Embed Size (px)

Citation preview

July 7, 2014

Reason for report:

PROPRIETARY INSIGHTS

Seamus Fernandez(617) [email protected]

Howard Liang, Ph.D.(617) [email protected]

Michael Schmidt, Ph.D.(617) [email protected]

Aneesh Kapur617 918 [email protected]

Ario Arabi(617) [email protected]

BIOPHARMAIO Market Forecasts Increased to $36B; BMY Still Leads butCompetitors Gaining

• Bottom Line: Following our detailed review of immuno-oncology (IO)data published at ASCO 2014, we are increasing our overall IO marketforecast to $36B (from $29B in November 2013 and $32B in May 2014)to reflect our increased conviction in the clinical utility of PD1/PDL1antibodies across a broad range of solid and liquid tumors. Evidence ofbenefit in predicted and new tumors, together with assigned breakthroughdesignations in bladder cancer and Hodgkin's lymphoma, more thanoffsets reduced non-squamous NSCLC forecasts. BMY's (OP) lead,while significantly narrowed by Roche and MRK (MP) as monotherapy inseveral tumors and by AZN (MP) as combination therapy in lung cancer,remains compelling although far from assured. And consistent with ourview that the overall market remains wide open for IO combinationsgiven safety/tolerability limitations of PD1 + CTLA4 combinations, wenow project "emerging biopharma companies" as the market shareleaders with BMY & Roche having comparable share vs. BMY's previouslyassumed leadership position. With data likely to emerge on new tumorsand new PD1/PDL1 combinations in the next 6-18 months, the onlyconstant is likely to be change.

• BMY IO forecasts revised down, but leadership remains compelling.With 13 registrational PD1 monotherapy/combination therapy trialsunderway, including exploratory PD1 combinations either started (Yervoy,anti-LAG3, anti-KIR, IL-21) or planned (INCY's [OP] IDO, CLDX's [OP]CDX-1127), we continue to assume that BMY leads the overall marketwith nivolumab and IO combinations. However, MRK, Roche, & AZN'sdevelopment gains together with waning enthusiasm for PD1 + Yervoycombinations cause us to reduce BMY's IO sales forecasts from $14B to$12B in 2025.

• Roche & MRK gain the most ground from new data & rapiddevelopment; AZN's "dark horse" status advancing. New data inH&N cancer (MRK) and bladder cancer (Roche) highlight the expansivepotential of PD1/PDL1 monotherapy. In addition to MRK & Roche's greatershare of the overall PD1/PDL1 backbone, we assume both companiescapture more of the IO combination market. Our IO market forecasts(PD1/PDL1 + combos) for MRK & Roche increased from $6.3B to $7.4Band $5.5B to $8.1B in 2025, respectively. Indications that AZN's earlyPDL1 + CTLA4 combo may be more combinable than BMY's need to beconfirmed before altering our sales forecasts; look for updated data atESMO 2014.

• Opportunity for "emerging biopharma companies" in IOcombinations wide open. Questions around safety/tolerability of PD1 +CTLA4 combinations together with suggestions of comparable response

S&P 500 Health Care Index: 715.94

Companies Highlighted:AMGN, AZN, BMY, CLDX, GILD, GSK LN, INCY, JNJ,LLY, MGNX, MRK, NVS, PFE, REGN, SAN FP, TSRO

Please refer to Pages 27 - 29 for Analyst Certification and important disclosures. Price charts and disclosures specific tocovered companies and statements of valuation and risk are available athttps://leerink2.bluematrix.com/bluematrix/Disclosure2 or by contacting Leerink Partners Editorial Department, OneFederal Street, 37th Floor, Boston, MA 02110.

BIOPHARMA July 7, 2014

rates and better tolerability with Yervoy + AMGN's (MP) T-VEC and Yervoy+ INCY's INCB024360 in melanoma indicate to us that the market for IOcombinations is still wide open, implying that this race will be a marathonand not a sprint, and that the winners could be much more fragmented asnew data emerge. Therefore, we now forecast IO combination sales from"emerging biopharma companies" at $4.2B in 2025 vs. $1.0B previously.Emerging biopharma pureplays in our coverage universe include CLDX(OP), INCY (OP), MGNX (OP) and IPH.FP (OP).

• Next 6-18 months of data catalysts could be transformative toour assumptions; scenario analyses highlight risk/reward. Inthis report, we highlight five potential market moving data catalystsexpected in the next 6-18 months. Of these, achievement of a statisticallysignificant OS benefit at the planned interim evaluation of BMY'sCHECKMATE-017 (2nd line squamous NSCLC) would be the biggestupside surprise in our opinion. By contrast, Roche's planned presentationof MPDL3280a monotherapy in a new tumor together with combinationdata for MDPL3280a + Avastin likely in kidney cancer has market-movingpotential. In addition, the presentation of the 1/1 (low) dose of nivo +Yervoy and presentation of AZN's MEDI4736 + tremelimumab data inmore patients at higher doses sets up an obvious (yet flawed, in our view)opportunity to compare across trials.

2

IMMUNO-ONCOLOGY MARKET MODEL

TOTAL ADDRESSABLE MARKET:

NEW TUMORS, COMPETITIVE DEVELOPMENTS COMPEL A REVISED LOOK

Our revised $36B forecast ($29B previously in November 2013) speaks to impressive

responses across a range of new tumors

Impressive responses indicated through: (1) breakthrough therapy designations (BTD), (2) ASCO

2014 data, and (3) registrational study starts throughout 1H14 highlight the case for a growing

total addressable market for immuno-oncology agents and lead us to revisit our forecasts. Given

the meaningful and rapid progress in nine additional tumors, by our tally, we now project the

market for immuno-oncology drugs will reach $36B by 2025 on a risk adjusted basis, with potential

upside to $46B, compared to our $29B projection from November 2013.

Building from the patient level up (applied epidemiology, prognosis, and unmet need in Appendix

I), we analyze the potential addressable IO market on a risk-adjusted, tumor-by-tumor basis for

both anti-PD1/PDL1 backbone therapy and combination therapy add-ons. We currently account

for potential IO therapy across 15 separate tumor types with the net increase in the revised model

(since November 2013) largely attributable to: (a) $6B from increased probabilities of success in

bladder and head and neck (H+N) cancer, and (b) $3B in additional revenue from the addition of

glioblastoma, pancreatic, gastroesophageal, and lymphoma (diffuse large B-cell, follicular,

Hodgkin’s). These increases are offset by a net $2B net decrease in risk adjusted forecasts in

existing tumors (discussion follows). Based on the breadth and strength of data presented at

ASCO 2014, we now include these additional tumors in our overall IO model with the most

significant impact on sales for Roche and MRK and other IO therapies.

Evolution of 2025 WW Immuno-Oncology Market Forecasts, US$ Billions

Source: Leerink Partners Research

$29 $29 $29

$32

$29 $29 $29

$36

$1 $1

$3$2 $4 $4

$3

-

Nov.

2013

May

2014

July

2014

Adj. in

„Primary‟

Tumors

Adj. Prob of Success

in Other Tumors

Adj. in

„Primary‟

Tumors

Adj. Prob of Success

in Other Tumors

New Tumors

Added

3

BIOPHARMA July 7, 2014

Notably, our new base case IO model forecast of $36B validates our bullish view of the broad and

transformational potential of IO – with a continued emphasis on PD1/PDL1 antibodies as

backbone therapy. Our update primarily focuses on the rapid acceleration and advancement into

novel tumors with critical developments from each of the major competitors: BMY, MRK, Roche,

and AZN. Our discussion of each company’s tumor-specific developments follows. Overall, we

continue to see a rising tide for immunotherapy where MEDACorp KOLs believe IO has the

potential to “replace chemotherapy” over time. We estimate that the addressable market for an

advance in cancer care that replaces chemotherapy could exceed $60B.

Market entry is modeled at 2016 for bladder cancer and Hodgkin’s lymphoma given breakthrough

therapy designation and severe unmet need, while head + neck cancer is modeled at 2018 given

trial timelines, and all other additional tumors are modeled at 2019. Transitions into first-line

therapy are modeled as follows primarily based on information provided by the companies or on

clinicaltrials.gov: for melanoma (2016), lung (2019 for squamous, 2021 for non-squamous), and

kidney cancer (2019), but also for bladder (2016), H+N (2018), glioblastoma (2019), and

Hodgkin’s lymphoma (2019) given both current trial inclusion criteria and unmet need.

2014 IO Model: „New‟ Tumors Included in Leerink Risk-Adjusted Forecasts

*1

st line utilization included in model as well

Source: Leerink Partners Research, Company Information, ASCO 2014, clinicaltrials.gov

Taxotere‟s performance in REVEL confirms underlying squamous NSCLC assumptions but

raises questions about underlying trial assumptions in non-squamous NSCLC

Overall, MEDACorp KOLs are most confident in the probability of success with PD1/PDL1-based

immunotherapy in lung cancer patients who are strongly PDL1 biomarker positive or in those

patients who were smokers. Among clinical data presented at ASCO 2014, the better-than-

expected performance of non-squamous NSCLC patients treated with Taxotere in LLY’s (OP)

REVEL study may have implications for the underlying assumptions for the performance of

Taxotere in several IO lung cancer studies. In particular, it raises some questions about the

powering of BMY’s unselected CHECKMATE-057 and Roche’s OAK and POPLAR studies. By

contrast, Taxotere’s performance in squamous NSCLC patients in the REVEL study was in line

with baseline expectations. And while the delay in the timelines for BMY’s registrational, overall

survival (OS)-based CHECKMATE-017 and CHECKMATE-057 programs in 2nd

line squamous

Tumor Development (Company)Assigned

Probability

Modeled

Market Entry

Bladder (UBC)Breakthrough Therapy Designation, Impressive Data at ASCO

(Roche)80% 2016*

Hodgkin‟s Lymphoma (HL) Breakthrough Therapy Designation (BMY) 80% 2016*

Head + Neck (H+N) ASCO Data (MRK), Registrational Trial Starts (MRK, BMY) 60% 2018*

Ovarian (EOC) ASCO Data (BMY, Ono) 60% 2019

Glioblastoma (GBM) Registrational Trial Start (BMY) 30% 2019

GastroesophagealEarly Signal Data Seen, Registrational Trial Start Announced

(AZN)30% 2019

Diffuse Large B-Cell

Lymphoma (DLBCL)Registrational Trial Start (BMY) 30% 2019

Folicular Lymphoma (FL) Registrational Trial Start (BMY) 30% 2019

Pancreatic Early Signal Data Seen (AZN) 15% 2019

4

BIOPHARMA July 7, 2014

and non-squamous NSCLC is consistent with the expected tail benefits of IO therapy, it is possible

that successful completion of both studies will take longer than we or the market initially forecast.

Consistent with Taxotere’s performance in the REVEL study, as well as MRK and Roche’s data

showing the positive correlation of responses to PD1/PDL1 therapy in smokers vs. never-smokers,

we retain an 80% probability of success in squamous NSCLC. Our revised 60% probability of

success in non-squamous NSCLC (previously 80%) reflects the potential risk to the underlying

statistical assumptions for companies conducting studies in non-PDL1-selected patients and

results in a $3B decrease in our risk-adjusted forecast.

REVEL Kaplan-Meier Survival Curves: Squamous & Non-Squamous NSCLC

Source: Garon et al., Lancet (Supplement), June 2, 2014

Our continued confidence in the outcome in squamous NSCLC stems from the extremely high

unmet need and the correlations with response and smoking status seen with PD1/PDL1

therapies from Roche and MRK. Critically important is the fact that nearly all squamous NSCLC

patients are smokers. Moreover, REVEL-reported figures are consistent with the high unmet need

in these patients. In squamous patients, the 10.5% RR and 2.7 mo PFS and 32-33% and ~10% 1-

and 2-year survival rates support the underlying assumptions that only 10% of NSCLC patients

respond to second-line docetaxel and ~30% of patients are alive at 12 months.

