Embed Size (px)

Citation preview

No. 35-2006 ICCSR Research Paper Series - ISSN 1479-5124

Best Practice Reporting on Gender Equality in the UK: Data, Drivers and Reporting Choices

Kate Grosser and Jeremy Moon

Research Paper Series

International Centre for Corporate Social Responsibility ISSN 1479-5124

Editor: Jeremy Moon

International Centre for Corporate Social Responsibility

Nottingham University Business School Nottingham University

Jubilee Campus Wollaton Road

Nottingham NG8 1BB United Kingdom

Tel: +44 (0) 115 951 4781 Fax: +44 (0)115 84 68074

Email [email protected] http://www.nottingham.ac.uk/business/ICCSR

Best practice reporting on gender equality in the UK:

data, drivers and reporting choices

Kate Grosser and Jeremy Moon

Abstract

The paper’s twin purpose is to investigate and explain whether there

have been improvements in reporting on gender equality in the workplace

by UK best practice companies in the last decade.

It deploys two complementary methodologies for investigating twenty companies claiming best practice external communications on this issue

(a) quantitative analysis of gender impact reporting by companies (b) qualitative analysis, through interviews with company representatives, of

the drivers for reporting and reasons for non-disclosure of information internally available.

The main findings are that despite new and substantial forms of gender

impact reporting and widespread reporting of gender/diversity policies and programmes, reporting of gender impacts and performance is still

generally low and idiosyncratic. Secondly, there are significant instances of non-disclosure of gender information internally generated for other

purposes.

Companies explain their reporting decisions with reference to three sorts

of drivers: market, civil society and governmental, along with firm-specific organisational factors, poor performance and anxieties about the misuse

of data. General company reluctance to report more is associated with perceptions of a lack of demand for more detailed impact reporting and

the risks arising from a negative media climate.

The implications are that further impact reporting appears dependent on greater demand expressed through one of three main drivers of company

behaviour.

The originality of the paper lies in the deployment of the three driver analytical framework and the use of qualitative research methods to

explain quantitative findings on gender equality. Limitations in the

research may lie in the relatively small sample.

Keywords gender equality; reporting, UK, companies, CSR drivers

2

Authors

Jeremy Moon is the Director of the International Centre for Corporate Social Responsibility (ICCSR) at the Nottingham University Business

School and a Professor of Corporate Social Responsibility.

Kate Grosser is a Visiting Fellow at ICCSR. She has worked with government, NGO’s, academia and the business community on a range of

economic, human rights and gender issues, Her recent research interests include the relationship between Corporate Social Responsibility, gender

equality and gender mainstreaming. She is currently working on a research project on corporate public reporting of equal opportunity for

women: a comparison of regulatory and voluntary frameworks in three countries (the UK, Australia and the USA), sponsored by the Association of

Chartered Certified Accountants.

Address for correspondence

(ICCSR), Nottingham University Business School, Jubilee Campus,

Wollaton Road, Nottingham, NG8 1BB, United Kingdom.

Jeremy Moon Email: [email protected]

Kate Grosser Email: [email protected]

INTRODUCTION[i]

Significant deficiencies have been found in UK corporate disclosure of

equal opportunities (Adams and Harte 1995; Benschop and Meihuizen

2002), particularly because it has mostly been confined to policies and

programmes with little disclosure of outcomes, impacts or performance

data (Adams and Harte 1998, 1999, TUC 2004). Opportunity Now {ON}

(2004) has noted improvements in business monitoring of their gender

equality programmes[ii] . This study investigates whether this increased

monitoring has been accompanied by improvements in reporting of

outcomes, impacts and performance relating to gender equality.

It does so by investigating companies that claim to be pioneering best

practice external communications on this issue. First, actual reports of

gender equality are analysed. Secondly, by applying the qualitative

approach (O’Dwyer 2002, 2003; Adams 2002; Larninga-Gonzalez 2001) of

interviews with managers, it investigates the nature and drivers of gender

equality reporting, and the reasons for non-/disclosure. Thirdly, it

evaluates the findings from these interviews through a framework

normally associated with explanations of corporate social responsibility

(CSR) which distinguishes three main drivers of company behaviour:

markets, civil society and government (Moon 2004a). It also addresses

organisational impediments to further reporting. We identify possibilities

for future action that relate to all three drivers and discuss the

2

implications for policy makers, NGOs, social accountants and others

interested in greater CSD on gender equality and diversity.

METHODOLOGY

The paper presents an analysis of twenty publicly listed companies which

benchmark their progress on gender equality with Opportunity Now[iii] and

which awarded themselves top marks for external communications in this

self-assessed benchmarking survey in 2002/3 or 2003/4.

Our selection of companies which monitor their gender equality progress

was designed to capture companies with reporting capacities (Adams and

Harte 1999:23, 2000:9) [iv]. Many companies included details of their ON

benchmarking scores in their public reporting as providing an authoritative

indication of their performance. Not all of our sample expressed full

satisfied with their monitoring systems thus far however, so systems

limitations could still explain some of the lack of disclosure[v] , In order

maximise the chances of interviewing those companies with the most

comprehensive monitoring systems interviews were held with detailed

reporters, all of whom claimed to have advanced montoring systems in

place. Secondly, our sample of reporting leaders allows reasonable

insights into possible future corporate behaviour because, apart from their

commitment to benchmarking progress towards gender equality, many of

our sample have won awards for gender equality or other human resource

policies.[vi]

3

As our original intention was to compare the financial sector

(characterised by high levels of female employment) with other sectors,

banks comprise over half the sample (n = 13). However, as no distinctive

findings appeared in either the analysis of reports or the interviews with

managers, sectoral issues do not feature in the paper. The other seven

companies sampled are in retail (2), transport (2), telecommunications

(1), energy (1) and manufacturing (1). The companies remain

anonymous as the ON benchmarking results are confidential and the

companies’ subsequent agreement to participate was on a confidential

basis.

The analysis is divided into two sections reflecting the respective

methodologies deployed. Quantitative analysis is based on investigation

of the twenty companies’ annual reports, CSR reports (2004) and websites

(2004-5). With reference to Gray’s (2001) discussion of how the

stakeholder model can be used to help define the categories used in social

accounting, our decisions about what information was relevant were

informed by academic literature, regulation for reporting in other

countries, voluntary guidance for UK human capital management

reporting, EOC and NGO comments on gendered human capital reporting,

and relevant private sector benchmarking initiatives[vii] (the questions

used in this data collection are available from the authors ). We searched

principally for performance data on: workplace profile; career

development, including recruitment, retention, promotion, training,

4

redundancy; equal pay; work-life balance; and aspects of governance and

general management related to gender issues.

Hackson and Milne (1996), Toms (2002) and Hasseldine et al (2005) have

developed qualitative variants on content analysis methodology. We have

adopted a simplified approach by differentiating two main categories. The

first includes rhetoric, declarative, policy, endeavour or intent, and

programme reporting, and the second includes targets, quantified (either

monetary or non-monetary) data, and descriptions of outcomes. We

record only the latter except where programme descriptions were deemed

to be unusual and therefore worthy of inclusion. This remains a broad

category and we give examples to illustrate the range of reporting found.

We included reporting of litigation/tribunal cases as performance

reporting.

Our findings are recorded as numbers/percentages of companies making

disclosures in any particular category (see Milne and Adler 1999). We did

not record how many times any particular piece of information is reported

or any other information about quantity of reporting. Nor did we confine

ourselves to information defined specifically as CSR, but searched more

broadly on websites, for example in recruitment sections. We confined our

research to the one question as to whether or not performance related

information was disclosed on each specific gender related issue.

5

Qualitative analysis is based on interviews with eleven representatives of

seven different companies from our sample.[viii] Companies were chosen

on the basis of the quality of their reporting. Interviewees were chosen

according to their responsibility for gender issues and /or reporting.[ix] As

reporting gender issues is often a point of functional overlap, in three

companies we interviewed more than one representative to ensure an

appropriate range of organisational perspectives. Interviews were by

telephone, lasting between 30 and 80 minutes[x].

