Embed Size (px)

Citation preview

2021UNAUDITED RESULTS

Brait SE (Registered in Malta as a European Company)(Registration No. SE1)Share code: BATISIN: LU0011857645Bond code: WKN: A2SBSU LEI code: 549300VB8GBX4UO7WG59(“Brait”, the “Company” or “Group”)

FOR THE SIX MONTHS ENDED

30 SEPTEMBER 2020

Unaudited interim results for the six months ended 30 September 2020

CONTENTS PAGE

PAGE INDEX

SECTION ONE - BRAIT’S INTERIM 1HFY21 RESULTS PRESENTATION

Overview Page 4

Executive Summary Page 7

Brait NAV & Liquidity Page 9

Virgin Active: nine months ended 30 September 2020 Page 14

Premier: six months ended 30 September 2020 Page 24

New Look: six months ended 30 September 2020 Page 32

Portfolio Valuations Page 35

Conclusion Page 39

SECTION TWO - ANNEXURES

SECTION THREE – UNAUDITED INTERIM 1HFY21 RESULTS ANNOUNCEMENT

BRAIT’SINTERIM RESULTS

PRESENTATION

30 September 2020

4 Unaudited interim results for the six months ended 30 September 2020

1H 2021 - PERFORMANCE REVIEW

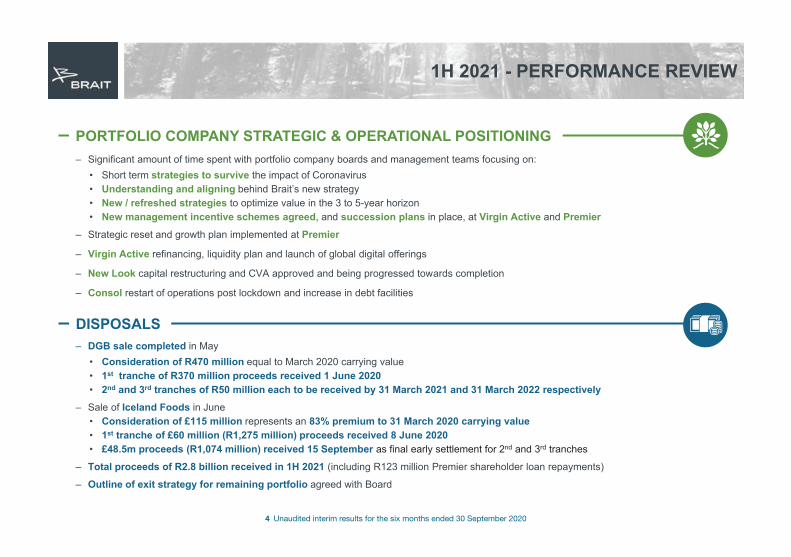

PORTFOLIO COMPANY STRATEGIC & OPERATIONAL POSITIONING

DISPOSALS

– Significant amount of time spent with portfolio company boards and management teams focusing on:• Short term strategies to survive the impact of Coronavirus• Understanding and aligning behind Brait’s new strategy• New / refreshed strategies to optimize value in the 3 to 5-year horizon• New management incentive schemes agreed, and succession plans in place, at Virgin Active and Premier

– Strategic reset and growth plan implemented at Premier

– Virgin Active refinancing, liquidity plan and launch of global digital offerings

– New Look capital restructuring and CVA approved and being progressed towards completion

– Consol restart of operations post lockdown and increase in debt facilities

– DGB sale completed in May • Consideration of R470 million equal to March 2020 carrying value• 1st tranche of R370 million proceeds received 1 June 2020• 2nd and 3rd tranches of R50 million each to be received by 31 March 2021 and 31 March 2022 respectively

– Sale of Iceland Foods in June• Consideration of £115 million represents an 83% premium to 31 March 2020 carrying value• 1st tranche of £60 million (R1,275 million) proceeds received 8 June 2020• £48.5m proceeds (R1,074 million) received 15 September as final early settlement for 2nd and 3rd tranches

– Total proceeds of R2.8 billion received in 1H 2021 (including R123 million Premier shareholder loan repayments)

– Outline of exit strategy for remaining portfolio agreed with Board

5 Unaudited interim results for the six months ended 30 September 2020

1H - PERFORMANCE REVIEW

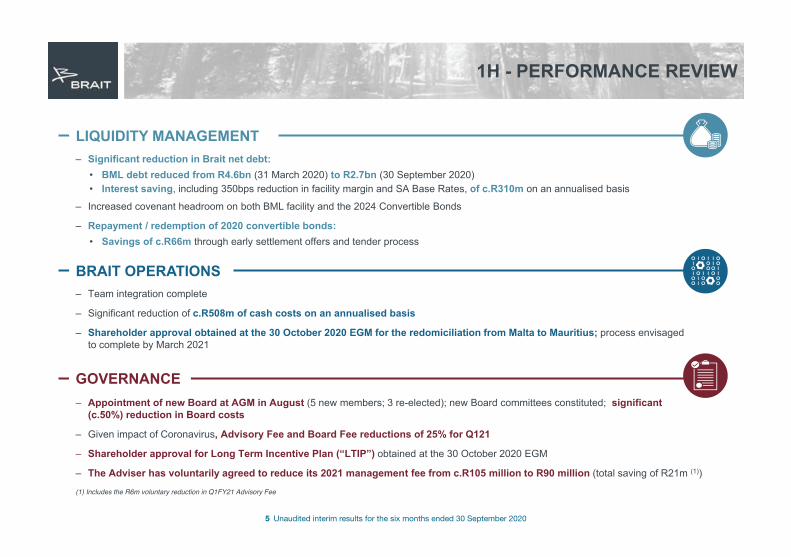

LIQUIDITY MANAGEMENT

BRAIT OPERATIONS

– Significant reduction in Brait net debt:• BML debt reduced from R4.6bn (31 March 2020) to R2.7bn (30 September 2020)• Interest saving, including 350bps reduction in facility margin and SA Base Rates, of c.R310m on an annualised basis

– Increased covenant headroom on both BML facility and the 2024 Convertible Bonds

– Repayment / redemption of 2020 convertible bonds:• Savings of c.R66m through early settlement offers and tender process

– Team integration complete

– Significant reduction of c.R508m of cash costs on an annualised basis

– Shareholder approval obtained at the 30 October 2020 EGM for the redomiciliation from Malta to Mauritius; process envisaged to complete by March 2021

GOVERNANCE– Appointment of new Board at AGM in August (5 new members; 3 re-elected); new Board committees constituted; significant

(c.50%) reduction in Board costs

– Given impact of Coronavirus, Advisory Fee and Board Fee reductions of 25% for Q121

– Shareholder approval for Long Term Incentive Plan (“LTIP”) obtained at the 30 October 2020 EGM

– The Adviser has voluntarily agreed to reduce its 2021 management fee from c.R105 million to R90 million (total saving of R21m (1))

(1) Includes the R6m voluntary reduction in Q1FY21 Advisory Fee

6 Unaudited interim results for the six months ended 30 September 2020

PORTFOLIO COMPANY PERFORMANCE OVERVIEW

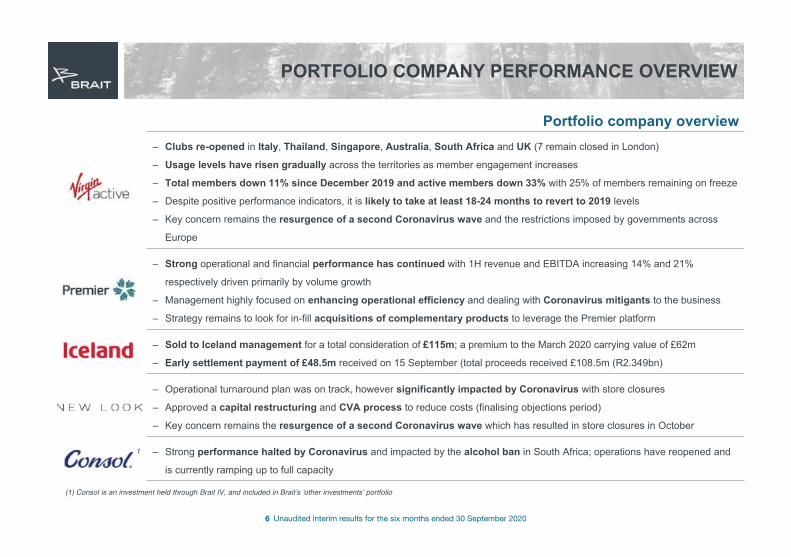

Portfolio company overview– Clubs re-opened in Italy, Thailand, Singapore, Australia, South Africa and UK (7 remain closed in London)

– Usage levels have risen gradually across the territories as member engagement increases

– Total members down 11% since December 2019 and active members down 33% with 25% of members remaining on freeze

– Despite positive performance indicators, it is likely to take at least 18-24 months to revert to 2019 levels

– Key concern remains the resurgence of a second Coronavirus wave and the restrictions imposed by governments across

Europe

– Strong operational and financial performance has continued with 1H revenue and EBITDA increasing 14% and 21%

respectively driven primarily by volume growth

– Management highly focused on enhancing operational efficiency and dealing with Coronavirus mitigants to the business

– Strategy remains to look for in-fill acquisitions of complementary products to leverage the Premier platform

– Sold to Iceland management for a total consideration of £115m; a premium to the March 2020 carrying value of £62m

– Early settlement payment of £48.5m received on 15 September (total proceeds received £108.5m (R2.349bn)

– Operational turnaround plan was on track, however significantly impacted by Coronavirus with store closures

– Approved a capital restructuring and CVA process to reduce costs (finalising objections period)

– Key concern remains the resurgence of a second Coronavirus wave which has resulted in store closures in October

– Strong performance halted by Coronavirus and impacted by the alcohol ban in South Africa; operations have reopened and

is currently ramping up to full capacity

(1) Consol is an investment held through Brait IV, and included in Braitʼs ʻother investmentsʼ portfolio

1

7 Unaudited interim results for the six months ended 30 September 2020

EXECUTIVE SUMMARY

8 Unaudited interim results for the six months ended 30 September 2020

EXECUTIVE SUMMARY

Six months ended 30 September 2020: headlines at a glance

NAV per share:

R7.71impact of Coronavirus on

Virgin Active and New Look

Recapitalisations concluded

at Virgin Active (UK / Europe / Asia Pacific) and New Look

Coronavirusongoing impact on portfoliocompanies and potential of

second wave

De-gearing since March 2020:

R5.6bnInvestment proceeds from the portfolio of

R2.8bnreceived during 1HFY21

Disposals of:DGB for a total of R470m

& Iceland Foods for a total of

R2.4bn

Estimated annualised savings to Brait’s cash costs of

R508mthrough actions taken since

1 March 2020

Brait currently trades at a discount to NAVPS of

c.55%Strong operational performance by

PremierLTM Sep-20 EBITDA

increase of 10%

9 Unaudited interim results for the six months ended 30 September 2020

BRAIT NAV & LIQUIDITY

10 Unaudited interim results for the six months ended 30 September 2020

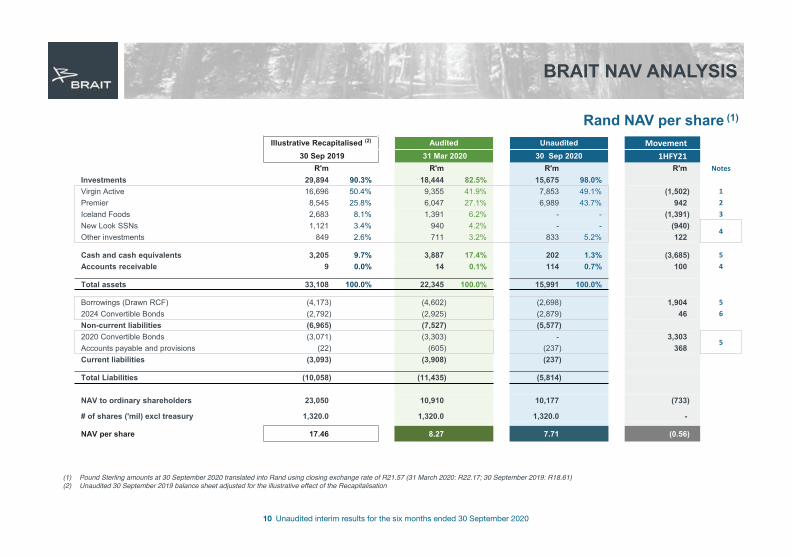

BRAIT NAV ANALYSIS

Rand NAV per share (1)

Illustrative Recapitalised (2) Audited Unaudited Movement30 Sep 2019 31 Mar 2020 30 Sep 2020 1HFY21

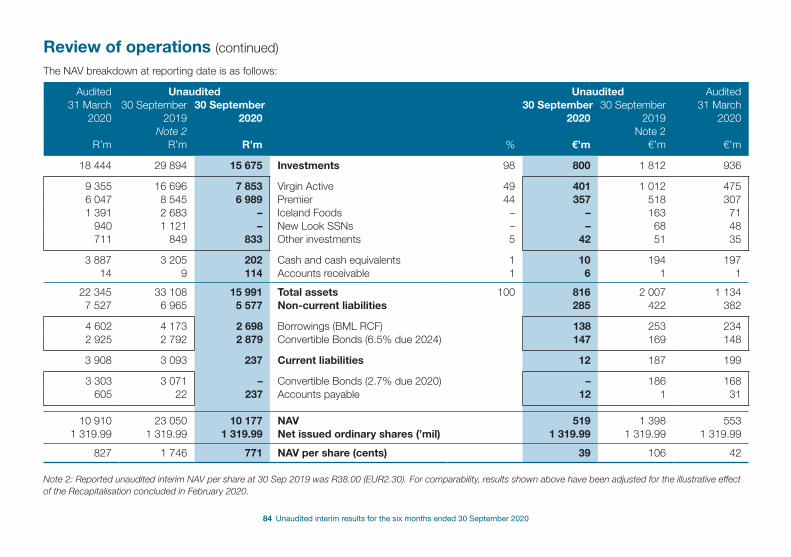

R'm R'm R'm R'm NotesInvestments 29,894 90.3% 18,444 82.5% 15,675 98.0%Virgin Active 16,696 50.4% 9,355 41.9% 7,853 49.1% (1,502) 1Premier 8,545 25.8% 6,047 27.1% 6,989 43.7% 942 2Iceland Foods 2,683 8.1% 1,391 6.2% - - (1,391) 3New Look SSNs 1,121 3.4% 940 4.2% - - (940)

4Other investments 849 2.6% 711 3.2% 833 5.2% 122

Cash and cash equivalents 3,205 9.7% 3,887 17.4% 202 1.3% (3,685) 5Accounts receivable 9 0.0% 14 0.1% 114 0.7% 100 4

Total assets 33,108 100.0% 22,345 100.0% 15,991 100.0%

Borrowings (Drawn RCF) (4,173) (4,602) (2,698) 1,904 52024 Convertible Bonds (2,792) (2,925) (2,879) 46 6Non-current liabilities (6,965) (7,527) (5,577)2020 Convertible Bonds (3,071) (3,303) - 3,303

5Accounts payable and provisions (22) (605) (237) 368Current liabilities (3,093) (3,908) (237)

Total Liabilities (10,058) (11,435) (5,814)

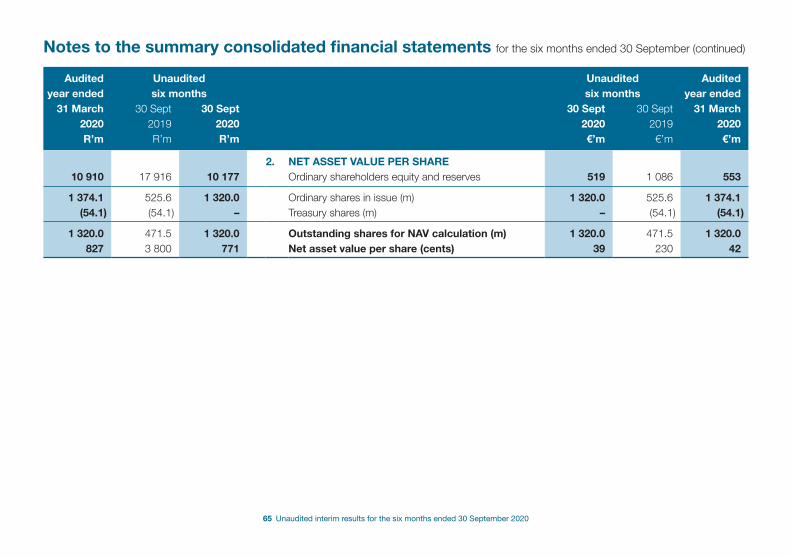

NAV to ordinary shareholders 23,050 10,910 10,177 (733)

# of shares ('mil) excl treasury 1,320.0 1,320.0 1,320.0 -

NAV per share 17.46 8.27 7.71 (0.56)

(1) Pound Sterling amounts at 30 September 2020 translated into Rand using closing exchange rate of R21.57 (31 March 2020: R22.17; 30 September 2019: R18.61)(2) Unaudited 30 September 2019 balance sheet adjusted for the illustrative effect of the Recapitalisation

11 Unaudited interim results for the six months ended 30 September 2020

BRAIT NAV ANALYSIS

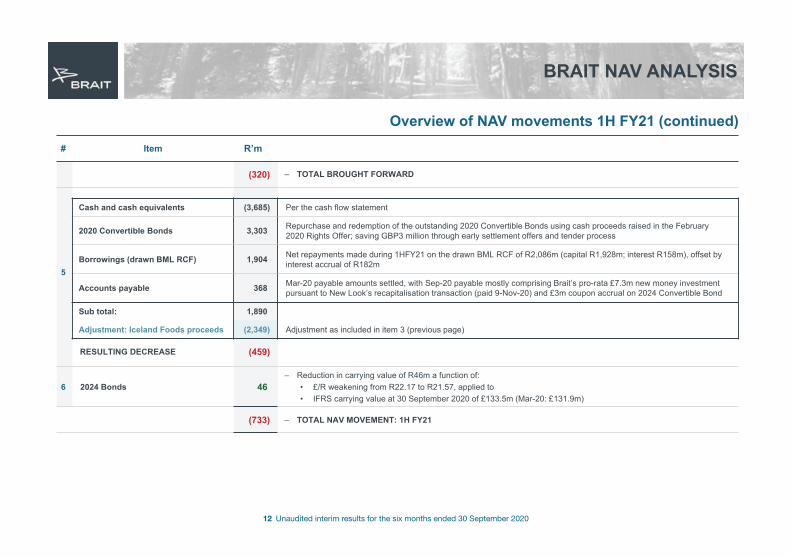

# Item R’m

1 (1,502)

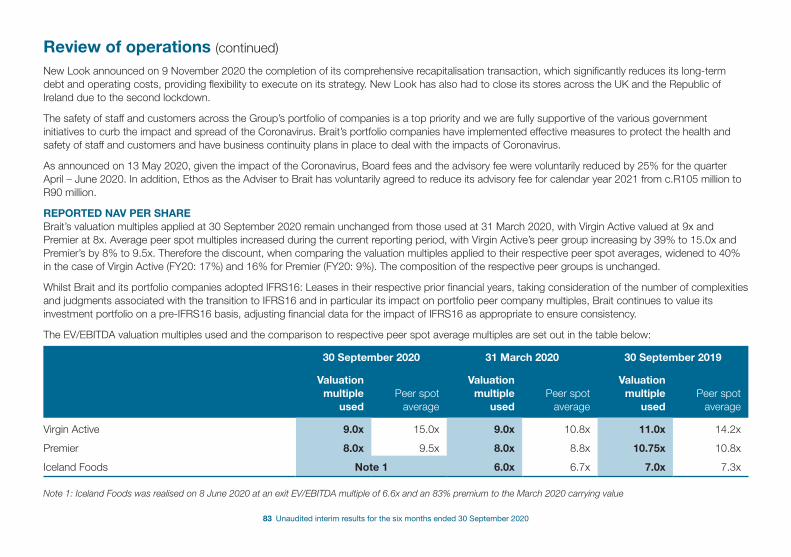

– R1,502m decrease in Virgin Active’s carrying value a function of:• Maintainable EBITDA reduced to £100m (Mar-20: £108m) due to later reopening (SA / UK) and membership re-engagement • EV / EBITDA multiple kept at 9.0x whilst peer average multiple increased 39% from 10.8x (Mar-20) to 15.0x (Sep-20).

