Embed Size (px)

Citation preview

2015Keeping Culture Alive | Annual Report

President’s Message 01

CEO’s Message 02

Board of Directors 03

A Message from the Board 04

2015 Financials 06

Corporate Profile 40

CONTENTS

I am pleased to present the theme of the 2015 Annual

Meeting…Keeping Culture Alive. The Village Seminar,

Culture Night, Annual Meeting and Banquet will be held

at the Egan Center in the Cook, LaPerouse and Arteaga

Rooms, October 8-10.

As our population ages and we sadly lose fluent Unangam

Tunuu speakers, we recognize the vital importance of

preserving our language and culture. Culture Camps were

developed as a way to preserve and teach the language,

traditional arts, beading, basketry, cooking and dance.

When I was growing up in King Cove there were no

Culture Camps. The first one was held in Unalaska in

1997. Now there are seven every year! Sand Point, King

Cove, Unalaska, St. Paul, Atka, Akutan, Anchorage and,

on occasion, St. George and the Pacific Northwest host

these gatherings that teach our traditions, our language

and keep our heritage alive. Over the years, Culture

Camps have grown in popularity and hundreds of

shareholders and descendants are taking part in them.

With the growing number

of descendants, Culture

Camps have never been more

important than today. The Aleut

Corporation contributes to them

annually, The Aleut Foundation

offers travel scholarships and

a countless number of people

volunteer their talent and time.

Please enjoy the many beautiful photos throughout this

year’s Annual Report showing cultural activities being

performed by our people.

Quyanaa,

Thomas Mack

President

PRESIDENT’S MESSAGE | 1

PRESIDENT’S MESSAGE

AlEuT CORPORATION | 3

Dear Shareholders,

For a corporation’s shareholders, the Annual Report is a very important document. It presents critical information about their company’s performance for the previous year. It is limited however, because it is a look back, not a look forward.

It is no secret that 2015 was a challenging year for the Aleut Corporation. The Board of Directors made dramatic changes to the management team, hiring a new CEO, CFO and Director of Human Resources. This team moved very quickly to understand our operations and the reasons why some TAC subsidiaries had a lackluster performance during the 2015 fiscal year. Compounding this unimpressive performance was the necessary write-off of intangible assets in two of our companies; C&H and Analytica. Though it did not affect our cash position, it did have a nearly $3 million negative impact on our bottom line. An additional blow to the financial statements resulted from the accounting treatment for our Deferred Tax Assets (estimated future tax savings from accumulated net operating losses). This adjustment was over $15 million. This write down of the tax asset did not impact cash nor did it reflect a loss from operations. It is shown solely as an additional income tax expense.

With that said, what are we doing to assure growth and continued improvements to TACs operations? In cooperation with the TAC Board of Directors, we have taken several steps to refocus the company’s efforts. We have

• increased operational scrutiny, review and accountability in our subsidiaries;

• emphasized project profitability among our contracting subsidiaries and reversed a focus on simply revenue;

• instituted an unrelenting focus on profitability, to be achieved through revenue growth, cost management, and improved bidding processes; and

• set benchmarks, strategic plans, and budgets that have allowed us to measure subsidiary progress.

Government Contracting

The primary source of work for AMS and ARS is through federal contracting and working through the Small Business Administration 8(a) program. The government has changed its approach and methodology for federal contracting by Alaska Native Corporations. Management still has confidence in this program, but our companies must evolve and adapt to remain competitive and become more profitable by improving overall gross margin performance, lowering overhead and improving net income.

Other Subsidiaries

C&H Testing continued to struggle in 2015 due the impact of low oil prices. Once oil dropped below $60/bbl much of the company’s work in the Bakersfield market simply dried up. This slowdown was the principal reason for C&H Testing’s 2015 losses. Management has reduced overhead and has shifted resources to its much more successful operations in North Dakota.

TAC’S other major contracting subsidiary, Patrick Mechanical, continues to perform well in its Alaska interior mechanical contracting niche, however it faces challenges related to potential reductions in state-funded projects.

Aleut Enterprise’s fueling operations struggled with diminished volumes and increasing costs. Aleut Real Estate’s investments were modestly profitable and our subsidiary Alaska Instrument, though relatively small, achieved stellar performance in 2015.

We see many areas where performance can be improved in succeeding years. That improvement will not occur overnight. Your new management team is confident and committed to making the changes necessary to assure greater future success.

Sincerely,

Matthew T. FagnaniChief Executive Officer

2 | CEO’S REPORT

CEO’S REPORT

A MESSAGE fROM ThE bOARD | 5

Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy nibh euismod tincidunt ut laoreet dolore magna aliquam erat volutpat. Ut wisi enim ad minim veniam, quis nostrud exerci tation ullamcorper suscipit lobortis nisl ut aliquip ex ea commodo consequat. Duis autem vel eum iriure dolor in hendrerit in vulputate velit esse molestie consequat, vel illum dolore eu feugiat nulla facilisis at vero eros et accumsan et iusto odio dignissim qui blandit praesent luptatum zzril delenit augue duis dolore te feugait nulla facilisi. Nam liber tempor cum soluta nobis eleifend option congue nihil imperdiet doming id quod mazim placerat facer possim assum. Typi non habent claritatem insitam; est usus legentis in iis qui facit eorum claritatem. Investigationes demonstraverunt lectores legere me lius quod ii legunt saepius. Claritas est etiam processus dynamicus, qui sequitur mutationem consuetudium lectorum. Mirum est notare quam littera gothica, quam nunc putamus parum claram, anteposuerit litterarum formas humanitatis per seacula quarta decima et quinta decima. Eodem modo typi, qui nunc nobis videntur parum clari, fiant sollemnes in futurum.

Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy nibh euismod tincidunt ut laoreet dolore magna aliquam erat volutpat. Ut wisi enim ad minim veniam, quis nostrud exerci tation ullamcorper consequat, vel illum dolore eu feugiat nulla facilisis at vero eros et accumsan et iusto odio dignissim qui blandit praesent luptatum zzril delenit augue duis dolore te feugait nulla facilisi. Nam liber tempor cum soluta nobis eleifend option congue nihil imperdiet doming id quod mazim placerat facer possim assum. Typi non habent claritatem insitam; est usus legentis in iis qui facit eorum claritatem. Investigationes demonstraverunt lectores legere me lius quod ii legunt saepius. Claritas est etiam processus dynamicus, qui sequitur mutationem consuetudium lectorum. Mirum est notare quam littera gothica, quam nunc putamus parum claram, anteposuerit litterarum formas humanitatis per seacula quarta decima et quinta decima. Eodem modo typi, qui nunc nobis videntur parum clari, fiant sollemnes in futurum.

Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy nibh euismod tincidunt ut laoreet

minim veniam, quis nostrud exerci tation ullamcorper suscipit lobortis nisl ut aliquip ex ea commodo consequat. Duis autem vel eum iriure dolor in hendrerit in vulputate velit esse molestie consequat, vel illum dolore eu feugiat nulla facilisis at vero eros et accumsan et iusto odio dignissim qui blandit praesent luptatum zzril delenit augue duis dolore te feugait nulla facilisi. Nam liber tempor cum soluta nobis eleifend option congue nihil imperdiet doming id quod mazim placerat facer possim assum. Typi non habent claritatem insitam; est usus legentis in iis qui facit eorum claritatem. Investigationes demonstraverunt lectores legere me lius quod ii legunt saepius. Claritas est etiam processus dynamicus, qui sequitur mutationem consuetudium lectorum. Mirum est notare quam littera gothica, quam nunc putamus parum claram, anteposuerit litterarum formas humanitatis per seacula quarta decima et quinta decima. Eodem modo typi, qui nunc nobis videntur parum clari, fiant sollemnes in futurum.

Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy nibh euismod tincidunt ut laoreet dolore magna aliquam erat volutpat. Ut wisi enim ad minim veniam, quis nostrud exerci tation ullamcorper etiam processus dynamicus, qui sequitur mutationem consuetudium lectorum. Mirum est notare quam littera gothica, quam praesent luptatum zzril delenit augue duis dolore te feugait nunc putamus parum claram, anteposuerit litterarum formas humanitatis per seacula quarta decima et quinta decima. Eodem modo typi, qui nunc nobis videntur parum clari, fiant sollemnes in futurum.

Dick JacobsenBoard Chair

4 | bOARD Of DIRECTORS

Stanley MackDirector

DIck JacOBSenChair

O. PatRIcIa lekanOFF GReGORySecretary / Treasurer

ShaROn lInDDirector

GaRy FeRGuSOnDirector

taRa BOuRDukOFSkyVice Chair

DeBI SchMIDtDirector

vIncent tutIakOFFDirector

JenIFeR SaMuelSOn nelSOnVice President

A MESSAGE fROM ThE bOARD

fINANCIAlS | 76 | fINANCIAlS

MANAGEMENT’S DISCuSSION AND ANAlySIS Of RESulTS Of OPERATIONS AND fINANCIAl CONDITION

Special note regarding forward-looking statements The statements contained are both historical & forward-looking statements. These statements may include management’s expectations, intentions, plans or strategies regarding the future. All forward-looking statements included in this document are based upon information available to the Company on the date hereof, and the Company assumes no obligation to update any such forward-looking statements. Future revenues and profits are influenced by a number of factors, which are inherently difficult to forecast. It is important to note that the Company’s actual results could differ significantly from those described in, or implied from, such forward-looking statements. Any statements related to future operations and financial conditions are subject to risk that could cause the actual results to vary materially from expectations. However, management believes that it has the competitive and financial resources for continued business success in the markets in which it chooses to operate. The following discussion and analysis has been prepared by management to explain the results of operations and financial condition. The Company

The Aleut Corporation (TAC or Company) is a regional Native corporation formed pursuant to the Alaska Native Claims Settlement Act of 1971 (ANCSA). As of March 31, 2015, there were approximately 3,951 shareholders of the Company. The Company’s primary activity is investing and managing in business ventures principally in the following industry segments:

• Federal government operations & maintenance and information technology contracting• Fuel sales, storage and related services• Rental properties• Natural resources• Industrial instrumentation & process control equipment sales• Oil well-testing services• Mechanical contracting and construction• Water quality testing• Hazardous materials analysis, testing, and decommissioning and remediation services

ResulTs of opeRaTions

The Aleut Corporation is reporting the results of operations for the fiscal year (FY) ended March 31, 2015.

