Embed Size (px)

Citation preview

Time Event Estimate Date Act.vs. Est. S&P

8:30 Non Farm Payrolls 165 1/4 128 3.43

8:30 Unemployment Rate 3.9 1/4 0.2 3.43

8:30 Avg Hourly Earnings 0.3 1/4 0.1 3.43

8:30 Avg Weekly Hours 34.5 1/4 0.0 3.43

10:00 ISM Manufact. 54.0 1/3 -3.4 -2.48

10:00 Michigan Sentiment 90.7 1/18 -6.1 1.32

Last Report

Time Event Estimate Date Est Act. Diff. S&P Best Worst

8:30 ECI 0.8 10/31 0.7 0.8 0.1 1.09 Tech Util

8:30 Initial Claims 215 1/24 218 199 -2 0.14 Tech C St.

8:30 Continuing Claims 1720 1/24 1730 1713 -2 0.14 Tech C St.

9:45 Chicago PMI 61.5 12/28 60.2 65.4 -1.7 -0.12 C Disc Ener

10:30 EIA Natural Gas Inventories

Last Report

Upgrades

Ticker Firm From To

ES Goldman Neutral Buy

HP Merrill Neutral Buy

OSK Merrill Neutral Buy

PFE Credit Suisse Neutral Outperf

SMG JP Morgan Underwgt Neutral

TROW Evercore Inline Outperf

Downgrades

Ticker Firm From To

AGN Credit Suisse Outperf Neutral

HRB Goldman Neutral Sell

IVZ Barclays Overwgt Mkt Wgt

OUT Citigroup Buy Neutral

SITE RBC Capital Outperf Mkt Perf

USCR SunTrust Buy Hold

Initiations/Reiterations

Ticker Firm Action Rating

BABA Ray James Reiterated Outperf

BILI Citigroup Initiated Buy

ICPT Credit Suisse Initiated Outperf

NOW BMO Capital Reiterated Outperf

WDAY Wlm Blair Reiterated Outperf

WYNN Telsey Reiterated Mkt Perf

- Gold Rallies to Highest Level Since Last May.

- US equity Futures Modestly Lower Following Wednesday FOMC Rally.

- Trump Will Reportedly Meet With China's Xi in Late February.

h 1.1 %

h 0.3

i -0.1

h 0.5

Oil 54.16 i -$0.1

Gold 1322.8 h $12.9

$/Euro 0.870 i 0.00

$/Yen 108.66 i -0.4

10-Yr 2.67 i -0.01

Japan

China

Germany

UK

Trading Up ($):

AMZN (33.07), CHTR (21.43), FB (17.21), NOW (16.5), WDAY (8.18), MLNX (5.66)

Trading Down ($):

TSLA (-13.27), RTN (-5.46), DWDP (-5.27), NOC (-4.82), PYPL (-4.19), DATA (-4.17)-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

16:00 18:00 20:00 22:00 0:00 2:00 4:00 6:00

Pe

rce

nt

Ch

ange

Asia Opens

Europe Opens

Today’s Events

Stock Specific News of Note

Noteworthy Macro EventsOther MarketsOvernight Trading

Tomorrow

Overnight Trading

Analyst Actions

Indicators/EventsMarket Timing Model

© Copyright 2019, Bespoke Investment Group, LLC. The information herein was obtained fromsources which Bespoke Investment Group, LLC believes to be reliable, but we do not guarantee itsaccuracy. Neither the information, nor any opinions expressed, constitute a solicitation of thepurchase or sale of any securities or related instruments. Bespoke Investment Group, LLC is notresponsible for any losses incurred from any use of this information.

Earnings Reports

Ticker Date TOD EPS Revs.