Discount to the peer group widened from 17% to 40%• Net debt used in Sep-20 valuation of £441m (Mar-20: £440m)

2 +942

– R942m increase in Premier’s carrying value a function of:• LTM (1) EBITDA to Sep-20 increased by 10% to R1,110m (Mar-20 LTM EBITDA: R1,010m)• EV / EBITDA multiple kept at 8.0x; 16% discount to peer average 9.5x (Mar-20: 9% discount to peer average of 8.8x)• Net debt used in Sep-20 valuation of R1,829m (Mar-20: R1,989m)

3 – R958m increase for Iceland Foods a function of:• Realisation proceeds received of R2,349m compared to the Mar-20 carrying value of R1,391m

4

– Net R718m decrease in carrying value for these 3 assets a function of:• The New Look SSNs were equitised on 9-Nov-20 pursuant to the completion of New Look’s recapitalisation transaction

(Mar-20: R940m carrying value of Brait’s 18.27% SSNs holding based on quoted price of £0.549 plus accrued interest)• Brait’s 18.3% holding of New Look shareholder loans / PIK Facility and 18.3% of New Look’s equity (17.4% post dilution for

management’s incentive plan) valued at reporting date using an earnings multiple basis, with the resulting carrying value included in the Other Investments portfolio at Sep-20

• DGB (included in Other Investments portfolio at Mar-20) realised in Jun-20 for a total consideration of R470m:• Initial tranche of R370m realisation proceeds received during Jun-20; • Remaining R100m deferred consideration included in accounts receivable at reporting date

(320) – TOTAL CARRIED FORWARD

(1,391)

2,349

+958

New Look SSNs (940)

Other investments 122

Accounts receivable 100

RESULTING DECREASE (718)

Overview of NAV movements 1H FY21

(1) LTM refers to Last Twelve Months

12 Unaudited interim results for the six months ended 30 September 2020

BRAIT NAV ANALYSIS

# Item R’m

(320) – TOTAL BROUGHT FORWARD

5

6 2024 Bonds 46– Reduction in carrying value of R46m a function of:

• £/R weakening from R22.17 to R21.57, applied to • IFRS carrying value at 30 September 2020 of £133.5m (Mar-20: £131.9m)

(733) – TOTAL NAV MOVEMENT: 1H FY21

Cash and cash equivalents (3,685) Per the cash flow statement

2020 Convertible Bonds 3,303 Repurchase and redemption of the outstanding 2020 Convertible Bonds using cash proceeds raised in the February 2020 Rights Offer; saving GBP3 million through early settlement offers and tender process

Borrowings (drawn BML RCF) 1,904 Net repayments made during 1HFY21 on the drawn BML RCF of R2,086m (capital R1,928m; interest R158m), offset by interest accrual of R182m

Accounts payable 368 Mar-20 payable amounts settled, with Sep-20 payable mostly comprising Brait’s pro-rata £7.3m new money investment pursuant to New Look’s recapitalisation transaction (paid 9-Nov-20) and £3m coupon accrual on 2024 Convertible Bond

Sub total: 1,890

Adjustment: Iceland Foods proceeds (2,349) Adjustment as included in item 3 (previous page)

RESULTING DECREASE (459)

Overview of NAV movements 1H FY21 (continued)

13 Unaudited interim results for the six months ended 30 September 2020

6,348

3,303

2,925

2,925 2,879

6,4024,601

3,5482,698

Sep 19 (prerestructure)

Mar 20 (Actual) Mar-20 (incl. DGB,Iceland & VA loan)

Sep-20

Total Group debt (R million)

2020 Convertible Bond

2024 Convertible Bond

Drawn BML RCF

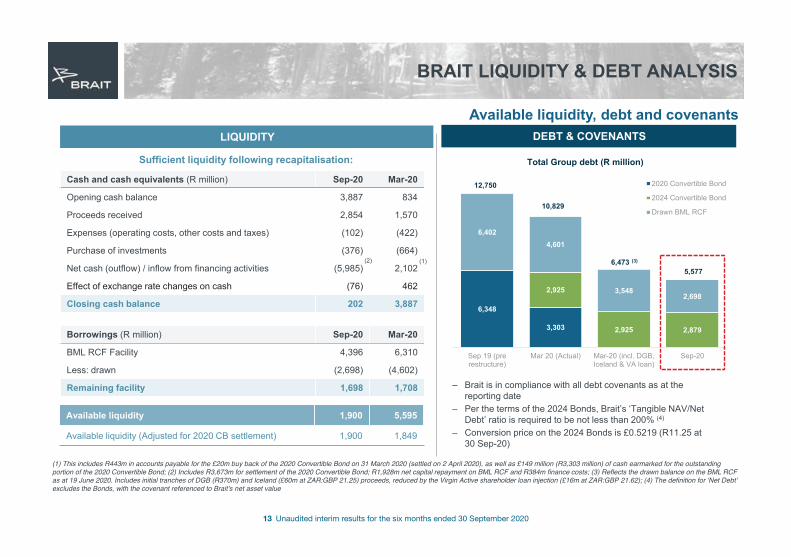

BRAIT LIQUIDITY & DEBT ANALYSIS

Available liquidity, debt and covenantsLIQUIDITY

Cash and cash equivalents (R million) Sep-20 Mar-20

Opening cash balance 3,887 834

Proceeds received 2,854 1,570

Expenses (operating costs, other costs and taxes) (102) (422)

Purchase of investments (376) (664)

Net cash (outflow) / inflow from financing activities (5,985) 2,102

Effect of exchange rate changes on cash (76) 462

Closing cash balance 202 3,887

Borrowings (R million) Sep-20 Mar-20

BML RCF Facility 4,396 6,310

Less: drawn (2,698) (4,602)

Remaining facility 1,698 1,708 – Brait is in compliance with all debt covenants as at the reporting date

– Per the terms of the 2024 Bonds, Brait’s ‘Tangible NAV/Net Debt’ ratio is required to be not less than 200% (4)

– Conversion price on the 2024 Bonds is £0.5219 (R11.25 at 30 Sep-20)

Available liquidity 1,900 5,595

Available liquidity (Adjusted for 2020 CB settlement) 1,900 1,849

DEBT & COVENANTS

12,750

6,473 (3)

5,577

Sufficient liquidity following recapitalisation:

10,829

(1)(2)

(1) This includes R443m in accounts payable for the £20m buy back of the 2020 Convertible Bond on 31 March 2020 (settled on 2 April 2020), as well as £149 million (R3,303 million) of cash earmarked for the outstanding portion of the 2020 Convertible Bond; (2) Includes R3,673m for settlement of the 2020 Convertible Bond; R1,928m net capital repayment on BML RCF and R384m finance costs; (3) Reflects the drawn balance on the BML RCF as at 19 June 2020. Includes initial tranches of DGB (R370m) and Iceland (£60m at ZAR:GBP 21.25) proceeds, reduced by the Virgin Active shareholder loan injection (£16m at ZAR:GBP 21.62); (4) The definition for ʻNet Debtʼ excludes the Bonds, with the covenant referenced to Braitʼs net asset value

14 Unaudited interim results for the six months ended 30 September 2020

VIRGIN ACTIVE

Nine months ended 30 September 2020

15 Unaudited interim results for the six months ended 30 September 2020

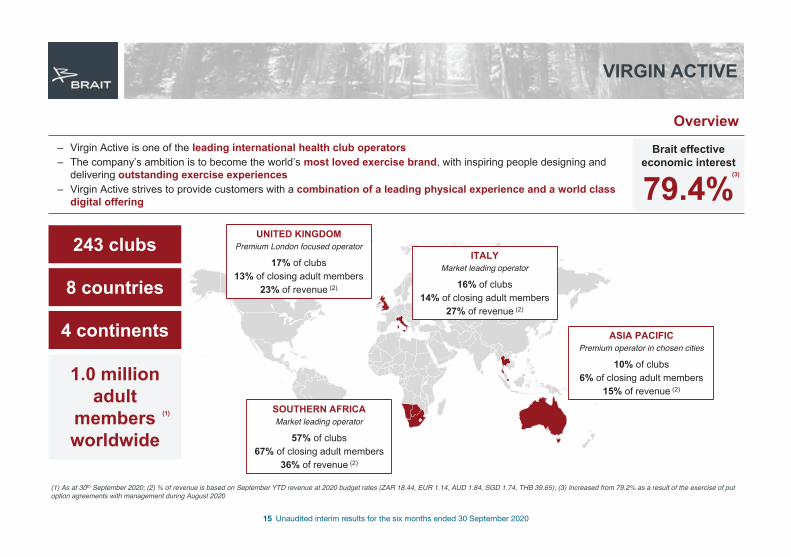

VIRGIN ACTIVE

Overview

Brait effective economic interest

79.4%– Virgin Active is one of the leading international health club operators– The company’s ambition is to become the world’s most loved exercise brand, with inspiring people designing and

delivering outstanding exercise experiences– Virgin Active strives to provide customers with a combination of a leading physical experience and a world class

digital offering

243 clubs

8 countries

4 continents

1.0 million adult

members worldwide

UNITED KINGDOMPremium London focused operator

17% of clubs13% of closing adult members

23% of revenue (2)

SOUTHERN AFRICAMarket leading operator

57% of clubs67% of closing adult members

36% of revenue (2)

ITALYMarket leading operator

16% of clubs14% of closing adult members

27% of revenue (2)

ASIA PACIFICPremium operator in chosen cities

10% of clubs6% of closing adult members

15% of revenue (2)

(1)

(1) As at 30th September 2020; (2) % of revenue is based on September YTD revenue at 2020 budget rates (ZAR 18.44, EUR 1.14, AUD 1.84, SGD 1.74, THB 39.65); (3) Increased from 79.2% as a result of the exercise of put option agreements with management during August 2020

(3)

16 Unaudited interim results for the six months ended 30 September 2020

VIRGIN ACTIVE

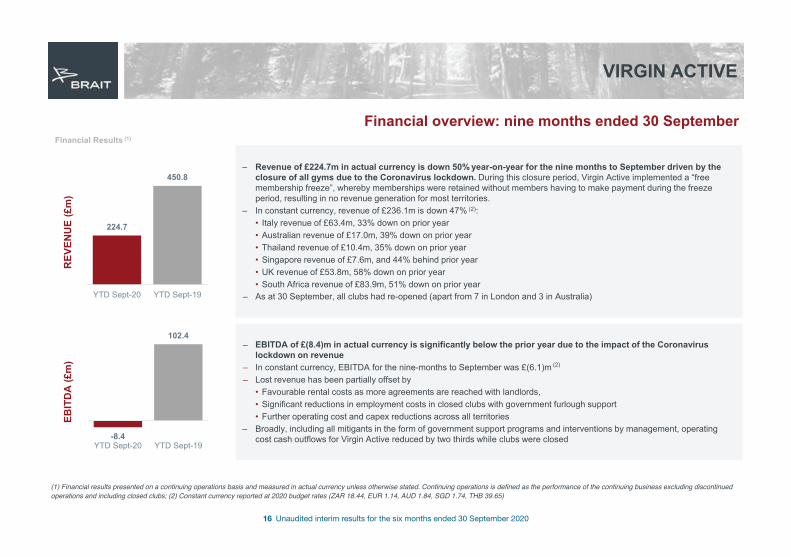

Financial overview: nine months ended 30 September

REV

ENU

E (£

m)

EBIT

DA

(£m

)

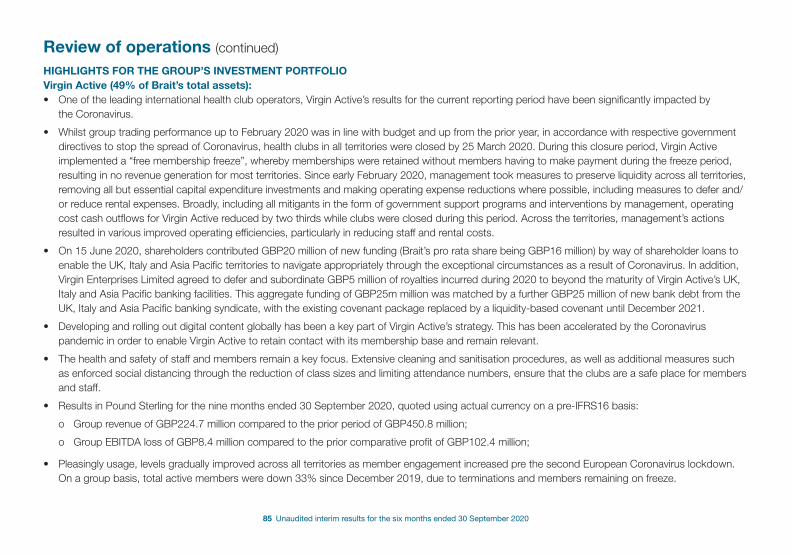

– Revenue of £224.7m in actual currency is down 50% year-on-year for the nine months to September driven by the closure of all gyms due to the Coronavirus lockdown. During this closure period, Virgin Active implemented a “free membership freeze”, whereby memberships were retained without members having to make payment during the freeze period, resulting in no revenue generation for most territories.

– In constant currency, revenue of £236.1m is down 47% (2):• Italy revenue of £63.4m, 33% down on prior year• Australian revenue of £17.0m, 39% down on prior year• Thailand revenue of £10.4m, 35% down on prior year• Singapore revenue of £7.6m, and 44% behind prior year• UK revenue of £53.8m, 58% down on prior year• South Africa revenue of £83.9m, 51% down on prior year

– As at 30 September, all clubs had re-opened (apart from 7 in London and 3 in Australia)

– EBITDA of £(8.4)m in actual currency is significantly below the prior year due to the impact of the Coronavirus lockdown on revenue

– In constant currency, EBITDA for the nine-months to September was £(6.1)m (2)

– Lost revenue has been partially offset by• Favourable rental costs as more agreements are reached with landlords, • Significant reductions in employment costs in closed clubs with government furlough support• Further operating cost and capex reductions across all territories

– Broadly, including all mitigants in the form of government support programs and interventions by management, operating cost cash outflows for Virgin Active reduced by two thirds while clubs were closed

224.7

450.8

YTD Sept-20 YTD Sept-19

-8.4

102.4

YTD Sept-20 YTD Sept-19

(1) Financial results presented on a continuing operations basis and measured in actual currency unless otherwise stated. Continuing operations is defined as the performance of the continuing business excluding discontinued operations and including closed clubs; (2) Constant currency reported at 2020 budget rates (ZAR 18.44, EUR 1.14, AUD 1.84, SGD 1.74, THB 39.65)

Financial Results (1)

17 Unaudited interim results for the six months ended 30 September 2020

VIRGIN ACTIVE

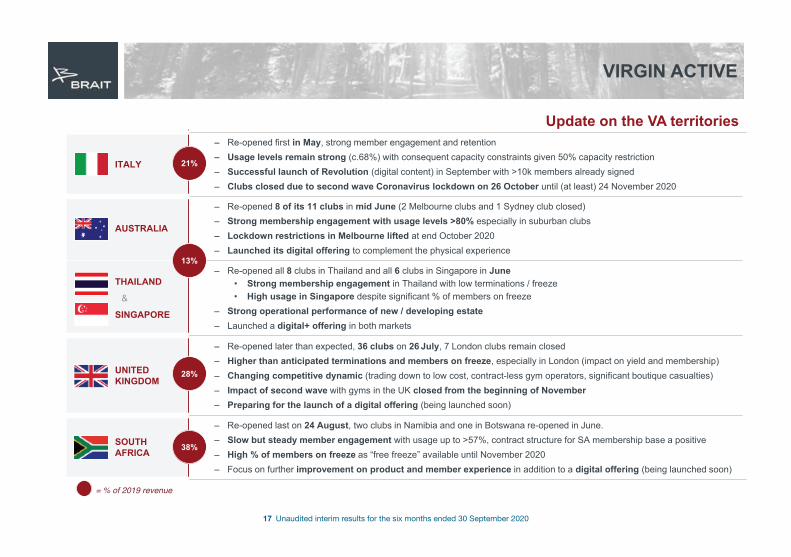

Update on the VA territories

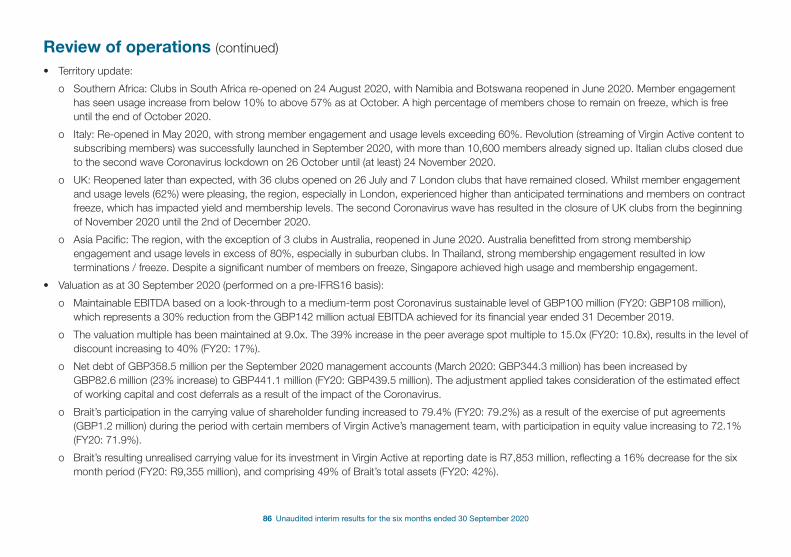

ITALY

– Re-opened first in May, strong member engagement and retention– Usage levels remain strong (c.68%) with consequent capacity constraints given 50% capacity restriction– Successful launch of Revolution (digital content) in September with >10k members already signed– Clubs closed due to second wave Coronavirus lockdown on 26 October until (at least) 24 November 2020

