Embed Size (px)

Citation preview

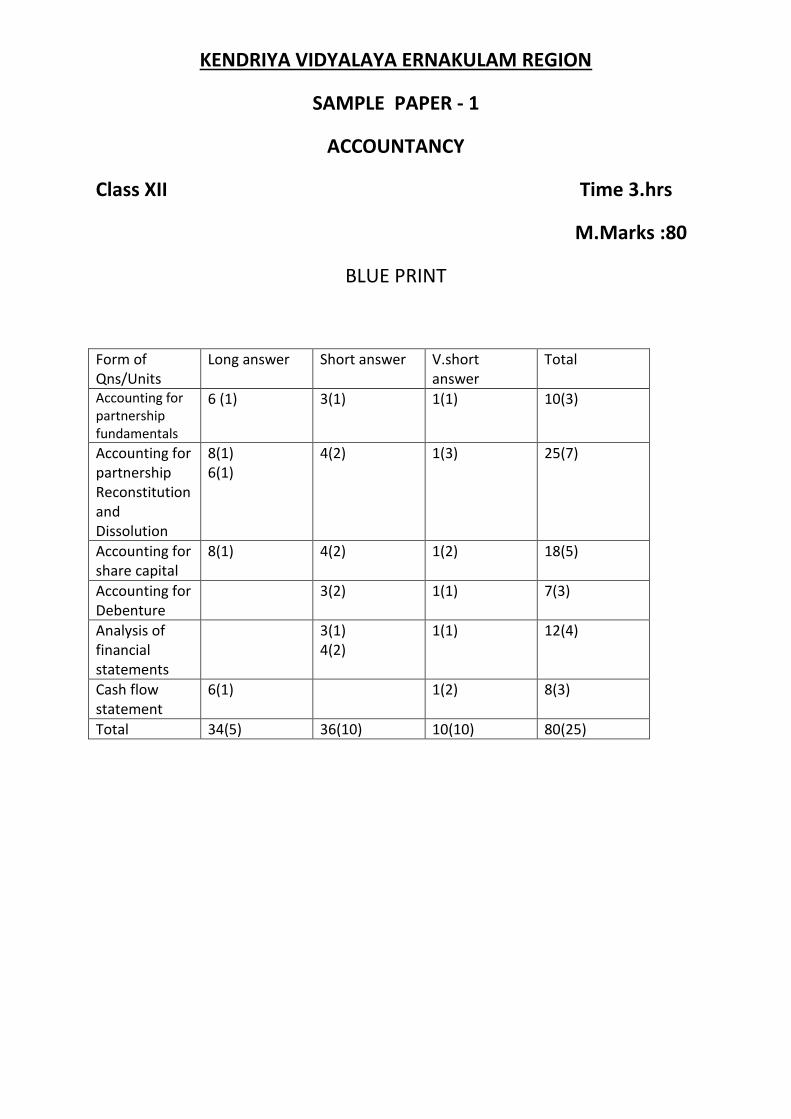

KENDRIYA VIDYALAYA ERNAKULAM REGION

SAMPLE PAPER - 1

ACCOUNTANCY

Class XII Time 3.hrs

M.Marks :80

BLUE PRINT

Form of Qns/Units

Long answer Short answer V.short answer

Total

Accounting for partnership fundamentals

6 (1) 3(1) 1(1) 10(3)

Accounting for partnership Reconstitution and Dissolution

8(1) 6(1)

4(2) 1(3) 25(7)

Accounting for share capital

8(1) 4(2) 1(2) 18(5)

Accounting for Debenture

3(2) 1(1) 7(3)

Analysis of financial statements

3(1) 4(2)

1(1) 12(4)

Cash flow statement

6(1) 1(2) 8(3)

Total 34(5) 36(10) 10(10) 80(25)

KENDRIYA VIDYALAYA ERNAKULAM REGION

SAMPLE QUESTION PAPER - 1

ACCOUNTANCY

Class XII Time 3.hrs

M.Marks: 80

General Instructions

a) This question paper contains Two parts A and B

b) All parts of the questions should be attempted at one place

PART – A

(Accounting for Partnership Firms and Companies)

1. State any two deductions that have to be made from the amount payable to the retiring partner’s capital at the time of retirement? (1)

2. Sundar, Vikram and Avinash were partners in a business dealing in tobacco

Products . After reading news on cancer Avinash gave a notice to dissolve the firm.

Others partners agreed to that. What is the value which induced them to take such

decision (1)

3. State any two reasons for the preparation of Revaluation Account on the Admission of a

Partner (1)

4. X and Y are partners in firm without partnership deed. They agreed to share profits in

the ratio of 3:2. They contributed Rs. 2, 00,000 and 1,50,000 as their capitals. In addition

Y advanced an amount of Rs. 25,000 as loan to the firm. Now he demands interest @

12% p.a on this advance. Is his claim permissible? Give reason in support your

answer? (1)

5. What do you mean by issue of shares as collateral security? (1) 6. What rate of interest is charged on Callas in arrear, if there is no article of association

for a company? (1) 7. What is meant by pro-rata allotment of shares? (1)

8. Ram and shyam are partners in a firm sharing profits and losses in the ratio of 3:2.

Their capital balances on 31 st March 2012 stood as Rs. 3,00,000 and 2,00,000

respectively. Their drawing for the year amounted to Rs. 30,000 and 25,000. After

finalising the financial statements for the year 2012, it is found that interest on drawing