AON 2/1/19 AM 2.13 2820

BAH 2/1/19 AM 0.59 1604

CI 2/1/19 AM 2.49 11384

CVX 2/1/19 AM 1.88 43552

D 2/1/19 AM 0.92 3273

HON 2/1/19 AM 1.89 9731

ITW 2/1/19 AM 1.82 3615

JCI 2/1/19 AM 0.25 5476

LYB 2/1/19 AM 2.30 9593

MRK 2/1/19 AM 1.03 10930

SF 2/1/19 AM 1.47 766

WY 2/1/19 AM 0.12 1711

XOM 2/1/19 AM 1.09 78939

ZBH 2/1/19 AM 2.17 2062

Estimate

9:45 Fed's Kaplan Speaks in Austin

13:00 Baker Hughes Rig Count

All day Total Vehicle Sales (17.2 mln est)

Conferences & Meetings

Economic Indicators & Events

Dividends & Splits

CZR Will replace DRQ in the S&P 400 effective 2/4.

DRQ Will replace ESND in the S&P 600 effective 2/4.

CONN Will replace ESIO in the S&P 600 effective 2/4.

Index Changes

PGR 2.51 WABC 0.40

NSC 0.86 SXT 0.36

C 0.45 PETS 0.27

BespokePremium.com

For Personal Use Only—Do Not Forward1

Ticker News

ABC Beat EPS forecasts by 9 cents (1.60 vs 1.51) on stronger revenues; raised guidance.

BC Beat EPS forecasts by 8 cents (0.98 vs 0.90) on inline revenues; lowered guidance.

BLL Missed EPS forecasts by 1 cent (0.55 vs 0.56) on stronger revenues.

DWDP Beat EPS forecasts by 1 cent (0.88 vs 0.87) on weaker revenues; lowered guidance.

FB Beat EPS forecasts by 20 cents (2.38 vs 2.18) on stronger revenues; MAUs higher than expected.

GE Missed EPS forecasts by 5 cents (0.17 vs 0.22) on stronger revenues.

MA Beat EPS forecasts by 3 cents (1.55 vs 1.52) on inline revenues.

MDC Missed EPS forecasts by 19 cents (0.95 vs 1.14) on stronger revenues.

MDLZ Reported inline EPS (0.63) on inline revenues.

MSFT Beat EPS forecasts by 1 cent (1.10 vs 1.09) on stronger revenues; lowered sales guidance.

MTH Beat EPS forecasts by 39 cents (1.91 vs 1.52) on stronger revenues.

NOC Beat EPS forecasts by 48 cents (4.93 vs 4.45) on inline revenues; lowered guidance.

NOW Beat EPS forecasts by 14 cents (0.77 vs 0.63) on inline revenues.

PYPL Beat EPS forecasts by 2 cents (0.69 vs 0.67) on inline revenues; guided inline to lower.

QCOM Beat EPS forecasts by 11 cents (1.20 vs 1.09) on inline revenues; guided to high end of range.

SHW Missed EPS forecasts by 1 cent (3.54 vs 3.55) on inline revenues; lowered guidance.

TSLA Missed EPS forecasts by 9 cents (1.93 vs 2.02) on stronger revenues.

UPS Beat EPS forecasts by 3 cents (1.94 vs 1.91) on inline revenues; lowered guidance.

V Beat EPS forecasts by 5 cents (1.30 vs 1.25) on stronger revenues; reaffirmed guidance.

WYNN Missed EPS forecasts by 29 cents (1.06 vs 1.35) on stronger revenues.

Bearish Bullish

Category One Week Two Weeks One Month

Sentiment 0.05 0.29 0.41

Technicals 0.04 0.18 0.40

Fundamental 0.13 0.13 0.46

Overall 0.05 0.18 0.42

Average (all days) 0.13 0.13 0.13

Expected S&P 500 Return (%)