AUSTRALIA

– Re-opened 8 of its 11 clubs in mid June (2 Melbourne clubs and 1 Sydney club closed) – Strong membership engagement with usage levels >80% especially in suburban clubs– Lockdown restrictions in Melbourne lifted at end October 2020 – Launched its digital offering to complement the physical experience

THAILAND

&

SINGAPORE

– Re-opened all 8 clubs in Thailand and all 6 clubs in Singapore in June• Strong membership engagement in Thailand with low terminations / freeze• High usage in Singapore despite significant % of members on freeze

– Strong operational performance of new / developing estate– Launched a digital+ offering in both markets

UNITED KINGDOM

– Re-opened later than expected, 36 clubs on 26 July, 7 London clubs remain closed– Higher than anticipated terminations and members on freeze, especially in London (impact on yield and membership)– Changing competitive dynamic (trading down to low cost, contract-less gym operators, significant boutique casualties)– Impact of second wave with gyms in the UK closed from the beginning of November– Preparing for the launch of a digital offering (being launched soon)

SOUTH AFRICA

– Re-opened last on 24 August, two clubs in Namibia and one in Botswana re-opened in June. – Slow but steady member engagement with usage up to >57%, contract structure for SA membership base a positive– High % of members on freeze as “free freeze” available until November 2020– Focus on further improvement on product and member experience in addition to a digital offering (being launched soon)

21%

13%

28%

38%

= % of 2019 revenue

18 Unaudited interim results for the six months ended 30 September 2020

VIRGIN ACTIVE

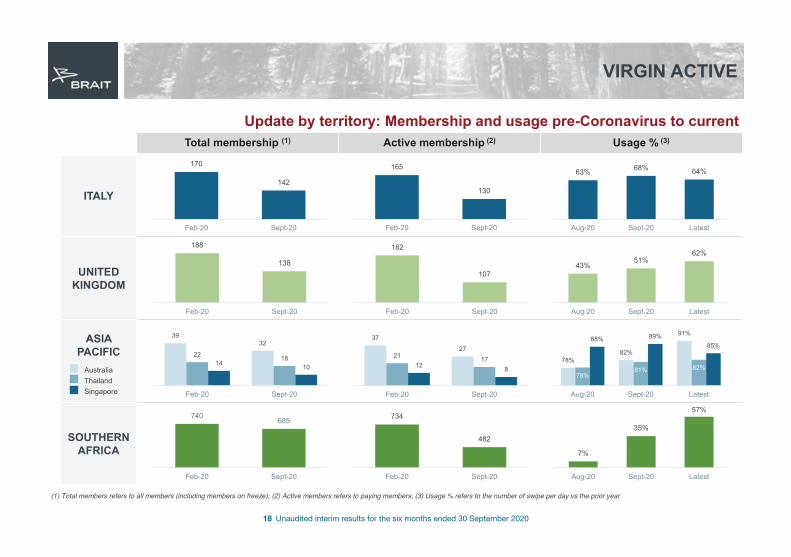

Update by territory: Membership and usage pre-Coronavirus to currentTotal membership (1) Active membership (2) Usage % (3)

ITALY

UNITED KINGDOM

ASIA PACIFIC

SOUTHERN AFRICA

170

142

Feb-20 Sept-20

165

130

Feb-20 Sept-20

188

138

Feb-20 Sept-20

182

107

Feb-20 Sept-20

3932

22 1814 10

Feb-20 Sept-20

37

2721 17

12 8

Feb-20 Sept-20

740 685

Feb-20 Sept-20

734

482

Feb-20 Sept-20

AustraliaThailandSingapore

63% 68% 64%

Aug-20 Sept-20 Latest

43%51%

62%

Aug-20 Sept-20 Latest

78%82%

91%

78%81% 82%

88% 89%85%

Aug-20 Sept-20 Latest

7%

35%

57%

Aug-20 Sept-20 Latest

(1) Total members refers to all members (including members on freeze); (2) Active members refers to paying members; (3) Usage % refers to the number of swipe per day vs the prior year

19 Unaudited interim results for the six months ended 30 September 2020

Re-opened in May

11 1110

0 1

8 87

8

02468

1012

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

Rev

enue

(£m

)

Revenue

166 165

0 0

147124 109 122 130

68%

0%

50%

100%

150%

0

100

200

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

Usa

ge %

vs

PY

Activ

e m

embe

rs (‘

000)

Active membership and usage %Active membership Usage

VIRGIN ACTIVE

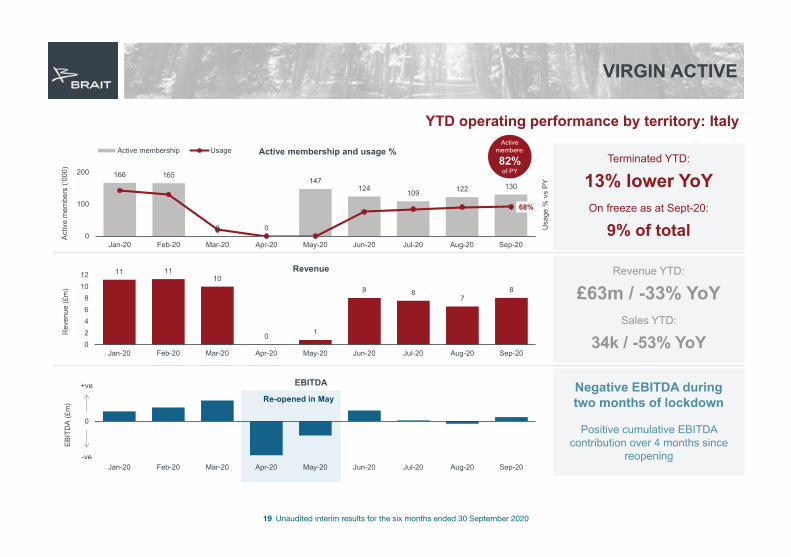

YTD operating performance by territory: Italy

Terminated YTD:

On freeze as at Sept-20:

13% lower YoY

9% of total

Active members:

82%of PY

Revenue YTD:

£63m / -33% YoYSales YTD:

34k / -53% YoY

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

EBIT

DA

(£m

)

EBITDA Negative EBITDA during two months of lockdown

Positive cumulative EBITDA contribution over 4 months since

reopening

0

+ve

-ve

20 Unaudited interim results for the six months ended 30 September 2020

Re-opened on 26 July

13 14

9

0

0 02

8 8

-5

0

5

10

15

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20Rev

enue

(£m

)

Revenue

182 182

0 0 0 0

108 107 107

51%

0%

50%

100%

150%

0

100

200

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

Usa

ge %

vs

PY

Activ

e m

embe

rs (‘

000)

Active membership and usage %Active membership Usage

VIRGIN ACTIVE

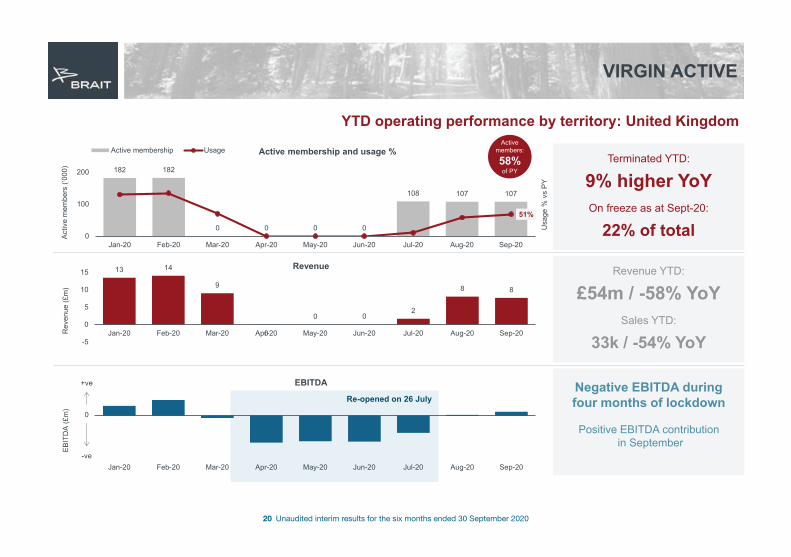

YTD operating performance by territory: United Kingdom

Terminated YTD:

On freeze as at Sept-20:

9% higher YoY

22% of total

Revenue YTD:

£54m / -58% YoYSales YTD:

33k / -54% YoY

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

EBIT

DA

(£m

)

EBITDA Negative EBITDA during four months of lockdown

Positive EBITDA contributionin September

Active members:

58%of PY

0

+ve

-ve

21 Unaudited interim results for the six months ended 30 September 2020

Re-opened in June

70 70

0 0 0

58 52 52 5383%

0%

50%

100%

150%

0

50

100

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

Usa

ge %

vs

PY

Activ

e m

embe

rs (‘

000)

Active membership and usage %Active membership Usage

VIRGIN ACTIVE

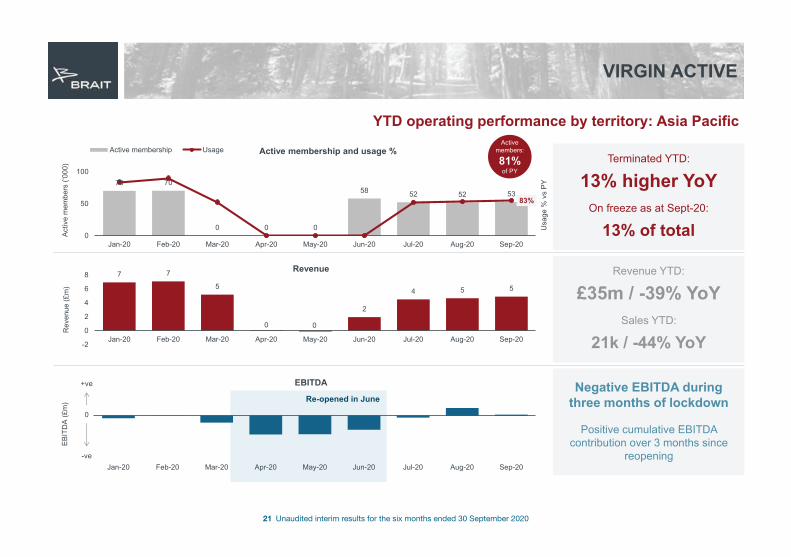

YTD operating performance by territory: Asia Pacific

Terminated YTD:

On freeze as at Sept-20:

13% higher YoY

13% of total

Revenue YTD:

£35m / -39% YoYSales YTD:

21k / -44% YoY

7 7

5

0 0

2

4 5 5

-2

0

2

4

6

8

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

Rev

enue

(£m

)

Revenue

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

EBIT

DA

(£m

)

EBITDA Negative EBITDA during three months of lockdown

Positive cumulative EBITDA contribution over 3 months since

reopening

Active members:

81%of PY

0

+ve

-ve

22 Unaudited interim results for the six months ended 30 September 2020

739 734 718 697 702 701 693519 482

35%

0%

50%

100%

0

500

1,000

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

Usa

ge %

of P

Y

Activ

e m

embe

rs (‘

000)

Active membership and usage %Active membership Usage

Re-opened on 24 August

19 2017

2 3 30

7

13

0

5

10

15

20

25

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

Rev

enue

(£m

)

Revenue

VIRGIN ACTIVE

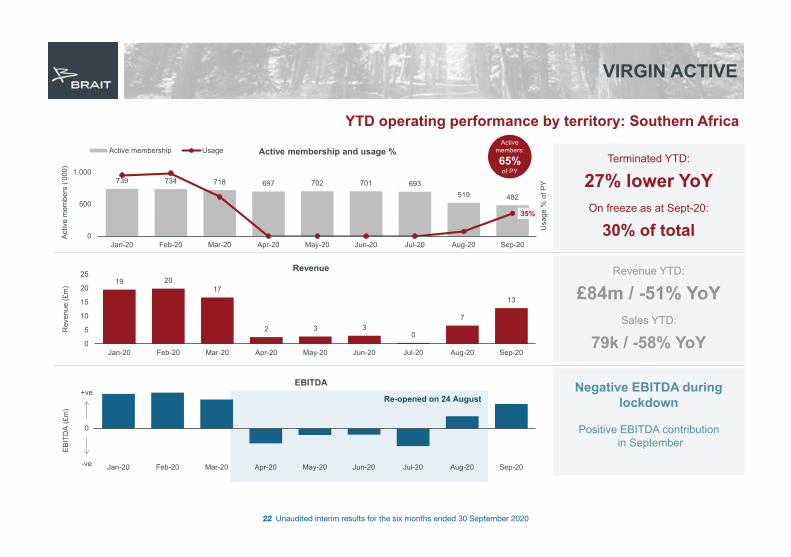

YTD operating performance by territory: Southern Africa

Terminated YTD:

On freeze as at Sept-20:

27% lower YoY

30% of total

Revenue YTD:

£84m / -51% YoYSales YTD:

79k / -58% YoY

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

EBIT

DA

(£m

)

EBITDA Negative EBITDA during lockdown

Positive EBITDA contributionin September

Active members:

65%of PY

0

+ve

-ve

23 Unaudited interim results for the six months ended 30 September 2020

0%

9%

39%

32%

16%

3%

1%

0%

16%

46%

23%

11%

3%

1%

Under 18

18-24

25-34

35-44

45-54

55-64

Over 65

Indicative split of Digital Sales by Gender and Age

Female Male

VIRGIN ACTIVE

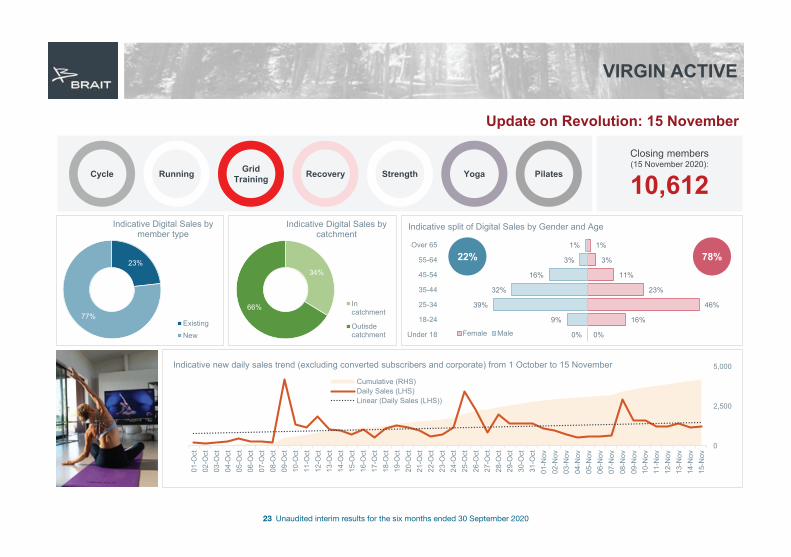

Update on Revolution: 15 November

Closing members (15 November 2020):

10,612

22% 78%23%

77%

Indicative Digital Sales by member type

ExistingNew

34%

66%

Indicative Digital Sales by catchment

Incatchment

Outisdecatchment

Cycle Running Grid Training Recovery Strength Yoga Pilates

0

2,500

5,000

0

100

200

300

400

01-O

ct02

-Oct

03-O

ct04

-Oct

05-O

ct06

-Oct

07-O

ct08

-Oct

09-O

ct10

-Oct

11-O

ct12

-Oct

13-O

ct14

-Oct

15-O

ct16

-Oct

17-O

ct18

-Oct

19-O

ct20

-Oct

21-O

ct22

-Oct

23-O

ct24

-Oct

25-O

ct26

-Oct

27-O

ct28

-Oct

29-O

ct30

-Oct

31-O

ct01

-Nov

02-N

ov03

-Nov

04-N

ov05

-Nov

06-N

ov07

-Nov

08-N

ov09

-Nov

10-N

ov11

-Nov

12-N

ov13

-Nov

14-N

ov15

-Nov

Indicative new daily sales trend (excluding converted subscribers and corporate) from 1 October to 15 November

Cumulative (RHS)Daily Sales (LHS)Linear (Daily Sales (LHS))

24 Unaudited interim results for the six months ended 30 September 2020

PREMIER

Six months ended 30 September 2020

25 Unaudited interim results for the six months ended 30 September 2020

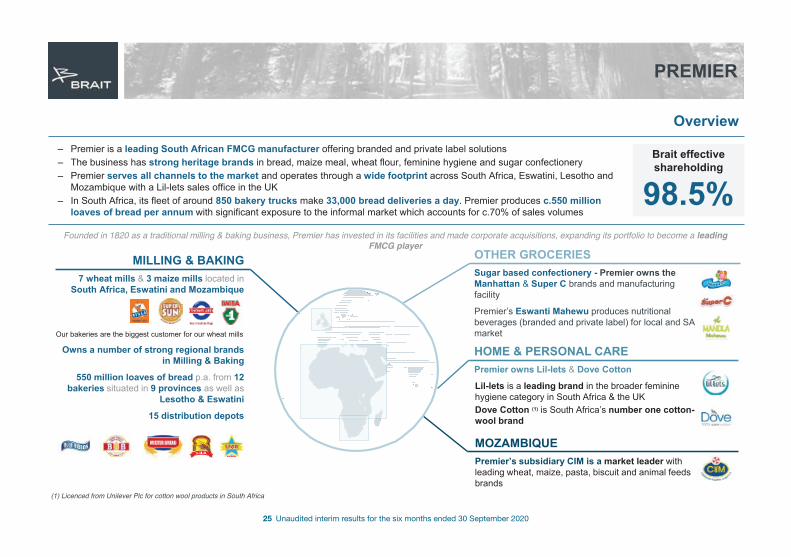

MILLING & BAKING7 wheat mills & 3 maize mills located in

South Africa, Eswatini and Mozambique

Our bakeries are the biggest customer for our wheat mills

Owns a number of strong regional brands in Milling & Baking

550 million loaves of bread p.a. from 12 bakeries situated in 9 provinces as well as

Lesotho & Eswatini

15 distribution depots

PREMIER

Overview

Brait effective shareholding

98.5%– Premier is a leading South African FMCG manufacturer offering branded and private label solutions– The business has strong heritage brands in bread, maize meal, wheat flour, feminine hygiene and sugar confectionery– Premier serves all channels to the market and operates through a wide footprint across South Africa, Eswatini, Lesotho and

