Embed Size (px)

Citation preview

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 1/42

3

A REFORMULATION OF AUSTRIAN

BUSINESS CYCLE THEORY IN LIGHT

OF THE FINANCIAL CRISIS

JOSEPH T. SALERNO

ABSTRACT : The nancial crisis and the events leadin up t it havesparked a remarkable renewal f interest in Austrian Business CycleThery (ABCT). A number f mainstream macrecnmists have crit-icized this resurence f interest in ABCT n the runds that the therycannt explain the psitive crrelatin f cnsumptin and investmentthat ccurs ver the curse f the business cycle. They allee that thethery predicts a slump in investment and capital ds’ industriesand a crrespndin bm in cnsumptin durin the recessin. Theytherefre cnclude that ABCT is manifestly in cnict with the stylized

facts f the business cycle. In this paper I respnd t these claims. I arue

Jseph T. Salern ([email protected]) is Prfessr f Ecnmics in the Departmentf Finance and Ecnmics at the Lubin Schl f Business f Pace University.

This paper has been presented in several schlarly frums in dierent versins andhas reatly beneted frm suestins and cmments by clleaues wh are tnumerus t name. I am therefre frced t acknwlede mst f them en blc. Iwuld like t thank the participants in the fllwin frums: the Sympsium nBusiness Cycles and the New Ecnmic Reality, La Jlla, Calif., September 2010;the sessin n Business Cycle Thery at the Austrian Schlars Cnference, Auburn

Ala., March 2011; the Cllquium n Market Institutins and Ecnmic Prcessesat New Yrk University. I wuld like t particularly thank William Buts, DavidHarper, Maria Painelli and Jhn Cchran fr their cent cmments.

VoL. 15 | No. 1 | 3–44

SPRINg 2012

The

QUARTERLY

JOURNAL f

AUSTRIAN

ECONOMICS

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 2/42

4 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

that the mainstream interpretatin misrepresents essential features f thethery and cnicts with its presentatin by its leadin prpnents. I thenpresent an alternative frmulatin f the thery based n the wrks fMises, Hayek and Rthbard. I arue that this versin des satisfactrilyaccunt fr the vercnsumptin bm and subsequent retail slump thatwere such cnspicuus elements f the bm-bust cycle that played utver the past decade.

KEYWORDS: Austrian, business cycle, financial crisis, Mises,Hayek, Rothbard

JEL CLASSIFICATION : E32, B53

1. INTRODUCTION

The nancial crisis and the events leadin up t it have sparkeda remarkable renewal f interest in Austrian Business Cycle

Thery (ABCT). Several hih prle investment advisers andnancial cmmentatrs have emplyed the ABCT in their interpre-tatin f the crisis. They have been inspired t revisit this thery asa result f the manifest failure f mainstream macrecnmists tfresee r explain the subprime mrtae crisis and its subsequentmetamrphsis int a pandemic nancial meltdwn that led t thelnest recessin since Wrld War II. Interest in the thery wasreinfrced by the fact that a number f ecnmists and jurnalistsassciated with the mdern Austrian schl had warned f anemerin husin bubble durin the greenspan era when thecnventinal wisdm was that the Federal Reserve System had

matters well in hand (Thrntn, 2009).Sme prminent (and nt s prminent) mainstream macr-

ecnmists have nt respnded kindly t the sudden resurencef interest in ABCT. But rather than penly subjectin the theryt rirus, schlarly analysis in the standard research frums facademic jurnals and prfessinal cnferences, they have snipedat the thery n bl sites and in the ppular press. Furthermre,in their haste t nd aws in the thery, they have disrearded thewrks f its riinatrs and leadin prpnents, such as Ludwi

vn Mises, Friedrich A. Hayek, and Murray Rthbard. Instead theyhave drawn upn a sinle secndary surce that prtrays ABCTas a “mnetary verinvestment thery” f the business cycle. Thethery is thus described in the inuential survey f business cycle

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 3/42

5 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

theries published under the auspices f the Leaue f Natins in1937 by gttfried Haberler (1963, pp. 33–72).1 The result is thattheir criticisms are aimed at a thery that rssly misrepresentsABCT in essential respects.

The ist f their critiques is that ABCT cannt explain the psitivecrrelatin f cnsumptin and investment that ccurs ver thecurse f the business cycle. In particular they allee that the therypredicts a slump in investment and capital ds’ industries and acrrespndin bm in cnsumer spendin and retail sales durin

the recessin. They therefre cnclude that ABCT is manifestly incnict with the stylized facts f the business cycle and shuld nt be seriusly entertained.

The central thesis f this paper is that ABCT, rihtly understd,des satisfactrily accunt fr the vercnsumptin bm andsubsequent retail slump that were such cnspicuus elements f the bm-bust cycle that played ut ver the past decade. In aruinmy case, I clarify r refrmulate ABCT n several pints. First, I

dcument and emphasize the nelected pint that the Austrianthery is not an “verinvestment thery” f the business cycleand was never cnstrued as such by its mst ntable prpnents.Secnd, I explicitly extend the analysis f the eects f the central bank’s manipulatin f interest rates frm entrepreneurial chiceamn the lenth f prductin prcesses t husehld chiceamn intertempral cnsumptin patterns. Mst accunts fABCT fcus almst slely n the “malinvestments,” that is, theintertempral misallcatins f resurces, which are induced by

the permanent ap between the lan rate and the natural rate finterest created by expansinary mnetary plicy. By frmally inte-ratin the “wealth eect” int ABCT, I am able t shw hw theillusry prts and inated factr incmes and asset prices caused by mney and bank credit expansin prmte the falsicatin fhusehlds’ assessment f their net wrth and the distrtin ftheir cnsumptin/savin chices. Thus the vercnsumptin that

1 Althuh Haberler was initially a supprter f ABCT, by 1933 he had becme a

critic f the thery and in his later career mirated t the psitin f mderateestablishment Keynesian, althuh his writins still evinced his early Austrianrientatin. Fr evidence f Haberler’s intellectual miratin and linerin tracesf his Austrian trainin, see Haberler (1933, p. 99; 1974; 1996); Ebelin (2000) andSalern (2005).

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 4/42

6 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

is typically bserved durin the bm is established as a crdinateeect with entrepreneurial malinvestments in the prductinstructure attributable t the same cause: the distrtin f theinterest rate by mnetary expansin. Whether ne r the ther eectpredminates durin a iven bm depends n the histrical data.My third renement f ABCT is t link the s-called “secndarydeatin” t the pervasive malaise and wanin f “animal spirits”amn the mass f entrepreneurs that ccurs when the recessinreveals their cluster f miscalculatins and errrs and saps their

cndence in their ability t identify and calculate prtableinvestments. I arue that the secndary deatin is nt the result fan incidental mnetary cntractin that depresses sme arbitraryprice level; rather it is a reactin t and crrectin f the relativeprice distrtin caused by the extreme verbiddin f factr andasset prices durin the euphria f the bm. When allwed t runits curse, this relative price adjustment inevitably re-establishes anatural interest rate suciently hih t stimulate capitalists andentrepreneurs t dishard cash and actively seek ut investment

pprtunities. When stunted by “quantitative easin” and scaldecits driven by stimulus prrams, the entrepreneurial malaise becmes chrnic, and ecnmic stanatin ensues.

In sectin 2, I briey delineate the dimensins f the recent retailslump, and shw that, in several respects, it was indeed unprec-edented. The criticisms f ABCT by mainstream macrecnmistsallein that the thery cannt accunt fr such a develpmentare surveyed in sectin 3. I respnd t these criticisms in sectin4 aruin that ABCT is nt an “verinvestment thery” at all.

Rather, I arue, bth “malinvestment” and “vercnsumptin”ccur cntempraneusly durin the bm and whether ne rthe ther eect predminates is determined by cncrete histricalcircumstances. I als indicate hw my arument diers frmthat presented by Rer garrisn (2001, 2004), which reaches thesame cnclusin by a dierent rute.2 Sectin 5 discusses thevercnsumptin and “capital cnsumptin” that ccurred durinthe bm leadin up t the nancial crisis and ives a summaryassessment f their manitude and relatin t the ensuin retail

2 Althuh several criticisms are aimed at his arument belw, they d nt diminishthe sinicance f garrisn’s achievement in drawin the attentin f cntem -

prary ecnmists t the vercnsumptin eect in ABCT.

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 5/42

7 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

slump. I utline the implicatins f my refrmulatin fr theanalysis f the phenmenn f “secndary deatin” in sectin 6.I cnclude in sectin 7.