Neutral

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

Jan-18 Mar-18 May-18 Jul-18 Sep-18 Nov-18 Jan-19

Bonds Outperforming Stocks

Stocks Outperforming Bonds

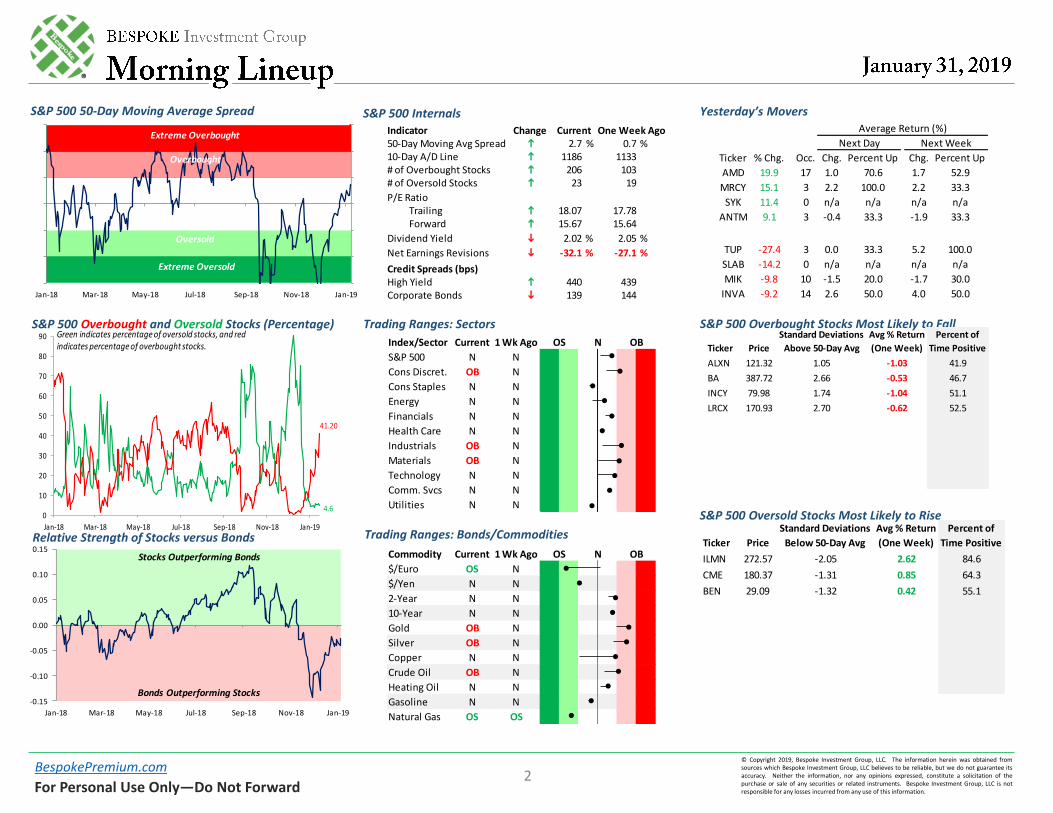

Ticker % Chg. Occ. Chg. Percent Up Chg. Percent Up

AMD 19.9 17 1.0 70.6 1.7 52.9

MRCY 15.1 3 2.2 100.0 2.2 33.3

SYK 11.4 0 n/a n/a n/a n/a

ANTM 9.1 3 -0.4 33.3 -1.9 33.3

IRDM

TUP -27.4 3 0.0 33.3 5.2 100.0

SLAB -14.2 0 n/a n/a n/a n/a

MIK -9.8 10 -1.5 20.0 -1.7 30.0

INVA -9.2 14 2.6 50.0 4.0 50.0

Average Return (%)

Next Day Next Week

Index/Sector Current 1 Wk Ago

S&P 500 N N

Cons Discret. OB N

Cons Staples N N

Energy N N

Financials N N

Health Care N N

Industrials OB N

Materials OB N

Technology N N

Comm. Svcs N N

Utilities N N

OS N OB

S&P 500 50-Day Moving Average Spread S&P 500 Internals Yesterday’s Movers

Relative Strength of Stocks versus Bonds

S&P 500 Overbought and Oversold Stocks (Percentage) Trading Ranges: Sectors

Trading Ranges: Bonds/Commodities

S&P 500 Overbought Stocks Most Likely to Fall

S&P 500 Oversold Stocks Most Likely to Rise

Jan-18 Mar-18 May-18 Jul-18 Sep-18 Nov-18 Jan-19

Extreme Overbought

Overbought

Oversold

Extreme Oversold

4.6

41.20

0

10

20

30

40

50

60

70

80

90

Jan-18 Mar-18 May-18 Jul-18 Sep-18 Nov-18 Jan-19

Green indicates percentage of oversold stocks, and red indicates percentage of overbought stocks.

