Embed Size (px)

Citation preview

Kenneth C. Gardiner, CPA, CCIFP, CDAJoseph Chemotti, CPA, CCIFP

Thomas V. Fiscoe, CPA, CGMA

Kenneth C. Gardiner, CPA, CCIFP, CDA, Audit [email protected]

Joseph Chemotti, CPA, CCIFP, Audit [email protected]

Thomas V. Fiscoe, CPA, CGMA, Audit [email protected]

Dannible & McKee’s 39th Annual Tax & Financial Planning Conference

DoubleTree by Hilton, East Syracuse, New York

November 10, 2016

Accounting, Reporting, and Corporate Governance Update

3

This presentation is © 2016 Dannible & McKee, LLP. All rights reserved. No part of thisdocument may be reproduced, transmitted or otherwise distributed in any form or by anymeans, electronic or mechanical, including by photocopying, facsimile transmission,recording, rekeying, or using any information storage and retrieval system, without writtenpermission from Dannible/McKee and Associates, Ltd. Any reproduction, transmission ordistribution of this form or any material herein is prohibited and is in violation of U.S. law.Dannible/McKee and Associates, Ltd. expressly disclaims any liability in connection withthe use of this presentation or its contents by any third party.

This presentation and any related materials are designed to provide accurate informationin regard to the subject matter covered, and are provided solely as a teaching tool, withthe understanding that neither the instructor, author, publisher, nor any other individualinvolved in its distribution is engaged in rendering legal, accounting, or other professionaladvice and assumes no liability in connection with its use. Because regulations, laws, andother professional guidance are constantly changing, a professional should be consultedif you require legal or other expert advice.

Copyright / Disclaimer

4

Any tax advice contained herein was not intended or written to be used, andcannot be used, for the purpose of avoiding penalties that may be imposedunder the Internal Revenue Code or applicable state or local tax law provisions.

Circular 230

5

Kenneth C. Gardiner, CPA, CCIFP, CDAPartner In-Charge of Assurance Services

2016 Tax and Financial Planning ConferenceNovember 10, 2016

New Standards for Revenue Recognition and Leases

6

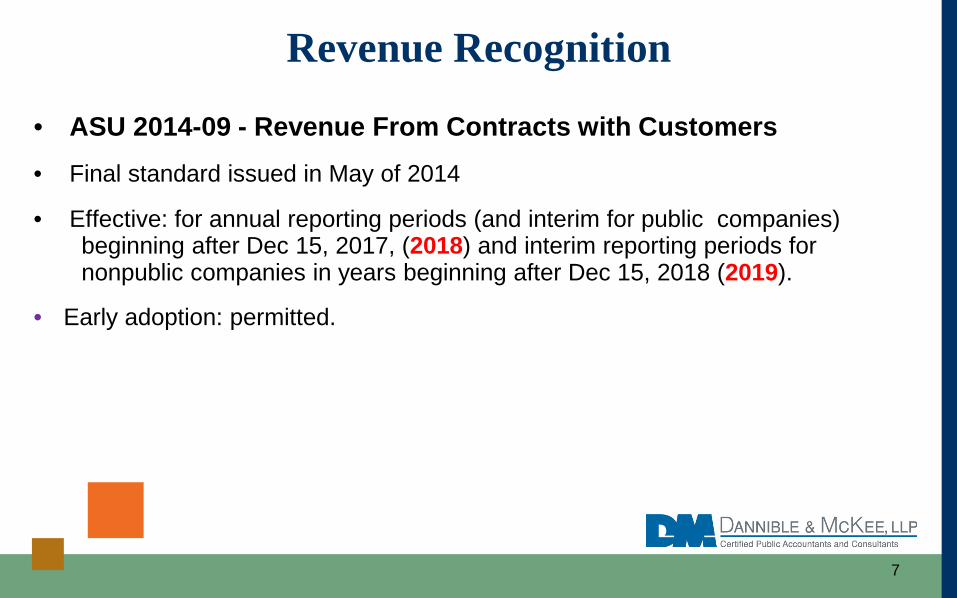

• ASU 2014-09 - Revenue From Contracts with Customers• Final standard issued in May of 2014

• Effective: for annual reporting periods (and interim for public companies) beginning after Dec 15, 2017, (2018) and interim reporting periods for nonpublic companies in years beginning after Dec 15, 2018 (2019).

• Early adoption: permitted.

Revenue Recognition

7

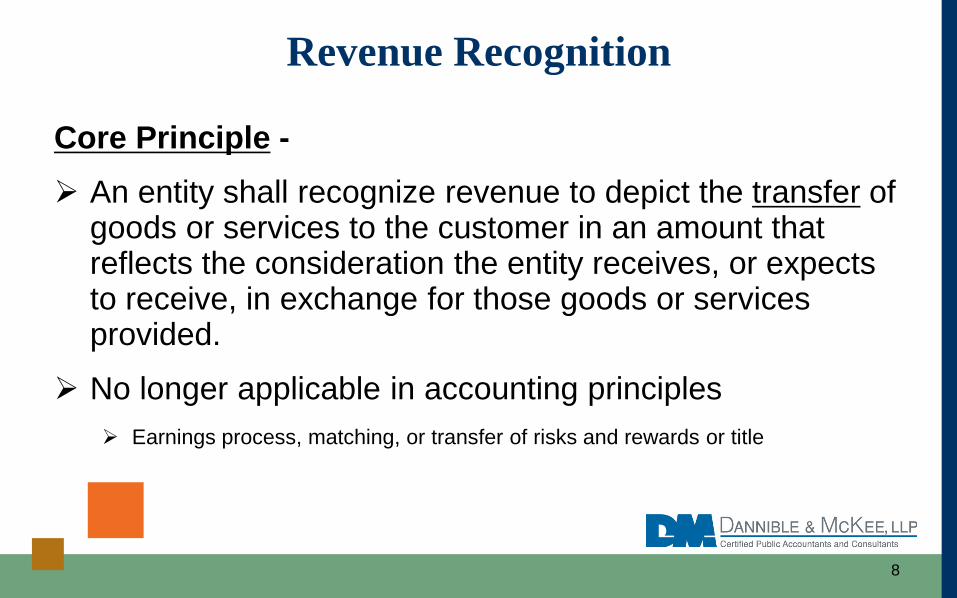

Core Principle - An entity shall recognize revenue to depict the transfer of

goods or services to the customer in an amount that reflects the consideration the entity receives, or expects to receive, in exchange for those goods or services provided.

No longer applicable in accounting principles Earnings process, matching, or transfer of risks and rewards or title

Revenue Recognition

8

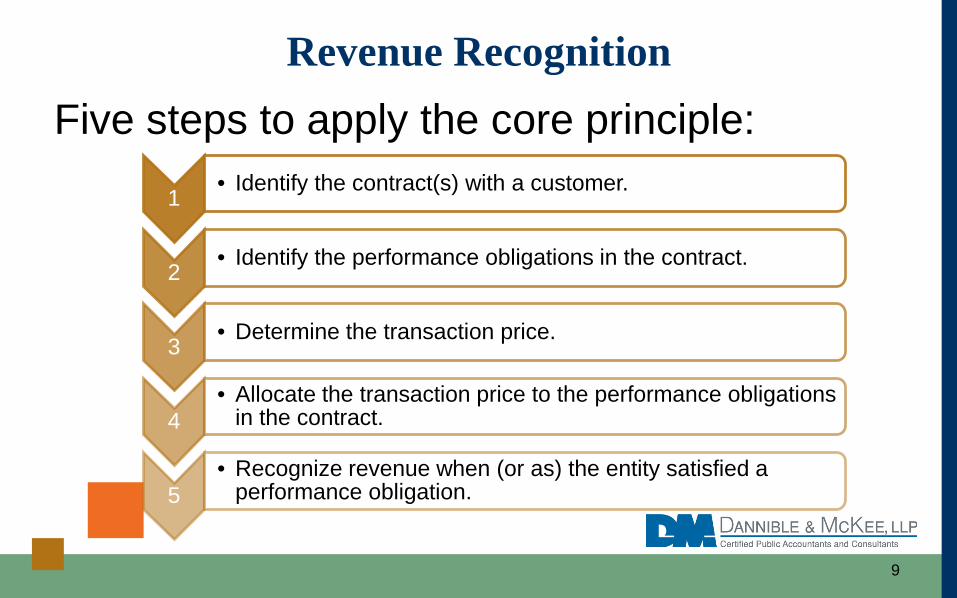

Five steps to apply the core principle:Revenue Recognition

9

1• Identify the contract(s) with a customer.

2• Identify the performance obligations in the contract.

3• Determine the transaction price.

4• Allocate the transaction price to the performance obligations

in the contract.

5• Recognize revenue when (or as) the entity satisfied a

performance obligation.

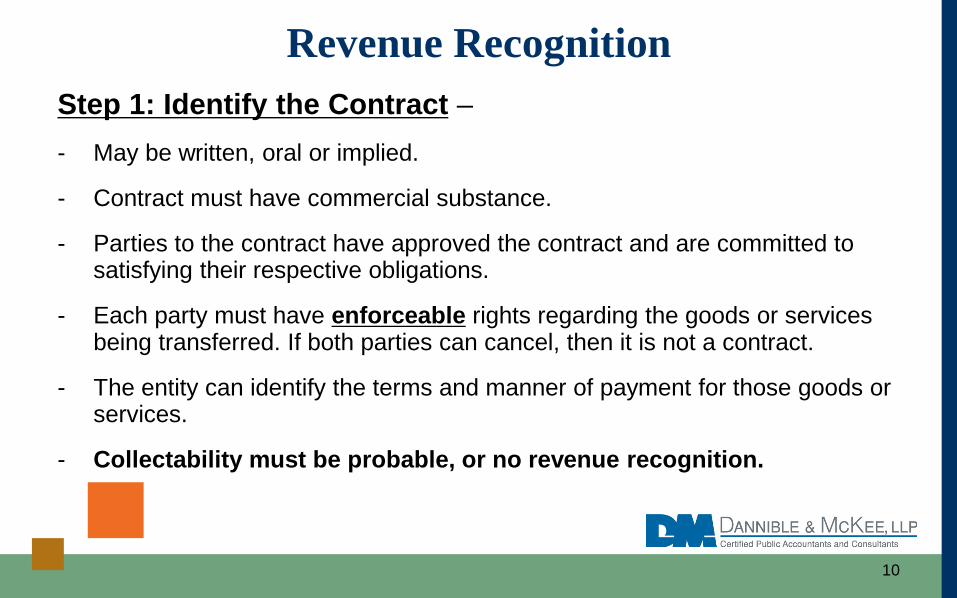

Step 1: Identify the Contract –- May be written, oral or implied.

- Contract must have commercial substance.

- Parties to the contract have approved the contract and are committed to satisfying their respective obligations.

- Each party must have enforceable rights regarding the goods or services being transferred. If both parties can cancel, then it is not a contract.

- The entity can identify the terms and manner of payment for those goods or services.

- Collectability must be probable, or no revenue recognition.

Revenue Recognition

10

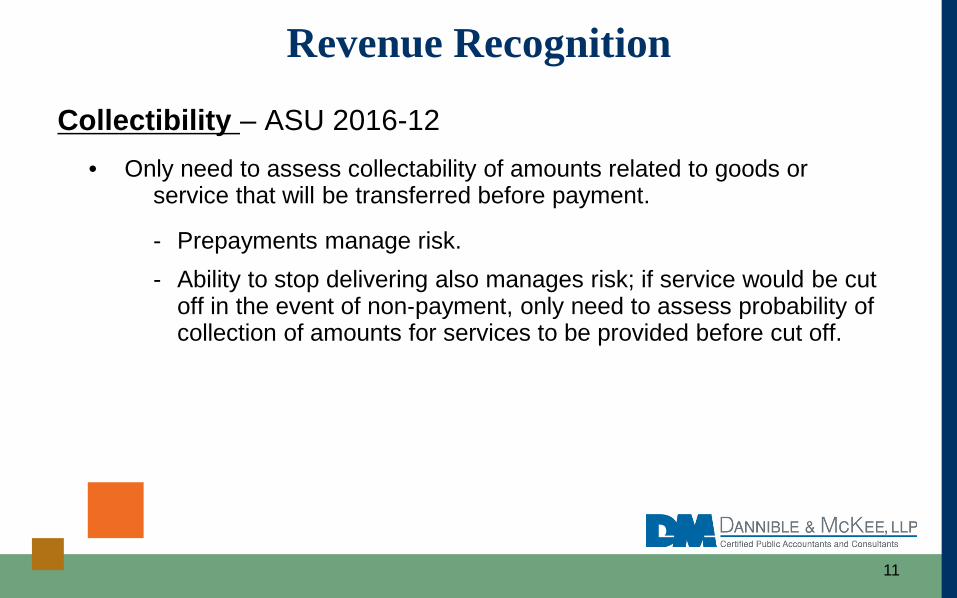

Collectibility – ASU 2016-12• Only need to assess collectability of amounts related to goods or

service that will be transferred before payment.

- Prepayments manage risk. - Ability to stop delivering also manages risk; if service would be cut

off in the event of non‐payment, only need to assess probability of collection of amounts for services to be provided before cut off.

Revenue Recognition

11

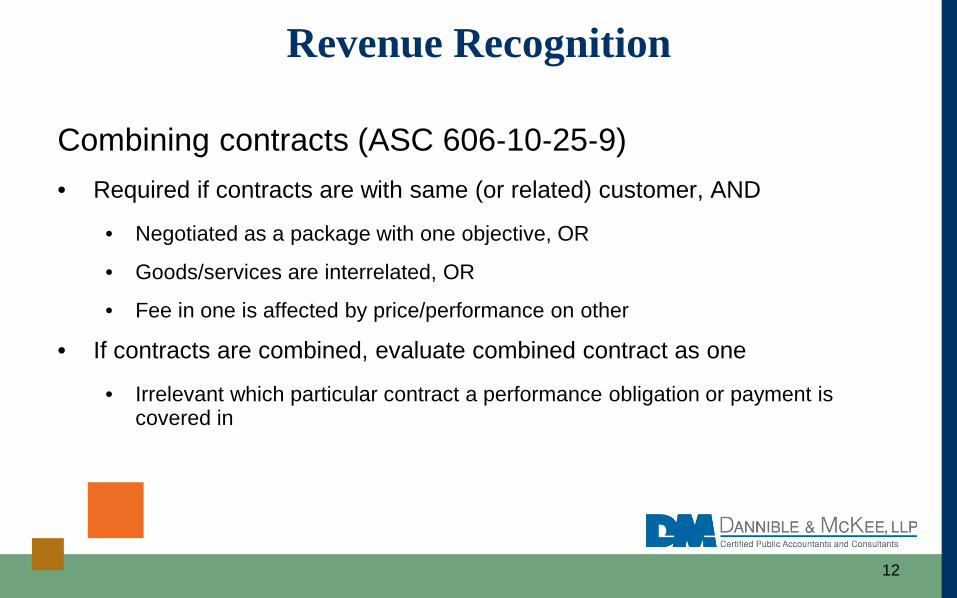

Combining contracts (ASC 606‐10‐25‐9)• Required if contracts are with same (or related) customer, AND

• Negotiated as a package with one objective, OR

• Goods/services are interrelated, OR

• Fee in one is affected by price/performance on other

• If contracts are combined, evaluate combined contract as one

• Irrelevant which particular contract a performance obligation or payment is covered in

Revenue Recognition

12

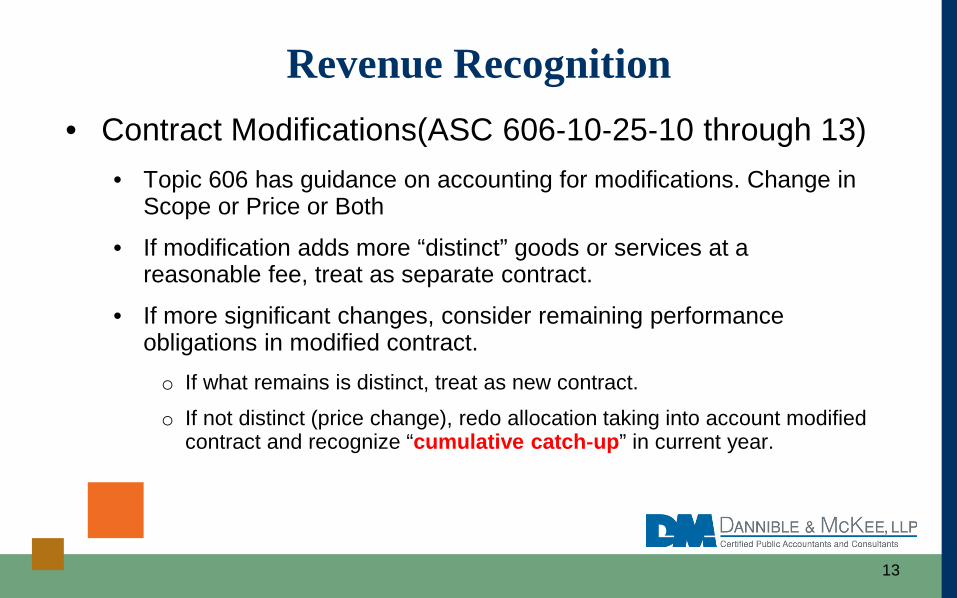

• Contract Modifications(ASC 606‐10‐25‐10 through 13)• Topic 606 has guidance on accounting for modifications. Change in

Scope or Price or Both

• If modification adds more “distinct” goods or services at a reasonable fee, treat as separate contract.

• If more significant changes, consider remaining performance obligations in modified contract.o If what remains is distinct, treat as new contract.

o If not distinct (price change), redo allocation taking into account modified contract and recognize “cumulative catch‐up” in current year.

Revenue Recognition

13

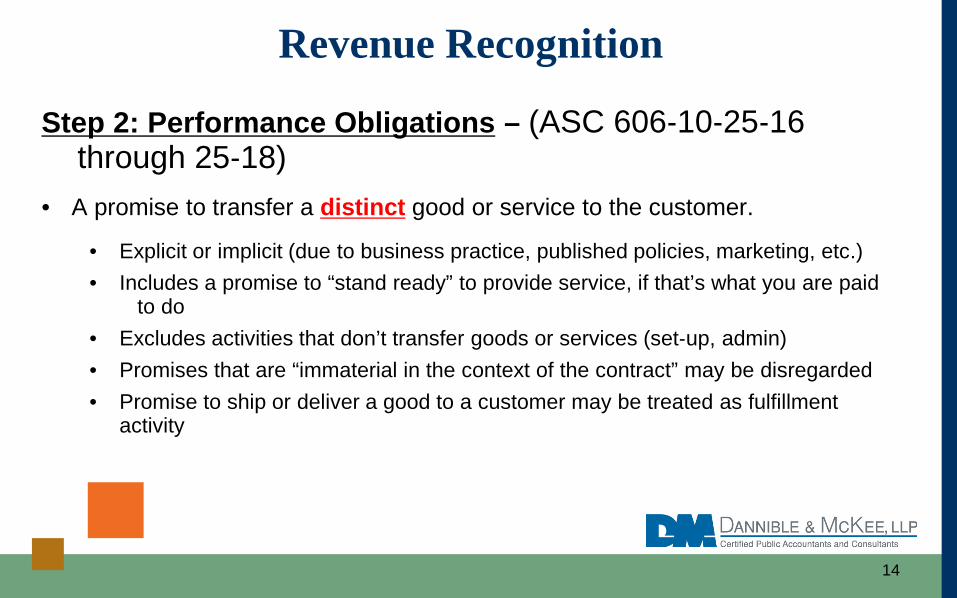

Step 2: Performance Obligations – (ASC 606‐10‐25‐16 through 25‐18)

• A promise to transfer a distinct good or service to the customer.