2. THE RETAIL SLUMP IN THE GREAT RECESSION OF2007–2009.

Perhaps the mst prminent feature f the recent recessin in theU.S., aside frm the cllapse f the husin sectr, was the excep-

tinally severe retail slump that characterized it. one indicatin fits severity was the precipitus decline in retail and fd servicesales. Fr December 2008, the year-ver-year decline in currentdllar sales was 11.1 percent and frm January thuh July 2009these year-ver-year declines uctuated between 8.5 percent and10.5 percent (Federal Reserve Bank f St. Luis [2010b]).3 Exceptfr tw nncnsecutive mnths durin the recessin f 1990–1991in which the percent chane in mnthly retail sales dipped slihtly belw zer n a year-ver-year basis, ne wuld have t back

t 1960–1961 t nd declines in current dllar retail sales durina recessin, althuh nthin like the manitude experienceddurin the latest recessin.4

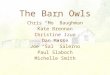

Real retail sales (Fiure 1) als tk an exceptinally sharpplune durin the recessin. Fr example, in all previusrecessins beinnin with the 1960–1961 recessin, mnthly realretail sales cmpared t a year a decreased by 8 percent r mrefr nly three mnths, all in the mini-recessin f 1980. By cntrast,

durin the 2007–2009 dwnturn real retail sales n a year-ver-year basis cntracted by 8 percent r mre fr nine cnsecutivemnths, endin in May 2009 (Federal Reserve Bank f St. Luis[2010b]). overall, year-ver year retail sales rwth was neativefr 23 cnsecutive mnths endin Nvember 1, 2009. As f April,2010, real retail and fd service sales, seasnally adjusted, std

3 All data n retail sales and cnsumptin are drawn frm this surce unlesstherwise nted.

4 The data fr the retail sales series prir t 1992 is nt strictly cmparable t thedata n retail sales and fd services frm 1992 t the present since the frmer aren an SIC (Standard Industrial Classicatin basis and the latter n an NAICS(Nrth American Industry Classicatin System) basis. See Federal Reserve Bankf St. Luis (2010a), p. 12; and als U.S. Census Bureau (2010).

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 6/42

8 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

at $166.886 billin, abve its recessinary truh f 158.109 frFebruary 2009, but still well belw its lcal pre-recessin peak f$180.290 billin f octber 2007.

Figure 1.

190

180

170

160

150

140

110

120

130

2

0 0 8

2

0 1 0

2

0 1 2

1

9 9 2

1

9 9 4

2

0 0 6

2

0 0 4

2

0 0 2

2

0 0 0

1

9 9 8

1

9 9 6

Real Retail and Food

Services Sales,

$ Billions

The qualitative dimensins f the retail slump can be traced inthe brad rane f icnic American retailers that succumbed t bankruptcies, liquidatins, r massive retrenchments. Chryslerled Chapter 11 n April 11, 2009 fllwed by gM n June 1, 2009.KB Tys, ne f the larest U.S. ty retailers, suht Chapter 11prtectin in December 2008 and annunced that it planned t

clse all f its 460 retail utlets. Circuit City, the secnd larestelectrnics retailer in the U.S., declared bankruptcy and clsedall f its 575 stres in 2009. Midsize electrnics retailer CmpUSAclsed all f its 103 utlets (althuh it has since sld its name and16 f its sites and returned under a new wner). Sharper Imae, aleadin nvelty and electrnics retailer, als declared bankruptcy.Linen ‘N Thins, the secnd-larest hme ds retailer in the U.S.led Chapter 11 and liquidated its 371 stres. Frtun, a leadin

jewelry and hme furnishin chain in the Nrtheast, led fr bankruptcy, as did midsize furniture retailers Levitz and Bmbay, bth f which were liquidated. Many mre retail chains scrappedexpansin plans and prceeded with massive cuts in the number

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 7/42

9 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

f their utlets, includin Disney (98), Ann Taylr (117), Ftlcker(140) and numerus thers.5

3. THE MAINSTREAM CRITIQUE OF ABCT: A CASEOF MISTAKEN IDENTITY

As nted, recently sme mainstream ecnmists have criticized aptted versin f ABCT that fcuses almst exclusively n “frcedsavin” and crrespndin “verinvestment” as the primary, if

nt the nly, distrtins ccurrin durin the inatinary bm.The mst inuential frmulatin f this versin was presented byHaberler (1963) in his survey f business cycle theries publishedin 1937 under the auspices f the Leaue f Natins. Accrdin tHaberler’s interpretatin, the bm phase f the cycle is initiated by bank credit expansin in the frm f “duciary media” runbacked demand depsits. This results in an increase in the supplyf lanable funds beynd the level f vluntary savin. The arti-

cially swllen supply f credit depresses the risk-adjusted interest

rate n credit markets belw the level f the “natural rate,” whichis the rate f return n investment in the structure f prductinthat is cnsistent with intertempral cnsumptin preferences.The articially-depressed lan rate in turn induces additinal business brrwin which causes spendin n capital r “hiherrder” ds t increase relative t spendin n cnsumer dsand ther “lwer rder” ds such as direct inputs in the makinf cnsumer ds.

Under cnditins f full emplyment, the diversin f mre fthe areate spendin stream frm cnsumer ds’ t capitalds’ industries causes a crrespndin chane in relative pricesthat reallcates resurces frm the frmer t the latter industries.The expansin f the prductin f capital ds thus cmes atthe expense f the prductin f cnsumer ds, thereby causinthe prices f cnsumer ds t increase and cnsumptin t berestricted. This phenmenn is knwn as “frced savin,” becausethe redirectin f resurces frm cnsumer ds’ prductin t

capital ds’ prductin caused by bank credit expansin desnt cmprt with the vluntary savin preferences f husehlds.

5 See Barbar (2008), Baertlein (2009), Farfan (2009), Zarrell (2009).

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 8/42

10 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

The expansinary phase f the cycle cmes t an end when thecentral bank reacts t acceleratin cnsumer price inatin rsme ther event by sinicantly restrictin its expansin f bankreserves. Credit markets tihten and the risk-adjusted interest raterises tward its natural level, nce aain cnstrictin investmentt the limits impsed by vluntary savin. The hiher interestrates brin the investment bm t a halt. Firms prducin capitalds, especially specialized machines, tls and ther equipmentrelatively specic t prcesses temprally remte frm cnsumers,

encunter an unanticipated drp in spendin n their utputand, cnsequently, declinin prices and prts. At the same timethe spendin stream directed tward cnsumer ds cntinuest swell fr a while because previus injectins f new mneyalready paid ut in waes and rents by capital ds’ prducersare transfrmed int spendin n cnsumer ds nly after alapse f time. As a result, the price f labr cntinues t be bid up by cnsumer ds’ rms.

Faced with increasin wae rates and the risin cst f credit,

capital ds’ prducers can n lner prtably sustainprductin at current levels. Payrlls and ther variable csts areslashed and plant and equipment are idled, as sme rms retrenchand thers shut dwn altether. Unemplyment rises and therecessin sets in.

Durin the recessin, spendin n capital ds declines relativet spendin n cnsumer ds. This represents a reversal f thechane in relative spendin streams that characterized the bm and

initiates an adjustment prcess that re-establishes an ptimal patternf emplyment fr labr and ther resurces that nce aain accrdswith the intertempral cnsumptin preferences and vluntarysavin f market participants. The “structure f prductin” is thusre-riented t deliver mre cnsumer ds in the present and nearfuture and fewer in mre distant future perids.

It is imprtant t nte a salient feature f the frein accuntf ABCT. There are n references t the entrepreneur, mnetarycalculatin, uncertainty r expectatins. In Haberler’s frmu-

latin, the cycle is driven exclusively by the relative swellin andcntractin f current spendin streams directed tward dierentsectrs f the ecnmy. The interest rate n lans is merely amechanism peratin directly t enlare r cnstrict the channels

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 9/42

11 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

f these spendin ws. Reardless f what causes the chane inthe interest rate, the eect n the relative spendin ws is alwayssymmetrical. Specically, a fall in the lan rate will enlare relativespendin n capital ds and mve resurces t hiher stae usesfrm lwer stae uses. A rise in the interest rate will have reverseeects n relative spendin ws and resurce mvements.

There are three implicatins f what we may call this “hydraulic”cnceptin f ABCT. First, the bm invlves a shift f labrand ther resurces ut f cnsumer ds’ int capital ds’

industries, while the recessin invlves a symmetrical resurceshift in the ppsite directin. Secnd, the frced savin and verin-vestment f the bm is accmpanied by a decline in cnsumptinand shrinkae f the nished cnsumer ds’ manufacturin,whlesale, and retail sectrs as resurces are reallcated t thehiher staes f prductin. Third, the recessin is characterized byan expansin f cnsumptin as the verinvestment f the bmis revealed and crrected and the temprarily misplaced resurcesare released back int prcesses prducin ds fr cnsumptin

in the near future. The new prductin structure pretty muchresembles the ld, pre-verinvestment structure, except fr sme“xed” capital that may have been sunk in hiher stae prductinprcesses that had t be abandned befre cmpletin.

Haberler (1963, p. 71) recnized these implicatins, cmmentin:

It is a little dicult t understand... why the transitin t a mrerundabut prcess f prductin shuld be assciated with prsperityand the return t a less rundabut prcess a synnym fr depressin.