Commodity Current 1 Wk Ago

$/Euro OS N

$/Yen N N

2-Year N N

10-Year N N

Gold OB N

Silver OB N

Copper N N

Crude Oil OB N

Heating Oil N N

Gasoline N N

Natural Gas OS OS

OS N OB

Indicator Change50-Day Moving Avg Spread h 2.7 % 0.7 %10-Day A/D Line h 1186 1133# of Overbought Stocks h 206 103# of Oversold Stocks h 23 19

P/E Ratio Trailing h 18.07 17.78 Forward h 15.67 15.64

Dividend Yield i 2.02 % 2.05 %

Net Earnings Revisions i -32.1 % -27.1 %

Credit Spreads (bps)High Yield h 440 439Corporate Bonds i 139 144

Current One Week Ago

© Copyright 2019, Bespoke Investment Group, LLC. The information herein was obtained fromsources which Bespoke Investment Group, LLC believes to be reliable, but we do not guarantee itsaccuracy. Neither the information, nor any opinions expressed, constitute a solicitation of thepurchase or sale of any securities or related instruments. Bespoke Investment Group, LLC is notresponsible for any losses incurred from any use of this information.

BespokePremium.com

For Personal Use Only—Do Not Forward2

Ticker Price

ALXN 121.32 1.05 -1.03 41.9

BA 387.72 2.66 -0.53 46.7

INCY 79.98 1.74 -1.04 51.1

LRCX 170.93 2.70 -0.62 52.5

Standard Deviations

Above 50-Day Avg

Avg % Return

(One Week)

Percent of

Time Positive

Ticker Price

ILMN 272.57 -2.05 2.62 84.6

CME 180.37 -1.31 0.85 64.3

BEN 29.09 -1.32 0.42 55.1

Standard Deviations

Below 50-Day Avg

Avg % Return

(One Week)