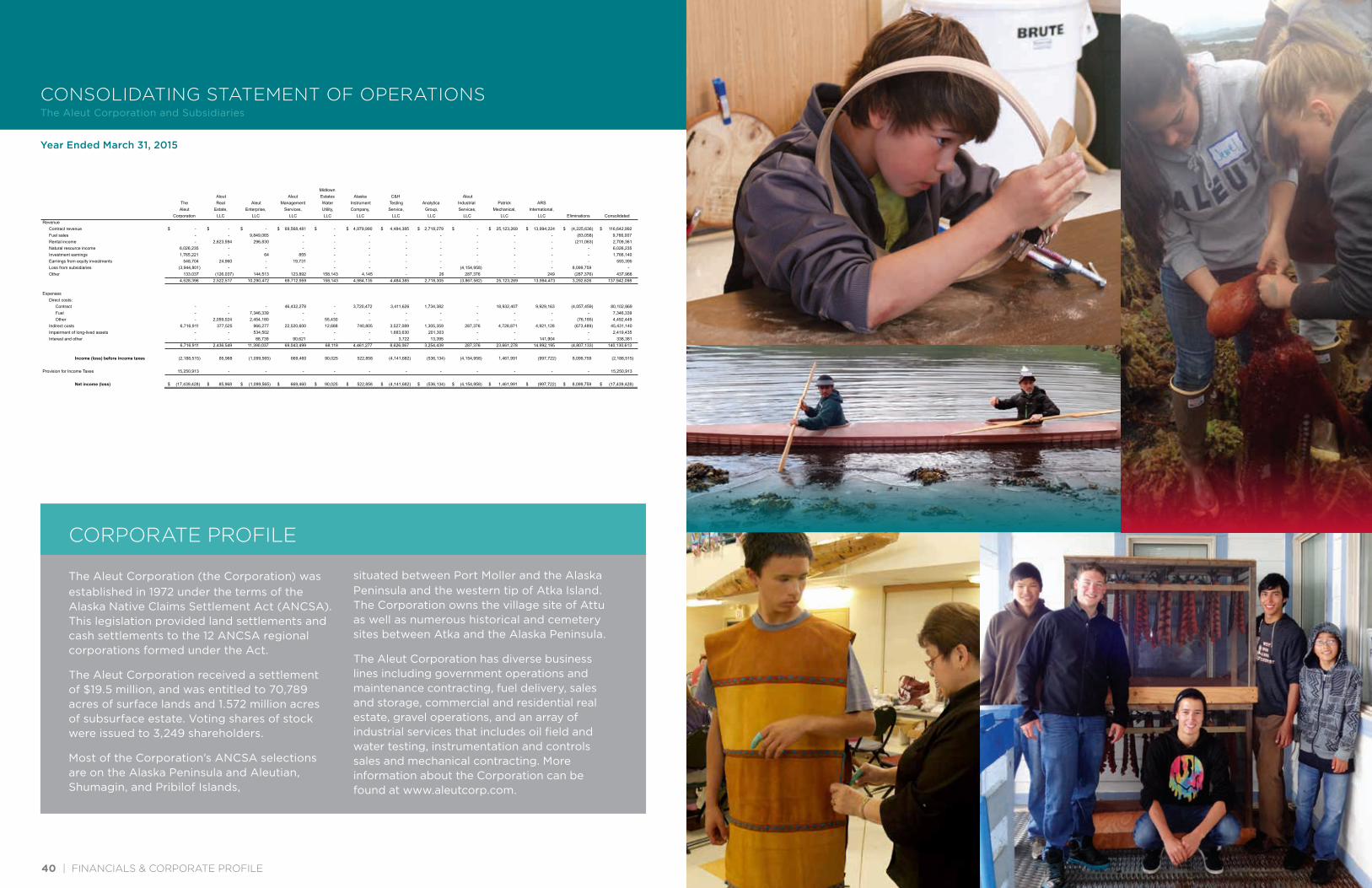

Consolidated gross revenues for FY 2015 totaled $137,942,098 as compared to $120,307,293 and $116,260,627 in FYs 2014 and 2013, respectively. This represents a 14.7% increase in revenues as compared to FY 2014.

Consolidated net loss before taxes for FY 2015 was $(2,188,515) as compared to income of $1,383,930 and $4,774,132 in FY 2014 and 2013, respectively. This represents an earnings decrease of $3,572,445 from FY 2014. Consolidated net loss after taxes for FY 2015 was $(17,439,428) as compared to income of $1,686,621 and $5,422,771 in FYs 2014 and 2013, respectively. The $19,126,049 decrease in net income from FY 2014 to FY 2015 results primarily from (i) $15,250,913 write-down of the deferred tax assets; (ii) impairment of long-lived assets $2,419,435; (iii) lower net incomes from Patrick Mechanical, LLC, Aleut Industrial Services, LLC and Aleut Enterprise, LLC wholly owned subsidiaries; and (iv) lower earnings from certain joint ventures.

The Deferred tax assets were created to reflect the potential tax savings that will result from the use of our Net Operating Losses (NOLS). The NOLs were principally generated by the Adak land transfer of 2004. The larger the income potential of the operations of the Company, the larger will be the potential tax savings from the NOLs and the larger value ascribed to the Deferred Tax Assets. The diminished earnings of the company in 2015 and previous years have required recalculation of the future tax savings and thus the value of the Deferred Tax Assets. This recalculation resulted in the $15,250,913 additional expense recognized in 2015. The Deferred Tax Assets are valued at $49,660,417 in 2015, $64,866,568 in 2014 and $64,545,830 in 2013.

ConTRaCT Revenue

Contract revenue represents the largest share of revenue of the Company’s business lines. Contract revenue comes from: (i) Aleut Management Services, LLC (AMS), which operates in the federal contracting arena; (ii) Aleut Industrial Services, LLC (AIS), which provides oil and well testing services, drinking and wastewater analytical services, and sales of instrumentation and process control products; (iii) Patrick Mechanical, LLC (PM), which provides engineering, design, and construction of complex piping and HVAC systems and (iv) ARS International, LLC (ARS), which provides hazardous and non-hazardous testing, analysis and decommissioning and remediation services.

2015Financials

fINANCIAlS | 98 | fINANCIAlS

MANAGEMENT’S DISCuSSION AND ANAlySIS Of RESulTS Of OPERATIONS AND fINANCIAl CONDITION

MANAGEMENT’S DISCuSSION AND ANAlySIS Of RESulTS Of OPERATIONS AND fINANCIAl CONDITION

CommeRCial and ResidenTial RenTal pRopeRTies (exclusive of fuel storage rental income)

The Company, through its wholly-owned subsidiary, Aleut Real Estate, LLC (ARE), has various real estate (commercial and residential) properties in Alaska (Anchorage, Adak, and Valdez) and Colorado (Colorado Springs).

In FY 2015, ARE had rental income of $2,623,594 as compared to $2,805,685 and $2,769,732 in FYs 2014 and 2013, respectively. This is a decrease of $182,091 or 6% lower compared to the prior year. Also, in FY 2015, ARE generated $24,960 of joint venture and other income as compared to $225,440 in the prior year. In FY 2015, ARE had net income of $85,968 as compared to $211,270 and $1,104,519 in FYs 2014 and 2013 respectively. This is a decrease of $125,302 or 59% lower compared to the prior year. The primary reason for the decrease was a lack of a special dividend from joint ventures in FY 2015; whereas, in FY 2014, a special dividend of $175,500 was declared and paid. Additionally, in FY 2015 a loss of $126,037 was incurred for the sale of vacant lot in Colorado Springs.

The Company also has a 50% interest in Black Brandt, LLC, a real estate holding company that has two real estate property holdings in Colorado and two property holdings in the Seattle, WA area. In FY 2015, Black Brandt generated $348,704 of income as compared to $313,442 and $405,630 in FYs 2014 and 2013, respectively.

naTuRal ResouRCes, invesTmenTs, and oTheR inCome

Natural Resources In FY 2015, 7(i) revenue sharing from the other Alaskan Native Regional Corporations totaled $5,781,246 compared to $4,692,449 and $3,852,583 in FYs 2014 and 2013, respectively. This is an increase of $1,088,797 or 23% higher compared to the prior year. The primary sources of 7(i) revenues come from NANA and ASRC.

In FY 2015, the Company had gravel revenue of $115,010 as compared to $409,846 and $378,493 in FYs 2014 and 2013, respectively. This is a decrease of $294,836 or 72% lower compared to the prior year. Gravel sales are primarily derived from the material management agreements between the Company and four Village Corporations in the Aleut region that have quarry operations (Shumagin Corporation, King

Cove Corporation, Tanadgusix Corporation, and Ounalashka Corporation).

Investment Earnings The Company has investment earnings primarily through money market accounts, bonds, and marketable securities. For FY 2015, investment earnings were $1,766,140 compared to $1,029,832 and $1,375,856 in FYs 2014 and 2013, respectively. This is an increase of $736,308 or 71% higher than the prior year. Investment earnings include income from the Company’s Permanent Fund.

The Company established the Permanent Fund on April 1, 1992. The goal of the Permanent Fund is to provide a cushion and diversification against the occasionally unpredictable operating performance. The Permanent Fund serves as a fund for future use for funding shareholder dividends and charitable contributions to The Aleut Foundation. Earnings of the Permanent Fund are reinvested in the fund. Withdrawals from the Permanent Fund require Board approval.