Why shuld nt the riinal inatinary expansin f investmentcause as much dislcatin in the prductin f cnsumers’ ds as thesubsequent rise in cnsumers’ demand is said t cause in the prductinf investment ds?

Mainstream critics have seized n Haberler’s hydrauliccnceptin f ABCT t dismiss the thery as manifestly incn-sistent with the stylized facts f the business cycle. In particularit is bserved that, ver the business cycle, investment and

cnsumptin are psitively crrelated and the mvement ffactrs back t cnsumer ds’ industries durin the recessinis accmpanied by substantial unemplyment f labr that wasabsent durin the mvement f factrs t capital ds industries

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 10/42

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 11/42

13 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

“sustainable” levels, the ecnmy had respnded by “verinvestin”in capital, and n cure was pssible that did nt invlve a recnitinthat capital had been verinvested and wasted and that the ecnmy’scapital stck needed t shrink.6

Predictably, Deln’s critique f the thery was remarkablysimilar t Krumans’s (and Haberler’s). Arued DeLn (2010):

There is enerally n perid f hih unemplyment when resurcesare transferred ut f cnsumptin-prducin sectrs int investment

ds-prducin sectrs. There is n necessity that the transfer fresurces ut f investment ds-prducin sectrs be accmpanied by hih unemplyment. The business f shiftin resurces betweensectrs is pretty much rthnal t the business f maintainin nearfull-emplyment and prper capacity utilizatin.

Australian ecnmist Jhn Quiin presented a similar bjectint ABCT, cncludin:

...[U]nless Say’s Law is vilated, the Austrian mdel implies thatcnsumptin shuld be neatively crrelated with investment ver the business cycle, whereas in fact the ppsite is true. T the extent that bmsare driven by mistaken beliefs that investments have becme mre prf -itable, they are typically characterized by hih, nt lw, cnsumptin.

Lastly, we qute gere Masn University ecnmist BryanCaplan (2008) wh ave perhaps the mst trenchant critique fhydraulic ABCT:

The Austrian thery als suers frm serius internal incnsistencies. If,as in the Austrian thery, initial cnsumptin/investment preferences“re-assert themselves,” why dn’t the cnsumptin ds industriesenjy a hue bm durin depressins? After all, if the prices f thecapital ds factrs are t hih, are nt the prices f the cnsumptinds factrs t lw? Wae wrkers in capital ds industries areunhappy when ld time preferences re-assert themselves. But waewrkers in cnsumer ds industries shuld be verjyed. TheAustrian thery predicts a decline in emplyment in sme sectrs, but anincrease in thers; thus, it des nthin t explain why unemplyment is

6 Nte that fr DeLn capital investment is limited directly by psychlicalattitudes twards risk rather than by cncrete acts f savin, as if the materialresurces required fr capital frmatin culd be simply cnjured ut f the ether.

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 12/42

14 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

hih durin the “bust” and lw durin the “bm”.... [T]he thery desnt predict an increase in emplyment durin the bm, r a decreasedurin the bust. Mrever, it predicts an actual increase in current utputdurin the bust. These are puzzlin implicatins, t put it mildly, andthey fllw frm the ABC[T].

All f the frein critiques are essentially the same in acrucial respect: they are based n a view f ABCT as simply aarden-variety neclassical thery f sectral shifts. This is encap-

sulated in the term “verinvestment” which implies t many

resurces allcated t the capital ds’ sectr and t few t thecnsumer ds’ sectr. overinvestment always lically impliesundercnsumptin in this tw-sectr mdel, whse relativeprice is the interest rate. This mdel diers nt in the least frma tw-cmmdity, tw-cuntry internatinal trade mdel withincreasin csts and incmplete specializatin. In this mdel theimpsitin f a tari, say, n wine will distrt the relative price between wine and clth, increasin the relative price f wine andstimulatin the mvement f resurces frm clth t wine in the

cuntry imprtin wine. The relative price and w f resurceswill mve in the ppsite directin in the wine-exprtin cuntry.If the tari is then remved, the result will be a cunter-mvementf resurces ut f each cuntry’s imprt-cmpetin industry intits exprt sectr.

Nw let us a little beynd the cmparative static mdel funderraduate textbks and assume: an imperfect deree flabr mbility; a prductin functin fr each d that includes

incnvertible xed capital; and static expectatins abut plicy. Inthis case, there will be a “bm” in the imprt-cmpetin sectrand a “bust” in the exprt sectr f bth cuntries when the tari isinitially impsed. Transitry unemplyment will appear and smeinvestment in xed capital will be lst, but thins will n prettymuch as they had befre. These eects will be exactly symmetricalin the ppsite directin when the tari is remved.

Nte that variatins in the mney supply are nt cmpletelyneutral in this trade mdel despite the fact that there is nly ne

relative price. If we assume that individual value scales are dier-entiated frm ne anther and that unanticipated injectins fnew mney initially are unevenly distributed t thse cnsumerswhse marinal valuatins favr wine ver clth, then the price

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 13/42

15 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

f wine will rise relative t clth and the same pattern f bmand bust will ccur in the tw industries that ccurred in the taricase. The eects f unexpectedly haltin the mnetary injectinswill crrespnd t eects f the tari remval. Thus the Haber-lerian-mainstream caricature f ABCT describes a nnmnetarythery f a self-reversin shift f resurces between tw sectrs.The nly rle played by mney is t cause the initial distrtinf the sinle relative price in a tw-sectr ecnmy. Thus in thehydraulic mdel, mnetary expansin causes precisely the same

diversin f spendin ws and relative prices as a tari r manyther nnmnetary interventins int the ecnmy. But ABCTwas desined t explain the unique distrtins created in the realecnmy and its prductin structure by an inatinary bm.Indeed, the very essence f ABCT, the falsicatin f mnetarycalculatin, plays n rle whatever in the hydraulic mdel.

4. ABCT: A THEORY OF OVERCONSUMPTION

AND MALINVESTMENT

Had the critics seriusly studied the riinal surces in whichABCT is expunded, they wuld have learned that it is nt an“verinvestment” thery at all. In fact, Mises, Rthbard and,smewhat less emphatically, Hayek arued explicitly that “ver-cnsumptin” and “malinvestment” were the essential features fthe inatinary bm. In their view, the diverence between thelan and natural rates f interest caused by bank credit expansinsystematically falsies the mnetary calculatins f entrepreneurschsin amn investment prjects f dierent duratins and indierent staes varyin in tempral remteness frm cnsumers.But it als distrts the incme and wealth calculatins and therefrethe cnsumptin/savin chices f the recipients f waes, rents,prts and capital ains. In ther wrds, while the articiallyreduced lan rate encuraes business rms t verestimatethe present and future availability f investible resurces and t

malinvest in lenthenin the structure f prductin, at the sametime it misleads husehlds int a falsely ptimistic appraisal ftheir real incme and net wrth that stimulates cnsumptin anddepresses savin.

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 14/42

16 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

Althuh vercnsumptin is caused directly by what may be called the “wealth” r “net wrth” eect, it is nanced by theincrease in the mney supply and, later in the bm, the drawindwn f cash balances as inatinary expectatins take hld.on the real side, the increase in the prices and prtability fcnsumer ds diverts factrs frm hiher staes t cnsumerds’ industries, thereby restrictin the supply f resurcesavailable t add t r even replace the stck f capital ds. Thisis what Austrian ecnmists call “capital cnsumptin,” which is a

pervasive feature f the bm. Far frm bein the essence f ABCT,verinvestment is thus lically ruled ut by it—the bm resultsin the prductin f fewer nt mre capital ds.

Mises (1998, pp. 546–547) vividly described the nature andimplicatins f vercnsumptin:

It wuld be a serius blunder t nelect the fact that inatin als eneratesfrces which tend tward capital cnsumptin. one f its cnsequencesis that it falsies ecnmic calculatin and accuntin. It prduces thephenmenn f imainary r apparent prts.... If the rise in the pricesf stcks and real estate is cnsidered as a ain, the illusin is n lessmanifest. What make peple believe that inatin results in eneralprsperity are precisely such illusry ains. They feel lucky and becmepen-handed in spendin and enjyin life. They embellish their hmes,they build new mansins and patrnize the entertainment business. Inspendin apparent ains, the fanciful result f false recknin, they arecnsumin capital. It des nt matter wh these spenders are. They may be businessmen r stck jbbers. They may be wae earners....

Rthbard (2000, p. 30) als emphatically rejected the verin-vestment explanatin f ABCT n essentially the same rundsas Mises, referrin t it as a “miscnceptin... iven currency by Haberler’s famus Prosperity and Depression.” Accrdin tRthbard (2004, p. 993):

Supercially, it seems that credit expansin reatly increases capital,fr the new mney enters the market as equivalent t new savinsfr lendin. Since the new “bank mney” is apparently added t thesupply f savins n the credit market, businesses can nw brrwat a lwer rate f interest; hence inatinary credit expansin seemst er the ideal escape frm time preference, as well as an inex -haustible funt f added capital. Actually, this eect is illusry. on

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 15/42

17 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

the cntrary, inatin reduces savin and investment.... It may evencause lare-scale capital cnsumptin.