Percent of

Time Positive

Gold Future: Last Six Months

Gold Front Month Future: Last 15 Trading Days

1150

1170

1190

1210

1230

1250

1270

1290

1310

1330

1350

7/31 8/28 9/26 10/24 11/21 12/20 1/22

1150

1170

1190

1210

1230

1250

1270

1290

1310

1330

1350

7/31 8/28 9/26 10/24 11/21 12/20 1/22

1282

1292

1302

1312

1322

1332

1/9 1/11 1/15 1/17 1/22 1/24 1/28 1/30

200-DMA: 1256

50-DMA: 1270

1324

S&P 500: Last Six Months

S&P 500: Last 15 Trading Days

2300

2400

2500

2600

2700

2800

2900

3000

7/30 8/27 9/25 10/23 11/20 12/20 1/22

2300

2400

2500

2600

2700

2800

2900

3000

7/30 8/27 9/25 10/23 11/20 12/20 1/22

2555

2575

2595

2615

2635

2655

2675

2695

1/9 1/11 1/15 1/17 1/22 1/24 1/28 1/30

200-DMA: 2741

50-DMA: 2610

2681

Russell 2000: Last Six Months

Russell 2000: Last 15 Trading Days

1250

1350

1450

1550

1650

1750

7/30 8/27 9/25 10/23 11/20 12/20 1/22

200-DMA: 1590

1420

1440

1460

1480

1500

1/9 1/11 1/15 1/17 1/22 1/24 1/28 1/30

50-DMA: 1437

1487

Nasdaq Composite: Last Six Months

Nasdaq Composite: Last 15 Trading Days

6150

6450

6750

7050

7350

7650

7950

8250

7/30 8/27 9/25 10/23 11/20 12/20 1/22

6100

6400

6700

7000

7300

7600

7900

8200

7/30 8/27 9/25 10/23 11/20 12/20 1/22

50-DMA: 6944

200-DMA: 7453

6850

6950

7050

7150

7250

1/9 1/11 1/15 1/17 1/22 1/24 1/28 1/30

7183

Oil Future: Last Six Months

Oil Future: Last 15 Trading Days

7/31 8/28 9/26 10/24 11/21 12/20 1/22

41.5

45.5

49.5

53.5

57.5

61.5

65.5

69.5

73.5

77.5

7/31 8/28 9/26 10/24 11/21 12/20 1/22

200-DMA: 64

50.3

51.3

52.3

53.3

54.3

55.3

1/9 1/11 1/15 1/17 1/22 1/24 1/28 1/30

50-DMA: 51

54

BBG US Dollar Index: Last Six Months

BBG US Dollar Index: Last 15 Trading Days

1150

1160

1170

1180

1190

1200

1210

1220

8/7 9/4 10/2 10/30 11/27 12/25 1/22

1150

1160

1170

1180

1190

1200

1210

1220

8/7 9/4 10/2 10/30 11/27 12/25 1/22

50-DMA: 1198

200-DMA: 1186

1176

1180

1184

1188

1192

1196

1/10 1/14 1/16 1/18 1/22 1/24 1/28 1/30

1180

© Copyright 2019, Bespoke Investment Group, LLC. The information herein was obtained fromsources which Bespoke Investment Group, LLC believes to be reliable, but we do not guarantee itsaccuracy. Neither the information, nor any opinions expressed, constitute a solicitation of thepurchase or sale of any securities or related instruments. Bespoke Investment Group, LLC is notresponsible for any losses incurred from any use of this information.

BespokePremium.com

For Personal Use Only—Do Not Forward3

DJ Transports: Last Six Months

DJ Transports: Last 15 Trading Days

8400

8900

9400

9900

10400

10900

11400

11900

7/30 8/27 9/25 10/23 11/20 12/20 1/22

8400

8900

9400

9900

10400

10900

11400

11900

7/30 8/27 9/25 10/23 11/20 12/20 1/22

200-DMA: 10574

9350

9550

9750

9950

10150

1/9 1/11 1/15 1/17 1/22 1/24 1/28 1/30

50-DMA: 9800

10079

Long Bond Future: Last Six Months

Long Bond Future Intraday: Last 15 Trading Days

134

136

138

140

142

144

146

148

150

8/2 8/30 9/28 10/26 11/26 12/26 1/25

134

136

138

140

142

144

146

148

150

8/2 8/30 9/28 10/26 11/26 12/26 1/25

200-DMA: 142

144.0

144.5

145.0

145.5

146.0

146.5

1/9 1/11 1/15 1/17 1/22 1/24 1/28 1/30

50-DMA: 144

146

For Personal Use Only—Do Not Forward

BespokePremium.com © Copyright 2019, Bespoke Investment Group, LLC. The information herein was obtained from

sources which Bespoke Investment Group, LLC believes to be reliable, but we do not guarantee its

accuracy. Neither the information, nor any opinions expressed, constitute a solicitation of the

purchase or sale of any securities or related instruments. Bespoke Investment Group, LLC is not

responsible for any losses incurred from any use of this information.

4

Overview: US equity markets are up about 20 bps headed into the open, though it should be noted

that thanks to some negative data from Europe the market is off overnight highs. The dollar is at four

month lows, UST rates continue to fall, curves are still steepening, but 2s10s has run up against re-

sistance. Commodity prices are mostly higher, while credit spreads are plunging both in the US and

Europe in response to yesterday’s dovish Fed. Gold continues to run and run hard, up four days in a

row for a total gain of 3.34%, the best since the yellow metal’s post-Brexit rally.

Yesterday, the BEA announced a partial timeline for economic data delayed by the shutdown; you can

view BEA’s here and the Census one here. It will probably be awhile before all the data is back to its

normal schedule. In the meantime, US data today includes ECI at 8:30, new home sales for November

at 10:00 AM, jobless claims (8:30), and Chicago PMI (9:45). Economic scorecard.

APAC Markets: Markets

roared higher in response to

the extremely dovish pivot by

the Fed, led by H-shares

(+1.3%) and India (+1.9%). A-

shares and Indonesia were

also up over 1%. In FX, virtual-

ly everything is up versus USD.

While AUD and NZD have the

biggest moves versus the dol-

lar since Tuesday’s close

(+1.7% and +1.2%), EM cross-

es have really broken out. In

addition, Chinese yuan is in

full blown rally mode with

USDCNH crashing below its

200-DMA in dramatic fashion

during the day yesterday.

