Embed Size (px)

Citation preview

FISH TO 2030: THE ROLE & OPPORTUNITY FOR AQUACULTURE

Kobayashi, M., S. Msangi, M. Batka, S. Vannucini, M.M. Dey, and J. L. Anderson. 2015. Aquaculture Economics & Management 19(3):282-300.

DEFINITION OF REGIONS

0

50

100

150

20019

8419

8819

9219

9620

0020

0420

0820

1220

1620

2020

2420

28

Million MT

Total (Data)

Total (Model)

Capture (Data)

Total Fish Production: 1984-2030

Commodity Groups

N AmericaEurope

L AmericaChinaIndia

Other S AsiaSE AsiaJapan

Other Asia &…CWANA

Sub-Saharan…

0 10 20 30 40 50 60Million MT

2030 (Model) 2020 (Model)

› More than 50% increase 2006 to 2030 China India Other South Asia Cent./West Asia & N.

Africa › Less than 20% increase

2006 to 2030 Southeast Asia Sub-Saharan Africa North America Latin America

• Regions with little growth or decline Other Asia & Pacific Europe Japan

Consumption Growth

ShrimpCrustaceans

MollusksSalmon

DemersalTuna

Cobia/SwordEel/Sturgeon

TilapiaPangasius

CarpMullet

Other FreshOther Carp

Other PelagicOther Marine

0 10 20 30Million MT

2030 (Model) 2020 (Model)2008 (Data)

• More than 100% increase 2008 to 2030 Other marine Fish (152%) Demersal (131%) Tilapia (126%) Mullet (113%) Shrimp (110%)

• 40-100% increase 2008 to 2030 Pangasius (90%) Carp (89%) Crustaceans (82%) Molluscs (64%) Other fresh fish (63%) Eeel/sturgeon (58%) Salmon (53%) Other carp (50%) Tuna (48%) Cobia/swordfish (42%)

Sources of Aquaculture Supply Growth By Commodity

Projected Global Prices Fish Meal and Oil

0

1000

2000

3000

4000

500020

0020

0220

0420

0620

0820

1020

1220

1420

1620

1820

2020

2220

2420

2620

2820

30

prices ($ pe

r mt)

c-FshOil

Projected Prices ($/MT): Fish Meal, Fish Oil

Projected Global Prices of Major Seafood Categories

0

5000

10000

15000

20000

2500020

0020

0220

0420

0620

0820

1020

1220

1420

1620

1820

2020

2220

2420

2620

2820

30

Prices ($ pe

r mt)

