Embed Size (px)

Citation preview

Socio-Economic Impact of IFC Financing in Jordan

– An Assessment of Employment and Value-added -

Final Report

November 2012

Ethan B. Kapstein

René Kim

Hedda Eggeling

1

Contents

Executive summary ............................................................................................... 2

1 Introduction, Objectives and Scope ....................................................................... 4

2 Jordan’s economy ............................................................................................... 4

2.1 Jordan’s Financial Structure ........................................................................... 6

3 IFC’s operations in Jordan .................................................................................... 7

4 Economic footprint of IFC Jordan .......................................................................... 8

4.1 Methodology description ............................................................................... 8

4.2 Strengths and Limitations of Input-Output Methodology .................................. 10

4.3 Economy-wide value-added of IFC Finance .................................................... 11

4.4 Economy-wide employment of IFC Finance .................................................... 16

4.5 Value-added and employment generation multipliers ...................................... 20

5. Overall impact of IFC non-FIs Clients ................................................................. 23

6. The combined impact of IFC and “participant” financing ....................................... 24

Appendix I Model description ................................................................................ 28

I.1 Modeling approach ...................................................................................... 28

I.2 Production Function .................................................................................... 28

I.3 Social Accounting Matrix .............................................................................. 29

I.4 Assumptions .............................................................................................. 30

Appendix II: Overview of sectors ........................................................................... 32

About the Authors - Steward Redqueen and Ethan B. Kapstein .................................. 34

Side Boxes:

Qualitative Impact of Advisory Services

Public-Private Partnership on Airport Development

Jordan Inspection Reform

Qualitative Impact of IFC Investment

2

Executive summary

In pursuing its goal of social and economic development by investing in the private sector,

the International Finance Corporation (IFC) seeks to understand how it can most

effectively contribute to job creation and poverty reduction. This socio-economic impact

assessment of IFC’s investments in Jordan models the economy-wide effects of IFC’s

financing to and private sector companies and Jordan-based banks on value-added and

job creation. This study is part of a pilot project which involves a companion assessment

conducted in Ghana along with two pro-forma analyses conducted for the IFC in Sri Lanka

and Tunisia.

The objective is to quantify IFC’s socio-economic impact in Jordan. As a lender to the

country’s financial and non-financial enterprises, the IFC is expected to influence Jordan’s

economy, but the size of its “multiplier effect” on such variables as job creation, GDP

contribution, and tax revenue cannot be estimated in the absence of formal modeling. On

the basis of the modeling approach adopted here, we find that, as of 30 June, 20111:

1. As of June 30, 2011 IFC had $297 million outstanding capital with Jordanian

financial institutions (FI) clients and private sector companies (non-FIs);

2. Owing to these lending activities, IFC in 2011 was directly and indirectly associated

with supporting2 at least 9,100 jobs (0.6% of the employed labor force)3;

3. Through this $297 million of outstanding financing the IFC contributes, directly and

indirectly, at least $212 million in value-added to the Jordanian economy. This is

equivalent to 0.8% of Jordan’s GDP;

Around half of $212 million in value-added is profit for companies

amounting to $94 million;

Private households benefit from at least $91 million of salaries and incomes

associated with IFC financing in Jordan;

The government benefits in the form of $28 million in tax revenues

generated as a result of IFC financing;

4. Besides these quantifiable impacts, the IFC is playing a significant developmental

role in the Jordanian economy by helping to mobilize international capital on behalf

of the nation’s growth; by boosting confidence in Jordan’s economic future through

long-term financing; and through its advisory services;

5. Generally, investing into FIs impacts the local economy to a larger extent in

absolute figures but financing non-FIs has the potential to raise productivity levels

relatively more.

1 The data generated in this report results “best estimated” based on the available macro-economic and firm-level information. 2 The term “supports” means that not all of the jobs or value-added would necessarily vanish if IFC had not invested in its clients, since other lenders may have provided the same level of financing. Please also notice the difference between “creation” and “support”; “creation” indicates a net or incremental change and “support” refers to an associated economic impact at a given point of time. 3 The term “associated with IFC financing” means that not all of the jobs or value-added would necessarily vanish if IFC had not invested in its clients. Other lenders may have provided the same level of financing.

3

6. Based on the methodology applied, we find that certain tensions may arise

between supporting absolute amounts of employment and the GDP contribution of

each of those jobs. In particular, there are trade-offs between lending to firms and

sectors which generate more employment but lower value-added per job (e.g.

agriculture) and lending to enterprises that generate fewer employment but greater

value-added per job (e.g. large-scale manufacturing).

7. Investing into capital abundant companies is likely to lead to relatively few

additional jobs in the short term, but those investments may have the greatest

potential to bring about long-term “transformational” effects.

8. Whereas the same tradeoffs as described above also apply to financing provided to

FIs, when comparing investments into non-FIs and FIs we generally find larger

multipliers for FIs investments. This can be explained by FIs having a wider spread

of companies in their portfolios while IFC supported non-FI companies tend to be

larger, more productive firms.

9. We recommend to IFC’s management that it is crucial to recognize the various

trade-offs that may exist when it comes to making investment decisions (e.g.

between short-run and long-run impacts, or between employment generation and

value-added creation). The IFC should therefore consider shaping a portfolio of

investments that helps advance its overall objectives in Jordan.

We stress that, while the underlying methodology used for this study, input-output

modeling, lets us quantify the wider socio-economic impact of IFC investments on various

sectors, it also has its limitations. Financing provided to individual sectors has been

translated into output, using a linear Leontief or fixed production function assuming

constant returns to input. But this might not always be the case. In particular any

“transformational” effects of IFC financing cannot be quantified this way. Moreover, the

study works with sectors’ average productivity and spending patterns. It does not take

into account differences between company sizes or the formal/informal sectors. Table 1

summarizes the main findings whereby we distinguish effects of IFC itself and the effects

for participants, other lenders than IFC that contributed as well.

Table 1: Outstanding Finance (30 June 2011) and associated impact findings

IFC

Client SegmentOutstanding Finance

in $ mlnAssociated Value Added

in $ mlnAssociated Employment

in ‘000 jobs

Direct/Indirect Induced Effect Direct/Indirect Induced Effect

NON-FIs 243.7 90.5 30% 3.4 45%

FIs 52.8 122.0 33% 5.6 40%

TOTAL 296.5 212.5 32% 9.1 42%

Participants

TOTAL 138.7 37.5 32% 3.2 21%

4

1 Introduction, Objectives and Scope

Employment creation is among the key contributions that the private sector can make to

poverty reduction. The specific policy interventions that are most likely to induce the

private sector to make investments in job creation, however, remain elusive. Even in the

industrial world these interventions remain a topic of ongoing debate, which of course has

been renewed in wake of the financial crisis of 2008-2009. In the developing world, where

economic growth has remained stronger in recent years, job creation has nonetheless

lagged in many economies. This is a particularly critical issue in those places where more

youth and women may be expected to enter the labor market in coming years, as in the

Middle East and North Africa (MENA). In light of these developments and challenges, the

IFC seeks to sharpen its understanding of the effects of its investment and advisory

activities on job creation and value-added (defined as corporate profits, household

incomes, and taxes).

The objectives of this study are to gain some general insights about the channels through

which the private sector contributes to job creation and poverty reduction, and more

specifically to quantify the impact that can be attributed to the IFC’s activities on job

creation in Jordan. Quantifying the impacts of a corporation on an economy can help

management decision-making by:

1. Anticipating the ex-ante estimate of potential effects by providing insights into the

scale of effects of various investments on the local economy designed to have

bolstering (positive) impacts;

2. Engaging IFC’s various stakeholders (including government agencies, non-

government organizations, and private sector managers and employees), in

discussions about how to improve IFC’s economic impacts, based on a realistic

interpretation of facts.

The economic impacts discussed in this report arise from IFC’s investments into non-FI

and FI clients in Jordan. Furthermore, the economic impacts of IFC’s advisory services,

and non-quantitative impacts of IFC’s investments are included as side boxes in a

qualitative manner. The report also contains some suggestions to IFC’s management.