Europe Markets: European

indices are less ecstatic this

morning than in the US with

Italy’s FTSE MIB down almost

half a percent on very large

volumes (more than double typical for this time of the session). The source of angst is Q4 GDP, which

showed the economy in recession. We’ll discuss European GDP more in the subsequent pages, but

suffice to say Italy remains a shockingly terrible grower relative to other Eurozone economies. Rates

are mostly unchanged, EURUSD is up for a 5th day running, but credit is rallying dramatically, with

iTraxx Xover (high yield) down over 12 bps in spread today thanks to the dovish Fed yesterday. It’s hard

to worry about Europe too much with that kind of credit price action!

Morning Commentary

USDCNH: Past Year

6.20

6.30

6.40

6.50

6.60

6.70

6.80

6.90

7.00

200-DMA

50-DMA

Bespoke EMFX Index (Spot)

58

60

62

64

66

68

70Equal-weight CLP, ZAR, BRL, COP, RUB, PHP,

PEN, ARS, IDR, MYR, MXN, TWD, INR, SGD, CNH, KRW, CZK, PLN, HUF, and TRY

For Personal Use Only—Do Not Forward

BespokePremium.com © Copyright 2019, Bespoke Investment Group, LLC. The information herein was obtained from

sources which Bespoke Investment Group, LLC believes to be reliable, but we do not guarantee its

accuracy. Neither the information, nor any opinions expressed, constitute a solicitation of the

purchase or sale of any securities or related instruments. Bespoke Investment Group, LLC is not

responsible for any losses incurred from any use of this information.

5

Global Data: Similar to last

night, there was a huge swath of

global data released overnight

that we will recap at length this

morning.

South Korea Leading Indicators:

For the last seven months

(ending in December), leading

indicators in South Korea have

dropped sequentially, the worst

such run since the 13 months

ended January of 2009. While a

better coincident than leading

indicator in our view, this series

has been unhappy for a long

time and continues to suggest

weak growth in Korea.

South Korea IP: Industrial pro-

duction missed by a wide margin

in South Korea with a 1.4% drop

rather than the 0.2% forecast;

manufacturing was down 1.8%

MoM in December, the worst

since September’s 2.3% drop.

The only good news—if you can

call it that—is that capacity has

been declining of late, reducing

slack as output continues its

sluggish climb higher.

Italian Sentiment: Japanese in-

dustrial production numbers

actually beat (along with hous-

ing starts) but still dropped on

the month. As shown at left, the

current sluggish pace of manu-

facturing production growth is

pretty consistent with surveys.

Morning Commentary

South Korea: Leading Indicators At New Lows Despite Q4 GDP

South Korea: Manufacturing Output Slows Once Again

Japanese Manufacturing Also Slow, As Tankan Suggests

-4

-2

0

2

4

6

8

10

12

14

16

-5

0

5

10

15

20

South Korea Leading Index YoY

South Korea GDP YoY

80

100

120

140

160

180

200

220

240

260

Production (1999 Avg = 100)

Capacity (1999 Avg = 100)

80

85

90

95

100

105

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

Tankan Business Conditions - LargeManufacturing

Japan Industrial Production(Manufacturing)

For Personal Use Only—Do Not Forward

BespokePremium.com © Copyright 2019, Bespoke Investment Group, LLC. The information herein was obtained from

sources which Bespoke Investment Group, LLC believes to be reliable, but we do not guarantee its

accuracy. Neither the information, nor any opinions expressed, constitute a solicitation of the

purchase or sale of any securities or related instruments. Bespoke Investment Group, LLC is not

responsible for any losses incurred from any use of this information.

6

China PMI: Shifting gears to

Chinese PMI, both manufactur-

ing and Services PMIs beat ex-

pectations and rose this month.

For manufacturing PMIs in Chi-

na, new export orders have

been a huge drag in the recent

deceleration. As shown at right,

in December new export orders

were reported to be shrinking

at roughly the same pace as Q1

of ‘16 when they bottomed.

Recent reports have showed a

bottoming process may be play-

ing out; MoM new export or-

ders were the most improved

versus last month since May.