Correlation of Smoking Status with Response Rate (MK-3475 & MPDL3280a)

Source: Garon et al., ASCO 2014; Soria et al., ESMO 2013

In non-squamous patients, on the other hand, the 14.5% RR, 3.7 month PFS, and 39-40% and 20-

21% 1- and 2-year survival rates on the Taxotere arm raise questions regarding how well the

comparator Taxotere arm will perform in -057, although the populations are likely substantially

5

BIOPHARMA July 7, 2014

different, with patients in BMY’s Phase I study (-003) having had an average of 3 prior lines of

therapy. Nonetheless, even though the specific underlying assumptions for the statistical design of

the CHECKMATE-057 have not been published, a trial design poster presentation from ASCO

2013 (Gettinger et. Al) cites 12-month median survival of 7-8 months and response rates of 8-10%

based on data from 2000-2004. Given our limited knowledge of the underlying assumptions for

CHECKMATE-057, we have lowered our probability of success in non-squamous disease to 60%

and look to near-term catalysts to instill greater confidence. BMY remains confident in what the

randomized nature of these Ph III studies will elucidate regarding the impact of PD1 agents on

survival, and we point to the fact that delayed completion dates (moved from late-2014 to mid-

2015 and early 2016) may reflect better-than-expected patient survival and the need to wait for

events (deaths or progression) to accrue.

We discuss below (in the catalysts section) the novel non-proportional hazard ratio of BMY’s OS

outcomes studies which gives us confidence that the tail effects of immuno-therapy on survival will

be ultimately captured by BMY’s 2nd

line monotherapy survival studies (-017 & -057). Nonetheless,

much remains to be told on the story of IO in lung cancer, and we believe our revised figures

better reflect the most up-to-date data in lung cancer. The $3B reduction in our non-squamous

NSCLC forecast was partially offset in the “primary” tumors by a $1B increase in risk adjusted

figures for melanoma given MRK’s filing and earlier-than-expected market entry timelines.

2014 IO Model: „Primary‟ Tumor Assumptions in Leerink Risk-Adjusted Forecasts

Source: Leerink Partners Research

More data to come through 1H15…

We continue to expect additional data to: (1) further inform the lung cancer story, particularly for

combination therapy with either a PD1 or PDL1 antibody with a CTLA4 antibody; and (2) bolster

the data supporting advancement into registrational studies for several “new” tumors. Avastin +

PDL1 combination data expected in 2H14 could add to the body of combination data in kidney

cancer, or expand upon the tumors where meaningful signals have been seen including either

liver or colorectal cancer. Roche also confirmed that it expects to present data before year-end

2014 in at least one new tumor where PDL1 antibody monotherapy is active. This suggests that

before year-end we may need to reconsider at least one of the tumors that do not contribute sales

to our IO market model. These include: liver, cervical, colorectal, breast (HER2+, ER+/HER2-,

triple negative), leukemia, and myeloma. With Roche and AstraZeneca highlighting ESMO 2014

(9/26-9/30) as “the most important cancer immunotherapy conference of the year,” we expect

investors to pay careful attention to further developments at major medical meetings in 2H14/

Tumor Development (Company)Assigned

Probability

Modeled

Market Entry

(1st Line)

Melanoma (MEL)Yervoy Refractory BLA Filing (MRK); Early 1st Line Trial Stoppage on

Overall Survivial (BMY)100% 2015 (2016)

Non-squamous NSCLCQuestions Around Underlying Assumptions for Taxotere’s Efficacy in

2nd Line; Delayed Completion Date for Overall Survival Study (BMY)60% 2016 (2021)

Squamous NSCLCRolling BLA Filing Ongoing (BMY); Delayed Completion Date for

Overall Survival Study, Interim Analysis Planned (BMY)80% 2016 (2019)

Kidney (RCC) Potential Completion of CHECKMATE-025 .vs Afinitor in 2015 (BMY) 80% 2016 (2019)

6

BIOPHARMA July 7, 2014

1H15. We also expect significant focus from investors on combination therapy trials as data

mature, are known internally, and potentially serve as an opportunity to advance new

combinations into registrational trials.

In addition to cataloging these key meetings and pot’l data/ company developments (Appendix II),

we include detailed analysis of five specific catalysts and their modeled market and revenue

impacts, starting on p. 18 (Catalyst section) below.

Bull ($46B), base ($36B), and bear ($18B) scenarios for 2025 highlight wide range of

potential IO market outcomes

Bull case: $46B WW, $20B US is based on increasing the probabilities of clinical

success in lung (squamous & non-squamous) and kidney cancer to 100% (from 80%,

60%, and 80%, respectively. All other probabilities are unchanged from the base case.

Additional upside to our bull case forecasts is possible with broad evidence of clinically

significant survival benefits in currently modeled tumors or from the inclusion of additional

tumors as new data emerge.

Base case: $36B WW, $16B US is based on our current assumptions of the probabilities

of success in the “primary” IO tumors (melanoma=100%, non-squamous=60% and

squamous NSCLC=80%, and renal=80%) as reviewed above. We assign high (80%)

probabilities of success in tumors with breakthrough therapy designation (BTD status;

bladder, Hodgkin’s); medium (60%) probabilities in tumors where compelling clinical data

were presented at ASCO (H+N, ovarian); and low (30%) and uncertain (15%)

probabilities in other solid (glioblastoma multiforme [GBM], gastroesophageal, pancreatic,

prostate) and liquid (follicular lymphoma [FL], diffuse large B-Cell lymphoma [DLBCL])

tumors where early data signals have been revealed or will soon be presented and/or

registrational trials have started.

Bear case: $18B WW, $8B US is based on base case probabilities of success (as

delineated above) but this scenario assumes no expansion to front line use outside of

melanoma, where BMY has already achieved this with nivolumab vs. DTIC in

CHECKMATE-066. This scenario considers the possibility that: (a) significant second/

third line utilization of PD1/PDL1 immunotherapies limits single agent PD1/PDL1 or other

single-agent immunotherapies from ever being able to show an OS benefit in the first line

setting, and (b) the toxicity of combination IO therapies is too significant to justify front-line

use. This scenario also assumes no IO utilization outside of melanoma, lung, bladder,

Hodgkin’s, and H+N cancers.

7

BIOPHARMA July 7, 2014

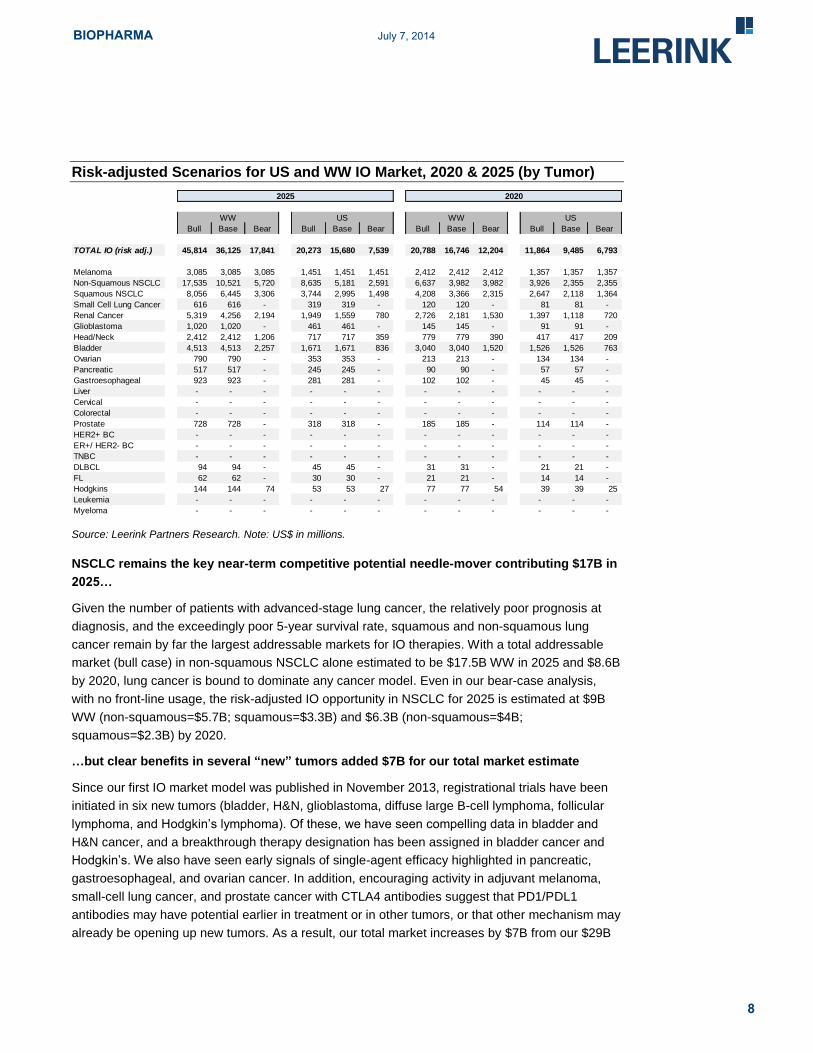

Risk-adjusted Scenarios for US and WW IO Market, 2020 & 2025 (by Tumor)

Source: Leerink Partners Research. Note: US$ in millions.

NSCLC remains the key near-term competitive potential needle-mover contributing $17B in

2025…

Given the number of patients with advanced-stage lung cancer, the relatively poor prognosis at

diagnosis, and the exceedingly poor 5-year survival rate, squamous and non-squamous lung

cancer remain by far the largest addressable markets for IO therapies. With a total addressable

market (bull case) in non-squamous NSCLC alone estimated to be $17.5B WW in 2025 and $8.6B

by 2020, lung cancer is bound to dominate any cancer model. Even in our bear-case analysis,

with no front-line usage, the risk-adjusted IO opportunity in NSCLC for 2025 is estimated at $9B

WW (non-squamous=$5.7B; squamous=$3.3B) and $6.3B (non-squamous=$4B;

squamous=$2.3B) by 2020.

…but clear benefits in several “new” tumors added $7B for our total market estimate

Since our first IO market model was published in November 2013, registrational trials have been

initiated in six new tumors (bladder, H&N, glioblastoma, diffuse large B-cell lymphoma, follicular

lymphoma, and Hodgkin’s lymphoma). Of these, we have seen compelling data in bladder and

H&N cancer, and a breakthrough therapy designation has been assigned in bladder cancer and

Hodgkin’s. We also have seen early signals of single-agent efficacy highlighted in pancreatic,

gastroesophageal, and ovarian cancer. In addition, encouraging activity in adjuvant melanoma,

small-cell lung cancer, and prostate cancer with CTLA4 antibodies suggest that PD1/PDL1

antibodies may have potential earlier in treatment or in other tumors, or that other mechanism may

already be opening up new tumors. As a result, our total market increases by $7B from our $29B

Bull Base Bear Bull Base Bear Bull Base Bear Bull Base Bear

TOTAL IO (risk adj.) 45,814 36,125 17,841 20,273 15,680 7,539 20,788 16,746 12,204 11,864 9,485 6,793

Melanoma 3,085 3,085 3,085 1,451 1,451 1,451 2,412 2,412 2,412 1,357 1,357 1,357

Non-Squamous NSCLC 17,535 10,521 5,720 8,635 5,181 2,591 6,637 3,982 3,982 3,926 2,355 2,355

Squamous NSCLC 8,056 6,445 3,306 3,744 2,995 1,498 4,208 3,366 2,315 2,647 2,118 1,364

Small Cell Lung Cancer 616 616 - 319 319 - 120 120 - 81 81 -

Renal Cancer 5,319 4,256 2,194 1,949 1,559 780 2,726 2,181 1,530 1,397 1,118 720

Glioblastoma 1,020 1,020 - 461 461 - 145 145 - 91 91 -

Head/Neck 2,412 2,412 1,206 717 717 359 779 779 390 417 417 209

Bladder 4,513 4,513 2,257 1,671 1,671 836 3,040 3,040 1,520 1,526 1,526 763

Ovarian 790 790 - 353 353 - 213 213 - 134 134 -

Pancreatic 517 517 - 245 245 - 90 90 - 57 57 -

Gastroesophageal 923 923 - 281 281 - 102 102 - 45 45 -

Liver - - - - - - - - - - - -

Cervical - - - - - - - - - - - -

Colorectal - - - - - - - - - - - -

Prostate 728 728 - 318 318 - 185 185 - 114 114 -

HER2+ BC - - - - - - - - - - - -

ER+/ HER2- BC - - - - - - - - - - - -

TNBC - - - - - - - - - - - -

DLBCL 94 94 - 45 45 - 31 31 - 21 21 -

FL 62 62 - 30 30 - 21 21 - 14 14 -

Hodgkins 144 144 74 53 53 27 77 77 54 39 39 25

Leukemia - - - - - - - - - - - -

Myeloma - - - - - - - - - - - -

2025 2020

USWW USWW

8

BIOPHARMA July 7, 2014

forecast in November 2013 to reflect both increased probabilities of success or the addition of

other tumors.

See scenario #2 and scenarios #4/5 for the impact near-term 2H14-1H15 catalysts could have on

the total addressable market in lung cancer and other incremental tumors, respectively.