The interviews took a semi-structured format around issues identified in

the CSD literature and in the quantitative analysis. These included: what

companies identify as key performance indicators of gender

equality/diversity; their reasons for reporting; target audiences and

drivers; criteria for what to report; reasons for not reporting; attitudes to

reporting bad news; feedback about reporting, and incentives for greater

disclosure. The analysis of these interviews is structured around the

questionnaire, although other issues that emerged in the interviews are

also considered.[xi]

Whereas CSD literature tends to focus on the regulated / non-regulated

dichotomy, our investigation of the reasons for non / reporting was

conducted in the framework of three drivers which have been used to

explain increased corporate social responsibility (CSR) among UK

companies: market, civil society and governmental (Moon 2004a). Market

drivers include pressure from consumers (e.g. niches, mass boycotts),

6

employees (to retain and attract employees), investors (ethical / social

responsible investment, mainstream investor interest), business

customers (through supply chain assurance) and competitors (where CSR

branding adds competitive edge). Civil society drivers, or social

regulation, refers to the more collective impacts on corporations than

those imposed by the sum of individual consumers. Non-government

organisations, in their adversarial and partnership modes, are drivers of

and self-appointed guardians of CSR norms, abetted by the media’s

appetite for stories of irresponsibility. Government can drive CSR without

recourse to ‘hard’ or coercive regulation. Soft regulation can encourage

improved reporting standards (e.g. amendments to the UK Pensions and

the Companies Acts). Governments encourage CSR through injunction, by

financial incentives and organisational resources (Moon 2004b). We

investigate the relative significance of these drivers in explaining

non/reporting of gender issues alongside organizational factors

ANALYSIS

The state of gender equality reporting by UK best practice companies

Table 1 indicates that those companies claiming to communicate well on

gender equality did indeed report publicly on gender issues, whether in

corporate values statements or in descriptions of policies, practices/

programmes and impacts. However, Table 2 indicates a great variety of

the workplace profile data reported.

7

Table 1

Sites of Reporting

% using this reporting method

% reporting gender equality by this method

Annual Report 100% 85%

Website 100% 100%

CSR Report 80% 100%

Table II

Gender in Workplace Profile

Number reporting Percentage reporting

Women as percentage of total workforce 14 70%

Women as percentage of management 15 75%

Trends in women as percentage of management 13 65% Targets for women as a percentage of management 11 55% Women as percentage of different grades 8 40% Trends in percentage of women by grade 9 45% Percentage of all staff working part-time/flexibly 9 45%

Women as part-time workers 1 5% Attracting women in to non-traditional jobs 8 40%

Women with other diversity indicators 1 5%

Note: Board members were named in Annual Reports meaning that it was possible to

ascertain the percentage of women on the Board in most company reporting, so we have

not included this as a separate reporting category.

While the Ethical Investment Research Service recommends that a ready

indicator of progress on gender equality is women as a percentage of the

total workforce and as compared to women as a percentage of

management (interview), 30% of our companies failed to report the

former and 25% the latter. Although two-thirds report trends relating to

women in management, and over half report targets for women in

8

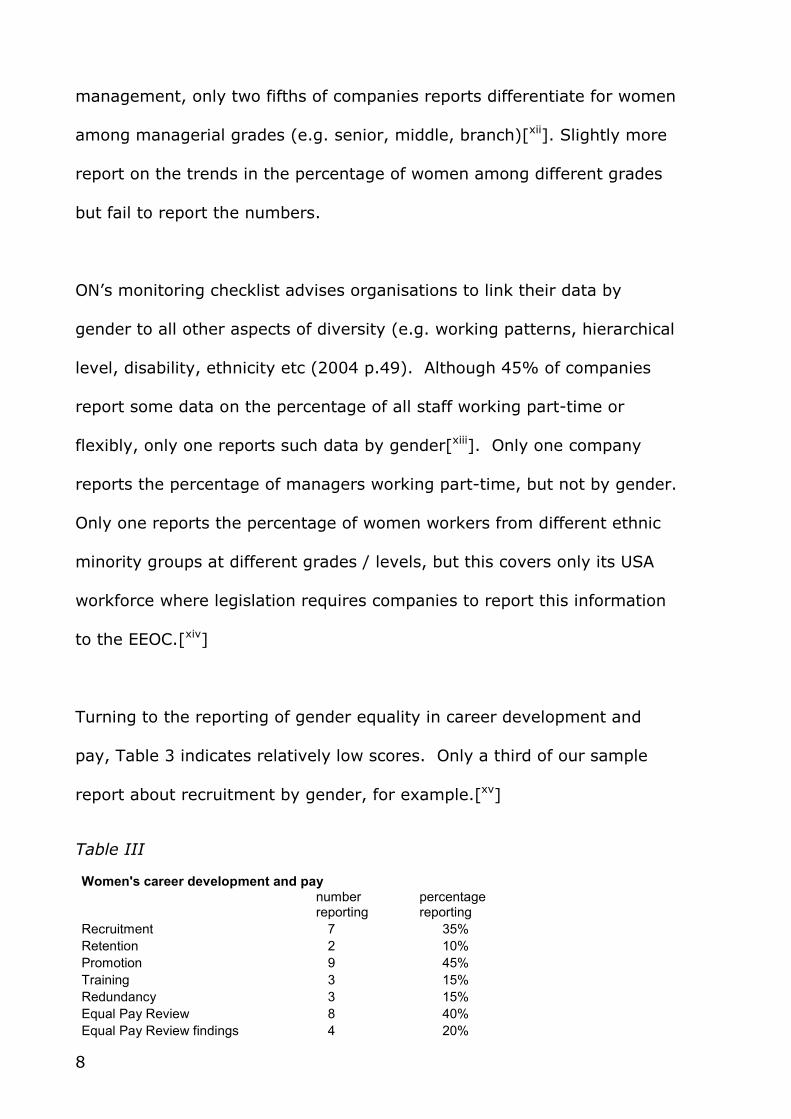

management, only two fifths of companies reports differentiate for women

among managerial grades (e.g. senior, middle, branch)[xii]. Slightly more

report on the trends in the percentage of women among different grades

but fail to report the numbers.

ON’s monitoring checklist advises organisations to link their data by

gender to all other aspects of diversity (e.g. working patterns, hierarchical

level, disability, ethnicity etc (2004 p.49). Although 45% of companies

report some data on the percentage of all staff working part-time or

flexibly, only one reports such data by gender[xiii]. Only one company

reports the percentage of managers working part-time, but not by gender.

Only one reports the percentage of women workers from different ethnic

minority groups at different grades / levels, but this covers only its USA

workforce where legislation requires companies to report this information

to the EEOC.[xiv]

Turning to the reporting of gender equality in career development and

pay, Table 3 indicates relatively low scores. Only a third of our sample

report about recruitment by gender, for example.[xv]

Table III

Women's career development and pay

number reporting

percentage reporting

Recruitment 7 35%

Retention 2 10%

Promotion 9 45%

Training 3 15%

Redundancy 3 15%

Equal Pay Review 8 40%

Equal Pay Review findings 4 20%

9

Companies sometimes report broad targets (e.g. women as a percentage

of the workforce), but in other cases more detailed targets are given (e.g.

percentage of new recruits, new women graduates, women as modern

apprentices or recruits to technical jobs). Some reporting focused on

women in management (e.g. targets and performance for women short-

listed for senior management positions). Others report the aim of

attracting more working mothers, or lone parents (approximately 90% of

whom are women) in order to reflect their customer base, but do not

necessarily report outcomes.

Gendered data and targets for workforce retention are reported much less

frequently (despite a quarter of our sample reporting some data on overall

staff turnover / retention targets or rates). Only one company reports its

maternity return rate, and one reports on how it implements plans to

improve retention of women following exit interview analysis.

Turning to promotion, many companies’ data do not distinguish women

externally recruited from those advancing internally, so this figure may be

artificially high, but others do report the proportion of women promoted to

management. Some report new training, career restructuring, and

rethinking promotion criteria (e.g. relocation requirements) in traditionally

male-dominated jobs, in order to increase the promotion of women.