As of March 31, 2015, the market value of the Permanent Fund was $13,775,474, which is an increase of $807,485 or 6% higher as compared to the market value of $12,967,989 a year ago. In FY 2015, the Permanent Fund was invested with an asset allocation of 49% to fixed income and 51% to equity. The Company also had other marketable securities of $21,300,750 as compared to $20,507,393 in FY 2014. This represents an increase of $793,357 or a 4% increase over the prior year. The other securities are conservatively invested at 66% fixed income and 34% equity. The Company anticipates that the Permanent Fund will continue to grow over the long term. Past performance is, however, no guarantee of future performance.

ChaRiTable ConTRibuTions

The Company made contributions in FY 2015 to charitable and not-for-profit organizations that benefit shareholders and their descendants totaling $1,099,008 compared to $1,432,862 and $1,003,937 in FYs 2014 and 2013, respectively. This is a decrease of $333,854 or 23% lower as compared to the prior year. Of this amount in FY 2015, $900,000 was given to The Aleut Foundation as compared to $1,200,000 and $800,000 given in FYs 2014 and 2013, respectively. These amounts do not include the Company’s burial assistance subsidy program that is run through The Aleut Foundation. The Aleut Foundation also provides scholarships to the Company’s

Aleut Management Services, LLC (AMS) Of the four sources of contract revenue, AMS represents the largest portion. In FY 2015, AMS had contract revenue of $69,568,481 as compared to $52,057,755 and $44,977,707 in FYs 2014 and 2013, respectively. This represents an increase of $17,510,726 or 34% higher than the prior year. In FY 2015 AMS had a net income of $669,460 as compared to $913,291 and $302,544 in FYs 2014 and 2013, respectively. This is a decrease of $243,831 or 27% lower as compared to the prior year.

Aleut Industrial Services, LLC (AIS) In 2009, the Company created Alaska Industrial Services, LLC (AIS) as a wholly-owned subsidiary. AIS is a holding company that serves as the parent company for Alaska Instrument Company, LLC (AIC), C&H Testing Service, LLC (C&H), and Analytica Group, LLC (AG). AIC is a manufacturer’s representative for instrumentation and process control products used in industrial operations (such as oil and gas operations), and is located in Anchorage, Alaska. C&H’s primary operation is well-testing services for the oil industry, and is located in California (Bakersfield and Signal Hill) and Dickinson, North Dakota Analytica Group LLC (AG) is a state certified water testing laboratory with offices in Alaska (Anchorage, Fairbanks, and Wasilla) and Colorado.

After March 31, 2015, the company has ceased using AIS as a holding company for other operating subsidiaries. The operations of AG have been transferred to become part of ARS. C&H and AIC have both become direct subsidiaries of Aleut Corporation. The AIS corporate shell will be retained for possible future use.

For FY 2015, AIS had contract revenues of $12,182,654 as compared to $12,235,664 and $13,764,850 in FYs 2014 and 2013, respectively. This is a decrease of $53,010 or 0.4% lower, as compared to the prior year. In FY 2015, AIS had a net loss of $(4,154,958) as compared to a net loss of $(2,200,128) and a net income of $(590,654) in FYs 2014 and 2013, respectively. This is a decrease of $1,954,830 as compared to the prior year. The primary reason for the decrease is the $1,884,993 impairment of intangible assets expensed in FY 2015.

Patrick Mechanical, LLC (PM) In October 2011, the Company acquired 100% of PM, which is a mechanical contracting company that specializes in engineering, design and construction of complex piping and HVAC systems primarily in and around Fairbanks, Alaska.

For FY 2015, PM had contract revenues of $25,123,269 as compared to $25,246,337 and $33,997,651 in FYs 2014 and 2013, respectively. This is a decrease of $123,068 compared to the prior year. For FY 2015, PM had a net income of $1,461,991 compared to $2,921,715 and $7,169,094 in FYs 2014 and 2013, respectively. This represents a decrease of $1,459,724 or 50% under the prior year. The primary reason for the decrease is the early adoption of ASU No. 2014-02 to amortize Goodwill and an earn-out increase of $209,267 over the increase from FY2014. In FY 2015 $757,407 of Goodwill was amortized which was not done in previous years.

ARS International, LLC (ARS) On June 1, 2014, the Company acquired 100% of ARS, which performs laboratory analysis, field testing, surveys for radioactive materials, decommissioning services for structures containing hazardous and non-hazardous materials, and land remediation and waste disposal project management services. ARS is headquartered in Port Allen, Louisiana.

For FY 2015, ARS had contract revenues of $13,994,224 as compared to $6,685,822 for the 10 months ending FY 2014. This is an increase of $7,308,402 or 109% higher as compared to the prior year. ARS had a net loss of $(997,722) for FY 2015 compared to $(1,610,207) for FY 2014. This represents an improvement of $612,485 from the prior year.

fuel sales, sToRage, and RelaTed aCTiviTies

In FY 2015, through a wholly-owned subsidiary, Aleut Enterprise, LLC (AE), had fuel sales, leasing and other revenues of $10,290,408 compared to $12,063,704 and $13,015,767 in FYs 2014 and 2013, respectively. This is a decrease of $1,773,296 or 15% lower compared to revenues of the prior year. The decrease is primarily coming from lower fuel revenue of $9,849,065 in FY 2015 compared to $10,919,755 in FY 2014. AE had a net loss of $(1,099,565) compared to income of $279,899 and a net loss of $(2,790,622) in FYs 2014 and 2013, respectively. This is a decrease of $1,379,464 compared to the prior year. This decrease is due to (i) the impairment of a long-lived asset in FY 15 of $534,502 of Adak Marine Services Fuel (a wholly-owned subsidiary of AE) (ii) the diminished business volume, (iii) a $198,797 in additional medical insurance costs due to cessation of self-funded plan.

10 | fINANCIAlS

MANAGEMENT’S DISCuSSION AND ANAlySIS Of RESulTS Of OPERATIONS AND fINANCIAl CONDITION

shareholders and descendants, along with career development opportunities, internships, and other programs and services. In FY 2015, The Aleut Foundation awarded 207 scholarships that totaled $708,803. The Aleut Foundation also provided community development training programs for 41 individuals and funded 18 shareholders and descendants to attend culture camps, three individuals to attend AFN, and four high school students to attend the Future Leaders Summit.

disTRibuTions and eldeR benefiTs

In February 2015, the Company declared dividends of $4.00 per share as compared to $7.00 and $6.00 per share in FYs 2014 and 2013, respectively. This is a decrease of $3.00 per share or 43% lower than the prior year. In February 2015, the Company also declared elder benefits of $500 per elder, which was the same amount in FYs 2014 and 2013. As of March 31, 2015, there were 1,001 elders as compared to 959 and 905 in FYs 2014 and 2013, respectively. Thus, the total amount of distributions declared in FY 2015 was $1,800,100 as compared to $2,753,800 and $2,401,900 in FYs 2014 and 2013, respectively.

In FY 2015, the Company also received 7j distributions of $5,781,246or ($17.79 per shareholder) compared to $4,692,449 ($14.44 per shareholder) and $3,852,583 ($11.86 per shareholder) in FYs 2014 and 2013, respectively. This is an increase of $1,088,797 ($3.35 per shareholder) as compared to the prior year.

financial Condition asseTs and liabiliTies

As of March 31, 2015, consolidated assets of the Company were $189,643,713, which is a decrease of $12,689,897 or 6% lower as compared to $202,333,610 as of March 31, 2014. This decline is principally due to the valuation reduction on the deferred tax asset.

As of March 31, 2015, total liabilities of the Company were $41,229,808, which is $6,549,631 or 19% higher compared to total liabilities of $34,680,177 as of March 31, 2014. The increase is primarily related to changes in:

(i) Accounts payable of $15,426,779 as of March 31, 2015 as compared to $10,752,348 a year ago. The increase is primarily related to a larger 7(j) liability and large year-

end fuel purchase.(ii) Accrued expenses of $10,775,253 as of March 31, 2015 as compared to $8,119,459 a year ago. The increase is primarily due to AMS increased contract activity. (iii) Contingent earn-out escrow payable of $5,109,267 as of March 31, 2015 as compared to $4,630,000 as of March 31, 2014. This item is in connection with the acquisition of Patrick Mechanical, LLC and ARS International, LLC.

liquidiTy and CapiTal ResouRCes

Management believes The Aleut Corporation is capable of funding its future cash needs with the cash generated from its operations, and with the careful use of established lines of credit. As of March 31, 2015, the Company maintained two lines of credit: (i) a $10,000,000 secured line of credit with Wells Fargo; and (ii) a $5,000,000 line of credit with Northrim Bank for the purposes of funding fuel purchases by AE.

In FY 2015, net cash provided by operations was $6,103,748 which was $14,037,909 more than 2014 & $4,578,424 in 2013. After investing and financing activities, cash and cash equivalents increased on March 31, 2015 by $4,465,910 from the previous year. The primary driver for the cash movement was operations.