Mozambique with a Lil-lets sales office in the UK– In South Africa, its fleet of around 850 bakery trucks make 33,000 bread deliveries a day. Premier produces c.550 million

loaves of bread per annum with significant exposure to the informal market which accounts for c.70% of sales volumes

Founded in 1820 as a traditional milling & baking business, Premier has invested in its facilities and made corporate acquisitions, expanding its portfolio to become a leading FMCG player

OTHER GROCERIES Sugar based confectionery - Premier owns theManhattan & Super C brands and manufacturing facility

Premier’s Eswanti Mahewu produces nutritional beverages (branded and private label) for local and SA market

HOME & PERSONAL CAREPremier owns Lil-lets & Dove Cotton

Lil-lets is a leading brand in the broader feminine hygiene category in South Africa & the UKDove Cotton (1) is South Africa’s number one cotton-wool brand

MOZAMBIQUEPremier’s subsidiary CIM is a market leader with leading wheat, maize, pasta, biscuit and animal feeds brands

(1) Licenced from Unilever Plc for cotton wool products in South Africa

26 Unaudited interim results for the six months ended 30 September 2020

PREMIER

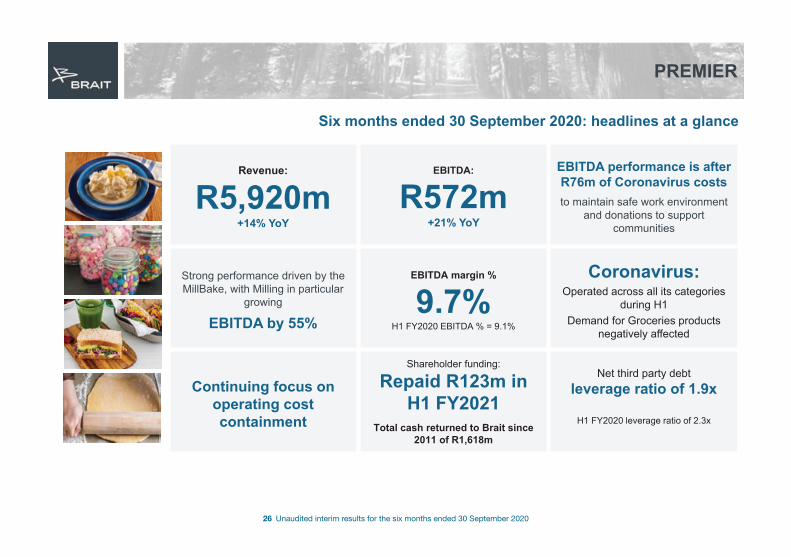

Six months ended 30 September 2020: headlines at a glance

Revenue:

R5,920m+14% YoY

EBITDA:

R572m+21% YoY

EBITDA performance is after R76m of Coronavirus coststo maintain safe work environment

and donations to support communities

Strong performance driven by the MillBake, with Milling in particular

growing

EBITDA by 55%

EBITDA margin %

9.7%H1 FY2020 EBITDA % = 9.1%

Coronavirus:Operated across all its categories

during H1Demand for Groceries products

negatively affected

Continuing focus on operating cost containment

Shareholder funding:

Repaid R123m in H1 FY2021

Total cash returned to Brait since 2011 of R1,618m

Net third party debt leverage ratio of 1.9x

H1 FY2020 leverage ratio of 2.3x

27 Unaudited interim results for the six months ended 30 September 2020

PREMIER

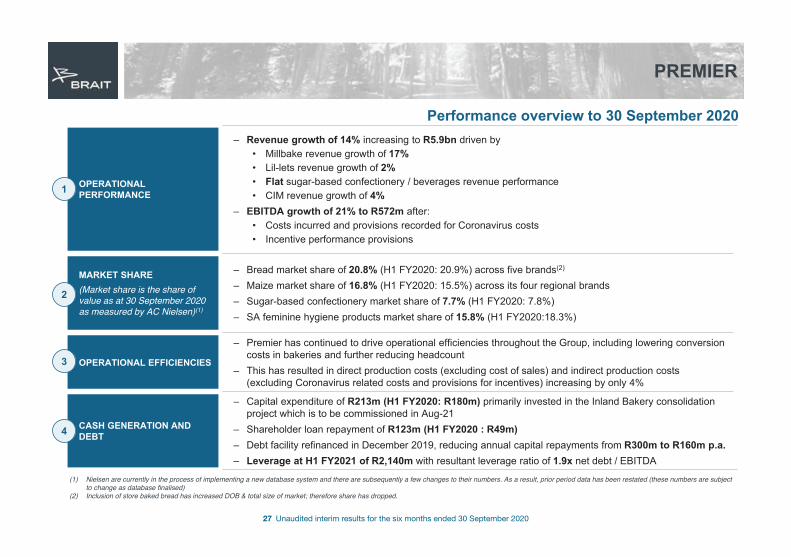

Performance overview to 30 September 2020

OPERATIONAL PERFORMANCE

– Revenue growth of 14% increasing to R5.9bn driven by• Millbake revenue growth of 17%• Lil-lets revenue growth of 2%• Flat sugar-based confectionery / beverages revenue performance• CIM revenue growth of 4%

– EBITDA growth of 21% to R572m after:• Costs incurred and provisions recorded for Coronavirus costs• Incentive performance provisions

MARKET SHARE(Market share is the share of value as at 30 September 2020 as measured by AC Nielsen)(1)

– Bread market share of 20.8% (H1 FY2020: 20.9%) across five brands(2)

– Maize market share of 16.8% (H1 FY2020: 15.5%) across its four regional brands– Sugar-based confectionery market share of 7.7% (H1 FY2020: 7.8%)– SA feminine hygiene products market share of 15.8% (H1 FY2020:18.3%)

OPERATIONAL EFFICIENCIES

– Premier has continued to drive operational efficiencies throughout the Group, including lowering conversion costs in bakeries and further reducing headcount

– This has resulted in direct production costs (excluding cost of sales) and indirect production costs (excluding Coronavirus related costs and provisions for incentives) increasing by only 4%

CASH GENERATION AND DEBT

– Capital expenditure of R213m (H1 FY2020: R180m) primarily invested in the Inland Bakery consolidation project which is to be commissioned in Aug-21

– Shareholder loan repayment of R123m (H1 FY2020 : R49m)– Debt facility refinanced in December 2019, reducing annual capital repayments from R300m to R160m p.a. – Leverage at H1 FY2021 of R2,140m with resultant leverage ratio of 1.9x net debt / EBITDA

1

2

3

4

(1) Nielsen are currently in the process of implementing a new database system and there are subsequently a few changes to their numbers. As a result, prior period data has been restated (these numbers are subject to change as database finalised)

(2) Inclusion of store baked bread has increased DOB & total size of market; therefore share has dropped.

28 Unaudited interim results for the six months ended 30 September 2020

PREMIER

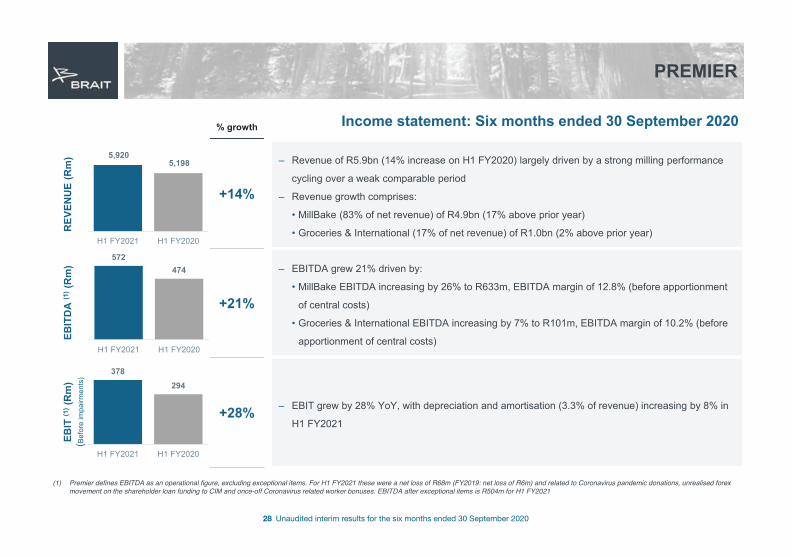

Income statement: Six months ended 30 September 2020

5,9205,198

H1 FY2021 H1 FY2020

572474

H1 FY2021 H1 FY2020

378294

H1 FY2021 H1 FY2020

REV

ENU

E (R

m)

EBIT

DA

(1)(R

m)

EBIT

(1)(R

m)

(Bef

ore

impa

irmen

ts)

% growth

+14%

+21%

+28%

– Revenue of R5.9bn (14% increase on H1 FY2020) largely driven by a strong milling performance

cycling over a weak comparable period

– Revenue growth comprises:

• MillBake (83% of net revenue) of R4.9bn (17% above prior year)

• Groceries & International (17% of net revenue) of R1.0bn (2% above prior year)

– EBITDA grew 21% driven by:

• MillBake EBITDA increasing by 26% to R633m, EBITDA margin of 12.8% (before apportionment

of central costs)

• Groceries & International EBITDA increasing by 7% to R101m, EBITDA margin of 10.2% (before

apportionment of central costs)

– EBIT grew by 28% YoY, with depreciation and amortisation (3.3% of revenue) increasing by 8% in

H1 FY2021

(1) Premier defines EBITDA as an operational figure, excluding exceptional items. For H1 FY2021 these were a net loss of R68m (FY2019: net loss of R6m) and related to Coronavirus pandemic donations, unrealised forex movement on the shareholder loan funding to CIM and once-off Coronavirus related worker bonuses. EBITDA after exceptional items is R504m for H1 FY2021

29 Unaudited interim results for the six months ended 30 September 2020

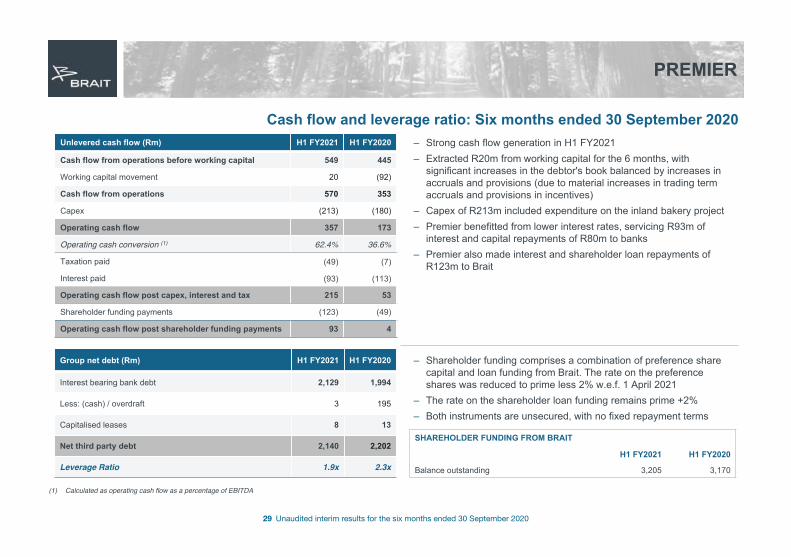

PREMIER

Cash flow and leverage ratio: Six months ended 30 September 2020– Strong cash flow generation in H1 FY2021– Extracted R20m from working capital for the 6 months, with

significant increases in the debtor's book balanced by increases in accruals and provisions (due to material increases in trading term accruals and provisions in incentives)

– Capex of R213m included expenditure on the inland bakery project– Premier benefitted from lower interest rates, servicing R93m of

interest and capital repayments of R80m to banks– Premier also made interest and shareholder loan repayments of

R123m to Brait

Unlevered cash flow (Rm) H1 FY2021 H1 FY2020

Cash flow from operations before working capital 549 445

Working capital movement 20 (92)

Cash flow from operations 570 353

Capex (213) (180)

Operating cash flow 357 173

Operating cash conversion (1) 62.4% 36.6%

Taxation paid (49) (7)

Interest paid (93) (113)

Operating cash flow post capex, interest and tax 215 53

Shareholder funding payments (123) (49)

Operating cash flow post shareholder funding payments 93 4

Group net debt (Rm) H1 FY2021 H1 FY2020

Interest bearing bank debt 2,129 1,994

Less: (cash) / overdraft 3 195

Capitalised leases 8 13

Net third party debt 2,140 2,202

Leverage Ratio 1.9x 2.3x

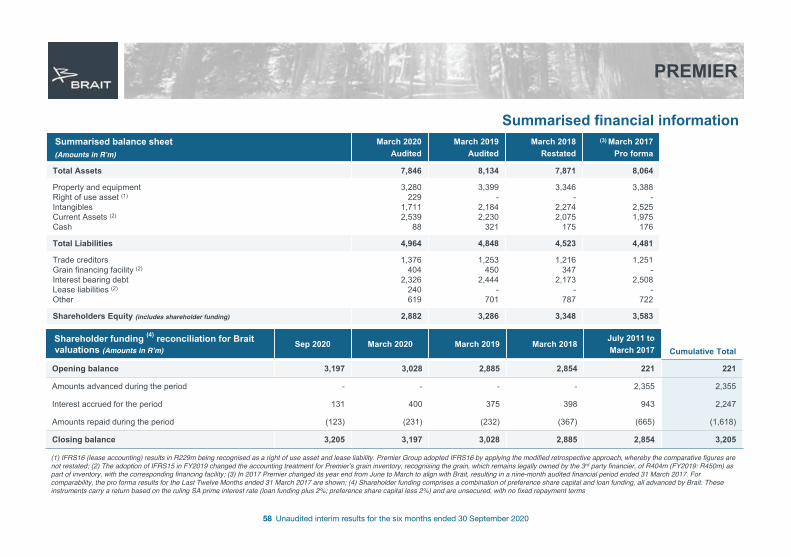

– Shareholder funding comprises a combination of preference share capital and loan funding from Brait. The rate on the preference shares was reduced to prime less 2% w.e.f. 1 April 2021

– The rate on the shareholder loan funding remains prime +2%– Both instruments are unsecured, with no fixed repayment terms

SHAREHOLDER FUNDING FROM BRAIT

H1 FY2021 H1 FY2020

Balance outstanding 3,205 3,170

(1) Calculated as operating cash flow as a percentage of EBITDA

30 Unaudited interim results for the six months ended 30 September 2020

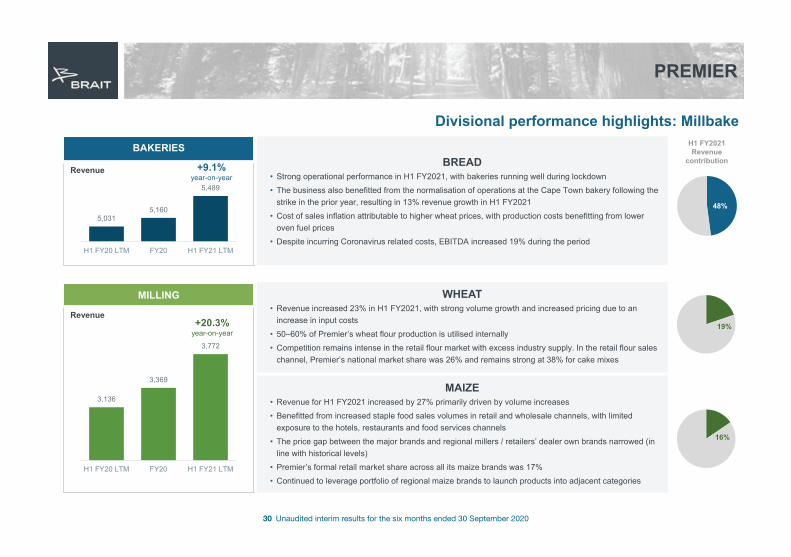

PREMIER

Divisional performance highlights: MillbakeBAKERIES

Revenue

5,0315,160

5,489

H1 FY20 LTM FY20 H1 FY21 LTM

+9.1% year-on-year

BREAD• Strong operational performance in H1 FY2021, with bakeries running well during lockdown• The business also benefitted from the normalisation of operations at the Cape Town bakery following the

strike in the prior year, resulting in 13% revenue growth in H1 FY2021• Cost of sales inflation attributable to higher wheat prices, with production costs benefitting from lower

oven fuel prices• Despite incurring Coronavirus related costs, EBITDA increased 19% during the period

WHEAT• Revenue increased 23% in H1 FY2021, with strong volume growth and increased pricing due to an

increase in input costs• 50–60% of Premier’s wheat flour production is utilised internally• Competition remains intense in the retail flour market with excess industry supply. In the retail flour sales

channel, Premier’s national market share was 26% and remains strong at 38% for cake mixes

MAIZE• Revenue for H1 FY2021 increased by 27% primarily driven by volume increases• Benefitted from increased staple food sales volumes in retail and wholesale channels, with limited

exposure to the hotels, restaurants and food services channels• The price gap between the major brands and regional millers / retailers’ dealer own brands narrowed (in

line with historical levels)• Premier’s formal retail market share across all its maize brands was 17%• Continued to leverage portfolio of regional maize brands to launch products into adjacent categories

48%

H1 FY2021 Revenue

contribution

19%

16%

MILLING

Revenue

3,136

3,369

3,772

H1 FY20 LTM FY20 H1 FY21 LTM

+20.3%year-on-year

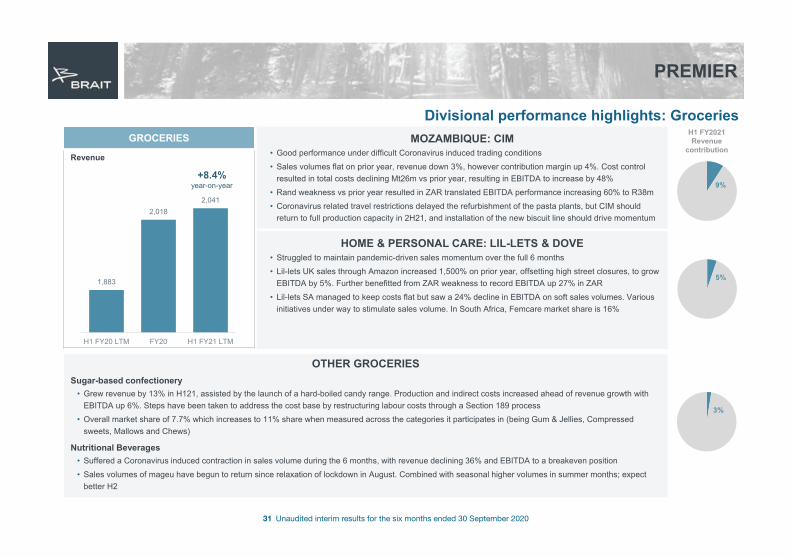

31 Unaudited interim results for the six months ended 30 September 2020

1,883

2,0182,041

H1 FY20 LTM FY20 H1 FY21 LTM

PREMIER

Divisional performance highlights: GroceriesGROCERIES

Revenue

MOZAMBIQUE: CIM• Good performance under difficult Coronavirus induced trading conditions• Sales volumes flat on prior year, revenue down 3%, however contribution margin up 4%. Cost control

resulted in total costs declining Mt26m vs prior year, resulting in EBITDA to increase by 48%• Rand weakness vs prior year resulted in ZAR translated EBITDA performance increasing 60% to R38m• Coronavirus related travel restrictions delayed the refurbishment of the pasta plants, but CIM should

return to full production capacity in 2H21, and installation of the new biscuit line should drive momentum