• Explicit or implicit (due to business practice, published policies, marketing, etc.)• Includes a promise to “stand ready” to provide service, if that’s what you are paid

to do• Excludes activities that don’t transfer goods or services (set‐up, admin)• Promises that are “immaterial in the context of the contract” may be disregarded• Promise to ship or deliver a good to a customer may be treated as fulfillment

activity

Revenue Recognition

14

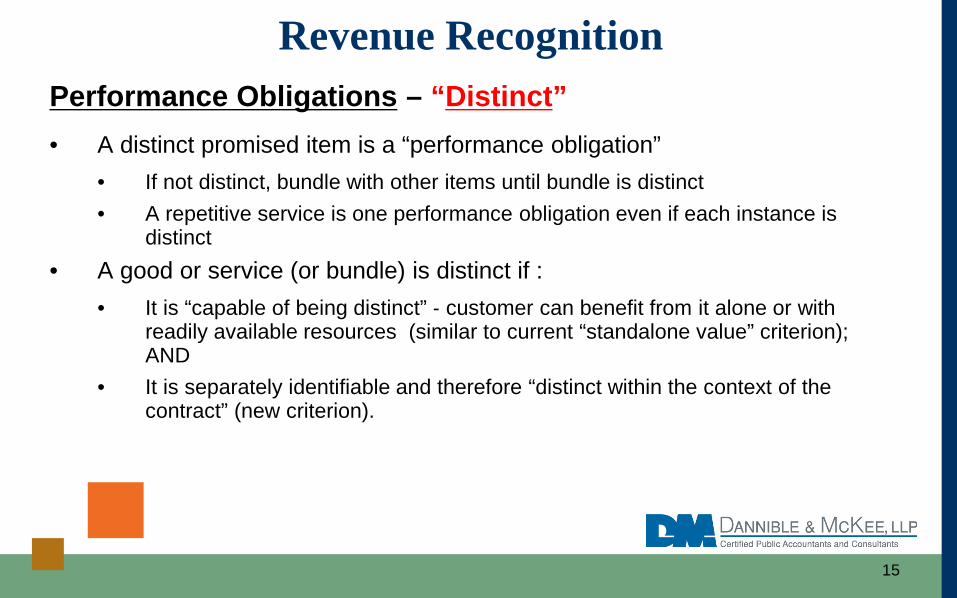

Performance Obligations – “Distinct”• A distinct promised item is a “performance obligation”

• If not distinct, bundle with other items until bundle is distinct• A repetitive service is one performance obligation even if each instance is

distinct• A good or service (or bundle) is distinct if :

• It is “capable of being distinct” ‐ customer can benefit from it alone or with readily available resources (similar to current “standalone value” criterion); AND

• It is separately identifiable and therefore “distinct within the context of the contract” (new criterion).

Revenue Recognition

15

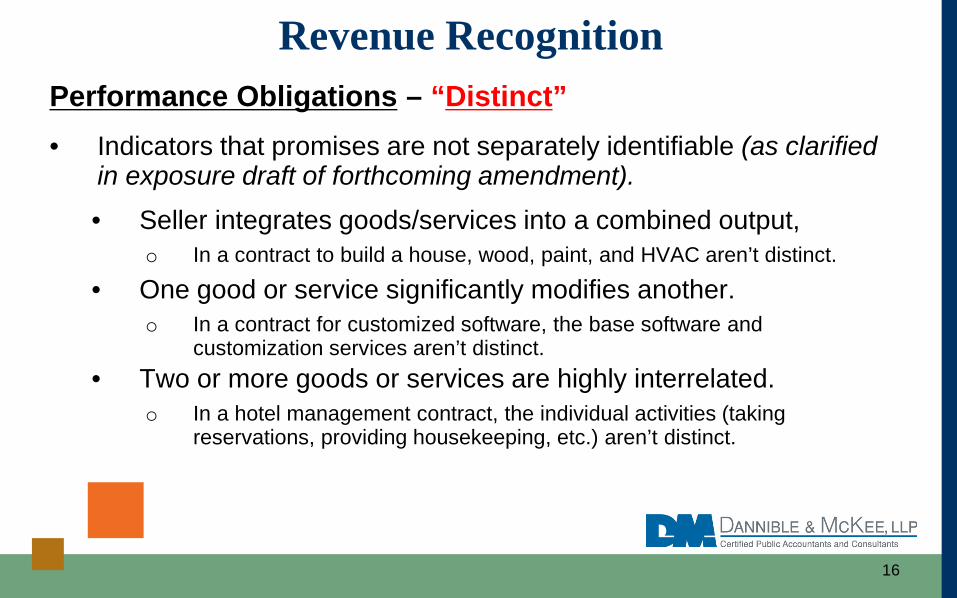

Performance Obligations – “Distinct”• Indicators that promises are not separately identifiable (as clarified

in exposure draft of forthcoming amendment).

• Seller integrates goods/services into a combined output,o In a contract to build a house, wood, paint, and HVAC aren’t distinct.

• One good or service significantly modifies another.o In a contract for customized software, the base software and

customization services aren’t distinct.• Two or more goods or services are highly interrelated.

o In a hotel management contract, the individual activities (taking reservations, providing housekeeping, etc.) aren’t distinct.

Revenue Recognition

16

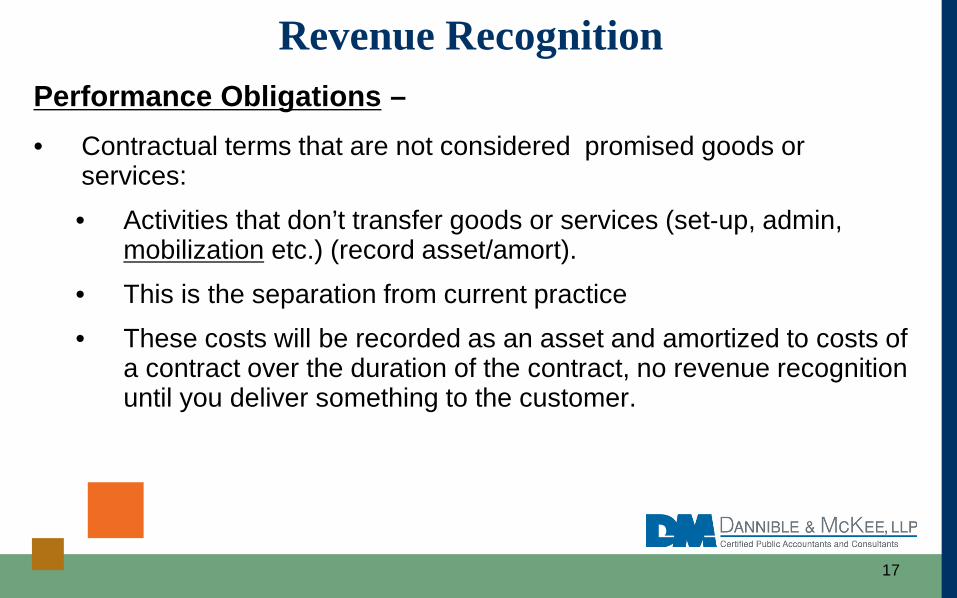

Performance Obligations –• Contractual terms that are not considered promised goods or

services:

• Activities that don’t transfer goods or services (set‐up, admin, mobilization etc.) (record asset/amort).

• This is the separation from current practice• These costs will be recorded as an asset and amortized to costs of

a contract over the duration of the contract, no revenue recognition until you deliver something to the customer.

Revenue Recognition

17

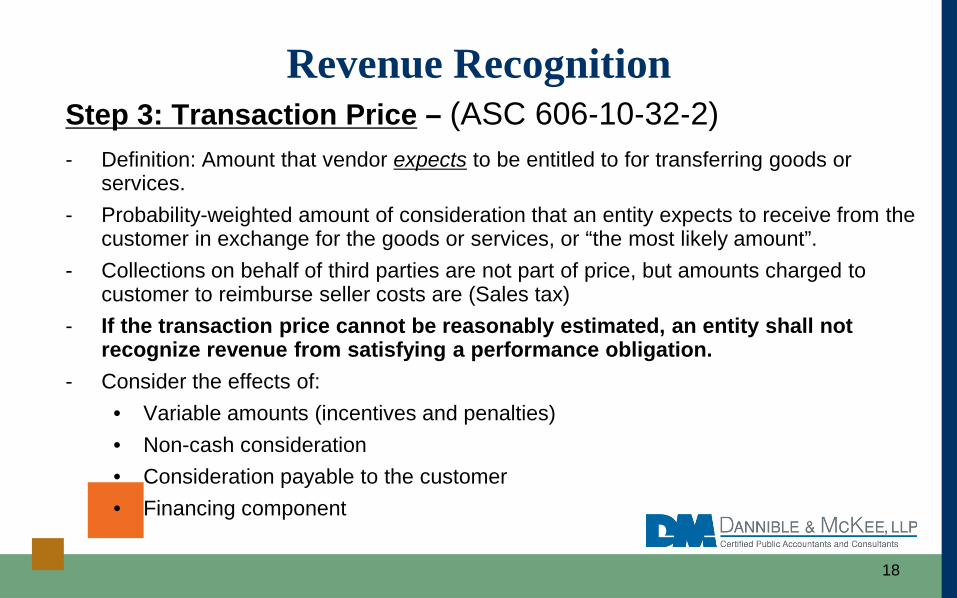

Step 3: Transaction Price – (ASC 606‐10‐32‐2)- Definition: Amount that vendor expects to be entitled to for transferring goods or

services. - Probability-weighted amount of consideration that an entity expects to receive from the

customer in exchange for the goods or services, or “the most likely amount”. - Collections on behalf of third parties are not part of price, but amounts charged to

customer to reimburse seller costs are (Sales tax)- If the transaction price cannot be reasonably estimated, an entity shall not

recognize revenue from satisfying a performance obligation. - Consider the effects of:

• Variable amounts (incentives and penalties)• Non-cash consideration • Consideration payable to the customer • Financing component

Revenue Recognition

18

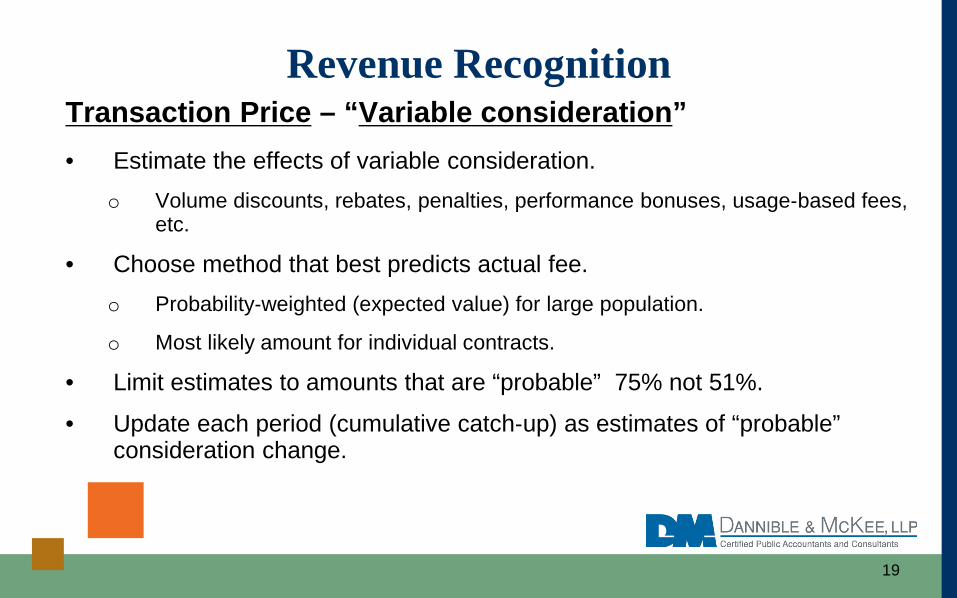

Transaction Price – “Variable consideration”• Estimate the effects of variable consideration.

o Volume discounts, rebates, penalties, performance bonuses, usage‐based fees, etc.

• Choose method that best predicts actual fee.o Probability‐weighted (expected value) for large population.

o Most likely amount for individual contracts.

• Limit estimates to amounts that are “probable” 75% not 51%.

• Update each period (cumulative catch‐up) as estimates of “probable” consideration change.

Revenue Recognition

19

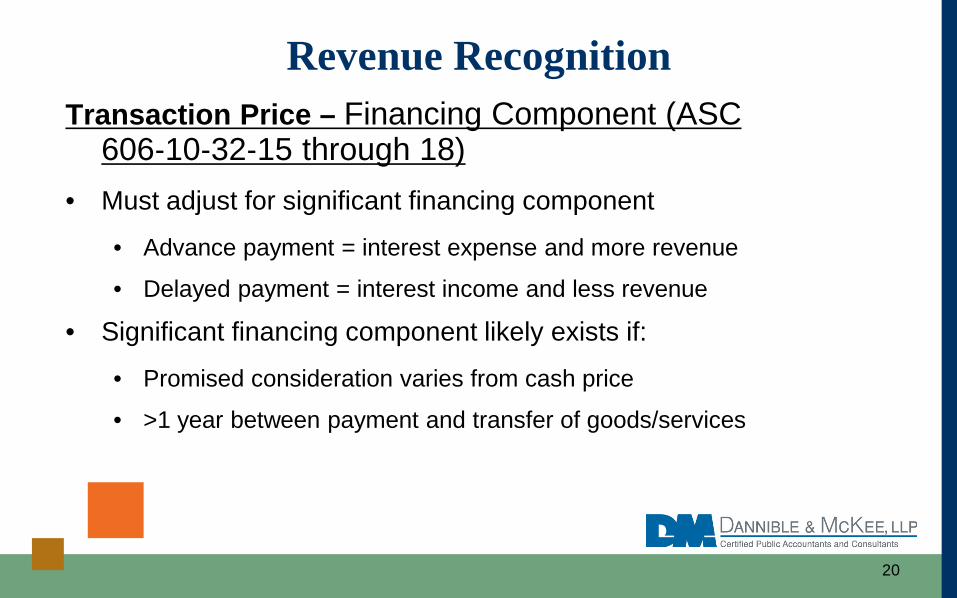

Transaction Price – Financing Component (ASC 606‐10‐32‐15 through 18)

• Must adjust for significant financing component

• Advance payment = interest expense and more revenue

• Delayed payment = interest income and less revenue

• Significant financing component likely exists if:

• Promised consideration varies from cash price

• >1 year between payment and transfer of goods/services

Revenue Recognition

20

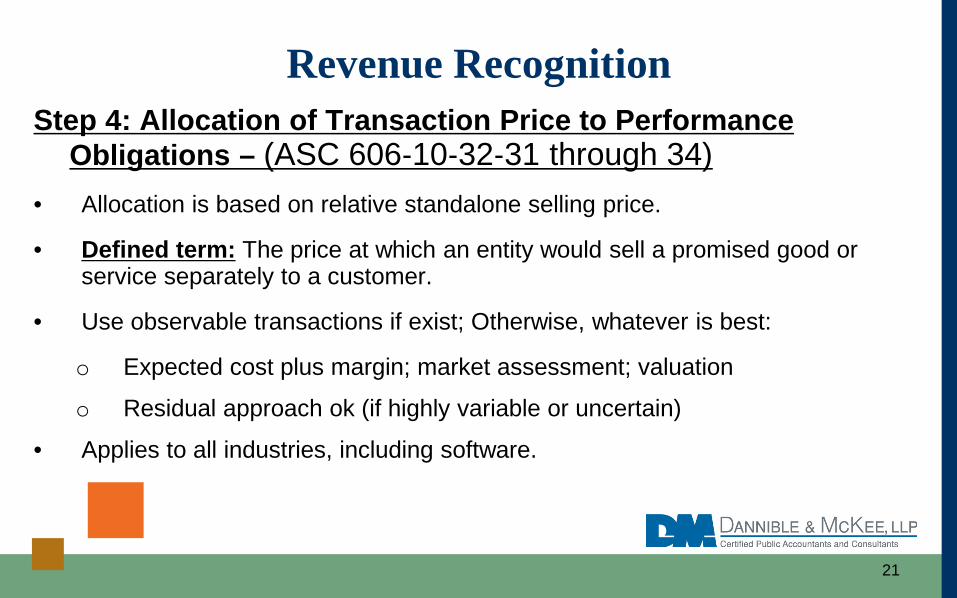

Step 4: Allocation of Transaction Price to Performance Obligations – (ASC 606‐10‐32‐31 through 34)

• Allocation is based on relative standalone selling price.

• Defined term: The price at which an entity would sell a promised good or service separately to a customer.

• Use observable transactions if exist; Otherwise, whatever is best:

o Expected cost plus margin; market assessment; valuation

o Residual approach ok (if highly variable or uncertain)

• Applies to all industries, including software.