We continue to expect the true inflection to come post-2020 as 1st line lung cancer studies

and incremental tumors mature

Our expectation for IO revenues to double between 2020 and 2025 ($18B and $36B WW in base

case) is driven by: (a) key front-line opportunities in NSCLC, and (b) a typical delayed uptake

curve in ex-US markets. First-line utilization in lung cancer has the potential to double the

treatable population in the critically important NSCLC tumors. As mentioned above, front-line

availability is estimated in 2019 for squamous and 2021 for non-squamous in the bull and base

case, without significant revenue impact until 2020 and beyond.

Utilization of IO in other developed markets is also expected to be a significant yet delayed driver

of revenues. Market uptake for each agent was based on the global launch trajectory for Erbitux.

This was selected due to a relatively limited group of indications allowing for a “purer” estimate of

the launch trajectory of an individual tumor. Erbitux’s market uptake reflects our expectations for

ex-US uptake in developed markets, given oft-delayed market entries and slower pricing and

reimbursement determinations. Whereas Erbitux reached 80% of its peak sales in its third year

after launch in the US, the same 80% benchmark was not achieved until year six in Ex-US sales.

Applying these uptake trends to IO agents leads to lung cancer and other revenues ramping

significantly between 2020 and 2025.

Increasing probabilities of success in additional tumors, particularly as clinical development

progresses, could add even more upside in the post-2020 period.

9

BIOPHARMA July 7, 2014

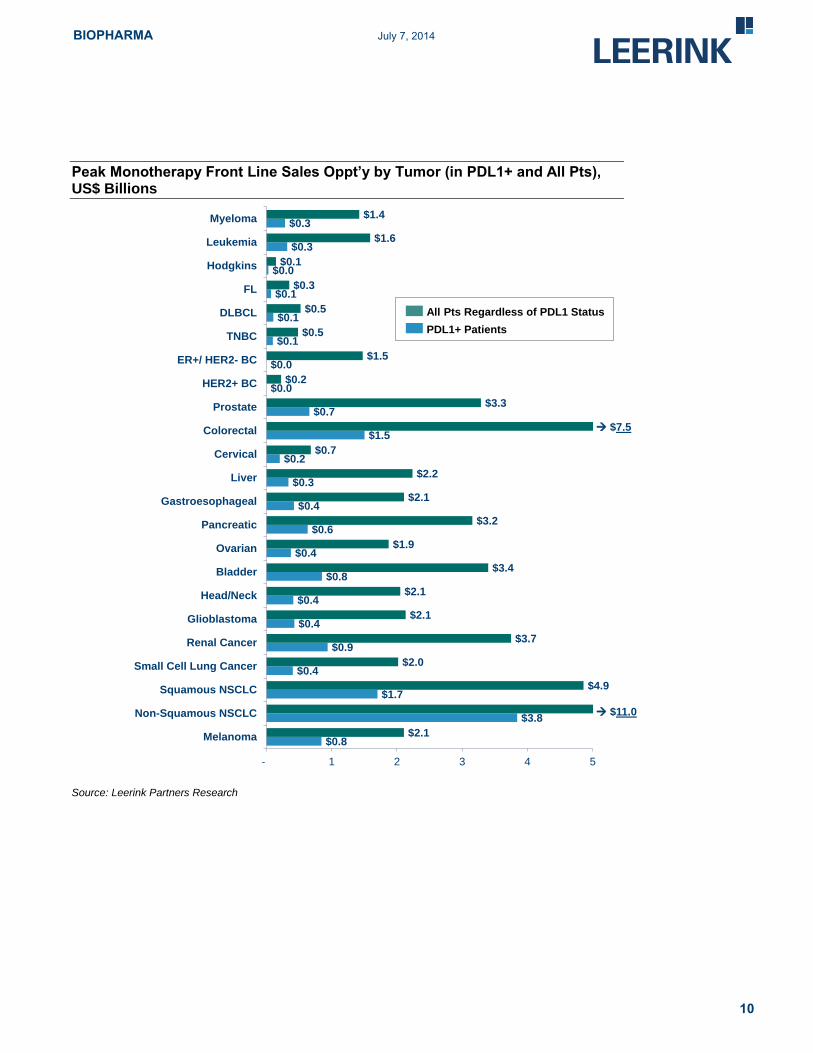

Peak Monotherapy Front Line Sales Oppt‟y by Tumor (in PDL1+ and All Pts), US$ Billions

Source: Leerink Partners Research

$11.0

$7.5

$0.8

$3.8

$1.7

$0.4

$0.9

$0.4

$0.4

$0.8

$0.4

$0.6

$0.4

$0.3

$0.2

$1.5

$0.7

$0.0

$0.0

$0.1

$0.1

$0.1

$0.0

$0.3

$0.3

$2.1

$4.9

$2.0

$3.7

$2.1

$2.1

$3.4

$1.9

$3.2

$2.1

$2.2

$0.7

$3.3

$0.2

$1.5

$0.5

$0.5

$0.3

$0.1

$1.6

$1.4

- 1 2 3 4 5

Melanoma

Non-Squamous NSCLC

Squamous NSCLC

Small Cell Lung Cancer

Renal Cancer

Glioblastoma

Head/Neck

Bladder

Ovarian

Pancreatic

Gastroesophageal

Liver

Cervical

Colorectal

Prostate

HER2+ BC

ER+/ HER2- BC

TNBC

DLBCL

FL

Hodgkins

Leukemia

Myeloma

PDL1+ Patients

All Pts Regardless of PDL1 Status

10

BIOPHARMA July 7, 2014

COMPETITIVE DYNAMICS AND MARKET SHARE:

BMY retains leadership but PD1/PDL1 share adjusted to account for Roche & MRK‟s gains

while AZN, Roche & other emerging biopharmas gain in combos

BMY is modeled to achieve sales that are 35 and 40% higher than its closest competitors

in 2020 and 2025, respectively, based on a continued, strong expected PD1/PDL1

backbone market share given its leadership position in melanoma, kidney, and lung

cancer survival studies as well as the broadest registrational study program of PD1/PDL1

backbone and combination therapies to date. BMY’s lead in kidney cancer is particularly

distinguished in our view, given a 2+ year lead over competitors with its 2nd

line OS study

vs. NVS’s (OP) Afinitor. BMY’s IO combination portfolio is also among the largest and

most advanced with Yervoy, anti-LAG3, anti-KIR (w/ Innate Pharma), anti-CD137, and IL-

21. However, versus our interim model, we now no longer assume that BMY retains a

long-term advantage in IO combinations and our revised probability of success in non-

squamous NSCLC further reduced our forecasts. As a result, the addition of $2B in sales

for BMY at our interim model update vs. our initial $12B forecast in November 2013 to

reflect increased affirmation of the near-term melanoma and renal cancer markets as well

as H+N and bladder cancer is reversed to reflect a more muted outlook for Yervoy

combinations (particularly in lung cancer) and a tempered view of the probability of

success in non-squamous NSCLC.

Roche is forecast to have the second-highest revenues given an early lead with BTD

status in a significant bladder cancer market, strong participation in the initial wave of IO

advancement into lung cancer, and a rapidly advancing portfolio of IO combination targets

across both gRED (Genentech research) and pRED (Roche research) portfolios. We

raise our forecasts to $8B in 2025 sales versus $5.5B in our model in November 2013 as

neither this strong position in lung cancer nor the company’s meaningful lead with a BTD

in bladder cancer was priced in. Roche’s sustained strength in combination

immunotherapy research and commitment to presenting data in a novel tumor before

YE14 present potential near-term upside, in our opinion.

MRK continues to maintain its #3 position in our overall IO market model driven by its

rapid development of MK-3475 across a broad range of tumors, including its leadership

position in melanoma and H+N cancer and as a fast-follower in lung and bladder cancers.

MRK’s momentum in melanoma and lung cancer provides it the chance to exceed

Roche’s IO revenues through 2020E, and while we see opportunity for MRK to participate

in the IO combination opportunity, internally developed pipeline assets are very early, and

we assume that any non-exclusive external research collaborations benefit MRK’s PD1

backbone but the combination products’ sales are attributed to “Other Emerging

Biopharma” in our model. We add nearly $1.5B in sales to MRK’s IO franchise since our

interim model and factor in revenues from combination therapy into the company model.

Since our last forecast of $4.5B in sales for MRK last November, our cumulative IO

market sales increased by nearly $3B to ~$7.5B in 2025.

AZN continues to be somewhat limited more by its 4th-to-market position with its PDL1

antibody, yet we continue to view the company as a “dark horse” given its aggressive

11

BIOPHARMA July 7, 2014

monotherapy development path in 2nd

line and Stage III chemotherapy-naive lung cancer

patients. With plans to advance its combination of MEDI4736 (anti-PDL1) +

tremelimumab (anti-CTLA4) in 2H14 now largely in line with to slightly ahead of BMY’s

Phase III development plans for nivolumab + Yervoy in lung cancer, AZN has the

potential to be among the leaders in combination therapy development. This is somewhat

tempered by tolerability/toxicity challenges with CTLA4 combinations. Additional data

from BMY and AZN’s PD1 and PDL1 + CTLA4 combinations to be presented in 2H14

may be critical to the market’s perception of both the efficacy and combinability of each

combination. Our $5B in forecasted 2025 sales could be bolstered by codification of a

safe MEDI4736 + tremelimumab combination in lung cancer and/or an established lead in

novel tumors such as gastroesophageal or pancreatic cancer, where AZN showed early

signals at ASCO. We are making no changes to our AZN forecasts at this time. See

Scenario #1 for our evaluation of the impact that data supporting PDL1 antibodies as the

more combinable agents in lung cancer could have on our sales forecasts.

Emerging IO biopharmaceutical companies (INCY, IPH.FP, AMGN, JNJ [OP], NVS, PFE

{MP], Bayer/CGEN, TSRO [OP], etc.) as a group are now forecast to account for 35% of

the market for combination therapies. As a result, our 2025 revenues for this group are

now increased 2x over our November 2013 expectations. Confirmation that combinations

can help resolve the inadequacy of PD1/PDL1 monotherapy in certain patients and

promising early safety profiles result in higher forecasted share capture of the add-on

combination therapy market among this group of companies given the disruptive potential

of IDO inhibitors, therapeutic vaccines, and natural killer (NK) cell targeted

antibodies/agents.

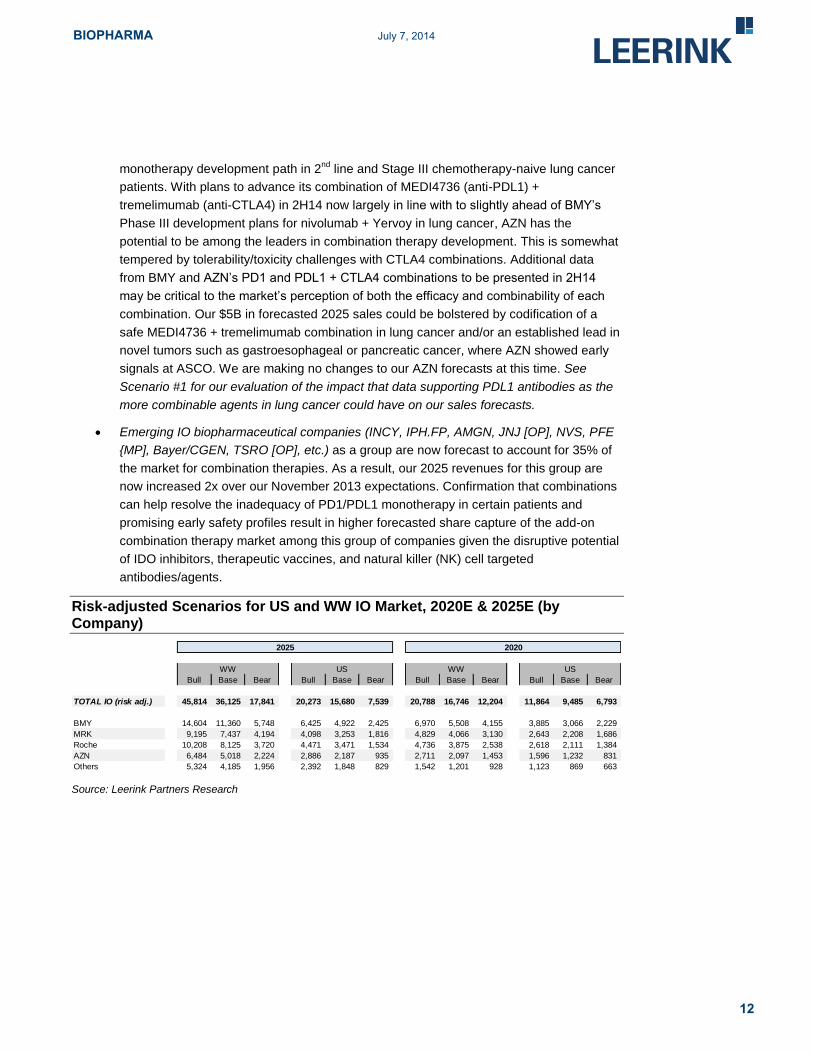

Risk-adjusted Scenarios for US and WW IO Market, 2020E & 2025E (by Company)

