Embed Size (px)

Citation preview

Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Should a Diocese form a captive?

Kevin Heffernan Sr VP ArtexTim Perr Managing Principal, CEO Perr & Knight

2Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Should a Diocese have a captive

Types of Captives– Pure (Single Parent) Captive– Group Captive– Risk Retention Groups

Captive Structure and ApplicationsMarket TrendsCaptive Feasibility StudyOperating a Captive Insurance Company

3Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

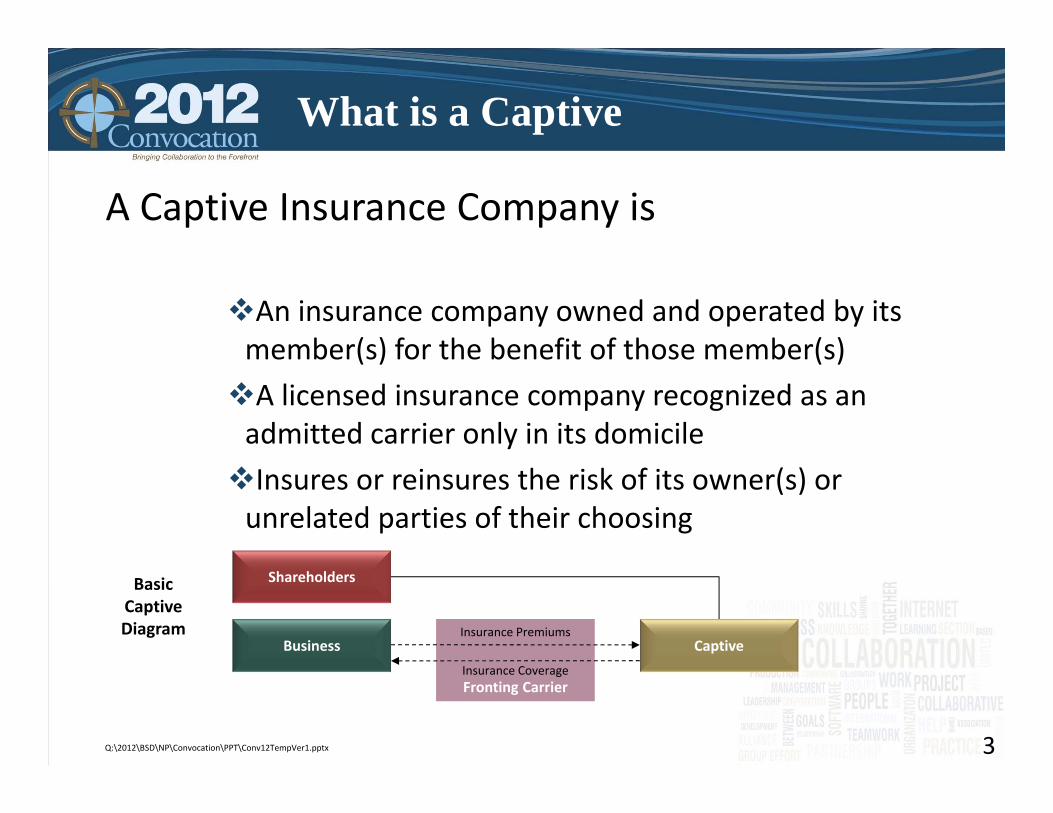

What is a Captive

A Captive Insurance Company is

An insurance company owned and operated by its member(s) for the benefit of those member(s)A licensed insurance company recognized as an admitted carrier only in its domicileInsures or reinsures the risk of its owner(s) or unrelated parties of their choosing