Revenue Recognition

21

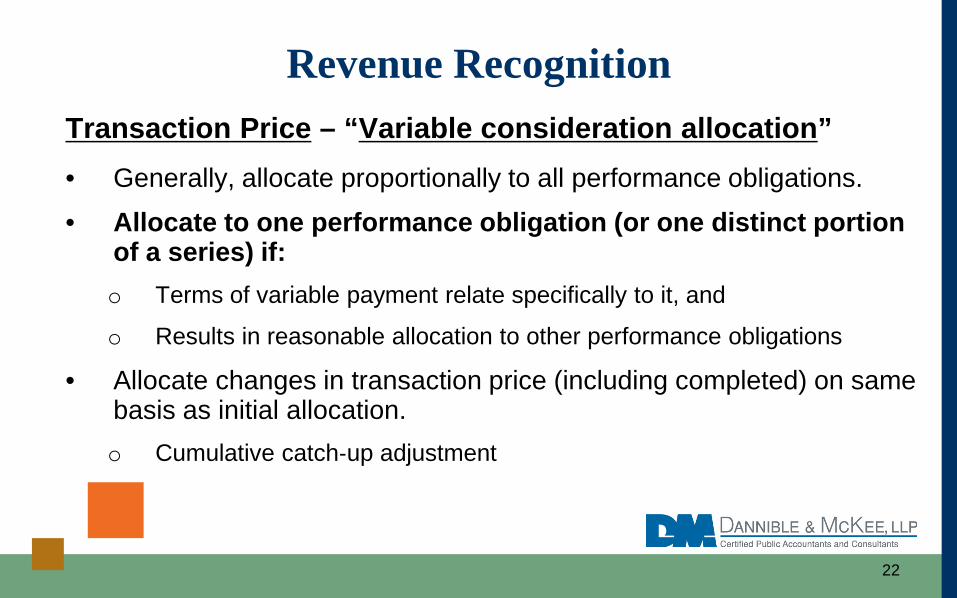

Transaction Price – “Variable consideration allocation”• Generally, allocate proportionally to all performance obligations.

• Allocate to one performance obligation (or one distinct portion of a series) if:o Terms of variable payment relate specifically to it, and

o Results in reasonable allocation to other performance obligations

• Allocate changes in transaction price (including completed) on same basis as initial allocation.o Cumulative catch‐up adjustment

Revenue Recognition

22

Allocation of Transaction Price – “Discounts”• Discount usually allocated proportionally to all performance obligations.

• If objective evidence from observable transactions support allocation to less than all obligations, then allocate to just those PO’s.

Revenue Recognition

23

Step 5: Recognize Revenue as Performance Obligations areSatisfied – Based on “Transfer of Control”

• Obligation is satisfied when control over good or service is transferred to customer.

• Control is the ability to direct use of the asset and obtain substantially all benefits from it.

• Control may pass at a point in time or over time.o “Over time” generally earlier recognition for goods and service, as delivery or

completion.

o “Point in time” generally earlier for IP licenses, as it would happen at start of license, rather than over time.

• Focus on control, rather than risks and rewards.

Revenue Recognition

24

Recognize Revenue as Performance Obligations –Transfer of control occurs over time if:(ASC 606‐10‐25‐17)• Customer benefits as performance occurs.

o E.g., replacement provider wouldn’t have to start over.

• Customer controls asset that vendor’s performance is creating or enhancing. (Most construction contracts)

• Work does not create an asset with alternative use to vendor AND vendor has right to payment for work to date if customer cancels.o Contract and practical considerations affect “alternative use”.

o Legal remedies affect “right to payment”.

More tasks will be “over time” than under current GAAP.

Revenue Recognition

25

Recognize Revenue as Performance Obligations –Transfer of control occurs over time Revenue recognized based on a single measure of progress.

• Can’t use multiple measures for multiple payment streams.

o Eliminates the “milestone method” and certain other commonly used methods.

• Input methods (costs, labor hours, time)

o Ignore costs that don’t relate to performance. (upfront costs)

o Adjust “cost” if pattern does not reflect performance.

• Output methods (hourly billings, milestones).

• “Passage of time” Ok if performance is even.

• If progress cannot be measured, no revenue.

Revenue Recognition

26

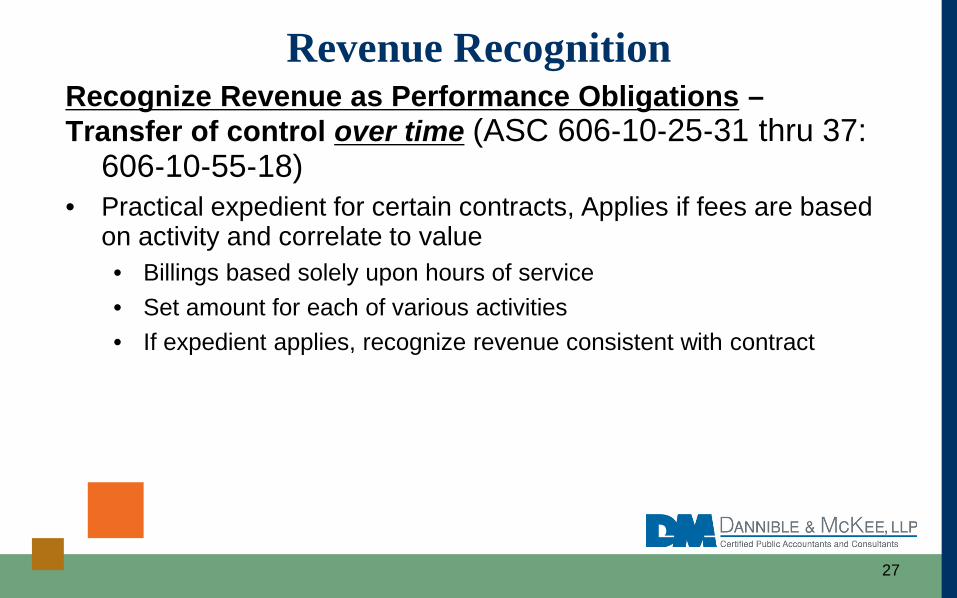

Recognize Revenue as Performance Obligations –Transfer of control over time (ASC 606‐10‐25‐31 thru 37:

606‐10‐55‐18)• Practical expedient for certain contracts, Applies if fees are based

on activity and correlate to value• Billings based solely upon hours of service• Set amount for each of various activities• If expedient applies, recognize revenue consistent with contract

Revenue Recognition

27

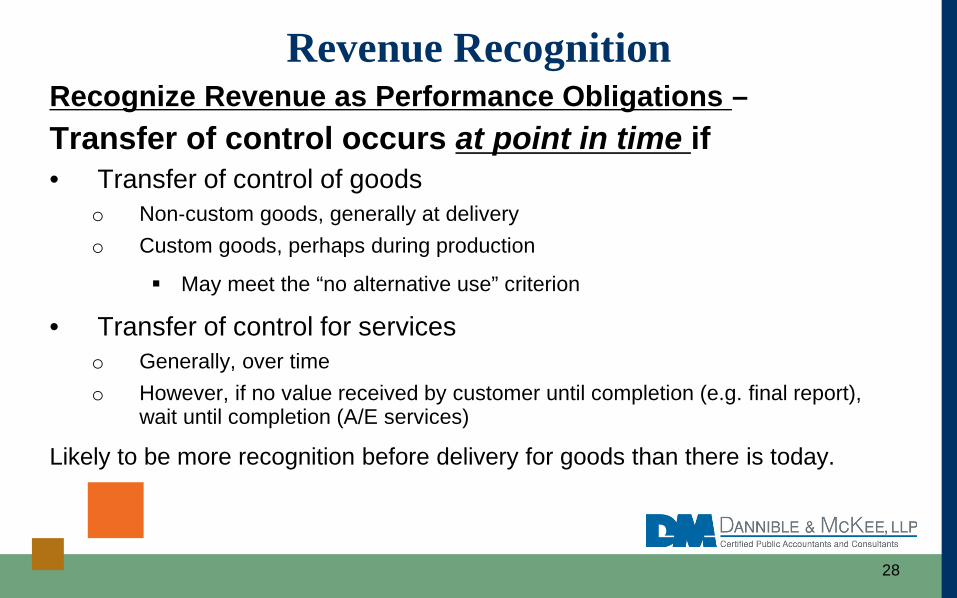

Recognize Revenue as Performance Obligations –Transfer of control occurs at point in time if• Transfer of control of goods

o Non‐custom goods, generally at deliveryo Custom goods, perhaps during production

May meet the “no alternative use” criterion

• Transfer of control for serviceso Generally, over timeo However, if no value received by customer until completion (e.g. final report),

wait until completion (A/E services)

Likely to be more recognition before delivery for goods than there is today.

Revenue Recognition

28

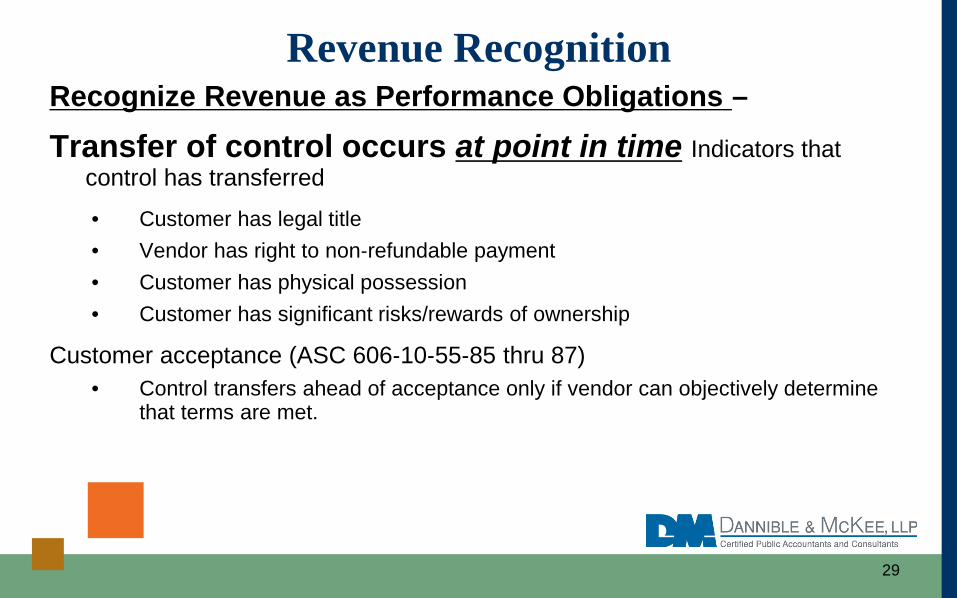

Recognize Revenue as Performance Obligations –

Transfer of control occurs at point in time Indicators that control has transferred

• Customer has legal title• Vendor has right to non‐refundable payment• Customer has physical possession• Customer has significant risks/rewards of ownership

Customer acceptance (ASC 606‐10‐55‐85 thru 87)• Control transfers ahead of acceptance only if vendor can objectively determine

that terms are met.

Revenue Recognition

29

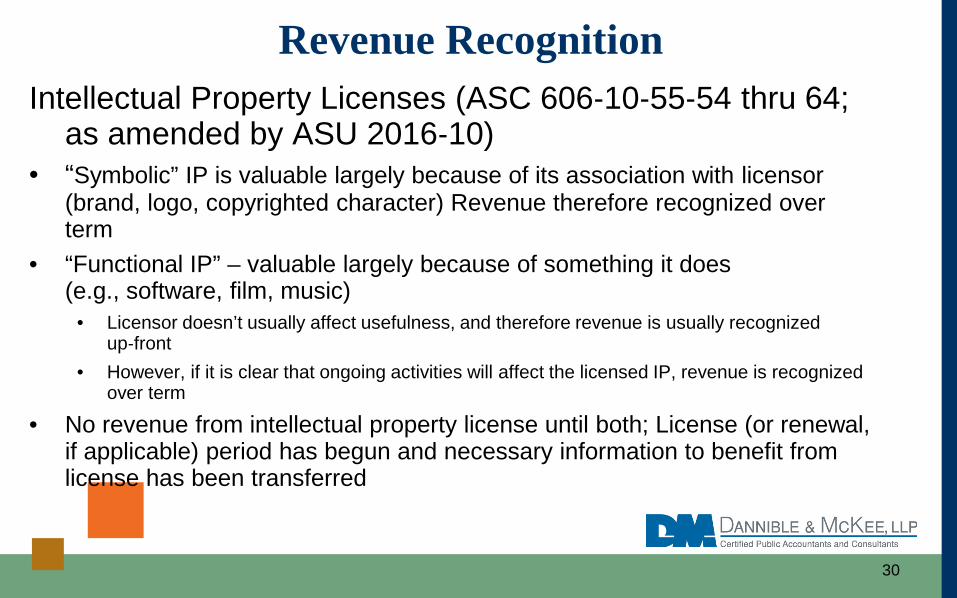

Intellectual Property Licenses (ASC 606‐10‐55‐54 thru 64; as amended by ASU 2016‐10)

• “Symbolic” IP is valuable largely because of its association with licensor (brand, logo, copyrighted character) Revenue therefore recognized over term

• “Functional IP” – valuable largely because of something it does (e.g., software, film, music)

• Licensor doesn’t usually affect usefulness, and therefore revenue is usually recognized up‐front

• However, if it is clear that ongoing activities will affect the licensed IP, revenue is recognized over term

• No revenue from intellectual property license until both; License (or renewal, if applicable) period has begun and necessary information to benefit from license has been transferred

Revenue Recognition

30

Warranties (ASC 606‐10‐55‐30 through 35)• If sold separately, treat as separate performance obligation.• Evaluate standard warranties for element that goes beyond

assurance that product works as promised.o E.g, free maintenance or coverage for accidental damage.o If no service or insurance element, just accrue costs.o Any service or insurance element is treated as separate performance

obligation, with revenue recognized over term.

• Generally same as current GAAP except for possible “insurance” element.o Accrue costs as a liability, no revenue impact.

o Warranty disclosure and roll forward of liability.

Revenue Recognition

31

Cost guidance (ASC 340‐40)• No new onerous (“loss”) contract requirements.

o Retain existing guidance in ASC 605‐35 (SOP 81‐1)o Accrue losses when identified

• Incremental costs of obtaining contract are an asset.o Ok to expense costs as incurred if amortization period would be one year or

less.

• Direct costs to fulfill a contract are an asset if they enhance resources to satisfy performance obligations in the future.

• Cost guidance is all new – should increase consistency.

Revenue Recognition

32

Rights of return (ASC 606‐10‐55‐22 through 29)

• Treat right of return like variable consideration.

• Record revenue for amounts that are probable of not being returned.

• Record refund liability (and asset for goods to be returned) for amounts that are not probable of not being returned.

Similar to current GAAP, but with more flexibility to recognize at least a minimum amount of revenue.

Revenue Recognition

33

Breakage (ASC 606‐10‐55‐46 through 49)

• Customers may not exercise all rights.o E.g., gift cards that are not fully redeemed

• If breakage is probable, take into account when evaluating performance obligations.o E.g., if, on average, customer entitled to 6 services only uses 5, recognize 1/5

of the revenue each time card is used

• If an estimate cannot be made, recognize breakage when likelihood of use is remote.

• Similar to today’s practice, which has developed without authoritative guidance.

Revenue Recognition

34

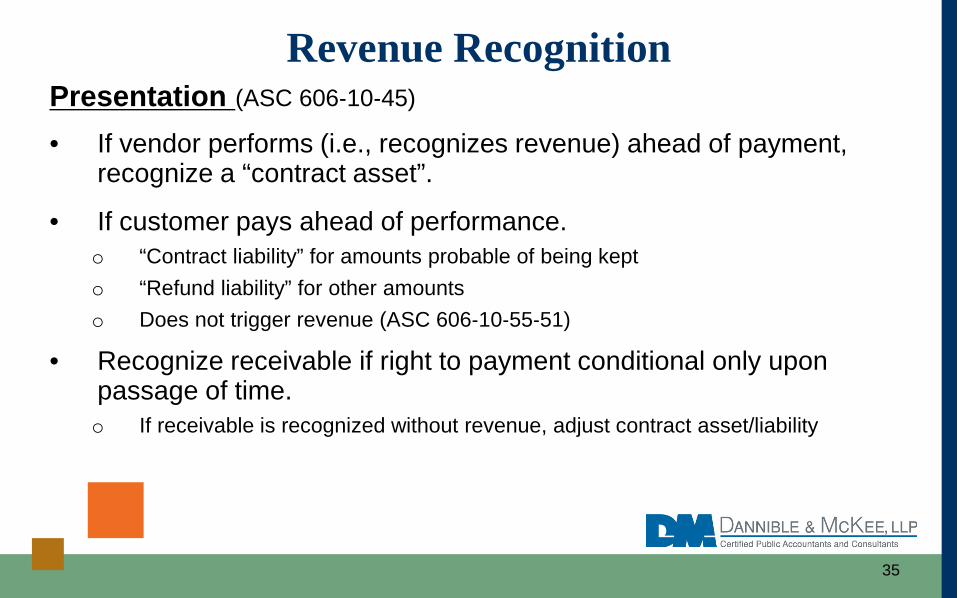

Presentation (ASC 606‐10‐45)

• If vendor performs (i.e., recognizes revenue) ahead of payment, recognize a “contract asset”.

• If customer pays ahead of performance.o “Contract liability” for amounts probable of being kepto “Refund liability” for other amountso Does not trigger revenue (ASC 606‐10‐55‐51)

• Recognize receivable if right to payment conditional only upon passage of time.o If receivable is recognized without revenue, adjust contract asset/liability

Revenue Recognition

35

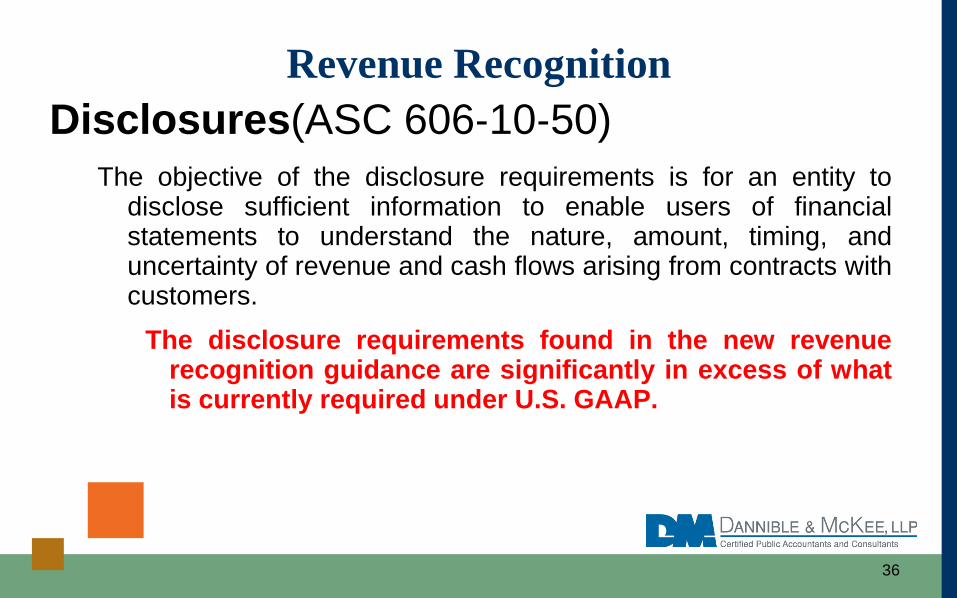

Disclosures(ASC 606‐10‐50)The objective of the disclosure requirements is for an entity to

disclose sufficient information to enable users of financialstatements to understand the nature, amount, timing, anduncertainty of revenue and cash flows arising from contracts withcustomers.