@10% p.a. was not charged before distributing the profits of Rs 75,000. Pass an

adjustment journal entry to rectify the above. Also show your working clearly. (3)

9. On 31 st December 2012 P. Ltd. Redeemed its 8,000, 12% Debentures of Rs 100 each at par. On that date Debenture redemption reserve showed a balance of Rs. 4,00,000. Show necessary journal entries on redemption of debentures (3)

10. On 1st April 2010 X Ltd issued 3,000, 10% debentures of Rs. 100 at par redeemable at a premium of 5% after I year. Pass journal entries for issue and redemption debentures. (3)

11. Anu and Binu were partners in a firm sharing profits and losses in the ratio of 3:2.

They admitted Ginu(an unemployed person) into partnership for 1/5 share in profits of

the business. He brought Rs. 1,50,000 as his share of capital but unable to bring

anything towards goodwill. Good will of the firm was valued at Rs. 1, 00,000.

Goodwill appeared in the balance sheet at Rs. 30,000 Pass necessary journal entries

on admission of Ginu stating the value involved in this context. (4)

12. Anju Ltd. purchased the business of Manju Ltd consisting assets of Rs. 20,00,000

and assumed Liabilities of Rs 5,00,000 for a purchase consideration of

Rs.13,00,000. Anju Ltd paid Rs. 4,00,000 immediately by cheque and for the

settlement of balance amount, issued equity shares of Rs.10 each at a discount of

1 0%. Pass the required journal entries in the books of Anju Ltd. (4)

13. Sad, Bad and Glad are partners sharing profits and losses in the ratio of 4:3:3. On 1st

January 2013 Glad retired from the business. Sad and Bad decided to acquire Glad’s

share of profit equally. The capital balance of the partners after all adjustments

amounted to Rs. 3, 60,000, 3, 00,000 and 2,50,000 respectively. After retirement of

Glad, remaining partners decided to adjust their capitals in their new profit sharing

ratio. Pass journal entries for the amount brought in or withdrawn by the partners.

Also show your working clearly (4)

14. Jint . Ltd issued 5,00,000 equity shares of Rs.10 each at a premium of Rs.50 per

share. The amount was payable Rs.20 on application (including premium of Rs.15)

and Rs.40 on allotment (including premium of Rs35). Applications were received for

6,00,000 shares and Board of Directors decided to allot the shares on a pro-rata

basis to all the applicants, excess application money being adjusted towards amount

due on allotment. Pass journal entries. (4)

15. Pawan,Dhiman and Rupam are partners with Fixed capital balances of Rs.5,00,000,Rs.2,50,000 and Rs.2,50,000 respectively. According to partnership deed the partners are entitled for the following i) Interest on capital @12% p.a. ii) Pawan and Rupam are entitled for a salary of Rs.5,000 each per month. iii) Profits are to be shared in the ratio of 5:3:2. iv) Dhiman, being a handicapped, is entitled to get a guaranteed minimum profit of Rs.15,000 annually.Any deficiency in this regard is to be borne by Pawan and Rupam equally.

Profits for the year ended 31st Dec. 2012 were Rs.2,80,000 (before interest on capital and salary)

Show profit and loss appropriation account for the year 2012 . Also mention the value involved in giving minimum guaranteed profit to Dhiman (6)

16. Rani, Mani and Soni were partners sharing profits and losses in the ratio of 3:2:1.On

31st March, 2007 their Balance Sheet was as under :

Liabilities Rs. Assets Rs.

Capital

Rani

Mani

Soni

General Reserve

Bills Payable

Creditors

20,000

12,000

8,000

12,000

12,000

14,000

Building

Debtors

Bills Receivable

Stock

Investment

Cash at Bank

21,000

12,000

12,000

4,750

13,250

25,000

78,000 78,000

Mani died on 12thJune, 2007.According to the partnership deed the executors are entitled

to the following :

1. the capital to his credit at the time of death and interest thereon @ 10 % p.a.

2. His proportionate share in the reserve

3. His share of profit for the intervening period will be based on the sales during that

period. Which was calculated as Rs.1,00,000. The rate of profit during the past years

had been 10 % on sales.

4. His share of goodwill to be calculated by taking twice the amount of average profits

of last 3 years. The profits were:2003-04 Rs. 8,200, 2004- 05 Rs. 9000 and 2005-06

Rs. 9,800. Pass Journal entries and Prepared Mani’s Capital account to be rendered to

his executors (6)

