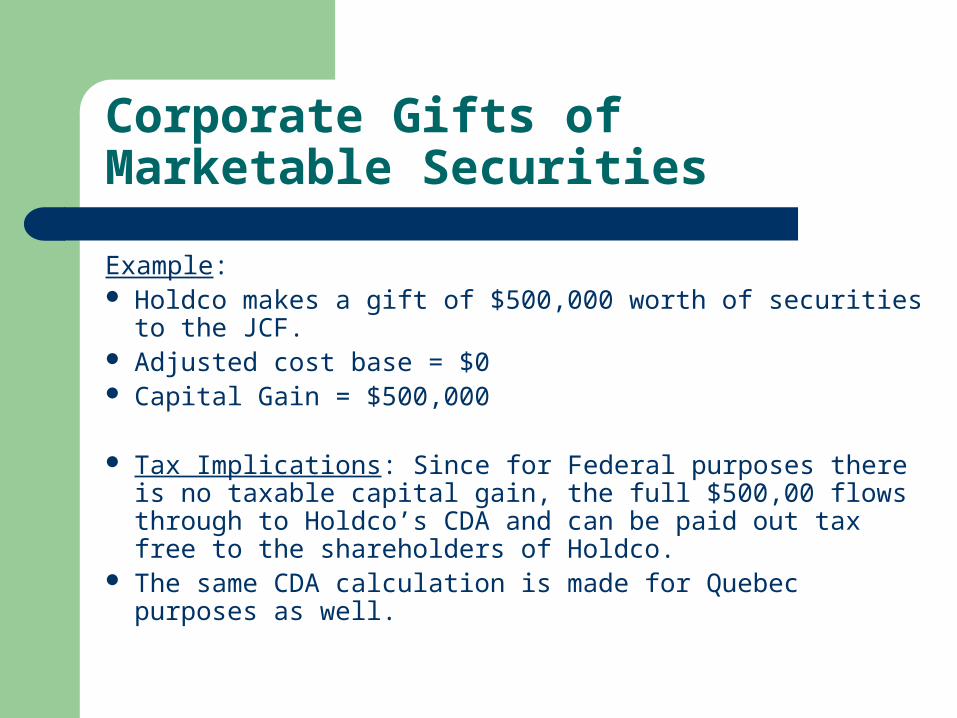

Corporate Gifts of Marketable Securities

Example: Holdco makes a gift of $500,000 worth of securities to the JCF. Adjusted cost base = $0 Capital Gain = $500,000

Tax Implications: Since for Federal purposes there is no taxable capital gain, the full $500,00 flows through to Holdco’s CDA and can be paid out tax free to the shareholders of Holdco.

The same CDA calculation is made for Quebec purposes as well.

If Holdco Wants to Keep the Stock…

With the proceeds from the CDA Holdco can buy back the the stock at a higher cost base.

Gifting Marketable Securities – Post Mortem Tax Planning

Deemed disposition of all assets on death. Gifts made in the will are deemed to be made

in the year of death. Full amount of donation receipt to be applied to

reduce taxes in the year of death. Reduce death taxes by donating marketable

securities.

