Embed Size (px)

Citation preview

Kevin O’TooleKevin O’TooleEDITOR EDITOR

AIRLINE BUSINESSAIRLINE BUSINESS

Air Transport and Tourism: Synergies and ParallelismsAir Transport and Tourism: Synergies and Parallelisms

University of SurreyUniversity of Surrey

Airline strategy: Airline strategy: The long viewThe long view

National champions

National marketsHeavy regulationLow competitionHigh growth rates 2xGDP

Market conditions

National champions

Dominant market shareRegulatory support/accessAbsorb/kill local competitorsMatch world standardsControl supply chain……control pricing

Strategies for success

National champions

National political constraintsComplexity/bureaucracyInflexibility on costLack of differentiationAll things to all men…within a

national boundary

The legacy

Global players

DeregulationGlobal economyFierce competition/market disciplinesMaturing markets – growth 1xGDPInternet democracy – smart buyers

The new market conditions

Global players

Global reachCustomer not product focusProfit driven not cost ledSegmented brandsDifferentiated productsCost flexibility

Strategies for success

The problem today is…

The industry as a whole has not sufficiently adapted to face those changed market conditions…

…it has often not been free to……BUT if airlines are not ready to

meet these challenges others will

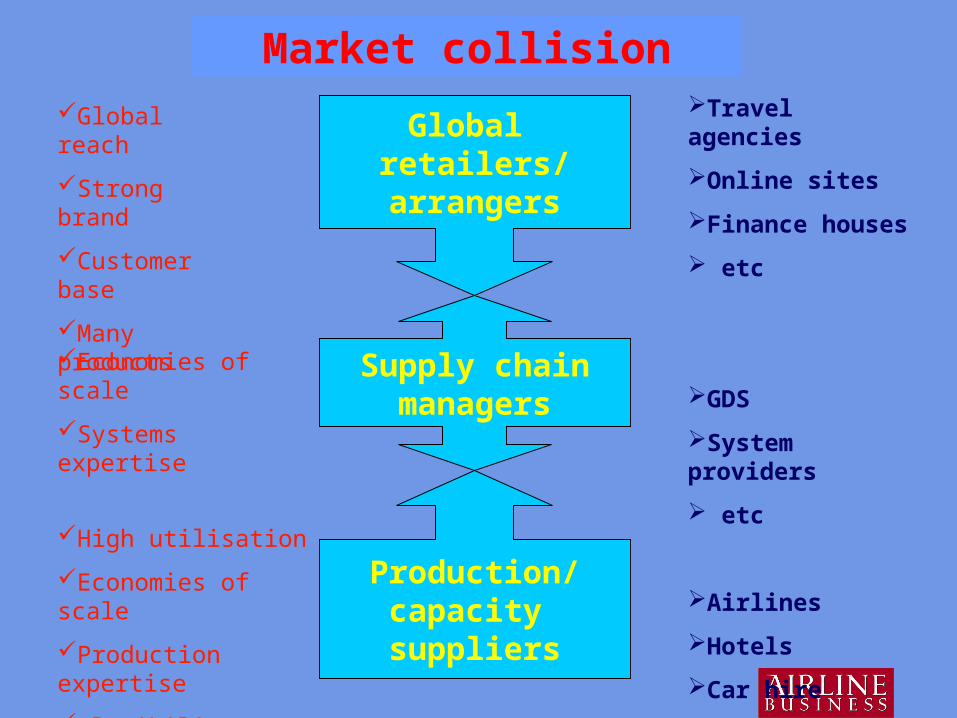

Market collision

Global retailers/arrangers

Supply chainmanagers

Production/capacity suppliers

Global reach

Strong brand

Customer base

Many products

Economies of scale

Systems expertise

High utilisation

Economies of scale

Production expertise

Flexibility

Travel agencies

Online sites

Finance houses

etc

GDS

System providers

etc

Airlines

Hotels

Car hire

etc

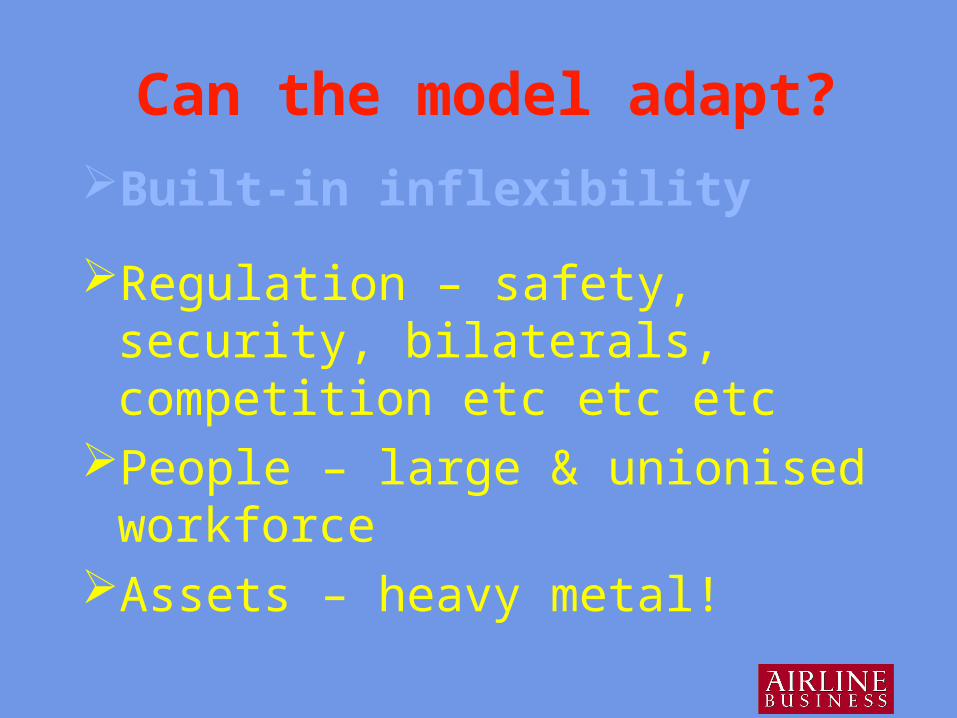

Can the model adapt?

Regulation – safety, security, bilaterals, competition etc etc etc

People – large & unionised workforceAssets – heavy metal!

Built-in inflexibility

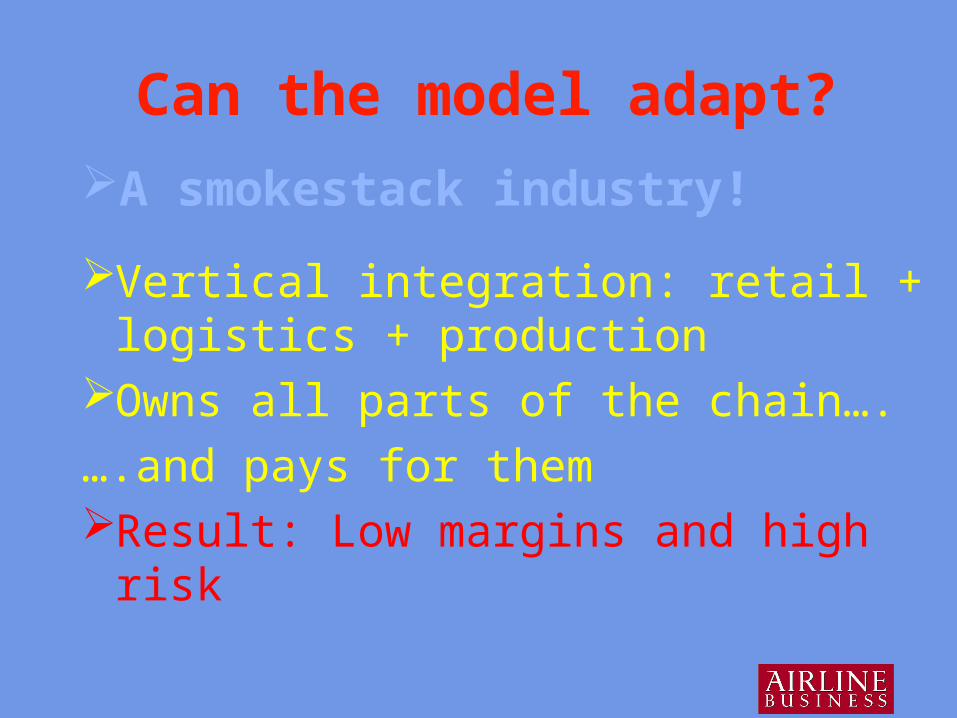

Can the model adapt?

