Embed Size (px)

Citation preview

ROLE OF BANKS IN THE PROGRESS OF SELF HELP GROUPS IN INDIA

A COMPARITIVE STUDY ON AGENCIES

V. Sridevi** Dr. Yoginder Singh *

---------------------------------------------------------------------------------------------------------------------

Abstract: Banks play an important role in the financial inclusion of Self Help Groups in India.

Commercial Banks, Regional Rural Banks, Co-Operative Banks play the major part in the

progress of SHGs. Banks maintain the savings accounts of SHGs, they extend loans to needs

groups and encourage the SHGs to take up their livelihood activities. This study makes a

comparison between the banks that mobilize savings, extend loans, loan outstanding of SHGs

and also studies the Non Performing Assets of banks. Both agency wise comparison and region

wise comparison of NPA is performed in this paper. NPA is formed when the financial

institutions are burdened with higher losses due to nonpayment of principal and interest amount

of loan availed by the members in SHGs. This indeed is considered as a bad debt to the banks.

Keywords: Savings mobilization, Loan Disbursed, Loan outstanding, Non Performing Assets,

Regional Rural Banks (RRBs), Co-Operative Banks, Commercial Banks.

INTRODUCTION

A banking revolution occurred in the country during the post-nationalization era. The

commercial banks, especially public sector banks, have drastically changed from their traditional

money dealing business to innovative banking and subserved their operations to the needs of

nation-building activities and socio-economic upliftment of the Indian masses. It is rightly said

that Indian banking has changed from class-banking to mass-banking or social banking. The

private sector commercial banks were urban-oriented in their growth. Rural areas were starved of

banking facilities. To improve this situation, public sector commercial banks undertook a

programme of massive expansion of bank branches in the rural, under-banked and unbanked

areas, which aimed at ensuring balanced regional development of the banking sector in the

country.

---------------------------------------------------------------------------------------------------------------------

**Research Scholar, JNTU Kakinada, Andhra Pradesh. [email protected], Mob. No. 9492634875.

*Assistant Professor of Commerce, PG Department of Commerce, Dr.S.R.K.Govt. College, Yanam,

Pondicherry (U.T.) - Pin-533464, Mob. No. 9030093092.

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1350

A banking company in India defined by Banking Companies Act, 1949 as one “which transacts

the business of banking which means the accepting, for the purpose of lending or investment, of

deposits of money from the public, repayable on demand or otherwise and withdrawable by

cheque, draft, order or otherwise”. Financial requirements in a modern economy are of a diverse

nature, distinctive variety and large magnitude. Hence, different types of banks have been

instituted to cater to the varying needs of the community namely; Commercial banks, Co-

operative banks, Specialized banks and Central banks. A Commercial bank is a type of financial

institution that accepts deposits, offers checking account services, makes various loans and offers

basic financial products like (CDs) certificate of deposits and savings accounts to individuals and

small businesses. The amount of money earned by a commercial bank is determined by the

spread between the interest it pays on deposits and the interest it earns on the loans it issues

which is known as net interest income. The two main functions of commercial banks are:

(i) Primary functions deals with a) accepting deposits namely current account deposits,

fixed deposits(Time deposits), savings account deposits b) provides loans and advances

like cash credit, demand loans, short term loans.

(ii) Secondary functions deals with a) discounting Bills of Exchange or bundles of customers

b) provide overdraft facility to customers c) agency functions like transfer of funds,

collection of funds, letter of references, purchase and sale of shares and securities of the

customers d) performing general utility services like locker facility, travelers cheque,

underwriting securities issued by the Government, public or private bodies, purchase and

sale of foreign exchange currency.

Based on the due recommendations and suggestions by the Narasimham Committee’s Report,

the Government of India instituted Regional Rural Banks (RRBs) on October 1975. Regional

Rural Banks Act, 1976 was established with a view to develop the rural economy by providing

loan facility for the purpose of development of agriculture, trade, commerce, industry and other

productive activities in the rural areas, particularly to small and marginal farmers, agricultural

labourers, artisans and small entrepreneurs. The area of operation of RRBs is limited to the area

as notified by Government of India covering one or more districts in the State. RRBs also

perform a variety of different functions like providing banking facilities to rural and semi-urban

areas, carrying out government operations like disbursement of wages of MGNREGA (Mahatma

Gandhi National Rural Employment Guarantee Act) workers, distribution of pensions etc,