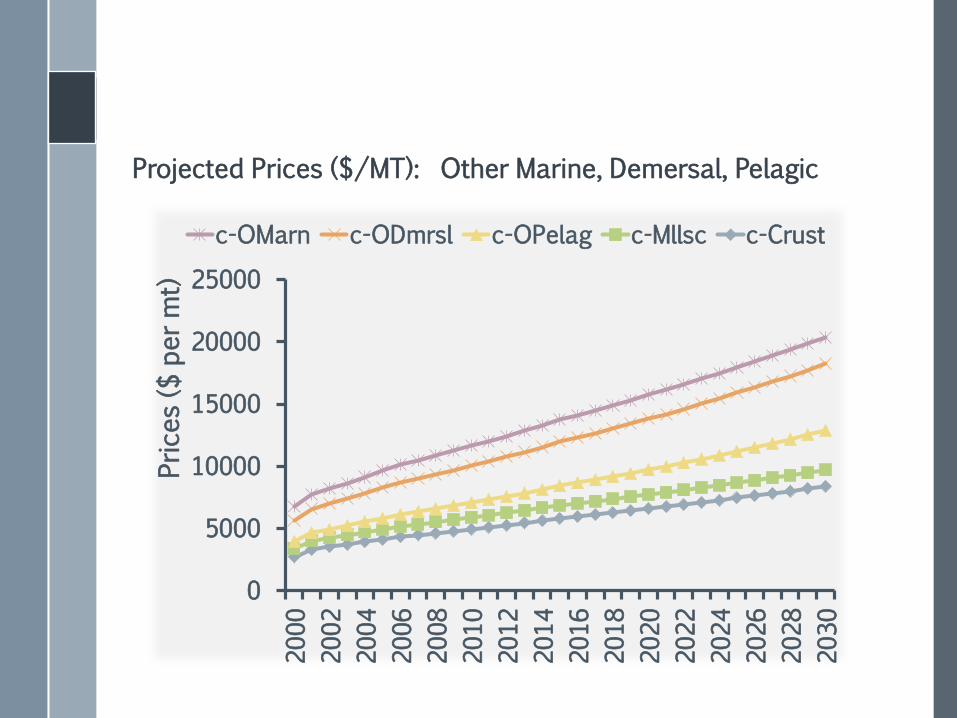

c-OMarn c-ODmrsl c-OPelag c-Mllsc c-Crust

Projected Prices ($/MT): Other Marine, Demersal, Pelagic

Projected Prices ($/MT): Shrimp, Salmon, Tuna, Freshwater

0100020003000400050006000700080009000

1000020

0020

0220

0420

0620

0820

1020

1220

1420

1620

1820

2020

2220

2420

2620

2820

30

prices ($ pe

r mt)

c-shrimp c-Salmon c-Tuna c-FrshD

-20.00 -10.00 0.00 10.00 20.00 30.00

North America

China

Latin America

SE Asia

Other E Asia

SS Africa

Europe

So Asia

Net trade (million mt)

2030 2010

Projected Net Trade in 2030 as Compared to 2010

SUPERMARKET SALES TRENDS FOR AQUACULTURE PRODUCTS

› In terms of value, restaurants account for about two-thirds of seafood sales

› However, in terms of quantity of seafood sold, grocery sector has almost equal share with restaurants (~50% each)

› Supermarkets are the fastest growing food-retailing businesses

› Supermarkets have: – Expanded seafood counters – Created separate seafood depts. – Established own brands of seafood.

What Is Retail Store Scanner Data?

INFORMATION COLLECTED THROUGH THE SCANNING OF UPC / BAR CODES

A very popular tool in marketing research; but not tried in seafood

marketing sector

Types of Stores Covered

Drug Stores

Gas Convenience Stores

Independent Food Stores

Supermarkets Mass Merchandisers

Chain Convenience Stores

Supercenters

Markets Covered

Portland

Seattle

Sacramento

San Francisco

Los Angeles

Salt Lake City/Boise Denver

PhoenixLas Vegas

San Diego West Texas/New Mexico

Oklahoma City/Tulsa

San Antonio

Dallas

Houston

Omaha Des Moines Minneapolis

TampaKansas City

Little Rock

Memphis

New Orleans/Mobile

Birmingham

Grand RapidsMilwaukee

St. LouisChicago

Cleveland

Detroit

Indianapolis

Cincinnati

ColumbusPittsburgh

Buffalo/Rochester

Nashville

Miami

Atlanta

Orlando

Louisville

Charlotte

Jacksonville

Richmond

Raleigh/Durham

Washington DC

BaltimorePhiladelphia

Hartford/New Haven

New York

Boston

Syracuse

Albany

Composition of Retail Seafood Sales

[CATEGORY NAME]

[PERCENTAGE]

[CATEGORY NAME]

[PERCENTAGE]

Frozen Unbreaded

Items 24%

Frozen Entrée Items 10%

Frozen Breaded Items 7%

Anchovy products <0.01%

The Three Frozen/Chilled Seafood Categories

Breaded seafood Seafood Entrée Unbreaded seafood Value-added products

16

% Shares of Product Categories (52 markets)

0

20

40

60

80

100

120

140

160

Y1 Y2 Y3 Y4 Y5

23 25 28 31 33

13 13 12 13 13 7 7 7 7 7

43 46 47

51 53

57 54 53

49 47

AllCannedItems

AllFrozenProducts

AllEntréeItems

AllBreadedItems

AllUnbreaded Items

17

Sales Volume of Frozen/chilled Products: Trends w.r.t 2005-06

-15-10-505

101520253035

Total fro

zen

seafoo

d

Brea

ded

froze

n

Froz

en E

ntrée

Unb

read

edfro

zen

4

-0.3

10 5 6

-6

1

13 8

-3 -8

18 17.9

-0.2

-10

33.8

% C

hang

e

Y2 Y3 Y4 Y5

18

WHAT’S WRONG WITH THIS PICTURE?