Shareholders

Business Captive

Fronting CarrierFronting Carrier

Insurance Premiums

Insurance Coverage

Basic Captive Diagram

4Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

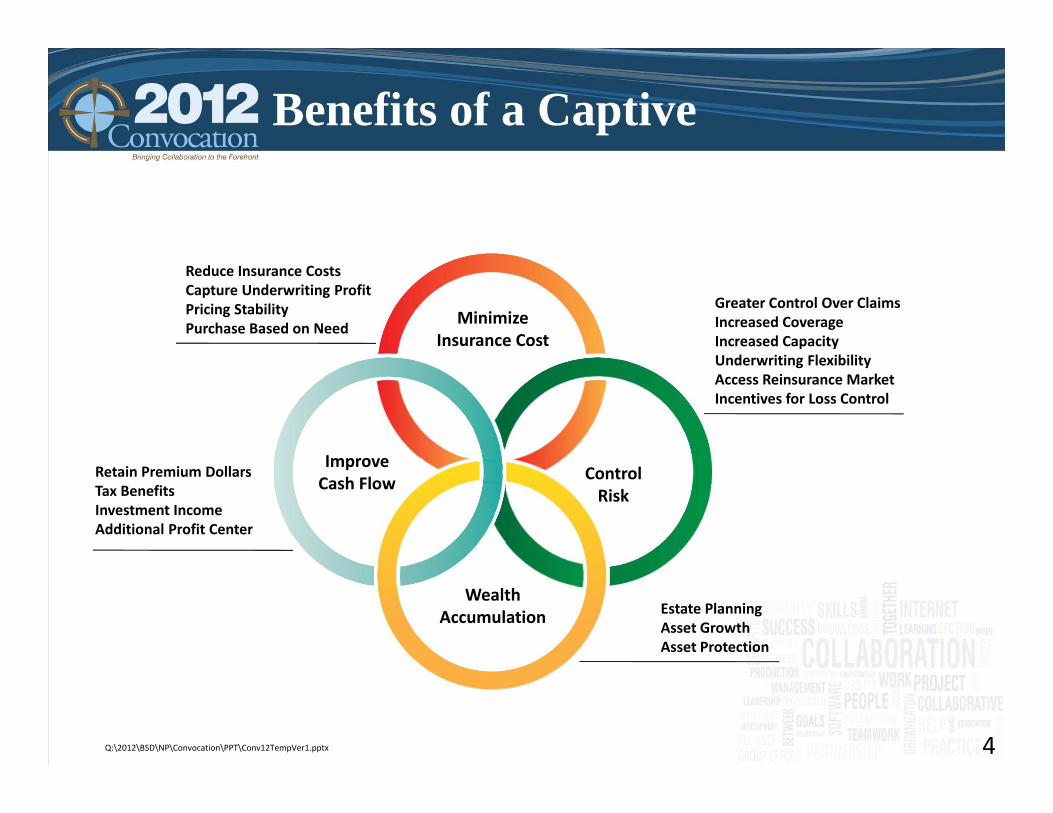

Benefits of a Captive

Minimize Insurance Cost

Improve Cash Flow

Wealth Accumulation

Control Risk

Reduce Insurance CostsCapture Underwriting ProfitPricing StabilityPurchase Based on Need

Greater Control Over ClaimsIncreased CoverageIncreased CapacityUnderwriting FlexibilityAccess Reinsurance MarketIncentives for Loss Control

Retain Premium DollarsTax BenefitsInvestment IncomeAdditional Profit Center

Estate PlanningAsset GrowthAsset Protection

5Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Pure Captive – Single ParentOwned by one company – parentInsures or reinsures risk of the parent

Group CaptiveOwned by two or more companiesInsures or reinsures risk of the group

Risk Retention GroupsEstablished under federal lawCan operate in all 50 states; insureds must be ownersCan write only liability risk

6Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Pure Captives

Insures the risk of an owner and it subsidiaries. traditionally used by large Fortune 2000 companies

Client is in control of the operation, lines of coverage, limits and domicile location

Allows for some direct writing of policies with access to the reinsurance market to follow form

Captive surplus can be used by owner as it needs: Stabilizing premiums in a hard market Increasing retention levels

Insuring new lines or expanding coverage on current lines

7Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Captive Structure

Diocese can establish not‐for‐profit insurance companies in some domiciles‐ including VT, DC, SC and HI.

The Diocesan (not‐for‐profit) captive can receive 501(c) 3 status, which makes it exempt from federal income tax.

The Diocesan Captive can build surplus in its captive and not have to commingle its insurance funds with those designed for programs.

The captive can be used similarly as traditional captives to smooth premiums or cover difficult to place risk.