Source: Leerink Partners Research

Bull Base Bear Bull Base Bear Bull Base Bear Bull Base Bear

TOTAL IO (risk adj.) 45,814 36,125 17,841 20,273 15,680 7,539 20,788 16,746 12,204 11,864 9,485 6,793

BMY 14,604 11,360 5,748 6,425 4,922 2,425 6,970 5,508 4,155 3,885 3,066 2,229

MRK 9,195 7,437 4,194 4,098 3,253 1,816 4,829 4,066 3,130 2,643 2,208 1,686

Roche 10,208 8,125 3,720 4,471 3,471 1,534 4,736 3,875 2,538 2,618 2,111 1,384

AZN 6,484 5,018 2,224 2,886 2,187 935 2,711 2,097 1,453 1,596 1,232 831

Others 5,324 4,185 1,956 2,392 1,848 829 1,542 1,201 928 1,123 869 663

2025 2020

USWW USWW

12

BIOPHARMA July 7, 2014

PD1/PDL1 RACE EXPANDS TO NEW TUMORS, WHILE COMBO OPPORTUNITY

REMAINS WIDE OPEN

PD1/PDL1 further cements itself as the backbone in more tumors, yet combos remain

critical to IO‟s full potential

We continue to factor in anti-PD1/PDL1 as a consistent backbone for immunotherapy across

tumors. Based on consistently strong (30%+) response rates in PDL1 biomarker positive patients

across a number of tumors together with the logistical reality that PD1/PDL1 antibodies currently

form the base for all combo studies being initiated/ sought after by pharma and biotech players,

we and MEDACorp KOLs see limited opportunity for PD1/PDL1 therapy to be unseated as the

primary IO backbone treatment option. The ability to augment two- to three-fold lower RRs in the

PDL1(-) patient population with combination therapy continues to be demonstrated in PD1 +

CTLA4 trials in melanoma, but data in kidney and lung cancer remain too immature to draw any

firm conclusions about the ability of IO combinations to enhance RRs in PDL1 biomarker positive

or negative patients vs. PD1/PDL1 monotherapy outside of melanoma. Nonetheless, preclinical

science and the rapid advancement of at least nine IO combinations to date with several additional

combinations planned support our longer-term expectation that combos will play a critical role in

IO’s ability to address a broader cancer patient population.

PDL1 status, despite its faults, plays an important role in conceptualizing the market

Though much has yet to evolve with PDL1 biomarkers, consistent data demonstrating the role of

PDL1 status in enriching for responders inform our underlying modeling assumption that in the

long term, PDL1(+) patients receive monotherapy treatment and PDL1(-) patients receive

combination IO. While this is obviously an oversimplification of how treatment is likely to evolve,

conceptualizing the market in this way allows us to use PDL1 biomarker status as an approximate

indicator of the number of patients that are estimated to need combination therapy as a first line

treatment option. It also is consistent with KOLs feedback regarding the need to select patients to

manage both toxicity and cost associated with combination cancer therapy.

Our summary analysis across available PDL1 expression data from immunohistochemistry (IHC)

assays being used by the major competitors (including BMY Dako 28-8, MRK CC23, Roche GNE,

and AZN VENTANA) informs tumor-specific PDL1 biomarker positive rates in 9 of the 15 tumors

modeled, with 3-4 corroborating assays in the primary tumors (melanoma, lung, kidney). We used

less inclusive high PDL1 expresser cutoffs in our base case, as we believe this is more likely to

represent the ultimate population that receives only PD1/PDL1 monotherapy. Our model assumes

that patients are likely to receive PD1/PDL1 therapy regardless of biomarker status in the

refractory (second and third line) setting, while sales in the first line setting for monotherapy vs.

combination therapy are determined on the basis of PDL1 biomarker status.

PD1/PDL1 market share is now modeled by tumor type, better accounting for competition

Despite the early stage of much of the available data and little clarity on which competitors will

ultimately perform the best by tumor, we now stratify our model by tumor and among the four

leading PD1/PDL1 antibody companies. For PD1/PDL1 monotherapy and backbone sales we

model tumor-specific market shares along with differences in expected development timelines for

competitors in each tumor.

13

BIOPHARMA July 7, 2014

Breakthrough designations and meaningful registrational trial leads rewarded; BMY still

stands out but MRK and Roche gaining ground

Given surprisingly similar safety and efficacy data of PD1 and PDL1 antibodies as monotherapy,

first-in-class status is the biggest driver of each company’s expected share. Known information on:

(a) breakthrough designations and (b) registrational trial timelines are used to inform individual

company market shares across the various tumors.

Breakthrough Therapy Designations (BTDs): We attribute 60% share to MRK in

melanoma (10/28 PDUFA), Roche in bladder, and BMY in Hodgkin’s based on BTDs

likely allowing more accelerated time to market. BMY is expected to take the remaining

share of the melanoma market as few other companies are running compelling

registrational trials in this tumor. The early and unexpected success of the CHECKMATE-

066, which showed an OS benefit in first-line melanoma vs. DTIC is likely to result in rapid

approvals in the EU and Canada, and we believe that demonstration of a superior survival

could provide an advantage when seeking government reimbursement.

Lung Cancer Registrational Timelines: BMY’s true revenue-driving lead on the PD1/PDL1

front comes from the 40% and 35% market share we attribute in squamous and non-

squamous NSCLC, respectively, based on: (1) an ongoing rolling filing with the FDA in 3rd

line squamous disease (CHECKMATE-063, which forms the basis of filing, to have data

at Thoracic Oncology 10/30-11/1); and (2) BMY being the leading and potentially only

company capable of showing an OS benefit in lung cancer irrespective of PDL1

biomarker status with the CHECKMATE-017 and -057 studies in 2nd

line patients.

Together, this assumed market share advantage adds $1.3B to BMY’s forecasted sales

vs. even share distribution in lung cancer. Scenario analyses evaluate potential market

moving 2H14-1H15 catalysts: see Scenario #3 for the impact of MRK and Roche catch up

in lung cancer filing.

Early Registrational Timeline Leads: We currently attribute 30% share to MRK as the fast-

follower in bladder cancer. MRK and BMY also are assumed to have 30% share each in

H+N given registrational study starts, which appear to put each company marginally

ahead of other competitors. Nonetheless, these could quickly change as others initiate

trials (as BMY has indicated it will do soon in bladder) and trials progress. BMY is given

65% in glioblastoma due to its registrational study initiation and the lack of any

involvement (based on our current knowledge) of other competitors. See Scenario #4 and

5 below for the impact that novel data could have on early timeline leads in genitourinary

(GU) and liquid tumors.

Where specific developments did not suggest any particular company had a lead but a signal of

single-agent efficacy was evident, market share was divided equally among the major four players

in the PD1/PDL1 market.

14

BIOPHARMA July 7, 2014

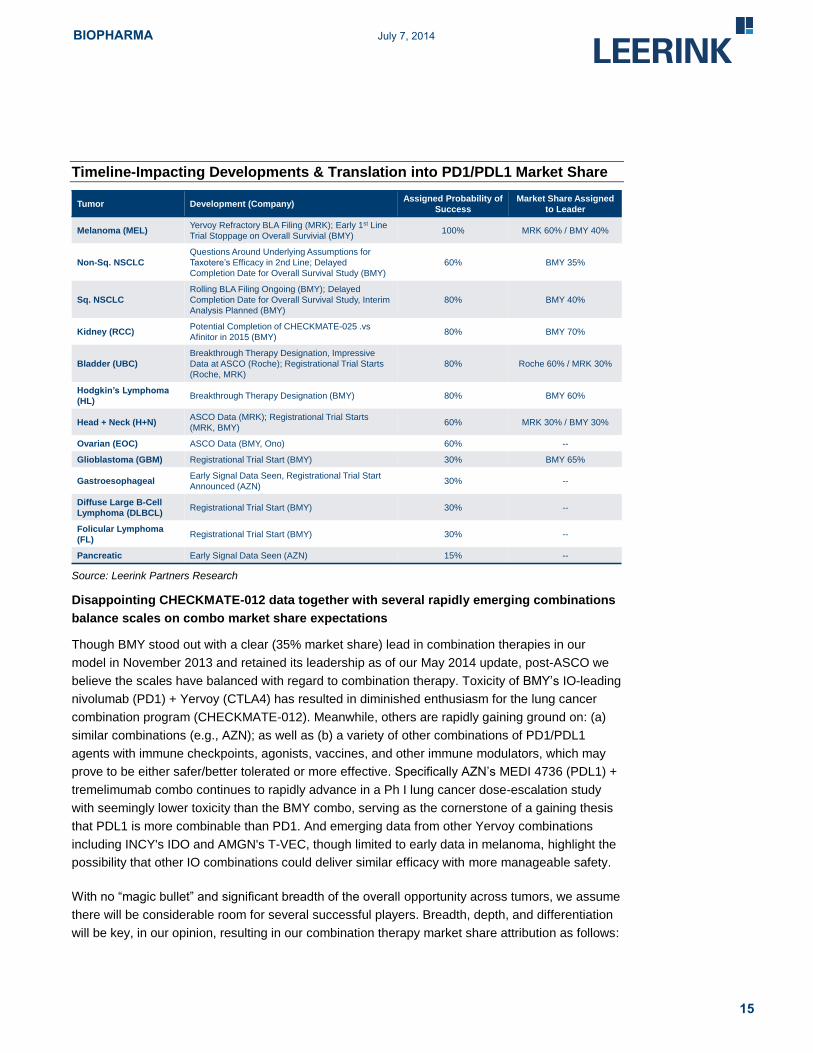

Timeline-Impacting Developments & Translation into PD1/PDL1 Market Share

Source: Leerink Partners Research

Disappointing CHECKMATE-012 data together with several rapidly emerging combinations

balance scales on combo market share expectations

Though BMY stood out with a clear (35% market share) lead in combination therapies in our

model in November 2013 and retained its leadership as of our May 2014 update, post-ASCO we

believe the scales have balanced with regard to combination therapy. Toxicity of BMY’s IO-leading

nivolumab (PD1) + Yervoy (CTLA4) has resulted in diminished enthusiasm for the lung cancer

combination program (CHECKMATE-012). Meanwhile, others are rapidly gaining ground on: (a)

similar combinations (e.g., AZN); as well as (b) a variety of other combinations of PD1/PDL1

agents with immune checkpoints, agonists, vaccines, and other immune modulators, which may

prove to be either safer/better tolerated or more effective. Specifically AZN’s MEDI 4736 (PDL1) +

tremelimumab combo continues to rapidly advance in a Ph I lung cancer dose-escalation study

with seemingly lower toxicity than the BMY combo, serving as the cornerstone of a gaining thesis

that PDL1 is more combinable than PD1. And emerging data from other Yervoy combinations

including INCY's IDO and AMGN's T-VEC, though limited to early data in melanoma, highlight the

possibility that other IO combinations could deliver similar efficacy with more manageable safety.