The disclosure requirements found in the new revenuerecognition guidance are significantly in excess of whatis currently required under U.S. GAAP.

Revenue Recognition

36

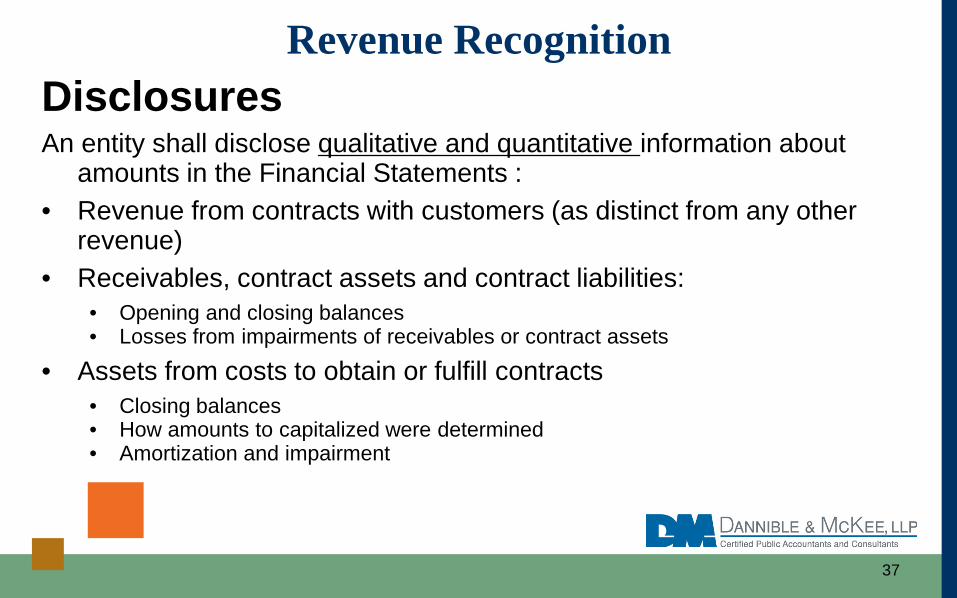

DisclosuresAn entity shall disclose qualitative and quantitative information about

amounts in the Financial Statements :• Revenue from contracts with customers (as distinct from any other

revenue) • Receivables, contract assets and contract liabilities:

• Opening and closing balances• Losses from impairments of receivables or contract assets

• Assets from costs to obtain or fulfill contracts• Closing balances• How amounts to capitalized were determined• Amortization and impairment

Revenue Recognition

37

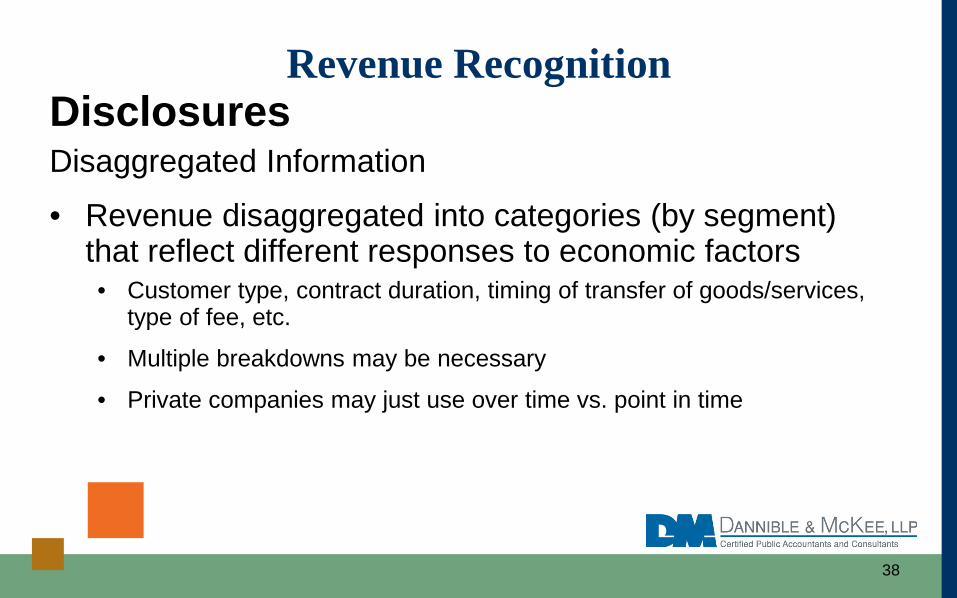

DisclosuresDisaggregated Information

• Revenue disaggregated into categories (by segment) that reflect different responses to economic factors• Customer type, contract duration, timing of transfer of goods/services,

type of fee, etc.

• Multiple breakdowns may be necessary

• Private companies may just use over time vs. point in time

Revenue Recognition

38

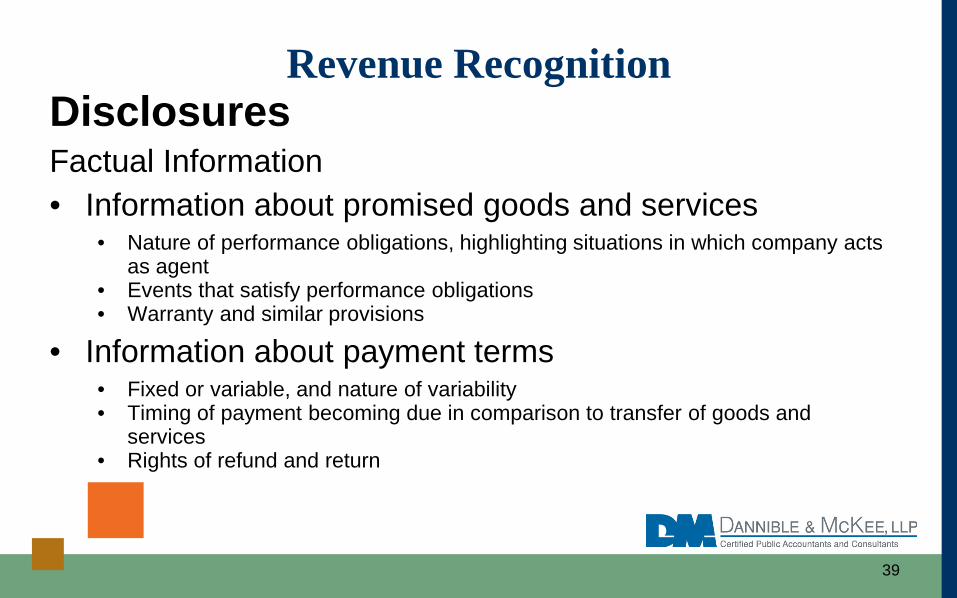

DisclosuresFactual Information• Information about promised goods and services

• Nature of performance obligations, highlighting situations in which company acts as agent

• Events that satisfy performance obligations• Warranty and similar provisions

• Information about payment terms• Fixed or variable, and nature of variability• Timing of payment becoming due in comparison to transfer of goods and

services• Rights of refund and return

Revenue Recognition

39

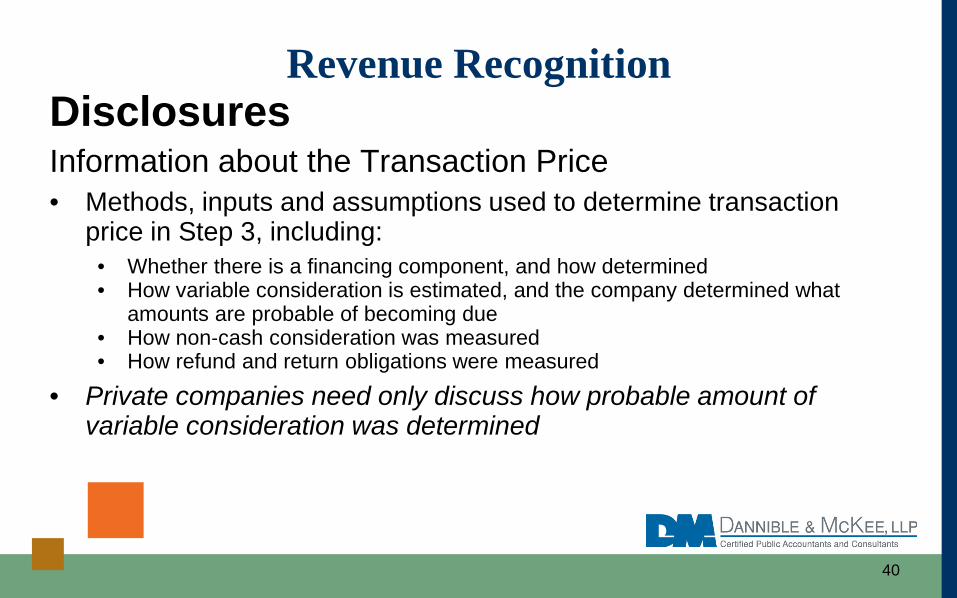

DisclosuresInformation about the Transaction Price• Methods, inputs and assumptions used to determine transaction

price in Step 3, including:• Whether there is a financing component, and how determined• How variable consideration is estimated, and the company determined what

amounts are probable of becoming due• How non‐cash consideration was measured• How refund and return obligations were measured

• Private companies need only discuss how probable amount of variable consideration was determined

Revenue Recognition

40

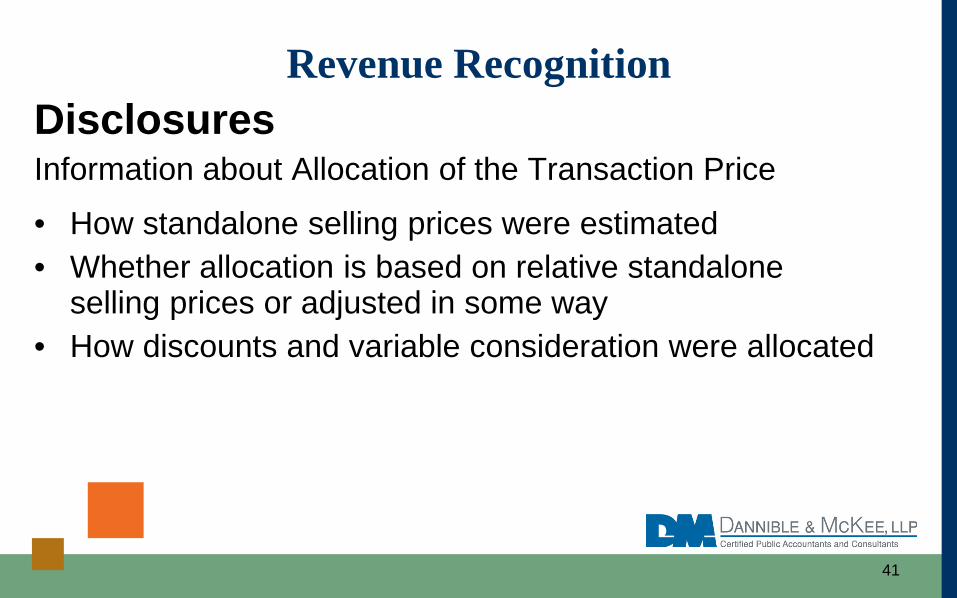

DisclosuresInformation about Allocation of the Transaction Price

• How standalone selling prices were estimated• Whether allocation is based on relative standalone

selling prices or adjusted in some way• How discounts and variable consideration were allocated

Revenue Recognition

41

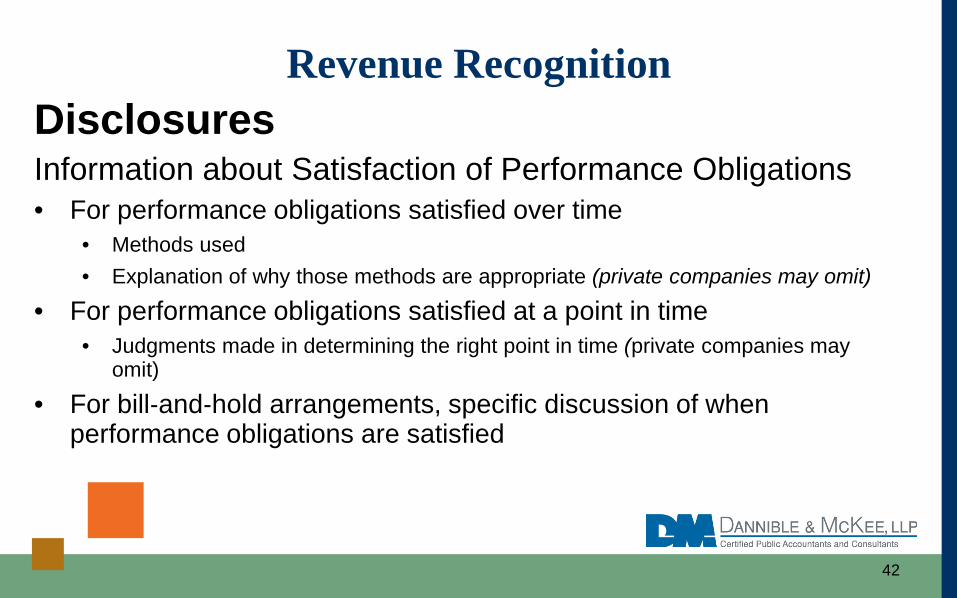

DisclosuresInformation about Satisfaction of Performance Obligations• For performance obligations satisfied over time

• Methods used• Explanation of why those methods are appropriate (private companies may omit)

• For performance obligations satisfied at a point in time• Judgments made in determining the right point in time (private companies may

omit)

• For bill‐and‐hold arrangements, specific discussion of when performance obligations are satisfied

Revenue Recognition

42

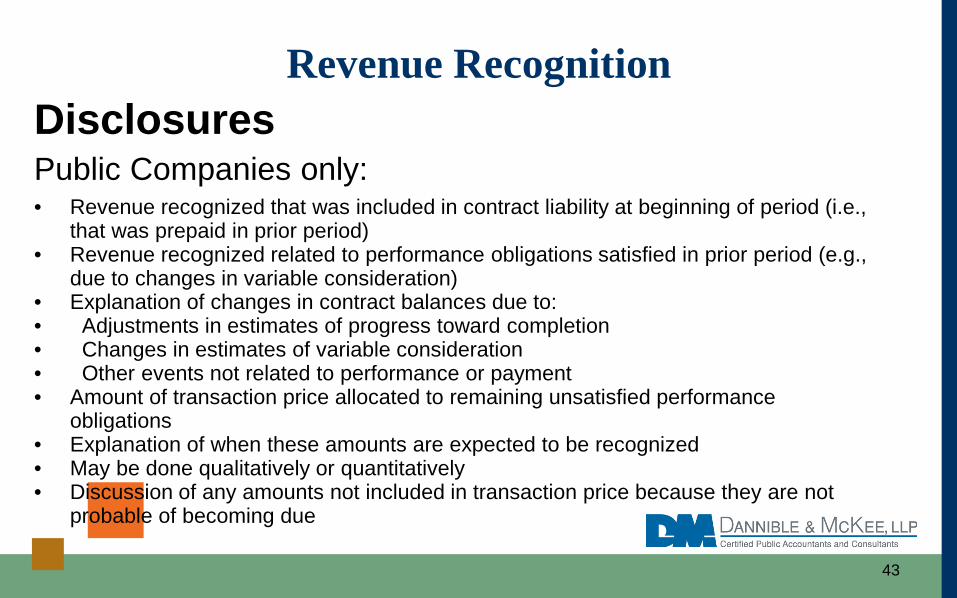

DisclosuresPublic Companies only:• Revenue recognized that was included in contract liability at beginning of period (i.e.,

that was prepaid in prior period)• Revenue recognized related to performance obligations satisfied in prior period (e.g.,

due to changes in variable consideration)• Explanation of changes in contract balances due to:• Adjustments in estimates of progress toward completion• Changes in estimates of variable consideration• Other events not related to performance or payment• Amount of transaction price allocated to remaining unsatisfied performance

obligations• Explanation of when these amounts are expected to be recognized• May be done qualitatively or quantitatively• Discussion of any amounts not included in transaction price because they are not

probable of becoming due

Revenue Recognition

43

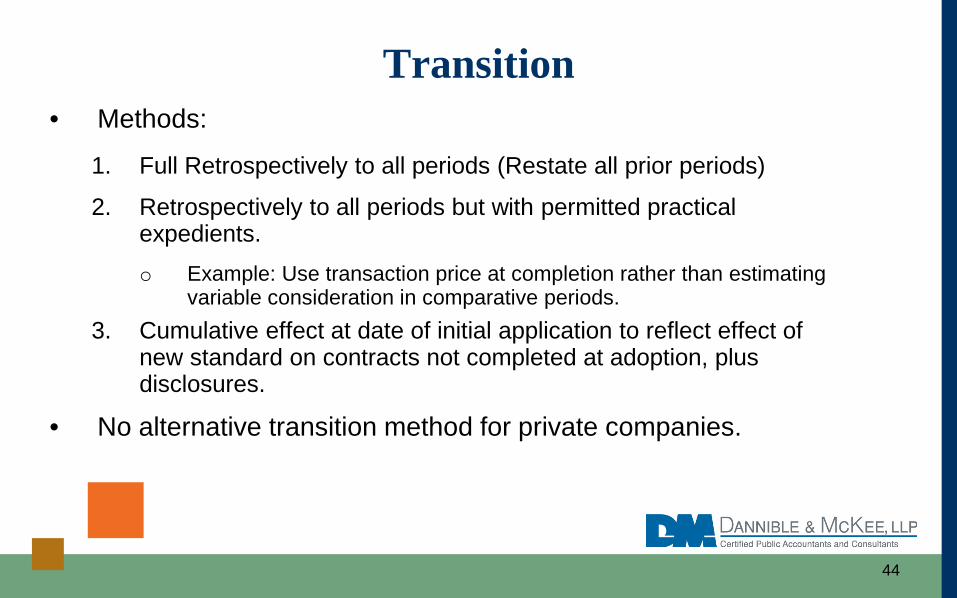

• Methods:

1. Full Retrospectively to all periods (Restate all prior periods)

2. Retrospectively to all periods but with permitted practical expedients.o Example: Use transaction price at completion rather than estimating

variable consideration in comparative periods.3. Cumulative effect at date of initial application to reflect effect of

new standard on contracts not completed at adoption, plus disclosures.

• No alternative transition method for private companies.