Although a number of companies report indicators of workforce training,

very few provide any gendered information. For those that do this is either

10

confined to training of women in senior roles (e.g. participation in

executive development) or women-only training courses (without

participation data). None report training of part-time workers (78% of

whom are women in the UK)[xvi]. However companies have begun to

report e-learning provision, with one reporting the percentage of (and

targets for) training provided via this flexibly accessed medium.

Reporting on redundancy by gender is rare, though some companies

report that this is monitored and that it is generally gender-neutral. One

reports that the percentage of female managers declined because of their

high take-up of redundancy packages.

Two fifths of companies report equal pay reviews. Only half of these

report any results. Box 1 illustrates the details reported.

Box 1

Examples of details relating to equal pay reported

Pay differentials between FT men & women; comparison with national pay gap Pay differentials between PT men and women Lowest starting salary Agreements with unions about equal pay reviews Explanations of pay gaps; programmes to address them (e.g. pay reviews at bottom of the pay scales, elimination of long service bonuses) Budget allocations to redress pay differentials Board support for equal pay reviews, integration of equal pay guidance into pay reviews Explanations of how the equal value issue is addressed Bonus payments inclusions in equal pay reviews Extension of equal pay reviews to race and disability issues

Some companies report problems encountered in addressing equal pay

(e.g. multiplicity of bonus schemes, decentralisation of individual

performance rewards). Overall, detailed reporting on equal pay reviews is

rare and generally in the form of a positive story.

11

Although more than one third of the pay gap is explained by women

combining care and paid employment (EOC, 2004), only a third of our

sample report performance on flexible working (Table 4).

Table IV

Work-life issues

Number reporting Percentage reporting

Flexible working performance 7 35%

Flexible working take-up by gender 0 0%

Childcare performance 3 15%

Childcare take-up by gender 0 0% Health and Safety with gender 3 15%

Box 2 illustrates the data reported. Although the ON benchmarking survey

asks whether companies regularly monitor the take-up of flexible working

schemes by gender, and by gender and hierarchical level, no sampled

company reports this data.

Box 2

Examples of flexible working performance/achievements data reported

Percentage of the workforce working flexibly (no gender) Savings associated with flexible working. Percentage of employee satisfaction with work-life balance or options, with trends (no gender breakdowns) Applications, and percentage granted, for flexible working arrangements (no gender breakdowns) Number of complaints under new legislation on the right to request flexible work. Awards for creating a flexible work structure, and rankings in graduate guides to best work-life balance employers Partnerships with NGOs to develop policy / assist staff access relevant external services Shortening of the working week for non-management grades Percentage of training provided via e-learning

Whilst many companies report their childcare and eldercare policies (e.g.

facilities, vouchers), few indicate outcomes or impacts. Exceptions report

the number of employees using facilities, cost savings to these employees,

12

the number of children participating in company programmes,

partnerships (e.g. with Employers for Carers) or NGO accreditation (e.g.

verifying company support for pregnant employees). None report the

take-up of childcare options by gender. One company reported its staff

percentage with parental responsibilities and another reported increased

take-up of paternity and unpaid parental leave. No data on parental leave

was reported by our sample.

Although health and safety policies increasingly extend to stress-related

illness (a leading cause of long-term absence), we found no overall

gendered data about health and safety in the workplace. One company

however reports support for women with post-natal depression and

another reports the number of employees screened in its breast cancer-

screening programme. A small number of companies report addressing

domestic violence as an issue with workplace implications (e.g. in the

context of collaboration with unions).

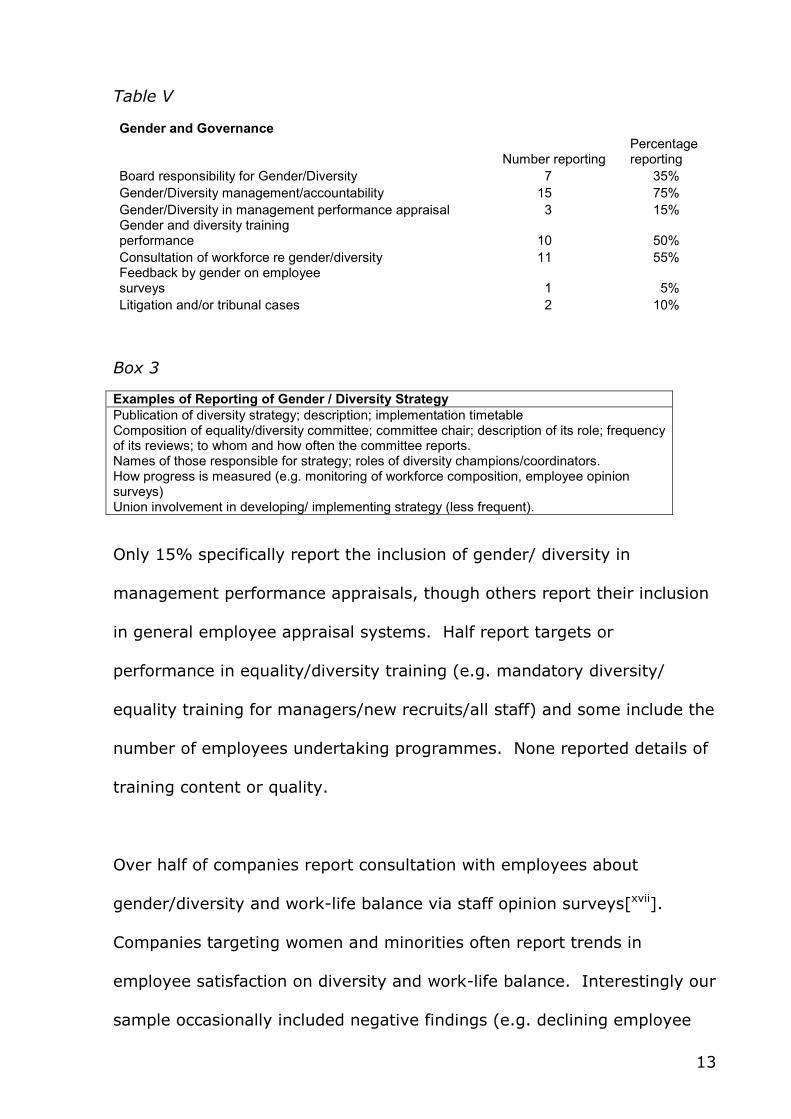

Table 5 indicates reporting on gender in governance and in broad

management systems. Over a third of companies report board level

responsibility and three quarters report on management accountability, for

gender/ equality/ diversity (Box 3).

13

Table V

Gender and Governance

Number reporting Percentage reporting

Board responsibility for Gender/Diversity 7 35%

Gender/Diversity management/accountability 15 75%

Gender/Diversity in management performance appraisal 3 15% Gender and diversity training performance 10 50%

Consultation of workforce re gender/diversity 11 55% Feedback by gender on employee surveys 1 5%

Litigation and/or tribunal cases 2 10%

Box 3

Examples of Reporting of Gender / Diversity Strategy

Publication of diversity strategy; description; implementation timetable Composition of equality/diversity committee; committee chair; description of its role; frequency of its reviews; to whom and how often the committee reports. Names of those responsible for strategy; roles of diversity champions/coordinators. How progress is measured (e.g. monitoring of workforce composition, employee opinion surveys) Union involvement in developing/ implementing strategy (less frequent).

Only 15% specifically report the inclusion of gender/ diversity in

management performance appraisals, though others report their inclusion

in general employee appraisal systems. Half report targets or

performance in equality/diversity training (e.g. mandatory diversity/

equality training for managers/new recruits/all staff) and some include the

number of employees undertaking programmes. None reported details of

training content or quality.

Over half of companies report consultation with employees about

gender/diversity and work-life balance via staff opinion surveys[xvii].