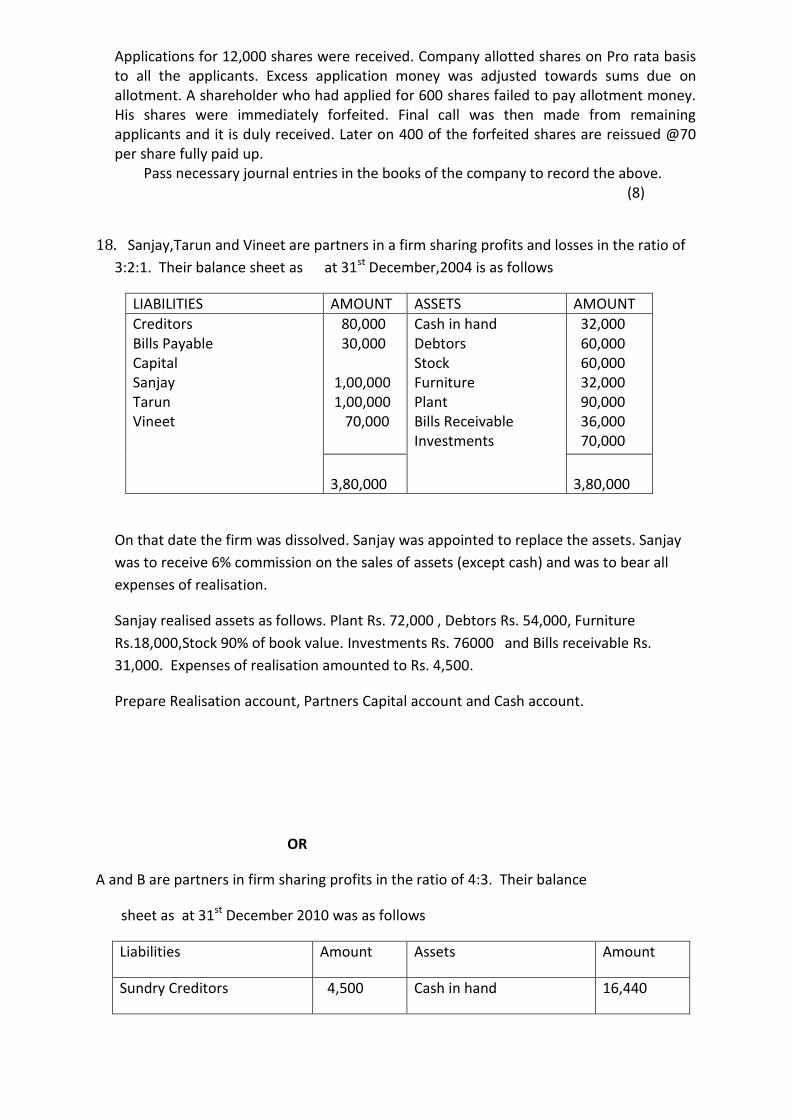

17. SVA Udyog Ltd. Invited applications for 50000 shares @ 10 each at a discount of

10%. Amount was payable as follows: - Application: - Rs. 2, Allotment: - Rs. 3, and

balance on irst and final call.applications were received for 70000 shares.

Directors rejected applications for 10,000shares and pro – rata allotment was

made to the remaining applicants. All the calls were made and amounts were duly

received except the allotment and final call money on 1000 shares. These shares

were forfeited after the call. These shares were re – issued for Rs. 8000 as fully paid

up. Record the journal entries in the books of Raman Ltd.

OR

Paarel Exports Ltd. invited applications for issuing 10,000 equity shares of Rs. 100 each at a premium of 20%.The amount was payable as follows: On Application Rs.30 per share. On Allotment Rs. 50 per share( Including premium) On 1st& final call balance

Applications for 12,000 shares were received. Company allotted shares on Pro rata basis to all the applicants. Excess application money was adjusted towards sums due on allotment. A shareholder who had applied for 600 shares failed to pay allotment money. His shares were immediately forfeited. Final call was then made from remaining applicants and it is duly received. Later on 400 of the forfeited shares are reissued @70 per share fully paid up.

Pass necessary journal entries in the books of the company to record the above. (8)

18. Sanjay,Tarun and Vineet are partners in a firm sharing profits and losses in the ratio of

3:2:1. Their balance sheet as at 31st December,2004 is as follows

LIABILITIES AMOUNT ASSETS AMOUNT

Creditors Bills Payable Capital Sanjay Tarun Vineet

80,000 30,000 1,00,000 1,00,000 70,000

Cash in hand Debtors Stock Furniture Plant Bills Receivable Investments

32,000 60,000 60,000 32,000 90,000 36,000 70,000

3,80,000

3,80,000

On that date the firm was dissolved. Sanjay was appointed to replace the assets. Sanjay

was to receive 6% commission on the sales of assets (except cash) and was to bear all

expenses of realisation.

Sanjay realised assets as follows. Plant Rs. 72,000 , Debtors Rs. 54,000, Furniture

Rs.18,000,Stock 90% of book value. Investments Rs. 76000 and Bills receivable Rs.

31,000. Expenses of realisation amounted to Rs. 4,500.

Prepare Realisation account, Partners Capital account and Cash account.

OR

A and B are partners in firm sharing profits in the ratio of 4:3. Their balance

sheet as at 31st December 2010 was as follows

Liabilities Amount Assets Amount

Sundry Creditors 4,500 Cash in hand 16,440

Employees’ provident Fund

Workmen comp.Reserve

Capitals

A

B

2,980

1,960

30,000

15,000

54,440

Sundry Debtors 6,000

Less Provisions 200

Stock

Fixed assets

Profit & Loss Account

5,800

7,500

24,000

700

54,440

C is admitted for 1/7 share in future profits. C brings Rs. 6.000 as capital and Rs.3,500 for

goodwill in cash. C acquires his share entirely from B. It was further agreed that.

a) provident Fund is to be increased by Rs.1,500.

b) Creditors are to be paid Rs.300 less.

c) All debtors are good.

d) Fixed assets are to be revalued at Rs.21,000

e) Stock included Rs. 900 for obsolete items

Prepare Revaluation account, Partners Capital account and balance sheet after C’s

admission (8)

Part B Financial statement Analysis & Cash Flow Statement

19 . How is ‘Window dressing’ a limitation of Financial statement analysis? (1)

20. State any 2 sources of in flow of cash under investing activity . (1)

21. State whether purchase of machinery by issue of cheque result in

inflow, outflow or no flow of cash (1)

22. Give major headings under which the items are shown on the liability side of a

Company’s Balance Sheet as per Schedule VI Part I of Companies Act 1956. (3)

23. Prepare a comparative income statement with the help of the following

information (4)

Particulars 2010 2011

Revenue from operations

Employee Expenses

Other expenses

10, 00,000

6, 00,000.