Transition

44

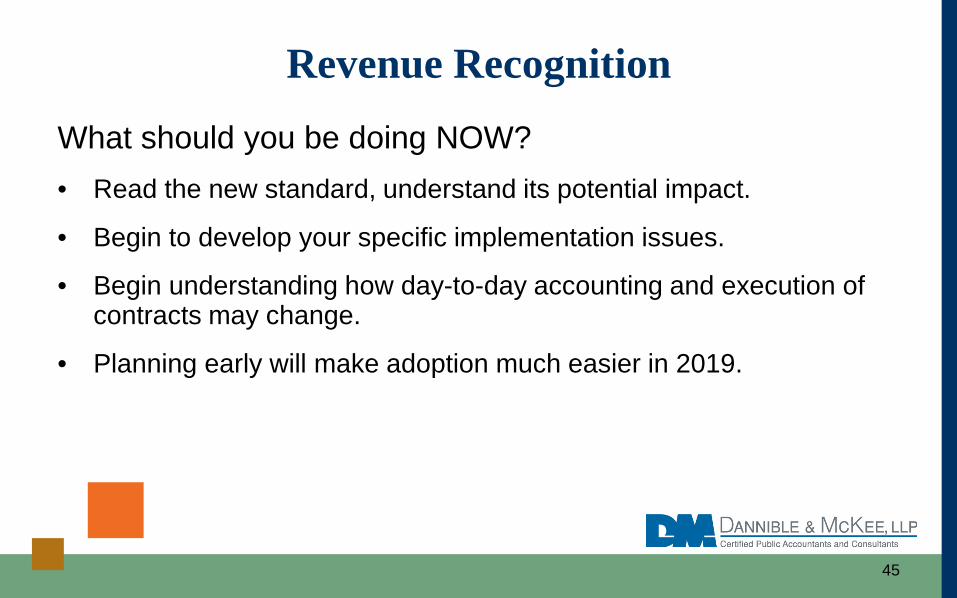

What should you be doing NOW?• Read the new standard, understand its potential impact.

• Begin to develop your specific implementation issues.

• Begin understanding how day-to-day accounting and execution of contracts may change.

• Planning early will make adoption much easier in 2019.

Revenue Recognition

45

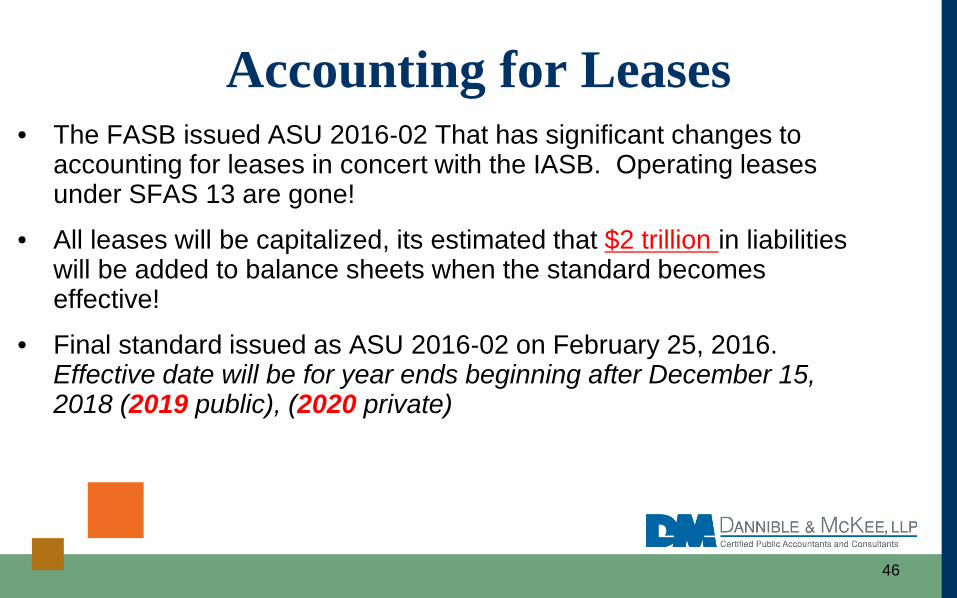

• The FASB issued ASU 2016‐02 That has significant changes to accounting for leases in concert with the IASB. Operating leases under SFAS 13 are gone!

• All leases will be capitalized, its estimated that $2 trillion in liabilities will be added to balance sheets when the standard becomes effective!

• Final standard issued as ASU 2016‐02 on February 25, 2016. Effective date will be for year ends beginning after December 15, 2018 (2019 public), (2020 private)

Accounting for Leases

46

Definition – “A contract in which the right to use a specified asset (the underlying asset) is conveyed for a period of time in exchange for consideration”.

• A physically distinct portion of a larger asset of which a customer has exclusive use is a specified asset. ( A building)

• A capacity portion of a larger asset that is not physically distinct (e.g., a capacity portion of a pipeline) is not a specified asset.

• Excludes all intangible assets.

• Excludes leases with a maximum possible term of 12 months or less, expense on straight line basis.

Accounting for Leases

47

• Lessees will recognize a “right-of-use” asset and a liability for their obligation to make lease payments for all leases. Measured using the present value of the lease payments using a discount rate.

• Lessors will “partially derecognize” a portion, or all, of the asset leased, theoretically the opposite accounting of lessees.

• Under an expected-outcome approach, contingent rentals and residual value guarantees as part of the lease liability. The lessee bases its inclusion of rentals for renewal periods in the lease liability on the longest possible term that is more likely than not to occur.

Accounting for Leases

48

Measure at present value ( PV) of lease payments• Based on both lease term and rentals

• Discount at lessee’s incremental borrowing rate or rate lessor charges, if known

• Include recoverable initial direct costs in the “Right of Use” asset

Accounting for Leases

49

Two elements form basis for PV of lease payments:1) Lease Term• Estimated as the non‐cancellable period of the lease• Include periods under option to extend IF lessee has

significant economic incentive to exercise option• Include periods under option to terminate IF lessee has

significant economic incentive NOT to exercise option

Accounting for Leases

50

Two elements form basis for PV of lease payments:2) Rentals• Fixed lease payments (less incentives to be paid by lessor)• Contingent rentals tied to an index• Contingent rentals which are in substance fixed payments• Residual value guarantees• Exercise price of purchase option IF lessee has significant economic

incentive to exercise option• Termination penalties IF lease term reflects lessee exercising option

Accounting for Leases

51

- Lease classification• Two approaches, based on the “lease classification test”.• Approach A – Financing Type (Capitalized lease)

- Subsequently measure the liability using the effective interest method.

• Amortize(depreciate) “right-of-use” asset on a systematic basis that reflects pattern of consumption over the term of the lease.

• Recognize interest and amortization expense separately in operations.

Lessees

52

- Approach A - Capitalized, continued

• Applies to asset leases other than property unless:

- Lease term is an insignificant portion of the asset economic life; or

- Present value of the fixed lease payments is insignificant relative to fair value of asset.

• Applies to property leases if:

- Lease term is for the major part of the economic life; or

- Present value of fixed lease payments accounts for substantially all of the fair value.

Lessees

53

Approach A - Capitalized, continued

Separately reflected in P&L:• Accretion of lease liability as interest• Amortization of Right of Use asset• Variable lease payments incurred after commencementAmortize on straight line basis• Shorter of the estimated lease term or underlying asset’s useful life• If significant economic incentive to exercise a purchase option,

amortize asset to end of useful life of underlying asset

Lessees

54

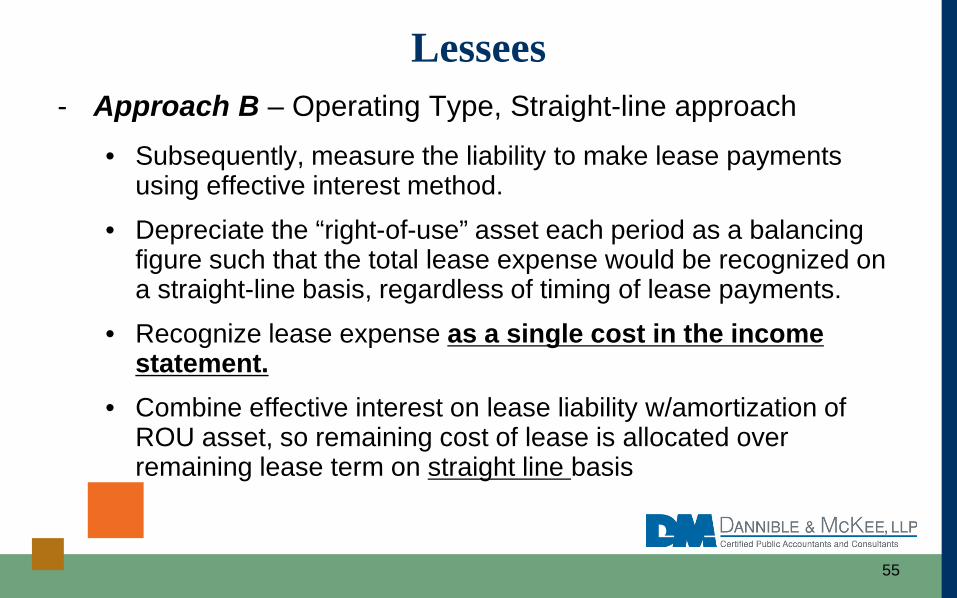

- Approach B – Operating Type, Straight-line approach

• Subsequently, measure the liability to make lease payments using effective interest method.

• Depreciate the “right-of-use” asset each period as a balancing figure such that the total lease expense would be recognized on a straight-line basis, regardless of timing of lease payments.

• Recognize lease expense as a single cost in the income statement.

• Combine effective interest on lease liability w/amortization of ROU asset, so remaining cost of lease is allocated over remaining lease term on straight line basis

Lessees

55

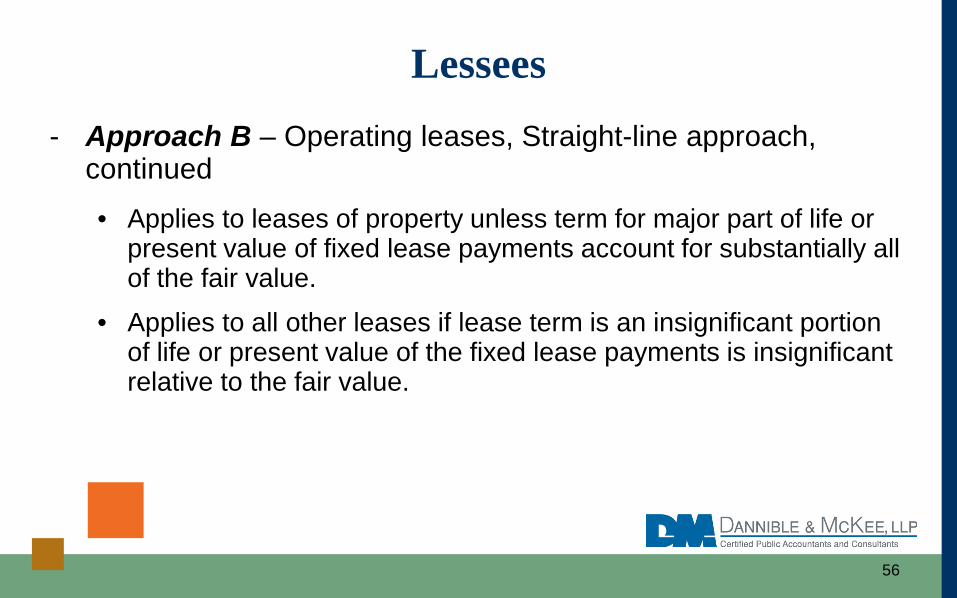

- Approach B – Operating leases, Straight-line approach, continued

• Applies to leases of property unless term for major part of life or present value of fixed lease payments account for substantially all of the fair value.

• Applies to all other leases if lease term is an insignificant portion of life or present value of the fixed lease payments is insignificant relative to the fair value.

Lessees

56

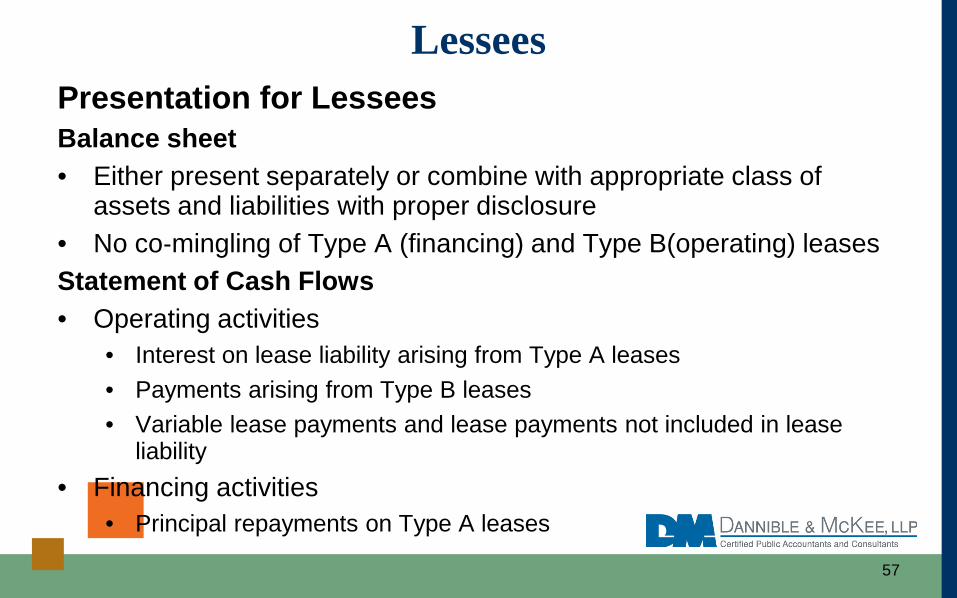

Presentation for LesseesBalance sheet• Either present separately or combine with appropriate class of

assets and liabilities with proper disclosure• No co‐mingling of Type A (financing) and Type B(operating) leasesStatement of Cash Flows• Operating activities

• Interest on lease liability arising from Type A leases• Payments arising from Type B leases• Variable lease payments and lease payments not included in lease

liability• Financing activities

• Principal repayments on Type A leases

Lessees

57

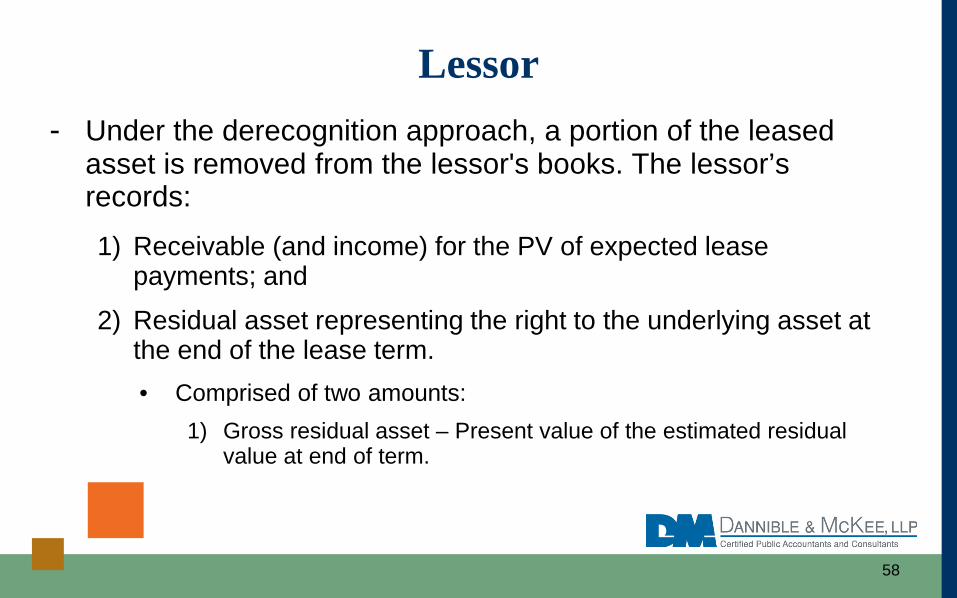

- Under the derecognition approach, a portion of the leased asset is removed from the lessor's books. The lessor’s records:

1) Receivable (and income) for the PV of expected lease payments; and

2) Residual asset representing the right to the underlying asset at the end of the lease term.• Comprised of two amounts:

1) Gross residual asset – Present value of the estimated residual value at end of term.

Lessor

58

• Comprised of two amounts, continued2) Deferred profit – Difference between the gross residual asset and

the allocation of the carrying amount.

• Subsequently accrete the gross residual asset. • Would not recognize deferred profit until residual asset is sold or

re-leased.

• Present gross residual asset and deferred profit together as net residual asset.