2 Jordan’s economy

With a Gross Domestic Product (GDP) of about $37.4 billion (PPP terms) in 2011, or

$6,000 in terms of income per capita, Jordan’s economy is among the smallest in the

Middle East and North Africa (MENA) region. Given its limited supplies of domestic natural

resources Jordan must import such commodities as petroleum, while its major sources of

foreign exchange include tourism, the export of goods and services (such as textiles), and

foreign aid. As a consequence of this economic structure, the economy is highly vulnerable

to external shocks, such as occurred with the “Arab Spring” of 2011 and its continuing

aftermath in the region, which has led to a reduction in tourism, a disruption in oil imports

from Egypt, and a rise in unemployment and government spending. At the present time,

some of the major economic challenges facing the government include high rates of

poverty (about 14% of the population lives below the poverty line), unemployment (the

official rate is 12.5%), inflation (which ran at 6% in 2011), and a large debt burden equal

to more than 60% of GDP. While Jordan’s King Abdullah has engaged in significant

economic reforms since attaining the throne in 1999, such as seeking membership in the

5

World Trade Organization, reducing or eliminating some subsidies, privatizing state-owned

companies, and actively attracting foreign investment, and while these reforms helped

spur economic growth, there are continuing demands among some segments of Jordanian

society for deeper political reforms as well. Further, not all of the economic reforms have

been well received, especially in light of the country’s unemployment and poverty levels.

An influx of foreign aid, especially from Gulf countries, has helped to offset the nation’s

economic pressures to some extent, but action is still needed to deal with the

deteriorating fiscal situation. On the brighter side of the economic ledger, Jordan's

financial sector has been relatively isolated from the international financial crisis that have

caused global turmoil since 2008, in part because of its limited exposure to overseas

capital markets. Nonetheless, the country suffered a “credit crunch” in the wake of the

crisis, highlighting the importance of investment from organizations like the International

Finance Corporation. Table 2 summarizes some key economic indicators of Jordan.

Table 2: Key indicators of the Jordanian economy in 2011

Population (2011) 6.1 million

Labor force 1.6 million

Gross Domestic Product (PPP) $37.4 billion

GDP per capita (PPP$) $6000

Sector breakdown of GDP

Agriculture 3%

Industry 31%

Services 67%

Consumption breakdown of GDP

Private consumption 85%

Government expenditure 21%

Real investment 15%

Exports 45%

Imports 66%

Source: The World Bank database

6

Exhibit 1: Gross Capital Formation (GCF) and Foreign Direct Investment (FDI) as

percentage of GDP4

Exhibit 2: Growth of real Gross National Income (GNI) per capita5 in current $

2.1 Jordan’s Financial Structure

The Jordanian banking system comprises the Central Bank of Jordan and over 20 licensed

banks, including:

13 local, conventional banks (most of which have some foreign ownership

and all of which are traded on the Amman Stock Exchange);

2 local Islamic banks;

8 branches of foreign banks, 5 of which are from Arab countries.

While the five largest banks continue to dominate the market, their share of deposits and

assets has decreased in recent years with rising competition. The Jordanian banking sector

is relatively well-capitalized. It did not suffer a great deal directly from the financial crisis

4 Source: The World Bank database 5 World Bank data

0

5

10

15

20

25

30

35

40

2005 2006 2007 2008 2009 2010

Foreign direct investment, net inflows (% of GDP) Gross capital formation (% of GDP)

in %

-

1.000

2.000

3.000

4.000

5.000

6.000

7.000

2005 2006 2007 2008 2009 2010

GNI per capita, PPP (current international $) GNI per capita, Atlas method (current US$)

7

that began in 2008 owing to its limited international exposure, including to such relatively

proximate financial centers like Dubai. Returns on equity of nearly 14% also indicate the

continuing profitability of this sector. According to the International Monetary Fund,

however, the country did suffer a “credit crunch” during the crisis owing to tightened

credit conditions, highlighting the importance of international lenders like the International

Finance Corporation. Traditionally, the vast majority of banking activity has centered on

the capital city of Amman and other regions have been less well-banked. Financial activity,

however, is spreading and the banking system now has over several hundred branches

throughout the country. In terms of lending practices, the banks operating in the

Jordanian environment have traditionally been conservative. As a result, access to small

and medium-sized enterprises (SME) finance is, compared to other countries in the region,

particularly constrained in Jordan.

3 IFC’s operations in Jordan

The total amount of financing that IFC is investing into the Jordanian economy has in 2011

been about 13 times as much as in 2006 ($23 million). Historically interesting is that non-

FI investment has always been higher than FI investment, where from around 2008 the

gap between the two investment channels widens. IFC’s Jordan outstanding loan portfolio

is depicted in Exhibit 3.

Exhibit 3: IFC’s outstanding loan amount over time (in $ million)

As of June 30, 2011 IFC had loans worth $2976 million outstanding with Jordanian clients.

Some of this money is invested directly into Jordanian companies (non-FIs) and some is

invested indirectly through financial institution (FIs). Table 3 provides an overview of

channels used. In addition to the outstanding loan amount, IFC has committed but not yet

disbursed capital accounting to $198 million. This amount has been excluded from the

study. At a more micro-level, the IFC supports local industry by providing financing to (i) a

pharmaceutical; (ii) phosphate and silica mines and (iii) a power distribution company.

6 Please note that $1.5 million outstanding in the Jordanian apparel industry have been excluded from the study

$ -

$ 50

$ 100

$ 150

$ 200

$ 250

$ 300

$ 350

2006 2007 2008 2009 2010 2011

Total IFC NON-FI FI

in mln

8

The services sector is supported by financing to (i) a transportation firm, (ii) a tourism

investment holding and (iii) the operator of Amman’s airport. Describing the

characteristics of the IFC’s clients, generally it holds that compared to FI portfolio

companies, non-FI clients tend to be bigger internationally operating firms with higher

productivity levels. This is especially true for the difference between non-FI clients and

firms supported by microfinance institutions, as well as SMEs in the portfolio of the FIs.

Portfolio clients of FIs tend to include more typical Jordanian firms, which are smaller, less

capital intensive organizations. IFC does not directly invest into SMEs in Jordan as it does

not have the capacity to assess the viability but through its FI investments targets SMEs

as FI operating in the local context are assumed to have the capacity and coverage to

assess the needs of SMEs.

The methodological approach applied for this study takes a picture in time rather than

taking into account a development over several years. The moment of time chosen to

conduct the study is June 30, 2011, the most recent end of IFC financial year figures.

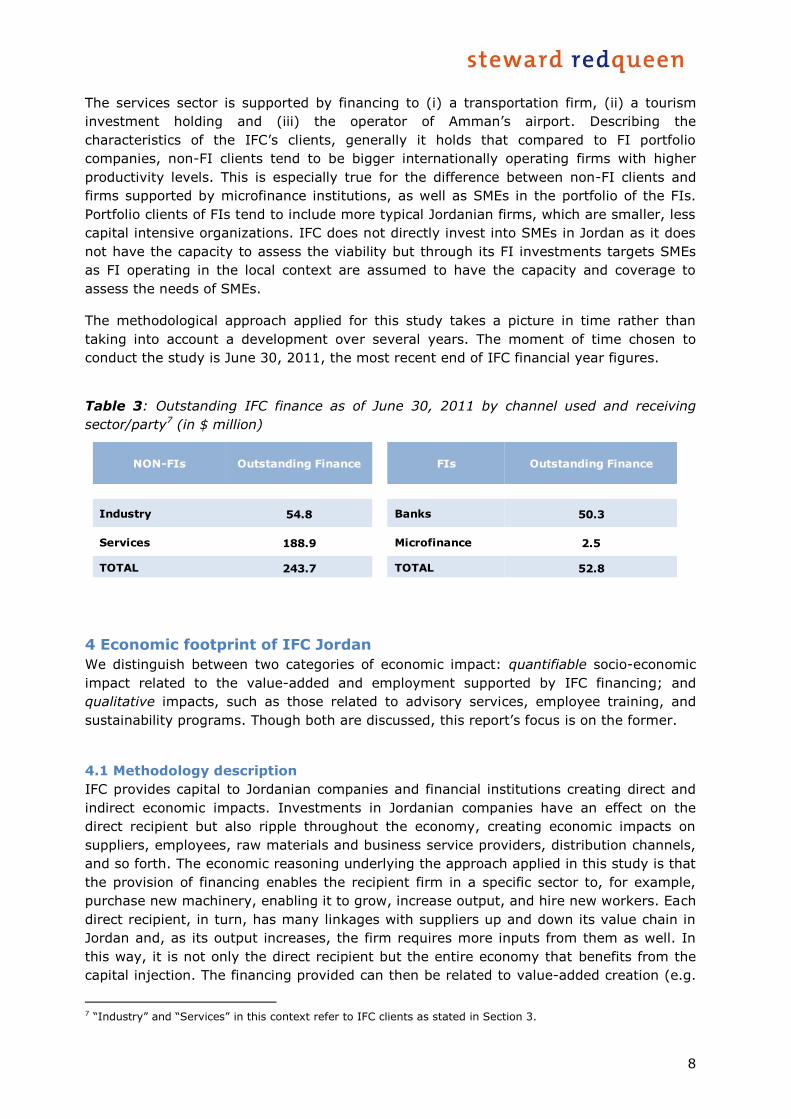

Table 3: Outstanding IFC finance as of June 30, 2011 by channel used and receiving

sector/party7 (in $ million)

4 Economic footprint of IFC Jordan

We distinguish between two categories of economic impact: quantifiable socio-economic

impact related to the value-added and employment supported by IFC financing; and

qualitative impacts, such as those related to advisory services, employee training, and

sustainability programs. Though both are discussed, this report’s focus is on the former.