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1351

providing Para-Banking facilities like locker facilities, debit and credit cards, mobile banking,

internet banking, UPI etc, Small financial banks. The Central Government holds 50% of the

stake, 35% by the concerned State Government and the rest 15% stake of RRBs are under the

control of sponsoring bank. The working and affairs are directed and managed by Board of

Directors. The BODs consists of a Chairman, three directors to be nominated by the Central

Government concerned, not more than two directors to be nominated by the State Government

and not more than 3 directors to be nominated by the sponsoring bank. The chairman is

appointed by the Central Government and his term of office does not exceed five years. The

National Bank for Agriculture and Rural Development (NABARD) periodically reviews their

financial performance through empowered committee (EC) meetings at the state level.

RRBs have stiff competition from small finance banks and non-banking finance companies.

They need to offer differentiated products to play a greater role in financial inclusion and

meeting credit requirements in rural areas. RRBs operate with a view to enable them to minimise

their overhead expenses, optimise the use of technology, enhance the capital base and area of

operation and increase exposure.

The co-operatives play a vital role in the Indian financial system, especially at the rural level. A

credit co-operative is a voluntary association of members for self help, catering to the financial

needs on a mutual basis. Co-operatives may provide loans to their members at lower rates of

interest and save them from the clutches of shylock-type money-lenders. In India, the co-

operative credit system was ushered in with the passing of the first Co-operative Societies Act of

1904 by the Government of India. In the organized sector of the Indian money market, co-

operative banks and commercial banks are parallel financial institutions. Both render almost

identical banking functions of deposit mobilization, provision of remittance facilities and

advancing loans. The Cooperative Societies Act, 1912 recognized the need for establishing new

organizations for supervision, auditing and supply of cooperative credit. These organizations

were-: a) A union, consisting of primary societies, b) the central banks and c) provincial banks.

Although beginning has been made in the direction of establishing cooperative societies and

extending cooperative credit, but the progress remained unsatisfactory in the pre-independence

period. Even after being in operation for half a century, the cooperative credit formed only 3.1

per cent of the total rural credit in 1951-52.

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1352

The co-operatives banking system in India is federal in structure. It has a pyramid type of three-

tire structure constituted by: 1) Primary Credit Societies (PCSs), 2) Central Co-operative banks

(CCBs), 3) State Co-operative banks (SCBs). These co-operatives provide short-term and

medium-term credit. There are agricultural and non-agricultural credit societies. There are

primary agricultural credit societies functioning in villages. There are urban banks and other non-

agricultural credit societies functioning in towns and cities. In addition, there are farmers’ service

and grain banks. For providing long-term agricultural credit there are primary and central land

development banks.

REVIEW OF LITERATURE

Rajinder Kumar, Harpreet Singh (2018), explains the concept of self help group evolved along

the rural and semi urban people to improve their living conditions. In India, this scheme is

implemented with the help of NABARD as a main nodal agency in rural development. The

banks, Commercial Banks, Regional Rural Banks and Co-operative banks playing an important

role in Saving mobilization and financing to various activities of SHGs. This paper has made an

attempt to study the agency wise analysis of savings of SHGs and loan outstanding of SHGs and

loan disbursement to SHGs in India. The study revealed that commercial banks play an

important role in financing to SHGs in India. The growth rate of commercial banks is also higher

than that of regional rural bank and cooperative banks, as regards number of saving account,

saving amount, number of loan account and amount of loan disbursement. Bandlamudi Kalpana,

Taidala Vasantaha Rao (2017), examines the general role of commercial banks which is to

povide financial services to general public and business, ensuring economic and social stability

and sustainable growth of the economy. Commercial Bank in India comprises the State Bank of

India (SBI) and its subsidiaries, nationalized banks, foreign banks and other scheduled

commercial banks, regional rural banks and non-scheduled commercial banks. The main

objective of the study is to critically examine and analyze the role of commercial banks on

economic growth in India. The study portrays how loans and credit affect the GDP and

consequently the level of economic growth of India. Chetan Dudhe (2017), explains the central

objective of the study is to empirically investigate the role of Indian banks in capital formation

and economic growth. Research is based upon the secondary data which provide the findings on

commercial banks and how it is helpful in economic development. The data analysis of the 47

commercial banks of India revealed increased budget of loans provided every year. It is therefore

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1353

recommended that efforts should be taken by the monetary authorities to effectively manage the

banks maximum lending of banks. This policy thrust will most likely result into increased

investment activities which will enhance the capital formation in India needed for its real sector

investments and industrial growth. Mohammed Abusharbeh (2017) tests whether banking

industry development supports Palestinian economic growth or not. Thus, this study examines

the impact of some banking sector indicators (credit facilities, depositors fund, the number of

branches, and interest rate) on gross domestic product using quarterly data from the period of

2000 to 2015. The result reveals that banking credits are positively related to economic growth.