Other indicators like output

also ticked up.

For right now, it’s hard to get

too excited about PMI data

from China but it at least gives

hopes that “green shoots” may

start sprouting in that part of

the global economy again soon.

For now, the rapid slowing of

Chinese profits is confirmation

that PMIs are still in tough

shape, although definitely not

in the same kind of trouble they

were in 2015-2016.

Finally, we note that while

manufacturing PMI has deterio-

rated a lot, Services has held up

much better. The result is a big

outperformance of Services

over Manufacturing, the big-

gest in more than half a decade

in fact.

Morning Commentary

China: Man'f PMI New Export Orders Improve Most Since May

China: Back To 2015 Territory And Slowing Further

China: At Least Services Is Outperforming (By A Lot!)

44

46

48

50

52

54

56

58

60

62Manufacturing Total, 49.5Output, 50.9New Orders, 49.6New Export Orders, 46.9Employment, 47.8

-15

-10

-5

0

5

10

15

20

25

30

35

48

49

50

51

52

53

54 China Manufacturing PMI

China Industrial Profits Cum. YoY

-2

0

2

4

6

8

10

12

14

China Services PMI - ChinaManufacturing PMI

For Personal Use Only—Do Not Forward

BespokePremium.com © Copyright 2019, Bespoke Investment Group, LLC. The information herein was obtained from

sources which Bespoke Investment Group, LLC believes to be reliable, but we do not guarantee its

accuracy. Neither the information, nor any opinions expressed, constitute a solicitation of the

purchase or sale of any securities or related instruments. Bespoke Investment Group, LLC is not

responsible for any losses incurred from any use of this information.

7

Eurozone GDPs: Yesterday,

French GDP beat estimates.

Today, it was the turn of Spain,

where growth picked up to

0.7% QoQ. As shown at left, of

the “core four” Eurozone econ-

omies which account for 80% of

the bloc’s output, only Italian

GDP has worsened sequentially.

Italy’s GDP is now down a sec-

ond quarter in a row, making it

three recessions (by that com-

mon definition) since the global

financial crisis.

At least the rest of the Euro-

zone is in better shape. In the

chart at left we show QoQ

growth rates by economy re-

ported so far, along with an

implied growth rate for the

46.2% of the zone by output

that has not yet reported

growth for Q4. Of that remain-

ing chunk, about two-thirds is

Germany. Given that, it’s un-

likely German growth was neg-

ative again in Q4 after a brutal

Q3 where it even lagged Italy!

Eurozone Labor: Italy, Germa-

ny, and the broad Eurozone all

released December unemploy-

ment data today, and while the

German methodology differs

from the other two, we can say

all three show ongoing im-

provement in labor markets

even as growth has slowed at

the margin over the last two

quarters.

Morning Commentary

Italian Recession, Germany Likely Grew In Q4

Eurozone GDP Growth QoQ (%)

December Labor Data Shows Nothing But Good News In EZ

-2

-1

0

1

2

3

4

5 FranceSpainItalyEurozoneGermany

0.30.2

1.1

1.6

0.3

0.7

-0.2

0.20.1

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.853.8% of EZ total output already

reported, Germany is 63.3% of remaining.

4

5

6

7

8

9

10

11

12

13

14 Italy ILO Unemployment (Prelim)Germany Unemployment Claims RateEurozone ILO Unemployment

For Personal Use Only—Do Not Forward

BespokePremium.com © Copyright 2019, Bespoke Investment Group, LLC. The information herein was obtained from

sources which Bespoke Investment Group, LLC believes to be reliable, but we do not guarantee its

accuracy. Neither the information, nor any opinions expressed, constitute a solicitation of the

purchase or sale of any securities or related instruments. Bespoke Investment Group, LLC is not

responsible for any losses incurred from any use of this information.

8

Standout Spain: Despite a

weakening of the backdrop

across the Eurozone, Spain’s

GDP growth has not fallen out

of the bottom of its 2.2%-3.9%

QoQ SAAR growth range of the

past few years. We note that

range tracks pretty well to the

range the Spanish economy oc-

cupied during the “boom” years

of the 2000s when investment

exploded thanks to massive cap-

ital inflows. This time, though,

Spanish growth looks much

more sustainable.