4.1 Methodology description

IFC provides capital to Jordanian companies and financial institutions creating direct and

indirect economic impacts. Investments in Jordanian companies have an effect on the

direct recipient but also ripple throughout the economy, creating economic impacts on

suppliers, employees, raw materials and business service providers, distribution channels,

and so forth. The economic reasoning underlying the approach applied in this study is that

the provision of financing enables the recipient firm in a specific sector to, for example,

purchase new machinery, enabling it to grow, increase output, and hire new workers. Each

direct recipient, in turn, has many linkages with suppliers up and down its value chain in

Jordan and, as its output increases, the firm requires more inputs from them as well. In

this way, it is not only the direct recipient but the entire economy that benefits from the

capital injection. The financing provided can then be related to value-added creation (e.g.

7 “Industry” and “Services” in this context refer to IFC clients as stated in Section 3.

NON-FIs Outstanding Finance FIs Outstanding Finance

Industry 54.8 Banks 50.3

Services 188.9 Microfinance 2.5

TOTAL 243.7 TOTAL 52.8

9

by transforming raw materials into finished products and thus corporate profits) and

employment generation throughout the Jordanian economy.

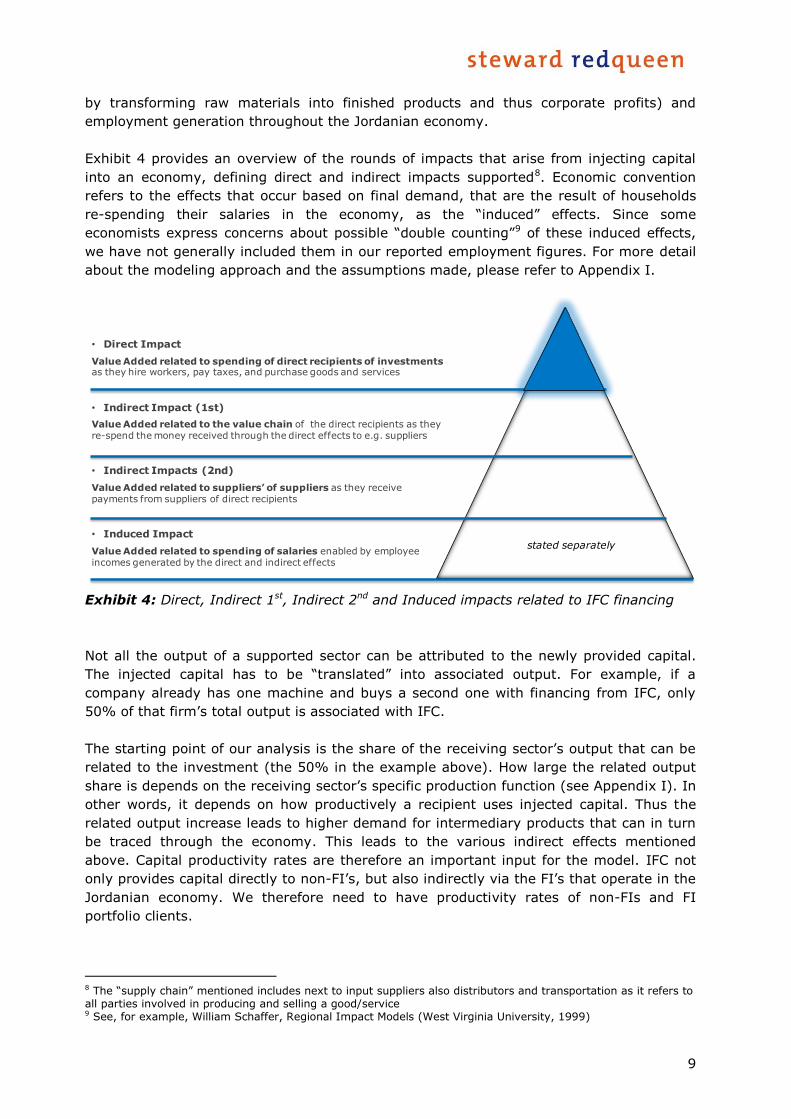

Exhibit 4 provides an overview of the rounds of impacts that arise from injecting capital

into an economy, defining direct and indirect impacts supported8. Economic convention

refers to the effects that occur based on final demand, that are the result of households

re-spending their salaries in the economy, as the “induced” effects. Since some

economists express concerns about possible “double counting”9 of these induced effects,

we have not generally included them in our reported employment figures. For more detail

about the modeling approach and the assumptions made, please refer to Appendix I.

Exhibit 4: Direct, Indirect 1st, Indirect 2nd and Induced impacts related to IFC financing

Not all the output of a supported sector can be attributed to the newly provided capital.

The injected capital has to be “translated” into associated output. For example, if a

company already has one machine and buys a second one with financing from IFC, only

50% of that firm’s total output is associated with IFC.

The starting point of our analysis is the share of the receiving sector’s output that can be

related to the investment (the 50% in the example above). How large the related output

share is depends on the receiving sector’s specific production function (see Appendix I). In

other words, it depends on how productively a recipient uses injected capital. Thus the

related output increase leads to higher demand for intermediary products that can in turn

be traced through the economy. This leads to the various indirect effects mentioned

above. Capital productivity rates are therefore an important input for the model. IFC not

only provides capital directly to non-FI’s, but also indirectly via the FI’s that operate in the

Jordanian economy. We therefore need to have productivity rates of non-FIs and FI

portfolio clients.

8 The “supply chain” mentioned includes next to input suppliers also distributors and transportation as it refers to all parties involved in producing and selling a good/service 9 See, for example, William Schaffer, Regional Impact Models (West Virginia University, 1999)

stated separately

• Direct Impact

Value Added related to spending of direct recipients of investments as they hire workers, pay taxes, and purchase goods and services

• Indirect Impact (1st)

Value Added related to the value chain of the direct recipients as they re-spend the money received through the direct effects to e.g. suppliers

• Indirect Impacts (2nd)

Value Added related to suppliers’ of suppliers as they receive payments from suppliers of direct recipients

• Induced Impact

Value Added related to spending of salaries enabled by employee incomes generated by the direct and indirect effects

10

For non-FIs (outstanding finance equal to $244 million) these can be obtained based on

the production functions of IFC clients for which balance sheet information is available

within the IFC’s system. This approach takes per company differences into account.

For FIs (outstanding finance equal to $53 million), balance sheet information for each of

the portfolio companies is not readily available. For FI’s productivity rates we hence adapt

an alternative approach to obtain those rates. Namely, we use production functions10 of

Jordan’s agricultural, industrial and services sectors in order to “translate” that investment

into output. We have assumed that the IFC’s capital has been spread equally over the

bank’s entire lending portfolio.

4.2 Strengths and Limitations of Input-Output Methodology

The major advantage of the methodology applied in this study is that it allows one to

quantify the wider (direct, indirect and induced) impacts of investing in various economic

sectors, both directly and through FIs, and both in terms of associated value-added (or

contribution to GDP growth) and jobs. It is a rigorous, widely-accepted academic method

(for which Leontief won the 1973 Nobel Prize).

However, it does have the following limitations (see Appendix I for details):

(i) Given that the analysis is conducted for a specific moment in time, it does not take

into account any structural changes of the economy (e.g. increased productivity);

(ii) Estimates are based on historical relations, that is, based on the most recent

(macro) economic data available;

(iii) Equity and debt are treated the same way;

(iv) No differentiation is made by size, and hence productivity, of firms within a sector;

(v) It does not take into account the effects of IFC’s advisory services (some examples

are therefore covered qualitatively in boxes);

(vi) IFC’s investments are treated as investments from any other lender and it has been

assumed that IFC’s financial support does not affect the relations of sectors within an

economy.