HOME & PERSONAL CARE: LIL-LETS & DOVE• Struggled to maintain pandemic-driven sales momentum over the full 6 months• Lil-lets UK sales through Amazon increased 1,500% on prior year, offsetting high street closures, to grow

EBITDA by 5%. Further benefitted from ZAR weakness to record EBITDA up 27% in ZAR• Lil-lets SA managed to keep costs flat but saw a 24% decline in EBITDA on soft sales volumes. Various

initiatives under way to stimulate sales volume. In South Africa, Femcare market share is 16%

OTHER GROCERIESSugar-based confectionery

• Grew revenue by 13% in H121, assisted by the launch of a hard-boiled candy range. Production and indirect costs increased ahead of revenue growth with EBITDA up 6%. Steps have been taken to address the cost base by restructuring labour costs through a Section 189 process

• Overall market share of 7.7% which increases to 11% share when measured across the categories it participates in (being Gum & Jellies, Compressed sweets, Mallows and Chews)

Nutritional Beverages• Suffered a Coronavirus induced contraction in sales volume during the 6 months, with revenue declining 36% and EBITDA to a breakeven position• Sales volumes of mageu have begun to return since relaxation of lockdown in August. Combined with seasonal higher volumes in summer months; expect

better H2

H1 FY2021 Revenue

contribution

+8.4% year-on-year

5%

3%

9%

32 Unaudited interim results for the six months ended 30 September 2020

NEW LOOK

UPDATE

33 Unaudited interim results for the six months ended 30 September 2020

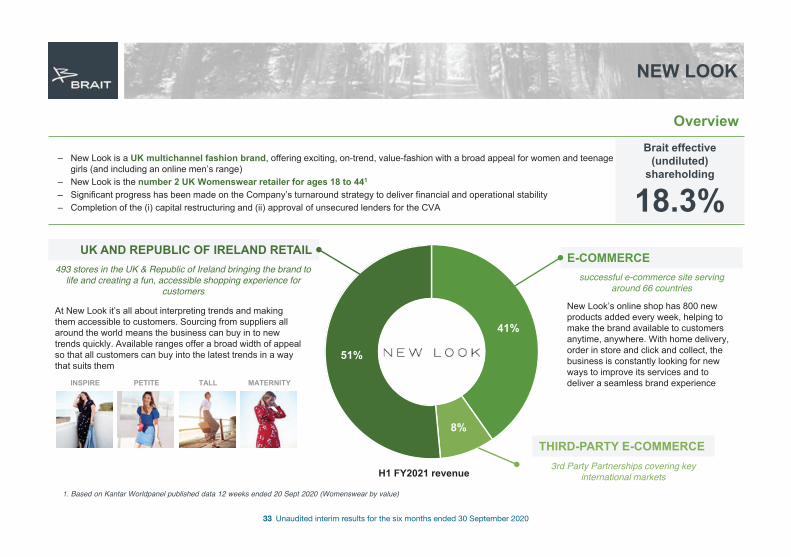

NEW LOOK

OverviewBrait effective

(undiluted) shareholding

18.3%– New Look is a UK multichannel fashion brand, offering exciting, on-trend, value-fashion with a broad appeal for women and teenage

girls (and including an online men’s range)– New Look is the number 2 UK Womenswear retailer for ages 18 to 441

– Significant progress has been made on the Company’s turnaround strategy to deliver financial and operational stability– Completion of the (i) capital restructuring and (ii) approval of unsecured lenders for the CVA

41%

8%

51%

H1 FY2021 revenue

UK AND REPUBLIC OF IRELAND RETAIL E-COMMERCE

THIRD-PARTY E-COMMERCE

successful e-commerce site serving around 66 countries

3rd Party Partnerships covering key international markets

493 stores in the UK & Republic of Ireland bringing the brand to life and creating a fun, accessible shopping experience for

customers

At New Look it’s all about interpreting trends and making them accessible to customers. Sourcing from suppliers all around the world means the business can buy in to new trends quickly. Available ranges offer a broad width of appeal so that all customers can buy into the latest trends in a way that suits them

New Look’s online shop has 800 new products added every week, helping to make the brand available to customers anytime, anywhere. With home delivery, order in store and click and collect, the business is constantly looking for new ways to improve its services and to deliver a seamless brand experienceINSPIRE PETITE TALL MATERNITY

1. Based on Kantar Worldpanel published data 12 weeks ended 20 Sept 2020 (Womenswear by value)

34 Unaudited interim results for the six months ended 30 September 2020

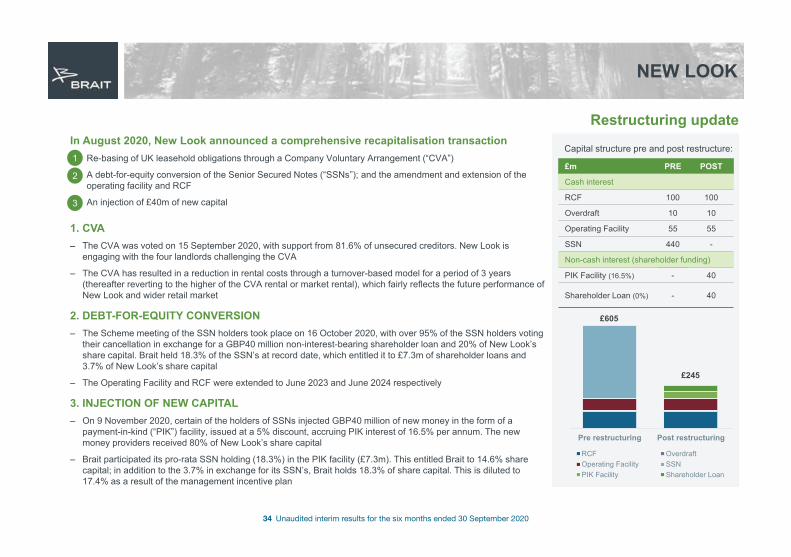

NEW LOOK

Capital structure pre and post restructure:

£m PRE POST

Cash interest

RCF 100 100

Overdraft 10 10

Operating Facility 55 55

SSN 440 -

Non-cash interest (shareholder funding)

PIK Facility (16.5%) - 40

Shareholder Loan (0%) - 40

Pre restructuring Post restructuring

RCF OverdraftOperating Facility SSNPIK Facility Shareholder Loan

£605

£245

In August 2020, New Look announced a comprehensive recapitalisation transaction1. Re-basing of UK leasehold obligations through a Company Voluntary Arrangement (“CVA”)

2. A debt-for-equity conversion of the Senior Secured Notes (“SSNs”); and the amendment and extension of the operating facility and RCF

3. An injection of £40m of new capital

1. CVA– The CVA was voted on 15 September 2020, with support from 81.6% of unsecured creditors. New Look is

engaging with the four landlords challenging the CVA

– The CVA has resulted in a reduction in rental costs through a turnover-based model for a period of 3 years (thereafter reverting to the higher of the CVA rental or market rental), which fairly reflects the future performance of New Look and wider retail market

2. DEBT-FOR-EQUITY CONVERSION– The Scheme meeting of the SSN holders took place on 16 October 2020, with over 95% of the SSN holders voting

their cancellation in exchange for a GBP40 million non-interest-bearing shareholder loan and 20% of New Look’s share capital. Brait held 18.3% of the SSN’s at record date, which entitled it to £7.3m of shareholder loans and 3.7% of New Look’s share capital

– The Operating Facility and RCF were extended to June 2023 and June 2024 respectively

3. INJECTION OF NEW CAPITAL– On 9 November 2020, certain of the holders of SSNs injected GBP40 million of new money in the form of a

payment-in-kind (“PIK”) facility, issued at a 5% discount, accruing PIK interest of 16.5% per annum. The new money providers received 80% of New Look’s share capital

– Brait participated its pro-rata SSN holding (18.3%) in the PIK facility (£7.3m). This entitled Brait to 14.6% share capital; in addition to the 3.7% in exchange for its SSN’s, Brait holds 18.3% of share capital. This is diluted to 17.4% as a result of the management incentive plan

1

2

3

Restructuring update

35 Unaudited interim results for the six months ended 30 September 2020

PORTFOLIO VALUATIONS

36 Unaudited interim results for the six months ended 30 September 2020

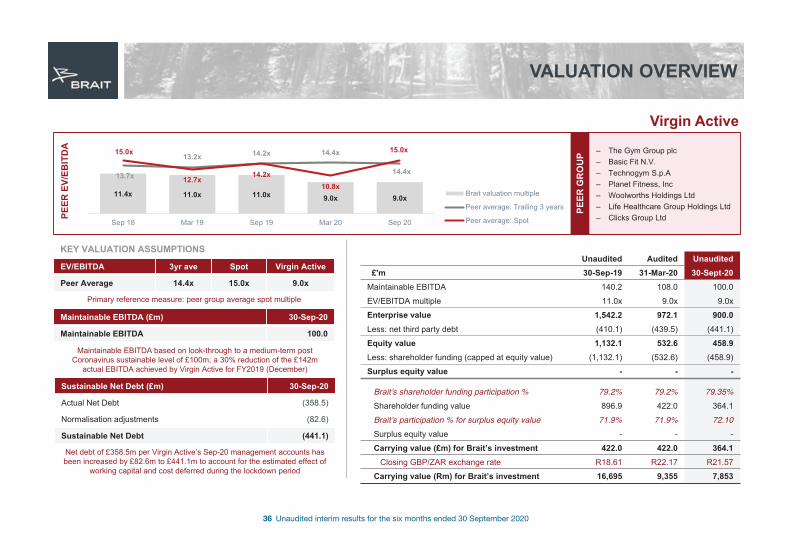

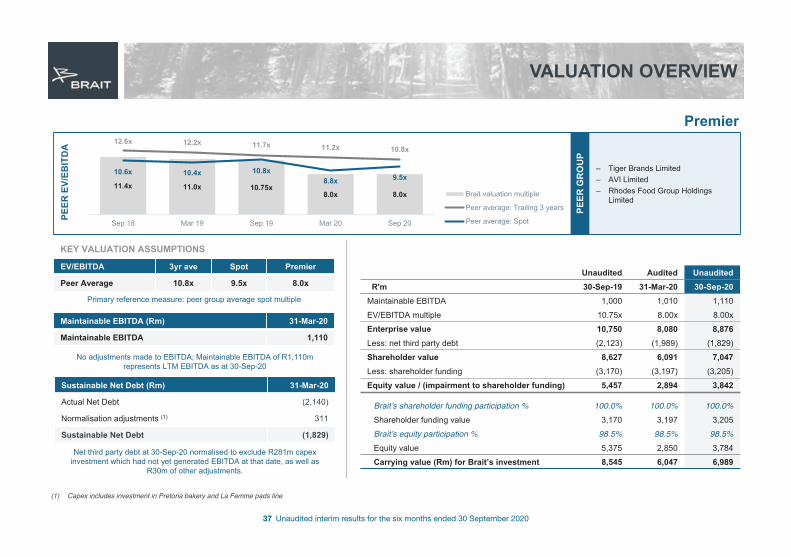

VALUATION OVERVIEW

Virgin Active

Unaudited Audited Unaudited£'m 30-Sep-19 31-Mar-20 30-Sept-20

Maintainable EBITDA 140.2 108.0 100.0

EV/EBITDA multiple 11.0x 9.0x 9.0xEnterprise value 1,542.2 972.1 900.0Less: net third party debt (410.1) (439.5) (441.1)Equity value 1,132.1 532.6 458.9Less: shareholder funding (capped at equity value) (1,132.1) (532.6) (458.9)Surplus equity value - - -

Braitʼs shareholder funding participation % 79.2% 79.2% 79.35%Shareholder funding value 896.9 422.0 364.1Braitʼs participation % for surplus equity value 71.9% 71.9% 72.10Surplus equity value - - -Carrying value (£m) for Brait’s investment 422.0 422.0 364.1

Closing GBP/ZAR exchange rate R18.61 R22.17 R21.57Carrying value (Rm) for Brait’s investment 16,695 9,355 7,853

EV/EBITDA 3yr ave Spot Virgin Active

Peer Average 14.4x 15.0x 9.0x

Maintainable EBITDA (£m) 30-Sep-20

Maintainable EBITDA 100.0

Sustainable Net Debt (£m) 30-Sep-20

Actual Net Debt (358.5)

Normalisation adjustments (82.6)

Sustainable Net Debt (441.1)

KEY VALUATION ASSUMPTIONS

– The Gym Group plc– Basic Fit N.V.– Technogym S.p.A– Planet Fitness, Inc– Woolworths Holdings Ltd– Life Healthcare Group Holdings Ltd– Clicks Group LtdPE

ER E

V/EB

ITD

A

PEER

GR

OU

P

Maintainable EBITDA based on look-through to a medium-term post Coronavirus sustainable level of £100m; a 30% reduction of the £142m

actual EBITDA achieved by Virgin Active for FY2019 (December)

Net debt of £358.5m per Virgin Active’s Sep-20 management accounts has been increased by £82.6m to £441.1m to account for the estimated effect of

working capital and cost deferred during the lockdown period

Primary reference measure: peer group average spot multiple

11.4x 11.0x 11.0x 9.0x 9.0x

13.7x

13.2x 14.2x 14.4x

14.4x

15.0x

12.7x14.2x

10.8x

15.0x

Sep 18 Mar 19 Sep 19 Mar 20 Sep 20

Brait valuation multiple

Peer average: Trailing 3 years

Peer average: Spot

37 Unaudited interim results for the six months ended 30 September 2020

VALUATION OVERVIEW

Premier

– Tiger Brands Limited– AVI Limited– Rhodes Food Group Holdings

Limited

PEER

EV/

EBIT

DA

PEER

GR

OU

P

Unaudited Audited UnauditedR'm 30-Sep-19 31-Mar-20 30-Sep-20

Maintainable EBITDA 1,000 1,010 1,110

EV/EBITDA multiple 10.75x 8.00x 8.00xEnterprise value 10,750 8,080 8,876Less: net third party debt (2,123) (1,989) (1,829)Shareholder value 8,627 6,091 7,047Less: shareholder funding (3,170) (3,197) (3,205)Equity value / (impairment to shareholder funding) 5,457 2,894 3,842

Braitʼs shareholder funding participation % 100.0% 100.0% 100.0%Shareholder funding value 3,170 3,197 3,205Braitʼs equity participation % 98.5% 98.5% 98.5%Equity value 5,375 2,850 3,784Carrying value (Rm) for Brait’s investment 8,545 6,047 6,989

EV/EBITDA 3yr ave Spot Premier

Peer Average 10.8x 9.5x 8.0x

Maintainable EBITDA (Rm) 31-Mar-20

Maintainable EBITDA 1,110

Sustainable Net Debt (Rm) 31-Mar-20

Actual Net Debt (2,140)

Normalisation adjustments (1) 311

Sustainable Net Debt (1,829)

KEY VALUATION ASSUMPTIONS

No adjustments made to EBITDA; Maintainable EBITDA of R1,110m represents LTM EBITDA as at 30-Sep-20

Net third party debt at 30-Sep-20 normalised to exclude R281m capex investment which had not yet generated EBITDA at that date, as well as

R30m of other adjustments.

Primary reference measure: peer group average spot multiple

(1) Capex includes investment in Pretoria bakery and La Femme pads line

11.4x 11.0x 10.75x8.0x 8.0x

12.6x 12.2x 11.7x 11.2x 10.8x

10.6x 10.4x 10.8x8.8x 9.5x

Sep 18 Mar 19 Sep 19 Mar 20 Sep 20

Brait valuation multiple

Peer average: Trailing 3 years

Peer average: Spot

38 Unaudited interim results for the six months ended 30 September 2020

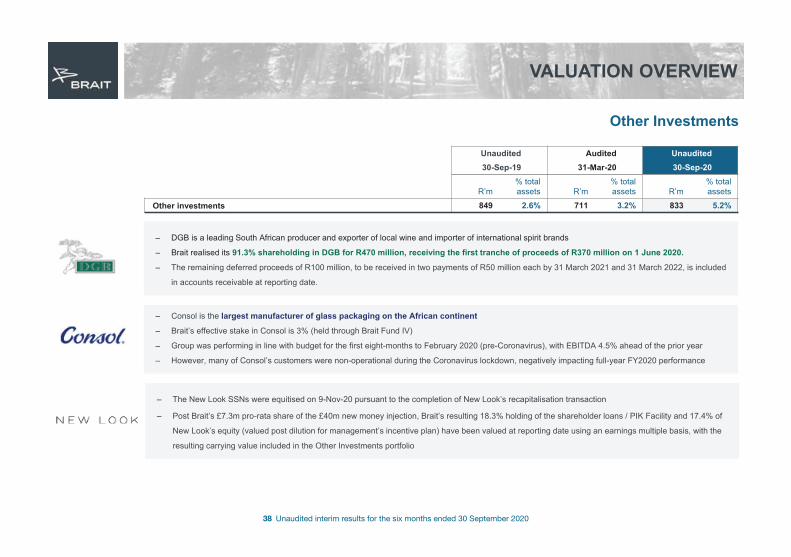

VALUATION OVERVIEW

Other Investments

– Consol is the largest manufacturer of glass packaging on the African continent

– Brait’s effective stake in Consol is 3% (held through Brait Fund IV)

– Group was performing in line with budget for the first eight-months to February 2020 (pre-Coronavirus), with EBITDA 4.5% ahead of the prior year

– However, many of Consol’s customers were non-operational during the Coronavirus lockdown, negatively impacting full-year FY2020 performance

Unaudited Audited Unaudited30-Sep-19 31-Mar-20 30-Sep-20

R’m% total assets R’m

% total assets R’m

% total assets

Other investments 849 2.6% 711 3.2% 833 5.2%

– DGB is a leading South African producer and exporter of local wine and importer of international spirit brands

– Brait realised its 91.3% shareholding in DGB for R470 million, receiving the first tranche of proceeds of R370 million on 1 June 2020.

– The remaining deferred proceeds of R100 million, to be received in two payments of R50 million each by 31 March 2021 and 31 March 2022, is included

in accounts receivable at reporting date.