With no “magic bullet” and significant breadth of the overall opportunity across tumors, we assume

there will be considerable room for several successful players. Breadth, depth, and differentiation

will be key, in our opinion, resulting in our combination therapy market share attribution as follows:

Tumor Development (Company)Assigned Probability of

Success

Market Share Assigned

to Leader

Melanoma (MEL)Yervoy Refractory BLA Filing (MRK); Early 1st Line

Trial Stoppage on Overall Survivial (BMY)100% MRK 60% / BMY 40%

Non-Sq. NSCLC

Questions Around Underlying Assumptions for

Taxotere’s Efficacy in 2nd Line; Delayed

Completion Date for Overall Survival Study (BMY)

60% BMY 35%

Sq. NSCLC

Rolling BLA Filing Ongoing (BMY); Delayed

Completion Date for Overall Survival Study, Interim

Analysis Planned (BMY)

80% BMY 40%

Kidney (RCC)Potential Completion of CHECKMATE-025 .vs

Afinitor in 2015 (BMY)80% BMY 70%

Bladder (UBC)

Breakthrough Therapy Designation, Impressive

Data at ASCO (Roche); Registrational Trial Starts

(Roche, MRK)

80% Roche 60% / MRK 30%

Hodgkin‟s Lymphoma

(HL)Breakthrough Therapy Designation (BMY) 80% BMY 60%

Head + Neck (H+N)ASCO Data (MRK); Registrational Trial Starts

(MRK, BMY)60% MRK 30% / BMY 30%

Ovarian (EOC) ASCO Data (BMY, Ono) 60% --

Glioblastoma (GBM) Registrational Trial Start (BMY) 30% BMY 65%

GastroesophagealEarly Signal Data Seen, Registrational Trial Start

Announced (AZN)30% --

Diffuse Large B-Cell

Lymphoma (DLBCL)Registrational Trial Start (BMY) 30% --

Folicular Lymphoma

(FL)Registrational Trial Start (BMY) 30% --

Pancreatic Early Signal Data Seen (AZN) 15% --

15

BIOPHARMA July 7, 2014

BMY – 20% of add-on combination therapies as the company continues to progress with

a portfolio including anti-LAG3, anti-KIR, IL-21, and 4-1BB agonist as well as right of first

refusal on CD27.

Roche – 20% of add-on combination therapies as the company demonstrates impressive

prowess in bringing novel and competitively less understood targets such as CSF1-R to

the clinic, in addition to the upcoming start of an OX40 trial in the clinic. Further,

leveraging Genentech’s history of oncology leadership provides both expertise and a

broad portfolio of other potential immune modulators. See Scenario #4 below for the

impact near-term data on PDL1+Avastin combos could have in opening and establishing

Roche’s combination lead in genitourinary (GU) tumors.

AZN – 15% of add-on combination therapies as a rapidly advancing PDL1 + CTLA4

combination looks to differentiate itself, and the company moves both an OX40 fusion

protein and antibody into the clinic before 1Q15. See Scenario #1 below for the impact if

PDL1 emerges with best-in-class combinatorial potential in lung cancer.

MRK – 10% of add-on combination therapies given a relatively slim set of in-house

combination agents compared to its competitors, though the company will likely have the

first GITR program in the clinic. While MRK is expected to generate PD1/PDL1 revenues

from combinations with others’ targeted agents and immune modulators (NVS – formerly

GSK – combos and INCY IDO combos), these are not wholly owned assets and MRK

runs the risk of losing access based on strategic partnerships or acquisitions by

competitors.

Other emerging biopharmaceutical players – 35% of add-on combination therapies

recognizing not only the impressive initial data for AMGN’s T-Vec and INCY’s IDO in

melanoma, but further acknowledgement that much remains to be determined in the

realm of combinations. In addition to the variety of publicly and privately funded biotechs

now participating in the field, we expect 1H15 will see other Major Pharma players (NVS,

PFE) initiate clinical trials as well.

16

BIOPHARMA July 7, 2014

OTHER MODELING ASSUMPTIONS

DURATION & PRICING REMAIN QUESTIONS – MRK WILL BE PRICE SETTER IN 2H14

For PD1/PDL1 therapy, we forecast pricing in line with modern therapies ($10K/pt per

month); MRK‟s price-leader status in melanoma a major event for the class

MRK’s pembrolizumab (MK-3475) potential launch in melanoma (10/28 PDUFA) will establish

pricing for the class – an important and likely controversial event given political and payer

backlash around GILD’s (OP) Sovaldi. We believe initial payer management and community

physician utilization given MRK’s price point are worth careful attention. Our assumed

$10K/pt/month cost would come at a slight premium to recent targeted therapy launches and in

line with the cost of a full course of Yervoy ($120K/pt/year). Though our model estimates ex-US

pricing at 70% of US prices, stronger-than-expected EU sales of Yervoy, to date, speak to the

positive impact of durable survival on use and pricing power. Current prices in both the UK and

Germany suggest nearly equivalent pricing to the US price of $30,000 per cycle, after foreign

exchange adjustments.

For add-on combination therapy, we only assume that each patient adds ~$60K/year on top of the

cost of the PD1/PDL1 backbone. Strategically, we continue to assume that more of the value per

patient accrues to the companies with PD1/PDL1 backbone agents.

Firm dose selection from MRK and BMY removes a long-term potential risk

Notably, an important longer-term risk is removed with MRK and BMY’s selection of a dose to

move forward with in single agent trials. MRK settled on its 2 mg/kg (mpk) every three weeks

(Q3W) dosing seeing little dose-response vs. the 10 mpk dose in lung cancer, while BMY selected

3 mpk Q2W with a nice convergence of data from melanoma, kidney, and lung cancer consistently

pointing to this as the optimal dose. These firm dose selections limit the risk that one of the drugs

would be made available and priced at an unnecessarily high dose particularly given the relatively

flat dose-response relationship with monoclonal antibodies overall.

Duration of therapy in practice remains significant unknown; we model based on median

PFS

Our discussions with MEDACorp KOLs and our impressions from oncologists at medical

conferences suggest that few expect the ideal dosing practices to be determined until physicians

have real-world experience with the products in different tumors. To account for different expected

treatment durations by tumor, we utilized current PFS levels as a base case for duration of

therapy. Adjustments were made in certain tumors, most notably melanoma and lung cancer,

where we expect an increase in duration of treatment with immunotherapy.

17

BIOPHARMA July 7, 2014

KEY 2H14-1H15 CATALYSTS & SCENARIO ANALYSES

Acknowledging both the number of assumptions underlying our market forecast and the number of

critical catalysts expected even before ASCO 2015, we highlight five key scenarios we believe

warrant investor attention. We believe that each scenario has the potential to credibly shift share

or increase overall market sales by $500M-$2B. These scenarios are focused both on lung cancer

filings and combo-controversies as well as new tumor/ mechanism information that could alter the

total addressable market (TAM). We list the scenarios here and provide additional detail on each

below. We recognize that while these five catalysts may have a significant and important impact

on market perceptions in the next 9-18 months, further advancement of PD1/PDL1 therapies into

other new tumors, and/or the acceleration or discontinuation of newer IO combos could make this

analysis quickly outdated.

Revenue Impact of Five Key 2H14-1H15 Catalysts & Scenarios in IO

RCC = renal cell carcinoma; CRC = colorectal cancer Source: Leerink Partners Research

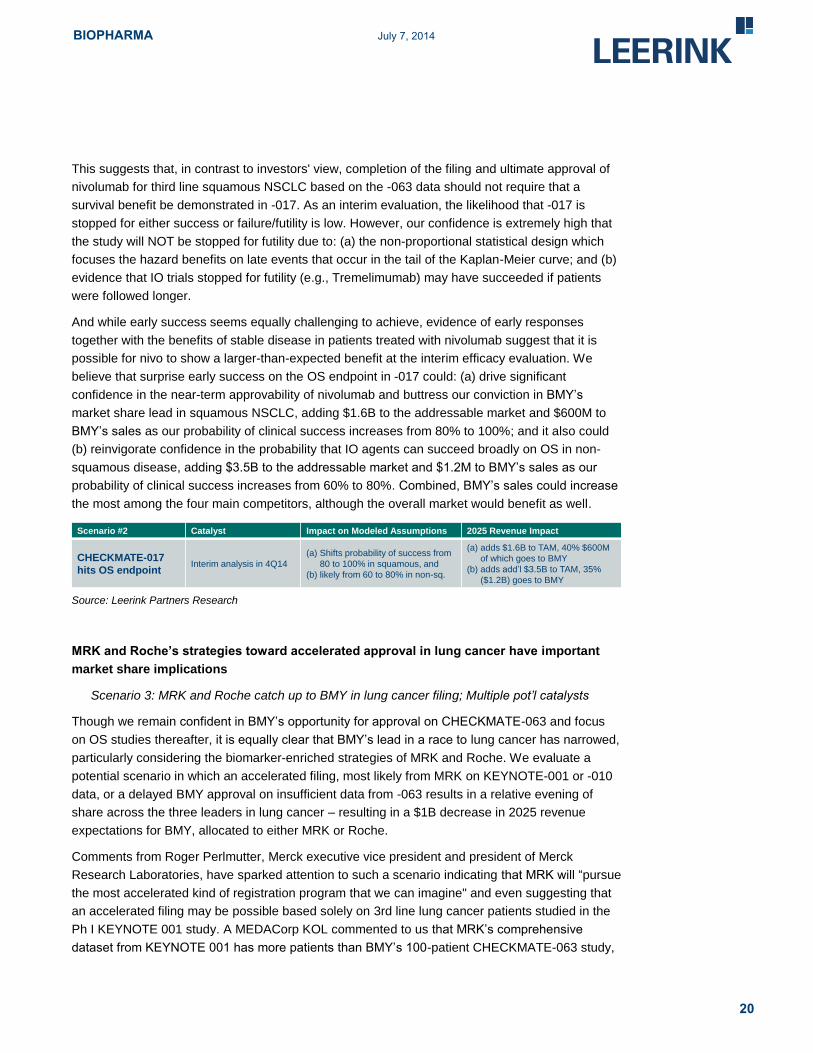

Scenario Catalyst Impact on Modeled Assumptions 2025 Revenue Impact

#1 PDL1 more

combinable in lung

cancer

PDL1 + CTLA4 data at

ESMO

Shifts backbone share to 60% PDL1

in lung cancer, reversing the current

assumption

Most marked negative impact on

BMY nearly $2B in lost revenues

attributed to Roche and AZN

#2 CHECKMATE-017

hits OS endpointInterim analysis in 4Q14

(a) Shifts probability of success from

80 to 100% in squamous, and

(b) likely from 60 to 80% in non-sq.

(a) adds $1.6B to TAM, 40% $600M

of which goes to BMY

(b) adds add’l $3.5B to TAM, 35%

($1.2B) goes to BMY

#3 MRK and Roche

catch up to BMY in

lung cancer filing

Examples: KEYNOTE-

001 filable with 3rd line

data; FIR filable for PDL1

Tier 2/3; KEYNOTE-010

filable on RR rate data in

PDL1 +; BMY delayed on

insufficient -063 data

Evens out share across 3 leaders in

lung cancer

$1B in lost BMY lung cancer

revenues attributed evenly to MRK

and Roche

#4 Strong Roche

PDL1 + Avastin

combo data

Ph Ib data at ESMO/

ASCO GU (9/14 primary

completion)

(a) Increases Roche share in RCC to

30%, drop BMY to 50%

(b) Adds CRC (30% probability of

success) with Roche share at

40% based on early lead

(a) $600M in revenue from BMY to

Roche

(b) Adds add’l $1.6B to TAM (70/30

CRC v. liver), 40% ($650M) goes

to Roche

#5 Strong PD1 liquid

tumor dataFL, DLBCL, Hodgkin’s

data at ASH

Argues for 3x increase in the level of

addressable unmet need from 15%

to 45% in lymphomas; Increases

probability of success (up to 60%) in

DLBCL and FL; Increase BMY

shares in DLBCL and FL to 40%

based on early lead

Adds $1B to TAM, $475M goes to

BMY

18

BIOPHARMA July 7, 2014

LUNG FILING DATA & COMBO-CONTROVERSIES WITH KEY IO RACE IMPLICATIONS

Combinability in lung cancer will be critical to “big four” market shares; AZN data at ESMO

an early potential catalyst

Scenario 1: PDL1 more combinable in lung cancer; Catalyst: PDL1 + CTLA4 data at ESMO

Given the attention that combinability of PD1 vs. PDL1 antibodies received at ASCO 2014, we

expect this to be a continued topic of interest, with companies eager to present updated data as

soon as possible. Operating on the offensive to try to establish a superior safety and/or efficacy

profile with the MEDI4736 + tremelimumab combination than BMY’s nivolumab + Yervoy combo,

AZN plans to show updated data from its Ph I trial at ESMO. All eyes likely will be on the

frequency of grade 3/4 toxicity as AZN continues to dose escalate patient numbers and exposure

expands. BMY also has confirmed that it will also be presenting the 1+1 mpk nivo + Yervoy arm

(started in October 2013) in 2H14, providing an important but admittedly dangerous opportunity for

cross-trial comparisons. Both companies have announced plans to initiate Phase III studies of

their respective PD1/PDL1 + CTLA4 combinations in 2H14. As with ASCO (regarding both lung

and renal safety data), we believe KOLs’ first blush reactions regarding the comparative toxicity

may have significant weight in shifting longer-term market expectations.