Structural changes could be triggered by increasing productivity (e.g. reducing

unnecessary or onerous business regulations, or improving power supply or transport

infrastructure, which allows many firms to be more productive). Structural changes could

also be brought about by increasing worker skill levels. So for example productivity in

IFC’s direct real-sector clients would be captured in this study, but productivity

improvements of their suppliers would not.

Where IFC works with client companies to strengthen local linkages this would not be

captured in this study. We have evidence from a more in-depth evaluation we conducted

for a mining project in Ghana (see Section 4.3), that IFC’s supply chain linkage program

and community development program contributed to significantly stronger effects on the

local economy than is usually seen in mining projects.

10 Output and credit facility figures per sector (2009) have been obtained from the Statistical Office of Jordan and the Central Bank of Jordan

11

The proportion of the firm’s revenues that can then be “attributed” to the outstanding

finance is equal to the share or proportion of newly provided financing out of the

borrower’s total capital. This means that the various types of financing provided to the

recipient (e.g. debt, equity or instruments such as guarantees) have been treated in the

same way in terms of their impact on the sector’s capital structure, and thus their ability

to generate more output11. This is likely to underestimate the impact of equity financing,

as this is generally assumed to allow companies to raise additional capital. This particular

limitation of input-output modeling will therefore mean results presented are somewhat

conservative. Similarly, the approach taken in this study does not allow differentiation

between long- and short-term finance provided.

As the model relies on sector average productivity rates, differentiating the impact of

investing in different sizes of company (e.g. large corporates, which are generally more

productive, compared with investing in smaller SMEs) cannot be addressed. The same

applies to direct financing versus indirect financing via FIs, where company size is one of

the factors explaining the different extent of related impacts.

IFC’s advisory services can help improve the investment climate, increase access to

finance and infrastructure, attract private investment into sectors previously often

dominated by the public sector, and strengthen the operations and local linkages of IFC

client companies. We have not tried to capture these effects quantitatively, but clearly

they can be significant and we provide some qualitative descriptions of such projects.

Finally, IFC’s investments are often “first-of-a-kind” investments (e.g. Queen Alia

International Airport and IFC’s investment in the Ghanaian oil industry). These can have

important demonstrative effects, leading to subsequent investments (e.g. further

development of an industry; similar “public-private partnerships” in other sectors; etc).

These effects were not quantitatively captured in this study, but could clearly be

significant. Therefore where IFC can bring about such “transformations”, either through

investments or advisory services, other assessment methods will be more appropriate.

4.3 Economy-wide value-added of IFC Finance

Table 4 shows how IFC’s investment relates to the output of recipient firms. The share of

total revenues of particular sectors and companies that can be associated with IFC is to a

large extent determined by the capital-output ratio12 of the sector’s or firm’s production

function; obviously, one unit of capital added to a capital intensive company or sector has

relatively little effect compared to one unit of capital provided to a relatively capital scarce

company or sector. The output-to-capital ratios presented below are the average ratios

but not the weighted average figures.

11 Assume a company has assets with a book value of $100, revenues of $200 and a loan from IFC of $15, this would mean that 15% of 200 = $30 in revenues are attributed to IFC. Technically this assumption implies that the asset turnover (sales/assets) of companies remain constant when the company grows. 12 Defined as the value of fixed production assets per unit of output

12

Table 4: “Translation” of IFC input (as of June 30 2011) into client output

Table 4a: non-FIs (in $ millions)

Table 4b: FIs (in $ millions)

Comparing the output per capital ratios for non-FI and FI companies, it becomes obvious

that FI portfolio clients are less productive. That means that in those companies relatively

more capital is needed to produce one unit of output. At the same time, it shows that

those companies are less capital intensive than non-FI clients. It appears to be related to

a possible IFC selection bias, choosing the large and productive companies.

Taking IFC related output presented in Table 4 as our starting point, Exhibit 5 provides an

overview of the direct, indirect and induced impacts related to IFC’s financing in Jordan.

This has been achieved by tracing the attributable output to the local economy.

Attributable Output

Client Segment Outstanding Finance Output per Capital Ratio Output Increase

NON-FIs & FIs 296.5 1.9 298.5

NON-FIs Attributable Output

Client Segment Outstanding Finance Output per Capital Ratio Output Increase

Agriculture - - -

Industry 54.8 0.7 38.5

Services 188.9 0.8 80.6

Households - - -

TOTAL 243.7 119.0

FIs Attributable Output

Client Segment Outstanding Finance Output per Capital Ratio Output Increase

Agriculture 5.4 5.3 28.6

Industry 16.9 6.2 105.0

Services 11.2 2.4 26.6

Households 19.3 - 19.3

TOTAL 52.8 179.4

13

Exhibit 5: Break down of value-added associated with IFC’s investments ($ millions)

The total value-added that is associated with IFC’s investments in Jordan sums up to at

least $212 million. Relative to Jordan’s GDP this is about 1.0% (see Table 2). The majority

of this value-added arises as profits to companies ($94 million), at least $91 million is

earned by employees, and the government benefits from the remaining $28 million (13%)

in form of taxes. Almost $120 million of the total value-added impact shown in Exhibit 5

arises directly at the non-FI receiving companies or at the portfolio companies of the FIs.

$47 million of value-added can be associated with the value chains (Indirect 1st) of the

direct recipients and $46 million is related to the suppliers of the direct recipients’

suppliers (Indirect 2nd).

In order to gain some insights into the sectors of the Jordanian economy that benefit from

IFC’s investment, Exhibit 6 provides an overview of the total value-added related to IFC’s

non-FI lending per sector. IFC’s classification distinguishes more sectors than the sectoral

division but has not been applied in this exercise. The capital and labor productivity rates

that would be required per sector are only available at a less detailed level. While the

GTAP database differentiates 57 sectors, macro-economic employment figures are only

collected for 14 sectors which not all correspond with GTAP sectors. Data on jobs per

economic sector is essential when determining, in conjunction with output figures, the

labor productivity per sector. This in turn determines the amount of supported

employment. Based on the lack of employment data it is hence not possible to break down

the sectors at a more detailed level even though this would be desirable. For non-FI

investment, where capital productivities are known at a firm level (see Section 4.1) the

impact can be distinguished for 14 sectors13. In principle the same limitation holds for FI

investment where however the impact of investments can only be differentiated for three

sectors (agriculture, industry, services). That is because of limited information on capital

productivity rates on sector level that takes into account productivity differences between

13 Here smaller sectors have been grouped together yielding a total of 9 sectors shown

Total

280.0

119.3

46.9

46.3

67.5

Tax income

36.7

16.7

9.0

Profits

122.4

54.9

20.0

19.0

28.6

Households income

120.8

47.8

20.5

22.6

29.9

Direct Impact

Indirect Impact 1st

Indirect Impact 2nd

Induced Impact

USD 212 million

USD 94 million

USD 91 million

USD 28 million

14

various firm sizes. That means that the direct effects from FI investing are bundled in the

three main sectors whereas in reality FI portfolios are broader spread.

Exhibit 6: Value-added per economic sector and channel ($ millions)14

Exhibit 6 also distinguishes the value-added related to non-FI financing compared to FI

financing where sectoral differences arise due to differences in lending portfolios and due

to value-added intensities of sectors. The total of $212 million corresponds to the total

value-added with IFC’s financing in Exhibit 5 ($281 million when considering induced

effects as well) whereby most value-added arises in the service and industry sectors.

IFC’s non-FI investments are diversified over various economic sectors in Jordan (see

Table 4). They include the pharmaceutical and the phosphor industry, tourism,

transportation and utilities. IFC has no direct investments into the agricultural sector in

Jordan, the majority of the value-added arising in that sector is caused by IFC’s

investment into FI-clients who in turn have agricultural businesses in their portfolios. Even

though IFC has not invested into agricultural directly, the fact that some IFC’s non-FI

clients have agricultural suppliers and arising third round impacts lead to some small

value-added effect ($0.7 million) of non-FI clients on agriculture. For multipliers per sector

please refer to Table 6. Exhibit 7 shows a somewhat different breakdown distinguishing

the round of impact.

14 For a full definition of sectors please refer to Appendix II

Mining

14.8

Trade

16.1

6.4

9.7

Agriculture

17.0

16.35.7

Business Services

37.9

30.4

7.5

Transport

46.9

10.4

36.5

Manufacturing

49.8

38.7

11.1

Public Services

Utilities Construction

12.6

9.0 8.3

6.92.7

7.7

12.36.4

Effect of Finance given to FIs

Effect of Finance given to NON-FIs

122

NON-FIs FIs

21291

15

Exhibit 7: Value-added per economic sector distinguishing the round of impact (in $

millions)

To the extent that investment decisions are made with the aim of strengthening local

supply chains, Exhibit 7 gives some indication on which sectors are more suitable than

others.