2,00,000

15, 00,000

8, 00,000

3,00,000

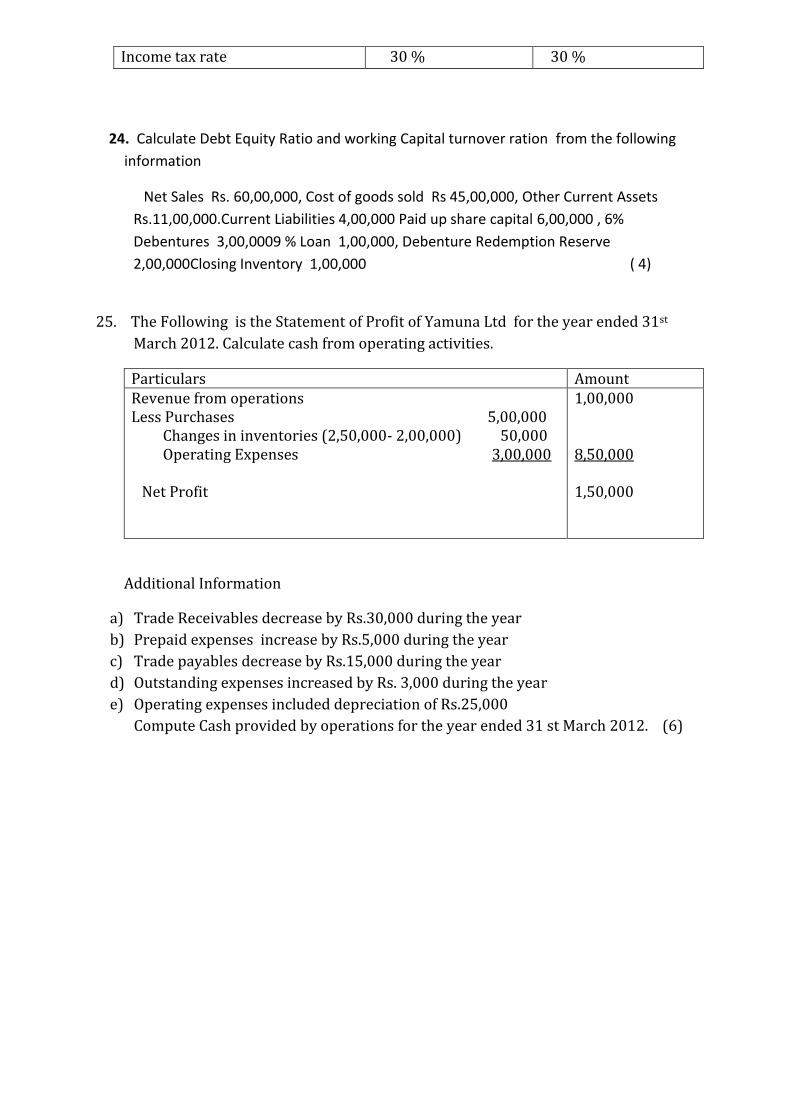

Income tax rate 30 % 30 %

24. Calculate Debt Equity Ratio and working Capital turnover ration from the following

information

Net Sales Rs. 60,00,000, Cost of goods sold Rs 45,00,000, Other Current Assets

Rs.11,00,000.Current Liabilities 4,00,000 Paid up share capital 6,00,000 , 6%

Debentures 3,00,0009 % Loan 1,00,000, Debenture Redemption Reserve

2,00,000Closing Inventory 1,00,000 ( 4)

25. The Following is the Statement of Profit of Yamuna Ltd for the year ended 31st

March 2012. Calculate cash from operating activities.

Particulars Amount Revenue from operations Less Purchases 5,00,000 Changes in inventories (2,50,000- 2,00,000) 50,000 Operating Expenses 3,00,000 Net Profit

1,00,000 8,50,000 1,50,000

Additional Information

a) Trade Receivables decrease by Rs.30,000 during the year

b) Prepaid expenses increase by Rs.5,000 during the year

c) Trade payables decrease by Rs.15,000 during the year

d) Outstanding expenses increased by Rs. 3,000 during the year

e) Operating expenses included depreciation of Rs.25,000

Compute Cash provided by operations for the year ended 31 st March 2012. (6)

CLASS XII – ACCOUNTANCY – SAMPLE PAPER - 1

MARKING SCHEME

1. Accumulated Losses and Revaluation Loss or any other two correct answer 1 mark

2. Social Value- Saving society from use of Tobacco products 1 mark

3. To show the assets and liabilities at their correct value and To ensure that no partner

is at an advantage or disadvantage due to change in the value of assets and liabilities

1 mark

4. No. In the absence of partnership deed interest on loan is provided @ 6% p.a 1 mark

5. Issue debentures as security in addition to the primary security for availing loan from

financial institutions . 1 mark

6. 5 % p.a. 1 mark

7. Allotment of shares on proportionate basis to the applicants in case of

oversubscription 1mark

8.