We currently attribute a significant market share advantage to PD1 players BMY and MRK (60%)

versus PDL1 competitors Roche and AZN (40%) based largely on BMY’s expected lead in

bringing the backbone therapy to market. However, the emergence of PDL1 antibody therapy as a

backbone therapy of choice for lung cancer combinations could trump the assumed first-in-class

advantage and flip our market share expectations for the class – with 60% attributed to PDL1s vs

40% to PD1s. The most marked negative impact would be for BMY where a significant reduction

to its market-leading share in lung cancer would result in a $2B reduction in 2025 nivolumab

revenues. AZN would be the biggest gainer, moving from an expected 15% market share in non-

squamous NSCLC to 30% (additional $1.5B in modeled 2025 revenues). This outcome would

have substantial positive implications for Roche and negative implications for MRK as well, with

potential $350-750M revenue swings given class expectations.

Source: Leerink Partners Research

Interim CHECKMATE-017 less binary than a final analysis, offering better risk/reward for an

upside surprise

Scenario 2: CHECKMATE-017 hits OS endpoint; Catalyst: Interim analysis in 4Q14E

With a rolling filing ongoing in 3rd

line squamous NSCLC based on CHECKMATE-063, we

continue to expect BMY to retain its leadership position in squamous NSCLC. It is our

understanding that the interim evaluation of CHECKMATE-017 will not be required for the 3rd

line

filing and the -063 study will stand on its own. That said, we believe the risk/reward of this interim

look is skewed positively, and BMY expects the events necessary for the company to take the

formal planned look before YE14.

Scenario #1 Catalyst Impact on Modeled Assumptions 2025 Revenue Impact

PDL1 more

combinable in lung

cancer

PDL1 + CTLA4 data at

ESMO

Shifts backbone share to 60% PDL1

in lung cancer, reversing the current

assumption

Most marked negative impact on

BMY nearly $2B in lost revenues

attributed to Roche and AZN

19

BIOPHARMA July 7, 2014

This suggests that, in contrast to investors' view, completion of the filing and ultimate approval of

nivolumab for third line squamous NSCLC based on the -063 data should not require that a

survival benefit be demonstrated in -017. As an interim evaluation, the likelihood that -017 is

stopped for either success or failure/futility is low. However, our confidence is extremely high that

the study will NOT be stopped for futility due to: (a) the non-proportional statistical design which

focuses the hazard benefits on late events that occur in the tail of the Kaplan-Meier curve; and (b)

evidence that IO trials stopped for futility (e.g., Tremelimumab) may have succeeded if patients

were followed longer.

And while early success seems equally challenging to achieve, evidence of early responses

together with the benefits of stable disease in patients treated with nivolumab suggest that it is

possible for nivo to show a larger-than-expected benefit at the interim efficacy evaluation. We

believe that surprise early success on the OS endpoint in -017 could: (a) drive significant

confidence in the near-term approvability of nivolumab and buttress our conviction in BMY’s

market share lead in squamous NSCLC, adding $1.6B to the addressable market and $600M to

BMY’s sales as our probability of clinical success increases from 80% to 100%; and it also could

(b) reinvigorate confidence in the probability that IO agents can succeed broadly on OS in non-

squamous disease, adding $3.5B to the addressable market and $1.2M to BMY’s sales as our

probability of clinical success increases from 60% to 80%. Combined, BMY’s sales could increase

the most among the four main competitors, although the overall market would benefit as well.

Source: Leerink Partners Research

MRK and Roche‟s strategies toward accelerated approval in lung cancer have important

market share implications

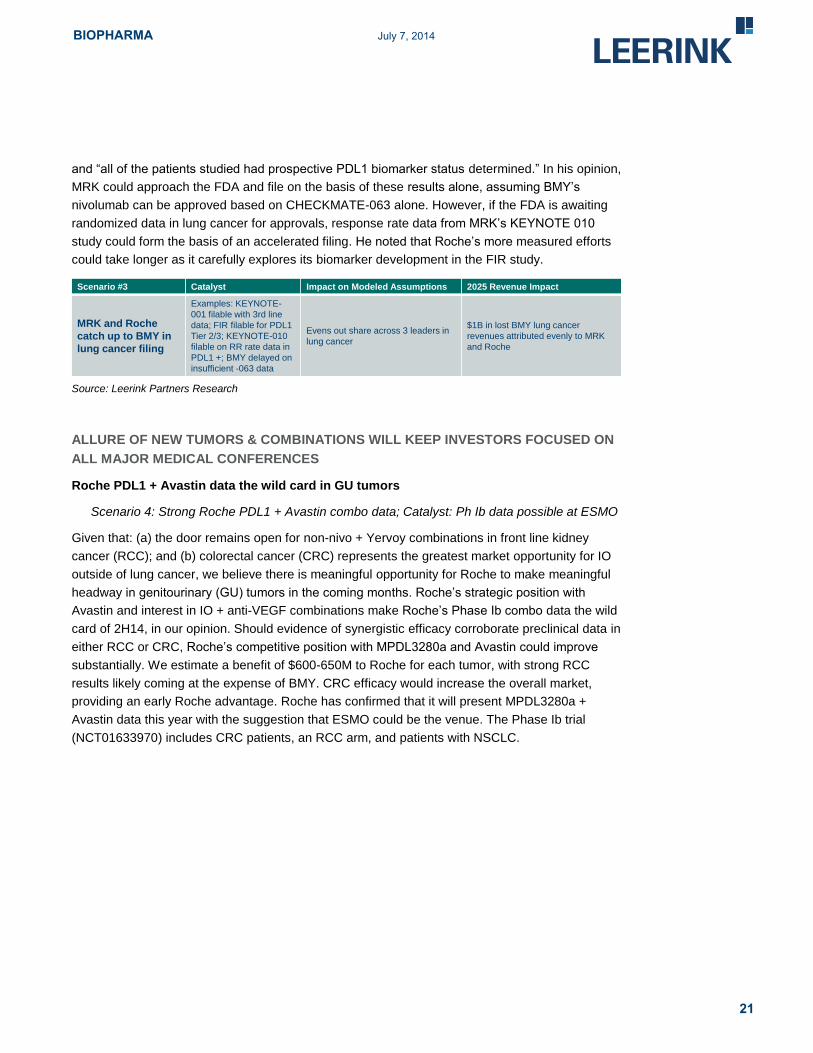

Scenario 3: MRK and Roche catch up to BMY in lung cancer filing; Multiple pot’l catalysts

Though we remain confident in BMY’s opportunity for approval on CHECKMATE-063 and focus

on OS studies thereafter, it is equally clear that BMY’s lead in a race to lung cancer has narrowed,

particularly considering the biomarker-enriched strategies of MRK and Roche. We evaluate a

potential scenario in which an accelerated filing, most likely from MRK on KEYNOTE-001 or -010

data, or a delayed BMY approval on insufficient data from -063 results in a relative evening of

share across the three leaders in lung cancer – resulting in a $1B decrease in 2025 revenue

expectations for BMY, allocated to either MRK or Roche.

Comments from Roger Perlmutter, Merck executive vice president and president of Merck

Research Laboratories, have sparked attention to such a scenario indicating that MRK will “pursue

the most accelerated kind of registration program that we can imagine" and even suggesting that

an accelerated filing may be possible based solely on 3rd line lung cancer patients studied in the

Ph I KEYNOTE 001 study. A MEDACorp KOL commented to us that MRK’s comprehensive

dataset from KEYNOTE 001 has more patients than BMY’s 100-patient CHECKMATE-063 study,

CHECKMATE-017

hits OS endpointInterim analysis in 4Q14

(a) Shifts probability of success from

80 to 100% in squamous, and

(b) likely from 60 to 80% in non-sq.

(a) adds $1.6B to TAM, 40% $600M

of which goes to BMY

(b) adds add’l $3.5B to TAM, 35%

($1.2B) goes to BMY

Scenario #2 Catalyst Impact on Modeled Assumptions 2025 Revenue Impact

20

BIOPHARMA July 7, 2014

and “all of the patients studied had prospective PDL1 biomarker status determined.” In his opinion,

MRK could approach the FDA and file on the basis of these results alone, assuming BMY’s

nivolumab can be approved based on CHECKMATE-063 alone. However, if the FDA is awaiting

randomized data in lung cancer for approvals, response rate data from MRK’s KEYNOTE 010

study could form the basis of an accelerated filing. He noted that Roche’s more measured efforts

could take longer as it carefully explores its biomarker development in the FIR study.

Source: Leerink Partners Research

ALLURE OF NEW TUMORS & COMBINATIONS WILL KEEP INVESTORS FOCUSED ON

ALL MAJOR MEDICAL CONFERENCES

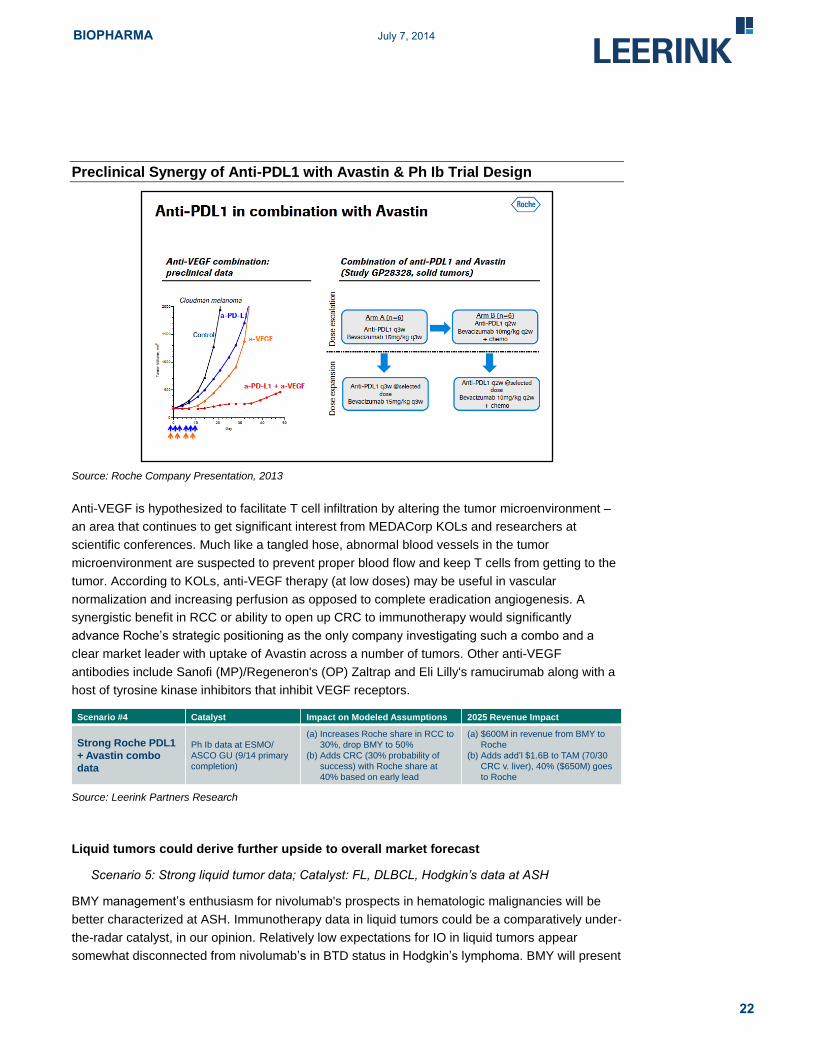

Roche PDL1 + Avastin data the wild card in GU tumors

Scenario 4: Strong Roche PDL1 + Avastin combo data; Catalyst: Ph Ib data possible at ESMO

Given that: (a) the door remains open for non-nivo + Yervoy combinations in front line kidney

cancer (RCC); and (b) colorectal cancer (CRC) represents the greatest market opportunity for IO

outside of lung cancer, we believe there is meaningful opportunity for Roche to make meaningful

headway in genitourinary (GU) tumors in the coming months. Roche’s strategic position with

Avastin and interest in IO + anti-VEGF combinations make Roche’s Phase Ib combo data the wild

card of 2H14, in our opinion. Should evidence of synergistic efficacy corroborate preclinical data in

either RCC or CRC, Roche’s competitive position with MPDL3280a and Avastin could improve

substantially. We estimate a benefit of $600-650M to Roche for each tumor, with strong RCC

results likely coming at the expense of BMY. CRC efficacy would increase the overall market,

providing an early Roche advantage. Roche has confirmed that it will present MPDL3280a +

Avastin data this year with the suggestion that ESMO could be the venue. The Phase Ib trial

(NCT01633970) includes CRC patients, an RCC arm, and patients with NSCLC.