Lessor

59

Facts: • Asset Life: 5 yrs • Lease of Asset: 3 yrs • Payments: 3 payments of $125 (total payments $375) at 2.5%

interest rate (discount rate) • Lease Liability: $357 • Underlying Asset for:

- Carrying Value: $950 - Fair Value: $975 ( $25 profit)

• End of lease asset value: $665 • Gross residual value: $618 ( PV = $665) Diff $47

Lessor - Example

60

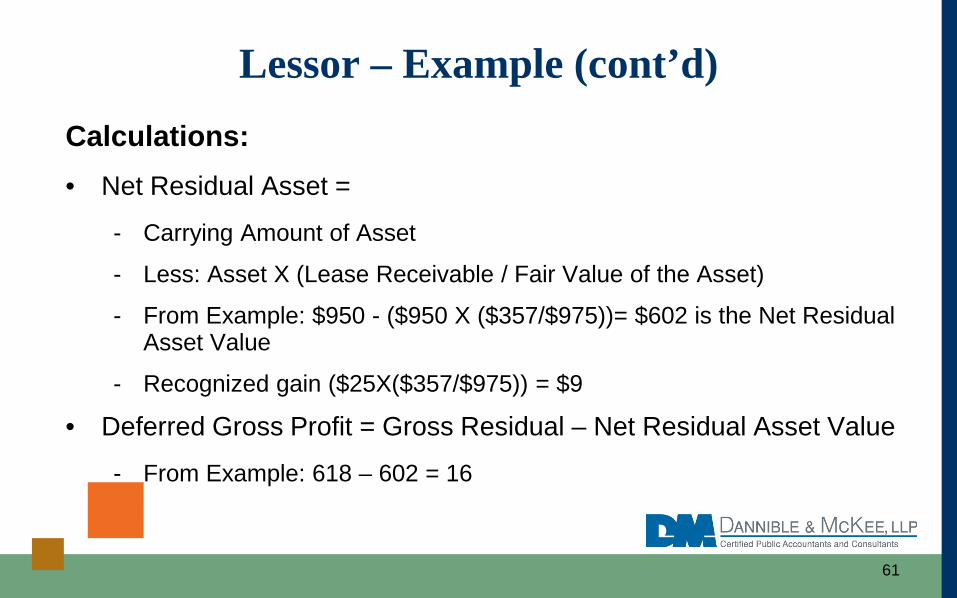

Calculations: • Net Residual Asset =

- Carrying Amount of Asset

- Less: Asset X (Lease Receivable / Fair Value of the Asset)

- From Example: $950 - ($950 X ($357/$975))= $602 is the Net Residual Asset Value

- Recognized gain ($25X($357/$975)) = $9

• Deferred Gross Profit = Gross Residual – Net Residual Asset Value

- From Example: 618 – 602 = 16

Lessor – Example (cont’d)

61

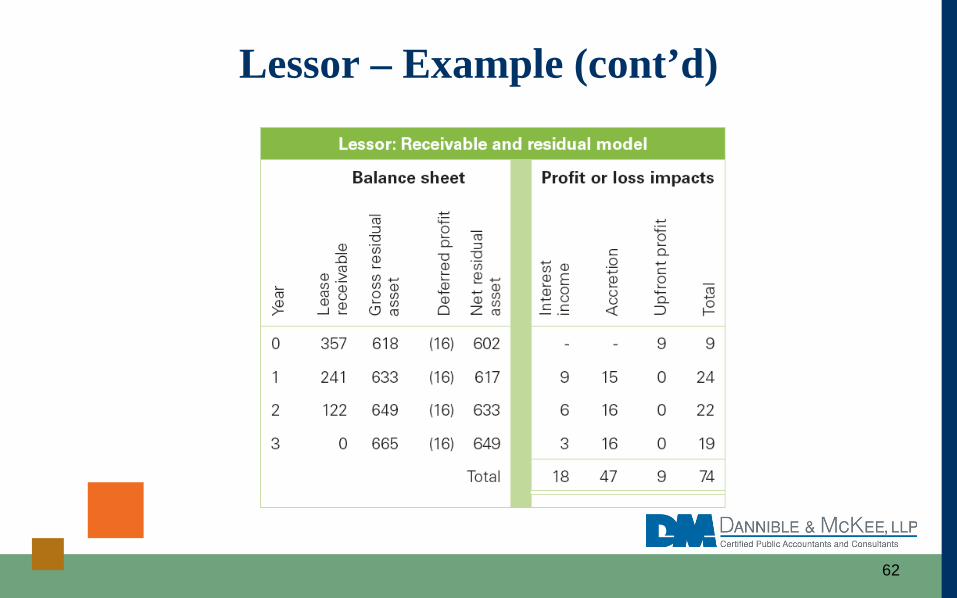

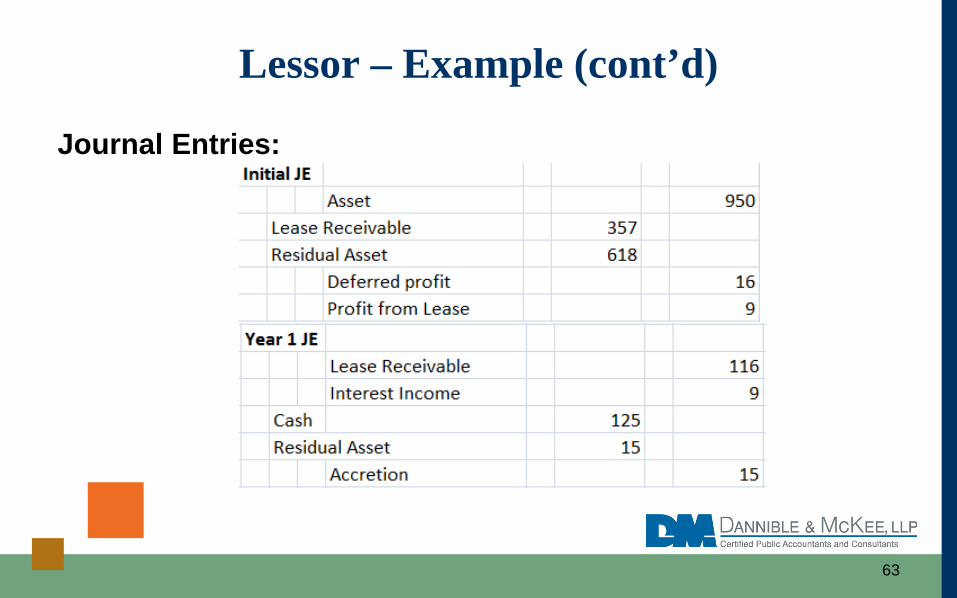

Lessor – Example (cont’d)

62

Journal Entries:

Lessor – Example (cont’d)

63

Journal Entries:

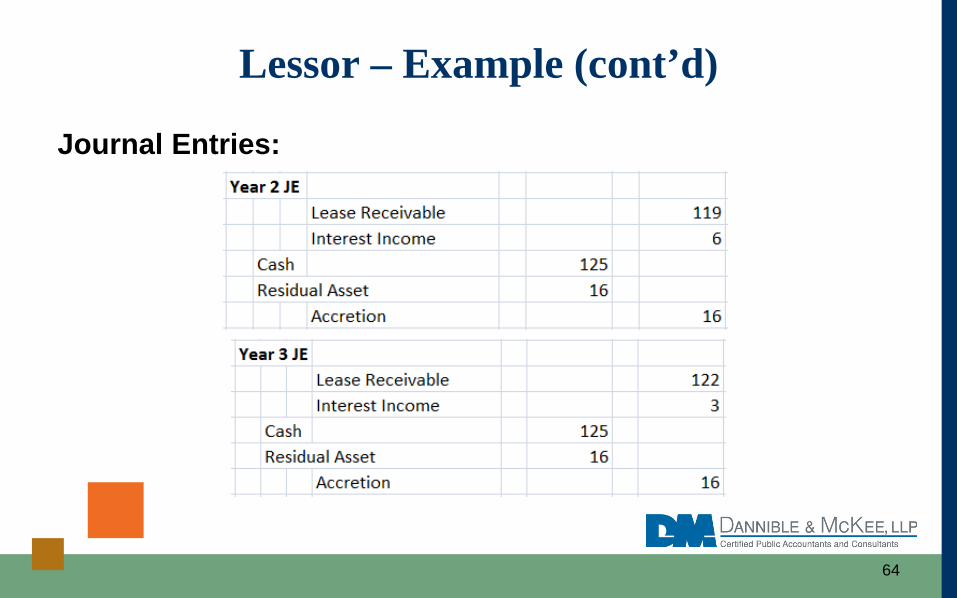

Lessor – Example (cont’d)

64

Journal Entries:

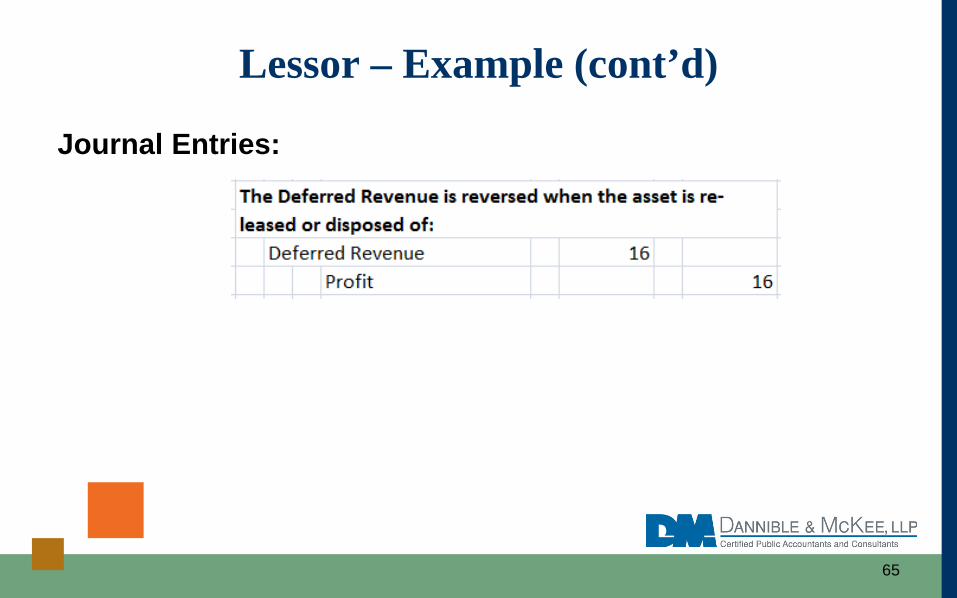

Lessor – Example (cont’d)

65

• Related party transactions will be disclosed in accordance with Topic 850. No specific guidance provided.

• Disclosures• Contractual details (lease term, contingent rentals, options, etc.) and

related accounting judgments• Maturity analyses of undiscounted lease payments• Reconciliations of amounts recognized in the balance sheet• Lessees: roll forwards of lease liabilities by class of underlying asset• Lessors: reconciliations of right to receive lease payments and residual

assets• Narrative disclosures about leases (including information about variable

lease payments and options)

Accounting for Leases

66

Transition to the new method• Applies to all leases existing at “the beginning of the first

comparative period” present upon adoption.

• No grandfathering of existing leases!

• Transition: modified retrospective approach or full retrospective approach(Restate all years presented)

Accounting for Leases

67

What should you being doing now?• Begin with a evaluation of the lease portfolio, starting with the largest

leases, and assess how they will be accounted for. Make certain consideration is given to renewal provisions, if favorable.

• Focus on reducing the spread between a lease’s liability and the corresponding “right of use” asset. The more these two items are out of balance, the more skewed the impact will be on the balance sheet and shareholder equity

• Consider renegotiating leases now, even if they are not up for renewal• Consider impact on loan covenants, talk to the banker now

Accounting for Leases

68

Email: [email protected]

Web: www.dmcpas.com and

Address: Dannible & McKee, LLPFinancial Plaza221 S. Warren St.Syracuse, New York 13202-1628

Phone: (315) 472-9127x123

Kenneth C. GardinerCPA, CCIFP, CDA, Partner

69

Scan to add Ken Gardiner to

your contacts.

Joseph Chemotti, CPA, CCIFP

Dannible & McKee, LLP2016 Tax & Financial Planning Conference

November 10, 2016

FASB, SSARS & ERISA Update

70

• Topics to cover:• FASB Accounting Standards Updates.• Statement on Standards for Accounting and Review

Services (SSARS) Update.• Pension/ERISA Update.

FASB, SSARS & ERISA Update

71

FASB Accounting Standards Updates• 17 FASB Accounting Standards

Updates released so far in 2016 (through October 31, 2016):• See detailed listing on PDF labeled 2016 FASB

Accounting Standards Updates.

FASB Update

72

• Few to discuss today:• ASU 2015-03 - Debt Issuance Costs.• ASU 2015-17 - Deferred Taxes.• ASU 2016-15 - Statement of Cash Flows - Classification

of Certain Cash Receipts and Cash Payments.• ASU 2016-17 - Consolidation with Related Parties under

Common Control.

FASB Update

73

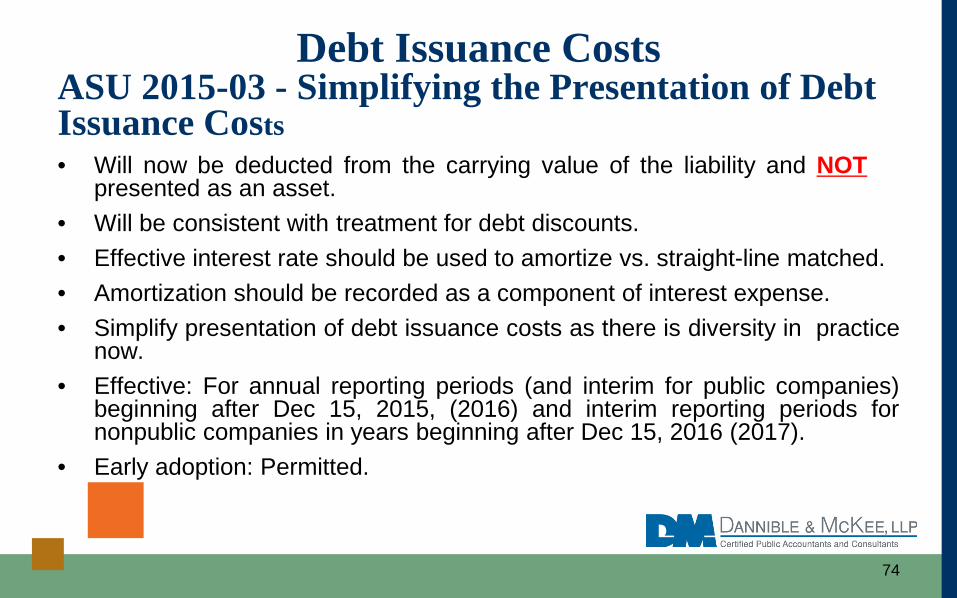

ASU 2015-03 - Simplifying the Presentation of Debt Issuance Costs• Will now be deducted from the carrying value of the liability and NOT

presented as an asset.• Will be consistent with treatment for debt discounts.• Effective interest rate should be used to amortize vs. straight-line matched.• Amortization should be recorded as a component of interest expense.• Simplify presentation of debt issuance costs as there is diversity in practice

now.• Effective: For annual reporting periods (and interim for public companies)

beginning after Dec 15, 2015, (2016) and interim reporting periods fornonpublic companies in years beginning after Dec 15, 2016 (2017).

• Early adoption: Permitted.

Debt Issuance Costs

74

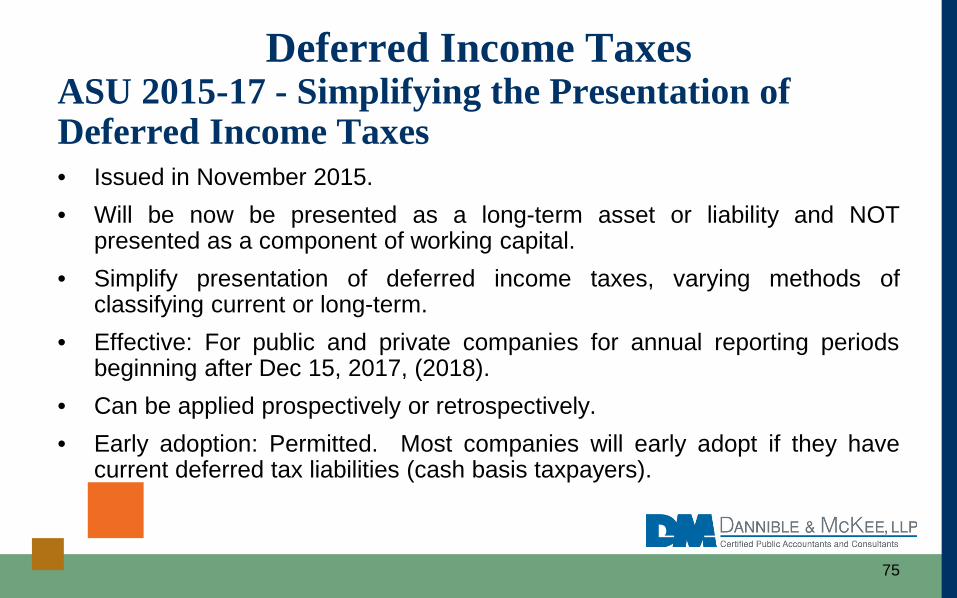

ASU 2015-17 - Simplifying the Presentation of Deferred Income Taxes• Issued in November 2015.• Will be now be presented as a long-term asset or liability and NOT

presented as a component of working capital.• Simplify presentation of deferred income taxes, varying methods of

classifying current or long-term.• Effective: For public and private companies for annual reporting periods

beginning after Dec 15, 2017, (2018).• Can be applied prospectively or retrospectively.• Early adoption: Permitted. Most companies will early adopt if they have

current deferred tax liabilities (cash basis taxpayers).

Deferred Income Taxes

75

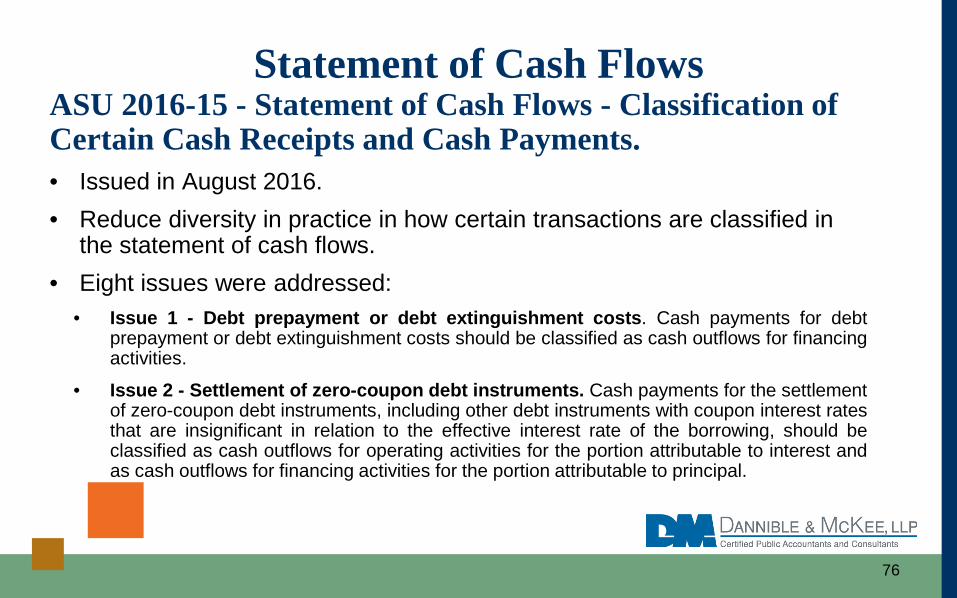

ASU 2016-15 - Statement of Cash Flows - Classification of Certain Cash Receipts and Cash Payments.• Issued in August 2016.• Reduce diversity in practice in how certain transactions are classified in

the statement of cash flows.• Eight issues were addressed:

• Issue 1 - Debt prepayment or debt extinguishment costs. Cash payments for debtprepayment or debt extinguishment costs should be classified as cash outflows for financingactivities.

• Issue 2 - Settlement of zero-coupon debt instruments. Cash payments for the settlementof zero-coupon debt instruments, including other debt instruments with coupon interest ratesthat are insignificant in relation to the effective interest rate of the borrowing, should beclassified as cash outflows for operating activities for the portion attributable to interest andas cash outflows for financing activities for the portion attributable to principal.