PRICES OF COD PRODUCTS: 12-OZ PACKS

0.001.002.003.004.005.006.007.008.009.00

10.00

Y1 Y2 Y3 Y4 Y5

B Cod fillet E Cod fillet U Cod fillet

Value-added products

0.001.002.003.004.005.006.007.008.009.00

Y1 Y2 Y3 Y4 Y5

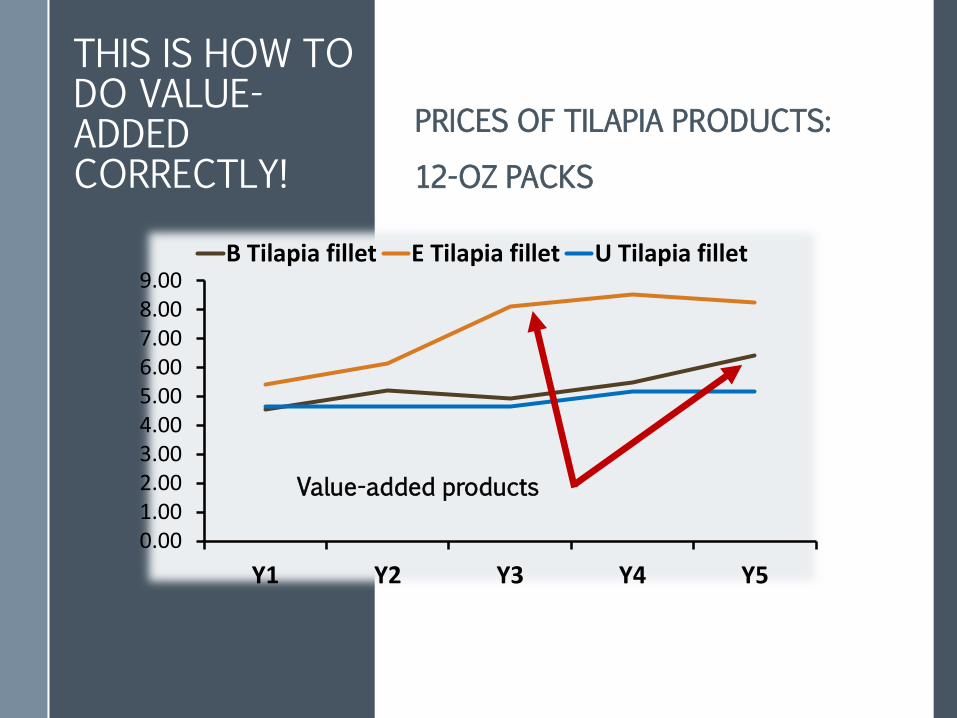

B Tilapia fillet E Tilapia fillet U Tilapia fillet

THIS IS HOW TO DO VALUE-ADDED CORRECTLY!