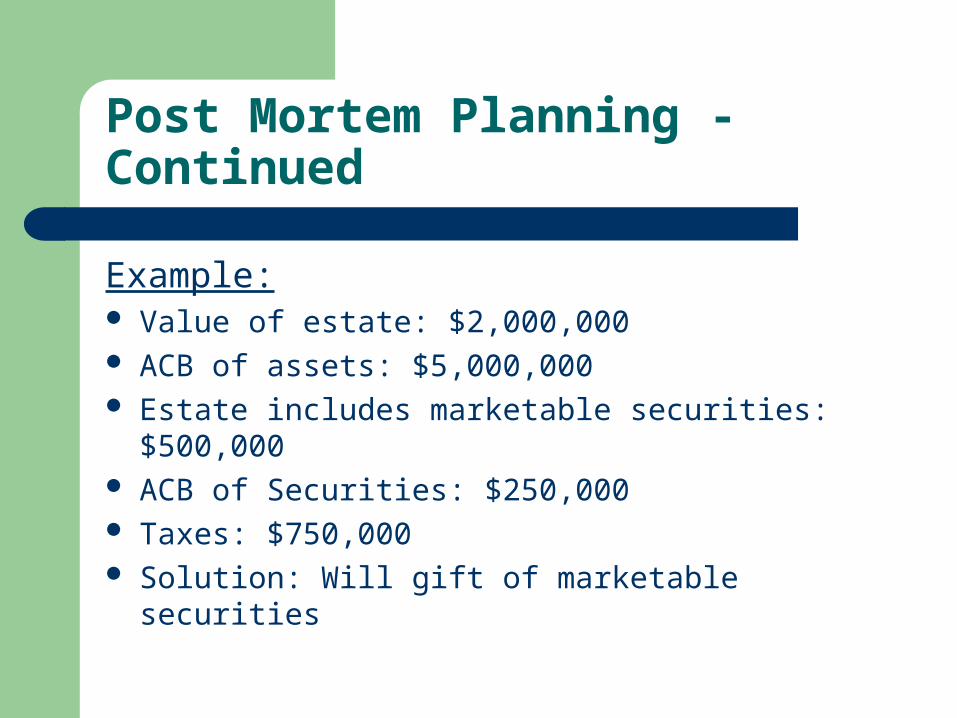

Post Mortem Planning - Continued

Example: Value of estate: $2,000,000 ACB of assets: $5,000,000 Estate includes marketable securities: $500,000 ACB of Securities: $250,000 Taxes: $750,000 Solution: Will gift of marketable securities

Post Mortem Tax Planning - Solution

Will to provide that on death – marketable securities to be gifted to the JCF.

Effect: Estate gets tax receipt for $500,000 applied to reduce taxes

from $750,000 to $250,000 in year of death. For Federal purposes, the entire capital gain of $250,000 is

not taxable. For Quebec purposes, only ½ of the taxable capital gain is

included in income. Estate can make a significant gift at relatively low cost.

Marketable Securities – Other Tricks With Flow Through Shares

Donor may purchase resource (mining or oil and gas) partnership units, convert the units into shares and then donate these shares to a charity.

Flow Through Shares – Example

Example: Mr. Schwartz purchases a $1,000 resource

unit. Mr. Schwartz can write off his investment for

tax purposes. For tax purposes the ACB of the units is nil.

Gift of Flow Through Shares - Continued

What would happen if after converting the units into shares, the shares were gifted to JCF?

Mr. Schwartz receives a tax receipt of $1,000 – the investment is effectively written off a second time.

The resulting capital gain ($1,000) will not be taxed (other than Quebec).

The cost of the donation is reduced significantly!

Flow Through Shares – A Word of Caution

The resource shares are not “worth” the original investment – there is a discount.

May not be able to dispose of shares until after certain holding period.

Ensure that charity receives a real donation. The original investment should be sound to ensure there is value to donate.

Gift of Stock Options

Donor who has stock options may donate the shares acquired pursuant to an option to the JCF.

In this case, the tax reduction will apply to both the capital gain and the employment income realized.

Donating Shares acquired pursuant to Stock Options - Criteria

Options must be acquired after Feb. 27, 2000 and must be donated:

1. In the same calendar year that stock option was exercised;and

2. Within 30 days of exercising the stock option.

Donating Shares Acquired Pursuant to Stock Options

Example Julie Wise is an employee of ACB co. On May 13, 2004 she acquires 1,000 options of the

corporation for $10 a share (the FMV of the shares at the time).

On June 13, 2006 she decides she would like to make a gift to the JCF.

The FMV of the shares at that time is $45 / share. Her option is to exercise the option and donate the shares

or exercise the option, sell the shares and donate the cash.

Donating Stock Acquired Through Employee Stock Options vs. Donating Cash from Sale of Stocks acquired from Options

Exercise, sell shares and donate $$$

Exercise and donate shares

Combined Federal Provincial Combined

FMV of shares $45,000 $45,000 $45,000

Exercise Price $10 $10 $10

Employee Benefit $35 $35 $35

Employee Benefit on 1,000 shares

$35,000 $35,000 $35,000

Qualifying shares deduction (on benefit)

($17,500) ($17,500) ($17,500)

Donation exemption $0 $(17,500) ($8,750)

Taxes payable on exercise of option

$8,400 $0 $2,100

Donation receipt $45,000 $45,000 $45,000

Tax Savings $21,600 $10,800 $10,800 $21,600

Net Tax Savings $13,200 $10,800 $8,700 $19,500

Summary

On a combined federal and provincial basis, Julie would save $6,300 in taxes by donating the stock acquired pursuant to a stock option rather than donating the cash to the JCF.

Key Points to Remember

Much less expensive to make a large gift using marketable securities.

Quebec has not yet harmonized its legislation. With corporations, additional advantage of using CDA. Create a foundation by making a gift of marketable

securities. Consider the use of flow-through shares and employee

stock options And most important………..

MOST IMPORTANT……

Consult with your professionals at the JCF. We would be more than happy to meet with

you to discuss any questions and help your clients achieve their tax and philanthropic goals!