Particulars Ram Shyam

Profit to be credited in the ratio of 3:2 Less Interest to be debited on drawing @ 5% Net amount to be credited

1650 1500

1100 1250

150 (cr) (-)150 ( Dr)

Shaym’ s Capital A/C Dr 150

To Ram’s Capital A/c 150

( Being adjustment for omission of interest on drawings)

Note : Interest on drawings is charged at an average rate of 5%

(2 marks for working in any form + 1 mark for entry)

9.

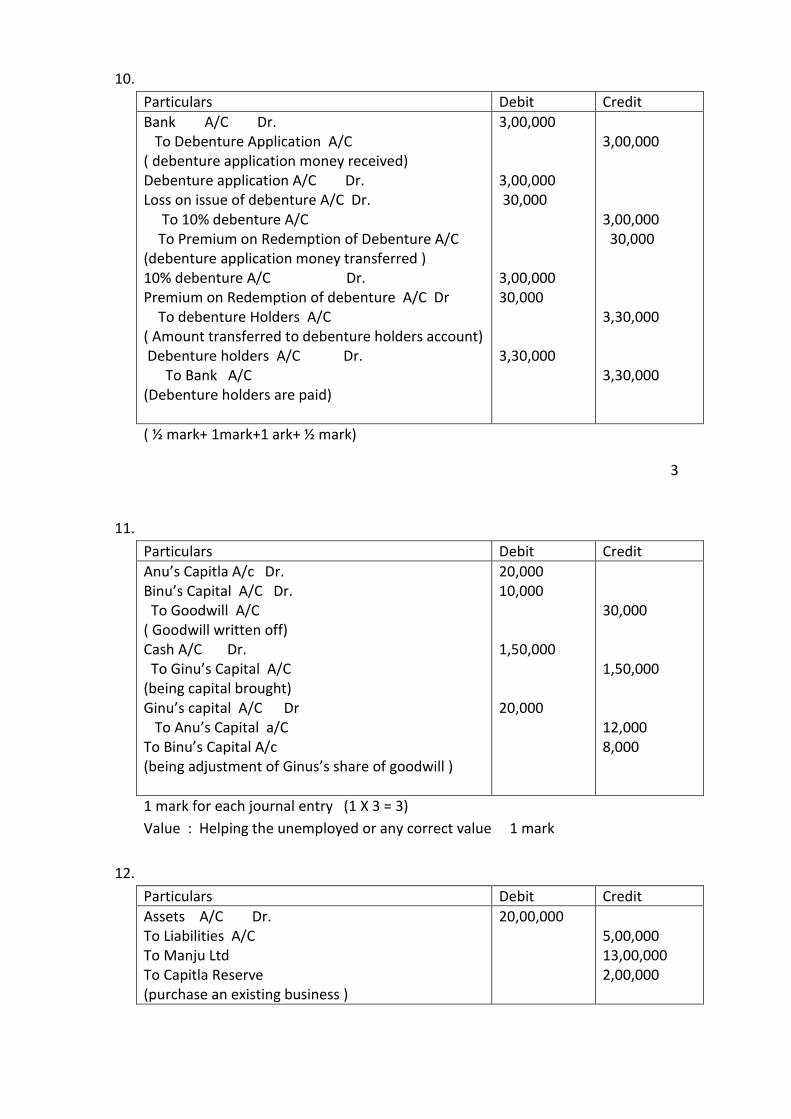

Particulars Debit Credit

12% Debenture A/C Dr. To Debenture Holders A/C ( debenture amount transferred to deb holders a/c) Debenture holders A/C Dr. To Bank A/C (debenture holders are paid) Debenture Redemption Reserve A/C To General Reserve A/C ( balance in the DRR transferred to General reserve)

8,00,000 8,00,000 4,00,000

8,00,000 8,00,000 4,00,000

1 mark for each journal entry.

10.

Particulars Debit Credit

Bank A/C Dr. To Debenture Application A/C ( debenture application money received) Debenture application A/C Dr. Loss on issue of debenture A/C Dr. To 10% debenture A/C To Premium on Redemption of Debenture A/C (debenture application money transferred ) 10% debenture A/C Dr. Premium on Redemption of debenture A/C Dr To debenture Holders A/C ( Amount transferred to debenture holders account) Debenture holders A/C Dr. To Bank A/C (Debenture holders are paid)

3,00,000 3,00,000 30,000 3,00,000 30,000 3,30,000

3,00,000 3,00,000 30,000 3,30,000 3,30,000

( ½ mark+ 1mark+1 ark+ ½ mark)

3

11.

Particulars Debit Credit

Anu’s Capitla A/c Dr. Binu’s Capital A/C Dr. To Goodwill A/C ( Goodwill written off) Cash A/C Dr. To Ginu’s Capital A/C (being capital brought) Ginu’s capital A/C Dr To Anu’s Capital a/C To Binu’s Capital A/c (being adjustment of Ginus’s share of goodwill )

20,000 10,000 1,50,000 20,000

30,000 1,50,000 12,000 8,000

1 mark for each journal entry (1 X 3 = 3)

Value : Helping the unemployed or any correct value 1 mark

12.