Impact of IFC’s Advisory Services:

Public-Private Partnership on Airport Development

The government of the Hashemite Kingdom of Jordan (GoJ) sought to invite private sector

participation in the expansion and rehabilitation of the Queen Alia International Airport (QAIA) in

Amman and appointed IFC as its lead advisor for structuring and implementing a balanced

transaction. The objective was to increase the terminal's capacity, develop it as a regional hub,

increase service-quality standards to align with international best practices, and ensure revenue

flows for the Government. As advisor to the GoJ, IFC was involved in a wide range of activities

among which the airport design, transaction structuring, being the intermediary of the

negotiations between the GoJ and potential investors to best allocate risks, and working with the

GoJ to implement the necessary changes in the legislative and regulatory frameworks for a timely

and successful project implementation.

IFC was able to implement the project in thirteen months, the fastest project implementation of

Public Private Partnerships with IFC engagement. The price achieved, 54.58% of gross revenue to

the Government on average, is the highest recorded arrangement of this kind in the world. The

project is estimated to create (i) concession income of over $2.5 billion for the Government (NPV,

10% discount rate: $800 million), (ii) mobilize over $1 billion in foreign direct investment over

the life of the project, which is the largest private sector transaction to date in Jordan, (iii) to free

$28 million per annum (over the life of the project) of the Government’s budget (NPV, 10%

discount: $285 million) and to (iv) create over 23,00015 jobs for the local economy.

Following the selection of the winning bidder, IFC also provided financing to the project in the

form of loans of US$120 million. In addition, IFC mobilized US$160 million in loans from

15 IFC Calculations taken from TAAS Completion 9/20/2007 Report, Project ID 24706

Business Services

37.9

19.2

Transport

46.9

29.5

9.7

7.8

Manufacturing

49.8

25.5

13.4

10.9

Agriculture Trade Mining Public Services

Utilities Construction

13.2

17.0

8.7

16.1

11.4

14.8

6.4

12.6

4.3

9.0

6.3

8.35.04.0

12.8

5.9

3.3

47 46

Direct Impact Indirect Impact 1st Indirect Impact 2nd

212119

Direct Impact

Indirect Impact 1st

Indirect Impact 2nd

16

international commercial banks.

This project provides an excellent example of the IFC’s “additionality” in the development finance

space. From a financial standpoint, the IFC was able to provide longer-tenor loans than are

generally available in Jordan, and its presence in this project also helped mobilize additional

capital from international banks, including in the form of Islamic financing. From a non-financial

standpoint, the IFC’s “stamp of approval” for the Airport project gave a confidence boost to

foreign investors, and it further signaled that the Government of Jordan was indeed serious about

pursing an ambitious privatization program.

4.4 Economy-wide employment of IFC Finance

The Jordanian Department of Statistics (DOS)16 publishes information on “Employees and

Enterprises by Economic Activity” that cover the size and allocation of the employed labor

force in Jordan. Based on the size of the employed labor force and output per sector

(2009) obtained from the DOS we determined the employment intensity for 11 sectors in

the Jordanian economy. As the DOS also collect data on the skill level and gender of

people employed, the results distinguish those indicators as well.

Employment associated with IFC’s investments in Jordan has been determined based on

these inputs, and the results shown in Exhibit 8. We emphasize that the total impact of

9,100 associated jobs17 (0.6 % of employed labor force) reported here excludes 3,800

jobs that are related to the induced effect of re-spending of household incomes.

Exhibit 8: Breakdown of employment associated with IFC’s investments per sector and

channel (in thousands)

16 http://www.dos.gov.jo/dos_home_e/main/index.htm 17

Jobs results are presented in terms of full time equivalent employment

Public Services

0.4

Transport

0.7

0.6

Agriculture

1.0

0.9

Business Services

1.1

0.9

0.2

Trade

2.2

0.9

1.3

Manufacturing

2.8

2.2

0.6

Utilities Construction Mining

0.40.3 0.2

0.30.20.3

0.2

Effect of Finance given to FIs

Effect of Finance given to NON-FIs

Effect of NON-FIs Effect of FIs

9.13.4 5.6

17

Most of the jobs associated with IFC’s finance arise, just as with the value-added, in the

service and industry sectors. This is due to the allocation of the portfolio and the specific

employment intensities per sector. The employment intensity indicates how much labor is

employed in order to produce one unit of output. In labor intensive sectors, like the

agricultural sector, one would expect a higher intensity. Keeping in mind the total

amounts invested into non-FIs ($244 million) in comparison to the amount invested into

FIs ($53 million) presented in Table 4, the number of jobs associated with one unit of

capital invested through the two different channels varies quite significantly. The

multipliers are discussed in more detail in Section 4.5.

Exhibit 9: Breakdown of employment per sector over various rounds associated with IFC’s

investments (in thousands)

In Exhibit 10 the related 9,100 jobs are broken down by skill level of employees and by

gender of the employee, where the female labor force seems to be relatively higher

educated. In general, male employees are dominating the Jordanian labor market.

Business Services

1.1

0.5

Trade

2.2

1.2

0.6

0.5

Manufacturing

2.8

1.4

0.8

0.6

Agriculture Transport Public Services

Utilities Construction Mining

0.8

1.0

0.4

0.70.3

0.4

0.2

0.4

0.2

0.3

0.2

0.2

0.2

0.2

0.2

Direct Impact Indirect Impact 1st Indirect Impact 2nd

9.15.0 2.1 1.9

Direct Impact

Indirect Impact 1st

Indirect Impact 2nd

18

Exhibit 10: Gender and skill breakdown of employment associated with IFC’s investments

(in thousands)

The absolute numbers presented in Exhibit 8 and 9 tell only one part of the job creation

story. A tradeoff occurs between the amount of employment and the type of employment.

High multipliers can also be an indicator of economic inefficiency, as relatively a lot of

labor is needed to produce a fixed amount of output and value-added. Hence, depending

on the sector where the employment is supported, not all the jobs are equally productive.

In order to reflect the different levels of productivity that characterize the Jordanian

economy, Exhibit 11 provides a view on the quality of employment by showing the value-

added per employee and sector. The surface area of the blocks indicate the total value-

added18 per jobs for each of the sectors.

Exhibit 11: Value-added per job associated with IFC financing in various sectors (in $)

18 Including arising induced effects

Legislators, Senior Officials & Managers, Clerks.

Service Workers & Shop & Market Sales Workers, Skilled Agricultural & Fishery Workers, Craft & Related Trades Workers. Plant & Machine Operators & Assemblers, Elementary Occupations.

Total

9.1

2.3

4.1

2.7

Female

0.7

0.10.4

Male

8.4

2.2

3.9

2.3

Low

Medium

High

5432 13121110

0

Value added per job(USD)

Number of Jobs (‘000)

9

Trade

7,328

Agriculture

17,320

Industry

20,871

30,682

10,000

65,645

40,000

20,000

30,000

50,000

1

60,000

70,000

876

32,701

Jordanian Average

ConstructionTransport Services

19

The difference in value-added per job is mostly related to the degree of efficiency and

productivity of the respective sectors in Jordan. The average GDP per worker in Jordan is

$17,75019. Not surprisingly, workers in the trade and agricultural sectors generally

contribute less to the Jordanian GPD than this figure. With the development of the Queen

Alia Airport in Amman, the Port of Aqaba and additional investment plans into the rail

system20, Jordan has reinforced its transit position of transportation between Europe, the

Middle East and the Gulf. The importance and competitiveness of the transport sector are

then also reflected in the higher value-added per job in that sector. The Jordanian figure is

then also higher than figures from other countries from that region. Keeping this in mind,

short-run employment creation can be achieved by investing into labor intensive sectors

as agriculture and trade. On the long-run however taking into account development goals,

investment into efficiency improvements (which could entail job losses in the short run)

can contribute to a more sustainable and long lasting growth of an economy.

Impact of IFC’s Advisory Services:

Jordan Inspection Reform

Inspections are governmental mechanisms to ensure compliance in key areas such as health, safety and the environment and are carried out through visits conducted by government- appointed officials to private sector facilities and premises. In many developing countries,

inspections can be a time-consuming and expensive burden, affecting business productivity and deterring owners from joining the formal economy if carried out poorly.