PRICES OF TILAPIA PRODUCTS: 12-OZ PACKS

Value-added products

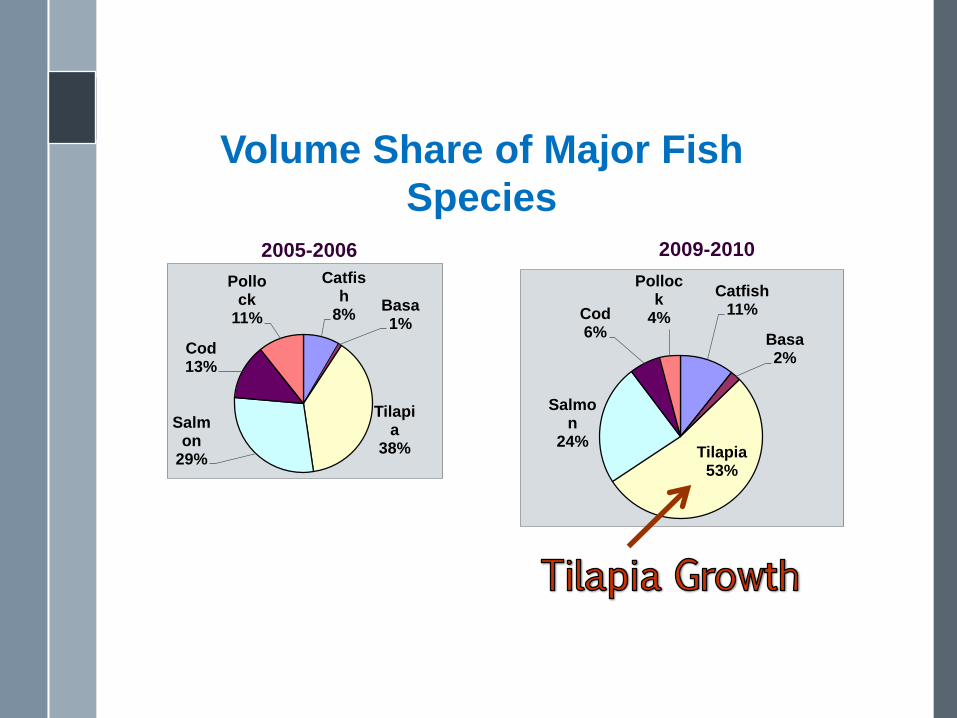

Volume Share of Major Fish Species

Catfish 11%

Basa 2%

Tilapia 53%

Salmon

24%

Cod 6%

Pollock

4%

Catfish

8% Basa 1%

Tilapia

38% Salm

on 29%

Cod 13%

Pollock

11%

2005-2006 2009-2010

Tortilla crusted chipotle lime W/pineapple, mango salsa

Gourmet with red pepper Stuffed with spinach & cheese

Parmesan crusted Tuscan herb

W/ adobo sauce

Herb crusted Parmesan W/ rolled scallop & red pepper

With artichoke & pesto Potato crunch Pecan encrusted W/chimichurri

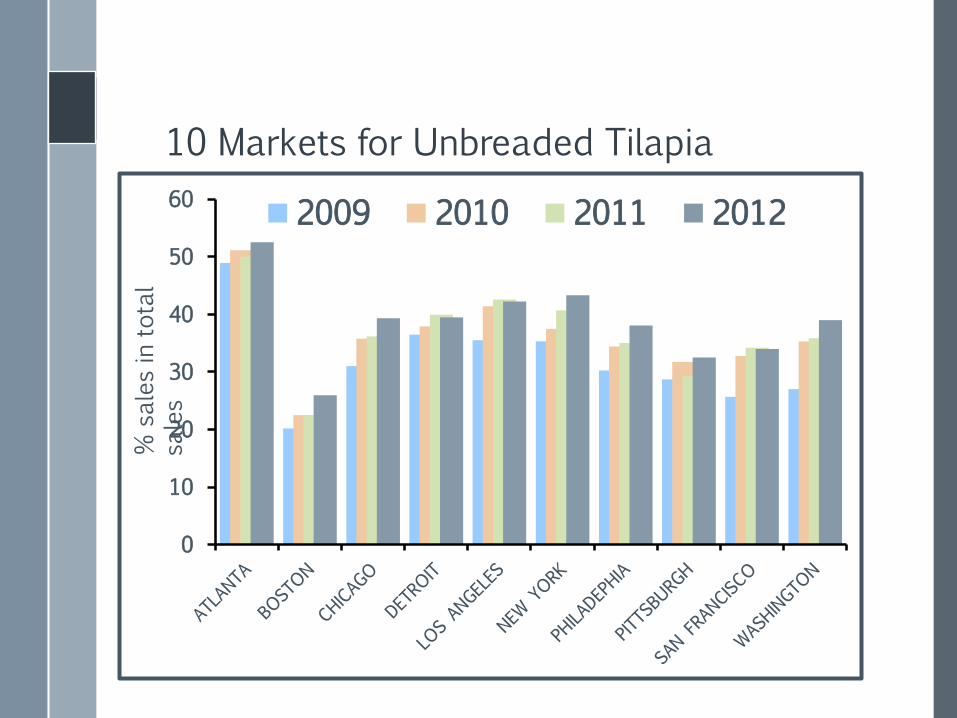

Markets covered Atlanta, Boston, Chicago, Detroit, Los Angeles,

New York, Philadelphia, Pittsburgh, San Francisco & Washington D.C

05

1015202530354045 2009 2010 2011 2012

10 Markets: Top 10 Unbreaded Finfish % sa

les in

total s

ales

10 Markets for Unbreaded Salmon % sales in total

sales

05

1015202530354045 2009 2010 2011 2012

10 Markets for Unbreaded Tilapia % sales in total

sales

0

10

20

30

40

50

60 2009 2010 2011 2012

Tilapia Own-price elasticity Expenditure elasticity

-2.25 -1.75 -1.25 -0.75 -0.25 0.25

Nov-Jan

Feb-April

May-July

Aug-Oct

Mid Atlantic

South Atlantic

East South Central

New England

East North Central

West South Central

Mountain

West North Central

Pacific

0.00 0.50 1.00 1.50

Nov-Jan

Feb-April

May-July

Aug-Oct

Mid Atlantic

South Atlantic

East South Central

New England

East North Central

West South Central

Mountain

West North Central

Pacific

To talk about pricing strategies, we need to talk about elasticities

Salmon Own-price elasticity Expenditure elasticity

-2.25 -1.75 -1.25 -0.75 -0.25

Nov-Jan

Feb-April

May-July

Aug-Oct

Mid Atlantic

South Atlantic

East South Central

New England