Particulars Debit Credit

Assets A/C Dr. To Liabilities A/C To Manju Ltd To Capitla Reserve (purchase an existing business )

20,00,000

5,00,000 13,00,000 2,00,000

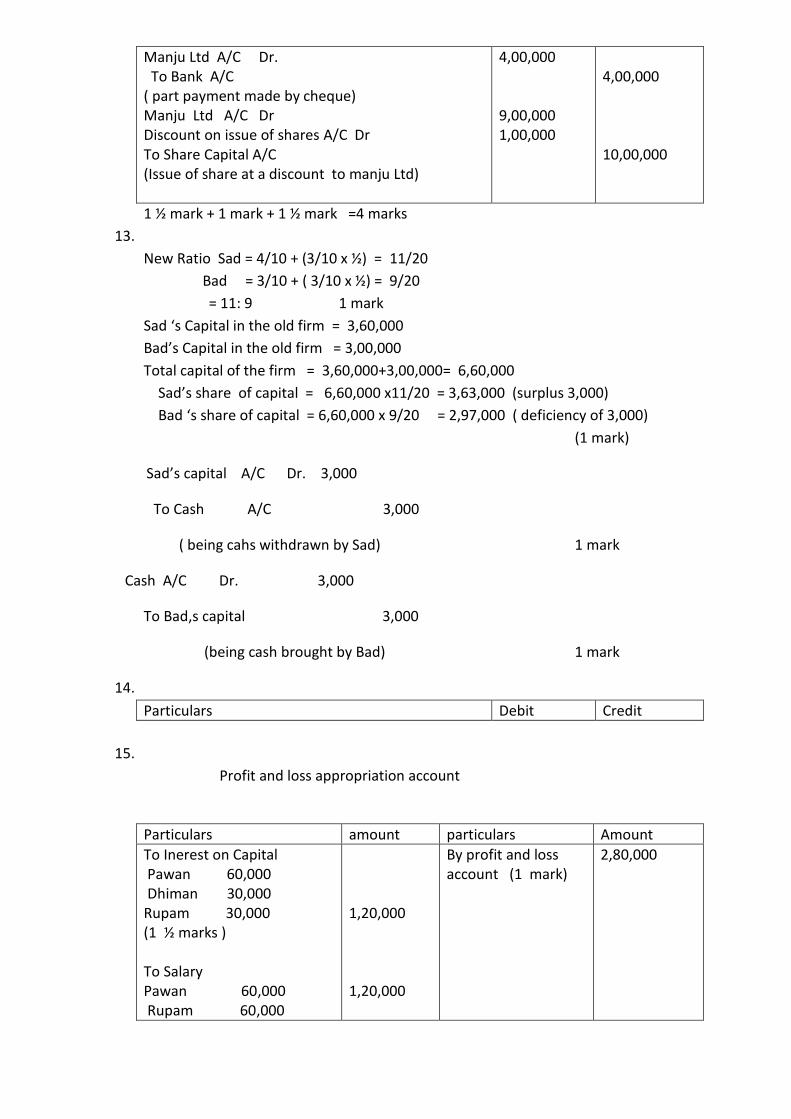

Manju Ltd A/C Dr. To Bank A/C ( part payment made by cheque) Manju Ltd A/C Dr Discount on issue of shares A/C Dr To Share Capital A/C (Issue of share at a discount to manju Ltd)

4,00,000 9,00,000 1,00,000

4,00,000 10,00,000

1 ½ mark + 1 mark + 1 ½ mark =4 marks

13.

New Ratio Sad = 4/10 + (3/10 x ½) = 11/20

Bad = 3/10 + ( 3/10 x ½) = 9/20

= 11: 9 1 mark

Sad ‘s Capital in the old firm = 3,60,000

Bad’s Capital in the old firm = 3,00,000

Total capital of the firm = 3,60,000+3,00,000= 6,60,000

Sad’s share of capital = 6,60,000 x11/20 = 3,63,000 (surplus 3,000)

Bad ‘s share of capital = 6,60,000 x 9/20 = 2,97,000 ( deficiency of 3,000)

(1 mark)

Sad’s capital A/C Dr. 3,000

To Cash A/C 3,000

( being cahs withdrawn by Sad) 1 mark

Cash A/C Dr. 3,000

To Bad,s capital 3,000

(being cash brought by Bad) 1 mark

14.

Particulars Debit Credit

15.

Profit and loss appropriation account

Particulars amount particulars Amount

To Inerest on Capital Pawan 60,000 Dhiman 30,000 Rupam 30,000 (1 ½ marks ) To Salary Pawan 60,000 Rupam 60,000

1,20,000 1,20,000

By profit and loss account (1 mark)

2,80,000

(1 mark) To Pawan’s Capital 18,500 Dhiman’s Capital 15,000 Rupam’s capital 6,500 (1 ½ marks)

40,000

2,80,000

2,80,000

Value : Helping the under privileged section of the society or any other correct value

(1 mark)

16.

Particulars Debit Credit

General Reserve A/C Dr. To Mani’s Capital A/C (Transfer of share of reserve to capital account) Interest on capital A/C Dr To Mani’s Capital A/C (interest on capital provided) Rani’s Capital A/C Dr Soni ‘ sCapital A/C Dr To Mani’s Capital A/C (adjustment for goodwill) Profit and loss Suspense A/C Dr To Mani’s Capital A/C (profit till the date of death adjusted) Mani’s Capital A/C Dr To Mani’s Executors A/C (Balance capital account transferred to Executors account)

4,000 240 3600 1200 3333 24373

4,000 240 4800 3333 24373

1 mark 1 mark 1 mark 1 mark 1 mark

Mani’s Capital Account

Particulars Amount Particulars Amount

To Mani’s Executor’s A/C 24,373 By Balance b/d By General Reserve By Interest on capital By Rani’s Capital By Soni’s capital By profit and loss suspense a/c

12,000 4,000 240 3,600 1,200 3,333

24,373 24,373

1 mark for the Capital Account

17.