Companies targeting women and minorities often report trends in

employee satisfaction on diversity and work-life balance. Interestingly our

sample occasionally included negative findings (e.g. declining employee

14

satisfaction with ‘various aspects of workplace diversity’). Many report

staff survey response rates but not by gender. Only one company

reported that feedback is monitored according to different diversity

strands, and targets relating to this. None reported analysis of overall

staff surveys by gender.

Whilst we found extensive reporting of other human capital management

issues (e.g. absentees, length of service, employee share options

schemes) this included no gender breakdowns. Only two companies

reported litigation and tribunal cases but neither specified whether these

were on gender issues[xviii]. Several reported their results in the ON

benchmark, and one included its results in the impact section of the

benchmark specifically.

To sum up, we found considerable variety of reporting on impacts by best

practice companies not identified in previous studies. However this is

patchy, unsystematic, not easily compared and rarely constituted a

comprehensive coverage of gender workplace issues as called for by social

accountants, NGOs and legislation in other countries. This confirms Gray’s

(2001:13) finding that ‘Voluntary initiatives do not produce widespread,

consistent, and systematic practice’. Very little negative information was

revealed, confirming findings that voluntary reporting consists largely of

favourable managerial accounts (Adams and Harte 2000), however, apart

from litigation, negative information which was reported appeared when

reporting against clear targets had been established, or when a pattern of

15

reporting trends year on year was in place. Whilst the best reporting

linked targets, policies and programmes on the one hand and impacts on

the other, most reports did not. Gender breakdowns are still rare in

human capital reporting.

Explaining gender reporting among UK best practice companies

In order to explain these findings and to understand their organisational

context, we turn to the results of our qualitative analysis: interviews with

responsible managers.

What gets measured and why

In order to report, companies must first design their own measurement

systems. This is necessary for internal management and accountability,

tracking progress, benchmarking, and identifying areas for further action.

One interviewee described their monitoring system as having both top-

down and bottom-up input to maximise buy-in, to connect with overall HR

strategy, and to track progress and causality. Monitoring was also

explained as a means of winning the attention and support of senior

management, enabling regular, structured internal reporting to the Board,

and as resource in the event of discrimination cases. Some companies

also specified the need to report externally on human capital

management, including diversity ,(e.g. DTI’s 2003, 2004). Our interviews

revealed that most companies collect the information we had sought in

their reporting (and often much more) but choose not to publicise much of

it.

16

Key performance indicators (KPIs)

KPIs are centrally important for effective tracking and reporting of

progress and impacts. Workplace profile data is considered key. Most

interviewees considered the percentage of women employees as

compared to the percentage of women in management, as used by EIRIS,

as necessary but not sufficient to monitor gender equality progress. Data

enabling the identification of trends were seen as vital:

‘what I’m looking for all the time is improvement. We should

instead ask “Can you show improvement?” I think that’s a

more sophisticated debate.’

Companies vary in the trends they monitor, tracking for example women’s

promotion in proportion to their population in feeder grade, or the

company overall, or ‘what the balance is moving through each particular

grade’. One interviewee noted that job segregation means that:

‘if you look at the numbers overall they are very misleading.

You have to look at them at different levels, and also within

different departments as well because obviously we have

some predominantly female areas and we have some very,

very male dominated areas like engineering.’

Several interviewees saw attention to a single indicator of female

representation (e.g. board membership) as misleading. One complained:

‘We went down that list this year, merely because other

boards have reduced in size and … [thereby got] … a better

17

percentage of women. And when we say to the people doing

that survey - hang on a minute we’ve got loads of women who

are in much more responsible jobs than being a board

member, paid higher salaries, with more responsibility - they

say “no we’re not interested in that”’[xix].

Although companies receive external encouragement to signal and report

against targets (e.g. by benchmarking organisations, rating agencies),

even committed managers can view targets as problematic:

‘the targets on the website are there because external people

want us to have [them]…internally we don’t bang on about

those targets very much at all, [rather] we report the facts,

and we expect our managers to react to [them]’.

‘This [avoidance of targets] means that we don’t get into…

positive discrimination. That’s a real concern because … if the

boss says you will get a 2% figure, guess where you end up?

And the mechanisms to deliver that then become aimed at

delivering (only) that.’

Many interviewees attested to the importance of a variety of indicators to

demonstrate improvements, because ‘Having the percentages doesn’t

mean it’s a good place to work and your colleagues are valued and

happy.’ Several mentioned that maternity return, post maternity

retention, and exit interviews explaining female attrition are important

success measures. Others talked in terms of measuring inputs:

‘I would be looking more at the training, education side… what

opportunities are given to staff to be able to work on a par

with each other, and flexible work.’

18

There was also agreement on the importance of trying to track cultural

change within the organisation but ‘that’s much more difficult to define’.

‘you want to …. look at whether women’s positions are part-

time, shift etc … because those are good indicators of how

good the policy is.’

Many felt that the take up of flexible working by gender and hierarchical

levels of the organisation was an important indicator of cultural change.

Others emphasised staff survey feedback about diversity, work-life

balance, job-satisfaction, feeling valued and being treated fairly.

‘what colleagues are …saying to us … is… an output that’s

going to be really critical in terms of how we’re doing. We’ve

already changed the timetable for that this year to reflect this

reporting in the future.’

Many companies monitored the results from these by gender and diversity

strand, and were thereby able to confirm for example that home-workers

were just as well engaged as other workers .

While it was not our research focus, nearly all interviewees’ companies

had rigorous internal reporting systems on equality and diversity.

‘[W]e report on everything… we’ve got a diversity leadership

group that the Chief- Exec chairs and he’s asked for diversity

KPIs within every division, and reporting to the Board on

whether the division/ business is green, red, or amber. I think

that reporting right up to the Board on a quarterly basis will

19

really keep the activity going at a lower level, and it’ll create a

lot of competition between the different divisions.’

‘[A]ll divisions have to report to the Chief Exec personally on

diversity twice a year and there’s nothing more powerful than

being sat in front of the Chief Exec for making things happen!’

A third company described reporting to unions in order to communicate

with workers internally, as well as reporting diversity statistics to the

Management Board on a monthly basis, and the main Board on a

quarterly basis.

Deciding what to report

Our interviews confirm that companies collect and analyse

gender/diversity information far in excess of what they publicly report.

Our main finding is that companies report on gender equality within

responses to key stakeholders/market drivers of investors and potential

employees, as both of these offer tangible company benefits. Other

market drivers specified in interviews were customers and clients. Civil

society drivers of the community and the general public, and government

drivers were also specified. Interviews revealed how companies try to

balance the needs of these different stakeholder groups in terms of the

length and content of their reporting:

‘Some of the public will say there’s too much information, and

reporting agencies will say, “we want more”, so what we’ve

tried to do is strike a balance between the two’.

20

When asked how they choose what to report, the emphasis was clear:

‘obviously good news, and progress rather than any negative

type things, and also what we’re going to do to get better.’

One interviewee noted that reporting on gender equality/diversity

supports the corporate responsibility agenda and ‘helps us to engage

customers and colleagues’.

Nonetheless, many interviewees emphasised that reporting should focus

on issues significant to the company:

‘we have to be careful that what we report on tells the story

as to what’s important to us… I’ve seen all sorts of scorecards

banded around, and yes, we will consider what’s in there, but

ultimately when we’re reporting it’s what’s material to us as a

business.’

Companies use external reporting guidelines reflecting market and civil

society drivers (e.g. benchmarks and questionnaires from ON, EIRIS,

Manifest, FTSE 4 Good,Business in the Community). However, the impact

of these drivers is subject to significant internal decision-making

processes. Our interviewees tell of submitting gender/diversity

information for inclusion in CSR and Annual Reports and that another

department, or inter-departmental committee decides on the final

content:

21

‘it (the CSR report) covers environmental, people-related and

business-related issues so a cross-section of people (including

from procurement and marketing) is represented on the

Steering Group and they all knit chunks of work and then it

gets pulled together by the Steering Group... I ( Head of

Diversity) draft the Diversity section for approval by the HR

Director; [it then goes] to the Steering Group and gets pulled

apart and then goes to the Leadership Team … and then to

the Board for approval and then it gets published.

