Embed Size (px)

Citation preview

KEY ENABLING TECHNOLOGIES AND SMART SPECIALISATION

FOR A COMPETITIVE ITALY

PROF. GABRIEL M CREAN VICE-PRESIDENT FOR TECHNOLOGY, CEA, FRANCE,

HIGH LEVEL GROUP ON KEY ENABLING TECHNOLOGIES

Bari, 23th of July 2013

2 2

KETs: Global perspective

KETs: Why are they important 2

Outline

1

3

• 26,522 million men and women in the EU-27 were unemployed in May 2013 (Eurostat May 2013)

• 12.2% of total EU workforce

• 5,525 million young persons (under 25) were unemployed in the EU-27 (Eurostat May 2013)

• 23.1% of total workforce

• Italy: Unemployment rate 12.2% in 2013, ( 5.9% in 2007) 3,14 million people

= Pop Rome 2,7 million + pop Bari 320,475

• Italy: Youth unemployment rate 36.9% in 2013 (27.8% in 2010) 3

SMART Specialisation is NOT smart if it does not create jobs

4

“The new era of manufacturing will be marked by highly

agile, networked entreprises that use information and

analytics as skillfully as they employ talent and machinery

to deliver products and services to diverse global market.

In advanced economies, manufacturing will

continue to drive innovation, exports, and

productivity growth. In developing economies,

manufacturing continue to provide a pathway to higher

living standards. As long as companies and

countries understand the evolving nature of

manufacturing, and act on the powerful trends

shaping the global competitive environment,

they can thrive in this promising future”.

4

The strategic importance of manufacturing

McKinsey report Manufacturing the future: the next era of global growth and innovation. Nov 2012

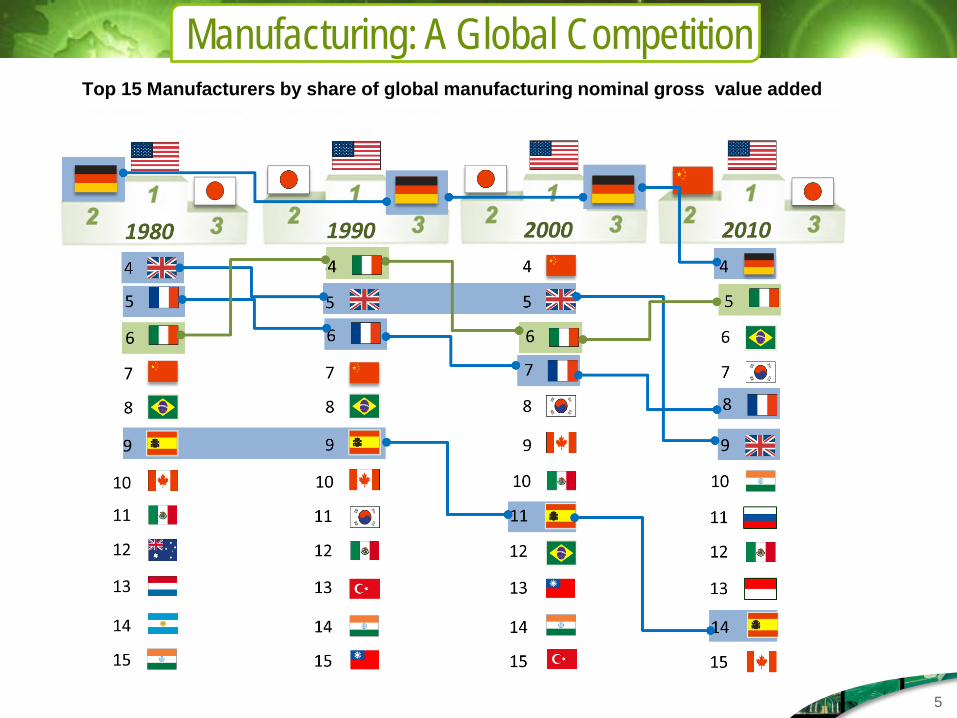

5 5

Manufacturing: A Global Competition Top 15 Manufacturers by share of global manufacturing nominal gross value added

6

McKinsey report Manufacturing the future: the next era of global growth and innovation. Nov 2012

Manufacturing drives innovation

Barack H. Obama, State of The Union 2011 speech, Jan 25

“At stake [right now] is whether new jobs and industries take root in this country, or somewhere else. […]

The rules have changed. In a single generation, revolutions in technology have transformed the way we live, work and do business. […]

The future is ours to win. But to get there, we can't just stand still.[…] We know what it takes to

compete for the jobs and industries of our time. We need to out-innovate, out-educate, and out-build the rest of the world. All these investments -- in innovation, education, and infrastructure -- will make America a better place to do business and create jobs.