Larger diocese can form a pure captive, offers greater flexibility than group captives.

8Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Move the SIR portion of their program into a captive, formalizing the SIR process by creating premiums charged by the captive.

Risk management cost can be shifted to the captive. Captive is a separate entity from the diocese and its surplus

grows independently from the diocese. Captive can access reinsurance markets, FET on reinsurance

placement is 1%. Coverage not found or hard to place coverage can be written

in the captive. A captive can access TRIA the Federal backstop.

Employee Benefits in a Captive.

Captive Applications

9Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Employee Benefits

Recent years has seen a growth in employers reinsuring benefit plans to their captive.

The benefit to the captive is its risks are diversified.

Diocese are exempt from ERISA so prior approval from Depart of Labor (DOL) to use a captive for employee benefits does not need to be part of the captive plan.

The discussion of employee benefits in a captive should consider the comprehensive use of a captive in an employers ERM.

10Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

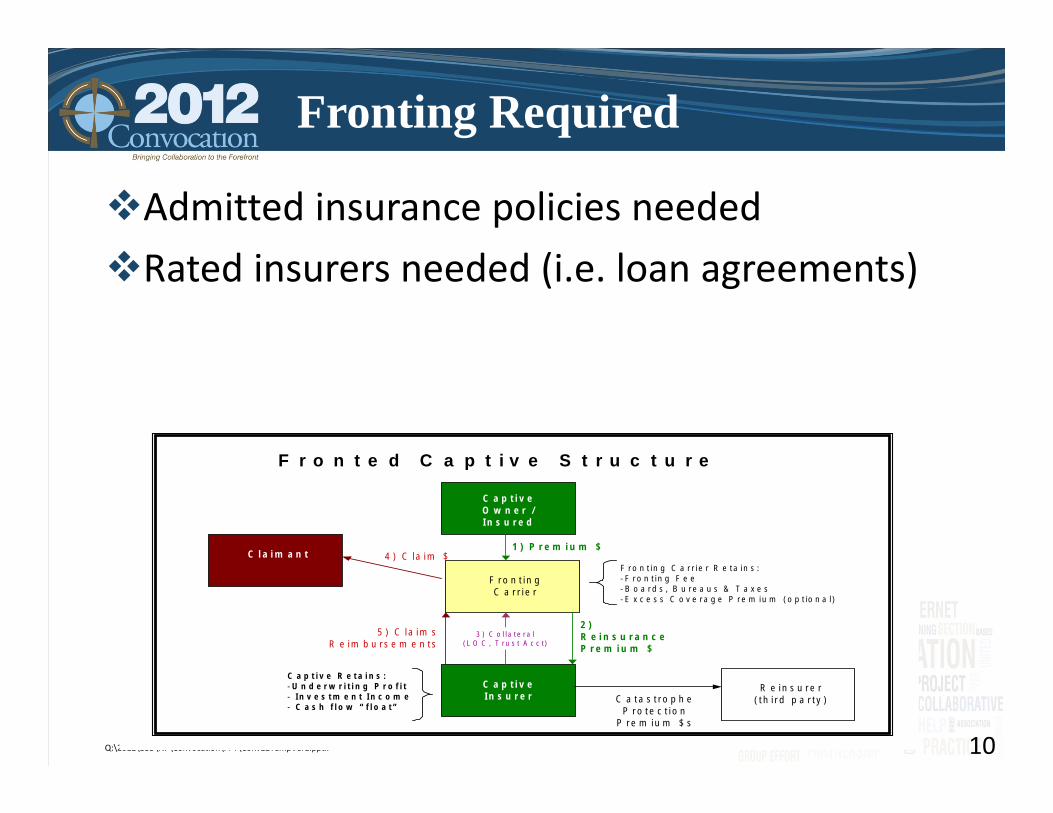

Fronting Required

Admitted insurance policies neededRated insurers needed (i.e. loan agreements)

F r o n t e d C a p t i v e S t r u c t u r e

C a p t i v e O w n e r / I n s u r e d

F r o n t i n g C a r r i e r

C a p t i v e I n s u r e r

R e i n s u r e r ( t h i r d p a r t y )