‘[Our] report goes via Investor Relations and the Press Office

[and] although my team put out as much as we can … it gets

pared down because there are so many people vying for

space.’

Descriptions of governance and accountability systems are also reported

to provide confidence in a company’s commitment:

‘we’re trying to report … an infrastructure of control… as well

as having the organisational structure to manage our

business, how does our organisation structure (itself) to

manage equality and diversity for example – we’re trying to

give confidence around that.’

The two companies reporting on litigation and tribunal cases explained

this, first , because as the information is already public it is advantageous

to present the company interpretation of the issues and, secondly,

because it is advantageous to report bad news ‘when we started to turn it

into good news.’

22

Finally case studies are given to illustrate success, however most

interviewees agreed that on their own they are not adequate indicators of

overall impact.

Reasons for non disclosure on gender equality

Finally, we asked our interviewees why companies don’t report gender

equality impacts in more detail and what would lead them to report more.

Whereas a small number considered that their reporting adequately

reflected their progress, a variety of reasons were also given for not

reporting gender equality impacts in more detail. In short, the

interviewees suggest that that there is little market, civil society or

governmental demand for more detailed information, and they perceive

significant risks in revealing more than they need to:

‘I would question why you would report it (more information).

Who is really interested in a lot more information in depth on

these things?’

‘Who do you want me to report it (further information) to?…

we report on what we think we need to report, in terms of

what we are legally obliged to do. And we communicate our

good work through other members of the CBI group. We work

with the North East Centre for Diversity, Race for Opportunity.

We work with ON. We work with lots of different organisations

to get the word around about (the company) and we promote

what we do through our advertising and our publications, so

when you say reporting, I’m not quite sure where else I could

report to’.

23

Smaller companies also allude to time and money as reasons for not

reporting in more detail:

‘you’re driving forward with the business, and you do what

you need to. In some respects if you don’t need to do any

more – well that’s probably one of the most practical answers

I can give you.’

Others refered to clarity of reporting:

‘More sometimes becomes less. There is a criticism sometimes

that you throw in everything that you can possibly collect and

have all these metrics and then it all gets lost in terms of what

the priorities are’.

Finally, interviewees from companies new to this agenda stated that they

didn’t report actual data as they do not feel that this yet reflects the

investment they have made in the field. They expect to report more once

their statistics look better.

Market drivers

The general lack of demand for more detailed reporting is articulated

specifically in market terms:

‘Basically the shareholders and investors want to know the

demographics, they might be interested in part-time

(workers). They want to know how many people we’ve got at

different levels, and that’s about it’.

Our interviews established that investors, rating agencies and job

applicants sometimes request information on gender equality/diversity

24

beyond what is reported. Whilst this is generally provided, it isn’t

necessarily subsequently included in public reporting. Most investor

inquiries are limited to:

‘How many women have you got with you? How many women

in senior roles? And (sometimes) the trends.’[xx]

‘what would really make me report [more] on it is if I believed that

that would generate better brand value for the company and better

sales…The point where this becomes really useful to me is where it

impacts on share price… [investors are] not banging anyone’s door

down and they’re certainly not rewarding or punishing companies

that are good or bad at it (reporting)’.

One interviewee emphasised the power of the market as a driver of

gender equality in the workplace, arguing that if equal pay reviews

determined investments then companies would do them. But mostly

investors lack interest in further details, and

‘do not want us to spend time producing statistics for nothing.’

Another market disincentive to further reporting is avoiding providing

information to competitors. There is also the fear of misinterpretation:

‘What do measures such as profit per colleague actually show

you, when you’ve got quite different organisations? You can

say something but you can also manipulate the figures and

25

the information in relation to other companies in

benchmarking processes, and then people judge you against

others that have done it very differently.’

Several interviewees indicated that gender equality information was

produced with future employees in mind. Interestingly, Aurora Gender

Capital Management has recently filled this market niche by publishing

information about UK companies gender practices on its publicly

accessible ‘Where women want to work’ web-site. A quarter of our

sample provide information to this website often beyond what they include

in their own reports.

Turning to consumers, despite women making the majority of consumer

decisions (Kingsmill 2001 p.39), our interviewees did not see them driving

reporting on gender issues:

‘Do I believe that more women buy from a particular

organisation because it employs more women? I really don’t

see that.’

‘you sometimes get a [consumer] complaint it’s not normally

related to gender but more likely to be about disability.’

One interviewee explained that advertising is a better way of

communicating with consumers:

‘We’ve very consciously placed adverts with people from

ethnic minorities, people with disabilities, lots of family

26

situations, lots of females. This impacts on the market more

effectively than reporting how many women we employ’.

The supply chain was seen as a potential driver of reporting:

‘I was in a brewers yesterday, and the reason that they

wanted to talk to me about my equality and diversity plans

was because they knew they were rubbish at it … the National

Union of Students (NUS) had asked them for a breakdown of

their workforce and a breakdown of their supply chain. And

they supply tens of thousands of pounds worth of beer to the

NUS each year.’

Another commented that:

‘We’re certainly now starting to ask our suppliers, so it’s

moved one step down the line and that means that

organisations that are ignorant are now being asked the

questions by people they are bothered about, such as

businesses like us who are spending money with them.’

Clearly market drivers count, though their relative significance varied

within our sample.

Civil society drivers

Our companies are not driven by public pressure to report beyond their

policies, programmes and success stories regarding their gender equality

impacts:

‘it’s much more important for us internally to understand the

return from maternity rate, and things like that, and the right

to request (flexible working) application success rate. I feel

27

that we have to understand that because it helps us to

understand the demographics…How many members of the

general public want this information?’

Despite evidence that lobby groups and NGOs have been drivers of CSD

(e.g. Tilt 2004) we found little such evidence for gender reporting. Most

interviewees had never received requests for more information about their

gender equality impacts or consumer issues from women’s NGOs, though

one had been contacted by Fathers Direct. Another indicated that

requests from small NGOs would be unlikely to affect public reporting

even though he probably would supply the NGO with the information.

Although unions periodically request more information, they do not appear

to demand greater public disclosure.

Companies are wary of reporting in what they perceive as a potentially

critical media environment:

‘I might report a 99% return rate from maternity leave -

fantastic story, and I’ll get asked “why don’t the other one

percent come back then?” I’ll get 10, 15, 20, or 30 women to

talk about this and the newspapers will go and try to find the

two women that we’ve treated badly.’

‘…people know that we don’t have any women on our

leadership team, (but) if we put it out in black and white in a

report then all we’d get is more challenge about it – there’d be

a headline in the press saying ‘No woman at the top’ or

something like that! So…why draw attention to something if

it’s not perfect?’

28

Companies are reluctant to reveal that they are doing equal pay reviews

until they have resolved any problems found:

‘If you uncover something you’re going to have to put it right.

And that’s going to lead us in to changing all our incremental

pay scales, and we’re not quite ready to do that as a whole

piece of work yet’.

Another noted generally:

‘The problem is that people want to see progress in

sustainability year on year and sometimes when you’ve seen

massive progress one year you’re not going to see the same

progress the next year’.

This echoes O’Dwyer’s (2002) finding that CSD often made things worse

for companies in the spotlight. Not reporting avoids the problems

associated with being accountable.

Given the perceptions of little public demand for further reporting of

gender equality impacts, and of press hostility, our interviews suggest

that there would need to be significant changes in civil society drivers for

them to encourage greater company disclosure of gender equality

impacts.

29

Government drivers

Many interviewees alluded to the fact that although UK government

agencies (e.g. EOC, DTI) inquire about gender equality workplace issues

and invite companies to policy consultations, there is no legal obligation to

report. Several interviewees thought their companies may report more in

their USA public reports because they are legally required to report data

on women, including ethnic minority and grade information, to

government. One explained they report only global workforce data

except where national legislation determines otherwise (e.g. the USA,

Brazil, South Africa):thus although it conducts UK equal pay reviews it

does not report them.