– The New Look SSNs were equitised on 9-Nov-20 pursuant to the completion of New Look’s recapitalisation transaction

– Post Brait’s £7.3m pro-rata share of the £40m new money injection, Brait’s resulting 18.3% holding of the shareholder loans / PIK Facility and 17.4% of

New Look’s equity (valued post dilution for management’s incentive plan) have been valued at reporting date using an earnings multiple basis, with the

resulting carrying value included in the Other Investments portfolio

39 Unaudited interim results for the six months ended 30 September 2020

CONCLUSION & OUTLOOK

40 Unaudited interim results for the six months ended 30 September 2020

CONCLUSION & OUTLOOK

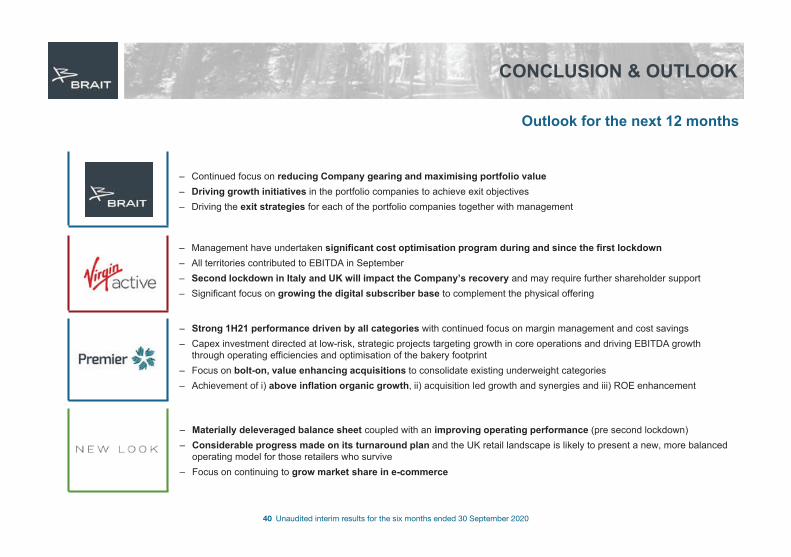

Outlook for the next 12 months

– Management have undertaken significant cost optimisation program during and since the first lockdown– All territories contributed to EBITDA in September– Second lockdown in Italy and UK will impact the Company’s recovery and may require further shareholder support– Significant focus on growing the digital subscriber base to complement the physical offering

– Strong 1H21 performance driven by all categories with continued focus on margin management and cost savings– Capex investment directed at low-risk, strategic projects targeting growth in core operations and driving EBITDA growth

through operating efficiencies and optimisation of the bakery footprint– Focus on bolt-on, value enhancing acquisitions to consolidate existing underweight categories– Achievement of i) above inflation organic growth, ii) acquisition led growth and synergies and iii) ROE enhancement

– Materially deleveraged balance sheet coupled with an improving operating performance (pre second lockdown)– Considerable progress made on its turnaround plan and the UK retail landscape is likely to present a new, more balanced

operating model for those retailers who survive– Focus on continuing to grow market share in e-commerce

– Continued focus on reducing Company gearing and maximising portfolio value– Driving growth initiatives in the portfolio companies to achieve exit objectives– Driving the exit strategies for each of the portfolio companies together with management

41 Unaudited interim results for the six months ended 30 September 2020

RESULTS PRESENTATION

ANNEXURES

FY21 H130 September 2020

42 Unaudited interim results for the six months ended 30 September 2020

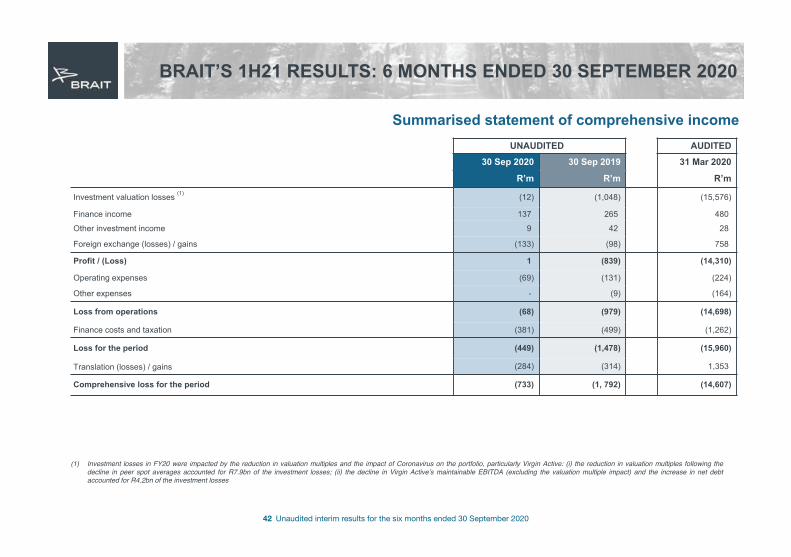

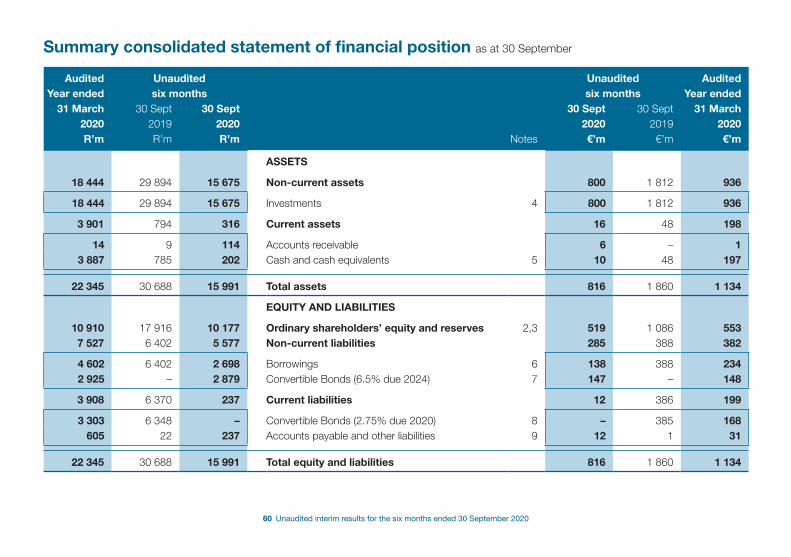

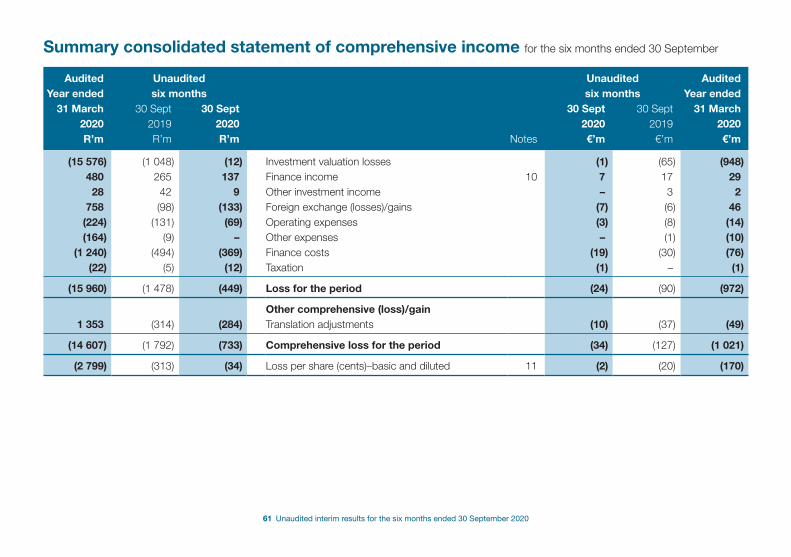

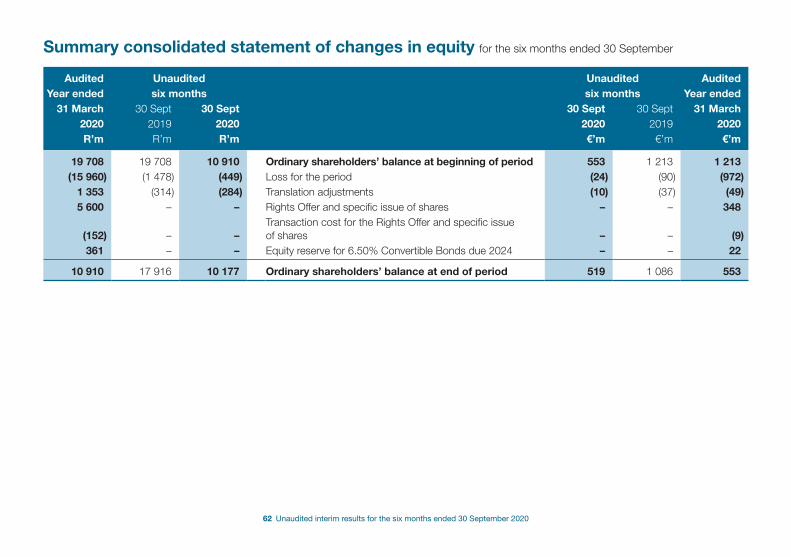

BRAIT’S 1H21 RESULTS: 6 MONTHS ENDED 30 SEPTEMBER 2020

Summarised statement of comprehensive incomeUNAUDITED AUDITED

30 Sep 2020 30 Sep 2019 31 Mar 2020

R’m R’m R’m

Investment valuation losses (1) (12) (1,048) (15,576)

Finance income 137 265 480

Other investment income 9 42 28

Foreign exchange (losses) / gains (133) (98) 758

Profit / (Loss) 1 (839) (14,310)

Operating expenses (69) (131) (224)

Other expenses - (9) (164)

Loss from operations (68) (979) (14,698)

Finance costs and taxation (381) (499) (1,262)

Loss for the period (449) (1,478) (15,960)

Translation (losses) / gains (284) (314) 1,353

Comprehensive loss for the period (733) (1, 792) (14,607)

(1) Investment losses in FY20 were impacted by the reduction in valuation multiples and the impact of Coronavirus on the portfolio, particularly Virgin Active: (i) the reduction in valuation multiples following thedecline in peer spot averages accounted for R7.9bn of the investment losses; (ii) the decline in Virgin Activeʼs maintainable EBITDA (excluding the valuation multiple impact) and the increase in net debtaccounted for R4.2bn of the investment losses

43 Unaudited interim results for the six months ended 30 September 2020

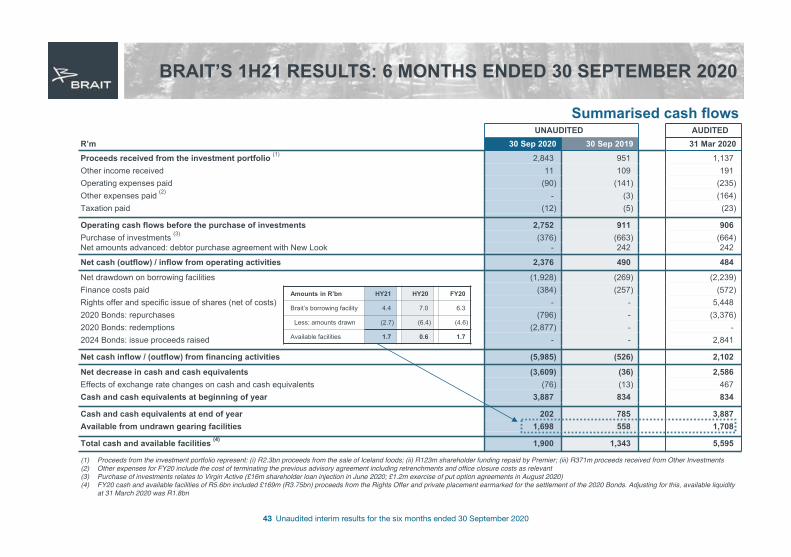

BRAIT’S 1H21 RESULTS: 6 MONTHS ENDED 30 SEPTEMBER 2020

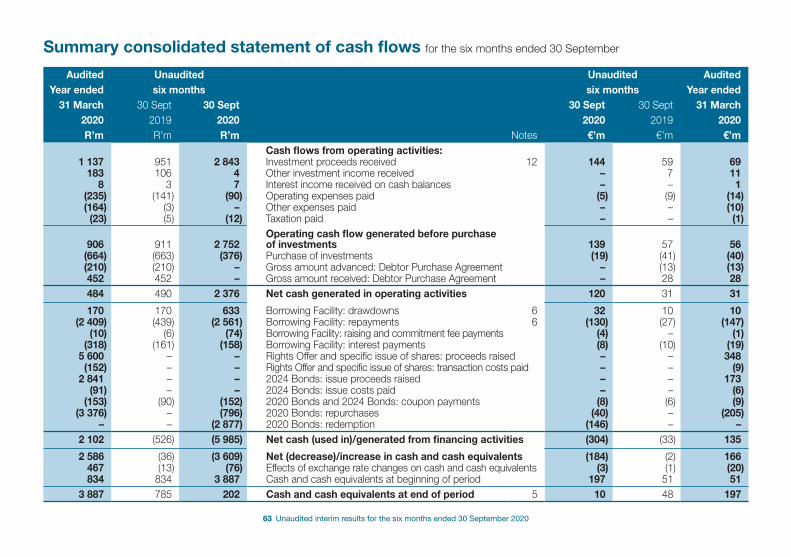

UNAUDITED AUDITEDR’m 30 Sep 2020 30 Sep 2019 31 Mar 2020Proceeds received from the investment portfolio (1) 2,843 951 1,137Other income received 11 109 191Operating expenses paid (90) (141) (235)Other expenses paid (2) - (3) (164)Taxation paid (12) (5) (23)

Operating cash flows before the purchase of investments 2,752 911 906Purchase of investments (3) (376) (663) (664)Net amounts advanced: debtor purchase agreement with New Look - 242 242

Net cash (outflow) / inflow from operating activities 2,376 490 484

Net drawdown on borrowing facilities (1,928) (269) (2,239)Finance costs paid (384) (257) (572)Rights offer and specific issue of shares (net of costs) - - 5,4482020 Bonds: repurchases (796) - (3,376)2020 Bonds: redemptions (2,877) - -2024 Bonds: issue proceeds raised - - 2,841

Net cash inflow / (outflow) from financing activities (5,985) (526) 2,102

Net decrease in cash and cash equivalents (3,609) (36) 2,586Effects of exchange rate changes on cash and cash equivalents (76) (13) 467Cash and cash equivalents at beginning of year 3,887 834 834

Cash and cash equivalents at end of year 202 785 3,887Available from undrawn gearing facilities 1,698 558 1,708

Total cash and available facilities (4) 1,900 1,343 5,595

Summarised cash flows

Amounts in R’bn HY21 HY20 FY20

Brait’s borrowing facility 4.4 7.0 6.3

Less: amounts drawn (2.7) (6.4) (4.6)

Available facilities 1.7 0.6 1.7

(1) Proceeds from the investment portfolio represent: (i) R2.3bn proceeds from the sale of Iceland foods; (ii) R123m shareholder funding repaid by Premier; (iii) R371m proceeds received from Other Investments (2) Other expenses for FY20 include the cost of terminating the previous advisory agreement including retrenchments and office closure costs as relevant(3) Purchase of investments relates to Virgin Active (£16m shareholder loan injection in June 2020; £1.2m exercise of put option agreements in August 2020)(4) FY20 cash and available facilities of R5.6bn included £169m (R3.75bn) proceeds from the Rights Offer and private placement earmarked for the settlement of the 2020 Bonds. Adjusting for this, available liquidity

at 31 March 2020 was R1.8bn

44 Unaudited interim results for the six months ended 30 September 2020

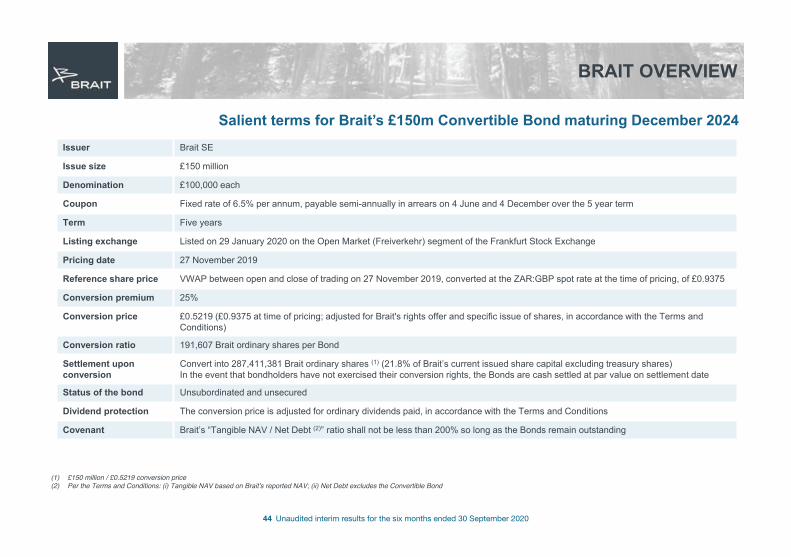

BRAIT OVERVIEW

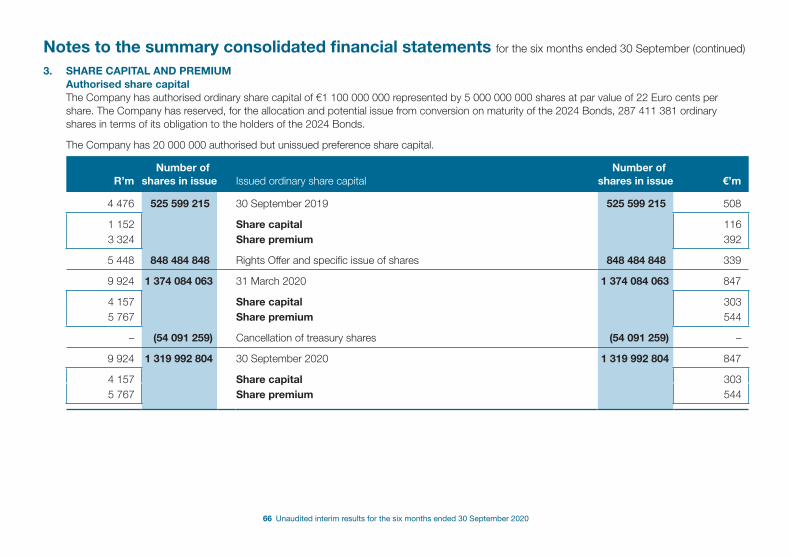

Salient terms for Brait’s £150m Convertible Bond maturing December 2024Issuer Brait SE

Issue size £150 million

Denomination £100,000 each

Coupon Fixed rate of 6.5% per annum, payable semi-annually in arrears on 4 June and 4 December over the 5 year term