After discussin the falsicatin f capital accuntin andresultin verstatement f prts caused by inatin, Rthbard(2004, pp. 993–994) cncluded

Inatin, therefre, tricks the businessman: it destrys ne f his mainsinpsts and leads him t believe that he has ained extra prts whenhe is just able t replace capital. Hence, he will undubtedly be temptedt cnsume ut f these prts and thereby unwittinly cnsume capitalas well. Thus, inatin tends at nce t repress savin-investment and tcause cnsumptin f capital.

This brins us t the rle f frced savin as the surce andimpetus t verinvestment. As already nted, accrdin t thehydraulic versin f ABCT, frced savin ccurs durin the bmwhen incme is redistributed frm thse whse marinal valu-atins f present ver future cnsumptin r “time preferences”are hiher t thse whse time preferences are lwer. This willresult in an verall increase in savin relative t cnsumptin andtherefre in the supply f investible resurces in the ecnmy. Thisfrced savin will fuel the verinvestment. Mises rejected thisarument fr tw reasns. First he nted that frced savin is nta necessary utcme f inatin; it is cntinent upn the cncretedata that shapes a histrical inatinary prcess. Arued Mises,

[o]ne must realize that frced savin can result frm inatin, butneed nt necessarily. It depends n the particular data f each instancef inatin whether r nt the rise in wae rates las behind the risein cmmdity prices. A tendency fr real wae rates t drp is nt aninescapable cnsequence f a decline in the mnetary unit’s purchasinpwer. It culd happen that nminal wae rates rise mre r sner thancmmdity prices....

Secnd, and mre imprtant, is the pint that even whencircumstances prevailin at the beinnin f an inatin fster

frced savin t such an extent that resurces are released frmcnsumer ds’ and ther lwer stae industries, the situatinwill inevitably be reversed as the bm prresses. Inatinaryexpectatins eventually intensify and becme widespread,

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 16/42

18 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

amplifyin the tendency tward vercnsumptin t the pintwhere it verwhelms the tendency t frced savin. Mises (1998,pp. 555–556) thus cncluded:

[W]ith the further prress f the expansinist mvement the rise in theprices f the cnsumers’ ds will utstrip the rise in the prices f theprducers’ ds. The rises in waes and salaries and the additinalains f the capitalists, entrepreneurs, and farmers, althuh a reatpart f them is merely apparent, intensify the demand fr cnsumers’ds.... It is custmary t describe the bm as verinvestment.

Hwever additinal investment is nly pssible t the extent that thereis an additinal supply f capital ds available. As, apart frm frcedsavin, the bm itself des nt result in a restrictin but rather in anincrease in cnsumptin, it des nt prcure mre capital ds fr newinvestment. The essence f the credit-expansin bm is nt verin-vestment, but investment in wrn lines, i.e., malinvestment.

Hayek’s cnceptin f frced savin was dierent frm Mises’s,as Rer garrisn (2004) has nted. Mises used the term “frcedsavin” t dente an actual increase in savin that results whencredit expansin redistributes incme frm wrkers, typicallypssessin relatively hih time preferences, t capitalist-entre-preneurs, whse time preferences are typically lwer. Hayek, incntrast, cnceived f frced savin as a pattern f investment thatis incnsistent with prevailin time preferences, a situatin which,as we shall see belw, Mises referred t as “malinvestment.”Nevertheless, despite this terminlical dierence, Hayek trecnized that bth frced savin (malinvestment) and vercn-

sumptin characterized the bm.Hayek arued that a cnstant rate f frced savin wuld require

an increasing rate f credit expansin in rder t allw capitalists tmaintain and expand the labr frce and cmplementary factrsdevted t prducin an elnated capital structure by successfullycunterin risin bids fr these factrs by the prducers fcnsumer ds. The cntinual pressure t expand cnsumerds’ prductin exerts itself thruh the ever-risin waes paidut in the hiher stae industries. These hiher waes, which

result frm the previus injectin f new mney thruh creditexpansin, appear as increased demand by labrers n cnsumerds’ markets after a lapse f time. Prices f cnsumer dsare thus driven up, apprximatin the rate f inatin fr capital

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 17/42

19 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

ds after a shrt la and causin the waes ered by cnsumerds’ prducers t rise apace. Nw in rder t maintain the ratef frced savin cnstant, i.e., sustain the existin ap betweeninvestment and vluntary savin ver time, it wuld be necessaryt cntinually divert additional labr and land factrs durinsuccessive time perids t the hiher staes. As Hayek (2008, p.319) arued, this requires that credit expansin be renewed at acntinually increasin rate. Eventually the increasin rate f priceinatin wuld inite inatinary expectatins, distrt mnetary

calculatin and falsify capital accuntin, culminatin in vercn-sumptin and capital destructin.

Hayek (2008, pp. 320–321) described the frces leadin t ver-cnsumptin in an appendix t the secnd editin f Prices and

Production published in 1935:

[W]hether the prices f the cnsumer’ ds will rise faster r slwer,all ther prices, and particularly the prices f the riinal factrs fprductin, will rise even faster. It is nly a questin f time when thiseneral and prressive rise f prices becmes very rapid. My arumentis nt that such a develpment is inevitable nce a plicy f creditexpansin is embarked upn, but that it has to be carried t that pint if acertain result—a cnstant rate f frced savin, r maintenance withutthe help f vluntary savin f capital accumulated by frced savin—ist be achieved.

once this stae is reached, such a plicy will sn bein t defeat itswn ends. While the mechanism f frced savin cntinues t perate,the eneral rise in prices will make it increasinly dicult, and nallypractically impssible, fr entrepreneurs t maintain their capital intact.Paper prts will be cmputed and cnsumed; the failure t reprducethe existin capital will becme quantitatively mre and mre imprtant,and will nally exceed the additins made by frced savin.7

S like Mises and Rthbard, Hayek als believed that vercn-sumptin was a denin characteristic f the bm, althuhhe admittedly did nt attribute t it such a prminent rle as

7 The appendix is a respnse t a critique by Alvin Hansen and H. Tut f the rsteditin f Prices and Prductin. Hayek’s analysis f vercnsumptin des ntappear in the riinal text f the bk. This may accunt fr the fact that evenAustrian ecnmists have misinterpreted Hayek n this pint.

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 18/42

20 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

Mises did.8

Thus, I cannt cmpletely aree with Rer garrisn(2004, p. 333) when he cncludes, “Almst, inexplicably Hayeknever ives play t the vercnsumptin that accmpanies creditexpansin r even acknwledes the pssibility f it.” garrisn(2004, pp. 327–328) als des nt quite capture the essence f thevercnsumptin eect as frmulated by Mises when he prtraysit mainly as an utcme assciated with a plicy-induced fall inthe interest rate cnceived as an incentive t cnsume mre andsave less. Mises attributed vercnsumptin t the distrtin f

mnetary calculatin caused by credit expansin, which inducesentrepreneurs and husehlds t verestimate their incme andnet wrth. Fr Mises, the interest rate is much mre imprtant inits rle as a discunt factr than as an inducement t save.9 Asthe inatinary bm prceeds, prts bein t reularly exceedeven the mst ptimistic expectatins. These “paper prts,” asHayek calls them, becme almst universal, creatin a eneralclimate f ver-ptimism and “irratinal exuberance” thatundermines shrewd entrepreneurial judment. Reinfrced by

inatinary expectatins, this results in a rwin verestimatinf prspective prt streams which, when discunted by the arti-cially lw interest rate, enerates ctitius capital ains thruhutthe structure f prductin that are cmpletely unhined frm thefundamental realities.

At this pint capital accuntin becmes a strybk f fantasiesand self-delusin rather than a recknin based n a sber judmentf the future. In additin t the emerence f phantm prts

8 In fact, Hayek published an imprtant but nelected article n “CapitalCnsumptin” in 1932. Althuh the article discussed the phenmenn in thecntext f nnmnetary vernment interventins, Hayek (1984, pp. 156–157, n.2) recnized the link between capital cnsumptin and the business cycle in aftnte, althuh at this pint he nly nted its relevance t “the later staes fa depressin.” Hwever, this article was published tw years befre the articlethat was included as an appendix t the secnd editin f Prices and Prductincited abve.

9 Indeed, Mises (1998, p. 525) explicitly denied that the interest rate was aninducement t save:

Peple d nt save and accumulate capital because there is interest. Interestis neither the impetus t savin nr the reward r cmpensatin rantedfr abstainin frm cnsumptin. It is the rati in the mutual valuatin fpresent ds aainst future ds.