Cash and cash equivalents do not include the Company’s Permanent Fund and other marketable securities. As of March 31, 2015, cash and cash equivalents and marketable securities (not including those in the Company’s Permanent Fund) totaled $43,408,925, which is an increase of $5,259,267 or 14% higher as compared to $38,149,658 as of March 31, 2014. The Company plans to utilize these resources to pay future dividends, fund shareholder programs, and grow the company for future generations by pursuing opportunities that provide a stable and growing stream of income in perpetuity.

fINANCIAlS | 11

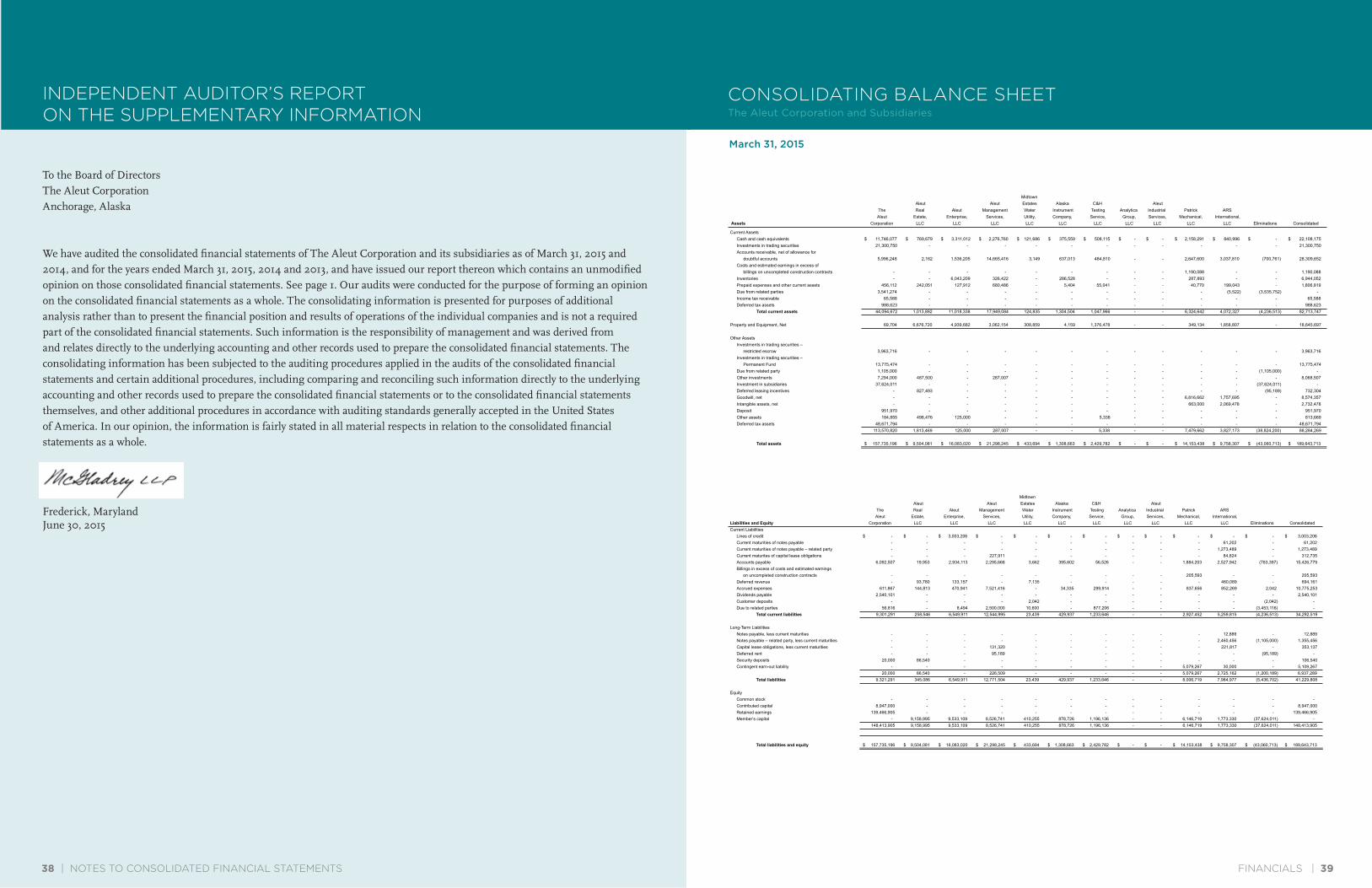

INDEPENDENT AuDITOR’S REPORT

To the Board of DirectorsThe Aleut CorporationAnchorage, Alaska

RepoRT on The finanCial sTaTemenTs We have audited the accompanying consolidated financial statements of The Aleut Corporation and its subsidiaries which comprise the consolidated balance sheets as of March 31, 2015 and 2014, and the related consolidated statements of operations, changes in equity and cash flows for the years ended March 31, 2015, 2014 and 2013, and the related notes to the consolidated financial statements.

managemenT’s ResponsibiliTy foR The finanCial sTaTemenTs Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

audiToR’s ResponsibiliTy Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

opinionIn our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of The Aleut Corporation and its subsidiaries as of March 31, 2015 and 2014, and the results of its operations and its cash flows for the years ended March 31, 2015, 2014 and 2013, in accordance with accounting principles generally accepted in the United States of America.

Frederick, MarylandJune 30, 2015

ThE AlEuT CORPORATION AND SubSIDIARIES | 1312 | ThE AlEuT CORPORATION AND SubSIDIARIES

CONSOlIDATED bAlANCE ShEETS March 31, 2015 and 2014

CONSOlIDATED bAlANCE ShEETS Continued March 31, 2015 and 2014

Assets 2015 2014 Current Assets Cash and cash equivalents $ 22,108,175 $ 17,642,265 Investments in trading securities 21,300,750 20,507,393 Accounts receivable, net of allowance for doubtful accounts 28,309,652 23,758,489 Costs and estimated earnings in excess of billings on uncompleted construction contracts 1,190,088 657,597 Inventories 6,944,052 6,302,176 Prepaid expenses and other current assets 1,806,819 906,171 Income tax receivable 65,588 65,588 Deferred tax asset 988,623 1,382,629 Total current assets 82,713,747 71,222,308 Property and Equipment, net 18,645,697 20,303,394 Other Assets Investments in trading securities – restricted escrow 3,963,716 3,836,412 Investments in trading securities - Permanent Fund 13,775,474 12,967,989 Other investments 8,068,507 10,930,072 Deferred leasing incentives 732,304 841,588 Goodwill, net 8,574,357 11,411,997 Intangible assets, net 2,732,478 5,546,422 Deposit 951,970 950,918 Other assets 813,669 838,571 Deferred tax asset 48,671,794 63,483,939 88,284,269 110,807,908

Total Assets $ 189,643,713 $ 202,333,610 See Notes to Consolidated Financial Statements.

See Notes to Consolidated Financial Statements.

Liabilities and Equity 2015 2014

Current Liabilities Lines of credit $ 3,003,206 $ 2,366,907 Current maturities of notes payable 61,202 300,199 Current maturities of notes payable – related party 1,273,489 670,617 Current maturities of capital lease obligations 312,735 267,702 Accounts payable 15,426,779 10,752,348 Billings in excess of costs and estimated earnings on uncompleted construction contracts 205,593 276,333 Deferred revenue 694,161 931,757 Accrued expenses 10,775,253 8,119,459 Dividends payable 2,540,101 3,615,187 Total current liabilities 34,292,519 27,300,509 Long-Term Liabilities Note payable, less current maturities 12,889 55,545 Notes payable – related party, less current maturities 1,355,456 1,963,328 Capital lease obligations, less current maturities 353,137 588,624 Security deposits 106,540 142,171 Contingent earn-out liability 5,109,267 4,630,000 6,937,289 7,379,668 Total liabilities 41,229,808 34,680,177

Commitments and Contingencies (Note 18) Equity Common stock: Class A; no par value; 1,000,000 shares authorized; 236,100 shares issued and outstanding – – Class B; no par value; 1,000,000 shares authorized; 88,800 shares issued and outstanding – – Contributed capital 8,947,000 8,947,000 Retained earnings 139,466,905 158,706,433 148,413,905 167,653,433 Total liabilities and equity $ 189,643,713 $ 202,333,610

ThE AlEuT CORPORATION AND SubSIDIARIES | 1514 | ThE AlEuT CORPORATION AND SubSIDIARIES

CONSOlIDATED STATEMENTS Of OPERATIONSyears ended March 31, 2015, 2014 and 2013

CONSOlIDATED STATEMENTS Of ChANGES IN EquITy years ended March 31, 2015, 2014 and 2013

2015 2014 2013Revenue: Contract revenue $ 116,642,992 $ 95,960,892 $ 92,649,208 Fuel sales 9,766,007 10,803,834 12,466,526 Rental income 2,709,361 3,149,322 2,785,566 Natural resource income 6,026,235 5,172,295 4,296,076 Investment earnings 1,766,140 1,029,832 1,375,856 Earnings from equity investments 593,395 2,415,634 1,236,550 Other 437,968 1,775,484 1,450,845 137,942,098 120,307,293 116,260,627 Expenses: Direct costs: Contract 80,102,869 63,930,797 54,896,311 Fuel 7,346,339 8,130,841 9,798,550 Other 4,492,449 4,652,670 4,937,569 Indirect costs 45,431,140 41,885,338 39,974,125 Impairment of long-lived assets 2,419,435 – 1,785,000 Interest and other 338,381 323,717 94,940 140,130,613 118,923,363 111,486,495 Income (loss) before income taxes (2,188,515) 1,383,930 4,774,132 Provision for Income Taxes (Benefit) 15,250,913 (302,691) (648,639) Net income (loss) $ (17,439,428) $ 1,686,621 $ 5,422,771 Basic and Diluted Income (Loss) Per Share – Based on 324,900 Weighted Average Shares Outstanding in 2015, 2014 and 2013 $ (53.68) $ 5.19 $ 16.69 See Notes to Consolidated Financial Statements.

Contributed Capital Retained Earnings Total Equity

Balance, March 31, 2012 $ 8,947,000 $ 156,752,741 $ 165,699,741

Net income – 5,422,771 5,422,771 Divendends declared – (2,401,900) (2,401,900)

Balance, March 31, 2013 8,947,000 159,773,612 168,720,612

Net Income – 1,686,621 1,686,621 Divendends declared – (2,753,800) (2,753,800)

Balance, March 31, 2014 8,947,000 $ 158,706,433 $ 167,653,433

Net loss – (17,439,428) (17,439,428) Divendends declared – (17,439,428) (1,800,100)

Balance, March 31, 2015 $ 8,947,000 $ 139,466,905 $ 148,413,905

See Notes to Consolidated Financial Statements.