Statement of Cash Flows

76

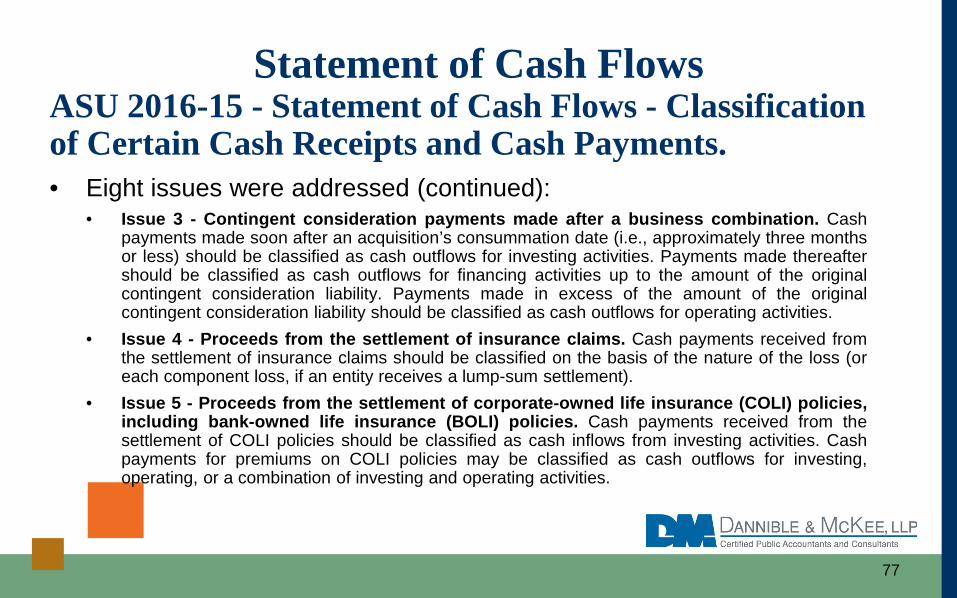

ASU 2016-15 - Statement of Cash Flows - Classification of Certain Cash Receipts and Cash Payments.• Eight issues were addressed (continued):

• Issue 3 - Contingent consideration payments made after a business combination. Cashpayments made soon after an acquisition’s consummation date (i.e., approximately three monthsor less) should be classified as cash outflows for investing activities. Payments made thereaftershould be classified as cash outflows for financing activities up to the amount of the originalcontingent consideration liability. Payments made in excess of the amount of the originalcontingent consideration liability should be classified as cash outflows for operating activities.

• Issue 4 - Proceeds from the settlement of insurance claims. Cash payments received fromthe settlement of insurance claims should be classified on the basis of the nature of the loss (oreach component loss, if an entity receives a lump-sum settlement).

• Issue 5 - Proceeds from the settlement of corporate-owned life insurance (COLI) policies,including bank-owned life insurance (BOLI) policies. Cash payments received from thesettlement of COLI policies should be classified as cash inflows from investing activities. Cashpayments for premiums on COLI policies may be classified as cash outflows for investing,operating, or a combination of investing and operating activities.

Statement of Cash Flows

77

ASU 2016-15 - Statement of Cash Flows - Classification of Certain Cash Receipts and Cash Payments.• Eight issues were addressed (continued):

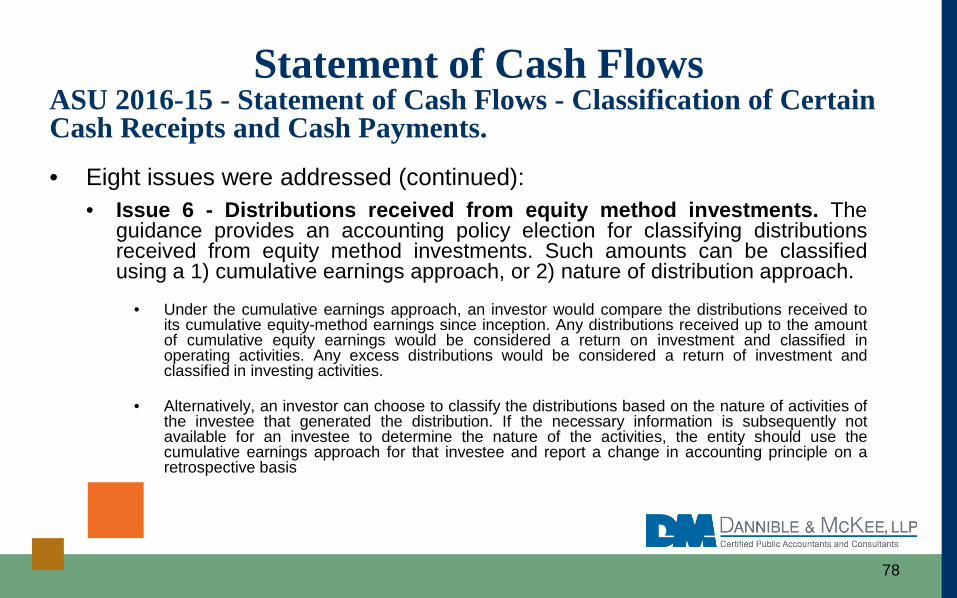

• Issue 6 - Distributions received from equity method investments. Theguidance provides an accounting policy election for classifying distributionsreceived from equity method investments. Such amounts can be classifiedusing a 1) cumulative earnings approach, or 2) nature of distribution approach.

• Under the cumulative earnings approach, an investor would compare the distributions received toits cumulative equity-method earnings since inception. Any distributions received up to the amountof cumulative equity earnings would be considered a return on investment and classified inoperating activities. Any excess distributions would be considered a return of investment andclassified in investing activities.

• Alternatively, an investor can choose to classify the distributions based on the nature of activities ofthe investee that generated the distribution. If the necessary information is subsequently notavailable for an investee to determine the nature of the activities, the entity should use thecumulative earnings approach for that investee and report a change in accounting principle on aretrospective basis

Statement of Cash Flows

78

ASU 2016-15 - Statement of Cash Flows - Classification of Certain Cash Receipts and Cash Payments.• Eight issues were addressed (continued):

• Issue 7 - Beneficial interests in securitization transactions. A transferor’s beneficialinterest obtained in a securitization of financial assets should be disclosed as a noncashactivity. Cash receipts from a transferor’s beneficial interests in securitized trade receivablesshould be classified as cash inflows from investing activities.

• Issue 8 - Separately identifiable cash flows and application of the predominanceprinciple. Entities should use reasonable judgement to separate cash flows. In the absenceof specific guidance, an entity should classify each separately identifiable cash source anduse on the basis of the nature of the underlying cash flows. For cash flows with aspects ofmore than one class that cannot be separated, the classification should be based on theactivity that is likely to be the predominate source or use of cash flow.

Statement of Cash Flows

79

ASU 2016-15 - Statement of Cash Flows - Classification of Certain Cash Receipts and Cash Payments.• Effective:

• For public business entities, the standard is effective for financial statementsissued for fiscal years beginning after December 15, 2017 (2018), and interimperiods within those fiscal years.

• For all other entities, the standard is effective for financial statements issued forfiscal years beginning after December 15, 2018 (2019), and interim periodswithin fiscal years beginning after December 15, 2019.

• Early adoption: Permitted, provided that all of the amendments are adopted inthe same period.

Statement of Cash Flows

80

• Two (2) new SSARS released so far in 2016 (through October 31st):• SSARS 22 - Compilation of Pro Forma Financial

Information.• SSARS 23 - Omnibus Statement on Standard for

Accounting and Review Services - 2016.

Statement on Standards for Accounting and Review Services (SSARS) Update

81

• SSARS 22• Issued in September 2016.• Supersedes SSARS 14 (same title).• Effective for compilation reports on pro forma

financial information dated on or after May 1, 2017.

SSARS Update

82

• SSARS 22 (continued)• When performing a compilation of pro forma

financial information, the accountant should takethe following steps:• Comply with the requirements set forth in AR-C Section

80, Compilation Engagements, adapted as necessary.• Obtain an understanding of the underlying transaction or

event.

SSARS Update

83

• SSARS 22 (continued)• Comply with the requirements set forth in AR-C

Section 80, Compilation Engagements, adapted asnecessary.

• Obtain an understanding of the underlying transaction orevent.

SSARS Update

84

• SSARS 22 (continued)• Ascertain that management has fulfilled its agreement to

include the following in any document that contains thepro forma financial information:• The complete financial statements of the entity for

the most recent year (or for the preceding year iffinancial statements for the most recent year are notyet available) or such financial statements arereadily available.

SSARS Update

85

• SSARS 22 (continued)• If pro forma financial information is presented for an

interim period, either historical interim financialinformation for that period (which may be incondensed form) or that such interim information isreadily available.

• In the case of a business combination, the relevantfinancial information for the significant constituentparts of the combined entity.

SSARS Update

86

• SSARS 22 (continued)• Ascertain that management has fulfilled its agreement to

ensure that the financial statements of the entity (or, inthe case of a business combination, of each significantconstituent part of the combined entity) on which the proforma financial information is based have been subjectedto a compilation, review, or an audit engagement.

SSARS Update

87

• SSARS 22 (continued)• Ascertain that management has fulfilled its agreement to

include the accountant’s compilation or review report orthe auditor’s report on the financial statements (or havereadily available) in any document containing the proforma financial information.

SSARS Update

88

• SSARS 23• Issued in October 2016.• Makes changes to various sections of the codified

standards resulting from the issuance of SSARS21.

SSARS Update

89

• SSARS 23• Effective upon issuance except for the

amendments to AR-C Sections 70 and 80 withrespect to prospective financial information. Thoseamendments are effective for prospective financialinformation prepared on or after May 1, 2017,and for compilation reports dated on or afterMay 1, 2017, respectively.

SSARS Update

90

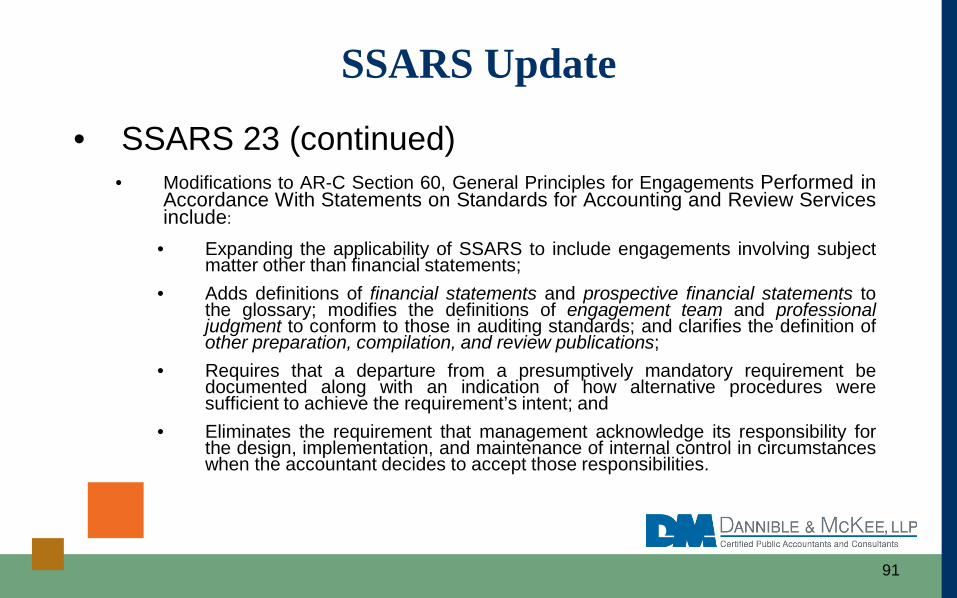

• SSARS 23 (continued)• Modifications to AR-C Section 60, General Principles for Engagements Performed in

Accordance With Statements on Standards for Accounting and Review Servicesinclude:

• Expanding the applicability of SSARS to include engagements involving subjectmatter other than financial statements;

• Adds definitions of financial statements and prospective financial statements tothe glossary; modifies the definitions of engagement team and professionaljudgment to conform to those in auditing standards; and clarifies the definition ofother preparation, compilation, and review publications;

• Requires that a departure from a presumptively mandatory requirement bedocumented along with an indication of how alternative procedures weresufficient to achieve the requirement’s intent; and

• Eliminates the requirement that management acknowledge its responsibility forthe design, implementation, and maintenance of internal control in circumstanceswhen the accountant decides to accept those responsibilities.

SSARS Update

91

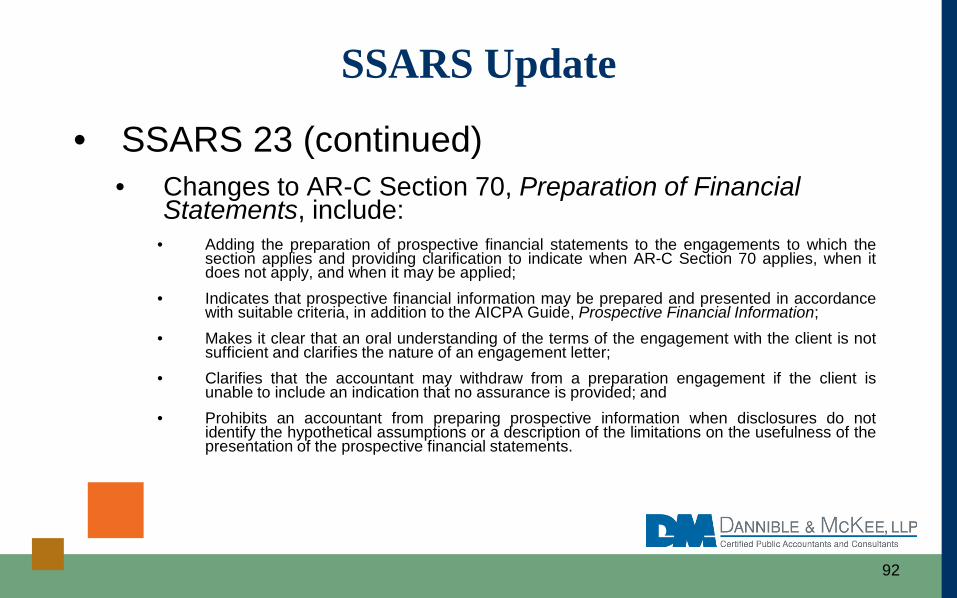

• SSARS 23 (continued)• Changes to AR-C Section 70, Preparation of Financial

Statements, include:• Adding the preparation of prospective financial statements to the engagements to which the

section applies and providing clarification to indicate when AR-C Section 70 applies, when itdoes not apply, and when it may be applied;

• Indicates that prospective financial information may be prepared and presented in accordancewith suitable criteria, in addition to the AICPA Guide, Prospective Financial Information;

• Makes it clear that an oral understanding of the terms of the engagement with the client is notsufficient and clarifies the nature of an engagement letter;

• Clarifies that the accountant may withdraw from a preparation engagement if the client isunable to include an indication that no assurance is provided; and

• Prohibits an accountant from preparing prospective information when disclosures do notidentify the hypothetical assumptions or a description of the limitations on the usefulness of thepresentation of the prospective financial statements.

SSARS Update

92

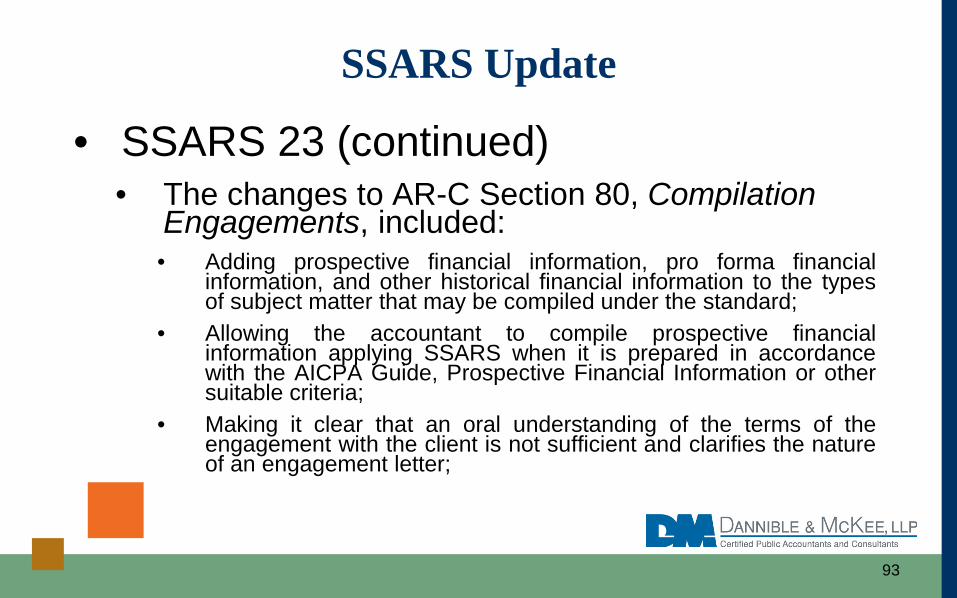

• SSARS 23 (continued)• The changes to AR-C Section 80, Compilation

Engagements, included:• Adding prospective financial information, pro forma financial

information, and other historical financial information to the typesof subject matter that may be compiled under the standard;

• Allowing the accountant to compile prospective financialinformation applying SSARS when it is prepared in accordancewith the AICPA Guide, Prospective Financial Information or othersuitable criteria;

• Making it clear that an oral understanding of the terms of theengagement with the client is not sufficient and clarifies the natureof an engagement letter;

SSARS Update

93

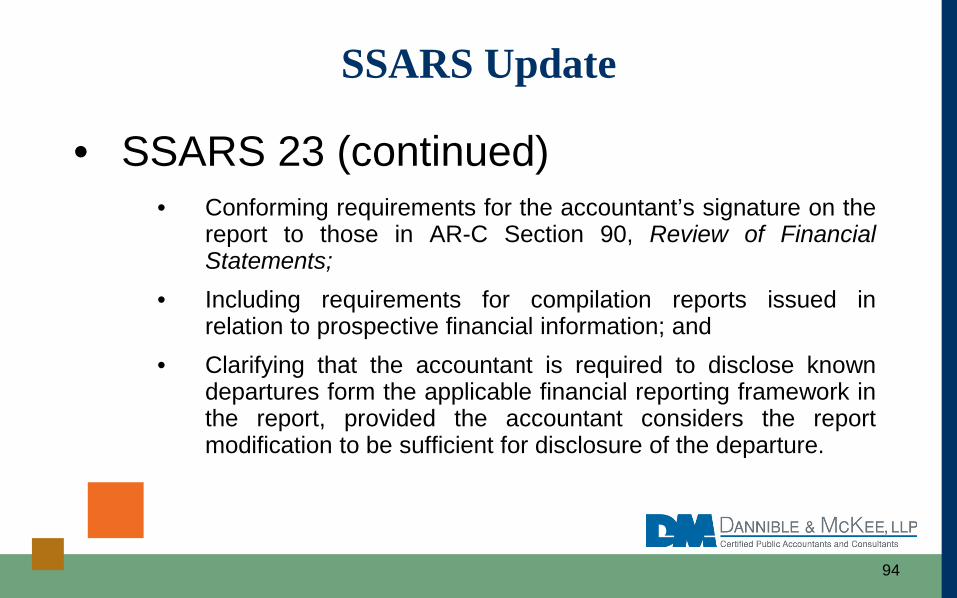

• SSARS 23 (continued)• Conforming requirements for the accountant’s signature on the

report to those in AR-C Section 90, Review of FinancialStatements;

• Including requirements for compilation reports issued inrelation to prospective financial information; and

• Clarifying that the accountant is required to disclose knowndepartures form the applicable financial reporting framework inthe report, provided the accountant considers the reportmodification to be sufficient for disclosure of the departure.