The first step in winning the future is encouraging American innovation. […] In America,

innovation doesn't just change our lives. It is how we make our living. […] This is our generation's Sputnik moment. […] We'll invest in biomedical research, information technology, and especially clean energy technology an investment that will strengthen our security, protect our planet, and create countless new jobs for our people.”

7

New US Re-industrialisation Policy

8 8

US political focus on manufacturing

9 9

US political focus on manufacturing

The policy agenda for U.S. manufacturing is changing.

Five years ago the debate was mostly about how to

rescue and retain existing footholds in manufacturing,

but lately the debate is increasingly about how to

set the stage to lead the world in new technologies

and innovations that are changing the face of

manufacturing. That shift in direction was underscored

when eight states prepared new strategies based not on

the desire to “save manufacturing” but with the idea,

“Let’s lead in what lies ahead,” including robotics,

nanotechnology, and advanced materials.

10 10

0

20

40

60

80

100

2009 2012

47%

5%

44%

4%

62%

5%

31%

2%

Asia

Europe US

0

20

40

60

80

100

2009 2012

54%

6%

29%

11%

62%

11% 17% 10% Others

The share in Machine Tool production for the period 2009-2012

World Machine Tool consumption / geographical repartition for the period 2009-2012

“Once the manufacturing base is lost,

it never comes back”. CECIMO President

Europe competitiveness in advanced manufacturing is rapidly declining

11 11

45% 28% 24%

32%

38% 27%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Europe

Asia

US

Patent share by competitor bloc for all KETs cumulated (2000-2010)

Europe is resilent - but the window of opportunity is reducing

2009

2012

12 12

The diffusion and exploitation of European generated IPRs outside Europe is accelerating

0 1 2 3 4 5 6 7

2010

2011

2012

Average growth of license and patent revenues from outside Europe (%)

Innovation Union Scoreboard 2013

13

Market Knowledge

The valley of death

The European “Valley of Death”

Global patent and Manufacturing shares: the case of Li-Ion Battery

Global patent and Manufacturing shares: the case of PV

2010 2012

High Level Group :Building a bridge to success for regions

© CEA. All rights reserved

| 15

Development of Technology building blocks within DG

CONNECT & DG Res

Re-industrialisation of Europe: KETs Pilot Lines & Deployment supported by

H2020 and Structural Funds

Capacity Build-out on a level playing field: KETs industrial Policy

Public

Financing

Private

Financing

16 16

US and Asia invest massively in development activities to sustain their industrial innovation

17 17

KETs: Global perspective

KETs: Why are they important 2

Outline

1

Advanced Materials

Electronics

Software

Optics Biotechnologies

Sensors

Nanotechnologies

Advanced Manufacturing

KETs are indispensable for advanced products

19

Camera

Photonics substrate

Advanced materials

Chip

Microelectronics

Mems

Nanotechnologies

Advanced Manufacturing

KETs are indispensable for advanced products

20

KETs: -Advanced materials -Nanotechnologies -Biotechnologies

KETs: -Advanced manufac turing Systems -Biotechnology KETs: -Nanoelectronics -Photonics Fr

om K

ETs

to fi

nal p

rodu

ct

Material

Equipment

Component

Fro

m p

rodu

ct

to so

ciet

al ch

alle

nge

Product

Solutions & services

Societal challenges

Biomass

Biolsoprene

Biobased Synthesis rubber,

Adhesives, elastomers

Car tyres

Biobased tyres

CO2 reduction Energy efficiency (Climate change)

Car industry

MOCVD reactor

Lighting

GaN

LED

Lamp

Lighting

Energy efficiency

(Climate change)

Nomadic communication

Nano component (Low power)

Litho scanner

Nanoelectronics

Knowledge society

SOI material

Mobile phone

20

KETs are strategic along all value chains

21 Source: Gartner, Own analysis

1980 - Production sites > 25,000 wspm 200mm eq.

Σ 299,953wspm 200mm eq.

Weight of semiconductors

production sites with respect to total semiconductor

production in Europe

GlenrothesGreenock

SwindonChippenham

Bedford

Kiev

ZelenogradMoscow

Vilnius

Bucharest

Zarnovica

Genoa

Catane

NantesTours

Toulouse

NijmegenStadskanaal

Hamburg

Freising

Kista-Stockholm

Munich

Cornaredo

Rennes

Oldham

Evolution de la production de semi-conducteurs en Europe

(k wspm éq 200’’)

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

1980 1985 1990 1995 2000 2005 2010

<100mm’100/125/150

200mm300mm

300mm RTO pilot line

Evolution of the semiconductor manufacturing landscape in Europe, by region, from 1980 to 2010

SMART SPECIALISATION: A CASE-STUDY