Vertical integration: retail + logistics + production

Owns all parts of the chain….

….and pays for themResult: Low margins and high risk

A smokestack industry!

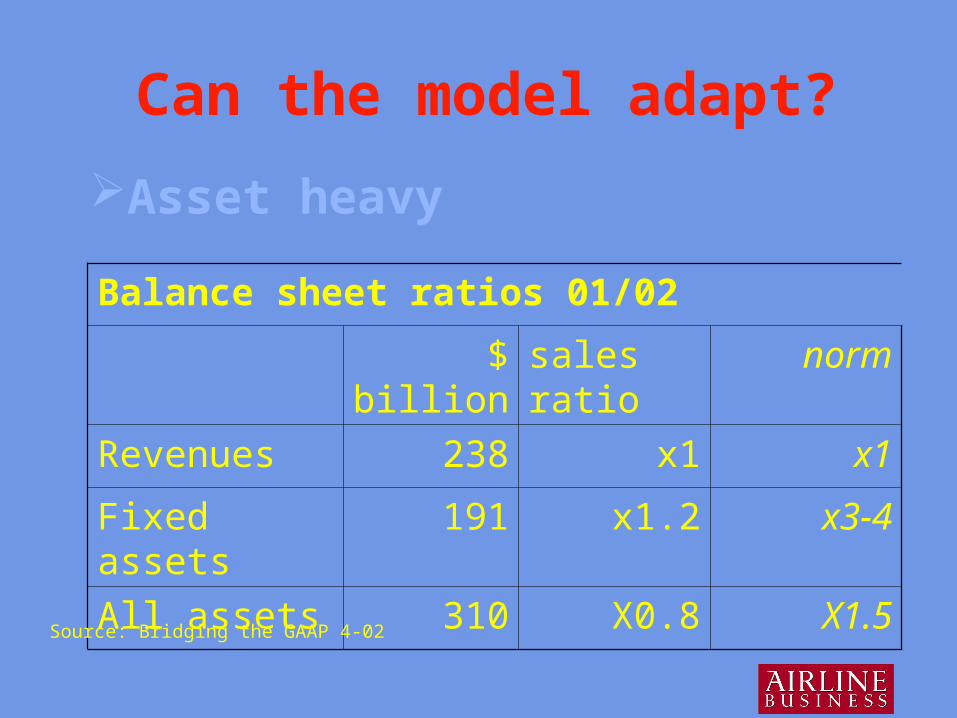

Can the model adapt?

Asset heavy

Balance sheet ratios 01/02

$ billion sales ratio norm

Revenues 238 x1 x1

Fixed assets 191 x1.2 x3-4

All assets 310 X0.8 X1.5

Source: Bridging the GAAP 4-02

Can the model adapt?