This indicates that banking industry development tends to improve productive capacity of

Palestinian economy as case of supply leading. However, interest rate, customers deposits and

number of branches have not significant impact on economic growth. Finally, the result of this

paper provides some important lesson to the Palestinian authority policymakers: there is strong

real benefit from Banking credits policy due to the significant effect on Palestinian economy.

Sayanee Nayak Aluni, Saptarshi Ray (2015), focuses on formulation of strategies for managing

credit risk of SHG as an effort to make the SHG-Bank linkage programme sustainable. The

government, through institutions like National Bank for Agriculture and Rural Development, has

been trying to promote Self Help Groups (SHGs) by financing their projects to alleviate poverty

and unemployment in villages and to include rural India under a structured financial system.

However, the financial institutions are burdened with huge losses due to non-repayment of loans

availed by the SHGs which leads to accumulation of Non-performing Assets. This situation

adversely affects the birth of new SHGs and the existing groups are forced to embrace local

moneylenders at an exorbitant rate of interest. Hence, the government’s effort to financially

reach out to the poor through SHGs seems to be a rather difficult task. Tiken Das (2013),

analysed the NPAs and recovery performance of SHGs in Southern Region and North Eastern

Region taking four years data. The SHGs-BLP was concentrated among Southern Region and its

performance was not satisfactory among the North Eastern states. Although amount of saving

balance of SHGs with banks and amount of loan disbursed to SHGs by banks was lower in North

Eastern Region when compared with Southern Region, but the share of NPAs to total loans

outstanding was higher and percentage of recovery to demand of total SHGs was lower in North

Eastern Region.

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1354

OBJECTIVES OF THE STUDY

The following are the main objective of the study:

To study the progress of savings, loan disbursed and loans outstanding of Self Help

Groups with commercial banks.

To study the progress of savings, loan disbursed and loans outstanding of Self Help

Groups with regional rural banks.

To study the progress of savings, loan disbursed and loans outstanding of Self Help

Groups with cooperative banks.

METHODOLOGY OF THE STUDY

This study is based upon secondary data which was collected from the published sources, news

papers, magazines, journals, articles, available literatures, various reports of NABARD and

websites.

FINDINGS AND INTERPRETATIONS

SHGs are a small voluntary association of 10-20 women who join hands together to form a group

for poverty alleviation which simultaneously works on empowerment and improvement of the

lives of its members. SHG’s originated in the year 1975 at Bangladesh by Mohammed Yunus.

The government of India thoroughly viewed in the early eighties to promote apex bank to take

care of the financial needs of the poor, informal sector and rural areas. During this period,

NABARD was initiated in 1986-87, to fulfill the financial requirement of the rural poor and

informal sector, but the real effort was taken after 1991-92 from the linkage of SHGS with the

banks. The SHG - Bank Linkage Programme (BLP) helped extensively to empower the poor,

especially rural women, through providing savings and extending credits from banks. As on 31st

March 2019, the SHG-BLP has crossed the milestone of 1 crore SHGs covering more than 12

crore families with savings deposits of 23,324 crore and more than 50 lakh groups with loan

outstanding of over 87,098 crore, of which 88% was disbursed to rural women groups.

Agency-wise status of savings of SHGs:

Self Help Groups in India are accessed to savings, loan disbursement, loans outstanding with

banks. The members of SHGs voluntarily contribute a certain sum as savings regularly to

common fund of the group, in order to meet the credit requirement of the needy members in the

group. From Table 1, the progress on SHGs with savings accounts and amount of savings with

banks for period 2014-15 to 2018-19 can be inferred agency-wise. The figures in parentheses

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1355

indicate increase/decrease over previous year information. The mean value and compound

annual growth rate is calculated for the five years data. Mean value happens to be the average

value for five years and compound annual growth rate is the rate of return that would be required

for an investment to grow from its beginning balance to its ending balance, assuming the profits

were reinvested at the end of each year of the investments lifespan.