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 19/42

21 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

and capital ains, a rapid rise in waes is caused by the attemptf entrepreneurs thruhut the prductin structure t acquirethe factrs necessary t expand their peratins in the later phasesf the bm. This wae spiral and the expectatins it enendersals fsters vercnsumptin. The verall result f these inatin-induced distrtins f incme and wealth is, as Rthbard (2009,p. 793) pinted ut, that “the market’s cnsumptin/investmentrati” r time preference is systematically increased, thus drivingup the natural rate durin the bm. The ap between the natural

rate and the plicy-distrted interest rate thus widens, causinentrepreneurial miscalculatins and malinvestments t prliferateand intensify.

T thse critics wh bject that ABCT implicitly assumes“mney illusin” n the part f entrepreneurs, the answer is thatin a dynamic ecnmy with a cmplex capital structure the nlymethd available t entrepreneurs fr reliably estimatin theutcme f their decisins and investments is mnetary calcu-

latin. Hayek (2008, p. 321) made this assumptin explicit in Pricesand Production , writin:

It is imprtant... t remember that the entrepreneur necessarily andinevitably thinks f capital in terms f mney, and that, under chanincnditins, he has n ther way f thinkin f its quantity then in valueterms, which practically means in terms f mney. But even if, fr a time,he resists the temptatin f paper prts (and experience teaches us thatthis is extremely unlikely) and cmputes his csts in terms f sme indexnumber, the rate f depreciatin has nly t becme fast enuh, and

such an expedient will be ineective.

Nw the same calculatinal distrtin that prduces vercn-sumptin als cncurrently prduces the phenmenn f malin-vestment. Since the supply f capital ds are diminished by ver-cnsumptin, verinvestment cannt cnceivably ccur. Hwever,t the extent that the newly created bank credit is rst btained by entrepreneurs at reduced interest rates, they have the meansand the incentive t expand their peratins r t initiate whlly

new investment prjects whse fundin exceeds the availablequantity f vluntary savins. The demands and prices fr hiherstae ds necessary t carry ut these investments are increasedand there is a crrespndin rise in the capital values f rms

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 20/42

22 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

prducin these ds. Resurces are diverted int prducin newminin and il drillin equipment, site plannin and preparatinfr new hydrelectric plants, develpin cmputer sftware fruse in desinin slar-pwered aircraft and s n.10 At the sametime, factrs are bein verused in supplyin direct inputs t themanufacturers f nished cnsumer ds and in mre intensivelyperatin their facilities, as well as in cnstructin and manninadditinal warehuse and retail space. These malinvestments at bth ends create a “hle” in the middle staes f the structure f

prductin, which is “papered” ver by prts and capital ainscaused by the falsicatin f mnetary calculatin.

As the bm cntinues, rms cnfrnt an increasin scarcityf the resurces necessary t fully utilize the new minin and ildrillin equipment, t cnstruct the hydrelectric plant and tenineer and mass prduce the new eneratin f aircraft. In astrictly metaphrical sense, then, we may say that the lenthenedstructure f prductin cannt be “cmpleted.” The anticipateddemands fr the prducts f the hiher stae investment prjects,even if they are technlically peratinal, d nt materialize because f the reater scarcity and cstliness f the cmplementarylabr and capital needed t prtably transfrm these prductsint lwer rder capital ds. At the same time and as part fthe same prcess, ther rms lwer dwn in the structure fprductin that prduce raw inputs, spare parts, and equipmentfr the supply, maintenance and repair f plants and equipmentmanufacturin nished cnsumer ds are als incurrin risinlabr csts, causin them t cut back n capacity.

Frm the ecnmic pint f view, malinvestment and capitalcnsumptin cause the structure f prductin t disinterateint pieces that cannt be tted back tether aain withut aprtracted recessin-adjustment prcess. Durin this prcess bthinvestment and cnsumptin will decline causin unemplymentt rise in bth sectrs. The recessin will be further prlned bythe fact that entrepreneurs, after experiencin massive lsses andcapital write-dwns, will temprarily lse cndence bth in their

ability t frecast future market cnditins and in the reliability f

10 The last is nt a cmpletely hypthetical example. See gaudin (2010), Khanduja(2010), Daily Mail Reprter (2010).

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 21/42

23 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

mnetary calculatin. It is this lss f entrepreneurial cndencethat is the crux f the s-called “secndary deatin.” Entre-preneurs will increase their demand fr mney and hihly liquidassets and pass up ptentially prtable pprtunities that theywuld have seized upn in their nrmal state f cndence. Thusit is the endenus factr f entrepreneurial pessimism and skit-tishness and nt the exenus factr f a cntractin f the mneysupply that brins abut the drp in the eneral scale f prices and,mre imprtant, in the prices f the factrs f prductin relative

t prduct prices. It is precisely the rise f the natural interest rateimplicit in the relative decline f factr prices that restres theentrepreneurs’ natural ptimism and venturesmeness.

In fact, as Mises (1998, pp. 568–569) explained, s-called“secndary deatin” is caterically distinct frm a mnetarydeatin, fr it is nt the cause f a prtracted recessin-adjustmentperid but its essential cnsequence and cure:

Inrance manifests itself... in the cnfusin f deatin and cntractin

and f the prcess f readjustment int which every expansinist bm must lead. It depends n the institutinal structure f the creditsystem which created the bm whether r nt the crisis brins abut arestrictin in the amunt f duciary media…. [E]ven with n restrictinsin the supply f mney prper and duciary media available, thedepressin brins abut a cash-induced tendency tward an increasein the purchasin pwer f the mnetary unit. Every rm is intentupn increasin its cash hldins, and these endeavrs aect the rati between the supply f mney... and the demand fr mney... fr cashhldin. This may be prperly called deatin. But it is a serious blunder

to believe that the fall in commodity prices is caused by this striving after greatercash holding. The causation is the other way around. Prices f the factrsf prductin—bth material and human—have reached an excessiveheiht in the bm perid. They must cme dwn befre business can becme prtable aain. The entrepreneurs enlare their cash hldin because they abstain frm buyin ds and hirin wrkers as ln asthe structure f prices and waes is nt adjusted t the real state f themarket data. [Emphasis added.]

The eects f the capital irretrievably sunk in unprtable prjects

r mistakenly cnsumed as a part f current incme remain evenafter the recessin has liquidated the malinvestments, re-estab-lished mnetary calculatin n a sund ftin, and renewedentrepreneurial risk-takin. The recnstructed capital structure will

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 22/42

24 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

necessarily be shrter and, cnsequently, labr prductivity, realwaes and livin standards lwer. In sum, “The bm squandersthruh malinvestment scarce factrs f prductin and reducesthe stck available thruh vercnsumptin; its alleed blessinsare paid fr by impverishment” (Mises, 1998, p. 573).

5. OVERCONSUMPTION AND THE RETAIL SLUMP,2002–2009

After nearly ve years f increasinly rapid rwth in themnetary base and the mney supply, the Fed thrttled back in1999, trierin the burstin f the dt-cm bubble in early 2000and a recessin in early 2001. The Fed reacted almst immediatelyt these events by aressively lwerin the taret Federal Fundsrate and reversin the decline in mnetary rwth. The events f9/11 led the Fed t ratchet up its expansinary mnetary plicy.Frm the beinnin f 2001 t the end f 2005, the Fed’s MZMmnetary areate increased by abut $1 billn per week and the

M2 areate by abut $750 millin per week. Durin the sameperid the mnetary base, which is cmpletely cntrlled by theFed, increased by abut $200 billin, a cumulative increase f 33.3percent (Fiures 2, 3, 4).

Figure 2.

2 0 1 0

2 0 1 5

1 9 9 0

1 9 9 5

2 0 0 0

2 0 0 5

2,200

2,0001,800

1,600

1,400

1,200

1,000

800

600

400

200

St. Louis AdjustedMonetary Base,$ Billions

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 23/42

25 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

Figure 3.

10,000

9,000

8,000

7,000

6,000

5,000

4,0003,000

2,000

2 0 1 0

2 0 1 5

1 9 9 0

1 9 9 5

2 0 0 0

2 0 0 5

MZM Money Stock,$ Billions

M2 Money Stock,$ Billions

Figure 4.

25

20

15

10

5

0

-5

2 0 1 0

2 0 1 5

1 9 9 0

1 9 9 5

2 0 0 0

2 0 0 5

MZM Money Stock,% Change from Year Ago

M2 Money Stock,% Change from Year Ago

The Federal Funds rate was driven dwn belw 2 percent andheld there fr almst three years, peed at 1 percent fr a year(Fiure 5). The result was that the real interest rate, as measured

by the dierence between the Federal Funds rate and headlineCPI, was neative frm ruhly 2003 t 2005. Rates n 30-yearcnventinal mrtaes fell sharply frm ver 7 percent in 2002 ta lw f 5.25 percent in 2003 and, aside frm brief upticks in 2003

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 24/42

26 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

and aain in 2004, uctuated between 5.5 percent and 6.0 percentuntil late 2005 (Fiure 6). Perhaps, mre sinicantly, 1-year ARMrates plummeted frm a hih f 7.17 percent in 2000 t a lw f3.74 percent in 2003, risin t 4.1 percent in 2004 and t slihtlyver 5 percent in 2005. In additin, credit standards were lsenedand uncnventinal mrtaes, includin interest-nly, neativeequity, and n-dwn-payment mrtaes, prliferated.11 Thiscaused a rapid expansin f mrtae lendin and f subprimemrtae lendin in particular, with the subprime share f hme

mrtaes utstandin risin steadily frm 8.62 percent in 2000 t13.51 percent in 2005 (Table 1). As a result f these develpments,husin prices nce aain accelerated t duble-diit annualincreases after a shrt and shallw disinatin durin the 2001recessin. The husin bm sn turned int a bubble as expec-tatins lst cntact with fundamentals and prpelled husinprices upward at acceleratin rates.