The IFC team supported the development of an inspection strategy covering the key pillars for inspection reforms such as planning, risk based targeting, human resources development, and process documentation and automation. IFC has also worked with the labor inspectorate as pilot inspectorate to implement leading practices. Reforms included the development of a quality

management system comprising inspection strategy and policy, an inspection organization structure, and a comprehensive operations manual with the needed standard operating procedures, forms and checklists. IFC has also delivered training courses to inspectors on newly developed procedures, inspection management, inspection skills, and communication skills to ensure the newly developed systems

is understood and properly implemented in a timely manner.

The project lead to increased efficiency of inspectorates and enhanced the transparency of

inspection operations and requirements through the implementation of improved regulations,

processes and procedures; and the adoption of risk-based inspection systems in addition to

awareness material to business owners. As a result of the rationalization of inspection processes,

the reforms are expected to result in $2 million21 in private sector savings per annum that will

increase the efficiency of businesses while at the same time ensuring high standards of labor and

working conditions.

19 GDP 2010 (27.6 bln USD)/ labor force 2010 (1.5 million) = 17.750 20 http://www.railwaygazette.com/nc/news/single-view/view/ambitious-strategy-ready-to-start.html 21 IFC Calculations ‘Jordan Inspection Reform: Lessons and Reflections’ by Wafa Aranki & Abeer Shalan

20

4.5 Value-added and employment generation multipliers

The results discussed in Sections 4.3 and 4.4 can be summarized by looking at how much

value-added and employment are associated with $1 million of financing (direct, indirect

and induced effects). In Tables 5 and 6 this has been done for the various channels and

economic sectors. The job multipliers in absolute figures presented below refer to direct

and indirect jobs supported per $1 million provided. Taking into account the induced

effects (presented as percentages of the direct/indirect multipliers) the total employment

and value-added multipliers per $1 million outstanding lending (direct + indirect +

induced) can be calculated. For non-FIs, the total job multiplier would hence be 14 +

(45% *14) = 20, meaning that on average 20 jobs are supported by providing $1 million

to the Jordanian economy when invested directly (non-FI client). The same multiplier

definition applies to the value-added and FI multipliers.

Table 5: Value-added and employment associated with $1 million financing

Table 6: Value-added and employment associated with $1 million financing

Table 5 shows that using indirect channels (FIs) to invest into companies leads to more

value-added and employment creation than investing through direct channels (non-FIs).

That is because the portfolios of financial institutions have a broader spread over the local

economy and are not focused on the largest, more capital intensive corporations. Direct

investment into non-FIs in Jordan is mostly focused on a few large, and mostly capital

intensive, companies. Adding one additional unit of capital here has only a marginal effect

on additional value-added and job creation. Similarly, Table 6 shows that the relatively

capital scarce agriculture sector has higher multipliers. Those higher marginal returns on

capital in the agricultural sector can be explained by the fact that it takes relatively little

capital to increase efficiency and productivity in the agricultural sector. Typically, the

agricultural sector encounters difficulties accessing finance as that sector is less formalized

than e.g. the industrial sector. IFC’s investment can overcome those obstacles and

contribute to value-added and employment creation to a large extent.

Channel

Economy-wide value added

related to $ 1 million

($ millions)

Economy-wide employment

related to $ 1 million

(number of jobs)

direct/indirect induced effect direct/indirect induced effect

NON-FIs 0.4 + 30% 14 + 45%

FIs 2.3 + 33% 107 + 40%

Weighted Average 0.7 + 32% 31 + 42%

Channel

Economy-wide value added

related to $ 1 million

($ millions)

Economy-wide employment

related to $ 1 million

(number of jobs)

direct/indirect induced effect direct/indirect induced effect

Agriculture 3.8 + 41% 207 + 42%

Industry 1.3 +32% 57 + 41%

Services 0.5 +30% 19 + 43%

Weighted Average 0.7 +32% 31 + 42%

21

If one was to differentiate the multipliers for non-FI and FI investments per sector, the

magnitude of the multipliers would still depend on productivity differences between

companies financed. As mentioned earlier, non-FI companies tend to be more capital

intensive where additional capital contributes relatively less, suggesting smaller multipliers

per sector for non-FIs compared to FIs.

As far as poverty reduction goals are involved, investment into agriculture offers a

possibility to create a relatively large number of jobs and therefore income to the low

skilled (given the low education levels required to work in agriculture). Similar effects can

be achieved by investing into other labor-intensive sectors like trade and distribution.

Reaching long-term development goals requires however raising levels of labor

productivity. This is more likely to be achieved by investments into larger non-FIs

companies operating in sectors that face international competition.

Compared to the results found in the socio-economic impact assessment conducted in

Ghana, the employment multipliers found for Jordan are considerably lower. This is for two

reasons. First, the IFC provides 60% of its financing in Ghana to FI clients compared to

40% provided to non-FI clients. This is different from Jordan where 80% of all outstanding

finance has been provided to non-FI clients. As described in Section 4.4, we find that

financing FIs generally supports more employment than investments in non-FI clients.

Second, higher multipliers in Ghana reflect the fact that producing in Jordan is relatively

less labor-intensive as the country is more capital abundant.

As pointed out earlier, the multiplier as presented above do not take into account any

“transformational” effects of IFC finance since those cannot be quantified using the

suggested approach. The World Bank Group’s Enterprise Surveys however offers another

way of looking at the impact that IFC investments into Jordan might have. Some 25% of

local firms identify access to finance as major constraint to doing business. Even though

this are relatively fewer firms than the 36% of total Sub-Saharan companies stating the

same, indicating that lack of financing is still an important issue in Jordan. Providing

finance can consequently be assumed to have substantial catalytic effects for the

development of the country. In addition, 24% of companies regard the supply of electricity

as a major constraint to growth. Investing into power plants, or power distribution

companies as the IFC is doing, hence can be thought of as being extremely relevant to

improve the playing field in which businesses operate contributing to value-added creation

relatively more than the multipliers in Table 7 suggest.

Table 7: Major business constraints as identified by Jordanian firms22

% of firm identifying as a major constraint: Jordan Middle East &

North Africa

Access to Finance 25.2 36.3

Electricity 23.7 47.7

Transportation 11.7 25.1

22 Source: World Bank Group Enterprise Surveys, Jordan, 2006

22

Presented with list of 15 business environment issues, managers (of 503 Jordanian firms)

got to choose the largest obstacles to their businesses. Exhibit 12 presents the results,

indicating areas in with IFC’s technical assistance programs can play an important role for

the progression of the Jordan.

Exhibit 12: Business obstacles in Jordan (percent of firms)23

Qualitative Impact of IFC Investment

Investing into client companies doesn’t only mean that the company benefits from additional

finance it receives, but the interaction with IFC also supports the companies in different ways.

As IFC requires some degree of professionalism, IFC clients progress during the interaction

process before reaching an agreement on the kind of collaboration and afterwards during the

investment period. So can the due diligence check required by IFC also be utilized for other (later)

purposes and might a company be required to write a new HR Manual, defining employee’s tasks

and positions. All of that contributes to a clients’ competitiveness in the global market.

In some cases, the IFC interaction next to contributing indirectly to society by investing into

companies, has a direct positive impact for Jordan’s citizens. IFC’s investment into an electricity

distribution company is an example for that where IFC’s finance has been used to build &

maintain a distribution network in remote areas of Jordan. Because of the high maintenance costs

and the few customers in that part of Jordan it is not very profitable to construct the network

there but with the support from IFC the company saw business opportunities there as well and

decided to serve those customers as well.

Having obtained an investment from IFC also serves as signal to potential clients or other

investors underlining the trustworthiness of the company. That way the company can distinguish

itself from competitors.

Whereas the sections above have focused on IFC’s contribution to impacts related to the

companies invested in, the two following sections focus on the overall economic impacts

associated with IFC clients and the contribution of third party finance that was mobilized

with the help of IFC.

23 Source: World Bank Group Enterprise Surveys, Jordan, 2006

4

6

6

6

8

9

9

9

11

25Business licenses and permits

Tax administration

Inadequately educated workforce

Access to land

Tax rates

Political instability

Corruption

Labor regulations

Practices of the informal sector

Access to finance

23

5. Overall impact of IFC non-FIs Clients

Irrespective of IFC’s financing, companies operating in the Jordanian economy impact their

local environment by purchasing local goods and services, paying taxes and employing

local employees. The impact that can be associated with the total operations of all non-FI

clients of IFC in Jordan is estimated in Exhibit 13. The starting point for this analysis is the

entire output of the companies and not, in comparison to the results presented in Exhibit 5

and 6, just the output share that can be related to IFC finance. In other words, the share

of IFC on the total IFC non-FI clients’ impact equals $94 million (Exhibit 6), whereas

Exhibit 13 depicts the entire impact of IFC’s non-FI clients. That means that IFC’s part of

the value-added related to the non-FI clients is on average some 7%, which is comparable

to IFC’s share of the total assets of those firms. The companies that IFC finances

indirectly, through FIs, also of course contribute to the Jordanian GDP and national

employment, but assessing their total output would require an investigation of each

portfolio company which is beyond the scope of this study.