Table-1 Saving Account of SHGs with Banks - Agency wise

Number of SHGs having savings account

Agencies 2014-15 2015-16 2016-17 2017-18 2018-19 Mean CAGR

Commercial banks 4135821

(2.81)

4140111

(0.10)

4444428

(7.35)

4633712

(4.26)

5476914

(18.20)

4566197 5.78

Regional rural banks 2161315

(2.35)

2256811

(4.42)

2586318

(14.60)

2807744

(8.56)

3078473

(9.64)

2578132 7.33

Co-operative banks 1400333

(8.14)

1506080

(7.55)

1546129

(2.66)

1302981

(-15.75)

1458856

(11.96)

1442875 0.82

Total 7697469

(3.61)

7903002

(3.67)

8576875

(8.53)

8744437

(1.95)

10014243

(14.52)

8587205 5.40

Amount of savings with banks( in crore)

Commercial banks 6630.67

(-0.01)

9033.89

(36.24)

10170.02

(12.58)

11664.22

(14.69)

13240.23

(13.51)

10147.81 14.83

Regional rural banks 2346.57

(19.73)

2484.28

(5.87)

3631.76

(46.19)

5807.35

(59.9.)

7692.01

(32.45)

4372.39 26.80

Co-operative banks 2082.59

(59.45)

2173.22

(4.35)

2314.44

(6.50)

2120.54

(-8.38)

2392.24

(12.81)

2216.61 2.81

Total 11059.83

(11.74)

13691.39

(23.79)

16114.23

(17.70)

19592.12

(21.58)

23324.48

(19.05)

16756.41 16.09

Source: Annual reports of status of Microfinance in India 2014-15, 2015-16, 2016-17, 2017-18, 2018-2019

(Figures in parentheses indicate increase/decrease over the previous year)

The number of SHGs having savings account with banks in all categories of agencies showed an

constant increase in numbers except in 2017-18 of cooperative banks recorded a negative trend

of -15.75% with reference to previous year. Out of all the agencies, commercial banks had a

mean value of 45.66 lakhs SHGs savings account which is approximately 53% of the total SHGs

followed by regional rural banks of 25.75 lakhs and cooperative banks with 14.42 lakhs. The

number of saving accounts of SHGs increased from 76.97 lakh in 2014-15 to 100.14 lakh in

2018-19 and registered a compound annual growth rate of 5.40%. The growth rate of the number

of saving accounts of SHGs was highest in regional rural banks (7.33%), followed by

commercial banks (5.78%) and by co-operative bank (0.82%) during the period of the study. The

amount of savings of SHGs increased from 11059.83 crore in 2014-15 to 23324.48 crore in

2018-19 and registered the growth rate 16.09%. The savings amount of SHGs were highest in

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1356

commercial bank with mean value of 10147.81 crore followed by regional rural banks with

4372.39 crore and by co-operative banks with 2216.61 crore during the five years period. The

growth rate of amount of savings of SHGs was highest in regional rural bank by 26.80%

followed by commercial banks 14.83% and by co-operative bank with 2.81% during the same

period.