ThE AlEuT CORPORATION AND SubSIDIARIES | 1716 | ThE AlEuT CORPORATION AND SubSIDIARIES

CONSOlIDATED STATEMENTS Of CASh flOwSyears ended March 31, 2015, 2014 and 2013

CONSOlIDATED STATEMENTS Of CASh flOwS Continued

years ended March 31, 2015, 2014 and 2013

2015 2014 2013Cash Flows from Operating Activities Net income (loss) $ (17,439,428) $ 1,686,621 $ 5,422,771 Adjustment to reconcile net income (loss) to net cash provided by (used in) operating activities: Depreciation and amortization 6,769,655 4,534,208 4,221,352 (Gain) loss on disposition of property and equipment 387 (29,453) (816,537) Income from equity investments (593,395) (2,415,634) (1,236,550) Deferred incom e taxes (benefit) 15,206,151 (320,738) (672,620) Allowance for doubtful accounts (100,980) 18,526 349,630 Realized gains on investments (430,034) (786,415) (275,855) Unrealized (gains) losses on investments (432,109) 525,925 (378,331) Impairment losses on long-lived asxsets 2,419,435 – 1,785,000 Deferred leasing incentives 109,284 (392,874) 56,581 Financed interest on notes payable – related party 102,900 57,781 – Increase in contingent earn-out liability 479,267 470,000 1,620,000 Changes in assets and liabilities: (Increase) decrease in: Investments in trading securities (469,991) (4,085,566) (5,360,267) Accounts receivable (4,450,183) (4,308,730) 7,196,615 Costs and estimated earnings in excess of billings on uncompleted construction contracts (532,491) (216,299) 438,210 Inventories (641,876) (996,279) 291,002 Prepaid expenses and other current assets (900,648) (30,078) (36,559) Income tax receivable – – 13,814 Deposit (1,052) (950,918) – Other assets 149,902 – (1,540) Increase (decrease) in: Accounts payable 4,674,431 (904,466) (3,985,666) Billings in excess of costs and estimated earnings on uncompleted construction contracts (70,740) (122,996) (1,061,491) Deferred revenue (237,596) 135,167 390,792 Accrued expenses 2,528,490 193,274 (6,390,889) Security deposits (35,631) 4,783 (44,138) Net cash provided by (used in) operating activities 6,103,748 (7,934,161) 1,525,324 Cash Flows from Investing Activities Proceeds from sale of property and equipment 4,425 778,439 4,836,176 Purchase of property and equipment (1,928,757) (1,788,761) (2,516,789) Distributions from other investments 3,454,960 11,909,107 3,162,987 Proceeds from sale of trading securities – Permanent Fund 2,487,770 4,275,599 2,579,432 Purchase of trading securities – Permanent Fund (2,756,478) (4,544,132) (2,883,913) Purchase of other investments – (2,312,372) (487,500) Net increase in trading securities – restricted escrow – 2,843 (2,843) Acquisition of wholly-owned subsidiary, net of cash acquired – (2,583,728) (199,712) Net cash provided by investing activities 1,261,920 5,736,995 4,487,838

(Continued)

2015 2014 2013Cash Flows From Financing Activities Net borrowings (repayments) on lines of credit 636,299 1,715,483 (1,089,643) Proceeds from long-term borrowings 98,440 106,593 – Principal payments on notes payable (380,093) (351,989) (128,167) Principal payments on notes payable related parties (107,900) (109,736) – Principal payments on capital lease obligations (271,318) (158,128) – Shareholder dividends paid (2,875,186) (2,098,848) (2,092,097) Net cash used in financing activities (2,899,758) (896,625) (3,309,907) Net (decrease) increase in cash 4,465,910 (3,093,791) 2,703,255 Cash and Cash Equivalents: Beginning 17,642,265 20,736,056 18,032,801 Ending $ 22,108,175 $ 17,642,265 $ 20,736,056 Supplemental Disclosures of Cash Flow Information Cash paid for: Interest $ (441,281) $ 265,936 $ 94,940 Income taxes $ 44,762 $ 18,047 $ 45,167 Cash received from: Income taxes $ – $ – $ 35,000 Supplemental Schedule of Noncash Investing and Financing Activities Acquisition of wholly-owned subsidiary: Working capital acquired, net of cash and cash equivalents of $416,272, $90,388 respectively $ – $ (71,526) $ (309,323) Long-term debt assumed – (3,057,406) (357,801) Fair value of other assets acquired: Property and equipment – 867,068 435,533 Other investments – 35,000 – Identifiable intangible assets – 3,267,597 230,000 Goodwill – 1,952,995 201,303 Contingent consideration payable – (410,000) – Cash paid for acquisition of wholly-owned subsidiary, net of cash acquired $ – $ 2,583,728 $ 199,712

Capital lease obligations incurred for purchase of property and equipment $ 80,864 $ 1,014,454 $ – Notes payable – related party incurred to finance interest expense $ 102,900 $ 57,781 $ – Book value of property and equipment transferred to inventory $ – $ 125,833 $ – Book value of property and equipment transferred to assets held for sale $ 659,502 $ 125,833 $ –

Accrued earnings on trading securities – restricted escrow $ 127,304 $ 136,412 $ –

See Notes to Consolidated Financial Statements.

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS | 1918 | NOTES TO CONSOlIDATED fINANCIAl STATEMENTS

NOTES TO CONSOlIDATED fINANCIAl STATEMENTSthe aleut corporation and Subsidiaries

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS Continued

the aleut corporation and Subsidiaries

noTe 1. naTuRe of business and signifiCanT aCCounTing poliCies

nature of business: The Aleut Corporation (the Company) is a regional native corporation formed pursuant to the Alaska Native Claims Settlement Act of 1971 (ANCSA or the Act). The Company operates as a managed holding company with corporate headquarters in Anchorage, Alaska. The Company manages natural resources income received from surface and subsurface rights obtained pursuant to ANCSA, participates in various partnerships, joint ventures and other business investments, including marketable and nonmarketable securities, and operates subsidiaries engaging in a variety of businesses as follows:

aleut Real estate llC (aRe): ARE primarily engages in the business of ownership and management of commercial real estate and the management of assets received under the ANCSA as well as other lands acquired. Real estate properties include commercial holdings in Anchorage, Valdez, and Adak, Alaska, and Colorado Springs, Colorado.

aleut enterprise, llC (ae): AE was formed primarily to assist in the privatization of the former U.S. Navy base on Adak Island, Alaska, and to develop commercial ventures on Adak in anticipation of the transfer of Adak Island land and facilities to the Company. AE conducts a significant portion of its business activity through fuel sales and storage services, port related services, and the rental of a fish processing plant.

aleut management services, llC (ams): AMS operates in the federal contracting arena providing services supporting a variety of Federal Agencies such as Department of Defense, Department of Homeland Security and General Services Administration, as well as civilian customers. Such services include communications, IT, system engineering, base supply, launch support, base operations services, maintenance and repair services, technology and technology support services, facilities management and support services, and other operations and support services.

midtown estates Water utility, llC (meWu): MEWU operates the water utility for a subdivision Midtown Estates in Palmer, Alaska. The subsidiary is considered to be a Class C public utility by the State of Alaska and, as a result, is subject to regulatory reporting, rate approval, and compliance statutes monitored by the Regulatory Commission of Alaska (RCA) (AS 42.05, Public Utilities).

aleut industrial services, llC (ais): AIS was a managed holding company who owned operating subsidiaries through March 31, 2015. On March 31, 2015, AIS was dissolved and ownership of its subsidiaries was transferred directly to the Company who continues to operate as follows:

C&h Testing services llC (C&h): C&H primarily engages in providing oil and well testing services based in Bakersfield, California, and Dickinson, North Dakota.

alaska instrument Company, llC (aiC): AIC is primarily engaged in the retail sales of instrumentation and process control products.

analytica group, llC (ag): Through February 2015, AG was engaged in providing drinking and waste water analytical services. On February 16, 2015, the Company dissolved AG and transferred its assets to another subsidiary, ARS International, LLC.

patrick mechanical, llC (pm): PM is a mechanical contracting company that specializes in engineering, design and construction of complex piping and HVAC systems.

aRs international, llC (aRs): On June 1, 2013, the Company acquired ARS (as further discussed in Note 22) who performs laboratory analysis, field testing and surveys for radioactive materials, and provides decommissioning services for structures containing both hazardous and non-hazardous materials as well as land remediation and waste disposal project management services.

The Company elected to early adopt Financial Accounting Standards Board (FASB) Accounting Standards Update (ASU) No. 2014-08, Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360): Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity, and has not reported the disposal of AIS and AG as discontinued operations since they do not represent a strategic shift that has a major effect on the Company’s operations and financial results. AG’s gross revenue and net loss for the years ended March 31, 2015 and 2014, was $2,718,305 and $(536,134), $3,061,249 and $(748,678), respectively. AG’s gross revenue and net loss for the period June 15, 2012 (date of acquisition) to March 31, 2013, was $2,453,848 and $(116,134), respectively. As a managed holding company, AIS’s revenue and net loss were eliminated during consolidation.

A summary of the Company’s significant accounting policies follows:

principles of consolidation: The consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries – Aleut Real Estate, LLC; Aleut Enterprise, LLC and its wholly-owned subsidiaries; Aleut Management Services, LLC and its wholly-owned subsidiaries; Midtown Estates Water Utility, LLC; Aleut Industrial Services, LLC and its wholly-owned subsidiaries; Patrick Mechanical, LLC, and ARS International, LLC and its wholly-owned subsidiaries. All material intercompany balances and transactions have been eliminated in consolidation.