Exhibit 13: Overall value-added of non-FIs supported by IFC (in $ million)

Total

1,736.1

836.6

210.9

306.2

382.4

Tax income

188.9

75.8

50.8

Profits

862.3

483.8

90.3

126.3

162.0

Households income

684.9

277.0

93.6

144.7

169.7

Direct Impact

Indirect Impact 1st

Indirect Impact 2nd

Induced Impact

USD 1,354 million= 6% of GDP

USD 700 million

USD 515 million

USD 138 million

24

Exhibit 14: Overall employment of non-FIs supported by IFC (in thousands)

Comparing the results of Exhibit 8 (non-FI results only) with the ones presented in Exhibit

14 indicates that the IFC’s contribution is equivalent to about 7% of the overall impact of

the companies on the Jordanian economy. That is in line with the share of IFC’s

outstanding loan amount as a percentage of the total assets of the clients (10%) and the

share of IFC related output to total output of the clients (7%).

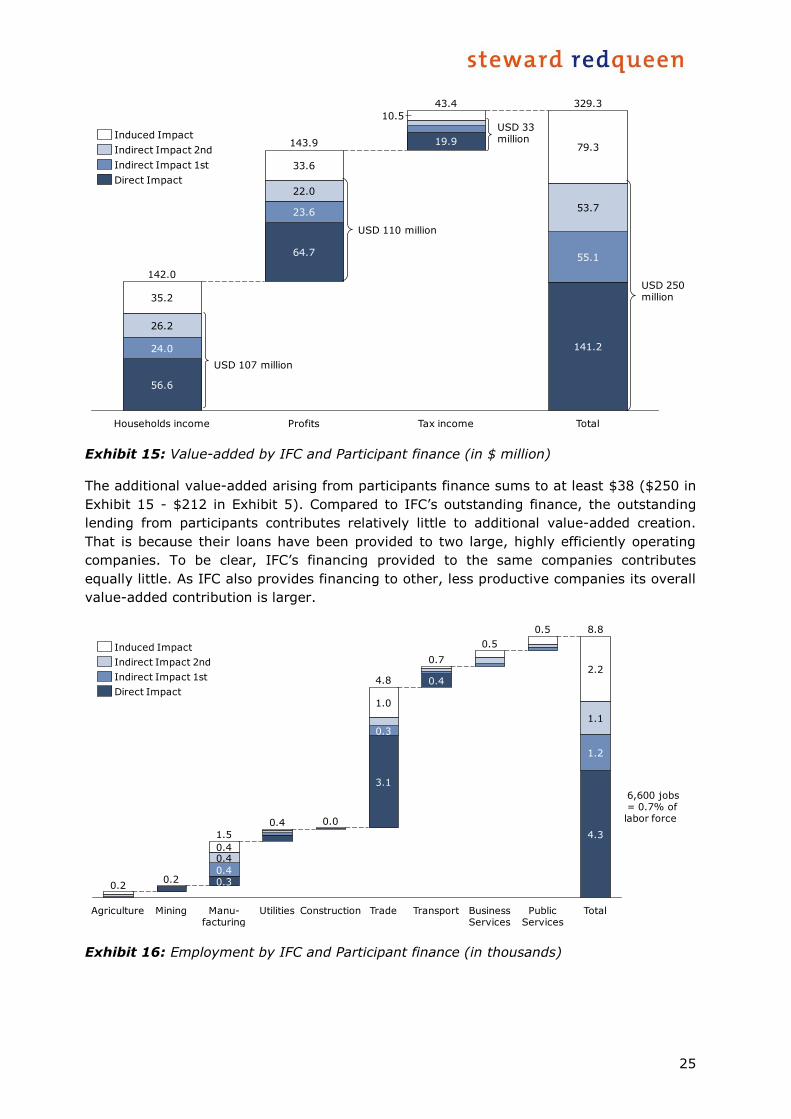

6. The combined impact of IFC and “participant” financing

The IFC’s investments can have an “additionality” effect on its clients by mobilizing funds

from third party investors (so-called “participants”) to these companies. In Jordan, these

participants had $139 million (as of June 30 2011) of finance outstanding with IFC clients

in the mining and trade sectors. Taking these loans into account as well, Exhibit 15 shows

the impact that can be associated with IFC’s and the mobilized third party capital. As the

output share of the client companies that can be attributed to the IFC plus the participants

is naturally larger than the output share that can be related to the IFC alone, the values

presented in Exhibit 15 are larger than the ones presented in Exhibit 5.

10.7

10.8

4.6

10.2

2.8

7.4

4.5

22.9

Trade Transport Business Services

21.5

24.7

Total

67.7

Public Services

4.9

Construction

0.4

Utilities

4.0

Manu-facturing

15.5

4.7

3.6

3.5

3.7

Mining

9.0

Agriculture

1.78.7

2.7

Indirect Impact 1st

Induced Impact

Indirect Impact 2nd

Direct Impact

46,200 jobs = 5% of labor force

25

Exhibit 15: Value-added by IFC and Participant finance (in $ million)

The additional value-added arising from participants finance sums to at least $38 ($250 in

Exhibit 15 - $212 in Exhibit 5). Compared to IFC’s outstanding finance, the outstanding

lending from participants contributes relatively little to additional value-added creation.

That is because their loans have been provided to two large, highly efficiently operating

companies. To be clear, IFC’s financing provided to the same companies contributes

equally little. As IFC also provides financing to other, less productive companies its overall

value-added contribution is larger.

Exhibit 16: Employment by IFC and Participant finance (in thousands)

Total

329.3

141.2

55.1

53.7

79.3

Tax income

43.4

19.9

10.5

Profits

143.9

64.7

23.6

22.0

33.6

Households income

142.0

56.6

24.0

26.2

35.2

Direct Impact

Indirect Impact 1st

Indirect Impact 2nd

Induced Impact

USD 250 million

USD 110 million

USD 107 million

USD 33 million

0.4

0.4

Agriculture

0.2

Construction Trade Transport Business Services

Public Services

Total

0.0

0.3

0.3

3.1

4.8 0.4

0.7

0.5

0.5

2.2

1.1

Utilities

4.3

8.8

0.4

Manu-facturing

1.0

1.5

0.4

Mining

0.2

1.2

Direct Impact

Indirect Impact 1st

Indirect Impact 2nd

Induced Impact

6,600 jobs = 0.7% of labor force

26

7. Recommendations

As this report demonstrates, the IFC has had an impact on employment creation and

value-added in the Jordanian economy through a variety of channels, including direct

loans to industrial companies, indirect financing of firms through support to financial

institutions (which in turn provide lending), the mobilization of third party or participant

capital, and via the provision of advisory services that improve the business environment.

The IFC’s impact, of course, is not just a function of its own operations but also is

determined by the economy in which it operates. To the extent that labor markets, for

example, are failing to provide workers whose skills match the demands of potential

employers, companies may not be able to operate at full efficiency or capacity. Other

factors, like the tax regime, the ease of doing business, and the state of the country’s

infrastructure, will also influence the level of employment and value-added in the

economy. International economic relations add a further degree of complexity to the

economic structure, including the degree of openness to trade and investment and the

level of foreign aid and remittances received.

These points suggest that an organization like the International Finance Corporation

should interact at both the “micro” and “macro” levels in Jordan to ensure that its funding

of firms and financial institutions will have the greatest possible impact on the nation’s

economy. Specifically, the IFC should consider the following recommendations:

1. To the extent that the IFC is interested in deploying its capital to generate more

employment in Jordan, it needs to recognize the tension between raising labor

productivity, creating fewer jobs or pursuing pure employment creation goals.

Financing well-capitalized companies directly increases labor productivity, but

generates relatively few additional jobs. Financing the banking sector to provide

loans to capital-needy firms enables those firms to bolster output and create, on

average, more jobs throughout the economy. Even though the immediate effect of

financing provided to private companies directly is less, it has the potential to

increase productivity and lead to “transformational” effects in the long-run.