A ‘softer’ government driver is the requirement to meet certain standards

in order to win public procurement contracts. One interviewee argued

that a good record on gender/diversity in the workplace assisted in

winning government contracts in the USA, and that this drove reporting

there. He said that while companies are increasingly asked for

information about their diversity policies when tendering for UK local

authority contracts and applying for training funding, they are not asked

for evidence of the impact of these. However, another said that she was

asked about diversity in

‘just about every tender with councils…. They ask for policies,

practices and statistics as well.’

30

She said however that this had not been a main driver of the company’s

project to improve human capital monitoring. Several interviewees

believed that the government did not adequately exploit its power to

increase market drivers for monitoring and reporting on gender and

diversity. One believed that if government raised reporting requirements

via the procurement process, this could raise market drivers through the

supply chain.

Organisational imperatives

Our interviews also revealed that the drivers for reporting impact on

companies in different ways, reflecting their own organisational

imperatives. One company was struggling to settle, let alone report, its

KPIs following a recent merger. Others indicated that they were not

approaching their inclusion and diversity strategies through a focus on

strand diversity:

‘I’m actually bothered that we are including as many people as

we can, rather than trying to run projects saying, lets get

three more people with disabilities employed in Edinburgh.’

‘the issue for me in the future is how you report on a more

integrated basis, rather than by issue or diversity strand. It’s

not just about gender equality… the issues about this are quite

similar to the issues on racial equality for example, and it’s

actually about getting cross-over about those sorts of things.

So whilst you’re always going to be aware of your

demographics, we’re finding a much greater integration of our

diversity work so that whilst we still have some parameters

31

under gender it becomes part of the integration for your

overall work.’[xxi]

An interviewee from a company headquartered in two countries explained

that despite collecting a lot of information about the UK workforce,

demographic targets are for global rather than national operations. This

means that despite considerable efforts to improve performance in flexible

working, childcare and equal pay, for example, these are not reported if

there are no global targets or national legislation.

Other organisational considerations for companies headquartered outside

the UK include the absence of a dedicated UK website, investor attention

to the company’s global operations, and the assumption that potential

employees expect to be internationally mobile so don’t require UK data.

The benefits of mandatory reporting or voluntary reporting

guidelines

In the light of these insights into the motivations for non/reporting of

gender issues we asked the interviewees their attitudes to mandatory

reporting and voluntary reporting guidelines. Several interviewees alluded

to the free-rider problem in reporting gender issues:

‘if everyone is not doing it then why should you do it?’

Several interviewees saw regulation as the key to more reporting,

accountability and progress on the issues:

32

‘if we were asked to do it, if there was some kind of

government influence which said you must do this, you must

do that, then we would without a doubt do it’.

‘personally I think it would be quite a good thing to have some

kind of mandatory reporting. I think it would sharpen up

people within organisations who produce the information. I

mean (our company) believes what it says – what we do is

above board, but I’m also quite certain that in other

organisations it’s not quite the same.’

One interviewee argued that reporting about gender equality impacts will

be determined by business priorities and interests, and any civil society

demand for further information should be driven by government:

‘If the government wants to get more women in the workforce

then it should just come out, say it, rattle the cages, give a

figure, say it expects all employers to be at least 15% women

or at least 25% women or whatever …They should be up front

and say it and ask you to report against it.’

This argument was applied to equal pay and the reporting thereof:

‘If the government wants equal pay for women… then it

shouldn’t ask us to do reviews. It should ask us to make pay

equal, and it should describe how it wants to define that pay is

equal, because nobody’s anywhere near that yet.’

So while this interviewee was against mandatory reporting from his

business perspective, he recognised a societal rationale for government to

be more proactive.

33

Others were simply against mandatory reporting: ‘…because it’s a

business cost’.

‘the problem with mandatory reporting is, well are you just

ticking a box? Anyone can do that, but the reporting has to

really link to genuine change within your industry so how do

you do that? How do you measure that? And that’s why you

need all the other things like benchmarks and employee

feedback, and all the genuine things rather than just reporting

for reporting’s sake.’

Following Adams and Harte’s observation that it is ‘possible that firms

need guidance on what to report and what form their disclosure should

take’ (1999:24) we found that even those opposed to mandatory

reporting were often interested in guidance on societal demands for

further gender equality information. One suggested:

‘…in all reporting on social responsibility areas there should be

standard templates for people to report against. Not

necessarily mandatory, but there should be a standard

template for say, the top 500 companies to report against,

when they put it in the annual report rather than going to the

extra expense …of producing a separate report of key data,

and there should be a definition of how to gather that key

data. Otherwise you will get 101 different interpretations and

different analysis of the figures.’

This point was illustrated in discussions on how to report flexible working

conditions given changing company practices:

34

‘Anybody can work from home in the company… We’re

changing from an hours based culture to an output based

culture… we’re no longer interested in whether they’re doing it

from nine till five. So that’s genuine flexible working but it’s

very subtle’.

‘The take up of flexible working hours… would be very difficult

to report, for example my section manager … can balance her

hours during a week, or a month, as she can pop to the shops

if she wants to and can pop to the gym at 10am when it is

empty, and she can come in late because of her child going to

school… But to actually report that individually would be very

difficult. We’ve just opened it up completely. It’s now a way

of life. Her life’s enriched in that way. She’s doing the work

that I want her to do. There’s no problem. It’s just the culture

now’.

For another company the expansion of part-time working was about

downsizing rather than gender policies. They were proud that some

managers now work shorter hours, but they had noticed that the take-up

of part-time and flexible working was ‘very highly female specific’ and saw

no benefit in reporting gender breakdowns. Another noted that the

company would not benefit from reporting gender breakdowns of flexible

working, but had a greater interest in reporting that the introduction of

flexible working had delivered costs savings, made the company more

environmentally friendly and had created increased markets for

communications equipment.

Discussion

35

Our analysis found that the best reporting practice has progressed to

include performance information, including workplace profile, progress in

recruiting, retaining and advancing women reported against clear targets;

detailed information about governance as it relates to gender equality;

and information about employee perceptions on this issue. The best

reporting includes scores achieved in the ON benchmark on gender

equality in the workplace, including the score obtained for impact.

However, despite identifying some excellent reporting practice, our study

reveals that this remains the exception rather than the rule, and that

many companies continue to communicate about policies and programmes

with little indication as to their impact. Without standard practices

company’s reporting is idiosyncratic making comparisons impossible.

Our interviews confirm Larrinaga-Gonzalez et al’s and Adams’ conclusions:

‘In the most proactive organizations identified, controlling the

scope of the environmental disturbance and constructing

public perception of corporate environmental performance,

take precedence over transparency.’(Larrinaga-Gonzalez et al

2001:234)

‘Concerns with image and demonstrating leadership in

reporting practices indicate that reporting in these companies

does not come from a concern to be accountable.’ (Adams

2002:235)

But our interviews also suggest that accountability in the provision of

information about gender issues is regarded in much more driver-specific

36

terms. It is clear that reporting strategies in large part reflect perceptions

of key drivers. These appear to be principally market drivers with more

modest impacts of civil society and governmental drivers. The reporting

deficits can also be explained with reference to these drivers, or their

absence, along with some firm specific organizational factors. Companies

were united in perceiving no market, civil society or government driver for

reporting gender issues in more detail.

‘If we could establish a particular interest, a particular

business need, an interested organisation that would require

the information for their purposes, we would report it, but at

the moment the feedback is that we’ve got enough in the

public domain to keep the majority of people happy, but I

mean the amount of information that we can put in the public

domain is almost unlimited if it’s not corporately sensitive’.

The literature on environmental disclosure has shown that once

investment has been made in improved processes and performance,

quality disclosure secures reputation advantages which cannot be

replicated by competitors offering up mere rhetoric (Hasseldine et al

2005). ‘Specified, quantifiable and verifiable information will be perceived

to be of higher quality’ (Toms 2002:261), and is difficult to replicate by

firms not genuinely committed to good practice. However ‘the process is

mediated by investor expectations’ (Toms 2002:263). Companies

committed to progress on gender equality perceive little advantage to

reporting such quality information, where market, social and

37

governmental drivers do not appear to be either demanding or rewarding

it.