Revenue and cost recognition: The Company and its subsidiaries are engaged in three types of contracts with the federal government and its prime contractors. Revenue from cost-type contracts is recognized on the basis of reimbursable costs incurred during the period, plus the fee earned. Revenue from time-and-material contracts is recognized on the basis of hours worked, multiplied by billable rates provided, plus other reimbursable contract costs incurred during the period. For revenue from firm-fixed- price contracts, the Company evaluates its contracts for multiple deliverables, which may require segmentation of each deliverable into separate accounting units for proper revenue recognition. On certain firm-fixed-price federal contracts, along with all construction contracts, revenue is recognized under the percentage-of-completion method. Under this method, individual contract revenue earned is based upon the percentage relationship that contract costs incurred bear to management’s estimate of total contract costs. Because of inherent uncertainties in estimating costs, it is at least reasonably possible that the estimates used will change within the near term. On other fixed-price federal contracts, revenue is recognized ratably over the contract term based on proportional performance or straight-line, as appropriate.

Contract costs include direct materials, subcontract costs, direct labor, combined with allocations of operational overhead and other direct costs. The provision for estimated losses on uncompleted contracts is made in the period in which such losses are determined. Changes in job performance, job conditions and estimated profitability may result in revisions to costs and revenue and are recognized in the period in which the revisions are determined.

The asset, costs and estimated earnings in excess of billings on uncompleted construction contracts, represents revenues

recognized in excess of amounts billed. The liability, billings in excess of costs and estimated earnings on uncompleted construction contracts, represents billings in excess of revenues recognized.

Revenue from fuel sales, industrial products, lab testing and other services is recognized at the time the service or fuel is delivered or provided to the customer.

Leasing revenue is recognized on a straight-line basis over the lease term. Recognition of rental income commences when control of the facility has been given to the tenant. Cost reimbursement income from pass-through expenses is recognized on an accrual basis over the periods in which the expenses were incurred. Pass-through expenses are comprised of real estate taxes, operating expenses and common area maintenance costs which are reimbursed by tenants in accordance with specific allowable costs per tenant lease agreements. Revenue is recognized on the sale of real estate at closing only when sufficient down payments have been obtained, possession and other attributes of ownership have been transferred to the buyer and the Company has no significant continuing involvement.

Natural resource revenues distributable to the Company under the terms of the ANCSA are recorded when the amount thereof is determinable and its receipt is reasonably assured.

Water utility revenues are recognized as water services are provided to the customer. Billings are prepared monthly using a flat rate by residence type as determined by the Regulatory Commission of Alaska.

Cash and cash equivalents: For the purposes of reporting consolidated cash flows, the Company considers all highly-liquid investments purchased with a maturity of three months or less to be cash equivalents, except such instruments held in brokerage accounts which are considered investments.

accounts receivable: Accounts receivable are carried at original invoice amount, less an estimate made for doubtful accounts, and primarily consist of contract receivables generated from prime and subcontracting arrangements with U.S. governmental agencies along with commercial construction contracts. Billed amounts represent invoices that have been prepared and sent to the customer. Unbilled costs are comprised principally of amounts of revenue recognized on contracts for which billings had not been presented to the customer at the consolidated balance sheet date.

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS | 2120 | NOTES TO CONSOlIDATED fINANCIAl STATEMENTS

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS Continued

the aleut corporation and Subsidiaries

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS Continued

the aleut corporation and Subsidiaries

Billed accounts receivables are considered past due if the invoice has been outstanding for more than 30 days. The Company does not charge interest on accounts receivable; however, U.S. governmental agencies pay interest on invoices outstanding for more than 30 days. The Company records interest income from U.S. governmental agencies when received.

In accordance with industry practices, accounts receivable relating to long-term contracts are classified as current, even though a portion of these accounts, including rate variances and retainages, are not expected to be realized within one year. Retention balances are typically collected within a year of completion of the contract.

Management determines the allowance for doubtful accounts by regularly evaluating individual customer receivables and considering a customer’s financial condition, credit history and current economic conditions. Management has established an allowance of $292,409 and $393,389 at March 31, 2015 and 2014, respectively. Accounts receivable are written off when deemed uncollectible. Recoveries of accounts receivable previously written off are recorded when received.

inventory: Inventory primarily consists of fuel, parts held for resale and excess construction materials from previously completed jobs to be used on future jobs. Inventory is stated at the lower of cost or market, cost being determined on the first-in, first-out basis.

investments in trading securities: The Company’s investments in trading securities primarily consist of equity securities, governmental and corporate bonds and are presented in the consolidated financial statements at fair value based on quoted prices in securities markets and are classified as trading securities. Realized and unrealized gains and losses are included in income.

property, equipment and depreciation: Property and equipment are recorded at cost. Depreciation is computed by use of the straight-line method over the estimated useful lives of the assets for financial reporting purposes. Leasehold improvements are amortized over the shorter of the useful life of the asset or the term of the corresponding lease. Major renewals and improvements are capitalized while maintenance and repairs are charged against income as incurred.other investments: Other investments consist of the Company’s equity ownership in business entities. The Company uses the equity method of accounting for those

investments with ownership interests where the Company exercises significant control or influence in the operations of the investee. Under the equity method, the Company records its proportionate share of earnings or loss. The Company uses the cost method of accounting for all other investments.

deferred leasing incentives: The Company capitalizes leasing incentives associated with the successful negotiation of leases. These incentives are amortized on a straight-line basis over the terms of the respective leases and the applicable amortization is recorded as a reduction of revenue. If a lease terminates prior to the expiration of its initial lease term, the carrying amounts of remaining incentives are written-off as a reduction of revenue.

goodwill and other intangibles: The Company records as goodwill the excess of purchase price over the fair value of identifiable net assets acquired. Under FASB Accounting Standards Codification (ASC) Topic 350 – Intangibles – Goodwill and Other, requires an entity to test goodwill for impairment on at least an annual basis by comparing the fair value of a reporting unit with its carrying amount, including goodwill (step one). If the fair value of a reporting unit is less than its carrying amount, the second step of the test must be performed to measure the amount of the impairment loss, if any. On September 15, 2011, the FASB issued ASU No. 2011-08 – Intangibles – Goodwill and Other (Topic 350): Testing Goodwill for Impairment. ASU No. 2011-08 allows an entity the option in its annual goodwill impairment test to first assess qualitative factors to determine whether it is more likely than not (a likelihood of more than 50%) that the fair value of a reporting unit is less than its carrying amount. If it is more likely than not that the fair value of a reporting unit is less than its carrying amount, an entity must still perform the existing two- step impairment test. Otherwise, an entity would not be required to perform the existing two-step impairment test. The Company has elected to perform its annual analysis during the fourth quarter of each fiscal year.

On January 16, 2014, the FASB further issued ASU No. 2014-02, Intangibles – Goodwill and Other (Topic 350): Accounting for Goodwill, a Consensus of the Private Company Council. ASU No. 2014-02 allows an accounting alternative whereby goodwill should be amortized on a straight-line basis over a period of ten years or less than ten years if the entity demonstrates that another useful life is more appropriate. Additionally, an entity that elects the accounting alternative is further required to make an accounting policy election to test goodwill for impairment at either the entity level or the

reporting unit level. The Company elected to early adopt ASU No. 2014-02 effective April 1, 2014, and began amortizing goodwill on a straight-line basis over ten years. Additionally, the Company has elected to test goodwill for impairment at the reporting unit level.

In March 2015, the Company recognized goodwill impairment losses for its C&H and AG reporting units in the amounts of $1,683,630 and $201,303, respectively. In March 2013, a goodwill impairment loss of $1,785,000 was recognized on the Company’s AE reporting unit. The Company determined the fair value of the reporting units utilizing a multiple of earnings before interest, taxes, depreciation, and amortization and incorporated assumptions that it believes marketplace participants would utilize. No impairment was identified for the year ended March 31, 2014.

Intangible assets include customer relationships, contractual rights, trade name, and non-compete agreements. Contractual rights are being amortized based upon the future discounted cash flows of management’s estimates of when the associated backlog of all contract rights purchased will be converted into delivered services varying from one to two years. The customer relationships, trade name and non-compete agreements are being amortized on a straight-line basis over their estimated useful lives ranging from three to ten years.

valuation of long-lived assets: The Company accounts for the valuation of long-lived assets under Accounting Standards Codification (ASC) 360-10-15, Impairment or Disposal of Long-Lived Assets. This guidance requires that long-lived assets and certain identifiable intangible assets be reviewed for impairment whenever events or circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of the long-lived assets is measured by a comparison of the carrying amount of the asset to future undiscounted net cash flows expected to be generated by the asset. If such assets are considered to be impaired, the impairment to be recognized is measured by the amount by which the carrying amount of the assets exceeds the estimated fair value of the assets. Assets to be disposed of are reported at the lower of the carrying amount or fair value, less costs to sell.

In March 2015, AE identified a piece of equipment with a net book value of $659,502 which was no longer being used in operations and was actively marketed for sale. Based on an independent third party appraiser, it was determined the equipment’s fair value was $125,000 resulting in an impairment loss of $534,502 being recognized for the year

ended March 31, 2015. The equipment was transferred out of property equipment and is included in other non-current assets.

deposit: The deposit represents requirements imposed by catastrophic and stop-loss insurance policies associated with the Company’s partially self-insured program.

deferred revenue: Deferred revenue primarily represents rental income and analytical services income received in advance of contractual terms.

income taxes: Deferred income taxes are provided on a liability method, whereby, deferred tax assets are recognized for deductible temporary differences and deferred tax liabilities are recognized for taxable temporary differences. Temporary differences are the differences between the reported amounts of assets and liabilities and their tax bases. Deferred tax assets are reduced by a valuation allowance when, in the opinion of management, it is more likely than not that some portion or all of the deferred tax assets will not be realized. Deferred tax assets and liabilities are adjusted for the effects of changes in tax laws and rates on the date of enactment.