MRK and Roche

catch up to BMY in

lung cancer filing

Examples: KEYNOTE-

001 filable with 3rd line

data; FIR filable for PDL1

Tier 2/3; KEYNOTE-010

filable on RR rate data in

PDL1 +; BMY delayed on

insufficient -063 data

Evens out share across 3 leaders in

lung cancer

$1B in lost BMY lung cancer

revenues attributed evenly to MRK

and Roche

Scenario #3 Catalyst Impact on Modeled Assumptions 2025 Revenue Impact

21

BIOPHARMA July 7, 2014

Preclinical Synergy of Anti-PDL1 with Avastin & Ph Ib Trial Design

Source: Roche Company Presentation, 2013

Anti-VEGF is hypothesized to facilitate T cell infiltration by altering the tumor microenvironment –

an area that continues to get significant interest from MEDACorp KOLs and researchers at

scientific conferences. Much like a tangled hose, abnormal blood vessels in the tumor

microenvironment are suspected to prevent proper blood flow and keep T cells from getting to the

tumor. According to KOLs, anti-VEGF therapy (at low doses) may be useful in vascular

normalization and increasing perfusion as opposed to complete eradication angiogenesis. A

synergistic benefit in RCC or ability to open up CRC to immunotherapy would significantly

advance Roche’s strategic positioning as the only company investigating such a combo and a

clear market leader with uptake of Avastin across a number of tumors. Other anti-VEGF

antibodies include Sanofi (MP)/Regeneron's (OP) Zaltrap and Eli Lilly's ramucirumab along with a

host of tyrosine kinase inhibitors that inhibit VEGF receptors.

Source: Leerink Partners Research

Liquid tumors could derive further upside to overall market forecast

Scenario 5: Strong liquid tumor data; Catalyst: FL, DLBCL, Hodgkin’s data at ASH

BMY management’s enthusiasm for nivolumab's prospects in hematologic malignancies will be

better characterized at ASH. Immunotherapy data in liquid tumors could be a comparatively under-

the-radar catalyst, in our opinion. Relatively low expectations for IO in liquid tumors appear

somewhat disconnected from nivolumab’s in BTD status in Hodgkin’s lymphoma. BMY will present

Strong Roche PDL1

+ Avastin combo

data

Ph Ib data at ESMO/

ASCO GU (9/14 primary

completion)

(a) Increases Roche share in RCC to

30%, drop BMY to 50%

(b) Adds CRC (30% probability of

success) with Roche share at

40% based on early lead

(a) $600M in revenue from BMY to

Roche

(b) Adds add’l $1.6B to TAM (70/30

CRC v. liver), 40% ($650M) goes

to Roche

Scenario #4 Catalyst Impact on Modeled Assumptions 2025 Revenue Impact

22

BIOPHARMA July 7, 2014

data at ASH in FL, DLBCL, and Hodgkin’s lymphoma. Much of what limits our forecasted market

opportunity in liquid tumors is a significant reduction in the addressable market based on the

unmet need by tumor. We apply no “unmet need” correction (i.e., unmet need population = 100%)

to melanoma, squamous NSCLC, or bladder cancer given the disease severity, currently available

treatments, and additional promise of IO. In liquid tumors we reduce the addressable patient pool

by 85%, setting the “unmet need” population at just 15% based on the robust standards of care in

lymphoma, leukemia, and myeloma with Rituxan, Tasigna, and Sprycel, not to mention more novel

Rituxan + regimens, Imbruvica, and idelalisib.

Nonetheless, we believe strong and durable PD1 data in liquid tumors could re-set expectations

regarding the unmet need addressable with immunotherapy in liquid tumors and substantially

increase the TAM, with a $1B swing in forecasted expectations not out of the question coming out

of ASH 2014. Though PD1 monotherapy may not be the ultimate therapy of choice in hematologic

malignancies, impressive and durable responses could re-invigorate interest in other IO

combinations which KOLs have previously touted. For example, the ability for CD137 (aka 4-1BB)

to activate NK cells and enhance ADCC in combination ADCC-promoting Rituxan, a combo

currently being investigated by both BMY and MRK / PFE, should be closely watched.

Source: Leerink Partners Research

ACCELERATION INTO FURTHER TUMORS & 2015 IO COMBINATION DATA

PRESENTATIONS COULD MAKE 2014 MOOT

With (1) expansion into other non-modeled tumors realistic if not inevitable and (2) the promise of

additional IO combinations not expected to unveil until later in 2015, there is the possibility that

additional catalysts will ultimately make the near-term lung cancer story and incremental tumor

developments moot. Early 2014 served as an example of this, where acceleration in bladder

cancer (with a BTD) and H+N cancer (with numerous Ph III starts) dwarfed other developments. In

particular we highlight: (a) Roche’s announced plans to present data in an additional new tumor

before YE14, and (b) that heavily anticipated combo studies with anti-LAG3 and IPH.FP’s (OP)

anti-KIR antibody may be available in house to BMY in late '14/early '15. In recent meetings with

BMY, management noted that while it plans to hold new combination data “very close to the vest,”

advancement of its combination programs could occur sooner and would be revealed via

announced studies on clinicaltrials.gov.

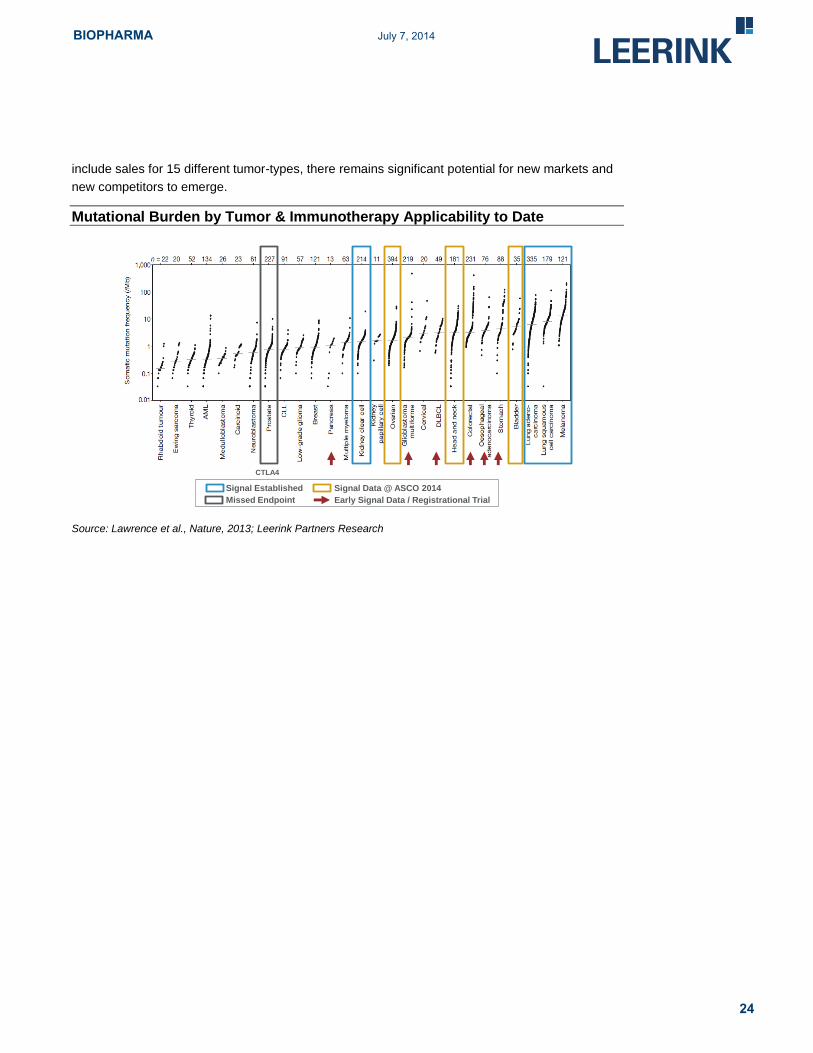

As we look to additional tumors that could be opened up, a look at the heavily cited tumor

mutation burden chart from Lawrence together with evidence that PD1/PDL1 agents may impact

virally induced tumors (e.g., MRK’s H+N data) draws our focus to cervical cancer. With companies

pursuing signal detection studies in all 23 tumors included in our model, of which we currently

Strong PD1 liquid

tumor dataFL, DLBCL, Hodgkin’s

data at ASH

Argues for 3x increase in the level of

addressable unmet need from 15%

to 45% in lymphomas; Increases

probability of success (up to 60%) in

DLBCL and FL; Increase BMY

shares in DLBCL and FL to 40%

based on early lead

Adds $1B to TAM, $475M goes to

BMY

Scenario #5 Catalyst Impact on Modeled Assumptions 2025 Revenue Impact

23

BIOPHARMA July 7, 2014

include sales for 15 different tumor-types, there remains significant potential for new markets and

new competitors to emerge.

Mutational Burden by Tumor & Immunotherapy Applicability to Date

Source: Lawrence et al., Nature, 2013; Leerink Partners Research

CTLA4

Signal Established

Missed Endpoint

Signal Data @ ASCO 2014

Early Signal Data / Registrational Trial

24

BIOPHARMA July 7, 2014

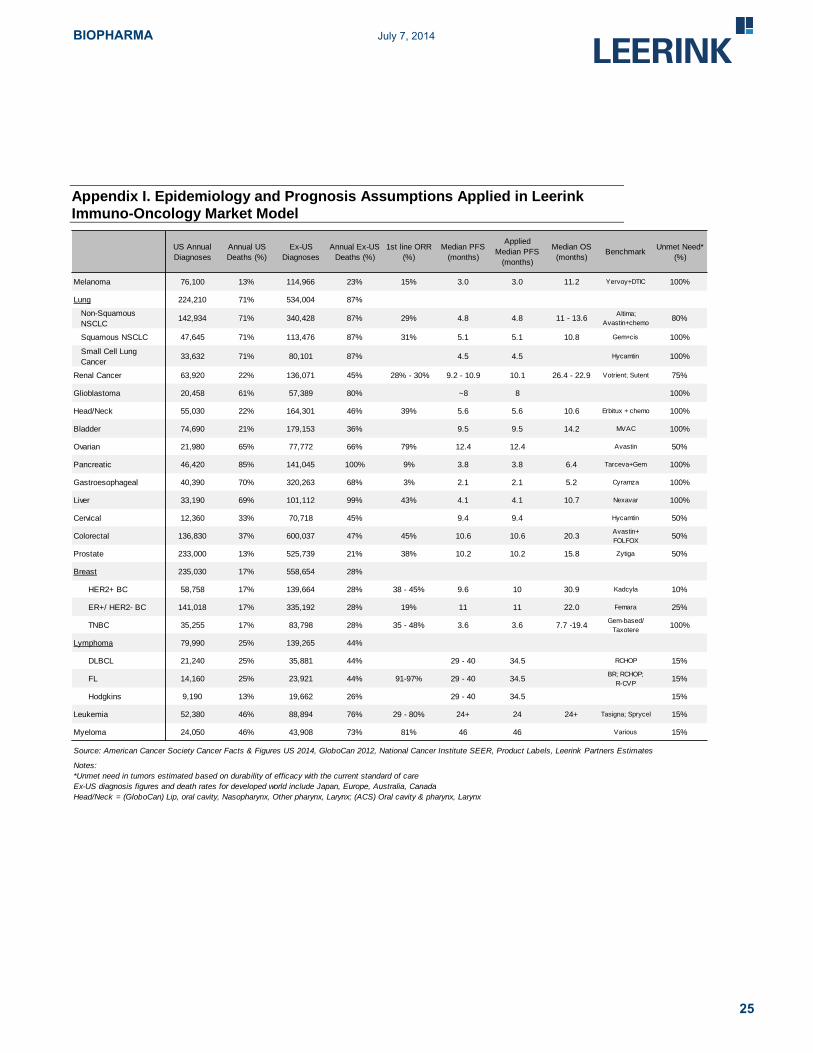

Appendix I. Epidemiology and Prognosis Assumptions Applied in Leerink

Immuno-Oncology Market Model

US Annual

Diagnoses

Annual US

Deaths (%)

Ex-US

Diagnoses

Annual Ex-US

Deaths (%)

1st line ORR

(%)

Median PFS

(months)

Applied

Median PFS

(months)

Median OS

(months)Benchmark

Unmet Need*

(%)

Melanoma 76,100 13% 114,966 23% 15% 3.0 3.0 11.2 Yervoy+DTIC 100%

Lung 224,210 71% 534,004 87%

Non-Squamous

NSCLC142,934 71% 340,428 87% 29% 4.8 4.8 11 - 13.6

Altima;