With reference to Adams and McPhail’s conclusions that inadequate

reporting reflects companies’ ‘desire to avoid being held fully

accountable’(2004: 427), our findings also suggest a lack of concern with

accountability for it’s own sake. However, while some interviewees

admitted to non-disclosure due to poor performance, others discussed

positive monitoring and outcomes relating to employee opinions with

gender breakdowns, the details of which they believed no-one is

interested in. Lack of disclosure is partly premised on the view that

further reporting would either be accountable to no-one in particular, or

based on non-comparable data which can hide very different

organisational circumstances, as illustrated in the case of flexible working.

O’Dwyer (2002) argues that CSD becomes difficult to justify from a

societal perspective if it cannot be seen to promote the public as opposed

to the corporate (private) interest. However, attempts by government to

give guidance on best practice reporting on human capital issues have

focussed on helping companies to identify what is material for them to

report on in this field (e.g. DTI 2003, 2004) while noting that stakeholder

interests could be material in the long run (DTI 2004). Gray (2001:12)

suggests that both kinds of information are important in reporting. Adams

and Harte 1999, 2000, and Vogel (2005) note the important role of

38

government in reconciling corporate and public interests especially in the

form of soft, such a reporting, regulation.

When the question of accountability was raised, a number of our

interviewees favoured mandatory reporting, but more favoured voluntary

guidance. The reasons appear to be principally to create a level playing

field, to prompt the laggards into adopting better practices, and to clarify

the information requirements of civil society. Whilst several governments

require companies to report a variety of gender related information either

to the government or publicly[xxii], several studies found high degrees of

non-compliance (e.g. Adams and Harte (1999)) and little government

commitment to monitoring and compliance of such regulation (Day and

Woodward 2004).

A further option is voluntary guidance on what to report. Indeed Sullivan

(2005) has noted the importance of clear goals and performance criteria if

self-regulation is to lead to accountability. On gender issues this could

include the suggestion that reporting on HCM issues which are material to

the business, include gender breakdowns as a matter of course. It could

also give guidance on reporting other gender equality issues that are of

importance to civil society, such as equal pay, job segregation and flexible

working. Gray et al (1996) suggested reporting on compliance with

legislation as a way to progress accountability to society. For gender

issues this could include reporting on compliance with the Equal Pay Act

(1970) and the Sex Discrimination Act (1975).

39

Civil society stakeholders (e.g. women’s NGOs, trade unions) are

important not just in defining reporting content, but also in ensuring that

‘what is reported is acted upon’ (Adams and Harte 2000:20)[xxiii] . Given

their weakness it may make sense for government to invest in capacity

building for civil society organisations working on gender equality in order

to improve engagement with business on these issues. This could make

for a better-informed process of gender mainstreaming in the field of CSR

and SRI benchmarks and systems (see Grosser and Moon 2005).

Conclusions

Our paper has responded to the challenge set by Adams and Harte:

‘Most studies … described the extent of disclosure, rather than

seeking to understand or explain (non) disclosure. Relatively

few studies have attempted to focus on a particular social

issue, or a particular firm, with a view to better understanding

the reasons for (non) disclosure.’ (1999:6)

This study includes an update on disclosure by best practice companies

and interviews with managers in companies which extensively monitor

progress on gender equality. It has addressed not only how progress was

measured, and reported internally, but also the reasons that so little of

the available data was reported publicly. Moreover, the interviews

enabled insights into the drivers that companies identify as significant for

gender equality reporting and the impact of certain organisational

imperatives.

40

Although we found developments in the range of gender issues reported,

we also confirmed a previous finding of a great disparity between

information collected, used internally and communicated to specific

stakeholders on the one hand, and that which gets reported on the other

(see Adams 2004; Adams and Harte 1999; Adams and McPhail 2004). We

thus confirm the conclusion that the ‘the current practice of very limited

reporting arises from a managerial choice’ (Adams and Harte 1999:53).

However we note similar findings relating to the reporting of human

capital more generally (Scarbrough and Elias 2002). Our interviews

provide a relatively nuanced interpretation of the factors behind these

choices. They reflect perceptions of the demand for reporting among a

range of drivers, firm-specific organisational factors, fears of the misuse

and misinterpretation of data as well as ‘poor equal opportunities

performance of firms’ (Adams and Harte 1999:24).

Our findings confirm (Adams et al’s) view that ‘disclosure is an

opportunity for firms to ‘tell their own story’ (1995:102). However the

view of legitimacy theory that firms ‘seek to portray themselves as

behaving in a socially acceptable manner, in return for recognition of their

right to exist’ (1995:103) does not appear to explain the reporting of

gender equality. Rather it is often aimed at attracting and satisfying

employees and meeting the information needs of rating agencies and

investors.

41

Our findings also echo Solomon and Lewis’s (2002) conclusion that

inadequate environmental disclosure within a voluntary reporting

framework is explained, among other things, by an absence both of

demand for information and a legal requirement, and by a fear of

exposure to competitors.

The importance of our approach is that the findings suggest that all three

drivers could usefully be addressed in a wider range of policy choices than

simply whether or not to regulate. The need for clear guidance for

voluntary reporting has emerged as an essential element of the self-

regulatory approach. This raises the question of capacity building among

gender-related NGOs to assist in developing and monitoring either a

mandatory or voluntary reporting regime. Finally the procurement process

was pinpointed by several interviewees. In forthcoming legislation for a

public sector duty to promote gender equality, the UK government

acknowledges the importance of public reporting in accountability systems

(WEU 2005:17) and specifically refers to the inclusion of gender equality

in procurement processes involving the private sector (WEU 2005:22).

Such legislation may offer new opportunities to stimulate greater private

sector reporting in the longer run[xxiv].

Finally, Toms (2002), notes that high quality disclosure may be limited in

that it applies only to limited aspects of company processes. While our

study focused on gender equality in reporting of information about

employees, the business literature has extended the debate to the

42

integration of gender/diversity into organisational culture (Opportunity

Now 2004a), and we also collected data about gender equality in CSR

reporting more broadly, relating to community, marketplace, and core

business impacts. Companies are only just beginning to address these

wider gender impacts and this is an area for further study.

i We would like to thank Opportunity Now for help with access to our sample companies,

and all our interviewees for their time and input. We would also like to thank The

Employers Forum on Disability for assistance with methodology, and Dave Owen and

Marcus Milne for comments relating to this research. ii Monitoring has particularly improved on training, development, appraisal and pay, and

also redeployment and redundancy. Improvements have also been made in monitoring of

employee feedback of their perception of pay equality, although the numbers of

employers who believe that they are doing this effectively remains low at 44%. iii Opportunity Now is a business-led organisation with about 350 members from the

private, public and education sectors aiming to realise the full potential of women at all

levels and in all sectors of the workforce. About half are private sector employers. iv The ON benchmarking scheme gives scores on three aspects of their gender

programmes, ‘Motivate’, ‘Act’ and ‘Impact’. Companies scoring highly on external

communications tended to score highly on the benchmark overall. v More than half of ON employers are not yet satisfied that they are monitoring

effectively. ‘Just 40% of employers are measuring the cost of not getting equality right

(for example measuring turnover and absenteeism) and only 33% are measuring the

impact that gender equality/diversity has made on the organisation (for example higher

customer satisfaction)’ (2004:6). ‘More needs to be done on measuring the impact of

equality on the organisation, both of particular initiatives such as flexible working but

also of the contribution that equality/diversity work as a whole makes to organisational

results’ (2004:7). vi E.g. recognition in Opportunity Now awards and Best Place to Work awards vii These include: The Global Inclusion Benchmark (Employers Forum on Disability,2003),

Opportunity Now benchmarking questionnaire (2003), The Global Reporting Initiative

Reporting Guidelines (GRI,2002), Business in the community (BITC,2003) ‘Indicators

that Count’, BITC survey for CSR Index (2003), BITC guidance notes for CSR Index

(2003), Accounting for People Report (DTI 2003), EOC submission to Accounting for

People Task Force, Women’s Budget Group submission to Accounting for People Task

Force, Equal Opportunities for Women in the Workforce Agency Guidelines in Australia,

(SECTION 709(c), TITLE VII, CIVIL RIGHTS ACT OF 1967 (As Amended by the Equal

Employment Opportunity Act of 1972) Employer Information Report EEO-1) in the USA,

Singh,V. and Vinnicombe,S. (2003),’Women pass a milestone: 101 directorships on the

FTSE 100 Boards’. The Female FTSE Index Report, Cranfield University School of

Management, Calvert Group (2004)’The Calvert Women’s Principles’, Adams,C. and

Harte,G. (1999 and 2000). viii Eight of these interviews were recorded and transcribed, and notes were taken

during the other three. ix Their job titles were: Employment Policy Advisor, Diversity Advisor, Senior

Recruitment Consultant, Diversity Manager, Head of Diversity, Head of Organisational

Development, European Director of Diversity, Head of Employment Policy, Personnel

Director, Corporate Social Responsibility Manager, and Head of a Human Capital

Reporting Project.