Service industry levels of people cost:employs 1.5-2 million worldwide

revenue/cost $200k per employee

ExpensiveHeavily unionised

Workforce heavy

A marginal business

Top 150 airline groups 5 year record

2001 2000 1999 1998 1997

Revenues -5.2% 8.2% 7.0% 2.0% 3.0%

Op margin -2.0% 4.2% 5.3% 6.8% 7.2%

Net margin -4.2% 1.1% 3.0% 3.1% 3.2%

Source: Airline Business World Airline Rankings

Source: Bridging the GAAP 4-02

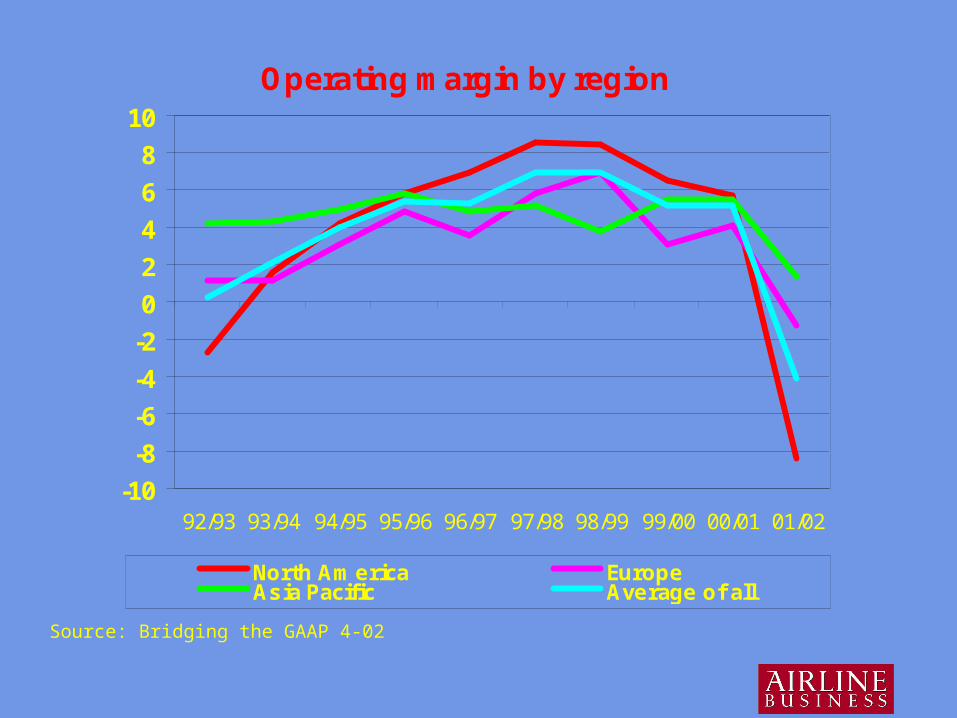

Operating margin by region

-10

-8

-6

-4

-2

0

2

4

6

8

10

92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02

North America EuropeAsia Pacific Average of all

Top 150 Airline Groups by typeType Revenues Groups Operating results

$ million 2001 2000Major 218,000 34 -6,654 12,789Flag-carrier 31,654 44 -577 162All cargo 25,257 9 618 1,199Independent 17,347 29 -50 927Low cost 9,272 10 988 1,288Leisure 6,911 13 -52 1Regional 4,330 11 5 232Grand Total 312,770 150 -5,721 16,598

Source: Airline Business World Airline Rankings

New models

Tackle costsOutsource what is not essentialBuild flexibility into capacity etcNew deals with partners eg power-

by-the hourNew deals with unions

The response

New models

Tackle fixed costsGain global scale

Economies of scaleMove beyond national boundariesMarket mobility

The response

New models

Tackle fixed costsGain global scaleIncrease offer

Match offer to customer valueExploit new distribution channelsCRMIncrease the offer

The response

62%

55%

33%

32%

25%

24%

16%

12%

20%

28%

21%

17%

19%

37%

21%

23%

Schedule information onarrivals and departures

Frequent flyer services /redemptions

Hotel booking sales

Excursions/ tour /package holiday sales

Corporate client sales

Car hire sales

Partner airline seats

'Call me back' facility

Currently offer

Plan to offer innext 2 years

Online services for customers(Base: All respondents)

New models

Choose where to sit in the chainAsset light service business….orPeople light production business

Don’t spend or depend on the wrong assets

Learn from other retail/production models

The longer term

New models

European charterFour integrated travel groups…led by retail packaging…flying is incidental/adaptable

CargoFew express integrators…and going further eg Deutsche PostBelly cargo becomes a commodity

Examples

New models

Branded producerDifferentiated, desired named brand

Unbranded producerEfficient, flexible, global and cheap

Retail consolidatorCustomer connection, broad offer

Niche playerExploiting inaccessible markets

Global giantSheer market power

Possible models