The Company has adopted the accounting standard on accounting for uncertainty in income taxes, which addresses the determination of whether tax benefits claimed or expected to be claimed on a tax return should be recorded in the financial statements. Under this guidance, the Company may recognize the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by taxing authorities, based on the technical merits of the position. The tax benefits recognized in the consolidated financial statements from such a position are measured based on the largest benefit that has a greater than 50% likelihood of being realized upon ultimate settlement. The guidance on accounting for uncertainty in income taxes also addresses de-recognition, classification, interest and penalties on income taxes and accounting in interim periods.

Management evaluated the Company’s tax positions and concluded that the Company had taken no uncertain tax positions that require adjustment to the consolidated financial statements to comply with the provisions of this guidance. As such, the Company did not recognize any interest or penalties for unrecognized tax benefits for the years ended March 31, 2015, 2014 and 2013.

The Company files income tax returns in the federal and

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS | 2322 | NOTES TO CONSOlIDATED fINANCIAl STATEMENTS

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS Continued

the aleut corporation and Subsidiaries

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS Continued

the aleut corporation and Subsidiaries

several state jurisdictions. With few exceptions, the Company is no longer subject to income tax examinations by the U.S. federal, state or local tax authorities for years before 2012. However, the Company’s net operating loss carryovers remain open to adjustment until the year(s) in which they are ultimately utilized are closed by examination or under the statute of limitations.

Monies and properties received from the Alaska Native Fund under provisions of the Act are not subject to any form of federal, state or local taxation at the time of receipt. However, income derived from real property interests, investments and operations are subject to applicable federal and state income taxes.

per share data: Basic earnings per share is generally computed by dividing net income or loss by the weighted average number of common shares outstanding for the period, whereas diluted earnings per share essentially reflects the potential dilution in basic earnings per share that could occur if other contracts to issue common stock were exercised. The Company does not have any stock options issued, and as a result, basic and diluted earnings per share are the same.

fair value of financial instruments: The carrying amounts including cash and cash equivalents, accounts receivable, costs and estimated earnings in excess of billings on uncompleted construction contracts, due from related parties, income tax receivable, accounts payable, accrued expenses, and billings in excess of costs and estimated earnings on uncompleted construction contracts approximate fair value because of the short maturity of these instruments. Investments in trading securities are carried at fair value. The carrying amount of the line of credit approximates fair value because the interest rate on this credit facility fluctuates with market rates. The carrying amount of the notes payable, notes payable – related party and capital lease obligations approximate fair value due to short maturity of these obligations. Contingent earn-out escrow payable is carried at fair value.

self-insurance: The Company is partially self-insured for workers compensation claims up to $250,000 per incident. The Company has catastrophic coverage through a commercial insurance carrier for claims above $250,000. Exposure to risk of these claims will be accrued, by a charge to operations, in the period in which a loss relating to that period, or prior period, becomes payable or the amount can be readily estimated.

Prior to 2015, the Company was also partially self-insured for group medical expenses. The risk of liability had been reduced through the purchase of stop-loss insurance with a $100,000 specific stop-loss limit. Expenses for group medical claims were charged to operations when incurred. Effective April 1, 2014, the Company was no longer self-insured and switched to a federal employee health benefits medical insurance program.

use of estimates: The preparation of consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates.

financial credit risk: The Company maintains its cash in bank deposit accounts which, at times, may exceed federally insured limits. The Company has not experienced any losses in such accounts. The Company believes it is not exposed to any significant credit risk on cash and cash equivalents. The Company grants credit to its customers in the normal course of business on an unsecured basis.

Recently issued accounting pronouncements: On May 28, 2014, FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606). The core principle of this update is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. ASU 2014-09 is effective for annual reporting periods beginning after December 15, 2017, including interim periods within that reporting period and is to be applied retrospectively, with early application not permitted. The Company’s management is evaluating the effect on its consolidated financial statements.

On December 23, 2014, FASB issued ASU No. 2014-18: Business Combinations (Topic 805) – Accounting for Identifiable Intangible Assets in a Business Combination, a Consensus of the Private Company Council. An entity within the scope of this update (all entities except for public business entities and nonprofits) that elects the accounting alternative to recognize or otherwise consider the fair value of intangible assets as a result of any in-scope transactions should no longer recognize separately from goodwill (1) customer-related intangible assets unless they are capable of being sold or

licensed independently from the other assets of the business and (2) noncompetition agreements. An entity that elects the accounting alternative in this update must adopt the private company alternative to amortize goodwill as described in ASU No. 2014-02, Intangibles—Goodwill and Other (Topic 350): Accounting for Goodwill. However, an entity that elects the accounting alternative in Update 2014-02 is not required to adopt the amendments in this update. The decision to adopt the accounting alternative in this Update must be made upon the occurrence of the first transaction within the scope of this accounting alternative in fiscal years beginning after December 15, 2015, with early application permitted.

Reclassifications: Certain amounts in the 2013 and 2014 consolidated financial statements have been reclassified to conform to the 2015 presentation. These reclassifications had no effect on previously reported net income.

subsequent events: The Company has evaluated subsequent events through June 30, 2015, which represents the date the consolidated financial statements were available to be issued.

noTe 2. alaska naTive Claims seTTlemenT aCT

Contributed capital: The Company was incorporated pursuant to ANCSA, which resolved the Alaska Native land claims. Under the terms of the Act (and amendments), the Company was entitled to $19,503,735, which it received in prior years and recorded as contributed capital.

land: Under the terms of the Act (and amendments), the Company also received the surface estate of approximately 66,000 acres of land and approximately 1,572,000 acres of subsurface estate. The Company records all land transferred under the terms of the Act at zero value, unless amounts were paid which directly related to a parcel acquired, as the aggregate fair market value, including the value of resources. The Company expenses costs related to land selections in the year incurred.

Until developed, leased, or sold to third parties, lands conveyed to the Company pursuant to the Act are exempt from adverse possession and similar claims and real property taxes. Except to the extent such lands are expressly pledged as security for a loan or committed to a commercial transaction or to the extent necessary to enforce a judgment pursuant to Section 7(i) or 14(c) of the Act, such lands are also exempt from judgments resulting from claims based on Title II or other laws affecting

creditors’ rights or judgments in any action to recover sums owed by the Company.

Common stock: The Act provided for the issuance of 100 shares of common stock to each eligible Alaska Native as follows:

Class a shares: Class A shares issued to Alaska Natives enrolled pursuant to the Act in the Aleut region who are shareholders in one of the village corporations in the Aleut region. As of March 31, 2015 and 2014, there were 236,100 Class A shares issued and outstanding.

Class b shares: Class B shares issued to Alaska Natives enrolled pursuant to the Act in the Aleut region but who are not shareholders in one of the village corporations in the Aleut region. As of March 31, 2015 and 2014, there were 88,800 Class B shares issued and outstanding.

Individuals certified by the Department of Interior have been recorded as shareholders. All holders of the stock have the same economic rights. Enrollment is now closed.

The Company’s stock, rights thereto, and rights to dividends or distributions declared with respect thereto may not be sold, subjected to a lien or judgment execution, assigned, treated as an asset under Title XI or any successor statute, any insolvency or moratorium law or other laws affecting creditors’ rights, or otherwise alienated, except that the stock may be transferred (i) to a Native or a descendant of a Native in certain circumstances by court decree or inter vivos gift or (ii) by will or the laws of intestate succession.

Until terminated by Amendment to the Articles of Incorporation, the stock will carry voting rights only if the holder thereof is an eligible Native or a descendant of a Native.

natural resource revenues: Section 7(i) of the Act, as amended by the ANCSA Land Bank Protection Act of 1998, requires 70% of the net revenues received from timber resources and subsurface estate patented to the 12 regional corporations, excluding sand and gravel revenues, be divided annually among these 12 regional corporations based on shareholder enrollment subject to certain annual exclusion amounts.

Section 7(j) of the Act requires that 50% of the 70% allocation established by Section 7(i) of the Act be distributed to village corporations and at large shareholders within each region. The amount distributed to village corporations is based on