East North Central

West South Central

Mountain

West North Central

Pacific

0.00 0.50 1.00

Nov-JanFeb-AprilMay-JulyAug-Oct

Mid AtlanticSouth Atlantic

East South CentralNew England

East North CentralWest South…

MountainWest North…

Pacific

-0.20

0.20.40.60.8

1Cr

oss p

rice

elas

ticity

(%) Salmon Whiting Catfish

Cross-price Elasticities of Tilapia (Substituting Tilapia for others) (substitute =

Positive value)

Cross-price Elasticities of Salmon (Substituting Salmon for others) (substitute = Positive value)

-1.5

-1

-0.5

0

0.5

1

1.5Cr

oss p

rice

elas

ticity

(%)

Tilapia Whiting Catfish

CONCLUDING REMARKS

Global trends indicate that North America has potential to reduce its seafood trade deficit as China becomes more of a net importer.

Degree of competition among products vary considerably across region

Substituting relationship in one region but complementary relationship in another region.

CONCLUDING REMARKS: MARKETING STRATEGIES

Not one uniform product/type/size

Regional variation in Trends Demand Substitutability

One- size- fits-all does not work

Importance of Market segmentation Product differentiation

CONCLUDING REMARKS: MARKETING STRATEGIES

Need to find ways to differentiate your product And continue to add new “value” to it; markets change constantly Does “local” matter?

• In some markets • May be a way to

differentiate your product • However, you have to tell

the story of why yours is better; not just assume that people will buy it because it’s local

Bottomline: More Important Than Ever to

Really Know Your Consumers

Carole R. Engle, Ph.D.

Questions?

![APRIL 1, 2014 WELCOME TO CARP @ [UNIV] “CARP America”](https://img.pdfslide.net/doc/110x75/56649ea45503460f94ba8f44/april-1-2014-welcome-to-carp-univ-carp-america-wwwcarplifeorg.jpg)