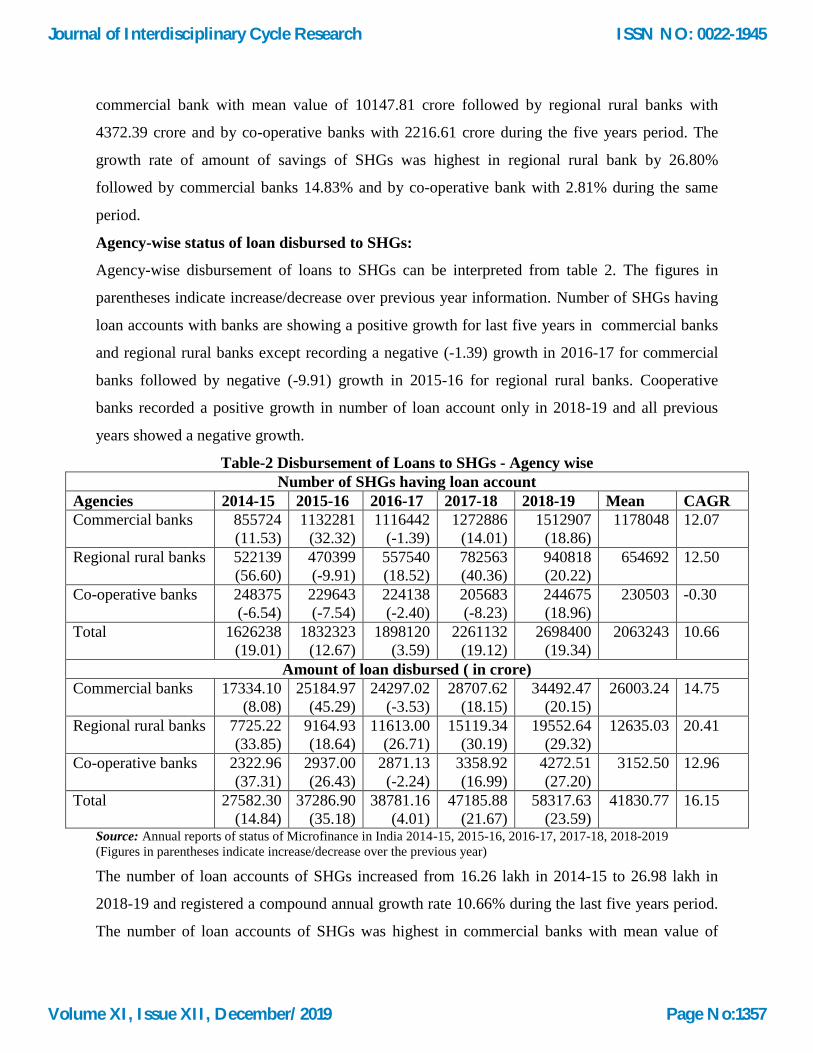

Agency-wise status of loan disbursed to SHGs:

Agency-wise disbursement of loans to SHGs can be interpreted from table 2. The figures in

parentheses indicate increase/decrease over previous year information. Number of SHGs having

loan accounts with banks are showing a positive growth for last five years in commercial banks

and regional rural banks except recording a negative (-1.39) growth in 2016-17 for commercial

banks followed by negative (-9.91) growth in 2015-16 for regional rural banks. Cooperative

banks recorded a positive growth in number of loan account only in 2018-19 and all previous

years showed a negative growth.

Table-2 Disbursement of Loans to SHGs - Agency wise

Number of SHGs having loan account

Agencies 2014-15 2015-16 2016-17 2017-18 2018-19 Mean CAGR

Commercial banks 855724

(11.53)

1132281

(32.32)

1116442

(-1.39)

1272886

(14.01)

1512907

(18.86)

1178048 12.07

Regional rural banks 522139

(56.60)

470399

(-9.91)

557540

(18.52)

782563

(40.36)

940818

(20.22)

654692 12.50

Co-operative banks 248375

(-6.54)

229643

(-7.54)

224138

(-2.40)

205683

(-8.23)

244675

(18.96)

230503 -0.30

Total 1626238

(19.01)

1832323

(12.67)

1898120

(3.59)

2261132

(19.12)

2698400

(19.34)

2063243 10.66

Amount of loan disbursed ( in crore)

Commercial banks 17334.10

(8.08)

25184.97

(45.29)

24297.02

(-3.53)

28707.62

(18.15)

34492.47

(20.15)

26003.24 14.75

Regional rural banks 7725.22

(33.85)

9164.93

(18.64)

11613.00

(26.71)

15119.34

(30.19)

19552.64

(29.32)

12635.03 20.41

Co-operative banks 2322.96

(37.31)

2937.00

(26.43)

2871.13

(-2.24)

3358.92

(16.99)

4272.51

(27.20)

3152.50 12.96

Total 27582.30

(14.84)

37286.90

(35.18)

38781.16

(4.01)

47185.88

(21.67)

58317.63

(23.59)

41830.77 16.15

Source: Annual reports of status of Microfinance in India 2014-15, 2015-16, 2016-17, 2017-18, 2018-2019

(Figures in parentheses indicate increase/decrease over the previous year)

The number of loan accounts of SHGs increased from 16.26 lakh in 2014-15 to 26.98 lakh in

2018-19 and registered a compound annual growth rate 10.66% during the last five years period.