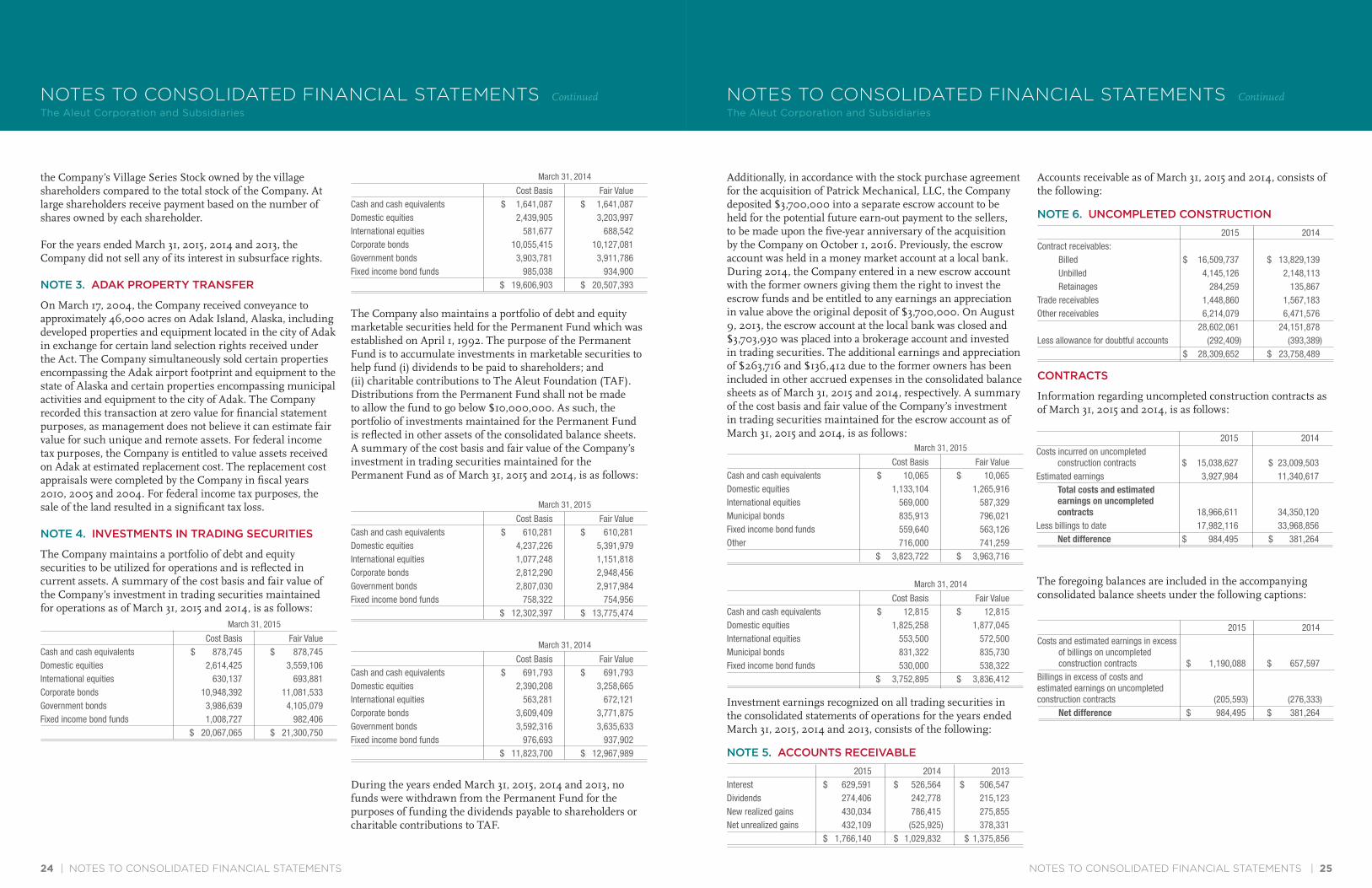

Additionally, in accordance with the stock purchase agreement for the acquisition of Patrick Mechanical, LLC, the Company deposited $3,700,000 into a separate escrow account to be held for the potential future earn-out payment to the sellers, to be made upon the five-year anniversary of the acquisition by the Company on October 1, 2016. Previously, the escrow account was held in a money market account at a local bank. During 2014, the Company entered in a new escrow account with the former owners giving them the right to invest the escrow funds and be entitled to any earnings an appreciation in value above the original deposit of $3,700,000. On August 9, 2013, the escrow account at the local bank was closed and $3,703,930 was placed into a brokerage account and invested in trading securities. The additional earnings and appreciation of $263,716 and $136,412 due to the former owners has been included in other accrued expenses in the consolidated balance sheets as of March 31, 2015 and 2014, respectively. A summary of the cost basis and fair value of the Company’s investment in trading securities maintained for the escrow account as of March 31, 2015 and 2014, is as follows:

Investment earnings recognized on all trading securities in the consolidated statements of operations for the years ended March 31, 2015, 2014 and 2013, consists of the following:

noTe 5. aCCounTs ReCeivable

Accounts receivable as of March 31, 2015 and 2014, consists of the following:

noTe 6. unCompleTed ConsTRuCTion

ConTRaCTs

Information regarding uncompleted construction contracts as of March 31, 2015 and 2014, is as follows:

The foregoing balances are included in the accompanying consolidated balance sheets under the following captions:

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS | 2524 | NOTES TO CONSOlIDATED fINANCIAl STATEMENTS

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS Continued

the aleut corporation and Subsidiaries

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS Continued

the aleut corporation and Subsidiaries

the Company’s Village Series Stock owned by the village shareholders compared to the total stock of the Company. At large shareholders receive payment based on the number of shares owned by each shareholder.

For the years ended March 31, 2015, 2014 and 2013, the Company did not sell any of its interest in subsurface rights.

noTe 3. adak pRopeRTy TRansfeR

On March 17, 2004, the Company received conveyance to approximately 46,000 acres on Adak Island, Alaska, including developed properties and equipment located in the city of Adak in exchange for certain land selection rights received under the Act. The Company simultaneously sold certain properties encompassing the Adak airport footprint and equipment to the state of Alaska and certain properties encompassing municipal activities and equipment to the city of Adak. The Company recorded this transaction at zero value for financial statement purposes, as management does not believe it can estimate fair value for such unique and remote assets. For federal income tax purposes, the Company is entitled to value assets received on Adak at estimated replacement cost. The replacement cost appraisals were completed by the Company in fiscal years 2010, 2005 and 2004. For federal income tax purposes, the sale of the land resulted in a significant tax loss.

noTe 4. invesTmenTs in TRading seCuRiTies

The Company maintains a portfolio of debt and equity securities to be utilized for operations and is reflected in current assets. A summary of the cost basis and fair value of the Company’s investment in trading securities maintained for operations as of March 31, 2015 and 2014, is as follows:

The Company also maintains a portfolio of debt and equity marketable securities held for the Permanent Fund which was established on April 1, 1992. The purpose of the Permanent Fund is to accumulate investments in marketable securities to help fund (i) dividends to be paid to shareholders; and(ii) charitable contributions to The Aleut Foundation (TAF). Distributions from the Permanent Fund shall not be made to allow the fund to go below $10,000,000. As such, the portfolio of investments maintained for the Permanent Fund is reflected in other assets of the consolidated balance sheets. A summary of the cost basis and fair value of the Company’s investment in trading securities maintained for the Permanent Fund as of March 31, 2015 and 2014, is as follows:

During the years ended March 31, 2015, 2014 and 2013, no funds were withdrawn from the Permanent Fund for the purposes of funding the dividends payable to shareholders or charitable contributions to TAF.

Cost Basis Fair ValueCash and cash equivalents $ 878,745 $ 878,745 Domestic equities 2,614,425 3,559,106 International equities 630,137 693,881 Corporate bonds 10,948,392 11,081,533 Government bonds 3,986,639 4,105,079 Fixed income bond funds 1,008,727 982,406 $ 20,067,065 $ 21,300,750

March 31, 2015

Cost Basis Fair ValueCash and cash equivalents $ 1,641,087 $ 1,641,087 Domestic equities 2,439,905 3,203,997 International equities 581,677 688,542 Corporate bonds 10,055,415 10,127,081 Government bonds 3,903,781 3,911,786 Fixed income bond funds 985,038 934,900 $ 19,606,903 $ 20,507,393

March 31, 2014

Cost Basis Fair ValueCash and cash equivalents $ 610,281 $ 610,281 Domestic equities 4,237,226 5,391,979 International equities 1,077,248 1,151,818 Corporate bonds 2,812,290 2,948,456 Government bonds 2,807,030 2,917,984 Fixed income bond funds 758,322 754,956 $ 12,302,397 $ 13,775,474

March 31, 2015

Cost Basis Fair ValueCash and cash equivalents $ 10,065 $ 10,065 Domestic equities 1,133,104 1,265,916 International equities 569,000 587,329 Municipal bonds 835,913 796,021 Fixed income bond funds 559,640 563,126 Other 716,000 741,259 $ 3,823,722 $ 3,963,716

March 31, 2015

Cost Basis Fair ValueCash and cash equivalents $ 691,793 $ 691,793 Domestic equities 2,390,208 3,258,665 International equities 563,281 672,121 Corporate bonds 3,609,409 3,771,875 Government bonds 3,592,316 3,635,633 Fixed income bond funds 976,693 937,902 $ 11,823,700 $ 12,967,989

March 31, 2014

Cost Basis Fair ValueCash and cash equivalents $ 12,815 $ 12,815 Domestic equities 1,825,258 1,877,045 International equities 553,500 572,500 Municipal bonds 831,322 835,730 Fixed income bond funds 530,000 538,322 $ 3,752,895 $ 3,836,412

March 31, 2014

2015 2014 2013Interest $ 629,591 $ 526,564 $ 506,547 Dividends 274,406 242,778 215,123 New realized gains 430,034 786,415 275,855 Net unrealized gains 432,109 (525,925) 378,331 $ 1,766,140 $ 1,029,832 $ 1,375,856

2015 2014Contract receivables: Billed $ 16,509,737 $ 13,829,139 Unbilled 4,145,126 2,148,113 Retainages 284,259 135,867 Trade receivables 1,448,860 1,567,183 Other receivables 6,214,079 6,471,576 28,602,061 24,151,878 Less allowance for doubtful accounts (292,409) (393,389) $ 28,309,652 $ 23,758,489

2015 2014Costs incurred on uncompleted construction contracts $ 15,038,627 $ 23,009,503 Estimated earnings 3,927,984 11,340,617 Total costs and estimated earnings on uncompleted contracts 18,966,611 34,350,120 Less billings to date 17,982,116 33,968,856 Net difference $ 984,495 $ 381,264

2015 2014Costs and estimated earnings in excess of billings on uncompleted construction contracts $ 1,190,088 $ 657,597 Billings in excess of costs and estimated earnings on uncompleted construction contracts (205,593) (276,333) Net difference $ 984,495 $ 381,264

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS | 2726 | NOTES TO CONSOlIDATED fINANCIAl STATEMENTS

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS Continued

the aleut corporation and Subsidiaries

NOTES TO CONSOlIDATED fINANCIAl STATEMENTS Continued

the aleut corporation and Subsidiaries

noTe 7. invenToRies

Inventories at March 31, 2015 and 2014, were comprised of the following:

noTe 8. pRopeRTy and equipmenT

Property and equipment as of March 31, 2015 and 2014, consists of the following: