Embed Size (px)

Citation preview

Are voluntary internal controls-related audit report disclosures informative in IPOs?

Keith Czerney

University of Nebraska – Lincoln

September 2015

Thank you to my dissertation committee at the University of Illinois Urbana-Champaign, Theodore Sougiannis

(Chair), Anne Thompson, Oktay Urcan, and Louis Chan, for invaluable guidance and support. I also thank workshop

participants at the 2015 International Symposium on Audit Research, Boston College, Northwestern University, and

the Universities of Connecticut, Illinois Urbana-Champaign, Miami (FL), Nebraska, and Pittsburgh, as well as Tom

Omer and Jeffrey Pittman, for helpful comments and suggestions. I gratefully acknowledge financial support from

the Accounting Doctoral Scholars Program, Irwin Family Foundation, AICPA Accounting Fellowship, and

University of Illinois Urbana-Champaign.

ABSTRACT

Initial public offering (IPO) companies are exempt from Section 404 of the Sarbanes-

Oxley Act of 2002, leaving investors to assess the quality of an IPO company’s internal controls,

which affect the quality of management-provided financial information, without an opinion on

internal controls effectiveness from management or the external auditor. When not engaged to

opine on the effectiveness of internal controls, auditing standards permit auditors to voluntarily

state that their opinion does not extend to internal control effectiveness. Given auditors’ limited

ability to distinguish financial reporting quality in the unqualified audit report, the costly nature

of audit report modifications, and auditors’ litigation risk concerns, these auditor voluntary

internal controls-related disclosures are likely informative as to the quality of internal controls.

Using a sample of IPOs completed on United States equity exchanges from 2005 through 2014, I

predict and find that auditor voluntary internal controls-related disclosure is associated with a

higher likelihood of post-IPO auditor-reported internal control deficiencies, higher IPO

accounting and auditing expenses, lower post-IPO returns, and lower post-IPO earnings. These

associations are robust to addressing the endogenous nature of the auditor’s disclosure decision.

Overall, my results suggest that auditor voluntary disclosures are informative. This research

should be of interest to investors, regulators tasked with reforming the audit reporting model, and

legislators who recently passed Title I of the Jumpstart Our Business Startups Act that exempts

qualifying IPO companies from Section 404(b) reporting requirements for up to five years.

Keywords: audit reports, voluntary disclosure, initial public offerings, internal controls

JEL: M40, M41, M42, G32

1

Are voluntary internal controls-related audit report disclosures informative in IPOs?

I. INTRODUCTION

This study examines the information content of voluntary internal controls-related

disclosures in the audit report among initial public offering (IPO) companies. IPO companies are

exempt from Section 404(b) of the Sarbanes-Oxley Act of 2002 (SOX), which requires auditors

to opine on management’s assessment of the effectiveness of internal controls over financial

reporting (ICOFR) for many public companies. Although not engaged to opine on ICOFR,

auditors are still required to consider internal controls in the conduct of their audit and can

voluntarily state in the audit report that their opinion on the financial statements does not extend

to the effectiveness of ICOFR (PCAOB 2001). Absent an explicit opinion on the effectiveness of

ICOFR, a non-standard audit report disclosure consistent with AU Section 9550 (hereafter “AU

9550 disclosure”) is not likely to convey new literal information. However, the current

unqualified audit report does not provide an outlet to communicate internal control deficiencies

when not engaged to opine on ICOFR. 1 Therefore, given its voluntary nature and limited

alternatives for distinguishing financial reporting quality in the unqualified audit report, AU

9550 disclosure is likely informative.

Studying the informativeness of auditor voluntary disclosure in the IPO registration

statement is important for at least two reasons. One, while Section 404’s objective is to improve

the reliability of information public companies provide to the financial markets (COSO 2006;

PCAOB 2004), neither management, nor the external auditor, is required to opine on a

company’s internal control effectiveness at the time of the IPO. SOX Section 404(b) requires

auditors of accelerated filers to opine on internal control effectiveness for the second fiscal year

1 In a financial statement audit, the auditor can overcome internal control deficiencies through additional substantive

testing in order to issue an unqualified opinion.

2

end after the IPO. IPO investors may benefit most from SOX’s enhanced reporting requirements

due to the absence of a financial reporting history. The non-applicability of Section 404 to IPO

companies stems from the legislation’s significant compliance cost, especially for smaller

companies. Despite delayed compliance, SOX’s cost has been linked to the significant decline in

IPOs since 2000 (Gao, Ritter, and Zhu 2013). The decline prompted legislators to pass Title I of

the Jumpstart Our Business Startups (JOBS) Act in 2012. Title I created a new class of registrant,

called an emerging growth company, that completes a modified IPO registration and is exempt

from the requirements of Section 404(b) for up to five years (PCAOB 2013).2 The Section

404(b) exemption is noteworthy because material weakness disclosures are more important for

smaller companies with higher pre-disclosure information asymmetry (e.g., IPO companies)

(Beneish, Billings, and Hodder 2008).3 The JOBS Act increases the need for investors to identify

timely sources of information for insight into the current and future internal control effectiveness

of emerging growth companies because an ICOFR opinion from the auditor may not be available

for five years. A pre-IPO AU 9550 disclosure may serve as a discerning source of information

about ICOFR effectiveness.

Two, the informativeness of non-standard audit report content under current auditing

standards is unclear. Financial statement users often indicate that U.S. audit reports are

uninformative unless they contain a going concern uncertainty (e.g., Humphrey, Loft, and

2 An emerging growth company had less than $1.0 billion in annual revenue during its most recently completed

fiscal year and may take advantage of any one or more of the following accommodations: meet with certain

institutional investors to gauge interest in a contemplated offering; receive an initial confidential review of the

registration statement from the SEC; present only two (rather than three) years of audited financial statements in the

registration statement and two (rather than five) years of selected financial data; exempt from the internal controls

audit required by Section 404(b) of SOX; provide streamlined executive compensation disclosure and exempt from

shareholder advisory votes on executive compensation; use private company phase-in periods for new accounting

standards; and, exempt from PCAOB rules pertaining to auditor rotation and proposed auditor discussion and

analysis. An emerging growth company maintains its status for up to five years after its IPO date. 3 Barth, Landsman, and Taylor (2014) examine emerging growth company IPOs and do not find any of the 158

companies sampled to voluntarily comply with Section 404(b) of SOX.

3

Woods 2009; Gray, Turner, Coram, and Mock 2011). Prior research provides mixed evidence on

the informativeness of required or recommended audit report modifications (e.g., Czerney,

Schmidt, and Thompson 2014a, b; Butler, Leone, and Willenborg 2004; Bradshaw, Richardson,

and Sloan 2001; Francis and Krishnan 1999). Practitioner views and academic research have

motivated the Public Company Accounting Oversight Board (PCAOB) to consider reforms to the

audit reporting model to make it more informative (PCAOB 2013). One proposed reform would

require the auditor to discuss some of the risks and uncertainties encountered in the conduct of

the audit. There has been limited research, however, on voluntary audit report modifications,

which may be differentially informative when compared to required modifications because of

their non-requisite nature. This is especially true in the IPO setting where publicly available

information is scarce and informational asymmetries are abundant (Willenborg 1999). Relative

to the high information and liquidity environments of U.S. public companies, the auditor is a

more significant information intermediary in the IPO setting.4

Audit report modifications are costly to auditors because they can strain the auditor-client

relationship and increase the risk of losing the client as a revenue source. AU 9550 disclosure is

a modification to the standard unqualified audit report and, due to its voluntary and costly nature,

is likely added for consequential reasons, suggesting that it is informative. Specifically, AU 9550

disclosure may be provided when internal controls are poor, to disassociate the auditor from the

underlying causes of a possible future financial reporting failure.

Considering the costly nature of audit report modifications and auditor litigation risk

concerns, I make four directional predictions as to the effects of auditor voluntary internal

4 The IPO setting is also an advantageous one in which to study the information content of auditor voluntary

disclosure because, whereas investors in established public companies after the passage of SOX expect the auditors

to opine on ICOFR, the expectation for IPO companies is that ICOFR was not audited. Therefore, the provision of

seemingly redundant, expectation consistent information may enable the auditor to subtly convey internal control-

related concerns.

4

controls-related disclosure. One, auditor voluntary disclosure is associated with an increased

likelihood of post-IPO Section 404(b) material weaknesses. The premise for this expectation is

that companies are less likely than auditors to detect internal control deficiencies (Bedard and

Graham 2011). Resource constrained companies are also less likely to remediate internal control

deficiencies (Bedard, Hoitash, Hoitash, and Westermann 2012). Therefore, pre-IPO internal

control deficiencies that motivate the disclosure will tend to persist until the auditor’s Section

404(b) audit in the second fiscal year after the IPO (at the earliest). Two, I predict that auditor

voluntary disclosure is associated with higher audit fees, as the auditor prices the increased effort

and engagement risk stemming from the poor internal control environment. Three, I predict

auditor voluntary disclosure is associated with lower post-IPO returns because the disclosure

suggests lower reliability of financial information when internal controls are unaudited. Four, I

expect auditor voluntary disclosure that reflects poor internal controls is associated with lower

post-IPO earnings. Strong internal controls enhance the quality of information systems

management uses to make resource allocation decisions (Lambert, Leuz, and Verrecchia 2007).

Poor internal controls contribute to the misallocation of resources and may require companies to

divert resources to improve internal controls, leading to lower future financial performance.

To test my hypotheses, I analyze the audit report text included in the S-1 or F-1 filing for

IPOs completed on U.S. stock exchanges between 2005 and 2014 to identify reports that contain

AU 9550 disclosures. I then test whether AU 9550 disclosure is associated with future auditor-

reported ICOFR deficiencies, accounting and auditing expenses, post-IPO returns, and post-IPO

earnings. I find that auditor voluntary disclosure is associated with an increased likelihood of

post-IPO auditor-reported ICOFR deficiencies. I also find that auditor voluntary disclosure is

associated with higher IPO accounting and auditing fees. Finally, I find that auditor voluntary

5

disclosure is associated with lower post-IPO returns and profitability. In an additional analysis, I

address the endogenous nature of the auditor’s decision to provide voluntary disclosure by

employing coarsened exact matching to identify a balanced sample of treatment and control

observations. My results continue to hold. Overall, I provide robust evidence that auditor

voluntary disclosures are informative as to internal controls quality, auditor effort/risk, perceived

financial information quality, and IPO company performance.

My research makes three primary contributions. One, I contribute to the literature on IPO

disclosures. Much of the prior research on IPO disclosure focuses on management-provided

disclosure and finds that management’s voluntary disclosures are useful in evaluating IPO

companies (e.g., Guo, Lev, and Zhou 2004; Leone, Rock, and Willenborg 2007; Schrand and

Verrecchia 2002). The focus on management disclosure is due, in part, to third parties’ limited

involvement in pre-IPO companies. Because of this limited involvement, there is a lack of

information available from third party information intermediaries, against which investors can

assess the credibility of management’s voluntary disclosures. The auditor is required to play a

role in the IPO process and the auditor’s required disclosures have been show to be informative

to IPO investors (e.g. Willenborg and McKeown 2001; Ghicas, Papadaki, Siougle, and

Sougiannis 2008). My research extends the IPO disclosure literature by studying the information

content of auditor voluntary internal controls-related disclosure as a unique type of non-

management voluntary disclosure.

Two, I contribute to the internal controls literature. Prior studies have analyzed the

determinants (e.g., Ashbaugh-Skaife, Collins, and Kinney 2007; Doyle, Ge, and McVay 2007b)

and consequences (e.g., Ashbaugh-Skaife, Collins, Kinney, and Lafond 2009; Doyle, Ge, and

McVay 2007a) of material weaknesses in ICOFR. I extend this line of research by examining the

6

inclusion of auditor voluntary internal controls-related disclosure in the pre-IPO audit report,

which is a more subtle indication of internal controls quality than an explicit opinion on ICOFR.

An association between such disclosure and future financial reporting quality, auditor effort/risk,

returns, and earnings suggests that voluntary auditor-provided information is relevant to the

assessment of information quality and risk. My results should be of interest to legislators who

passed Title I of the JOBS Act, which postpones the public communication of deficiencies in

ICOFR that may have reasonably been known at the time of the IPO. In passing Title I,

legislators may have weighed public companies’ SOX compliance cost concerns more heavily

than the potential cost of unaudited control systems to investors.

Three, my research enhances our understanding of the information content of the audit

report, as currently constituted, in two key ways. One, I study previously unexamined AU 9550

disclosure, which answers the call from Church, Davis, and McCracken (2008) for further

research on the effect of different disclosures in the audit report. Disclosure of this nature has

been of recent interest to regulators who have discussed requiring auditors or management to

state whether the company has obtained an attestation on internal controls from the auditor, in an

effort to increase transparency and investor protections (GAO 2013). Two, I am the first, to my

knowledge, to study the information content of the audit report for IPO companies strictly in the

post-SOX regulatory environment characterized by heightened skepticism of both new issuances

and auditors. Studying this period is important because auditors’ communications may be

differentially informative under PCAOB regulation versus self-regulated regimes.

The remainder of the paper is organized into four additional sections. Section II provides

background information and develops the hypotheses. Section III details the sample selection

7

procedure and research design. I review my empirical results in Section IV and, in Section V, I

discuss additional analyses and results. My conclusions are presented in Section VI.

II. BACKGROUND INFORMATION AND HYPOTHESIS DEVELOPMENT

AU Section 9550

I utilize the non-standard audit report content provided in accordance with AU Section

9550 as a mechanism to study the information content of auditor voluntary disclosures. Although

an IPO company’s auditor is not required to opine on the effectiveness of ICOFR, professional

standards require the auditor to obtain a detailed understanding of internal controls in order to

assess control risk, which impacts the nature, timing, and extent of substantive audit procedures

underlying the opinion on the fair presentation of the financial statements (Asare, Fitzgerald,

Graham, Joe, Negangard, and Wolfe 2013). This detailed understanding of the internal control

environment not only impacts the conduct of the financial statement audit, but may also

influence the auditor’s decision to provide voluntary disclosure in the audit report, following AU

Section 9550. AU Section 9550 permits the addition of non-standard content to the audit report

when the auditor does not opine on effectiveness of ICOFR. Specifically, AU Section 9550.10

states that the auditor may consider adding, but is not required to add, the following disclosure to

the standard unqualified audit report:

“We were not engaged to examine management’s assertion about the effectiveness of

[name of entity’s] internal control over financial reporting as of [date] included in the

accompanying [title of management’s report] and, accordingly, we do not express an

opinion thereon.”

Refer to Appendix A for examples of AU 9550 disclosure from IPO companies in my sample.5

5 In my sample, there is little variation in AU 9550 disclosure content and form, beyond that evident in the Appendix

A examples, to further investigate empirically.

8

Voluntary Disclosure in the IPO Setting

Enhanced disclosure is one way to reduce information asymmetry in IPOs. The extent of

voluntary disclosures is associated with lower post-IPO information asymmetry (Guo, Lev, and

Zhou 2004) and disclosure specificity in IPO registration statements reduces ex ante uncertainty

(Leone, Rock, and Willenborg 2007). Voluntary company-provided news disclosures outside

regulatory filings are associated with less underpricing for companies with the highest first-day

returns (Schrand and Verrecchia 2002). The limited information available from third party

sources for IPO companies (Aharony, Lin, and Loeb 1993; Friedlan 1994), however, makes it

difficult to judge the appropriateness of reported accounting numbers (Fan 1997). When other

outlets do not provide credible information, the audit report becomes particularly useful (Church

et al. 2008). Collectively, these results indicate that disclosure (particularly voluntary disclosure)

is informative for IPO companies, but its impact on information asymmetry is limited when the

disclosures are unverified.

Auditors, as third party information intermediaries, play a key role in shaping a

company’s information environment and enhance the credibility of disclosed information (Beyer,

Cohen, Lys, and Walther 2010). They reduce information asymmetry in IPOs by opining on the

financial statements included in the registration statement and ensuring that material facts in

regulatory filings are properly disclosed (Willenborg 1999). Datar, Feltham, and Hughes (1991)

analytically show that the content of the audit report is informative when higher audit quality is

more costly. Subsequent empirical research supports this result, as going concern opinions

(Willenborg and McKeown 2001) and “quantifiable qualifications” in international equity

9

markets (Ghicas, Papadaki, Siougle, and Sougiannis 2008) are informative for IPO companies.6

In sum, audit report content is informative for IPO companies, but empirical tests to date have

been limited to required auditor disclosures. My research adds to this literature by exploring the

informativeness of auditor-provided AU 9550 disclosure – a form of voluntary, non-

management-provided disclosure.

Audit Report Informativeness

The audit report is the outcome of a negotiation between management and the auditor

(Antle and Nalebuff 1991; Gibbins, Salterio, and Webb 2001), during which auditors must

balance client preferences against their fiduciary duty to act in the interest of financial market

constituents. Companies are more likely to terminate their auditor after the auditor issues an

audit report containing non-standard content (e.g. Chow and Rice 1982; Mutchler 1984; Geiger,

Raghunandan, and Rama 1998), suggesting a company preference for a standard unqualified

audit report and potential adverse consequences to the auditor for issuing a non-standard report.

Financial statement users’ tendencies to limit their review of the audit report to whether or not it

is unqualified reinforce this client preference (Gray et al. 2011). The auditor’s relationship with

the company influences her likelihood of including not only adverse non-standard content in the

audit report (Lennox 2005; Ye, Carson, and Simnett 2011), but also non-standard content that

could be perceived unfavorably.7 The payment of audit fees from the company to the auditor

6 Ghicas et al. (2008, p. 513) define “quantifiable qualifications” as “monetary amounts missing or misstated on the

financial statements but disclosed in the auditor’s report.” A comparable qualification does not exist under U.S.

auditing standards. 7 Financial statement users do not fully understand auditors’ responsibilities (Church et al. 2008), which could be

due, in part, to their inability to process the content of the audit report. Investors generally find, “The [audit] report

is useful if one can read between the lines … sometimes there are nuances, which can let the careful reader note the

state of affairs is not as it should be” (CFA 2011, p. 9). Unsophisticated investors merely observe that a disclosure

has been made without being able to infer the value of the disclosure (Fishman and Hagerty 2003) and may not

recognize the nuanced nature of the audit report. A lack of understanding as to the auditor’s responsibilities can lead

financial statement users to perceive AU 9550 disclosure as conveying new information that a Section 404(b) audit

was not conducted.

10

strengthens the company’s potential influence on the auditor (DeFond and Francis 2005; Francis

2006). To the extent non-standard audit report disclosure influences companies’ auditor retention

decisions or audit fee concessions, non-standard audit report disclosure is costly and as a result,

when voluntary, is not likely added for trivial reasons.

Public companies’ audit reports are generally “boilerplate” (Gray et al. 2011), conveying

little of the auditor’s vast private information, due to the Securities and Exchange Commission’s

(SEC) requirement for all audit reports to be unqualified. Auditors can leverage the voluntary

nature of AU Section 9550 to distinguish financial reporting and disclosure quality, the

foundations of which are internal controls, in the unqualified audit report. I expect auditors to

voluntarily include AU 9550 disclosure in the audit report when internal controls are poor, in

response to auditors’ heightened litigation risk exposure for IPOs relative to existing public

companies (Venkataraman, Weber, and Willenborg 2008).8 Auditor litigation risk stems from the

higher likelihood of being sued as a result of a failure in financial reporting (Palmrose 1987,

1988; Stice 1991; Lys and Watts 1994). Enhanced disclosure is an effective hedge against all

types of litigation (Hanley and Hoberg 2012), with AU 9550 disclosure being a form of

enhanced auditor disclosure. As such, auditors’ AU 9550 disclosure can reduce litigation risk by

disassociating the auditor from the poor internal controls underlying financial reporting failures

that may trigger future lawsuits.

Hypothesis Development

Hypothesis 1

8 Venkataraman et al. note that companies register their IPO under the Securities Act of 1933 but, after going public,

file under the Securities Exchange Act of 1934. Litigation risk exposure is higher under the 1933 Act than under the

1934 Act because the 1933 Act, in effect, imposes strict liability on issuers for material misstatements or omissions

in a registration statement. Comparatively, under the 1934 Act, a plaintiff must demonstrate that an issuer knowingly

misled investors.

11

The first hypothesis predicts a positive association between auditor voluntary disclosure

and post-IPO auditor-reported material weaknesses. Private (pre-IPO) companies typically have

weaker internal controls than public companies (Gray et al. 2011). Although private companies

may have internal processes in place to evaluate internal controls, weaker controls persist

because, relative to auditors, companies tend to neither detect (and correct) as many internal

control deficiencies, nor detect deficiencies most-likely to affect financial reporting (Bedard and

Graham 2011). As IPO companies transition from private to public companies, many must

improve their control environments to meet the higher standard for public companies.

The auditor can informally communicate observations on the company’s ICOFR from its

pre-IPO financial statement audit to management or the audit committee, providing a starting

point for improvement efforts. However, resource-constrained companies, such as IPO

companies, are less likely to remediate control problems that involve significant resources –

especially large capital investments (Bedard et al. 2012). Control deficiencies not remediated

will become reportable conditions in the auditor’s opinion on the effectiveness of ICOFR.

I expect auditor voluntary disclosure that reflects the auditor’s lack of comfort with the

effectiveness of ICOFR to be associated with an increased likelihood of auditor-identified

internal control deficiencies in the first year after the IPO in which the auditor renders a Section

404(b) opinion. I formally state H1, in the alternative form, as follows:

H1: Auditor voluntary disclosure is associated with an increased likelihood of post-IPO

auditor-reported internal control deficiencies.

Hypothesis 2

The second hypothesis predicts a positive association between auditor voluntary

disclosure and audit fees. In his seminal work, Simunic (1980) shows that audit fees are a linear

combination of the marginal cost of auditing and the expected losses from litigation. Pratt and

12

Stice (1994) and Venktataraman et al. (2008) more specifically characterize the marginal cost of

auditing as the amount of audit evidence collected. When internal controls are ineffective and

cannot be relied upon in a financial statement audit, auditors assess the risk of material

misstatement to be higher, for a given level of inherent risk, and must increase the extent of audit

procedures performed. Hogan and Wilkins (2008) find that auditors seem to increase their fees

when control deficiencies exist, and to a greater extent when problems are more severe. Further,

auditors tend to increase their effort in response to increased control risk. This leads me to expect

auditor voluntary disclosure that reflects poor internal controls to be associated with higher fees

for the audit of the financial statements included in the IPO registration statement. I formally

state H2, in the alternative form, as follows:

H2: Auditor voluntary disclosure is associated with higher IPO audit fees.

Hypothesis 3

The third hypothesis predicts a negative association between auditor voluntary disclosure

and post-IPO returns. The company and its underwriters typically set the final offer price after

market close on the day before the offering (Lowry and Schwert 2004), taking into consideration

investors’ perceptions of the issue gleaned from the road show (Benveniste and Spindt 1989).

The offer price is set without the company or its underwriters knowing precisely what the

market’s valuation of the stock will be (Benveniste and Spindt 1989). IPO issuers’ information

advantage over investors (Ritter and Welch 2002; Demers and Joos 2007) and absence of a

reference market price prior to the IPO (Friedlan 1994) make it difficult for investors to evaluate

an IPO (Ritter and Welch 2002; Demers and Joos 2007). Information asymmetry between the

company and investors can lead prospective investors to discount their valuation (Myers and

Majluf 1984).

13

Accounting information is a key source of non-price information used to evaluate IPO

companies (Friedlan 1994). Auditors reduce the information asymmetry between the company

and prospective investors by certifying the financial information management provides. The

auditor’s influence on the reliability of the financial information may be limited, however,

because she is not required to conduct an audit of internal controls in accordance with Section

404(b) of SOX, the intent of which is to improve the reliability of information public companies

provide (COSO 2006; PCAOB 2004). Auditor voluntary disclosure stating that a SOX audit was

not conducted suggests that the reliability of financial statement information provided is lower.

This should be of interest to prospective investors because the risk stemming from the likelihood

that company-specific information is of poor quality is relevant for pricing decisions (Francis,

LaFond, Olsson, and Schipper 2005).9

Prior studies have examined the relationship between assessments of internal controls

quality and returns. Material weakness disclosures are informative to equity investors, given their

negative association with stock returns (Beneish et al. 2008; Hammersley, Myers, and

Shakespeare 2008). Companies with internal control deficiencies have significantly higher

idiosyncratic risk, systematic risk, and cost of equity (Ashbaugh-Skaife et al. 2009; Beneish et al.

2008). Ashbaugh-Skaife et al. interpret this result as demonstrating the link between financial

information quality and risk. Increases in the perceived riskiness of a company are important

because they can raise the cost of capital (Froot, Perold, and Stein 1992). Collectively, I expect

auditor voluntary disclosure to be associated with lower post-IPO returns and formally state my

expectation as H3, in the alternative form, as follows:

H3: Auditor voluntary disclosure is associated with lower post IPO returns.

9 Ecker (2014) finds evidence consistent with the hypothesis that information precision at the time of the IPO is

unknown to investors and, therefore, must be estimated with considerable error due to the little or no public

information history about a company’s fundamentals.

14

Hypothesis 4

The fourth hypothesis predicts that auditor voluntary disclosure is associated with lower

post-IPO earnings. The quality of information systems, of which the effectiveness of internal

controls is a key component, directly affects the quality of the financial data available for

informed decision-making (Lambert et al. 2007). A good internal control system can improve the

accuracy of disclosures and other decisions made using internal financial data (Feng, Li, and

McVay 2009) by providing more timely, complete, and accurate financial information. ICOFR,

therefore, can have an economically significant effect on company operations (Feng, Li, McVay,

and Ashbaugh-Skaife 2014). For example, Cheng, Dhaliwal, and Zhang (2013) show that

investment inefficiency is mitigated after the disclosure of ICOFR weaknesses. It follows that

internal controls-related voluntary disclosure is likely associated with lower future earnings due

to internal controls’ adverse impact on earnings through poorer quality internal decision-making

and through the diversion of financial resources to improve the internal control environment.

The effect of internal control quality can also influence future earnings through its impact

on the quality of accruals. Internal control weaknesses are associated with poorly estimated

accruals that are not subsequently realized as cash flows (Doyle et al. 2007a). As well, in the

presence of Section 404 internal control deficiencies, management tends to guide (Feng, Li, and

McVay 2009), and analysts tend to forecast (Clinton, Pinello, and Skaife 2014), less accurately,

suggesting that earnings are more difficult to forecast when internal controls are poor. In sum, I

expect auditor voluntary disclosure that reflects poor internal controls to be associated with

lower future earnings. I formally state my prediction as follows:

H4: Auditor voluntary disclosure is associated with lower post-IPO earnings.

15

III. RESEARCH DESIGN

Sample Selection

I analyze the content of the audit report included in the registration statement for a

sample of 1,669 IPOs completed on U.S. public equity exchanges from January 1, 2005 through

mid 2014 to identify the presence of AU Section 9550 disclosure. I use a Python script to

download IPO data from www.nasdaq.com.10 I restrict my analysis to companies that originally

file their registration statement with the SEC on form S-1 or F-1. Consistent with prior IPO

research and to limit the influence of economically small outliers on my results, I exclude 109

observations with missing IPO offer prices or prices less than $5 per share and 328 observations

with pre-IPO total assets of less than $1,000,000 (inclusive) or missing. The audit report could

not be extracted from the registration statement for 125 observations. I exclude 16 IPOs with pre-

IPO Section 404(b) audit reports because I am interested in studying a setting where explicit

auditor-provided information on the effectiveness of ICOFR is not available at the time of the

IPO. Finally, I exclude 8 IPOs of non-operating companies (Standard Industrial Classification

Code 9995). After these exclusions, the sample of IPOs eligible for my multivariate analyses is

1,083. The final sample size for my test of H1 is 549 because AuditAnalytics does not contain

SOX Section 404(b) data for 339 observations, Section 404(b) data is not available within 27

months of the IPO date for 40 observations, and data necessary to compute control variables is

missing for 155 observations.11 I use a sample size of 975 to test H2, after excluding 102 IPOs

without accounting or auditing expense information in the registration statement and 6 IPOs

10 http://www.nasdaq.com includes data for IPOs completed on multiple U.S. equity exchanges, including the

NASDAQ, New York, and American Stock Exchanges, as well as on the Over the Counter Bulletin Board. 11 New registrants are not required to comply with Section 404(b) of SOX until their second annual report filed as a

public company. I restrict my analysis to 27 months after the IPO to include two full years, plus three months that it

typically takes to prepare annual financial statements. My results are unchanged when I include the 40 observations

with delayed compliance.

16

missing data for control variables. The sample size for my test of H3 is 821 due to 234

observations missing CRSP data and 28 observations lacking data necessary to compute control

variables. The final sample for my test of H4 contains 866 observations because 58 observations

have pre-IPO return on assets of less than -100 percent, Compustat data is not available for 26

observations for a fiscal year ending within a year after the IPO, and 133 observations are

missing data for control variables. The final sample for my test of H4 includes 834 observations,

as CRSP data was missing for 234 observations and data was not available for control variables

for 15 observations.

Multivariate Analysis

Material Weakness Model

I test H1, which predicts an increased likelihood of auditor-reported material weaknesses

in ICOFR when the audit report included in the IPO registration statement includes AU 9550

disclosure, using a logistic regression model where ICDEF404_A is the dependent variable and

AU9550 is the independent variable of interest, as follows:

𝐼𝐶𝐷𝐸𝐹404_𝐴 = 𝛽0 + 𝛽1𝐴𝑈9550 + 𝛽2𝐴𝑈508𝑂𝑇𝐻𝐸𝑅 + 𝛽3𝐴𝑈508𝐺𝐶 + 𝛽4𝐿𝑂𝑆𝑆_𝐴 +𝛽5𝐶𝑅𝐴𝑇𝐼𝑂_𝐴 + 𝛽6𝐼𝑁𝑉𝐸𝑁𝑇𝑂𝑅𝑌_𝐴 + 𝛽7𝑍𝑆𝐶𝑂𝑅𝐸_𝐴 + 𝛽8𝐿𝑜𝑔(𝑀𝐾𝑇𝑉𝐴𝐿404_𝐴) +𝛽9𝑆𝑄𝐸𝑀𝑃𝐿𝑂𝑌𝐸𝐸𝑆_𝐴 + 𝛽10𝐿𝑜𝑔(𝑆𝐸𝐺𝑀𝐸𝑁𝑇𝑆𝐴) + 𝛽11𝐵𝐼𝐺𝑁404 +𝛽12𝐶𝐻𝐺𝐴𝑈𝐷𝐼𝑇𝑂𝑅_𝐴 + 𝛽13𝑁𝐴𝐹𝑅𝐴𝑇𝐼𝑂_𝐴 + 𝛽14𝐿𝑜𝑔(𝐴𝑈𝐷𝐼𝑇𝐹𝐸𝐸𝑆𝐴) + 𝛽15𝐿𝐼𝑇𝑅𝐼𝑆𝐾 +𝛽16𝐴𝑆5_404_𝐴 + 𝜀 (1)

ICDEF404_A is an indicator variable that equals one if the audit report identifies an ICOFR

deficiency in the first fiscal year (after the IPO) the auditor opines on the effectiveness of

ICOFR, and zero otherwise. The independent variable of interest in this and all subsequent

analyses, AU9550, is an indicator variable equal to one if the audit report included in the

registration statement states that the auditor was not engaged to audit the effectiveness of ICOFR

and, accordingly does not express an opinion thereon, and zero otherwise. I identify the presence

17

of AU 9550 disclosure using text-parsing routines that search for keywords and phrases in the

audit report that are indicative of internal control-related scope limitations. I manually validate

the accuracy of my analysis for a sample of audit reports.

AU508OTHER and AU508GC control for other non-standard content in the audit report.

AU Section 508.11 identifies eight circumstances that require the auditor to add non-standard

content to the audit report. One circumstance is when there exists substantial doubt about the

company’s ability to continue as a going concern. The other circumstances convey information

relevant to non-viability risks that may also be important considerations in the IPO context.

Accordingly, I control for this other non-standard audit report content. AU508OTHER is an

indicator variable equal to one if the audit report contains non-standard content, other than a

going concern uncertainty, in accordance with AU Section 508, and zero otherwise. AU508GC is

an indicator variable equal to one if the audit report expresses substantial doubt about the

company’s ability to continue as a going concern, and zero otherwise. I identify the presence of

AU Section 508 content using text-parsing procedures consistent with Czerney et al. (2014a, b).

While AU9550, AU508OTHER, and AU508GC are measured using the content of the audit

report in the IPO registration statement, all other regression variables are calculated as of (for)

the fiscal year end(ed) in which the auditor opines on the effectiveness of ICOFR.

The control variables in this model follow Ashbaugh-Skaife et al. (2007) and Doyle et al.

(2007b). I control for companies’ financial soundness using an indicator variable that equals one

if the company reports a loss, and zero otherwise (LOSS), the ratio of current assets to current

liabilities (CRATIO_A), and the Zmijewski (1984) financial distress measure (ZSCORE_A). I

control for company size with the market value of equity as of fiscal year end (MKTVAL404_A).

I measure organizational complexity with the square root of the number of employees at the

18

company as of fiscal year end (SQEMPLOYEES_A) and the natural logarithm of the number of

geographic segments (Log(SEGMENTS_A)).

I control for the auditor’s ability to identify internal control deficiencies and incentives to

disclose material weaknesses using four measures. BIGN404 equals one if the company’s auditor

that issues the first opinion on ICOFR in accordance with Section 404(b) is Deloitte, Ernst &

Young, KPMG, or PriceWaterhouseCoopers, and zero otherwise. CHGAUDITOR_A equals one

if the auditor that opines on the effectiveness of ICOFR is different from the auditor that signs

the audit report included in the IPO registration statement, and zero otherwise. I measure the

economic bond between the company and auditor using the ratio of non-audit fees to total fees

(NAFRATIO_A) and the natural logarithm of the total audit fees (Log(AUDITFEES_A)) to

control for any potential economic bonding and auditor effort.

Consistent with Ashbaugh-Skaife et al. (2007), I control for heightened litigation risk

using an indicator variable that equals one if the company is in a high litigation risk industry, and

zero otherwise (LITRISK). I identify high litigation risk industries following Venkataraman et al.

(2008). Finally, I include an indicator variable associated with the passage of Auditing Standard

No. 5 (AS5_404_A) that equals one if the period end date of the first audit report that includes an

opinion on ICOFR is on or after November 15, 2007, and zero otherwise. I winsorize all

continuous variables at the 1 percent and 99 percent levels. Refer to Appendix B for further

discussion of variable construction and data sources.

Audit Fees Model

H2 predicts a positive association between AU 9550 disclosure and audit fees. To test

H2, I use Ordinary Least Squares to estimate the following audit fee model:

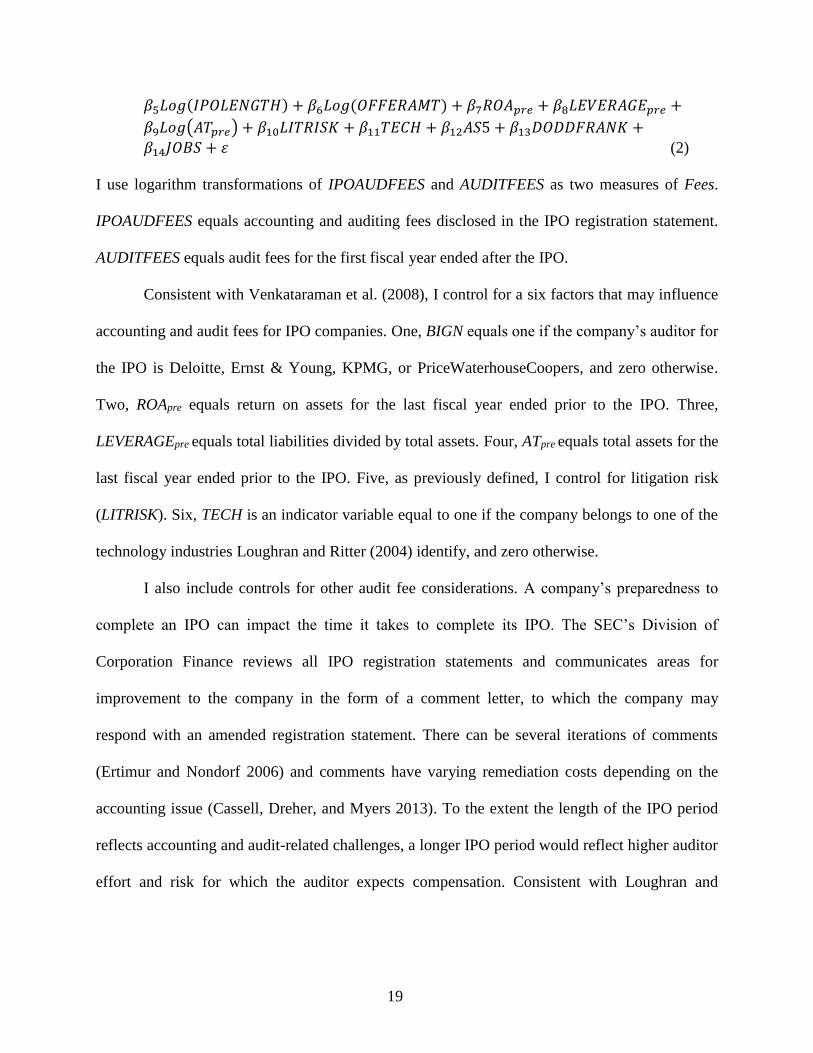

𝐹𝑒𝑒𝑠 = 𝛽0 + 𝛽1𝐴𝑈9550 + 𝛽2𝐴𝑈508𝑂𝑇𝐻𝐸𝑅 + 𝛽3𝐴𝑈508𝐺𝐶 + 𝛽4𝐵𝐼𝐺𝑁 +

19

𝛽5𝐿𝑜𝑔(𝐼𝑃𝑂𝐿𝐸𝑁𝐺𝑇𝐻) + 𝛽6𝐿𝑜𝑔(𝑂𝐹𝐹𝐸𝑅𝐴𝑀𝑇) + 𝛽7𝑅𝑂𝐴𝑝𝑟𝑒 + 𝛽8𝐿𝐸𝑉𝐸𝑅𝐴𝐺𝐸𝑝𝑟𝑒 +

𝛽9𝐿𝑜𝑔(𝐴𝑇𝑝𝑟𝑒) + 𝛽10𝐿𝐼𝑇𝑅𝐼𝑆𝐾 + 𝛽11𝑇𝐸𝐶𝐻 + 𝛽12𝐴𝑆5 + 𝛽13𝐷𝑂𝐷𝐷𝐹𝑅𝐴𝑁𝐾 +

𝛽14𝐽𝑂𝐵𝑆 + 𝜀 (2)

I use logarithm transformations of IPOAUDFEES and AUDITFEES as two measures of Fees.

IPOAUDFEES equals accounting and auditing fees disclosed in the IPO registration statement.

AUDITFEES equals audit fees for the first fiscal year ended after the IPO.

Consistent with Venkataraman et al. (2008), I control for a six factors that may influence

accounting and audit fees for IPO companies. One, BIGN equals one if the company’s auditor for

the IPO is Deloitte, Ernst & Young, KPMG, or PriceWaterhouseCoopers, and zero otherwise.

Two, ROApre equals return on assets for the last fiscal year ended prior to the IPO. Three,

LEVERAGEpre equals total liabilities divided by total assets. Four, ATpre equals total assets for the

last fiscal year ended prior to the IPO. Five, as previously defined, I control for litigation risk

(LITRISK). Six, TECH is an indicator variable equal to one if the company belongs to one of the

technology industries Loughran and Ritter (2004) identify, and zero otherwise.

I also include controls for other audit fee considerations. A company’s preparedness to

complete an IPO can impact the time it takes to complete its IPO. The SEC’s Division of

Corporation Finance reviews all IPO registration statements and communicates areas for

improvement to the company in the form of a comment letter, to which the company may

respond with an amended registration statement. There can be several iterations of comments

(Ertimur and Nondorf 2006) and comments have varying remediation costs depending on the

accounting issue (Cassell, Dreher, and Myers 2013). To the extent the length of the IPO period

reflects accounting and audit-related challenges, a longer IPO period would reflect higher auditor

effort and risk for which the auditor expects compensation. Consistent with Loughran and

20

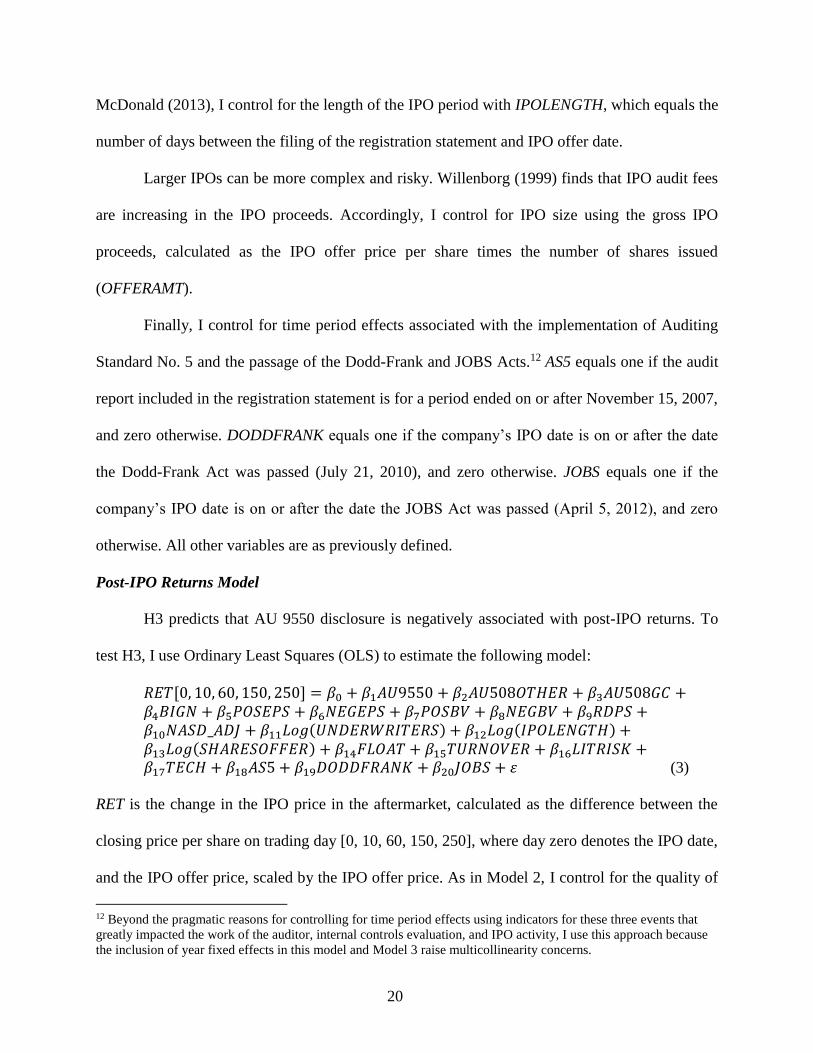

McDonald (2013), I control for the length of the IPO period with IPOLENGTH, which equals the

number of days between the filing of the registration statement and IPO offer date.

Larger IPOs can be more complex and risky. Willenborg (1999) finds that IPO audit fees

are increasing in the IPO proceeds. Accordingly, I control for IPO size using the gross IPO

proceeds, calculated as the IPO offer price per share times the number of shares issued

(OFFERAMT).

Finally, I control for time period effects associated with the implementation of Auditing

Standard No. 5 and the passage of the Dodd-Frank and JOBS Acts.12 AS5 equals one if the audit

report included in the registration statement is for a period ended on or after November 15, 2007,

and zero otherwise. DODDFRANK equals one if the company’s IPO date is on or after the date

the Dodd-Frank Act was passed (July 21, 2010), and zero otherwise. JOBS equals one if the

company’s IPO date is on or after the date the JOBS Act was passed (April 5, 2012), and zero

otherwise. All other variables are as previously defined.

Post-IPO Returns Model

H3 predicts that AU 9550 disclosure is negatively associated with post-IPO returns. To

test H3, I use Ordinary Least Squares (OLS) to estimate the following model:

𝑅𝐸𝑇[0, 10, 60, 150, 250] = 𝛽0 + 𝛽1𝐴𝑈9550 + 𝛽2𝐴𝑈508𝑂𝑇𝐻𝐸𝑅 + 𝛽3𝐴𝑈508𝐺𝐶 +𝛽4𝐵𝐼𝐺𝑁 + 𝛽5𝑃𝑂𝑆𝐸𝑃𝑆 + 𝛽6𝑁𝐸𝐺𝐸𝑃𝑆 + 𝛽7𝑃𝑂𝑆𝐵𝑉 + 𝛽8𝑁𝐸𝐺𝐵𝑉 + 𝛽9𝑅𝐷𝑃𝑆 +𝛽10𝑁𝐴𝑆𝐷_𝐴𝐷𝐽 + 𝛽11𝐿𝑜𝑔(𝑈𝑁𝐷𝐸𝑅𝑊𝑅𝐼𝑇𝐸𝑅𝑆) + 𝛽12𝐿𝑜𝑔(𝐼𝑃𝑂𝐿𝐸𝑁𝐺𝑇𝐻) +𝛽13𝐿𝑜𝑔(𝑆𝐻𝐴𝑅𝐸𝑆𝑂𝐹𝐹𝐸𝑅) + 𝛽14𝐹𝐿𝑂𝐴𝑇 + 𝛽15𝑇𝑈𝑅𝑁𝑂𝑉𝐸𝑅 + 𝛽16𝐿𝐼𝑇𝑅𝐼𝑆𝐾 +𝛽17𝑇𝐸𝐶𝐻 + 𝛽18𝐴𝑆5 + 𝛽19𝐷𝑂𝐷𝐷𝐹𝑅𝐴𝑁𝐾 + 𝛽20𝐽𝑂𝐵𝑆 + 𝜀 (3)

RET is the change in the IPO price in the aftermarket, calculated as the difference between the

closing price per share on trading day [0, 10, 60, 150, 250], where day zero denotes the IPO date,

and the IPO offer price, scaled by the IPO offer price. As in Model 2, I control for the quality of

12 Beyond the pragmatic reasons for controlling for time period effects using indicators for these three events that

greatly impacted the work of the auditor, internal controls evaluation, and IPO activity, I use this approach because

the inclusion of year fixed effects in this model and Model 3 raise multicollinearity concerns.

21

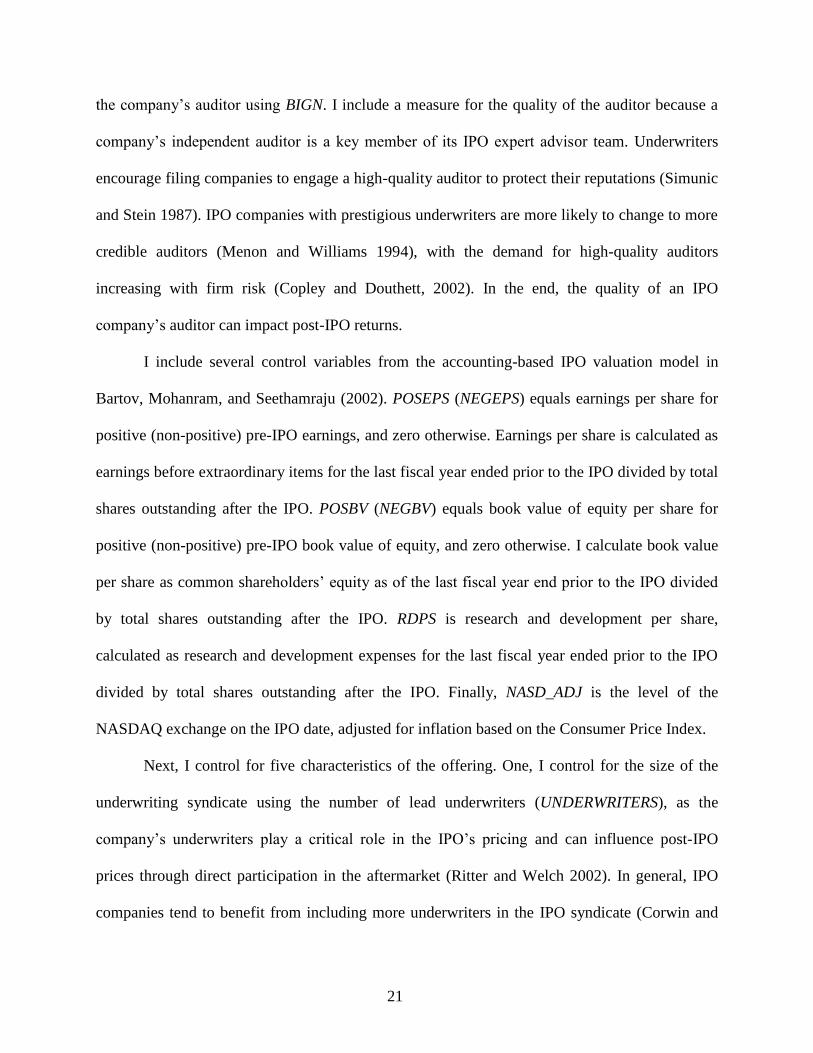

the company’s auditor using BIGN. I include a measure for the quality of the auditor because a

company’s independent auditor is a key member of its IPO expert advisor team. Underwriters

encourage filing companies to engage a high-quality auditor to protect their reputations (Simunic

and Stein 1987). IPO companies with prestigious underwriters are more likely to change to more

credible auditors (Menon and Williams 1994), with the demand for high-quality auditors

increasing with firm risk (Copley and Douthett, 2002). In the end, the quality of an IPO

company’s auditor can impact post-IPO returns.

I include several control variables from the accounting-based IPO valuation model in

Bartov, Mohanram, and Seethamraju (2002). POSEPS (NEGEPS) equals earnings per share for

positive (non-positive) pre-IPO earnings, and zero otherwise. Earnings per share is calculated as

earnings before extraordinary items for the last fiscal year ended prior to the IPO divided by total

shares outstanding after the IPO. POSBV (NEGBV) equals book value of equity per share for

positive (non-positive) pre-IPO book value of equity, and zero otherwise. I calculate book value

per share as common shareholders’ equity as of the last fiscal year end prior to the IPO divided

by total shares outstanding after the IPO. RDPS is research and development per share,

calculated as research and development expenses for the last fiscal year ended prior to the IPO

divided by total shares outstanding after the IPO. Finally, NASD_ADJ is the level of the

NASDAQ exchange on the IPO date, adjusted for inflation based on the Consumer Price Index.

Next, I control for five characteristics of the offering. One, I control for the size of the

underwriting syndicate using the number of lead underwriters (UNDERWRITERS), as the

company’s underwriters play a critical role in the IPO’s pricing and can influence post-IPO

prices through direct participation in the aftermarket (Ritter and Welch 2002). In general, IPO

companies tend to benefit from including more underwriters in the IPO syndicate (Corwin and

22

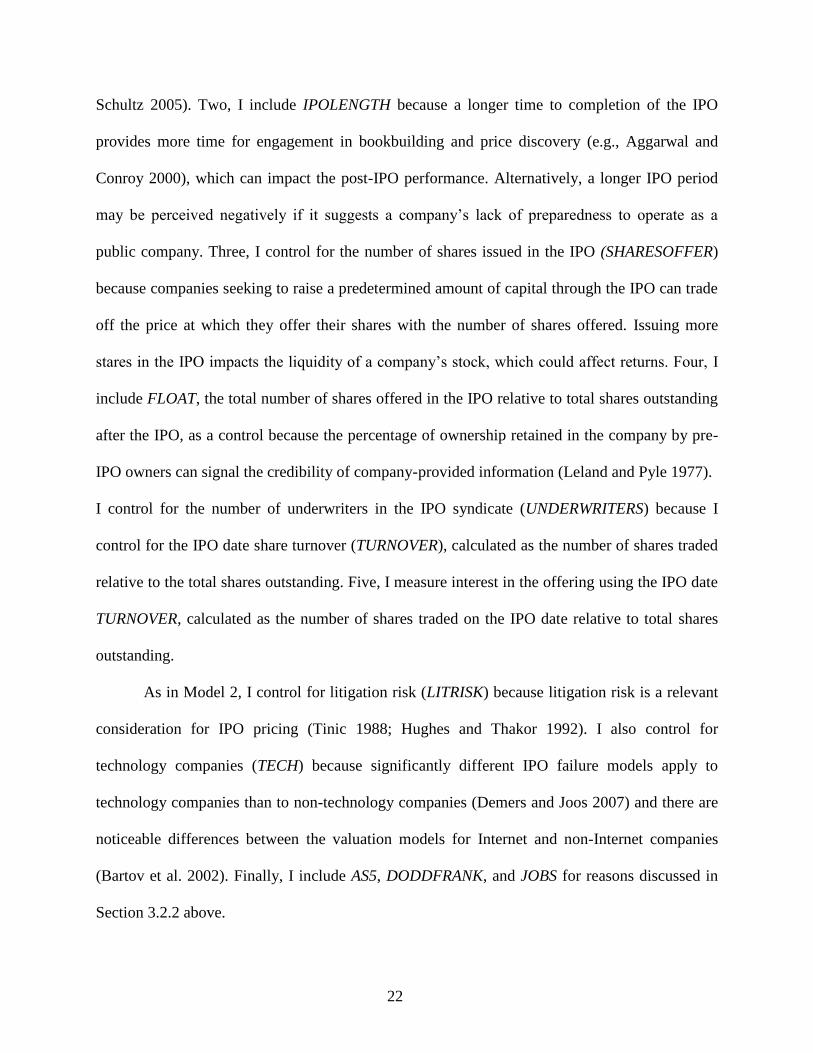

Schultz 2005). Two, I include IPOLENGTH because a longer time to completion of the IPO

provides more time for engagement in bookbuilding and price discovery (e.g., Aggarwal and

Conroy 2000), which can impact the post-IPO performance. Alternatively, a longer IPO period

may be perceived negatively if it suggests a company’s lack of preparedness to operate as a

public company. Three, I control for the number of shares issued in the IPO (SHARESOFFER)

because companies seeking to raise a predetermined amount of capital through the IPO can trade

off the price at which they offer their shares with the number of shares offered. Issuing more

stares in the IPO impacts the liquidity of a company’s stock, which could affect returns. Four, I

include FLOAT, the total number of shares offered in the IPO relative to total shares outstanding

after the IPO, as a control because the percentage of ownership retained in the company by pre-

IPO owners can signal the credibility of company-provided information (Leland and Pyle 1977).

I control for the number of underwriters in the IPO syndicate (UNDERWRITERS) because I

control for the IPO date share turnover (TURNOVER), calculated as the number of shares traded

relative to the total shares outstanding. Five, I measure interest in the offering using the IPO date

TURNOVER, calculated as the number of shares traded on the IPO date relative to total shares

outstanding.

As in Model 2, I control for litigation risk (LITRISK) because litigation risk is a relevant

consideration for IPO pricing (Tinic 1988; Hughes and Thakor 1992). I also control for

technology companies (TECH) because significantly different IPO failure models apply to

technology companies than to non-technology companies (Demers and Joos 2007) and there are

noticeable differences between the valuation models for Internet and non-Internet companies

(Bartov et al. 2002). Finally, I include AS5, DODDFRANK, and JOBS for reasons discussed in

Section 3.2.2 above.

23

Earnings Forecast Model

H4 predicts a negative association between AU 9550 disclosure and post-IPO earnings.

To test H4, I use OLS to estimate an accounting-based earnings prediction model modified from

Harford, Mansi, and Maxwell (2008), in which return on assets (ROA) represents a scaled

measure of earnings. My multivariate model is as follows:

𝑅𝑂𝐴𝑝𝑜𝑠𝑡 = 𝛽0 + 𝛽1𝐴𝑈9550 + 𝛽2𝐴𝑈508𝑂𝑇𝐻𝐸𝑅 + 𝛽3𝐴𝑈508𝐺𝐶 + 𝛽4𝑅𝑂𝐴𝑝𝑟𝑒 +

𝛽5𝑁𝑊𝐶𝑝𝑟𝑒 + 𝛽5𝐿𝐸𝑉𝐸𝑅𝐴𝐺𝐸𝑝𝑟𝑒 + 𝛽6𝐿𝑜𝑔(𝐴𝑇𝑝𝑟𝑒) + 𝛽7𝐿𝑜𝑔(𝑂𝐹𝐹𝐸𝑅_𝐴𝑀𝑇) +

𝑌𝑒𝑎𝑟 𝐼𝑛𝑑𝑖𝑐𝑎𝑡𝑜𝑟𝑠 + 𝜀 (4)

My dependent variable (ROApost) is return on assets for the first fiscal year ended after the

IPO. I calculate return on assets using net income before extraordinary items divided by total

assets. NWCpre equals net working capital, calculated as total current assets (excluding cash and

cash equivalents) less total current liabilities, scaled by total assets. I include year fixed effects,

based on the IPO year, to control for macroeconomic factors that can influence year over year

changes in profitability. All other variables are as previously defined.

IV. EMPIRICAL RESULTS

Descriptive Statistics

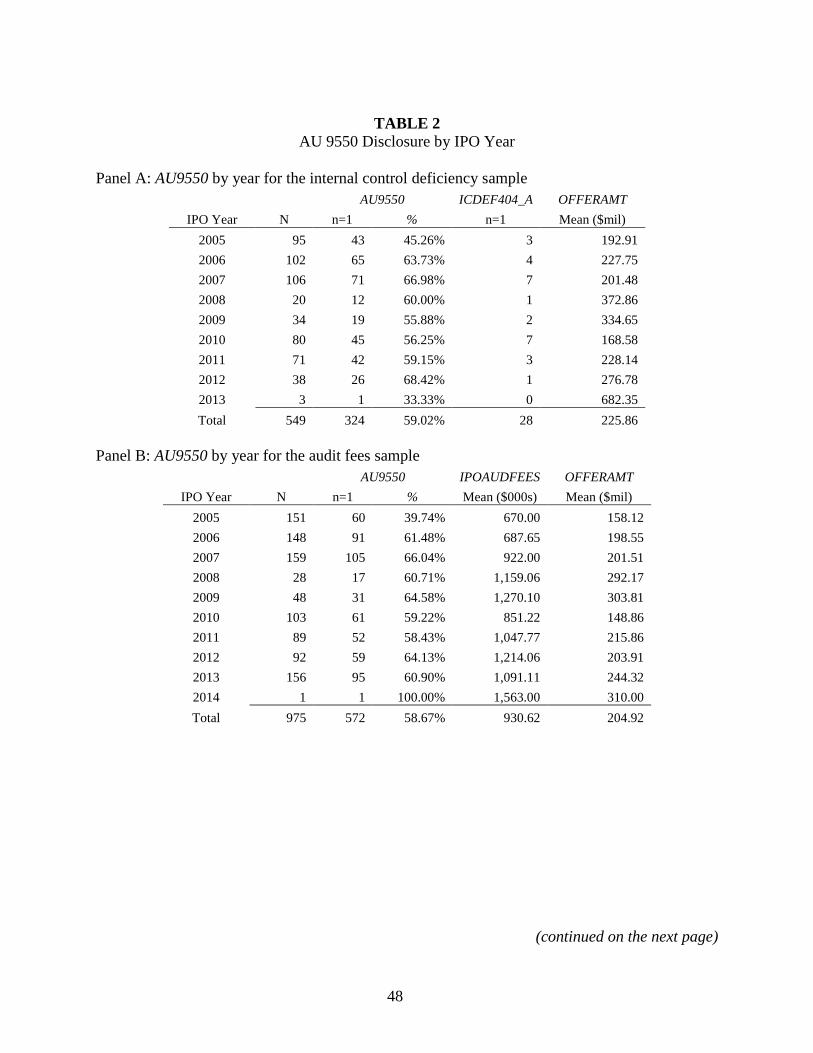

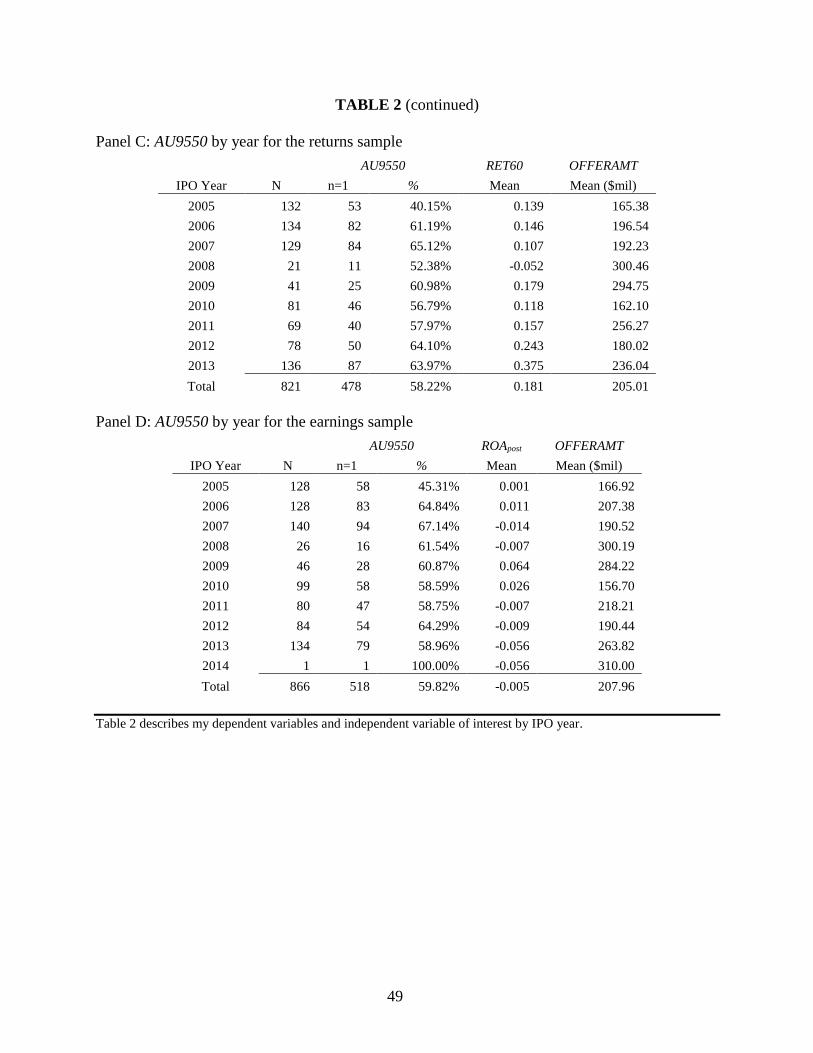

Table 2 presents descriptive statistics for AU 9550 disclosure by IPO year. Table 2, Panel

A, displays the frequency of AU9550, the number of instances of ICDEF404_A, and mean

OFFERAMT by IPO year for the material weakness sample. Table 2, Panel B, displays the

frequency of AU9550 by IPO year and the mean IPOAUDFEES and OFFERAMT for the IPO

audit fees sample. Table 2, Panel C, shows the frequency of AU9550 and means for RET60 and

OFFERAMT by IPO year for the returns sample. Table 2, Panel C, presents the frequency of

AU9550 and means for ROApost and OFFERAMT by IPO year for the earnings forecast sample.

24

All four panels indicate that AU 9550 disclosure is present in more than 50 percent of IPOs in

each year after 2005. Gross IPO proceeds average at little more than $200 million overall. The

mean OFFERAMT for the internal control deficiency sample is larger, relative to the samples for

the other analysis, at $225 million because only accelerated filers are required to comply with

Section 404(b). Panel A reveals that internal control deficiencies are more prevalent in IPOs

completed in 2007 and 2010. Panel B shows that accounting and auditing expenses in connection

with the IPO, on average, exceed $1 million after 2007, except in 2010 when the mean offering

size was substantially lower. As observed in Panel C, post-IPO returns are positive, on average,

throughout the sample period other than in 2008, which represented a low point for IPO activity.

Finally, Panel D shows that companies completing IPOs, on average, are not profitable in the

near term after the IPO. The immediate post financial crisis years of 2009 and 2010 are notable

exceptions, indicating that only companies with stronger earnings prospects completed IPOs

during this time.

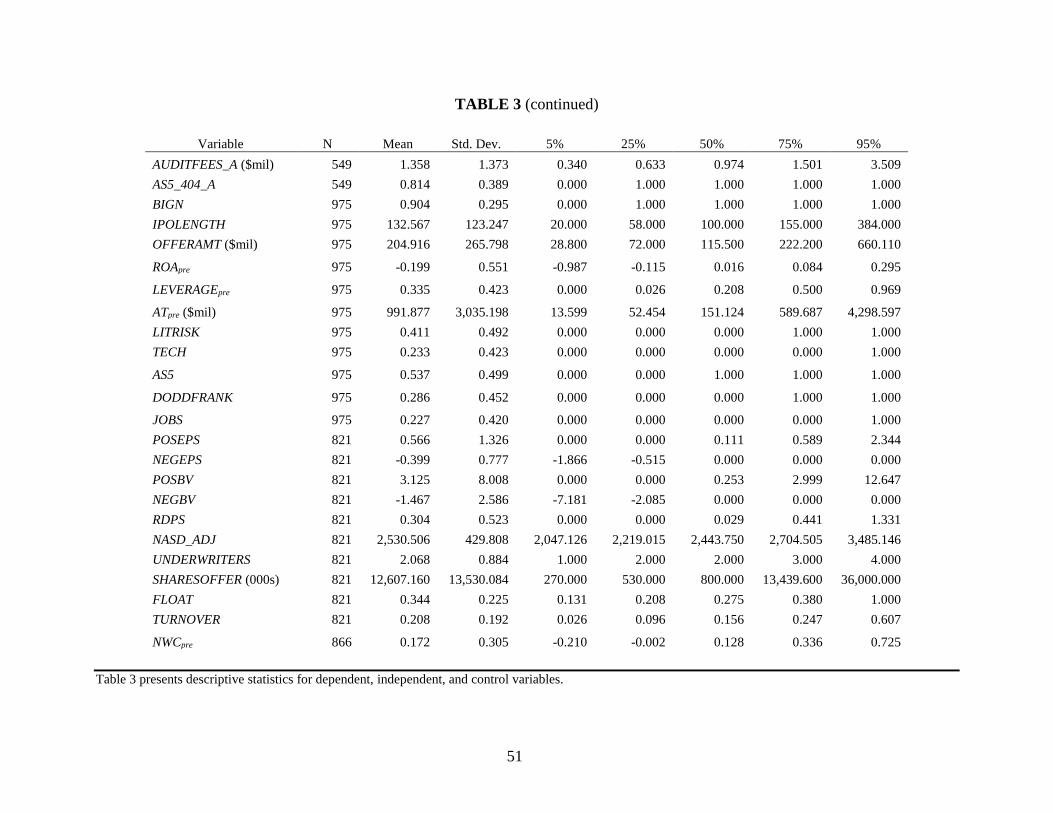

Table 3 presents descriptive statistics for my dependent, independent, and control

variables. Table 3, Panel A, displays descriptive statistics for my dependent variables. The

percentage of observations reporting internal control deficiencies after the IPO (ICDEF404_A) is

5.1 percent.13 Audit fees for first fiscal year after the IPO (AUDITFEES) tend to be higher than

the accounting and auditing expenses associated with the IPO (IPOAUDFEES). Companies have

an average return on assets in the first year after their IPO of -0.5 percent, but more than half of

the companies have a positive return on assets (ROApost).

Table 3, Panel B, displays descriptive statistics for my independent and control variables.

The percentage of observations with AU 9550 disclosure (AU9550) is 58.6 percent, while 41.8

13 Comparatively, of the 5,935 companies Doyle et al. (2007b) identify in the 2003 Compustat database, 779

disclose material weaknesses between August 2002 and 2005, for a rate of 13.1 percent.

25

percent of observations contain other non-going concern non-standard content (AU508OTHER)

and 4.3 percent of observations contain going concern uncertainties (AU508GC). On average, at

the time of the first Section 404(b) report, IPO companies are profitable (LOSS_A), liquid

(CRATIO_A), not at risk of bankruptcy (ZSCORE_A), and carry relatively little inventory

(INVENTORY_A). IPO companies appear to routinely engage high quality auditors (BIGN) and

half of the IPOs use two or more lead underwriters (UNDERWRITERS). Sample IPO companies

complete their IPO in an average of 130 days (IPO_LENGTH) and issue 12.6 million shares

(SHARES_OFFER). The mean (median) IPO date turnover (TURNOVER) is 20.7 percent (15.6

percent). Statistics for variables included in more than one multivariate model are presented only

once for brevity.

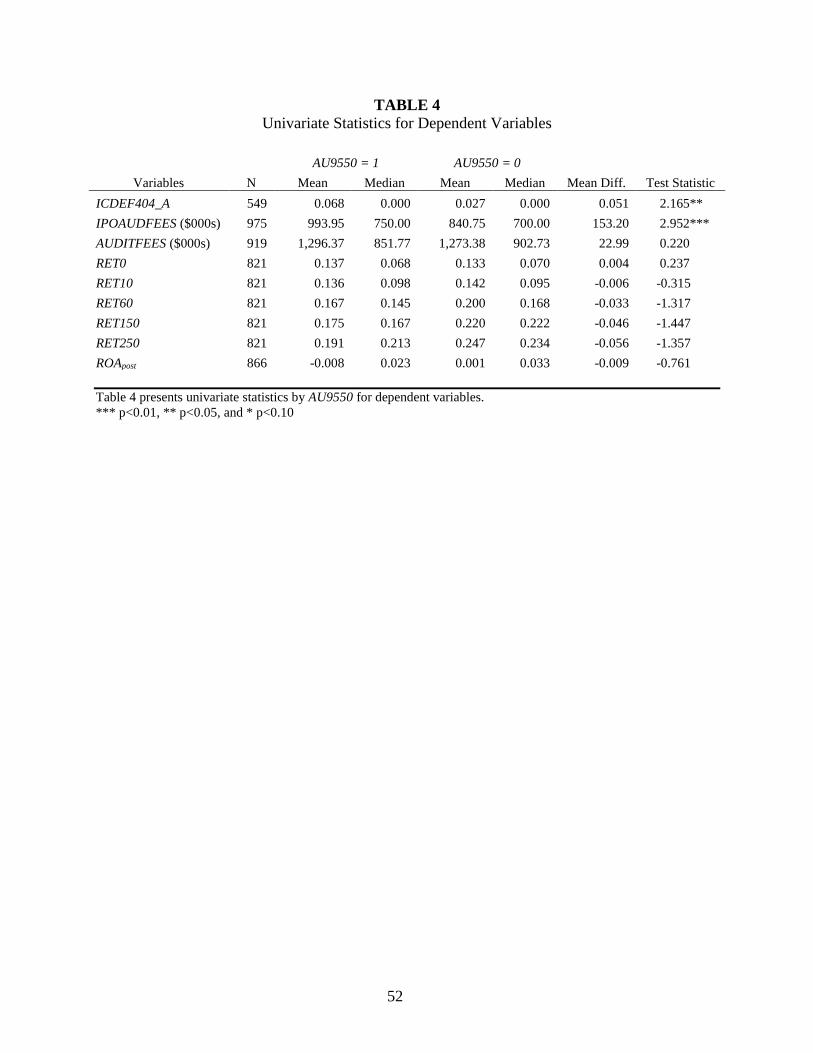

Table 4 presents univariate statistics for the dependent variables in my multivariate

analyses, by observations with and without AU9550. The table shows that IPO companies with

AU9550 are significantly more likely to have post-IPO auditor-reported internal control

deficiencies (p<0.05, two-tailed), indicating a univariate association between AU 9550

disclosure and poor internal controls (ICDEF404_A). I also find a positive and significant

association (p<0.01, two-tailed) between AU9550 and IPO accounting and auditing expenses

(IPOAUDFEES), suggesting that AU9550 is associated with increased auditor effort/risk. The

univariate differences for the post-IPO return and earnings measures are not statistically

significant. Overall, these results provide univariate support for hypotheses H1 and H2.

I analyze the correlations (not reported) between my independent variable and controls in

my multivariate analyses. Correlations between AU9550 and each of the control variables in my

models do not exceed 0.150 in absolute terms. I also perform collinearity diagnostics and find

26

variance inflation factors for all variables are between one and five. Collectively, the results of

these analyses suggest multicollinearity is not a significant concern.

Multivariate Analysis

Table 5 presents the logistic regression results for Model 1. Model 1 includes controls for

factors from prior research found to be associated with the likelihood of auditor-reported

material weaknesses in ICOFR. The discriminant ability of the model is excellent (ROC=0.81),

following Lemeshow and Hosmer (1982). I use Model 1 to test H1, in which I predict that

auditor voluntary disclosure is associated with an increased likelihood of post-IPO auditor-

reported deficiencies in ICOFR in the first year the auditor renders such an opinion. The

coefficient for AU9550 is positive and statistically significant (p<0.05, one-tailed). The

coefficient for AU9550 of 1.260 corresponds to an odds ratio of 4.604, which means that a

company with AU 9550 disclosure is 4.6 times more likely to subsequently have a material

weakness in ICOFR than a company without AU 9550 disclosure. These results provide support

for my prediction in H1 that auditor voluntary disclosure is associated with an increased

likelihood of post-IPO auditor-reported control deficiencies and are consistent with the notion

that AU 9550 disclosure reflects a poor internal control environment.

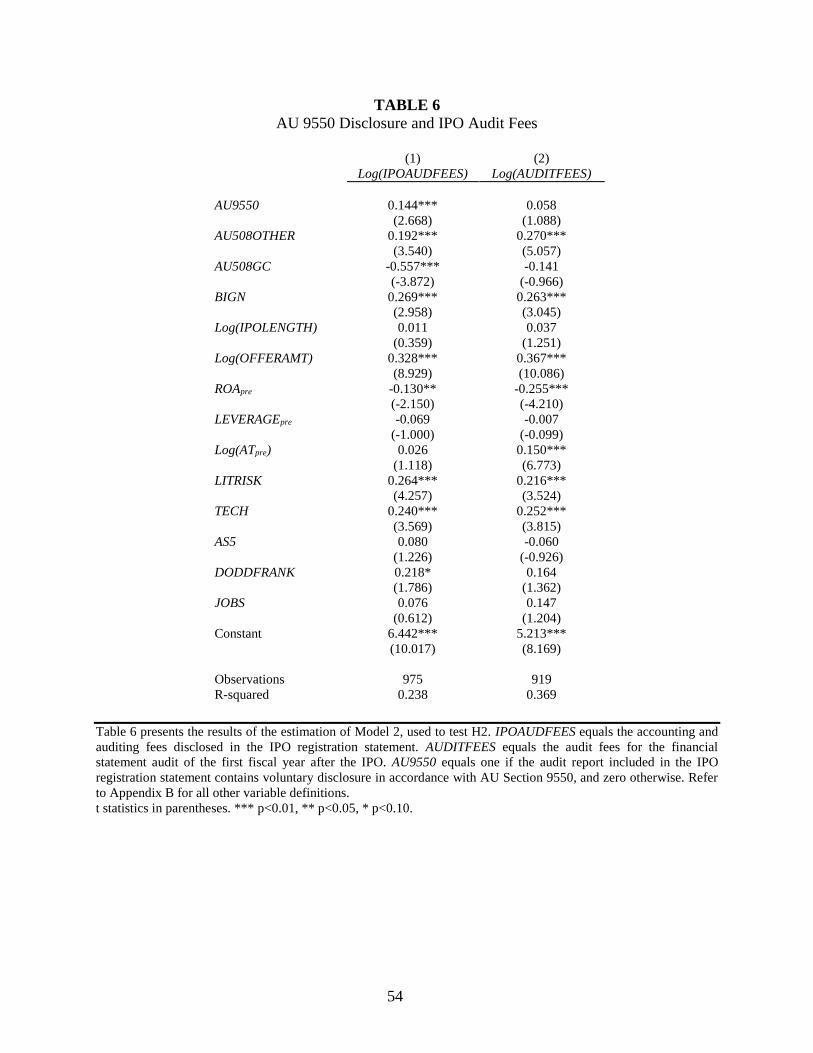

Table 6 presents my estimation of Model 2, which I use to test H2. In H2, I predict a

positive association between auditor voluntary disclosure and audit fees. Column 1 presents the

results for Model 2 estimated using Log(IPOAUDFEES) as the dependent variable. The positive

and statistically significant (p<0.01, one-tailed) coefficient for AU9550 indicates that auditor

voluntary internal controls-related disclosure is associated with higher IPO accounting and

auditing expenses. Column 2 presents the estimation of Model 2 with Log(AUDITFEES) as the

27

dependent variable. The coefficient for AU9550 remains positive, but is not statistically

significant. These results provide some support for H2.

Table 7 presents the results for test of H3, which predicts a negative association between

AU 9550 disclosure and post-IPO returns, where post-IPO returns are measured over various

return windows up to 250 trading days after the IPO date. I find that the coefficient for AU9550

is negative and statistically significant in all five columns, providing support for H3. I interpret

these results to indicate that auditor voluntary internal controls-related disclosure is associated

with lower post-IPO returns.

Table 8 presents the estimation of Model 4, which I use to test the prediction that auditor

voluntary disclosure is associated with lower post-IPO earnings (H4). Consistent with my

prediction, the coefficient for AU9550 is negative and statistically significant (p<0.10, one-

tailed) in Column 1, suggesting that IPO companies that receive AU 9550 disclosure have post-

IPO return on assets that is, on average, 1.3 percent lower than companies without AU 9550

disclosure.

To better understand whether the association between auditor voluntary disclosure and

post-IPO earnings is attributable to real activities or financial reporting quality, I bifurcate

earnings into its accrual and cash flow components. The results of the accrual-based estimation

of Model 4 are presented in Column 2. ACCRUALpost equals income statement-based accruals,

calculated as the difference between earnings before extraordinary items and operating cash

flows, scaled by total assets for the first fiscal year ended after the IPO. The coefficient for

AU9550 is negative and statistically significant (p<0.05, one-tailed). As shown in the cash flow-

based estimation of Model 4 presented in Column 3, there is not a statistically significant

association between AU9550 and OCFpost. Together, these results suggest that the significant

28

association between AU9550 and ROApost can be attributed to the relation between internal

controls and financial reporting quality, rather than to the relation between internal controls and

operating activities.

To summarize, I find results consistent with my hypotheses. Auditor voluntary disclosure

is associated with a higher likelihood of auditor-reported internal control deficiencies in the first

year the auditor opines on ICOFR. I also find that auditor voluntary disclosure is associated with

higher audit fees around the time of the IPO, indicating that the risks conveyed by auditor

voluntary disclosure are reflected in the auditor’s compensation. Finally, I find that auditor

voluntary disclosure is associated with lower post-IPO returns and earnings. Overall, auditor

voluntary disclosure appears informative, as it conveys information relevant to the assessment of

information quality, risk, and future performance.

Addressing Selection Bias

Auditors’ decisions to provide voluntary disclosure do not arise randomly and pose a

potential source of selection bias. I attempt to address the endogeneity in my setting using

coarsened exact matching (CEM). Using stringent matching procedures, like CEM, reduces

endogeneity concerns and the sensitivity of the subsequent regression-based estimation to

specific functional form assumptions (Singh and Agrawal 2011). This approach groups the data

so that substantively indistinguishable values are grouped together and prunes observations from

the data to better balance treated (those with AU 9550 disclosure) and control (those without AU

9550 disclosure) groups. CEM dominates other equal percent bias reducing matching methods

(like propensity score matching) in its ability to reduce imbalance, model dependence, estimation

error, bias, variance, and mean square error (Iacus, King, and Porro 2012).

29

I implement the CEM approach for each of my four multivariate models, forcing the

algorithm to create strata with equal numbers of treated and control observations. For Model 1,

the matching criteria are Big N auditors, market value of equity, and audit fees. The matching

criteria for Model 2 are Big N auditors, IPO offer amount, and pre-IPO return on assets. I use the

number of lead underwriters, number of shares offered, and the proportion of shares issued in the

IPO to total shares outstanding as the matching criteria for Model 3. For Model 4, the matching

criteria are the IPO offer amount and pre-IPO return on assets. I re-estimate each of the

multivariate models using the subset of matched observations and weight by the importance

weights from the CEM output.