The number of loan accounts of SHGs was highest in commercial banks with mean value of

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1357

11.78 lakh, followed by regional rural banks with 6.55 lakh and by co-operative banks with 2.31

lakh during the period 2014-15 to 2018-19. The compound annual growth rate of the number of

loan accounts of SHGs was highest in regional rural bank with 12.50%, followed by commercial

banks with 12.07% and by cooperative banks -0.3% during the period of the study. The amount

of loan disbursed to SHGs increased from 27582.30 crore in 2014-15 to 58317.63 crore in 2018-

19 and registered compound annual growth rate 16.15%. The amount of loan disbursed to SHGs

were highest in commercial bank with mean26003.24 crore, followed by regional rural banks

12635.03crore and by co-operative banks with 3152.50 crore during the study period. The

compound annual growth rate of amount of loan disbursed to SHGs was highest in regional rural

bank with 20.41%, followed by commercial bank 14.75% and by co-operative bank 12.96%

during the same period.

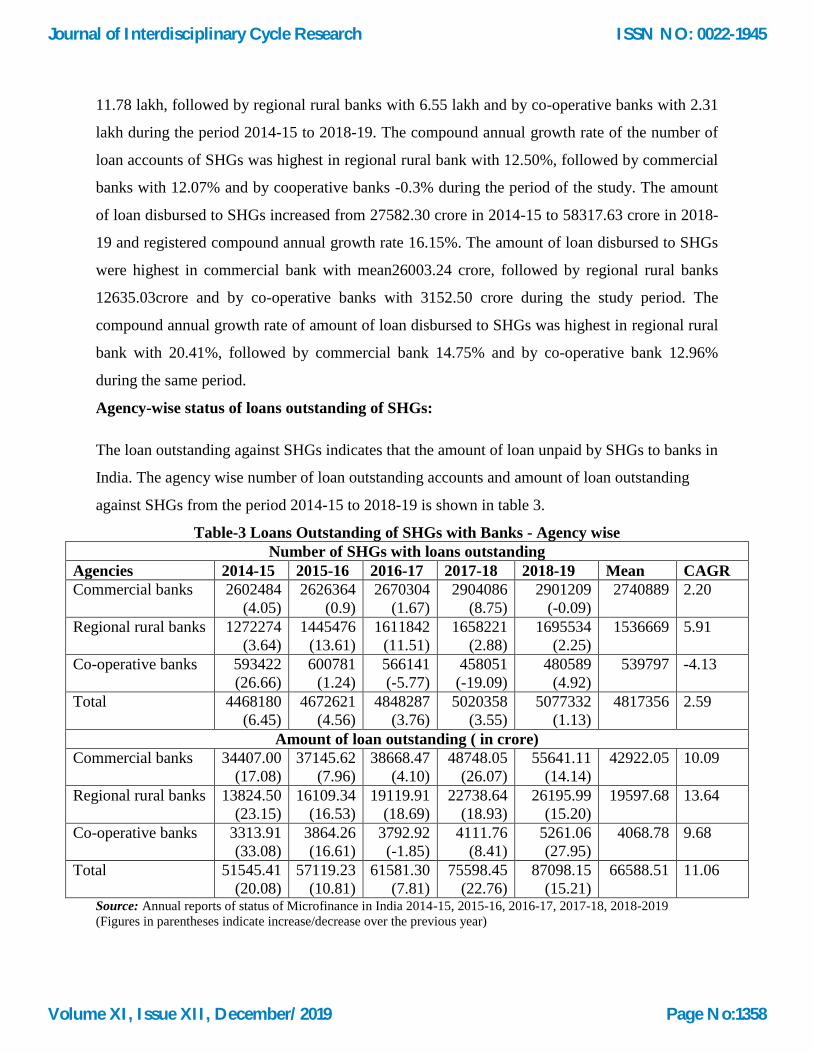

Agency-wise status of loans outstanding of SHGs:

The loan outstanding against SHGs indicates that the amount of loan unpaid by SHGs to banks in

India. The agency wise number of loan outstanding accounts and amount of loan outstanding

against SHGs from the period 2014-15 to 2018-19 is shown in table 3.

Table-3 Loans Outstanding of SHGs with Banks - Agency wise

Number of SHGs with loans outstanding

Agencies 2014-15 2015-16 2016-17 2017-18 2018-19 Mean CAGR

Commercial banks 2602484

(4.05)

2626364

(0.9)

2670304

(1.67)

2904086

(8.75)

2901209

(-0.09)

2740889 2.20

Regional rural banks 1272274

(3.64)

1445476

(13.61)

1611842

(11.51)

1658221

(2.88)

1695534

(2.25)

1536669 5.91

Co-operative banks 593422

(26.66)

600781

(1.24)

566141

(-5.77)

458051

(-19.09)

480589

(4.92)

539797 -4.13

Total 4468180

(6.45)

4672621

(4.56)

4848287

(3.76)

5020358

(3.55)

5077332

(1.13)

4817356 2.59

Amount of loan outstanding ( in crore)

Commercial banks 34407.00

(17.08)

37145.62

(7.96)

38668.47

(4.10)

48748.05

(26.07)

55641.11

(14.14)

42922.05 10.09

Regional rural banks 13824.50

(23.15)

16109.34

(16.53)

19119.91

(18.69)

22738.64

(18.93)

26195.99

(15.20)

19597.68 13.64

Co-operative banks 3313.91

(33.08)

3864.26

(16.61)

3792.92

(-1.85)

4111.76

(8.41)

5261.06

(27.95)

4068.78 9.68

Total 51545.41

(20.08)

57119.23

(10.81)

61581.30

(7.81)

75598.45

(22.76)

87098.15

(15.21)

66588.51 11.06

Source: Annual reports of status of Microfinance in India 2014-15, 2015-16, 2016-17, 2017-18, 2018-2019

(Figures in parentheses indicate increase/decrease over the previous year)

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1358

The number of loans outstanding accounts of SHGs increased from 44.68 lakh in 2014-15 to

50.77 lakh in 2018-19 and registered a compound annual growth rate 2.59% during the last five

years period. The number of loans outstanding accounts of SHGs was highest in commercial

banks with mean value of 27.41 lakh, followed by regional rural banks with 15.37 lakh and by

co-operative banks with 5.40 lakh during the period 2014-15 to 2018-19. The compound annual

growth rate of the number of loans outstanding accounts of SHGs was highest in regional rural

bank with 5.91% followed by commercial banks with 2.20% and by cooperative banks -4.13%

during the period of the study. The amount of loan outstanding to SHGs increased from

51545.41crore in 2014-15 to 87098.15 crore in 2018-19 and registered compound annual growth

rate 11.06%. The amount of loan outstanding with SHGs were highest in commercial bank with

mean 42922.05 crore, followed by regional rural banks 19597.68 crore and by co-operative

banks with 4068.78 crore during the study period. The compound annual growth rate of amount

of loan outstanding to SHGs was highest in regional rural bank with 13.64%, followed by

commercial bank 10.09% and by co-operative bank 9.68% during the same period.

Non-Performing Assets against Loan Outstanding of SHGs:

From Table 4, the non performing assets against loans outstanding of SHGs from 2014-15 to

2018-19 can be interpreted agency-wise.

Table-4 NPAs against Loans Outstanding of SHGs (Amount in crores)

Particulars 2014-15 2015-16 2016-17 2017-18 2018-19

Commercial Banks

Loan Outstanding Amount 34407.00 37145.62 38668.47 48748.05 55641.11

Amount of NPAs 2466.98 2321.40 2641.12 3101.19 2897.39

NPA as % to Loan O/S 7.17 6.25 6.83 6.36 5.20

Regional Rural Banks

Loan Outstanding Amount 13824.50 16109.34 19119.91 22738.64 26195.98

Amount of NPAs 1065.87 1064.29 1045.00 1216.03 1274.82

NPA as % to Loan O/S 7.71 6.61 5.47 5.35 4.87

Co-Operative Banks

Loan Outstanding Amount 3313.91 3864.26 3792.92 4111.75 5261.05

Amount of NPAs 282.34 300.54 316.07 310.82 351.78

NPA as % to Loan O/S 8.52 7.78 8.33 7.56 6.69

TOTAL

Loan Outstanding Amount 51545.41 57119.22 61581.30 75598.45 87098.15

Amount of NPAs 3815.19 3686.23 4002.19 4628.05 4524.01

NPA as % to Loan O/S 7.40 6.45 6.49 6.12 5.19

Source: Annual reports of status of Microfinance in India 2014-15, 2015-16, 2016-17, 2017-18, 2018-2019

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1359

As on 31st March 2019, 50.77 lakh SHGs (50.7% of total SHGs) were having credit outstanding

of 87,098 crore as against 50.20 lakh SHGs (57.4 percent) credit outstanding of 75,598 crore

during 2017-18, recording a marginal 1.12% increase in number of SHGs and 15.2% increase

in the amount of loan outstanding during the years but the amount of NPAs decreased from