Particulars Debit Credit

Bank A/C Dr. To Share Application A/C (application money received) Share application A/C Dr To Share Capital A/C To Share allotment A/C To Bank A/C (application money adjusted) Share allotment A/C Dr Discount on issue of shares A/C Dr To share capital A/C (allotment money due along with premium) Bank A/C Dr Calls in arrear A/C Dr. To Share allotment A/C ( allotment money received) Share Call A/C Dr To Share Capital A/C (share call money due) Bank a/C Dr Calls in arrear A/C Dr To Share Call A/C (call money due with arrear) Share Capital A/C Dr To Share forfeited A/C To Calls in arrear A/C To Discount on issue of share A/C (1000 shares forfeited) Bank A/C Dr

1,40,000 1,,40,000 1,50,000 50,000 1,27,400 2,600 2,00,000 1,96,000 4,000 10,000 8,000 2,000

1,40,000 1,00,000 20,000 20,000 2,00,000 1,30,000 2,00,000 2,00,000 2,400 6,600 1,000

½ mark 1 mark 1 mark 1 mark ½ mark 1 mark 1 mark

Share forfeited A/C Dr To share Capital A/C ( reissue of 1000 shares at for Rs 8000) Share forfeited A/C Dr To Capital Reserve A/C (profit on reissue transferred to capital reserve)

400

10,000 400

1 mark 1 mark

OR

Particulars Debit Credit

18.

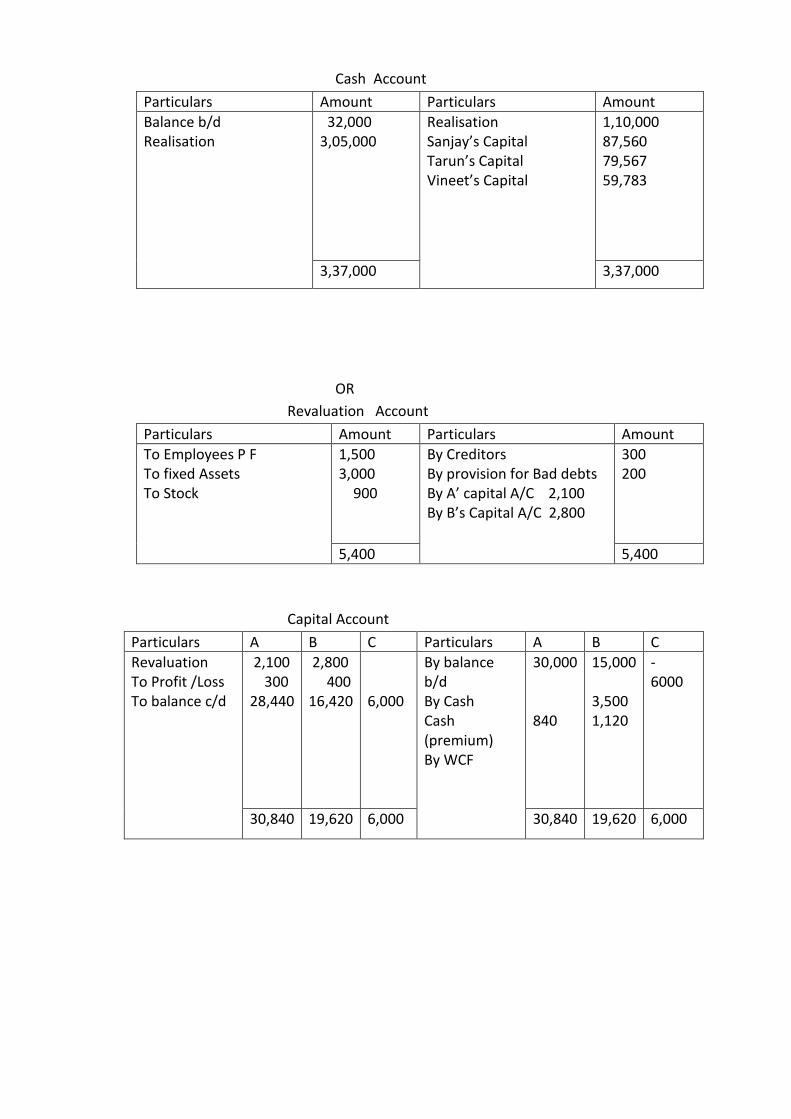

Realisation Account

Particulars Amount Particulars Amount

To plant To debtors To Furniture To stock To investments To B/R To cash (Crs+B/P) To sanjay’s Capital(commission)

90,000 60,000 32,000 60,000 70,000 36,000 1,10,000 18,300

By creditors By Bills Payable By Cash Plant 72,000 Debtors 54,000 Furniture 18,000 Stock 54,000 Investments 76.000 Bills receivable 31,000 By Capitals Sanjay 30,650 Tarun 20,433 Vineet 10,217

80,000 30,000 3,05,000 61,300

4,76,300 4.76.300

Capital Account

Particulars Sanjay Tarun Vineet Particulars Sanjay Tarun Vineet

Realisation Cash

30,650 87,650

20,433 79,567

10,217 59,783

balance b/d Realisation

100000 18,300

100000 70000

118300 100000 70000 118300 100000 70000

Cash Account

Particulars Amount Particulars Amount

Balance b/d Realisation

32,000 3,05,000

Realisation Sanjay’s Capital Tarun’s Capital Vineet’s Capital

1,10,000 87,560 79,567 59,783

3,37,000 3,37,000

OR

Revaluation Account

Particulars Amount Particulars Amount

To Employees P F To fixed Assets To Stock

1,500 3,000 900

By Creditors By provision for Bad debts By A’ capital A/C 2,100 By B’s Capital A/C 2,800