As shown at right, the huge and

growing current account deficits

of the 2000s (representing the

mirror image of capital inflows)

have disappeared, with the cur-

rent account running a persis-

tent but small surplus since

2013. That surplus has dropped

recently, but even still looks to-

tally reasonable and nothing like

the imbalances of the 2000s.

Tourism growth has been una-

ble to accelerate over the past

year after surging from 2013

onward. That, along with higher

oil prices and slower global de-

mand overall are an explanation

of the weaker Spanish current

account surplus over the last

few quarters. If tourism returns

to growth, so will Spanish cur-

rent account surpluses but at

worst small deficits are not a

significant concern.

Morning Commentary

Spain's Economy Much More Balanced Than During 2000s Boom

Source of Current Account Downtick: Tourism Growth Stops

Spain: Growth In-Line With 2000s, Sustainably This Time

-12

-10

-8

-6

-4

-2

0

2

4

Spain Current Account(bn EUR, SA byBespoke)

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

Tourist Arrivals (mmpersons, SA byBespoke)

-8

-6

-4

-2

0

2

4

6

8

Spain GDP QoQ SAAR

For Personal Use Only—Do Not Forward

BespokePremium.com © Copyright 2019, Bespoke Investment Group, LLC. The information herein was obtained from

sources which Bespoke Investment Group, LLC believes to be reliable, but we do not guarantee its

accuracy. Neither the information, nor any opinions expressed, constitute a solicitation of the

purchase or sale of any securities or related instruments. Bespoke Investment Group, LLC is not

responsible for any losses incurred from any use of this information.

9

US Earnings: Facebook (FB) shook off privacy concerns to report a blow-out Q4 last night, and is up

11% on massive revenues and margins. Tesla (TSLA) is down almost 5% after the CFO retired last night

in the wake of a big EPS miss. In energy, ConocoPhillips (COP) smashed estimates and raised its divi-

dend more than expected. With the 40% of the S&P 500 having reported, every sector is reporting rev-

enue growth of over 1% YoY, and only 1 sector (Materials) is reporting an EPS decline versus last year.

Economic scorecard. Interactive Earnings Calendar.

Morning Commentary

Asset Level Change 5d Chg 3m Chart Asset Level Change 5d Chg 3m Chart

S&P 500 2685.75 12.1 184.9 Gold 1328.20 96.5 327.3

Russell 1490.50 12.8 191.5 Silver 16.12 121.2 518.8

VIX Fut 17.91 -36.2 -696.1 WTI 54.23 0.0 197.4

TSX 925.90 16.2 124.7 Copper 278.75 72.3 532.8

2 Year 250.20 -0.6 -6.2 Nikkei 20773.49 105.5 96.7

5 Year 248.33 0.0 -6.7 CSI 300 3201.63 104.6 135.7

10 Year 267.38 -0.4 -4.2 ASX 200 5864.65 -37.5 -1.8

30 Year 302.69 -0.5 -0.7 Stoxx 600 358.19 -8.9 70.9

2s10s 16.98 0.2 2.0 BBG USD 1178.41 -15.1 -111.0

5s30s 54.20 -0.5 6.0 EURUSD 1.1486 5.2 161.0

5 Yr BE 169.80 0.3 168.2 USDJPY 108.65 -35.8 -90.3

10 Yr BE 183.37 0.5 181.6 EM FX 64.34 35.6 132.0

Mar '19 97.35 0.5 3.0 CDX IG 67.51 0.5 -6.6

Jun '19 97.35 2.0 6.0 iTraxx IG 70.54 2.0 -6.2

Sep '19 97.34 2.0 5.5 CDX HY 355.80 2.0 -28.2

Dec '19 97.33 2.0 6.5 iTraxx HY 308.65 2.0 -20.5

Euro

do

llar

s

Cre

dit

Major Asset Class Dashboard

Equ

ity

Futs

Co

mm

od

ity

Trsy

Yie

lds

Int'

l Eq

uit

y

Cu

rve

s/B

E

FX

(bps)(bps)