Table 9 presents the results of my re-estimated multivariate models. For each model, I

present the ℒ1 statistic from the CEM output. This statistic indicates the balance between the

treated and control groups, taking values between 0 (perfect balance) and 1 (complete

separation). The ℒ1 statistics range from 0.138 for the earnings model (Column 4) to 0.236 for

the returns model (Column 3), suggesting good balance between treated and control has been

achieved. The coefficients for AU9550 remain statistically significant and in the predicted

directions in all four models, providing further support for my hypothesized predictions.14

V. UNTABULATED ADDITIONAL ANALYSES

More prestigious auditors are associated with IPOs that are inherently less risky and have

better long-term performance (Michaely and Shaw 1995). In my sample, roughly 90 percent of

IPO companies engage a Big N auditor, providing little opportunity for companies to signal their

14 In untabulated analyses, I also re-estimate my multivariate models on propensity score matched samples. AU9550

remains statistically significant in Models 1, 2, and 3. In Model 4, where balance between the treated and control

groups for the propensity score matched sample is poor, the coefficient for AU9550 has a p-value of 0.11 (one-

tailed).

30

quality based on auditor choice. To confirm that non-Big N audited IPOs are not driving my

results, I re-estimate my multivariate models on the subset of IPO companies that engage a Big

N auditor for their IPO. AU9550 remains statistically significant and in the predicted direction in

all analyses.

IPO companies provide information pertaining to internal controls in the risk factors

section of the IPO registration statement (Basu, Krishnan, Lee, and Zhang 2013). As such,

management-provided risk factor disclosures are a potential additional source of internal control-

related information available to financial statement users. To confirm that auditor voluntary

disclosure is informative, incremental to management-provided internal control risk factor

disclosures, I search the risk factors section of the registration statements for ‘internal control’. I

include an indicator variable that equals one if the company mentions internal controls, and zero

otherwise, in each of my multivariate models. My results with respect to AU9550 are unchanged

after controlling for internal controls risk factor disclosures.

Table 2 reveals that AU 9550 disclosure was relatively less prevalent for IPOs completed

in 2005, as SOX was in its initial stages of implementation. To confirm that the year 2005 IPOs

do not have an overly influential impact on my results, I re-estimate my multivariate models

excluding the year 2005 IPOs and obtain consistent results.

Internal Control Deficiencies Additional Analyses

Management is required to assess the effectiveness of the company’s internal controls in

accordance with Sections 404(a) and 302 after the IPO.15 I re-estimate Model 1 using two

15 Whereas Section 302 primarily addresses controls over disclosures and does not require independent auditor

attestation, Section 404 more broadly concerns internal controls over financial reporting and does require auditor

attestation. Further, management is required to assess control effectiveness in accordance with Section 302 as early

as the first quarter after the IPO, but has two years (minimum) before Section 404(a) attestation is required.

31

alternative dependent variables.16 One, an indicator variable that equals one if the first Section

404(a) report (after the IPO) in which the company’s management opines on the effectiveness of

ICOFR identifies internal control deficiencies, and zero otherwise. Two, an indicator variable

that equals one if management’s first Section 302 report (after the IPO) identifies internal control

deficiencies, and zero otherwise. AU9550 is not statistically significant in either re-estimation,

indicating that AU9550 is not informative as to Section 404(a) or Section 302 internal control

deficiencies. Prior research that examines internal controls under both Sections 302 and 404 also

finds inconsistent results between the two sections of SOX (e.g., Beneish et al. 2008). Differing

results can largely be attributed to management’s tendency to detect fewer, less severe, and less

pervasive internal control deficiencies (Bedard and Graham 2011). The inconsistent results

suggest that auditor voluntary disclosure indicates more pervasive internal control problems.

There are 28 companies in my sample whose first Section 404(b) report identifies

ineffective internal controls. As a result, the incidence of a control deficiency for IPO companies

is a relatively rare event. In finite samples of rare events data, the method of computing

probabilities of events in logistic analysis can lead to errors in the same direction as biases in the

coefficients (King and Zeng 2001). To confirm that my results are robust to correcting for this

potential bias, I re-estimate Model 1 using rare events logistic regression (King and Zeng 2001)

and Firth logistic regression (Firth 1993; Heinze and Schemper 2002). The coefficient for

AU9550 remains positive and statistically significant (p<0.05, one-tailed) in both estimations.

16 Control variables are re-computed using data from the first fiscal year in which management provides its Section

404(a) report.

32

VI. CONCLUSION

This study investigates the informativeness of auditor voluntary internal controls-related

disclosure in IPO registration statements. Using a sample of initial public offerings completed on

U.S. equity exchanges between 2005 and 2014, I find that auditor voluntary internal controls-

related disclosure is associated with a higher likelihood of post-IPO auditor-reported internal

control deficiencies, higher IPO accounting and auditing expenses, lower post-IPO returns, and

lower post-IPO returns. My results are robust for a sub-sample of IPOs identified using

coarsened exact matching to address the potentially endogenous nature of the auditor’s voluntary

disclosure decision. Overall, my results indicate that auditor voluntary internal controls-related

disclosures are informative in the IPO setting.

My research makes three primary contributions to the accounting literature. One, I

contribute to the voluntary disclosure literature by documenting that auditor voluntary internal

controls-related disclosures are informative as to financial information quality and company risk

in the post-SOX environment. This finding should be of interest to IPO investors and to

regulators reforming the current auditor’s reporting model. Two, I contribute to the internal

controls literature by identifying information in the audit report included in the IPO registration

statement that is informative of future auditor-reported deficiencies in internal controls over

financial reporting. This result should be of interest to legislators that recently passed legislation

to further delay the public communication of internal control deficiencies that may be known at

the IPO date. Finally, I contribute to the audit report literature by studying a previously

unexamined type of auditor disclosure and providing evidence as to the informativeness of audit

report content strictly in the post-SOX regulatory environment.

33

I conduct my research in the IPO setting where companies are not required, nor are they

expected, to have an external auditor opine on the effectiveness of their internal controls. As

well, the information environment for IPO companies is not as complex as that for existing

public companies. Future research may examine whether auditor voluntary disclosure is

differentially informative for existing public companies. Subsequent studies may also consider

how non-equity investor financial statement users and information intermediaries, such as

analysts, appear to use these non-standard audit report disclosures.

34

REFERENCES

Aggarwal, R. and R. Conroy. 2000. Price discovery in the initial public offerings and the role of

the lead underwriter. Journal of Finance 55 (6): 2903-2922

Aharony, J., C. Lin, and M.P. Loeb. 1993. Initial public offerings, accounting choices, and

earnings management. Contemporary Accounting Research 10 (1): 61-81.

Antle, R. and B. Nalebuff. 1991. Conservatism and auditor-client negotiations. Journal of

Accounting Research 29: 31-54.

Asare, S.K., B.C. Fitzgerald, L.E. Graham, J.R. Joe, E.M. Negangard, and C.J. Wolfe. 2013.

Auditors’ internal control over financial reporting decisions: Analysis, synthesis, and

research directions. Auditing: A Journal of Practice & Theory 32 (1): 131-166.

Ashbaugh-Skaife, H., D.W. Collins, and W.R. Kinney Jr. 2007. The discovery and reporting of

internal control deficiencies prior to SOX-mandated audits. Journal of Accounting and

Economics 44: 166-192.

__________, __________, __________, and R. Lafond 2009. The effect of SOX internal

control deficiencies on firm risk and cost of equity. Journal of Accounting Research 47

(1): 1-43.

Barth, M.E., W.R. Landsman, and D.J. Taylor. 2014. The JOBS Act and information uncertainty

in IPO firms. Working paper.

Bartov, E., P. Mohnram, and C. Seethamraju. 2002. Valuation of internet stocks – An IPO

perspective. Journal of Accounting Research 40 (2): 321-346.

Basu, S., J. Krishnan, J.E. Lee, and Y. Zhang. 2013. Economic determinants and consequences

of voluntary disclosure of internal control effectiveness: Evidence from initial public

offerings. Working paper.

Bedard, J.C. and L. Graham. 2011. Detection and severity classifications of Sarbanes-Oxley

Section 404 internal control deficiencies. The Accounting Review 86 (3): 825-855.

__________, R. Hoitash, U. Hoitash, and K. Westermann. 2012. Material weakness remediation

and earnings quality: A detailed examination by type of control deficiency. Auditing: A

Journal of Practice & Theory 31 (1): 57-78.

Beneish, M.D., M.B. Billings, and L. Hodder. 2008. Internal control weaknesses and information

uncertainty. The Accounting Review 83 (3): 665-703.

Benveniste, L.M. and P.A. Spindt. 1989. How investment bankers determine the offer price and

allocation of new issues. Journal of Financial Economics 24: 343-361.

35

Beyer, A., D.A. Cohen, T.Z. Lys, and B.R. Walther. 2010. The financial reporting environment:

Review of the recent literature. Journal of Accounting and Economics 50: 296-343.

Bradshaw, M.T., S.A. Richardson, and R.G. Sloan. 2001. Do analysts and auditors use

information in accruals? Journal of Accounting Research 39 (1): 45-74.

Butler, M., A.J. Leone, and M. Willenborg. 2004. An empirical analysis of auditor reporting and

its association with abnormal accruals. Journal of Accounting and Economics 37: 139-

165.

Cassell, C.A., L.M. Dreher, and L.A. Myers. 2013. Reviewing the SEC’s review process: 10-K

comment letters and the cost of remediation. The Accounting Review 88 (6): 1875-1908.

CFA Institute. 2011. Usefulness of the Independent Auditor’s Report: Survey to the CFA

Institute Financial Reporting Survey Pool. Available at:

http://www.cfainstitute.org/survey/usefulness_of_independent_auditors_report_survey_re

sults_march_2011.pdf

Cheng, M., D. Dhaliwal, and Y. Zhang. 2013. Does investment efficiency improve after the

disclosure of material weaknesses in internal control over financial reporting? Journal of

Accounting and Economics 56 (1): 1-18.

Chow, C.W., and S.J. Rice. 1982. Qualified audit opinions and auditor switching. The

Accounting Review 57 (2): 326-335.

Church, B.K., S.M. Davis, S.A. McCracken. 2008. The audit reporting model: A literature

overview and research synthesis. Accounting Horizons 22 (1): 69-90.

Clinton, S.B., A.S. Pinello, and H.A. Skaife. 2014. The implications of ineffective internal

control and SOX 404 reporting for financial analysts. Journal of Accounting and Public

Policy 33: 303-327.

Committee of Sponsoring Organizations (COSO). 2006. Internal Control over Financial

Reporting – Guidance for Smaller Public Companies. New York, NY: AICPA.

Copley, P.A. and E.B. Douthett, Jr. 2002. The association between auditor choice, ownership

retained, and earnings disclosure by firms making initial public offerings. Contemporary

Accounting Research 19 (1): 49-75.

Corwin, S.A. and P. Schultz. 2005. The role of underwriting syndicates: Pricing, information

production, and underwriter competition. Journal of Finance 55 (1): 443-486.

Czerney, K., J.J. Schmidt, and A.M. Thompson. 2014a. Does auditor explanatory language in

unqualified audit reports indicate increased financial misstatement risk? The Accounting

Review 89 (6): 2115-2149.

36

Czerney, K., J.J. Schmidt, and A.M. Thompson. 2014b. Do investors respond to explanatory

language included in unqualified audit reports? Working paper. Available at:

http://ssrn.com/abstract=2446708

Datar, S.M., G.A. Feltham, and J.S. Hughes. 1991. The role of audits and audit quality in valuing

new issues. Journal of Accounting and Economics 14: 3-49.