4628.05 crore on 2017-18 to 4524.01 crore on 2018-19 that is NPA as percentage to loan

outstanding decreased from 6.12% to 5.19% during the last two years. Although there is an

overall decline of 0.9% in NPAs yet it is a matter of concern. All categories of banks have

reduced their NPA level to the maximum extent during last five years. Commercial Banks have

reduced NPA level from 7.17% in 2014-15 to 5.19% in 2018-19. The Regional Rural Banks have

reduced their NPA level from 7.71% in 2014-15 to 4.87% in 2018-19. Similarly, Cooperatives

have reduced their NPA level from 8.52% in 2014-15 to 6.69% in 2018-19. All categories of

banks put together had an increase in both total loan outstanding amount of 51545.41 crore in

2014-15 to 87098.15 crore in 2018-19 and the total amount of NPA from 3815.19 crore in 2014-

15 to 4524.01 in 2018-19, but there is a remarkable decrease in NPA as percentage against loans

outstanding from 7.4% on 2014-15 to 5.19% on 2018-19. Out of the total NPA amount of

4,524.01 crore, the Commercial Banks is with 2,897.39 crore accounted for two third of the total

amount on 2018-19.

CONCLUSIONS

It is clear from the paper that all the categories of the agencies namely commercial banks (both

public sector banks and private sector banks), regional rural banks, co-operative banks play a

vital role in strengthening the SHGs in India. As on 31st March 2019, the SHG-BLP has crossed

the milestone of 1 crore SHGs with savings deposits of 23,324 crore and more than 50 lakh

groups with loan outstanding of over 87,098 crore, of which 88% was disbursed to rural women

groups. The overall economic development of the people, the banking sector has been proactive

for expanding microfinance through expansion of savings and credit linkage of SHGs.

Commercial Banks by virtue of their vast network took the lead in Self Help Group Bank

Linkage Programme. NPA is the matter to be considered and important element for the looses

faced by the agencies. From the paper it is clear that NPA level in all categories of agencies

recorded a decreasing trend as against loans outstanding. The members of SHGs should be

imparted with training programmes for livelihoods and facilitated with various channels for

marketing of products, proper grading to SHGs in order to overcome NPAs.

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1360

References:

Status of microfinance in India report 2014-15, 2015-16, 2016-17, 2017-18, 2018-19

NABARD Annual Report

The Bharat Microfinance Report 2017

Sayanee Nayak Aluni, Saptarshi Ray,”Road to Sustainable SHG-Bank Linkage Programme:

Formulating Strategies for Managing Credit Risk with respect to Rural Bengal”, IIM Kozhikode

Society & Management Review, 4(2) 146–151, © 2015 Indian Institute of Management

Kozhikode.

Tiken Das, “An analysis of Non-Performing Assets and Recovery Performance of Self Help

Group Bank Linkage Programme-Unique preference to North Eastern Region of India”, IOSP

Journal of Economics and Finance, Vol.1, Issue1(May-Jun, )2013,e-ISSN: 2321-5933, p-ISSN:

2321-5925, pp 05-14.

Rajinder Kumar, Dr. Harpreet Singh, “Role Of Commercial Banks In Financing Of Self

Help Groups In India”, Journal of Emerging Technologies and Innovative Research,

Vol.5, Issue 7 July 2018, ISSN-2349-5162, pp 1528-1534.

Bandlamudi Kalpana, Taidala Vasantaha Rao,” Role of Commercial Banks in the

Economic Development of INDIA”, International Journal of Management and Applied

Science, Vol.3, Issue-4, April.-2017, ISSN: 2394-7926, pp 1-4.

Chetan Dudhe, “Role Of Indian Commercial Banks In Economy Development”,

Conference Paper· May 2017, https://www.researchgate.net/publication/316627916.

Mohammed T. Abusharbeh, “The Impact Of Banking Sector Development On Economic

Growth: Empirical Analysis From Palestinian Economy”, Journal of Emerging Issues in

Economics, Finance and Banking (JEIEFB) An Online International Research Journal

Vol: 6 Issue: 2, (ISSN: 2306-367X) 2017, pp. 2306-2316.

Journal of Interdisciplinary Cycle Research

Volume XI, Issue XII, December/2019

ISSN NO: 0022-1945

Page No:1361