Avastin+chemo80%

Squamous NSCLC 47,645 71% 113,476 87% 31% 5.1 5.1 10.8 Gem+cis 100%

Small Cell Lung

Cancer33,632 71% 80,101 87% 4.5 4.5 Hycamtin 100%

Renal Cancer 63,920 22% 136,071 45% 28% - 30% 9.2 - 10.9 10.1 26.4 - 22.9 Votrient; Sutent 75%

Glioblastoma 20,458 61% 57,389 80% ~8 8 100%

Head/Neck 55,030 22% 164,301 46% 39% 5.6 5.6 10.6 Erbitux + chemo 100%

Bladder 74,690 21% 179,153 36% 9.5 9.5 14.2 MVAC 100%

Ovarian 21,980 65% 77,772 66% 79% 12.4 12.4 Avastin 50%

Pancreatic 46,420 85% 141,045 100% 9% 3.8 3.8 6.4 Tarceva+Gem 100%

Gastroesophageal 40,390 70% 320,263 68% 3% 2.1 2.1 5.2 Cyramza 100%

Liver 33,190 69% 101,112 99% 43% 4.1 4.1 10.7 Nexavar 100%

Cervical 12,360 33% 70,718 45% 9.4 9.4 Hycamtin 50%

Colorectal 136,830 37% 600,037 47% 45% 10.6 10.6 20.3Avastin+

FOLFOX50%

Prostate 233,000 13% 525,739 21% 38% 10.2 10.2 15.8 Zytiga 50%

Breast 235,030 17% 558,654 28%

HER2+ BC 58,758 17% 139,664 28% 38 - 45% 9.6 10 30.9 Kadcyla 10%

ER+/ HER2- BC 141,018 17% 335,192 28% 19% 11 11 22.0 Femara 25%

TNBC 35,255 17% 83,798 28% 35 - 48% 3.6 3.6 7.7 -19.4Gem-based/

Taxotere100%

Lymphoma 79,990 25% 139,265 44%

DLBCL 21,240 25% 35,881 44% 29 - 40 34.5 RCHOP 15%

FL 14,160 25% 23,921 44% 91-97% 29 - 40 34.5BR; RCHOP;

R-CVP15%

Hodgkins 9,190 13% 19,662 26% 29 - 40 34.5 15%

Leukemia 52,380 46% 88,894 76% 29 - 80% 24+ 24 24+ Tasigna; Sprycel 15%

Myeloma 24,050 46% 43,908 73% 81% 46 46 Various 15%

Source: American Cancer Society Cancer Facts & Figures US 2014, GloboCan 2012, National Cancer Institute SEER, Product Labels, Leerink Partners Estimates

Notes:

*Unmet need in tumors estimated based on durability of efficacy with the current standard of care

Ex-US diagnosis figures and death rates for developed world include Japan, Europe, Australia, Canada

Head/Neck = (GloboCan) Lip, oral cavity, Nasopharynx, Other pharynx, Larynx; (ACS) Oral cavity & pharynx, Larynx

25

BIOPHARMA July 7, 2014

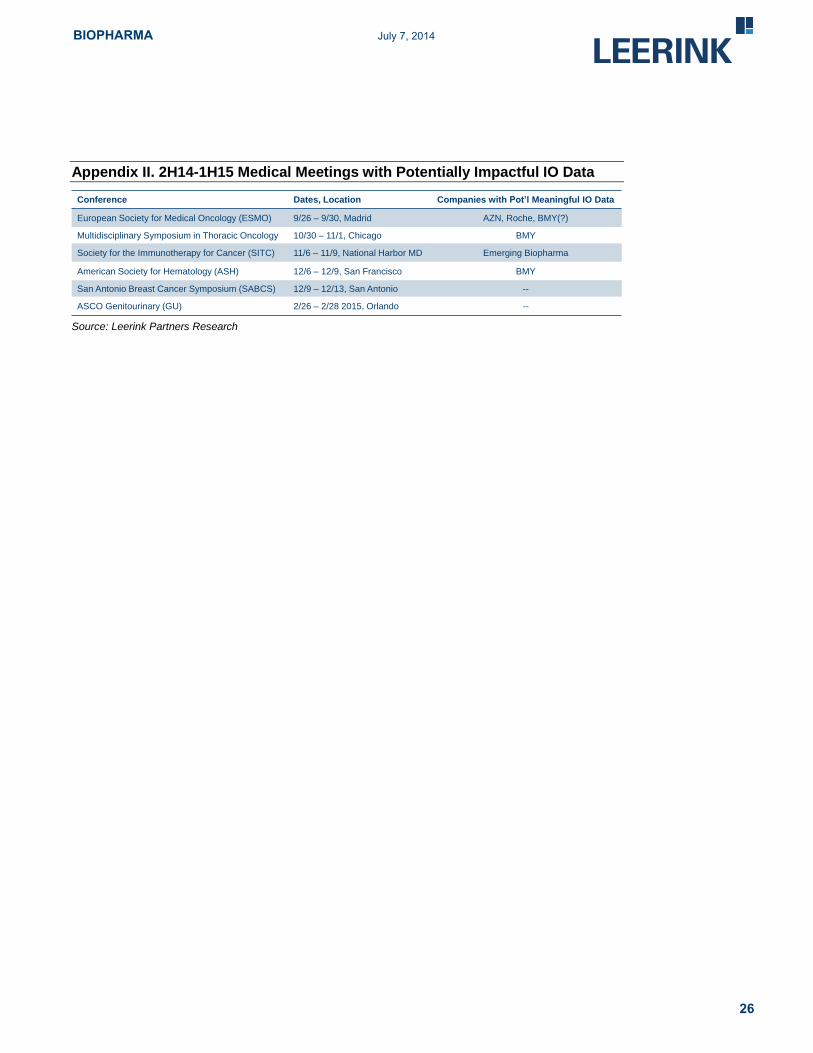

Appendix II. 2H14-1H15 Medical Meetings with Potentially Impactful IO Data

Source: Leerink Partners Research

Conference Dates, Location Companies with Pot‟l Meaningful IO Data

European Society for Medical Oncology (ESMO) 9/26 – 9/30, Madrid AZN, Roche, BMY(?)

Multidisciplinary Symposium in Thoracic Oncology 10/30 – 11/1, Chicago BMY

Society for the Immunotherapy for Cancer (SITC) 11/6 – 11/9, National Harbor MD Emerging Biopharma

American Society for Hematology (ASH) 12/6 – 12/9, San Francisco BMY

San Antonio Breast Cancer Symposium (SABCS) 12/9 – 12/13, San Antonio --

ASCO Genitourinary (GU) 2/26 – 2/28 2015, Orlando --

26

BIOPHARMA July 7, 2014

BIOPHARMA July 7, 2014

Disclosures AppendixAnalyst CertificationI, Seamus Fernandez, certify that the views expressed in this report accurately reflect my views and that no part of mycompensation was, is, or will be directly related to the specific recommendation or views contained in this report.

I, Howard Liang, Ph.D., certify that the views expressed in this report accurately reflect my views and that no part ofmy compensation was, is, or will be directly related to the specific recommendation or views contained in this report.

I, Michael Schmidt, Ph.D., certify that the views expressed in this report accurately reflect my views and that no part ofmy compensation was, is, or will be directly related to the specific recommendation or views contained in this report.

27

BIOPHARMA July 7, 2014

Distribution of Ratings/Investment Banking Services (IB) as of 03/31/14IB Serv./Past 12

Mos.Rating Count Percent Count PercentBUY [OP] 131 68.23 46 35.11HOLD [MP] 61 31.77 3 4.92SELL [UP] 0 0.00 0 0.00

Explanation of RatingsOutperform (Buy): We expect this stock to outperform its benchmark over the next 12 months.

Market Perform (Hold/Neutral): We expect this stock to perform in line with its benchmark over the next 12months.

Underperform (Sell): We expect this stock to underperform its benchmark over the next 12 months.The degreeof outperformance or underperformance required to warrant an Outperform or an Underperform rating shouldbe commensurate with the risk profile of the company.

For the purposes of these definitions the relevant benchmark will be the S&P 600® Health Care Index forissuers with a market capitalization of less than $2 billion and the S&P 500® Health Care Index for issuers witha market capitalization over $2 billion.

28

BIOPHARMA July 7, 2014

Important DisclosuresThis information (including, but not limited to, prices, quotes and statistics) has been obtained from sourcesthat we believe reliable, but we do not represent that it is accurate or complete and it should not be reliedupon as such. All information is subject to change without notice. This is provided for information purposesonly and should not be regarded as an offer to sell or as a solicitation of an offer to buy any product to whichthis information relates. The Firm, its officers, directors, employees, proprietary accounts and affiliates mayhave a position, long or short, in the securities referred to in this report, and/or other related securities, andfrom time to time may increase or decrease the position or express a view that is contrary to that containedin this report. The Firm's salespeople, traders and other professionals may provide oral or written marketcommentary or trading strategies that are contrary to opinions expressed in this report. The Firm's proprietaryaccounts may make investment decisions that are inconsistent with the opinions expressed in this report.The past performance of securities does not guarantee or predict future performance. Transaction strategiesdescribed herein may not be suitable for all investors. Additional information is available upon request bycontacting the Editorial Department at One Federal Street, 37th Floor, Boston, MA 02110.

Like all Firm employees, analysts receive compensation that is impacted by, among other factors, overall firmprofitability, which includes revenues from, among other business units, Institutional Equities, and InvestmentBanking. Analysts, however, are not compensated for a specific investment banking services transaction.

MEDACorp is a network of healthcare professionals, attorneys, physicians, key opinion leaders and otherspecialists accessed by Leerink and it provides information used by its analysts in preparing research.

For price charts, statements of valuation and risk, as well as the specific disclosures for covered companies,client should refer to https://leerink2.bluematrix.com/bluematrix/Disclosure2 or send a request to LeerinkPartners Editorial Department, One Federal Street, 37th Floor, Boston, MA 02110.

©2014 Leerink Partners LLC. All rights reserved. This document may not be reproduced or circulated withoutour written authority.

29

Leerink Partners LLC Equity Research

Director of Equity Research John L. Sullivan, CFA (617) 918-4875 [email protected]

Associate Director of Research Alice C. Avanian, CFA (617) 918-4544 [email protected]

Healthcare Strategy John L. Sullivan, CFA (617) 918-4875 [email protected]

Alice C. Avanian, CFA (617) 918-4544 [email protected]

Biotechnology Howard Liang, Ph.D. (617) 918-4857 [email protected]

Joseph P. Schwartz (617) 918-4575 [email protected]

Marko Kozul, M.D. (415) 905-7221 [email protected]

Michael Schmidt, Ph.D. (617) 918-4588 [email protected]

Gena Wang, Ph.D., CFA (212) 277-6073 [email protected]

Jonathan Chang, Ph.D. (617) 918-4015 [email protected]

Paul Matteis (617) 918-4585 [email protected]

Richard Goss (617) 918-4059 [email protected]

Life Science Tools Dan Leonard (212) 277-6116 [email protected]

and Diagnostics Justin Bowers, CFA (212) 277-6066 [email protected]

Pharmaceuticals/Major Seamus Fernandez (617) 918-4011 [email protected]

Ario Arabi (617) 918-4568 [email protected]

Aneesh Kapur (617) 918-4576 [email protected]

Specialty Pharmaceuticals

Jason M. Gerberry, JD

(617) 918-4549

Medical Devices, Cardiology Danielle Antalffy (212) 277-6044 [email protected]

Puneet Souda (212) 277-6091 [email protected]

& Orthopedics Richard Newitter (212) 277-6088 [email protected]

Ravi Misra (212) 277-6049 [email protected]

Healthcare Services Ana Gupte, Ph.D. (212) 277-6040 [email protected]

Healthcare Technology David Larsen, CFA (617) 918-4502 [email protected]

& Distribution Christopher Abbott (617) 918-4010 [email protected]

Sr. Editor/Supervisory Analyst Mary Ellen Eagan, CFA (617) 918-4837 [email protected]

Supervisory Analysts Robert Egan [email protected]

Amy N. Sonne [email protected]

Editorial Cristina Diaz-Dickson (617) 918-4548 [email protected]

Research Assistant Carmen Augustine (212) 277-6012 [email protected]

New York 299 Park Avenue, 21st floor New York, NY 10171 (888) 778-1653

Boston One Federal Street, 37th Floor

Boston, MA 02110 (800) 808-7525

San Francisco 201 Spear Street, 16th Floor

San Francisco, CA 94105 (800) 778-1164