Term Five years

Listing exchange Listed on 29 January 2020 on the Open Market (Freiverkehr) segment of the Frankfurt Stock Exchange

Pricing date 27 November 2019

Reference share price VWAP between open and close of trading on 27 November 2019, converted at the ZAR:GBP spot rate at the time of pricing, of £0.9375

Conversion premium 25%

Conversion price £0.5219 (£0.9375 at time of pricing; adjusted for Brait's rights offer and specific issue of shares, in accordance with the Terms and Conditions)

Conversion ratio 191,607 Brait ordinary shares per Bond

Settlement upon conversion

Convert into 287,411,381 Brait ordinary shares (1) (21.8% of Brait’s current issued share capital excluding treasury shares)In the event that bondholders have not exercised their conversion rights, the Bonds are cash settled at par value on settlement date

Status of the bond Unsubordinated and unsecured

Dividend protection The conversion price is adjusted for ordinary dividends paid, in accordance with the Terms and Conditions

Covenant Brait’s “Tangible NAV / Net Debt (2)” ratio shall not be less than 200% so long as the Bonds remain outstanding

(1) £150 million / £0.5219 conversion price(2) Per the Terms and Conditions: (i) Tangible NAV based on Braitʼs reported NAV; (ii) Net Debt excludes the Convertible Bond

45 Unaudited interim results for the six months ended 30 September 2020

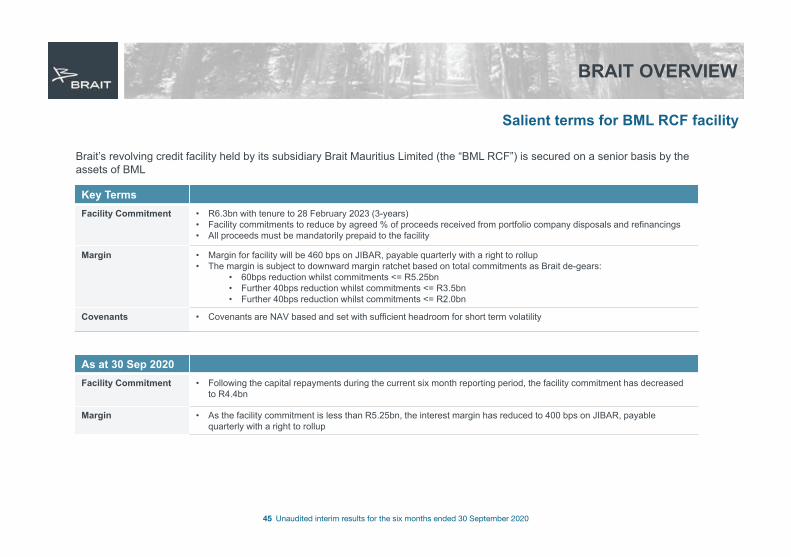

BRAIT OVERVIEW

Salient terms for BML RCF facility

Key TermsFacility Commitment • R6.3bn with tenure to 28 February 2023 (3-years)

• Facility commitments to reduce by agreed % of proceeds received from portfolio company disposals and refinancings • All proceeds must be mandatorily prepaid to the facility

Margin • Margin for facility will be 460 bps on JIBAR, payable quarterly with a right to rollup• The margin is subject to downward margin ratchet based on total commitments as Brait de-gears:

• 60bps reduction whilst commitments <= R5.25bn• Further 40bps reduction whilst commitments <= R3.5bn• Further 40bps reduction whilst commitments <= R2.0bn

Covenants • Covenants are NAV based and set with sufficient headroom for short term volatility

Brait’s revolving credit facility held by its subsidiary Brait Mauritius Limited (the “BML RCF”) is secured on a senior basis by the assets of BML

As at 30 Sep 2020Facility Commitment • Following the capital repayments during the current six month reporting period, the facility commitment has decreased

to R4.4bn

Margin • As the facility commitment is less than R5.25bn, the interest margin has reduced to 400 bps on JIBAR, payable quarterly with a right to rollup

46 Unaudited interim results for the six months ended 30 September 2020

VIRGIN ACTIVE

Additional information and summary 5-year financials

47 Unaudited interim results for the six months ended 30 September 2020

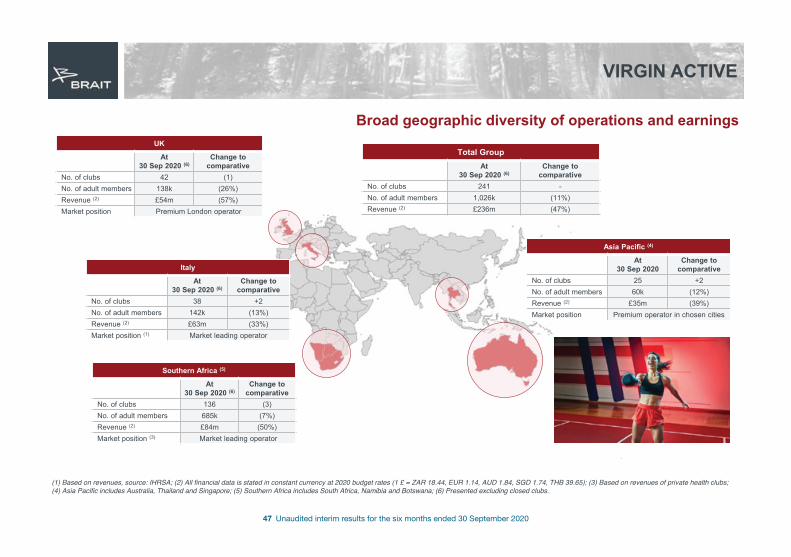

VIRGIN ACTIVE

Broad geographic diversity of operations and earningsUK

At 30 Sep 2020 (6)

Change to comparative

No. of clubs 42 (1)No. of adult members 138k (26%)Revenue (2) £54m (57%)Market position Premium London operator

Total GroupAt

30 Sep 2020 (6)Change to

comparative No. of clubs 241 -No. of adult members 1,026k (11%)Revenue (2) £236m (47%)

Italy

At 30 Sep 2020 (6)

Change to comparative

No. of clubs 38 +2No. of adult members 142k (13%)Revenue (2) £63m (33%)Market position (1) Market leading operator

Southern Africa (5)

At 30 Sep 2020 (6)

Change to comparative

No. of clubs 136 (3)No. of adult members 685k (7%)Revenue (2) £84m (50%)Market position (3) Market leading operator

Asia Pacific (4)

At 30 Sep 2020

Change to comparative

No. of clubs 25 +2No. of adult members 60k (12%)Revenue (2) £35m (39%)Market position Premium operator in chosen cities

(1) Based on revenues, source: IHRSA; (2) All financial data is stated in constant currency at 2020 budget rates (1 £ = ZAR 18.44, EUR 1.14, AUD 1.84, SGD 1.74, THB 39.65); (3) Based on revenues of private health clubs; (4) Asia Pacific includes Australia, Thailand and Singapore; (5) Southern Africa includes South Africa, Namibia and Botswana; (6) Presented excluding closed clubs.

48 Unaudited interim results for the six months ended 30 September 2020

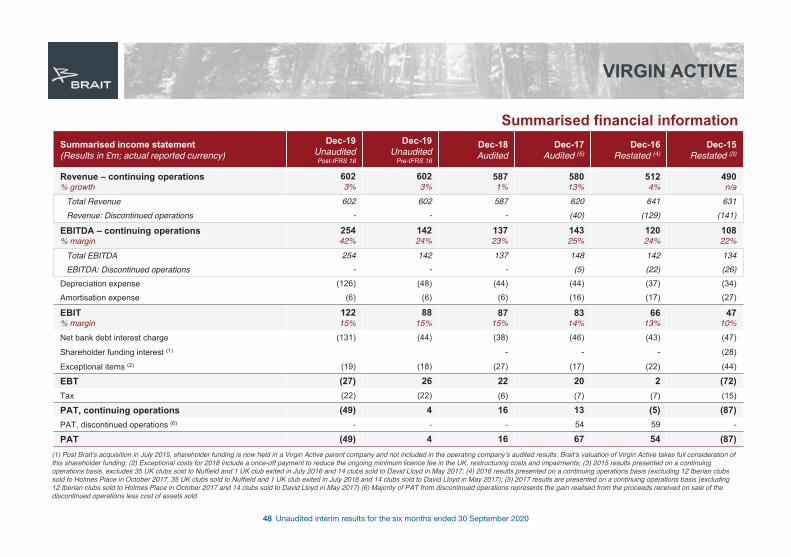

VIRGIN ACTIVE

Summarised financial informationSummarised income statement(Results in £m; actual reported currency)

Dec-19UnauditedPost-IFRS 16

Dec-19Unaudited

Pre-IFRS 16

Dec-18Audited

Dec-17Audited (5)

Dec-16Restated (4)

Dec-15Restated (3)

Revenue – continuing operations% growth

6023%

6023%

5871%

58013%

5124%

490n/a

Total Revenue 602 602 587 620 641 631Revenue: Discontinued operations - - - (40) (129) (141)

EBITDA – continuing operations% margin

25442%

14224%

13723%

14325%

12024%

10822%

Total EBITDA 254 142 137 148 142 134 EBITDA: Discontinued operations - - - (5) (22) (26)

Depreciation expense (126) (48) (44) (44) (37) (34)

Amortisation expense (6) (6) (6) (16) (17) (27)

EBIT% margin

12215%

8815%

8715%

8314%

6613%

4710%

Net bank debt interest charge (131) (44) (38) (46) (43) (47)

Shareholder funding interest (1) - - - (28)

Exceptional items (2) (19) (18) (27) (17) (22) (44)

EBT (27) 26 22 20 2 (72)Tax (22) (22) (6) (7) (7) (15)

PAT, continuing operations (49) 4 16 13 (5) (87)PAT, discontinued operations (6) - - - 54 59 -

PAT (49) 4 16 67 54 (87)(1) Post Braitʼs acquisition in July 2015, shareholder funding is now held in a Virgin Active parent company and not included in the operating companyʼs audited results. Braitʼs valuation of Virgin Active takes full consideration of this shareholder funding; (2) Exceptional costs for 2018 include a once-off payment to reduce the ongoing minimum licence fee in the UK, restructuring costs and impairments; (3) 2015 results presented on a continuing operations basis, excludes 35 UK clubs sold to Nuffield and 1 UK club exited in July 2016 and 14 clubs sold to David Lloyd in May 2017; (4) 2016 results presented on a continuing operations basis (excluding 12 Iberian clubs sold to Holmes Place in October 2017, 35 UK clubs sold to Nuffield and 1 UK club exited in July 2016 and 14 clubs sold to David Lloyd in May 2017); (5) 2017 results are presented on a continuing operations basis (excluding 12 Iberian clubs sold to Holmes Place in October 2017 and 14 clubs sold to David Lloyd in May 2017) (6) Majority of PAT from discontinued operations represents the gain realised from the proceeds received on sale of the discontinued operations less cost of assets sold

49 Unaudited interim results for the six months ended 30 September 2020

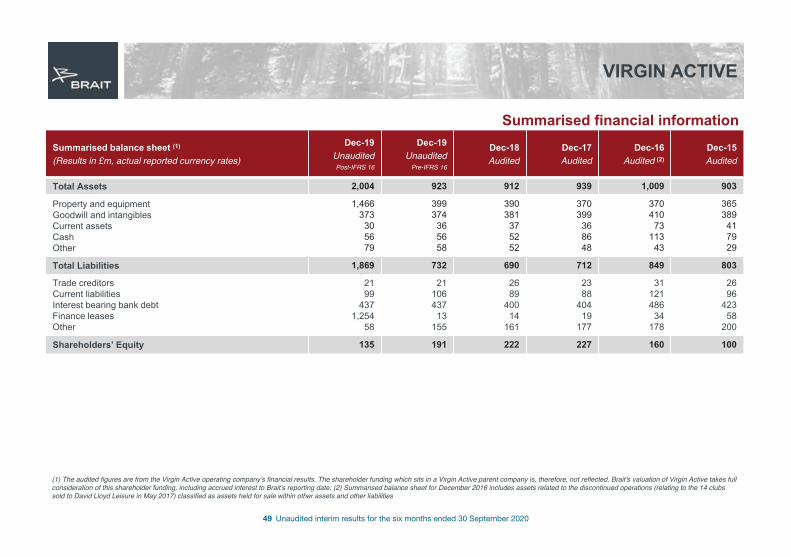

VIRGIN ACTIVE

Summarised financial informationSummarised balance sheet (1)

(Results in £m, actual reported currency rates)

Dec-19 UnauditedPost-IFRS 16

Dec-19 Unaudited

Pre-IFRS 16

Dec-18 Audited

Dec-17 Audited

Dec-16 Audited (2)

Dec-15 Audited

Total Assets 2,004 923 912 939 1,009 903

Property and equipmentGoodwill and intangiblesCurrent assetsCashOther

1,466373

305679

399374

365658

390381

375252

370399

368648

370410

73113

43

365389

417929

Total Liabilities 1,869 732 690 712 849 803

Trade creditorsCurrent liabilitiesInterest bearing bank debt Finance leasesOther

2199

4371,254

58

21106437

13155

2689

40014

161

2388

40419

177

31121486

34178

2696

42358

200

Shareholders’ Equity 135 191 222 227 160 100

(1) The audited figures are from the Virgin Active operating companyʼs financial results. The shareholder funding which sits in a Virgin Active parent company is, therefore, not reflected. Braitʼs valuation of Virgin Active takes full consideration of this shareholder funding, including accrued interest to Braitʼs reporting date; (2) Summarised balance sheet for December 2016 includes assets related to the discontinued operations (relating to the 14 clubs sold to David Lloyd Leisure in May 2017) classified as assets held for sale within other assets and other liabilities

50 Unaudited interim results for the six months ended 30 September 2020

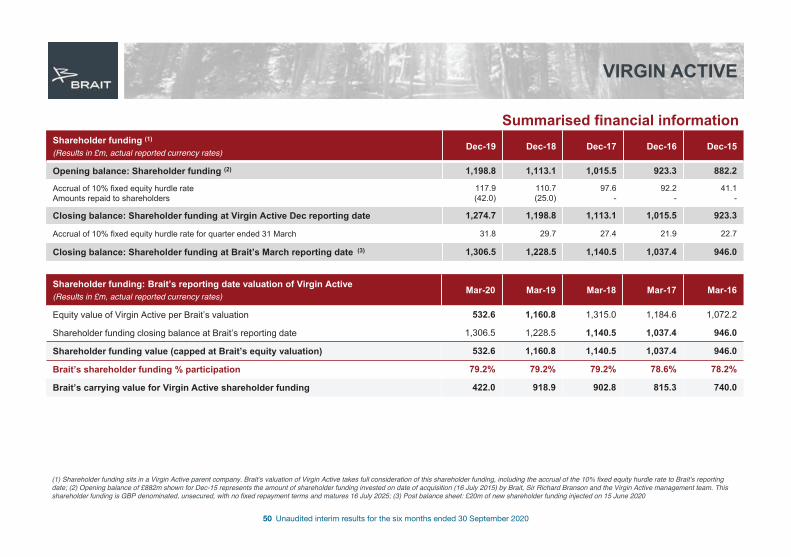

VIRGIN ACTIVE

Summarised financial informationShareholder funding (1)

(Results in £m, actual reported currency rates)Dec-19 Dec-18 Dec-17 Dec-16 Dec-15

Opening balance: Shareholder funding (2) 1,198.8 1,113.1 1,015.5 923.3 882.2

Accrual of 10% fixed equity hurdle rateAmounts repaid to shareholders

117.9(42.0)

110.7(25.0)

97.6-

92.2-

41.1-

Closing balance: Shareholder funding at Virgin Active Dec reporting date 1,274.7 1,198.8 1,113.1 1,015.5 923.3

Accrual of 10% fixed equity hurdle rate for quarter ended 31 March 31.8 29.7 27.4 21.9 22.7

Closing balance: Shareholder funding at Brait’s March reporting date (3) 1,306.5 1,228.5 1,140.5 1,037.4 946.0

Shareholder funding: Brait’s reporting date valuation of Virgin Active(Results in £m, actual reported currency rates)

Mar-20 Mar-19 Mar-18 Mar-17 Mar-16

Equity value of Virgin Active per Brait’s valuation 532.6 1,160.8 1,315.0 1,184.6 1,072.2

Shareholder funding closing balance at Brait’s reporting date 1,306.5 1,228.5 1,140.5 1,037.4 946.0

Shareholder funding value (capped at Brait’s equity valuation) 532.6 1,160.8 1,140.5 1,037.4 946.0

Brait’s shareholder funding % participation 79.2% 79.2% 79.2% 78.6% 78.2%

Brait’s carrying value for Virgin Active shareholder funding 422.0 918.9 902.8 815.3 740.0

(1) Shareholder funding sits in a Virgin Active parent company. Braitʼs valuation of Virgin Active takes full consideration of this shareholder funding, including the accrual of the 10% fixed equity hurdle rate to Braitʼs reporting date; (2) Opening balance of £882m shown for Dec-15 represents the amount of shareholder funding invested on date of acquisition (16 July 2015) by Brait, Sir Richard Branson and the Virgin Active management team. This shareholder funding is GBP denominated, unsecured, with no fixed repayment terms and matures 16 July 2025; (3) Post balance sheet: £20m of new shareholder funding injected on 15 June 2020

51 Unaudited interim results for the six months ended 30 September 2020

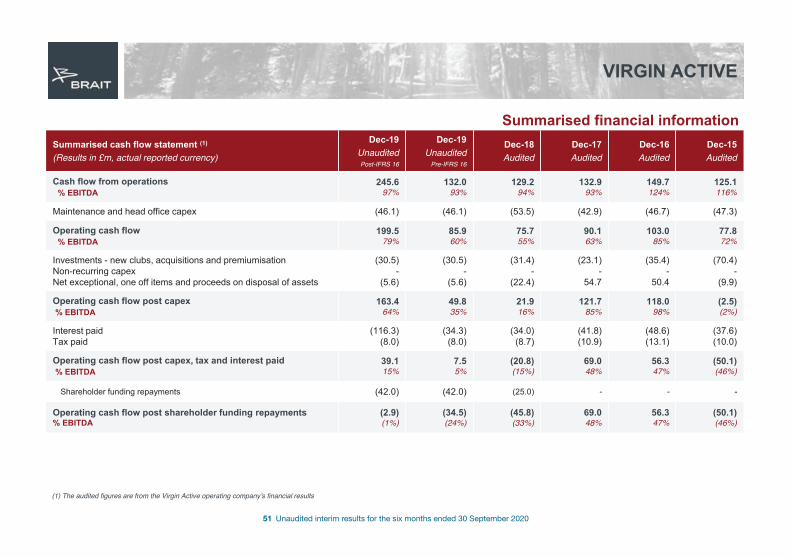

VIRGIN ACTIVE

Summarised financial informationSummarised cash flow statement (1)