2. In particular, the IFC could play a more significant role in the agriculture sector,

which faces limited access to capital due in part to the banking sector’s

conservative lending practices. In addition, relatively high job multipliers in that

sector have the potential to contribute to IFC’s job creation aim even though the

quality of jobs created should be kept in mind;

3. Similarly, IFC's might want to consider to intensify its impact on the Jordan

economy by investing relatively more into labor intensive industries like agriculture

and trade, sectors with relatively higher multipliers. This would contribute to short-

term poverty reduction goals;

4. The IFC should analyze the extent to which its financing and advisory services

serve to promote the SME sector in Jordan. Based on the labor rather than capital

intensive nature of SMEs, IFC's investment can make a relatively large difference

for those companies;

27

5. Related, the IFC should continue to collaborate with the Government of Jordan in

promoting an environment that is conducive to entrepreneurship, innovation, and

business development that encourages business investment and risk-taking.

28

Appendix I Model description

I.1 Modeling approach

The approach developed for this study is based on the socio-economic impact assessment

(SEIA) models and combines outstanding IFC loan data with a so-called Social Accounting

Matrix (SAM) of the Jordanian economy and the allocation of the work force over the

various economic sectors. A SAM describes inter-industry linkages in an economy,

depicting how the output of one industry goes to another, where it serves as an input. It

therefore essentially makes one industry dependent on another, both as customer of

outputs and as supplier of inputs. Exhibit I.1 depicts an overview of the modeling

approach, including the information sources used to arrive at the two main model outputs.

Exhibit I.1: Overview of the modeling approach

I.2 Production Function

IFC’s outstanding financing has been “translated” into company output based on the firm

production function that is depending on the company capital structure. A production

function describes the firm’s economic output as a function of its inputs, namely capital

and labor: P = f(L,K). Although classic production functions are written in terms of

physical outputs we have used economic output in order to more easily incorporate

different firms. Labor (L) has been measured in terms of the Full Time Equivalents (FTEs)

and Capital (K) has been defined as Capital Employed (defined as total assets in $). For

example, assume a company has assets with a book value of $100, revenues of $200 and

a loan from IFC of $15, this would mean that 15% of 200 = $30 in revenues can be

attributed to IFC.

Due to data constraints we used the Leontief (Linear) or fixed Production Function, a

simpler model for which only current data is needed. The more accurate, but also more

Micro economic analysis Macro economic analysis

IFC Financing

FinancialIntermediary

Firm Capital Structure

Economic Output

Value Added

Employment

• Wages

• Taxes

• Profits

Procurement

• Domestic

• Imports

Direct effect

Indirect effect

Induced effect

1

2 2

3

2 2

1

3

2

Production function

Social Accounting Matrix

Employment intensities

These are described in more

detail in separate sections

Financial instrument

29

complex and data-intensive Cobb-Douglas Production Function, would have been an

alternative.

All expenditures necessary to produce the output share related to IFC can then be traced

through the Jordanian economy estimating the associated value-added and employment

created.

For FIs, IFC’s financing was allocated over different economic sectors according to the

lending portfolios of the FIs IFC invest in. For each sector an “economy-wide” production

function was used to determine the direct impact of IFC’s capital which was then treated

as output generated at non-FIs. We have not conducted any interviews with borrowers of

FIs. Value-added and employment effects supported by financing provided to FIs have

been quantified relying on macro-economic production functions per sector based on local

statistics. The additional output related to the IFC’s investments based on the production

functions has then been followed through the economy as intermediary products and

distribution services were necessary to produce/ship this additional output. The basis for

this exercise was the SAM as described under I.3.

Further, the size of the FI portfolio companies has not been taken into consideration. The

size of companies supported plays a role for productivity levels. Given data availability for

Jordan, this study is based on average productivity levels per sector.

I.3 Social Accounting Matrix

The key ingredient of the model is the Social Accounting Matrix (SAM). The SAM describes

the financial flows of all economic transactions that take place within the Jordanian

economy. It is a statistical and static24 representation of the economic and social structure

of Jordan. As shown in Exhibit I.2, in the SAM the number of columns and rows are equal

because all sectors or economic actors (industry sectors, households, government and the

foreign sector) are both buyers and sellers. Columns represent buyers (expenditures) and

rows represent sellers (receipts).

Of the four quadrants in the SAM, three are relevant here. Final consumption induces

production which leads to financial transfers between the various sectors which

subsequently generates incomes for households, governments (taxes) and profits

(dividends and savings). For Jordan, the most recent SAM dates back to 2004 and has

been taken from the GTAP25 database. Using data from the Jordan Statistical Office26, the

SAM has been updated for the year 2009.

24 SAMs are valid for a specific year. Economies are subject to change and SAMs must be updated periodically. 25 Global Trade Analysis Project (www.gtap.agecon.purdue.edu). 26 http://www.dos.gov.jo

30

Exhibit I.2: Social Accounting Matrix

The last step in constructing the SAM is to normalize it such that all columns add up to

one. Then spending of IFC clients can be traced in money terms throughout the economy.

In doing so, the economic effect related to the presence of IFC can be divided into three

effects:

1. Direct effects: effects arising directly at clients financed by IFC and directly at FI

portfolio companies (e.g. jobs and salaries paid by direct clients/portfolio

companies)

2. Indirect effects (1st tier trade partners): effects arising at suppliers of IFC

clients/portfolio companies that result from spending of direct beneficiaries to

produce the IFC related output.

3. Indirect effects (2nd tier trade partners): effects arising at suppliers’ of

suppliers directly cooperating with IFC’s clients/portfolio companies (e.g. jobs and

salaries provided by suppliers’ suppliers);

4. Induced effects: effects due to the increased expenditures of households enabled

by the increasing incomes generated by the direct and indirect effects.

I.4 Assumptions

1. Constant returns to scale, constant technology and constant capital & labor productivity

For all sectors, the Social Accounting Matrix (SAM) implicitly assumes Leontief (linear)

production functions in which the inputs increase proportionally with output. Across the

economy and over not too long a period, this assumption is possibly not overly restrictive,

as new technologies and business practices take time to translate into higher productivity.

Input-output modeling is not capable of reflecting transformative change such as comes

with, say, the introduction of cell phone or internet technology. For this reason, SAMs are

periodically (or sometimes sporadically) updated. Only by studying the change of SAMs

over time can one infer the effect of transformative technology of business practices. If

one were to update the SAMs every five years or so, and assume technology was constant

during the period, one would incorporate the transient change of technology in a quasi-

Value added(Incomes)

Transfers Finaldemand

Investm

ents

Export

Taxes

Household

Consum

ptio

n

Reta

il

Manufa

cturin

gAgric

ultu

re

...

...

...

Agriculture

Manufacturing

...

...

...

Retail

Taxes

Households

Imports

Dividends/savings

IFC financing results in additional output which leads to

Transfers of money between sectors which in turn generate

Incomes for households, companies & governments which

create

Additional final demand

IFC Financing per sector

...

...

IFC attributable output per sector

Production functions

31

steady way. This, however, would not quantify IFC’s contribution to this (transformative)

technology change. In input-output modeling, the marginal capital and labor productivities

are equal to overall capital and labor productivity. Although in reality one would expect

diminishing marginal returns to scale, the lack of skills and capital typically present in

emerging markets probably mean that this is a reasonable assumption. For firms with

good access to finance (possibly IFC clients), however, the assumption is more restrictive.

Using, as proposed, Cobb-Douglas production functions for these companies will improve

results but only in terms of the “direct” impacts.

2. Different products within one sector have identical cost structures

Although economies of scale and scope surely influence the production process within an

individual company, we assume that production processes are not too dissimilar across a

sector. This restrictive assumption could only be relaxed with more disaggregated data.

3. Demand is totally inelastic and input structures are fixed

In a SAM, the use of inputs does not depend on price but only on final demand.

Unreasonable as it may sound, this assumption may not be overly restrictive unless one

supposes that firms are price-makers instead of price-takers. More restrictive is that the

production function relies on a fixed proportion of inputs (i.e. no substitution takes place).

Again, this may not be problematic over a given time-horizon.

4. Supply of inputs is totally elastic

Supply of labor intensive products can be expected to be fairly elastic for unskilled labor.

For skilled labor this would be more problematic. Inputs from capital intensive industries

will typically violate this assumption, as capital is typically scarce in emerging economies

and economic impact would then be overestimated.

5. Time invariance

Input-output modeling yields a “snapshot in time”. In a sense, it is as if the effects of any

IFC intervention result in a new “steady state” immediately. In reality, of course, it would

take a substantial amount of time for these effects to percolate through the economy. In

other words, the methodology produces a snapshot of the economy and does not take the