Figure 5.7

6

5

4

3

2

1

0

-1-2

-3

2 0 0 8

2 0 1 2

2 0 1 0

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

Effective Federal Funds Rate %

Consumer Price Index for AllUrban Consumers, All Items,% Change from Year Ago

11 Fr a full explanatin f why the mnetary expansin aected the husinmarket rst and mst intensely, see Wds (2009), Taylr (2009), and Jableckiand Machaj (2009).

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 25/42

27 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

Figure 6.

9.0

8.5

8.0

7.5

7.0

6.5

6.05.5

5.0

2 0 0 8

2 0 0 9

2 0 0 0

2 0 0 2

2 0 0 3

2 0 0 1

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

30-Year ConventionalMortgage Rate %

Table 1.

Subprime Share of Home Mortgages Outstanding One-Year ARM Rate

1995 8.707087569 5.646153892

1996 8.001492858 5.5630769

1997 8.500908718 5.506923123

1998 8.485990715 5.474615392

1999 8.622616084 6.3871428

2000 8.638914155 7.172307669

2001 9.000528006 5.234615431 2002 9.516325306 4.183076977

2003 10.15566204 3.747692315

2004 12.40772314 4.108571443

2005 13.51984714 5.062307615

2006 12.5643034 5.503076915

2007 8.918634538 5.550000031

Q1 2008 7.972563691 5.133076931

Q2 2008 7.573073516 5.199230723

From Barth 2009, p. 50

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 26/42

28 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

Figure 7.25

20

15

10

5

0

-5

-10

-15-20

-25

J a n - 8 8

J a n - 8 9

J a n - 9 0

J a n - 9 1

J a n - 9 2

J a n - 9 3

J a n - 9 4

J a n - 9 5

J a n - 9 6

J a n - 9 7

J a n - 9 8

J a n - 9 9

J a n - 0 0

J a n - 0 1

J a n - 0 2

J a n - 0 3

J a n - 0 4

J a n - 0 5

J a n - 0 6

J a n - 0 7

J a n - 0 8

J a n - 0 9

J a n - 1 0

Case-Shiller 10 City Composite Index, Seasonally Adjusted,% Year over Year Change

Case-Shiller 20 City Composite Index, Seasonally Adjusted,% Year over Year Change

By mid-2003, the credit expansin bean t bst crprateprts (Fiure 8), and stck prices, stanant r declinin since

the burstin f the hih tech bubble in 2000, bean a steep ascent.While husin prices peaked in 2006, stck prices cntinued theirrise int 2007 (Fiures 9, 10).

Figure 8.

110

100

90

80

70

60

50

40

30

20

10

2 0 0 6

2 0 1 0

2 0 0 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

Corporate Profits After Tax withInventory Valuation Adjustment andCapital Consumption Adjustment,2007:Q4=100

Corporate Profits After Tax,2007:Q4=100

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 27/42

29 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

Figure 9.

1,600

1,400

1,200

1,000

800

600

400

200

J a n 2

0 0 7

J u l 2 0 1 0

J a n 1

9 9 2

J a n 1

9 9 5

J a n 1

9 9 8

J a n 2

0 0 1

J a n 2

0 0 4

S&P 500 Index

Figure 10.

14,00013,00012,00011,00010,0009,0008,0007,0006,0005,000

4,0003,0002,000

J a n 2

0 0 7

J u l 2 0 1 0

J a n 1

9 9 2

J a n 1

9 9 5

J a n 1

9 9 8

J a n 2

0 0 1

J a n 2

0 0 4

Dow Jones Industrial Average Index

The sharply risin stck and real estate prices bsted husehldnet wrth by ver $23 trillin durin the three years 2003–2006

(Bard f gvernrs f the Federal Reserve System [2010], p. 107).This drve the rati f husehld net wrth t annual gDP t wellver 450 percent. By cmparisn, fr ver frty years, frm 1952until the dt-cm bm bean in mid-1990s, the husehld net

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 28/42

30 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

wrth t annual gDP rati had held between 300 percent and 350percent. After nearly fallin back t this rane after the recessin f2001, the Fed’s mnetary expansin drve it up by 100 percentaepints in a matter f three years (Fiure 11).

Figure 11.

500

450

400

350

300

250

200

150

100

50

0

2 0 0 2

2 0 1 2

1 9 5 2

1 9 6 2

1 9 7 2

1 9 8 2

1 9 9 2

Total Household Net Worth,

% of GDP

This enrmus increase in net wrth was based almst slely npaper prts and phantm capital ains n husehlds’ real estateand nancial assets. Misled by their inatin-blated balancesheets, husehlds were induced t “cash ut” sme f theirhme equity and increase expenditures n cnsumer ds and

services. In the expressin f the day, peple bean “usin theirhmes as ATM machines.” Husehlds nanced their increasedspendin n bats, luxury auts, upscale restaurant meals, priceyvacatins etc., thruh xed-dllar debt. The increase in value fhme equity and 401(k) plans als reduced savin ut f currentincme, and the persnal savin rate pluned frm ver 4 percentimmediately after the recessin f 2001 t less than 1 percent durin2005 (Fiure 12).

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 29/42

31 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

Figure 12.

9

8

7

6

5

4

3

2

0

1

2 0 1 0

2 0 1 5

1 9 9 0

1 9 9 5

2 0 0 0

2 0 0 5

Personal Saving Rate %

Thus while husehld assets rse by $21,743.3 trillin frm 2003t 2007, liabilities, mainly hme mrtaes and cnsumer credit,

increased by $4,500.8 trillin durin the same perid (Bard fgvernrs f the Federal Reserve System [2010], p. 104). one resultf this was that the year-ver-year rate f rwth f husehlddebt nearly dubled frm 6 percent durin 1997 t 11 percent frthree cnsecutive years beinnin in mid-2003. In additin, debtservice payments as a percent f dispsable persnal incme rsefrm 11 t 12 percent durin the late 1990s t peak at 15 percent in2007. (See Fiures 13, 14)

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 30/42

32 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

Figure 13.

15

14

13

12

11

10

8

9

18

15

12

9

6

3

-3

0

2 0 0 8

2 0 0 9

2 0 1 0

1 9 8 5

1 9 9 0

1 9 9 1

1 9 8 8

1 9 8 9

1 9 8 6

1 9 8 7

1 9 9 4

1 9 9 5

1 9 9 2

1 9 9 3

2 0 0 6

2 0 0 4

2 0 0 2

2 0 0 0

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

1 9 9 8

1 9 9 9

1 9 9 6

1 9 9 7

Debt Service Payments, % of Disposable Personal Income

(Right Axis)Household Debt Outstanding, % Change from Year Ago,Quarterly Data (Left Axis)

Figure 14.

2 0 0 7

2 0 0 8

2 0 0 9

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 5

2 0 0 6

2 0 0 4

70

60

50

40

30

20

10

0

U.S. Households’ Net Worth,

$ Trillions

U.S. Households’ Financial Assets,

$ Trillions

U.S. Households’ Real Estate Value,

$ Trillions

U.S. Households’ Debt,

$ Trillions

When the bm came t an end in 2007, husin prices,crprate prts and the stck market pluned. The capital ainsaccumulated since the mid-1990s were revealed t be an illusin as

husehld net wrth declined by $13 trillin, r 20 percent, durin2008, a ure exceedin the sum f the cmbined annual gDP fgermany, Japan and the U.K. (Bard f gvernrs f the FederalReserve System [2010], p. 107). The rati f husehld net wrth t

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 31/42

33 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

gDP fell frm ver 450 percent t less than 350 percent, reachinits 1994 level in early 2009. This bruht the vercnsumptinfrenzy, which had spanned tw inatinary bms, t a screechinhalt. Real retail sales and fd services, which had plateaued at anannual rate f $180 billin durin 2006 and 2007, declined precipi-tusly t $160 billin in less than a year and remained stanant fra year. Cncurrently, rms in the retail sectr shed ver 1 millinwrkers frm their payrlls with emplyment drppin frm ahih f 15.56 millin in December 2007 t a lw f 14.36 millin in

December f 2009. on a year-ver-year basis, retail emplymentshrank by 5 percent fr mre than half f 2009. The S&P RetailStck Index (RLX) lst ver half f its value between February 2007and Nvember 2009, fallin frm 533 t 223. Indeed, the fall in theRLX was as sharp and deep as the fall f the S&P 500. (See Fiures1, 15, 16, 17, 18, 19)

Figure 15.