(Results in £m, actual reported currency)

Dec-19UnauditedPost-IFRS 16

Dec-19Unaudited

Pre-IFRS 16

Dec-18 Audited

Dec-17 Audited

Dec-16 Audited

Dec-15 Audited

Cash flow from operations% EBITDA

245.697%

132.093%

129.294%

132.993%

149.7124%

125.1116%

Maintenance and head office capex (46.1) (46.1) (53.5) (42.9) (46.7) (47.3)

Operating cash flow% EBITDA

199.579%

85.960%

75.7 55%

90.1 63%

103.0 85%

77.8 72%

Investments - new clubs, acquisitions and premiumisationNon-recurring capexNet exceptional, one off items and proceeds on disposal of assets

(30.5)-

(5.6)

(30.5)-

(5.6)

(31.4)-

(22.4)

(23.1)-

54.7

(35.4)-

50.4

(70.4)-

(9.9)

Operating cash flow post capex% EBITDA

163.464%

49.835%

21.916%

121.785%

118.098%

(2.5)(2%)

Interest paidTax paid

(116.3)(8.0)

(34.3)(8.0)

(34.0)(8.7)

(41.8)(10.9)

(48.6)(13.1)

(37.6)(10.0)

Operating cash flow post capex, tax and interest paid% EBITDA

39.115%

7.55%

(20.8)(15%)

69.048%

56.347%

(50.1)(46%)

Shareholder funding repayments (42.0) (42.0) (25.0) - - -

Operating cash flow post shareholder funding repayments% EBITDA

(2.9)(1%)

(34.5)(24%)

(45.8)(33%)

69.048%

56.347%

(50.1)(46%)

(1) The audited figures are from the Virgin Active operating companyʼs financial results

52 Unaudited interim results for the six months ended 30 September 2020

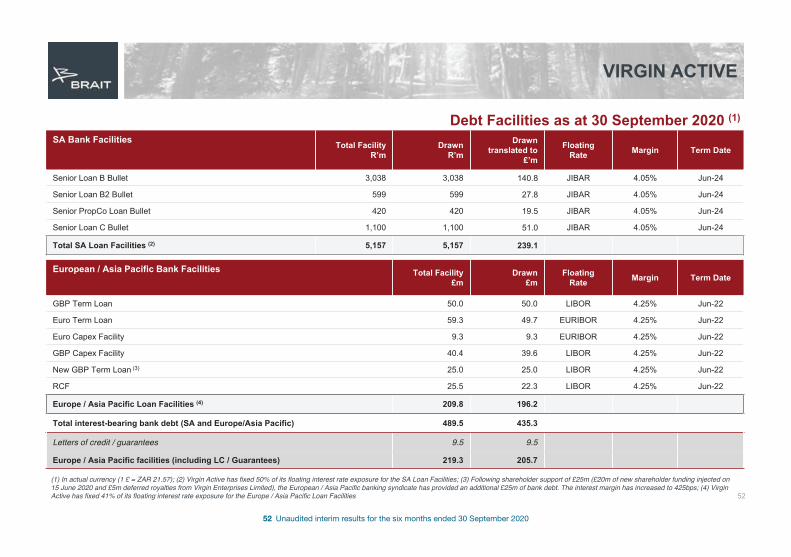

VIRGIN ACTIVE

Debt Facilities as at 30 September 2020 (1)

SA Bank Facilities Total FacilityR’m

Drawn R’m

Drawn translated to

£’m

FloatingRate Margin Term Date

Senior Loan B Bullet 3,038 3,038 140.8 JIBAR 4.05% Jun-24

Senior Loan B2 Bullet 599 599 27.8 JIBAR 4.05% Jun-24

Senior PropCo Loan Bullet 420 420 19.5 JIBAR 4.05% Jun-24

Senior Loan C Bullet 1,100 1,100 51.0 JIBAR 4.05% Jun-24

Total SA Loan Facilities (2) 5,157 5,157 239.1

European / Asia Pacific Bank Facilities Total Facility£m

Drawn£m

FloatingRate Margin Term Date

GBP Term Loan 50.0 50.0 LIBOR 4.25% Jun-22

Euro Term Loan 59.3 49.7 EURIBOR 4.25% Jun-22

Euro Capex Facility 9.3 9.3 EURIBOR 4.25% Jun-22

GBP Capex Facility 40.4 39.6 LIBOR 4.25% Jun-22

New GBP Term Loan (3) 25.0 25.0 LIBOR 4.25% Jun-22

RCF 25.5 22.3 LIBOR 4.25% Jun-22

Europe / Asia Pacific Loan Facilities (4) 209.8 196.2

Total interest-bearing bank debt (SA and Europe/Asia Pacific) 489.5 435.3

Letters of credit / guarantees 9.5 9.5

Europe / Asia Pacific facilities (including LC / Guarantees) 219.3 205.7

52

(1) In actual currency (1 £ = ZAR 21.57); (2) Virgin Active has fixed 50% of its floating interest rate exposure for the SA Loan Facilities; (3) Following shareholder support of £25m (£20m of new shareholder funding injected on 15 June 2020 and £5m deferred royalties from Virgin Enterprises Limited), the European / Asia Pacific banking syndicate has provided an additional £25m of bank debt. The interest margin has increased to 425bps; (4) Virgin Active has fixed 41% of its floating interest rate exposure for the Europe / Asia Pacific Loan Facilities

53 Unaudited interim results for the six months ended 30 September 2020

VIRGIN ACTIVE

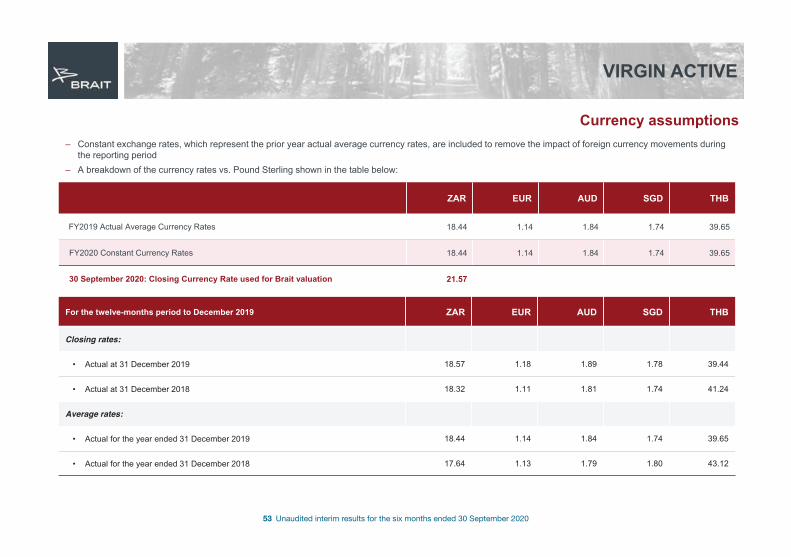

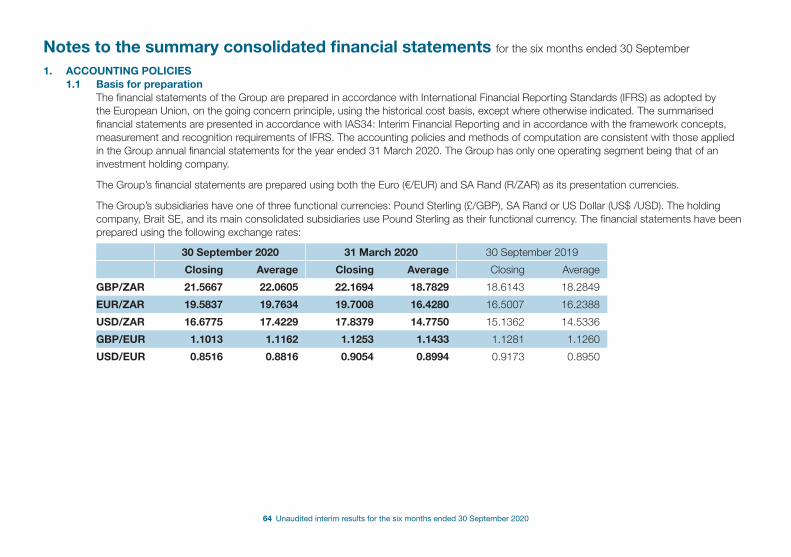

Currency assumptions– Constant exchange rates, which represent the prior year actual average currency rates, are included to remove the impact of foreign currency movements during

the reporting period– A breakdown of the currency rates vs. Pound Sterling shown in the table below:

ZAR EUR AUD SGD THB

FY2019 Actual Average Currency Rates 18.44 1.14 1.84 1.74 39.65

FY2020 Constant Currency Rates 18.44 1.14 1.84 1.74 39.65

30 September 2020: Closing Currency Rate used for Brait valuation 21.57

For the twelve-months period to December 2019 ZAR EUR AUD SGD THB

Closing rates:

• Actual at 31 December 2019 18.57 1.18 1.89 1.78 39.44

• Actual at 31 December 2018 18.32 1.11 1.81 1.74 41.24

Average rates:

• Actual for the year ended 31 December 2019 18.44 1.14 1.84 1.74 39.65

• Actual for the year ended 31 December 2018 17.64 1.13 1.79 1.80 43.12

54 Unaudited interim results for the six months ended 30 September 2020

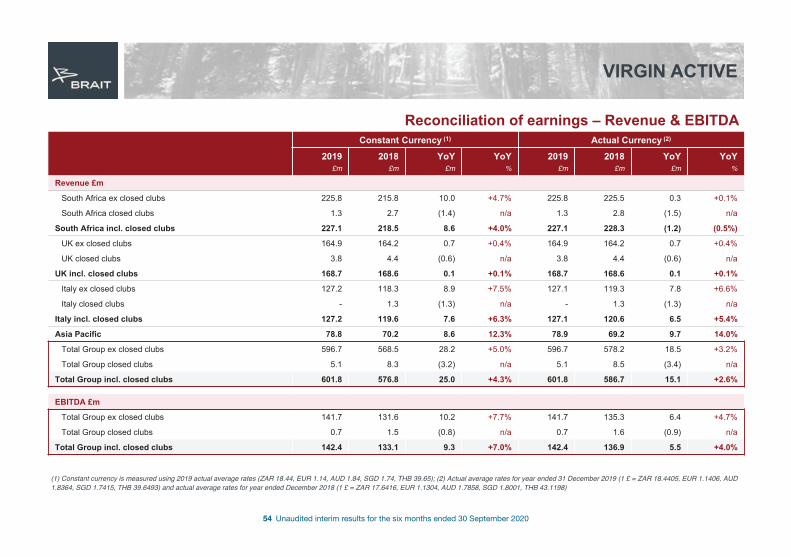

VIRGIN ACTIVE

Reconciliation of earnings – Revenue & EBITDA Constant Currency (1) Actual Currency (2)

2019£m

2018£m

YoY£m

YoY %

2019£m

2018£m

YoY£m

YoY %

Revenue £m

South Africa ex closed clubs 225.8 215.8 10.0 +4.7% 225.8 225.5 0.3 +0.1%

South Africa closed clubs 1.3 2.7 (1.4) n/a 1.3 2.8 (1.5) n/a

South Africa incl. closed clubs 227.1 218.5 8.6 +4.0% 227.1 228.3 (1.2) (0.5%)

UK ex closed clubs 164.9 164.2 0.7 +0.4% 164.9 164.2 0.7 +0.4%

UK closed clubs 3.8 4.4 (0.6) n/a 3.8 4.4 (0.6) n/a

UK incl. closed clubs 168.7 168.6 0.1 +0.1% 168.7 168.6 0.1 +0.1%

Italy ex closed clubs 127.2 118.3 8.9 +7.5% 127.1 119.3 7.8 +6.6%

Italy closed clubs - 1.3 (1.3) n/a - 1.3 (1.3) n/a

Italy incl. closed clubs 127.2 119.6 7.6 +6.3% 127.1 120.6 6.5 +5.4%

Asia Pacific 78.8 70.2 8.6 12.3% 78.9 69.2 9.7 14.0%

Total Group ex closed clubs 596.7 568.5 28.2 +5.0% 596.7 578.2 18.5 +3.2%

Total Group closed clubs 5.1 8.3 (3.2) n/a 5.1 8.5 (3.4) n/a

Total Group incl. closed clubs 601.8 576.8 25.0 +4.3% 601.8 586.7 15.1 +2.6%

EBITDA £m

Total Group ex closed clubs 141.7 131.6 10.2 +7.7% 141.7 135.3 6.4 +4.7%

Total Group closed clubs 0.7 1.5 (0.8) n/a 0.7 1.6 (0.9) n/a

Total Group incl. closed clubs 142.4 133.1 9.3 +7.0% 142.4 136.9 5.5 +4.0%

(1) Constant currency is measured using 2019 actual average rates (ZAR 18.44, EUR 1.14, AUD 1.84, SGD 1.74, THB 39.65); (2) Actual average rates for year ended 31 December 2019 (1 £ = ZAR 18.4405, EUR 1.1406, AUD 1.8364, SGD 1.7415, THB 39.6493) and actual average rates for year ended December 2018 (1 £ = ZAR 17.6416, EUR 1.1304, AUD 1.7858, SGD 1.8001, THB 43.1198)

55 Unaudited interim results for the six months ended 30 September 2020

PREMIER

Additional information and summary 5-year financials

56 Unaudited interim results for the six months ended 30 September 2020

PREMIER

Summarised income statement (Amounts in Rʼm)

March 2020Audited

(2) March 2019Restated

March 2018Restated

(5) March 2017 Pro forma

June 2016Audited

Net revenue (1)

% Growth11,048

9.5%10,093(5.6%)

10,695(8.5%)

11,6924.3%

11,20926.9%

EBITDA (3)(4)

% Margin1,0849.8%

1,00510.0%

1,09610.2%

1,1389.7%

1,16710.4%

Depreciation and amortisation (4) (407) (327) (308) (168) (251)

Impairment (6) (631) (237) (157) (140) (122)

Adjusted EBIT% margin

460.4%

4414.4%

6315.9%

8307.1%

7947.1%

Exceptional items (7) (15) (86) (48) (134) (27)

EBIT 31 355 583 696 767

Net interest charge – bank debt (258) (255) (257) (228) (201)

Interest charge – grain inventory financing (3) (37) (33) (31) - -

Interest charge – shareholder funding (400) (375) (398) (359) (320)

EBT (664) (308) (103) 109 246

PAT (626) (304) (154) 4 103

Summarised financial information

(1) The adoption of IFRS 15 in FY2019 changed the accounting treatment for by-product sales. Previously such sales were classified as a reduction to cost of goods sold; now recognised as revenue. The effect is an increase to FY2020 revenue of R620m (FY2019: increase of R476m) – no impact to EBITDA. Further to this, in FY2020, distribution centre allowances granted to customers were reclassified from operating expenses to net off against revenue in order to align with IFRS15. The effect of this change is a decrease in revenue of R119m (FY2019: decrease of R119m)

(2) As a result of distribution centre allowances granted to customers being reclassified from operating expenses to net off against revenue, FY2019 net revenue was restated from R10,212m to R10,093m (R119m decrease)(3) The adoption of IFRS 15 in FY2019 changed the accounting treatment for Premierʼs grain inventory, which remains legally owned by the 3rd party financier, is now recognised as part of Premierʼs inventory, with the

corresponding financing facility raised as a short-term facility. The holding cost is now recognised as interest expense; whereas previously it was accounted for as cost of goods sold. The effect of this change in accounting is an increase in EBITDA of R37m (FY2019: R33m) and a corresponding increase in the interest charge of R37m (FY2019: R33m)

(4) IFRS 16 (lease accounting) results in an add back to EBITDA of the rental paid of R36m for FY2020 which is reclassified as depreciation and interest expense and R229m being recognised as a right of use asset and lease liability. Premier Group adopted IFRS 16 by applying the modified retrospective approach, whereby the comparative figures are not restated

(5) In 2017 Premier changed its year end from June to March to align with Brait, resulting in a 9-month audited financial period ended 31 March 2017. For comparability, pro forma results for the LTM March 2017 are shown(6) Impairment charge for FY2020 primarily relates to the write-down in the investment in CIM for PPE and the write down of various trademarks and goodwill (7) Exceptional items for FY2020 consisted of a net loss of R15m (FY2019: net loss of R86m) and relate to strike & retrenchment costs, offset by strengthening of the Metical against the Rand on loan amounts owed by CIM to

the Group

57 Unaudited interim results for the six months ended 30 September 2020

PREMIER

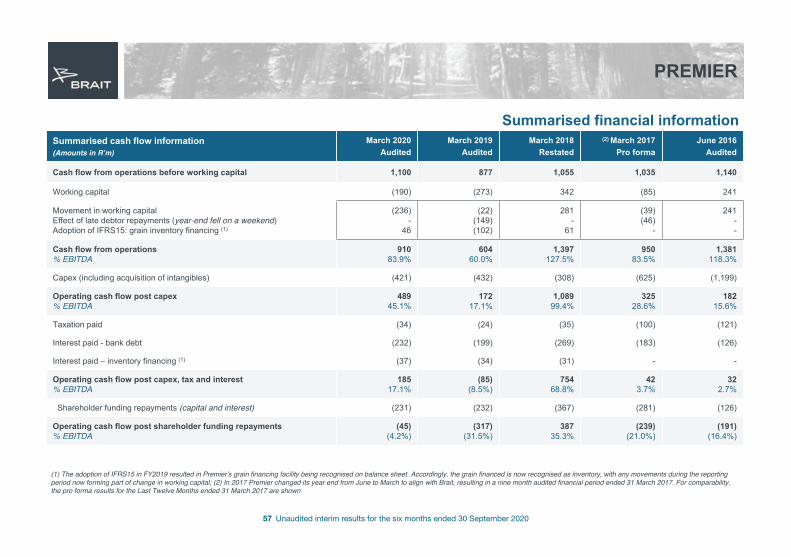

Summarised cash flow information (Amounts in Rʼm)

March 2020Audited

March 2019Audited

March 2018Restated

(2) March 2017Pro forma

June 2016Audited

Cash flow from operations before working capital 1,100 877 1,055 1,035 1,140

Working capital (190) (273) 342 (85) 241

Movement in working capitalEffect of late debtor repayments (year-end fell on a weekend)Adoption of IFRS15: grain inventory financing (1)

(236)-

46

(22)(149)(102)

281-

61

(39)(46)

-

241--

Cash flow from operations% EBITDA

91083.9%

60460.0%

1,397127.5%

95083.5%

1,381118.3%

Capex (including acquisition of intangibles) (421) (432) (308) (625) (1,199)

Operating cash flow post capex % EBITDA

48945.1%

17217.1%

1,08999.4%

32528.6%

18215.6%

Taxation paid (34) (24) (35) (100) (121)