300 200

5,400 5,400

Capital Account

Particulars A B C Particulars A B C

Revaluation To Profit /Loss To balance c/d

2,100 300 28,440

2,800 400 16,420

6,000

By balance b/d By Cash Cash (premium) By WCF

30,000 840

15,000 3,500 1,120

- 6000

30,840 19,620 6,000 30,840 19,620 6,000

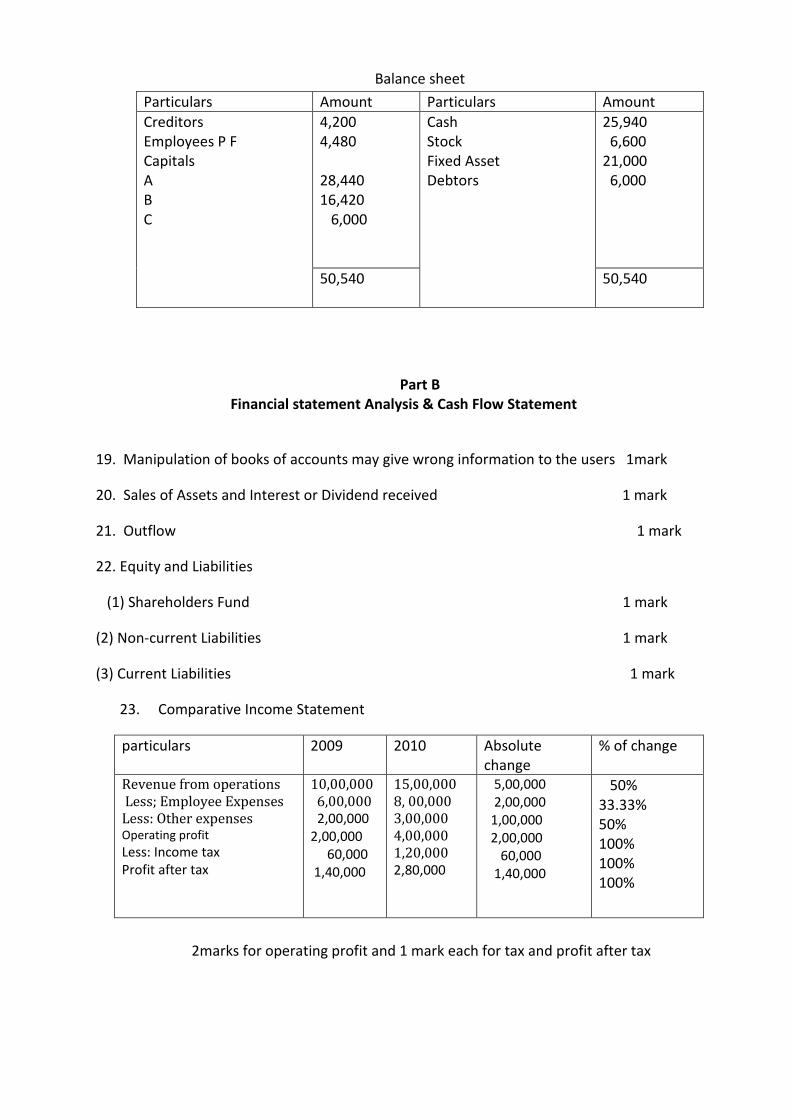

Balance sheet

Particulars Amount Particulars Amount

Creditors Employees P F Capitals A B C

4,200 4,480 28,440 16,420 6,000

Cash Stock Fixed Asset Debtors

25,940 6,600 21,000 6,000

50,540 50,540

Part B Financial statement Analysis & Cash Flow Statement

19. Manipulation of books of accounts may give wrong information to the users 1mark

20. Sales of Assets and Interest or Dividend received 1 mark

21. Outflow 1 mark

22. Equity and Liabilities

(1) Shareholders Fund 1 mark

(2) Non-current Liabilities 1 mark

(3) Current Liabilities 1 mark

23. Comparative Income Statement

particulars 2009 2010 Absolute change

% of change

Revenue from operations Less; Employee Expenses Less: Other expenses Operating profit

Less: Income tax Profit after tax

10,00,000 6,00,000 2,00,000 2,00,000 60,000 1,40,000

15,00,000 8, 00,000 3,00,000 4,00,000 1,20,000 2,80,000

5,00,000 2,00,000 1,00,000 2,00,000 60,000 1,40,000

50% 33.33% 50% 100% 100% 100%

2marks for operating profit and 1 mark each for tax and profit after tax

24. Debt Equity Ratio = Debt /Equity

= 4,00,000/8,00,000 = .5:1 2 marks

Working Capital Turnover Ratio = Net Sales / working Capital

= 6,00,000/8,00,000 = 7.5 Times 2 marks

25 Cash from Operating Activity

Particulars Amount Amount

Net profit before Tax Adjustment for Depreciation Operating profit before working capital changes Add: Decrease in Current Assets Inventory Trade Receivables Increase in Current Liabilities Outstanding Expenses Less : Increase in current Assets Prepaid Expenses Decrease in Current Liabilities Trade Payables

50,000 30,000 3,000

1,50,000 25,000

1,75,000 83,000

5,000 15,000

2,58,000 20,000

2,38,000