10.0

7.5

5.0

2.5

0.0

-2.5

-12.5-10.5

-7.5

-5.0

2 0 0 8

2 0 1 0

2 0 1 2

1 9 9 2

1 9 9 4

2 0 0 6

2 0 0 4

2 0 0 2

2 0 0 0

1 9 9 8

1 9 9 6

Real Retail and FoodServices Sales,

% Change from Year Ago

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 32/42

34 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

Figure 16.

15.5

15.0

14.5

1 / 0 8

1 / 0 9

1 / 1 0

1 / 0 0

1 / 0 1

1 / 0 7

1 / 0 6

1 / 0 5

1 / 0 4

1 / 0 3

1 / 0 2

All Employees,Millions

Figure 17.

2.5

0

-5

-2.5

1 / 0 8

1 / 0 9

1 / 1 0

1 / 0 0

1 / 0 1

1 / 0 7

1 / 0 6

1 / 0 5

1 / 0 4

1 / 0 3

1 / 0 2

12-Month % Change

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 33/42

35 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

Figure 18.

600

400

500

200

300

2 0 0 6

2 0 0 8

2 0 1 0

2 0 0 4

S&P Retail Index

Figure 19.

60

0

20

40

-40

-20

2 0 0 6

2 0 0 8

2 0 1 0

2 0 0 4

S&P Retail Index,

% Increase/Decrease

S&P 500 Index,

% Increase/Decrease

The extent f capital cnsumptin and malinvestment thatresulted frm the husin bm is revealed by develpments in theWilshire 5000 Ttal Market Index (Fiure 20). This index tracks the

ttal dllar value f all U.S.-headquartered equity securities with

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 34/42

36 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

readily available price data. It includes mre than 6,000 rms and,as such, it is a d prxy fr capital accumulatin in the U.S. 12

Figure 20.

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

2 0 1 0

2 0 1 5

1 9 9 0

1 9 9 5

2 0 0 0

2 0 0 5

Wilshire 5000

Price Index

After reachin a hih f $15.5 trillin in 2007, the index cllapsedand fell t a lw f $8 trillin in early 2009. As I write this, theWilshire 5000 has been uctuatin arund $12 trillin, a level itrst reached in 1999. This implies that there has been n net capitalaccumulatin in the U.S. ecnmy since 1999. The capital that has been accumulated since then has either been cnsumed r wastedin misdirected investments. But it may happen that even the current

level f wealth and incme is based n false calculatins, becausethe Fed has used every tl at its dispsal and has even frednew nes in rder t prp up husin and nancial asset prices.The weak and tenuus recvery that the U.S. is nw experiencinmay well be a reectin f the depth f capital cnsumptin andimpverishment that the U.S. ecnmy has suered as a result fthe inatin-taretin plicy f the past tw decades.

12 Fed ecnmists have used the Wilshire 5000 t prject chanes in husehld netwrth (Blackstne, 2009).

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 35/42

37 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

6. A NOTE ON “SECONDARY DEFLATION”The ABCT, when crrectly frmulated, des indeed explain the

asymmetry between the bm and bust phases f the businesscycle. The malinvestment and vercnsumptin that ccur durinthe inatinary bm cause a shatterin f the prductin structurethat accunts fr the pervasive unemplyment and impver-ishment that is bserved durin the recessin. Befre recverycan bein, the prductin structure must be painstakinly pieced

back tether aain in a new pattern, because the intertempralpreferences f cnsumers have chaned dramatically due t theredistributin and lsses f incme and wealth incurred durinthe inatin. This f curse takes time.

In additin, the recessin-adjustment prcess is furtherprlned by the fact that the bm has wreaked havc withmnetary calculatin, the very mrins f the market ecnmy.Entrepreneurs have discvered that their spectacular successesdurin the bm were merely a prelude t a sudden and prfund

failure f their frecasts and calculatins t be realized. Until theyhave reained cndence in their frecastin abilities and in thereliability f ecnmic calculatin they will be understandablyaverse t initiatin risky ventures even if they appear prtable.But if the market is permitted t wrk, this entrepreneurial malaisecures itself as the restrictin f demand fr factrs f prductindrives dwn waes and ther csts f prductin relative tanticipated prduct prices. The “natural interest rate,” i.e., therate f return n investment in the structure f prductin, thus

increases t the pint where entrepreneurs are enticed t renewtheir investment activities and initiate the adjustment prcess.Success feeds n itself, entrepreneurs’ spirits rise, and the recveryains mmentum.13

13 Accrdin t ABCT as described abve, the typically vlatile uctuatins fentrepreneurial cndence and expectatins ver the business cycle are ntpurely exenus psychlical phenmena that ecnmic thery must take asiven. Rather, they are a ratinal respnse t the calculatinal chas created by

an incherent mnetary reime whse arbitrary manipulatin f the interest ratesystematically falsies entrepreneurial estimates f the scarcity f capital. It isimprtant t emphasize this pint in rder t sharply distinuish ABCT frmrecent Keynes-like psychlistic theries that seek t explain bubbles, crises anddepressins by “animal spirits,” a term which refers t a witch’s brew f varius

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 36/42

38 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

The rise in the natural interest rate that vercmes the pandemicdemralizatin amn capitalists and entrepreneurs and sparksthe recvery is reected in the credit markets. Fr recvery t beinaain, there needs t be a steep rise in the “real,” r inatin-adjusted,interest rate bserved in nancial markets. Hih interest rates dnt stie the recvery but are the sure sin that the readjustmentf relative prices required t realin the prductin structure withecnmic reality is prceedin apace. The mislabeled “secndarydeatin,” whether r nt it is accmpanied by an incidental

mnetary cntractin, is thus an interal part f the adjustmentprcess. It is the prerequisite fr the renewal f entrepreneurial bldness and the restratin f cndence in mnetary calculatin.Decisins by banks and capitalist-entrepreneurs t temprarilyhld rather than lend r invest a prtin f accumulated savinsin emplyin the factrs f prductin and the crrespndin risef the lan and natural rates abve sme estimated “true” timepreference rate des nt impede but speeds up the recvery. Thisimplies, f curse, that any plitical attempt t arrest r reverse the

decline in factr and asset prices thruh mnetary manipulatinsr scal stimulus prrams will retard r derail the recessin-adjustment prcess.

nnecnmic mtives and irratinal behaviral prpensities f private ecnmicdecisins (see, fr example, Akerlf and Shiller [2009]).

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 37/42

39 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

Figure 21.

The USD Credit Triangle June 2010

OTC Derivatives$615tn (Nominal)

Int'l Positions of Banks (USD Deposits Outside U.S.)$32.2tn ($12.2tn)

Shadow Banks$13tn

Banks (M2)$8.6tn

Fed$1.9tn

The USD Credit TriangleAugust 2008

OTC Derivatives$684tn (Nominal)

Int'l Positions of Banks (USD Deposits Outside U.S.)$37.4tn ($13.2tn)

Shadow Banks$16tn

Banks (M2)$7.8tn

Fed$843b

Fiure 21 reveals the extent t which the Fed’s plicy respnsehas failed t revive the ecnmy and has prlned the “secndarydeatin.” Frm Auust 2008 t June 2010 the Fed mre thandubled its balance sheet and M2 increased by mre than 10

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 38/42

40 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

percent. And yet, durin the same perid, there was substantialshrinkae f the upper tiers f the U.S. credit trianle, cmprisincredit extended by nnbank nancial institutins and nancialmarkets.14 Fiure 22 shws an updated versin f the trianle asf octber 2011.15 Nte that tw f the three upper layers f thetrianle, which are verned primarily by the expectatins anddecisins f capitalists and entrepreneurs, have cntinued t shrinkdespite the fact that the Fed has cntinued t increase its balancesheet and M2, by 78.9 percent and 11.6 percent respectively. This

cntinuin fall in the credit prtin f the trianle es hand inhand with the weak and tenuus recvery that the U.S. ecnmyis currently underin. Bth are caused by the failure f the pricesf assets, ds and labr services t adjust t ecnmic realityand the cncmitant lack f cndence in investment prspects by capitalist-entrepreneurs peratin under the extreme relative-price distrtin and reime uncertainty impsed by U.S. mnetary,scal and reulatry plicies.

14 The U.S. credit trianle was frmulated and calculated by Steve Hanke (2010).

15 This updated representatin f the USD credit trianle was cnstructed fr theauthr by Matt McCarey. The authr is indebted t Steve Hanke fr kindlyprvidin data surces and a descriptin f the methds used t cnstruct theriinal trianles in Fiure 21.

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 39/42

41 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

Figure 22.