SSARS Update

94

• SSARS 23 (continued)• Changes to AR-C Section 90, Review of Financial

Statements, including:• Clarifying that a review of any historical financial information,

including pro forma financial information, is performed inaccordance with SSARS;

• Making it clear that an oral understanding of the terms of theengagement with the client is not sufficient and clarifies the natureof an engagement letter;

• Clarifying the definition of supplementary information;

SSARS Update

95

• SSARS 23 (continued)• Changing the language regarding the requirement for the

accountant’s or firm’s signature and the signature of appropriateparties from the client on the engagement letter to be consistentwith the language in AR-C Sections 70 and 80;

• Harmonizing the requirements for the accountant’s or firm’ssignature on the review report with the language in AR-C Section80; and

• Revising the accountant’s reporting responsibilities whensupplementary information accompanies the reviewed financialstatements.

SSARS Update

96

• Topics:• Cybersecurity.• Benchmarking Investment Expenses.• Mortality Improvement Scale Released.• New Fiduciary Rules Taking Affect.• 2017 Pension Limits.

Pension/ERISA Update

97

• Cybersecurity:• DOL expressed concerns that employee benefit

plans may be vulnerable to cyberattacks.

• Responsibility to implement processes andcontrols to restrict access to plan’s systemsresides with those charged with governance.

Pension/ERISA Update

98

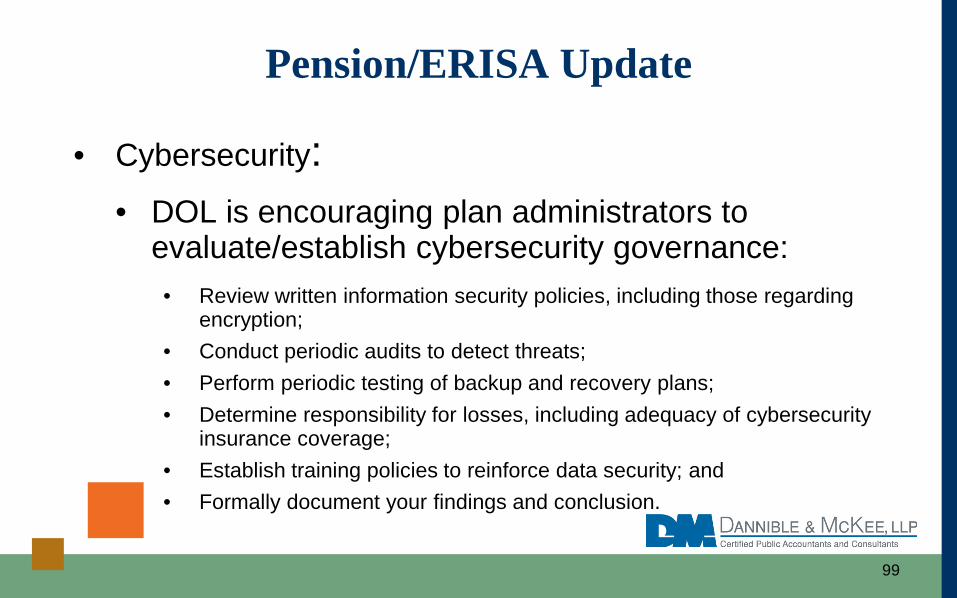

• Cybersecurity:• DOL is encouraging plan administrators to

evaluate/establish cybersecurity governance:• Review written information security policies, including those regarding

encryption;• Conduct periodic audits to detect threats;• Perform periodic testing of backup and recovery plans;• Determine responsibility for losses, including adequacy of cybersecurity

insurance coverage;• Establish training policies to reinforce data security; and• Formally document your findings and conclusion.

Pension/ERISA Update

99

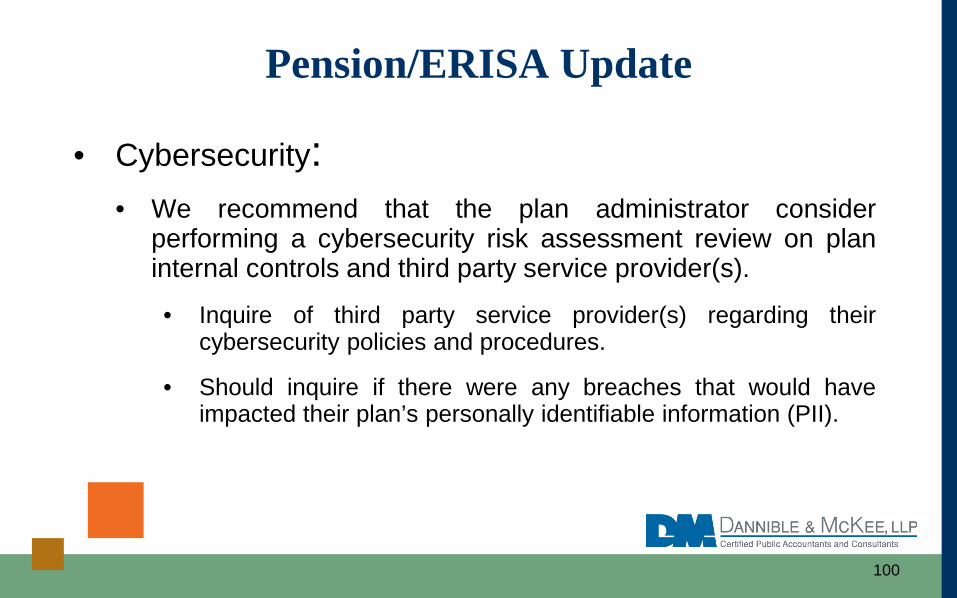

• Cybersecurity:• We recommend that the plan administrator consider

performing a cybersecurity risk assessment review on planinternal controls and third party service provider(s).

• Inquire of third party service provider(s) regarding theircybersecurity policies and procedures.

• Should inquire if there were any breaches that would haveimpacted their plan’s personally identifiable information (PII).

Pension/ERISA Update

100

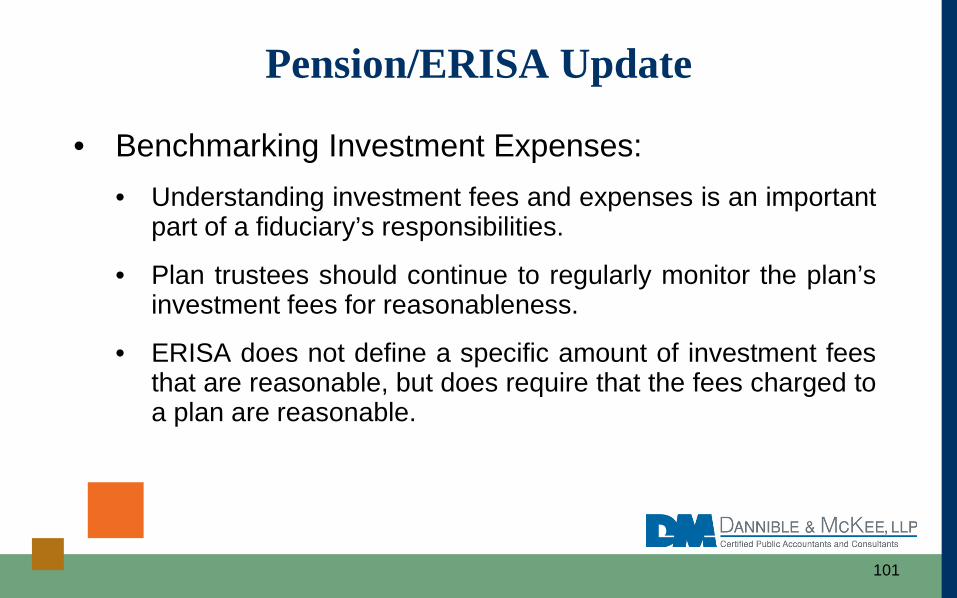

• Benchmarking Investment Expenses:• Understanding investment fees and expenses is an important

part of a fiduciary’s responsibilities.

• Plan trustees should continue to regularly monitor the plan’sinvestment fees for reasonableness.

• ERISA does not define a specific amount of investment feesthat are reasonable, but does require that the fees charged toa plan are reasonable.

Pension/ERISA Update

101

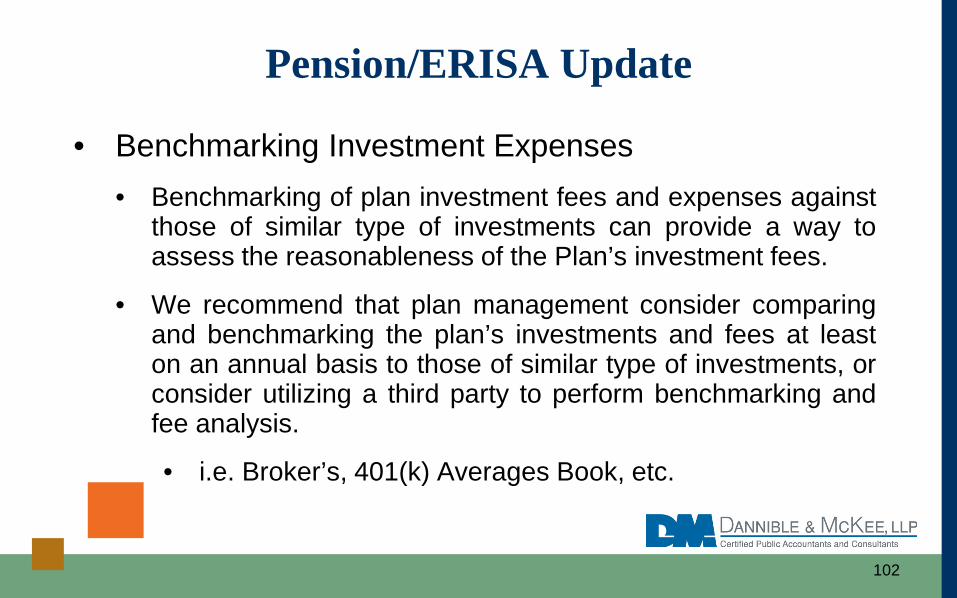

• Benchmarking Investment Expenses• Benchmarking of plan investment fees and expenses against

those of similar type of investments can provide a way toassess the reasonableness of the Plan’s investment fees.

• We recommend that plan management consider comparingand benchmarking the plan’s investments and fees at leaston an annual basis to those of similar type of investments, orconsider utilizing a third party to perform benchmarking andfee analysis.

• i.e. Broker’s, 401(k) Averages Book, etc.

Pension/ERISA Update

102

• Mortality Improvement Scale Released:• On October 20, 2016, Society of Actuaries (SOA) released

the 2016 Mortality Improvement Scale for pension plans(MP-2016 Scale).

• Annual update to the RP-2014 base model that reflectsthree additional years of Social Security mortality data.

• Does not affect those plans that recently filed byOctober 17, 2016.

Pension/ERISA Update

103

• Mortality Improvement Scale Released:

• However, those plans that yet to file will need toevaluate the effect MP-2016 will have on theirfinancial statements.

• The updated scale reflects a trend towardsomewhat smaller improvements in longevity.

• The SOA preliminary estimates suggest that theupdating to the MP-2016 scale might reduce aplan’s liabilities between 1½ - 2%.

Pension/ERISA Update

104

• New Fiduciary Rules:• In February 2015, President Obama introduced new rules at curbing conflicts of

interest and excessive fees.• New regulations were implemented by the DOL, which are effective in

April 2017.• Under the new regulations, financial advisors will be required “to act in

the best interest of their financial planning clients” as opposed to sellingthem financial products.• Financial advisors must either offer low-cost funds OR be able to defend

when offering more expensive options.• Regulations do not ban commissions or revenue sharing, but clients must

sign a “best interest contract exemption (BICE)” in these cases.

Pension/ERISA Update

105

• New Fiduciary Rules:• Financial advisors will be required to maintain additional

documentation showing how their clients best interest arebeing put first.

• Ensure that you are working with your financial advisors tosee if they are in compliance with these new regulations.

Pension/ERISA Update

106

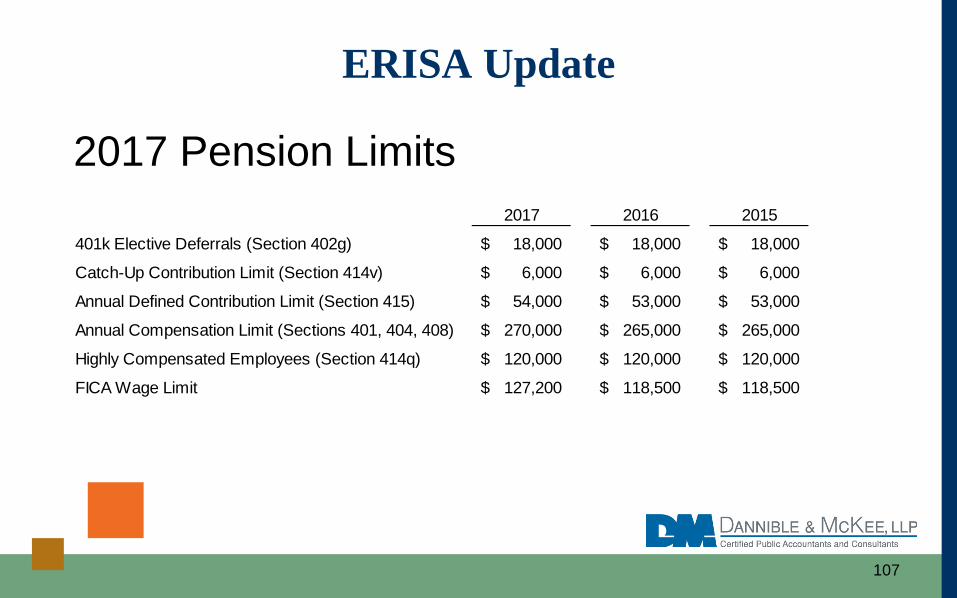

2017 Pension Limits

ERISA Update

107

2017 2016 2015

401k Elective Deferrals (Section 402g) 18,000$ 18,000$ 18,000$

Catch-Up Contribution Limit (Section 414v) 6,000$ 6,000$ 6,000$

Annual Defined Contribution Limit (Section 415) 54,000$ 53,000$ 53,000$

Annual Compensation Limit (Sections 401, 404, 408) 270,000$ 265,000$ 265,000$

Highly Compensated Employees (Section 414q) 120,000$ 120,000$ 120,000$

FICA Wage Limit 127,200$ 118,500$ 118,500$

FASB, SSARS & ERISA Update

108

Joseph Chemotti, CPA, CCIFP

Email: [email protected]: www.dmcpas.com and

www.dmconsulting.comAddress:Financial Plaza221 South Warren Street Scan to add5th Floor Joseph Chemotti toSyracuse, NY 13202 your contacts.

Phone: (315) 472-9127

109

Thomas V. Fiscoe, CPA, CGMA

Dannible & McKee, LLP2016 Tax & Financial Planning Conference

November 10, 2016

Corporate Governance Update

110

High priority for reporting companies and SEC.

Resources found on SEC website. Public companies are required to discuss

security measures. All companies should consider IT structure

and measures such as insurance for data breaches.

Cyber Security

111

Discussed last year and still should be a high priority.

Begin to plan spots that will be vacant. Look for bench strength by recruiting

those with industry expertise. Consider cyber security and IT strengths.

Board Succession Planning

112

Public companies are receiving a lot of attention around incentive compensation.

Dodd Frank Act proposal being vetted to prohibit or limit incentive compensation that encourages inappropriate risks.

Concern is safeguards and financial fraud could occur as we have seen in the past.

Proposal to also reduce mandated disclosure in compensation discussion and analysis on Form 10-K.

Incentive Compensation

113

Discussed last year – Complex rules but simple ratio.

Median annual total compensation of all employees except CEO.

Annual compensation of CEO.

Pay Ratio Disclosure

114

Compute ratio. Effective January 1, 2017. Not small reporting companies.

Pay Ratio Disclosure

115

Another topic from last year. Pilot project still underway. Provided to enhance communication

between auditor and audit committee. There are 28 indicators being looked at. PCAOB website has webcast that is

informative (25 mins.)

Audit Quality Indicators

116

Still both public and private company initiatives in effect.

SEC publishes quarterly disclosure manual for reference and to incorporate current issues.

FASB still looking to simplify GAAP.

Disclosure Effectiveness

117

Provides for small companies to raise capital within certain limits with reduced disclosure and regulation.

Result of Jump Start our Business Startups (JOBS) Act.

Broker dealers and funding portals register with SEC.

Crowd Funding

118

Bad actor disqualification and companies can raise up to $1,000,000.

Limits what an investor can purchase. Resources on SEC website.

Crowd Funding

119

Effective for audit reports issued after January 31, 2017.

Reported on Form AP. Name of engagement partner and

partner ID.

Disclosure of Audit Participants

120

Also other accounting firms participating in the audit where responsibility is not divided.

Filed within 35 days or 10 days.

Disclosure of Audit Participants

121

Thomas V. Fiscoe, CPA, CGMAManaging Partner

Email: [email protected]: www.dmcpas.com and

www.dmconsulting.comAddress:

Financial Plaza221 South Warren Street 5th FloorSyracuse, NY 13202

Phone: (315) 472-9127

Scan to add Thomas Fiscoe to

your contacts.

QUESTIONS

123

Any tax advice contained herein was not intended or written to be used, andcannot be used, for the purpose of avoiding penalties that may be imposedunder the Internal Revenue Code or applicable state or local tax law provisions.

Circular 230

124

This presentation is © 2016 Dannible & McKee, LLP. All rights reserved. No part of thisdocument may be reproduced, transmitted or otherwise distributed in any form or by anymeans, electronic or mechanical, including by photocopying, facsimile transmission,recording, rekeying, or using any information storage and retrieval system, without writtenpermission from Dannible/McKee and Associates, Ltd. Any reproduction, transmission ordistribution of this form or any material herein is prohibited and is in violation of U.S. law.Dannible/McKee and Associates, Ltd. expressly disclaims any liability in connection withthe use of this presentation or its contents by any third party.

This presentation and any related materials are designed to provide accurate informationin regard to the subject matter covered, and are provided solely as a teaching tool, withthe understanding that neither the instructor, author, publisher, nor any other individualinvolved in its distribution is engaged in rendering legal, accounting, or other professionaladvice and assumes no liability in connection with its use. Because regulations, laws, andother professional guidance are constantly changing, a professional should be consultedif you require legal or other expert advice.

Copyright / Disclaimer

125