43

x Six interviewees were from the banking sector, two from the energy sector, one from

telecoms, one from transport, and one from manufacturing, xi The questionnaire can be obtained from the authors. xii As companies do not usually define ‘management’, these data are hard to compare. xiii This company reports part-timers as a percentage of its male and female workforce. xiv This information is not available to the public, except in aggregated form where

specific companies cannot be identified (SECTION 709(c), TITLE VII, CIVIL RIGHTS ACT

OF 1967 (As Amended by the Equal Employment Opportunity Act of 1972) Employer

Information Report EEO-1). ON employers benchmarking in 2003-4 show more ethnic

minority women employed in the private sector than the public or education sectors in

the UK. No information is reported concerning disabled women, older women, and other

diversity strands. xv ON (2004) reveals that 50% of benchmarking companies claim to effectively monitor

recruitment by gender. xvi UK part-time workers receive on average 40% less training than their full-time

counterparts (EOC 2005) xvii Employers often consult women managers and women’s networks about gender

equality also. xviii One included percentages of discrimination tribunal and litigation cases with details of

outcomes. xix The Female FTSE index is now addressing this issue xx This interviewee specified ‘By market pressure I don’t mean little lobby groups… the

question is are the pension funds or the institutional shareholders really, really asking?

They do ask, but mostly not in great detail’ xxi This parallels some public policy developments e.g.the creation of an integrated

Commission for Equality and Human Rights xxii E.g. the Australian Equal Opportunity for Women in the Workplace Act (1999) requires

companies, public sector and other organisations with 100 or more people to establish a

workplace program to remove the barriers to women entering and advancing in their

organization and to report annually to the Equal Opportunities for Women in the

Workplace Agency giving a workplace profile and details on several key gender issues.

The Canadian Employment Equities Act of 1995 (section 9 (3)) includes similar

requirements for private companies with Federal Government contracts. See paragraph,

page 10 for the USA. xxiii The TUC advises trade union pension fund trustees to request company reporting on a

range of gender/diversity issue including workforce profile and equal pay (TUC 2004). xxiv See for example the CRE website for details of procurement guidance relating to the

public sector duty to promote racial equality.

References

Adams, C. (2002) “Internal organisational factors influencing corporate social and ethical reporting. Beyond current theorizing”, Accounting,

Auditing & Accountability Journal, Vol 15 No 2, pp. 223-250.

Adams, C. (2004) “The ethical, social and environmental reporting-performance portrayal gap”, Accounting, Auditing & Accountability

Journal, Vol 17 No 5, p.731.

Adams, C., Coutts, A. and Harte.G (1995) “Corporate equal opportunities (non-) disclosure”, British Accounting Review, 27, pp. 87-108.

Adams, C and Harte, G (1998) “The changing portrayal of the employment

of women in British banks’ and retail companies’ corporate annual

reports”, Accounting, Organization and Society, Vol 23 No 8, pp. 781-812.

Adams, C. and Harte, G. (1999) “Towards corporate accountability for

equal opportunities performance”, Association of Chartered Certified Accountants, London

Adams, C and Harte, G. (2000) “Making Discrimination Visible: The

Potential for Social Accounting”, Accounting Forum, Vol 24 No 1, pp. 56-79.

Adams, C. and McPhail, K. (2004) “Reporting and the Politics of

Difference: (Non) Disclosure on Ethnic Minorities”, ABACUS, Vol 40, No 3, pp. 405-435.

Benschop, Y. and Meihuizen, H (2002) “Keeping up gendered appearances: representations of gender in financial annual reports”,

Accounting, Organizations and Society, Vol 27 No 7, pp.611-636.

Day, R. and Woodward, T. (2004) “Disclosure of information about employees in the Directors’ report of UK published financial

statements: substantive or symbolic?”, Accounting Forum, Vol 28, pp. 43-59.

DTI (2003). Accounting for People Report. Department of Trade and

Industry. London

DTI. (2004). Draft Regulations on the Operating and Financial Review and Director’s Report. A consultation document. Department of Trade

and Industry. London.

EOC, 2004. Britain’s competitive edge: women. Unlocking the potential,

October 2004.

2

Gray, R (2001) “Thirty years of social accounting, reporting and auditing:

what (if anything) have we learnt?”, Business Ethics: A European Review, Vol 10 No 1, pp. 9-15.

Gray, R., Owen, D. & Adams, C. (1996), Accounting and Accountability:

Changes and Challenges in Corporate Social and Environmental

Reporting, Prentice Hall, Harlow.

Grosser, K. and Moon, J. (2005) “Gender Mainstreaming and Corporate Social Responsibility: Reporting Workplace Issues”, Journal of

Business Ethics, Vol 62 No 4, pp. 327-340.

Hackston, D. and Milne, M. (1996) “Some determinants of social and environmental disclosures in New Zealand companies”, Accounting,

Auditing & Accountability Journal, Vol 9 No 1, pp. 77-109.

Hasseldine, J., Salama, A. and Toms, J. (2005) “Quantity versus quality: the impact of environmental disclosures on the reputations of UK

Plcs”, The British Accounting Review, Vol 37, pp.231-248.

Larrinaga-Gonzalez, C. (2001) “The role of environmental accounting in

organizational change. An exploration of Spanish companies”, Accounting, Auditing & Accountability Journal, Vol 14 No 2, pp. 213-

239.

Milne, J. and Adler, R. (1999) “Exploring the reliability of social and environmental disclosures content analysis”, Accounting, Auditing &

Accountability Journal, Vol 12 No 2, pp. 237-256.

Moon, J (2004a) “CSR in the UK: an explicit model of business – society relations” in

A Habisch, J Jonker, M Wegner, R Schmidpeter (Ed.), CSR Across Europe, Springer-Verlag, Berlin, pp. 51-66.

Moon, J (2004b) “Government as a Driver of Corporate Social

Responsibility: The UK in Comparative Perspective”, International

Centre for Corporate Social Responsibility Working Papers No. 20, University of Nottingham.

O’Dwyer, B. (2002) “Managerial perceptions of corporate social disclosure.

An Irish story”, Accounting, Auditing & Accountability Journal, Vol 15 No 3, pp. 406-436.

O’Dwyer, B. (2003) “Conceptions of corporate social responsibility: the

nature of managerial capture”, Accounting, Auditing & Accountability Journal, Vol 16 No 4, pp. 523-557.

Opportunity Now (2004), Benchmarking report. Diversity at Work:

Tracking Progress on Gender, Opportunity Now, London.

3

Opportunity Now (2004a), Diversity dimensions. Integration into organisational culture, Opportunity Now, London.

Scarbrough, H. and Elias, J. (2002), Evaluating Human Capital, CIPD,

London.

Solomon, A. and Lewis, L. (2002) “Incentives and disincentives for

corporate environmental disclosure”, Business Strategy and the Environment, Vol 11, pp.154-169.

Sullivan, R. (2005) “Self-regulation has serious limits”, News release 29