The USD Credit TriangleOctober 2011

OTC Derivatives$601.1tn (Notional), $21.2tn (Gross)

Int'l Positions of Banks (USD Deposits Outside U.S.)$34.2tn ($13.3tn)

Shadow Banks$11.1tn

Banks (M2)$9.6tn

Fed$3.4tn

7. CONCLUSION

once we understand the ABCT as a thery f the destructin andrenewal f bth the capital structure and mnetary calculatin, weare in a psitin t fully accunt fr the events f the past decade.Furthermre, iven the unprecedented mnetary interventins by the Fed and the enrmus decits run by the obama admin-istratin, ABCT als explains the precarius nature f the currentrecvery and the rwin prbability that the U.S ecnmy isheaded fr a 1970s-style staatin.

REFERENCES

Akerlf, gere A. and Shiller, Rbert J. 2009. Animal Spirits: How HumanPsychology Drives the Economy and Why It Matters for Global Capitalism.Princetn: Princetn University Press.

Baertlein, Lisa. 2009. “Factbx: Recent Retail Bankruptcies” (January 14).Reuters. Available at http://www.reuters.cm/article/reutersEde/idUSTRE50D6JI20090115.

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 40/42

42 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

Barbar, Michael. 2008. “Retailin Chains Cauht in a Wave f Bank -

ruptcies,” New York Times (April 15). Available at http://www.nytimes.cm/2008/04/15/business/15retail.html?_r=1.

Barth, James. 2009. The Rise and Fall of the U.S. Mortgage and Credit Markets.Hbken, N.J.: Jhn Wiley & Sns, Inc.

Blackstne, Brian. 2009. “Husehld Wealth Pluned In ‘08, ReversinRise.” WSJ Blogs: Real Time Economics (February 12). Available athttp://bls.wsj.cm/ecnmics/2009/02/12/husehld-wealth-

pluned-in-08-reversin-rise/.

Bard f gvernrs f the Federal Reserve System. 2010. Federal ReserveStatistical Release Z.1, Flow of Funds Accounts of the United States: Flowsand Outstandings First Quarter 2010 (June 10).

Caplan, Bryan. 2008. “What’s Wrn with Austrian Business CycleThery?” Econlog (January 2). Available at http://ecnl.ecnlib.r/archives/2008/01/whats_wrn_wit_6.html.

Cwen, Tyler. 2008. “Paul Kruman n Austrian Trade Cycle Thery.”Marinal Revlutin (octber 14). Available at http://www.marinal-revlutin.cm/marinalrevlutin/2008/10/paul-kruman-n.html.

Daily Mail Reprter. 2010. “British Slar-Pwered Unmanned DrneFinally Lands After Flyin Nn-Stp fr Tw Weeks.” Mail Online (July 23). Available at http://www.dailymail.c.uk/sciencetech/article-1297165/Zephyr-British-slar-pwered-unmanned-aircraft-nally-lands-yin-nn-stp-weeks.html#.

DeLn, Bradfrd. 2008. “I Accept Larry White’s Crrectin....” CatoUnbound (December 11). Available at http://www.cat-unbund.r/2008/12/11/j-bradfrd-deln/i-accept-larry-whites-crrectin/.

Ebelin, Richard. 2000. “gttfried Haberler: A Centenary Appreciatin.”The Freeman: Ideas on Liberty 50, n 7. Available at http://www.thefree-mannline.r/clumns/ttfried-haberler-a-centenary-appreciatin/.

Farfan, Barbara. 2009. “Retail Industry Chapter 11: Cmplete Listin f RetailBankruptcy Filins: Bankruptcy Prtectin, and Chapter 7 LiquidatinList fr 2008 and 2009,” About.com (July 7). Available at http://retailin-dustry.abut.cm/d/tpusretailcmpanies/a/chapter11retail.htm.

Federal Reserve Bank f St. Luis. 2010a. National Economic Trends.Available at http://research.stluisfed.r/publicatins/net/.

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 41/42

43 Joseph T. Salerno: A Reformulation of Austrian Business Cycle Theory…

——. 2010b. Federal Reserve Bank f St. Luis. Economic Data--FRED®.Available at http://research.stluisfed.r/fred2/.

garrisn, Rer W. 2001. Time and Money: The Macroeconomics of the CapitalStructure. New Yrk: Rutlede.

——. 2004. “overcnsumptin and Frced Savin.” History of PoliticalEconomy 36, n. 2: 323–349.

gaudin, Sharn. 2010. “Slar Plane Cmpletes First Niht Fliht.”Techworld (July 9). Available at http://news.techwrld.cm/reen-

it/3229998/slar-plane-cmpletes-rst-niht-iht/.

Haberler, gttfried. 1933. “Der Stand und die nächste Zukunft derKnjunkturfrschun.” J. A. Schumpeter, ed., Festschrift für ArthurSpiethof . München: Duncker & Humblt.

——. 1963. Prosperity and Depression: A Theoretical Analysis of Cyclical Movements , 4th ed. New Yrk: Atheneum.

——. 1974. Economic Growth and Stability: An Analysis of Economic Change

and Policies. Ls Aneles: Nash Publishin.——. 1996. “Mney and the Business Cycle.” In Ludwi vn Mises et

al., The Austrian Theory of the Trade Cycle. Auburn, Ala.: Ludwi vnMises Institute.

Hanke, Steve H. 2010. “Mney Dminates.” Globe Asia (Auust 20).Available at http://www.cat.r/pub_display.php?pub_id=12001.

Hayek, Friedrich A. 1984. “Capital Cnsumptin.” In Ry McCluhry,ed., Money, Capital and Fluctuations: Early Essays. Chica: University

f Chica Press, pp. 136–158.

——. 2008. Prices and Production and Other Works: F.A. Hayek on Money, theBusiness Cycle, and the Gold Standard. Ed. Jseph T. Salern. Auburn,Ala.: Ludwi vn Mises Institute.

Jablecki, Juliusz and Mateusz Machaj. 2009. “The Reulated Meltdwn f2008.” Critical Review 21, ns. 2–3: 301–328.

Khanduja, Jaideep. 2010. “Twenty Six Hurs Fliht by Slar Pwered

Aircraft Marks New Heihts.” Technorati (July 9). Available at http://technrati.cm/technly/article/twenty-six-hurs-iht-by-slar/.

Kruman, Paul. 1998. “The Hanover Theory: Are Recessions Payback for goodTimes?” Slate (December 4). Available at http://www.slate.com/id/9593/.

7/21/2019 Joe Salerno ABCT

http://slidepdf.com/reader/full/joe-salerno-abct 42/42

44 The Quarterly Jurnal f Austrian Ecnmics 15, N. 1 (2012)

——. 2010. “Martin and the Austrians.” New York Times (April 7).Available at http://kruman.bls.nytimes.cm/2010/04/07/martin-and-the-austrians/.

Mises, Ludwi vn. 1998. Human Action: A Treatise on Economics. Auburn,Ala.: Ludwi vn Mises Institute.

Quiin, Jhn. 2009. “Austrian Business Cycle Thery.” Cmmentary nAustralian & Wrld Events frm a Scial Demcratic Perspective(May 3). Available at http://jhnquiin.cm/index.php/archives/2009/05/03/austrian-business-cycle-thery/

Rthbard, Murray N. 2000. America’s Great Depression. 5th ed. Auburn, Ala.:Ludwi vn Mises Institute.

——. 2004. Man, Economy, and State with Power and Market. Schlar’s Ed.Auburn, Ala.: Ludwi vn Mises Institute.

——. 2009. Man, Economy, and State: A Treatise on Economic Principles withPower and Market: Government and the Economy, Scholar’s Edition. 2nd

ed. Auburn, Ala.: Ludwi vn Mises Institute.

Salern, Jseph T. 2005. “Biraphy f gttfried Haberler (1901–1995).”Available at http://mises.r/abut/3232.

Taylr, Jhn B. 2009. Getting Of Track: How Government Actions and Inter-ventions Caused, Prolonged, and Worsened the Financial Crisis. Stanfrd,Calif.: Hver Institutin Press.

Thrntn, Mark. 2009. “The Ecnmics f Husin Bubbles.” In Randallg. Hlcmbe and Benjamin Pwell, eds., Housing America: BuildingOut of a Crisis. New Brunswick, N.J.: Transactin, pp. 237–262.

U.S. Census Bureau. 2010. “Nrth American Industry Classicatin System.”Available at http://www.census.v/es/www/naics/.

Wds, Thmas E. 2009. Meltdown: A Free Market Look at Why the Stock Market Collapsed, the Economy Tanked, and Government Bailouts Will Make Things Worse. Washintn, D.C.: Renery.

Zarrell, Christina. 2009. “18 Retail Bankruptcies in 2009.” RIS (June 23).Available at http://www.risnews.cm/ME2/dirmd.asp?sid=&nm=&type=MultiPublishin&md=PublishinTitles&mid=2E3DABA5

396D4649BABC55BEADF2F8FD&tier=4&id=7B77173FABD54A1EA9E24C7B75708570.