C l a i m a n t1 ) P r e m i u m $

2 ) R e i n s u r a n c eP r e m i u m $

C a t a s t r o p h e P r o t e c t i o n

P r e m i u m $ s

F r o n t i n g C a r r i e r R e t a i n s :- F r o n t i n g F e e- B o a r d s , B u r e a u s & T a x e s- E x c e s s C o v e r a g e P r e m i u m ( o p t i o n a l )

4 ) C l a i m $

5 ) C l a i m sR e i m b u r s e m e n t s

C a p t i v e R e t a i n s :- U n d e r w r i t i n g P r o f i t- I n v e s t m e n t I n c o m e- C a s h f l o w “ f l o a t ”

3 ) C o l l a t e r a l( L O C , T r u s t A c c t )

11Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

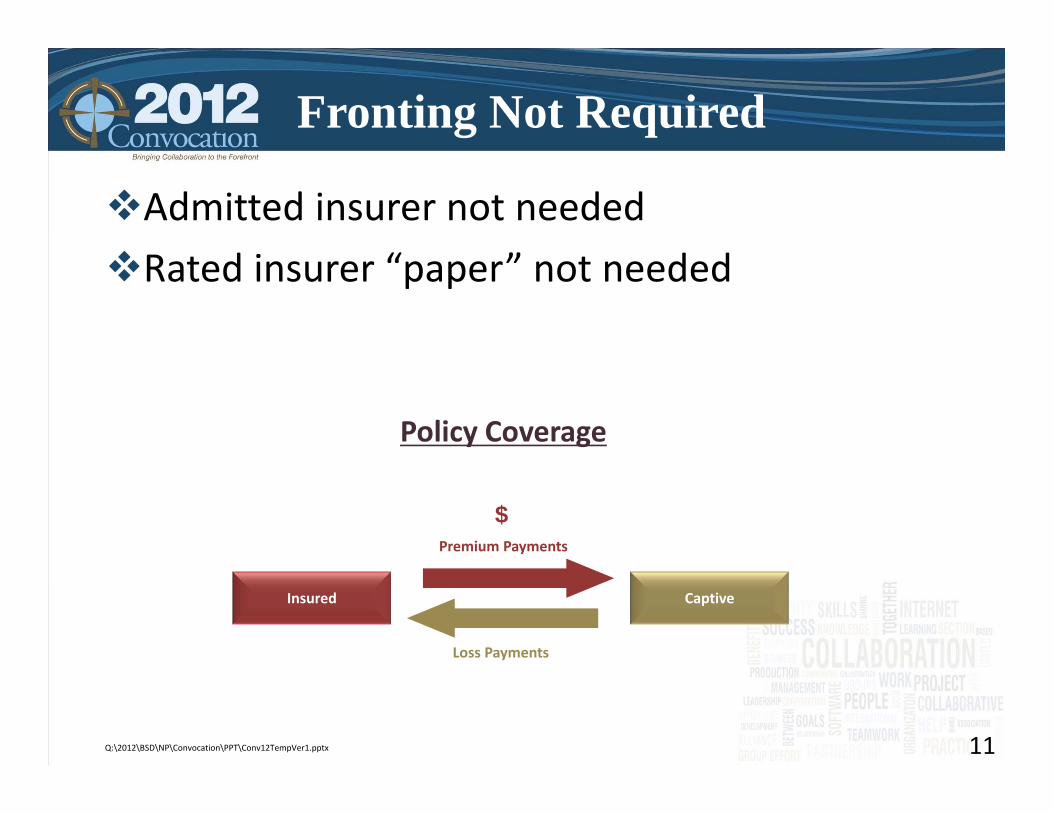

Fronting Not Required

Admitted insurer not neededRated insurer “paper” not needed

$

Policy Coverage

Loss Payments

Premium Payments

Insured Captive

12Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Should a Diocese Form a Captive?

Actuarial Perspective

Tim PerrManaging Principal & Consulting ActuaryPerr&Knight

13Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

How About a Captive?

Flexibility – You Choose the StructureSelf‐Insured RetentionsDeductiblesCoinsuranceLimits and Excess AttachmentsCreative Coverages (e.g., iPads)

14Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

How About a Captive?

Surplus ProtectionCaptives are regulated by domiciliary stateCommissioner must approve all surplus releasesDouble edged sword

• Protected against debtors/claimants• Can be difficult to access

15Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

How About a Captive?

Claims Trends – Workers Compensation Medical claim costs increasing moderately Medicare set‐asides (MSAs) significant expense Indemnity (lost time) claims costs flat as wages stagnant during

recession Claims frequencies down offsetting most claims cost inflation Costs expected to increase moderately going forward

• Claim frequency stabilizes• Wage inflation returns• Continued medical cost inflation

California approves 37% increase on 1/1/2012 FWIW, California Diocesanal experience does not support that

increase Marketplace: Moderate price increases but continued availability

16Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

How About a Captive?

Claims Trends – Auto & General LiabilityBenign claim frequency and severity trends industry‐wideAuto claims costs have increased due to medical inflation however increase has been neutralized by decreasing claim frequency – less car accidents

Marketplace: Stable prices and widespread availability

17Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

How About a Captive?

Claims Trends – Employment Practices LiabilityModerate increases in both claim frequency and severity over past 5 years in Diocesanal experience

Much higher trends in non‐church businessPerhaps correlated with recessionDiocesanal experience appears to have stabilized in 2011Marketplace: Price increases expected on all Management Liability Coverages (EPLI, D&O, Crime, Fidelity)

18Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

How About a Captive?

Claims Trends – Sexual Misconduct LiabilityOlder claims

• Very few emerging any more• Most barred by statute• Low frequency/high severity

Newer claims• Tend to involve non‐clergy• Much lower settlements• Moderate frequency

High Political Risk• Quarry case in California• Law changes that extend statute of limitations

Marketplace: Meaningful coverage very difficult to find

19Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

How About a Captive?

Claims Trends – PropertyCurrent value inflationCatastrophes upUnderlying trends not changing much but prices areExpect higher retentionsMarketplace: Much higher rates, restrictions on coverage and higher retentions

20Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

How About a Captive?

Other TopicsHealth Insurance

• PPACA – aka Obamacare• Captive can be used as reinsurer of Church Program

Property• Single parent captive (tax exempt) can be used to spread risk across years

• Allows Diocese to smooth costs through market cycles

21Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

How About a Captive?

What you should expect from your ActuaryIndependence and honestyGood communication skillsCross‐discipline knowledgeExperience

22Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Operating a Captive

A captive is a regulated insurance company and the company follows the regulation of your domicileThe captive should maintain a active business plan to guide the board of directors

23Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Items to Review Before and During Feasibility Study

Long‐term commitmentAdverse developmentCommitment of capitalDomicile taxesCaptive fixed operating costs

24Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

The Feasibility Study

Key ObjectiveA key component of the feasibility study is to help an investor understand their return on investment

Base DataThis objective is best achieved if the captive investor has its own loss experience to use in the study

25Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Feasibility Study Results

Analysis of retention scenarios or loss projectionsProgram structureCapital and collateral requirementsProject performanceDomicile analysisTax considerations

26Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

The Captive Formation Process

Business Plan Forecasts of Annual Expected LossesProgram Structure (Premiums, Limits, Capitalization)Proforma Captive Financial Statements

Selection of Service ProvidersCaptive Manager LegalAuditorsActuarial

Preliminary Meeting with Domicile Regulators45 to 60 day Process (Most Major Domiciles)

27Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Costs Related to Forming A Captive

Feasibility Study or Plan$30,000 ‐ $50,000, plus tax planning

Ownership Cost $100,000 ‐ $200,000Domicile taxesCaptive management feesAudit feesDomicile meetingsCost of collateralActuarial fees Legal feesPolicy issuance cost

28Q:\2012\BSD\NP\Convocation\PPT\Conv12TempVer1.pptx

Operating a Captive

Operation of a captive are summarized in seven broad categoriesInsuranceClaimsCash ManagementInvestment ManagementFinancial reportingRegulatory complianceGeneral Operations

![Elt Artex Manual[1]](https://img.pdfslide.net/doc/110x75/5571f85c49795991698d4105/elt-artex-manual1.jpg)